Monitoring the Insurance Industry

The Costa Rican Experience

OECD-ASSAL Regional Expert SeminarSeptember 26 and 27, 2013

Celia González HaugDirectora, División de Normativa y Autorizaciones

Agenda

Background and recent developments in the Costa Rican insurance market. Context of monitoring and insurance market statistics

Legal frameworkInsurance market monitoring strategyApplicable regulations

Current situation: What do we have?What are we working on to enhance transparency and monitoring of the insurance market?

Background and recent developments in the Costa Rican insurance market

Costa Rican Insurance Market Background

5 years since insurance market openingA unique state agency operated as a monopoly during 84 years, and currently maintains about 90% of the total market share. A limited insurance culture in most of the populationLimited banking and financial inclusion. Sectorial monitoring (banking, insurance, pensions and stocks) coordinated by a single direction board. IFRS adopted for the financial system prior to market opening, with some exceptions approved by the National Supervision Council.Existence of a uniform accounting manual for all supervised institutions in the financial system and information transparency norms established.

PREMIUMS/GDP 1925-20122,43%

2,05%

Source: Hasta 2003, Estudio del mercado de Seguros, Gilberto Arce; 2004 , actualizad by SUGESE

PREMIUMS/GDP & PREMIUMS PER CAPITAAMÉRICA LATINA: PROFUNDIDAD Y DENSIDAD DEL MERCADO DE SEGUROS, 2011.

Profundidad (Primas como % PIB) Densidad (primas per cápita)

Premiums/GDP (average):

2.52% (2009), 2.49% (2010), 2.43% (2011)

Premiums p.c. (average): US$190 (2009), US$204 (2010), US$236 (2011).

Costa Rica: Under the average, but around it. Increasing performance on premiums per capita

is opposed to Latin America’s trend.

Latin America: Premiums/GDP, 2011 Latin America: Premiums P.C., 2011

Year Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Total 83,4 92,8 116,7 137,4 140,5 163,0 172,0 198,9

Compulsory 24,5 29,1 35,8 45,9 37,9 50,2 54,9 61,8

Personal 11,1 13,6 13,2 17,8 20,1 22,1 29,7 40,1

P&C 47,9 50,1 67,8 73,6 82,4 90,7 87,4 97,1

Total 1,85% 1,80% 1,87% 2,14% 2,11% 2,01% 1,94% 2,06%

Compulsory 0,54% 0,56% 0,57% 0,72% 0,57% 0,62% 0,62% 0,64%

Personal 0,25% 0,26% 0,21% 0,28% 0,30% 0,27% 0,33% 0,41%

P&C 1,06% 0,97% 1,08% 1,15% 1,24% 1,12% 0,99% 1,00%

Total Received Premiums Per Capita (US$)

Total Received Premiums / GDP

TOTAL RECEIVED PREMIUMSTotal

Voluntary Insurance

Growing rate (US$)

29% 31% 31% 33% 27% 31% 32% 31%13% 15% 11%13% 14%

14%17%

20%

57%54%

58%54% 59%

56% 51%

49%

0

100

200

300

400

500

600

700

800

900

1.000

Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

US$

Milli

ons

Compulsory Personal P&C

355,8

512,2

743,8

401,5

611,5 633,3

793,9

928,5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Automobile Fire & associate Life Accid, Sickn & Health Other

42%

13%

14%

5%

43%44% 37%

7%4%

24%

7%

13%

26%

6%

12%

15%

27%

14%

13%

44%

12% 12%

22%

12%

12%

25%

46%

13%

41%

7%

37%

18%12%

16%

26% 24% 22%

10% 12%

12%

Insurance Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Total 13% 28% 19% 4% 17% 7% 17%Voluntary 10% 29% 15% 14% 11% 5% 18%Compulsory 21% 25% 30% -16% 34% 11% 14%Personal 25% -2% 37% 14% 11% 36% 36%P&C 6% 37% 10% 13% 11% -3% 12%

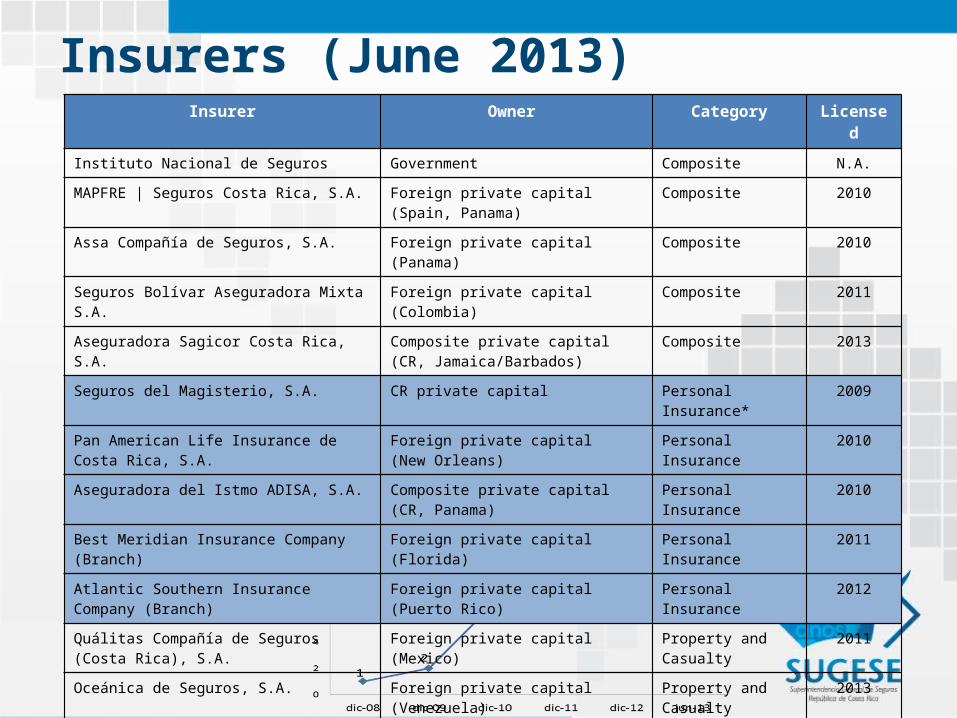

Insurers (June 2013)Insurer Owner Category Licensed

Instituto Nacional de Seguros Government Composite N.A.

MAPFRE | Seguros Costa Rica, S.A. Foreign private capital (Spain, Panama) Composite 2010

Assa Compañía de Seguros, S.A. Foreign private capital (Panama) Composite 2010

Seguros Bolívar Aseguradora Mixta S.A. Foreign private capital (Colombia) Composite 2011

Aseguradora Sagicor Costa Rica, S.A. Composite private capital (CR, Jamaica/Barbados)

Composite 2013

Seguros del Magisterio, S.A. CR private capital Personal Insurance* 2009

Pan American Life Insurance de Costa Rica, S.A. Foreign private capital (New Orleans) Personal Insurance 2010

Aseguradora del Istmo ADISA, S.A. Composite private capital (CR, Panama) Personal Insurance 2010

Best Meridian Insurance Company (Branch) Foreign private capital (Florida) Personal Insurance 2011

Atlantic Southern Insurance Company (Branch) Foreign private capital (Puerto Rico) Personal Insurance 2012

Quálitas Compañía de Seguros (Costa Rica), S.A. Foreign private capital (Mexico) Property and Casualty 2011

Oceánica de Seguros, S.A. Foreign private capital (Venezuela) Property and Casualty 2013

Context of monitoring and insurance market statistics

Context: Legal Framework(1)

Insurer obligations

Provide to SUGESE correct and complete information within the time limits and formalities

required.

Properly carry, accounting or legally required registries.

Define control policies and procedures. Establish accounting, financial, informatics,

communications and internal control systems.

Refer and publish complete and correct information required by

the public.

Context: Legal Framework (2)

Superintendency Functions

Make available to the public all the relevant information about insurance market and insurance

companies activities.

Dictate all other technical or operative rules and guidelines.

Propose general norms for accounting registry and the

preparations and presentation of financial

statements.

Propose accounting manuals to allow the

accounting information to reasonably reflect

the situation.

Information Infrastructure

Solvency Capital

Requirement

SBR

Evaluation Model SBR

Accounting Norm ReformIn force 2014

Integral Solvency ReformIn force 2014 Pilot Scheme

(october 2012 )

Context: Insurance market monitoring strategyt

Context: Applicable Regulations

Accounting Plan for the Insurance

Market

Referral information Standards

Insurer´s Financial Statements Model

Standards.

General Accounting disposition for

Financial System.IFRS Adoption

External Auditor Regulation

Audited Statements publishing norms.

Current situation: What do we have?

Current situation: What do we have?

Information submission through excel files, market´s basic information revelationImplementation of Insurance Supervision System began, for remission, processing and storage of financial and accounting information from insurer companies. Monthly publication of information for the public through website.Availability of financial statements in website.

Audited (annual and intermediate)Monthly summary of financial statements in website

Current situation: What do we have?

Available Information

Accounting Balances-M

(Trial Balance

Financial Statements (T)

Direct premiums, by branch, by

insurer (M)

Clains by branch, by insurer. (M)

Ceded and retroceded reinsurance

information. (M)

solvency and minimum equity information. (M)

Current situation: What do we have?

Current Admonitory for supervisory tasks

• Accounting registry and consistency revision.

• Accounting registry reasonability

• Solvency and minimum capital regimes monitoring.

• Basic indicators construction.

¿What are we working on to enhance transparency and monitoring of the

insurance market?

What are we working on to enhance transparency and monitoring of the insurance market?

Insurance Supervision

System

Early Warning Indicator System

Improve information revelation

for the public

• Charge• Validate• Process• Notify

SUGESE

Insurer

Information Models

Notification

Consultation of Remittance Status

Intermediary Supervision I Intermediary Supervision II Electronic FleManagerial Info. Panel

In Site SupervisionInsurer Supervision

Remittance Procedure

Consultation Procedure

Supervision Procedure

PROCESO GENERACION

INSURANCE SUPERVISION

Web Service

What are we working on to enhance transparency and monitoring of the insurance market?

Stages of Insurance Supervision System (SSS)

1IV T 201

3

• Marketing Channels information (T)• Run off (T)• Production Information: contracts, insured and premiums (T)

2I T

2014

• Accounting Balances (trial balance) (M)• Technical Account by branch(T)• Solvency information detail (M)

3201

4

• Financial Intermediaries Information (T)• Information for equity adequacy(M)

4

2014

• Insurance companies information for Central Bank (national accounts, monetary statistics and Balance of Payments)

What are we working on to enhance transparency and monitoring of the insurance market?

Early Warning Indicator System (SIAT)

• Product generated from the development of the Insurance Supervision System. (SSS)

• System synthesizes indicators of early warning with the one that assesses identified risk areas for monitoring purposes of the insurance company.

• Relevant areas are established: • Capital and debt adequacy.• Management and profitability.• Liquidity and asset management.

What are we working on to enhance transparency and monitoring of the insurance market?

Early Warning Indicator System (SIAT) (1)

Capital and debt adequacy• Total Debt• Financial Debt• Net equity loss gross provision.• Net equity loss net provision. • Gross risk rate• Equity retaining or net risk rate. • Minimum capital index• Capital adequacy index• Capital adequacy index variation

Liquidity and asset management. • Liquidity Ratio• Technical provision coverage.

What are we working on to enhance transparency and monitoring of the insurance market?

Sistema de Indicadores de Alerta Temprana (SIAT) (2)

Management and profitability.• Direct insurance premium growth. • Return on Investements• Return on equity (ROE)• Sinister Index• Expenses index• Combined Ratio • Run off Indicator • Sinister average cost • Liquidation average velocity • Rescue index• Reinsurance Concentration index • Rescue amount divided by average mathematic provision.

Concluding Remarks…

• Costa Rica has many pending statistic tasks and much more to learn.

• The country has sought to establish the basis to build a system of statistics and an integral and adjusted to international practices monitoring.

• Having a proper statistical system will require coordination and negotiation of the Superintendency with the Insurance Industry.

¡THANK YOU!

Recommended