1

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

Technology Education Section, Curriculum Development InstituteEducation Bureau, HKSARG

August 2008

Unit 4 : Financial Analysis

Course 1 : Contemporary Perspectives on Accounting

2Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

2

Learning objectives

On completion of this unit, you should be able to:

1. Understand different kinds of financial analysis, including horizontal analysis, vertical analysis, trend analysis and ratio analysis;

2. Calculate commonly used ratios relating to a company’s profitability, liquidity, solvency, management efficiency and return on investment;

3. Interpret and evaluate the ratios; and

4. Explain the limitations of ratios in financial analysis.

3Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

3

Organisation of Unit 4

Financial AnalysisObjectives of ratio analysis

Use of ratios in interpretation of financial statements

Profitability ratios Short-term liquidity and

efficiency ratios

Long-term solvency

ratios

Limitations of ratio analysis

Investment ratios

Percentage analysisLearning Resources

Corner

4Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

4

1. Introduction (1)

One purpose of financial statement analysis is to use the PAST PERFORMANCE of a company to PREDICT its future profitability and cash flows.

Another purpose is to EVALUATE the performance of a company with an eye toward identifying problem areas.

Financial analysis is the examination of both the relationships among financial statement numbers and the trends in those numbers over time.

5Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

5

1. Introduction (2)

Financial statements can be evaluated in different ways. The DuPont Framework (named after a system of ratio analysis developed internally at DUPONT around 1920) provides a systematic approach to identifying general factors causing Return on Equity to deviate from normal.

6Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

6

Major Users (1)

Internal users

• Management

• Employee

How about external users?

7Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

7

Major Users (2)

External users

• Shareholders

• Prospective investors

• Suppliers

• Bankers

• Customers

• Debenture holders

• Inland Revenue

8Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

8

2. Objectives of ratio analysis

Evaluate the current performance Evaluate the current performance and financial position of the and financial position of the companycompany

e.g. profitability, gearing

Make predictionsMake predictions

e.g. profits and dividends prospects

Evaluate the relative Evaluate the relative performance of a company performance of a company

e.g. trend analysis, industry analysis

9Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

9

3. Classification of ratios

Profitability ratios

Short-term liquidity and efficiency ratios

Long-term solvency ratios

Investment ratios

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

4. Profitability ratios

11Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

11

4. Profitability ratios (1)

Management: avoid companies with poor profit and return on investment

Investors: avoid poor earning potential companies

Bankers: avoid lending to companies with low profitability

Profitability ratios are used to assess the company’s performance and its efficiency of operation. These ratios show the relationship between profit and resources employed in the operation.

12Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

12

4. Profitability ratios (2)

The following are the commonly used ratios to assess the effectiveness and efficiency of a company in generating profit:

1) Gross profit ratio (Chick here for detail explanation)

2) Net profit ratio (Chick here for detail explanation)

3) Return on owners’ equity (before tax) (Chick here for detail explanation)

4) Return on capital employed (before tax) (Chick here for detail explanation)

Go back to organisation of unit 45) Assets turnover (Chick here for detail explanation)

13Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

13

4. Profitability ratios (3)

(a) Gross profit ratio (Gross profit margin)

Indicate how much profit is earned out of sales before operating costs

Measure the company’s ability to increase sales price and decrease cost of goods sold

Salesx 100%

Gross profit

Example – Click here Go back to section menu

14Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

14

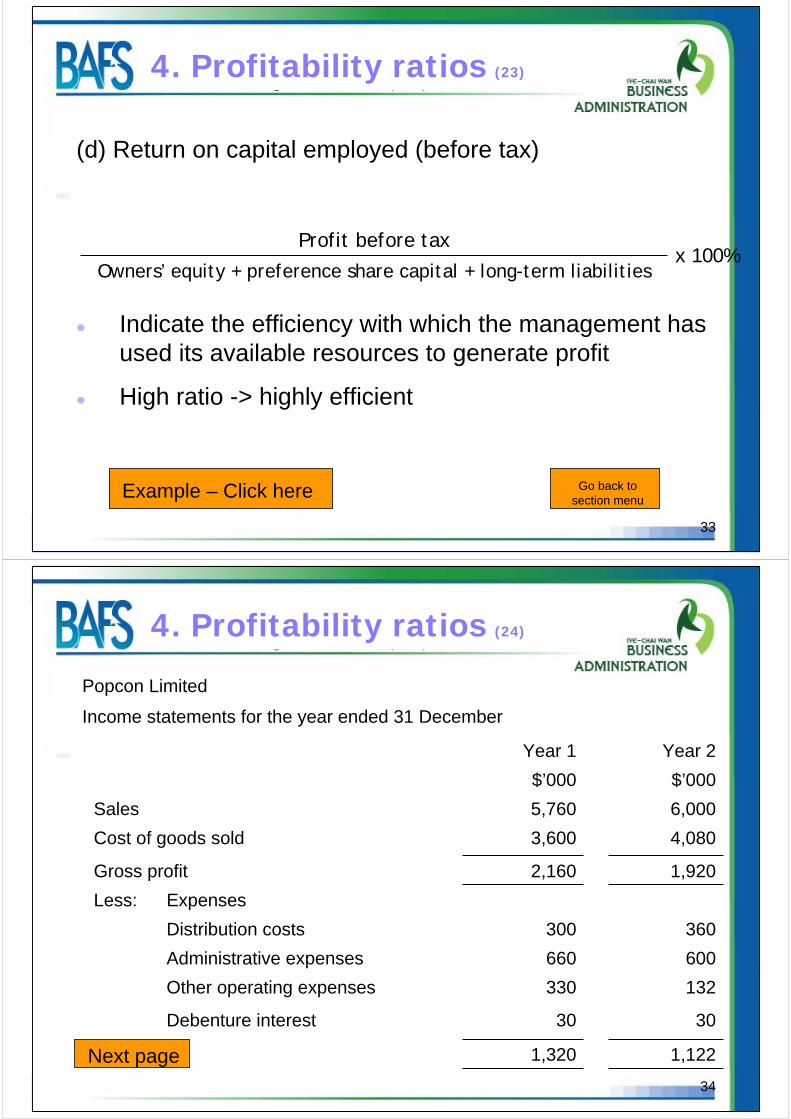

Popcon Limited

Income statements for the year ended 31 December

1,1221,320

132

30

330

30

Other operating expenses

Debenture interest

600660Administrative expenses

360300Distribution costs

ExpensesLess:

1,9202,160Gross profit

4,0803,600Cost of goods sold

6,0005,760Sales

$’000$’000

Year 2Year 1

4. Profitability ratios (4)

Next page

15Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

15

4. Profitability ratios (5)

Click here for some hints Click here for suggested answer

Self-test 1

Now! Try to calculate the Gross profit ratio (Gross profit margin)

16Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

16

4. Profitability ratios (6)

(a) Gross profit ratio (Gross profit margin)

Salesx 100%

Gross profit

Year 2Year 1

= %= %

x 100%x 100%

Go Back to previous page

17Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

17

4. Profitability ratios (7)

(a) Gross profit ratio (Gross profit margin)

Salesx 100%

Gross profit

6,0005,760

Year 2Year 1

= 32.0%= 37.5%

x 100%1,920

x 100%2,160

What’s your comment?

18Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

18

4. Profitability ratios (8)

(a) Gross profit ratio (Gross profit margin)

Salesx 100%

Gross profit

6,0005,760

Year 2Year 1

= 32.0%= 37.5%

x 100%1,920

x 100%2,160

The higher ratio in Year 1 indicates that the company’s ability to increase selling price and reduce cost of goods sold is better in Year 1 than in Year 2. Accordingly, the performance in Year 1 is better than in Year 2.

Next ratio

19Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

19

4. Profitability ratios (9)

(b) Net profit ratio (Net profit margin)

Indicate the profitability generated from sales

Low operating costs -> high ratio

High ratio -> efficient cost control

Generally use profit before tax (PBT)

Use profit before interest and tax (PBIT) -> useful for bankers and lenders

Salesx 100%

Net profit

Example – Click here Go back to section menu

20Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

20

Popcon Limited

Income statements for the year ended 31 December

1,1221,320

132

30

330

30

Other operating expenses

Debenture interest

600660Administrative expenses

360300Distribution costs

ExpensesLess:

1,9202,160Gross profit

4,0803,600Cost of goods sold

6,0005,760Sales

$’000$’000

Year 2Year 1

4. Profitability ratios (10)

Next page

21Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

21

Popcon Limited

Income statements for the year ended 31 December

684720Profit after tax

114120Tax

798840Profit before tax

540576Retained profit for the year

144144Dividend paid

Bal c/f

$’000$’000

Year 2Year 1

4. Profitability ratios (11)

Next page

22Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

22

4. Profitability ratios (12)

Click here for some hints Click here for suggested answer

Self-test 2

Now! Try to calculate the Net profit ratio (before interest and tax)

23Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

23

4. Profitability ratios (13)

(b) Net profit ratio (before interest and tax)

Salesx 100%

Profit before interest and tax

Year 2Year 1

= %= %

X 100%X 100%

Go Back to previous page

24Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

24

4. Profitability ratios (14)

(b) Net profit ratio (before interest and tax)

Salesx 100%

Profit before interest and tax

6,0005,760

Year 2Year 1

= 13.8%= 15.1%

X 100%798 + 30X 100%840 +

30

What’s your comment?

25Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

25

4. Profitability ratios (15)

(b) Net profit ratio (before interest and tax)

Salesx 100%

Profit before interest and tax

6,0005,760

Year 2Year 1

= 13.8%= 15.1%

X 100%798 + 30X 100%840 +

30

The higher the ratio, the better is the company’s performance. Accordingly, the performance in Year 1 is better than in Year 2.

Next ratio

26Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

26

4. Profitability ratios (16)

(c) Return on owners’ equity (before tax)

Measure profit before tax attributable to ordinary shareholders after deduction of any interest payments

High ratio -> good return to owners

Owners’ equity (ordinary share capital + reserves)

x 100%Profit before tax

Example – Click here Go back to section menu

27Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

27

Popcon Limited

Income statements for the year ended 31 December

684720Profit after tax

114120Tax

798840Profit before tax

540576Retained profit for the year

144144Dividend paid

$’000$’000

Year 2Year 1

4. Profitability ratios (17)

Next page

28Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

28

Popcon Limited

Balance sheets as at 31 December

1,5601,020Retained profit

Capital and reserves

120120Ordinary share capital, $1.20 each

1,6801,140

1,6801,140Net assets

30030010% Debentures (Year 6)

Long-term liabilities

$’000$’000

Year 2Year 1

4. Profitability ratios (18)

Next page

29Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

29

4. Profitability ratios (19)

Click here for some hints Click here for suggested answer

Self-test 3

Now! Try to calculate the Return on owners’ equity (before tax)

30Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

30

4. Profitability ratios (20)

(c) Return on owners’ equity (before tax)

Owners’ equity (ordinary share capital + reserves)

x 100%Profit before tax

Year 2Year 1

= %= %

x 100%x 100%

Go Back to previous page

31Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

31

4. Profitability ratios (21)

(c) Return on owners’ equity (before tax)

Owners’ equity (ordinary share capital + reserves)

x 100%Profit before tax

1,6801,140

Year 2Year 1

= 47.5%= 73.7%

x 100%798

x 100%840

What’s your comment?

32Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

32

4. Profitability ratios (22)

(c) Return on owners’ equity (before tax)

Owners’ equity (ordinary share capital + reserves)

x 100%Profit before tax

1,6801,140

Year 2Year 1

= 47.5%= 73.7%

x 100%798

x 100%840

The higher the ratio, the better is the company’s performance. Accordingly, the performance in Year 1 is better than in Year 2.

Next ratio

33Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

33

4. Profitability ratios (23)

(d) Return on capital employed (before tax)

Indicate the efficiency with which the management has used its available resources to generate profit

High ratio -> highly efficient

Owners’ equity + preference share capital + long-term liabilitiesx 100%

Profit before tax

Example – Click here Go back to section menu

34Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

34

Popcon Limited

Income statements for the year ended 31 December

1,1221,320

132

30

330

30

Other operating expenses

Debenture interest

600660Administrative expenses

360300Distribution costs

ExpensesLess:

1,9202,160Gross profit

4,0803,600Cost of goods sold

6,0005,760Sales

$’000$’000

Year 2Year 1

4. Profitability ratios (24)

Next page

35Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

35

Popcon Limited

Income statements for the year ended 31 December

684720Profit after tax

114120Tax

798840Profit before tax

540576Retained profit for the year

144144Dividend paid

$’000$’000

Year 2Year 1

4. Profitability ratios (24)

Next page

36Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

36

Popcon Limited

Balance sheets as at 31 December

1,5601,020Retained profit

Capital and reserves

120120Ordinary share capital, $1.20 each

1,6801,140

1,6801,140Net assets

30030010% Debentures (Year 6)

Long-term liabilities

$’000$’000

Year 2Year 1

4. Profitability ratios (25)

Next page

37Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

37

4. Profitability ratios (26)

Click here for some hints Click here for suggested answer

Self-test 4

Now! Try to calculate the Return on capital employed (before tax)

38Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

38

4. Profitability ratios (27)

(d) Return on capital employed (before tax)

Year 2Year 1

= %= %

x 100%x 100%

Owners’ equity + preference share capital + long-term liabilitiesx 100%

Profit before tax

Go Back to previous page

39Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

39

4. Profitability ratios (28)

(d) Return on capital employed (before tax)

300 + 1,680300 + 1,140

Year 2Year 1

= 40.3%= 58.3%

x 100%798

x 100%840

Owners’ equity + preference share capital + long-term liabilitiesx 100%

Profit before tax

What’s your comment?

40Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

40

4. Profitability ratios (29)

(d) Return on capital employed (before tax)

300 + 1,680300 + 1,140

Year 2Year 1

= 40.3%= 58.3%

x 100%798

x 100%840

Owners’ equity + preference share capital + long-term liabilitiesx 100%

Profit before tax

The higher the ratio, the better is the company’s performance. Accordingly, the performance in Year 1 is better than in Year 2.

Next ratio

41Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

41

4. Profitability ratios (30)

(e) Assets turnover

Measure a company’s ability to efficiently utilise its assets in generating sales

High ratio -> highly efficient

Total assets less current liabilities

Sales

Example – Click here Go back to section menu

42Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

42

Popcon Limited

Income statements for the year ended 31 December

1,1221,320

132

30

330

30

Other operating expenses

Debenture interest

600660Administrative expenses

360300Distribution costs

ExpensesLess:

1,9202,160Gross profit

4,0803,600Cost of goods sold

6,0005,760Sales

$’000$’000

Year 2Year 1

4. Profitability ratios (31)

Next page

43Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

43

Popcon Limited

Balance sheets as at 31 December

2,0401,620Current assets

540360Non-current assets

1,4401,080Net current assets

1,9801,440Total assets less current liabilities

600540Current liabilities

$’000$’000

Year 2Year 1

4. Profitability ratios (32)

Next page

44Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

44

4. Profitability ratios (33)

Click here for some hints Click here for suggested answer

Self-test 5

Now! Try to calculate the Assets turnover

45Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

45

4. Profitability ratios (34)

(e) Assets turnover

Year 2Year 1

= =

Total assets less current liabilities

Sales

Go Back to previous page

46Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

46

4. Profitability ratios (35)

(e) Assets turnover

1,9801,440

Year 2Year 1

= 3.0 times= 4.0 times

6,0005,760

Total assets less current liabilities

Sales

What’s your comment?

47Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

47

4. Profitability ratios (36)

(e) Assets turnover

1,9801,440

Year 2Year 1

= 3.0 times= 4.0 times

6,0005,760

Total assets less current liabilities

Sales

The higher the ratio, the better is the company’s performance. Accordingly, the performance in Year 1 is better than in Year 2.

Next section

48Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

48

In this section,

Profit may be measured either by Profit before interest and tax and Profit before tax.

Profit before tax is used generally as the numerator in calculating Return on owners’ equity and Return on capital employed.

In calculating profitability ratios, it is suggested that Profit after tax may also be used.

Have you thought about why Profit before interest and taxor Profit before tax is used as the numerator in our calculations?

4. Profitability ratios (37)

49Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

49

Profit before interest and tax is the amount of profit which the company earned before having to pay interest to the providers of loan capital and other long-term liabilities. This profit figure is of particular importance to the bankers and lenders.

4. Profitability ratios (38)

50Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

50

Profit after tax measures a company’s final return. However, there are often unusual variations in the tax charge (e.g. due to tax planning, loss brought forward) from year to year which would distort the underlying profit figure. Hence, Profit before tax may be considered as a better measure of the profitability of a company’s operations.

4. Profitability ratios (39)

Go back to section menu

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

5. Short-term liquidity ratios

52Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

52

5. Short-term liquidity ratios (1)

Liquid assets include:

1. Cash;

2. Short-term investments;

3. Current deposits with a bank;

4. Accounts receivable; and

5. Bills of exchange receivable.

A company must have sufficient liquid assets to meet its debts when they fall due. Short-term liquidity ratios are used to assess the amount of cash a company can put its hands on quickly to settle its debts.

53Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

53

5. Short-term liquidity ratios (2)

The following are the commonly used ratios to assess the short-term liquidity of a company:

a) Current ratio (Chick here for detail explanation)

b) Liquid ratio (Chick here for detail explanation)

c) Inventory turnover (Chick here for detail explanation)

d) Accounts receivable turnover (Chick here for detail explanation)

e) Accounts payable turnover (Chick here for detail explanation)

Go back to organisation of unit 4

54Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

54

5. Short-term liquidity ratios (3)

(a) Current ratio (Working capital ratio)

Measure a company’s ability to meet its current liabilities out of current assets

Low ratio - indicates that the company may not be able to pay off bills as rapidly as it should

High ratio – indicates the money that could be working for the business is tied up in cash saving or other safe funds and has not being utilised

Generally accepted standard: “rule of thumb” – Current assets are about twice of current liabilities, or ratio of 2:1

However, depend on type of business

Be careful about the component of current assets

Current liabilities

Current assets

Example – Click here Go back to section menu

55Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

55

Popcon Limited

Balance sheets as at 31 December

540360Property, plant and equipment

2,0401,620

300540Bank balances and cash

1,200720Trade and other receivables

540360Inventory

Current assets

Non-current assets

Assets

$’000$’000

Year 2Year 1

5. Short-term liquidity ratios (4)

Next page

56Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

56

Popcon Limited

Balance sheets as at 31 December

1,9801,440

Total assets less current liabilities

1,4401,080Net current assets

600540

114120Current tax payable

486420Trade and other payables

Current liabilities

$’000$’000

Year 2Year 1

5. Short-term liquidity ratios (5)

Next page

57Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

57

5. Short-term liquidity ratios (6)

Click here for some hints Click here for suggested answer

Self-test 6

Now! Try to calculate the Current ratio

58Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

58

5. Short-term liquidity ratios (7)

(a) Current ratio

Year 2Year 1

= =

Current liabilities

Current assets

Go Back to previous page

59Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

59

5. Short-term liquidity ratios (8)

(a) Current ratio

600540

Year 2Year 1

= 3.4= 3.0

2,0401,620

Current liabilities

Current assets

What’s your comment?

60Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

60

5. Short-term liquidity ratios (9)

(a) Current ratio

600540

Year 2Year 1

= 3.4= 3.0

2,0401,620

Current liabilities

Current assets

The company’s current assets are adequate to cover the commitments to settle its current liabilities.

However, the ratios for the two years were well above the rule of thumb (1.5-2). It might not be good for the company as a whole.

Next ratio

61Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

61

5. Short-term liquidity ratios (10)

(b) Liquid ratio (Quick assets ratio or acid test ratio)

Indicate a company’s ability to meet its immediate commitments

Rule of thumb - 1:1

Again, depend on the type of business

Poor ratio -> a sign of approaching insolvency

Current liabilities

Current assets less inventory

Example – Click here Go back to section menu

62Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

62

Popcon Limited

Balance sheets as at 31 December

540360Property, plant and equipment

2,0401,620

300540Bank balances and cash

1,200720Trade and other receivables

540360Inventory

Current assets

Non-current assets

Assets

$’000$’000

Year 2Year 1

5. Short-term liquidity ratios (11)

Next page

63Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

63

Popcon Limited

Balance sheets as at 31 December

1,9801,440Total assets less current liabilities

1,4401,080Net current assets

600540

114120Current tax payable

486420Trade and other payables

Current liabilities

$’000$’000

Year 2Year 1

5. Short-term liquidity ratios (12)

Next page

64Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

64

5. Short-term liquidity ratios (13)

Click here for some hints Click here for suggested answer

Self-test 7

Now! Try to calculate the Liquid ratio (also named as quick assets ratio or acid test ratio)

65Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

65

5. Short-term liquidity ratios (14)

(b) Liquid ratio (Quick assets ratio or acid test ratio)

Year 2Year 1

= =

Current liabilities

Current assets less inventory

Go Back to previous page

66Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

66

5. Short-term liquidity ratios (15)

(b) Liquid ratio (Quick assets ratio or acid test ratio)

600540

Year 2Year 1

= 2.5=2.3

2,040 - 5401,620 - 360

Current liabilities

Current assets less inventory

What’s your comment?

67Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

67

5. Short-term liquidity ratios (16)

(b) Liquid ratio (Quick assets ratio or acid test ratio)

600540

Year 2Year 1

= 2.5=2.3

2,040 - 5401,620 - 360

Current liabilities

Current assets less inventory

The ratios for the two years were well above the rule-of-thumb. The company has sufficient liquid resources to meet its immediate liabilities.

Next ratio

68Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

68

5. Short-term liquidity ratios (17)

(c) Inventory turnover (inventory holding period)

Average inventory= ? times OR

Cost of goods sold

Cost of goods soldx 365 days

Average inventory

Inventory turnover measures how many times inventories have beenturned over (into cost of goods sold).

Inventory holding period indicates the average number of days that the average inventories are held for. A longer inventory turnover period from one year to the next indicates either a slow down intrading or the inventory level is becoming higher.

Example – Click here Go back to section menu

69Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

69

Popcon Limited

Balance sheets as at 31 December

540360Property, plant and equipment

2,0401,620

300540Bank balances and cash

1,200720Trade and other receivables

540360Inventory

Current assets

Non-current assets

Assets

$’000$’000

Year 2Year 1

5. Short-term liquidity ratios (18)

Next page

70Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

70

Popcon Limited

Income statements for the year ended 31 December

1,1221,320

132

30

330

30

Other operating expenses

Debenture interest

600660Administrative expenses

360300Distribution costs

ExpensesLess:

1,9202,160Gross profit

4,0803,600Cost of goods sold

6,0005,760Sales

$’000$’000

Year 2Year 1

5. Short-term liquidity ratios (19)

Next page

71Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

71

5. Short-term liquidity ratios (20)

Click here for some hints Click here for suggested answer

Self-test 8

Now! Try to calculate the Inventory holding period

72Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

72

5. Short-term liquidity ratios (21)

(c) Inventory holding period

Year 2Year 1

= days= days

x daysx days

Cost of goods soldx 365 days

Average inventory *

Go Back to previous page

* In this case, we assume that the closing inventory is equal to average inventory

73Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

73

5. Short-term liquidity ratios (22)

(c) Inventory holding period

4,0803,600

Year 2Year 1

= 48.3 days= 36.5 days

x 365 days540

x 365 days360

Cost of goods soldx 365 days

Average inventory

What’s your comment?

74Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

74

5. Short-term liquidity ratios (23)

(c) Inventory holding period

4,0803,600

Year 2Year 1

= 48.3 days= 36.5 days

x 365 days540

x 365 days360

Cost of goods soldx 365 days

Average inventory

Year 2 has longer inventory holding period than Year 1. It indicates either a slow down in trading or higher inventory level. Next ratio

75Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

75

5. Short-term liquidity ratios (24)

Indicate the average time to collect accounts receivable

The trend of the collection period over time is probably the best guide. If accounts receivable days are increasing year-by-year, it indicates the company’s poor management on the credit control function.

Credit salesx 365 days

Accounts receivable

(d) Accounts receivable turnover (in days)

Next ratio

76Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

76

5. Short-term liquidity ratios (25)

Indicate the average time to pay the suppliers

This ratio shows the average credit period allowed to the company by the suppliers. The longer the period is, the better to the company.

Credit purchasesx 365 days

Accounts payable

(e) Accounts payable turnover (in days)

Next ratio

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

6. Long-term solvency ratios

78Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

78

6. Long-term solvency ratios (1)

Long-term solvency ratios are concerned with how much the company owes, whether it is getting into heavier debts or improving its situation, and whether its debts burden seems heavy or light.

For example: If a company has heavy debts burden, high interest charges will reduce profit available to shareholders and make it potentially vulnerable if interest rates go up.

79Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

79

6. Long-term solvency ratios (2)

The following are the commonly used ratios to assess the long-term solvency of a company:

a) Gearing ratio (Chick here for detail explanation)

b) Interest cover (Chick here for detail explanation)

c) Debt to equity ratio (Chick here for detail explanation)

Go back to organisation of unit 4

80Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

80

6. Long-term solvency ratios (3)

(a) Gearing

Gearing -> long-term capital structure

Acceptable level of gearing is about 30% to 35%

High gearing ratio -> high financial risk

Owners’ equity + preference share capital + long-term liabilities

(long-term liabilities + preference share capital) x 100%

Example – Click here Go back to section menu

81Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

81

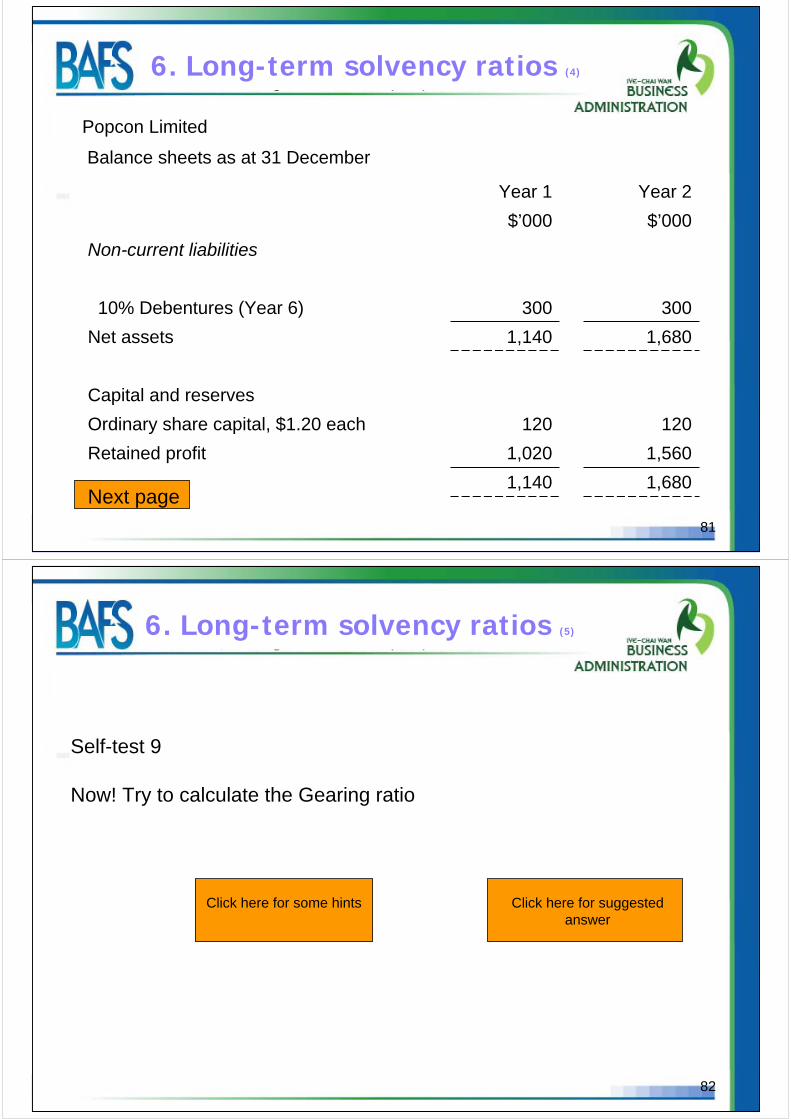

Popcon Limited

Balance sheets as at 31 December

1,5601,020Retained profit

Capital and reserves

120120Ordinary share capital, $1.20 each

1,6801,140

1,6801,140Net assets

30030010% Debentures (Year 6)

Non-current liabilities

$’000$’000

Year 2Year 1

6. Long-term solvency ratios (4)

Next page

82Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

82

6. Long-term solvency ratios (5)

Click here for some hints Click here for suggested answer

Self-test 9

Now! Try to calculate the Gearing ratio

83Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

83

6. Long-term solvency ratios (6)

(a) Gearing ratio

Owners’ equity + preference share capital + long-term liabilities

x 100%

Long-term liabilities + preference share capital

(owners’ equity + debentures)

Year 2Year 1

= %= %

x 100%X100%(debentures)

Go Back to previous page

84Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

84

6. Long-term solvency ratios (7)

(a) Gearing ratio

Owners’ equity + preference share capital + long-term liabilities

x 100%

Long-term liabilities + preference share capital

1,9801,440 (owners’ equity + debentures)

Year 2Year 1

= 15.2%= 20.8%

x 100%300

x 100%300 (debentures)

What’s your comment?

85Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

85

6. Long-term solvency ratios (8)

(a) Gearing ratio

1,9801,440 (owners’ equity + debentures)

Year 2Year 1

= 15.2%= 20.8%

x 100%300

x 100%300 (debentures)

Next ratio

The gearing ratio in Year 2 is lower than in Year 1. The lower risk to the ordinary shareholders will strengthen the company’s ability to survive in times of poor business.

86Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

86

6. Long-term solvency ratios (9)

Interest

Profit before interest and tax

Interest cover shows whether a company is earning enough profit to pay interest cost comfortably. It also shows possible effects on profit available for ordinary shareholders in the event of a fall in profit before interest and tax.

The higher the interest cover ratio, the lower will be the financial risk of the company.Note: The example for calculating interest cover is included in the Learning Resources Centre.

(b) Interest cover

Next ratio

87Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

87

6. Long-term solvency ratios (10)

(c) Debt to equity ratio

Owners’ equityx 100%

Total debts

(Long-term liabilities + current liabilities)

1) Indicate the proportion of the total debts to owners’ equity2) Rule of thumb - 50% as a safe limit.

Next ratioNote: The example for calculating debt to equity ratio is included in the Learning

Resources Centre

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

7. Investment ratios

89Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

89

7. Investment ratios (1)

Investment ratios help investors and analysts to assess the value and quality of an investment in the ordinary shares of a company.

It is important for investors and financial managers who are interested in the market price of the shares quoted on the stock exchange

90Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

90

7. Investment ratios (2)

The following are the commonly used investment ratios:

a) Earnings per share (EPS) (Chick here for detail explanation)

b) Dividend cover (Chick here for detail explanation)

c) Dividend yield (Chick here for detail explanation)

d) Price earnings (P/E) ratio (Chick here for detail explanation)

Go back to organisation of unit 4

91Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

91

7. Investment ratios (3)

(a) Earnings per share

Numerator: profit attributable to ordinary shareholders

Denominator: reflect the amount of shareholders’ capital that may have varied during the period as a result of a larger or lesser number of shares outstanding at any time

A traditional performance measure

EPS- -> good news

Weighted average number of ordinary shares outstanding

Profit after tax – preference dividends

Example – Click here Go back to section menu

92Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

92

Popcon Limited

Income statements for the year ended 31 December

684720Profit after tax

114120Tax

798840Profit before tax

540576Retained profit for the year

144144Dividend paid

$’000$’000

Year 2Year 1

7. Investment ratios (4)

Next page

93Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

93

Popcon Limited

Balance sheets as at 31 December

1,5601,020Retained profit

Capital and reserves

120120Ordinary share capital, $1.20 each

1,6801,140

1,6801,140Net assets

30030010% Debentures (Year 6)

Non-current liabilities

$’000$’000

Year 2Year 1

7. Investment ratios (5)

Next page

94Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

94

7. Investment ratios (6)

Click here for some hints Click here for suggested answer

Self-test 10

Now! Try to calculate the Earnings per share (EPS)

95Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

95

7. Investment ratios (7)

(a) Earnings per share (EPS)

Weighted average number of ordinary shares outstanding

Profit after tax – preference dividends

Year 2Year 1

= = Go Back to previous page

96Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

96

7. Investment ratios (8)

(a) Earnings per share (EPS)

Weighted average number of ordinary shares outstanding

Profit after tax – preference dividends

*100*100

Year 2Year 1

= $6.8= $7.2

$684$720

* Number of ordinary shares = $120 / $1.2 = 100

The company’s EPS in Year 1 is better than in Year 2.

Next ratio

97Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

97

7. Investment ratios (9)

(b) Dividend cover

Indicate the number of times which the ordinary dividends are covered by profit

High dividend cover

retain high profit for investment

may signal earnings growth in the futureNote: The example for calculating dividend cover is included in the Learning Resources Centre.

Ordinary dividends

Profit after tax – preference dividends

Next ratio

98Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

98

7. Investment ratios (10)

(c) Dividend yield

Market price per shareX 100%

Ordinary dividend per share

Example – Click here Go back to section menu

Dividend yield is the rate of return a shareholder is expecting on an investment in ordinary shares

Shareholders expect high dividend yield and capital growth. Dividend yield is an important indicator of a share’s performance

99Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

99

Popcon Limited

Income statements for the year ended 31 December

684720Profit after tax

114120Tax

798840Profit before tax

540576Retained profit for the year

144144Dividend paid

$’000$’000

Year 2Year 1

7. Investment ratios (11)

Next page

100Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

100

Popcon Limited

Balance sheets as at 31 December

$20$21.6Market price per share

1,5601,020Retained profit

Capital and reserves

120120Ordinary share capital, $1.20 each

1,6801,140

1,6801,140Net assets

30030010% Debentures (Year 6)

Non-current liabilities

$’000$’000

Year 2Year 1

7. Investment ratios (12)

Next page

101Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

101

7. Investment ratios (13)

Click here for some hints Click here for suggested answer

Self-test 11

Now! Try to calculate the Dividend yield

102Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

102

7. Investment ratios (14)

(c) Dividend yield

Market price per shareX 100%

Ordinary dividends per share

Year 2Year 1

==

x 100%x 100%

Go Back to previous page

103Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

103

7. Investment ratios (15)

(c) Dividend yield

Market price per shareX 100%

Ordinary dividends per share

$20$21.6

Year 2Year 1

= 7.2%= 6.7%

x 100%$144/100

x 100%$144/100

What’s your comment?

104Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

104

7. Investment ratios (16)

(c) Dividend yield

Market price per shareX 100%

Ordinary dividends per share

$20$21.6

Year 2Year 1

= 7.2%= 6.7%

x 100%$144/100

x 100%$144/100

Next ratio

In Year 2, the rate of return to shareholders is higher than in Year 1.

105Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

105

7. Investment ratios (17)

(d) Price earnings (P/E) ratio

Indicate the number of years required to earn the price paid for the shares out of profit at the current rate

Reflect the market’s appraisal of the share’s future prospects

Need to compare with the industry P/E ratio

Earnings per share

Current market price per share

106Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

106

7. Investment ratios (18)

(d) Price earnings (P/E) ratio

High P/E ratio may indicate:

1. The investors expect the company’s earnings to increase faster than the others

2. The investors expect the company to be a less risky company

3. The company operates in a more secure industry

In general, P/E ratio around 18 is considered reasonable for a large and established company.

Go back to organisation of unit 4

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

8. Limitations of ratio analysis

108Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

108

8. Limitations of ratio analysis (1)

Some people said that ratio analysis is often difficult to be applied. Why? (Click here for answer)

l Any limitations on ratio analysis?

109Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

109

8. Limitations of ratio analysis (2)

Limitations of financial statements:

Historical cost figures

Seasonal businesses

Accounting policies may be different among companies

For large companies, difficult to categorise into industry segments to allow cross-sectional comparison

Industry averages are not necessarily useful

Go back to organisation of unit 4

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

9. Percentage Analysis

111Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

111

9. Percentage analysis (1)

Horizontal analysis

A trend of changes over years

% change / base-year amount

Useful to determine:

Cause of the change

Whether the change is favourable or unfavourable

Whether any trends are expected to continue

Whether the change affects other related items in the financial statements

112Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

112

9. Percentage analysis (2)

Vertical analysis

Provide evidence of structural changes

Balance sheet: individual components are stated as a % of total assets or total liabilities and shareholders’equity

Income statement: each item is expressed as a % of sales

Useful for comparing companies of different sizes

113Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

113

9. Percentage analysis (4)

Trend analysis

Used to compare the financial data for three or more years

Used to assess a company’s growth

The earliest period is the base year

Base year: 100%

114Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

114

End of the Unit

This is the end of Unit 4. This is the end of Unit 4. Please go to the Unit Please go to the Unit Assessment before Assessment before attempting the next unit.attempting the next unit.

EndEnd--ofof--unit Assessmentunit Assessment

115Unit 4Department of Business Administration

Professional Development Programme (BAFS)Hong Kong Institute of Vocational Education (Chai Wan)

115

Unit 4 Financial Analysis

If you would like to:

(a) go through a comprehensive case on financial analysis,

(b) know more about an integrated analysis of ratios,

please go to the Learning Resources Corner.

Recommended