Embed Size (px)

DESCRIPTION

EVERYTHING THAT YOU NEVER WANTED TO KNOW ABOUT THE INFAMOUS BANK DEBENTURE PRIVATE PLACEMENT TRADING PROGRAMS (PPP) and much more

Citation preview

by Ralphh Joseph Philippii

ii

TITLE PAGE

PUBLISHER:

PROSPERITY INTERNATIONAL CORPORATION, LIMITED

ROOM 813, HOLLYWOOD PLAZA

610 NATHAN ROAD, KOWLOON, HONG KONG

PH.: +852 2132 9661 OR +86 898 6857 2551

FAX: +852 3007 1270 E-MAIL: [email protected]

CONTACT: RALPH JOSEPH PHILIPPI, Director, and Author

TITLE: “EVERYTHING THAT YOU NEVER WANTED TO KNOW ABOUT THE INFAMOUS BANK DEBENTURE PRIVATE PLACEMENT TRADING PROGRAMS (PPP) AND MUCH MORE”

FIRST PUBLISHED: 26 July 2010

RELEASE DATE: 9 August 2010

ISBN 978-988-19313-1-3

All rights are reserved. No part of this Book can be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior written permission from RALPH

JOSEPH PHILIPPI, the Author, except in the case of brief quotations embodied in critical articles and reviews.

Please refer all pertinent questions, or comments, to the Author. The Author is responsible for the contents of this Book.

PRINTED IN HONG KONG by, PROSPERITY INTERNATIONAL CORPORATION, LIMITED.

THIS IS AN ENGLISH LANGUAGE PUBLICATION.

THIS Book consists of 272 pages, as a HARD BOUND BOOK, IN ITS ORIGINAL FORM, BUT IT IS

ALSO BEING MADE AVAILABLE IN AN ELECTRONICALLY TRANSMITTABLE VERSION.

This Book IS “NOT INTENDED TO BE FOR SALE”.

THIS BOOK IS INTENDED TO “HELP PEOPLE”, and it will be given “FREE-OF-CHARGE” to anyone who desires to have an original of this Book in the electronically transmittable version only. Hard Bound Books are available, at our costs of printing, binding, and shipping.

The picture on the front cover is titled “The Wishing Lamp”, from STOCK.EXCHNG. Refer to the “Appreciation & Acknowledgement” Section of this Book for further information.

iii

PEOUR

EACE AN

iv

R WISHND PROTO ALL

H OF OSPERITL

TY

Reainforeadnot form No wardisc Usepoliperm Theassodamconsfrom Thisfor No c Thepurpoffe

sonable rmation der shou constitum. Profe

Liabilityrranties. claimed.

of this cy. If mitted to

Authoociates,

mages sequent

m the us

s Book isnon-com

copyrigh

informposes o

er, to buy

care presentuld undeute legaessionals

y: This All wa

Book, cyou do

o use, or

or, Puband affiwhatso

ial loss e of this

s being wmmercial

ht infring

ation conly, andy or sell

Dis

has beted in therstand tl, financ

s in these

Book rranties

constitut not agr distribu

lisher, iliates, soever,

or dams Book, s

written, , educat

gement i

ontainedd is not any form

v

sclaim

een takhis Bookthat thecial, or e fields s

is supp, expres

tes accegree witute, this

their eshall not

includinmage, dishould a

publishetional pu

s intend

in thist intendem of sec

mer

ken to k is accue informaprofessishould a

plied “assed or

ptance oh this p product

employet be liabng, wrectly ony occur

ed, and gurposes o

ed.

s Book ed as a

curities, o

ensurerate. Hation pronal adv

always b

s is” aimplied,

of the “policy, yt.

es, stale for an

without r indirer.

given freonly.

is for ina solicitaor anyth

e that owever,ovided dvice, in e consul

and with are her

No Liabiyou are

aff, ageny losse

limitatctly, ari

ee-of-cha

nformatiation, orhing else

the the does any

lted.

hout reby

ility” not

ents, es or tion, ising

arge,

onal r an

e.

vi

“Have patience with all things,

but chiefly have patience with yourself. Do not lose courage in considering your own imperfections

but instantly set about remedying them? Every day begin the task anew.”

-- Saint Francis de Sales --

vii

EDICATION

This Book is dedicated to all of you, whom have tried, and lost, and probably, a whole lot more than

mere money, over your quest of trying to win at the PPP Game.

I have known of many, some personally, whom have lost everything, including their business, family, home, and even their self-esteem, over their personal quest of attempting to win at the PPP Game.

It is said “Knowledge is Power”, which is what I certainly do hope that this Book will bring to all of you.

It is extremely difficult, if not impossible, to play a game that you do not know the rules to. This would be like me attempting to win at playing

Mahjong, a real impossibility. Therefore, I do not even attempt to play that game, not even for fun, as it is often said.

May your God, by whichever name you choose to call that Entity by, or any other Power of the Universe that you may believe in, be with each and every one of you, in all of your quests, especially in your quest of PPP.

Believe me, you are going to need all of the help that you can obtain, from everywhere and anywhere possible, if you are intent on playing the PPP Game. Good Luck to all of you, whom decide on taking the course, of

either, staying in, or entering, the PPP Game. The basic rules are in here.

May Peace, Prosperity, and the Powers of Enlightenment, be with all,

Ralph Joseph Philippi Author

D

viii

“All right Mister, let me tell you what winning

means? You're willing to go longer, work harder, and give more than anyone else.”

-- Vince Lombardi --

I WAN

CONTR

STOCK

I WOU

AT, A

ESPEC

IT WO

OTHER

WOND

FROM, NO ON

THANK

I WOU

PERSO

GIVEN

SOME

MUCH.

A PPRECIA

NT TO EXT

RIBUTORS

K.EXCHNG

ULD ALSO

AND CON

IALLY THE

OULD HAV

R BOOKS

DERFUL PH

, IT IS INC

NE CAN PO

K YOU ALL

ULD ALSO

ONS / AUT

“JUST DU

OF THIS I

. THE INF

A ATION &

TEND MY

S TO:

G – http

LIKE TO E

NTRIBUTOR

E CONTRI

VE BEEN E

S, TOGET

HOTOS. YCREDIBLE.

OSSIBLE V

L, VERY M

O LIKE TO

THORS OF

UE” TO, BINFORMAT

FORMATIO

ACKNOW

SINCERE

://www

EXTEND M

RS TO

BUTORS T

EXTREMEL

THER, W

YOU HAVE

.

VIEW ALL O

UCH. ALL

EXPRESS

F MATERIA

ECAUSE ITION FRO

ON THAT Y

ix

WLEDGEM

ST APPRE

.sxc.hu/

MY SINCER

flickr

TO “CREAT

LY DIFFICU

WITHOUT

SO MANY

OF THEM,

L OF YOU

S MY HEA

ALS USED

I DO NOT

M. HOWE

YOU PROVI

MENT

ECIATION

/

REST APPR

@ httTIVE COM

ULT TO P

A NICE

Y WONDER

IN A LIFE

ARE APPR

RTFELT A

IN THIS B

REMEMBE

EVER, TH

IDED TO M

TO THE

RECIATION

p://wwwMMONS”.

UT THIS

SELECT

RFUL PHOT

E TIME.

RECIATED

APPRECIAT

BOOK, WH

ER WHERE

ANK YOU

ME IS NOW

FOLKS AT

N TO THE

w.flickr.c

BOOK, A

TION OF

TOS TO C

.

TION TO, HICH I HAV

I HAVE G

, ALL, SO

W BEING U

T, AND

FOLKS

com/,

AND MY

YOUR

HOOSE

OTHER

VE NOT

GOTTEN

O VERY

USED.

x

ROAD LESS TRAVELED

Two roads diverged in a yellow wood

And sorry I could not travel both And be one traveler, long I stood

And looked down one as far as I could To where it bent in the undergrowth

Then took the other as just as fair

And having perhaps the better claim Because it was grassy and wanted wear

Through as for that, the passing there Had worn them really about the same

And both that morning equally lay In leaves, no step had trodden black Oh, I kept the first for another day!

Yet, knowing how way leads onto way I doubted if I should ever come back

I shall be telling this with a sigh Somewhere ages and ages hence Two roads diverged in a wood

And I took the one less traveled by And that has made all the difference

-- Robert Lee Frost --

xi

REFACE

As you begin to read through his Book, you will see that you are being given a whole lot of background information, based upon fact and history, which is boring to read, but important for you to understand, even if it is just for your general understanding and knowledge, for it will serve you well, in your everyday life, including those of you that are construction, factory, or officer, worker. This information will serve you well. In most of my other books, I have refrained from using as many big words, and words that are only familiar to the professionals, as I possibly can, because when you go past a word that you do not understand, that is where boredom enters, and your learning stops. Unfortunately, in this Book, I must use some these types of words that you may not be familiar with, therefore, I strongly suggest that you keep a dictionary beside you, as you go over the information inside of this Book. You, even, may want to look us some of the words, and phrases, used, on the internet, in a financial, or law, dictionary. This Book will not be an easy book for you to go through, and understand everything that you have read, your first time through, because I am assembling the parts of a puzzle for you, piece-by-piece. Therefore, you may have to go through this material several times, before you are able to see the entire picture, clearly. However, I can assure you that the entire picture is being presented in this Book, with just a few details being intentionally left out, which are the ones that do not concern you, because there are different levels to this Game, commonly referred to as the international and national financial systems. Many of which are not important for you to know, or understand, and, much better that you do not. I have not left out any of the important information, which you do need to assimilate (absorb) and understand, for you to gain a proper knowledge of this field. In addition, be ready for some big surprises, as you go through this information, and, some aspects that you are going to find very difficult to believe, also, but all of the information in the Book is based upon fact, not fiction. It is, as it is, and, you are going to come to know, exactly as it actually is. Much of the information within this Book is taken from my set of 8 books, entitled, “The National Prosperity Plan”, soon to be on line, the basics herein, are the same basic information as is presented in the first part of this Book, which is fully compatible with, and implemental within, the scope of System 2000, and, in compliance with all applicable, international rules, regulations, and laws.

P

xii

"The reason most people never reach their goals is that they don't define them, learn about them,

or even seriously consider them as believable or achievable. Winners can tell you where they are going,

what they plan to do along the way, and who will be sharing the adventure with them."

-- Denis Waitley --

xiii

NTRODUCTION

I would like to do some clarification to begin with, because as you start reading through this Book, you may get the initial impression that this Book is just too complicated and/or too complex for you to be able to understand and digest most of it. So, as I said before, keep your dictionary close at hand, and use it, on every word that you do not completely understand, please do look those up, every time that you come across one of these. Then, just take a few general notes, jotting down the page numbers of the notes that you take. Slowly, but surely, a clear picture will start to develop, of the complex system that this Book is explaining to you, in the simplest terms available. It is this basic information that will develop the foundation for the advanced information that will be developed towards the end. It is not necessary for you to remember all of the historical information given to you in the first Eight Chapters, and part of the Ninth Chapter, of this Book. You can always go back to that information, as you need to, or, when you have not gotten a clear picture of how the present system works, and why. You will need to understand the historical aspects of our present financial system, to be able to fully understand how it actually works, and why, because that is, where the benefit to you will come from. You will not only come to know and understand the rules of this Game, but the “how” and “why” they came in to existence, which will form your operational foundation. Specific rules may change from time to time, but the underlying principles will never change, until The System does, which will not be up to you or me to do, even though it will have to be changed some day, because what we presently have is not sustainable, but so be it, for now. It will have to be changed, when the time is right, not before. The emphasis of this Book is for you to be able to gain an understanding of what we presently have, and how to operate within its structure. Nothing more, and certainly nothing less, along with a certain perspective towards international law, is what will be presented to you in this Book.

Enjoy !!!

I

xiv

“Ever notice that people never say

‘It's only a Game’ when they're Winning?”

-- Ivern Ball --

xv

ABLE OF CONTENTS

TITLE PAGE ................................................................................................... ii

DISCLAIMER ................................................................................................. v

DEDICATION ................................................................................................ vii

APPRECIATION & ACKNOWLEDGEMENT ............................................................ ix

PREFACE ..................................................................................................... xi

INTRODUCTION ........................................................................................... xiii

TABLE OF CONTENTS ................................................................................... xv

CHAPTER 1 - THE HISTORY OF BANKING ........................................................... 1

EARLIEST BANKS ........................................................................................ 1

RELIGIOUS RESTRICTIONS ON INTEREST ...................................................... 2

DURING LATE ANTIQUITY AND MIDDLE AGES ................................................. 3

WESTERN BANKING HISTORY ....................................................................... 6

CAPITALISM ............................................................................................... 6

GLOBAL BANKING ....................................................................................... 6

MAJOR EVENTS IN BANKING HISTORY ........................................................... 8

OLDEST PRIVATE BANKS ............................................................................. 9

OLDEST NATIONAL BANKS ......................................................................... 10

UNITED STATES BANKING ......................................................................... 10

CHAPTER 2 - THE HISTORY OF MONEY ............................................................ 13

BARTER ................................................................................................... 13

COMMODITY MONEY ................................................................................. 13

REPRESENTATIVE MONEY .......................................................................... 14

WAREHOUSE RECEIPTS ............................................................................. 15

TALLIES .................................................................................................. 16

TRADE BILLS OF EXCHANGE ...................................................................... 17

T

xvi

GOLDSMITH BANKERS ............................................................................... 18

BANKNOTES ............................................................................................ 19

DEMAND DEPOSITS .................................................................................. 20

GOLD-BACKED BANKNOTES ....................................................................... 20

FIAT MONEY ............................................................................................ 21

CHAPTER 3 - THE HISTORY OF ACCOUNTING ................................................... 23

EARLY HISTORY ....................................................................................... 23

LUCA PACIOLI AND THE BIRTH OF MODERN ACCOUNTANCY ........................... 23

POST-PACIOLI .......................................................................................... 24

ACCOUNTANCY QUALIFICATIONS AND REGULATION ..................................... 25

THE "BIG FOUR" ACCOUNTANCY FIRMS ....................................................... 26

CHAPTER 4 - BASIC ACCOUNTING .................................................................. 29

CHAPTER 5 - DEBITS AND CREDITS ............................................................... 35

INTRODUCTION ........................................................................................ 35

ORIGIN OF THE TERMS DEBIT AND CREDIT .................................................. 37

PRINCIPLES OR RULES OF DEBIT AND CREDIT ............................................. 40

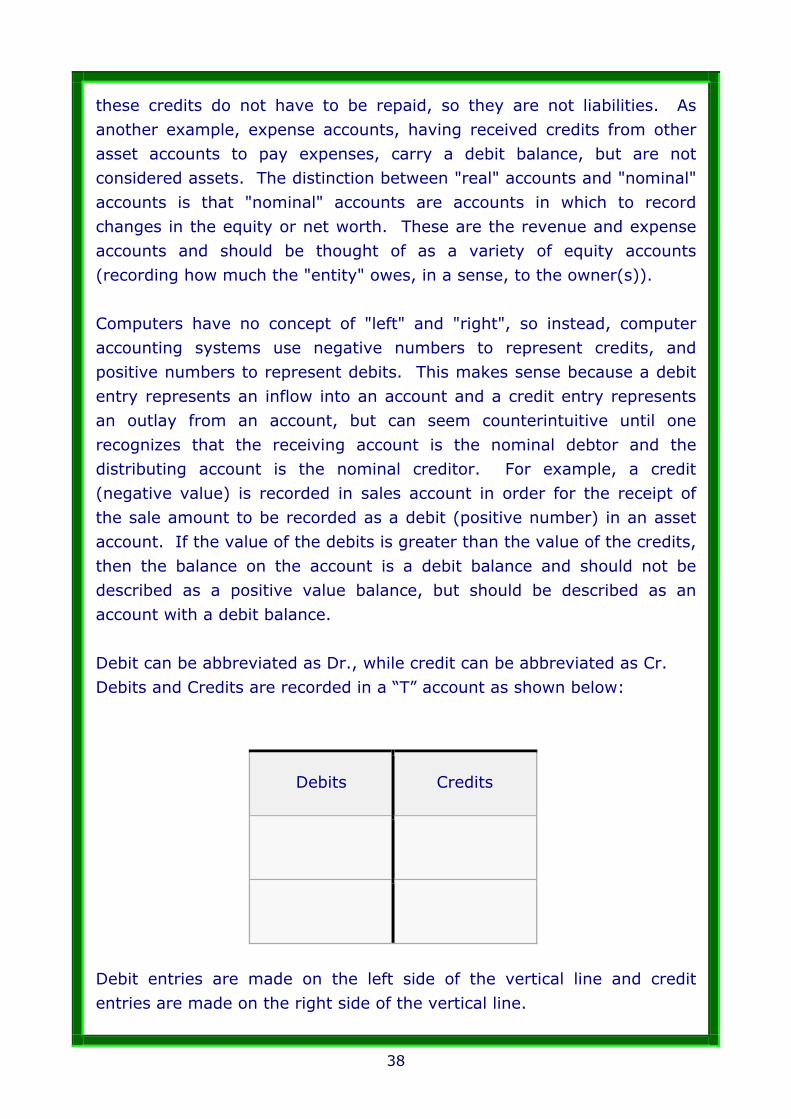

JOURNAL ENTRY ....................................................................................... 40

CHAPTER 6 - MONEY BASICS ......................................................................... 43

THE THREE TYPES OF MONEY ..................................................................... 43

FIAT MONEY AS A TAX CREDIT ................................................................... 44

BASE MONEY ........................................................................................... 44

BANK MONEY ........................................................................................... 44

CONTROLLING THE PRICE OF RESERVES ..................................................... 45

CENTRAL BANKS REACTIVE ROLE ............................................................... 45

LIMITING BANK LENDING .......................................................................... 46

LIMITING MONEY SUPPLY GROWTH ............................................................. 46

CHAPTER 7 - THE MODERN BANKING SYSTEM ................................................. 49

xvii

TYPE 1. MERCHANT BANKS ....................................................................... 49

TYPE 2. INVESTMENT BANKS ..................................................................... 50

TYPE 3. COMMERCIAL BANKS .................................................................... 50

TYPE 4. GIRO BANKS ............................................................................... 51

CENTRAL BANKS AND THE BANK FOR INTERNATIONAL SETTLEMENTS (BIS) ..... 51

FUNCTIONS OF CENTRAL BANKS ................................................................ 51

THE BANK FOR INTERNATIONAL SETTLEMENTS (BIS) .................................... 52

FRACTIONAL RESERVE BANKING ................................................................ 53

HOW BANKS MEET RESERVE REQUIREMENTS ............................................... 54

HOW THE FED MANAGES RESERVES ............................................................ 54

SIZE AND COMPOSITION OF THE MONETARY BASE ....................................... 54

LINKAGE BETWEEN RESERVES AND MONEY SUPPLY ...................................... 55

HOW IT ALL WORKS .................................................................................. 55

NOW, HERE IS WHERE THE REAL RUB COMES IN TO PLAY .............................. 56

ONLY ONE MORE DEBT ISSUE, TO ADDRESS ................................................ 59

A UNIQUE SUMMARY OF THE FRACTIONAL RESERVE BANKING SYSTEM ........... 61

CHAPTER 8 - THE IMF AND THE WORLD BANK ................................................. 71

INTERNATIONAL MONETARY FUND .............................................................. 71

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

(THE WORLD BANK) .................................................................................. 73

WORLD BANK GROUP ................................................................................ 74

WORLD BANK GROUP AGENCIES ................................................................ 76

MONEY SUPPLY - M0, M1, M2, M3, M4 ......................................................... 79

CHAPTER 9 – BANK DEBENTURE TRADING PROGRAMS ...................................... 83

AN INTRODUCTION TO BANK DEBENTURE TRADING PROGRAMS (PPP) ............. 83

HISTORY AND DEVELOPMENT OF BANK INSTRUMENTS .................................. 86

PRESENT TIME VALUE OF FUTURE MONEY, OR FUTURE DEBT. ......................... 93

xviii

THE CALCULATIONS .................................................................................. 93

TECHNICAL DETAILS .............................................................................. 94

RISK FREE CAPITAL ACCUMULATION ........................................................... 99

A WORD OF CAUTION ............................................................................. 115

CHAPTER 10 - PUTTING IT ALL TOGETHER .................................................... 117

FIRST THINGS FIRST .............................................................................. 117

WHAT YOU HAVE LEARNED ...................................................................... 117

YOUR ACTION PLAN ................................................................................ 127

CHAPTER 11 - AND MUCH MORE .................................................................. 145

OKAY, SO YOU WANT TO PLAY THE PPP GAME ............................................... 145

PRESENTMENTS ......................................................................................... 145

PRESENTMENTS INDEX ............................................................................ 146

PART I - BACKGROUND, CONTEXT, AND UNDERPINNINGS ............................ 146

WHENEVER YOU RECEIVE A PRESENTMENT OF ANY KIND ............................. 146

PART II - ATTITUDES AND ACTIONS .......................................................... 160

EVERY TIME YOU EVER MAIL ANYTHING, PUT POSTAGE STAMPS ON THE ENVELOPE 164

IN COURT ........................................................................................... 172

PART III - CIVIL AND CRIMINAL CHARGES ................................................. 184

PART IV - REDEMPTION IN COURT ............................................................ 205

PART V - COURT BOND ............................................................................ 217

PART VI - POSTAL POWER ........................................................................ 222

PART VII - ESOTERIC KNOWLEDGE ........................................................... 228

THE CONCLUSION ...................................................................................... 245

PROJECT FUNDING ................................................................................. 245

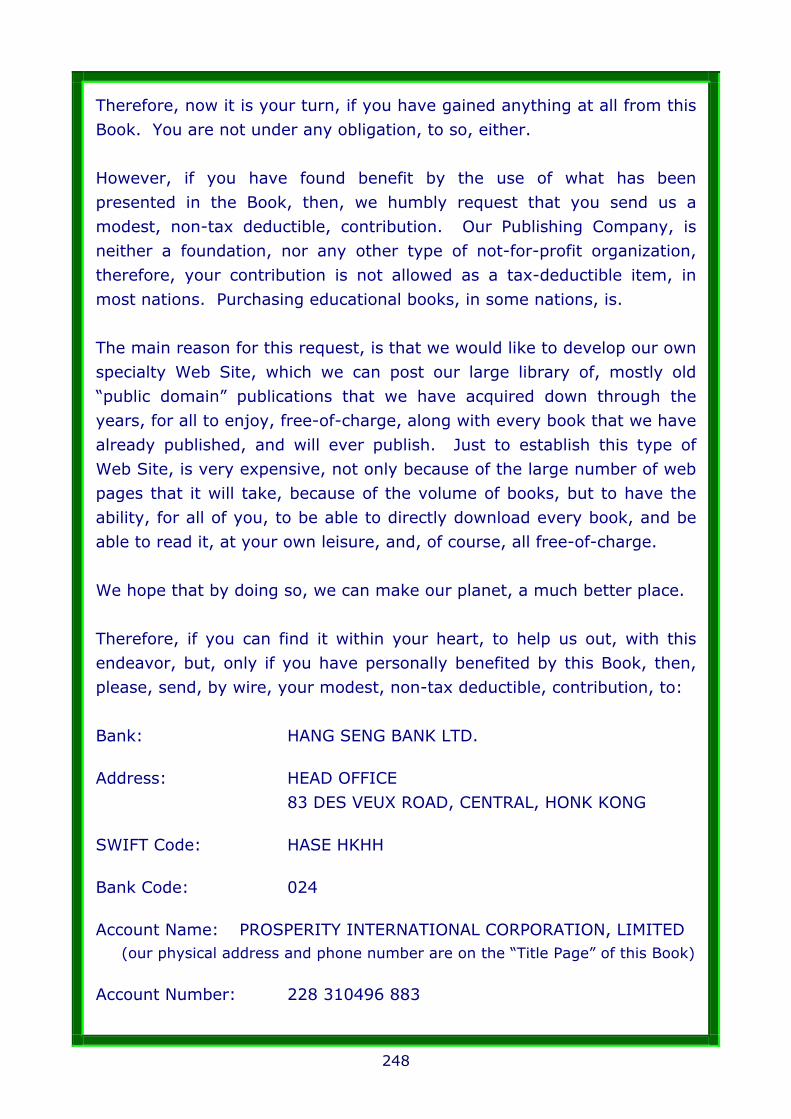

A SPECIAL REQUEST / EXCHANGE FACTOR .................................................... 247

HOW TO PRINT THIS BOOK ........................................................................ 251

~ LIGHT ~ A CHINESE PROVERB .................................................................... 252

xix

“Do your little bit of good where you are, it's those little bits of good put together

that overwhelm the world.”

-- Bishop Desmond Tutu --

xx

“All life is an experiment.

The more experiments you make the better.”

-- Ralph Waldo Emerson --

HAPTER 1 - THE HISTORY OF BANKING

Earliest Banks The first banks were probably the religious temples of the ancient world, and were probably established sometime during the third millennium B.C. Banks in effect, predated the invention of money. Deposits initially consisted of grain and later other goods to include cattle, agricultural implements, and eventually precious metals such as gold, in the form of easy to carry compressed plates. Temples and palaces were the safest places to store gold as they were constantly attended, maintained, and well built. As sacred places, temples presented an extra deterrent to would-be thieves. There are to be in existence records of loans from the 18th century BC in Babylon that were made by temple priests/monks to merchants. By the time of Hammurabi's Code, banking was well enough developed to justify the promulgation of laws governing banking operations.[1] Ancient Greece holds further evidence of banking. Greek temples, as well as private and civic entities, conducted financial transactions such as loans, deposits, currency exchange, and validation of coinage. There is evidence as well of credit, whereby in return for a payment from a client, a moneylender in one Greek port would write a credit note for the client who could "cash" the note in another city, saving the client the danger of carting coinage with him on his journey. Pythius, who operated as a merchant banker throughout Asia Minor at the beginning of the 5th century B.C., is the first individual banker of whom we have records. Many of the early bankers in Greek city-states were “metics” or foreign residents. Around 371 B.C., Pasion, a slave, became the wealthiest and most famous Greek banker, gaining his freedom and Athenian citizenship in the process. The fourth century B.C. saw an increased use of credit-based banking in the Mediterranean world. In Egypt, from early times, grain had been used as a form of money in addition to precious metals, and state granaries functioned as banks. When Egypt fell under the rule of a Greek dynasty, the Ptolemies (330-323 B.C.), the numerous scattered

C

2

government granaries were transformed into a network of grain banks, centralized in Alexandria where the main accounts from all the state granary banks were recorded. This banking network functioned as a trade credit system in which payments were affected by transfer from one account to another without money passing between individuals. In the late third century B.C., the barren Aegean island of Delos, known for its magnificent harbor and famous temple of Apollo, became a prominent banking center. As in Egypt, cash transactions were replaced by real credit receipts and payments were made based on simple instructions with accounts kept for each client. With the defeat of its main rivals, Carthage and Corinth, by the Romans, the importance of Delos increased. Consequently, it was natural that the bank of Delos should become the model most closely imitated by the banks of Rome. Ancient Rome perfected the administrative aspect of banking and saw greater regulation of financial institutions and financial practices. Charging interest on loans and paying interest on deposits became more highly developed and competitive. The development of Roman banks was limited, however, by the Roman preference for cash transactions. During the reign of the Roman emperor Gallienus (260-268 CE), there was a temporary breakdown of the Roman banking system after the banks rejected the flakes of copper produced by his mints. With the ascent of Christianity, banking became subject to additional restrictions, as the charging of interest was seen as immoral. After the fall of Rome, banking was abandoned in Western Europe, and did not revive until the time of the crusades. Religious restrictions on interest Most early religious systems in the ancient Near East, and the secular codes arising from them, did not forbid usury. These societies regarded inanimate matter as alive, like plants, animals and people, and capable of reproducing itself. Hence if you lent 'food money', or monetary tokens of any kind, it was legitimate to charge interest.[2] Food money in the shape of olives, dates, seeds or animals was lent out as early as 5000 BC, if not earlier. Among the Mesopotamians, Hittites, Phoenicians and Egyptians, interest was legal and often fixed by the state. However, the Jews took a different view of the matter.[3]

3

The Torah and later sections of the Hebrew Bible criticize interest taking, but interpretations of the Biblical prohibition vary. One common understanding is that Jews are forbidden to charge interest upon loans made to other Jews, but allowed to charge interest on transactions with non-Jews, or Gentiles. However, the Hebrew Bible itself gives numerous examples where this provision was evaded.[4] Johnson holds that the Hebrew Bible treats the lending as philanthropy in a poor community whose aim was collective survival, but which is not obliged to be charitable towards outsiders. During Late Antiquity and Middle Ages Jews were ostracized from most professions by local rulers, the Church and the guilds included so they were pushed into marginal occupations considered socially inferior, such as tax and rent collecting or money lending, while the provision of financial services was increasingly being demanded by the expansion of European trade and commerce. Medieval trade fairs, such as the one in Hamburg, contributed to the growth of banking in a curious way: moneychangers issued documents redeemable at other fairs, in exchange for hard currency. These documents could be cashed at another fair in a different country or at a future fair in the same location. If redeemable at a future date, they would often be discounted by an amount comparable to a rate of interest. Eventually, these documents evolved into bills of exchange, which could be redeemed at any office of the issuing banker. These bills made it possible to transfer large sums of money without the complications of hauling large chests of gold and hiring armed guards to protect the gold from thieves. Beginning around 1100, the need to transfer large sums of money to finance the Crusades stimulated the reemergence of banking in Western Europe. In 1156, in Genoa, occurred the earliest known foreign exchange contract. Two brothers borrowed 115 Genoese pounds and agreed to reimburse the bank's agents in Constantinople the sum of 460 bezants one month after their arrival in that city. In the following century, the use of such contracts grew rapidly, particularly since profits from time differences were seen as not infringing canon laws against usury. In 1162,

4

Henry II levied a tax to support the crusades, the first of a series of taxes levied by Henry over the years with the same objective. The Templars, and Hospitallers, acted as Henry's bankers in the Holy Land. The Templars' wide flung, large land holdings across Europe also emerged in the 1100 - 1300 time frame as the beginning of Europe’s-wide banking, as their practice was to take in local currency, for which a demand note would be given that would be good at any of their castles across Europe, allowing movement of money without the usual risk of robbery while traveling. By 1200, there was a large and growing volume of long-distance and international trade in a number of agricultural commodities and manufactured goods in Western Europe, to include corn, wool, finished cloth, wine, salt, wax and tallow, leather and leather goods, weapons and armor. Individual trading concerns and intermix blends often specialized in one or more of these, as did individual producers, because a large amount of capital was required to establish, e.g., a cloth manufacturing business, only the largest firms could diversify. As a result, businesses, and clusters of businesses, tended to market narrow product lines. Big firms like the Medici bank could and did specialize, the Medici’s manufacturing division had a number of manufacturing facilities producing many different types of cloth. Perhaps the best example of product policy comes from the Cistercian monastic order, where individual monasteries and granges tended to specialize in particular agricultural products or types of industrial production, usually with an eye to meeting particular local or regional market needs. Ironically, the Papal bankers were the most successful of the Western world, though often goods taken in pawn were substituted for interest in the institution termed the Monte di Pietà. When Pope John XXII (born Jacques d'Euse (1249 - 1334) was crowned in Lyon in 1316, he set up residency in Avignon. Civil war in Florence between the rival Guelph and Ghibelline factions resulted in victory for a group of Guelph merchant families in the city. They took over papal banking monopolies from rivals in nearby Siena and became tax collectors for the Pope throughout Europe. In 1306, Philip IV expelled Jews from France. In 1307 Philips had the Knights Templar arrested and had gotten hold of their wealth, which had come to serve as the unofficial treasury of France. In 1311, he

5

expelled Italian bankers and collected their outstanding credit. In 1327, Avignon had 43 branches of Italian banking houses. In 1347, Edward III of England defaulted on loans. Later there was the bankruptcy of the Peruzzi (1374) and Bardi (1353). The accompanying growth of Italian banking in France was the start of the Lombard moneychangers in Europe, who moved from city to city along the busy pilgrim routes important for trade. Key cities in this period were Cahors, the birthplace of Pope John XXII, and Figeac. Perhaps it was because of these origins that the term Lombard is synonymous with Cahorsin in medieval Europe, and means 'pawnbroker'. Banca Monte dei Paschi di Siena SPA (MPS) Italy is the oldest surviving bank in the world. After 1400, political forces turned against the methods of the Italian free enterprise bankers. In 1401, King Martin I of Aragon expelled them. In 1403, Henry IV of England prohibited them from taking profits in any way or means in his kingdom. In 1409, Flanders imprisoned and then expelled Genoese bankers. In 1410, all Italian merchants were expelled from Paris. In 1401, the Bank of Barcelona was founded. In 1407, the Bank of St George was founded in Genoa. This bank dominated business in the Mediterranean. In 1403, charging interest on loans was ruled legal in Florence despite the traditional Christian prohibition of usury. Italian banks such as the Lombards, who had agents in the main economic centers of Europe, had been making charges for loans. The lawyer and theologian Lorenzo di Antonio Ridolfi won a case that legalized interest payments by the Florentine government. In 1413, Giovanni di Bicci de’Medici was appointed banker to the pope. In 1440, Gutenberg invents the modern printing press although Europe already knew of the use of paper money in China. The printing press design was subsequently modified, by Leonardo da Vinci among others, for use in minting coins nearly two centuries before printed banknotes were produced in the West. By the late 1390’s silver was short all over Europe, except in Venice. The silver mines at Kutná Hora had begun to decline in the 1370s, and finally closed down after being sacked by King Sigismund in 1422. By 1450, almost all of the mints of northwest Europe had closed down for lack of silver. The last moneychanger in the major French port of Dieppe went out of business in 1446. In 1455, the Turks overran the Serbian silver mines, and in 1460 controlled the last Bosnian mine. The last Venetian silver grosso was minted in 1462. Several Venetian banks failed, as well

6

as, the Strozzi bank of Florence, the second largest in the city. Even the smallest of small change became scarce. Western Banking History Modern Western economic and financial history is usually traced back to the coffee houses of London. The London Royal Exchange was established in 1565. At that time, moneychangers were already called bankers, though the term "bank" usually referred to their offices, and did not carry the meaning it does today. There was also a hierarchical order among professionals, at the top were the bankers who did business with heads of state, next were the city exchanges, and at the bottom were the pawnshops or "Lombards”. Some European cities today have a Lombard street where the pawnshop was located. It was after the siege of Antwerp that trade moved to Amsterdam. In 1609 the Amsterdamsche Wisselbank (Amsterdam Exchange Bank) was founded which made Amsterdam the financial centre of the world until the Industrial Revolution. Banking offices were usually located near centers of trade, and in the late 17th century, the largest centers for commerce were the ports of Amsterdam, London, and Hamburg. Individuals could participate in the lucrative East India trade by purchasing bills of credit from these banks, but the price they received for commodities was dependent on the ships returning (which often didn't happen on time) and on the cargo they carried (which often wasn't according to plan). The commodities market was very volatile for this reason, and because of the many wars that led to cargo seizures and loss of ships. Capitalism Around the time of Adam Smith (1776), there was a massive growth in the banking industry. Within the new system of ownership and investment, the State's intervention in economic affairs was reduced and barriers to competition were removed. Global Banking In the 1970s, a number of smaller crashes tied to the policies put in place following the depression, resulted in deregulation and privatization of

7

government-owned enterprises in the 1980s, indicating that governments of industrial countries around the world found private-sector solutions to problems of economic growth and development preferable to state-operated, semi-socialist programs. This spurred a trend that was already prevalent in the business sector, large companies becoming global and dealing with customers, suppliers, manufacturing, and information centers all over the world. Global banking and capital market services proliferated during the 1980s and 1990s as a result of a great increase in demand from companies, governments, and financial institutions, but also because financial market conditions were buoyant and, on the whole, bullish. Interest rates in the United States declined from about 15% for a two-year U.S. Treasury note to about 5% during that 20-year period, and financial assets grew then at a rate approximately twice the rate of the world economy. Such a growth rate would have been lower, in the last twenty years, were it not for the profound effects of the internationalization of financial markets especially U.S. Foreign investments, particularly from Japan, who not only provided the funds to corporations in the U.S., but also helped finance the federal government, thus, transforming the U.S. stock market by far into the largest in the world. Nevertheless, in recent years, the dominance of the U.S. financial markets has been disappearing and there has been an increase interest in foreign stocks. The extraordinary growth of the foreign financial markets results from both large increases in the savings category in foreign countries, such as Japan, and, especially, the deregulation of foreign financial markets, which has enabled them to expand their activities. Thus, American corporations and banks have started seeking investment opportunities abroad, prompting the development in the U.S. of mutual funds specializing in the trading in foreign stock markets. Such growing internationalization and opportunity in financial services has entirely changed the competitive landscape, as now many banks have demonstrated a preference for the “universal banking” model so prevalent in Europe. Universal banks are free to engage in all forms of financial services, make investments in client companies, and function as much as possible as a “one-stop” supplier of both retail and wholesale financial

8

services. Many such possible alignments could be accomplished only by large acquisitions, and there were many of them. By the end of 2000, a year in which a record level of financial service transactions occurred with a market value of $10.5 trillion, the top ten banks commanded a market share of more than 80% and the top 5, 55%. Of the top ten banks ranked by market share, seven were large universal-type banks (three American and four European), and the remaining three were large U.S. investment banks among them accounted for a 33% market share. This growth and opportunity, led to an unexpected outcome, entrance into the market of other financial intermediaries: non-banks. Large corporate players were beginning to find their way into the financial service community, offering competition to established banks. The main services offered included insurances, pension, mutual, money market and hedge funds, loans and credits and securities. By the end of 2001, the market capitalization of the world’s 15 largest financial service providers included four non-banks. In recent years, the process of financial innovation has advanced enormously, increasing the importance and profitability of non-bank finance. Such profitability, previously, had been restricted to the non-banking industry, which has prompted the Office of the Comptroller of the Currency (OCC), to encourage banks to explore other financial instruments, by diversifying a banks' business, as well as, in general improving the economic health of the bank. Hence, as the distinction of financial instruments are being explored and adopted by the banking and non-banking industries, the distinction between different financial institutions is gradually vanishing. Major events in banking history Florentine banking — The Medicis and Pittis among others. Knights Templar- The earliest Euro wide /Mideast banking system during 1100-1300. Banknotes — Introduction of paper money

9

1602 - First joint-stock company, the Dutch East India Company founded. 1720 - The South Sea Bubble and John Law's Mississippi Scheme, which caused a European financial crisis and forced many bankers out of business. 1781 - The Bank of North America was found by the Continental Congress. 1800 - Rothschild family founds Euro wide banking. 1803 - The Louisiana Purchase was the largest land deal in history. 1929 - Stock market crash, which triggered the Great Depression. 1989 - Junk bond scandal and charges against Michael Milken resulted in new legislation for investment banks. 2001 - Enron bankruptcy, causing new legislation for annual reporting. 2007 - The International Financial Crisis, triggered by the meltdown in Sub-Prime Special Investment Vehicles (SIVs), or, so we were told. Oldest Private Banks Monte dei Paschi di Siena 1472 – At present is the oldest surviving bank in the world. Founded in 1472 by the Magistrate of the city and state of Siena, Italy. C. Hoare & Co founded 1672. Barclays, which was founded by John Freame and Thomas Gould in 1690[5] and renamed to Barclays by Freame's son-in-law, James Barclay, in 1736. Rothschild family 1700 - present. Hope & Co., founded in 1762. For French banking history, read the History of banks in France (in English

10

or in French) on the FBF website. Oldest National Banks Bank of Sweden - the rise of the national banks, began operations in 1668. Bank of England - the evolution of modern central banking policies, established in 1694. The Pennsylvania Land Bank was founded in 1723 and by receiving the support of Benjamin Franklin, who wrote, "Modest Enquiry into the Nature and Necessity of a Paper Currency" in 1729. Imperial Bank of Persia (Iran) - History of banking in the Middle East. United States Banking Bank of America - The invention of centralized check and payment processing technology References [1] The word "bank" reflects the origins of banking in temples. According to the famous passage from the New Testament, when Christ drove the moneychangers out of the temple in Jerusalem, he overturned their tables. Matthew 21.12. In Greece, bankers were known as trapezitai, a name derived from the tables where they sat. Similarly, the English word bank comes from the Italian banca, for bench or counter. [2] Johnson cites Fritz E. Heichelcheim: An Ancient Economic History, 2 vols. (Trans. Leiden 1965), i.104-566 [3] Johnson, Paul: A History of the Jews (New York: HarperCollins Publishers, 1987) ISBN 0-06-091533-1. Pgs.172-173 [4] I Samuel 22:2, II Kings 4:1, Isaiah 50:1, Ezekiel 22:12, Nehemiah 5:7 and 12:13 [5] "Barclays - Our Beginnings". Retrieved on 2007-09-21.

11

“Some of us will do our jobs well

and some will not, but we will all be judged by only one thing –

the result.”

-- Vince Lombardi --

12

“The act of taking the first step

is what separates the winners from the losers”

-- Brian Tracy --

13

HAPTER 2 - THE HISTORY OF MONEY

Money is an invention of the human mind. The creation of money is made possible because human beings have the capacity to accord value to symbols. Money is a symbol that represents the value of goods and services. The acceptance of any object as money – be it wampum, a gold coin, a paper currency note or a digital bank account balance – involves the consent of both the individual user and the community. Thus, all money has a psychological and a social, as well as, economic dimension. As human consciousness has evolved, the nature and function of money has evolved also. While a history of money may trace the origin and usage of different forms of money at different times and in different parts of the world, an evolutionary perspective on money traces the social and psychological changes in human attitude and collective behavior that made possible this historical development. Barter Before the invention of money, barter was the primary medium of exchange. An individual possessing a material object of value, such as a measure of grain, could directly exchange that object for another object perceived to have equivalent value, such as a small animal, a clay pot or a tool. The capacity to carry out transactions was severely limited since it depended on a coincidence of wants. The seller of food grain had to find a buyer who wanted to buy grain and who could offer in return something the seller wanted to buy. There was no common medium of exchange, into which both seller and buyer could convert their tradable commodities. There was no standard, which could be applied to measure the relative value of various goods and services. Commodity Money The first stage in the evolution of money was the acceptance of certain inherently valuable objects, such as metals, cows, goats, or food grains, as a common standard of measure and unit of exchange. It was relatively easy for people to accept any of these as money because each had

C

14

inherent use value for every individual and, therefore, their wide acceptance by other people was assured. All metals were accepted because they could be readily converted into precious tools and weapons, such as knives, axes, spears, and spades. Gold and silver had secondary advantages, as they, were also easy to identify and visually attractive. Gold, silver, copper, including other usable materials, or desired objects, such as salt and peppercorns are categorized as commodity money, since they combine the attributes as both a usable commodity and a symbol. People accepted foods and metals as money because they were sure of their intrinsic value to themselves and others. The introduction of metal coins marked a step or bridge in the evolution from usable commodities to symbolic forms of money. Although metal had a use value of its own, coins were accepted in trade for their symbolic value as a medium and standard of measure for exchanging other goods and services to establish value rather than for the utilization of the metal they contained. The term commodity money is also applied to other objects of less obvious utility such as shells, beads and stones, whose utilitarian value was only decorative. This classification tends to blur an important distinction between money consisting of usable commodities and pure symbolic money. Representative Money Representative money was the next stage in the evolution of money involved a further transition from money as an object with inherent usefulness and value to money as a pure symbol of value. Representative money is symbolic money that is based on useful commodities. This category includes the warehouse receipts issued by the ancient Egyptian grain banks, the goldsmith receipts issued by England’s goldsmith bankers, bills of exchange based on tradable goods, and more recent forms of paper currency that were backed by and redeemable for gold or silver. The adoption of representative money represented a significant evolution in human consciousness.

15

Psychologically, the individual had to transfer the sense of value from a usable material object to an abstract symbol. Socially, groups of people had to agree on the common usage of the same symbol. Warehouse Receipts Warehouse receipts became a very successful form of representative money in ancient Egypt during the reign of the Ptolemies around 330 BC. Farmers deposited their surplus food grains for safekeeping in royal or private warehouses and received in exchange written receipts for specific quantities of grain. The receipts were backed and redeemable for a usable commodity. Being much easier to carry, store and exchange than bags of grain, they were accepted in trade as a secure and more convenient form of payment, acting as a symbolic substitute for the quantities of food grain they represented. The warehouse receipt itself had no inherent value. It was only a symbol for something of value. The invention of representative money had a profound effect on the evolution of both money and society. It directly led to the creation of a new social organization, banking. The network of royal and private banks that were created during the reign of the Ptolemies constituted a national grain or giro-banking system. Grains were deposited in ‘banks’ for safekeeping. Warehouse receipts were accepted as form of symbolic money because they were fully ‘backed’ by the grains in the warehouse. More important but less obvious, the introduction of banking by the pharaohs made possible the creation of money. Until then new money could be grown as a crop, raised as an animal or discovered as metal in the earth. Now it could simply be created by writing a warehouse receipt. At first, these receipts were issued only when additional grain was deposited and cancelled whenever the grain was withdrawn from the warehouse. However, it required only a small step in imagination for the bankers to realize that they could also create new grain receipts on other occasions. If someone applied to the bank for financial assistance, the bank need not provide it in the form of grain. It could simply create and give to the borrower a new warehouse receipt that was indistinguishable from those issued when grain was deposited. Although the new receipts

16

were not backed by addition deposits of grain, they were still backed by the total value of grain on deposit at the warehouse and, therefore, readily accepted in the market as a medium of exchange, so long as the public had trust and confidence in the overall financial strength of the grain bank. This stage marks a crucial transition from money as a thing to money as a symbol of trust. In the case of commodity money, trust was placed in the inherent value of the metal or grain, which constituted the form of payment. In the case of the warehouse receipt, trust was extended from the commodity to the social organization that held the grain and issued the receipts. This shift required a psychological willingness on the part of the individual to accept a symbol in place of a physical object and a social willingness on the part of the collective to evolve organizations and systems of account that could gain and hold the public trust. The invention of a new social organization was based on emergence of a new consciousness in society. These ancient giro banks went even further. They introduced standardized accounting methods and bank accounts for their depositors. Deposits could be recorded as numerical entries in their books of account. Large transfers of money from one account holder to another could be done without even exchanging warehouse receipts, simply by changing the account balances in the bank’s record books. The number in the record book became a symbolic form of representative money, an ancient forerunner of modern electronic forms of money. Tallies The acceptance of symbolic forms of money opened up vast new realms for human creativity. A symbol could be used to represent something of value that was available in physical storage somewhere else in ’’space’’, such as grain in the warehouse. It could also be used to represent something of value that would be available later in ‘’time’’, such as a promissory note or bill of exchange, a document ordering someone to pay a certain sum of money to another on a specific date or when certain conditions have been fulfilled. In the 12th Century, the English monarchy introduced an early version of the bill of exchange in the form of a notched piece of wood known as a tally stick. Tallies originally came into

17

use at a time when paper was rare and costly, but their use persisted until the early 19th Century, even after paper forms of money had become prevalent. The notches were used to denote various amounts of taxes payable to the crown. Initially tallies were simply used as a form of receipt to the taxpayer at the time of rendering his dues. As the revenue department became more efficient, they began issuing tallies to denote a promise of the tax assessee, to make future tax payments at specified times during the year. Each tally consisted of a matching pair – one stick was given to the assessee at the time of assessment representing the amount of taxes to be paid later and the other held by the Treasury representing the amount of taxes be collected at a future date. The Treasury discovered that these tallies could also be used to create money. When the crown had exhausted its current resources, it could use the tally receipts representing future tax payments due to the crown as a form of payment to its own creditors, who in turn could either collect the tax revenue directly from those assessed or use the same tally to pay their own taxes to the government. The tallies could also be sold to other parties in exchange for gold or silver coin at a discount reflecting the length of time remaining until the taxes was due for payment. Thus, the tallies became an accepted medium of exchange for some types of transactions and an accepted medium for store of value. Like the giro banks before it, the Treasury soon realized that it could also issue tallies that were not ‘backed’ by any specific assessment of taxes. By doing so, the Treasury created new money that was backed by public trust and confidence in the monarchy rather than by specific revenue receipts. Trade Bills of Exchange Bills of Exchange became prevalent with the expansion of European trade toward the end of the Middle Ages. A flourishing Italian wholesale trade in cloth, woolen clothing, wine, tin, and other commodities was heavily dependent on credit for its rapid expansion. Goods were supplied to a buyer against a bill of exchange, which constituted the buyer’s promise to make payment at some specified future date. If the buyer was reputable or the bill was endorsed by a credible guarantor, the seller could then present the bill to a merchant banker and redeem it in money at a discounted value before it actually became due. These bills could also be used as a form of payment by the seller to make additional purchases

18

from his own suppliers. Thus, the bills (an early form of credit) became both a medium of exchange and a medium for storage of value. Like the loans made by the Egyptian grain banks, this trade credit became a significant source for the creation of new money. In England, bills of exchange became an important form of credit and money during last quarter of the 18th century and the first quarter of the 19th century before banknotes, checks and cash credit lines were widely available. Goldsmith Bankers The highly successful ancient grain bank also served as a model for the emergence of the goldsmith bankers in 17th Century England. These were the early days of the mercantile revolution before the rise of the British Empire when merchant ships began plying the coastal seas laden with silks and spices from the orient and shrewd traders amassed huge hoards of gold in the bargain. Since no banks existed in England at the time, these entrepreneurs entrusted their wealth with the leading goldsmith of London, who already possessed stores of gold and private vaults within which to store it safely, and paid a fee for that service. In exchange for each deposit of precious metal, the goldsmiths issued paper receipts certifying the quantity and purity of the metal they held on deposit. Like the grain receipts, tallies and bills of exchange, the goldsmith receipts soon began to circulate as a safe and convenient form of money backed by gold and silver in the goldsmiths’ vaults. Knowing that goldsmiths were laden with gold, it was only natural that other traders in need of capital might approach them for loans, which the goldsmiths made to trustworthy parties out of their gold hoards in exchange for interest. Like the grain bankers, goldsmiths began issuing loans by creating additional paper gold receipts that were generally accepted in trade and were indistinguishable from the receipts issued to parties that deposited gold. Both represented a promise to redeem the receipt in exchange for a certain amount of metal. Since no one other than the goldsmith knew how much gold he held in store and how much was the value of his receipts held by the public, he was able to issue receipts for greater value than the gold he held. Gold deposits were relatively stable, often remaining with the goldsmith for years on end, so there was little risk of default so long as public trust in the goldsmith’s integrity and financial soundness was maintained.

19

Thusly, the goldsmiths of London became the forerunners of British banking and prominent creators of new money. They created money based on public trust. Banknotes The history of money and banking are inseparably interlinked. The multiplication of money really took off when banks got into the business. Inspired by the success of the London goldsmiths, some of which became the forerunners of great English banks, banks began issuing paper notes quite properly termed ‘banknotes’ which circulated in the same way that government issued currency circulates today. In England, this practice continued up to 1694. Scottish banks continued issuing notes until 1850. In the USA, this practice continued through the 19th Century, where at one time there were more than 5000 different types of bank notes issued by various commercial banks in America. Only the notes issued by the largest, most creditworthy banks were widely accepted. The script of smaller, lesser-known institutions circulated locally. Farther from home, it was only accepted at a discounted rate, if it was accepted at all. The proliferation of types of money went hand in hand with a multiplication in the number of financial institutions. These banknotes were a form of representative money, which could be converted into gold or silver by application at the bank. Since banks issued notes far in excess of the gold and silver they kept on deposit, sudden loss of public confidence in a bank could precipitate mass redemption of banknotes and result in ‘’bankruptcy’’. The use of bank notes issued by private commercial banks as legal tender has gradually been replaced by the issuance of bank notes authorized and controlled by national governments. The Bank of England was granted sole rights for the issuance of banknotes in England after 1694. In the USA, the Federal Reserve Bank was granted similar rights after its establishment in 1913. Until recently, these government-authorized currencies were forms of representative money, since they were partially backed by gold or silver and convertible into metal under certain circumstances.

20

Demand Deposits The primary business of the grain and goldsmith bankers was safe storage of savings. The primary business of the early merchant banks was promotion of trade. The new class of commercial banks made accepting deposits and issuing loans their principal activity. They lent the money they received on deposit. They created additional money in the form of new bank notes. They also created additional money in the form of demand deposits simply by making numerical entries in the ledgers of their account holders. The money they created was partially backed by gold, silver, or other assets and partially backed only by public trust in the institutions that created it. Gold-Backed Banknotes For most of us, the term gold standard is erroneously thought to refer to a time when currency notes were fully backed by and redeemable in an equivalent amount of gold. The British pound was the strongest, most stable currency of the 19th Century and often considered the closest equivalent to pure gold, yet at the height of the gold standard, there was only sufficient gold in the British treasury to redeem a small fraction of the currency then in circulation. In 1880, the US government’s gold stock was equivalent in value to only 16% of currency and demand deposits in commercial banks. By 1970, it was about 0.5%. The gold standard was only a system for exchange of value between national currencies, never an agreement to redeem all paper notes for gold. The classic gold standard prevailed during the period 1880 and 1913 when a core of leading trading nations agreed to adhere to a fixed gold price and continuous convertibility for their currencies. Gold was used to settle accounts between these nations. With the outbreak of World War I, Britain was forced to abandon the gold standard even for their international transactions. Other nations quickly followed suit. After a brief attempt to revive the gold standard during the 1920s, it was finally abandoned by Britain and other leading nations during the Great Depression. Prior to the abolition of the gold standard, the following words were printed on the face of every US dollar: “I promise to pay the bearer on

21

demand, the sum of one dollar”, followed by the signature of the US Secretary of the Treasury. Other denominations carried similar pledges proportionate to the face value of each note. The currencies of other nations bore similar promises too. In earlier times, this promise signified that a bearer could redeem currency notes for their equivalent value in gold or silver. The US adopted a silver standard in 1785, meaning that the value of the US dollar represented a certain equivalent weight in silver, and could be redeemed in silver coins. However, even at its inception, the US Government was not required to maintain silver reserves sufficient to redeem all the notes that it issued. Through much of the 20th Century until 1971, the US dollar was ‘backed’ by gold, but from 1934, only foreign holders of the notes could exchange them for metal. Fiat Money Since 1971, the US dollar is not backed by anything. It is pure fiat money. The promise was quietly withdrawn and currency notes no longer carry that pledge. The same is true of all major currencies in the world today. This marks the final stage in the evolution of pure fiat money, which is backed neither, by a commodity, nor convertible into a commodity. Fiat money has become the standard form of national currency since abandonment of the gold standard. Banknotes issued by private banks were backed by the total deposits of the banks that issued them, however inadequate those deposits might be to reimburse all depositors. Notes issued by the US Federal Reserve or other central banks are backed only by the perception of public confidence in the stability of government and the productive capacity of the country that issues them. The transition from bank notes to government-guaranteed currency marks the evolution from trust in a financial institution to trust in the economic capacity and future prosperity of the nation. The greater a country’s production and productivity, the more the goods and services it offers in exchange for legal tender, and therefore the greater the confidence and trust in that currency. That is a major reason why the value of the euro has risen as the European Union had expanded to include more countries with greater productive capacity.

22

“The Doors of Wisdom are never shut.”

-- Benjamin Franklin --

23

HAPTER 3 - THE HISTORY OF ACCOUNTING

Early History Accountancy's infancy dates back to the earliest days of human agriculture and civilization (the Sumerians in Mesopotamia, and the Egyptian Old Kingdom). Ancient economic thought of the Near East facilitated the creation of accurate records of the quantities and relative values of agricultural products, methods that were formalized in trading and monetary systems by 2000 BC. Simple accounting is mentioned in the Christian Bible (New Testament) in the Book of Matthew, in the Parable of the Talents. The Islamic Quran also mentions simple accounting for trade and credit arrangements. Twelfth-century A.D. Arab writer Ibn Taymiyyah mentioned in his book Hisba (literally, "verification" or "calculation") detailed accounting systems used by Muslims as early as in the mid-seventh century A.D. These accounting practices were influenced by the Roman and the Persian civilizations, which Muslims interacted with. The most detailed example Ibn Taymiyyah provides a complex governmental accounting system is the Divan of Umar, the second Caliph of Islam, in which all revenues and disbursements were recorded. The Divan of Umar has been described in detail by various Islamic historians and was used by Muslim rulers in the Middle East with modifications and enhancements until the fall of the Ottoman Empire. Luca Pacioli and the Birth of Modern Accountancy Luca Pacioli (1445 - 1517), also known as Friar Luca dal Borgo, is credited for the "birth" of accounting. His Summa de arithmetica, geometrica, proportioni et proportionalita (Summa on arithmetic, geometry, proportions and proportionality, Venice 1494), was a textbook used in the abbaco schools of northern Italy, where the sons of merchants, and artisans, were educated. It was a compendium of the mathematical knowledge of his time, and includes the first printed description of the method of keeping accounts that Venetian merchants used at that time, known as the double-entry accounting system. Although Pacioli codified rather than invented this system, he is widely regarded as the "Father of Accounting". The system he published included most of the accounting

C

24

cycle, as we know it today. He described the use of journals and ledgers, and warned that a person should not go to sleep at night until the debits equaled the credits! His ledger had accounts for assets (including receivables and inventories), liabilities, capital, income, and expenses - the account categories that are reported on an organization's balance sheet and income statement, respectively. He demonstrated year-end closing entries and proposed that a trial balance be used to prove a balanced ledger. His treatise also touches on a wide range of related topics from accounting ethics to cost accounting. Post-Pacioli The first known book in the English language on accounting was published in London, England by John Gouge (or Gough) in 1543. It is described as A Profitable Treatise called the Instrument, or Book, to learn to know the good order of the keeping of the famous reckoning, called in Latin, Dare, and Habere, and, in English, debtor and Creditor. A short book of instructions was also published in 1588 by John Mellis of Southwark, England, in which he says, "I am but the renuer and reviver of an ancient old copies printed here in London on the 14 of August 1543: collected, published, made, and set forth by one Hugh Oldcastle, Schoolmaster, who, as reappeared by his treatise, then taught Arithmetic, and this book in Saint Ollaves parish in Marko Lane.” Mellis refers to the fact that the principle of accounts he explains (which is a simple system of double entry) is "after the former of Venice". A book described as The Merchants Mirror, or directions for the perfect ordering and keeping of his accounts formed by way of Debtor and Creditor, after the (so termed) Italian manner, by Richard Dafforne, accountant, published in 1635, contains many references to early books on the science of accountancy. In a chapter in this book, headed "Opinion of Book-keeping's Antiquity," the author states, on the authority of another writer, that the form of book-keeping referred to had then been in use in Italy about two hundred years, "but that the same, or one in many parts very like this, was used in the time of Julius Caesar, and in Rome long before.” He gives quotations of Latin bookkeeping terms in use in ancient times, and refers to "ex Oratione Ciceronis pro Roscio Comaedo", and he adds:

25

That the one side of their book was used for Debtor, the other for Creditor, is manifest in a certain place, Naturalis Historiae Plinii, lib. 2, cap. 7, where he, speaking of Fortune, saith thus: Huic Omnia Expensa. Huic Omnia Feruntur accepta et in tota Ratione mortalium sola. Utramque Paginam facit. An early Dutch writer appears to have suggested that double entry bookkeeping was even in existence among the Greeks, pointing to scientific accountancy having been invented in remote times. There were several editions of Richard Dafforne's book - the second edition in 1636, the third in 1656, and another in 1684. The book is a very complete treatise on scientific accountancy, beautifully prepared and containing elaborate explanations. The numerous editions tend to prove that the science was highly appreciated in the 17th century. From this time on, there has been a continuous supply of literature on the subject, many of the authors styling themselves accountants and teachers of the art, and thus proving that the professional accountant was then known and employed. Accountancy Qualifications and Regulation The expectations for qualification in the profession of accounting vary between different jurisdictions and countries. Accountants may be certified by a variety of organizations or bodies, such as the Association of Accounting Technicians (AAT),[6] British qualified accountancy bodies including the Chartered Institute of Management Accountants (CIMA), Association of Chartered Certified Accountants (ACCA), Association of International Accountants (AIA) and Institute of Chartered Accountants, and are recognized by titles such as Chartered Management Accountant (ACMA or FCMA) Chartered Certified Accountant (ACCA or FCCA), International Accountant (AAIA or FAIA) and Chartered Accountant (UK, Australia, New Zealand, Canada, India, Pakistan, South Africa, Ghana), Certified Public Accountant (Ireland, Japan, US, Singapore,

26

Hong Kong, the Philippines), Certified Management Accountant (Canada, U.S.), Certified General Accountant (Canada, Caribbean, China, Hong Kong, Bermuda), or Certified Practicing Accountant (Australia). Some Commonwealth countries (Australia and Canada) often recognize both the certified and chartered accounting bodies. The majority of "public" accountants in New Zealand and Canada are Chartered Accountants, however, Certified General Accountants are also authorized by legislation to practice public accounting and auditing in all Canadian provinces, except Ontario and Quebec, as of 2005. There is, however, no legal requirement for an accountant to be a paid-up member of one of the many Institutes. The "Big Four" Accountancy Firms The "Big Four auditors" are the largest multinational accountancy firms. PricewaterhouseCoopers Deloitte Touche Tohmatsu KPMG Ernst & Young These firms are associations of the partnerships in each country rather than having the classical structure of a holding company and subsidiaries, but each has an international 'umbrella' organization for coordination (technically known as a Swiss Verein). Before the Enron and other accounting scandals in the United States, there were five large firms and were called the Big Five: Arthur Andersen, PricewaterhouseCoopers, KPMG, Deloitte Touche Tohmatsu, and Ernst & Young. On June 15, 2002, Arthur Andersen was convicted (later overturned) of obstruction of justice for shredding documents related to its audit of Enron. Nancy Temple (Andersen Legal Dept.) and David Duncan (Lead Partner for the Enron account) were cited as the responsible managers in this scandal as they had given the order to shred relevant documents.

27

Since the U.S. Securities and Exchange Commission do not allow convicted felons to audit public companies, the firm agreed to surrender its licenses and its right to practice before the SEC on August 31, 2002. A plurality of Arthur Andersen joined KPMG in the US and Deloitte & Touche outside of the US. Historically, there had also been groupings referred to as the "Big Six" (Arthur Andersen, plus Coopers & Lybrand before its merger with Price Waterhouse) and the "Big Eight" (Ernst and Young prior to their merger were Ernst & Whinney, and Arthur Young and Deloitte & Touche was formed by the merger of Deloitte, Haskins and Sells with the firm Touche Ross). The accounting scandals at Enron, WorldCom, and other high profile companies in the USA and Europe have had, and continue to have, far reaching consequences for the accounting industry. Application of International Accounting Standards originating in International Accounting Standards Board headquartered in London and bearing more resemblance to UK than current US practices is often advocated by those who note the relative stability of the UK accounting system (which reformed itself after scandals in the late 1980s and early 1990s).

28

“Whatever you do, you need courage. Whatever course you decide upon,

there is always someone to tell you that you are wrong. There are always difficulties arising that tempt you

to believe your critics are right. To map out a course of action and follow it to an end

requires some of the same courage that a soldier needs. Peace has its victories,

but it takes brave men and women to win them.”

-- Ralph Waldo Emerson --

29

HAPTER 4 - BASIC ACCOUNTING

Double entry bookkeeping stretches back centuries perhaps even as early as the 12th century and is now accepted worldwide as the accounting standard to be employed by all companies in recording the financial accounting records. The first written explanation of the accounting system was reportedly by a Venetian mathematician Luca Pacioli towards the end of the 15th century. The accounting industry has grown somewhat since then and today contains many technical words known but largely ignored by non-accountants. The understanding and desire to understand accounting terms is further confused by the banking industry while adopting double entry bookkeeping as standard use what appears to be diametrically opposed terms in the presentation of information to their customers. In accounting terms, an asset such as money in the bank is a debit balance while bank customers are told if they have money in the bank, it is a credit balance. This arises because what the bank is really saying is when a customer has money in the bank that the balance represents a creditor to the bank, as it owes the customer money and is a creditor in the bank’s books. Hence, the bank describes the balance as a credit balance. The simplest way to understand double entry bookkeeping is the understanding that every financial transaction has a double effect. One effect is to change the profit and loss of the business with sales income increasing the financial profit and purchases reducing the financial profit. While the double entry is that every profit and loss transactions also has a balance sheet effect in either increasing assets or increasing liabilities. In more complex accounting areas such as journal entries or bank transactions both sides of a transaction may have no impact on the profit and loss account as both sides of the double entry effect the value of

C

30