Managing Risk in the Supply Chain

David Simchi-Levi

Joint work with Xin Chen, Victor Martínez-de-Albéniz, Melvyn Sim, Peng Sun

Approaches to Risk Management

2

Economics literatureVon Neumann-Morgenstern utilities

Expected utility E{U(Π)}

Finance literatureCapital Asset Pricing Model (CAPM)

Markowitz Mean-Variance tradeoff E{Π}- kVar{Π}Portfolio Approach

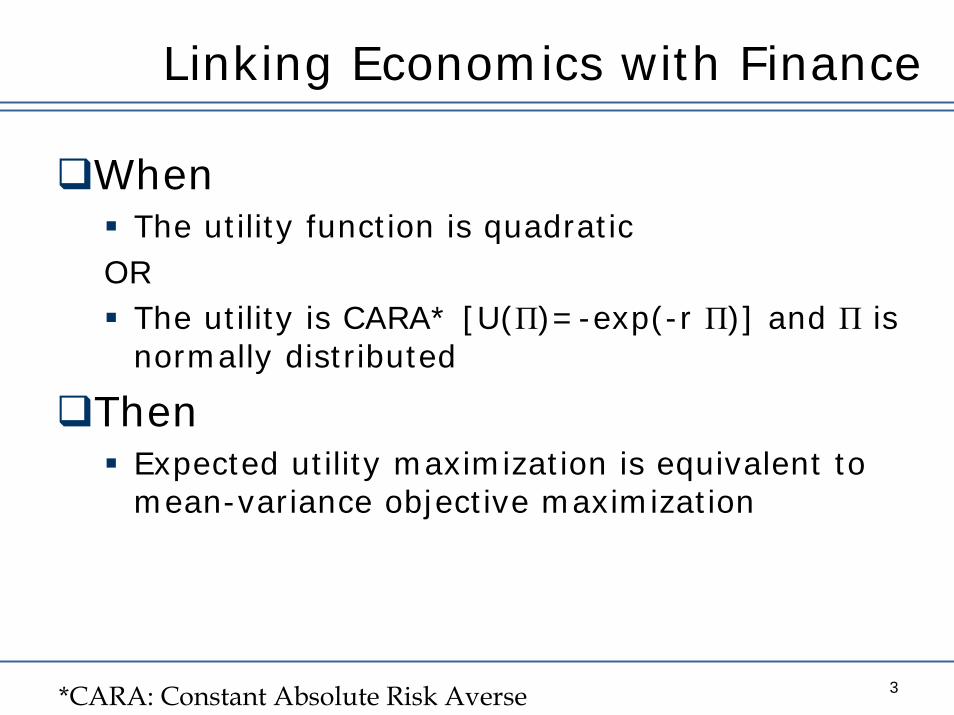

Linking Economics with Finance

3

WhenThe utility function is quadratic

ORThe utility is CARA* [U(Π)=-exp(-r Π)] and Π is normally distributed

ThenExpected utility maximization is equivalent to mean-variance objective maximization

*CARA: Constant Absolute Risk Averse

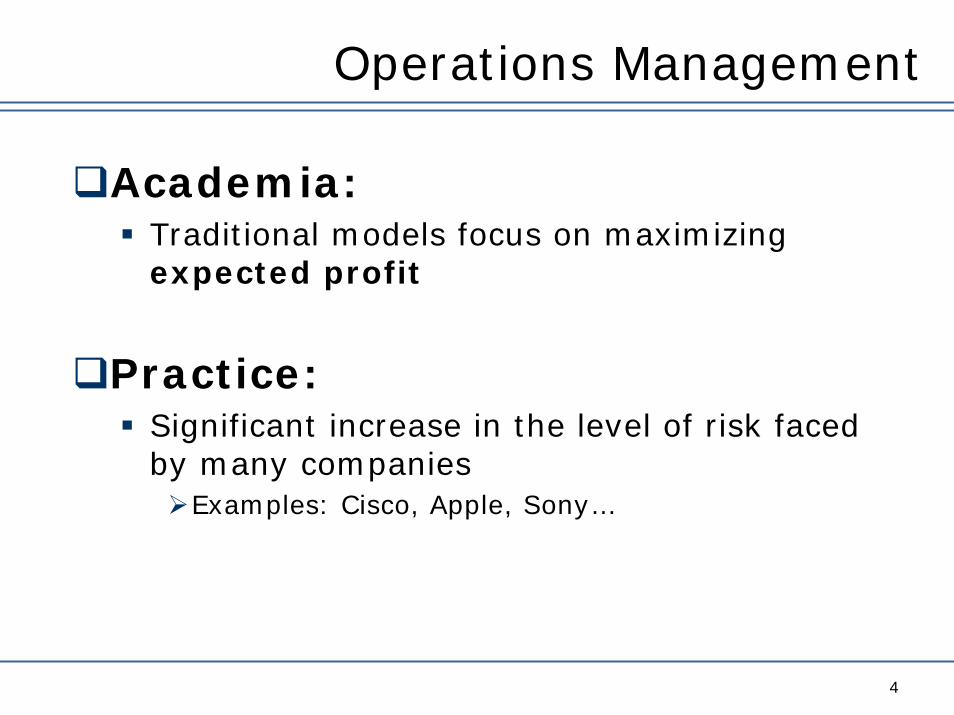

Operations Management

4

Academia:Traditional models focus on maximizing expected profit

Practice:Significant increase in the level of risk faced by many companies

Examples: Cisco, Apple, Sony…

Outline

5

Literature Review

Portfolio Contracts

Risk-Averse Inventory Models

Conclusion

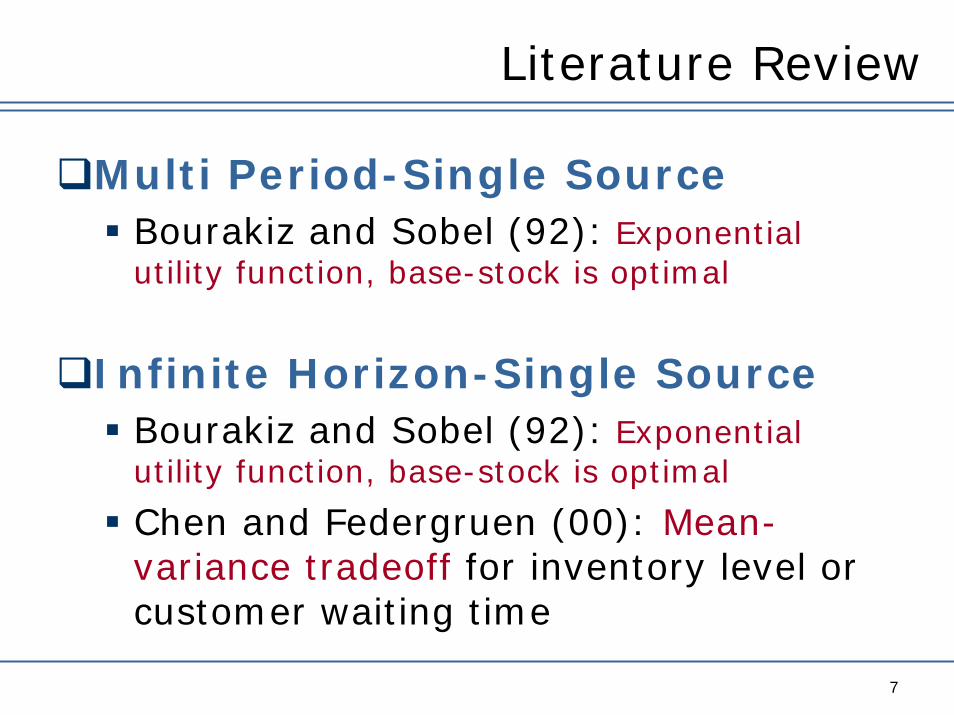

Literature Review

6

Single Period-Single Source

Lau (80): Tradeoff between profit mean and standard deviation

Eeckhoudt, Gollier and Schlesinger (95):Exponential utility function

Chen and Federgruen (00): Mean-variance tradeoff

Schweitzer and Cachon (00): Empirical work

Literature Review

7

Multi Period-Single SourceBourakiz and Sobel (92): Exponential utility function, base-stock is optimal

Infinite Horizon-Single SourceBourakiz and Sobel (92): Exponential utility function, base-stock is optimal

Chen and Federgruen (00): Mean-variance tradeoff for inventory level or customer waiting time

Outline

8

Literature Review

Portfolio Contracts

Risk-Averse Inventory Models

Conclusion

Supplier/manufacturer Relationships

9

Non-strategic components?Supplier selection problemContract optimizationExample: memory for a PC, display for a cell phone

Commodity Procurement

10

Standard componentsMultiple suppliers

Different terms: price, flexibility in orders

Spot market

How should a manufacturer take advantage of these

multiple supply channels to increase earnings?

The Impact of Uncertainty

11

Demand uncertaintyFixed commitment is cheaper but creates high inventory riskFlexible commitment allows to match supply and demand but more expensive

Spot market uncertaintyContracting creates price risk

Modeling Example

12

3 demand scenariosHighest – mean – lowest

Available sourcingFixed commitment contractFlexible commitment contract (or option)Spot market

What should the purchasing strategy be?

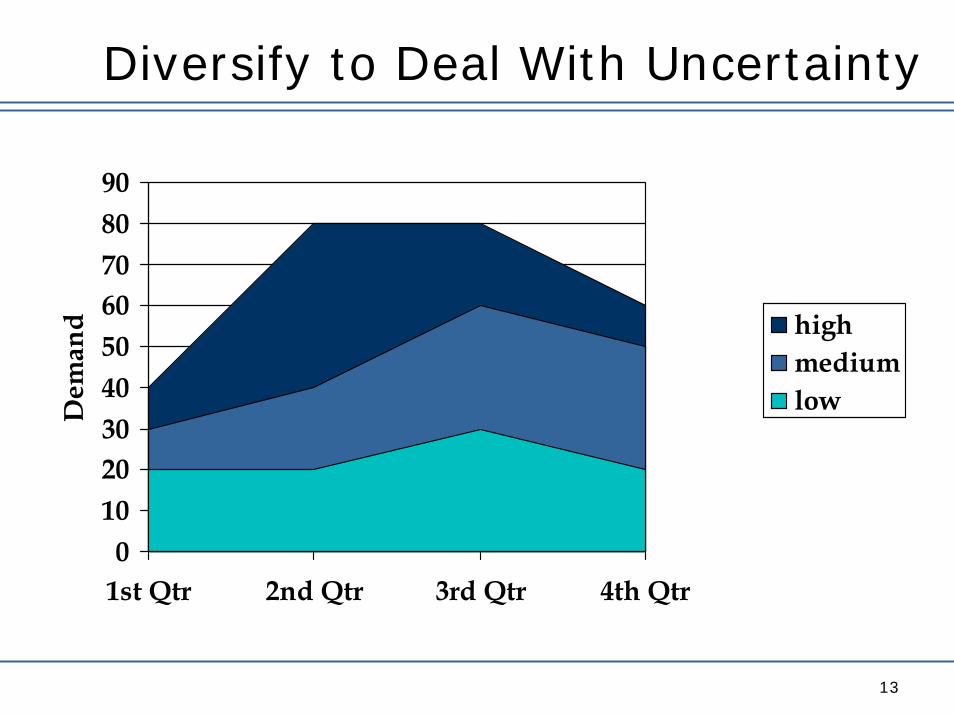

Diversify to Deal With Uncertainty

13

0102030405060708090

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr

Dem

and high

mediumlow

Portfolio Contracts: Outline

14

ModelTwo problems

Optimal replenishment policiesOptimal contract purchasing

Mean-Variance TradeoffSuppliers Competition

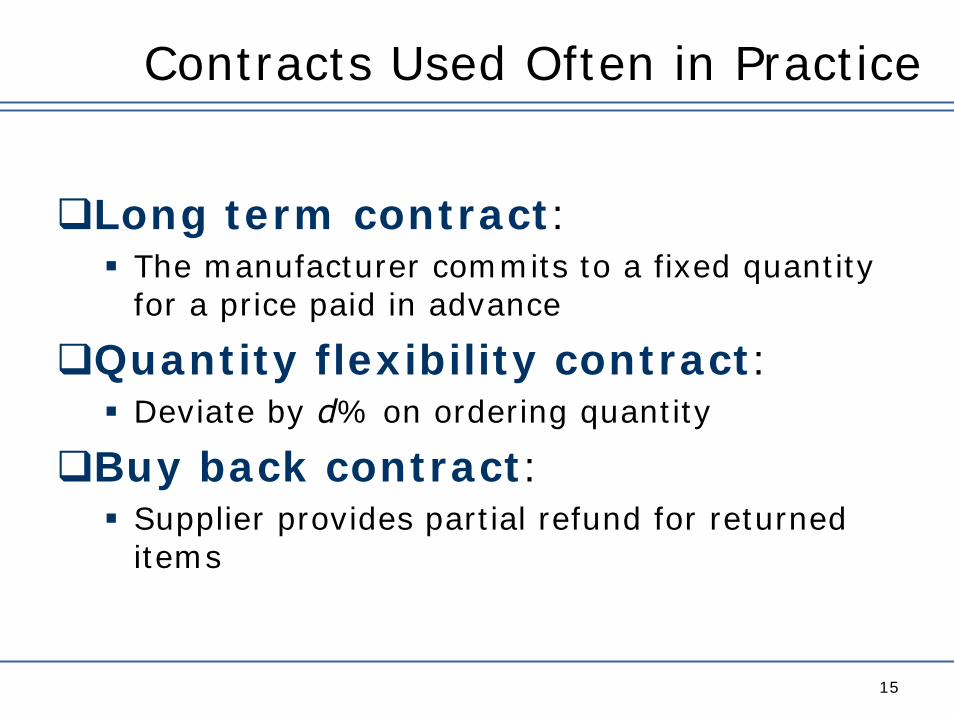

Contracts Used Often in Practice

15

Long term contract:The manufacturer commits to a fixed quantity for a price paid in advance

Quantity flexibility contract:Deviate by d% on ordering quantity

Buy back contract:Supplier provides partial refund for returned items

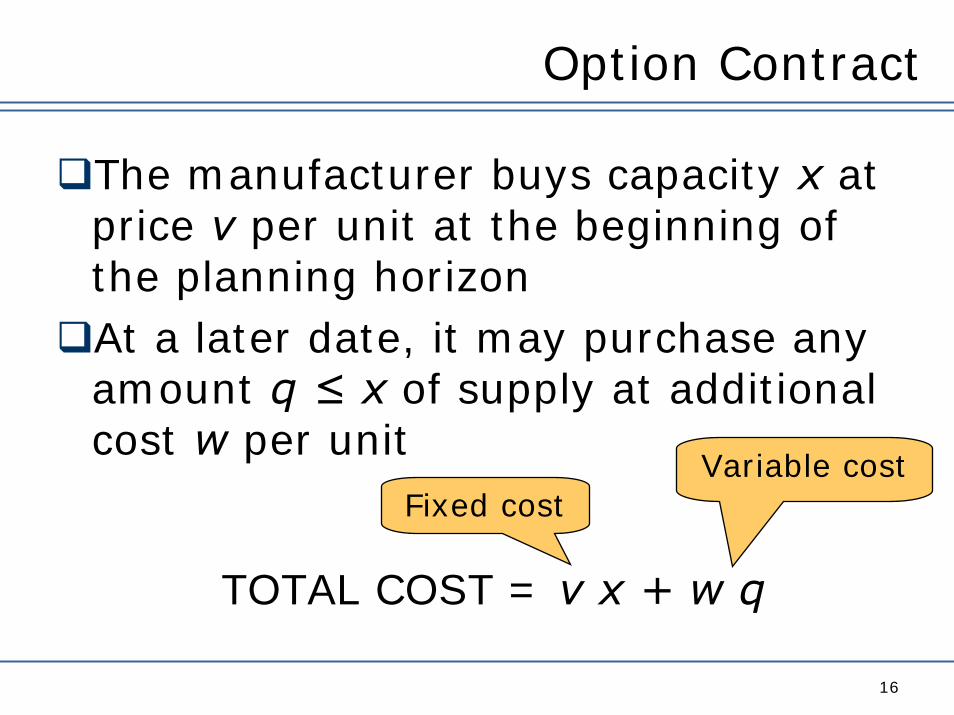

Option Contract

16

The manufacturer buys capacity x at price v per unit at the beginning of the planning horizonAt a later date, it may purchase any amount q ≤ x of supply at additional cost w per unit

TOTAL COST = v x + w q

Fixed costVariable cost

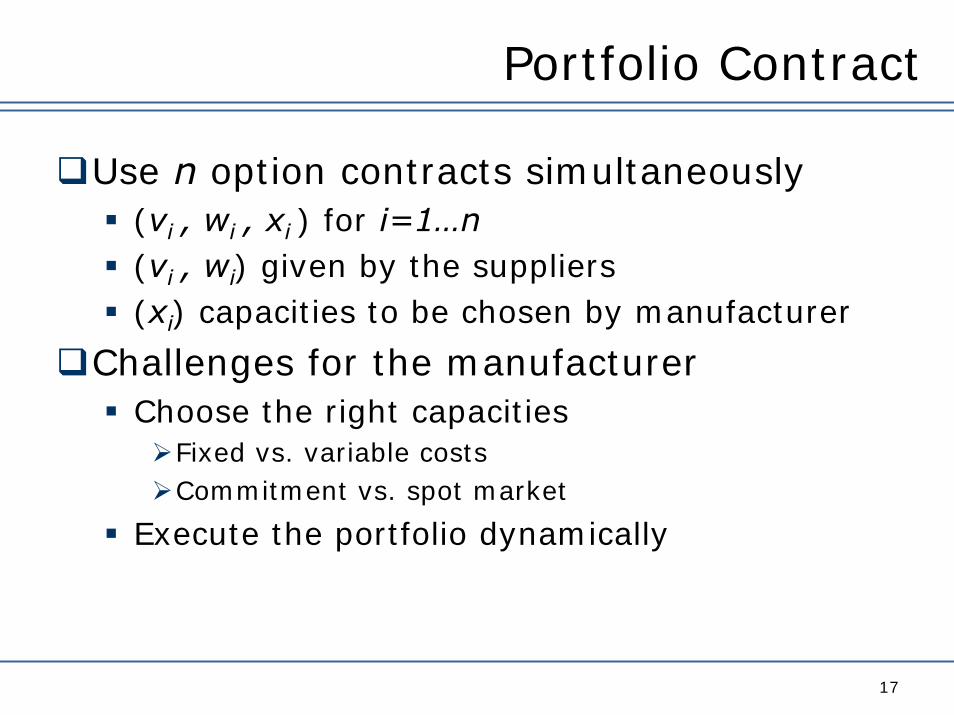

Portfolio Contract

17

Use n option contracts simultaneously(vi , wi , xi ) for i=1…n(vi , wi) given by the suppliers(xi) capacities to be chosen by manufacturer

Challenges for the manufacturerChoose the right capacities

Fixed vs. variable costsCommitment vs. spot market

Execute the portfolio dynamically

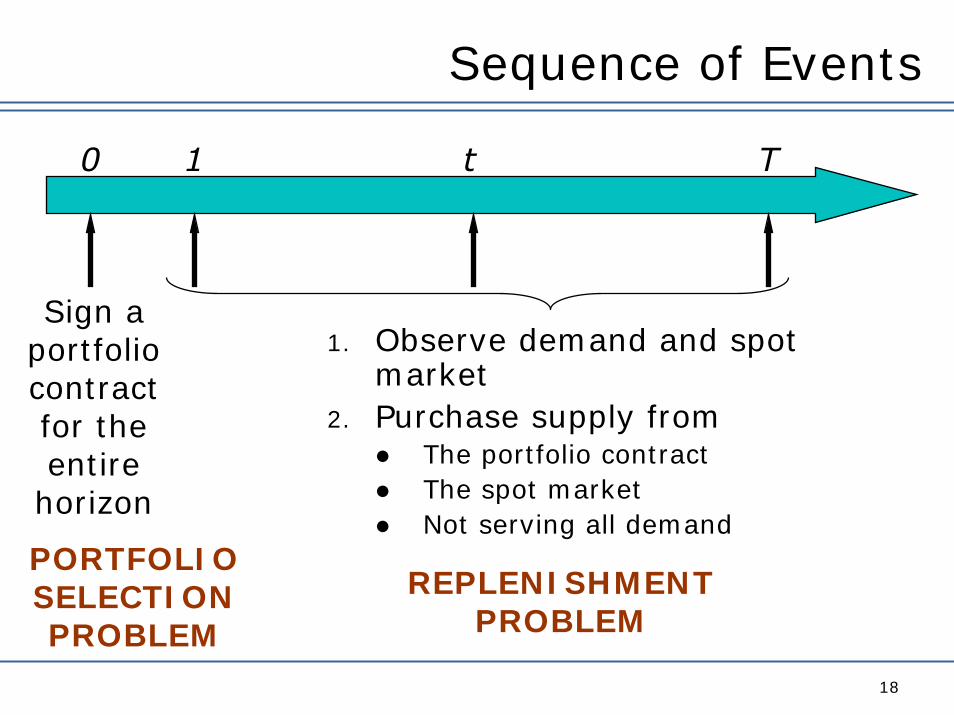

Sequence of Events

18

0 t1 T

Sign a portfolio contract for the entire

horizon

1. Observe demand and spot market

2. Purchase supply fromThe portfolio contractThe spot marketNot serving all demand

PORTFOLIO SELECTION PROBLEM

REPLENISHMENT PROBLEM

The Model

19

Objective: maximize expected profitLost sales modelExogenous pricesConvex inventory holding costsDynamic programming framework

Learning process: more accurate information on future demands and spot prices as time goes by

Spot Market Modeling

20

At every time period, a spot market exists, with random unit cost ct and random capacity κt

Allow correlation between customer demand and spot market conditions

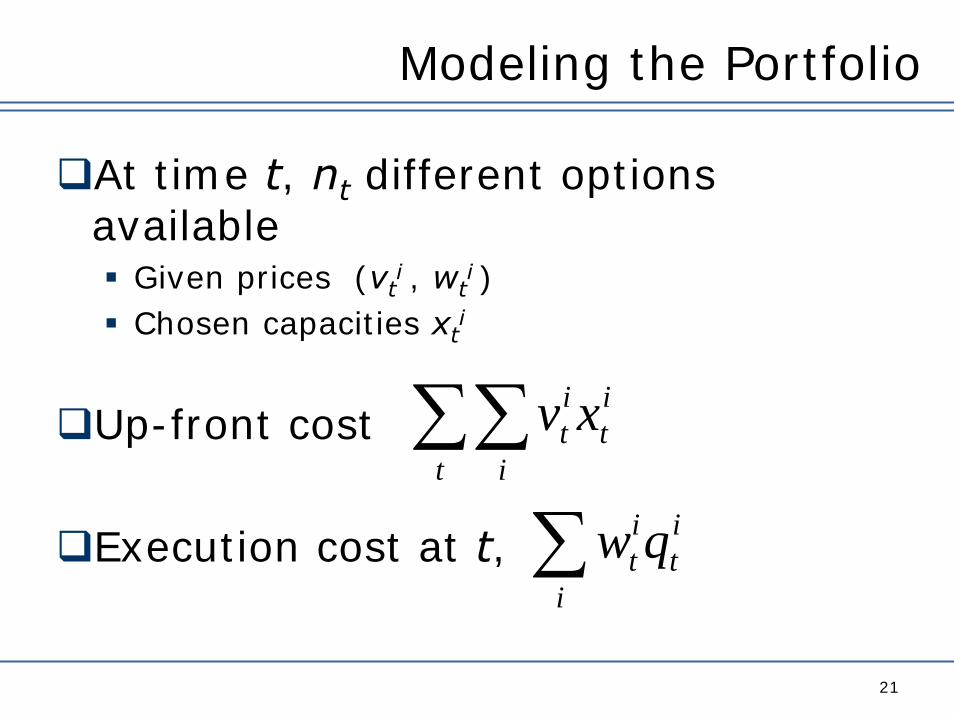

Modeling the Portfolio

21

At time t, nt different options available

Given prices (vti , wt

i )Chosen capacities xt

i

Up-front cost

Execution cost at t,

∑∑t i

it

it xv

∑i

it

it qw

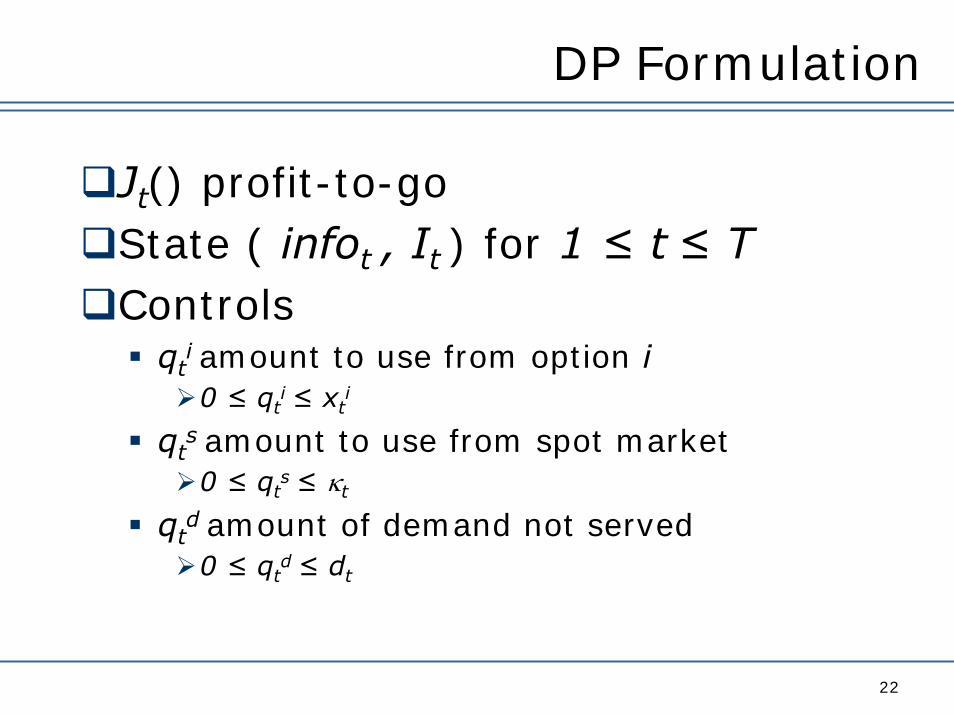

DP Formulation

22

Jt() profit-to-goState ( infot , It ) for 1 ≤ t≤ TControls

qti amount to use from option i0 ≤ qt

i≤ xti

qts amount to use from spot market0 ≤ qt

s≤ κt

qtd amount of demand not served0 ≤ qt

d≤ dt

Characterizing the Profit-to-go

23

TheoremAt each time t, given the present information infot , the profit-to-go, Jt( infot , It ), is concave in It

The Structure of the Optimal Policy

24

TheoremFor each time period t, order the sources such that w1 ≤ …≤ wn.Every source is used following a modified base-stock policy

For a source i, find base-stock level Si

Execute qi =0 if Si ≤ ISi – I if Si - xi ≤ I ≤ Si

xi if I ≤ Si -xi

Si+1 ≤ Si - xi

25

Option 1S1=80x1=20

Option 2S2=40x2=10

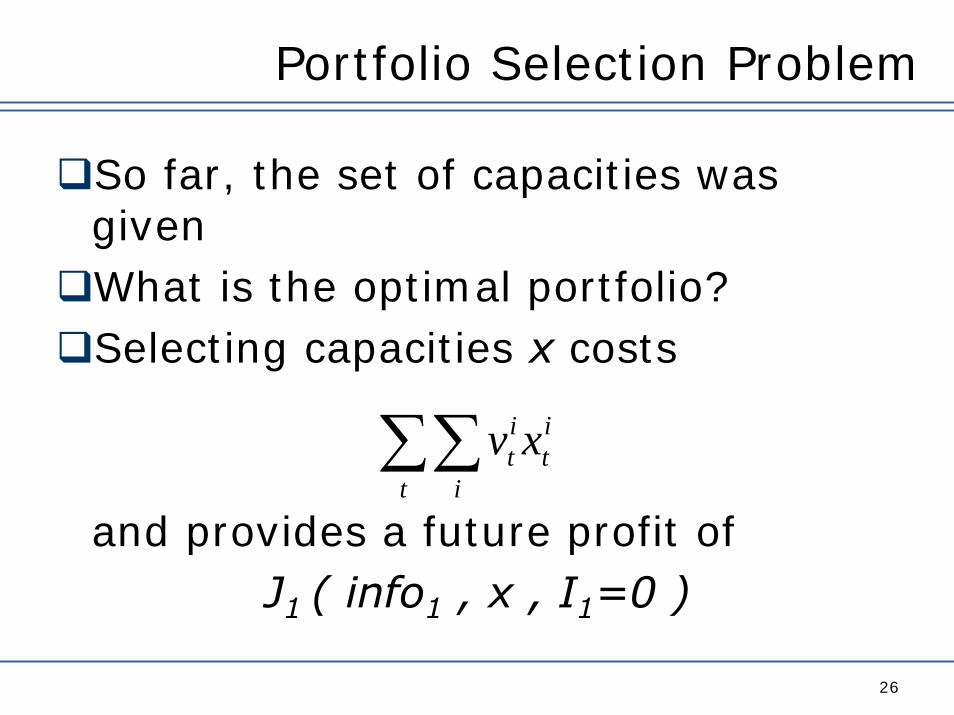

Portfolio Selection Problem

26

So far, the set of capacities was givenWhat is the optimal portfolio?Selecting capacities x costs

and provides a future profit ofJ1 ( info1 , x , I1=0 )

∑∑t i

it

it xv

Portfolio Selection Problem

27

TheoremThe function J1(info1, x, I1=0) is concave in x ≥ 0

CorollarySelecting the optimal capacities is a concave maximization problem

Characterizing Optimal Portfolios

28

Non-attractive contractsContracts dominated by the spot market

E[(SPOT-w)+] ≤ vContracts dominated by other options

Numerical Results

31

2 contractsLong term contract [v1=7, w1=0]Option contract [v2=2, w2=7]

Comparison of profit distributionThrough Montecarlo simulationBetween one contract only and a portfolio

Insights from variances

Outline

33

Portfolio contracts modelingTwo problems

Optimal replenishment policiesOptimal contract purchasing

Mean-Variance TradeoffSuppliers Competition

Risk Analysis

34

Demand DSpot price S

S and D are independent

Profit Variance

35

TheoremThe lower-level sets of the profit variance are connected.

Any portfolio that locally minimizesthe variance is a global minimizer

Single Supplier Case

37

TheoremConsider a buyer focusing on profit mean-variance. In this case, the set of efficient contracts is a segment [yE,yV] or [yV,yE], where

- yE is the maximum expected profit contract, and

- yV is the minimum variance contract.

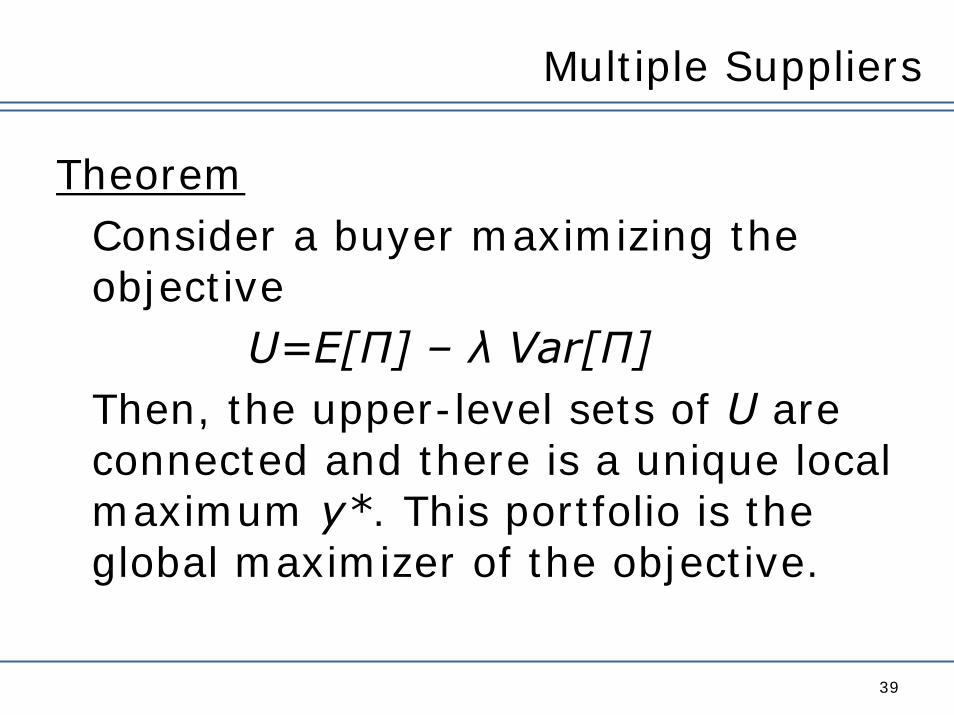

Multiple Suppliers

39

TheoremConsider a buyer maximizing the objective

U=E[Π] – λ Var[Π]Then, the upper-level sets of U are connected and there is a unique local maximum y*. This portfolio is the global maximizer of the objective.

Outline

40

Portfolio contracts modelingTwo problems

Optimal replenishment policiesOptimal contract purchasing

Mean-Variance TradeoffSuppliers Competition

What About the Suppliers?

41

Suppliers’ strategic bidding

Manufacturersbuy portfolios

Uncertaindemand

How should suppliersprice flexibility?

Players in the Game

42

nsuppliers

1buyer Customersp

Finishedproduct

SingleComponent

Costs in the System

43

Reservation cost: per-unit cost paid by the supplier to build or reserve capacity for the buyer

{fi } i=1,…,nExecution cost: per-unit production and delivery cost paid by the supplier

{ci } i=1,…,n

c1 ≤… ≤ cn≤ pThis is public information

Sequence of Events

44

Suppliers submit bids

Manufacturer buys portfolio composed of

different suppliers

Demand becomes known

(xi)

DEMAND SERVEDOR LOST

Manufacturer requests supply from suppliers

under contract

(vi , wi)

45

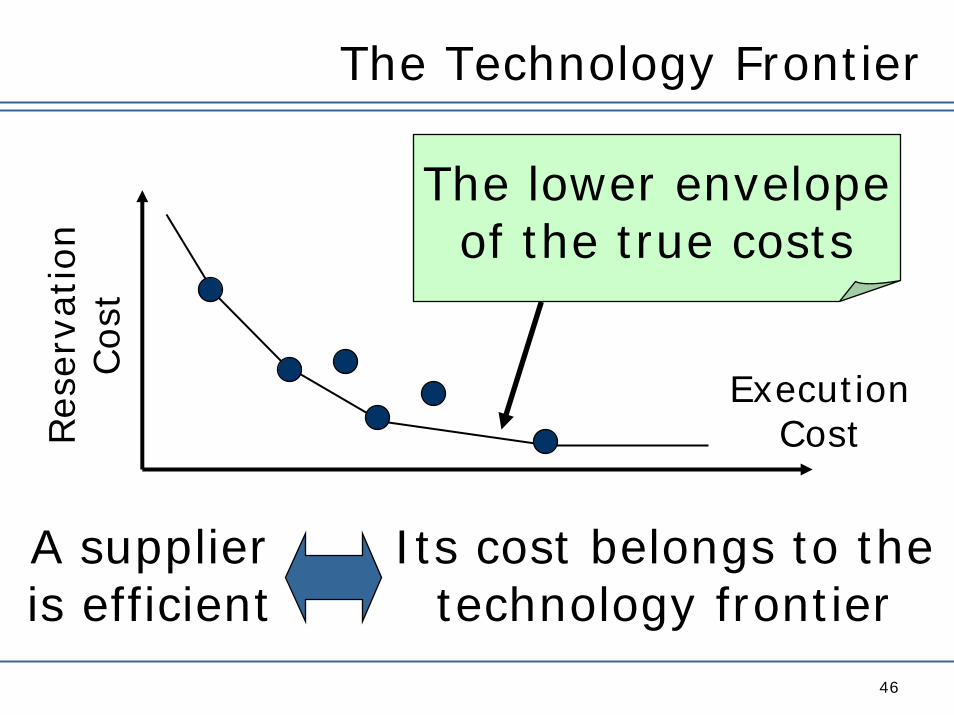

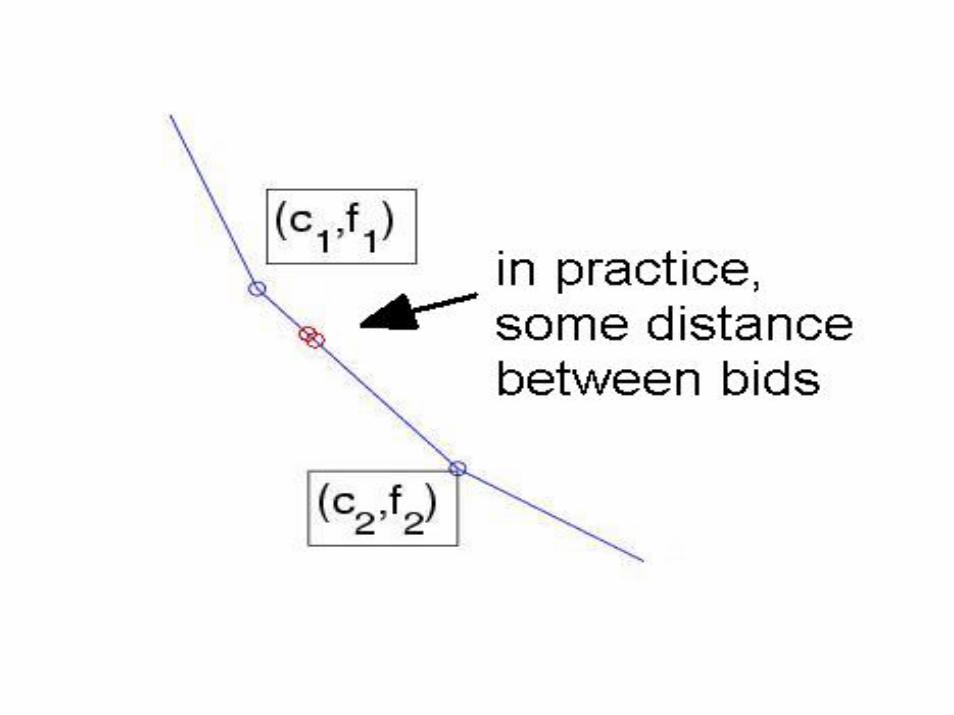

The Technology Frontier

46

A supplieris efficient

Its cost belongs to thetechnology frontier

ExecutionCost

The lower envelopeof the true costs

Res

erva

tion

Cost

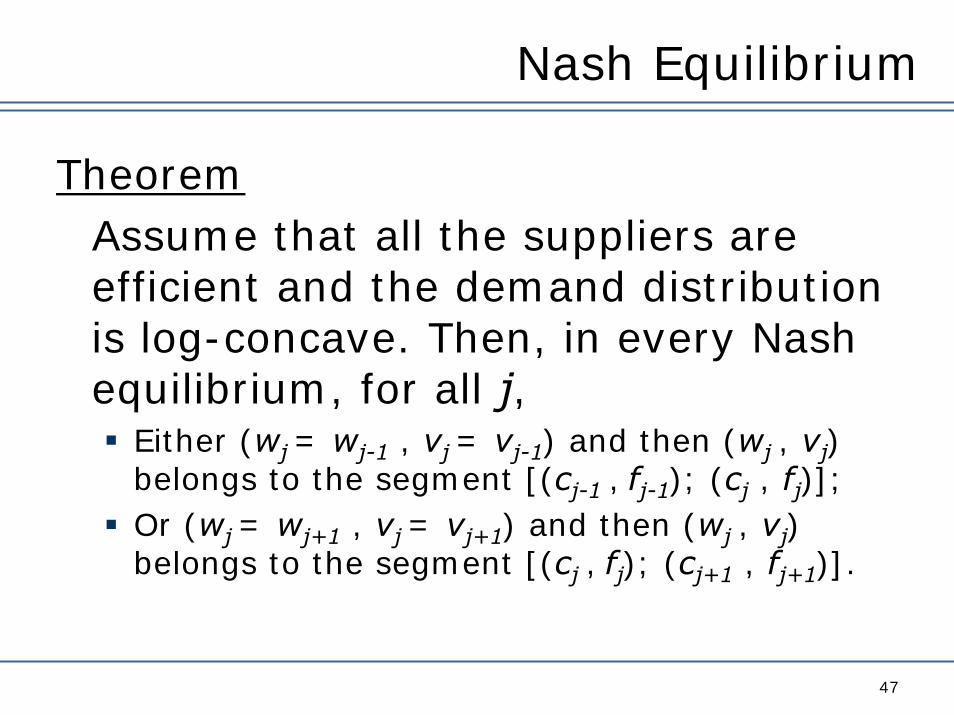

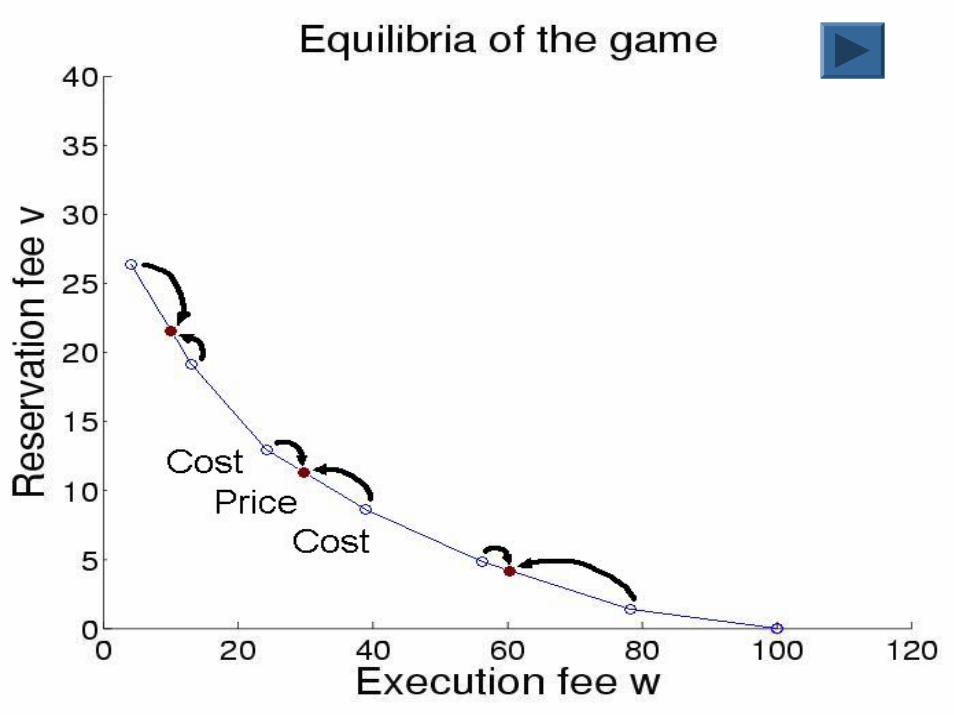

Nash Equilibrium

47

TheoremAssume that all the suppliers are efficient and the demand distribution is log-concave. Then, in every Nash equilibrium, for all j,

Either (wj = wj-1 , vj = vj-1) and then (wj , vj) belongs to the segment [(cj-1 , fj-1); (cj , fj)];Or (wj = wj+1 , vj = vj+1) and then (wj , vj) belongs to the segment [(cj , fj); (cj+1 , fj+1)].

48

Insights

49

Equilibrium analysis1. If a supplier is efficient, it will capture market

share2. Suppliers compete locally against similar

technologies3. Competition preserves diversity and

segments the market4. Prices are related to true costs

Comparison With the Bertrand Model

50

In the Bertrand model1-dimensional competitionThe supplier with the lowest cost captures all the ordersThe price is equal to the second lowest cost

Here2-dimensional competitionMany suppliers coexist at equilibriumThe prices are linear combinations of the costs of the suppliers

52

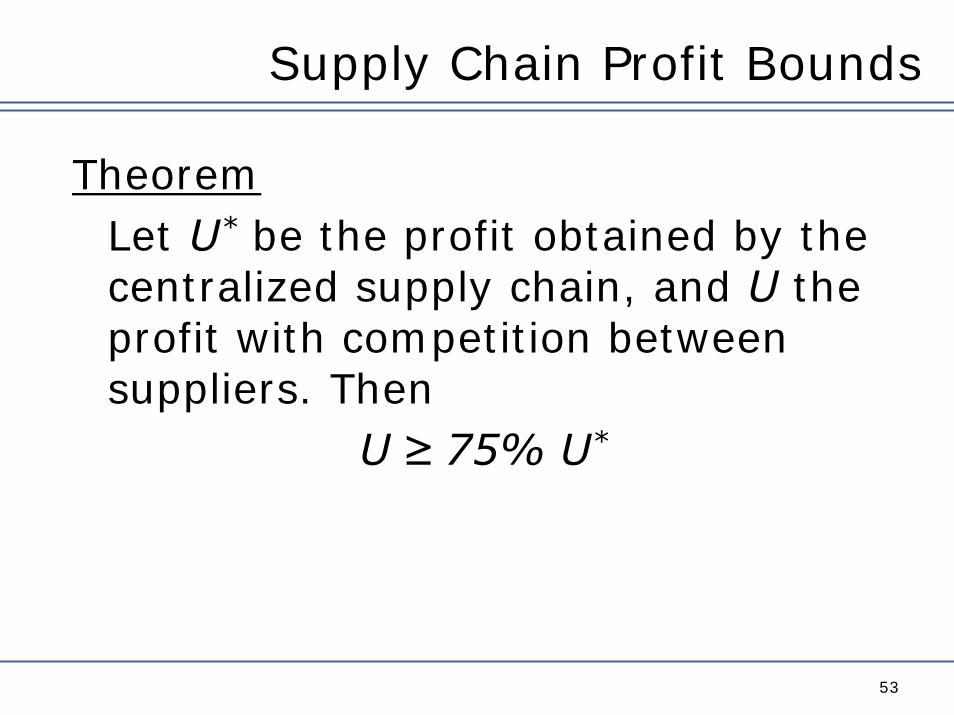

Supply Chain Profit Bounds

53

TheoremLet U* be the profit obtained by the centralized supply chain, and U the profit with competition between suppliers. Then

U≥ 75% U*

Outline

54

Literature Review

Portfolio Contracts

Risk-Averse Inventory Models

Conclusion

Risk Measures

55

Mean-Variance LimitationEqually penalizes desirable upside and undesirable downside outcomes

Other Risk MeasuresUtility functionsCVaR

Risk Measure: Utility Function

56

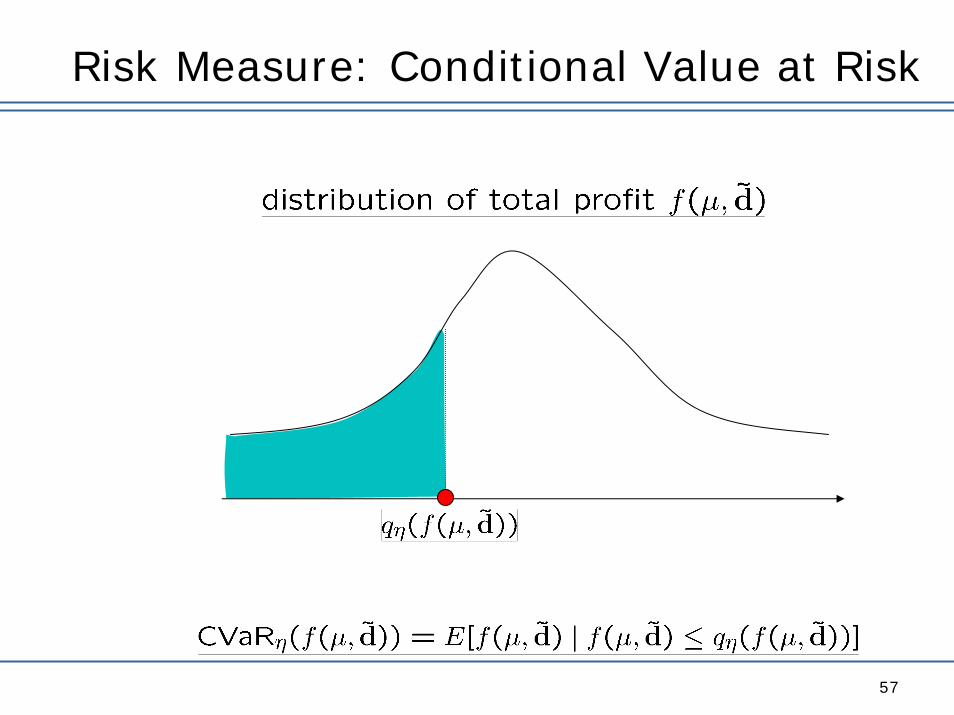

Risk Measure: Conditional Value at Risk

57

Single Product-Periodic Review

58

Finite horizonFixed ordering cost: Variable ordering cost: Convex inventory and backorder cost Demand function:

tcK

ttt pd βα +−=

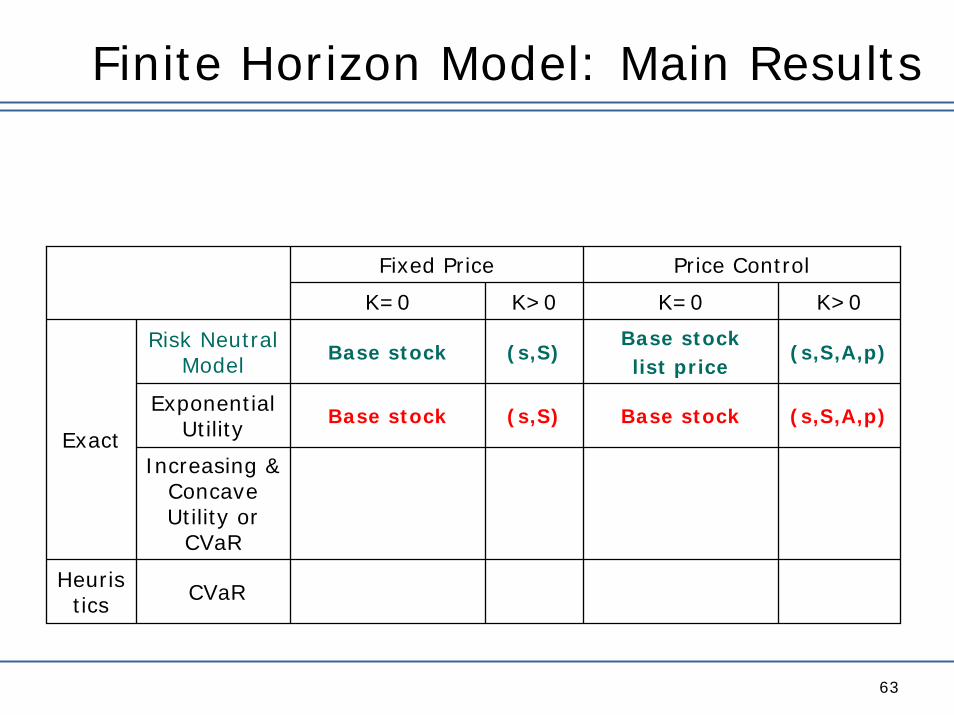

Finite Horizon Model: Main Results

59

Fixed Price Price Control

K=0 K>0 K=0 K>0

Risk NeutralModel

Base stock (s,S)Base stock list price

(s,S,A,p)

Exponential Utility

Increasing & Concave Utility or

CVaR

Heuristics CVaR

Exact

K-Concavity

60

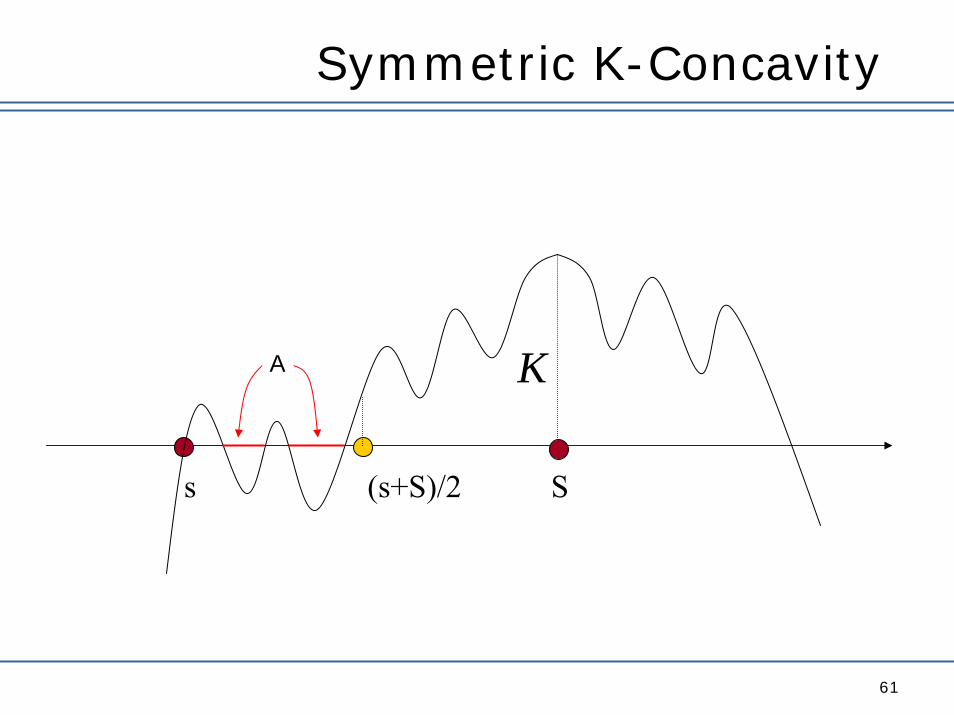

K

s S

Symmetric K-Concavity

61

KA

s S(s+S)/2

Finite Horizon Model: Main Results

62

Fixed Price Price Control

K=0 K>0 K=0 K>0

Risk NeutralModel

Base stock (s,S)Base stock list price

(s,S,A,p)

Exponential Utility

Increasing & Concave Utility or

CVaR

Heuristics CVaR

Exact

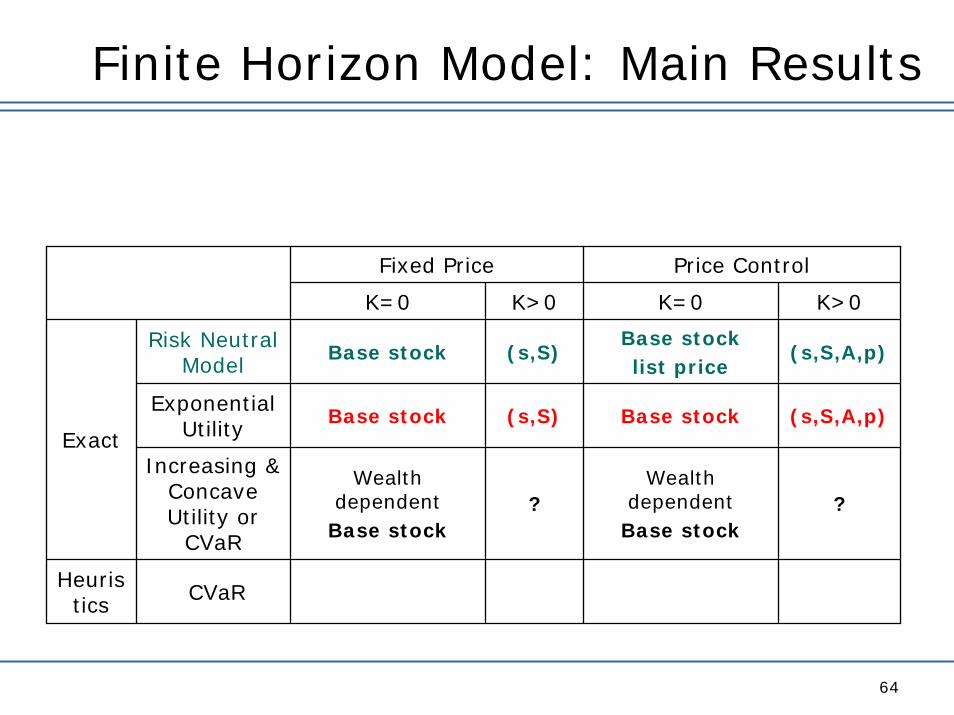

Finite Horizon Model: Main Results

63

Fixed Price Price Control

K=0 K>0 K=0 K>0

Risk NeutralModel

Base stock (s,S)Base stock list price

(s,S,A,p)

Exponential Utility

Base stock (s,S) Base stock (s,S,A,p)

Increasing & Concave Utility or

CVaR

Heuristics CVaR

Exact

Finite Horizon Model: Main Results

64

Fixed Price Price Control

K=0 K>0 K=0 K>0

Risk NeutralModel

Base stock (s,S)Base stock list price

(s,S,A,p)

Exponential Utility

Base stock (s,S) Base stock (s,S,A,p)

Increasing & Concave Utility or

CVaR

Wealth dependent

Base stock?

Wealth dependent

Base stock?

Heuristics CVaR

Exact

Finite Horizon Model: Main Results

65

Fixed Price Price Control

K=0 K>0 K=0 K>0

Risk NeutralModel

Base stock (s,S)Base stock list price

(s,S,A,p)

Exponential Utility

Base stock (s,S) Base stock (s,S,A,p)

Increasing & Concave Utility or

CVaR

Wealth dependent

Base stock?

Wealth dependent

Base stock?

Heuristics CVaR Bass stock (s,S) Base stock (s,S,A,p)

Exact

Extensions

66

Risk Averse Infinite Horizon Models

The Stochastic Cash Balance Problem

Models with Capacity Constraints

Questions

67

Extensions

69

Quantity flexibility contractDeviate by d % on ordering quantity x in a long term contract at price kConsider a portfolio of:

x1=(1-d) x units of long term v=k, w=0x2=2 d x units of option v=0, w=k

Equivalent contractsOptimize on (x1, x2) subject to

x1/(1-d)- x2/ 2d=0

Extensions

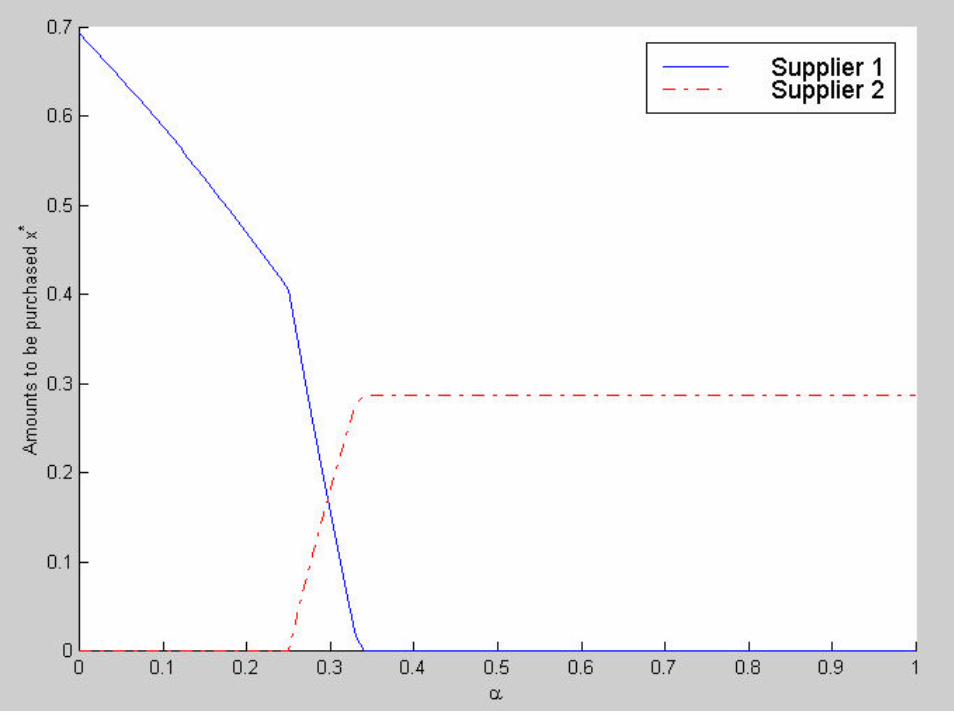

70

Disruption managementSupplier 1 cheaper but disrupted with probability α (e.g. in Malaysia)Supplier 2 more expensive but secure (e.g. in Mexico)Trade-off here

Not flexibilityBut “credit risk” management

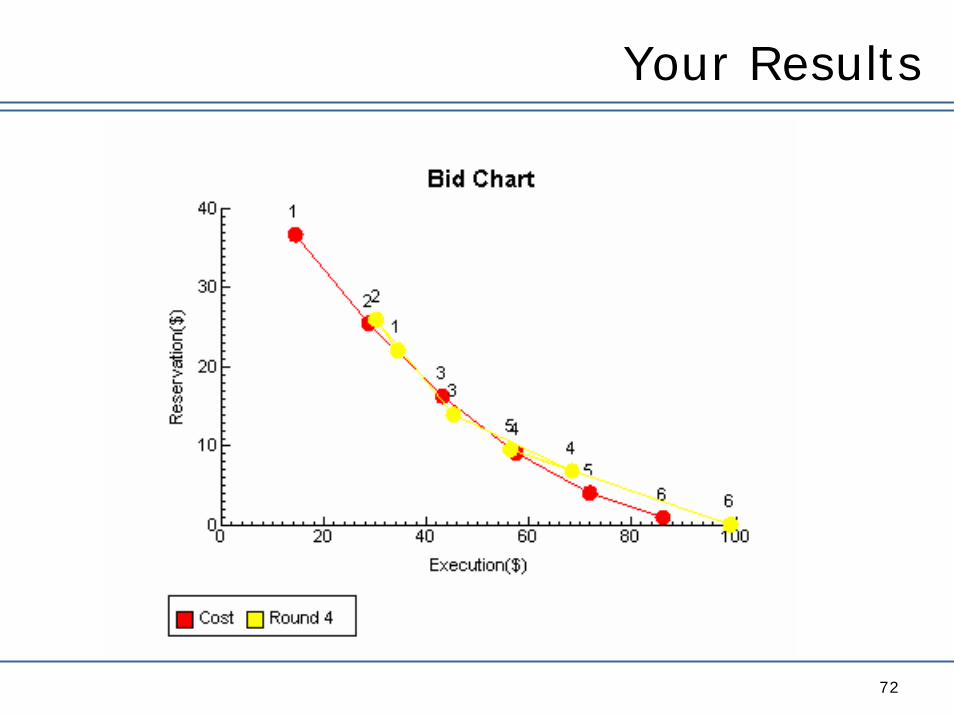

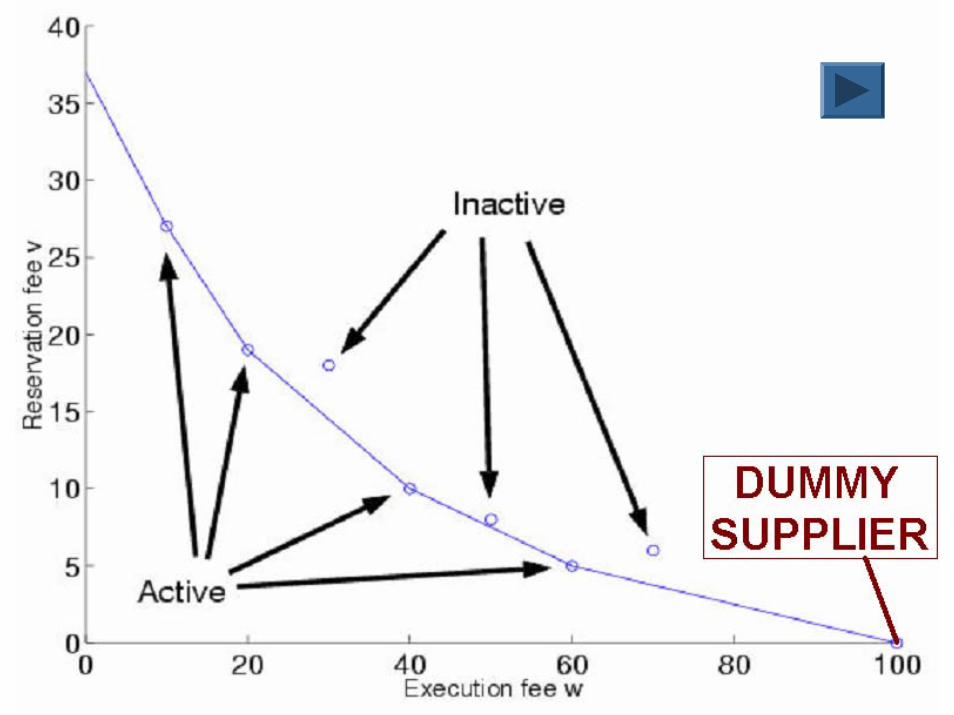

Your Results

72

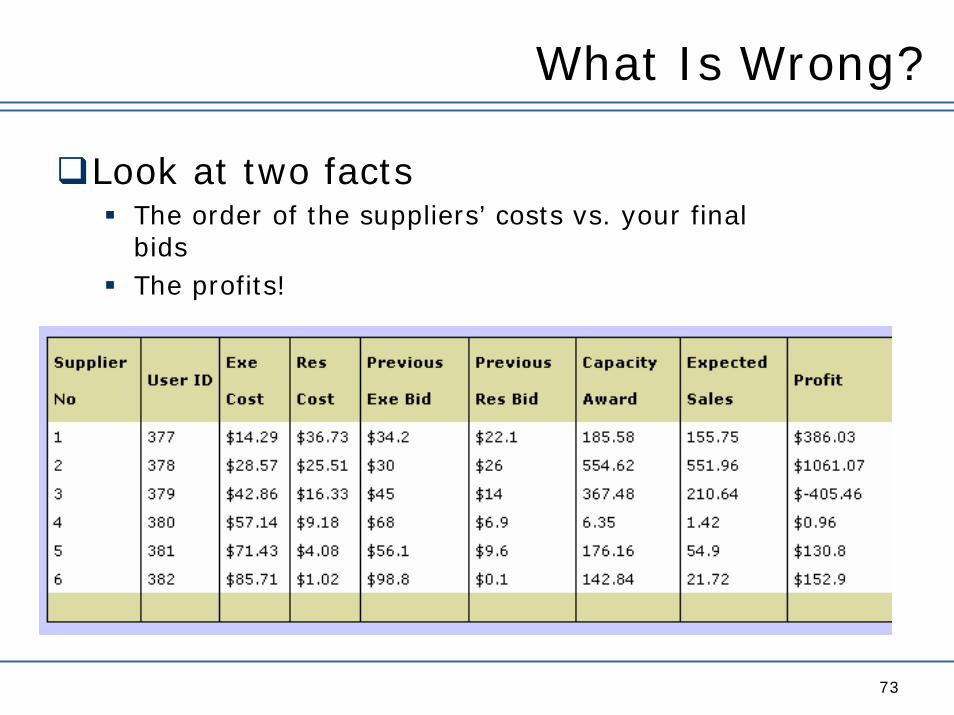

What Is Wrong?

73

Look at two factsThe order of the suppliers’ costs vs. your final bidsThe profits!

Motivation

74

Cost structure has two parametersIn electricity: stand-by vs. production cost

Example with 3 players

76

3 suppliersthe dummy supplier

( w=p, v=0 )

Possible outcomesCluster of 1 and 2; 3 bids with dummyCluster of 1,2 and 3: at ( w = c2 , v = f2 )

78

Region betweenbids A and B

A

B

Equilibrium Convention

79

Rationing rule: if 2 suppliers bid the same parameters (w, v)

The buyer reserves capacity and requests deliveries to both suppliers as if they were one single companyThe suppliers must share the allocations through bargainingThey cooperate in equilibriumIf there is no cooperation, by changing its bid by ε, a supplier can obtain higher profits

Alternative formalization using ε-Nash equilibrium

Recommended