Page 2

Disclosure Statement

This presentation and the accompanying slides (the “Presentation”) which have been prepared by

Samsonite International S.A. (“Samsonite” or the “Company”) do not constitute any offer or invitation to

purchase or subscribe for any securities, and shall not form the basis for or be relied on in connection

with any contract or binding commitment whatsoever. This Presentation has been prepared by the

Company based on information and data which the Company considers reliable, but the Company

makes no representation or warranty, express or implied, whatsoever, on the truth, accuracy,

completeness, fairness and reasonableness of the contents of this Presentation. This Presentation

may not be all-inclusive and may not contain all of the information that you may consider material.

Any liability in respect of the contents of or any omission from this Presentation is expressly excluded.

Certain matters discussed in this presentation may contain statements regarding the Company’s

market opportunity and business prospects that are individually and collectively forward-looking

statements. Such forward-looking statements are not guarantees of future performance and are

subject to known and unknown risks, uncertainties and assumptions that are difficult to predict. The

Company’s actual results, levels of activity, performance or achievements could differ materially and

adversely from results expressed in or implied by this Presentation, including, amongst others:

whether the Company can successfully penetrate new markets and the degree to which the Company

gains traction in these new markets; the sustainability of recent growth rates; the anticipation of the

growth of certain market segments; the positioning of the Company’s products in those segments; the

competitive environment; and general market conditions. The Company is not responsible for any

forward-looking statements and projections made by third parties included in this Presentation.

Page 3

Agenda

Results Highlights

Business Overview

Financial Overview

Outlook and Strategy for 2015

Q&A

Page 4

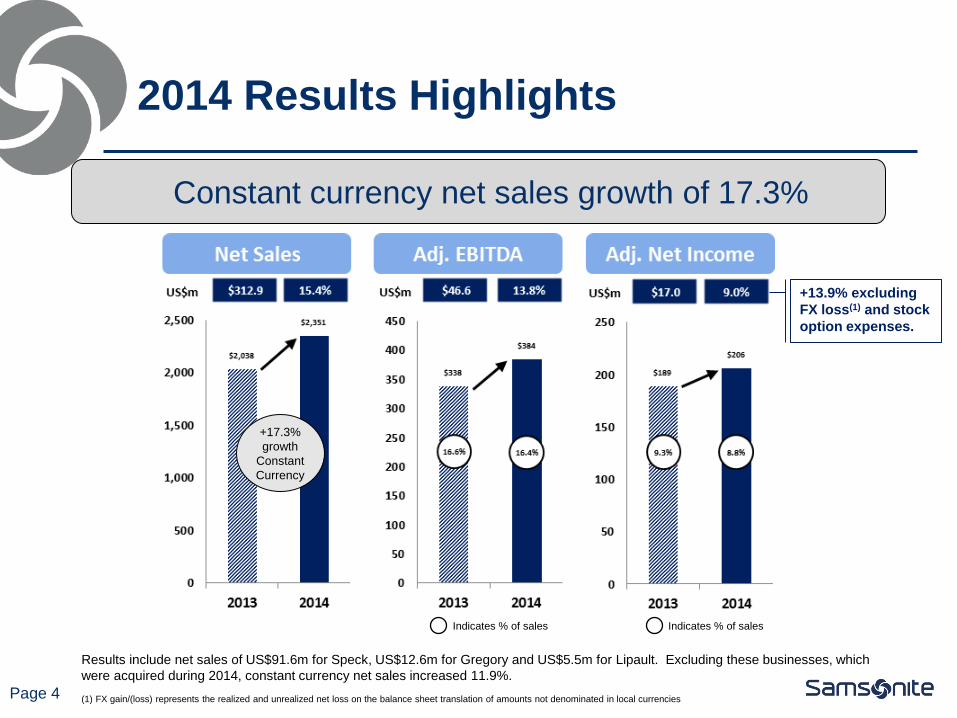

2014 Results Highlights

Results include net sales of US$91.6m for Speck, US$12.6m for Gregory and US$5.5m for Lipault. Excluding these businesses, which

were acquired during 2014, constant currency net sales increased 11.9%.

Indicates % of sales Indicates % of sales

+17.3%

growth

Constant

Currency

Constant currency net sales growth of 17.3%

+13.9% excluding

FX loss(1) and stock

option expenses.

(1) FX gain/(loss) represents the realized and unrealized net loss on the balance sheet translation of amounts not denominated in local currencies

Page 5

Key Financial Highlights

Net Sales:

Net sales increased by 17.3% on a constant currency basis to a

record US$2,351 million.

Currency fluctuation had a negative impact of approximately

US$40 million on year-over-year sales, driven mostly by the

devaluation of the Chilean Peso (US$8.7 million), Russian

Ruble (US$7.2 million), Japanese Yen (US$7.1 million), India

Rupee (US$5.9 million) and Australian Dollar (US$3.1 million) to

the USD.

Excluding the net sales from 2014 acquisitions of Speck

(US$91.6 million), Gregory (US$12.6 million) and Lipault

(US$5.5 million), growth in net sales was US$203.2 million or

10.0%, or 11.9% on a constant currency basis.

Gross Margin:

Gross margin increased 14.3%. As a percentage of sales,

gross margin decreased 50bps due largely to the impact of

acquisitions, mainly Speck which has margins similar to US

Wholesale business, and lower gross margin percent in Latin

America as we transitioned Brazil to a direct sales model, partly

offset by higher gross margin percent in Asia and Europe.

Excluding acquisitions, gross margin as a percentage of sales

increased by 30bp to 53.7%.

+17.3%

growth

Constant

Currency

Indicates % of sales

Page 6

Key Financial Highlights

Adjusted EBITDA:

Adjusted EBITDA is up 13.8% driven by sales growth in all

regions. Adjusted EBITDA margin decrease is due mainly to:

Impact of acquisitions (approximately -40bp);

Temporary reduction in Latin America’s Adjusted EBITDA

margin from reduced gross margins and ramp up of Brazil

operations;

Excluding acquisitions, Adjusted EBITDA margin increased by

approximately 20bp to 16.8%.

Adjusted Net Income:

Excluding FX loss(1) and stock compensation expense, Adjusted

Net Income is up 13.9% from 2013 and, as a percentage of

sales, is down 20bp from 9.7% in 2013 to 9.5% in 2014 due

largely to the impact of acquisitions.

Effective tax rate increase from 27.0% in 2013 to 27.3% in

2014.

Indicates % of sales (1) FX gain/(loss) represents the realized and unrealized net loss on the balance sheet translation of amounts

not denominated in local currencies

Page 7

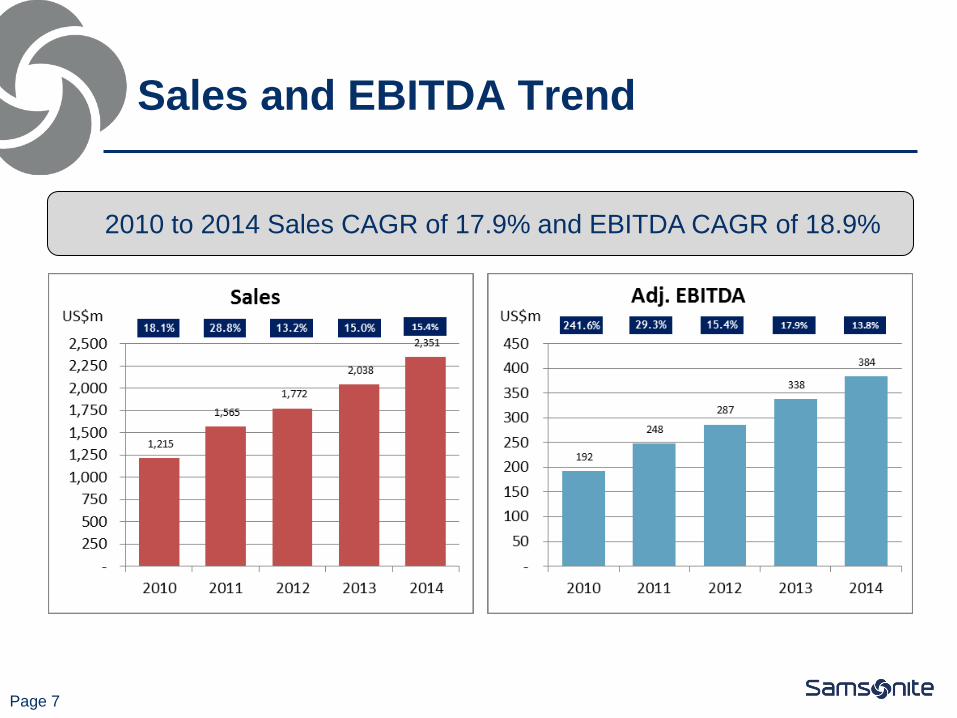

Sales and EBITDA Trend

2010 to 2014 Sales CAGR of 17.9% and EBITDA CAGR of 18.9%

Page 8

Agenda

Results Highlights

Business Overview

Financial Overview

Outlook and Strategy for 2015

Q&A

Page 9

Record net sales performance underpinned by robust growth in world travel and supported by product

innovation and marketing. All regions contributing strong year-over-year growth on a constant currency

basis.

Approximately 1,138 million tourists travelled abroad in 2014, up 51 million or 4.7% from 2013.(1)

Devaluation of many currencies to the USD has had a negative net sales impact of approximately US$40

million and an estimated US$6 million negative impact to Adjusted EBITDA and is likely to have a

continuing impact on 2015 reported USD results.

American Tourister brand continues to expand with 19.0% constant currency growth in sales, while

Samsonite brand also maintains strong constant currency sales growth of 10.2%.

High Sierra and Hartmann brands have launched into new markets with constant currency net sales

growth of 24.9% and 10.3%, respectively.

Successful acquisitions of Lipault, Speck and Gregory help to further diversify our product base into non-

travel categories.

Strong constant currency growth in direct-to-consumer channel sales with retail up 15.6% and direct-to-

consumer e-commerce up 37.4%.

Advertising and promotions spend of US$145 million in 2014 continues to strengthen brand and product

awareness and drive sales ahead of the industry.

Operating cash flow of US$229.9 million and net cash position at December 31, 2014 of US$72.9 million

provides solid platform to execute future growth plans.

Business Highlights

(1) Source: UNWTO World Tourism Barometer, Volume 13, January 2015

Page 10

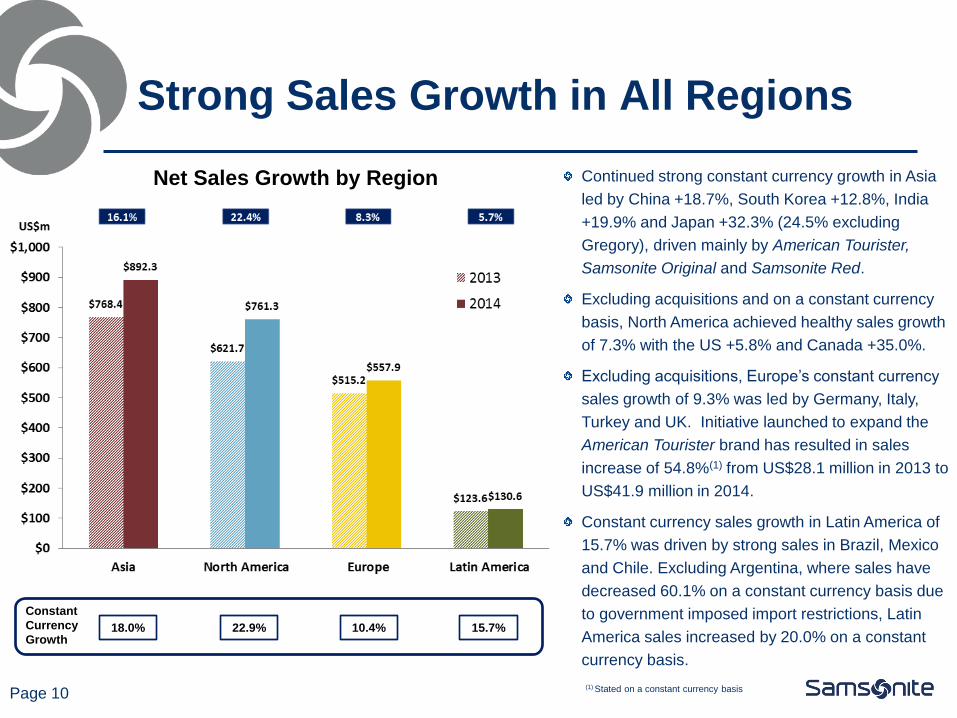

Strong Sales Growth in All Regions

Net Sales Growth by Region Continued strong constant currency growth in Asia

led by China +18.7%, South Korea +12.8%, India

+19.9% and Japan +32.3% (24.5% excluding

Gregory), driven mainly by American Tourister,

Samsonite Original and Samsonite Red.

Excluding acquisitions and on a constant currency

basis, North America achieved healthy sales growth

of 7.3% with the US +5.8% and Canada +35.0%.

Excluding acquisitions, Europe’s constant currency

sales growth of 9.3% was led by Germany, Italy,

Turkey and UK. Initiative launched to expand the

American Tourister brand has resulted in sales

increase of 54.8%(1) from US$28.1 million in 2013 to

US$41.9 million in 2014.

Constant currency sales growth in Latin America of

15.7% was driven by strong sales in Brazil, Mexico

and Chile. Excluding Argentina, where sales have

decreased 60.1% on a constant currency basis due

to government imposed import restrictions, Latin

America sales increased by 20.0% on a constant

currency basis.

Constant

Currency

Growth 18.0% 22.9% 10.4% 15.7%

(1) Stated on a constant currency basis

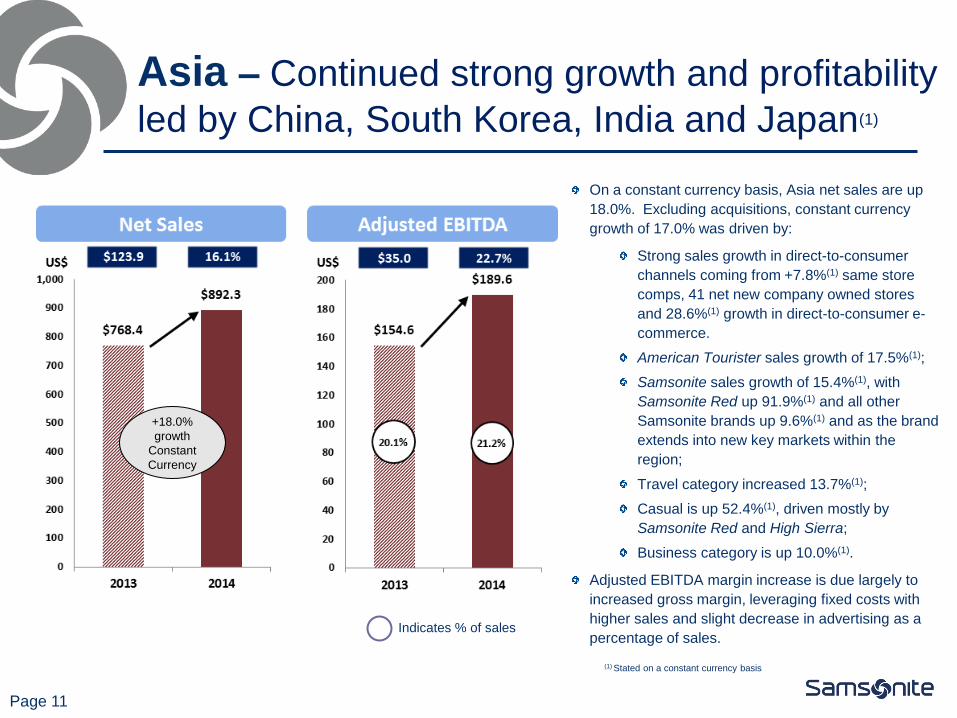

Asia – Continued strong growth and profitability

led by China, South Korea, India and Japan(1)

On a constant currency basis, Asia net sales are up

18.0%. Excluding acquisitions, constant currency

growth of 17.0% was driven by:

Strong sales growth in direct-to-consumer

channels coming from +7.8%(1) same store

comps, 41 net new company owned stores

and 28.6%(1) growth in direct-to-consumer e-

commerce.

American Tourister sales growth of 17.5%(1);

Samsonite sales growth of 15.4%(1), with

Samsonite Red up 91.9%(1) and all other

Samsonite brands up 9.6%(1) and as the brand

extends into new key markets within the

region;

Travel category increased 13.7%(1);

Casual is up 52.4%(1), driven mostly by

Samsonite Red and High Sierra;

Business category is up 10.0%(1).

Adjusted EBITDA margin increase is due largely to

increased gross margin, leveraging fixed costs with

higher sales and slight decrease in advertising as a

percentage of sales.

Page 11

+18.0%

growth

Constant

Currency

Indicates % of sales

(1) Stated on a constant currency basis

Key Asia Markets - Continued strong growth

in all key markets(1)

Page 12

* Includes Macau

(1) Stated on a constant currency basis

Strong China sales growth of 18.7%(1) driven by

American Tourister, Samsonite Original and

Samsonite Red. Solid growth in the direct-to-

consumer channels is the result of 6.7%(1) retail

comps, 13 net new stores and direct-to-consumer e-

commerce growth of 75.7%(1). Additionally, wholesale

growth of 17.1%(1) is due largely to increases in TV

home shopping and B2B.

South Korea sales growth of 12.8%(1) is driven by the

continued strong growth of the Samsonite Red brand,

up 66.9%(1) to US$31.2 million, as well as Samsonite

Original, American Tourister and High Sierra.

Sales growth in India of 19.9%(1) is driven by the

continued success of American Tourister and the

introduction of High Sierra, which increased from

US$0.5 million in 2013 to US$4.6 million in 2014.

Japan sales are up 32.3%(1). Excluding the acquisition

of Gregory, sales growth of 24.5%(1) is led by strong

growth of Samsonite and American Tourister.

Hong Kong* sales growth of 12.2%(1) is led by growth

of Samsonite Red and the acquisition of Gregory.

Sales experienced a slowdown at the end of the year

due to protesters.

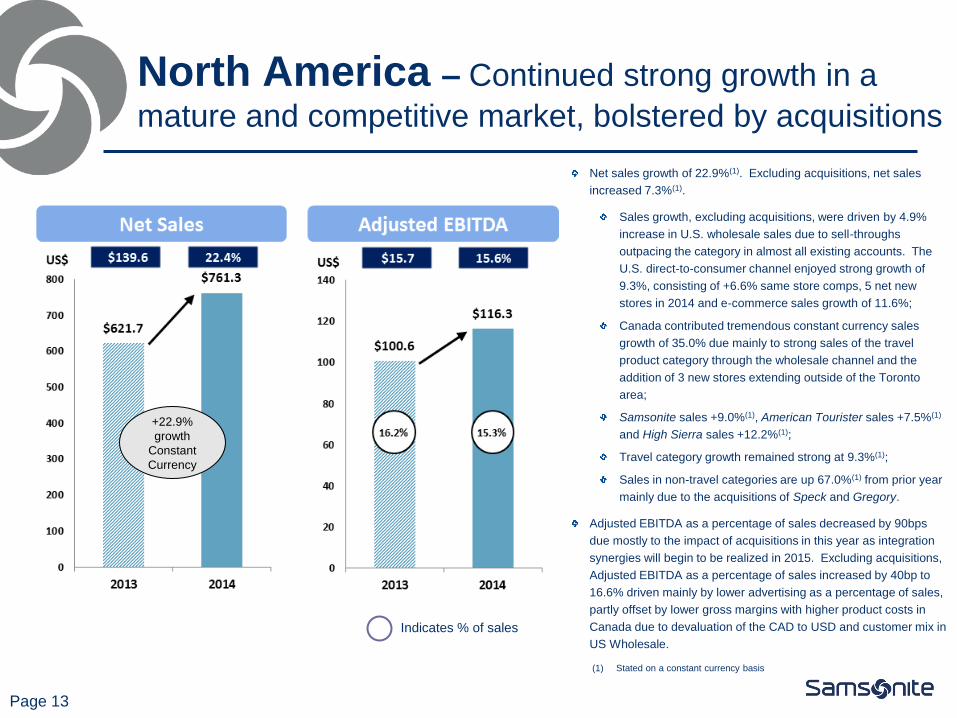

Net sales growth of 22.9%(1). Excluding acquisitions, net sales

increased 7.3%(1).

Sales growth, excluding acquisitions, were driven by 4.9%

increase in U.S. wholesale sales due to sell-throughs

outpacing the category in almost all existing accounts. The

U.S. direct-to-consumer channel enjoyed strong growth of

9.3%, consisting of +6.6% same store comps, 5 net new

stores in 2014 and e-commerce sales growth of 11.6%;

Canada contributed tremendous constant currency sales

growth of 35.0% due mainly to strong sales of the travel

product category through the wholesale channel and the

addition of 3 new stores extending outside of the Toronto

area;

Samsonite sales +9.0%(1), American Tourister sales +7.5%(1)

and High Sierra sales +12.2%(1);

Travel category growth remained strong at 9.3%(1);

Sales in non-travel categories are up 67.0%(1) from prior year

mainly due to the acquisitions of Speck and Gregory.

Adjusted EBITDA as a percentage of sales decreased by 90bps

due mostly to the impact of acquisitions in this year as integration

synergies will begin to be realized in 2015. Excluding acquisitions,

Adjusted EBITDA as a percentage of sales increased by 40bp to

16.6% driven mainly by lower advertising as a percentage of sales,

partly offset by lower gross margins with higher product costs in

Canada due to devaluation of the CAD to USD and customer mix in

US Wholesale.

North America – Continued strong growth in a

mature and competitive market, bolstered by acquisitions

Page 13

+22.9%

growth

Constant

Currency

Indicates % of sales

(1) Stated on a constant currency basis

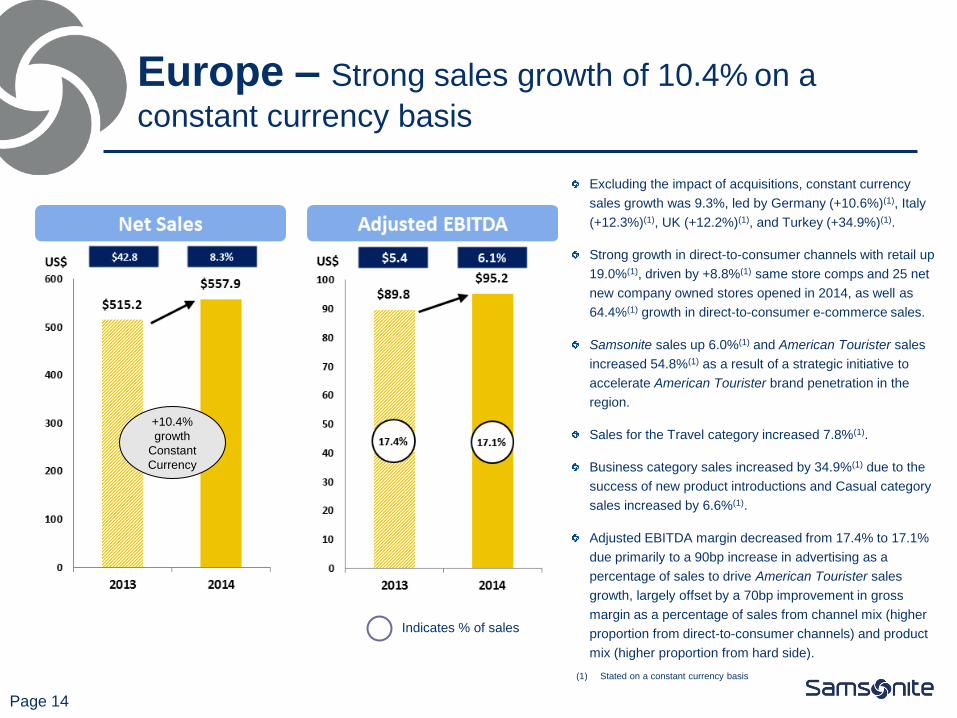

Europe – Strong sales growth of 10.4% on a

constant currency basis

Excluding the impact of acquisitions, constant currency

sales growth was 9.3%, led by Germany (+10.6%)(1), Italy

(+12.3%)(1), UK (+12.2%)(1), and Turkey (+34.9%)(1).

Strong growth in direct-to-consumer channels with retail up

19.0%(1), driven by +8.8%(1) same store comps and 25 net

new company owned stores opened in 2014, as well as

64.4%(1) growth in direct-to-consumer e-commerce sales.

Samsonite sales up 6.0%(1) and American Tourister sales

increased 54.8%(1) as a result of a strategic initiative to

accelerate American Tourister brand penetration in the

region.

Sales for the Travel category increased 7.8%(1).

Business category sales increased by 34.9%(1) due to the

success of new product introductions and Casual category

sales increased by 6.6%(1).

Adjusted EBITDA margin decreased from 17.4% to 17.1%

due primarily to a 90bp increase in advertising as a

percentage of sales to drive American Tourister sales

growth, largely offset by a 70bp improvement in gross

margin as a percentage of sales from channel mix (higher

proportion from direct-to-consumer channels) and product

mix (higher proportion from hard side).

Page 14

+10.4%

growth

Constant

Currency

(1) Stated on a constant currency basis

Indicates % of sales

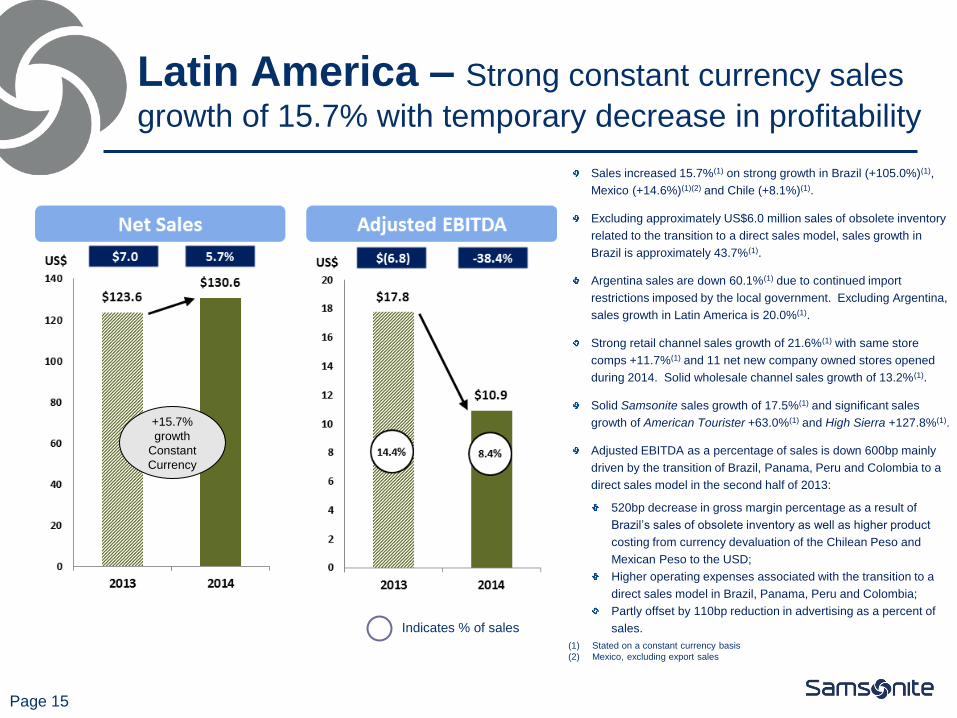

Sales increased 15.7%(1) on strong growth in Brazil (+105.0%)(1),

Mexico (+14.6%)(1)(2) and Chile (+8.1%)(1).

Excluding approximately US$6.0 million sales of obsolete inventory

related to the transition to a direct sales model, sales growth in

Brazil is approximately 43.7%(1).

Argentina sales are down 60.1%(1) due to continued import

restrictions imposed by the local government. Excluding Argentina,

sales growth in Latin America is 20.0%(1).

Strong retail channel sales growth of 21.6%(1) with same store

comps +11.7%(1) and 11 net new company owned stores opened

during 2014. Solid wholesale channel sales growth of 13.2%(1).

Solid Samsonite sales growth of 17.5%(1) and significant sales

growth of American Tourister +63.0%(1) and High Sierra +127.8%(1).

Adjusted EBITDA as a percentage of sales is down 600bp mainly

driven by the transition of Brazil, Panama, Peru and Colombia to a

direct sales model in the second half of 2013:

520bp decrease in gross margin percentage as a result of

Brazil’s sales of obsolete inventory as well as higher product

costing from currency devaluation of the Chilean Peso and

Mexican Peso to the USD;

Higher operating expenses associated with the transition to a

direct sales model in Brazil, Panama, Peru and Colombia;

Partly offset by 110bp reduction in advertising as a percent of

sales.

Latin America – Strong constant currency sales

growth of 15.7% with temporary decrease in profitability

Page 15

+15.7%

growth

Constant

Currency

(1) Stated on a constant currency basis

(2) Mexico, excluding export sales

Indicates % of sales

Page 16

Sales in Key Markets

Strong constant currency growth in all key markets

* Includes Macau

Page 17

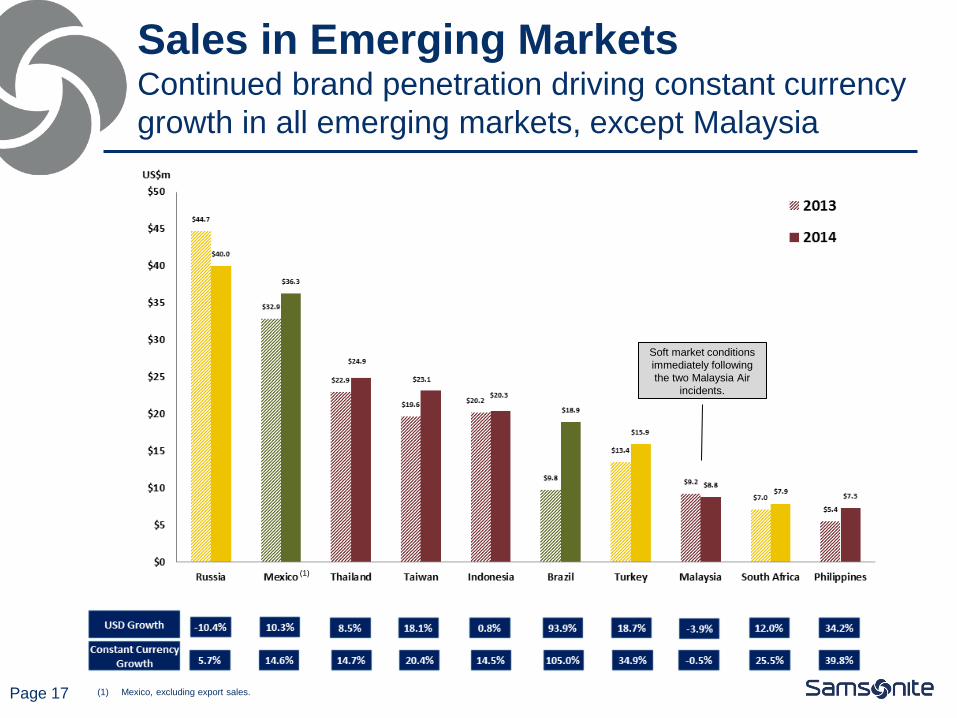

Sales in Emerging Markets

Continued brand penetration driving constant currency

growth in all emerging markets, except Malaysia

Soft market conditions

immediately following

the two Malaysia Air

incidents.

(1) Mexico, excluding export sales.

(1)

Constant

Currency

Growth 10.2% 19.0% NA 24.9%

Strong Sales Growth in Key Brands

Page 18

Net Sales Growth by Brand Continued growth in Samsonite across all regions with

net sales up 10.2% on a constant currency basis:

Asia +15.4%(1), North America +9.0%(1),

Europe +6.0%(1), and Latin America +17.5%(1)

Strong growth in Asia driven by deeper

penetration of Samsonite Red into key markets

(+US$28.2 million or 91.9% constant currency

growth)

American Tourister net sales up 19.0% on a constant

currency basis as the brand continues to flourish in

established markets while the brand further extends

into new global markets:

Asia +17.5%(1), North America +7.5%(1)

Focus on further globalizing the brand has

resulted in strong growth in Europe +54.8%(1)

and Latin America +63.0%(1)

High Sierra and Hartmann brands represent

approximately 4.5% of total 2014 net sales as they

continue to extend into more global markets.

Constant currency growth of 2.4% in Other brands is

driven mainly by the acquisition of Lipault and

increased sales of the Secret and Xtrem brands in

Latin America, partly offset by decreases in private

label sales and licensing revenue in North America.

(1) Stated on a constant currency basis

(2) Speck, Gregory and Lipault brands were acquired in May 2014, July 2014 and April 2014, respectively. Lipault 2014 sales of US$5.5 million are included in Other brands

10.3% NA 2.4%

(2) (2) (2)

Samsonite – Asia

Key Product Assortment

Page 19

Fashionaire Cosmolite

Inova

Marshmallow

Oval

Engenero Canimals

Torus Pro-DLX 4

Mover

Red - Mondo

Red - Newyorker Red - Liebe

Locus

Samsonite – North America

Key Product Assortment

Page 20

Lift2

Hyperspace

Ziplite

Fiero

Spin Tech Silhouette Sphere

Hardside

Columbian

Leather

Flapover

Briefcast

Tectonic PFT

Backpack

Xenon2 PFT

Briefcase

Ripstop

Rolling

Duffle

Andante

Wheeled

Duffle

Samsonite – Europe

New Product Assortment

Page 21

Neopulse

B-Lite

Lite-Shock

S’Cure Spark

Cosmolite

2.0

GT Supreme

Backpack

GT Supreme

Bailhandle

Urban Arc

Backpack

Disney

licensed

products

Samsonite – Latin America

Key Product Assortment

Page 22

Fiero

Xenon II Metropolis Torus

Locus

Jumbo

Ember

Firelite

Puzzle Cosmolite

Glide

I-Lite B-Lite Silhouette

Sphere

Lightcase

American Tourister – Asia

Key Product Assortment

Page 23

HS MV+ Cube Pop

Spot-lite IV

Bon Air

Sky

AT Speedair

Citi-Pro Backpack

American Tourister – North America

Key Product Assortment

Page 24

Meridian

360 XLT

Atmosphera

ILite

Supreme

ILite

X’Treme

Disney

Licensed

Product

Star Wars

Licensed

Product

American Tourister – Europe

Key Product Assortment

Page 25

Lock‘n Roll

San Francisco

Vivotek Lightway

2014 Acquisitions

Page 26

Lipault is a youthful, vibrant and chic French luggage brand known for its

functional and fashionable designs.

Acquired all of the outstanding capital stock on April 1, 2014 for approximately

€20 million in cash (approximately US$28 million).

Extends the Company’s brand portfolio to engage with a wider base of

fashionable female consumers through its signature Parisian style and vibrant

colors.

Strategy is to utilize Samsonite’s well-established distribution network and

extensive retail presence to expand Lipault’s respected brand in France and

into additional markets in Europe (historically, over 90% of Lipault’s sales

came from France) while evaluating opportunities to expand further in Asia

and the Americas.

2014 pro-forma full year net sales of US$7.6 million.

Key Product Assortment

Page 27

Originale Plume Spinner

Plume

Business

Case

Wheeled

Pliable

Upright

Lady Plume

Handbag

Pliable

Upright

Lady Plume Weekend

Bag Wheeled

Lady Plume

Weekend Bag

2014 Acquisitions

Page 28

Speck produces a diverse range of sleek, stylish, and functionally innovative products

that provide superior military-grade protection for mobile devices across multiple brands

and is particularly well-known for its “slim protection” designs such as the iconic

CandyShell “hard-soft” material case – a technology that Speck pioneered.

Acquired all of the outstanding capital stock on May 28, 2014 for approximately US$85

million in cash.

Extends the Company’s brand portfolio beyond its traditional strength in travel luggage

products and provides the Company with a strong brand and product offering resulting

in an immediate foothold in the market for protective cases for smartphones, tablets,

laptops and other personal electronic devices. The market size for phones cases is

estimated to be US$2.3 billion.

Strategy is to utilize Samsonite’s resources, excellence in operations and marketing and

well-established distribution network to further strengthen Speck’s business in the U.S.

and significantly expand the brand’s presence across Asia, Europe and Latin America.

2014 pro-forma full year net sales of US$137.0 million.

Key Product Assortment

Page 29 SeeThru StyleFolio

CandyShell

CARD

CandyShell CandyShell

INKED

CandyShell

GRIP

iGuy

MightyShell

2014 Acquisitions

Page 30

Gregory Mountain Products (“Gregory”) is an iconic technical outdoor backpack brand

that is known as a pioneer in its field and is well-respected by active outdoor and

adventure enthusiasts. Gregory is also a popular brand for lifestyle products in Japan.

The purchase of substantially all of the assets of Gregory was closed July 23, 2014 for

approximately US$84 million in cash.

Extends the Company’s brand portfolio into the premium segment of the outdoor bag

category as a perfect complement to High Sierra, which is a well-known and respected

brand in the mid-market segment.

Gregory's lifestyle products which are widely popular in Japan represents a unique

opportunity to further develop and replicate the success of the premium lifestyle fashion

brand in other key Asian markets.

Strategy is to leverage Samsonite’s marketing, sourcing and well-established

distribution capabilities to further expand Gregory’s business in the U.S. and

significantly grow the Gregory brand internationally.

2014 pro-forma full year net sales of US$31.2 million.

Key Product Assortment

Page 31

All Day

Jade Series

Z Series

Deva

Baltoro

Amber

Stout

Sunrise Tote

Metro Messenger

Pace 3

Tempo 3

Offshore Day

Quick Pocket

Switch Sling

Sundowner

Shoulder

Kletter Day

Progress on Hartmann

All core classic collections have been redesigned to ensure product aesthetic and quality are

consistent with loyal and premium consumer expectations.

Designed and launched new, lightweight and modern travel collections in North America and

Asia that appeal to a broader consumer market. New collections are receiving strong

placement at premium customers and specialists.

Global retail expansion is underway with 11 new store openings in the second half of 2014 in

North America and Asia, including flagship stores on Madison Avenue in NYC and the Ginza

district in Tokyo, Japan.

Advertising spend has been increased since the acquisition to US$7.9 million in 2014 to re-

establish brand identity and support expansion into new markets.

2014 sales growth of US$1.5 million, or 10.3% on a constant currency basis, over 2013.

Key initiatives include:

Further retail expansion in North America and Asia;

Substantiate global brand identity in the premium luxury segment;

Extend product assortment into accessories, business and casual lifestyle products.

Page 32

2 Flagship Hartmann Stores

Page 33

Hartmann – Ginza Flagship, Tokyo, Japan

Page 34

Key Product Assortment

7R

Heritage

Innovaire

LineAire

Minimalist

Vigor

Belting Wristlet

Belting Continental Wallet

Intensity Belting

Tweed

Belting

Progress on High Sierra

Leveraging the brand in North America, Asia and Europe with each region

developing new products consistent with the brand image to meet the needs

of the consumer in each market.

Brand has launched in Asia, where it has grown from US$5.5 million in 2013

to US$11.7 million in 2014 and in Europe, with 2014 sales of US$1.9 million.

Advertising spend has been increased to US$9.9 million in 2014 to enhance

brand awareness and support global expansion.

2014 sales growth of US$17.2 million, or 24.9% on a constant currency basis,

over 2013.

Initiatives include:

Further expansion into Asia and Europe wholesale accounts supported

with additional marketing;

License the brand for other outdoor products and launch apparel.

Page 35

Page 36

Key Product Assortment

Rock (Asia)

UFO (Asia) Wheeled

Duffle

(Asia)

Tactic (Asia)

Classic 2

Hiking Collection

Tech 2

Hiking Collection

Tech Hydration XBT

Collection Lifestyle Collection

Ski Boot Bag

BTS Collection

Ultimate Access 2.0 Wheeled Duffle

Page 37

Strong Sales Growth in Travel and

Casual Product Categories

Net Sales Growth by Product Category Travel remains our largest product category and

traditional strength with all regions contributing

to growth of 10.9%(1).

Casual category net sales rose 25.1%(1) driven

by the acquisition of Gregory and growth of

Samsonite Red in Asia and High Sierra in all

regions.

Net sales in Business category increased by

34.6%(1) (12.1%(1), excluding Speck) with strong

organic growth in Asia and Europe:

106.6%(1) increase in North America (1.4%

increase, excluding Speck.)

34.9%(1) growth in Europe driven by

successful new product introductions.

Increase of 10.0%(1) in Asia.

Growth of 76.3%(1) in the Accessories category

(20.4%(1), excluding Speck).

Growth in the Other category is driven largely by

increased sales of kids products with Disney-

licensed product beginning to ship in the second

half of 2014.

(1) Stated on a constant currency basis

Constant

Currency

Growth 10.9% 25.1% 34.6% 76.3% 12.4%

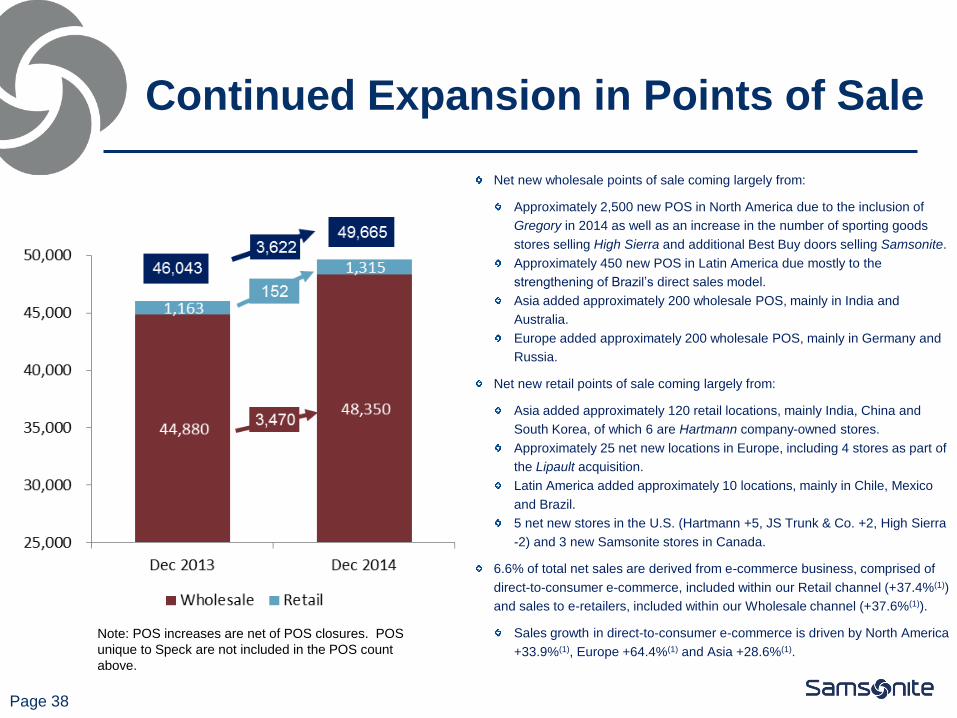

Continued Expansion in Points of Sale

Note: POS increases are net of POS closures. POS

unique to Speck are not included in the POS count

above.

Page 38

Net new wholesale points of sale coming largely from:

Approximately 2,500 new POS in North America due to the inclusion of

Gregory in 2014 as well as an increase in the number of sporting goods

stores selling High Sierra and additional Best Buy doors selling Samsonite.

Approximately 450 new POS in Latin America due mostly to the

strengthening of Brazil’s direct sales model.

Asia added approximately 200 wholesale POS, mainly in India and

Australia.

Europe added approximately 200 wholesale POS, mainly in Germany and

Russia.

Net new retail points of sale coming largely from:

Asia added approximately 120 retail locations, mainly India, China and

South Korea, of which 6 are Hartmann company-owned stores.

Approximately 25 net new locations in Europe, including 4 stores as part of

the Lipault acquisition.

Latin America added approximately 10 locations, mainly in Chile, Mexico

and Brazil.

5 net new stores in the U.S. (Hartmann +5, JS Trunk & Co. +2, High Sierra

-2) and 3 new Samsonite stores in Canada.

6.6% of total net sales are derived from e-commerce business, comprised of

direct-to-consumer e-commerce, included within our Retail channel (+37.4%(1))

and sales to e-retailers, included within our Wholesale channel (+37.6%(1)).

Sales growth in direct-to-consumer e-commerce is driven by North America

+33.9%(1), Europe +64.4%(1) and Asia +28.6%(1).

6 Hartmann Stores Opened in the 2nd

Half of 2014 in Asia

Page 39

Hartmann – Ginza Flagship, Japan

Hartmann – Seoul Cheongdam Flagship, South Korea

Hartmann – Beijing Lufthansa, China

Hartmann – Taichung Top City, Taiwan

5 Hartmann Stores Opened in the 2nd

Half of 2014 in North America

Page 40

Hartmann – King of Prussia, PA

Hartmann – Charlotte, NC

Hartmann – Madison Avenue, New York City

House of Samsonite – Coex Mall, Seoul, South Korea

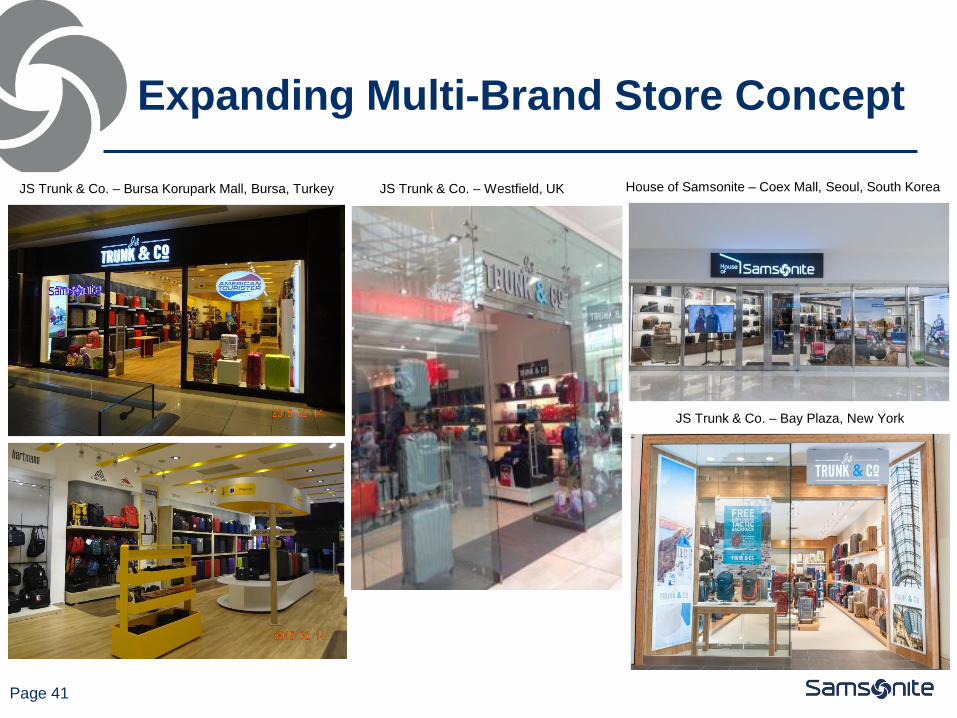

Expanding Multi-Brand Store Concept

Page 41

JS Trunk & Co. – Westfield, UK

JS Trunk & Co. – Bay Plaza, New York

JS Trunk & Co. – Bursa Korupark Mall, Bursa, Turkey

Lipault Acquisition Included 4 Stores

Page 42 Lipault – Mozart, Paris, France

Lipault – Madeleine, Paris, France

Lipault – Rennes, Paris, France

Retail Expansion in Latin America

Page 43

Samsonite - Mall Tesoro, Medellin, Colombia

Samsonite - Mall Andino, Bogota, Colombia

Samsonite – Jardins, Sao Paulo, Brazil Samsonite - Mall Sante Fe, Medellin, Colombia Samsonite - Mall Unicentro, Bogota, Colombia

Samsonite - Mall Santa Fe, Mexico City, Mexico

Selection of Other Retail Stores Opened

in the 2nd Half of 2014

Page 44

Samsonite – Mirabel, Quebec, Canada

Samsonite – Capucines, France

Samsonite – Gotheburg, Sweden

American Tourister – Marina Square, Singapore

Samsonite – Grand Kawanua City, Indonesia

Samsonite – Budapest Allee Mall 2, Hungary

Page 45

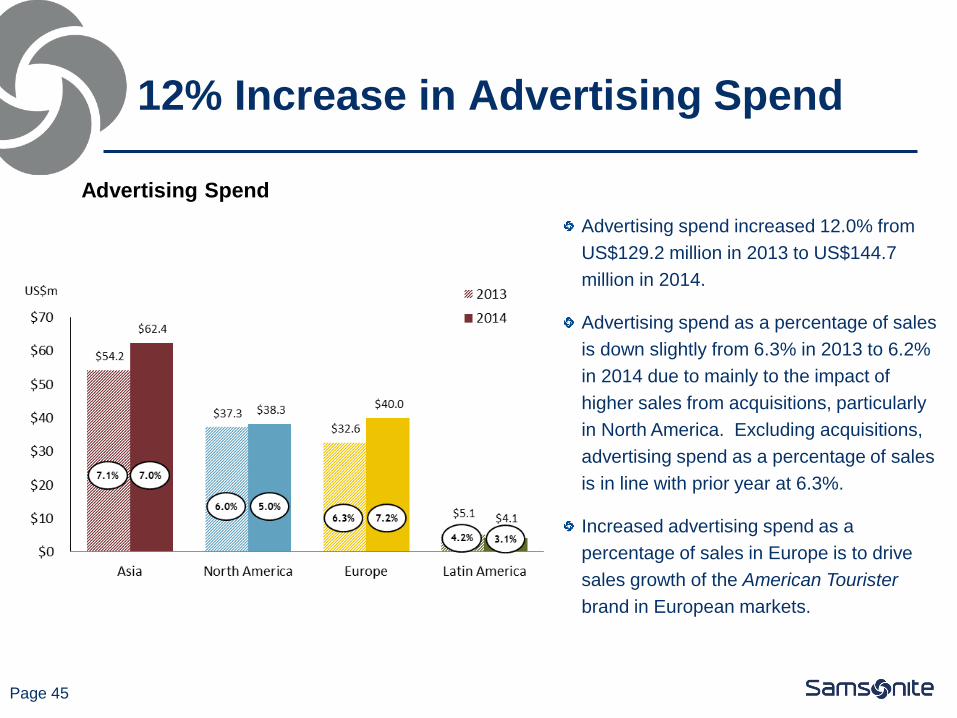

12% Increase in Advertising Spend

Advertising Spend

Advertising spend increased 12.0% from

US$129.2 million in 2013 to US$144.7

million in 2014.

Advertising spend as a percentage of sales

is down slightly from 6.3% in 2013 to 6.2%

in 2014 due to mainly to the impact of

higher sales from acquisitions, particularly

in North America. Excluding acquisitions,

advertising spend as a percentage of sales

is in line with prior year at 6.3%.

Increased advertising spend as a

percentage of sales in Europe is to drive

sales growth of the American Tourister

brand in European markets.

Targeted Brand Advertising

Asia - Samsonite

Page 46

Airport Billboards – Melbourne/Sydney, Australia

Highway Billboards – Sydney/Melbourne, Australia

Airport Billboard/lightbox – Delhi, India

Airport Billboard/lightbox – Hyderabad, India

Highway Billboards – Bangalore, India POS Displays - AnYang, Gyeonggi-do, Korea

On TV

Train Station Platform Digital Screen – Seoul, Korea

Page 47

Targeted Brand Advertising

Asia – American Tourister

Station Domination – Sydney Metro Station, Australia – “Take on the World” campaign featuring Prismo

Station Domination – Shenzhen Metro Station, China – “I Travel the World”

campaign featuring Cube Pop Billboards – Manila, Philippines - “I Travel the World”

campaign featuring Cube Pop with local ambassador

Window Display and POS Displays Station Domination – Guangzhou metro station, China – “I Travel the World” campaign featuring Cube Pop

On TV

Page 48

Targeted Product Advertising

North America - Samsonite

Airport Billboards – Chicago O’Hare, Illinois, USA

Train Billboards – Atlanta, Georgia, USA

Airport Billboards – Boston Logan, Massachusetts, USA

Print Media

Page 49

Targeted Brand Advertising

North America – American Tourister

Page 50

Targeted Product Advertising

Europe - Samsonite

POS Display (Live Windows) – Vienna, Austria

Airport Lightbox – Brussels Airport, Belgium Airport Billboards – Brussels Airport, Belgium Airport Billboards – Istanbul Airport, Turkey

Online and Social Media

Page 51

Targeted Product Advertising

Europe – American Tourister

Billboards - Picadilly Circus, UK

Billboards - Alexanderplatz Berlin, Germany

Airport Billboards – Istanbul Airport, Turkey

Targeted Product Advertising

Latin America

Page 52

Print Media

TV Exposure Social Media

Out-of-Home Placements

Page 53

Agenda

Results Highlights

Business Overview

Financial Overview

Outlook and Strategy for 2015

Q&A

Page 54

Excluding acquisitions, Adjusted EBITDA margin increased by approximately 20bp to

16.8%.

Net cash position of US$72.9 million with borrowing capacity on the revolving credit

facility of US$437.5 million as of December 31, 2014.

Net working capital efficiency of 12.7% continues to run better than target level of 14%.

Capital expenditure of US$69.6 million in 2014 is up from US$57.2 million in 2013, as

the Company invested in expanding its warehouse and production facilities in Europe

and expanded retail doors.

Reported net income attributable to the equity holders is up 5.8%, Adjusted Net Income

up 9.0%. Excluding FX loss(1) and stock compensation expense, Adjusted Net Income

is up 13.9% from 2013.

Basic earnings per share on an adjusted basis rose 9.7% from US$0.134 in 2013 to

US$0.147 in 2014.

The Board recommends a cash distribution of US$88.0 million or approximately

US$0.0625 per share, up 10% from the US$80.0 million distribution paid in 2014.

Key Financial Highlights

(1) FX loss represents the realized and unrealized net loss on the balance sheet translation of amounts not denominated in local currencies

Page 55

Strong Balance Sheet

Net cash decreased by US$137.0

million from US$209.8 million at

December 31, 2013 to US$72.9 million

at December 31, 2014 with cash flows

from operations of US$229.9 million

offset by outflows for acquisitions of

US$197 million (Speck US$85 million,

Gregory US$84 million and Lipault

US$28 million).

Continued strong working capital

efficiency of 12.7%.

Revolving credit facility expanded from

US$300 million to US$500 million in

June 2014. At December 31, 2014,

US$437.5 million is available to be

borrowed with US$60 million of

outstanding borrowings and the

utilization of US$2.5 million of the

facility for outstanding letters of credit

extended to certain creditors.

US$m December 31, December 31,

2014 2013

Cash and cash equivalents 140.4 225.3 (84.9) -37.7%

Trade and other receivables, net 290.8 246.4 44.5 18.0%

Inventories, net 332.3 298.4 33.9 11.4%

Other current assets 71.7 65.3 6.5 9.9%

Non-current assets 1,296.0 1,099.5 196.5 17.9%

Total Assets 2,131.3 1,934.9 196.4 10.2%

Current liabilities (excluding debt) 538.4 488.1 50.3 10.3%

Non-current liabilities (excluding debt) 220.3 202.5 17.7 8.8%

Total borrowings 65.1 13.7 51.5 376.3%

Total equity 1,307.4 1,230.6 76.9 6.2%

Total Liabilities and Equity 2,131.3 1,934.9 196.4 10.2%

Total Net Cash (Debt)(1) 72.9 209.8 (137.0) -65.3%

(1) Total Net Cash (Debt) excludes deferred financing costs, which are included in total borrowings

$ Chg Dec-14

vs. Dec-13

% Chg Dec-14

vs. Dec-13

Page 56

Efficiently Managing Working Capital

• Inventory turnover days calculated as ending inventory balance divided by cost of sales for the period and multiplied by the number of days in the period.

• Trade and other receivables turnover days calculated as ending trade and other receivables balance divided by sales for the period and multiplied by the number of days in the period.

• Trade payables turnover days calculated as ending trade payables balance divided by cost of sales for the period and multiplied by the number of days in the period.

Working capital continues to be managed

efficiently at 12.7% of sales at December

31, 2014.

Inventory turnover of 106 days is down 9

days from December 31, 2013.

Trade and other receivables turnover of

44 days is consistent with December 31,

2013.

Trade payables turnover of 100 days is

down 8 days from December 31, 2013

due largely to the timing of inventory

purchases and payments.

(1)

(1) 2014 net working capital as a percentage of sales and turnover days are adjusted for pro forma full year sales

and COGS of Lipault, Speck and Gregory.

US$m December 31, December 31,

2014 2013

Working Capital Items

Inventories 332.3$ 298.4$ 33.9$ 11.4%

Trade and Other Receivables 290.8$ 246.4$ 44.5$ 18.0%

Trade Payables 316.5$ 282.2$ 34.3$ 12.2%

Net Working Capital 306.6$ 262.6$ 44.0$ 16.8%

% of Net Sales 12.7% 12.9%

Turnover Days

Inventory Days 106 115

Trade and Other Receivables Days 44 44

Trade Payables Days 100 108

Net Working Capital Days 50 51

$ Chg Dec-14

vs. Dec-13

% Chg Dec-14

vs. Dec-13

Page 57

Capital Expenditure

Capital Expenditure by Project Type

2014 Retail Capex consists mainly of new

stores and remodels in Asia of US$12.9 million,

North America of US$7.2 million and Europe of

US$4.6 million with 85 net new company-owned

stores opened in 2014.

Capex on product development / R&D / Supply

includes US$11.6 million on manufacturing

facilities and equipment, US$7.3m on product

tooling and molds and US$7.0 million on

warehousing in Europe. US$2.8 million was

spent on tooling and equipment for Speck.

Information Services and Facilities consists

largely of retail and e-commerce software and

finance and business intelligence system

enhancements.

US$m 2014 2013

Retail 27.9 20.5

Product Development / R&D/ Supply 32.4 23.5

Information Services and Facilities 7.2 11.0

Other 2.1 2.2

Total Capital Expenditures $69.6 $57.2

Page 58

Shareholder Information and

Distribution to Shareholders

On January 7, 2015, the Group granted 16,006,812 options to certain directors, key management personnel, and other

employees.

On January 7, 2015, the Group granted an additional 10,040,399 options with a longer term vesting schedule to an Executive

Director and to five additional members of the Group’s senior management team.

Shares outstanding 1,408,026,456

Stock Price (HK$) 23.09

Amounts below stated in US$

2014 Basic EPS (US$) $0.132

2014 Adjusted EPS (US$) $0.147

Recommended distribution to shareholders (US$) $88,000,000

Payout ratio 47.2%

Distribution per share (US$) $0.0625

Distribution yield* 2.10%

*Assumes stock price of HK$23.09 at an exchange rate of 7.755HKD/USD

Shareholder Information as of December 31, 2014

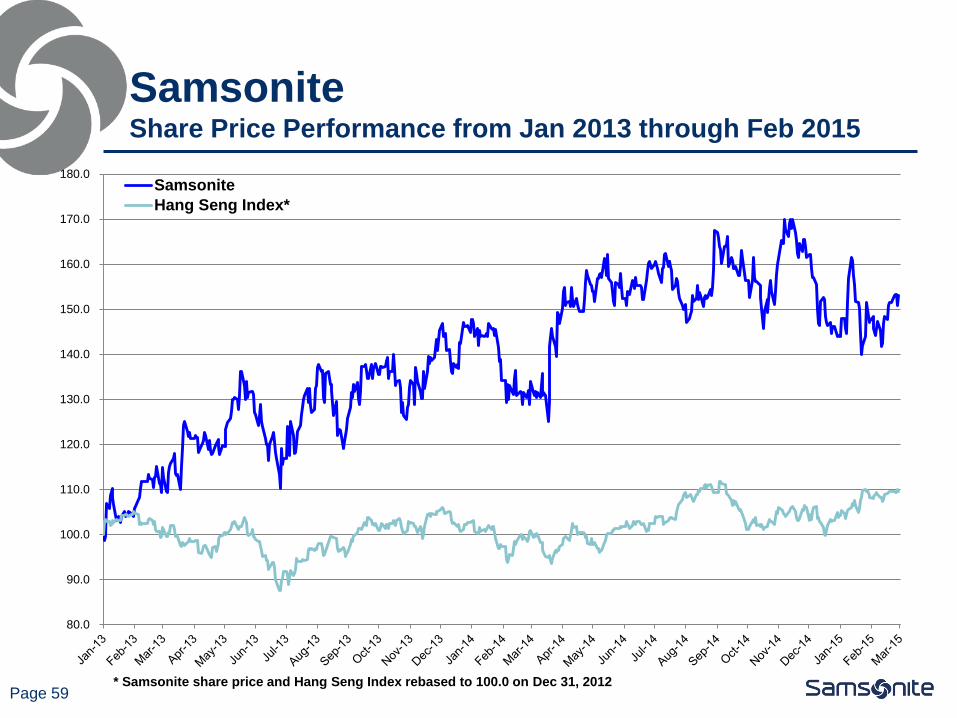

Page 59 * Samsonite share price and Hang Seng Index rebased to 100.0 on Dec 31, 2012

Samsonite Share Price Performance from Jan 2013 through Feb 2015

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0Samsonite

Hang Seng Index*

Page 60

Agenda

Results Highlights

Business Overview

Financial Overview

Outlook and Strategy for 2015

Q&A

Engines Of Future Growth

Page 61

Continuing global expansion of travel & tourism

“UNWTO forecasts international tourist arrivals to grow between 3% and 4% in 2015. By region, growth

is expected to be strongest in the Americas and in Asia and the Pacific (both +4% to +5%), and

somewhat more moderate in Europe (+3% to +4%)”(1).

Increase the proportion of sales from our direct-to-consumer channels by growing our e-commerce sales and

expanding our retail presence.

Raise the Hartmann brand in the premium and luxury segments of North America, Asia and Europe by offering a

full category assortment of exceptional products supported by brand marketing and retail expansion.

Implement synergies and execute on market opportunities for newly acquired brands to further diversify our

product offering into non-travel categories.

Continue to invest in our core brands with exciting products, new materials and increased marketing spend.

Tactfully deploy multiple brands to operate wider price points and wider consumer demographics in each

category.

Continue to explore strategic M&A opportunities in adjacent spaces to gain distribution in less represented

markets or to grow direct-to-consumer sales.

We see merit in continuing and even strengthening our existing strategy of developing Samsonite into a well

diversified multi-brand, multi-category and multi-channel bag and luggage business.

(1) Source: UNWTO World Tourism Barometer, Volume 13, January 2015

Page 62

Agenda

Results Highlights

Business Overview

Financial Overview

Outlook and Strategy for 2015

Q&A

Recommended