Priorsforthelongrun

Giannone,Lenza,Prim iceri Priors for the long run

Domenico GiannoneNewYorkFed

MicheleLenzaEuropeanCentralBank

GiorgioPrimiceriNorthwesternUniversity

9th ECB Workshop on Forecasting TechniquesJune3,2016

Giannone,Lenza,Prim iceri Priors for the long run

Whatwedo

n ProposeaclassofpriordistributionsforVARsthatdisciplinethelong-runimplicationsofthemodel

Priorsforthelongrun

Giannone,Lenza,Prim iceri Priors for the long run

Whatwedo

n ProposeaclassofpriordistributionsforVARsthatdisciplinethelong-runimplicationsofthemodel

Priorsforthelongrun

n PropertiesØ BasedonmacroeconomictheoryØ Conjugateà Easy toimplement andcombinewithexistingpriors

n Performwell inapplicationsØ Good(long-run)forecastingperformance

Giannone,Lenza,Prim iceri Priors for the long run

Outline

n Aspecificpathologyof(flat-prior)VARsØ Toomuchexplanatorypowerofinitialconditionsanddeterministic trendsØ Sims(1996and2000)

n PriorsforthelongrunØ IntuitionØ Specificationandimplementation

n Alternativeinterpretationsandrelationwiththeliterature

n Application:macroeconomicforecasting

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

€

yt = c + ρyt−1 +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

n Iteratebackwards:

€

yt = c + ρyt−1 +ε t

€

yt = ρ t y0 + ρ jcj=0

t−1∑ + ρ jε t− jj=0

t−1∑

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

n Iteratebackwards:

➠ModelseparatesobservedvariationofthedataintoØ DC:deterministic component,predictablefromdataattime0Ø SC:unpredictable/stochastic component

€

yt = c + ρyt−1 +ε t

€

yt = ρ t y0 + ρ jcj=0

t−1∑ + ρ jε t− jj=0

t−1∑

SCDC

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

n Iteratebackwards:

➠ModelseparatesobservedvariationofthedataintoØ DC:deterministic component,predictablefromdataattime0Ø SC:unpredictable/stochastic component

n Ifρ =1,DCisasimplelineartrend:

€

yt = c + ρyt−1 +ε t

€

yt = ρ t y0 + ρ jcj=0

t−1∑ + ρ jε t− jj=0

t−1∑

€

DC = y0 + c⋅ t

SCDC

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

n Iteratebackwards:

➠ModelseparatesobservedvariationofthedataintoØ DC:deterministic component,predictablefromdataattime0Ø SC:unpredictable/stochastic component

n Ifρ =1,DCisasimplelineartrend:

n Otherwisemorecomplex:

€

yt = c + ρyt−1 +ε t

€

yt = ρ t y0 + ρ jcj=0

t−1∑ + ρ jε t− jj=0

t−1∑

€

DC = y0 + c⋅ t

€

DC =c

1− ρ+ ρ t y0 −

c1− ρ

$

% &

'

( )

SCDC

Giannone,Lenza,Prim iceri Priors for the long run

Pathologyof(flat-prior)VARs(Sims,1996and2000)

n OLS/MLEhasatendencyto“use”thecomplexityofdeterministiccomponentstofitthelowfrequencyvariationinthedata

n Possiblebecauseinferenceistypicallyconditionalony0Ø Nopenalizationforparameterestimates ofimplyingsteadystates ortrendsfar

awayfrominitialconditions

Giannone,Lenza,Prim iceri Priors for the long run

DeterministiccomponentsinVARs

n ProblemmoreseverewithVARsØ implieddeterministic component ismuchmorecomplexthaninAR(1)case

Giannone,Lenza,Prim iceri Priors for the long run

DeterministiccomponentsinVARs

n ProblemmoreseverewithVARsØ implieddeterministic component ismuchmorecomplexthaninAR(1)case

n Example:7-variableVAR(5)withquarterlydataonØ GDPØ ConsumptionØ InvestmentØ RealWagesØ HoursØ InflationØ Federalfundsrate

n Sample:1955:I– 1994:IV

n FlatorMinnesotaprior

Giannone,Lenza,Prim iceri Priors for the long run

“Over-fitting”ofdeterministiccomponentsinVARs

1960 1980 2000

5.55.65.75.85.9

66.16.26.36.4

GDP

1960 1980 20003.9

44.14.24.34.44.54.64.7

Investment

1960 1980 2000

-0.65

-0.6

-0.55

-0.5

Hours

1960 1980 2000

-1.7-1.65

-1.6-1.55

-1.5-1.45

-1.4-1.35

-1.3-1.25

Investment-to-GDP ratio

1960 1980 2000-0.015

-0.01-0.005

00.005

0.010.015

0.020.025

Inflation

1960 1980 2000

-0.01

0

0.01

0.02

0.03

0.04

Interest rate

Data Flat MN PLR

Giannone,Lenza,Prim iceri Priors for the long run

“Over-fitting”ofdeterministiccomponentsinVARs

1960 1980 2000

5.55.65.75.85.9

66.16.26.36.4

GDP

1960 1980 20003.9

44.14.24.34.44.54.64.7

Investment

1960 1980 2000

-0.65

-0.6

-0.55

-0.5

Hours

1960 1980 2000

-1.7-1.65

-1.6-1.55

-1.5-1.45

-1.4-1.35

-1.3-1.25

Investment-to-GDP ratio

1960 1980 2000-0.015

-0.01-0.005

00.005

0.010.015

0.020.025

Inflation

1960 1980 2000

-0.01

0

0.01

0.02

0.03

0.04

Interest rate

Data Flat MN PLR

Giannone,Lenza,Prim iceri Priors for the long run

Pathologyof(flat-prior)VARs(Sims,1996and2000)

n OLS/MLEhasatendencyto“use”thecomplexityofdeterministiccomponentstofitthelowfrequencyvariationinthedata

n Possiblebecauseinferenceistypicallyconditionalony0Ø Nopenalizationforparameterestimates ofimplyingsteadystates ortrendsfar

awayfrominitialconditions

➠Flat-priorVARsattributean(implausibly) largeshareofthelowfrequencyvariationinthedatatodeterministiccomponents

Giannone,Lenza,Prim iceri Priors for the long run

Pathologyof(flat-prior)VARs(Sims,1996and2000)

n OLS/MLEhasatendencyto“use”thecomplexityofdeterministiccomponentstofitthelowfrequencyvariationinthedata

n Possiblebecauseinferenceistypicallyconditionalony0Ø Nopenalizationforparameterestimates ofimplyingsteadystates ortrendsfar

awayfrominitialconditions

➠Flat-priorVARsattributean(implausibly) largeshareofthelowfrequencyvariationinthedatatodeterministiccomponents

n Needapriorthatdownplaysexcessiveexplanatorypowerofinitialconditionsanddeterministiccomponent

n Onesolution:centerprioron“non-stationarity”

Giannone,Lenza,Prim iceri Priors for the long run

Outline

n Aspecificpathologyof(flat-prior)VARsØ Toomuchexplanatorypowerofinitialconditionsanddeterministic trendsØ Sims(1996and2000)

n PriorsforthelongrunØ IntuitionØ Specificationandimplementation

n Alternativeinterpretationsandrelationwiththeliterature

n Application:macroeconomicforecasting

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

€

VAR(1) : yt = c + Byt−1 +ε t , ε t ~ N 0,Σ( )

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n RewritetheVARintermsoflevelsanddifferences:

€

VAR(1) : yt = c + Byt−1 +ε t , ε t ~ N 0,Σ( )

€

Δyt = c +Πyt−1 +ε tΠ = B − I

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n RewritetheVARintermsoflevelsanddifferences:

n Priorforthelongrun prioroncenteredat0

€

VAR(1) : yt = c + Byt−1 +ε t , ε t ~ N 0,Σ( )

€

Δyt = c +Πyt−1 +ε tΠ = B − I

€

Π

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n RewritetheVARintermsoflevelsanddifferences:

n Priorforthelongrun prioroncenteredat0

n Standardapproach(DLS,SZ,andmanyfollowers)Ø Pushcoefficientstowardsallvariablesbeingindependentrandomwalks

€

VAR(1) : yt = c + Byt−1 +ε t , ε t ~ N 0,Σ( )

€

Δyt = c +Πyt−1 +ε tΠ = B − I

€

Π

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n Rewriteas

€

Δyt = c +Πyt−1 +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n Rewriteas

n ChooseH andputprioronΛ conditionalonH

€

Δyt = c +Πyt−1 +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n Rewriteas

n ChooseH andputprioronΛ conditionalonH

n Economictheorysuggeststhatsomelinearcombinationsofy areless(more)likelytoexhibitlong-runtrends

€

Δyt = c +Πyt−1 +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n Rewriteas

n ChooseH andputprioronΛ conditionalonH

n Economictheorysuggeststhatsomelinearcombinationsofy areless(more)likelytoexhibitlong-runtrends

n Loadingsassociatedwiththesecombinationsareless(more)likelytobe0

€

Δyt = c +Πyt−1 +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

ΔxtΔctΔit

#

$

% % %

&

'

( ( (

= c +

Λ11 Λ12 Λ13

Λ21 Λ22 Λ23

Λ31 Λ32 Λ33

#

$

% % %

&

'

( ( (

xt−1 + ct−1 + it−1

ct−1 − xt−1

it−1 − xt−1

#

$

% % %

&

'

( ( ( +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

ΔxtΔctΔit

#

$

% % %

&

'

( ( (

= c +

Λ11 Λ12 Λ13

Λ21 Λ22 Λ23

Λ31 Λ32 Λ33

#

$

% % %

&

'

( ( (

xt−1 + ct−1 + it−1

ct−1 − xt−1

it−1 − xt−1

#

$

% % %

&

'

( ( ( +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Possibly stationary linear combinations

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

ΔxtΔctΔit

#

$

% % %

&

'

( ( (

= c +

Λ11 Λ12 Λ13

Λ21 Λ22 Λ23

Λ31 Λ32 Λ33

#

$

% % %

&

'

( ( (

xt−1 + ct−1 + it−1

ct−1 − xt−1

it−1 − xt−1

#

$

% % %

&

'

( ( ( +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Common trend

Possibly stationary linear combinations

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

ΔxtΔctΔit

#

$

% % %

&

'

( ( (

= c +

Λ11 Λ12 Λ13

Λ21 Λ22 Λ23

Λ31 Λ32 Λ33

#

$

% % %

&

'

( ( (

xt−1 + ct−1 + it−1

ct−1 − xt−1

it−1 − xt−1

#

$

% % %

&

'

( ( ( +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Common trend

Possibly stationary linear combinations

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

n ConjugateØ Canimplement itwithTheilmixedestimation intheVARinlevels

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

n ConjugateØ Canimplement itwithTheilmixedestimation intheVARinlevelsØ Canbeeasilycombinedwithexistingpriors

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

n ConjugateØ Canimplement itwithTheilmixedestimation intheVARinlevelsØ CanbeeasilycombinedwithexistingpriorsØ CancomputetheMLinclosedform

n Usefulforhierarchicalmodelingandsettingofhyperparameters ϕ (GLP,2013)

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVAR

n ForecastingØ 3-variableVARØ 5-variableVARØ 7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

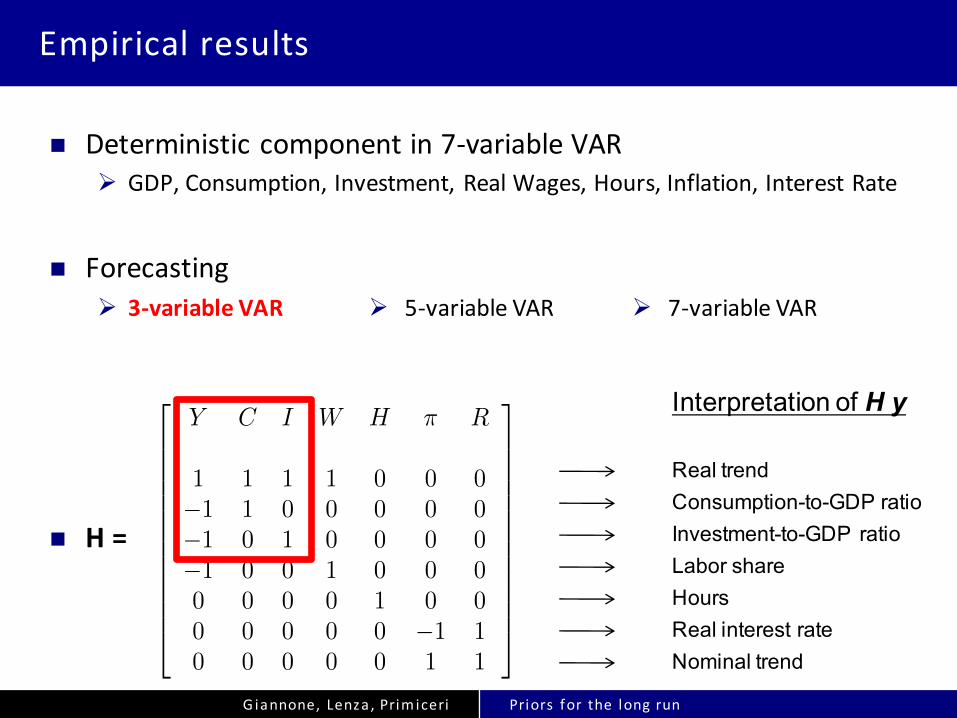

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

n H=

Real trendConsumption-to-GDP ratioInvestment-to-GDP ratioLabor shareHoursReal interest rateNominal trend

Interpretation of H y2

6666666666664

Y C I W H ⇡ R

1 1 1 1 0 0 0�1 1 0 0 0 0 0�1 0 1 0 0 0 0�1 0 0 1 0 0 00 0 0 0 1 0 00 0 0 0 0 �1 10 0 0 0 0 1 1

3

7777777777775

1

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

n ForecastingØ 3-variableVAR

n H=

Real trendConsumption-to-GDP ratioInvestment-to-GDP ratioLabor shareHoursReal interest rateNominal trend

Interpretation of H y2

6666666666664

Y C I W H ⇡ R

1 1 1 1 0 0 0�1 1 0 0 0 0 0�1 0 1 0 0 0 0�1 0 0 1 0 0 00 0 0 0 1 0 00 0 0 0 0 �1 10 0 0 0 0 1 1

3

7777777777775

1

Ø 5-variableVAR Ø 7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

n ForecastingØ 3-variableVAR

n H=

Real trendConsumption-to-GDP ratioInvestment-to-GDP ratioLabor shareHoursReal interest rateNominal trend

Interpretation of H y2

6666666666664

Y C I W H ⇡ R

1 1 1 1 0 0 0�1 1 0 0 0 0 0�1 0 1 0 0 0 0�1 0 0 1 0 0 00 0 0 0 1 0 00 0 0 0 0 �1 10 0 0 0 0 1 1

3

7777777777775

1

Ø 5-variableVAR Ø 7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

n ForecastingØ 3-variableVAR

n H=

Real trendConsumption-to-GDP ratioInvestment-to-GDP ratioLabor shareHoursReal interest rateNominal trend

Interpretation of H y2

6666666666664

Y C I W H ⇡ R

1 1 1 1 0 0 0�1 1 0 0 0 0 0�1 0 1 0 0 0 0�1 0 0 1 0 0 00 0 0 0 1 0 00 0 0 0 0 �1 10 0 0 0 0 1 1

3

7777777777775

1

Ø 5-variableVAR Ø 7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

DeterministiccomponentsinVARs

1960 1980 2000

5.55.65.75.85.9

66.16.26.36.4

GDP

1960 1980 20003.9

44.14.24.34.44.54.64.7

Investment

1960 1980 2000

-0.65

-0.6

-0.55

-0.5

Hours

1960 1980 2000

-1.7-1.65

-1.6-1.55

-1.5-1.45

-1.4-1.35

-1.3-1.25

Investment-to-GDP ratio

1960 1980 2000-0.015

-0.01-0.005

00.005

0.010.015

0.020.025

Inflation

1960 1980 2000

-0.01

0

0.01

0.02

0.03

0.04

Interest rate

Data Flat MN PLR

Giannone,Lenza,Prim iceri Priors for the long run

DeterministiccomponentsinVARswithPriorfortheLongRun

1960 1980 2000

5.5

6

6.5GDP

1960 1980 2000

4

4.2

4.4

4.6

4.8

5Investment

1960 1980 2000

-0.65

-0.6

-0.55

-0.5

Hours

1960 1980 2000

-1.7-1.65

-1.6-1.55

-1.5-1.45

-1.4-1.35

-1.3-1.25

Investment-to-GDP ratio

1960 1980 2000-0.015

-0.01-0.005

00.005

0.010.015

0.020.025

Inflation

1960 1980 2000

-0.01

0

0.01

0.02

0.03

0.04

Interest rate

Data Flat MN PLR

Giannone,Lenza,Prim iceri Priors for the long run

Forecastingresultswith3-,5- and7-variableVARs

n Recursiveestimationstartsin1955:I

n Forecast-evaluationsample:1985:I– 2013:I

Giannone,Lenza,Prim iceri Priors for the long run

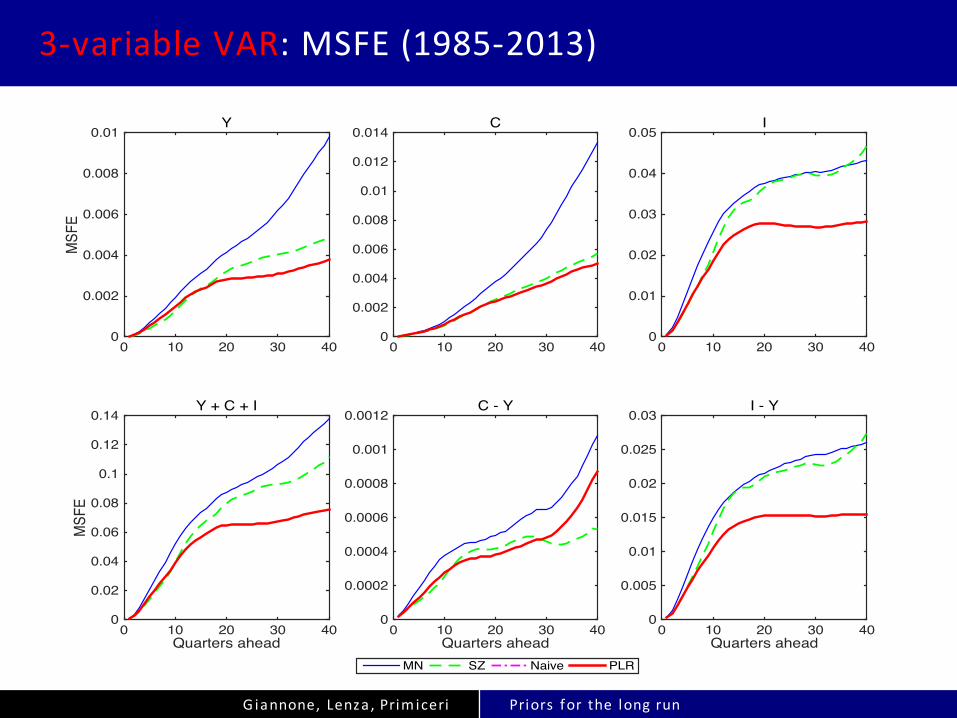

3-variableVAR:MSFE(1985-2013)

0 10 20 30 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01Y

Quarters ahead0 10 20 30 40

MSF

E

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14Y + C + I

0 10 20 30 40 0

0.002

0.004

0.006

0.008

0.01

0.012

0.014C

Quarters ahead0 10 20 30 40

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012C - Y

0 10 20 30 40 0

0.01

0.02

0.03

0.04

0.05

0

0.01

0.02

0.03I

Quarters ahead0 10 20 30 40

0

0.005

0.01

0.015

0.02

0.025

0.03I - Y

MN SZ Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

3-variableVAR:MSFE(1985-2013)

0 10 20 30 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01Y

Quarters ahead0 10 20 30 40

MSF

E

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14Y + C + I

0 10 20 30 40 0

0.002

0.004

0.006

0.008

0.01

0.012

0.014C

Quarters ahead0 10 20 30 40

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012C - Y

0 10 20 30 40 0

0.01

0.02

0.03

0.04

0.05I

Quarters ahead0 10 20 30 40

0

0.005

0.01

0.015

0.02

0.025

0.03I - Y

MN SZ Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

Consumption- andInvestment-to-GDPratios

1960 1970 1980 1990 2000 2010-0.65

-0.6

-0.55

-0.5

C - Y

1960 1970 1980 1990 2000 2010-1.7

-1.6

-1.5

-1.4

-1.3

I - Y

Actual Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

Forecasts(5yearsahead)

1960 1970 1980 1990 2000 2010-0.65

-0.6

-0.55

-0.5

C - Y

1960 1970 1980 1990 2000 2010-1.7

-1.6

-1.5

-1.4

-1.3

I - Y

Actual Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

Forecasts(5yearsahead)

1960 1970 1980 1990 2000 2010-0.65

-0.6

-0.55

-0.5

C - Y

1960 1970 1980 1990 2000 2010-1.7

-1.6

-1.5

-1.4

-1.3

I - Y

Actual Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

5-variableVAR:MSFE(1985-2013)

0 10 20 30 40

MSF

E

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008Y

0 10 20 30 40M

SFE

0

0.002

0.004

0.006

0.008

0.01

0.012C

0 10 20 30 40

MSF

E

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08I

Quarters Ahead0 10 20 30 40

MSF

E

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007H

Quarters Ahead0 10 20 30 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01

0.012W

MNSZNaivePLR

Giannone,Lenza,Prim iceri Priors for the long run

7-variableVAR:MSFE(1985-2013)

0 20 40

MSF

E

00.0010.0020.0030.0040.0050.0060.0070.0080.009 0.01

Y

0 20 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014C

0 20 40

MSF

E

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08I

0 20 40

MSF

E

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008

0.009H

Quarters Ahead0 20 40

MSF

E

00.0020.0040.0060.008 0.01

0.0120.0140.0160.018 0.02

W

Quarters Ahead0 20 40

MSF

E

0

2e-05

4e-05

6e-05

8e-05

0.0001

0.00012:

Quarters Ahead0 20 40

MSF

E

0

5e-05

0.0001

0.00015

0.0002

0.00025

0.0003R

MNSZNaivePLR

𝝅

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

n Economictheoryisuseful,butnotsufficienttouniquelypindownHØ Macromodelsaretypically informativeabout𝜷%andsp(𝜷)

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

n Economictheoryisuseful,butnotsufficienttouniquelypindownHØ Macromodelsaretypically informativeabout𝜷%andsp(𝜷)

➠ ExtensionofourPLRthatisinvarianttorotationsof𝜷

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

n Economictheoryisuseful,butnotsufficienttouniquelypindownHØ Macromodelsaretypically informativeabout𝜷%andsp(𝜷)

➠ ExtensionofourPLRthatisinvarianttorotationsof𝜷

BaselinePLR: Λ*+ * 𝐻+*𝑦-. |𝐻, Σ~𝑁 0,𝜙+6Σ , 𝑖 = 1, … ,𝑛

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

n Economictheoryisuseful,butnotsufficienttouniquelypindownHØ Macromodelsaretypically informativeabout𝜷%andsp(𝜷)

➠ ExtensionofourPLRthatisinvarianttorotationsof𝜷

BaselinePLR: Λ*+ * 𝐻+*𝑦-. |𝐻, Σ~𝑁 0,𝜙+6Σ , 𝑖 = 1, … ,𝑛

InvariantPLR: ;Λ*+ * 𝐻+*𝑦-. |𝐻, Σ~𝑁 0,𝜙+6Σ , 𝑖 = 1, … ,𝑛 − 𝑟

∑ Λ*+ * 𝐻+*𝑦-. |𝐻, Σ~𝑁 0,𝜙?@ABC6 Σ?+D?@ABC

Giannone,Lenza,Prim iceri Priors for the long run

7-variableVAR:Forecasting resultswith“invariant”PLR

0 20 40

MS

FE

0

0.002

0.004

0.006

0.008

0.01Y

0 20 40M

SFE

0

0.002

0.004

0.006

0.008

0.01C

0 20 40

MS

FE

0

0.01

0.02

0.03

0.04

0.05I

0 20 40

MS

FE

0

0.002

0.004

0.006

0.008H

0 20 40

MS

FE

0

2e-05

4e-05

6e-05

8e-05

0.0001π

0 20 40M

SFE

0

2e-05

4e-05

6e-05

8e-05

0.0001

0.00012R

Quarters Ahead0 20 40

MS

FE

0

0.0005

0.001

0.0015

0.002

0.0025

0.003C - Y

Quarters Ahead0 20 40

MS

FE

0

0.005

0.01

0.015

0.02

0.025I - Y

Quarters Ahead0 20 40

MS

FE

0

0.0005

0.001

0.0015

0.002W - Y

PLR baseline PLR invariant PLR invariant (except C-Y)

Giannone,Lenza,Prim iceri Priors for the long run

Hy inthedata

1940 1960 1980 2000 2020-0.7

-0.65

-0.6

-0.55

-0.5

-0.45C-Y

1940 1960 1980 2000 2020-1.8

-1.7

-1.6

-1.5

-1.4

-1.3

-1.2I-Y

1940 1960 1980 2000 2020-0.72-0.7-0.68-0.66-0.64-0.62-0.6-0.58-0.56-0.54-0.52

H

1940 1960 1980 2000 2020-0.62

-0.6

-0.58

-0.56

-0.54

-0.52

-0.5W-Y

1940 1960 1980 2000 2020-0.01

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07R+:

1940 1960 1980 2000 2020-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03R-:𝝅 𝝅

Giannone,Lenza,Prim iceri Priors for the long run

7-variableVAR:Forecasting resultswith“invariant”PLR

0 20 40

MS

FE

0

0.002

0.004

0.006

0.008

0.01Y

0 20 40M

SFE

0

0.002

0.004

0.006

0.008

0.01C

0 20 40

MS

FE

0

0.01

0.02

0.03

0.04

0.05I

0 20 40

MS

FE

0

0.002

0.004

0.006

0.008H

0 20 40

MS

FE

0

2e-05

4e-05

6e-05

8e-05

0.0001π

0 20 40M

SFE

0

2e-05

4e-05

6e-05

8e-05

0.0001

0.00012R

Quarters Ahead0 20 40

MS

FE

0

0.0005

0.001

0.0015

0.002

0.0025

0.003C - Y

Quarters Ahead0 20 40

MS

FE

0

0.005

0.01

0.015

0.02

0.025I - Y

Quarters Ahead0 20 40

MS

FE

0

0.0005

0.001

0.0015

0.002W - Y

PLR baseline PLR invariant PLR invariant (except C-Y)

Giannone,Lenza,Prim iceri Priors for the long run

Strengthsandweaknesses

n StrengthsØ Imposesdiscipline onlong-runbehaviorofthemodelØ BasedonrobustlessonsoftheoreticalmacromodelsØ Performswellinforecasting(especially atlongerhorizons)Ø Veryeasytoimplement

Giannone,Lenza,Prim iceri Priors for the long run

Strengthsandweaknesses

n StrengthsØ Imposesdiscipline onlong-runbehaviorofthemodelØ BasedonrobustlessonsoftheoreticalmacromodelsØ Performswellinforecasting(especially atlongerhorizons)Ø Veryeasytoimplement

n “Weak”pointsØ Non-automaticprocedureà needtothinkaboutitØ Mightprovedifficulttosetupinlarge-scalemodelsà mightrequiretoo

muchthinking

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n Rewriteas

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Δyt = c+ Λ1 Λ2[ ] β⊥ 'β '$

%&

'

()yt−1 +εt

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n Rewriteas

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Δyt = c+ Λ1 Λ2[ ] β⊥ 'β '$

%&

'

()yt−1 +εt

Δyt = c+Λ1β⊥ ' yt−1 +Λ2β ' yt−1 +εt

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Giannone,Lenza,Prim iceri Priors for the long run

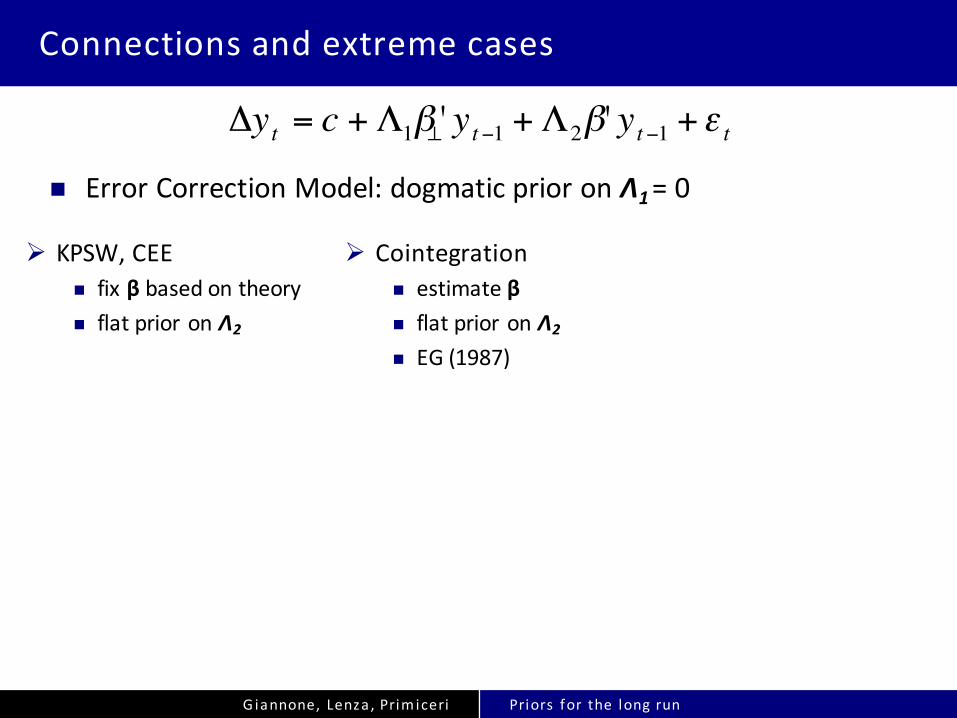

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Ø Cointegrationn estimateβn flatprioronΛ2

n EG(1987)

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø Bayesiancointegrationn uniform prioronsp(β)n KSvDV (2006)

Ø Cointegrationn estimateβn flatprioronΛ2

n EG(1987)

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

n VARinfirstdifferences:dogmaticprioronΛ1=Λ2=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Ø Cointegrationn estimateβn flatprioronΛ2

n EG(1987)

Ø Bayesiancointegrationn uniform prioronsp(β)n KSvDV (2006)

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

n VARinfirstdifferences:dogmaticprioronΛ1=Λ2=0

n Sum-of-coefficientsprior(DLS,SZ)Ø [β’ β’]’ =H=IØ shrinkΛ1 andΛ2 to0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Ø Cointegrationn estimateβn flatprioronΛ2

n EG(1987)

Ø Bayesiancointegrationn uniform prioronsp(β)n KSvDV (2006)

Giannone,Lenza,Prim iceri Priors for the long run

3-varVAR:MeanSquaredForecastErrors(1985-2013)

0 10 20 30 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01Y

Quarters ahead0 10 20 30 40

MSF

E

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14Y + C + I

0 10 20 30 40 0

0.002

0.004

0.006

0.008

0.01

0.012

0.014C

Quarters ahead0 10 20 30 40

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012C - Y

0 10 20 30 40 0

0.01

0.02

0.03

0.04

0.05I

Quarters ahead0 10 20 30 40

0

0.005

0.01

0.015

0.02

0.025

0.03I - Y

MN SZ Naive PLR

Recommended