UNICREDIT CORPORATE DIVISION: GROWTH OPPORTUNITIES AND RISK CONTROL FRAMEWORK

Verona, July 15th, 2004

2

Pietro Modiano – Head of Corporate Division

UCI Corporate Division identity card

UBI’s highlights

Corporate lending scenario

UBI’s strategy and its ‘pact for growth’

Francesco Giordano – Head of UBI Planning, Research and Strategy

Focus on Credit Quality

Ferdinando Samaria – UBM Chief Financial Officer

Focus on Revenue Diversification and Financial Risk Management

AGENDA

3

UCI Corporate Division identity card

UBI’s highlights

Corporate lending scenario

UBI’s strategy and its ‘pact for growth’

AGENDA

4

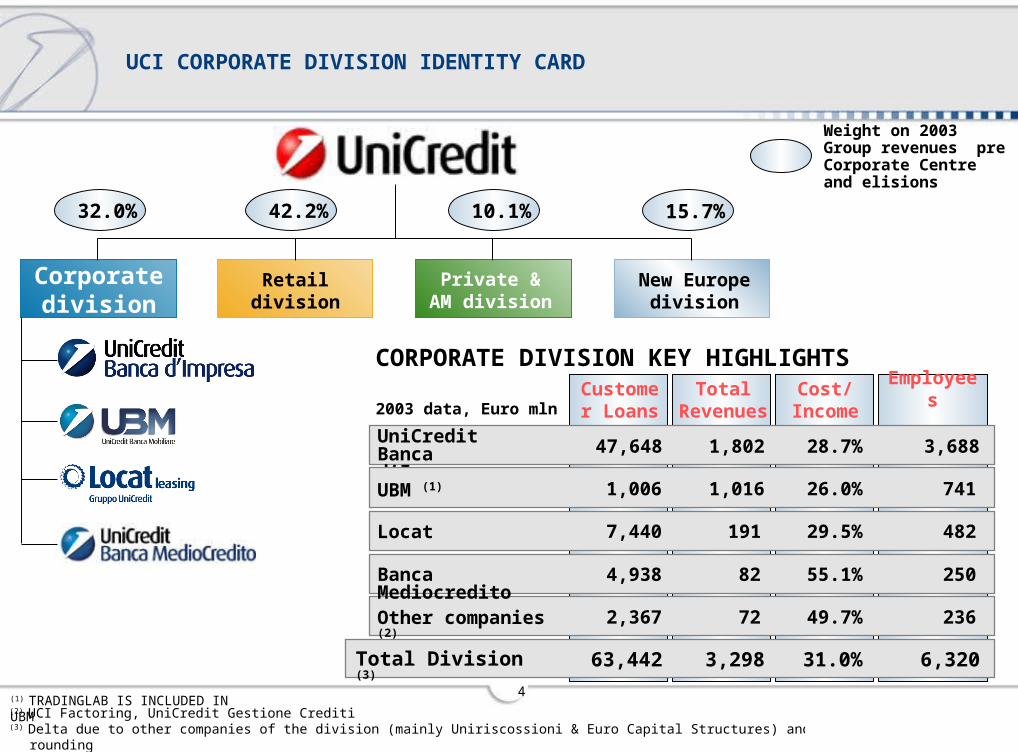

UCI CORPORATE DIVISION IDENTITY CARD

New Europe division

Private & AM division

Retail division

Corporate division

32.0% 42.2% 10.1% 15.7%

Weight on 2003 Group revenues pre Corporate Centre and elisions

(2) UCI Factoring, UniCredit Gestione Crediti(3) Delta due to other companies of the division (mainly Uniriscossioni & Euro Capital Structures) and rounding

2003 data, Euro mln

UniCredit Banca d’Impresa

Customer Loans

47,648

UBM (1) 1,006

Total Division (3) 63,442

Total Revenues

1,802

1,016

3,298

28.7%

26.0%

31.0%

Cost/ Income

Locat 7,440

Other companies (2) 2,367

191

72

29.5%

49.7%

3,688

741

6,320

Employees

482

236

CORPORATE DIVISION KEY HIGHLIGHTS

Banca Mediocredito 4,938 82 55.1% 250

(1) TRADINGLAB IS INCLUDED IN UBM

5

UCI Corporate Division identity card

UBI’s highlights

Corporate lending scenario

UBI’s strategy and its ‘pact for growth’

AGENDA

6

UBI has combined the competencies in the corporate sector of a major national bank with those of six banks with a strong local presence

UBI’s core clients are companies with revenues of over 1.5 mln euro. This client segment covers around 120,000 companies that account for a total of 350 bln euros bank loans

Of Italy’s 120,000 SMEs around 56,500 are UBI’s clients of which 41,000 (72%) have an open lending relationship with UBI

UBI: THE FOCAL POINT OF THE CORPORATE DIVISION

Source: Source: UBI calculations on internal data, using Italian Credit Bureau definitions

(*) Client coverage refers to the number of UBI clients with outstanding loans, according to Italian Credit Bureau, relative to an estimate of the total number of corporate enterprises.

% UBI clientswith

outstanding loans on

core clients

Total Market

Total corporate enterprises 72%

Largest groups

Other corporate and SMEs

43%

72%

119,682

56,527

512

56,015

47%

UBI CoreClients

Client Coverage

(*)

7

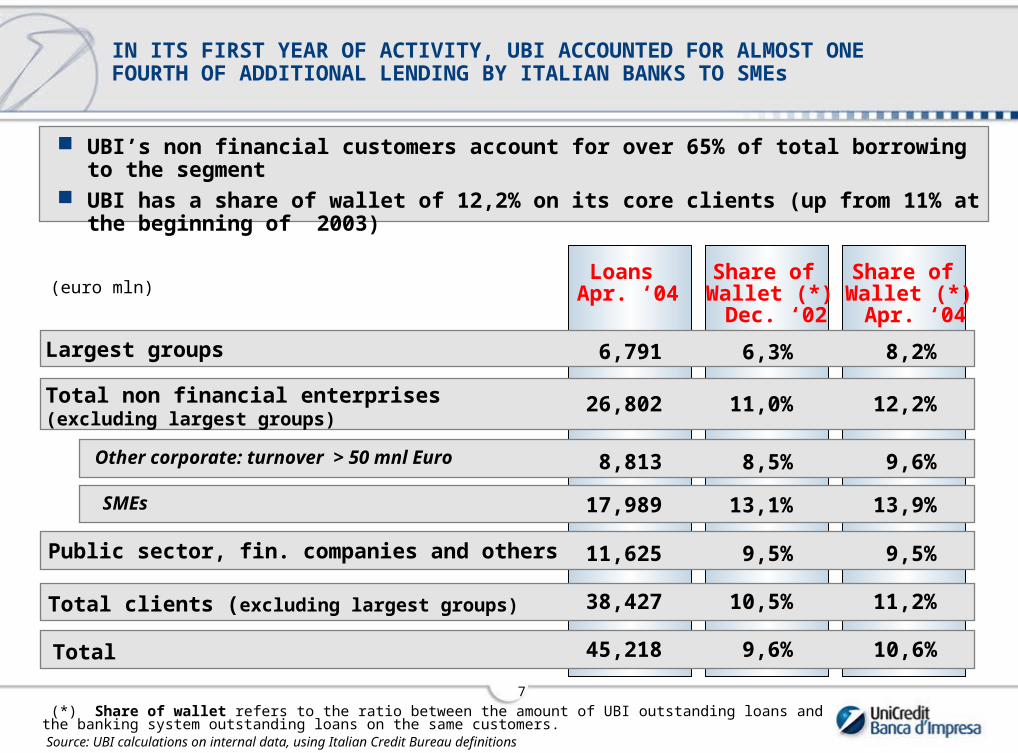

IN ITS FIRST YEAR OF ACTIVITY, UBI ACCOUNTED FOR ALMOST ONE FOURTH OF ADDITIONAL LENDING BY ITALIAN BANKS TO SMEs

UBI’s non financial customers account for over 65% of total borrowing to the segment UBI has a share of wallet of 12,2% on its core clients (up from 11% at the beginning of

2003)

Source: UBI calculations on internal data, using Italian Credit Bureau definitions

(*) Share of wallet refers to the ratio between the amount of UBI outstanding loans and the banking system outstanding loans on the same customers.

Share of Wallet (*) Dec. ‘02

6,3%

11,0%

13,1%

9,5%

10,5%

8,5%

9,6%

Loans Apr. ‘04

Share of Wallet (*) Apr. ‘04

(euro mln)

Largest groups

Public sector, fin. companies and others

Total clients (excluding largest groups)

Total non financial enterprises (excluding largest groups)

Total

SMEs

Other corporate: turnover > 50 mnl Euro

6,791

11,625

38,427

26,802

45,218

17,989

8,813

8,2%

9,5%

11,2%

10,6%

13,9%

9,6%

12,2%

8

A CORPORATE BANK, WITH A WELL BALANCED REVENUE BASE IN TERMS OF CLIENT SEGMENTATION AND OF INTEREST vs FEE INCOME

Total (excluding largest groups) 396 92% 62% 34%

Total 430 100% 61% 35%

Total Revenues

Total Revenues

Breakdown

Weight of Interest

Income on revenues

Weight of Fee Income on revenues(euro mln)

Quarterly data as March 2004

94 22% 65% 30%Public sector, fin. companies and others

34 8% 59% 36%Largest groups

Other corporates and SMEs 302 70% 61% 36%

79 18% 68% 29%SMEs: turnover 1,5 - 5 mnl Euro

Other corp: turnover > 50 mnl Euro 59 14% 52% 43%

SMEs: turnover 5- 50 mnl Euro 164 38% 60% 37%

Source: UBI calculations on internal data

9

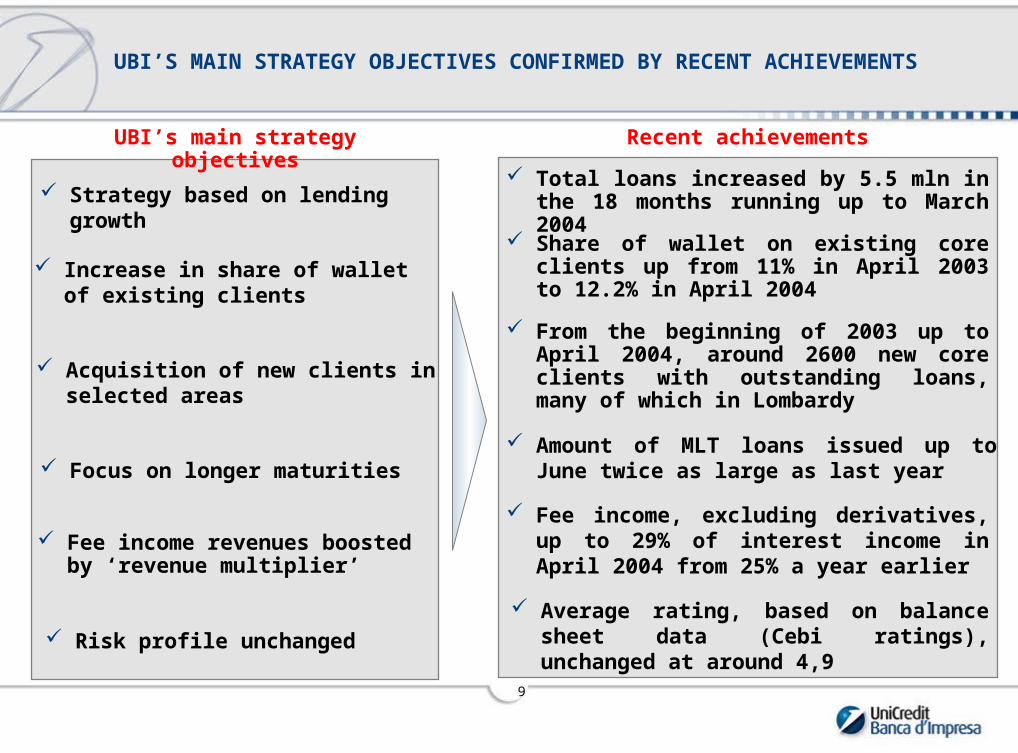

UBI’S MAIN STRATEGY OBJECTIVES CONFIRMED BY RECENT ACHIEVEMENTS

Strategy based on lending growth

Increase in share of wallet of existing clients

Acquisition of new clients in selected areas

UBI’s main strategy objectives Recent achievements

Focus on longer maturities

Total loans increased by 5.5 mln in the 18 months running up to March 2004

Share of wallet on existing core clients up from 11% in April 2003 to 12.2% in April 2004

From the beginning of 2003 up to April 2004, around 2600 new core clients with outstanding loans, many of which in Lombardy

Amount of MLT loans issued up to June twice as large as last year

Fee income, excluding derivatives, up to 29% of interest income in April 2004 from 25% a year earlier

Fee income revenues boosted by ‘revenue multiplier’

Average rating, based on balance sheet data (Cebi ratings), unchanged at around 4,9 Risk profile unchanged

10

UCI Corporate Division identity card

UBI’s highlights

Corporate lending scenario

UBI’s strategy and its ‘pact for growth’

AGENDA

11

90

92

94

96

98

100

102

104

106

108

Apr-01 Oct-01 Apr-02 Oct-02 Apr-03 Oct-03 Apr-0490

92

94

96

98

100

102

104

106

108

110

Turnover 3mma

Turnover

Orders 3mma sc. dx

Orders sc. dx.

Italy’s industrial production recovery considerably slower than in previous downturns…

… but recent data (e.g. orders and business turnover) highlight that the global recovery is finally reaching Italy

Source: UBI on ISTAT

ITALY’S MANUFACTURING SLOWDOWN HAS LASTED LONGER THAN IN PAST CYCLES, BUT THERE ARE CLEAR SIGNS OF RECOVERY AHEAD

Note: The cyclical low is set at 100. X axis shows the number of months from the cyclical low

98

100

102

104

106

108

110

112

114

-12 -10 -8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18 20 22 24 26

92-94 95-97

98-00 01-?

Industrial production index

12

DESPITE PROLONGED PRODUCTION WEAKNESS, COMPANIES’ PROFITABILITY SHOWS CONSIDERABLE RESILIENCE

2000 2001 2002

EBITDA/ turnover

Gross financial charges / op. income

ROE

Equity/ Total assets

1993

11.1 9.7 9.59.6

142.5 50.6 53.348.3

-6.3 5.0 2.66.5

23.9 26.9 28.426.7

Italian companies key ratios (%)

’92-’93 ’02-’03

Food, beverages and tobacco

Textile and clothes production

Chemical products, rubber and plastics

Leather

’90-’03

10.4 10.811.4

11.9 11.011.9

12.7 12.211.3

8.6 6.210.4

Italian manufacturing sectors:EBITDA/ production (%)

Machinery and mechanical products 9.9 7.911.0

Source: UBI on BACH and ISTAT

13

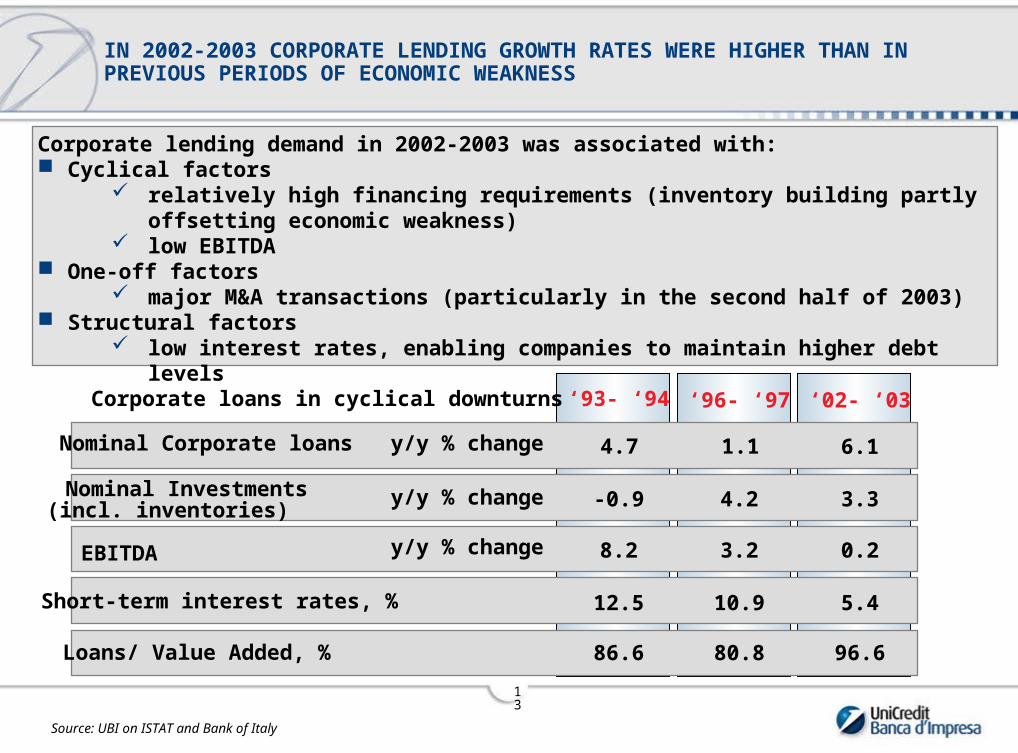

‘93- ‘94 ‘96- ‘97 ‘02- ‘03Corporate loans in cyclical downturns

Loans/ Value Added, % 86.6 80.8 96.6

Nominal Corporate loans 4.7 1.1 6.1

EBITDA 8.2 3.2 0.2y/y % change

Short-term interest rates, % 12.5 10.9 5.4

y/y % change

(incl. inventories)Nominal Investments -0.9 4.2 3.3y/y % change

IN 2002-2003 CORPORATE LENDING GROWTH RATES WERE HIGHER THAN IN PREVIOUS PERIODS OF ECONOMIC WEAKNESS

Corporate lending demand in 2002-2003 was associated with: Cyclical factors

relatively high financing requirements (inventory building partly offsetting economic weakness)

low EBITDA One-off factors

major M&A transactions (particularly in the second half of 2003) Structural factors

low interest rates, enabling companies to maintain higher debt levels

Source: UBI on ISTAT and Bank of Italy

14

0

2

4

6

8

10

12

14

Mar-98

Sep-98

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

Mar-03

Sep-03

Mar-04

Sep-04

Mar-05

Sep-05

Mar-06

Sep-06

Mar-07

Sep-07

Annual average

End ofperiod

IN COMING YEARS, CORPORATE LENDING SHOULD RETURN TO GROWTH RATES CONSISTENT WITH THE CYCLE…

2004 5.4 5.7

2005 7.0 6.4

2006 6.2 5.7

2007 5.1 4.8

The moderate economic recovery should keep corporate lending growth rates relatively low (around 5.9% on average in 2004-2007)

The influence of low interest rates on Italian companies’ debt levels should gradually lessen

The loans/value added ratio is higher than in the early 1990s and should remain at current levels

Corporate loans, y/y % change

Source: UBI on ISTAT and Bank of Italy

15

45.0

47.0

49.0

51.0

53.0

55.0

57.0

59.0

61.0

63.0

Mar-95

Sep-95

Mar-96

Sep-96

Mar-97

Sep-97

Mar-98

Sep-98

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

Mar-03

Sep-03

… WHILE GROWTH IN MEDIUM/LONG-TERM LOANS SHOULD CONTINUE TO OUTDO SHORT-TERM LOAN GROWTH AS OCCURRED IN THE PAST TWO YEARS…

Short-term corporate bank debt overtotal corporate bank debt

Shortterm

M/Lterm

2000 12.1 9.4

2001 12.2 7.2

2002 -0.8 12.4

2003 0.1 12.9

Different trends in short-term and medium/long-term loans reflect: Cyclical factors

cyclical weakness and low interest rates One-off factors

debt restructuring undertaken by a number of large industrial groups Structural factors

the propensity for companies to hold a higher proportion of medium/long-term debt in a trend towards convergence with the rest of Europe

Corporate Loans, y/y % change

Source: Bank of Italy

16

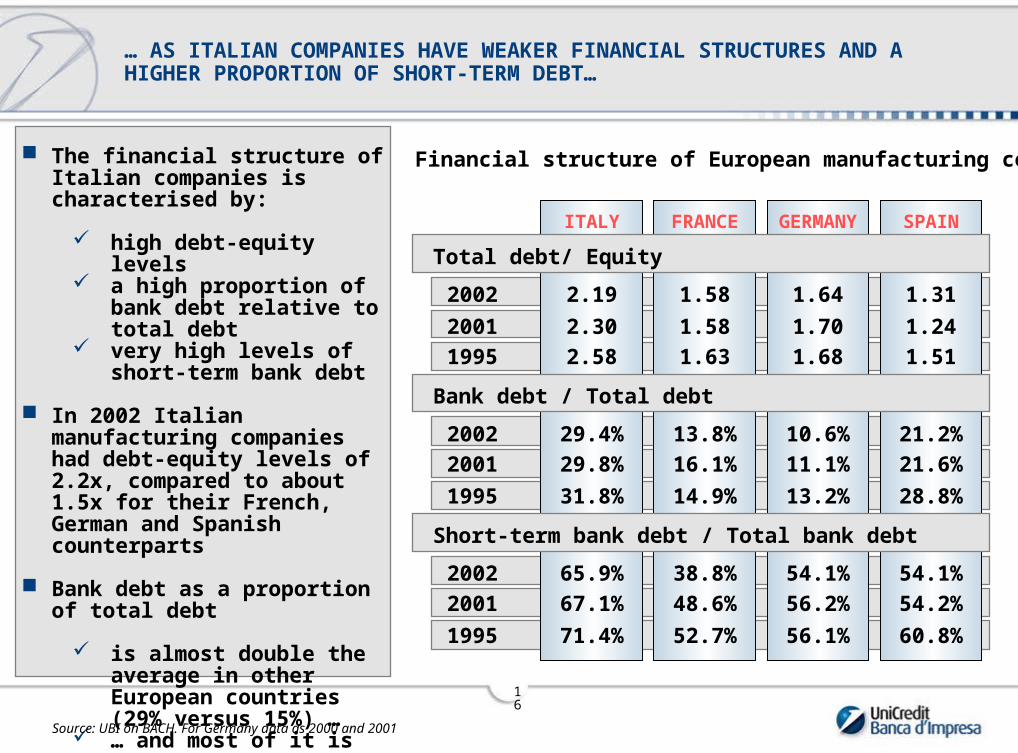

… AS ITALIAN COMPANIES HAVE WEAKER FINANCIAL STRUCTURES AND A HIGHER PROPORTION OF SHORT-TERM DEBT…

The financial structure of Italian companies is characterised by:

high debt-equity levels a high proportion of bank

debt relative to total debt very high levels of short-

term bank debt

In 2002 Italian manufacturing companies had debt-equity levels of 2.2x, compared to about 1.5x for their French, German and Spanish counterparts

Bank debt as a proportion of total debt

is almost double the average in other European countries (29% versus 15%) …

… and most of it is short-term debt

FRANCE GERMANY SPAINITALY

1.58 1.64 1.31

1.58 1.70 1.24

1.63 1.68 1.51

13.8% 10.6% 21.2%

16.1% 11.1% 21.6%

14.9% 13.2% 28.8%

38.8% 54.1% 54.1%

48.6% 56.2% 54.2%

2.19

2.30

2.58

29.4%

29.8%

31.8%

65.9%

67.1%

71.4% 52.7% 56.1% 60.8%

2002

2001

2001

2002

1995

1995

2002

2001

1995

Bank debt / Total debt

Total debt/ Equity

Short-term bank debt / Total bank debt

Source: UBI on BACH. For Germany data as 2000 and 2001

Financial structure of European manufacturing companies

17

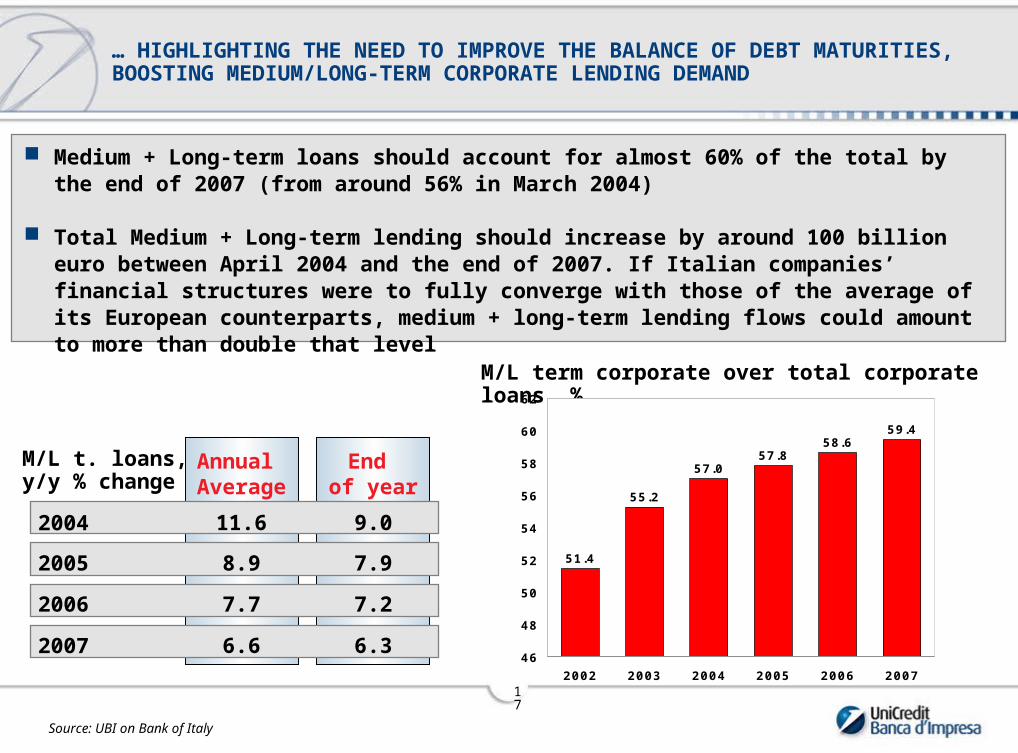

… HIGHLIGHTING THE NEED TO IMPROVE THE BALANCE OF DEBT MATURITIES, BOOSTING MEDIUM/LONG-TERM CORPORATE LENDING DEMAND

Medium + Long-term loans should account for almost 60% of the total by the end of 2007 (from around 56% in March 2004)

Total Medium + Long-term lending should increase by around 100 billion euro between April 2004 and the end of 2007. If Italian companies’ financial structures were to fully converge with those of the average of its European counterparts, medium + long-term lending flows could amount to more than double that level

Source: UBI on Bank of Italy

M/L term corporate over total corporate loans, %

Annual Average

End of year

11.6 9.0

8.9 7.9

7.7 7.2

6.6 6.3

2004

2005

2006

2007

M/L t. loans,y/y % change

51.4

55.2

57.057.8

58.659.4

46

48

50

52

54

56

58

60

62

2002 2003 2004 2005 2006 2007

18

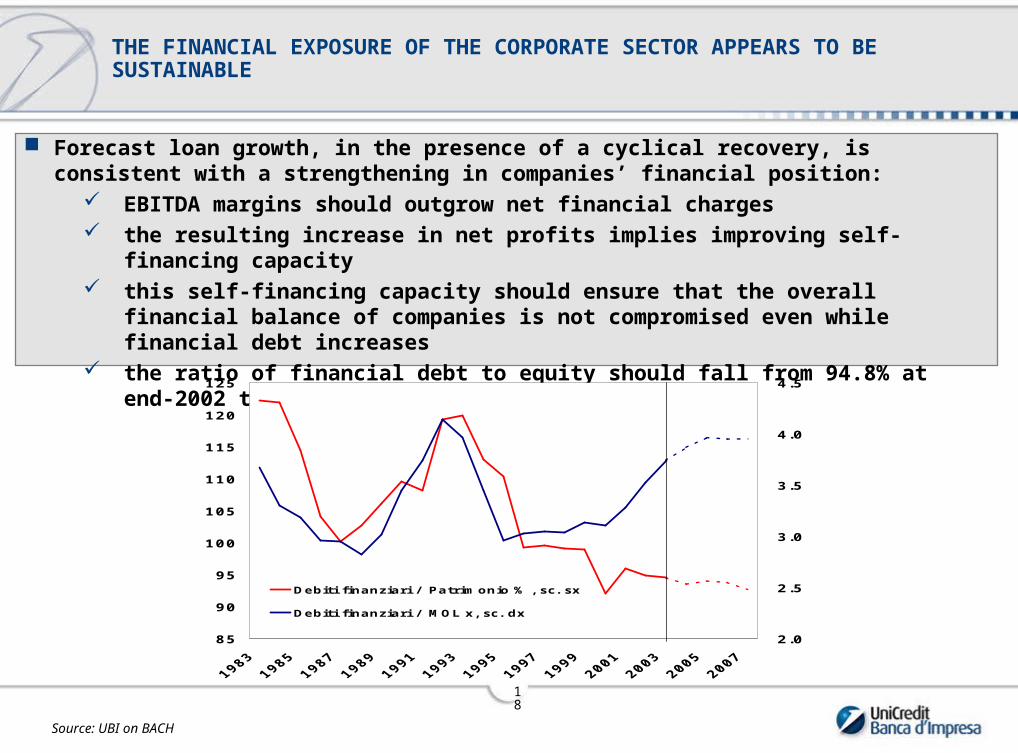

Forecast loan growth, in the presence of a cyclical recovery, is consistent with a strengthening in companies’ financial position:

EBITDA margins should outgrow net financial charges the resulting increase in net profits implies improving self-financing capacity this self-financing capacity should ensure that the overall financial balance of

companies is not compromised even while financial debt increases the ratio of financial debt to equity should fall from 94.8% at end-2002 to 92.6% at

end- 2007

THE FINANCIAL EXPOSURE OF THE CORPORATE SECTOR APPEARS TO BE SUSTAINABLE

Source: UBI on BACH

85

90

95

100

105

110

115

120

125

2.0

2.5

3.0

3.5

4.0

4.5

Debiti finanziari / Patrimonio % , sc. sx

Debiti finanziari / MOL x, sc. dx

19

UCI Corporate Division identity card

UBI’s highlights

Corporate lending scenario

UBI’s strategy and its ‘pact for growth’

AGENDA

20

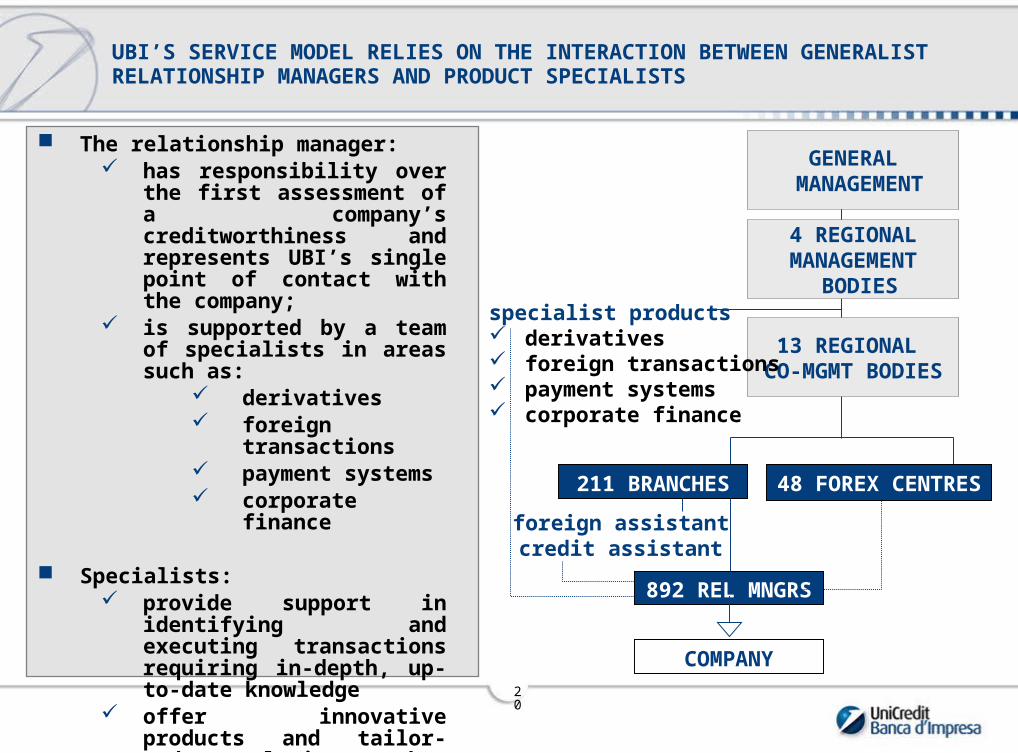

UBI’S SERVICE MODEL RELIES ON THE INTERACTION BETWEEN GENERALIST RELATIONSHIP MANAGERS AND PRODUCT SPECIALISTS

The relationship manager: has responsibility over the

first assessment of a company’s creditworthiness and represents UBI’s single point of contact with the company;

is supported by a team of specialists in areas such as:

derivatives foreign transactions payment systems corporate finance

Specialists: provide support in identifying

and executing transactions requiring in-depth, up-to-date knowledge

offer innovative products and tailor-made solutions that meet companies’ needs

foreign assistantcredit assistant

GENERAL MANAGEMENT

4 REGIONALMANAGEMENT

BODIES

13 REGIONAL CO-MGMT BODIES

211 BRANCHES 48 FOREX CENTRES

COMPANY

892 REL MNGRS

specialist products derivatives foreign transactions payment systems corporate finance

21

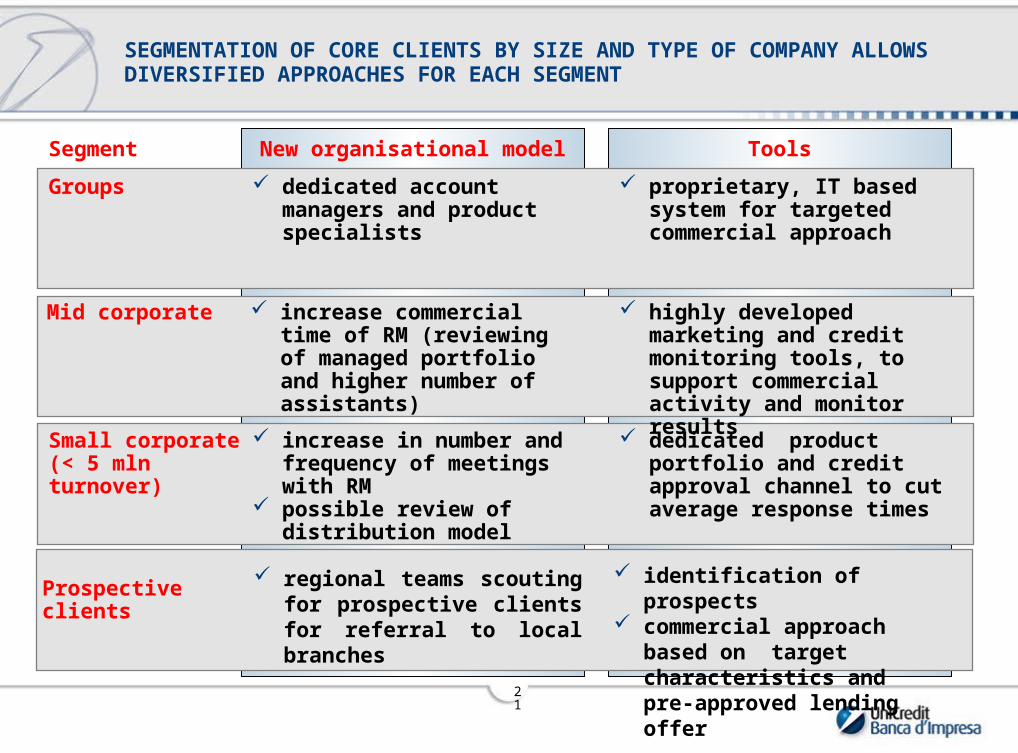

SEGMENTATION OF CORE CLIENTS BY SIZE AND TYPE OF COMPANY ALLOWS DIVERSIFIED APPROACHES FOR EACH SEGMENT

dedicated account managers and product specialists

Groups proprietary, IT based system for targeted commercial approach

increase commercial time of RM (reviewing of managed portfolio and higher number of assistants)

Mid corporate highly developed marketing and credit monitoring tools, to support commercial activity and monitor results

increase in number and frequency of meetings with RM

possible review of distribution model

Small corporate(< 5 mln turnover)

dedicated product portfolio and credit approval channel to cut average response times

New organisational modelSegment Tools

regional teams scouting for prospective clients for referral to local branches

Prospectiveclients

identification of prospects commercial approach based

on target characteristics and pre-approved lending offer

22

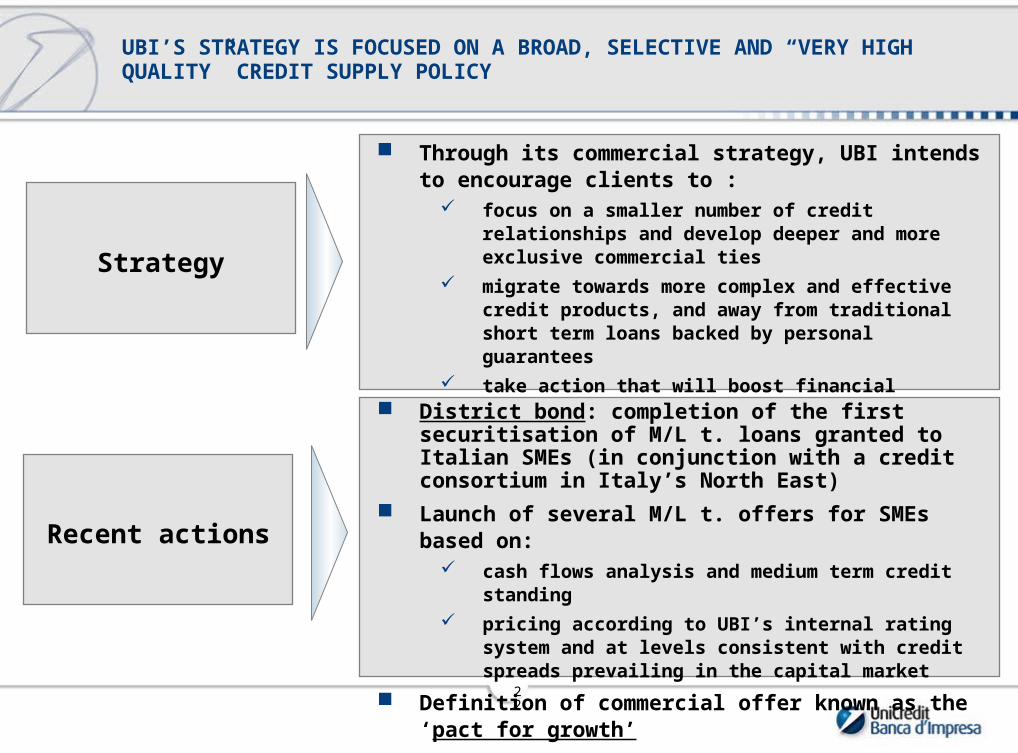

Strategy

Through its commercial strategy, UBI intends to encourage clients to :

focus on a smaller number of credit relationships and develop deeper and more exclusive commercial ties

migrate towards more complex and effective credit products, and away from traditional short term loans backed by personal guarantees

take action that will boost financial strength while offering specialised support for that purpose

District bond: completion of the first securitisation of M/L t. loans granted to Italian SMEs (in conjunction with a credit consortium in Italy’s North East)

Launch of several M/L t. offers for SMEs based on: cash flows analysis and medium term credit standing

pricing according to UBI’s internal rating system and at levels consistent with credit spreads prevailing in the capital market

Definition of commercial offer known as the ‘pact for growth’

UBI’S STRATEGY IS FOCUSED ON A BROAD, SELECTIVE AND “VERY HIGH QUALITY” CREDIT SUPPLY POLICY

Recent actions

23

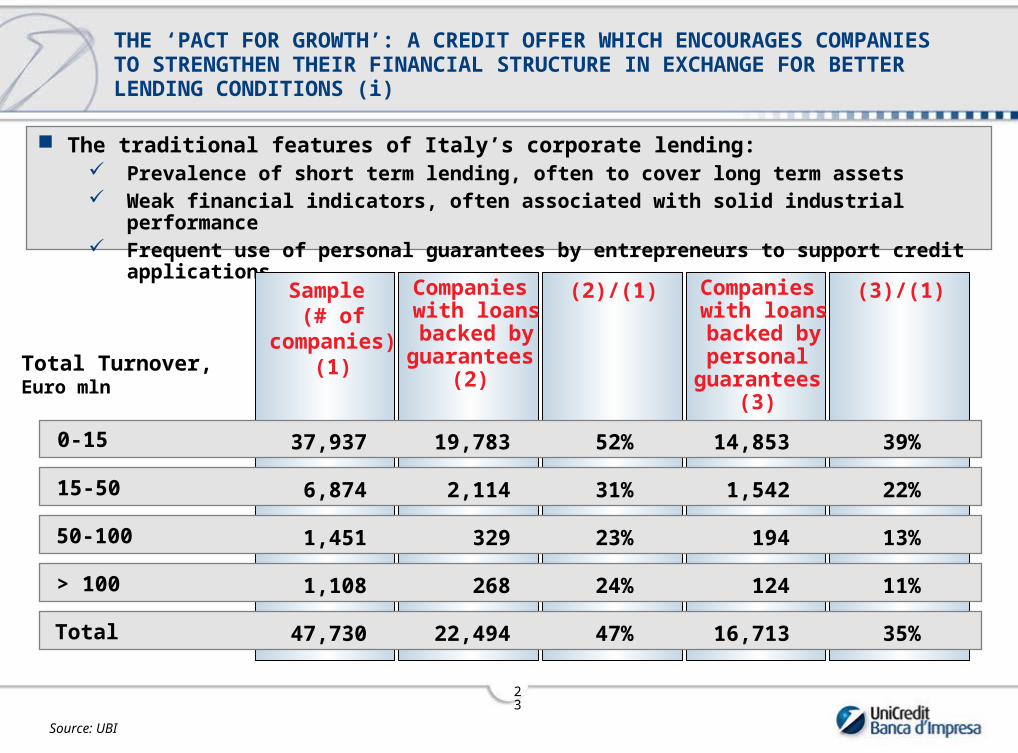

The traditional features of Italy’s corporate lending: Prevalence of short term lending, often to cover long term assets Weak financial indicators, often associated with solid industrial performance Frequent use of personal guarantees by entrepreneurs to support credit applications

THE ‘PACT FOR GROWTH’: A CREDIT OFFER WHICH ENCOURAGES COMPANIES TO STRENGTHEN THEIR FINANCIAL STRUCTURE IN EXCHANGE FOR BETTER LENDING CONDITIONS (i)

Companies with loans backed byguarantees

(2)

(2)/(1) Companies with loans backed by personal

guarantees(3)

(3)/(1)

0-15

15-50

50-100

> 100

Total

Sample (# of

companies) (1)

37,937 52% 14,853 39%19,783

6,874 31% 1,542 22%2,114

1,451 23% 194 13%329

1,108 24% 124 11%268

47,730 47% 16,713 35%22,494

Source: UBI

Total Turnover,Euro mln

24

UBI is now marketing a credit offer – known as the ‘pact for growth’ – based on the following features:

Offer of medium-/long-term financing of an amount that will improve the financial structure of the company

Require companies to increase equity by a level that will improve the company’s rating

Set covenants to be monitored every six months

If a satisfactory level of creditworthiness is reached, UBI is prepared to give up personal guarantees

THE ‘PACT FOR GROWTH’ (ii)

Such ample use of personal guarantees implies that:

the availability of bank lending is often based on the creditworthiness of the entrepreneur rather than on the company’s true capacity to generate income

our estimates indicate that the banking system tends to overestimate the reduction in LGD* granted by personal guarantees

(*) LGD: Loss Given Default

25

UBI strategy has been confirmed by recent results: UBI has increased its share of wallet, boosted fee revenues (ex. derivatives), while keeping an unchanged risk profile

To achieve further, significant growth UBI also needs to update its supply policy: the flow of Italian corporate lending should focus on medium to long term maturities

Both the economic and the lending scenarios should ensure that lending growth is achieved without a deterioration in creditworthiness

At the same time companies should migrate towards more complex and effective credit products, and away from traditional short term loans backed by personal guarantees. A reduction in Italy’s multibanking tradition is also likely

UBI’s service model, client segmentation and risk management capabilities put us in an ideal position to capture a more than proportional share of the new lending flows

SUMMING UP

26

Francesco Giordano – Head of UBI Planning, Research and Strategy

Focus on Credit Quality

AGENDA

27

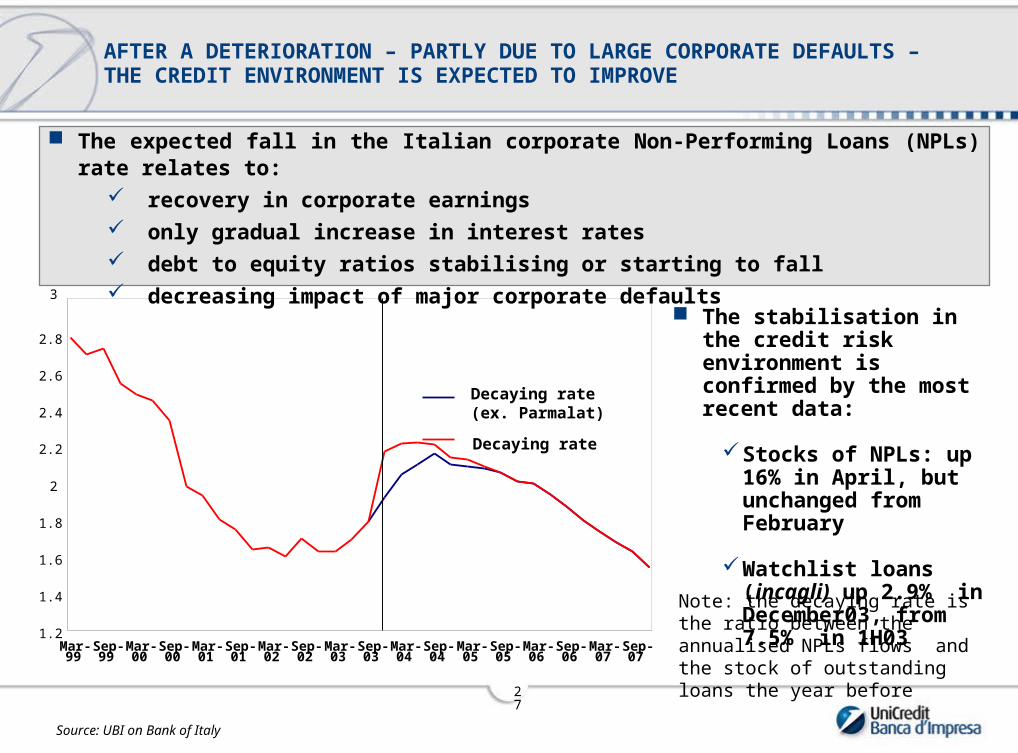

The expected fall in the Italian corporate Non-Performing Loans (NPLs) rate relates to: recovery in corporate earnings only gradual increase in interest rates debt to equity ratios stabilising or starting to fall decreasing impact of major corporate defaults

AFTER A DETERIORATION – PARTLY DUE TO LARGE CORPORATE DEFAULTS – THE CREDIT ENVIRONMENT IS EXPECTED TO IMPROVE

Note: the decaying rate is the ratio between the annualised NPLs flows and the stock of outstanding loans the year before

1.2

1.4

1.6

1.8

2

2.2

2.4

2.6

2.8

3

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

Mar-03

Sep-03

Mar-04

Sep-04

Mar-05

Sep-05

Mar-06

Sep-06

Mar-07

Sep-07

Source: UBI on Bank of Italy

Decaying rate(ex. Parmalat)

Decaying rate

The stabilisation in the credit risk environment is confirmed by the most recent data:

Stocks of NPLs: up 16%

in April, but unchanged from February

Watchlist loans (incagli) up 2.9% in December03, from 7.5% in 1H03

28

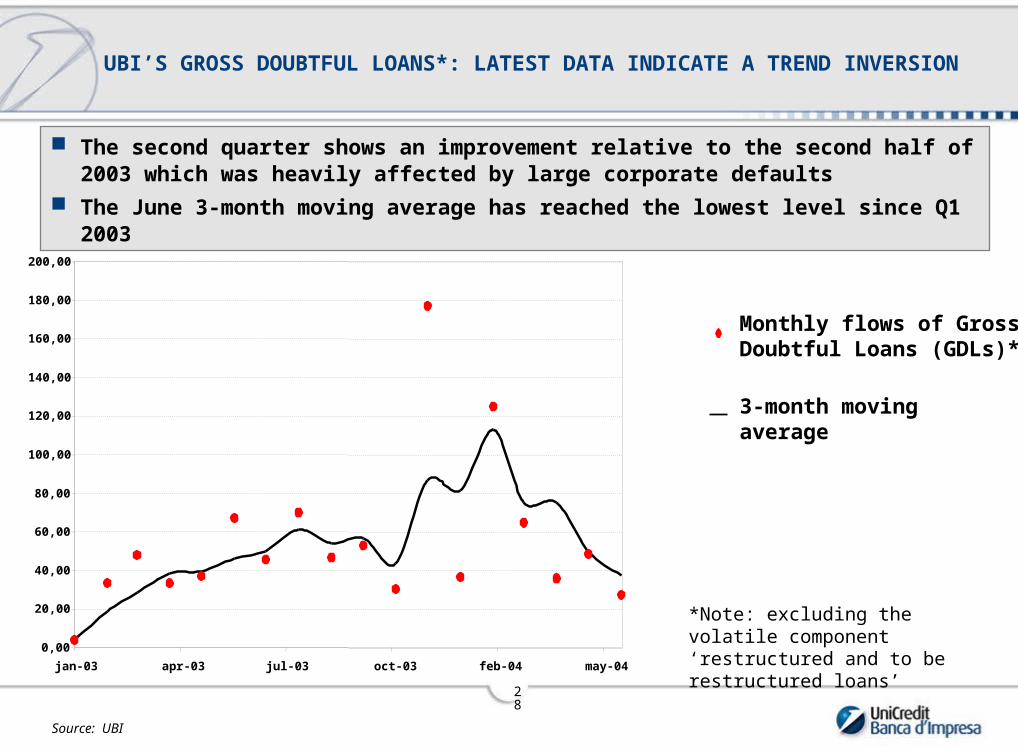

The second quarter shows an improvement relative to the second half of 2003 which was heavily affected by large corporate defaults

The June 3-month moving average has reached the lowest level since Q1 2003

Monthly flows of Gross Doubtful Loans (GDLs)*

3-month moving average

UBI’S GROSS DOUBTFUL LOANS*: LATEST DATA INDICATE A TREND INVERSION

0,00

20,00

40,00

60,00

80,00

100,00

120,00

140,00

160,00

180,00

200,00

jan-03 apr-03 jul-03 oct-03 feb-04 may-04

Source: UBI

*Note: excluding the volatile component ‘restructured and to be restructured loans’

29

EXCLUDING THE TWO LARGEST POSITIONS, THE TREND INVERSION APPEARS TO BE CONFIRMED

Excluding the two single largest positions (each month), GDLs show early signs of a trend inversion

Current June levels, if confirmed by subsequent observations, would be below expectations based on economic forecasts

Monthly flows of Gross Doubtful Loans (GDLs)* ex. 2 largest positions

3-month moving average

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

jan-03 apr-03 jul-03 oct-03 feb-04 may-04

Source: UBI

*Note: excluding the volatile component ‘restructured and to be restructured loans’

30

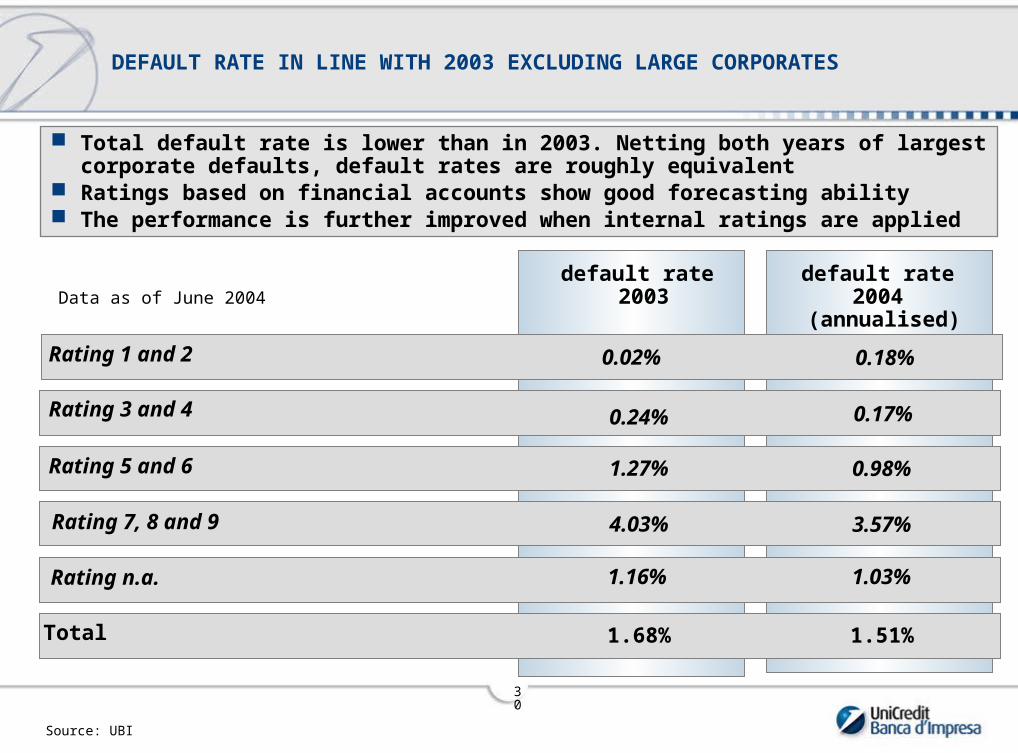

DEFAULT RATE IN LINE WITH 2003 EXCLUDING LARGE CORPORATES

Source: UBI

Rating 1 and 2 0.02% 0.18%

Rating 3 and 4 0.24% 0.17%

Rating 5 and 6 1.27% 0.98%

Rating 7, 8 and 9 4.03% 3.57%

Rating n.a. 1.16% 1.03%

Total 1.68% 1.51%

default rate 2003

default rate 2004

(annualised) Data as of June 2004

Total default rate is lower than in 2003. Netting both years of largest corporate defaults, default rates are roughly equivalent

Ratings based on financial accounts show good forecasting ability The performance is further improved when internal ratings are applied

31

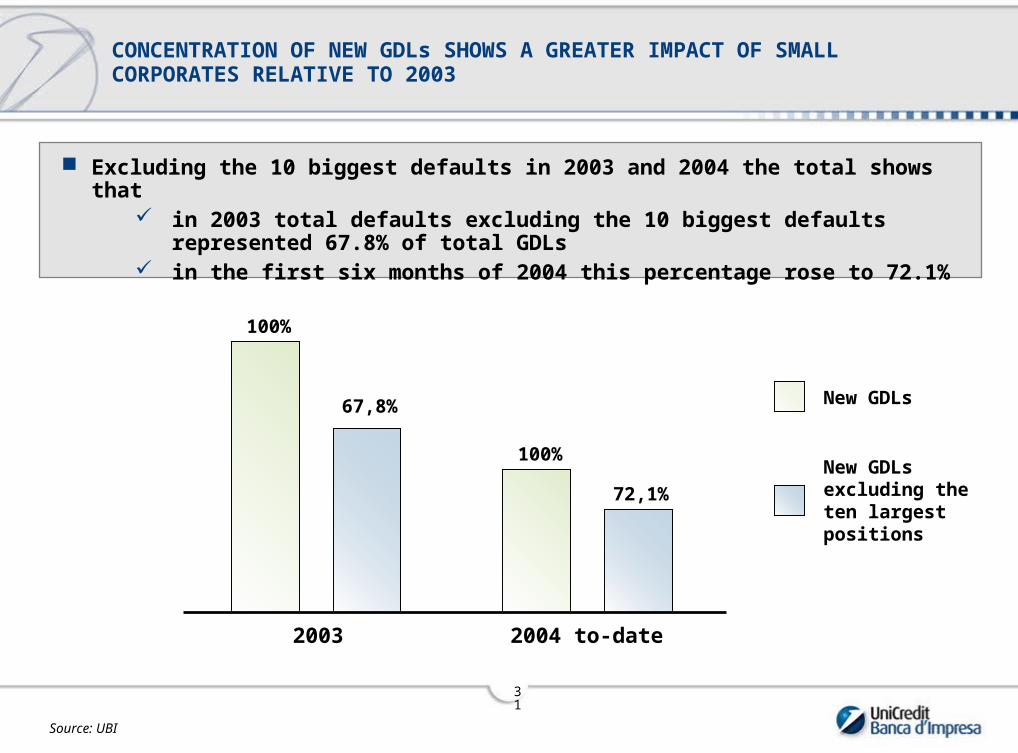

Excluding the 10 biggest defaults in 2003 and 2004 the total shows that in 2003 total defaults excluding the 10 biggest defaults represented 67.8% of

total GDLs in the first six months of 2004 this percentage rose to 72.1%

CONCENTRATION OF NEW GDLs SHOWS A GREATER IMPACT OF SMALL CORPORATES RELATIVE TO 2003

Source: UBI

New GDLs excluding the ten largest positions

New GDLs

100%

2004 to-date2003

67,8%

100%

72,1%

32

DEFAULT RATES ARE OVER-REPRESENTED IN CYCLICAL SECTORS

Branch of economic activity

Strongly cyclical activitiesTEXTILE / LEATHER / FOOTWEAR / AND CLOTHES PRODUCTIONAGRICULTURAL AND INDUSTRIAL MACHINERY PRODUCTIONMETAL PRODUCTS EXCLUDING MACHINERY / TRANSPORTELECTRICAL MATERIAL AND SUPPLIESOTHER INDUSTRIAL PRODUCTS TRANSPORT PRODUCTS CHEMICAL PRODUCTSRUBBER AND PLASTIC

OFFICE MACHINERY FOR DATA ELABORATION / AND PRECISION MACHINERY

BUILDING AND PUBLIC WORKS AGRICULTURE/ SILVICOLTURE / AND FISH

SERVICES CONNECTED TO TRANSPORTSCOMMERCE / RECOVERIES / REPAIRS SERVICES OTHER SALE ORIENTED SERVICESSERVICES OF INNER TRANSPORTATIONSHOTEL SERVICES / OTHER PUBLICS EXERCISESTRANSPORT MARINE AND AERIAL SERVICES

COMMUNICATIONS SERVICES

VolumeShare

DefaultShare

4.7% 7.9%3.8% 7.3%3.5% 5.3%3.3% 3.8%3.3% 4.4%1.3% 3.7%2.0% 2.6%1.5% 2.0%1.2% 0.9%

7.7% 9.6%1.3% 0.7%

2.6% 12.9%12.6% 13.3%14.4% 13.9%0.8% 1.1%1.2% 0.6%0.6% 0.4%1.1% 0.0%

FOOD / BEVERAGES / AND TOBACCO PRODUCTS PAPER / PRESS AND EDITORIAL PRODUCTS

MINERAL AND NOT FERROUS MINERAL PRODUCTS MINERALS AND FERROUS METALS AND NON FERROUS ONES

3.8% 3.0%1.4% 2.3%

2.7% 2.0%2.2% 0.5%

Cyclical activities

Anti-cyclical activities

Other activities

Services

Source: UBI

ENERGY PRODUCTS 3.7% 0.1%

33

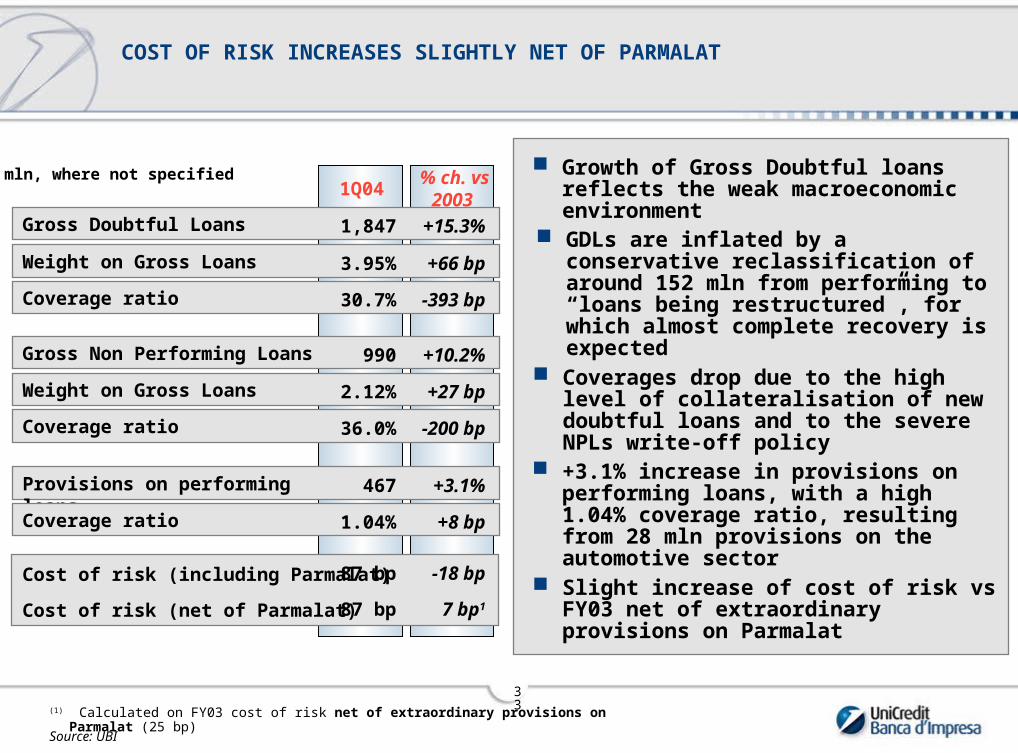

COST OF RISK INCREASES SLIGHTLY NET OF PARMALAT

Coverage ratio 36.0% -200 bp

1Q04% ch. vs

2003

Provisions on performing loans 467 +3.1%

Coverage ratio 1.04% +8 bp

Gross Doubtful Loans 1,847 +15.3%

Coverage ratio 30.7% -393 bp

Cost of risk (including Parmalat) 87 bp -18 bp

Weight on Gross Loans 3.95% +66 bp

mln, where not specified

Gross Non Performing Loans 990 +10.2%

Weight on Gross Loans 2.12% +27 bp

(1) Calculated on FY03 cost of risk net of extraordinary provisions on Parmalat (25 bp)

Cost of risk (net of Parmalat) 87 bp 7 bp1

Growth of Gross Doubtful loans reflects the weak macroeconomic environment

+3.1% increase in provisions on performing loans, with a high 1.04% coverage ratio, resulting from 28 mln provisions on the automotive sector

Slight increase of cost of risk vs FY03 net of extraordinary provisions on Parmalat

GDLs are inflated by a conservative reclassification of around 152 mln from performing to “loans being restructured”, for which almost complete recovery is expected

Coverages drop due to the high level of collateralisation of new doubtful loans and to the severe NPLs write-off policy

Source: UBI

34

1Q04(including write-offs)

COVERAGE LEVELS EXPLAINED BY CONSERVATIVE RECLASSIFICATION AND WRITE-OFFS

Coverage ratio 73.9%

1Q04Net of new

restructured loans

Gross Doubtful Loans 1,847 1,695

Coverage ratio 30.7% 33.2%

mln, where not specified

Gross Non Performing Loans 2,418

Conservative “loans being restructured” reclassification of around 152 mln in 1Q04 weighed on the GDLs coverage ratio

Net of this effect, the ratio improved by around 250 bp

Write-offs of highly covered positions have a negative impact on coverage figures

Summing up write-offs both to NPLs stock and provisions, NPLs coverage gross of write-offs shows a very conservative provision policy

75.9%

2,226

1Q03(including write-offs)

mln, where not specified

Source: UBI

35

Ferdinando Samaria – UBM Chief Financial Officer

Focus on Revenue Diversification and Financial Risk Management

AGENDA

36

Conceived in 1998, formally spun off in 2000 569 employees, average age 35 S&P Rating: AA- Gross Revenues: EUR 770m Net income: EUR 340m Average daily VaR: EUR 4.4m ROE: 61% Net income/employee: EUR 598k

Derivatives portfolio’s outstanding notional > €1000b Outstanding trades > 200,000 Total risk factors > 40,000 Total web transactions on capital guaranteed products > 500,000 Number of daily trade revaluations > 15m

KEY FACTS – UBM AS OF 31 DEC 2003

COMPANY PROFILE

SOME TRADING BOOK STATISTICS

Regulatory Capital Requirements

-

200

400

600

800

1,000

1,200

Mar-03 Jun-03 Sep-03 Dec-03

EU

R/m

37

UBM has completed the merger with TradingLab, the bank dedicated to providing UniCredito retail customers with financial products and services

The merged trading book, particularly in equity derivatives, becomes one of Europe’s largest

Synergies in terms of pricing capability and risk management

Some savings in infrastructure costs

Negotiating with regulators extension of internal model to TradingLab books

Increased overall ability to generate diversified revenues

UBM AFTER MERGER WITH TRADINGLAB

38

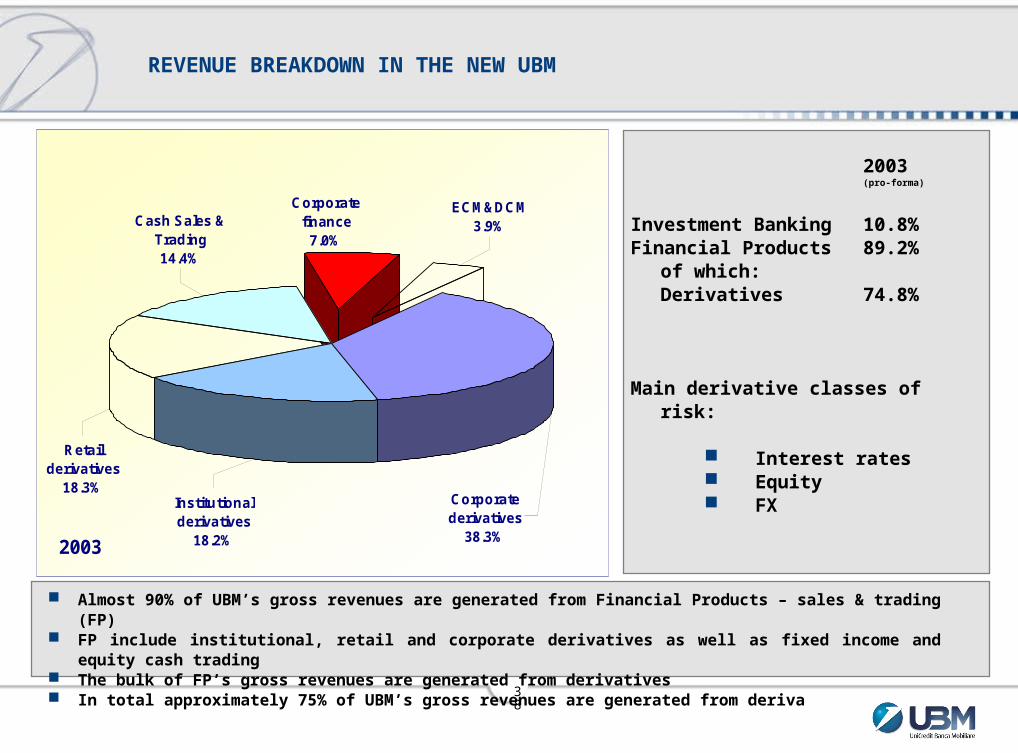

2003

ECM&DCM3.9%

Corporate finance

7.0%Cash Sales &

Trading14.4%

Retail derivatives

18.3%Institutional derivatives

18.2%

Corporate derivatives

38.3%

Almost 90% of UBM’s gross revenues are generated from Financial Products – sales & trading (FP) FP include institutional, retail and corporate derivatives as well as fixed income and equity cash trading The bulk of FP’s gross revenues are generated from derivatives In total approximately 75% of UBM’s gross revenues are generated from derivatives

REVENUE BREAKDOWN IN THE NEW UBM

2003(pro-forma)

Investment Banking 10.8%Financial Products 89.2%

of which:Derivatives74.8%

Main derivative classes of risk:

Interest rates Equity FX

39

FOCUS ON FINANCIAL PRODUCTS

UBM has completed the merger with TradingLab, the bank dedicated to providing UniCredito retail

From the beginning of operations, market risk management has been a distinctive element in UBM

Derivative products are traded on all asset classes

Ability to address a broad segment of corporate and institutional customers with innovative financial products

Core skills in pricing, hedging and trading

Products are unbundled into elementary risk components by proprietary pricing models and hedged through wholesale markets

Limited back-to-back trading

Industrial approach: large volumes, high throughput, efficient time-to-market

UBM transforms derivatives risks into market, model, counterparty and operational risks

40

UBM

CLIENT1

CLIENT2

CLIENTn

CTPY1

CTPY2

CTPY3

CTPYm

DERIVATIVE PRODUCT

SALES TRADINGRISK

MANAGEMENT

OPERATIONAL

RISK

MARKET

RISK

MODEL

RISK

COUNTERPARTY

RISK

THE RISK MANAGEMENT STAGES

41

Daily VaR vs P&L

-7

-5

-3

-1

1

3

5

7

Date

P&

L (

EU

R/m

)

PL

VaR

MARKET RISK

UBM’s portfolio affected by more than 40,000 risk factors VaR calculated daily through a proprietary VaR engine via historical simulation VaR parameters: 99% double-tail confidence level, 1-day holding period, daily update

of time series VaR model has been validated by Italian regulators for capital requirement purposes

UBM daily VaR limit is €7m, against a one-year average of €4.4m (max €6.6m)

Daily back-testing against “clean” P&L series as well as crash/stress tests

42

Market Surface

1

3

5

7

9

12

3.0

%3

.5%

4.0

%4

.5%

4.8

%5

.0%

5.5

%6

.0%

7.0

%8

.0%

9.0

%

10%11%12%13%14%15%16%17%18%19%20%21%22%23%24%25%

Maturity

Strike

10.

0%

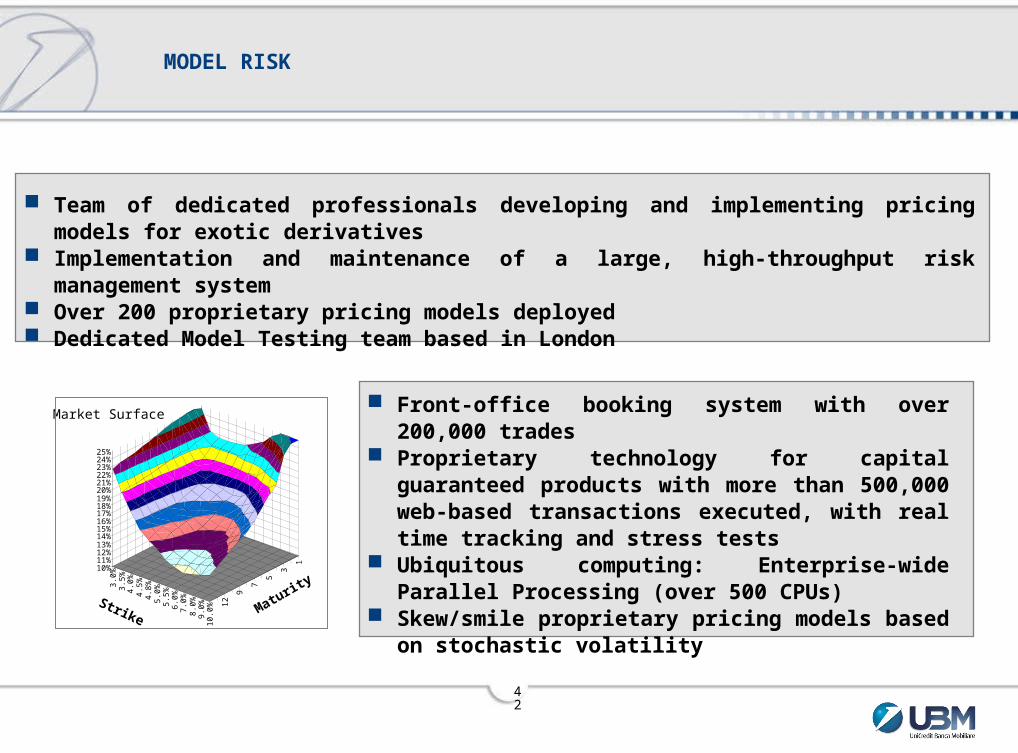

Team of dedicated professionals developing and implementing pricing models for exotic derivatives

Implementation and maintenance of a large, high-throughput risk management system Over 200 proprietary pricing models deployed Dedicated Model Testing team based in London

Front-office booking system with over 200,000 trades Proprietary technology for capital guaranteed

products with more than 500,000 web-based transactions executed, with real time tracking and stress tests

Ubiquitous computing: Enterprise-wide Parallel Processing (over 500 CPUs)

Skew/smile proprietary pricing models based on stochastic volatility

MODEL RISK

43

MEASURING COUNTERPARTY RISK

Derivative portfolio size > €1,000b Market risks are hedged through OTC trades with other market counterparties Traditionally counterparty risk has been monitored using fixed coefficients Need to quantify the effective cost of substitution The cost of substitution is the value of each trade increased by the potential variation that

may occur Estimate the cost of substitution as the marked-to-market valuation plus a simple add-on

METHOD’S ADVANTAGES

Quantifies more accurately the real counterparty risk Uses standard product control techniques Can be used with risk mitigation tools such as close-out netting and collateral agreements When using netting, portfolio diversification is captured Dynamic methodology in line with market variations More in line with market practice and central bank models Can bring in market risk techniques (substitution of the simple add-on with VaR)

COUNTERPARTY RISK

44

ASSESSING AND CONTROLLING OPERATIONAL RISK

Operational risk is defined as the risk of losses resulting from inadequate or failed internal processes, people and systems or from external events. This definition includes legal risk, but excludes strategic and reputational risk (Basel, September 2001)

Risk control is achieved through process mapping, risk assessment and business process reengineering

The “Operational risk control” project is an on-going activity that advances by gradual improvements

Main steps: Definition of roles and responsibility Implementation of techniques of process analysis and representation Application development to support historical loss data collection Study of risk assessment methodology to influence business process and

control reengineering

OPERATIONAL RISK

Recommended