VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 1 of 21

General Guidelines

Eligibility

• Owner Occupied - must occupy within 60 days of the closing date

• LTV 100% based on VA County Loan Limits VA Loan Limits

• Veteran must have sufficient entitlement available to meet the minimum 25% loan guarantee - loan may require a down payment to lower loan amount

• Purchase: Minimum 620 FICO

• Type I Cash-Out & Type II Cash-Out Refinance: Minimum 660 FICO

Ineligible Loans

• Joint loans between a Veteran and a non-spouse co-obligor

• Non-occupant co-borrower

• Supplemental Loans

• Construction financing with draws

• Energy Efficient Mortgage Program

• Borrower who has experience a prior foreclosure on the subject property is ineligible to purchase or refinance the same property

• Non-traditional Credit (no credit scores)

Maximum LTV

• Follow VA County Loan Limits VA Loan Limits

• Purchase: 100% NOT including Financed Funding Fee • Type I and Type II Cash-Out Refinance: 100% including Financed Funding Fee

Maximum CLTV • 100% - No Subordinate Financing

Property Types

Eligible:

• SFR, 2-4 Units, Detached Condos (Michigan), PUDs

• VA Approved Attached and Detached Condos

Ineligible:

• Manufactured Homes, Non-Warrantable Condos, Hotel/Resort Projects, Leaseholds, Co-ops, Farms/Ranches, Earth Berm, Geodesic Dome, Timeshares, Condo Hotels, Log Homes, Income Producing Properties (crops, tree farms, etc.) or other unique properties (not permanently affixed heat source, zero bedrooms above grade, major functional obsolescence like in fall area of power lines, etc.)

• The borrower must not have had prior ownership in the subject property for purchase transactions

• A borrower who has experienced a prior foreclosure on the subject property is ineligible to purchase or refinance the same property

• When there is an identity of interest between the purchaser and seller, the seller cannot have acquired the property due to borrower default

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 2 of 21

Eligible States HVF State Licensing Map

General Guidelines

Geographic Restrictions

Texas cash out refinance not allowed, including section50(a)(6)

Eligible Terms

Conforming and High Balance Fixed Rate (No Buydowns)

• 10 years

• 15 years

• 20 years

• 30 years

Qualifying Rate Note Rate

Qualifying Ratios

• 41%

• May exceed 41% with o DU Approve Eligible (up to 50%) AND o Residual income calculation exceeding 120%

Residual Income Calculation for VA

Loan Analysis

In addition to standard monthly reoccurring debts, the following obligations are also added to liabilities:

• Child Care Expenses (for children 12 years and younger)

• Deductions/Allotments on paystubs & any extra ordinary commuting expenses Maintenance & Utility calculations are based on 14 per square foot of the GLA Calculate tax deductions to support net take home pay VA Residual Income Calculation Tables

• Determine region

• Determine family size – must include all occupants (not just dependents of the Veteran)

Underwriting

• DU Approve/Eligible

• Manual underwrite permitted o AUS Downgrade o AUS Refer o Credit Score 660

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 3 of 21

Funding Fee

• Can be rolled into 100% financing unless property is at the maximum county loan limit

• Amortized over the life of the loan, with no refund

• If Veteran is exempt or previously used their entitlement, it will be noted on the Certificate of Eligibility

• Funding fee can be reduced with a down payment on purchase transactions unless source is a ‘gift of equity’.

• VA Funding Fee Table

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 4 of 21

General Guidelines

Power of Attorney

• For purchase: Military Power of Attorney OR ‘specific to the transaction’ Power of Attorney is allowed

• For cash out: a ‘specific to transaction’ Power of Attorney is allowed that includes max amount of cash out to be included

• Title policy may not include any exceptions related to the POA

• Verify the Veteran is alive and well at the time of closing using Lender Certificate of Power of Attorney for VA Home Loan

• Active Veteran: Must provide a written statement from the borrower or commanding officer, the day of closing that the Veteran is alive and well and not missing in action using Veteran’s Alive and Well Statement

• Discharged Veteran: Must provide a written statement the day of closing, that they are alive and well

• Must not be an interested party (realtor, seller, closing agent)

Age of Documents • Credit documents including but not limited to credit reports income, assets,

and title documentation cannot exceed 120 days from the Note Date

• Effective date of the appraisal cannot exceed 180 days from the Note Date

LDP/GSA Required for all parties associated in the transaction

CAIVRS Clear CAIVR is required for all borrowers. Veteran must not have any unpaid Federal Debts.

Eligible Borrowers • Veterans • Veterans and spouse • Only Veteran and Spouse can be on title

Certificate of Eligibility

• A Certificate of Eligibility (COE) is the ONLY acceptable proof of eligibility and is issued by the VA through webLGY

• A COE is required for all VA purchase and cash out refinance transactions • COEs greater than 4 months old are considered expired and an updated COE

is required prior to close • A COE may be processed manually through the VA Atlanta RLC office

however documentation must be uploaded to the webLGY system (you may call this office to follow up on requests at 888-768-2132)

• The Veteran’s name on the Certificate of Eligibility must MATCH the Veteran’s name in webLGY, the loan guaranty certificate and the note and mortgage

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 5 of 21

Identity of Interest No restrictions

General Guidelines

Non-Purchasing Spouse

Except for obligations specifically excluded by state law, the debts of the non-purchasing/non-borrowing spouse must be included in the borrower’s qualifying ratios, if the borrower resides in a community property state, or property being insured is located in a community property state such as but not limited to Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin. The non-purchasing/non-borrowing spouse’s obligations must be considered in the debt-to-income (DTI) ratio unless excluded by state law. A tri-merged credit report must be provided for the non-purchasing/non-borrowing spouse in order to determine the debts that must be counted in the DTI ratio. The non-purchasing spouse/non-borrowing spouse must provide a signed/dated Borrower’s Credit Authorization.

Refinances

Not including

IRRRL

Type I Cash-Out The loan amount (including the VA funding fee) does not exceed the payoff amount of the loan being refinanced.

Type II Cash-Out The loan amount (including the VA funding fee) exceeds the payoff amount of the loan being refinanced.

VA to VA Non-VA to VA

VA to VA Non-VA to VA

• Max Loan-to-Value (LTV) 100%

• Property may not be owned free & clear

• Existing lien must be reflected on title policy

• Appraisal required

• Net Tangible Benefit (NTB) required details in NTB section

• Comparison Worksheet, Equity Disclosure, and NTB Disclosure must be delivered to borrower within 3 business days of application and at closing

• Loan Seasoning Required1

• Fee Recoupment2

• Interest Rate Requirement3

• FRM to ARM4

Loan Seasoning Required1

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 6 of 21

1 - Loan being refinanced must be seasoned using the later of 210 days after the first monthly payment is made and at least 6 monthly payments have been made. 2 - Recoupment of all fees, closing costs, expenses (other than taxes, escrow, insurance, and like assessments) must be < 36 months from the date of closing. 3 - Interest Rate Requirements

• FRM to FRM: the interest rate on new loan must be > 0.5% lower than the interest rate of the loan being refinanced

• FRM to ARM: the interest rate on new loan must be > 2% lower than the interest rate of the loan being refinanced

4 - Max 90% LTV when financing discount points >1%

General Guidelines

Net Tangible Benefits (NTB)

For Cash Out Refinance

Type I and Type II Cash-Out Refinance Loans must satisfy at least 1 of 8 benefits (listed below) over the existing loan being refinanced:

1. The new loan eliminates monthly mortgage or guaranty insurance 2. The term of the new loan is shorter 3. The interest rate on the new loan is lower 4. The principle & interest payment on the new loan is lower 5. The new loan results in an increase in the borrower’s monthly residual income 6. The new loan refinances an interim loan to construct, alter, or repair the home 7. The new loan amount is < 90% of the reasonable value of the home 8. The new loan refinances an ARM to FRM

Land Contract Refinances

• 100% LTV

• Land Contract payoff and roll in allowable costs. No cash in hand permitted.

• Use the lessor of acquisition cost or appraised value to determine LTV when land contract prepared date is less than 12 months.

• The following documentation is required: Copy of land contract, most recent 12 months cancelled checks or bank statements to evidence on time payments, amortization schedule and a payoff statement from land contract holder. Short payoff figures from comparison by underwriter to the amortization schedule are not acceptable.

• Maximum loan amount is $144,000 (bonus entitlement is not available)

• Appraisal required

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 7 of 21

Property Flipping

• No seasoning for seller ownership of subject - must be in title prior to execution of the purchase agreement.

• It is underwriter discretion to review value and any increases to value must be warranted and/or otherwise supported in the loan file. Appraiser to provide complete list of any renovations or upgrades made to subject since its recent acquisition by seller, appraiser could further elaborate on being sold previously under market value conditions as a foreclosure sale, short sale, estate sale, etc.

Payoff/Pay Down Debt for

Qualification

• Installment loans may be paid off and payment excluded from qualifying ratios • Revolving trades that are paid to a zero balance and closed prior to closing

are excluded from ratios (asset sourcing is required) • Installment debt paid down to 6 remaining monthly payment is not permitted • Installment debt with 6 payments remaining is allowed under the following

guidance: o The debt may not be automatically excluded as a liability o Underwriter must determine if the debt will impact the borrower’s ability to

repay mortgage by reviewing ratio with debt, verifying residual income meets guidelines including debt, OR borrower has sufficient liquid assets to cover debt

• Underwriter justification must be noted on VA Loan Analysis

Other Co-owned Property

• When the borrower is on title to a property as an owner but is not on the Note, Mortgage or Land Contract as a borrower, they must qualify with the taxes, insurance and HOA dues, if applicable, for said property in the DTI ratios.

Debt Paid by/ through

Borrower’s Business

The account payment does not need to be considered as part of the borrower’s individual recurring monthly debt obligations if: • the account in question does not have a history of delinquency AND • the business provides acceptable evidence that the obligation was paid out of

company funds such as 12 months of canceled company checks • The debt was considered in the cash flow analysis of the borrower’s business

Liabilities

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 8 of 21

Court Ordered Assignment of

Debt / Contingent Liabilities

When a borrower has outstanding debt that was assigned to another party by court order, such as under a divorce decree or separation agreement, and the creditor does not release the borrower from liability, the borrower has a contingent liability. The lender is not required to count this contingent liability as part of the borrower’s recurring monthly debt obligations.

The lender is not required to evaluate the payment history for the assigned debt after the effective date of the assignment. The lender cannot disregard the borrower’s payment history for the debt before its assignment.

401K & Other Retirement

Loan Payments

401K or 403B loan types do not need to be included in the veteran’s ratios or residual calculations

Student Loan Payments

• If a borrower provides written evidence that the student loan debt will be deferred beyond 12 months of closing, a monthly payment does not need to be considered

• If a student loan is in repayment or scheduled to begin within 12 months of closing, the lender MUST consider the anticipated monthly payment and utilize the payment established by: o Calculating each loan at a rate of 5% of the outstanding balance divided

by 12 months o If the payments reported on the credit report are less than the threshold

payment calculation (above) the lender must use the payments on the credit report

o If the payment reported on the credit report is less than the threshold payment calculation (above), to count the lower payment, the file must contain a statement from the student loan servicer reflecting actual terms and payment for each loan

• Statement must be dated within 60 days of loan closing

• Lender’s discretion regarding credit supplementation

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 9 of 21

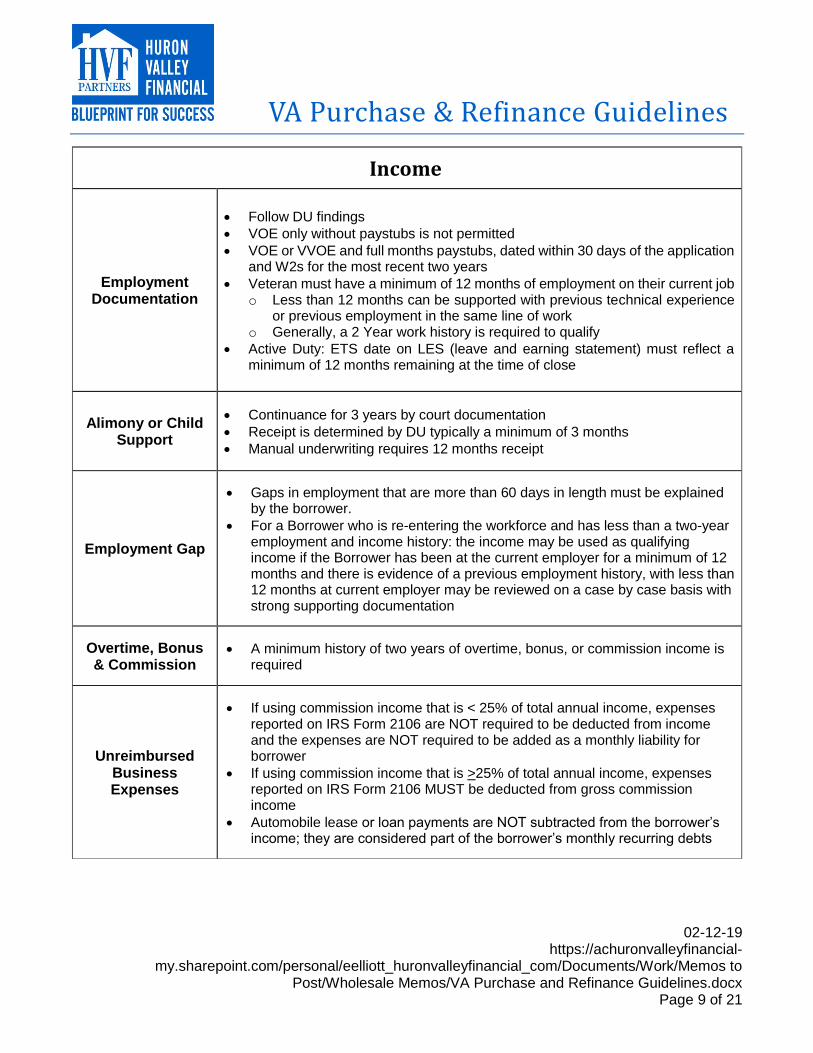

Income

Employment Documentation

• Follow DU findings

• VOE only without paystubs is not permitted

• VOE or VVOE and full months paystubs, dated within 30 days of the application and W2s for the most recent two years

• Veteran must have a minimum of 12 months of employment on their current job o Less than 12 months can be supported with previous technical experience

or previous employment in the same line of work o Generally, a 2 Year work history is required to qualify

• Active Duty: ETS date on LES (leave and earning statement) must reflect a minimum of 12 months remaining at the time of close

Alimony or Child Support

• Continuance for 3 years by court documentation

• Receipt is determined by DU typically a minimum of 3 months

• Manual underwriting requires 12 months receipt

Employment Gap

• Gaps in employment that are more than 60 days in length must be explained by the borrower.

• For a Borrower who is re-entering the workforce and has less than a two-year employment and income history: the income may be used as qualifying income if the Borrower has been at the current employer for a minimum of 12 months and there is evidence of a previous employment history, with less than 12 months at current employer may be reviewed on a case by case basis with strong supporting documentation

Overtime, Bonus & Commission

• A minimum history of two years of overtime, bonus, or commission income is required

Unreimbursed Business Expenses

• If using commission income that is < 25% of total annual income, expenses reported on IRS Form 2106 are NOT required to be deducted from income and the expenses are NOT required to be added as a monthly liability for borrower

• If using commission income that is >25% of total annual income, expenses reported on IRS Form 2106 MUST be deducted from gross commission income

• Automobile lease or loan payments are NOT subtracted from the borrower’s income; they are considered part of the borrower’s monthly recurring debts

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 10 of 21

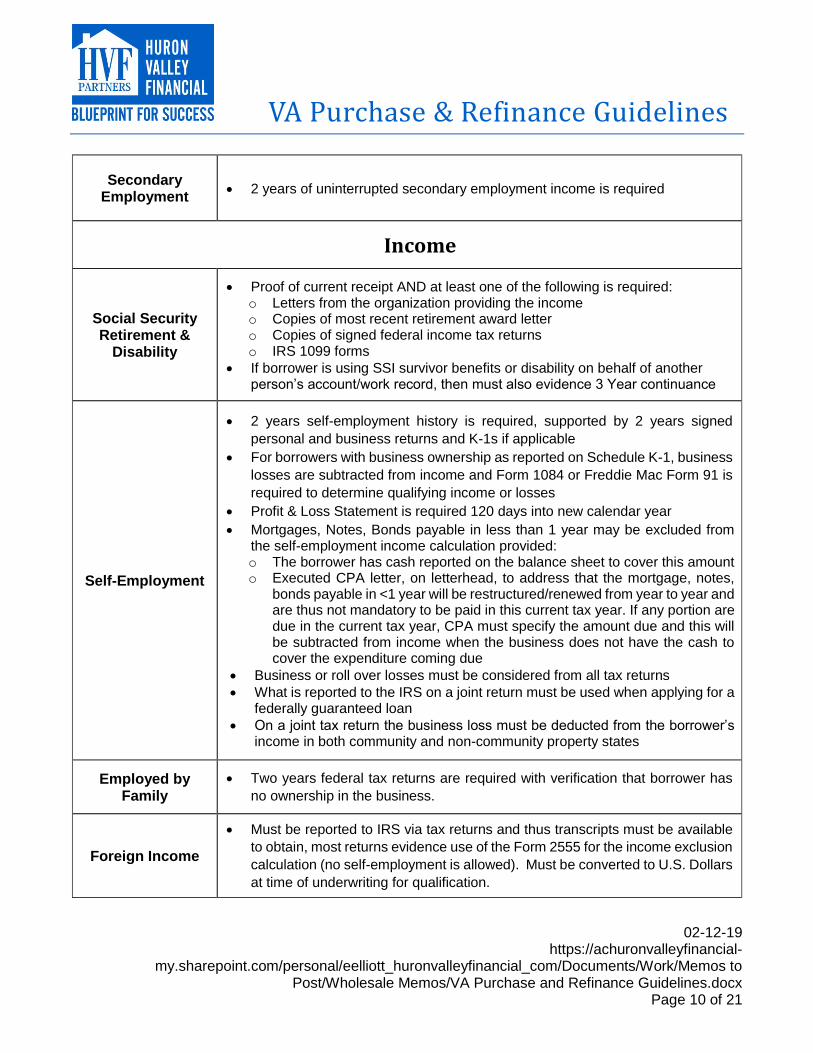

Secondary Employment

• 2 years of uninterrupted secondary employment income is required

Income

Social Security Retirement &

Disability

• Proof of current receipt AND at least one of the following is required: o Letters from the organization providing the income o Copies of most recent retirement award letter o Copies of signed federal income tax returns o IRS 1099 forms

• If borrower is using SSI survivor benefits or disability on behalf of another person’s account/work record, then must also evidence 3 Year continuance

Self-Employment

• 2 years self-employment history is required, supported by 2 years signed

personal and business returns and K-1s if applicable

• For borrowers with business ownership as reported on Schedule K-1, business

losses are subtracted from income and Form 1084 or Freddie Mac Form 91 is

required to determine qualifying income or losses

• Profit & Loss Statement is required 120 days into new calendar year

• Mortgages, Notes, Bonds payable in less than 1 year may be excluded from the self-employment income calculation provided: o The borrower has cash reported on the balance sheet to cover this amount o Executed CPA letter, on letterhead, to address that the mortgage, notes,

bonds payable in <1 year will be restructured/renewed from year to year and are thus not mandatory to be paid in this current tax year. If any portion are due in the current tax year, CPA must specify the amount due and this will be subtracted from income when the business does not have the cash to cover the expenditure coming due

• Business or roll over losses must be considered from all tax returns

• What is reported to the IRS on a joint return must be used when applying for a federally guaranteed loan

• On a joint tax return the business loss must be deducted from the borrower’s income in both community and non-community property states

Employed by Family

• Two years federal tax returns are required with verification that borrower has

no ownership in the business.

Foreign Income

• Must be reported to IRS via tax returns and thus transcripts must be available

to obtain, most returns evidence use of the Form 2555 for the income exclusion

calculation (no self-employment is allowed). Must be converted to U.S. Dollars

at time of underwriting for qualification.

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 11 of 21

Income

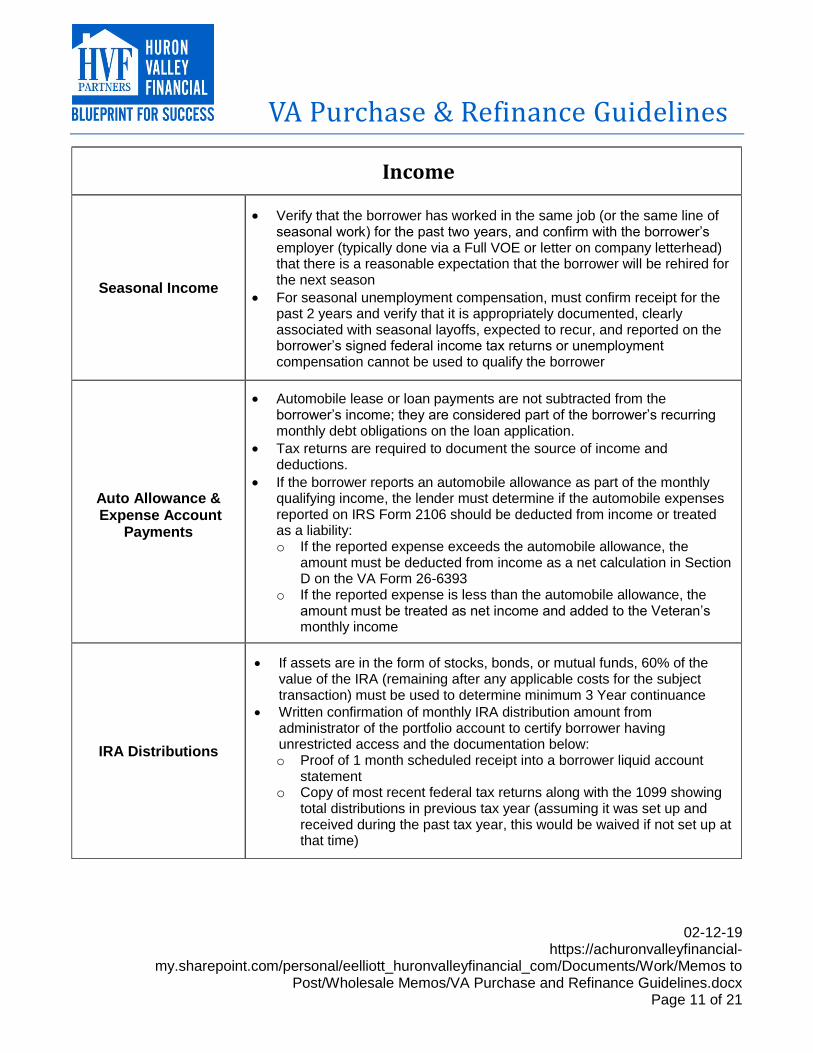

Seasonal Income

• Verify that the borrower has worked in the same job (or the same line of seasonal work) for the past two years, and confirm with the borrower’s employer (typically done via a Full VOE or letter on company letterhead) that there is a reasonable expectation that the borrower will be rehired for the next season

• For seasonal unemployment compensation, must confirm receipt for the past 2 years and verify that it is appropriately documented, clearly associated with seasonal layoffs, expected to recur, and reported on the borrower’s signed federal income tax returns or unemployment compensation cannot be used to qualify the borrower

Auto Allowance & Expense Account

Payments

• Automobile lease or loan payments are not subtracted from the borrower’s income; they are considered part of the borrower’s recurring monthly debt obligations on the loan application.

• Tax returns are required to document the source of income and deductions.

• If the borrower reports an automobile allowance as part of the monthly qualifying income, the lender must determine if the automobile expenses reported on IRS Form 2106 should be deducted from income or treated as a liability: o If the reported expense exceeds the automobile allowance, the

amount must be deducted from income as a net calculation in Section D on the VA Form 26-6393

o If the reported expense is less than the automobile allowance, the amount must be treated as net income and added to the Veteran’s monthly income

IRA Distributions

• If assets are in the form of stocks, bonds, or mutual funds, 60% of the value of the IRA (remaining after any applicable costs for the subject transaction) must be used to determine minimum 3 Year continuance

• Written confirmation of monthly IRA distribution amount from administrator of the portfolio account to certify borrower having unrestricted access and the documentation below: o Proof of 1 month scheduled receipt into a borrower liquid account

statement o Copy of most recent federal tax returns along with the 1099 showing

total distributions in previous tax year (assuming it was set up and received during the past tax year, this would be waived if not set up at that time)

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 12 of 21

Non-Taxable Income Income verified as non-taxable income may be grossed up by 25%. The grossed-up portion may not be used to calculate the residual income requirements.

Income

Declining Income Trending

If the trend is declining, the income may not be stable. Additional analysis must be conducted to determine if able to continue and what qualifying income average can be used. For self-employed borrowers, an unaudited YTD profit & loss will be required to show if the trending was declining further from the most recent tax return years average, if it was then no income will be used to qualify from this activity (as its stability and continuance at a given level was unable to be evidenced). Any increase in income shown on the P&L statement when compared to most recent tax returns cannot be used to qualify and only the most recent tax returns average would be able to be used in this case.

Rental Income

2 – 4 Unit Purchase: • Fully executed lease from the non-occupied units

• 75% of lease amounts or the appraiser’s opinion of fair market rents can be used as income

• If this is a negative result, must be counted as a liability

• If rental income is not needed to qualify, reserves and landlord experience are not necessary

• 6 months reserves

• Previous landlord experience

• Occupancy for veteran must be established

Retaining Current Residence:

• Letter of explanation/motivation letter from borrower

• Occupancy must be established

SFR/Rental income requires lease and evidence of security deposit, may use 75% of lease to offset current mortgage payment, any negative cash flow will be considered as a liability

Tax Transcripts • When tax returns are required to validate income, 2 years 1040

transcripts must be obtained from an acceptable vendor.

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 13 of 21

Verbal Verification of Employment

• Is required on all loans within 10 business days from the Note date (or funding date for escrow states) for wage income and verification of the existence of the borrower’s business through a 3rd party source is required within 30 calendar days for self-employment income.

• When using 3rd party services such as the work number the request date must be within 10 business days of the note date and the data reported up to date they provide must be within 30 calendar days of the noted date.

Credit

Minimum Trade Lines

• A tri-merged credit report with a minimum of 1 generated credit score and

AUS approval

• Manual underwriting trade line requirement: 3 trade lines and 12 Month

reporting history. A rental history is required. Less than 12 Months

reporting history or lack of rental history will require non-traditional credit

and will be reviewed on a case by case basis

• Authorized user accounts are not considered a valid trade line

Mortgage History • 0 x 30 on mortgage in the past 12 months

• For cash out, must be current through month of closing

Modified or Restructured

Mortgage

• For refinances of a current restructured or modified mortgage, there must have been 24 months of consecutive on time payments made to it to be eligible

• Balance forgiveness is not allowed for cash out refinance

Bankruptcy

• 2 years from discharge or dismissal date for Chapter 7

• 1 year from filing date for Chapter 13 subject to the following:

o Borrower has made 12 scheduled payments into the repayment plan o Documentation to support the payment amount and that all payments

have been made on time o Court permission to enter into the mortgage o Loan must accompany a satisfactory explanation

Foreclosure or Deed-in-Lieu

• 2 years from the completion date of the foreclosure or deed-in-lieu action

• If a foreclosure, deed in lieu, or short sale process is in conjunction with a bankruptcy, use the latest date of either the discharge of the bankruptcy or transfer of title for the home to establish the beginning date of re-established credit

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 14 of 21

Judgements, Collections,

& Charge Offs

• All judgments and federal debts must be paid in full unless a satisfactory payment arrangement is in place and 12 scheduled have been made on time and the debt will be subordinate to mortgage lien

• Collections and charge-off accounts require an explanation, third party documentation, and underwriter discretion to omit from being paid off

Short Sale &

Pre-Foreclosure

• Develop complete information on the facts and circumstances if the borrower(s) voluntarily surrendered the property

• If the borrower’s payment history before the short sale or DIL was satisfactory, a waiting period from the date of transfer of the property may not be necessary

• If the foreclosure, DL, or short sale was on a VA loan, a borrower may not have full entitlement

Disputed Trade Lines • Reviewed on a case by case basis

Refreshed Credit (LRR)

Not Required

Cash Back at Closing For purchase only up to the documented earnest money deposit paid with documentation to support clearing borrower’s account

Compensating Factors

• Excellent long-term credit

• Conservative use of consumer credit

• Minimal consumer debt

• Significant assets or down payment

• High residual income

• Long term employment

• No payment shock

Assets

Asset Verification

Two consecutive monthly account statements (or acceptable print screen history with all required elements present including URL) are required to document the borrower’s assets. Account statements most recent history must be within 30 days of application. Quarterly account statements dated greater than 30 days outside of application date, but less than 90 days are acceptable with verification that the funds are still available.

Interested Party

Contributions

The maximum allowable contributions that interested parties may make for a VA loans is 4% lesser of the property’s sales price or appraised value. This does not include lender paid closing costs on veteran’s behalf.

Reserves 6 months reserves required on 2-4 Unit properties when using rental income to qualify

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 15 of 21

Financing Contributions

&

Sales Concessions

• Financing contributions are allowed and typically paid by seller for borrower closing and pre-paid costs. Other eligible costs include: origination fees, discount fees, appraisal, stamps, attorney fees, real estate tax service fees, HOA fees for up to 12 months

• Sales concessions are NOT allowed and the value of them must be deducted from the sales price when calculating LTV and CLTV ratios. These non-realty items include giveaways and inducements to purchase in the form of furniture, cash, autos, vacations, moving costs paid for, repair allowances, etc

In instances where personal property items (also known as chattel) are included in the purchase contract (examples include bar stools, pool tables, hot tubs, furniture, lawn mower, etc.), provide a fully executed purchase agreement addendum reflecting the specific personal property/chattel listed in the PA as being removed from the purchase transaction

Assets

Large Deposits

When bank statements are used, the lender must evaluate any non-payroll deposits. Documentation is required to paper trail/source any non-payroll deposits. to be certain the Veteran did not take out a loan resulting in the large deposit

Sale of Personal Assets

Proceeds received from a sale of personal assets are an acceptable source of funds for the down payment, closing costs, and reserves as long as the individual purchasing the asset is not a party to either the property sale transaction or the mortgage financing transaction. When the borrower relies on the sale of personal assets as a source of funds, documentation must be obtained to evidence:

• The ownership of the asset - title copy if applicable or other documentation

• The value of the asset - as determined by an independent source

• The transfer of ownership of the asset with its sale - such as a bill of sale or a statement from the purchaser

• The receipt of the proceeds of the sale - such as a deposit slip, bank statement, and copy of the purchaser’s check

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 16 of 21

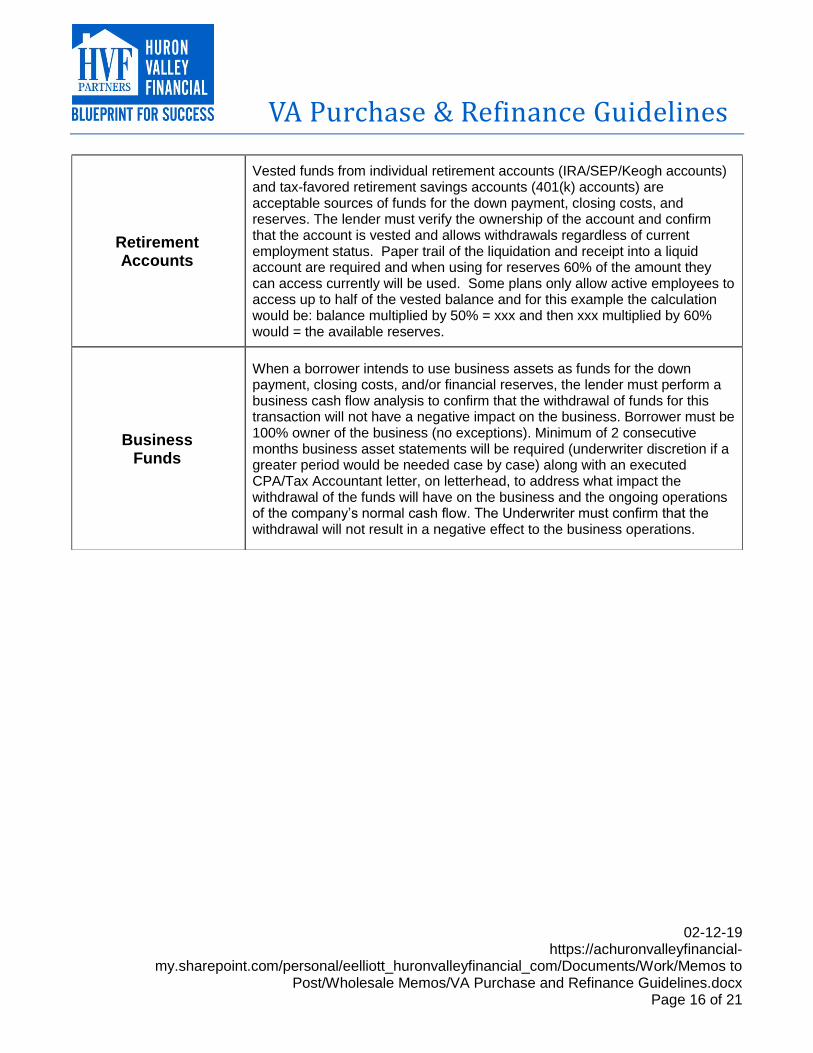

Retirement Accounts

Vested funds from individual retirement accounts (IRA/SEP/Keogh accounts) and tax-favored retirement savings accounts (401(k) accounts) are acceptable sources of funds for the down payment, closing costs, and reserves. The lender must verify the ownership of the account and confirm that the account is vested and allows withdrawals regardless of current employment status. Paper trail of the liquidation and receipt into a liquid account are required and when using for reserves 60% of the amount they can access currently will be used. Some plans only allow active employees to access up to half of the vested balance and for this example the calculation would be: balance multiplied by 50% = xxx and then xxx multiplied by 60% would = the available reserves.

Business Funds

When a borrower intends to use business assets as funds for the down payment, closing costs, and/or financial reserves, the lender must perform a business cash flow analysis to confirm that the withdrawal of funds for this transaction will not have a negative impact on the business. Borrower must be 100% owner of the business (no exceptions). Minimum of 2 consecutive months business asset statements will be required (underwriter discretion if a greater period would be needed case by case) along with an executed CPA/Tax Accountant letter, on letterhead, to address what impact the withdrawal of the funds will have on the business and the ongoing operations of the company’s normal cash flow. The Underwriter must confirm that the withdrawal will not result in a negative effect to the business operations.

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 17 of 21

Gifts

Gift funds may fund all or part of the down payment, closing costs, or financial reserves subject to the minimum borrower contribution requirements.

• A gift can be provided by: o Relative, defined as the borrower’s spouse, child or other dependent or

by any other individual who is related to the borrower by blood, marriage, adoption or legal guardianship

o Fiancé, fiancée or domestic partner *Domestic Partner: An unrelated individual who shares a committed relationship with the primary wage earner, currently resides in the same household as the primary wage earner and intents to occupy the security property with the primary wage earner.

o Gift donor may not have any affiliation with builder, developer, realtor or any other interested party to the transaction

• The gift letter must: o Specify the dollar amount of the gift o Specify the date the funds were transferred o Include the donor’s statement that no repayment is expected o Indicate the donor’s name, address, telephone number and

relationship to the borrower o Identification of the property being purchased

• Fiancé, fiancée or domestic partner gifts has no additional requirements. Verification of donor availability of funds: for personal checks can be either a copy of the donor’s cancelled gift check front and back with bank stamp. Or a front copy along with their monthly bank statement with all pages including or acceptable print screen bank history with URL present covering a minimum 30 days period that shows the money coming out on it. For other types including cashier’s checks, wires, money orders, certified checks, etc. then will need those copies along with either the full monthly statement or print screen assets histories with URL present and indication of institution name, account holder, account number, type of account all present on it and showing the money coming out of it. Cash is not an acceptable source of gifted funds and it cannot be used. HVF Partners does not allow for gifts to be given directly at the closing to the borrower or title/escrow company.

• Gifts of Equity: a “gift of equity” refers to a gift provided by the seller of a property to the buyer. The gift represents a portion of the seller’s equity in the property and is transferred to the buyer as a credit in the transaction. Gift of equity cannot be used to reduce the funding fee requirement.

• Gifts Funds from a Wedding: are acceptable, must document proof of the wedding (copy of the marriage certificate) and that the gift funds were all deposited in a timely fashion (within a couple weeks or so of the wedding and all at once, if there were any that were outliers and deposited even a couple weeks after the majority of the rest were all deposited, those will be excluded from being able to be counted)

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 18 of 21

Stocks, Bonds, &

Mutual Funds

Stocks, government bonds, and mutual funds are acceptable sources of funds for the down payment, closing costs and financial reserves - 100% of their verified value may be used as reserves, documentation of the borrower’s actual receipt of funds realized from the sale or liquidation must be obtained.

Foreign Assets

Foreign assets may be used for down payment and closing costs. The sale of

foreign assets and conversion of foreign currency must be fully documented via:

• Borrower must transfer funds into US bank/deposit account & document receipt

• Foreign documentation to be translated to English for review/approval by UW

• Document the transferred funds leaving the foreign account, evidence they belonged to the borrower(s) prior to transfer and a translated assets history of ownership for a minimum 60-day period

• Documented proof of wire transfer either present on the U.S. banking pages or by an independent third-party translation service company

Underwriter will obtain a currency converter page online as of the date of the wire to either match or closely match up with the conversion that is seen for further authentication

Collateral

Appraisal and Review Requirements

• Appraisal expiration is 180 days

• Appraisal must be ordered through VA’s webLGY system and Appraiser assigned by VA

• Designated SAR Underwriter must review the appraisal and issue the Notice of Value, (NOV) within 5 days of receipt of the appraisal.

• All requirements on the NOV must be documented in the loan file

• Property must meet VA’s minimum property standards of safe, sanitary, and soundness

Appraisal Fee Schedules by State

Appraisal Portability • Appraisals may be transferrable from LAPP Lender to LAPP Lender for the

same Veteran, however, a new Veteran will require a new appraisal

Rental Income

• Single Family Rent Comparable Schedule is not applicable

• Operating Income statement is required on all 2-4 Unit properties

Recert of Value • New appraisal required after 6 months

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 19 of 21

Subsequent Transaction

• Use of an Appraisal from a subsequent transaction is not permitted

Zoning

• Illegal zoning is not allowed. A legal conforming or non-conforming (grandfathered use) are eligible as long as the appraiser, or local township/municipality can confirm that the subject can be rebuilt 100% to its current density if it were to be destroyed without requiring special review/approval in order to rebuild it.

Accessory Apartment or

In-Law Suite

An accessory unit is typically an additional living area independent of the primary dwelling unit and includes a fully functioning kitchen & bathroom. Whether a property is 1-Unit with an accessory unit, or a 2-Unit property will be based on the characteristics of the property, which may include, but are not limited to, the existence of separate utilities, unique postal address, & whether the unit is rented.

• If the accessory unit complies with local zoning, the property is eligible when: o The property is one-unit o The appraisal report demonstrates that the improvements are typical

for the market by providing at least one recent closed comparable sale also containing an accessory unit, and

• Borrower qualifies without considering rental income from the accessory unit

Properties Listed for Sale

• Cash Out: must be off the market 1 day prior to application and appraisal date

• Borrower explanation addressing why the property was recently listed for sale and to confirm their intent to occupy

Inadequate Heat Source

• Properties with non-affixed non-permanent heat sources such as space heaters or fireplaces are not eligible

• Baseboard or affixed wall furnace heating would be eligible provided the appraiser states this is typical for the area, is an adequate heat source and appraiser provides comps with similar heat sources in the local market area

Community Well & Septic

The owner must have a recorded and legally binding agreement for access and maintenance of the community well/septic facilities; said agreement must be ongoing and transfer to future owners; appraiser to provide:

• Note presence of community well/septic facilities

• At least one comparable must have community well/septic facilities

• Address any impact on marketability and make market adjustment if warranted for comparable that do not have community well/septic facilities

• Confirm the party that oversees its maintenance

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 20 of 21

Multiple Parcels

The subject property may consist of more than one parcel if:

• Parcels must be adjoining

• Each parcel must have the same basic zoning

• Only one parcel may have a dwelling unit (limited non-residential improvements such as a garage on the second parcel are acceptable but second parcel must be evidenced to be a non-buildable lot in terms of a full dwelling and evidence must be included in the loan file).

• A home that has been built across lot lines is acceptable, i.e. the home is built across both parcels and the lot line runs under the home

• The mortgage must be a valid first lien on each parcel

• Two separate deeds are not permitted

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 21 of 22

Private Road • Recorded private road maintenance agreement is required

• A permanent recorded easement must be recorded

Maximum Acreage • 25 acres

PIW • Property Inspection Waivers are not applicable

Collateral

Escrow Holdback

Permitted for postponed improvements. Escrow holdback funds will be reviewed and approved by Underwriting. Escrow holdback funds will be held at closing for weather-related items only that do not affect property habitability, are not health or safety related, nor affect ability to obtain occupancy permit.

• All weather-related work must be completed within 180 days of closing

• Two separate contractor bids for the cost of completing the improvements (for

new construction only the builder’s bid/estimate is required) and copies of

each license

• Amount withheld from the purchase proceeds must equal 150% of the higher

of two bids/estimates, however, if the builder offers a guaranteed fixed price

contract for completion, the funds in the completion escrow can be equal to

the full amount of the contract price

• The cost of completing improvements must not represent more than 10% of

the “as completed” appraised value of the property

• 1004D completion appraisal must state improvements were completed in accordance with the requirements and conditions in the original appraisal report and provide accompanying photos and be completed by same appraiser that did original report

• Fully executed escrow holdback agreement is required to be signed at closing

Condominiums

• Attached/detached condominiums must be on VA’s approved Condo list. https://vip.vba.va.gov (not required for detached condos in Michigan)

• VA Condo approval must be supported in the loan file

• PUD/Condo HOA form must be signed by the HOA to support that HOA dues are subordinate to the VA Mortgage

• See HVF Condominium Matrix for information

HOA Dues

PUD/Condo HOA form must be signed by the Home Owners Association representative any time a Home Owners Association is indicated on the appraisal to certify that Home Owners Association dues are subordinate to the VA Mortgage.

VA Purchase & Refinance Guidelines

02-12-19 https://achuronvalleyfinancial-

my.sharepoint.com/personal/eelliott_huronvalleyfinancial_com/Documents/Work/Memos to Post/Wholesale Memos/VA Purchase and Refinance Guidelines.docx

Page 22 of 22

Termite Requirements

• Termite inspection is determined necessary by the VA at the county level

• Termite inspections must be signed by seller/veteran prior to close

• Valid for 90 days

Well Water Quality Test Requirements

• Must meet county water quality requirements and be safe to drink

• When the county does not specify water quality requirements, the water must be tested for Lead, Nitrate, Nitrite, Coliform, and E-coli

• Borrower to acknowledge water test and sign hold harmless agreement

• Valid for 90 days

Compliance / Vendor Requirements

Appraisal Requirements

• Broker and NDC: order appraisal and VA Case Number directly through VAWebLY - select appraisal type: IND (Individual NOV)

• HVF Partners with SAR Underwriter on staff may order appraisal, VA Case Number, and issue NOV

Fraud Detection Tool

Delegated Correspondents to provide an acceptable fraud detection report with all variances cleared. Acceptable vendors are DataVerify and Fraudguard

Flood Certificate Delegated Correspondents to provide life of loan flood certificate from Corelogic

Recommended