Embed Size (px)

DESCRIPTION

a project work done in andhrabank regarding financing to msme units

Citation preview

A STUDY ON FINANCING TO MSME’s IN THE PERSPECTIVE OF

BANKS AS WELL AS BORROWERS

WITH REFERENCE TO

ANDHRA BANK, ZONAL OFFICE, VISAKHAPATNAM

A PROJECT REPORT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENT

FOR THE AWARD OF THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION

Submitted BY

RAVI KUMAR CH

REGD. NO PG111201084

Under the esteemed guidance of

Mrs. P.HIMAJAGATHI MBA, M.Phil

Asst. Professor

GAYATRI VIDYA PARISHAD COLLEGE FOR DEGREE & PG COURSES

(Autonomous)

ACCREDITED by NAAC with B++ Institution

Approved by AICTE, Affiliated to Andhra University

RISHI KONDA, Visakhapatnam- 530 045

Batch: 2011-13

DECLARATION

I hereby declare that the project work entitled “Financing to MSME’s in the

perspective of Banks as well as Borrowers” with reference to Andhra Bank, Zonal

Office, Visakhapatnam is a bonafide work submitted by me in partial fulfillment for

the award of Master of Business Administration, Andhra University, Visakhapatnam.

I also declare that this project is a result of my own effort and that it has not

been submitted to any other university for the award of any Degree or Diploma. The

empirical findings in the project report are based on the data collected by me.

RAVI KUMAR CH

Rg.No: PG111201084

CERTIFICATE

This is to certify that the project entitled a study on “FINANCING TO MSME’s

IN THE PERSPECTIVE OF BANKS AS WELL AS BORROWERS” is the

bonafide record for work done by Mr. RAVI KUMAR CH during the period 2011-2013

in partial fulfillment of the requirement for the award of the degree of MASTER OF

BUSINESS ADMINISTRATION in GAYATRI VIDYA PARISHAD COLLEGE FOR

DEGREE AND P.G COURSES, VISAKHAPATNAM, under my guidance and

supervision.

Visakhapatnam Mrs. P.HIMAJAGATHI

Date: Asst. Professor

School of Management Studies

GVP College for Degree and PG Courses

ACKNOWLEDGEMENTS

I express my sincere gratitude to Prof.S.RAJANI, the Director; School of

Management studies Gayatri Vidya Parishad College for Degree and P.G courses for

giving me opportunity to work on this Project.

I am grateful to Dr.K.V.V.MURALI SOMESWARA RAO Head of

Department; School of Management studies Gayatri Vidya Parishad College for Degree

and P.G courses for giving me opportunity to work on this Project and for valuable

advices.

I wish to take great Pleasure in recording my profound gratitude and sincere

thanks to Mrs.P.HIMAJAGATHI Assistant Professor in School of Management

studies Gayatri Vidya Parishad College for Degree and P.G courses for her inspiring

guidance and keen interest and critical evaluation of the work for the successful

completion of the project work.

It’s immense pleasure to thank Ms.K.VIMALA, Financial Analyst; Andhra

Bank, Zonal Office at Visakhapatnam, and her team for their co-operation in providing

the required information at each stage to complete my project successfully.

RAVI KUMAR CH

CONTENTS

CH NO. CHAPTERS PAGE NO.

I. INTRODUCTION 1

II. INDUSTRY PROFILE 5

III. PROFILE OF ANDHRA BANK 23

IV. CONCEPTUAL FRAME WORK 33

V. ANALYSIS AND INTERPRETATION 73

VI. FINDINGS AND SUGGESTIONS 94

VII. CONCLUSION 97

VIII. BIBLIOGRAPHY 99

IX. ANNEXURES 101

Page | 1

INTRODUCTION

Page | 2

Introduction:

Micro, Small and Medium Enterprises (MSMEs) have played a significant role

world over in the economic development of various countries. India, certainly, is no exception.

Keeping in view its importance, the promotion and development of MSMEs has been

an important plank in our policy for industrial development and a well- structured programme

of support has been pursued in successive five-year plans for the promotion and development of

MSMEs in the country. There exists a well-developed network of financial institutions at

national and state level to channelize credit to MSMEs. SIDBI is the national level

principal financial institution for promotion, financing and development of MSMEs. It

provides direct assistance to the SSI sector through several schemes like direct discounting,

project finance, assistance for technological up gradation and modernization,

marketing, finance, resource support to institutions engaged in developing SSIs, venture

capital, factoring services, etc. It also provides indirect assistance comprising refinance, bills re-

discounting (equipment) and against inland supply of bills through an organized

network of 910 Primary Lending Institutions (PLIs) including banks and SFCs with more

than 65,000 outlets throughout the country.

Lending norms of the banks has been changing from time to time. So it is

necessary to know the basis for the banks to provide credit to different sectors. In India

most of the business entities are in MSME sector. They need adequate funds to run and

expand their businesses. For getting loans from banks, they need to fulfill some

eligibility criteria and norms. So the main purpose of this study is to study the

availability of credit for Micro, Small and Medium scale enterprises.

Page | 3

Need for the study:

The MSME sector is a very vast area and contributing nearly 7% of GDP. This study is useful

for the MSME organizations as it contains RBI guidelines for raising funds for MSME

sector, eligibility criteria and norms. It helps new entrepreneurs to know whether they will get

the credit from the banks or not according to their business plan and how much they can get according

to their financial structure. The wide range of information regarding the lending norms and

conditions will help the business man to take decision about funding of long term,

working capital and other requirements of the organization.

Objectives of the study:

To learn the financing procedures for MSMEs i.e.,

To study the chain of events of processing a loan proposal- from receiving the application from the

borrower, doing credit rating of the borrower and the company, analyzing the financial statements,

sanctioning to disbursement and the post sanction reviews for MSMEs.

To study the borrowers opinion towards fund raising norms and other criteria.

To study the structure of MSMEs.

Scope of the study:

The study was intended to obtain the information about:

To study the Credit Appraisal Methods.

In understanding the commercial, financial & technical viability of the project

proposed & it’s funding pattern.

To know the knowledge of the borrowers and their responses on different criteria.

Page | 4

Research methodology:

The study is mainly relying up on both Primary and as well as Secondary Data. A sample of

limited number of customers (Borrowers) has been taken for the study. It includes various websites and

articles.

Tools used for analyzing the Secondary data:

For analyzing the Secondary data, the tools used are the Financial Ratios such as Current Ratio,

Debt equity Ratio, Debt Service Coverage Ratio (DSCR), TOL / TNW, and some Profitability Ratios,

capitalization ratios as well as Activity Ratios.

Tools used for analyzing the primary data:

Tool used: Percentage

Formula: Xi * 100 / N

Tool used: Weighted Average

Formula: n

∑ WiXi

i=1

-------------------------

n

∑ Wi

i=1

Limitations of the study:

This study is limited to only one zone of Andhra Bank, the geographical scope of

the project was limited to Andhra Bank circle and the loans studied were of solely

of businesses established majorly in Visakhapatnam.

There are the constraints of time and cost.

Banks are more confidential about their internal data.

RBI internal guidelines are not available.

Page | 5

Industrial

profile

Page | 6

INDUSTRY PROFILE:

Banking Industry:

The Webster’s dictionary defines Bank as “an establishment for the custody, loan,

exchange, or issue of money, for the extension of credit, and for facilitating the

transmission of funds: the table, counters, or place of business of a money changer.” A

Bank can also be defined as a financial institution that accepts deposits and channels

the money into lending activities.

History of Banking:

The first banks were probably the religious temples of the ancient world, and were

probably established sometime during the 3rd millennium B.C. Banks probably

predated the invention of money. Deposits initially consisted of grain and later other

goods including cattle, agricultural implements, and eventually precious metals such as

gold, in the form of easy-to-carry compressed plates. Temples and palaces were the

safest places to store gold as they were constantly attended and well built. As sacred

places, temples presented an extra deterrent to would-be thieves. There are extant

records of loans from the 18th century BC in Babylon that were made by temple priests

to merchants.

Modern western economic and financial history is usually traced back to the coffee

houses of London. The London Royal Exchange was established in 1565. At that time

moneychangers were already called bankers, though the term "bank" usually referred to

their offices, and did not carry the meaning it does today. There was also a hierarchical

order among professionals; at the top were the bankers who did business with heads of

state, next were the city exchanges, and at the bottom were the pawn shops or

Lombard’s. Global banking and capital market services proliferated during the 1980s

and 1990s as a result of a great increase in demand from companies, governments, and

financial institutions, but also because financial market conditions were buoyant and,

on the whole, bullish.

Page | 7

Growing internationalization and opportunity in financial services entirely changed

the competitive landscape, and now many banks prefer the “universal banking” model.

Today universal banks are free to engage in all forms of financial services, make

investments in client companies, and function as much as possible as a “one-stop”

supplier of both retail and wholesale financial services.

The Indian Story:

Banking in India originated in the first decade of 18th century with The General

Bank of India coming into existence in 1786. This was followed by Bank of Hindustan.

Both these banks are now defunct. The oldest bank in existence in India is the State

Bank of India being established as "The Bank of Bengal" in Calcutta in June 1806. A

couple of decades later, foreign banks like Credit Lyonnais started their Calcutta

operations in the 1850s. At that point of time, Calcutta was the most active trading port,

mainly due to the trade of the British Empire, and due to which banking activity took

roots there and prospered. The first fully Indian owned bank was the Allahabad Bank,

which was established in 1865.

By the 1900s, the market expanded with the establishment of banks such as Punjab

National Bank in 1895 in Lahore and Bank of India in 1906 in Mumbai - both of which

were founded under private ownership. The Reserve Bank of India formally took on the

responsibility of regulating the Indian banking sector from 1935. After India's

independence in 1947, the Reserve Bank was nationalized and given broader powers.

Page | 8

Introduction to the Banking Sector in India:

Banks are the most significant players in the Indian financial market. They are the biggest

purveyor of credit, and they also attract most of the savings from the population. Dominated by

public sector, the banking industry has so far acted as an efficient partner in the growth

and the development of the country. Driven by the socialist ideologies and the welfare state

concept, public sector banks have long been the supporters of agriculture and other

priority sectors. They act as crucial channels of the government in its efforts to economic

development. The Indian banking can be broadly categorized into nationalized (government

owned), private banks and specialized banking institutions.

The Reserve Bank of India acts a centralized body monitoring any discrepancies and

shortcoming in the system. Since the nationalization of banks in 1969, the nationalized

banks have acquired a place of prominence and has since then seen tremendous progress. The

need to become highly customer focused has forced the slow-moving public sector banks to

adopt a fast track approach. In India the banks are being segregated in different groups.

Each group has their own benefits and limitations in operating in India. Each has their

own dedicated target market. Few of them only work in rural sector while others in both rural as

well as urban and many even only catering in cities.

The banks are of several types. Types of banks in India are (a) Public sector banks (b) Private

sector banks (c) Cooperative banks (d) Regional Rural banks and (e) Foreign banks.

Page | 9

Classification of Banks:

The Indian banking industry, which is governed by the Banking Regulation Act of India

1949 can be broadly classified into two major categories, non-scheduled banks and

scheduled banks. Scheduled banks comprise commercial banks and the co-operative banks. In

Terms of ownership, commercial banks can be further grouped into nationalized banks, the

State Bank of India and its group banks, regional rural banks and private sector banks

(domestic and foreign). These banks have over 67,000 branches spread across the county. The

Indian banking industry is a mix of the public sector, private sector and foreign banks. The

private sector banks are again spilt into Indian banks and foreign banks.

Page | 10

Competitive forces model in the banking industry:

(PORTER’S FIVE-FORCE MODEL)

Prof. Michael Porter’s competitive forces Model applies to each and every company as

well as industry. This model with regards to the Banking Industry is presented below.

(2)

Potential Entrants is high

as development financial

institutions as well as

private and foreign banks

have entered in a big way.

(5)

Organizing power of the

supplier is high. With the

new financial instruments

they are asking higher

return on the investments.

(1)

Rivalry among existing

firms has increased with

liberalization. New products

and improved customer

services is the focus.

(4)

Bargaining power of

buyers is high as

corporate can raise funds

easily due to high

competition.

(3)

Threat from substitute is

high due to competition

from NBFCs and insurance

companies as they offer a

high rate of interest than

banks.

Page | 11

1. Rivalry among existing firms

With the process of liberalization, competition among the existing banks has

increased. Each bank is coming up with new products to attract the customers and tailor

made loans are provided. The quality of services provided by banks has improved

drastically.

2. Potential Entrants

Previously the Development Financial Institutions mainly provided project finance

and development activities. But they now entered into retail banking which has resulted

into stiff competition among the exiting players.

3. Threats from Substitutes

Banks face threats from Non-Banking Financial Companies. NBFCs offer a higher

rate of interest.

4. Bargaining Power of Buyers

Corporate can raise their funds through primary market or by issue of GDRs,

FCCBs. As a result they have a higher bargaining power. Even in the case of personal

finance, the buyers have a high bargaining power. This is mainly because of

competition.

5. Bargaining Power of Suppliers

With the advent of new financial instruments providing a higher rate of returns to

the investors, the investments in deposits is not growing in a phased manner. The

suppliers demand a higher return for the investments.

6. Overall Analysis

The key issue is how banks can leverage their strengths to have a better future.

Since the availability of funds is more and deployment of funds is less, banks should

evolve new products and services to the customers. There should be a rational thinking

in sanctioning loans, which will bring down the NPAs. As there is a expected revival in

the Indian economy Banks have a major role to play. Funding corporate at a low cost of

capital is a special requisite.

Page | 12

INTRODUCTION TO MSMEs:

Micro, Small and Medium Enterprises (MSMEs) have played a significant role

world over in the economic development of various countries. Over a period of time, it

has been proved that MSMEs are dynamic, innovative and most importantly, the

employer of first resort to millions of people in the country. The sector is a breeding

ground for entrepreneurship.

The importance of MSME sector is well-recognized world over owing to its

significant contribution in achieving various socio-economic objectives, such as

employment generation, contribution to national output and exports, fostering new

entrepreneurship and to provide depth to the industrial base of the economy. Micro,

Small and medium-sized enterprises (MSMEs) are the backbone of all economies and

are a key source of economic growth, dynamism and flexibility in advanced

industrialized countries, as well as in emerging and developing economies. MSMEs

constitute the dominant form of business organization, accounting for over 95% and up

to 99% of enterprises depending on the country. They are responsible for between 60-

70% net job creations in Developing countries.

Small businesses are particularly important for bringing innovative products or

techniques to the market. Microsoft may be a software giant today, but it started off in

typical MSME fashion, as a dream developed by a young student with the help of

family and friends. Only when Bill Gates and his colleagues had a saleable product

were they able to take it to the marketplace and look for investment from more

traditional sources. MSMEs are vital for economic growth and development in both

industrialized and developing countries, by playing a key role in creating new jobs.

Financing is necessary to help them set up and expand their operations, develop new

products, and invest in new staff or production facilities.

Page | 13

Many small businesses start out as an idea from one or two people, who invest

their own money and probably turn to family and friends for financial help in return for

a share in the business. But if they are successful, there comes a time for all developing

MSMEs when they need new investment to expand or innovate further. That is where

they often run into problems, because they find it much harder than larger businesses to

obtain financing from banks, capital markets or other suppliers of credit.

Common Characteristics of MSMEs:

(a) Born out of individual initiatives & skills

MSME startups tend to evolve along a single entrepreneur or a small group of

entrepreneurs; in many cases; leveraging on a skill set. There are other MSMEs being

set up purely as a means of earning livelihood. These includes many trading and retail

establishments while most countries continue MSMEs to manufacturing services,

others adopt a broader definition and include retailing as well.

(b) Greater operational flexibility

The direct involvement of owner(s), coupled with flat hierarchical structures and

less number of people ensure that there is greater operational flexibility. Decision

making such as changes in price mix or product mix in response to market conditions is

faster.

(c) Low cost of production

MSMEs have lower overheads. This translates to lower cost of production, least

upto limited volumes.

(d) High propensity to adopt technology

Traditionally MSMEs have shown a propensity of being able to adopt and

internalize the technology being used by them.

(e) High capacity to innovate export:

MSMEs skill in innovation, improvisation and reverse engineering are legendary.

By being able to meet niche requirements, they are also able to capture export markets

where volumes are not huge.

Page | 14

(f) High employment orientation:

MSMEs are usually the prime drives of jobs, in some cases creating up to 80%.

Jobs MSMEs tend to be labour intensive per se and are able to generate more jobs for

every unit of investment, compared to their bigger counterparts.

(g) Reduction of regional imbalances

Unlike large industries where divisibility of operations is more difficult, MSMEs

enjoy the flexibility of location. Thus, any country, MSMEs can be found spread

virtually right across, even through some specific location s emerge as ‘clusters’.

MSMEs in India:

India has a vibrant MSME sector that plays an important role in sustaining

economic growth, increasing trade, generating employment and creating new

entrepreneurship in India. In keeping in view its importance, the promotion and

development of MSMEs has been an important plank in our policy for industrial

development and a well-structured programme of support has been pursued in

successive five-year plans for. MSMEs in India have recorded a sustained growth

during last five decades. The number of MSMEs in India is estimated to be around 13

million while the estimated employment provided by this sector is over 31 million. The

MSME sector accounts for about 45 per cent of the manufacturing output and over 40

per cent of the national exports of the country.

India embarked on the path of opening up its economy and integrating it with the

global economy in 1991. The liberalization of economy, while offering tremendous

opportunities for the growth and development of Indian industry including MSMEs, has

also thrown up new challenges in terms of fierce competition. The very rules which

provide increased access for our products in the global markets also put domestic

industry under increased competition from other countries. In today’s world, access on

a global basis to modern technology, capital resources and markets have become the

most critical determinants of international competitiveness.

Page | 15

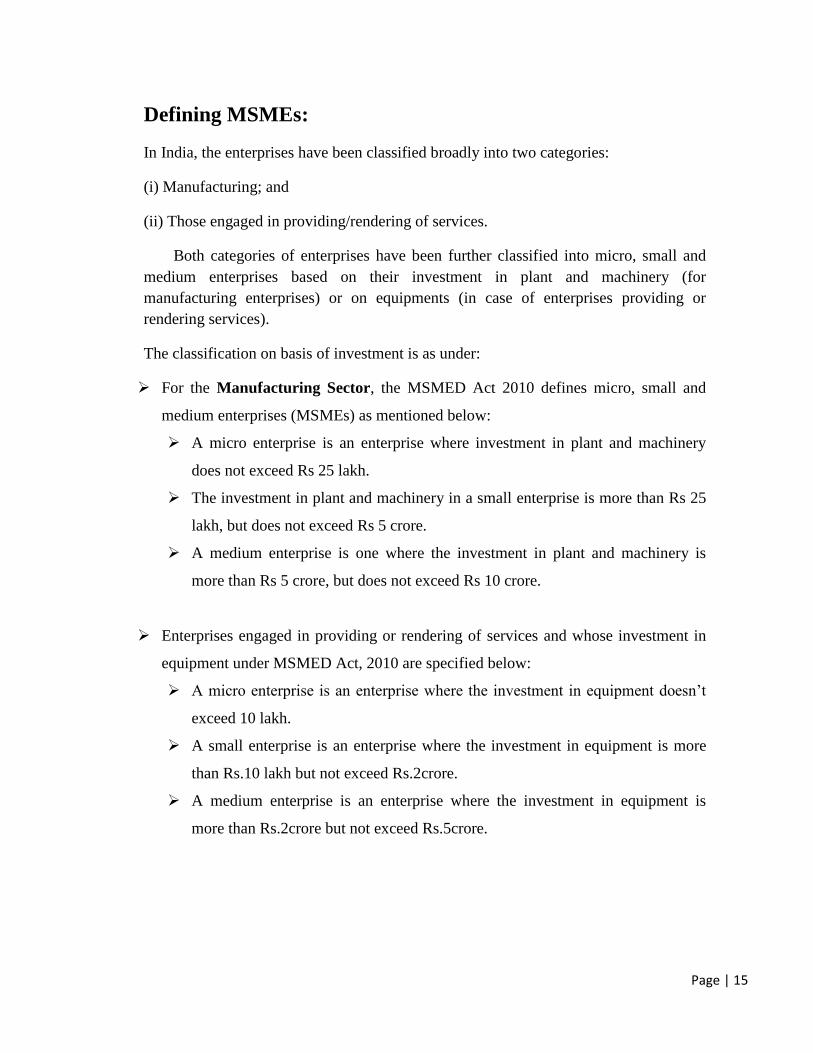

Defining MSMEs:

In India, the enterprises have been classified broadly into two categories:

(i) Manufacturing; and

(ii) Those engaged in providing/rendering of services.

Both categories of enterprises have been further classified into micro, small and

medium enterprises based on their investment in plant and machinery (for

manufacturing enterprises) or on equipments (in case of enterprises providing or

rendering services).

The classification on basis of investment is as under:

For the Manufacturing Sector, the MSMED Act 2010 defines micro, small and

medium enterprises (MSMEs) as mentioned below:

A micro enterprise is an enterprise where investment in plant and machinery

does not exceed Rs 25 lakh.

The investment in plant and machinery in a small enterprise is more than Rs 25

lakh, but does not exceed Rs 5 crore.

A medium enterprise is one where the investment in plant and machinery is

more than Rs 5 crore, but does not exceed Rs 10 crore.

Enterprises engaged in providing or rendering of services and whose investment in

equipment under MSMED Act, 2010 are specified below:

A micro enterprise is an enterprise where the investment in equipment doesn’t

exceed 10 lakh.

A small enterprise is an enterprise where the investment in equipment is more

than Rs.10 lakh but not exceed Rs.2crore.

A medium enterprise is an enterprise where the investment in equipment is

more than Rs.2crore but not exceed Rs.5crore.

Page | 16

While calculating the investment in plant and machinery/equipment referred to

above, the original price thereof shall be taken into account, irrespective of whether the

plant and machinery/equipment are new or second hand. In case of imported

machinery/equipment, the following duty/charges/costs shall be included in calculating

their value:

Import Duty (not to include miscellaneous expenses such as transportation from

the port to the site of the factory, demurrage paid at the port);

Shipping Charges;

Customs Clearance charges; and Sales Tax or Value-added Tax. Cost of the

following plant & machinery/equipments etc would be excluded:;

Equipments such as tools, jigs, dies, moulds, and spare parts for maintenance

and the cost of consumable stores;

Installation of plant &machinery;

Research and development and pollution control equipments;

Power generation set and extra transformer installed by the enterprises as per

the Regulations of the State Electricity Board;

Bank charges and Service Charges paid to the National Small Industries

Corporation or the State Small Industries Corporation;

Procurement or Installation of cables, wiring bus bars, electrical control panels

(not mounted on individual machines)

Oil circuit breakers or miniature circuit breakers which are necessarily to be

used for providing electrical power to the plant and machinery or for safety

measures;

Gas producer plants;

Transportation charges (other than sales tax or value-added tax and excise duty)

for indigenous machinery from the place of their manufacture to the site of the

enterprise);

Charges paid for technical know-how for erection of plant machinery;

Page | 17

Such storage tanks which store raw materials and finished products only and are

not linked with the manufacturing process;

Fire-fighting equipment; and

Such other items as may be specified, by notification from time to time.

In case of Service Enterprises, the original cost to exclude furniture, fittings and

other items not directly related to the services rendered. Land and Building

would also not be included while computing the machinery/equipments cost.

MSME would be meant to include Micro Small and Medium Enterprises

(MSMEs). The above definitions of Micro, Small and Medium Enterprises would be in

place of the existing definitions of Small & Medium Industries and SSSBEs/Tiny

Enterprises.

Micro Enterprises would include Tiny Industries also.

Small Enterprises (Manufacturing) would mean Small Scale Industries (SSIs).

Medium Enterprises (Manufacturing) would mean Medium Industries (MIs).

Small Enterprises (Services) and Medium Enterprises (Services) would mean

other Small & Medium Enterprises. Thus, MSME Advances would be

categorized as under:

All advances to segments viz. Micro, Small and Medium Enterprises in the

Manufacturing sector irrespective of sanctioned limits, (including advances

against TDRs/Govt. Securities etc for business purposes to these categories of

Borrowers), and

Advances to Services Sectors such as Professional & Self-Employed, Small

Business Enterprises, and Small Road/Water Transport Operators and other

enterprises, engaged in providing/rendering of services, conforming to the

above investment criteria and enjoying borrowing/non-borrowing facilities with

the Bank (including advances against TDRs/Govt. Securities etc for business

purposes to these categories of Borrowers).

Those enterprises exceeding the investment ceilings would be categorized as

Large Enterprises and be outside the purview of MSME.

Page | 18

The sanctioned limits would no longer be the criteria determining the status as

micro or small or medium enterprises in these cases.

Development of MSMEs in India:

Making the best use of the material resources by employing higher order of skill

and artistic talents through traditional handicrafts, India has occupied a permanent place

of pride in the world before industrial resolution. However, the advent of modern large

scale mechanized industry, the imposition of restrictions on Indian trade by the British

rulers and deteriorating socio-economic conditions lead to the decline of Small Scale

Industry. But with the provisions of permanent place in the nation's policy of economic

development after the attainment of the Independence, it has staged a grand recovery

and is now well entrenched on the path of progress towards great expansion.

MSME has emerged into prominent sector in Indian economy in general and

industry in particular. SSI sector in India has posted impressive growth in 1990's from

15% in 1991-92 to 55% in 2001-02.The growth in employment generation has been

equally impressive from 3% to 45% during the same period. Employment in MSME

touched 19 million, just behind agriculture. Share of SSI exports crosses 40% of total

exports.

Growth by itself in MSME sector is impressive enough indicating a positive

response to the Economic Reform process initiated in the country since 1991.

Development of infrastructure

Assured supply of Raw Materials

Availability of Cheap Credit

Concessionary Taxes and Tariffs.

Financial subsidies

Equity contributions are all the protective measures for the sector

Page | 19

Role of MSME sector in Nation Development:

The Small and Medium sector plays an important role in the Indian economy in

terms of employment and growth has recorded a high rate of growth after

independence. MSMEs play a vital role for the growth of Indian economy by

contributing 45% of the industrial output, 40% of exports, 42 million in employment,

create one million jobs every year and produces more than 8000 quality products for

the Indian and international markets. As a result, MSMEs are today exposed to greater

opportunities for expansion and diversification across the sectors.

The root cause for unemployment in India is the over growing population which

has outpaced the development of industry and agriculture. For a country like ours, with

limited financial resources and huge reservoir of human resources, Small and Medium

industry is the only means for solving the unemployment problem. Small and Medium

industry is providing employment at an increased rate.

The Indian market is growing rapidly and Indian industry is making remarkable

progress in various Industries like Manufacturing, Precision Engineering, Food

Processing, Pharmaceuticals, Textile & Garments, Retail, IT, Agro and Service sectors.

MSMEs are finding increasing opportunities to enhance their business activities in core

sectors. The good performance of the small scale units is evident from their number,

production, employment and foreign exchange earnings.

Page | 20

Problems of MSMEs

Despite its commendable contribution to the Nation's economy, MSME Sector

does not get the required support from the concerned Government Departments,

Banking Sector, Financial Institutions and Corporate Sector, which is a handicap in

becoming more competitive in the National and International Markets and which needs

to be taken up for immediate and proper redressal. MSME sector faces a number of

problems - absence of adequate and timely banking finance, limited knowledge and

non-availability of suitable technology, low production capacity, follow up with various

agencies in solving regular activities and lack of interaction with government agencies

on various matters.

Some of the major problems are briefly as follows:

a) Financial problems of MSMEs:

The financial problem of MSMEs is the Root Cause for all the other problems

faced by the MSME sector. The small and medium industrialists are generally poor and

there are no facilities for cheap credit. They fall into the clutches of money lender who

charges very high rates of interest, or else they borrow from the dealers of their goods,

who exploit them by completing them to sell their products at very low price. After the

nationalization of 14 major Indian Banks in July, 1969, the Commercial banks were

providing only a small proportion of MSMEs financial requirements. Credit to the

MSME sector continues to be non-commensurate with its contribution to the total

industrial output. As against the share of the village and MSME at 40% in the industrial

output, its share in total credit to the industrial sector is only about 30%.

b) Raw Material problem of MSMEs:

This difficulty is experienced in a very pronounced form. The quantity, quality and

regularity of the supply of raw materials are not satisfactory. There are no quantity

discounts, since they are purchased in small quantities and hence charged, higher prices

by suppliers. Difficulty is also experienced in procuring semi-manufactured materials.

Page | 21

Financial weakness stands in the way of securing raw materials in bulk in a competitive

market.

c) Production problem of MSMEs:

MSME units suffer from inadequate work space, power, lighting and ventilation,

and safety measures etc. These short comings have tended to endanger the health of

workmen and have adversely affected the rate of production. Many units are following

primitive methods of production. Adoption of modern techniques is either disliked by

the entrepreneurs is not feasible. Wage rates and service conditions of small industries

are not attractive to skilled labor.

d) Technological problem of MSMEs:

Today technology is changing at a very fast phase; it becomes difficult for MSMEs

to cope up with changing technology. Technology up gradation and the frequent need

to renew the equipment has emerged as a big problem.

e) Marketing problem of MSMEs:

As marketing is not properly organized, the helpless artisans are completely at the

mercy of middle man. The potential demand for their goods remains under developed.

The MSMEs have to face the competitions from large scale units in marketing their

products. It causes damage to the growth and stability of MSMEs. MSMEs cannot

afford to spend lavishly for advertisement to promote their sales.

f) Managerial problem of MSMEs:

Small scale industries in our country have suffered from the lack of entrepreneurial

ability to develop initiative and undertake risks in the unexplored industrial fields. The

in efficiency in management comes first among managerial problems. The

entrepreneurial ability of promoters of cottage industries and MSMEs are handicapped

by technical knowhow in the areas of production, finance, accounting and marketing

management.

Page | 22

g) Sickness of MSMEs:

A serious problem which is hampering small and medium sector has been sickness.

Many small units have fallen sick due to one problem or the other. Sickness is caused

by two sets of factors, Internal and external factors. From among the various internal

and external causes of sickness the important ones are bud management, high rate of

capital gearing, inadequacy of finance, short of raw materials, outdated plant and

machinery, low labor productivity etc.

Page | 23

COMPANY

PROFILE

Page | 24

COMPANY PROFILE:

Andhra Bank is a medium-sized public sector bank (PSB), with a network of

1,712 branches, 15 extension counters, 38 satellite offices and 1056 automated teller

machines (ATMs) as on march 31, 2012. Andhra Bank was founded by the eminent

freedom fighter, Dr. Bhogaraju Pattabhi Sitaramayya. The Government of India owns

51.55% of its share capital and is going to increase it to 58% by infusing 1100 crore.

The state owned Life Insurance Corporation of India holds 10% of the shares.

The bank has done a total business of Rs. 1,90,535 crore as on 31.03.2012. The

bank's operations are mostly concentrated in southern India, the region accounts for

over 60% of the bank’s advances and deposits.

Bank is migrating to "Centralized Core Banking Solution"118 Branches have

already migrated to CBS. It is proposed to cover 550 branches by September 2009. This

will benefit the customers, who will have access to banking and financial services

anytime, anywhere through multiple delivery channels. Andhra Bank is a pioneer in

introducing Credit Cards in the country in 1981.

The Bank introduced Internet Banking Facility (AB INFI-net) to all customers of

cluster linked branches. Rail Ticket Booking Facility is made available to all debit card

holders through IRCTC Website through a separate gateway. Corporate Website is

available in English, Hindi and Telugu Languages communicating Bank's image and

information. Bank has been given 'BEST BANK AWARD' a banking technology award

by IDRBT, Hyderabad for extensive use of IT in Semi Urban and Rural Areas on

02.09.2010. IBA Jointly with TFCI has conferred the Joint Runner-up Award to the

Bank in the Bet Payments initiative in recognition of outstanding achievement of the

Page | 25

Bank in promoting ATM Channel. Bank successfully conducted " Bancon 2010", a two

day event at Hyderabad, deliberating on Inclusive Growth - A New Challenge. Kiddy

Bank Scheme, with insurance benefits, was re-launched to inculcate savings habit

among the children. Bank has mobilized nearly 90000 new accounts during 2011-08.

As a part of "Financial Inclusion", Bank adopted two districts, namely,

Srikakulam in Andhra Pradesh and Ganjam in Orissa and achieved 100% coverage.

Bank has introduced Smart Card Scheme Pilot project in Warangal District and the

same will be extended to other Lead Districts in due course. Bank has opened 2.11 lakh

accounts under "No-frill accounts" category till 30.06.2008.

Andhra Bank, along with A P State Government, NABARD, Canara Bank, Indian

Bank, IOB and SBH sponsored the Andhra Pradesh Banker's Institute of

Entrepreneurship Development, which will offer training to unemployed youth for

improving their skills in Andhra Pradesh.

Bank adopted Gundugolanu village, West Godavari District, Andhra Pradesh -

birth place of Dr. Bhogaraju Pattabhi Sitaramayya for all-round development. A

comprehensive budget with an outlay of Rs.5.50 Crore is finalized for improving

health, sanitation, education and social service facilities in the village.

Page | 26

History:

Andhra Bank was founded by Dr. Bhogaraju Pattabhi Sitaramayya in 1923 in

Machilipatnam, Andhra Pradesh. The founder Dr. Bhogaraju Pattabhi Sitaramayya was

an eminent freedom fighter and a multifaceted genius. The Bank was registered on

November 20, 1923 and commenced business on 28 November 1923 with a paid up

capital of Rs 1.00 lakh and an authorised capital of Rs 10.00 lakhs. In 1956, linguistic

division of States was promulgated and Hyderabad was made the capital of Andhra

Pradesh. The registered office of the Bank was subsequently shifted to Andhra Bank

Buildings, Sultan Bazaar, Hyderabad, and Andhra Pradesh. In the second phase of

nationalization of commercial banks commenced in April 1980, the bank became a

wholly owned Government bank. In 1964, the bank merged with Bharat Lakshmi Bank

and further consolidated its position in Andhra Pradesh.

Page | 27

Corporate Identity:

“TOGETHERNESS IS THE THEME”

The Symbol of Infinity denotes a Bank that is prepared to do anything, to go to

any lengths, for the customer

The Blue pointer on the top represents the philosophy of a Bank that is always

looking for growth and newer directions.

The Key hole represents Safety and Security

The Chain indicates togetherness

The colours Red and Blue denote dynamism and solidity

Page | 28

VISION AND MISSION:

Vision:

“Andhra Bank is committed to create a customer centric organization with a deep

sense of social responsibility and to continuously leverage technology to attain world

class standards of performance.”

Mission:

“Beside the core activity of banking, Andhra Bank will venture into a spectrum of

Financial Services. Utmost concern will be accorded to customer satisfaction by

offering innovative and need-based financial products and services using state of the art

technology.”

Products and Services:

The products and services provided by the bank are mainly categorized into

businesses of Retail, Corporate, NRI, MSME, and Agricultural industries. Under the

Retail Business, the bank offers Deposits, Loans, Cards, DMAT Services, Payment

Services, Insurance, and Mutual Funds to individual customers. Under the Corporate

Business, the bank offers Loans & Advances, Project Appraisal services, and

Syndication of Loans to the business entities. Under the NRI business segment, the

bank offers Deposit schemes, Loans, Remittance services, and Investment services to

the Non Resident Indians.

Under the MSME business segment, the bank offers different schemes that

aimed at providing loan and transaction services to Micro Small and Medium

Enterprises (MSME). Some of the MSME schemes available are OTS Scheme,

Composite loan scheme, Open cash credit (OCC), Artisans Credit Card (ACC), AB

Laghu Udhyami Credit Card (LUCC), AB Power Tools (Shakti), Technology

upgradation fund scheme (TUFs), Credit guarantee fund trust for small industries

(CGTSI), AB Doctor Plus...etc. Under the Agriculture business segment, bank provides

different credit schemes to farmers, Women Empowerment schemes, and Andhra Bank

Page | 29

Rural Development Trust (ABRDT) helps Rural Self Employment Training Institutes

(RSETIs).

Deposit Schemes

o AB Savings Accounts

o AB Current Accounts

o AB Term Deposits

o AB Arogyadaan Scheme

o AB Bancassurance Life

o AB Bancassurance (Non Life)

Retail Loans

Agricultural Loans

Corporate Banking

NRI Banking

o NRI Products and Services

o NOSTOR details for remittance

o Western Union Money Transfer

Technology Products

o Multi City Cheque Facility

o On-Line Tax Accounting System (OLTAS)

o Real Time Gross Settlement (RTGS)

o Instant Funds Transfer

o ATM Services

o Any Branch Banking

o Electronic Clearing Service (ECS)

o National Electronic Funds Transfer

Page | 30

Value added services:

Introduced 8 a.m. to 8 p.m. and 7 day banking in select branches to extend the

Service hours to clientele.

Opened a Representative Office in Dubai to coordinate with NRIs for increasing

our NRI customer base.

Imparting training to Agriculturists, Rural Un- employed youth on vocational

courses by our 9 Rural Development Institutes.

Mobile Banking – Connected branches improved to 453, registered users 4175

Daily ATM hits crossed 1 lakh per day.

Mobile Recharging facility

Tech savvy products such as e-Seva, e-Hundi, Utility Bill Payment, Visa Electron

Debit Card, Instant Funds Transfer, On-line Tax Accounting System, RTGS etc.

Various Insurance Linked Deposit products like AB Jeevan Abhaya, AB Jeevan

Prakash, AB Jeevan Prakash Plus, AB Arogyadaan and AB Flex.

New Tech savvy product AB Kisan Vikas ATM Card has been introduced.

Shortly introducing – Internet Payment Gateway, Internet Banking.

Page | 31

Corporate Social Responsibility (CSR):

Being an integral part of society, Bank is aware of its corporate social

responsibilities and has engaged in community and social investments. During the year,

Bank has taken many initiatives with the objective of providing philanthropic assistance

for development, education etc.

Under the aegis Andhra bank rural development trust bank is imparting training to

youth in rural and semi urban areas so that poor people can take up self

employment ventures. They also conduct vocational and human resource

development training. So far they have provided training to 71,666 participants.

The bank has taken initiatives for including more people from the marginalized

and down trodden sections into the banking system. The bank has already

implemented financial inclusions in districts of Orissa and Andhra Pradesh.

During the year '07-08' the bank has adopted Gundugolanu village in Andhra

Pradesh for improving health, sanitation, education facilities with a comprehensive

budget of 5.50 cr.

The bank is setting up a school in the campus of Andhra University in

Vishakhapatnam.

Along with the Andhra Pradesh Government and NABARD, it has set up

APBIRED for providing training to unemployed youth for improving their skills.

In the year 2011-2008, the bank has donated 2.14 cr to various trusts and NGOs.

Under the aegis of Andhra Bank Rural Development Trust, Bank is imparting

training to youth in rural and semi-urban areas so that the poor people can take up

self-employment ventures. This also conducts various vocational and human

resource development training programmes. So far, training has been imparted to

71,666 participants in self-employment ventures and in capacity building.

The Bank has taken initiatives towards implementing financial inclusion in some

of the districts for bringing more and more people of the marginalized and the

downtrodden sections into banking system.

The Bank has already implemented 100% financial inclusion in the districts of

Srikakulam (Andhra Pradesh) and Ganjam (Orissa). During the year 2011-08,

Page | 32

Bank has adopted the Gundugolanu village in the district of West Godavari in

Andhra Pradesh tor improving health, sanitation, education and social service

facilities in the village, with a comprehensive budget of Rs. 5.50 crore.

In a move towards encouraging higher studies, Bank is setting up Andhra Bank

School of Business in the campus of Andhra University, Visakhapatnam (Andhra

Pradesh).

The Bank along with Government of Andhra Pradesh, NABARD and other select

banks sponsored the Andhra Pradesh Bankers / Institute of Rural & Entrepreneurship

Development (APBIRED), which will offer training to unemployed youth for

improving their skills. This is located at Hyderabad. The Bank is also making donations

to charitable trusts and other institutions engaged in the upliftment of the society.

As per Karmayog.org research work they ranked Andhra Bank as No. 3

organization out of top organizations with regard to corporate social responsibility.

Page | 33

CONCEPTUAL

FRAME WORK

Page | 34

Theoretical Aspects:

Overview of Credit Appraisal

Credit appraisal means an investigation/assessment done by the banks before

providing any Loans & advances/project finance & also checks the commercial,

financial & technical viability of the project proposed, its funding pattern & further

checks the primary & collateral security cover available for recovery of such funds.

Brief overview of Credit

Credit Appraisal is a process to ascertain the risks associated with the extension of

the credit facility. It is generally carried by the financial institutions, which are involved

in providing financial funding to its customers. Credit risk is a risk related to non-

repayment of the credit obtained by the customer of a bank. Thus it is necessary to

appraise the credibility of the customer in order to mitigate the credit risk. Proper

evaluation of the customer is performed this measures the financial condition and the

ability of the customer to repay back the Loan in future. Generally the credits facilities

are extended against the security know as collateral. But even though the Loans are

backed by the collateral, banks are normally interested in the actual Loan amount to be

repaid along with the interest. Thus, the customer's cash flows are ascertained to ensure

the timely payment of principal and the interest.

It is the process of appraising the credit worthiness of a Loan applicant. Factors

like age, income, number of dependents, nature of employment, continuity of

employment, repayment capacity, previous Loans, credit cards, etc. are taken into

account while appraising the credit worthiness of a person. Every bank or lending

institution has its own panel of officials for this purpose.

Page | 35

However the 3 ‘C’ of credit are crucial & relevant to all borrowers/ lending, which

must be kept in mind, at all times.

Character

Capacity

Collateral

If any one of these are missing in the equation then the lending officer must question

the viability of credit. There is no guarantee to ensure a Loan does not run into

problems; however if proper credit evaluation techniques and monitoring are

implemented then naturally the Loan loss probability / problems will be minimized,

which should be the objective of every lending Officer.

Credit is the provision of resources (such as granting a Loan) by one party to another

party where that second party does not reimburse the first party immediately, thereby

generating a debt, and instead arranges either to repay or return those resources (or

material(s) of equal value) at a later date. The first party is called a creditor, also known

as a lender, while the second party is called a debtor, also known as a borrower.

Credit allows you to buy goods or commodities now, and pay for them later. We use

credit to buy things with an agreement to repay the Loans over a period of time. The

most common way to avail credit is by the use of credit cards. Other credit plans include

personal Loans, home Loans, vehicle Loans, student Loans, small business Loans, trade.

A credit is a legal contract where one party receives resource or wealth from another

party and promises to repay him on a future date along with interest. In simple Terms, a

credit is an agreement of postponed payments of goods bought or Loan. With the

issuance of a credit, a debt is formed.

Page | 36

Basic types of credit

There are four basic types of credit. By understanding how each works, you

will be able to get the most for your money and avoid paying unnecessary charges.

Service credit is monthly payments for utilities such as telephone, gas,

electricity, and water. You often have to pay a deposit, and you may pay a late

charge if your payment is not on time.

Loans let you borrow cash. Loans can be for small or large amounts and for a

few days or several years. Money can be repaid in one lump sum or in several

regular payments until the amount you borrowed and the finance charges are

paid in full. Loans can be secured or unsecured.

Installment credit may be described as buying on time, financing through the

store or the easy payment plan. The borrower takes the goods home in exchange

for a promise to pay later. Cars, major appliances, and furniture are often

purchased this way. You usually sign a contract, make a down payment, and

agree to pay the balance with a specified number of equal payments called

installments. The finance charges are included in the payments. The item you

purchase may be used as security for the Loan.

Credit cards are issued by individual retail stores, banks, or businesses. Using a

credit card can be the equivalent of an interest-free Loan- end of each month.-if

you pay for the use of it in full at the

Brief overview of Loans

Loans can be of two types fund base & non-fund base:

Fund Base includes:

Working Capital

Term Loan

Page | 37

Non-fund Base includes:

Letter of Credit

Bank Guarantee

Bill Discounting

Fund Base:

Working capital

The objective of running any industry is earning profits. An industry will require

funds to acquire “fixed assets” like land, building, plant, machinery, equipments,

vehicles, tools etc., & also to run the business i.e. its day-to-day operations.

Funds required for day to-day working will be to finance production & sales. For

production, funds are needed for purchase of raw materials/ stores/ fuel, for employment

of labor, for power charges etc. financing the sales by way of sundry debtors/

receivables.

Capital or funds required for an industry can therefore be bifurcated as fixed capital

& working capital. Working capital in this context is the excess of current assets over

current liabilities. The excess of current assets over current liabilities is treated as net,

for storing finishing goods till they are sold out & for working capital or liquid surplus

& represents that portion of the working capital, which has been provided from the long-

Term source.

Term Loan

A Term Loan is granted for a fixed Term of not less than 3 years intended normally

for financing fixed assets acquired with a repayment schedule normally not exceeding 8

years.

A Term Loan is a Loan granted for the purpose of capital assets, such as purchase of

land, construction of, buildings, purchase of machinery, modernization, renovation or

Page | 38

rationalization of plant, & repayable from out of the future earning of the enterprise, in

installments, as per a prearranged schedule.

From the above definition, the following differences between a Term Loan & the

working capital credit afforded by the Bank are apparent:

o The purpose of the Term Loan is for acquisition of capital assets.

o The Term Loan is an advance not repayable on demand but only in installments

ranging over a period of years.

o The repayment of Term Loan is not out of sale proceeds of the goods & commodities

per se, whether given as security or not. The repayment should come out of the future

cash accruals from the activity of the unit.

o The security is not the readily saleable goods & commodities but the fixed assets of

the units.

It may thus be observed that the scope & operation of the Term Loans are entirely

different from those of the conventional working capital advances. The Bank’s

commitment is for a long period & the risk involved is greater. An element of risk is

inherent in any type of Loan because of the uncertainty of the repayment. Longer the

duration of the credit, greater is the attendant uncertainty of repayment & consequently

the risk involved also becomes greater.

However, it may be observed that Term Loans are not so lacking in liquidity as they

appear to be. These Loans are subject to a definite repayment programme unlike short

Term Loans for working capital (especially the cash credits) which are being renewed

year after year. Term Loans would be repaid in a regular way from the anticipated

income of the industry/ trade.

These distinctive characteristics of Term Loans distinguish them from the short Term

credit granted by the banks & it becomes necessary therefore, to adopt a different

approach in examining the applications of borrowers for such credit & for appraising

such proposals.

The repayment of a Term Loan depends on the future income of the borrowing unit.

Hence, the primary task of the bank before granting Term Loans is to assure itself that

Page | 39

the anticipated income from the unit would provide the necessary amount for the

repayment of the Loan. This will involve a detailed scrutiny of the scheme, its capital

assets. Financial aspects, economic aspects, technical aspects, a projection of future

trends of outputs & sales & estimates of cost, returns, flow of funds & profits.

Non-fund Base:

Letter of credit

The expectation of the seller of any goods or services is that he should get the

payment immediately on delivery of the same. This may not materialize if the seller &

the buyer are at different places (either within the same country or in different

countries). The seller desires to have an assurance for payment by the purchaser. At the

same time the purchaser desires that the amount should be paid only when the goods are

actually received. Here arises the need of Letter of Credit (LCs). The objective of LC is

to provide a means of payment to the seller & the delivery of goods & services to the

buyer at the same time.

Definition

A Letter of Credit (LC) is an arrangement whereby a bank (the issuing bank) acting at

the request & on the instructions of the customer (the applicant) or on its own behalf,

o Is to make a payment to or to the order of a third party (the beneficiary), or is to

accept & pay bills of exchange (drafts drawn by the beneficiary); or

o Authorizes another bank to effect such payment, or to accept & pay such bills of

exchanges (drafts); or

o Authorizes another bank to negotiate the Terms & conditions of the credit are

complied with against stipulated document(s), provided.

Page | 40

Bank Guarantees:

A contract of guarantee is defined as ‘a contract to perform the promise or discharge

the liability of the third person in case of the default’. The parties to the contract of

guarantees are:

a) Applicant: The principal debtor – person at whose request the guarantee is executed

b) Beneficiary: Person to whom the guarantee is given & who can enforce it in case of

default.

c) Guarantee: The person who undertakes to discharge the obligations of the applicant

in case of his default.

Thus, guarantee is a collateral contract, consequential to a main co applicant & the

beneficiary.

Purpose of Bank Guarantees

Bank Guarantees are used to for both preventive & remedial purposes. The guarantees

executed by banks comprise both performance guarantees & financial guarantees. The

guarantees are structured according to the Terms of agreement, viz., security, maturity &

purpose.

Branches may issue guarantees generally for the following purposes:

a) In lieu of security deposit/earnest money deposit for participating in tenders;

b) Mobilization advance or advance money before commencement of the project by the

contractor & for money to be received in various stages like plant layout,

design/drawings in project finance;

c) In respect of raw materials supplies or for advances by the buyers;

d) In respect of due performance of specific contracts by the borrowers & for obtaining

full payment of the bills;

e) Performance guarantee for warranty period on completion of contract which would

enable the suppliers to period to be over; realize the proceeds without waiting for

warranty) To allow units to draw funds from time to time from the concerned

indenters against part execution of contracts, etc.

Page | 41

f) Bid bonds on behalf of exporters

g) Export performance guarantees on behalf of exporters favoring the Customs

Department under EPCG scheme.

Bill discounting:

Definition:

As per Negotiable Instrument Act, “The bill of exchange is an instrument in

writing containing an unconditional order, signed by the maker, directing a certain

person to pay a certain sum of money only to, or to the order of, a certain person, or to

the bearer of that instrument.”

Discounting of bill of exchange:

A seller (Drawer) if need cash, may handover the B/E to the Bank, NBFC, a

company or a high Net worth Individual and obtain ready cash this is known as

discounting of bill. the practice in India is that, the financing organization holds the

original B/E till the drawee pays on maturity. For discounting the bill, financiers charge

an interest on the bill amount for the duration of the bill which is called discount

charges.normal maturity periods are 30, 60, 90, 120 days.

Types of Bills

1. Demand Bill

2. Usance Bill

3. Documentary Bills

a. Documents against acceptance (D/A) bills

b. Documents against payment (D/P) bills

4. Clean Bills

Page | 42

Advantages

To Investors

1. Short Term source of finance

2. Outside the purview of Section 370 of Indian Companies Act 1956

3. No tax deducted at source

4. Flexibility

To Banks

1. Safety of funds

2. Certainty of payment

3. Profitability

Page | 43

Credit Appraisal Process

Receipt of application from applicant

Receipt of documents

(Balance sheet, KYC papers, Different govt. registration no., MOA, AOA, and

properties documents

Pre-sanction visit by bank officers

Check for RBI defaulters list, willful defaulters list, CIBIL data, ECGC, Caution list

etc

Title clearance reports of the properties to be obtained from empanelled

Advocates

Proposal preparation

Valuation reports of the properties to be obtained from empanelled valuer/engineers

Preparation of financial data

Assessment of proposal

Page | 44

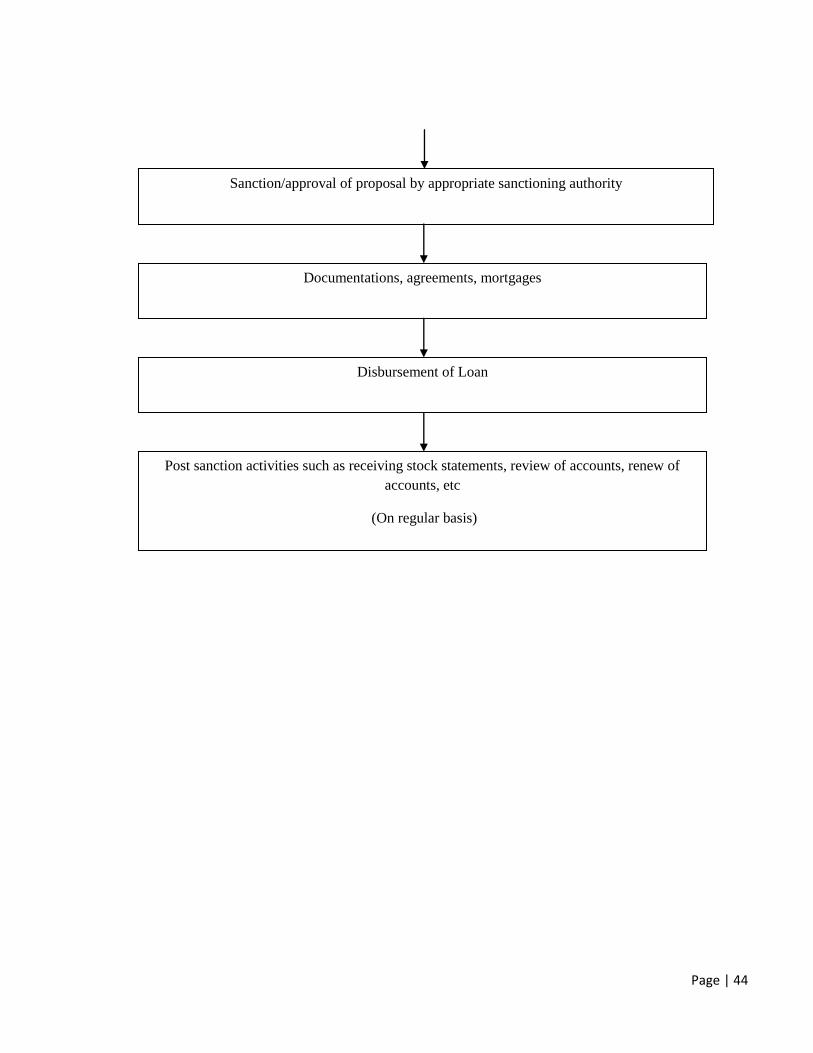

Documentations, agreements, mortgages

Sanction/approval of proposal by appropriate sanctioning authority

Disbursement of Loan

Post sanction activities such as receiving stock statements, review of accounts, renew of

accounts, etc

(On regular basis)

Page | 45

CREDIT PROCESS

Pre-Sanction Process

Indicative list of Activities in the Appraisal Function

A. Preliminary appraisal

Obtain

i. Application for working capital Finance

ii. Audited financial for the previous three years

iii. Details of existing borrowing arrangements

iv. Reports from existing Banker on the application copy

v. Financial statements, borrowings relationship of Associate

firm/group companies

vi. Profile of promoters /senior management personnel

If request includes project financing, obtain additional:

i. Project report

ii. Appraisal report form Financial institutions in case Appraisal

has been done by them

iii. NOC form term lenders if already financed by them

iv. Report form Merchant bankers in case capital market is being

accessed

Examine the following:

i. Bank’s lending policy/RBI guidelines, policies

ii. Prudential Exposure norms

iii. Industry Exposure restrictions

iv. Group Exposure restrictions

v. Industry related risk factor List of defaulters

vi. Caution lists

vii. Compliances regarding transfer of borrowal accounts from one

bank to another, it applicable

viii. Gov. regulation/legislation impacting on the industry

Page | 46

ix. Acceptability of the promoters

x. Application’s status vis-à-vis other units in the industry

xi. Financial status in broad term and whether it is acceptable

xii. Examine also the following in case of request of project finance :

xiii. Weather the project cost is prima facie acceptable

xiv. Debt/equity gearing proposed and whether acceptable

xv. Promoter’s ability to access capital market for debt/equity support

xvi. Whether critical aspect of project –demand, product cost

profitability etc. are prima facie in order

xvii. Arrived at a preliminary decision to support or not to support the

request.

B. Detailed appraisal

Carry out a detailed appraisal alter a pre-sanction visit to applicant Company/their

office/project site.

Working capital facilities

Examine/Analyze/Assess;

i. Financials (in the prescribed form)

ii. Financial ratio and other ratios relevant to the project- Dividend policy

iii. Other aspects viz.

Depreciation method and Revaluation method

Record of defaults (tax duties etc.)

Pending suits having financial implications (custom excise etc.)

Qualification of balance sheets, Auditor remarks etc.

iv. Trends in sale and probability

v. Past deviation in sale and profit projections

vi. Product capacity & use-past and projected

vii. Estimate/ projections of sales values

viii. Estimated working capital gap with reference to acceptable build up of

inventory/receivable/other current asset.

ix. Project levels whether acceptable

Page | 47

By sourcing information where necessary from:

Stock Exchange Directory financial journals/ publications, professional entities like

INFAC, CMIE etc. with emphasis on following aspects:

Market share of the units under comparison

Unique features

Profitability factors

Financial pattern of the business

Inventory receivable levels

Capacity utilizations

Production efficiency and costs

Bank borrowing patterns

Financial ratio & other relevant ratio

Credit rating

Draw up trading for:

Working capital

Term finance

Opinion reports

Compile opinion report on partners/promoters and the proposed

guarantors

Review of the proposal

Strength and weakness of the exposure proposed

Risk factor and steps proposed to mitigate them

Deviations proposed from usual norms of the bank and the reasons

Proposal of sanction:

Prepare a draft proposal in prescribed format with required back-up details

and with recommendations for sanction

Page | 48

Sanction

Indicative list of Activities Involve in the sanction Function

Peruse the proposal to see if the report prima facie presents the

proposal; remit it back to the Assessor for the required

data/clarifications.

Examine critically the following aspect of the proposed

exposure

1. Bank’s lending policy

2. Borrowers status in the industry

3. Industry aspect

4. Experience with units in similar industry

5. Overall strength of the borrower

6. Project level of operation

7. Risk Factors critical to the exposure and adequacy of

safeguards there against proposed.

8. Value of existing connection with the borrower

9. Credit risk rating

10. Security pricing charges and concessions proposed for the

exposure and covenants stipulated vis-à-vis the risk perception

POST SANCTION PROCESS

1. Follow up

The follow-up functions will cover the following:

(a) Ensuring on an ongoing basis compliance with terms and conditions of

sanction through the system of control measures/feedback viz. Inspection

visits, prescribed financial/ operation statements from the borrower interaction

with borrower etc.

Page | 49

(b) Tracking performance of the borrower, ensuring safety and recoverability

of the advances

(c) Ensuring compliance with all the internal and external reporting

requirements covering the advances.

Indicative list of the activities involved in the Follow-up function is as follows:

Conveying sanction of advances to the borrower detailing the terms and

conditions and obtaining acceptance thereof

Preparation-submission of control returns for sanction

CMA reporting of sanction where applicable

Completion of applicable documentation; maintaining custody and validity

of the documents.

Creation of charge over security and completion of all relevant and

applicable formalities, including:

1. Creation of Registered or Equitable mortgage

2. Creation of second charge

3. Registration of charge with ROC

4. Periodical search of charge with ROC

Ongoing scrutiny of transaction in the various accounts by perusal of leaders,

registers, vouchers etc. to watch for proper conduct of the accounts, healthy turnover

therein and proper- end use of funds.

Ongoing verification of assets charged as security, to ensure availability and safety

of the assets.

Maintaining ongoing contact with the borrower and co-leaders and keeping abreast

of developments in the borrower entities and business environment.

Preparation of reviews of IRAC, identification of deterioration assets and

initiations of corrective action where warranted.

Account wise follow up of NPAs for recovery /rehabilitation, preparation of

related recommendations to appropriate authority for approval.

Page | 50

Supervision

i. Supervision function should primarily ensure that the effective fallow of

advances is in the place of the asset quality of good order is maintained.

Supervisor should look out for early warning signals, identity ‘incipient

sickness’ and initiate proactive remedial actions.

ii. Indicative list of activities involved in supervision function is as follows

Ensuring proper flow-up of advances and observations at the operating level of

the system laid down by the bank. Periodic and random examination of

statements received, control register and files/record covering the advance will

assist this process.

Ensuring the security documents are kept current and that all related

documentation formalities are observed by the officials responsible.

Ensure that the function at the follow-up level are performed diligently and as

per extant instructions of the bank.

Monitoring and Controlling

i. Monitoring and controlling function ensures that effective supervision is

maintained on advance and appropriate responses are initiated whenever early

warning signals are seen. The function also tracks customer satisfaction and

provides responses where necessary.

ii. Indicative list of activity involved in monitoring control function are as follows:

Ensure that the effective supervision id maintained on advance by the lower level

functionaries responsible for follow-up and supervision scrutiny of returns /

reports received from these line functionaries, interaction with them, feedback

from the customer, commentary in inspection/audit reports etc. will assess this

process.

Monitoring high value advances through specific focus on these in the

return/report received on advance and by keeping watch on the developments in

the borrower company/industry

Page | 51

Ensuring non-recurrence at the operating level of the company noticed

lapses/irregularities pointed out in various audit reports.

Ongoing monitoring of asset portfolio by tracking changes from time to time;

chalk out and arrange for carrying out specific action to ensure high standard

asset content.

Extending guidelines to down the line functionaries on the follow-up and

‘supervision’ of the exposures at risk.

Assessment of Risk, Profitability and Efficiency:

1. Industry Risks

2. Management Risks

3. Operational Risks

4. Collateral Security

5. Financial Risks

a) Industry Risks:

i) Production stage

(1) Raw materials

(2) Power, Fuel, Labour

(3) Technology

(4) Infrastructure

(5) R & D

ii) Post Production Process

(1) Demand

(2) Competition

(3) Marketing arrangements

Page | 52

b) Management risks:

i) Promoters

(1) Experience of the group

(2) Management proficiency

(3) Experience of promoters

(4) Employed executives

c) Operational risks:

i) Supply of information to banks

ii) Record of irregularity

iii) Limit management

iv) Compliance of sanction stipulations

d) Collateral security:

i) Collateral cover

e) Financial risks:

i) Liquidity

(1) Current ratio

(2) Non-working capital

ii) Profitability

(1) Operational profit

(2) Return of capital employed

(3) Net profit

iii) Interest coverage

(1) PBDIT / Interest

(2) Term indebtness

(3) Overall indebtness

iv) Efficiency in utilization of current assets

Page | 53

Interpretation:

Above tables shows how Banks assess the risk, profitability and efficiency. In

order to award loan to the business entity banks has to look in to the risk, return and

efficiency by using the past and present information available about the company. Banks

consider the following factors to assess the risk.

Industry Risk

Here the banks will look in to the all risk factors that related to an industry. Include

the production stage risk and post production risk. Production stage risk assessed by

considering the factors like raw materials, technology, Infrastructure etc and post

production risk involves demand, competition and marketing challenges.

Management Risk

Promotes experience, management proficiency, employed executives are the

factors which comes here.

Operational risk

Here banks look in to the past records of the customer’s transactions. Supply of

information to the bank, record of the irregularities and compliance of sanctions and

stipulations are considered here.

Collateral security

The collateral cover offered by the customer review comes here.

Financial risk

Liquidity, profitability and interest coverage ratios are assessed here to determine

short term and long term solvency of the company.

Page | 54

CREDIT APPRAISAL STANDARDS:

QUALITATIVE:

At the outset, the proposition is examined from the angle of viability and also from

the bank prudential levels of exposure to the borrower, group and industry. Thereafter, a

view is taken about bank’s past experience with the promoters, if there is a track record

to go by. Where it is a new connection for the bank but the entrepreneurs are already in

business, opinion reports from existing bankers and published data if available are

carefully perused.

In case of a maiden venture, in addition to the drill mentioned heretofore, an

element of subjectivity has to be perforce introduced as scant historical data would be

available and weightage has to be placed on impressions gained out of the serious

dialogues with the promoters and his business contacts.

QUANTITATIVE:

1. Working capital: the basic quantitative parameters underpinning the Bank’s

credit appraisal are as follows:

i. Liquidity: current ratio (CR) of 1.33 will generally be considered as a

benchmark level of liquidity. However, the approach has to be flexible. Cr of

1.33 is only indicative and may not be deemed mandatory. In cases where the

Cr is projected at a level lower than the benchmark or a slippage in the CR is

proposed, it alone will not be a reason for rejection of the loan proposal or for

sanction of loan. In such cases, the reasons for low CR should be carefully

examined and in deserving cases the CR as projected may be accepted. In cases

where projected CR is found acceptable, working capital finance as requested

may be sanctioned.

ii. Net working capital: although this is a corollary of current ratio, the

movements in Net working capital are watched to ascertain whether there is a

mismatch of long term sources via-a-vis long term uses for purposes which

may not be readily acceptable to the Bank so that corrective measures can be

suggested.

Page | 55

iii. Financial Soundness: this will be dependent upon the owner’s stake or the

leverage. Here again the benchmark will be different for manufacturing,

trading, hire purchase and leasing concerns. For industrial ventures Total

Outside Liability/Tangible Net Worth ratio of 6.0 is reasonable but

deviations in selective cases for understandable reasons may be accepted by the

sanctioning authority.

iv. Turn –over: the trend in turn-over is carefully gone into both in terms of

quantity and value as also market share wherever such data are available. What

is more important is to establish a steady output if not a rising trend in

quantitative terms because sales realization may be varying on account of price

fluctuations.

v. Profits: while net Profit is the ultimate yardstick, cash accruals, i.e. profit

before depreciation and taxation conveys the more comparable picture in view

of changes in rate of depreciation and taxation which may have taken place in

the intervening years. However, for the sake of proper assessment, the non-