California Municipal Utilities Association

Annual Conference

March 30, 2011

Daniel S. Hentschke, General Counsel

San Diego County Water Authority

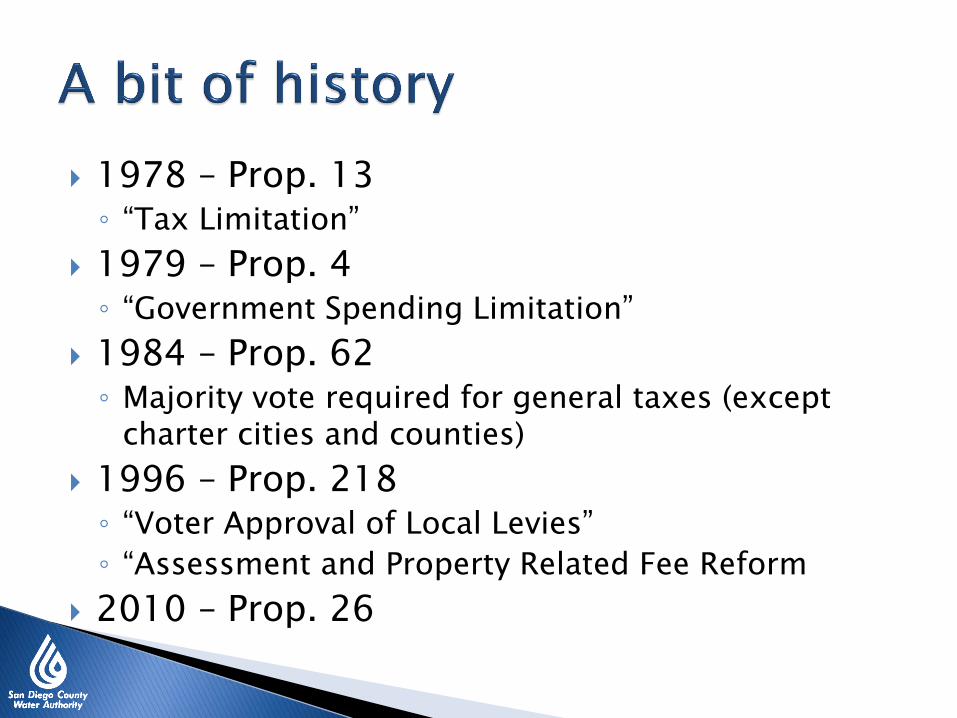

1978 – Prop. 13 ◦ “Tax Limitation”

1979 – Prop. 4 ◦ “Government Spending Limitation”

1984 – Prop. 62 ◦ Majority vote required for general taxes (except

charter cities and counties)

1996 – Prop. 218 ◦ “Voter Approval of Local Levies”

◦ “Assessment and Property Related Fee Reform

2010 – Prop. 26

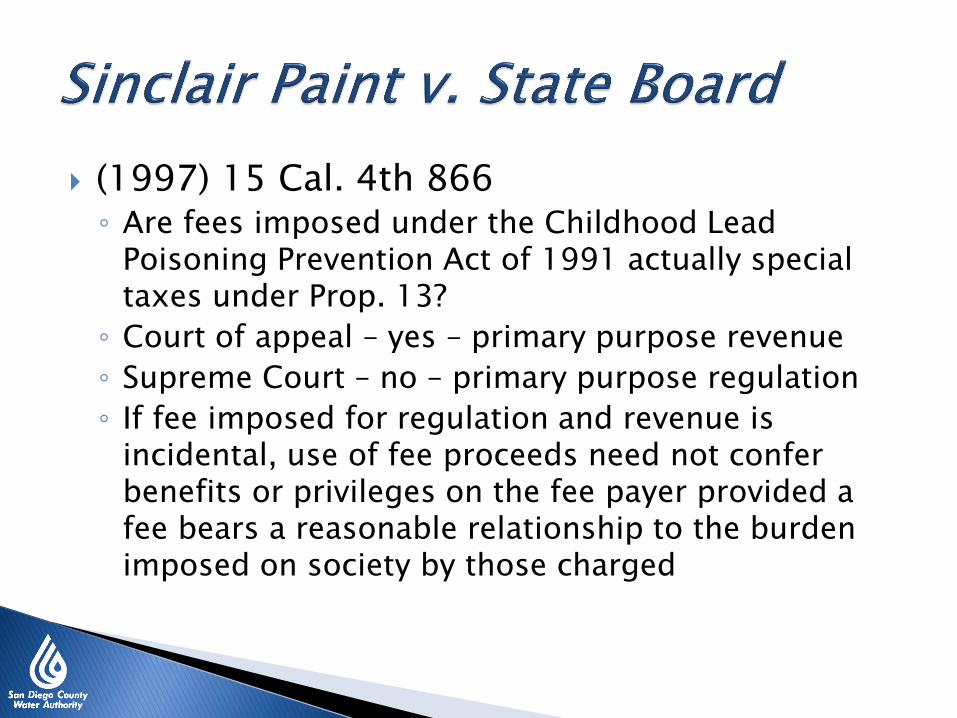

(1997) 15 Cal. 4th 866 ◦ Are fees imposed under the Childhood Lead

Poisoning Prevention Act of 1991 actually special taxes under Prop. 13?

◦ Court of appeal – yes – primary purpose revenue

◦ Supreme Court – no – primary purpose regulation

◦ If fee imposed for regulation and revenue is incidental, use of fee proceeds need not confer benefits or privileges on the fee payer provided a fee bears a reasonable relationship to the burden imposed on society by those charged

Despite Prop. 13 and Prop. 218 “California taxes have continued to escalate.”

“Legislature and local government have disguised new taxes as „fees‟” to avoid voter approval.

Fees that exceed reasonable cost of actual regulation, or simply raise revenue for a new program, or are not part of a licensing or permitting program are taxes.

Taxes defined so government cannot avoid restrictions by adopting “fees.”

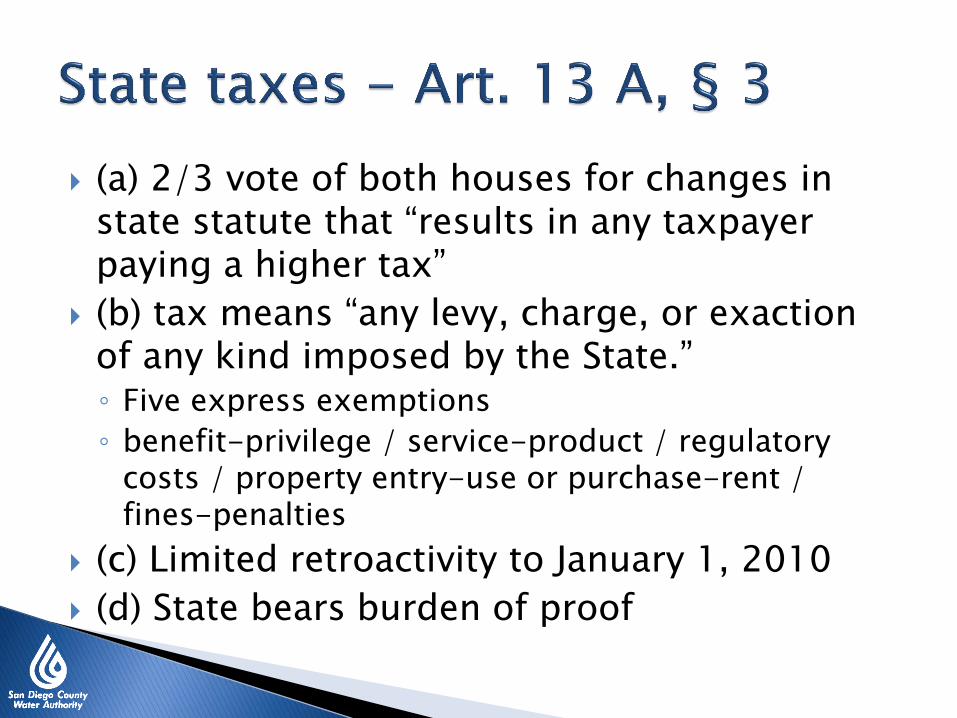

(a) 2/3 vote of both houses for changes in state statute that “results in any taxpayer paying a higher tax”

(b) tax means “any levy, charge, or exaction of any kind imposed by the State.” ◦ Five express exemptions

◦ benefit-privilege / service-product / regulatory costs / property entry-use or purchase-rent / fines-penalties

(c) Limited retroactivity to January 1, 2010

(d) State bears burden of proof

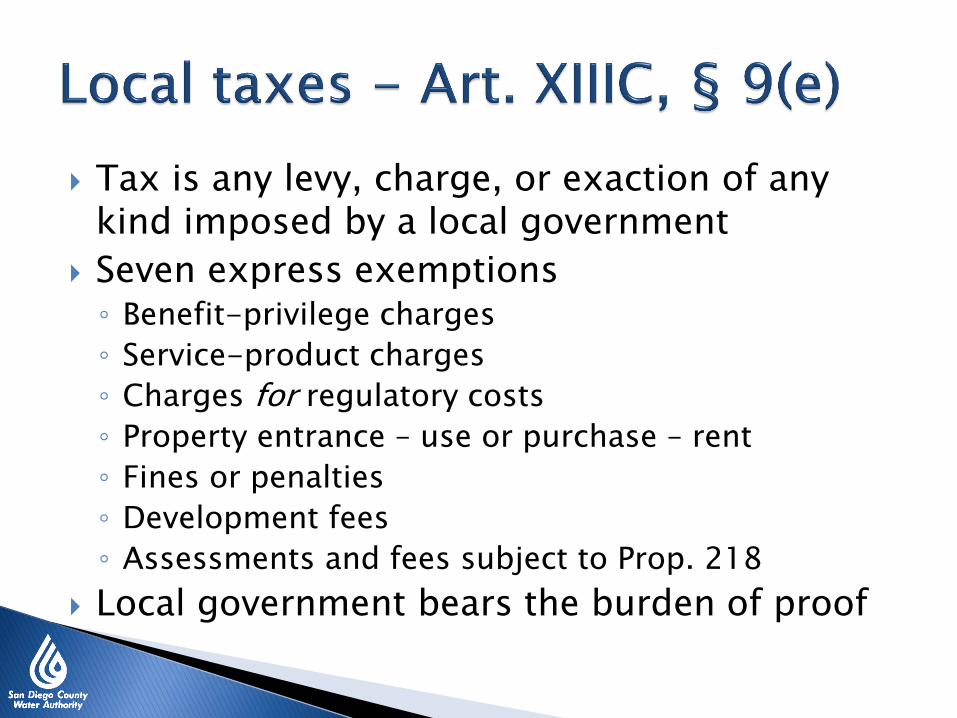

Tax is any levy, charge, or exaction of any kind imposed by a local government

Seven express exemptions ◦ Benefit-privilege charges

◦ Service-product charges

◦ Charges for regulatory costs

◦ Property entrance – use or purchase – rent

◦ Fines or penalties

◦ Development fees

◦ Assessments and fees subject to Prop. 218

Local government bears the burden of proof

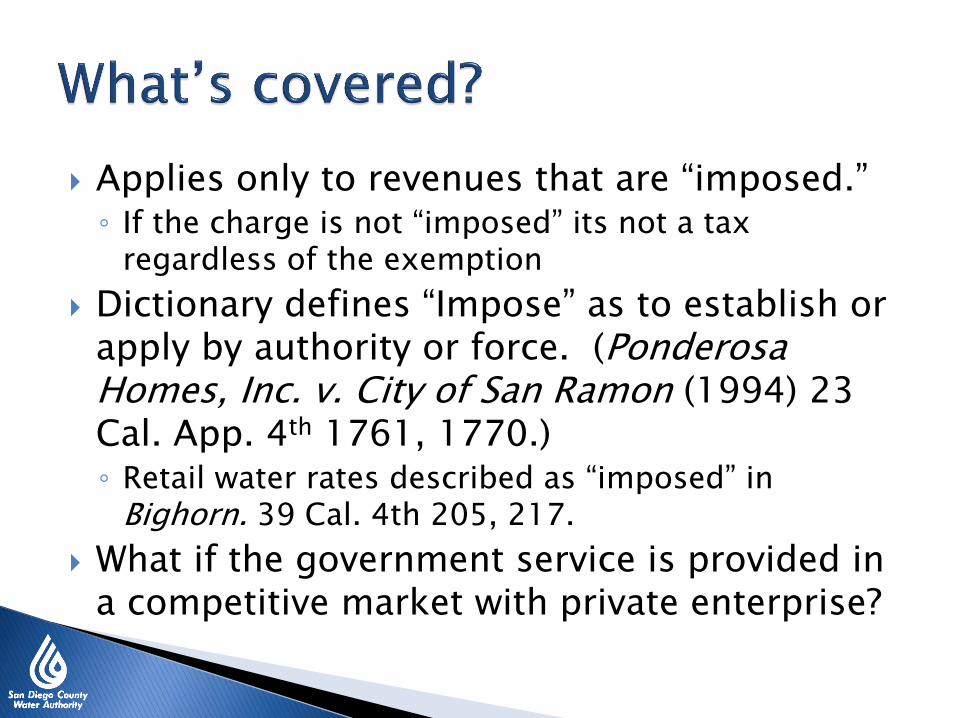

Applies only to revenues that are “imposed.” ◦ If the charge is not “imposed” its not a tax

regardless of the exemption

Dictionary defines “Impose” as to establish or apply by authority or force. (Ponderosa Homes, Inc. v. City of San Ramon (1994) 23 Cal. App. 4th 1761, 1770.) ◦ Retail water rates described as “imposed” in

Bighorn. 39 Cal. 4th 205, 217.

What if the government service is provided in a competitive market with private enterprise?

General rule ◦ taxes benefit the public as a whole and are not

allocated according to benefits received

◦ fees for benefits, privileges, service, or products benefit a discrete group and are allocated based on actual or anticipated use

Prop. 26 exemption ◦ charge for benefit granted or service provided

“directly to the payor that is not provided to those not charged”

◦ does not exceed the reasonable cost to the local government of providing (granting) the service (benefit)

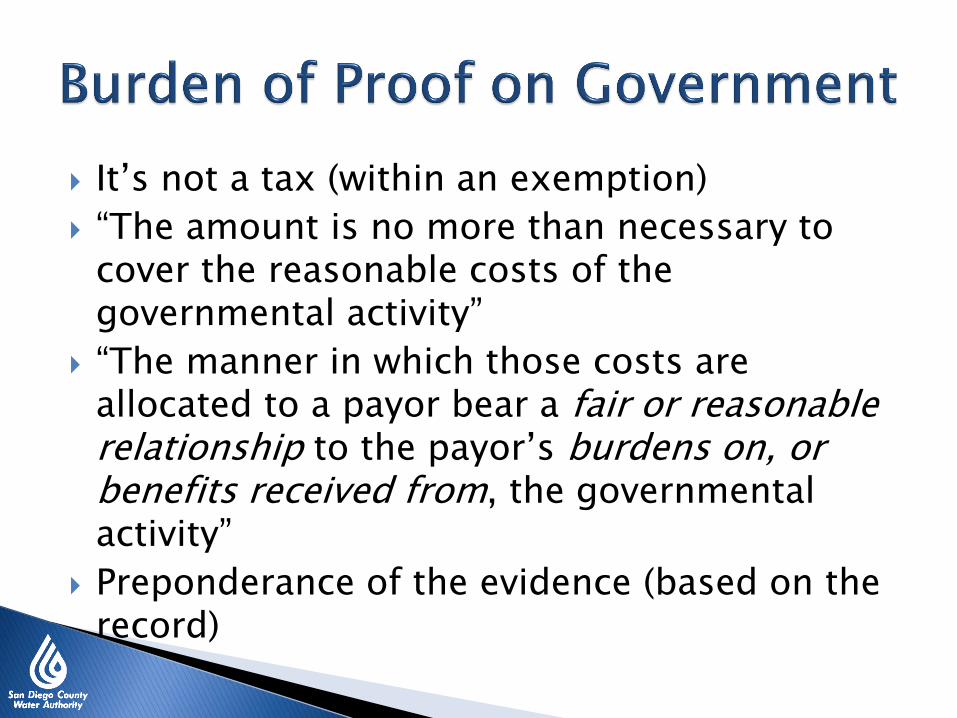

It‟s not a tax (within an exemption)

“The amount is no more than necessary to cover the reasonable costs of the governmental activity”

“The manner in which those costs are allocated to a payor bear a fair or reasonable relationship to the payor‟s burdens on, or benefits received from, the governmental activity”

Preponderance of the evidence (based on the record)

Charges for on-going domestic water service are subject to Prop. 218 ◦ But not connection or capacity charges

Electric and gas service exempt from Prop. 218 ◦ But not from Prop. 26

Art. XIII D, § 6 (b) has express substantive “cost of service” requirements ◦ But Prop. 26 has more general language

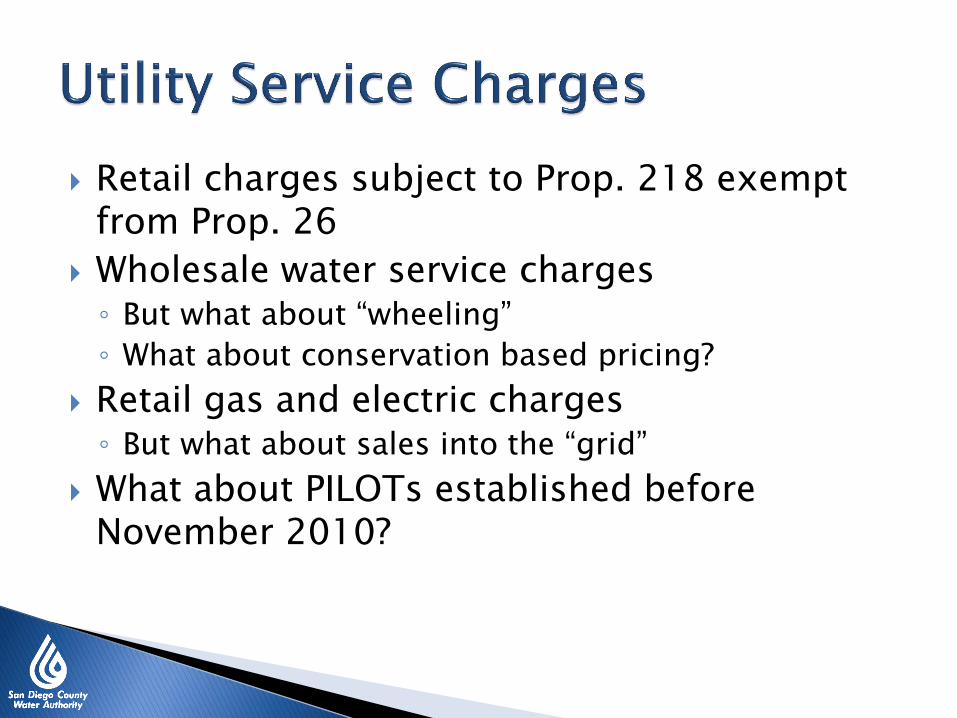

Retail charges subject to Prop. 218 exempt from Prop. 26

Wholesale water service charges ◦ But what about “wheeling”

◦ What about conservation based pricing?

Retail gas and electric charges ◦ But what about sales into the “grid”

What about PILOTs established before November 2010?

Free/discounted services ◦ OK if funded by non-fee revenues

◦ Subsidies problematic, but may have different prices for different services

Inflation adjustments ◦ Gov‟t Code 53750(h)(2)(A)

◦ Prop. 26 amends Prop. 218

◦ Greene v. Marin Co. Flood Control etc. Dist. 49 Cal. 4th 277

Creating the record ◦ Preponderance of the evidence

Public goods charges ◦ If pursuant to a preexisting statutory mandate then

maybe ok

◦ If new, likely taxes

AB 32 ◦ H&S Code § 38597 authorizes CARB to impose fees

◦ CARB adopted fees in 2009; OAL approved 6/17/10

◦ Prop. 26 applies to “state statutes” not regulations

◦ Prop. 26 retroactive for State taxes adopted after 1/1/10 – “reenacted by the Legislature

Recommended