Australian Farmland Values2017

32

This report is intended to provide general information on a particular subject or subjects and is not an exhaustive treatment of such subject(s). The information herein is believed to be reliable and has been obtained from public sources believed to be reliable. Rural Bank Limited, ABN 74 083 938 416 AFSL / Australian Credit Licence 238042 makes no representation as to or accepts any responsibility for the accuracy or completeness of information contained in this report. Any opinions, estimates and projections in this report do not necessarily reflect the opinions of Rural Bank and are subject to change without notice. Rural Bank has no obligation to update, modify or amend this report or to otherwise notify a recipient thereof in the event that any opinion, forecast or estimate set forth therein, changes or subsequently becomes inaccurate. This report is provided for informational purposes only. The information contained in this report does not take into account your personal circumstances and should not be relied upon without consulting your legal, financial, tax or other appropriate professional.

© Copyright Rural Bank Ltd ABN 74 083 938 416 and Bendigo and Adelaide Bank Ltd ABN 11 068 049 178 (BEN50RBMB021) (04/18)

Executive Summary 4

State Performance 5

New South Wales 6

Queensland 14

Victoria 22

Western Australia 30

South Australia 38

Tasmania 46

Northern Territory 52

About the Research 54

Contents

3

Understanding farming’s most valuable asset is

important to everyone in agribusiness, especially Australia’s farmers. The

Australian Farmland Values report tells the story of national and regional

farmland performance over the past 23 years.

54

Executive summaryThe value of farmland underpins farming businesses and rural communities. Understanding farmland value is important because it reflects the strength and confidence of agricultural industries.

The Australian Farmland Values 2017 report is our third national edition providing analysis at state, region and municipality level, and is based on data compiled since 1995. The analysis tracks the median price of commercial farmland in dollars per hectare by eliminating, where possible, metropolitan and small block sales as well as sales where one party has compulsory powers.

The analysis draws on over 239,000 transactions, accounting for 288 million hectares of land with a combined value of $139.8 billion over 23 years.

The national median farmland price increased by 7.1 per cent in 2017. This follows a 9.3 per cent increase in 2016 and a 5.3 per cent increase in 2015. The average annual five year growth in median value per hectare is 5.1per cent.

The performance of farmland prices in different states was mixed in 2017. The median farmland price increased in Tasmania (+19.3 per cent), South Australia (+17.1 per cent), Victoria (+9.5 per cent) and New South Wales (+8.8 per cent). A decrease in median value per hectare was recorded in Queensland (-2.8 per cent), Western Australia (-6.5 per cent) and the Northern Territory (-35.1 per cent), compared to the previous year.

The volume of transactions in Tasmania and South Australia increased significantly in 2017. This altered the mix of properties traded, with a greater percentage of high value transactions compared to previous years leading to a growth in median value per hectare. The transaction volume in Victoria increased slightly, and the mix of properties that sold remained similar to 2016. In New South Wales, the transaction volume decreased slightly but the growth in median value per hectare was evident across most parcel sizes. The transaction volume was flat in Queensland with smaller parcel sizes recording a growth in median price, while larger parcels of land dropped. In Western Australia, the transaction volume decreased with both small and large parcel sizes recording a decline in median price, however value did increase for mid-sized parcels of land.

Taking a long term view of the performance of Australian farmland values is appropriate given the cyclical and often volatile climate and market conditions that characterise farming in Australia. The relevance of this view is further supported when considering that farming is usually considered as a long-term career by Australian farmers.

FARMLAND PERFORMANCE (average annual median price growth)

2015 5.3%

2016 9.3%

2017 7.1%

5 years 5.2%

10 years 2.9%

20 years 6.6%

5

5.0%WA

5.2%NT

6.3%QLD

7.0%NSW

6.5%VIC

7.7%TAS

6.3%SA

Farmland prices are a function of many variables including, but not limited to:

• rainfall

• location

• agricultural industry

• productivity

• land quality

• sentiment

• interest rates

• commodity prices

• the performance of the wider economy.

Isolating the reason for a particular movement in the median price for a region is complex. Therefore, the focus of this report is to describe regional and state trends more so than the drivers behind the observed trends.

Median prices are only a guide to market activity. This report is not intended for use as a valuation tool. A qualified professional is required to assess the value of a property.

Average annual growth in farmland median prices over 20 years

76

New South Wales

6.4%New South Wales

Average annual growth over 5 years

Western

5.6%

Northern

7.0%

Central

4.0%

Southern

6.9%South East

6.2%

AVERAGE ANNUAL MEDIAN PRICE GROWTH

2017 8.8%

5 years 6.4%

10 years 4.0%

20 years 7.0%

Average annual growth over five years

7

The median value of farmland in New South Wales (NSW) increased by 8.8 per cent to $3,946/ha in 2017, following a 10.1 per cent increase in 2016.

The median value per hectare has recorded positive growth for the last four years, averaging 9.1 per cent since 2014.

Transaction volume has remained flat, indicating a plateau of supply which has led to increased demand from NSW buyers.

In 2017, the estimated number of farmland transactions was 3,740, a decrease of 4.7 per cent compared to 2016.

Approximately 2.2 million hectares of farmland was traded in 2017, an increase of 13 per cent compared to 2016. The area of farmland traded has increased for the last three consecutive years.

The total value of farmland value traded in NSW was approximately $3.7 billion in 2017.

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$3,500

$1,500

$2,000

$4,000

$2,500

$500

$4,500

$3,000

$1,000

4,000

1,000

5,000

2,000

6,000

3,000

New South Wales

Number of transactions (RHS) Median $/ha (LHS)

98

The mix of parcel sizes traded in 2017 was largely unchanged, however volume was down across all parcel sizes except for the 300-499 hectare bracket, which reported an increase of 2.6 per cent.

‘There were fewer listings in 2017, however demand remained strong. A greater percentage of off-market sales occurred with robust demand from domestic and international investors. Commodity prices, interest rates and debt levels are key drivers of current land value trends.’

Richard Gemmell, Elders.

New South Wales

The median price increased across all parcel sizes in 2017. Smaller parcels between:

• 30-99 hectares increased by 5.1 per cent

• 100-299 hectares increased by 12.7 per cent

• 300-499 hectares increased by five per cent

• 500+ hectares increased by 24 per cent.

Performance by land size

Parcel size (ha)

2013 2014 2015 2016 2017

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

30-99 37% 5,240 41% 5,876 43% 6,410 44% 7,104 43% 7,467

100-299 31% 2,530 30% 2,719 28% 2,818 27% 3,007 27% 3,388

300-499 12% 1,889 10% 1,963 11% 2,026 10% 2,188 10% 2,297

500+ 20% 1,259 19% 991 18% 1,249 19% 1,349 19% 1,672

Overall 3,594 2,789 3,843 2,989 3,825 3,294 3,924 3,628 3,740 3,946

Trans = Transactions

Over the last five years the 500+ hectare bracket has averaged 10.1 per cent growth in median value:

• 30-99 hectares 6.6 per cent

• 100-299 hectares six per cent

• 300-499 hectares 2.6 per cent.

9

1995

1995

1995

2003

2003

2003

1999

1999

1999

2007

2007

2007

2014

2014

2014

1996

1996

1996

2004

2004

2004

2011

2011

2011

2000

2000

2000

2008

2008

2008

2015

2015

2015

1997

1997

1997

2005

2005

2005

2012

2012

2012

2001

2001

2001

2009

2009

2009

2016

2016

2016

1998

1998

1998

2006

2006

2006

2013

2013

2013

2002

2002

2002

2010

2010

2010

2017

2017

2017

0

0

0

0

0

0

$3,500

$1,500$2,000

$4,000

$2,500

$500

$4,500$5,000

$3,000

$1,000

$140

$60

$80

$100

$20

$120

$40

$5,000

$1,000

$2,000

$3,000

$4,000

$6,000

1,500

2,000

500

2,500

1,000

80

800

2010

30

200

90

1,000

4050

400

100

1,200

6070

600

Northern

Western

South East

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

1110

1995

1995

2003

2003

1999

1999

2007

2007

2014

2014

1996

1996

2004

2004

2011

2011

2000

2000

2008

2008

2015

2015

1997

1997

2005

2005

2012

2012

2001

2001

2009

2009

2016

2016

1998

1998

2006

2006

2013

2013

2002

2002

2010

2010

2017

2017

0

0

0

0

1,200

600

200

1,6001,400

1,800

800

400

$3,500

$1,500

$2,000

$2,500

$500

$3,000

$1,000

$3,500

$1,500

$2,000

$2,500

$500

$3,000

$4,000

$1,000

2,000

800

200

1,000

400

1,200

600

1,000

Southern

Central

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

New South Wales

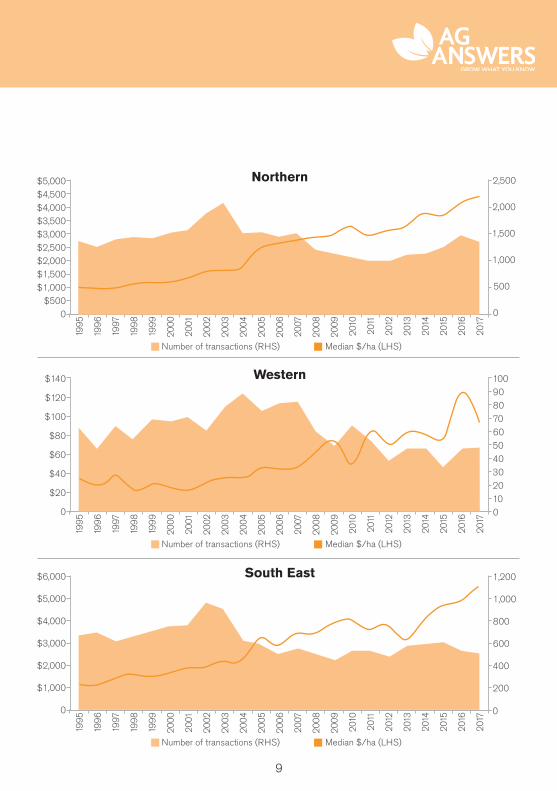

The median value per hectare in Northern NSW increased by 6.1 per cent in 2017. The volume of transactions fell by eight per cent. The increase in median price was due to growth in the median price in the municipalities of Walgett, Uralla and Gunnedah. Central NSW values increased by 6.8 per cent and transaction volume decreased by five per cent. Municipalities that contributed to the increase in median value included Parkes, Warren and Gilgandra. In Western NSW, median value decreased by

25.7 per cent in 2017 and transaction volume was flat. The municipalities of Balranald and Cobar contributed to the decline. The median price in South East NSW increased by eight per cent and transaction volume increased 1.6 per cent. The municipalities of Yass Valley and Upper Lachlan led growth in values in the region. Southern NSW values increased by 24.3 per cent in 2017 while transaction volume decreased by 1.2 per cent. The municipalities of Murray River, Carrathool and Murrumbidgee led the growth in median price.

11

Farmland sales by municipality – New South Wales

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Albury* Southern 4,720 2

Armidale Northern 2,987 3,649 59

Ballina Northern 13,318 11,450 14

Balranald Western 159 148 6

Bathurst Central 5,592 4,166 54

Bega Valley South East 7,129 6,591 61

Bellingen Northern 8,963 9,356 28

Berrigan Southern 4,188 3,571 9

Bland Southern 1,882 1,630 58

Blayney Central 9,562 7,134 17

Bogan Central 445 405 13

Bourke Western 77 72 8

Brewarrina Western 198 186 7

Byron* Northern 16,134 3

Cabonne Central 6,215 5,150 53

Carrathool Southern 1,222 991 19

Central Darling Western 79 63 9

Cessnock Central 9,589 11,525 39

Clarence Valley Northern 5,159 5,069 181

Cobar Western 124 111 14

Coffs Harbour Northern 13,941 9,505 14

Coolamon Southern 3,996 3,210 13

Coonamble Central 1,483 1,265 29

Cootamundra-Gundagai Southern 4,786 4,050 38

Cowra Central 5,741 5,237 44

Dubbo Central 2,321 2,455 55

Dungog Central 6,902 7,315 53

Edward River Southern 2,768 2,643 34

Eurobodalla South East 11,357 9,630 25

Federation Southern 4,764 3,799 15

1312

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Forbes Central 2,948 2,579 31

Gilgandra Central 2,115 1,752 29

Glen Innes Severn Northern 3,295 2,940 48

Goulburn Mulwaree South East 8,073 7,889 84

Greater Hume Southern 5,507 4,897 52

Griffith Southern 1,931 2,422 5

Gunnedah Northern 5,244 4,510 53

Gwydir Northern 2,153 1,952 67

Hay Southern 429 446 10

Hilltops Southern 3,815 3,964 62

Inverell Northern 2,748 2,639 73

Junee Southern 5,181 4,298 6

Kempsey Northern 6,301 5,711 67

Kyogle Northern 4,873 4,756 90

Lachlan Central 1,159 1,047 49

Leeton Southern 3,202 2,878 16

Lismore Northern 10,266 9,652 48

Lithgow Central 5,730 6,503 45

Liverpool Plains Northern 3,992 3,980 27

Lockhart Southern 4,692 3,717 18

Maitland Central 13,876 15,417 4

Mid-Coast Central 8,646 7,529 209

Mid-Western Central 3,424 3,158 114

Moree Plains Northern 3,099 2,962 52

Murray River Southern 2,299 1,851 52

Murrumbidgee Southern 2,985 2,362 34

Muswellbrook Central 7,295 7,533 33

Nambucca Northern 6,406 7,227 32

Narrabri Northern 2,000 2,031 76

Narrandera Southern 2,471 2,187 21

Narromine Central 2,850 2,336 43

Oberon Central 5,229 5,460 33

13

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Orange* Central 12,987 3

Parkes Central 2,650 1,728 39

Port Macquarie-Hastings Northern 8,271 8,258 84

Queanbeyan-Palerang South East 5,390 5,189 87

Richmond Valley Northern 5,836 4,841 71

Shoalhaven South East 19,400 16,810 24

Singleton Central 10,516 7,800 55

Snowy Monaro South East 2,299 2,199 101

Snowy Valleys Southern 3,691 3,145 30

Tamworth Northern 4,161 4,060 103

Temora Southern 3,583 3,116 23

Tenterfield Northern 2,215 2,180 83

Tweed Northern 14,463 13,597 18

Unincorporated Far West* Western 50 3

Upper Hunter Central 2,710 2,949 49

Upper Lachlan South East 5,481 4,216 99

Uralla Northern 3,760 2,886 23

Wagga Wagga Southern 4,449 4,251 51

Walcha Northern 4,903 4,206 27

Walgett Northern 1,321 971 18

Warren Central 1,776 1,335 24

Warrumbungle Central 1,706 1,710 101

Weddin Central 2,848 2,595 29

Wentworth* Western 80 3

Yass Valley South East 7,297 5,648 35

Central 3,697 3,414 1,247

Northern 4,358 4,057 1,359

Western 96 102 50

Southern 3,303 2,904 568

South East 5,489 5,134 516

* Price information with a small volume of transactions should be used with caution. The median price for municipalities with less than four sales in 2017 is not reported.

1514

Queensland

2.1%Queensland

Average annual growth over 5 years

North

5.9%

East

3.3%1.1%

West

AVERAGE ANNUAL MEDIAN PRICE GROWTH

2017 -2.8%

5 years 2.1%

10 years 1.1%

20 years 6.3%

Average annual growth over five years

15

‘Land prices for quality, well developed, sugar cane properties in tightly held areas of the Burdekin and the Hinchinbrook Shire continue to show positive growth. Land owners are taking the opportunity to expand holdings as quality properties come on the market.’

Angelo Rigano, Rural Bank

The median price of farmland in Queensland decreased by 2.8 per cent to $4,051/ha in 2017 following a 10.3 per cent increase in 2016.

For three consecutive years to 2016, the median value per hectare had recorded positive growth. However, values eased in the east of the divide, where the majority of land transactions occur.

The estimated number of farmland transactions in 2017 was 1,720, 1.7 per cent

higher than 2016. Transaction volume has remained stable since 2009 and far below the peak volume of 3,327 in 2003.

The area of farmland traded in 2017 was approximately 3.97 million hectares, a decrease of 50 per cent due to fewer large pastoral sales compared to 2016.

The total value of farmland traded in 2017 was approximately $1.97 billion, a decrease of eight per cent.

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$4,000

$500

$1,000

$1,500

$4,500

$2,000

$2,500

$3,000

$3,5002500

500

1000

3000

1500

3500

2000

Queensland

Number of transactions (RHS) Median $/ha (LHS)

1716

Queensland

Transactions falling into the 30-99 hectares bracket make up a large segment of the Queensland farmland market. Total transaction volume was almost the same as last year, however the mix by parcel size changed. The 100-299 hectares bracket had two per cent fewer transactions in 2017, while transaction volume in the 500+ hectares bracket increased by 6.8 per cent in 2017.

The median value for:

• 30-99 hectare parcels increased by 3.3 per cent in 2017

• 100-299 hectares increased by 3 per cent

• 300-499 hectares decreased by 5.1 per cent

• 500+ hectares also decreased by 9.7 per cent.

Each parcel size bracket has recorded positive average annual growth over the past five years. The 30-99 hectare bracket has seen the highest five year average growth at 3.6 per cent.

‘The Queensland rural property market in 2017 was again impacted by the lack of rainfall recorded in the northern and western pastoral areas where adverse seasonal conditions limited sales activity. In contrast, the eastern seaboard cropping and horticulture areas and the central highlands beef producing areas recorded strong enquiry and sales. In the South, demand was solid for the better quality beef and irrigation properties. The underlying strength of commodity prices should continue to drive the demand for rural property across the board in 2018.’

John Burke, Elders

Performance by land size

Parcel size (ha)

2013 2014 2015 2016 2017

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

30-99 43% 6,833 46% 6,609 45% 7,324 45% 7,709 45% 7,967

100-299 26% 3,179 27% 3,089 25% 3,227 26% 3,755 25% 3,866

300-499 7% 1,907 6% 1,977 6% 2,058 6% 2,105 6% 1,998

500+ 24% 735 22% 739 24% 768 23% 785 24% 709

Overall 1,732 3,481 1,726 3,655 1,744 3,776 1,692 4,167 1,720 4,051

Trans = Transactions

17

1995

1995

1995

2003

2003

2003

1999

1999

1999

2007

2007

2007

2014

2014

2014

1996

1996

1996

2004

2004

2004

2011

2011

2011

2000

2000

2000

2008

2008

2008

2015

2015

2015

1997

1997

1997

2005

2005

2005

2012

2012

2012

2001

2001

2001

2009

2009

2009

2016

2016

2016

1998

1998

1998

2006

2006

2006

2013

2013

2013

2002

2002

2002

2010

2010

2010

2017

2017

2017

0

0

0

0

0

350

50

100

150

200

$7,000$8,000$9,000

$4,000

$2,000$3,000

$1,000

$10,000

$5,000$6,000

$350

$150

$200

$250

$50

$100

$300

$400

2,000

2,500

1,000

500

3,000

1,500

700

200

300

100

400

800

500

600

250

300

East

North

West

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

0

$4,000

$500

$1,000

$1,500

$4,500

$2,000

$2,500

$3,000

$3,500

1918

QueenslandThe median price for North Queensland increased by 14.5 per cent in 2017 taking the five year average annual growth to 5.9 per cent. The volume of transactions increased slightly to 287, compared to 279 in 2016. The increase in median price was driven by a larger percentage of high value sales in the Burdekin, Hinchinbrook, Whitsunday, Tablelands and Cassowary Coast municipalities.

The median price for East Queensland farmland decreased by 3.8 per cent in 2017 taking five year average annual growth to 3.3 per cent. The volume of transactions

increased 0.4 per cent to 1,264. Municipalities where median value per hectare decreased included Fraser Coast, Gympie, Goondiwindi and Scenic Rim. Growth in the median price per hectare occurred in the municipalities of Rockhampton, Lockyer Valley, Isaac, Central Highlands, Banana, Bundaberg and Toowoomba.

The West Queensland median price per hectare increased by 1.7 per cent in 2017. The volume of transactions increased by 9.7 per cent. The median value per hectare increased in municipalities such as Maranoa, Paroo and McKinlay.

19

Farmland sales by municipality – Queensland

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Balonne West 593 539 20

Banana East 3,152 2,720 54

Barcaldine West 164 268 6

Barcoo West 100 73 4

Blackall Tambo* West 530 2

Boulia* West 82 1

Bulloo West 49 90 5

Bundaberg East 4,420 3,992 69

Burdekin North 16,347 11,554 34

Burke* West 81 0

Cairns North 10,238 9,202 19

Carpentaria* West 152 0

Cassowary Coast North 9,352 8,312 33

Central Highlands East 2,054 1,750 47

Charters Towers North 459 1,441 24

Cloncurry* West 61 0

Cook North 88 1,772 5

Croydon* North 41 0

Douglas** North 11,581 4

Etheridge* North 497 1

Flinders West 238 249 12

Fraser Coast East 4,513 5,521 31

Gladstone East 2,852 2,368 55

Goondiwindi East 1,690 1,729 53

Gympie East 5,023 6,020 80

Hinchinbrook North 8,825 6,619 22

Isaac East 1,546 1,597 23

Livingstone** East 4,566 9

Lockyer Valley East 11,584 9,604 38

Longreach West 148 141 7

2120

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Mackay North 6,937 7,420 53

Maranoa West 1,146 940 60

Mareeba** North 8,405 13

McKinlay West 266 233 4

Moreton Bay East 15,473 15,243 13

Mount Isa* West 32 0

Murweh West 182 214 12

North Burnett East 2,710 2,656 72

Paroo West 67 59 13

Quilpie West 50 47 13

Richmond West 229 241 4

Rockhampton East 5,139 3,800 25

Scenic Rim East 9,504 9,491 71

Somerset East 8,593 8,777 82

South Burnett East 3,889 4,051 100

Southern Downs East 4,528 4,162 102

Sunshine Coast East 12,671 12,336 12

Tablelands North 9,921 9,004 51

Toowoomba East 6,178 5,716 162

Townsville North 3,686 6,754 12

Western Downs East 2,181 2,132 166

Whitsunday North 6,508 4,328 16

Winton West 93 138 6

North 8,694 7,636 287

East 4,103 4,032 1,264

West 282 311 169* Price information with a small volume of transactions should be used with caution. The median price for municipalities with less than four sales in 2017 is not reported.

**These municipalities are yet to accumulate three years of data under their current name.

21

2322

Victoria

7.2%Victoria

Average annual growth over 5 years

Farmland performance(average annual growth)

2016 10.1%

5 years 6.35

10 years 4.1%

20 years 6.7%

North West

8.2%

Gippsland

3.0%

Northern

7.8%

South West

6.0%

AVERAGE ANNUAL MEDIAN PRICE GROWTH

2017 9.5%

5 years 7.2%

10 years 3.2%

20 years 6.5%

Average annual growth over five years

23

In 2017, the median price of Victorian farmland increased by 9.5 per cent compared to 2016.

Average annual growth over five years is now 7.2 per cent.

Favourable seasonal conditions in the North West of the state led to an increase in demand for the tightly held regions of the Wimmera and Mallee. The strength of lamb and wool prices contributed to the rise of land values in the state’s grazing regions, with a reduced number of properties available for purchase in 2017.

The estimated number of farmland transactions in 2017 was 1,827, up 1.7 per cent compared to 2016.

The area of farmland traded in 2017 was approximately 253,000 hectares, which is an increase of 11.7 per cent compared to 2016.

The total value of farmland traded in 2017 was approximately $1.2 billion, an increase of 10.1 per cent compared to 2016.

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

2,500

3,000

500

1,000

1,500

2,000

Victoria

Number of transactions (RHS) Median $/ha (LHS)

2524

Victoria

Parcel sizes of 30-49 and 50-99 hectares make up a large segment of the Victorian farmland market.

The volume of transactions increased by:

• 9.0 per cent for the 30-49 hectares bracket

• 2.6 per cent for the 100-199 hectares

• 6.4 per cent for the 200+ hectare bracket.

Performance by land size

Parcel size (ha)

2013 2014 2015 2016 2017

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

30-49 29% 7,957 30% 7,537 27% 7,438 29% 8,215 31% 8,681

50-99 32% 5,155 31% 5,340 30% 5,815 33% 6,186 30% 6,619

100-199 23% 3,192 21% 3,412 24% 3,520 21% 3,623 22% 4,146

200+ 16% 1,888 17% 2,090 19% 1,857 17% 2,289 17% 2,279

Overall 1,454 4,701 1,963 4,907 2,210 4,796 1,797 5,416 1,827 5,932

Trans = Transactions

The volume of transactions for the 50-99 hectares bracket decreased by 7.8 per cent compared to 2016.

In 2017 the median value for:

• 30-49 hectare parcels increased by 5.7 per cent

• 50-99 hectares increased by 7.0 per cent

• 100-199 hectares increased by 14.4 per cent

• 200+ hectares decreased by 0.4 per cent.

Larger land parcels have recorded higher average annual growth over the past five years. Transactions in the 100-199 hectare bracket have recorded the highest five year average growth at 9.6 per cent with 200+ hectares at 5.8 per cent.

‘In Gippsland, smaller blocks sold at a premium price in 2017. Some are being purchased as additions to existing farms, but in the 30-50ha market there was a higher percentage of lifestyle purchases. Larger parcels of land are tightly held particularly in East Gippsland, between Bairnsdale and the high country.’

Benjamin Gebert, Rural Bank.

25

1995

1995

1995

2003

2003

2003

1999

1999

1999

2007

2007

2007

2014

2014

2014

1996

1996

1996

2004

2004

2004

2011

2011

2011

2000

2000

2000

2008

2008

2008

2015

2015

2015

1997

1997

1997

2005

2005

2005

2012

2012

2012

2001

2001

2001

2009

2009

2009

2016

2016

2016

1998

1998

1998

2006

2006

2006

2013

2013

2013

2002

2002

2002

2010

2010

2010

2017

2017

2017

0

0

0

0

0

0

1,200

600

$6,000

$2,000

$3,000

$7,000

$4,000

800

200

400

$5,000

$1,000

$1,500

$2,000

$2,500

$500

$3,000

$1,000

$6,000

$2,000

$3,000

$4,000

$1,000

$5,000

$7,000

200

700

100

200

250

800

300

50

400

300

900

100

500

150

600

1,000

South West

North West

Northern

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

2726

Victoria

The median price in South West Victoria increased by 16.6 per cent in 2017, driven by a larger percentage of high value sales in the municipalities of Central Goldfields, Glenelg, Colac-Otway, Corangamite, Northern Grampians and West Wimmera. The volume of transactions decreased by 4.7 per cent in 2017 due to fewer sales in the municipalities of Colac-Otway, Southern Grampians, Moorabool and Moyne.

The median price in Northern Victoria increased by 6.4 per cent in 2017, driven by a larger percentage of high value sales in the municipalities of Loddon, Benalla and Strathbogie. The volume of transactions in Northern Victoria increased by 1.7 per cent in 2017. The small rise in transaction volume was due to increases in the municipalities of Loddon and Wangaratta.

North West Victoria recorded the highest median value per hectare increase in 2017, up 21.6 per cent. Top performing municipalities included Yarriambiack, Buloke and Horsham. Transaction volumes increased by 34.4 per cent due to increased activity in the municipalities of Buloke and Hindmarsh.

The median price of farmland in Gippsland increased by 15.4 per cent in 2017, following a 3.8 per cent decrease in 2016. The growth in median was due to a larger percentage of high value sales in the municipalities of East Gippsland, Wellington and Baw Baw. Transaction volume decreased by 5.1 per cent in 2017 driven by decreased volume in Wellington and Baw Baw.

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$10,000

$2,000

$4,000

$12,000

$6,000

$8,000500

100

200

600

300

700

400

Gippsland

Number of transactions (RHS) Median $/ha (LHS)

27

Farmland sales by municipality – Victoria

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Alpine Northern 5,448 5,649 12

Ararat South West 4,246 4,335 44

Ballarat South West 4,424 5,865 6

Bass Coast Gippsland 16,144 14,164 26

Baw Baw Gippsland 16,537 15,219 36

Benalla Northern 7,531 6,202 35

Bendigo Northern 4,659 4,330 43

Buloke North West 1,748 1,475 70

Campaspe Northern 4,849 5,239 74

Cardinia Gippsland 18,266 19,428 13

Central Goldfields South West 4,813 3,161 9

Colac - Otway South West 10,478 9,084 35

Corangamite South West 8,477 7,885 84

East Gippsland Gippsland 5,778 4,319 80

Gannawarra Northern 2,772 2,532 39

Glenelg South West 7,454 5,761 44

Golden Plains South West 7,027 6,543 30

Hepburn South West 7,790 8,116 19

Hindmarsh North West 2,760 2,672 41

Horsham North West 5,440 4,302 38

Indigo Northern 7,699 7,184 28

La Trobe Gippsland 8,474 8,785 15

Loddon Northern 2,994 2,444 67

Macedon Ranges South West 8,208 8,048 15

Mansfield Northern 8,049 8,205 28

Mildura North West 1,146 1,149 23

Mitchell Northern 6,344 5,248 28

Moira Northern 6,000 5,516 79

Moorabool South West 11,435 10,031 4

Mount Alexander Northern 6,587 7,078 23

2928

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Moyne South West 8,158 7,265 69

Murindindi Northern 8,481 7,567 26

Northern Grampians South West 3,356 2,765 57

Pyrenees South West 3,908 3,682 54

Shepparton Northern 6,818 6,173 52

South Gippsland Gippsland 12,982 12,290 103

South Grampians South West 5,560 4,865 31

Strathbogie Northern 5,812 4,994 70

Surf Coast South West 9,001 10,259 4

Swan Hill North West 2,169 1,927 27

Towong Northern 3,501 3,523 32

Wangaratta Northern 6,800 6,834 57

Wellington Gippsland 7,879 7,290 86

West Wimmera South West 3,220 2,803 46

Wodonga Northern 8,105 11,273 5

Yarriambiack North West 3,800 2,696 20

South West 6,539 5,699 528

Gippsland 10,149 9,361 355

Northern 5,788 5,332 698

North West 2,390 2,009 246

29

3130

Western Australia

Central

0.4% South Coast

0.7%

Eastern

6.4%

Northern

-4.2%

-0.1%Western Australia

Average annual growth over 5 years

South West

-2.8%

AVERAGE ANNUAL MEDIAN PRICE GROWTH

2017 -6.5%

5 years -0.1%

10 years 0.7%

20 years 5.0%

Average annual growth over five years

31

The area of farmland traded in 2017 was approximately 483,000 hectares, a decrease of 2.7 per cent compared to 2016.

The total value of farmland traded in 2017 was approximately $788 million, a decrease of 4.2 per cent.

‘Buyer interest in WA was strong in 2017 underpinned by corporate investor enquiry particularly around the central wheat belt. Strong leasing values negotiated through early 2018 are being sustained by good commodity prices particularly in traditional reliable rainfall areas where mixed farming practices are carried out.’

Jim Sangalli, Elders.

In 2017, the median price of Western Australian farmland decreased by 6.5 per cent compared to 2016. This follows a 3.1 per cent increase in 2016.

Average annual growth over five years in Western Australia is -0.1 per cent.

The estimated number of farmland transactions in 2017 was 677, down by 6.5 per cent compared to 2016.

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$1,000

$1,500

$2,000

$2,500

$500

600

800

1,000

1,200

200

1,400

400

Western Australia

Number of transactions (RHS) Median $/ha (LHS)

3332

Western Australia

In 2017, there was a higher percentage of 100-399 hectare sales. In contrast, the 400-699 and 700+ hectare brackets represented a smaller percentage of total transactions in 2017. The median price for 400-699 hectare parcels decreased significantly in 2017, down by 20.2 per cent after increasing by 23 per cent in 2016. Smaller parcel sizes between 50-99 hectares also experienced a decrease in the median, down by 15.8 per cent.

The 50-99 hectare category once again has the highest five year average annual growth rate at 3.6 per cent, despite the decrease in 2017. The 100-399 hectare category increased for the third consecutive year up by 6.3 per cent in 2017, averaging 3.3 per cent growth over the last five years. The 400-699 hectare category has averaged 2.9 per cent.

The median value of larger parcels above 700 hectares decreased by 9.8 per cent in 2017, an average of 1.5 per cent growth over the last five years.

‘In 2017, demand in reliable rainfall areas remained strong but for the remainder of the state demand was patchy. Demand was modest in the smaller holdings segment of the market. After some favourable seasonal conditions the overall outlook for the state appears positive.’

Tim Clark, Rural Bank

Performance by land size

Parcel size (ha)

2013 2014 2015 2016 2017

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

50-99 25% 5,341 21% 5,710 27% 6,015 23% 7,326 23% 6,168

100-399 30% 2,490 31% 2,279 28% 2,397 27% 2,607 30% 2,771

400-699 17% 1,331 17% 1,258 15% 1,389 17% 1,708 16% 1,362

700+ 28% 1,084 30% 967 30% 1,055 33% 1,132 31% 1,021

Overall 676 1,953 881 1,811 734 2,003 723 2,066 677 1,931

Trans = Transactions

33

1995

1995

1995

2003

2003

2003

1999

1999

1999

2007

2007

2007

2014

2014

2014

1996

1996

1996

2004

2004

2004

2011

2011

2011

2000

2000

2000

2008

2008

2008

2015

2015

2015

1997

1997

1997

2005

2005

2005

2012

2012

2012

2001

2001

2001

2009

2009

2009

2016

2016

2016

1998

1998

1998

2006

2006

2006

2013

2013

2013

2002

2002

2002

2010

2010

2010

2017

2017

2017

0

0

0

0

0

0

100

40

$1,200

$400

$600

$1,400

$800

140

120

160

60

20

$1,600

$1,000

$200

$3,500

$1,500

$2,000

$2,500

$500

$3,000

$1,000

$700

$800

$300

$400

$500

$100

$600

$900

$200

180

140160

20

180

6040

80

200

100120

200

50

250

100

300

150

80

Northern

South Coast

Eastern

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

3534

Western Australia

Northern values decreased by 20.4 per cent in 2017. The municipalities of Greater Geraldton, Dalwallinu and Irwin drove the decline. South West values increased by 5.5 per cent. The municipalities of Donnybrook-Balingup and Dardanup contributed to this increase. The median price for the South Coast decreased by 2.7 per cent in 2017. Values in the municipalities of Esperance, Albany and Manjimup eased in 2017. Values in Central Western Australia increased by 2.7 per cent,

while the transaction volume decreased. Growth in value came from the municipalities of Kojonup, Beverley and Dowerin. Eastern farmland values increased by 50.2 per cent in 2017. There was a lower volume of low value sales in 2017 compared to 2016, which led to a significant increase in the median value per hectare. Strong growth occurred in Yilgarn, Westonia, Koora, Narembeen and Mount Marshall.

1995

1995

2003

2003

1999

1999

2007

2007

2014

2014

1996

1996

2004

2004

2011

2011

2000

2000

2008

2008

2015

2015

1997

1997

2005

2005

2012

2012

2001

2001

2009

2009

2016

2016

1998

1998

2006

2006

2013

2013

2002

2002

2010

2010

2017

2017

0

0

0

0

$3,000

$1,000

$1,500

$2,000

$2,500

$500

$14,000

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$16,000

400

100

120

20

500

140

100

40

60

600

160

200

300

80

Central

South West

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

35

Farmland sales by municipality – Western Australia

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Albany South Coast 5,527 6,135 23

Beverley Central 3,061 3,129 10

Boddington* South West 4,945 2

Boyup Brook Central 3,057 3,035 14

Bridgetown-Greenbushes South Coast 4,815 4,424 12

Brookton Central 2,404 2,883 11

Broomehill-Tambellup Central 3,293 2,904 5

Bruce Rock Central 1,242 1,197 4

Busselton South West 10,223 11,162 14

Capel South West 6,894 9,965 5

Carnamah Northern 722 935 6

Chapman Valley Northern 897 1,722 4

Collie* South West 4,010 2

Coorow Northern 1,025 885 5

Corrigin Central 1,076 1,358 5

Cranbrook Central 1,766 1,978 16

Cuballing Central 2,471 2,436 5

Cunderdin Central 1,606 1,760 4

Dalwallinu Northern 666 756 11

Dandaragan Northern 1,482 1,547 9

Dardanup South West 13,148 16,733 7

Denmark South Coast 8,622 8,898 12

Donnybrook-Balingup South West 7,390 7,271 14

Dowerin Central 1,683 1,763 12

Dumbleyung Central 1,240 1,184 9

Esperance South Coast 1,290 1,853 39

Gnowangerup South Coast 2,125 1,676 11

3736

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Goomalling Central 2,382 2,050 6

Greater Geraldton Northern 472 895 12

Harvey South West 9,497 10,018 11

Irwin Northern 732 1,238 6

Jerramungup South Coast 1,374 1,346 10

Katanning Central 3,310 2,430 7

Kellerberrin Central 1,085 1,256 5

Kent South Coast 1,220 972 12

Kojonup Central 3,105 2,693 16

Kondinin Eastern 868 832 10

Koorda Eastern 591 528 13

Kulin Eastern 802 845 9

Lake Grace Eastern 997 963 16

Manjimup South Coast 7,871 7,928 13

Merredin Eastern 907 877 18

Mingenew Northern 1,858 1,653 4

Moora Northern 3,273 2,537 5

Morawa* Northern 657 2

Mount Marshall Eastern 542 472 9

Mukinbudin Eastern 543 450 5

Murray South West 9,433 10,538 4

Nannup South Coast 5,508 7,248 6

Narembeen Eastern 899 704 5

Narrogin Central 2,721 2,837 11

Northam Central 5,174 4,863 10

Northampton Northern 1,033 1,025 13

Nungarin Eastern 450 471 6

Perenjori Northern 793 818 4

Pingelly Central 2,995 3,037 6

Plantagenet South Coast 4,146 4,062 36

37

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Quairading Central 2,003 1,846 8

Ravensthorpe South Coast 1,369 1,215 13

Tammin* Central 1,971 1

Three Springs Northern 2,282 1,875 4

Toodyay Central 1,990 2,867 4

Trayning Central 631 776 4

Victoria Plains* Central 2,951 3

Wagin Central 2,296 2,086 5

Wandering Central 5,053 3,566 5

Waroona* South West 13,845 3

West Arthur Central 2,081 1,865 18

Westonia Eastern 985 715 4

Wickepin Central 1,608 1,789 4

Williams Central 1,587 2,622 8

Wongan-Ballidu Central 1,161 1,139 8

Woodanilling Central 1,671 1,832 4

Wyalkatchem* Central 1,080 1

Yilgarn Eastern 637 466 8

York Central 4,192 4,451 11

Northern 891 1,130 85

Eastern 805 645 103

South Coast 2,904 2,828 187

South West 9,579 9,629 62

Central 2,403 2,371 240

* Price information with a small volume of transactions should be used with caution. The median price for municipalities with less than four sales in 2017 is not reported.

3938

South Australia

2.8%South Australia

Average annual growth over 5 years

Eyre Peninsula

-6.5%

Yorke and North

3.0%

Adelaide and

Fleurieu

5.1%

South East

5.9%

AVERAGE ANNUAL MEDIAN PRICE GROWTH

2017 17.1%

5 years 2.8%

10 years 1.9%

20 years 6.3%

Average annual growth over five years

39

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$3,500

$1,500

$2,000

$4,000

$2,500

$500

$3,000

$1,000

800

200

1,100

400

1,200

600

South Australia

Number of transactions (RHS) Median $/ha (LHS)

The median price of farmland in South Australia increased by 17.1 per cent in 2017, after almost a decade of a relatively unchanged median price.

The number of farmland transactions also increased in 2017, up 16.8 per cent to 855. This was the fourth consecutive year of growth in the number of transactions, a reversal of the downwards trend observed from 2006 to 2013.

There was a higher volume of larger properties traded in 2017. This contributed to a 46 per cent increase in the area of land traded and an 80 per cent increase in the total value of land traded, up to $812 million.

4140

South Australia

Performance by land size

Parcel size (ha)

2013 2014 2015 2016 2017

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

30-99 41% 6,617 38% 5,737 38% 7,412 42% 7,059 39% 7,413

100-199 21% 2,803 20% 2,977 21% 2,720 20% 2,507 18% 4,321

200-399 15% 2,017 18% 2,202 17% 2,003 16% 2,184 15% 2,399

400+ 23% 803 24% 795 24% 897 22% 873 29% 1,188

State 555 2,856 645 3,005 678 2,948 732 2,989 855 3,500

Trans = Transactions

The median price increased in 2017 for all parcel size segments with the 100-199 hectare segment experiencing the greatest growth, up 72 per cent on 2016. This is a sharp turnaround for this segment which had experienced significant declines in median price for 2013, 2015 and 2016. The South East and Yorke and North regions account for 75 per cent of the state’s transactions in this segment. These regions saw increases in median price of 76 per cent and 20 per cent, respectively.

Transactions greater than 400 hectares saw an acceleration in the median price which has been steadily increasing since 2012. The median price increased 36 per cent in 2017. The number of transactions increased 52 per cent, indicating strong demand for properties of this scale. The South West accounted for half of the state’s transactions above

400 hectares, experiencing a 24 per cent lift in median up to $1,371/ha, after staying between $880 and $1,130 since 2007. The median price of this segment dropped 17 per cent on the Eyre Peninsula, where it accounted for 73 per cent of the region’s transactions.

The 30-99 hectare segment experienced a five per cent increase in median price. At a regional level, the medians for this segment increased 13 per cent in Adelaide and Fleurieu, 2 per cent in the South East and three per cent in Yorke and North.

The median price of the 200-399 hectare segment increased by 10 per cent, driven by growth of 15 per cent in this segment in the Yorke and North. The South East experienced a seven per cent decline in the median price of this segment.

41

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

250

100

150

50

$12,000

$4,000

$6,000

$8,000

$2,000

$10,000

$14,000

200

Adelaide and Fleurieu

Number of transactions (RHS) Median $/ha (LHS)

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$1,200

$400

$600

$1,400

$800

$1,000

$200

100

20

40

120

60

140

80

Eyre Peninsula

Number of transactions (RHS) Median $/ha (LHS)

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$1,500

$2,000

$2,500

$500

$3,000

$1,000

350

50

100

400

150

200

450

250

300

South East

Number of transactions (RHS) Median $/ha (LHS)

4342

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$2,000$2,500$3,000$3,500$4,000$4,500

$500

$1,500

$5,000

$1,000

350

50

400

150

100

200

250

300

Yorke and North

Number of transactions (RHS) Median $/ha (LHS)

South Australia

Yorke and North experienced the largest increase in median price in 2017, up 37.8 per cent to $4,706/ha. The increased median price is linked to 36.9 per cent more transactions. The Mid and Lower North sub-regions showed strong growth with the Barunga West, Northern Areas and Port Pirie municipalities standing out.

In the Adelaide and Fleurieu region, the median price increased by 19.3 per cent while the number of transactions was down by 11.3 per cent. This growth was driven by increased median prices in the Adelaide Hills (+46 per cent) and the Barossa (+18 per cent). The Barossa has seen a rapid rise in the number of transactions in recent years, up from nine in 2014 to 26 in 2017.

The South East built upon strong growth in 2016 by adding another 7.4 per cent to the median price in 2017. Buyers appeared willing to accept increased prices, with a 28.2 per cent rise in the number of transactions. Growth was experienced across the region with Grant, Robe and Mid Murray showing the largest increases.

The Eyre Peninsula median price declined 17.3 per cent in 2017. At a more local level, increased medians were recorded in Tumby Bay, Cleve and on the West Coast in Ceduna and Streaky Bay. The number of transactions for the region was down one per cent. Ceduna stood out with 18 transactions for the year, after a period of very low activity.

43

Farmland sales by municipality – South Australia

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Adelaide Hills Adelaide and Fleurieu

17,916 19,046 12

Alexandrina Adelaide and Fleurieu

11,703 11,525 43

Barossa Adelaide and Fleurieu

11,239 11,359 26

Barunga West* Yorke and North 3,349 3

Berri Barmera* South East 670 2

Ceduna Eyre Peninsula 495 393 18

Clare & Gilbert Valleys Yorke and North 9,181 8,700 29

Cleve Eyre Peninsula 1,147 975 10

Coorong South East 2,534 2,065 28

Copper Coast Yorke and North 6,528 5,610 6

Elliston Eyre Peninsula 689 633 9

Flinders Ranges* Yorke and North 974 2

Franklin Harbour Eyre Peninsula 296 431 7

Goyder Yorke and North 2,023 2,067 36

Grant South East 10,150 7,411 33

Kangaroo Island Adelaide and Fleurieu

2,345 2,383 31

Karoonda East Murray South East 607 543 18

Kimba Eyre Peninsula 443 567 8

Kingston South East 4,037 3,715 12

Light Yorke and North 11,384 10,196 19

Lower Eyre Peninsula Eyre Peninsula 2,980 3,565 16

Loxton Waikerie South East 841 673 16

Mallala* Yorke and North 8,601 0

Mid Murray South East 1,782 1,395 55

Mount Barker Adelaide and Fleurieu

17,190 15,120 11

4544

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Mount Remarkable Yorke and North 2,116 1,870 24Murray Bridge South East 2,185 2,222 27

Naracoorte South East 4,433 4,614 40

Northern Areas Yorke and North 5,482 3,596 15

Onkaparinga* Adelaide and Fleurieu

16,273 3

Orroroo Carrieton Yorke and North 675 1,020 10

Peterborough Yorke and North 948 994 5

Port Pirie Yorke and North 3,470 2,746 20

Renmark Paringa* South East 1,015 3

Robe South East 6,631 5,318 11

Southern Mallee South East 1,115 1,085 32

Streaky Bay Eyre Peninsula 410 340 9

Tatiara South East 3,270 2,675 60

Tumby Bay Eyre Peninsula 3,473 2,517 12

Victor Harbor Adelaide and Fleurieu

10,003 12,288 10

Wakefield Yorke and North 3,764 2,950 17

Wattle Range South East 7,482 6,568 36

Wudinna Eyre Peninsula 737 910 6

Yankalilla Adelaide and Fleurieu

12,281 11,339 21

Yorke Peninsula Yorke and North 5,566 4,958 44

Adelaide and Fleurieu 10,703 10,578 157

South East 2,742 2,486 373

Eyre Peninsula 733 835 95

Yorke and North 4,706 3,881 230* Price information with a small volume of transactions should be used with caution. The median price for municipalities with less than four sales in 2017 is not reported.

45

‘Improved commodity prices, low interest rates and longer term gains in productivity have enabled many farmers to pay down debt and greatly increased confidence to reinvest into agriculture. This has created heightened competition in the market by allowing smaller and medium sized operations to compete hard with larger farming and corporate enterprises to secure land.’

Phil Keen, Elders, South Australia

4746

Tasmania

King Island

9.3%

Flinders Island

2.1%

Northern

7.8%

South

9.2%

10.2%Tasmania

Average annual growth over 5 years

AVERAGE ANNUAL MEDIAN PRICE GROWTH

2017 19.3%

5 years 10.2

10 years 3.9%

20 years 7.7%

4.8%

North West

Average annual growth over five years

47

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

$10,000

$2,000

$4,000

$12,000

$6,000

$8,000500

100

200

600

300

700

400

Tasmania

Number of transactions (RHS) Median $/ha (LHS)

The median price of Tasmanian farmland increased by 19.3 per cent in 2017, following a 0.3 per cent decrease in 2016.

The number of farmland transactions also increased in 2017, up by 19.1 per cent to 274. The combination of increased transactions and a higher median price suggests that more sellers were drawn out, but demand from buyers still exceeded supply.

The area of farmland traded in 2017 was 27,629 hectares, an increase of 23 per cent from 2016.

The combination of a larger area of land traded and higher median price led to a 40 per cent increase in the value of farmland traded, which reached $232 million.

4948

Tasmania

Performance by land size

Parcel size (ha)

2013 2014 2015 2016 2017

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

% of Trans

Median $/ha

15-39 28% 11,259 32% 10,256 31% 11,364 36% 11,000 36% 14,092

40-79 29% 9,122 26% 9,235 25% 9,005 27% 8,419 29% 10,328

80-149 19% 7,651 21% 6,778 20% 9,492 22% 8,346 21% 7,560

150+ 24% 2,981 21% 3,505 24% 4,685 15% 4,408 15% 5,293

Overall 247 8,656 243 7,718 216 8,709 230 8,679 274 10,354

Higher median prices were spread across all land size segments except for 80-149 hectares. Increased transaction activity was also consistent across segments ranging from 12 per cent growth for 80-149 hectares up to 27 per cent growth for the 40-79 hectare segment. The number of transactions increased by 18 per cent for both the 15-39 hectare and greater than 150 hectare segments. The consistency in strong median price growth and higher volumes of transactions is another signal of the strength in demand for a wide range of land types in Tasmania. This is evidence of the underlying confidence in agriculture, with low interest rates and stable but strong commodity prices prompting land holders to look at expanding existing holdings.

The median price for 15-39 hectare properties increased by 28 per cent in 2017, the largest increase of the four segments. The median for this segment grew by 43 per cent in the Northern region and 28 per cent

in the North West, but lost eight per cent in the South.

An increase in median of 23 per cent occurred for the 40-79 hectare segment. This was consistent across regions with 61 per cent growth in the northern region, 15 per cent in the North West and 12 per cent in the South.

The nine per cent decrease in median for 80-149 hectare properties was largely due to a 22 per cent decline in the median price for this segment in the North West, which accounted for 40 per cent of the state’s transactions in this range. The median price for this segment increased by 51 per cent in Northern Tasmania and 75 per cent in the South.

Transactions above 150 hectares experienced a 20 per cent rise in median price. Of these transactions, 40 per cent occurred in the North West where the median price increased by 83 per cent.

Trans = Transactions

49

1995

1995

1995

2003

2003

2003

1999

1999

1999

2007

2007

2007

2014

2014

2014

1996

1996

1996

2004

2004

2004

2011

2011

2011

2000

2000

2000

2008

2008

2008

2015

2015

2015

1997

1997

1997

2005

2005

2005

2012

2012

2012

2001

2001

2001

2009

2009

2009

2016

2016

2016

1998

1998

1998

2006

2006

2006

2013

2013

2013

2002

2002

2002

2010

2010

2010

2017

2017

2017

0

0

0

0

0

0

160

40

60

$12,000

$4,000

$6,000

$14,000

$8,000

80

100

20

$10,000

$2,000

$10,000

$12,000

$14,000

$4,000

$2,000

$16,000

$6,000

$8,000

$7,000

$3,000

$4,000

$5,000

$1,000

$2,000

$6,000

$8,000

100

20

120

60

40

140

80

350

100

150

50

200

400

250

300

120

140

Northern

North West

South

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

Number of transactions (RHS) Median $/ha (LHS)

5150

Tasmania

The strong demand for Tasmanian farmland in 2017 was evident across the state with all regions except King Island recording increases in both median price and number of transactions.

The strongest growth in median price was recorded in Northern Tasmania which increased by 72.5 per cent, more than recovering from a 26 per cent decline in 2016. The number of transactions in the Northern region increased 35.6 per cent.

The median price in the North West increased by 11 per cent, building upon solid growth from 2016. Transaction volumes also increased, up 10.8 per cent. Central Highlands and Dorset were the stand out municipalities in this region.

The South added 2.7 per cent to the median price, holding onto the strong gains of the previous two years. Transaction volume increased by 7.5 per cent. Southern Midlands and Sorell showed exceptional growth in median.

Flinders Island recorded a 33.5 per cent increase in median price after a stable year in 2016. The King Island median fell 1.5 per cent, losing some of the exceptional gains recorded in 2016.

Average annual growth over the last five years has been strong for all regions, led by the South (9.2 per cent) and Northern (7.8 per cent) where there has been significant investment in irrigation and improved access to water.

‘The outlook for Tasmanian farmland values remains positive with strong demand for a historically low number of property listings. Interstate and international buyers are recognising the value of farming in Tasmania, adding further competition to the market.’

Dean Lalor, Rural Bank, Tasmania.

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

40

10

15

20

25

5

$7,000

$3,000

$4,000

$5,000

$1,000

$2,000

$6,000

$8,000

30

35

Tasmanian islands

Flinders transactions (RHS) Flinders median $/ha (LHS) King transactions (RHS) King median $/ha (LHS)

51

Farmland sales by municipality – Tasmania

MUNICIPALITY REGIONMEDIAN $/HA EST. #

SALES 20172017 3 YEAR AVG

Break O’Day* Northern 3,305 1Brighton* South 6,196 1

Burnie North West 8,159 9,157 5Central Coast North West 14,429 13,987 21Central Highlands South 5,107 3,223 8Circular Head North West 14,117 11,836 29Clarence South 10,796 4Derwent Valley* South 4,819 2Devonport North West 21,803 21,147 6Dorset Northern 10,851 7,804 15Flinders Island Islands 3,464 2,883 12George Town Northern 15,596 10,863 4Glamorgan-Spring Bay South 1,626 2,922 6Huon Valley South 9,184 9,114 11Kentish North West 14,410 13,866 16King Island Islands 6,673 5,930 21Kingborough South 9,609 11,489 5Latrobe North West 15,191 15,386 12Launceston Northern 14,400 10,055 8Meander Valley North West 12,956 12,071 22Northern Midlands Northern 8,292 9,827 19Sorell South 14,433 8,238 5Southern Midlands South 5,166 3,408 14Tasman* South 7,031 1Waratah-Wynyard North West 18,857 14,320 12West Tamar Northern 12,446 9,222 14

Northern 11,460 9,036 61North West 14,089 12,841 123South 7,030 6,254 57

* Price information with a small volume of transactions should be used with caution. The median price for municipalities with less than four sales in 2017 is not reported.

5352

Northern Territory

Top End

3.7%

Cattle Regions

18.8%

-12.4%Northern Territory

Average annual growth over 5 years

AVERAGE ANNUAL MEDIAN PRICE GROWTH

2017 -35.1%

5 years -12.4%

10 years 2.7%

20 years 5.2%

The median price of farmland in the Northern Territory fell by 35.1 per cent in 2017. The movement in the Territory’s median price is largely a factor of the mix of properties sold between the two distinct categories of land types, and the low number of transactions, more than a change in the market. In 2017, there was a low proportion of transactions in the higher valued Top End region between Darwin and Katherine, pushing the Territory median towards the lower end of those transactions, compared to 2016.

Cattle regions of the Northern Territory recorded growth in median prices of 96.8 per cent in 2017. A shift to higher land prices is evident, with seven of the 11 transactions in 2017 transacting above $4,000/km2, compared to three out of 11 in 2016.

The median price of farmland in the Top End region fell by 15.3 per cent in 2017, following two strong years of growth. An easing of the median came from less than half of the number of transactions recorded in 2016, down from 37 to 14.

Farmland values are based on the total sale price of all farmland (including improvements and stock), not just arable land.

Average annual growth over five years

53

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

500

100

200

300

400

600

60

10

70

20

80

40

30

50

Top End

Number of transactions (RHS) Median indexed* (LHS)

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

800

300

400

500

600

100

700

200

80

20

10

30

90

40

50

60

70

Northern Territory

Number of transactions (RHS) Median indexed* (LHS)

South Australia

1995

2003

1999

2007

2014

1996

2004

2011

2000

2008

2015

1997

2005

2012

2001

2009

2016

1998

2006

2013

2002

2010

2017

0 0

1,000

200

400

600

800

1,200

10

12

14

2

4

16

6

8

Cattle Regions

Number of transactions (RHS) Median indexed* (LHS)

Indexed numbers simplify the study of disparate data, in this case the median price of Top End and Cattle Region farmland. The index base value is set at 100 for the year 2000, and the performance of farmland prices in other years are shown relative to the base value. For example, if 2005 has a value of 137, then land values were 37% higher in 2005 than in 2000.

5554

The Australian Farmland Values report is based on actual farm sales using data collected by the official government agency in each state and territory, which is then compiled by APM PriceFinder.

A number of municipalities in NSW merged in 2017. These changes have been accommodated in this research, altering some of the historical results compared with previous editions of this report.

The Australian Farmland Values report is a guide to the market value trends of commercial farming property. To that end, where possible, transactions between family members or where one party has compulsory powers are excluded from the analysis. Further, small farms are also excluded to limit the impact of ‘lifestyle farming’ on the results.

As property settlement periods vary, some 2017 sales will not be captured in this report at the time of publication. The median price for the most recent year is preliminary and will be revised at least annually.

The values used in this report are based on the total sale price and therefore include the value of capital improvements. Growth in values may reflect an element of capital improvement on properties. The value of water entitlements attached to a land title and therefore sold with the property will be reflected in the sale price of the land. If water entitlements are sold separately from the land, this value will not be captured in the sale price.

Median prices are only a guide to market activity. Compared with an average, the median is not as readily distorted by unusually high or low prices. Even so, in areas where there have been very few sales, the results should be viewed with caution as the year-on-year change in median price may not be indicative of an actual change in farmland value. A higher proportion of lower-priced sales can result in a lower median and vice-versa.

Farmland sales volume is reported as the number of transactions. Farms are sold as single or multiple lots, which obscures the view of the number of farms sold, particularly in cases where one farm is sold as multiple lots to multiple buyers. Accordingly, the ‘number of transactions’ should not be interpreted as the number of farms sold and should only be used as a guide to market activity.

Median value per hectare differs according to parcel size. Smaller blocks of land often have more valuable improvements on them and are located closer to towns. Large parcels of land are often located in more remote regions and/or have lower rainfall, fewer improvements and may be limited to single enterprise farming. Overall state medians are calculated using all transactions and will be influenced by the volume of transactions and the value per hectare. The state median is therefore closer to higher volume parcel size groups.

This report is not intended for use as a farm valuation tool. A qualified professional is required to assess the value of a property.

About the research

55

About Ag Answers Ag Answers is a specialist insights division of Rural Bank. Recognising that good information is the key to making good business decisions, Ag Answers provides research and analysis into commodities, farmland values, farm business performance and topical agricultural issues to enable farmers to make informed decisions.

About Rural Bank Rural Bank has been a wholly-owned subsidiary of Bendigo and Adelaide Bank Limited since 2010. It is the only Australian-owned and operated dedicated agribusiness bank in the country, providing exceptional financial services, knowledge and leadership for Australian farmers to grow.

For report enquiries:

AG ANSWERS

P 1300 796 101

For banking enquiries:

RURAL BANK

P 1300 660 115

W ruralbank.com.au

ELDERS

P 1300 618 367

Recommended