CALFRAC WELL SERVICES LTD. 2016 Barclays CEO Energy-Power Conference

TSX:CFW

Certain information contained within this presentation and statements made in conjunction with this presentation constitute forward-looking statements. These statements relate to future events or the future performance of the Company. All statements other than statements of historical fact may be forward-looking statements. Forward-looking statements are often, but not always, identified by the use of words such as “seek”, “anticipate,” “plan”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “predict”, “potential”, “targeting”, “intend”, “could”, “might”, “should”, “believe”, “forecast”, “can” and similar expressions. In particular, forward-looking statements in this presentation include, but are not limited to, statements with respect to future capital expenditures, future financial resources, anticipated equipment utilization levels, future oil and gas well activity, projections of market prices and costs, outcomes of specific events and trends in the oil and gas industry.

The forward-looking statements within this presentation and made in conjunction with this presentation are derived from certain assumptions and analyses made by the Company based on its experience and perception of historical trends, current conditions, expected future developments and other factors that it believes are appropriate in the circumstances, including assumptions and analyses relating to: the economic and political environment in which the Company operates; the Company’s expectations for its customers’ capital budgets and geographical areas of focus; the effect unconventional oil and gas projects have had on supply and demand fundamentals for oil and natural gas; the Company’s existing contracts and the status of current negotiations with key customers and suppliers; the effectiveness of cost reduction measures instituted by the Company; and the likelihood that the current tax and regulatory regime will remain substantially unchanged. Forward-looking statements are subject to a number of known and unknown risks and uncertainties that could cause actual results to differ materially from the Company’s expectations. Such risks and uncertainties include the items discussed under the heading “Business Risks” in the Company’s 2015 Annual Report and under the heading “Risk Factors” in the Company’s most recently filed Annual Information Form. Consequently, all of the forward-looking statements contained within this presentation and made in conjunction with this presentation are qualified by these cautionary statements and there can be no assurance that actual results or events anticipated by the Company will be realized or that they will have the expected consequences or effects on the Company or its business or operations.

Other than as required by applicable securities laws, the Company assumes no obligation to update publicly any such forward-looking statements, whether as a result of new information, future events or otherwise.

Forward Looking Statement

© Calfrac Well Services Ltd. 2

© Calfrac Well Services Ltd. 3

Company Snapshot

* As at 16:00:00 ET 9/1/2016

TSX Stock Symbol: CFW

Share Price* $2.93

30-Day Average Volume* 690,000

Market Capitalization* $338.7 million

Enterprise Value* $1.1 billion

Shares Outstanding* 115.6 million

Insider Ownership ~25%

Canada Frac Crew Operator (2012). Calfrac Well Services Photo

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1/4/2013 1/4/2014 1/4/2015 1/4/2016

Nu

mb

er

of

Rig

s

Lower 48 Active Land Rig Count

0

100

200

300

400

500

600

700

800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Nu

mb

er

of

Act

ive

WC

SB L

an

d R

igs

2012 2013 2014 2015 2016

Active Rig Counts: North America & International

© Calfrac Well Services Ltd. 4

- U.S. land rig count down ~75% from

peak, up ~110 rigs from trough

- International rig count down ~30% from

peak

Source: Baker Hughes

- WCSB active rig count down ~40% Y/Y

QTD Q3/16

200

220

240

260

280

300

320

340

360

700

750

800

850

900

950

1,000

1,050

1,100

Nu

mb

er o

f O

ffsh

ore

Rig

s

Nu

mb

er o

f O

nsh

ore

Rig

s

International Land Rig Count International Offshore Rig Count

© Calfrac Well Services Ltd. 5

Global Supply/Demand

Global oil demand growth continues

U.S. oil production declines accelerating and expected to continue into 2017

U.S. inventories need to see a sustained drawdown to move prices higher

Global oversupply overstated – unreliable data

Market rebalancing without OPEC intervention

Expect a more balanced market in H2/16 driven by price

Source: Bloomberg

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1/6/2012 1/6/2013 1/6/2014 1/6/2015 1/6/2016

00

0's

Bb

ls/d

Weekly Lower 48 Oil Production

Full Service Pressure Pumping

Canada Fleet: 410,000 Horsepower

13 Coiled Tubing Crews

U.S. Fleet: 611,000 Horsepower

11 Cementing Crews

5 Coiled Tubing Crews

Latin America Fleet: 131,000 Horsepower

14 Cementing Crews

7 Coiled Tubing Crews

Russia Fleet: 70,000 Horsepower

7 Coiled Tubing Crews

As at June 30, 2016

© Calfrac Well Services Ltd. 6

Canadian Operations

© Calfrac Well Services Ltd. 7

Canada Fleet: 410,000 Horsepower

13 Coiled Tubing Crews

Calfrac Market Positioning

Positioned in key areas of frac demand:

– Montney, Duvernay, Deep Basin,

Cardium and Viking

Diversified customer base gives us

exposure to all key areas of the world-class

Montney resource play

Greater proportion of 24-hour operations

Pricing & Utilization

Pricing fell ~5-10% sequentially in Q2/16,

pricing not expected to fall further

~50% of horsepower parked

7 of 13 coil units idled

Market Trends

Stages per well increasing

Frac spacing tightening

Operators refocusing on highest quality

plays and assets

Market Outlook

Rig count down ~40% Y/Y Q3/16 quarter-

to-date

Anticipate strong utilization through Q3/16

aside from weather related issues

Visibility for Q4/16 improving but still limited

© Calfrac Well Services Ltd. 8

Canada – Market Update

United States Operations

U.S. Fleet: 611,000 Horsepower

11 Cementing Crews

5 Coiled Tubing Crews

© Calfrac Well Services Ltd. 9

Calfrac Market Positioning

Focus on customers that are financially strong and intend to remain active in key plays across the U.S.

Positioned in key areas of frac demand:

– Bakken, Marcellus, Rockies, Utica, Eagle Ford

– ~90% of work is 24-hour operations

Pricing & Utilization

Pricing largely stabilized but remains down ~40% from peak

~60% of horsepower parked

Temporarily suspended coiled tubing and cementing operations

Market Trends

Stages per well increasing

Frac spacing tightening

Market Outlook

U.S. land rig count troughed and has

started to rebound

Recent customer inquiries about increasing

activity is encouraging

Visibility for Q4/16 is limited

United States – Market Update

© Calfrac Well Services Ltd. 10

Neuquén, Argentina Frac Operation (2014). Calfrac Well Services Photo

© Calfrac Well Services Ltd. 11

Latin America Operations

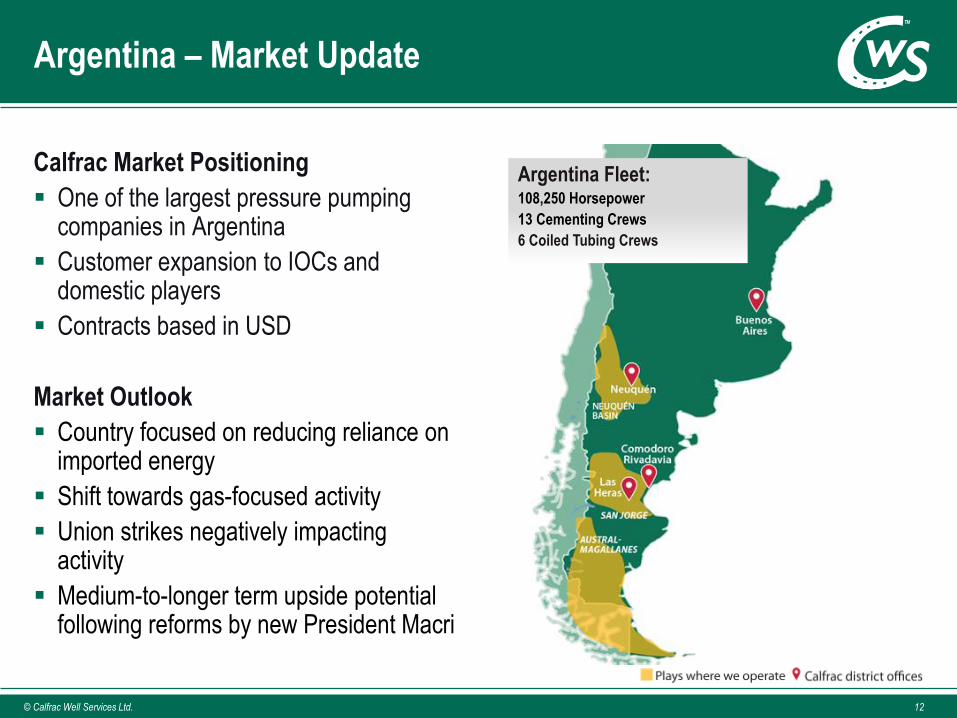

Calfrac Market Positioning

One of the largest pressure pumping companies in Argentina

Customer expansion to IOCs and domestic players

Contracts based in USD

Market Outlook

Country focused on reducing reliance on imported energy

Shift towards gas-focused activity

Union strikes negatively impacting activity

Medium-to-longer term upside potential following reforms by new President Macri

Argentina – Market Update

Argentina Fleet: 108,250 Horsepower

13 Cementing Crews

6 Coiled Tubing Crews

© Calfrac Well Services Ltd. 12

Calfrac Market Positioning

Long-term opportunity due to

Mexican energy industry reforms

– Low oil prices will limit

immediate impact

Round One tenders are ongoing

Market Outlook

Limited near-term activity

Right-sized business to reflect

current activity levels

Mexico – Market Update

© Calfrac Well Services Ltd. 13

Mexico Fleet: 22,500 Horsepower

1 Cementing Crew

1 Coiled Tubing Crew

Russian Operations

Russia Fleet: 7 Fracturing Spreads

70,000 Horsepower

7 Coiled Tubing Crews

© Calfrac Well Services Ltd. 14

Calfrac Market Positioning

Horizontal fracturing in conventional reservoirs is a significant amount of Calfrac’s activity

Rouble devaluation has negatively impacted reported financial results

Russia – Market Update

© Calfrac Well Services Ltd. 15

Russia Fracturing Crew (2015). Calfrac Well Services Photo

Market Outlook

2016 activity expected to be down

modestly from 2015

Change in customer mix

Introduction of multi-stage annular

fracture treatments is a market

differentiator

LICENSE TO OPERATE

Committed To Safety, Quality And Flawless Execution

© Calfrac Well Services Ltd. 16

Our License to Operate

Plan ▪ Do ▪ Assess ▪ Adjust HSE

QUALITY

SUPPLY CHAIN Evaluate ▪ Negotiate ▪ Finalize ▪ Implement

Monitor ▪ Refine ▪ Execute ▪ Improve

Calfrac employee on a Canadian hydraulic fracturing job. Calfrac Well Services Photo

TECHNOLOGY Research ▪ Develop ▪ Test ▪ Refine

Calfrac sand terminal in Whitecourt, Alberta. Calfrac Well Services Photo

© Calfrac Well Services Ltd. 17

NAVIGATING THROUGH THE DOWNTURN

© Calfrac Well Services Ltd. 18

© Calfrac Well Services Ltd. 19

Margin Erosion To Below Breakeven

Source: Company Reports, Morgan Stanley

© Calfrac Well Services Ltd. 20

North American Pressure Pumping Supply

Number of competitors decreasing through both bankruptcies and consolidation

Supply of horsepower decreasing as a result of cannibalization of equipment, lack of R&M and fleet retirements

Expect ~5-6 million horsepower to permanently exit the U.S. pumping

market (~30% of peak supply)

Expect Canadian supply to decrease by ~200k HHP

Fracturing Operation (2015) Calfrac Well Services Photo

Service Line Strategy

– Equipment has been idled when operating margins do not meet the company’s return requirements

Utilization and Maintenance Planning

– More efficient equipment utilization and maintenance schedules

– Unnecessary discretionary spending has been eliminated

Logistics and Supplier Initiatives

– Transload facilities in key locations and increase in rail car fleet

– Supplier costs have been reduced

Working Capital

– Focus has been on improving working capital management

– Maintaining lower levels of inventory (sand, chemicals and spare parts) in line with expected work

programs

Workforce & Fixed Cost Optimization

– Meaningfully reduced field workforce in Canada and the U.S. since January 2015

– In Canada, transportation and majority of fracturing and coiled tubing groups transitioned to variable pay

© Calfrac Well Services Ltd. 21

Managing The Downturn

Strong management team and Board of Directors that have been through multiple downturns

Optimized cost structure and developed operational efficiencies

Maintained core customer and supplier relationships

Strong existing employee base and recruiting capabilities

Well maintained equipment – initial fleet reactivations require minimal time and cost

“License To Operate” upheld through downturn

Proceeds from second lien term loan and undrawn credit facilities provide the liquidity needed to fund incremental working capital requirements associated with a recovery

© Calfrac Well Services Ltd. 22

Positioned For Recovery

© Calfrac Well Services Ltd. 23

Service Intensity Continues To Increase

Source: Rystad Energy, Morgan Stanley

FINANCIAL HIGHLIGHTS

© Calfrac Well Services Ltd. 24

Term Debt

US$600 mm with an interest rate of 7.5%

Matures in 2020

Second Lien Term Loan

$200 mm with an interest rate of 9%

Matures in 2020

Credit Facilities

Loan facility $300 mm (largely undrawn)

Matures in 2018

Capital Program

2016 capital budget set at $40 million – Includes $30 mm of carryover

© Calfrac Well Services Ltd. 25

The Balance Sheet

Neuquén, Argentina Frac Operation (2014). Calfrac Well Services Photo

APPENDIX

© Calfrac Well Services Ltd. 26

Introduction of Equity Cure:

– Applicable up to December 31, 2017

– Not to exceed the greater of 50% of total EBITDA over the prior twelve month period

or $25 million per cure

– Positively impacts both EBITDA and Funded Debt

– Can be utilized twice during period of covenant relief

– Can not be utilized in consecutive quarters

The Total Debt to Capitalization ratio removed

Funded Debt to Capitalization ratio introduced - 30% (does not include Calfrac’s

unsecured senior notes or second lien term loan)

© Calfrac Well Services Ltd. 27

Relaxation Of Covenants (Credit Facility)

Funded Debt/EBITDA covenant amendments including two periods of waivers

On June 10, 2016, AIMCo provided Calfrac a $200 million second lien senior secured term loan facility maturing in September 2020.

– 9% interest rate paid quarterly with option to pay interest “in kind” at 12% rate (8 quarters max)

– ~6.9 mm warrants were issued to AIMCo priced at $4.14/share exercisable prior to June 10, 2019

The proceeds of the term loan will be used by Calfrac for working capital needs and general corporate purposes, including:

– Repayment of all of Calfrac’s current bank indebtedness under its syndicated revolving credit facility and all borrowings of Calfrac Well Services (Argentina) S.A.

Positions Calfrac to assess opportunities to repurchase some of its unsecured senior notes due 2020

– Currently limited to $200 million

– Subject to a minimum liquidity requirement of $100 million

– Repurchase of notes must result in a reduction of annual net interest costs (dollar for dollar basis)

Following this financing, Calfrac still has $200 million of second lien capacity.

Overall, this financing leaves Calfrac well-positioned to navigate this period of market weakness and capitalize on the opportunities expected to arise as market conditions recover.

© Calfrac Well Services Ltd. 28

Second Lien Term Loan

Recommended

![COMPUTERSHARE TRUST COMPANY OF CANADAcalfrac.investorroom.com/download/Calfrac+-+Shareholder+Rights+… · COMPUTERSHARE TRUST COMPANY OF CANADA Dated as of [ ]1, 2020 1 ... 2.5 Execution,](https://img.dokumen.tips/doc/110x75/601a6821e12e5e0c597f55e3/computershare-trust-company-of-shareholderrights-computershare-trust-company.jpg)