Embed Size (px)

Citation preview

Market Risk and Counterparty Credit Risk Expert Network

23 February 2017

About

Zhong Zhi Hu – European Banks Supervision

• Joined DNB in November 2015 with focus on Market Risk, Counterparty

Credit Risk, Liquidity Risk, Interest Rate Risk and Central Clearing

• Nerd at heart

• Fitness junkie and in love with travelling

Agenda

• This agenda item have been removed from this

“non-confidential/public” version

• This agenda item have been removed from this

“non-confidential/public” version

• Bilateral Margining and ISDA’s Standard Initial Margining Model

(SIMM)

• Round-table

Disclaimer

• Several slides that contain “confidential/non-public” content have

been removed

• Therefore this presentation can be shared. This document is for

educational purposes only

Bilateral Margining and ISDA’s Standard Initial Margining Model

(SIMM)

Zhong Zhi Hu – European Banks Supervision, 23-02-17

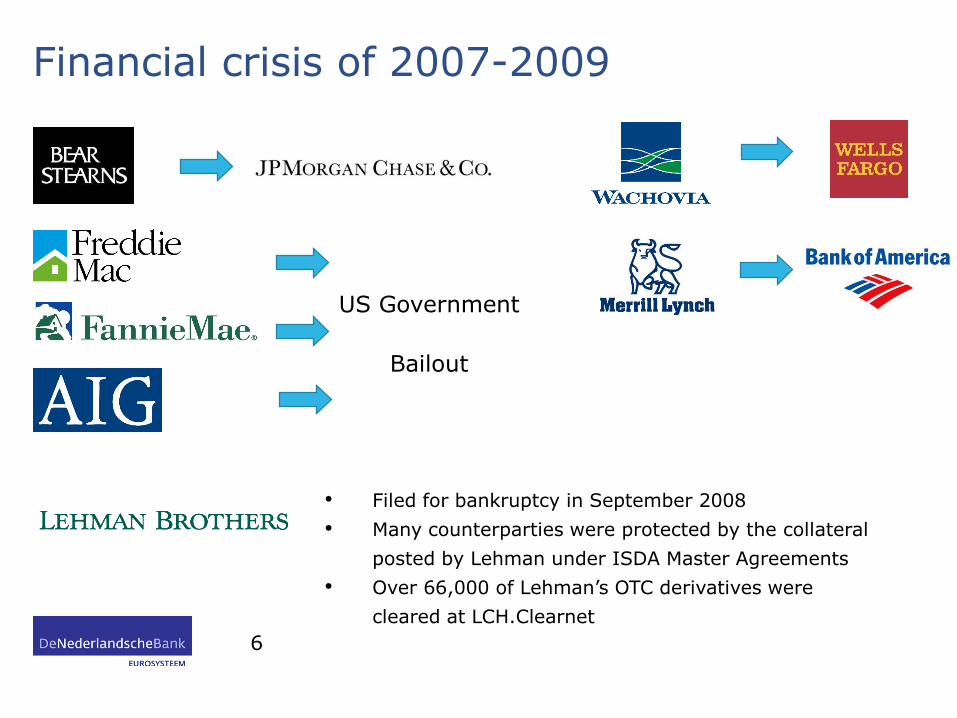

Financial crisis of 2007-2009

6

US Government

Bailout

• Filed for bankruptcy in September 2008

• Many counterparties were protected by the collateral

posted by Lehman under ISDA Master Agreements

• Over 66,000 of Lehman’s OTC derivatives were

cleared at LCH.Clearnet

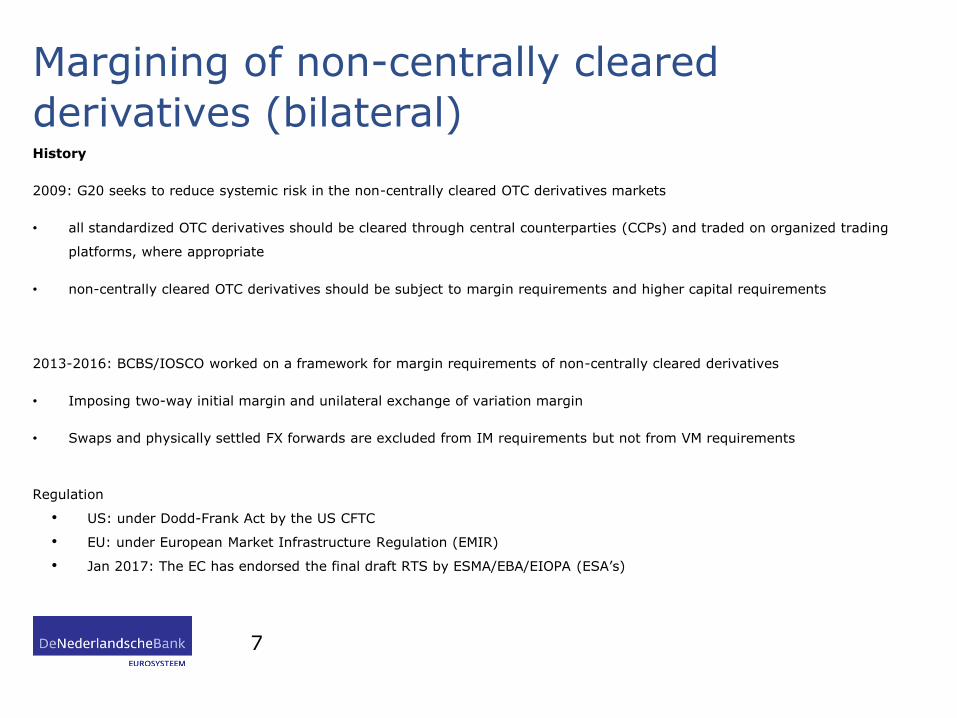

Margining of non-centrally cleared

derivatives (bilateral)History

2009: G20 seeks to reduce systemic risk in the non-centrally cleared OTC derivatives markets

• all standardized OTC derivatives should be cleared through central counterparties (CCPs) and traded on organized trading

platforms, where appropriate

• non-centrally cleared OTC derivatives should be subject to margin requirements and higher capital requirements

2013-2016: BCBS/IOSCO worked on a framework for margin requirements of non-centrally cleared derivatives

• Imposing two-way initial margin and unilateral exchange of variation margin

• Swaps and physically settled FX forwards are excluded from IM requirements but not from VM requirements

Regulation

• US: under Dodd-Frank Act by the US CFTC

• EU: under European Market Infrastructure Regulation (EMIR)

• Jan 2017: The EC has endorsed the final draft RTS by ESMA/EBA/EIOPA (ESA’s)

7

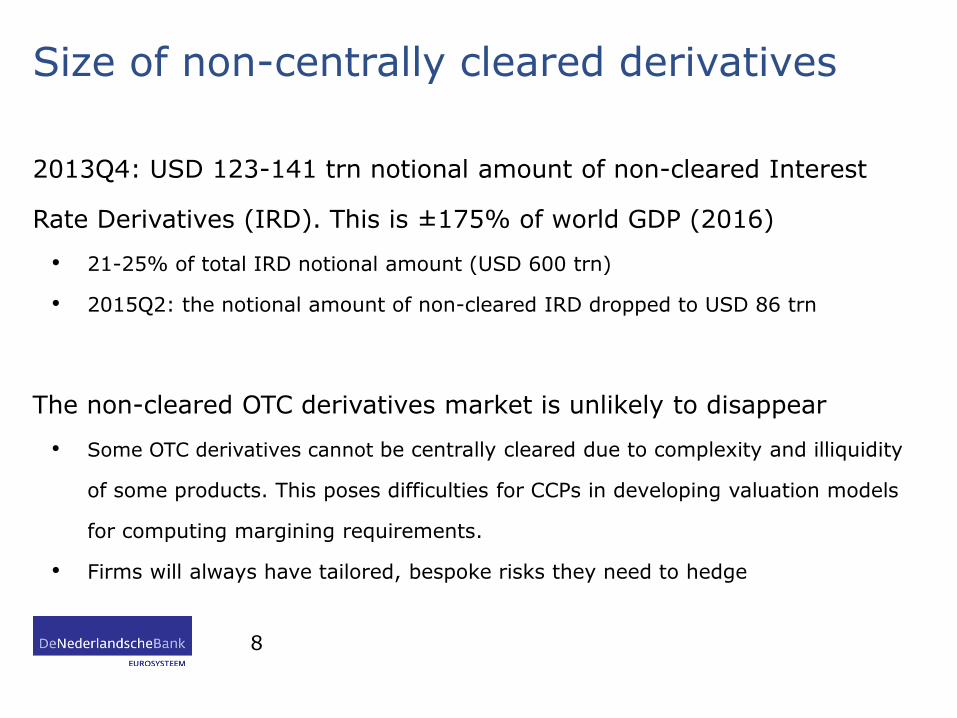

Size of non-centrally cleared derivatives

2013Q4: USD 123-141 trn notional amount of non-cleared Interest

Rate Derivatives (IRD). This is ±175% of world GDP (2016)

• 21-25% of total IRD notional amount (USD 600 trn)

• 2015Q2: the notional amount of non-cleared IRD dropped to USD 86 trn

The non-cleared OTC derivatives market is unlikely to disappear

• Some OTC derivatives cannot be centrally cleared due to complexity and illiquidity

of some products. This poses difficulties for CCPs in developing valuation models

for computing margining requirements.

• Firms will always have tailored, bespoke risks they need to hedge

8

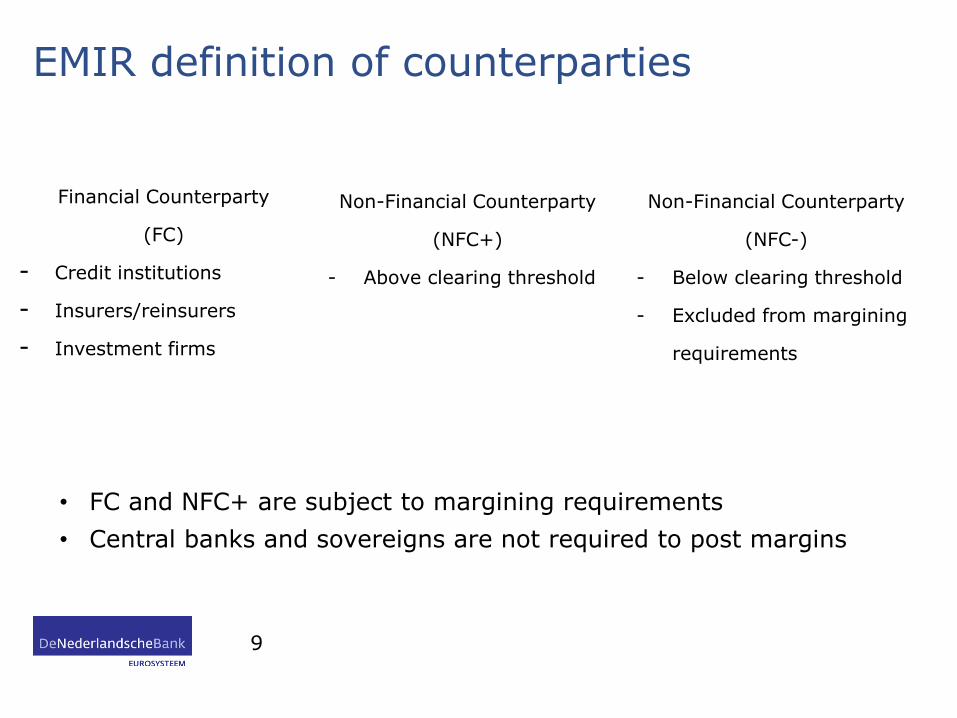

EMIR definition of counterparties

Financial Counterparty

(FC)

- Credit institutions

- Insurers/reinsurers

- Investment firms

9

Non-Financial Counterparty

(NFC+)

- Above clearing threshold

Non-Financial Counterparty

(NFC-)

- Below clearing threshold

- Excluded from margining

requirements

• FC and NFC+ are subject to margining requirements

• Central banks and sovereigns are not required to post margins

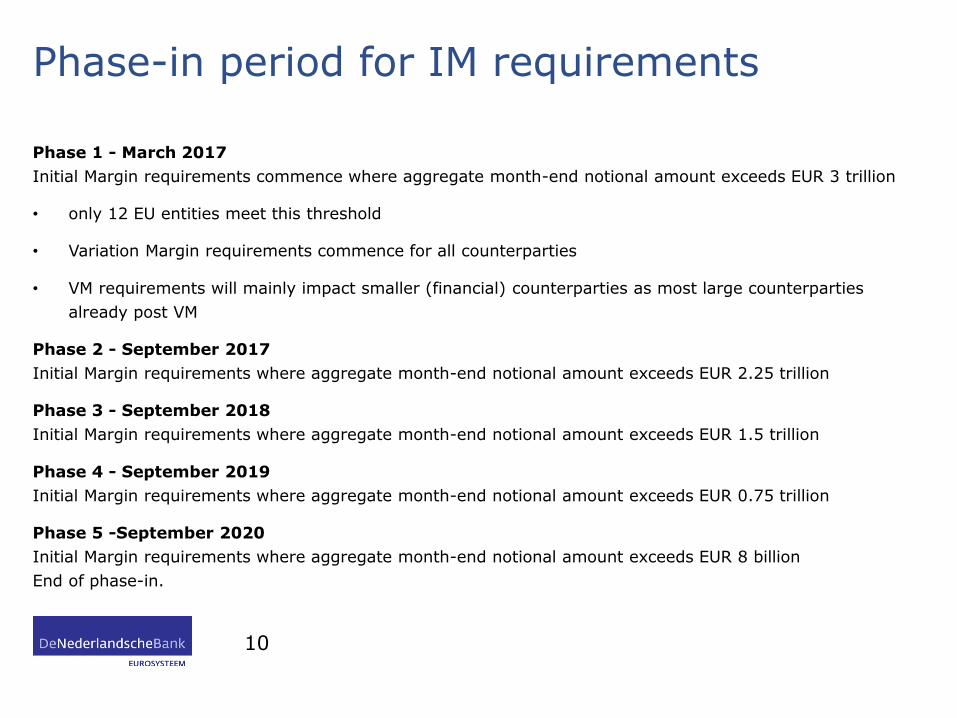

Phase-in period for IM requirements

Phase 1 - March 2017

Initial Margin requirements commence where aggregate month-end notional amount exceeds EUR 3 trillion

• only 12 EU entities meet this threshold

• Variation Margin requirements commence for all counterparties

• VM requirements will mainly impact smaller (financial) counterparties as most large counterparties

already post VM

Phase 2 - September 2017

Initial Margin requirements where aggregate month-end notional amount exceeds EUR 2.25 trillion

Phase 3 - September 2018

Initial Margin requirements where aggregate month-end notional amount exceeds EUR 1.5 trillion

Phase 4 - September 2019

Initial Margin requirements where aggregate month-end notional amount exceeds EUR 0.75 trillion

Phase 5 -September 2020

Initial Margin requirements where aggregate month-end notional amount exceeds EUR 8 billion

End of phase-in.

10

Margining rules

• EU entities are obliged to collect and post margins to non-EU FC and NFC+

• Intragroup transactions are exempted from bilateral margining requirements if certain conditions

are met

Initial Margining

• No netting of IM between 2 parties, whereas ISDA master agreement allows for bilateral netting

• Concentration limit for IM collateral depending on nature (cash, bonds, equities)

• Strict rules on the segregation and rehypothecation of initial margin collateral

Variation Margining

• Parties are required to exchange VM daily subject to a minimum transfer amount of EUR 500k (EU)

or USD 500k (US)

• VM collateral can be rehypothecated and does not need to be segregated

11

Margining computation

12

Initial margining

• BCBS/IOSCO: IM may be calculated using a standardised margin schedule or an internal models (or a third party model)

• IM models should cover potential future exposure (PFE) at the 99% confidence level over a 10-day horizon

Variation margining

• Based on current exposure and is calculated by the mark-to-market value of derivatives

Standardised initial margin schedule (BCBS/IOSCO)

.

Fundamentals of ISDA SIMM

ISDA estimates the total IM for the entire market under standardised is USD 10.2 trn vs USD

1.7 trn under internal models

ISDA key requirements for a standard internal model

Similarity with FRTB

• Adopts essentially the same risk factors and models them in a similar way

• SIMM takes into account non-delta risks: vega and curvature sensitivities

• Main difference: IM is based on a 99% VaR while FRTB is based on a 97.5% Expected Shortfall

13

• Easy to replicate and transparent

• Quick

• Extensible

• Low cost

• Governance

• Margin appropriateness

ISDA SIMM

Four product classes

• Interest rates and FX

• Equities

• Credit Qualifying (investment grade) and non-qualifying

• Commodities

IM amount

• IM per risk class IMrisk class = Deltarisk class + Vegarisk class + Curvaturerisk class

• Curvature and vega only need to be computed for products with optionality and volatility sensitivity respectively

• Netting only within product class: no cross-product class netting

• IM for product class

• r = risk class

• 𝜓 = correlation

• Total IM requirement for institution

14

Six risk classes

• Interest rates

• FX

• Equities

• Credit Qualifying

• Credit non-qualifying

• Commodities

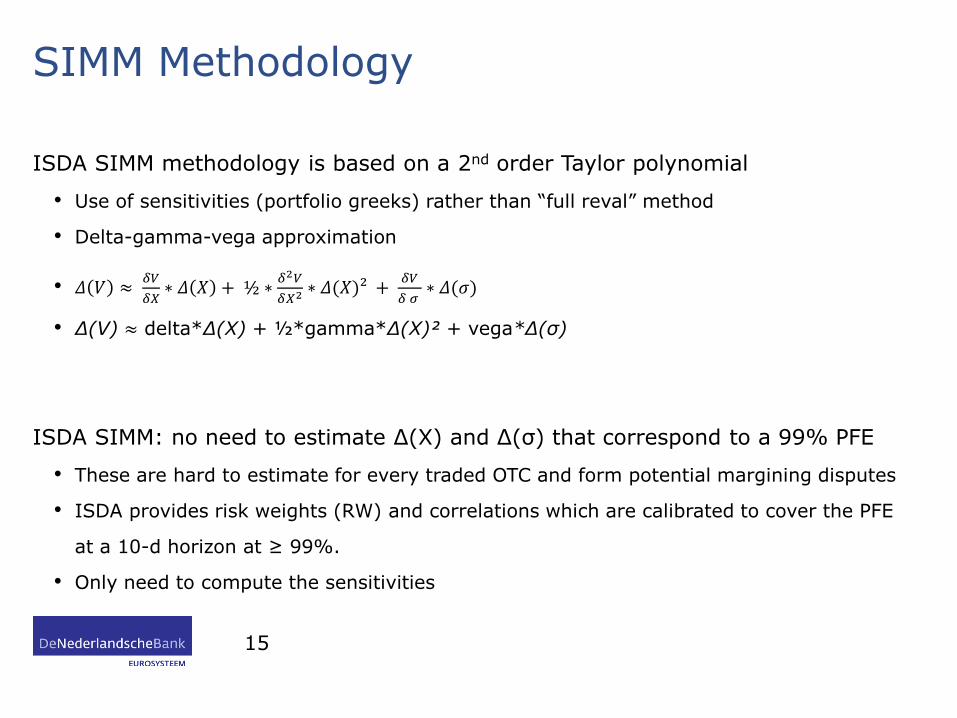

SIMM Methodology

ISDA SIMM methodology is based on a 2nd order Taylor polynomial

• Use of sensitivities (portfolio greeks) rather than “full reval” method

• Delta-gamma-vega approximation

• 𝛥 𝑉 ≈𝛿𝑉

𝛿𝑋∗ 𝛥 𝑋 + ½ ∗

𝛿2𝑉

𝛿𝑋2 ∗ 𝛥(𝑋)² +𝛿𝑉

𝛿 𝜎∗ 𝛥(𝜎)

• Δ(V) ≈ delta*Δ(X) + ½*gamma*Δ(X)² + vega*Δ(σ)

ISDA SIMM: no need to estimate Δ(X) and Δ(σ) that correspond to a 99% PFE

• These are hard to estimate for every traded OTC and form potential margining disputes

• ISDA provides risk weights (RW) and correlations which are calibrated to cover the PFE

at a 10-d horizon at ≥ 99%.

• Only need to compute the sensitivities

15

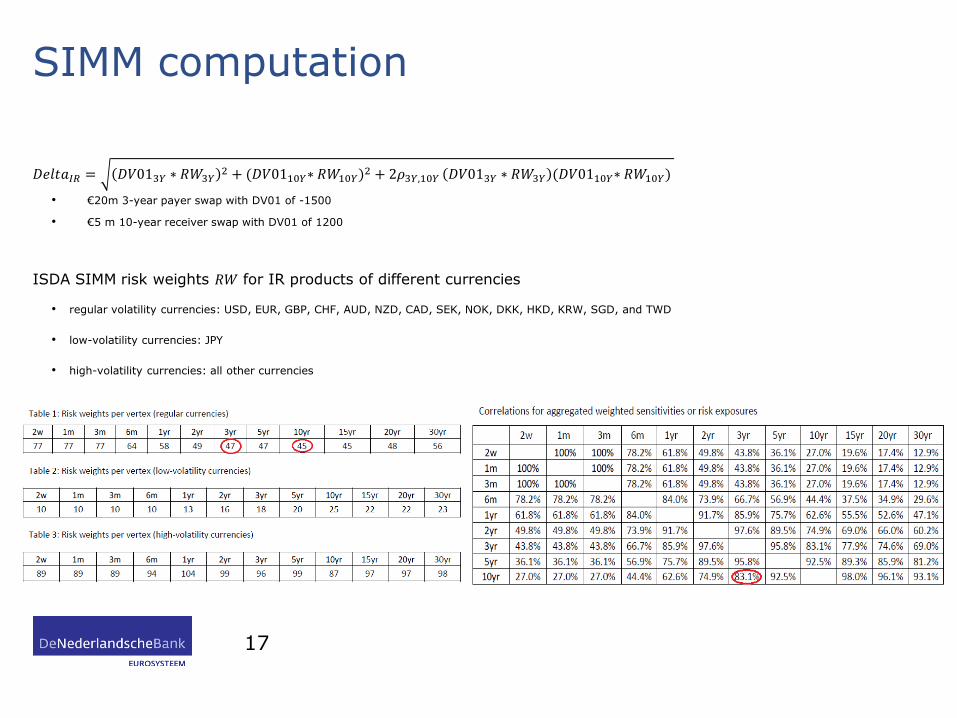

SIMM computation

Netting set of two trades

• €20m 3-year payer swap with DV01 of -1500

• €5 m 10-year receiver swap with DV01 of 1200

𝑆𝐼𝑀𝑀𝐼𝑅 & 𝐹𝑋 = 𝐷𝑒𝑙𝑡𝑎𝐼𝑅 & 𝐹𝑋 + 𝐶𝑢𝑟𝑣𝑎𝑡𝑢𝑟𝑒𝐼𝑅 & 𝐹𝑋 + 𝑣𝑒𝑔𝑎𝐼𝑅 & 𝐹𝑋

𝑆𝐼𝑀𝑀𝐼𝑅 = 𝐷𝑒𝑙𝑡𝑎𝐼𝑅 (curvature and vega do not have to be calculated for IR swaps)

• 𝐷𝑒𝑙𝑡𝑎𝐼𝑅 = 𝐷𝑉013𝑌 ∗ 𝑅𝑊3𝑌2 + (𝐷𝑉0110𝑌∗ 𝑅𝑊10𝑌)

2 + 2𝜌3𝑌,10𝑌 𝐷𝑉013𝑌 ∗ 𝑅𝑊3𝑌 ∗ (𝐷𝑉0110𝑌∗ 𝑅𝑊10𝑌)

• 𝑅𝑊3𝑌, 𝑅𝑊10𝑌 and 𝜌3𝑌,10𝑌 can be found from ISDA SIMM tables

16

SIMM computation

𝐷𝑒𝑙𝑡𝑎𝐼𝑅 = 𝐷𝑉013𝑌 ∗ 𝑅𝑊3𝑌2 + (𝐷𝑉0110𝑌∗ 𝑅𝑊10𝑌)

2 + 2𝜌3𝑌,10𝑌 𝐷𝑉013𝑌 ∗ 𝑅𝑊3𝑌 (𝐷𝑉0110𝑌∗ 𝑅𝑊10𝑌)

• €20m 3-year payer swap with DV01 of -1500

• €5 m 10-year receiver swap with DV01 of 1200

ISDA SIMM risk weights 𝑅𝑊 for IR products of different currencies

• regular volatility currencies: USD, EUR, GBP, CHF, AUD, NZD, CAD, SEK, NOK, DKK, HKD, KRW, SGD, and TWD

• low-volatility currencies: JPY

• high-volatility currencies: all other currencies

17

SIMM computation

𝐷𝑒𝑙𝑡𝑎𝐼𝑅 = 𝐷𝑉013𝑌 ∗ 𝑅𝑊3𝑌2 + (𝐷𝑉0110𝑌∗ 𝑅𝑊10𝑌)

2 + 2𝜌3𝑌,10𝑌 𝐷𝑉013𝑌 ∗ 𝑅𝑊3𝑌 (𝐷𝑉0110𝑌∗ 𝑅𝑊10𝑌)

• €20m 3-year payer swap with DV01 of -1500

• €5 m 10-year receiver swap with DV01 of 1200

The margining rules allow for netting within product class

• 𝐷𝑒𝑙𝑡𝑎𝐼𝑅 = −1500 ∗ 47 2 + (1200 ∗ 45)2+2 ∗ 0.831 −1500 ∗ 47 (1200 ∗ 45)

• 𝑆𝐼𝑀𝑀𝐼𝑅 = 𝐷𝑒𝑙𝑡𝑎𝐼𝑅=39,484

Under no netting within product-class

• 𝐼𝑀3𝑌 = −1500 ∗ 47 2 = 70,500

• 𝐼𝑀10𝑌 = 1200 ∗ 45 2 = 54,000

• Individual margining amounts are higher due absence of netting benefits

18

Concerns

• IM impacts market-wide liquidity as the IM collateral cannot be re-

used except in a fairly narrow set of circumstances

• It becomes harder to access the OTC markets, while most market

participants use OTC derivatives to hedge their risks

• Procyclicaclity

19

Links

• BCBS/IOSCO http://www.bis.org/bcbs/publ/d317.pdf

• ISDA SIMM Methodology http://isda.link/simmmethodology

20