Copyright IDC. Reproduction is forbidden unless authorized. All rights reserved.

Israel Datacenter Trends and Strategies 2011Israel Datacenter Trends and Strategies 2011

Gideon LopezIDC Israel

04/18/23© IDC

Agenda

2

04/18/23© IDC

New Business Cycle for ITConvergence and Clouds Reign for the Next 10 Years

19901985 1995

Mainframe/m

inicomputer

Integrated architecture

2000 2005 2010

Integrated architecture

Unix/RISC

Modular archite

cture

Transactional applications

and Database

ERP, Analytics and Datamarts

Application Development

Web

File/Print and Networking

Collaborative

Integrated

architecture

x86

Modular archite

cture

2015

Microservers?

Compute/Memory

Boards?

Modular

architecture

Bu

sin

ess

Val

ue

Converged Infrastructure

& Private Clouds

PublicClouds

Virtualizatio

n

Virtualizatio

n

Lower Cost of Computing Per Unit of Work

3

04/18/23© IDC

3.0% Servers

6.7% Servers

11.9% Servers

Israel Server Installed Base (‘000)

Thousands of Servers

Virtualization Management

Gap

Changing Realities in the Datacenter

Source: IDC Israel, 2012

04/18/23© IDC

New Economic Model for the DatacenterShifts to Automation Tools are a Requirement

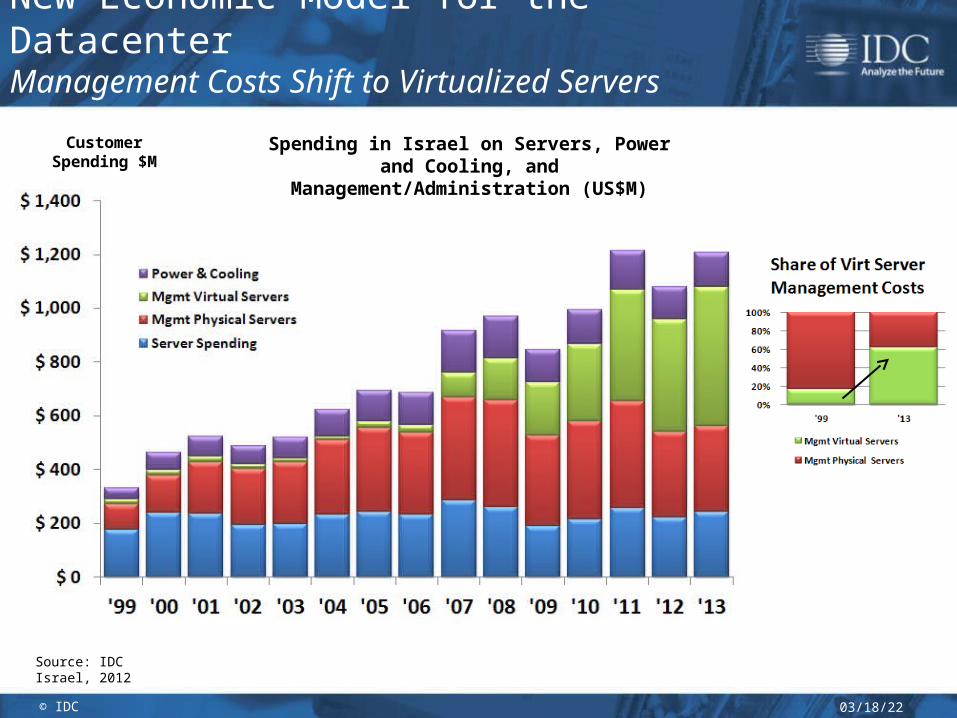

Spending in Israel on Servers, Power and Cooling, and Management/Administration (US$M)

Customer Spending $M

Source: IDC Israel, 2012

04/18/23© IDC

Customer Spending $M

New Economic Model for the DatacenterManagement Costs Shift to Virtualized Servers

Spending in Israel on Servers, Power and Cooling, and Management/Administration (US$M)

Source: IDC Israel, 2012

04/18/23© IDC

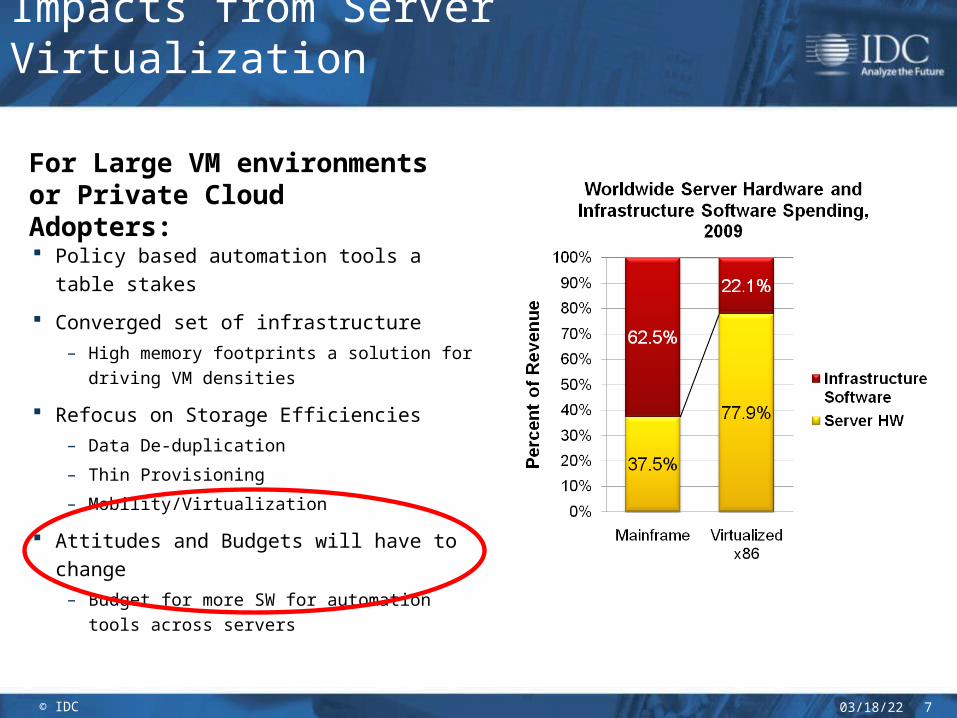

Impacts from Server Virtualization

Policy based automation tools a table stakes

Converged set of infrastructure

– High memory footprints a solution for driving

VM densities

Refocus on Storage Efficiencies

– Data De-duplication

– Thin Provisioning

– Mobility/Virtualization

Attitudes and Budgets will have to change

– Budget for more SW for automation tools

across servers

For Large VM environments or Private Cloud Adopters:

7

04/18/23© IDC 8

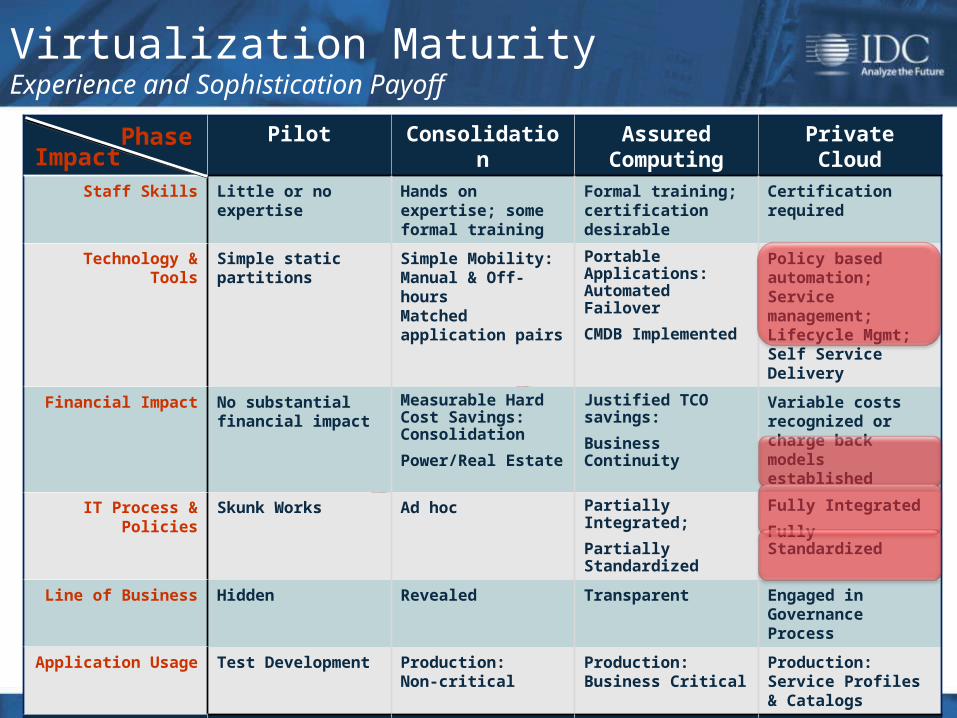

Pilot Consolidation Assured Computing

Private Cloud

Staff Skills Little or no expertise

Hands on expertise; some formal training

Formal training; certification desirable

Certification required

Technology & Tools

Simple static partitions

Simple Mobility:Manual & Off-hoursMatched application pairs

Portable Applications: Automated Failover

CMDB Implemented

Policy based automation; Service management; Lifecycle Mgmt; Self Service Delivery

Financial Impact No substantial financial impact

Measurable Hard Cost Savings: Consolidation

Power/Real Estate

Justified TCO savings:

Business Continuity

Variable costs recognized or charge back models established

IT Process & Policies

Skunk Works Ad hoc Partially Integrated;

Partially Standardized

Fully Integrated

Fully Standardized

Line of Business Hidden Revealed Transparent Engaged in Governance Process

Application Usage Test Development Production: Non-critical

Production: Business Critical

Production: Service Profiles & Catalogs

% of Customers 15% 55% 25% 5%

Average VM Density

4 6 10 35

Experience 9-12 months 9 months - 2 years 1.5 - 3 years 3-5 years

% Virtualized Servers

<10% 25% 50% 80%

Virtualization MaturityExperience and Sophistication Payoff

PhaseImpact

04/18/23© IDC

Top 10 Datacenter Efficiency Strategies

1. Virtualization2. Site Rationalization and Consolidation3. Operational Best Practices4. Automation Tools and Software5. Datacenter Redesign6. Application Rationalization7. Modular Datacenter Construction8. Lifecycle Management and Planning9. Rack-based Power and Cooling Retrofit10. Architectural and Technology Refresh

Continuous Improvement

Less interest in long term strategies; more emphasis on making incremental changes that drive new organizational

behaviors and processes

Understand how all these changes fit together for

greatest payback

9

04/18/23© IDC

Evolving Datacenter Construction:Modularity is the New Industry Standard

Containerized Brick and MortarHybrid

10

04/18/23© IDC

Datacenter Build-out & ProvisioningClasses of Applications Matter

High Availability

High-Density Blade

Standard

Standard

Database

The days of the monolithic datacenter are numbered

WaterPowerNetwork Datacenter

Central Nervous System

11

04/18/23© IDC

Millions

Israel Installed Server KWh by Datacenter Type, 2007-2013Includes Power Consumed and Cooling Required

Major Datacenter efficiency moves done in enterprise (inc. government & SP)

Source: IDC Israel, 2012

04/18/23© IDC

Datacenter Infrastructure (DCIM) Management Moving beyond Excel and Visio

Measure and Monitor Datacenter KPI’s•Space

•Power

•Cooling

•Security

•Environmentals

13

04/18/23© IDC 14

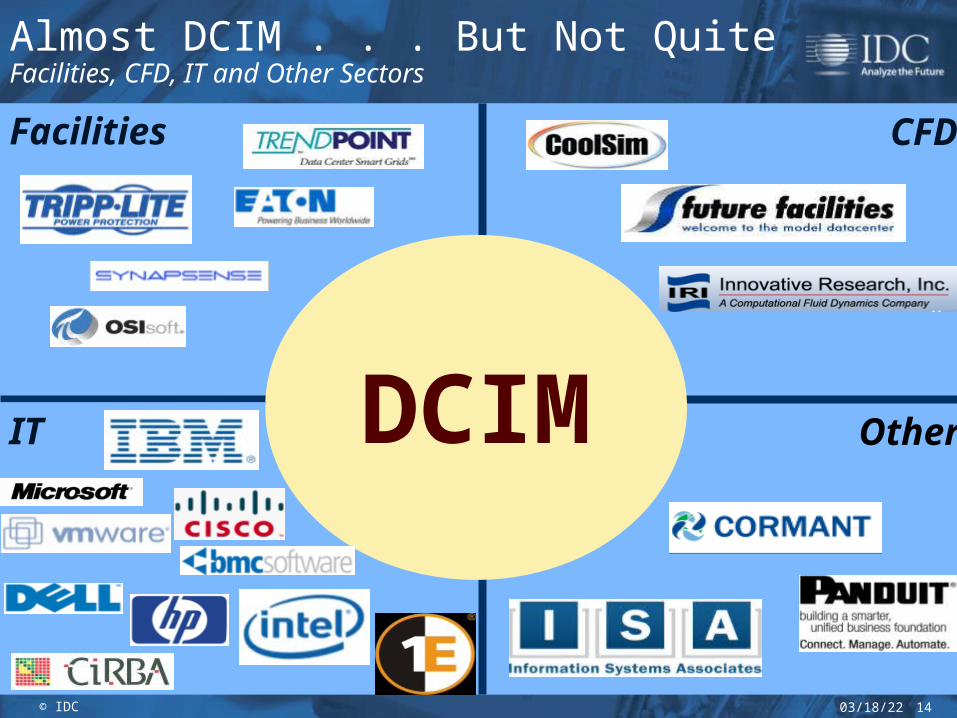

Almost DCIM . . . But Not QuiteFacilities, CFD, IT and Other Sectors

DCIM

CFD

Other

Facilities

IT

04/18/23© IDC

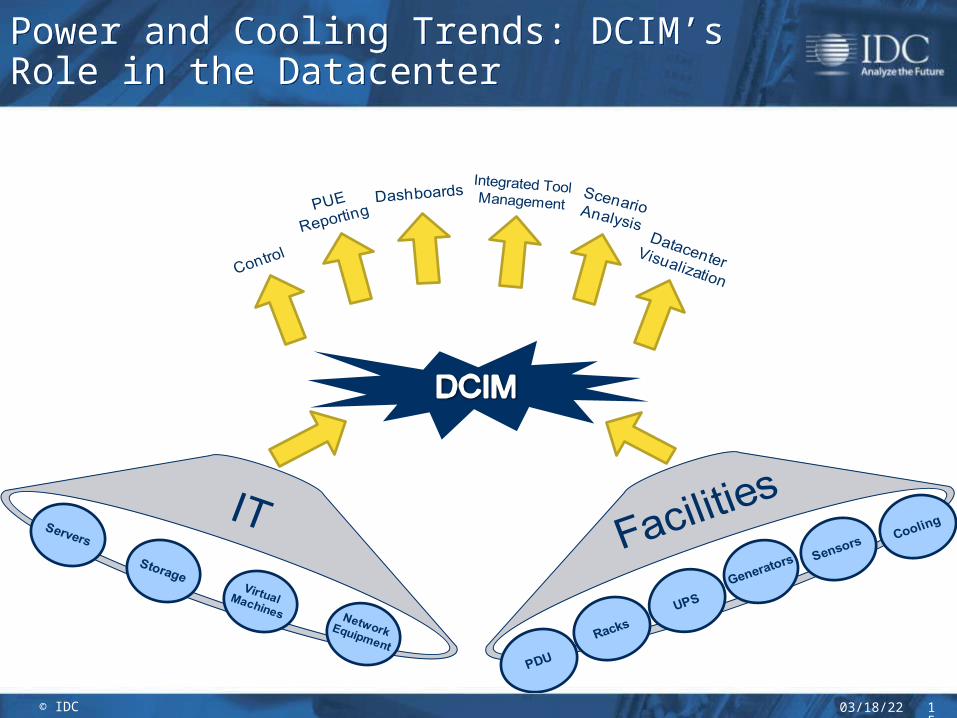

Power and Cooling Trends: DCIM’s Role in the DatacenterPower and Cooling Trends: DCIM’s Role in the Datacenter

15

04/18/23© IDC

$0

$100

$200

$300

$400

$500

$600

2010 2011 2012 2013 2014 2015

Software Services

Datacenter Infrastructure Management Forecast 2010-2015Datacenter Infrastructure Management Forecast 2010-2015

16

Worldwide Packaged Software and Services DCIM Revenue Forecast ($M)

CAGR 2010-2015 = 25.5%• DCIM is a rapidly evolving

market with a CAGR of over 25%

• The majority of revenue is from software with services representing 46% of revenues in 2010, decreasing to 30% by 2015

• Cloud computing, increased deployment model competition, and availability concerns are drivers of DCIM in enterprise and service provider environments.

04/18/23© IDC

Essential Guidance

Server virtualization is outpacing management & automation – This often creates more drain than gain. Investing in virtualization management is not a

luxury

There is no one solution for datacenter design– Business oriented analysis of different application groups – what needs to stay where

and why– Flexibility in design will allow more rapid adaptation of datacenter to business needs

It’s all about management– Datacenter Infrastructure Management is not another software solution, but the focal

point through which IT infrastructure is aligned with business– IT is but one element in these solutions and we are still some distance from fully

integrated DCIM

17

Recommended