Embed Size (px)

Citation preview

High‐frequency trading in ScandinaviaBjörn Hagströmer [email protected]

The 2015 Copenhagen Business School Symposium on High‐Frequency TradingOct. 5, 2015

0

10

20

30

40

2010 2011 2012 2013 2014

Realized volatility

0

5

10

15

20

2010 2011 2012 2013 2014

Order traffic

0

2

4

6

8

2010 2011 2012 2013 2014

Bid‐ask spread

0,00,51,01,52,02,5

2010 2011 2012 2013 2014

Fragmentation

Aug 2011: We have a problem

Squared 10‐second returns (sq. bps)

Halfspread relative midpoint (bps)

# orders / # trades

Fragmentation index (range 1‐5)

Björn Hagströmer, Stockholm Business School

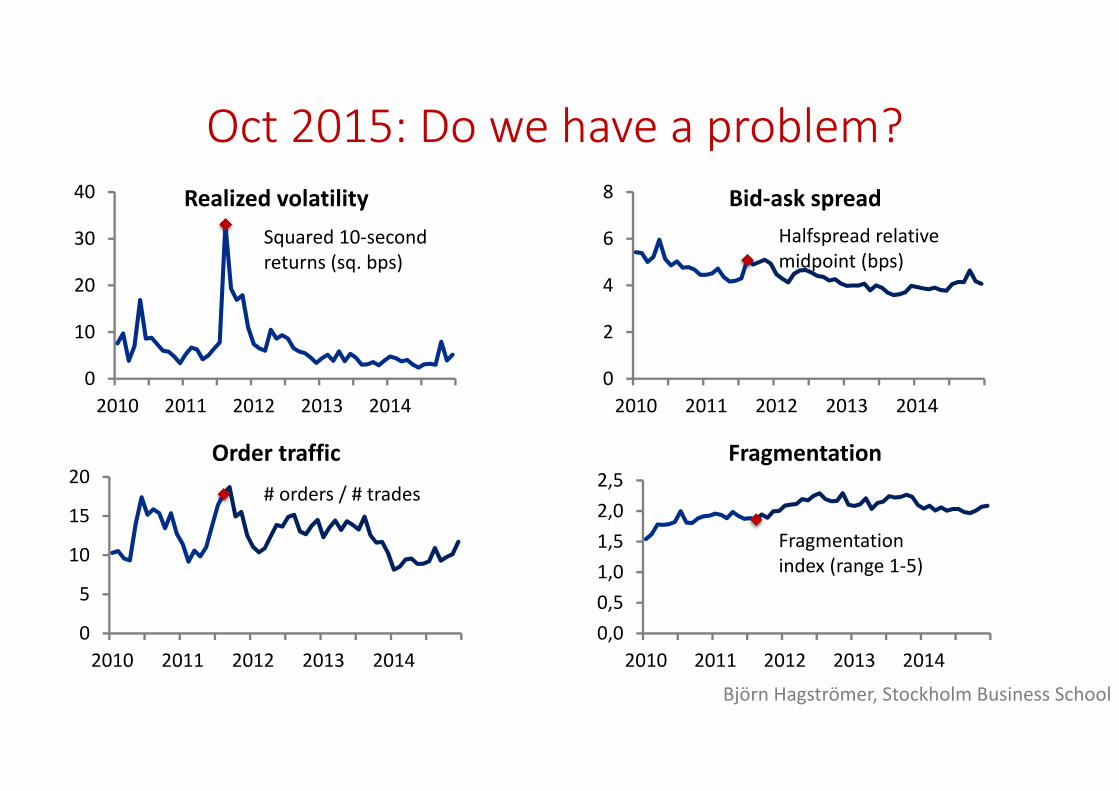

0

10

20

30

40

2010 2011 2012 2013 2014

Realized volatility

0

5

10

15

20

2010 2011 2012 2013 2014

Order traffic

0

2

4

6

8

2010 2011 2012 2013 2014

Bid‐ask spread

0,00,51,01,52,02,5

2010 2011 2012 2013 2014

Fragmentation

Aug 2011: We have a problemOct 2015: Do we have a problem?

Squared 10‐second returns (sq. bps)

Halfspread relative midpoint (bps)

# orders / # trades

Fragmentation index (range 1‐5)

Björn Hagströmer, Stockholm Business School

1. The Diversity of High‐Frequency TradersHow do HFT strategies affect volatility?

2. Trading Fast and Slow: Colocation and LiquidityHow does trading speed affect liquidity?

3. High‐Frequency Trading Around Large Institutional OrdersHow do HFTs affect the execution costs for institutions?

Three studies on HFT in Scandinavia

Björn Hagströmer, Stockholm Business School

HFTsProprietary trading only

Arbitrage strategies

Directional strategies

Market making

Non‐HFTsClient trading only

Execution algorithms

Traditional client

services

HybridsBoth clients and proprietary

HFTs; 29

Non‐HFTs; 49

Hybrids; 22

The Diversity of High‐Frequency TradersBjörn Hagströmer & Lars Nordén

Published in Journal of Financial Markets, 2013

Björn Hagströmer, Stockholm Business School

HFT26%

Hybrids algo18%

Hybrids non‐algo22%

Non‐HFT non‐algo30%

Non‐HFT algo4%

48% AT volume (AUTD) 26% pure HFT (broadly defined)

Many definitions of HFT exist Order‐to‐trade ratios Latency

Many exchange members employ manual trading, AT and HFT parallel

AT/HFT market share in OMX S30 stocks(Feb 2012, SEK trading volume)

Björn Hagströmer, Stockholm Business School

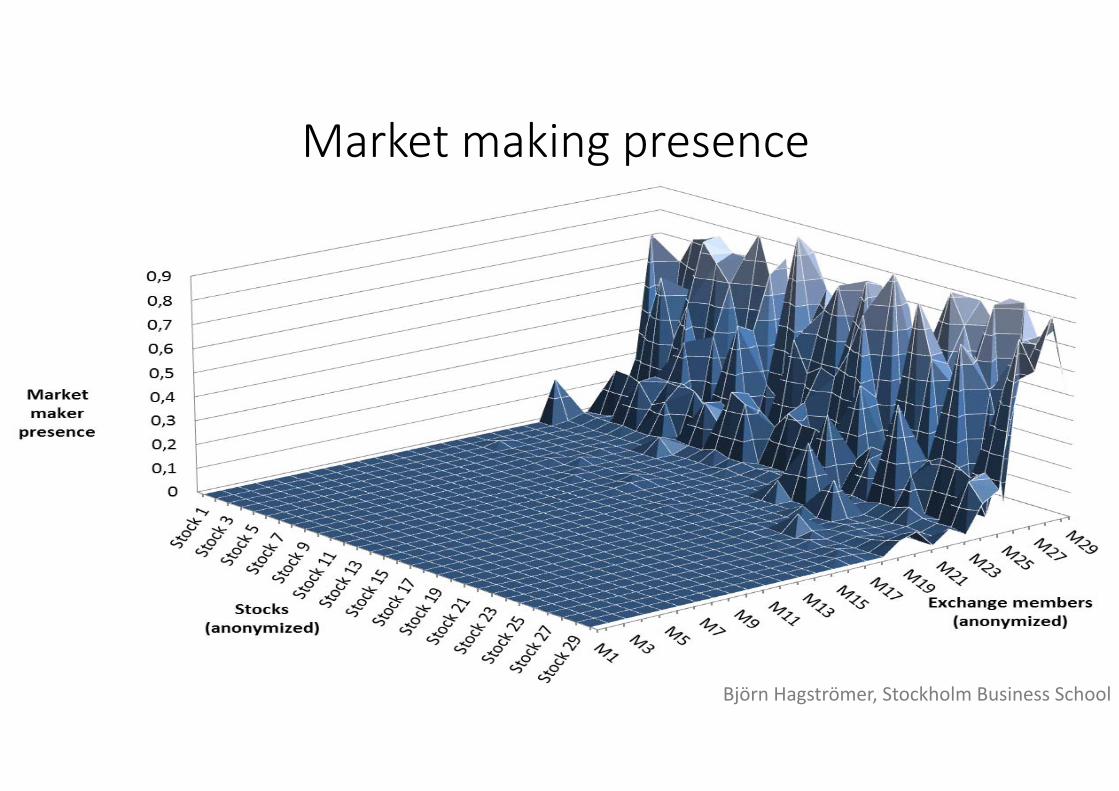

Market making presence How often does each HFT have an order posted at the BBO? Snapshots of the order book every 10 seconds Check in each stock which MPIDs are on the BBO Calculate the % of snapshots where a MPID is present at the BBO

HFTsProprietary trading

only

Arbitrage strategies

Directional strategies

Market making

Distinguishing market makers from other HFTs

Björn Hagströmer, Stockholm Business School

Market making presence

Björn Hagströmer, Stockholm Business School

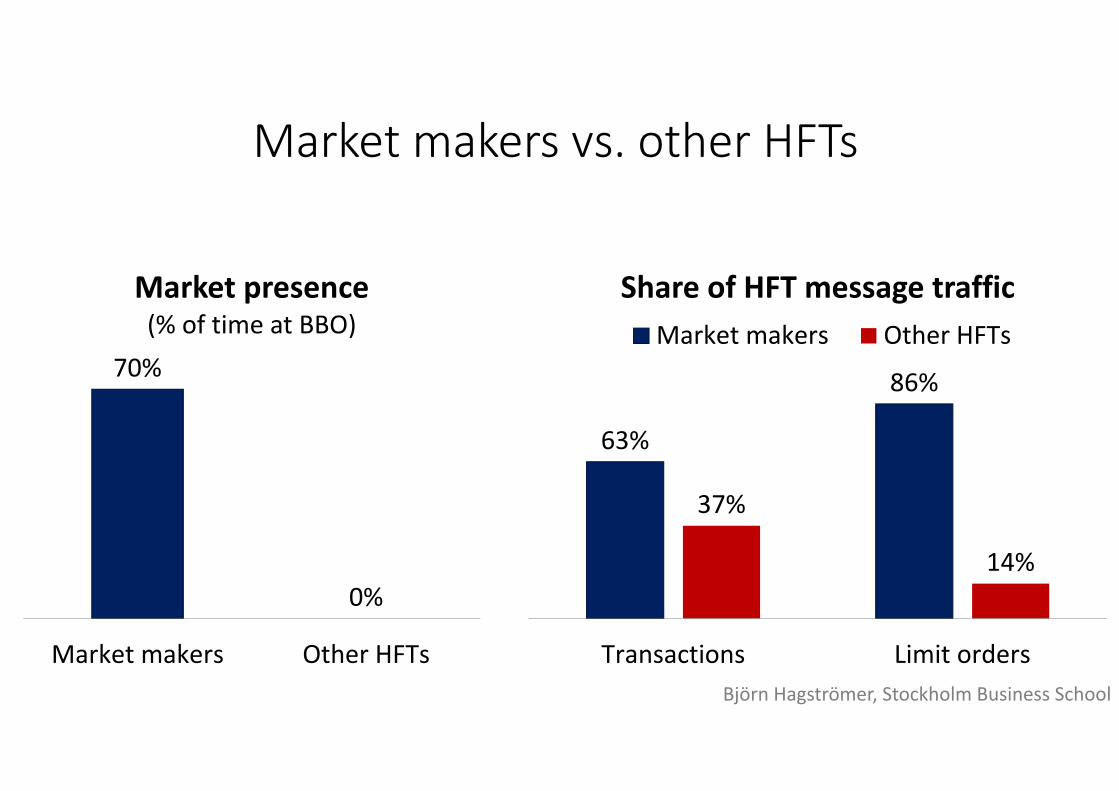

70%

0%

Market makers Other HFTs

Market presence(% of time at BBO)

63%

86%

37%

14%

Transactions Limit orders

Share of HFT message trafficMarket makers Other HFTs

Market makers vs. other HFTs

Björn Hagströmer, Stockholm Business School

90

95

100

105

110

20 Feb

21 Feb

22 Feb

23 Feb

24 Feb

27 Feb

28 Feb

29 Feb

1 Mar

2 Mar

5 Mar

6 Mar

7 Mar

8 Mar

9 Mar

Sandvik 2012

Event date After dateBefore date

Event date: A day when the closing price breaks through a tick size levelE.g., Price SEK 101 SEK 99 changes tick SEK 0.10 SEK 0.05

Before date: Last date before the event with all prices on one side of the limit

After date: First date after the event with all prices on the other side of the limit

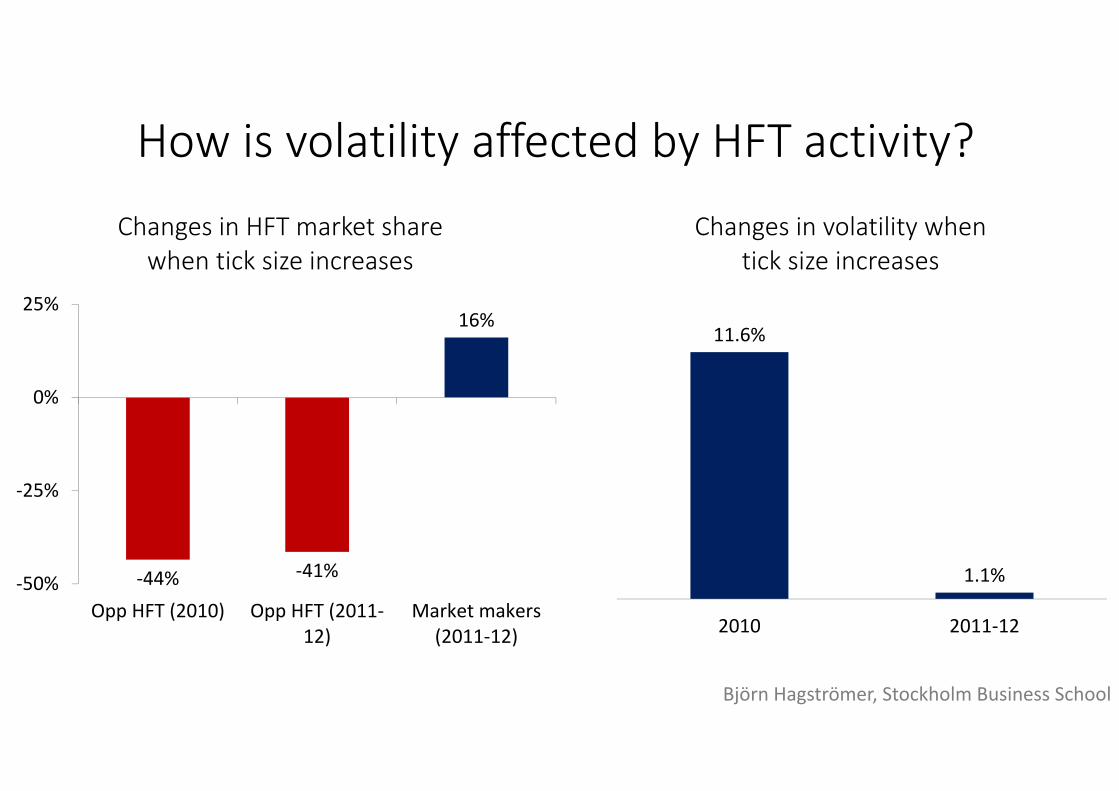

How is volatility affected by HFT?

Björn Hagströmer, Stockholm Business School

11.6%

1.1%

2010 2011‐12

Changes in volatility when tick size increases

‐44% ‐41%

16%

‐50%

‐25%

0%

25%

Opp HFT (2010) Opp HFT (2011‐12)

Market makers(2011‐12)

Changes in HFT market share when tick size increases

How is volatility affected by HFT activity?

Björn Hagströmer, Stockholm Business School

Trading Fast and Slow: Colocation and LiquidityJonathan Brogaard, Björn Hagströmer, Lars Nordén, Ryan Riordan

Published in Review of Financial Studies, 2015

Björn Hagströmer, Stockholm Business School

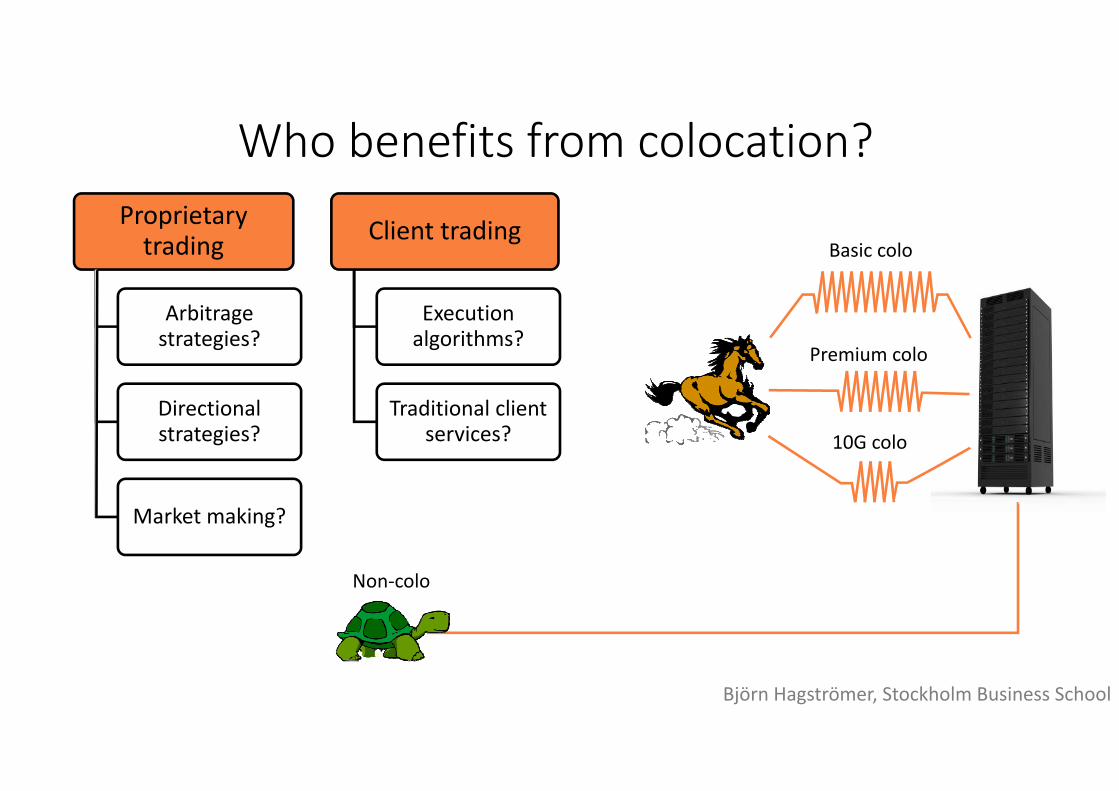

Basic colo

Premium colo

10G colo

Trader group Date of introduction

Basic colocation Feb 8, 2010

Premium colocation Mar 14, 2011

10G colocation Sep 17, 2012

Colocation at NASDAQ OMX Nordic

Non‐colo

Björn Hagströmer, Stockholm Business School

What fast traders do

17% 2%

27%55%

Limit orders

NonColo BasicColoPremiumColo 10GColo

56%

4%

19%

22%

Trades

NonColo BasicColoPremiumColo 10GColo

Björn Hagströmer, Stockholm Business School

Proprietary trading

Arbitrage strategies?

Directional strategies?

Market making?

Market making?

Client trading

Execution algorithms?

Traditional client services?

Basic colo

Premium colo

10G colo

Who benefits from colocation?

Non‐colo

Björn Hagströmer, Stockholm Business School

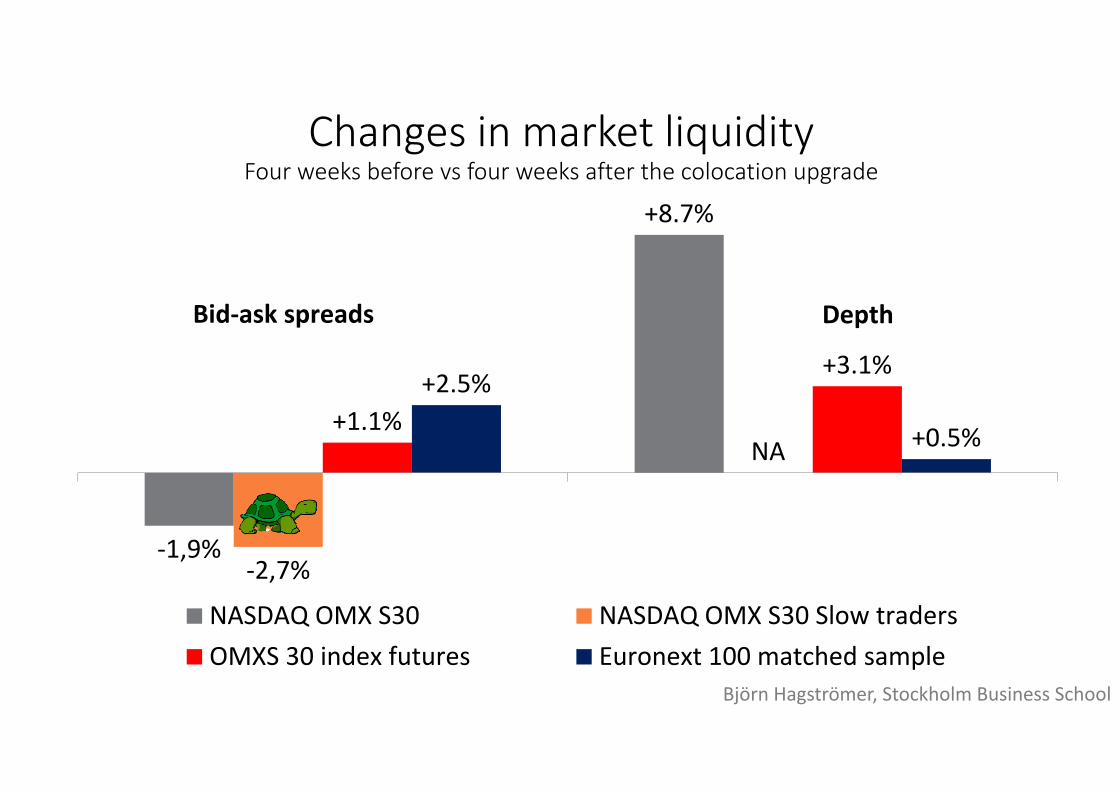

Changes in market liquidityFour weeks before vs four weeks after the colocation upgrade

‐1,9%

+8.7%

‐2,7%

NA+1.1%

+3.1%+2.5%

+0.5%

NASDAQ OMX S30 NASDAQ OMX S30 Slow tradersOMXS 30 index futures Euronext 100 matched sample

Bid‐ask spreads Depth

Björn Hagströmer, Stockholm Business School

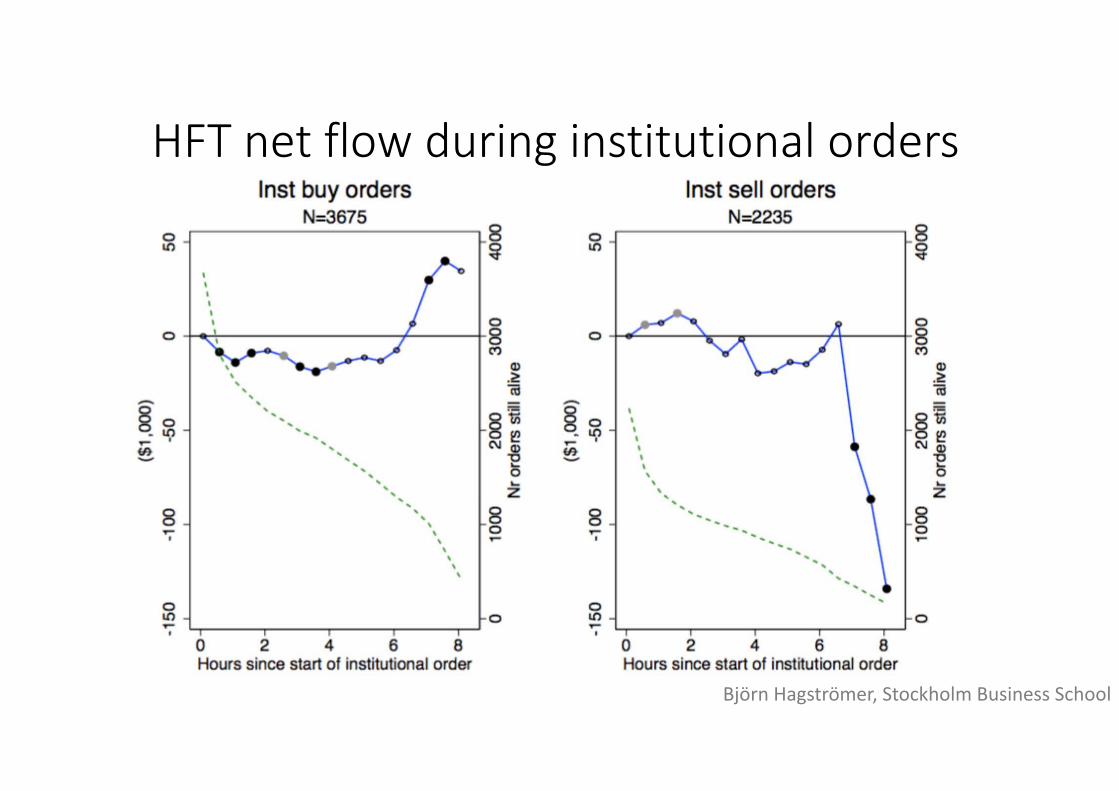

High‐Frequency Trading Around Large Institutional Orders

Vincent van Kervel & Albert J. MenkveldWorking paper, 2015

Björn Hagströmer, Stockholm Business School

HFT net flow during institutional orders

Björn Hagströmer, Stockholm Business School

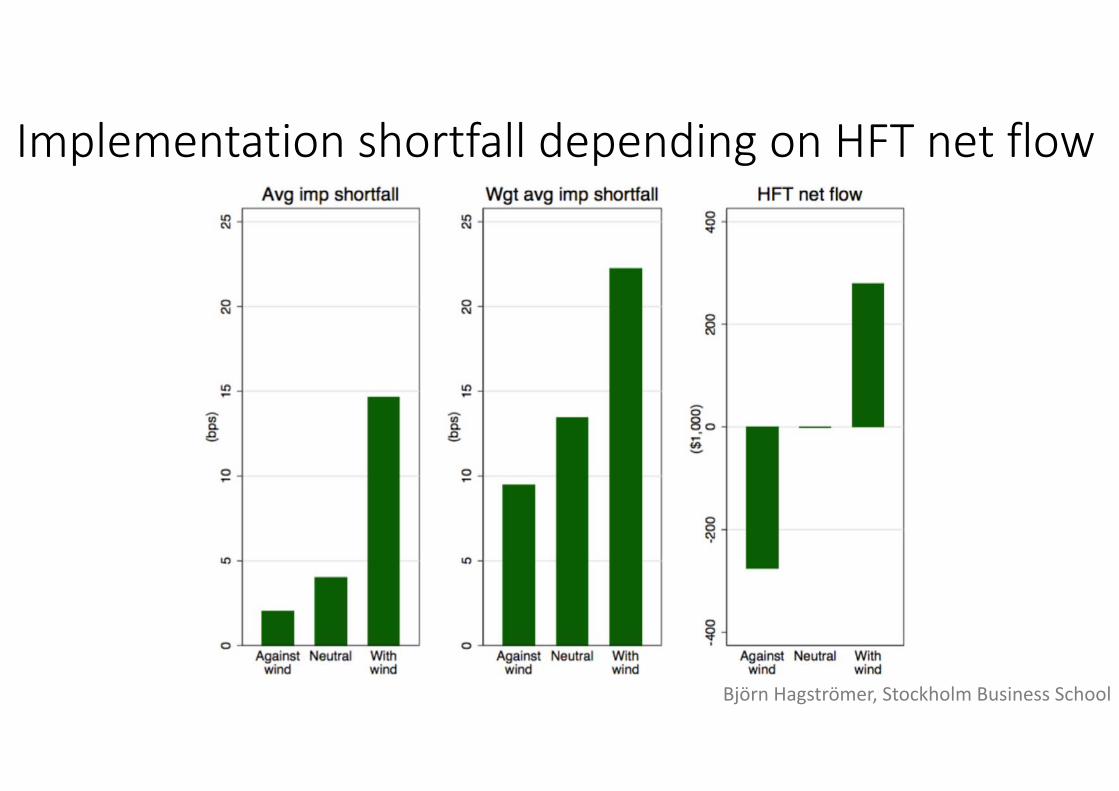

Implementation shortfall depending on HFT net flow

Björn Hagströmer, Stockholm Business School

• Most academic studies find that HFT is good for market quality in the short term

• Remaining issues

• Is the level of technology investments sustainable in the long‐term?

• Fast trading and fragmentation leads to high market complexity. How is best execution for clients influenced by this environment?

Conclusion

Björn Hagströmer, Stockholm Business School