Embed Size (px)

Citation preview

13 April 2013

National Institute of Management, Islamabad

15th Midcareer Management Course

“Rise in Fuel Price and its Repercussions”

• Presented By: Muhammad Shahid Dayo (ExCadre) • Sponsor DS: Raja Afshain Afzal

13 April 2013 2

Sequence of Presentation Statement of Problem Introduction Issues & Challenges Analysis Conclusion Recommendation Thanks/Q&A

13 April 2013 3

Statement of Problem Since last one decade, Pakistan’s economy has

witnessed a persistently upward trend in fuel prices. To understand the severity of problem it is envisaged to identify and analyze issues and challenges of rising fuel prices and their socio-economic repercussions.

Based on the analysis, policy recommendations

will be offered to solve and/or to mitigate the problem.

13 April 2013 4

Introduction (Cont’d) Fuels

Chemical Nuclear fuels

13 April 2013 5

Primary (Natural) Secondary (Artificial)

Solid fuels wood, coal, peat, dung coke, charcoal

Liquid fuels petroleum diesel, gasolines, kerosene, LPG, coal tar, naphtha, ethanol

Gaseous fuels Natural gas hydrogen, propane, coal gas, water gas, blast furnace gas, CNG

Introduction Legal Framework Policy making by Federal Government Petroleum Policies by Ministry of P&NR.

Policy Administration by OGRA under OGRA Ordinance 2002 Pricing of petroleum including petroleum surcharge

and petroleum levy under Petroleum Products (Petroleum Development Levy) Ordinance, 1961

Price administration under Section 6 of OGRA Ordinance

13 April 2013 6

Issues & Challenges (Cont’d) Supply & Demand Imbalances Low oil reserves Low exploration Low refining capacity Low production Huge consumption

Greater dependence on oil imports High vulnerability to world oil price shocks High domestic prices

13 April 2013 7

Issues & Challenges (Cont’d) Oil a Major Source of Energy High share of oil in energy mix Escalating power generation cost Rising price of electricity Tough times for major engines of economy;

Industry Transport Agriculture

13 April 2013 8

Issues & Challenges (Cont’d) Oil Fueled Depreciation & Ineffective Monetary Policy

High import bill Pressure of forex reserves Decline in rupee dollar parity Oil fueled inflation limits effectiveness of monetary policy

Agriculture Rising cost of operating agricultural tube wells Transporting agricultural produce becoming expensive Rising cost

electricity/seed/implements/machinery/fertilizer. Agricultural imports flooding local market

13 April 2013 9

Issues & Challenges (Cont’d) Trade Increase in cost of industrial and agricultural

production driving export prices up Decline in demand for exports Competing countries capturing our export markets Imports outstrip exports in both volume and value Failure to compete in High Value Exports Chronic Trade deficits Unfavorable Terms of trade Dwindling forex reserves

13 April 2013 10

Issues & Challenges (Cont’d) Industry Increase in primary input costs Low profitability Dismal BMR investments by textile-the backbone Low value addition Low demand for exports Industries operate below capacity Low demand for Industrial credit hampers capacity

utilization/expansion Industrial output stagnates/declines

13 April 2013 11

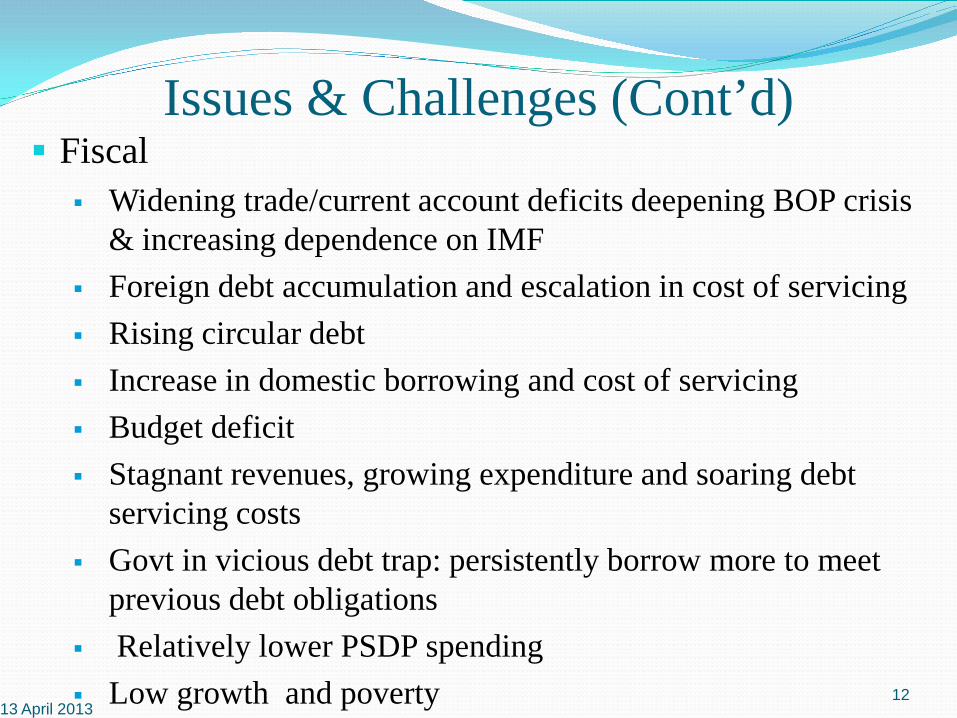

Issues & Challenges (Cont’d) Fiscal

Widening trade/current account deficits deepening BOP crisis & increasing dependence on IMF

Foreign debt accumulation and escalation in cost of servicing Rising circular debt Increase in domestic borrowing and cost of servicing Budget deficit Stagnant revenues, growing expenditure and soaring debt

servicing costs Govt in vicious debt trap: persistently borrow more to meet

previous debt obligations Relatively lower PSDP spending Low growth and poverty

13 April 2013

12

Issues & Challenges (Cont’d) Employment Idle industrial capacity impedes employment

generation Industries losing export markets to other countries Factory workers face layoffs causing unemployment

Fragile Investment Climate Investors avoiding exposure to long term investment

Low growth in LSM Dried up FDI

Growing Speculative Activities Booming bourses 13 April 2013 13

Issues & Challenges Growing social unrest Widespread protests Rampant Crime Violent tendencies Growing corruption

High political uncertainty State’s orientation to profiting from fuel price hike Onslaught from judiciary, opposition and media Survival speculation

Economic slump

13 April 2013 14

Analysis (Cont’d)

13 April 2013 15

Proven Oil Reserves 481 mn barrels Oil Production 63,000 barrels/day Oil Consumption 410,000 barrels/day Net Imports 347,000 barrels/day

410000

63000

Oil Demand & Supply Gap (Barrels/day)

Daily Oil Consumption

Daily Oil production

Source: CIA World Fact Book

Analysis (Cont’d)

13 April 2013 16

$31 $41

$56 $66 $72

$100

$62

$79

$95 $94 $107

2002 2004 2006 2008 2010 2012 2014

World Crude Oil Price (US$ per barrel)

Data Source: ww.forecast-chart.com/forecast-crude-oil.html

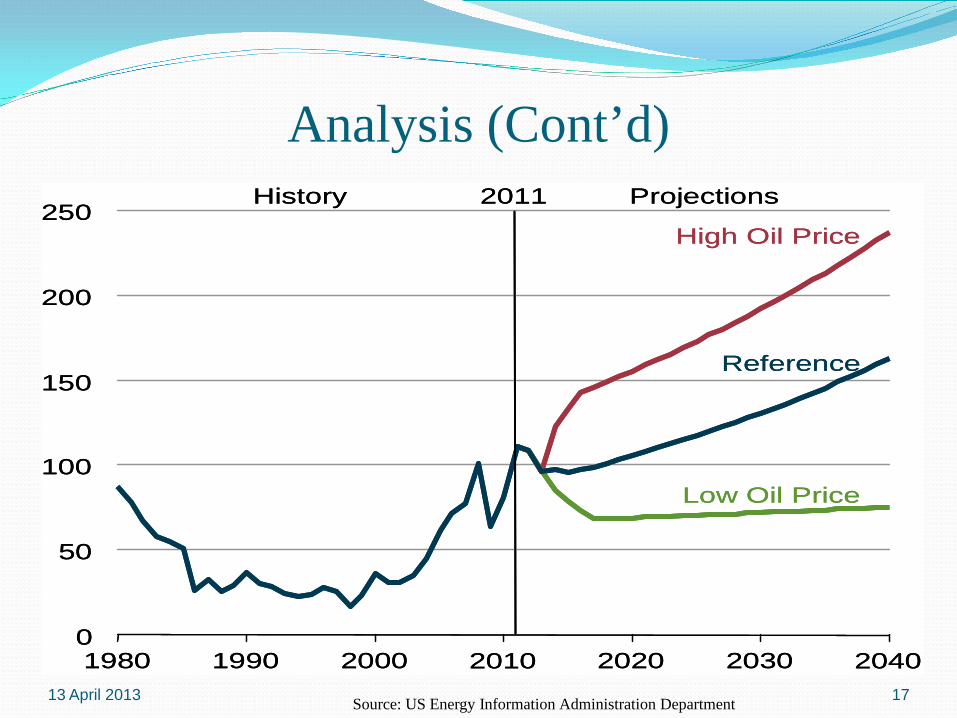

Analysis (Cont’d)

13 April 2013 17

History 2011 Projections

0

50

100

150

200

250

1980 1990 2000 2020 2030 2040

Low Oil Price

Reference

High Oil Price

2010

History 2011 Projections

0

50

100

150

200

250

1980 1990 2000 2020 2030 2040

Low Oil Price

Reference

High Oil Price

2010

Source: US Energy Information Administration Department

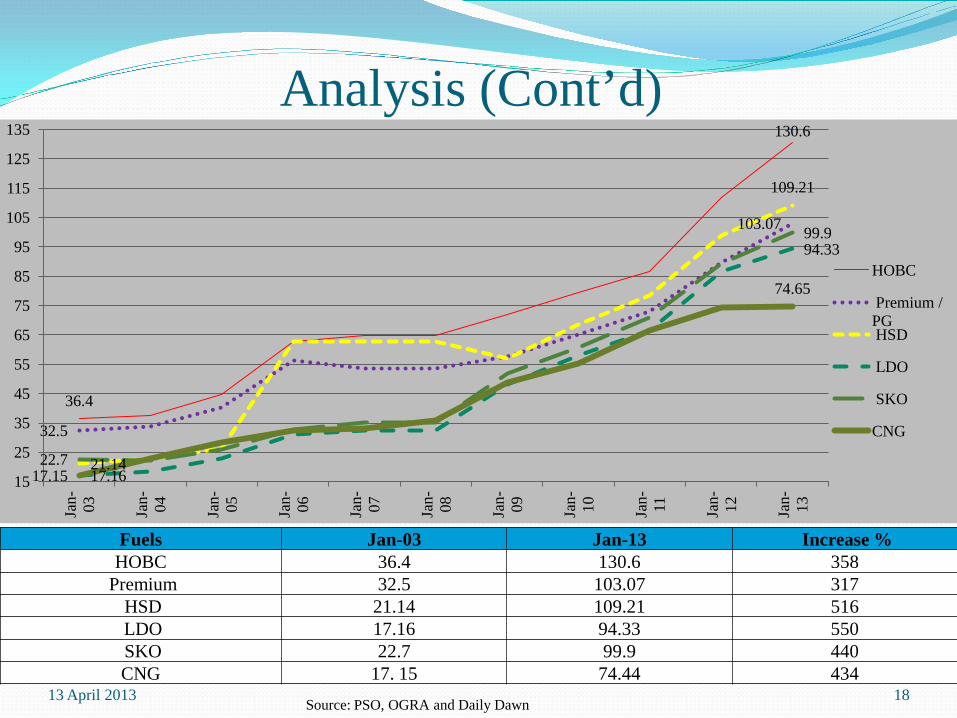

Analysis (Cont’d)

13 April 2013 18 Source: PSO, OGRA and Daily Dawn

36.4

130.6

32.5

103.07

21.14

109.21

17.16

94.33

22.7

99.9

17.15

74.65

15

25

35

45

55

65

75

85

95

105

115

125

135

Jan- 03

Jan- 04

Jan- 05

Jan- 06

Jan- 07

Jan- 08

Jan- 09

Jan- 10

Jan- 11

Jan- 12

Jan- 13

HOBC

Premium / PG HSD

LDO

SKO

CNG

Fuels Jan-03 Jan-13 Increase % HOBC 36.4 130.6 358

Premium 32.5 103.07 317 HSD 21.14 109.21 516 LDO 17.16 94.33 550 SKO 22.7 99.9 440 CNG 17. 15 74.44 434

Analysis (Cont’d)

13 April 2013 19

3240400

12644000

7264700

2935525 2921

868

9008

980

6026

611

1638

457

3185

32

3635

020

1238

089

1297

068

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

000 Kgs 000 M2 Tonnes Nos.

Cotton Yarn Cotton Cloth Fertilizer Motorcycles

No.

of M

easu

re

Items & Unit of Measure

Extent of Capacity Underutilization Installed Capacity Capacity Utilization Unutilized Capacity

Source: Pakistan Economic Survey 2011-12

Analysis (Cont’d)

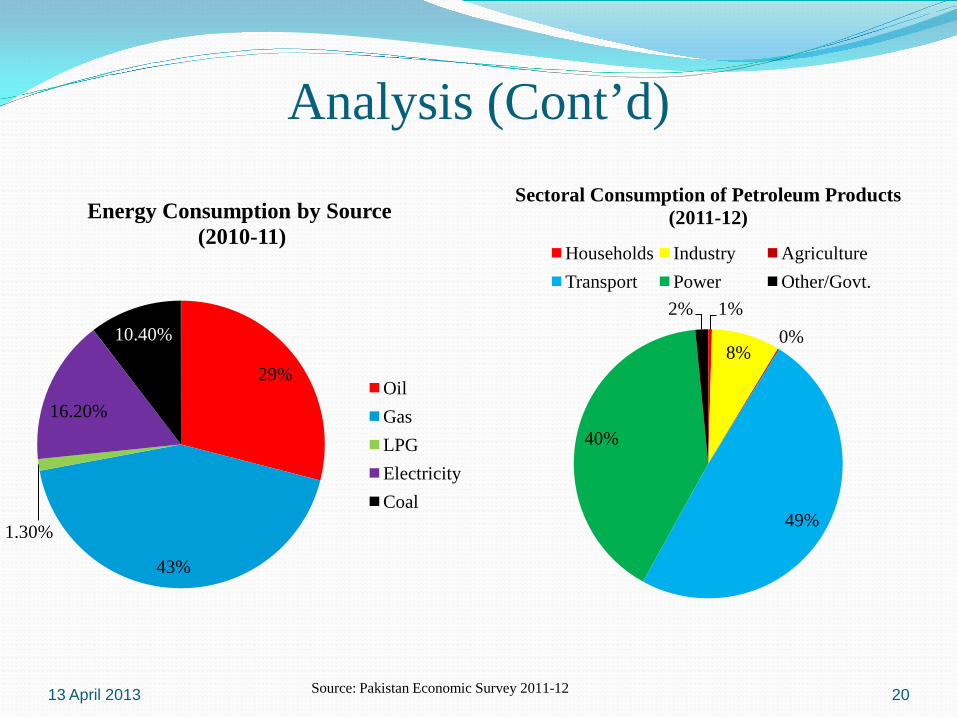

13 April 2013 20

29%

43%

1.30%

16.20%

10.40%

Energy Consumption by Source (2010-11)

Oil Gas LPG Electricity Coal

1%

8% 0%

49%

40%

2%

Sectoral Consumption of Petroleum Products (2011-12)

Households Industry Agriculture Transport Power Other/Govt.

Source: Pakistan Economic Survey 2011-12

Analysis (Cont’d) Crude oil prices as a primary driver up by over 3 times Persistent rise in inflation Decline and stagnation in economic growth

13 April 2013 21

2.9

7.4 9.1 7.9 7.6

20.3

13.7 13.9 12.2

10.1 9

4.8 7.4 7.7 6.2 5.7

1.6 3.6 4.1 3.3 4.1 4.4

0

5

10

15

20

25

2002 2004 2006 2008 2010 2012 2014

Inflation and Economic Growth Rate in Pakistan

inflation Real GDP Growth Rate Source: World Economic Situation & Prospects 2012 , UN

Analysis (Cont’d)

13 April 2013 22

10.8 9.5 10.1

5.5

0

2

4

6

8

10

12

Pakistan India Bangladesh Srilanka

YoY

Incr

ease

Countries

Regional Countries Inflation (2012)

Source: Pakistan Economic Survey 2011-12

Analysis (Cont’d)

13 April 2013 23 Source: Pakistan Economic Survey 2011-12

29 30 25 39 30 31 22 42 24 27 30 37 25 27 40 39

0 50

100 150 200 250 300 350 400 450 500

Pric

e

Item

Essential Item Prices 2002-03 2011-12 Per year Increase %

Analysis (Cont’d)

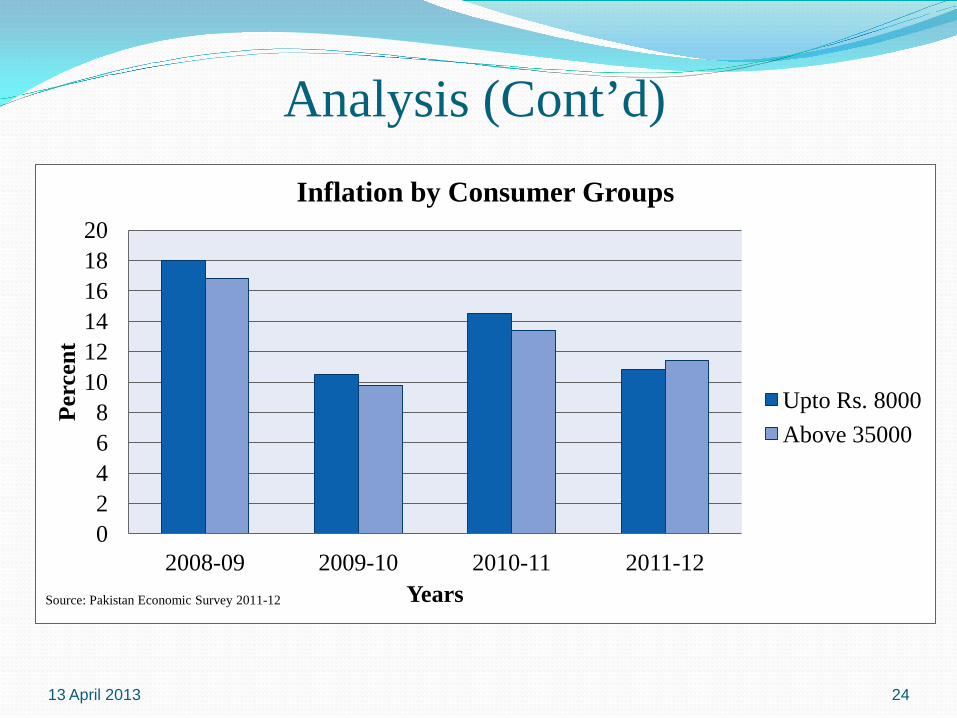

13 April 2013 24

0 2 4 6 8

10 12 14 16 18 20

2008-09 2009-10 2010-11 2011-12

Perc

ent

Years

Inflation by Consumer Groups

Upto Rs. 8000 Above 35000

Source: Pakistan Economic Survey 2011-12

Analysis (Cont’d)

602.39

238.77

699.99

482.50

16.20

102.08

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

Machinary & Transport equipment

Mfg goods

Rs.

Bill

ion

Growth in Import of Consumer and Capital Goods

2007-08 2011-12 Growth (times)

13 April 2013 25 Data Source: External Trade Statistics, PBS (2011-12)

Analysis (Cont’d)

13 April 2013 26

1196.64

897.88

75.03

2110.61

1487.99

70.50

-4.53

Primary/Semi Manufactured

Manufactured

Mfg Goods a %age of P/S Mfg Goods

Rs. Billion

Growth in Export of Primary & Manufactured Goods

Growth 2011-12 2007-08

Data Source: External Trade Statistics, PBS (2011-12)

Analysis (Cont’d)

13 April 2013 27

602.39 238.77 121.76 364.14

773.20

115.46

699.99

482.50 179.56 637.82

1420.17

228.73

0.00

500.00

1000.00

1500.00

2000.00

2500.00

Machinary & Transport equipment

Mfg goods Food & Live Animals

Chemicals Fuels & Lubricants

Animal/Veg Oils & Fats

Rs.

Bill

ion

Import by Commodity Groups

2007-08 2011-12

Data Source: External Trade Statistics, PBS (2011-12)

Analysis (Cont’d) Another BOB crisis in the making

13 April 2013

import bill repayment Forex Series1 -7.4 -1 7.2

-10 -8 -6 -4 -2 0 2 4 6 8

US$

Bill

ion

BOP Crisis

Sources: SBP’s latest Economic Statistics

Analysis (Cont’d)

13 April 2013 29

0 1

2

3

4

5

6

2007-08

2012-13

5.5

0.525 US$

Bill

ion Dried up FDI

Source: Daily Dawn

Analysis (Cont’d)

13 April 2013 30

0 10 20 30 40 50 60 70 80 90

Price Effect Quantity Effect

%ag

e

Sources of Changes in Petroleum Imports (July-April 2011-12)

Sources: Pakistan Economic Survey 2011-12

Analysis(Cont’d)

13 April 2013 31

85877 9%

834911 91%

1358

No. of Diesel/Electric PoweredTubewells in Pakistan

Electric Diesel Others

Per Hectare Irrigation Cost of Tubewell

Crop Electric powered

Diesel powered

Area cultivated by Tubewell

Electric to Diesel Tubewell ratio

Wheat 815 2150 6/19

million hectares

1:10 Maize 710 2020

Sugarcane 2230 7245

Source: Sarhad J. Agric. Vol. 23, No. 1, 2007

Source: PBS 2011-12 Agri Statistics

Analysis Pakistan Homicide Rate

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

6.2 6.5 6.2 6.1 6.2 6.1 6.2 6.4 7.2 7.3

13 April 2013 32

NAB Chief revealed corruption of Rs. 10-12 billion a day Fuel hike led price instability and unchecked corruption

being major economic failures of government brought government and judiciary on collision course sparking political uncertainty which further compounded economic problems.

Conclusion Rise in fuel prices has affected economy at both macro and micro

level. The major direct effects at macro level are deteriorating trade balance due to higher import bill, reflecting a worsening terms of trade; and a weakening fiscal balance. At micro level, investment uncertainty results from higher risks of engaging in new projects which slows down economic growth. The major indirect effects are rising inflation which reduces household spending and disrupts long term investment plans due to loss of competitiveness from higher power generation and transport costs, leading to decreased international competitiveness.

Rising trend in fuel prices in our country is driven by international

oil prices, hence unavoidable. However, with a well thought out short-medium-long term strategy focusing on mitigating risks of future increases; achieving energy efficiency and conservation; and diversifying energy mix, enhancing refining capacities, shoring up exploration and production, the problem can be mitigated in the short run and greatly solved in the long run.

13 April 2013 33

Recommendations (Cont’d) Short-medium term strategy The government should move from spot buying to hedge buying

of oil Medium-long term strategy Fuel conservation and Energy efficiency Electricity conservation by offering bulk consumers rebates on

reduced consumption Discouraging fuel guzzling vehicles by banning their

import/taxing heavily Vehicle fitness rules may be enforced to deter old vehicles. Restricting CNG to public transport Phased and targeted conversion of big office buildings

including government to solar power through enabling legislation so as to penalize non compliers.

13 April 2013 34

Recommendations Medium-long term strategy Diversification of energy mix Blending ethanol in petrol Enhancing coal power Duty free import of quality coal for power generation by

industry Enhance exploration/production specially in Baluchistan Providing security to investors Giving guarantees to pay royalty to locals Training, educating and engaging local workers Promoting and incentivizing local investors/ consortium of

overseas Pakistani investors Enhancing refining capacity of existing refineries Regional integration with countries endowed with abundant oil

and gas

13 April 2013 35

Implementation Time Frame

13 April 2013 36

Developing & prioritizing plans to cope with future oil price shocks so as to contain domestic fuel price increases

Short Term Medium Term Long Term

Hedge buying of oil

Energy efficiency/conservation

Diversification; enhancing refining capacity; Increasing exploration & production

13 April 2013 37

![Presentation on toyota_motors[1]](https://img.dokumen.tips/doc/110x75/541293428d7f72314e8b4629/presentation-on-toyotamotors1.jpg)

![Presentation on toyota motors[1]](https://img.dokumen.tips/doc/110x75/55d4df86bb61ebff298b4700/presentation-on-toyota-motors1.jpg)