Embed Size (px)

Citation preview

AGF MANAGEMENT LIMITED

Scotia Capital Financials Summit

Tuesday September 14, 2004

Blake C. Goldring, CFAPresident and Chief Executive Officer

Randy AmbrosieExecutive Vice-President, Sales and Marketing

AGF: A GLOBAL INVESTMENT MANAGEMENT COMPANY

Established in 1957

Market capitalization: $1.6 billion

Total assets under management: $31.1 billion

Dividend yield: 2.51%

August 31, 2004

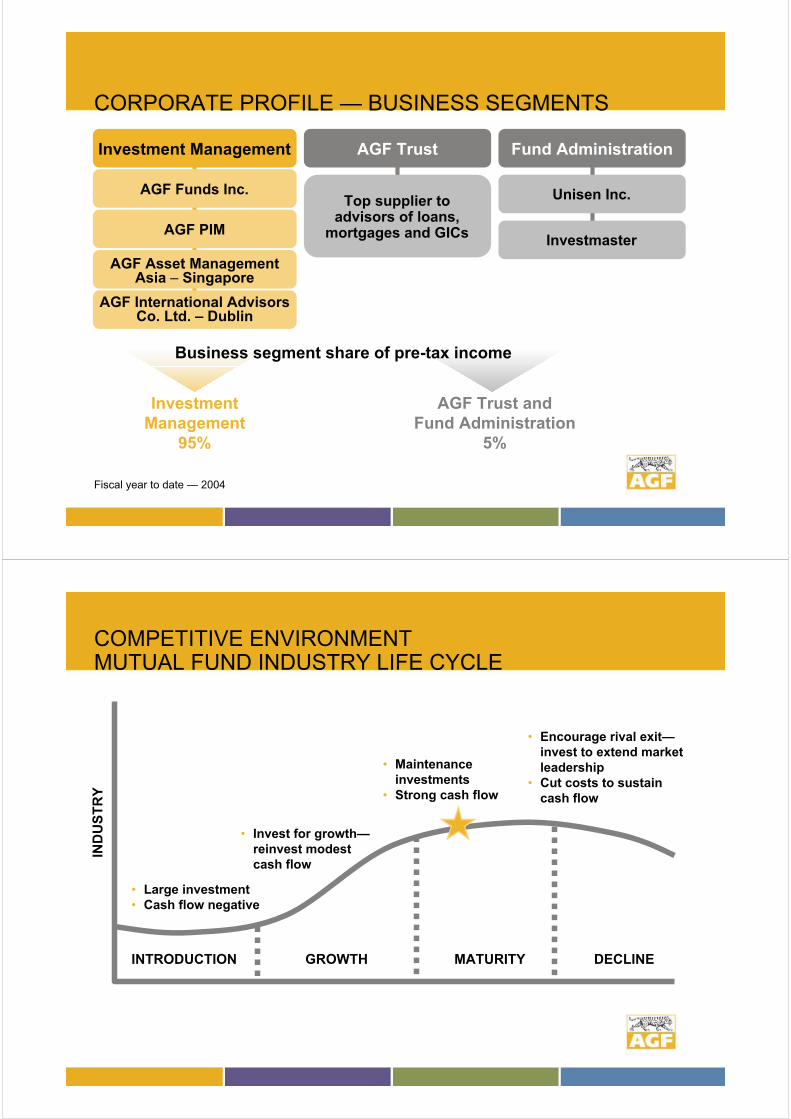

CORPORATE PROFILE — BUSINESS SEGMENTS

Investment Management

AGF Funds Inc.

AGF PIM

AGF International Advisors Co. Ltd. – Dublin

AGF Asset Management Asia – Singapore

AGF Trust

Top supplier to advisors of loans,

mortgages and GICs

Fund Administration

Unisen Inc.

Investmaster

Investment

95%

AGF Trust andFund Administration

5%

Business segment share of pre-tax income

Management

Fiscal year to date — 2004

COMPETITIVE ENVIRONMENTMUTUAL FUND INDUSTRY LIFE CYCLE

IND

US

TR

Y

INTRODUCTION GROWTH MATURITY DECLINE

• Large investment• Cash flow negative

• Invest for growth—reinvest modest cash flow

• Maintenance investments

• Strong cash flow

• Encourage rival exit—invest to extend market leadership

• Cut costs to sustain cash flow

COMPETITIVE ENVIRONMENTCHALLENGING CYCLICAL FACTORS

Equity funds have been 6% of total industry sales 2004 YTD.

Dividend & Income 31%

Balanced 25%

Canadian Common Shares 0%

US and Foreign Shares 6%

Bond & Income 36%

Mortgage & Real Estate 2%

2004 YTD Industry Net Sales*

* Calendar year to July, 2004

Fund Type — July, 2004*

59%41%

74%

17%

14%

14%23%

43%

11%1%2%1%

0%

20%

40%

60%

80%

100%

Industry Banks AGF

Equities Balanced Fixed Income Real Estate

COMPETITIVE ENVIRONMENTEMERGING CYCLICAL TRENDS

* IFIC

STRATEGIC PRIORITIES

• Reinforce investment management excellence

• Build a client centric organization focused on multi-channel distribution

• Pursue strategic acquisitions to supplement organic growth

• Undertake disciplined review of support entities

STRATEGIC PRIORITIES

• Reinforce investment management excellence

• Build a client centric organization focused on multi-channel distribution

• Pursue strategic acquisitions to supplement organic growth

• Undertake disciplined review of support entities

LONG-TERM PERFORMANCE TELLS A STORY:STRENGTH IN NUMBERS

Fund Performance Comparison — July 31, 2004% of Total Assets Above Median

AGF 61% 75%

C.I. 49% 28%

CIBC 47% 37%

Fidelity 70% 73%

IG 41% 21%

MacKenzie 61% 87%

Royal Bank 51% 29%

TD Bank 55% 82%

AIM/Trimark 92% 54%

COMPANY FIVE YEAR TEN YEAR

Source: BellCharts as at July 31, 2004Top companies by assets

OUR CATEGORY KILLER POTENTIAL

• AGF Canadian Real Value Fund

– We have one of the best value managers in the business in Keith Graham

• AGF European Equity Fund

– #2 European Equity Fund Manager Worldwide — Mercer Investment Consulting*

• AGF International Value Fund

– Harris Associates named one of Kiplinger’s top 10 U.S. fund companies

• Harmony

– “AGF Harmony was the only wrap program that advanced in asset ranking last year . . . and posted the highest year-over-year [AUM] growth rate for 2003”**

* Source: Financial Times, in a survey conducted by Mercer Investment Consulting for the three years ended December 31, 2003

** Source: Investor Economics, Fee-based Report: Winter 2004, HEFW Category

INVESTMENT MANAGEMENT — TACTICS

1. Clarify and articulate each fund’s philosophy and style

2. Investigate sub brand strategy

3. Review our investment disciplines

– Extract better performance from our processes

STRATEGIC PRIORITIES

• Reinforce investment management excellence

• Build a client centric organization focused on multi-channel distribution

• Pursue strategic acquisitions to supplement organic growth

• Undertake disciplined review of support entities

AGF MANAGEMENT LIMITED

Randy AmbrosieExecutive Vice-President, Sales and Marketing

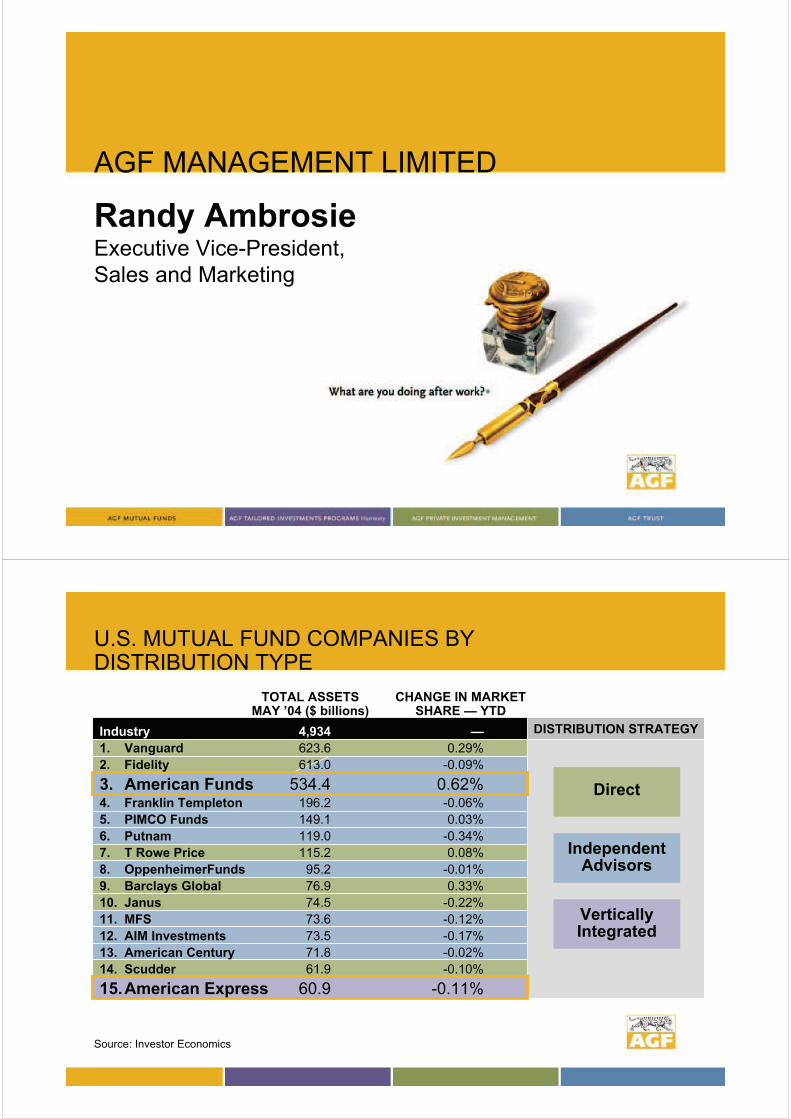

U.S. MUTUAL FUND COMPANIES BY DISTRIBUTION TYPE

DISTRIBUTION STRATEGY

Direct

Independent Advisors

VerticallyIntegrated

Industry 4,934 —

1. Vanguard 623.6 0.29%

2. Fidelity 613.0 -0.09%

3. American Funds 534.4 0.62%4. Franklin Templeton 196.2 -0.06%

5. PIMCO Funds 149.1 0.03%

6. Putnam 119.0 -0.34%

7. T Rowe Price 115.2 0.08%

8. OppenheimerFunds 95.2 -0.01%

9. Barclays Global 76.9 0.33%

10. Janus 74.5 -0.22%

11. MFS 73.6 -0.12%

12. AIM Investments 73.5 -0.17%

13. American Century 71.8 -0.02%

14. Scudder 61.9 -0.10%

15.American Express 60.9 -0.11%

Source: Investor Economics

TOTAL ASSETSMAY ’04 ($ billions)

CHANGE IN MARKET SHARE — YTD

PERCENT OF A TYPICAL CANADIAN ADVISOR’S SALES BY FUND FAMILY

0 10 20 30 40 50 60

Rank 1

Rank 2

Rank 3

Rank 4

Rank 5

Rank 6

Rank 7

Rank 8

2003

2003e

2002

2001

2000

Top 4 fund families =

90% of sales in 200384% of sales in 200283% of sales in 200184% of sales in 2000

Co

re s

up

po

rter

of

the

se

fu

nd

fam

ilie

sS

ec

on

d-t

ier

su

pp

ort

er

of

the

se

fu

nd

fa

mil

ies

On average, advisors continue to represent 6.4 fund families.

BUT!BUT!

BOTTOM UP APPROACHADVISOR CHANNEL

• Increase coverage capabilities– 29 core coverage teams

• Rationalize sales team compensation

– New assets

– Asset retention

• Additional coverage

– Strategic relationships

CLIENT CENTRIC — SALES TACTICS

Sales & Marketing

Advisor

Sales

Institutional

Sales

Customer

Relationship

Management

Product

Development

Marketing

Services

National

Accounts

STRATEGIC PRIORITIES

• Reinforce investment management excellence

• Build a client centric organization focused on multi-channel distribution

• Pursue strategic acquisitions to supplement organic growth

• Undertake disciplined review of support entities

STRATEGIC ACQUISITIONS —AGF PRIVATE INVESTMENT MANAGEMENT

Montreal•$1.2B in assets•Core Value•Large Cap

Calgary• Organic growth• Leverage PM’s

in Vancouver

Toronto• Organic

growth

Vancouver• $2B in assets• Oil & Gas• Small Cap

Ottawa• $1B in assets• Core Value• Fixed Income

Targets:

•50% cash flow margins

•15-20% ROI

STRATEGIC PRIORITIES

• Reinforce investment management excellence

• Build a client centric organization focused on multi-channel distribution

• Pursue strategic acquisitions to supplement organic growth

• Undertake disciplined review of support entities

SUPPORT BUSINESSES — AGF TRUST

AGF TRUST

• Leverages financial advisor offerings through loans, mortgages and GICs

• Consumer loans (investment and RSP) rose 16% in Q2 2004 versus Q1 2004

• Net income for Q2 2004 up 160%* over Q2 2003

*Increase does not include one-time gain of $0.6 million in Q2 2004

SUPPORT BUSINESSES — AGF TRUST

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2000 2001 2002 2003 2004

CAGR 41%

annualized

AGF Trust — Income Before Taxes($ 000’s)

100,

200,

300,

400,

500,

600,

700,

800,

000

000

000

000

000

000

000

000

2000 2001 2002 2003 2004

AGF Trust — Total Assets($ 000’s)

CAGR 43%

forecast

SUPPORT BUSINESSES

• Administration and/or technology solutions for 28 million investment fund accounts with $210 billion in assets

• Over 170 client relationships

• EBITDA for the fund administration segment for YTD 2004 up 156% over prior year

May 31, 2004

YTD 2004 RESULTS — DRIVING MOMENTUM

Revenue up 13.4%

Cash flow from operations up 26.7%

EBITDA up 13.8%

Net income up 55.5%

Includes $7.1 million tax benefit realized in Q2 2004.

Does not include $12.8 million capital gain in Q1 2003.

STRENGTH IN KEY MEASURES — BUSINESS GROWTH

EBITDA and Cash Flow Growth

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Year

EBITDA Cash Flow From Operations

CAGR: 28%

CAGR: 33%

annualized

UTILIZATION OF FREE CASH FLOW($ millions)

*2004 Data

• Debt reduction is a forecast

• Dividends and share repurchases are YTD annualized

• Acquisitions are YTD

0

20

40

60

80

100

120

140

160

2002 2003 2004*

Debt Reduction

Dividends

Acquisitions

Share Repurchases

DIVIDEND GROWTH —A PRIORITY USE OF FREE CASH FLOW

annualized

Annual Dividends Paid Per Share*

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

'97 '98 '99 '00 '01 '02 '03 '04

CAGR 24%

Dividends increased 37.5% in Q2 2004 to an annual rate of $0.44 per share

*Fiscal years ending November 30

RECOGNIZED LONG-TERM OUTPERFORMANCE

20-year performance among the 79 companies in the S&P/TSX composite that have been listed on the TSX for 20 years ending Nov 25 2003. Reported by National Post BUSINESS February 2004.

FORWARD LOOKING INFORMATION

This presentation contains certain forward-looking

statements that are made based on management’s

judgment and expectations but are inherently subject to

risks and uncertainties beyond the Corporation’s control.

These risks and uncertainties include economic conditions,

market fluctuations, interest rate and foreign exchange

movements, political events, regulatory change and

competitive developments. Actual results may differ

materially from those anticipated in the

forward-looking statements.