Embed Size (px)

Citation preview

Investor Presentation February 2015

These slides and the accompanying oral discussion contain certain statements that are not historical facts, including information concerning possible or assumed future results of our operations. Those statements constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements involve known and unknown risks, uncertainties and other factors that could cause the actual results of the Company to differ materially from the results expressed in or implied by our forward-looking statements, including the availability and cost of raw materials and purchased components, the level of construction and remodeling activity, changes in general economic and business conditions, conditions affecting the industries we serve and our customers, the rate of sales growth, availability of labor force and efficiencies, product liability claims, our high degree of leverage and other factors discussed in the Company’s offering circular relating to the 6.50% senior unsecured notes due 2022, including the documents incorporated therein by reference to the Company’s filings with the Securities and Exchange Commission, including the Company’s most recent Annual and Quarterly Reports on Form 10-K and Form 10-Q. Many of these factors are outside of the Company’s control and all of these factors are difficult or impossible to predict accurately. The Company undertakes no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise. In addition, these slides and the accompanying oral discussion reference financial information determined by methods other than in accordance with accounting principles generally accepted in the United States of America (“GAAP”), such as adjusted EBITDA. The Company’s management uses these non-GAAP measures in its analysis of the Company’s performance. The Company believes that the presentation of certain non-GAAP measures provides useful supplemental information that is essential to a proper understanding of the operating results of the Company’s core business. These non-GAAP measures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. A reconciliation of each non-GAAP financial measure to the most directly comparable GAAP financial measure is provided as an appendix to the slides.

Legal Disclaimer

1

Ply Gem Overview

2

• $1.8 Billion in LTM 9/27/14 (1)

• Approximately 8,700 associates

One of the Largest Manufacturers of Exterior Building and Home Improvement Products in North America

3

Company Overview

(1) LTM 9/27/14; Pro Forma for the Simonton acquisition.

44% 56% 52% 48%

NEW CONSTRUCTION / R&R(1) WINDOWS / SIDING (1)

16%

84%

U.S. / Canada(1)

• #1 in vinyl siding in North America

• #1 in aluminum accessories in U.S.

• #1 in vinyl / aluminum windows in U.S.

• #1 in windows in Western Canada

Leading Manufacturer of Exterior Building Products

4

Company Overview

Provider of branded products for new construction and home improvement markets, sold through a multitude of distribution channels covering a variety of price points

Extensive Exterior Product Portfolio

Engineered roofing products

Gable vents and accessories

Gutter protection systems

Vinyl and aluminum soffit

Window mantles

Manufactured stone

Vinyl and aluminum siding

Shutters

Mounting blocks

Decorative corner posts

Rain removal systems

Door surround systems

Patio Doors

Windows

Railing and fencing

Outdoor structures

Exterior doors

PVC trim

5

Company Overview

• Provides differentiation for Ply Gem customers

• Provides a single sourcing opportunity

• Hits the sweet spot of an emerging trend

• Features NAHB Green Approved products

• Fulfills the “One Ply Gem” MISSION

Alexandria, VA Designed Exterior Remodel

BEFORE

Three Weeks later using The Designed Exterior concept

AFTER

Complete Exterior Solution Offering for Customers Company Overview

6

Vinyl Siding Market Leader

• #1 vinyl siding manufacturer in North America (~39% share in the US)

• Consolidated industry with 4 participants holding over 90% share

• Strong trade brands

• Multi-channel distribution network servicing both new construction and R&R

• State-of-the-art automated manufacturing facilities with excess capacity

~$5,600

~$1,500 $738

Exterior CladdingMarket Size

Vinyl SidingMarket Size

Ply Gem 2013Net Sales

($ in mm)

Market size: According to Principia Partners.

Why Ply Gem Key Brands

North American Market Summary

7

Company Overview

• #1 vinyl and aluminum window manufacturer in the US

• #1 window and door manufacturer in Western Canada

• Multi-channel distribution network servicing both new construction and R&R covering every price point

• Highly efficient, vertically integrated production

• Continued to gain market share during downturn

$9,000

$628

Market Size Ply Gem 2013 Net Sales

($ in mm)

Market size: Company estimate – new construction and R&R. (1) Excludes Simonton net sales.

~

Vinyl and Aluminum Windows Market Leader

Why Ply Gem Key Brands

North American Market Summary

8

Company Overview

(1)

Regional local one-step distributors

New Construction

Regional/local one-step distributors

National one-step distributors

Retailers

Two-step distributors

Home Repair and Remodeling

• Homebuilders

• Contractors

• Contractors

• Individuals

Two-step distributors

National one-step distributors

Retailers

Homebuilders

Representative Customers Broad Supply Chain

Diversity of channels and customers with limited customer concentration Top 10 customers account for only ~40% of 2013 net sales 9

Multi-Channel Distribution Network Serving a Broad Customer Base

Company Overview

Manufacturing & Distribution Platform

10

Company Overview

Ply Gem Windows Manufacturing Siding Manufacturing Fence + Rail Manufacturing Corporate / HQ Stone Manufacturing Window Distribution – Canada Siding Distribution - Canada

Simonton Windows Manufacturing

29 Manufacturing Plants

34 Distribution Centers

• Customer solutions

• Customer experience

• Leading brands

• Measure, Engagement

• New Products / Solutions

• Utilize technology

• Open collaboration

• Sustainability

• Business diversity

• Cross sell our products

• Double digit growth

• World class safety & quality

• Low cost producer

• Efficient supply chain

Customer Focus

Innovation

Profitable Growth

Continuous Improvement

Human Resources

LEVERAGE

Company Overview

11

• Associate development

• Succession planning

• Communicate & empower

Company Overview

3.99 3.98

3.30

1.81 1.76 1.59 1.88 1.98

7.26 7.11

6.65

5.42 5.47 5.21 5.27

4.56

2006 2007 2008 2009 2010 2011 2012 2013

Ply Gem Combined National (US) Trend

WORLD CLASS

Ply Gem Safety is Top Priority

Recordable Incident Rate

Market and Housing Update

13

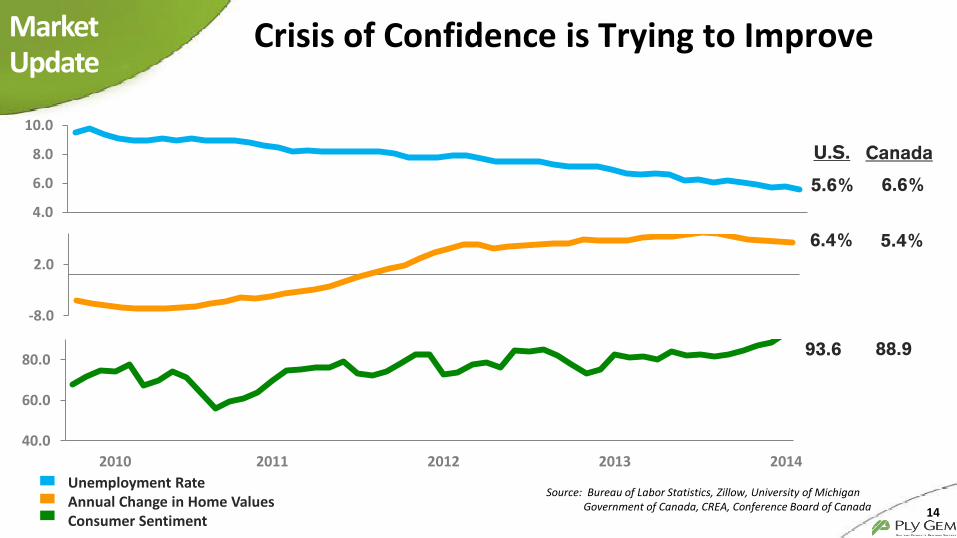

Crisis of Confidence is Trying to Improve

14

Market Update

-8.0

2.0

4.0

6.0

8.0

10.0

40.0

60.0

80.0

2010 2011 2012 2013 2014

Source: Bureau of Labor Statistics, Zillow, University of Michigan Government of Canada, CREA, Conference Board of Canada

Unemployment Rate Annual Change in Home Values Consumer Sentiment

5.6%

6.4%

93.6

Canada

6.6%

5.4%

88.9

U.S.

U.S. SFHS Forecasted to Increase

15

1,719 1,474

1,036

616 442 471 434 537 621 647

803 1,100

354

338

306

284

112 114 178 247

309 357 365

359

0

500

1,000

1,500

2,000

2,500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E

Single-Family Multi-Family(in thousands)

-75%

Market Update

Source: NAHB

Canada SFHS Forecast

16

121 119 93 76

94 82 84 77 75 78 75

106 109

118

73

97 112 131

111 114 112 112

0

50

100

150

200

250

2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015E 2016E

Single-Family Multi-Family

Market Update

Source: CMHC

(in thousands)

Growth Will be in Healthier Markets

17

Market Update

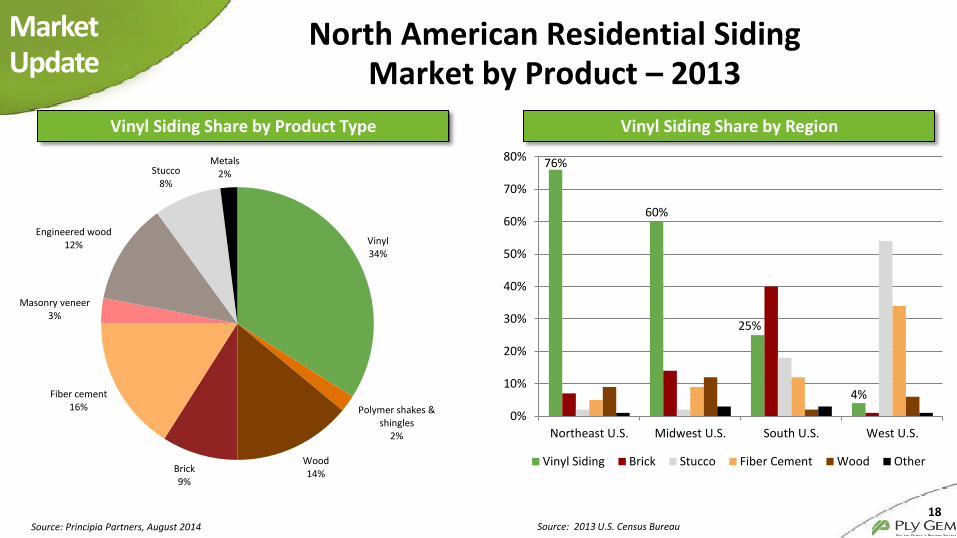

North American Residential Siding Market by Product – 2013

18

Market Update

Source: Principia Partners, August 2014

Vinyl 34%

Polymer shakes & shingles

2%

Wood 14% Brick

9%

Fiber cement 16%

Masonry veneer 3%

Engineered wood 12%

Stucco 8%

Metals 2%

76%

60%

25%

4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Northeast U.S. Midwest U.S. South U.S. West U.S.

Vinyl Siding Brick Stucco Fiber Cement Wood Other

Source: 2013 U.S. Census Bureau

Vinyl Siding Share by Region Vinyl Siding Share by Product Type

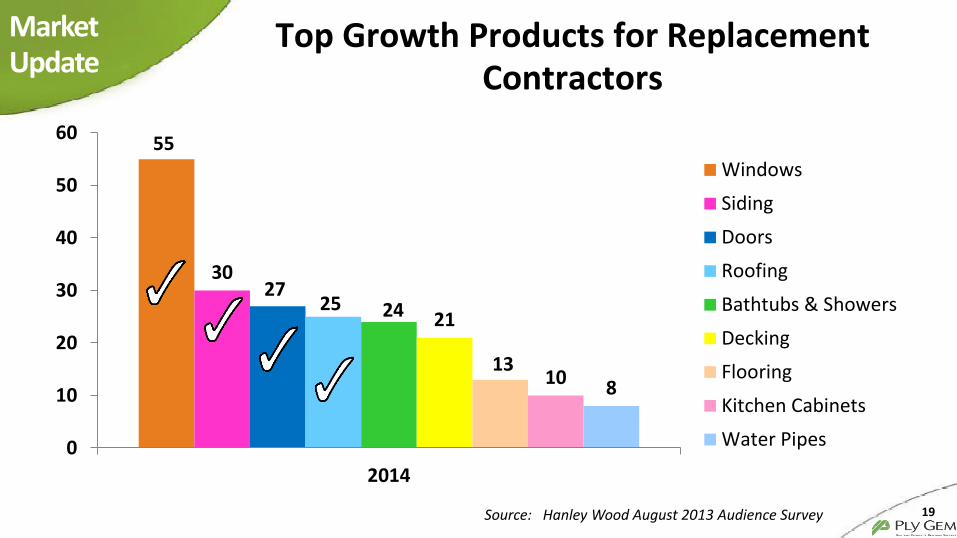

Top Growth Products for Replacement Contractors

19

55

30 27

25 24 21

13 10 8

0

10

20

30

40

50

60

2014

Windows

Siding

Doors

Roofing

Bathtubs & Showers

Decking

Flooring

Kitchen Cabinets

Water Pipes

Market Update

Source: Hanley Wood August 2013 Audience Survey

Financial Overview

20

Expected Achieved

MW Windows

($331mm)

2004 2005 2006 2007 2008

Alenco Windows

($127mm)

MHE (Alcoa) siding business ($296mm)

CT Windows

($37mm)

United Stone Veneer

($4mm)

Ply Gem purchased

by CI Capital

Expected Achieved Expected Achieved

2013

Gienow

(CAD$20mm)

Acq

uis

itio

ns

Co

st s

avin

gs

Mitten

(CAD$79mm)

Proven Track Record of Acquisition Integration / Cost Savings Realization

Acquisitions provide incremental capabilities and growth along with significant synergy opportunities

$6.8 $11.0 $4.0 $4.9 $22.0

$55.0

($ in mm)

21

Company Overview

Simonton

($130mm)

2014

Net Sales Adjusted EBITDA

$176

$96 $116 $123 $115 $127 $117 $114

0%

6%

12%

18%

24%

30%

2007 2008 2009 2010 2011 2012 2013 LTM9/27/14

Adj. EBITDA % of Sales

$1,364 $1,175

$951 $996 $1,035 $1,121

$1,366 $1,449

0

400

800

1200

1600

2007 2008 2009 2010 2011 2012 2013 LTM9/27/14

Ply Gem sales Single family housing starts

Key Consolidated Financial Performance

($ in mm) ($ in mm)

Source: Management, U.S. Census Bureau. Note: 2Q13 numbers include Gienow and Mitten from date of acquisition. 3Q14 numbers include Simonton from date of acquisition.

22

Financial Overview

Consistent Seasonal Adjusted EBITDA Performance

$12 $7 $15 $12

($1)

1Q10 1Q11 1Q12 1Q13 1Q14

$47 $44 $45 $41 $44

2Q10 2Q11 2Q12 2Q13 2Q14

$23 $24 $25 $16

4Q10 4Q11 4Q12 4Q13

$41 $40 $42 $48

$55

3Q10 3Q11 3Q12 3Q13 3Q14

% of net

sales 5.9% 3.3% 5.1% 4.6% (0.5%) 15.3% 14.5% 14.4% 11.2% 10.8% 14.9% 13.2% 13.3% 11.9% 12.6% 10.0% 9.8% 9.2% 4.8%

($ in mm)

Ply Gem 38%

CertainTeed 26%

Associated Materials 12%

Exterior/Royal 15%

Kaycan 5%

Other 4%

Ply Gem/Simonton 14%

Atrium 3%

Other(1) 26%

Pella 16%

Jeld Wen (includes doors) 13%

Marvin 8%

Anderson 20%

$535 $466

$374 $392 $396

$463

$628 $667

(20.0%)

(10.0%)

0.0%

10.0%

20.0%

30.0%

40.0%

$0

$200

$400

$600

$800

$1,000

2007 2008 2009 2010 2011 2012 2013 LTM 9/27/14

Sales Operating earnings margin

Andersen Pella Marvin JELD-WEN Atrium Associated Materials Milgard Simonton

Windows manufacturers (all substrates)

Source: Principia Partners 2014 study, management estimates.

One, Integrated Business with Two Reportable Segments

($ in mm) ($ in mm)

Siding, Fencing, and Stone Windows and Doors

Window Market Share in Units (All Types) - 2013 Vinyl Siding Market Share -2013

23

Company Overview

(1) Includes Associated Materials, Milgard, MI, Weathershield, Windsor, Harvey, Champion, Amsco, Cascade, and Kolbe.

$828

$709

$577 $604 $639 $658

$738 $782

(20.0%)

(10.0%)

0.0%

10.0%

20.0%

30.0%

40.0%

$0

$200

$400

$600

$800

$1,000

2007 2008 2009 2010 2011 2012 2013 LTM 9/27/14

Sales Operating earnings margin

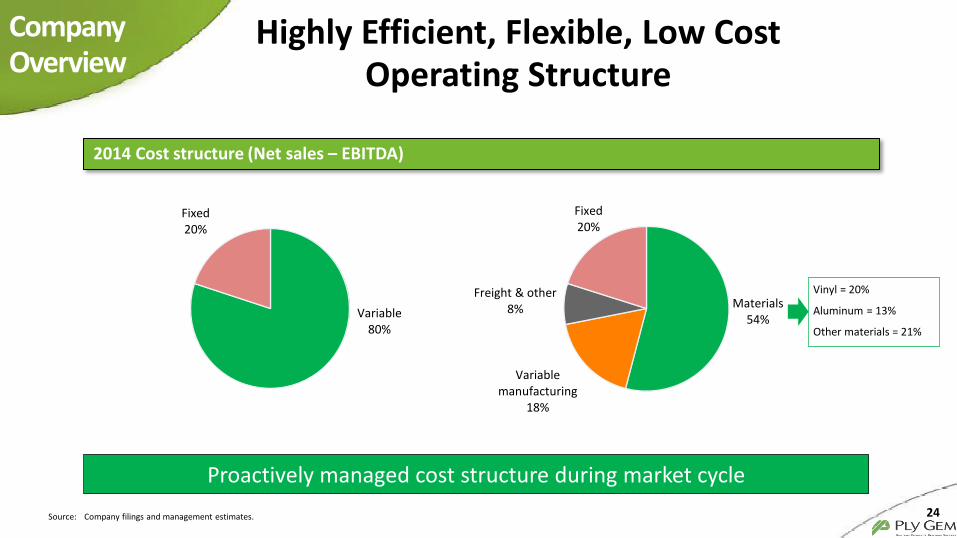

2014 Cost structure (Net sales – EBITDA)

Variable 80%

Fixed 20%

Materials 54%

Variable manufacturing

18%

Freight & other 8%

Fixed 20%

Vinyl = 20%

Aluminum = 13%

Other materials = 21%

Highly Efficient, Flexible, Low Cost Operating Structure

Source: Company filings and management estimates. 24

Company Overview

Proactively managed cost structure during market cycle

$20 $17

$8 $11 $11

$25 $26 $24

0.0%

0.8%

1.6%

2.4%

3.2%

2007 2008 2009 2010 2011 2012 2013 LTM9/27/14Capex % of Sales

FCF: Adjusted EBITDA – Capital Expenditures Capital Spending

• Modest capex ~1.7% of sales in LTM 9/27/14

• In excess of $248M in available liquidity at 3Q14

• No near-term maturities

$20

$430

$650

2017 2018 2019 2020 2021 2022ABL Term Loan Senior Notes

Debt Maturity - 3Q14

Substantial / Sustainable Free Cash Flow

History of strong EBITDA performance, modest capital expenditure requirements and efficient use of working capital 25

Financial Overview

$156

$80 $108 $112 $103

$103 $91 $90

2007 2008 2009 2010 2011 2012 2013 LTM9/27/14

($ in mm) ($ in mm)

($ in mm)

Questions

26

Appendix

27

Year Ended December 31,

(amounts in thousands) 2007 2008 2009

Net income (loss) $4,982 $(498,475) $(76,752)

Interest expense, net 97,994 137,398 135,303

Benefit for income taxes 3,634 (69,951) (17,966)

Depreciation and amortization 54,067 61,765 56,271

EBITDA $160,677 $(369,263) $96,856

Non cash loss (gain) on foreign currency transactions (3,961) 911 (475)

Goodwill impairment - 450,000 -

Intangible asset impairment 4,150 - -

Customer inventory buybacks - 1,890 8,345

Restructuring/integration expense 10,356 10,859 8,992

Non cash charge of purchase price allocated to inventories 1,289 19 -

Management fees 3,505 1,679 2,497

Adjusted EBITDA $176,016 $96,095 $116,215

28

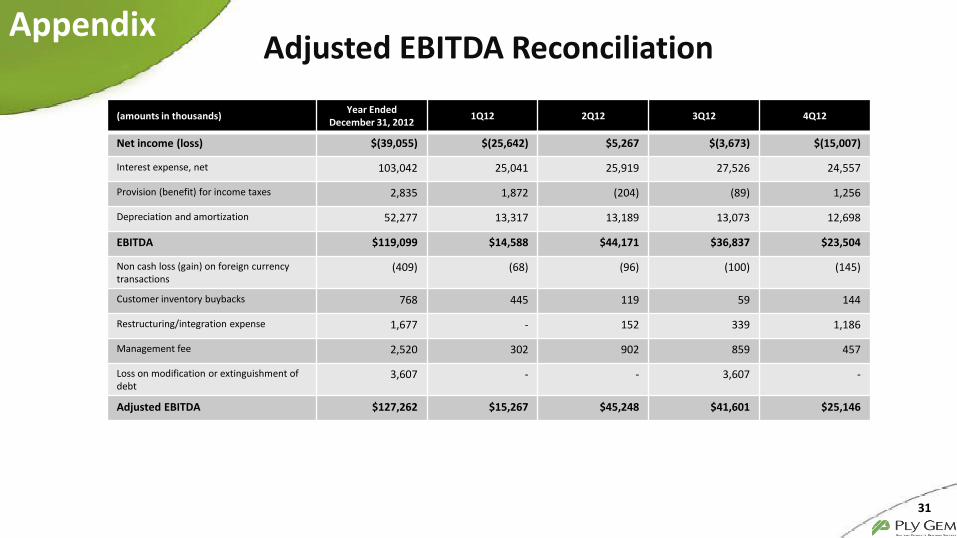

Adjusted EBITDA Reconciliation Appendix

(amounts in thousands) Year Ended

December 31, 2010 1Q10 2Q10 3Q10 4Q10

Net income (loss) $27,667 $54,102 $(409) $(6,394) $(19,632)

Interest expense, net 122,833 33,954 30,152 29,752 28,975

Provision (benefit) for income taxes 5,027 6,532 664 1,332 (3,501)

Depreciation and amortization 60,718 15,454 15,711 15,133 14,420

EBITDA $216,245 $110,042 $46,118 $39,823 $20,262

Non cash loss (gain) on foreign currency transactions

(510) (104) (122) (104) (180)

Write-off capitalized offering costs 1,571 1,571

Customer inventory buybacks 574 252 124 117 81

Restructuring/integration expense 910 106 83 405 316

Loss on modification or extinguishment of debt

(98,187) (98,187) - - -

Management fee 2,451 200 900 900 451

Adjusted EBITDA $123,054 $12,309 $47,103 $41,141 $22,501

29

Adjusted EBITDA Reconciliation Appendix

(amounts in thousands) Year Ended

December 31, 2011 1Q11 2Q11 3Q11 4Q11

Net income (loss) $(84,507) $(70,892) $2,063 $(458) $(15,220)

Interest expense, net 101,384 26,424 24,911 25,176 24,873

Provision (benefit) for income taxes 683 2,472 (959) 466 (1,296)

Depreciation and amortization 54,020 13,690 13,393 13,471 13,466

EBITDA $71,580 $(28,306) $39,408 $38,655 $21,823

Non cash loss (gain) on foreign currency transactions

(492) (133) (218) (115) (26)

Environmental remediation 1,580 - - - 1,580

Customer inventory buybacks 10,087 6,692 2,971 315 110

Restructuring/integration expense 1,616 429 477 547 163

Gain on modification or extinguishment of debt

27,863 27,863 - - -

Management fee 2,267 100 900 800 467

Adjusted EBITDA $114,501 $6,645 $43,538 $40,201 $24,117

30

Adjusted EBITDA Reconciliation Appendix

(amounts in thousands) Year Ended

December 31, 2012 1Q12 2Q12 3Q12 4Q12

Net income (loss) $(39,055) $(25,642) $5,267 $(3,673) $(15,007)

Interest expense, net 103,042 25,041 25,919 27,526 24,557

Provision (benefit) for income taxes 2,835 1,872 (204) (89) 1,256

Depreciation and amortization 52,277 13,317 13,189 13,073 12,698

EBITDA $119,099 $14,588 $44,171 $36,837 $23,504

Non cash loss (gain) on foreign currency transactions

(409) (68) (96) (100) (145)

Customer inventory buybacks 768 445 119 59 144

Restructuring/integration expense 1,677 - 152 339 1,186

Management fee 2,520 302 902 859 457

Loss on modification or extinguishment of debt

3,607 - - 3,607 -

Adjusted EBITDA $127,262 $15,267 $45,248 $41,601 $25,146

31

Adjusted EBITDA Reconciliation Appendix

(amounts in thousands) Year Ended

December 31, 2013 1Q13 2Q13 3Q13 4Q13

Net income (loss) $(79,520) $(28,107) $(50,877) $16,895 $(17,431)

Interest expense, net 91,684 23,653 24,833 21,760 21,438

Provision (benefit) for income taxes 298 3,849 (731) (1,442) (1,378)

Depreciation and amortization 45,646 9,715 11,171 12,097 12,663

EBITDA $58,108 $9,110 $(15,604) $49,310 $15,292

Non cash loss (gain) on foreign currency transactions

1,533 33 346 376 778

Acquisition costs 1,490 315 1,025 150 -

Customer inventory buybacks 4,837 - 2,172 2,503 162

Restructuring/integration expense 11,759 2,380 1,439 1,529 6,411

Non cash charge of purchase price allocated to inventories

2,015 - 883 1,132 -

Management fee 410 235 175 - -

Loss on modification or extinguishment of debt

18,948 - 18,948 - -

Initial public offering costs 23,527 - 23,527 - -

Tax receivable agreement liability adjustment

(5,167) - 8,143 (6,669) (6,641)

Adjusted EBITDA $117,460 $12,073 $41,054 $48,331 $16,002 32

Adjusted EBITDA Reconciliation Appendix

(amounts in thousands) 1Q14 2Q14 3Q14 LTM Sept 14

Net income (loss) $(51,578) $11,380 $21,405 $(36,224)

Interest expense, net 18,494 17,225 16,282 73,439

Provision (benefit) for income taxes (12,470) 7,051 (10,514) (17,311)

Depreciation and amortization 11,284 11,254 11,378 46,579

EBITDA $(34,270) $46,910 $38,551 $66,483

Non cash loss (gain) on foreign currency transactions

228 (477) 766 1,295

Acquisition costs - - 664 664

Customer inventory buybacks 123 359 306 950

Restructuring/integration expense 1,717 1,462 1,067 10,657

Litigation settlement 5,000 - - 5,000

Loss on modification or extinguishment of debt 21,364 - - 21,364

Non cash charge of purchase price allocated to inventories

- - 38 38

Tax receivable agreement liability adjustment 4,373 (3,942) 13,988 7,778

Adjusted EBITDA $(1,465) $44,312 $55,380 $114,229

33

Adjusted EBITDA Reconciliation Appendix