1

PQP/7B/Jan 2013

Accounting Principles

Question Paper, Answers and

Examiners Comments

Level 3 Diploma January 2013

2

PQP/7B/Jan 2013

Copyright of the Institute of Credit Management Institute of Credit Management The Water Mill, Station Road, South Luffenham, Oakham, Leicestershire LE15 8NB Bookshop Tel: 01780 722901. Education Tel: 01780 722909 Switchboard Tel: 01780 722900. Fax: 01780 721333

3

PQP/7B/Jan 2013

Accounting Principles questions, answers and examiners’ comments

UNIT 02 LEVEL 3 DIPLOMA IN CREDIT MANAGEMENT

JANUARY 2013

Instructions to candidates

Answer any FIVE questions. All questions carry equal marks. Time allowed: 3 hours

All ledger accounts must be prepared in continuous balance format

Final accounts must be prepared in vertical format

Where appropriate, VAT is to be calculated at 20%

Questions start on the next page

A good paper including a range of questions to cover the syllabus and which gave the

more able the chance to gain high marks - highest = 83. The paper really tested the less

well prepared (lowest mark 6). Candidates generally appeared prepared to deal with the

mix of numerical and written questions and the overall standard achieved was in line with

expectations.

The majority of candidates appeared to have sufficient time to complete the questions,

with one candidate attempting 6 questions, another answering all 8 questions set which

clearly wasted time. However approx 10% of candidates only attempted 3 or 4 of the set

questions, which does affect the marks awarded. Candidates are encouraged to attempt

the required 5 questions so that they can be awarded marks for their ability. Candidates

should also attempt all parts of each question which some candidates did not; this

restricted the marks they could achieve.

Some candidates still do not include their workings which doesn’t allow the examiner to

award any marks whilst one or two still use ‘T’ account format when the study text and

exam paper make it clear that the continuous balance format is a requirement.

4

PQP/7B/Jan 2013

1. a) Read the following cutting from the financial press, and then answer the questions

which follow:

‘Profits Warning at Leading Cars: From Ivor Pound, Financial Correspondent’

The share price of Leading Cars plc, the car retailing group, dipped sharply in January to

456p from its high of 587p last month following a profits warning from the company’.

TASK

How might the following users of these accounts be affected if Leading Cars plc does, in fact,

make a loss?

Shareholders

Managers

Suppliers. (6 marks)

b) When preparing final accounts it is important to distinguish between capital and revenue

expenditure.

TASK

i) Define capital expenditure using two appropriate examples. (3 marks)

ii) Define revenue expenditure using two appropriate examples. (3 marks)

iii) Explain why it is important to classify these types of expenditure correctly in the accounting

system. (4 marks)

iv) Show the relevant double entries for the following expenditure:

A business purchases a new air conditioning system costing £15,000 paying by

cheque, receiving a cash settlement discount of 5% for immediate payment

The businesses’ employees are used to install the new air conditioning system.

Included in total wages is the cost of £1,000 for labour costs

Plumbing and other materials cost of £1,500 was included in total purchases.

(4 marks)

Total 20 marks

Question aims

To test the candidate’s ability to:

Describe the requirements of the different users of accounting information and their

application of the data

Describe the difference between capital and revenue expenditure and give examples of

both.

5

PQP/7B/Jan 2013

Suggested answer

a) Shareholders:

As there has been a profits warning they will want to understand that their money is

safe and that there is a prospect of the company returning to previous levels of profit

and paying dividends

In the worst case scenario, shareholders could loose their investment if the company

makes a loss or becomes insolvent.

Managers

Managers, and employees are interested in information about the stability and

profitability of their employer

They need to assess the likelihood of future employment as they might lose their jobs

if Imperial Cars continues to make a loss

Firms that operate profitably are more likely to offer job security including

promotion/advancement

Managers might also be concerned about the ability of the firm to offer pay increases

and/or bonuses in the future

They will also be interested in the ability of the firm to continue to offer retirement

benefits.

Suppliers

These are people the business owes money to and they will be concerned about the

ability of Leading Cars to make payment within agreed credit terms

Suppliers might lose their money and future business/trading opportunities with the

firm

If Leading Cars is their major customer, then the suppliers will be concerned about the

long term survival of the business, as failure of this business will ultimately affect the

trading success/profitability of their own firm.

b) i) Capital expenditure results in the acquisition of fixed assets, or an improvement in their

earning capacity

Capital expenditure can be defined as expenditure incurred on the purchase, alteration

or improvement of fixed assets, e.g. land and buildings; motor vehicles; fixtures and

fittings; plant and machinery; computers)

Fixed assets are ’permanent’ assets of the business, which will be used for a number

of years to generate profit and thus the funds to buy these assets will be tied up for a

long time

If expenditure improves a fixed asset i.e. by making it superior to what it was when it

was first owned by the business (e.g. building an extension to a warehouse) then it is

treated as capital expenditure

Included in capital expenditure are costs such as Delivery of fixed assets; Installation

of fixed assets; Improvements (but NOT repair) of fixed assets; Legal costs of buying

property; Carriage inwards on machinery bought.

6

PQP/7B/Jan 2013

ii) Revenue expenditure is for the purpose of the trade of the business or to maintain the

existing earning capacity of fixed assets

Revenue expenditure is expenditure incurred on running expenses i.e. the day-to-day

expenses of a business, e.g. the cost of petrol or diesel for a motor vehicle or repairs

to a building

This is because the expenditure is used up in a short time, and does not add to the

value of the fixed assets

Included in revenue expenditure are the costs of maintenance and repairs of fixed

assets; administration of the business; selling and distribution of the goods or

products in which the business trades.

iii) Revenue expenditure is charged as an expense to the profit and loss account, provided

that it relates to the trading activity and sales of that particular period, which reduces

the net profit

Capital expenditure is charged to the balance sheet and results in the addition of fixed

assets to the business

Depreciation reduces the fixed asset value, and is treated as revenue expenditure,

although no ‘cash’ transaction takes place

Getting the classification wrong will affect the reported profits as well as the asset

values (and capital account) in the financial statements

If expenditure is treated as revenue expenditure, then it reduces the profit

immediately by the amount spent. However, if this is treated as capital expenditure,

then the reported profits are higher as the expense is shown as an asset on the

balance sheet

Following the dual-entry concept, if the fixed asset values are over-stated (i.e.

because revenue expenditure is treated as capital expenditure) then the profits will

also be over-stated

If the expenditure also affects items in the trading account, then the gross profit figure

will also be incorrect.

iv) This is capital expenditure and should increase fixed assets because it is an addition

to the property.

Dr Fixed Assets (air conditioning) 15,000

Cr Bank account 14,250

Cr Cash discount received 750

Wages should be reduced by £1,000 and Materials reduced by £1,500

Dr fixed assets (air conditioning) 2,500

Cr wages 1,000

Cr purchases 1,500

7

PQP/7B/Jan 2013

This was a popular choice, with a good range of marks being achieved.

Part a)

Although some candidates were clearly not prepared for a question which required them to

explain how a ‘profits warning’ would affect users of the accounts, more able candidates gave

fully developed explanations. Weaker candidates did not answer the question as set, for

example incorrectly explaining how managers would need to review budgets and cash flow by

arranging overdraft facilities and how Leading Cars would need to change to cheaper supplies.

Part (b)

Should have been expected and many candidates were able to correctly define both capital and

revenue expenditure giving two valid examples. However, the majority of candidates did not

fully appreciate the need to classify these correctly so that both gross and net profits and fixed

assets are correctly stated in the financial statements.

The final part of this question required candidates to apply concepts already covered when

dealing with capital expenditure. Although more able candidates showed correct entries,

weaker candidates did not recognise that the £750 discount would be deducted from the

payment, showing the gross figure of £15,000 as a credit to the bank account. Weaker

candidates were also confused by the mis-posting of wages and purchases by showing these

as debit entries to each account and then credit to the bank account in error. As the payment

had already been in the relevant costs, the correct entries increase (debit) fixed assets and

reduce (credit) costs.

8

PQP/7B/Jan 2013

2. a) The following balances were extracted from the books of Graham Weston, a sole trader,

as at 31October 2012:

£

Trade creditors 2,065

Stock held at 31 October 2012 3,073

Wages owing 225

Premises 27,400

Cash 500

Trade debtors 5,127

Furniture and fittings - cost 5,000

Furniture and fittings - accumulated depreciation 1,925

Motor vehicles - cost 10,000

Motor vehicles - accumulated depreciation 3,900

Plant and machinery - cost 20,000

Plant and machinery - accumulated depreciation 6,160

Bank overdraft 1,875

Insurance paid in advance 50

5 year loan from Loamshire Finance Co 7,500

Drawings 10,800

Net profit for the year ended 31 October 2012 12,970

Capital ?

No provision for depreciation has yet been made for the year ending 31October 2012.

Depreciation is to be provided using reducing balance method as follows:

Motor vehicles 25% per annum

Plant and machinery 15% per annum

Furniture and fittings 20% per annum

9

PQP/7B/Jan 2013

TASK

a) i) Prepare the balance sheet for Graham Weston as at 31 October 2012.

Note: An amended trial balance is not required. (11 marks)

ii) What is the meaning of the words ‘as at’ for the balance sheet heading?

(1 mark)

b) Graham Weston keeps referring to the motor vehicle as my car. His accountant has told

him that the car does not belong to him but to the firm. He replies that of course it

belongs to him, and furthermore, if the firm went bankrupt he would be able to keep the

car.

Use the appropriate accounting concept to help explain to Graham whose approach is

correct. (3 marks)

c) Graham Weston informs you that his business will use depreciation as a means to set

aside cash each year so that it eventually has the funds to purchase a replacement car

when this becomes necessary.

i) Comment briefly on the above statement. (2 marks)

ii) Use an appropriate accounting concept to help explain why a business will provide for

depreciation. (3 marks)

Total 20 marks

v) Question aims

To test the candidate’s ability to:

Construct a balance sheet for a sole trader business including both accruals and

prepayments, from information in a trial balance

State the purpose of a balance sheet

Explain the reasons for a depreciation provision

Calculate and include depreciation in the balance sheet of a business

Identify and explain relevant accounting concepts.

Suggested answer

Starts on next page

10

PQP/7B/Jan 2013

a) Workings - full trial balance not required – for information only

£ £

Trade creditors 2,065

Stock held at 31 October 2012 3,073

Wages owing 225

Premises 27,400

Cash 500

Trade debtors 5,127

Furniture and fittings – cost 5,000

Furniture and fittings – accumulated depreciation 1,925

Motor vehicles – cost 10,000

Motor vehicles – accumulated depreciation 3,900

Plant and machinery - cost 20,000

Plant and machinery – accumulated depreciation 6,160

Bank overdraft 1,875

Insurance paid in advance 50

5 year loan from Loamshire Finance Co 7,500

Drawings 10,800

Net profit for the year ended 31 October 2012 12,970

Capital = balancing figure 45,330

81,950 81,950

Motor vehicles

Cost £10,000 – 3,900 = £6,100 x

25%

= 1,525

Plant and machinery Cost £20,000 – 6,160 = £13,840 x

15%

= 2,076

Furniture and fittings Cost £5,000 – 1,925 = £3,075 x

20%

= 615

4,216

11

PQP/7B/Jan 2013

i) Balance sheet for Graham Weston as at 31 October 2012

£ £ £

Fixed assets Cost Depreciation NBV

Premises 27,400 0 2,740

Furniture and fittings 5,000 2,540 2,460

Motor vehicles 10,000 5,425 4,575

Plant and machinery 20,000 8,236 11,764

46,199

Current Assets

Stock 3,073

Debtors 5,127

Prepayments 50

Cash 500

8,750

Current Liabilities

Creditors 2,065

Accruals 225

Bank overdraft 1,875

(4,165)

Working capital/net current assets 4,585

50,784

Long-Term Liabilities

Loan from Loamshire Finance Co (7,500)

Net Assets 43,284

Financed by:

Capital Account (Graham Weston)

Opening capital (missing figure) 45,330

Add: net profit (12,970 - 4,216) 8754

57,084

Less: drawings (10,800)

43,284

ii) The balance sheet is a statement of the assets, liabilities and capital of a business at a

particular moment in time, i.e. 31 October 2012.

The balance sheet does not reflect a financial period, but only shows the value of assets,

liabilities and capital at a particular date.

12

PQP/7B/Jan 2013

b) Business Entity concept.

This refers to the fact that final accounts record and report on the activities of one

particular business. They do not include the assets and liabilities of those who play a

part in owning or running the business

The owner and the business are treated as two separate entities. The business affairs

are kept completely separate from those of the owner

As the car is shown on the firm’s balance sheet, it is an asset of Graham’s firm, not a

personal asset

As Graham is a sole trader he has unlimited liability, which means should he be unable

to pay the debts of the firm, then his personal assets may well be used to cover any

shortfall.

c) i) Depreciation is a non-cash expense, i.e. unlike the other expenses in the profit and

loss account, no cheque is written out, or cash paid, for depreciation

In cash terms, depreciation causes no outflow of money and is not a method of

providing a fund of cash which can be used to replace the asset at the end of its life

In order to do this, it is necessary to create a separate fund into which cash is

transferred at regular intervals , known as a reserve account

This technique is often known as a sinking fund and it needs to be represented by a

separate bank account e.g. deposit account, which can be drawn against when the

new fixed asset is to be purchased. This is not, however, a common practice.

ii ) Depreciation is an application of the accruals (matching) concept because we are

recording the timing difference between payment for the fixed asset and the asset’s

loss in value

Depreciation is an estimate of the amount of loss in the value of fixed assets over an

estimated time period

As a fixed asset will be used by the business in the generation of profits for a number

of years, the full cost is not charged to the profit and loss account in a single year i.e.

when it is bought, only a proportion of the cost of the asset is charged to the profit

and loss account and matched against the revenue which it helps to generate

Fixed assets lose value as time goes by largely as a result of wear and tear. This loss

in value is known as depreciation and in business accounts it is necessary to record

the amount of this loss in value in order to present a realistic view of the business

The balance sheet must reflect as accurately as possible the value of fixed assets in

accordance with the prudence concept so that profits and asset values are not

overstated.

This was another reasonably popular question choice, with the full range of marks being

achieved.

Part a) required the preparation of a balance sheet from given information, although the trial

balance required a calculation of working capital = balancing figure of £45,330 only attempted

by a few candidates. The majority of candidates did recognise that ‘both sides’ of the balance

sheet should equal the same amount, but did not realise that the profit figure would need to be

adjusted for the current year’s total depreciation (£4,216). Weaker candidates did not adjust

the depreciation figure for fixed assets, showing the total from the trial balance in error, and

thus losing valuable marks. Despite being told that the bank was overdrawn, some candidates

treated this as a current asset in error.

13

PQP/7B/Jan 2013

Only more well prepared candidates correctly identified and explained the business entity

concept, although many recognised the business and owner are treated as two separate entities.

Only a few candidates explained the effect of unlimited liability on the owner’s personal assets.

Part c) was also only answered fully by the more able candidates. Weaker candidates applied

the consistency concept which is not appropriate here as it an approach for applying

depreciation, not matching cost with wear and tear. As a result, some candidates wasted time

explaining the difference between reducing balance and straight line depreciation and/or which

should be used for the motor vehicle.

14

PQP/7B/Jan 2013

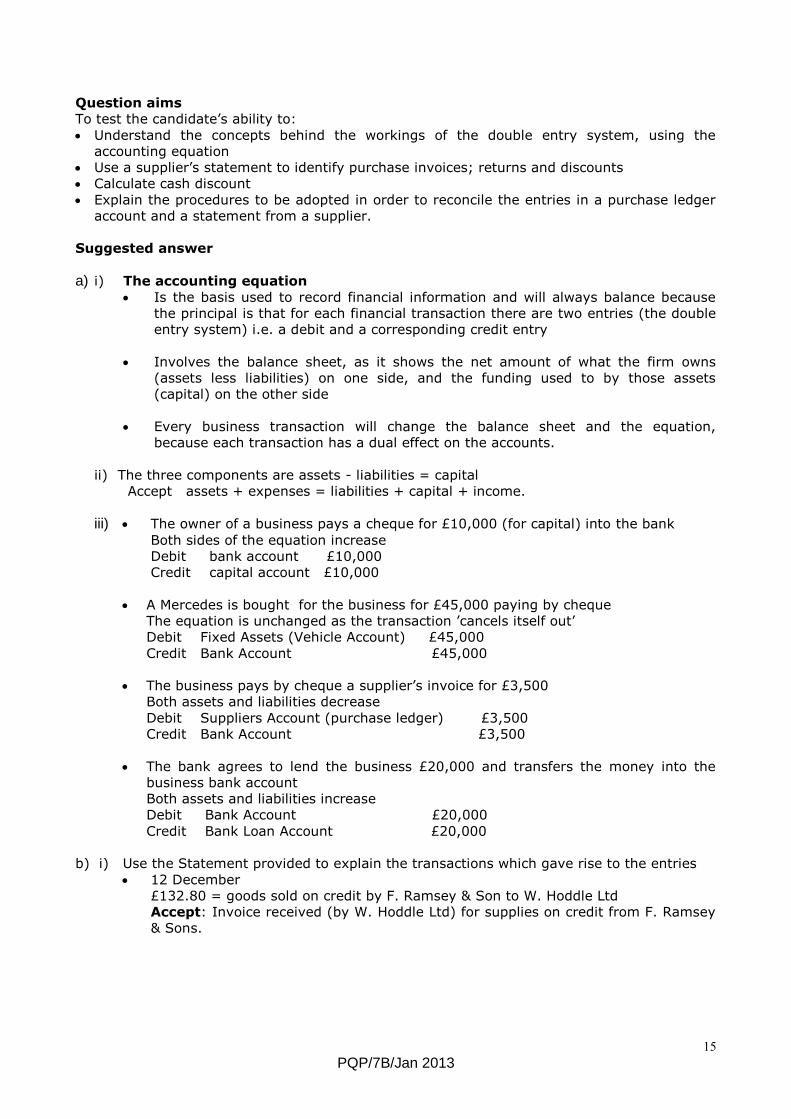

3. a) i) Explain what is meant by the term accounting equation. (2 marks)

ii) Identify the components of the equation. (1 mark)

iii) State how the accounting equation is affected by the following transactions:

The owner of a business pays a cheque for £10,000 (for initial capital) into the

bank

A Mercedes is bought for the business for £45,000 paying by cheque

The business pays by cheque a supplier’s invoice for £3,500

The bank agrees to lend the business £20,000 and transfers the money into the

business bank account. (4 marks)

b) You have received the following statement of account from F. Ramsey & Son who are

VAT registered traders. However, their book-keeper has not had any formal training

and so the information and layout provided may not be wholly correct.

Statement Of Account

F. Ramsey & Son

31 North Street, Liverpool

W Hoddle Limited

Black Pool Road

Manchester

31 December 2012

Date 2012 Reference Dr Cr Balance

1 December B/F Dr 522. 80

8 December 62290 178. 00 700. 80

12 December 63492 132. 80 833. 60

14 December Cheque and

discount 522. 80 310. 80

17 December 89247 480. 00 790. 80

20 December 864 58. 00 732. 80

30 December 91082 347. 20 1,080. 00

Cash discount 5% if paid within one month of the date of this statement

TASK

i) Explain the transactions which gave rise to the entries dated:

12 December

14 December

20 December. (4 marks)

ii) Calculate the amount of cash discount W. Hoddle Ltd will receive if they pay the above

account on 18 January 2013. (1 mark)

iii) Explain why it is good practice to reconcile entries in a purchase ledger account and a

statement from a supplier. (3 marks)

iv) Explain why the purchase ledger and suppliers’ statement are unlikely to agree.

(5 marks)

Total 20 marks

15

PQP/7B/Jan 2013

Question aims

To test the candidate’s ability to:

Understand the concepts behind the workings of the double entry system, using the

accounting equation

Use a supplier’s statement to identify purchase invoices; returns and discounts

Calculate cash discount

Explain the procedures to be adopted in order to reconcile the entries in a purchase ledger

account and a statement from a supplier.

Suggested answer

a) i) The accounting equation

Is the basis used to record financial information and will always balance because

the principal is that for each financial transaction there are two entries (the double

entry system) i.e. a debit and a corresponding credit entry

Involves the balance sheet, as it shows the net amount of what the firm owns

(assets less liabilities) on one side, and the funding used to by those assets

(capital) on the other side

Every business transaction will change the balance sheet and the equation,

because each transaction has a dual effect on the accounts.

ii) The three components are assets - liabilities = capital

Accept assets + expenses = liabilities + capital + income.

iii) The owner of a business pays a cheque for £10,000 (for capital) into the bank

Both sides of the equation increase

Debit bank account £10,000

Credit capital account £10,000

A Mercedes is bought for the business for £45,000 paying by cheque

The equation is unchanged as the transaction ’cancels itself out’

Debit Fixed Assets (Vehicle Account) £45,000

Credit Bank Account £45,000

The business pays by cheque a supplier’s invoice for £3,500

Both assets and liabilities decrease

Debit Suppliers Account (purchase ledger) £3,500

Credit Bank Account £3,500

The bank agrees to lend the business £20,000 and transfers the money into the

business bank account

Both assets and liabilities increase

Debit Bank Account £20,000

Credit Bank Loan Account £20,000

b) i) Use the Statement provided to explain the transactions which gave rise to the entries

12 December

£132.80 = goods sold on credit by F. Ramsey & Son to W. Hoddle Ltd

Accept: Invoice received (by W. Hoddle Ltd) for supplies on credit from F. Ramsey

& Sons.

16

PQP/7B/Jan 2013

14 December

£522.80 = payment received by F. Ramsey & Son from W. Hoddle Ltd, including

settlement discount allowed to W. Hoddle Ltd

Accept: Payment made to F. Ramsey & Son which cleared the balance brought

forward on 1st December.

Settlement discount = £21.78; cheque = £501.02

20 December

£58.00 = goods returned by W. Hoddle Ltd to F. Ramsey & Son

Credit note issued by F. Ramsey & Son.

ii) £1,080 = £900 x 5% = £45. 00

1.20 VAT

iii) The statement is the suppliers’ (F. Ramsey & Son) record of transactions that have

taken place with a customer and should contain the same information as the customer’s

ledger (W. Hoddle Ltd), in a similar format

In a small firm it is relatively easy to check that goods as ordered have been supplied

but it is important that there is some mechanism in place to verify that the goods have

been received before an invoice from a supplier is entered in to the purchase ledger and

authorised for payment

W. Hoddle Ltd should check the statement from F. Ramsey & Son with their own

records of the transactions that have taken place using the purchase ledger

In most instances the reconciliation of the two sets of figures will be straightforward as

invoices, credit notes and other documentation will carry dates and reference numbers,

which make for easy referencing by both firms

The entries in the statement and the purchase ledger account can then be reconciled

and agreed for payment.

iv) Reconciliation does not mean that every invoice the supplier has listed on the

statement is in order, and should be paid. There may be reasons for differences, and

action should be taken to rectify these differences before payment is made.

These differences could arise as follows:

Goods have been sent back to the supplier shortly before the statement date, and the

supplier has not yet issued a credit note

The supplier may have offered a specific trade discount but the suppliers accounts

department have not been notified, and the goods have been invoiced at normal price

Payments may have been made after the statement date so that the supplier has not

included this in the latest statement

Goods from an order may not yet have been delivered to the customer i.e. marked ‘to

follow’ but the supplier has included these on the invoice and on the statement

There may be items on the statement that do not relate to the firm at all

Settlement discount may have been taken when it is outside the terms agreed and

therefore has been disallowed

17

PQP/7B/Jan 2013

Invoices and credit notes may have been issued but not yet received, i.e. timing

differences

Invoices and credit notes may have gone missing i.e. not received at all.

This was not a particularly popular question choice, although more able candidates did achieve

good marks.

Part a) relied on the relationships assets - liabilities = capital although weaker candidates

used current assets and liabilities = working capital, which was not required. Candidates were

required to explain what is meant by this equation, although weaker candidates tried to

explain and give examples for each element of the accounting equation which was not

required. Candidates were then required to apply the accounting equation and to recognise

the ‘double entry’ transactions which had taken place. Although more able candidates gave

fully correct answers, the less able simply repeated the information provided linking it to the

accounting equation and not identifying the Debit and Credit entries. Some candidates used

the cumulative figures provided, and were not able to identify the ‘new’ transactions taking

place at each stage.

Part b) had not previously been examined in this way, and although more able candidates

were able to fully explain the transactions, weaker candidates did not appear to have read the

initial information stating that the layout ‘might not be wholly correct’ and confused invoices

with payments and credit notes with invoices, thus gaining few marks. The calculation of cash

discount also confused many candidates who did not exclude the VAT element and so

calculated £1,080 x 5% = £54 instead of the actual net figure of £900 x 5% = £45.

Part c) required candidates to apply a standard requirement for the credit manager i.e. the

reconciliation of the purchase ledger with supplier’s statement, and then identify reasons for

disagreement. Again, only the very well prepared candidates gained good marks for this part

of the question, with weaker candidates confusing the two aspects of the question, and thus

gaining few marks overall.

18

PQP/7B/Jan 2013

4. Byron Beasley Limited manufactures components for the motor vehicle industry. The

following is a summary of some of its accounting ratios as at 31 December 2011 and 31

December 2012.

2012 2011

Current ratio 1.7 : 1 1.5 : 1

Quick ratio 0.8 : 1 1.1 : 1

Stock turnover 63 days 59 days

Debtors’ ratio 63 days 52 days

Creditors’ ratio 78 days 71 days

Interest cover 6.2 times 7 times

TASK

a) State the formulae which will have been used to calculate each ratio. (3 marks)

b) Explain the meaning and purpose of these ratios. (9 marks)

c) Identify and comment on possible reasons for any changes in the ratios for Byron Beasley

Limited. (3 marks)

d) Calculate and explain the cash operating cycle. (2 marks)

e) Discuss what actions Byron Beasley Limited could take to improve the cash operating cycle.

(3 marks)

Total 20 marks

Question aims

To test the candidate’s ability to:

Analyse the financial statements of a given organisation and evaluate their reliability as a key

indicator of performance:

State the formulae for a number of accounting ratios

Assess the performance of the business based on calculated ratios

Explain the importance of working capital and calculate the cash operating cycle for a

business.

Suggested answer

a)

Current ratio Current assets

Current liabilities

Quick ratio Current assets - stock

Current liabilities

Stock turnover Average stock x 365

Cost of sales

Debtors’ ratio Debtors x 365

Credit Sales

Creditors’ ratio Creditors x 365

Purchases

Interest cover Profit before interest and tax

Interest payments

19

PQP/7B/Jan 2013

b) Current ratio

This measures the relationship between current assets and current liabilities i.e. working

capital. These figures are usually taken from the balance sheet.

Although there is no ideal working capital ratio 2:1 is often accepted i.e. there are £2 of

current assets for each £1 of current liabilities. This indicates how well a firm can meet its

day-to-day liabilities.

Quick ratio

This is also known as the ‘acid test’ which uses current assets and current liabilities from

the balance sheet, but stock is omitted.

This is because stock is the most illiquid of assets i.e. it has to be sold, turned into debtors

and then the cash collected from the debtors.

The balance between liquid assets (debtors and cash/bank) and current liabilities should

ideally be 1: 1 i.e. £1 of liquid assets to each £1 of current liabilities. At this ratio a

business is expected to be able to pay its current liabilities from its liquid assets. A figure

below 1: 1 indicates that the company would have difficulty in meeting pressing demands

from creditors.

Stock turnover

This ratio uses information from the Trading Account. Average stock is usually found by

making the simple average of the opening and closing stocks i.e.

(Opening Stock + Closing Stock

2

Stock turnover is the number of days’ stock held on average. As Byron Beasley Limited

manufacture components for the motor vehicle industry they may hold large volumes of

stock items.

Debtor’s ratio

This calculation shows how long, on average, debtors take to pay for goods sold to them

by the business. Some businesses make the majority of their sales on credit, but others

will have a lower proportion of credit sales. As the company manufacture components for

the motor vehicle industry it would be anticipated that the majority of their sales are on

credit terms.

The debt collection time should be compared with terms offered to contextualise the result

and should be compared with the previous year to show how efficient the firm is at

collecting the money that is due.

Results can also be compared with other businesses in the same sector for benchmarking.

Creditor’s ratio

This measures the speed at which a firm pays its creditors (i.e. suppliers) and should be

compared to the credit terms given. Efficient management of payment to creditors is that

it should be longer than the time taken to collect payment from debtors. Firms should

take full use of the credit period given, but while creditors can be a useful temporary

source of finance, delaying payment too long, may cause problems.

20

PQP/7B/Jan 2013

Interest cover

This indicates the number of times the profit before interest and tax can cover the interest

payable. This is a useful ratio for lenders, as banks will usually specify a required ratio

(usually 3 times) when dealing with any loan agreement.

Although the ratio may show that there is sufficient profit to cover the interest due, this

does not necessarily mean that there is cash available to pay the interest, so that the

liquidity ratio must also be considered. However, there is no information to indicate

whether loans have been paid and/or increased during the year, which will affect the

interest cover.

c) The current ratio (working capital) has improved (2012 = 1.7; 2011 = 1.5) which is below

the average of 2:1, but the quick (liquidity) ratio has got worse (2012 = 0.8; 2011 = 1.1)

and is also now below the average of 1:1. This suggests a possible build up of stocks held

for re-sale.

The stock turnover has increased (2012 = 63 days; 2011 = 59 days) which also points to

an increase in stocks and/or a decrease in sales.

The debtors’ ratio (2012 = 63 days; 2011 = 52 days) shows that debtors are being

allowed to take a considerably longer period of credit.

The creditors’ ratio (2012 = 78 days; 2011 = 71 days) shows that this company is taking

longer to pay its debts.

The interest cover is decreasing (2012 = 6.2 times; 2011 = 7 times) which is above the

average of 3 times. This may be an indicator that there may be insufficient profits in the

future, and the firm may have difficulty in paying interest.

Overall there is deterioration in liquidity and control of working capital as well as interest

cover. It appears there may be:

Overstocking i.e. money is tied up un-necessarily in unsold stock which could lead to

loss of sales

Poor stock control, which could mean that some of the stock included in the balance

sheet figure may be un-saleable or obsolete

A relaxation of credit control procedures as it now takes on average 11 days longer to

collect debts due, which may lead to bad debts increasing.

d) Calculate and explain the cash operating cycle

Stock turnover + Debtor Collection time – Creditor payment time

2012 63 + 63 = 126 - 78 = 48 days

2011 59 + 52 = 111 - 71 = 40 days.

This is a further use of ratios to calculate the period of time between payments for goods

received into stock and the collection of cash from customers in respect of their sale.

The shorter the length of time between the initial cash outlay and the ultimate collection of

cash, the lower the value of working capital to be financed by the business.

21

PQP/7B/Jan 2013

e) Whilst the cash operating cycle is the same for both years, it might be appropriate for the

firm to consider actions which will reduce the cycle by either:

Reducing stocks, which will lower the number of days that stock is held but this might

mean that a poorer service is offered to customers, who might take their business

elsewhere. The firm might also consider investing in a stock management system to

improve stock control.

Speeding up the rate of debtor collection i.e. allowing debtors less time to pay, but

this may also cause customers to seek alternative suppliers who are offering better credit

terms. Alternatively there may be an option to offer discounts for early settlement, or to

charge interest on overdue accounts.

Slowing down the rate of creditor payments i.e. taking longer to pay the creditors,

but this may be difficult, as suppliers might decline to supply goods unless immediate

payment is forthcoming i.e. may ask for cash with order. This could have a detrimental

effect on the firm’s credit rating and other suppliers might also refuse to supply goods.

Ratio analysis is a very common type of question and was popular with some well developed

answers which achieved good marks. However, weaker candidates appeared to be confused

by the lack of financial statements and were confused by the fact that the actual ratios had

already been calculated.

Part a) required the relevant formula for each ratio and whilst many gained max marks here,

the ratio for interest cover caused most difficulty.

Part b) and c) should have been anticipated and again, many gave good explanations although

weaker candidates gave very basic comments and did not achieve the development required.

Only the more well prepared candidates fully recognised the reasons for the changes in the

ratios over the two years.

Part c) and d) required candidates to apply and discuss the cash operating cycle and again whilst

many did well, weaker candidates did not calculate the cycle for both years, and thus their

explanation about how the cycle could be improved was not fully correct.

22

PQP/7B/Jan 2013

5. a) Explain the main similarities and differences between ordinary shares and debenture

loans. (6 marks)

b) You have been provided with the following selected balances of Filo plc as at 31

December 2012, together with the additional information which follows:

£

Retained profits as at 31 December 2011 102,000

Stocks held at 1 January 2012 84,000

Purchases 1,462,000

Turnover 2,456,000

Returns inwards 108,000

Returns outwards 37,000

Carriage inwards 14,700

Wages and salaries 136,000

Rent and business rates 14,000

General distribution expenses 28,000

General administrative expenses 24,000

Discounts allowed 36,000

Bad debts 5,000

Loan interest 12,000

Motor expenses 16,000

Interest received on bank deposits 6,000

Other income 7,000

Motor vehicles at cost 146,000

Equipment at cost 27,000

Ordinary share dividends paid 120,000

Stocks held at 31 December 2012 £102,000

Wages and salaries accrued amount to £12,000

Rent and business rates prepaid amount to £1,700

Depreciate motor vehicles 20% and equipment 10% on cost

Ordinary share dividend proposed £42,000

Accrue auditors’ remuneration of £11,000

Accrue corporation tax for the year on ordinary profits £364,000.

TASK

Prepare a trading, profit & loss and appropriation account for internal use. (14 marks)

Total 20 marks

23

PQP/7B/Jan 2013

Question aims

To test the candidate’s ability to:

Explain and describe the terminology used in the preparation of statutory accounts for

limited companies

Use an extract of a trial balance to construct a trading, profit and loss and appropriation

account, including adjustments for accruals, prepayments and depreciation

Suggested answer

a) Ordinary shares

Also known as equity shares, they are the ultimate risk takers

Shareholders are owners of the company who are normally entitled to vote at general

meetings of the company e.g. to elect directors and appoint auditors

Shareholders may receive a dividend annually, at a rate decided by the company’s

directors. The dividend varies each year depending on the profit, and is an

appropriation of the profit. If the company is not profitable enough a dividend may

not be paid.

They are last to be repaid the value of their shares in the event of the company going

into liquidation

Shareholders funds are Non-repayable except on the liquidation of the company

Their rights are outlined in the Articles of Association

Dividends are non-deductible from company profits i.e. for tax purposes.

Debenture loans

These are long-term loans, which are usually secured against the assets of the

company

Debenture holders have no voting rights

Receive a fixed rate of interest which constitutes a charge against income when

calculating the profit

They have priority over preference dividends (and thus over ordinary shareholders)

They are repaid before either preference or ordinary shareholders in the event of

liquidation as they are usually secured creditors

They are normally repayable after a fixed period of time

Their rights are specified at the time of issue of the loan agreement

Interest is deducted from profits for tax purposes.

24

PQP/7B/Jan 2013

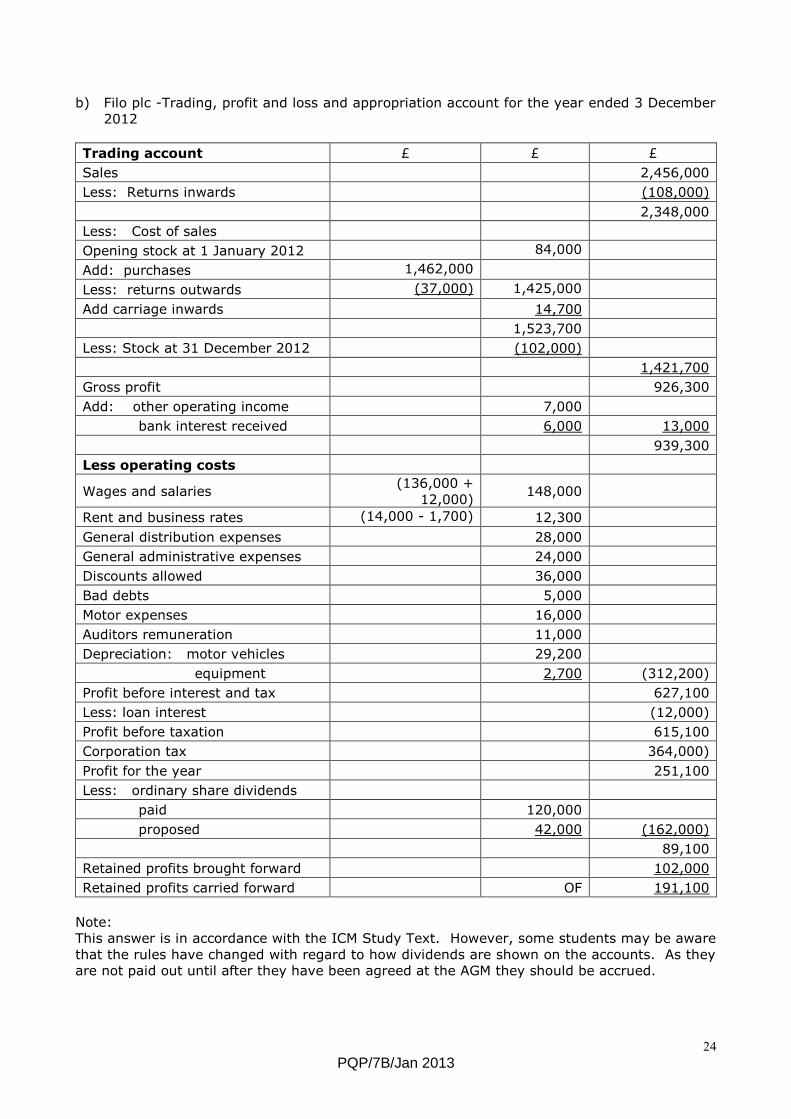

b) Filo plc -Trading, profit and loss and appropriation account for the year ended 3 December

2012

Trading account £ £ £

Sales 2,456,000

Less: Returns inwards (108,000)

2,348,000

Less: Cost of sales

Opening stock at 1 January 2012 84,000

Add: purchases 1,462,000

Less: returns outwards (37,000) 1,425,000

Add carriage inwards 14,700

1,523,700

Less: Stock at 31 December 2012 (102,000)

1,421,700

Gross profit 926,300

Add: other operating income 7,000

bank interest received 6,000 13,000

939,300

Less operating costs

Wages and salaries (136,000 +

12,000) 148,000

Rent and business rates (14,000 - 1,700) 12,300

General distribution expenses 28,000

General administrative expenses 24,000

Discounts allowed 36,000

Bad debts 5,000

Motor expenses 16,000

Auditors remuneration 11,000

Depreciation: motor vehicles 29,200

equipment 2,700 (312,200)

Profit before interest and tax 627,100

Less: loan interest (12,000)

Profit before taxation 615,100

Corporation tax 364,000)

Profit for the year 251,100

Less: ordinary share dividends

paid 120,000

proposed 42,000 (162,000)

89,100

Retained profits brought forward 102,000

Retained profits carried forward OF 191,100

Note:

This answer is in accordance with the ICM Study Text. However, some students may be aware

that the rules have changed with regard to how dividends are shown on the accounts. As they

are not paid out until after they have been agreed at the AGM they should be accrued.

25

PQP/7B/Jan 2013

This was a popular question choice and many of the candidates who attempted this question

found it manageable and achieved high marks.

Part a) required an understanding of the differences and similarities between ordinary share

capital and debenture loans. As anticipated only the very well prepared candidates achieved

max marks for this part of the question.

For part b) candidates were required to prepare the trading, profit and loss account and the

adjustments were done accurately by the more able candidates. Some still had difficulty

dealing with opening/closing stock reversing these figures. Common errors included:

Including the £108,000 returns inwards as part of operating costs (expenses) and not

deducting from sales

Treating carriage inwards £14,700 as expenses not cost of sales

£37,000 returns outwards either treated as “+” rather than deduction from cost of sales

and/or treating this as sales returns

Including the £12,000 loan interest as part of expenses and not recognising the profit

should be calculated before interest and tax

A few candidates treated PBIT as Gross Profit in error.

The appropriation account was only prepared accurately by the more able, as weaker

candidates ignored the £120,000 dividend paid. The retained profit b/f £102,000 was also

ignored by less able candidates.

26

PQP/7B/Jan 2013

6. a) Claire Hamilton runs an ironing service, and now wishes to buy a more reliable motor

vehicle for her business.

TASK

Explain two advantages and two disadvantages of these two alternatives:

i) Hire purchase. (4 marks)

ii) Leasing. (4 marks)

b) Revamp Furniture Ltd prepare annual figures to 31 May and have provided you with the

following management figures for month 7, and the cumulative budget for the year 2013:

Budget trading and profit and loss account for the year ended 31 May 2013

Period 7 Cumulative Whole Year

Budget Actual Variance Budget Actual Variance Budget

Latest forecast

£000 £000 £000 £000 £000 £000 £000 £000

Sales 500 600 100 3,500 3,420 (80) 6,000 6,200

Direct cost of sales

280 322 (42) 1,960 1,951 9 3,500 3,850

Factory overheads

58 69 (11) 420 400 20 700 750

Administration

& selling costs 122 123 (1) 840 800 40 1,320 1,147

Total costs 460 514 (54) 3,220 3,151 69 5,520 5,747

Operating profit

40 86 46 280 269 (11) 480 453

Profit: sales % 8% 14.3% 8% 7.9% 8% 7.3%

TASK

i) For each item of income and expenditure, explain what this information tells the directors

of Revamp Furniture Ltd about their business profits. (10 marks)

ii) Explain the circumstances when an auditor might issue a qualified opinion on the financial

statements. (2 marks)

Total 20 marks

27

PQP/7B/Jan 2013

Question aims

To test the candidate’s ability to:

Explain the advantages and disadvantages of medium-term debt finance for a sole trader

Understand the process of monitoring and analysing budgets using variance analysis

Explain why and when an auditor might issue a qualified opinion.

Suggested answer

a) i) Hire purchase

Hire purchase is actually two agreements, one for hire and the other an option to

purchase at the end of the term by paying an additional amount. Purchase is usually via

a secured loan that is paid back monthly across the agreed period, usually 3 - 5 years.

Monthly payments are therefore much higher than when ‘leasing’.

Advantages of Hire purchase

Hire Purchase is a method of acquiring assets without having to invest the full amount

in buying them. Typically, a hire purchase agreement allows the hire purchaser sole use

of an asset for a period after which they have the right to buy them, often for a small or

nominal amount. The benefit of this system is that companies gain immediate use of

the asset without having to pay a large amount for it or without having to borrow a

large amount.

Hire purchase is cheaper than an, ‘unsecured’, personal loan because the ownership of

the car is retained by the finance company, i.e. it is secured, and if you don’t make

your monthly payments then they will simply take the vehicle back. However, you will

still have to pay any outstanding installments, plus any interest due.

Hire purchase is relatively quick as it is offered directly by most dealers and

manufacturers and is agreed to more easily than personal loans

Deposits are lower than with personal loans

If you intend to own and retain the same car for more than 4 or 5 years, than hire

purchase is cheaper over the long term than leasing because there are no further

payments once you own it completely.

Disadvantages of Hire Purchase

Often the finance company will expect all of the VAT for the whole value of the car to be

paid with the first installment, whereas with leasing the upfront payment is only the

equivalent of three months payments:

The monthly payment required is always much higher

You are paying interest on the full value of the car, even if you don’t intend to retain

it for longer than 2-4 years

There are often hidden fees and so you would need to shop widely before being sure

you have a good deal

The termination fee is significant if your circumstances change and you don’t want

the car anymore.

You are not the owner of the car from day one so you can not modify or sell it.

28

PQP/7B/Jan 2013

ii) Leasing

Leasing is a contract between the leasing company, the lessor, and the customer (the

lessee). The leasing company buys and owns the asset that the lessee requires. The

customer hires the asset from the leasing company and pays rental over a pre-determined

period for the use of the asset. There are two types of leases:

Finance Leases

Under a finance lease the rental covers virtually all of the costs of the asset therefore the

value of the rental is equal to or greater than 90% of the cost of the asset. The leasing

company claims writing down allowances, whilst the customer can claim both tax relief and

VAT on rentals paid

Operating Leases

The lease will not run for the full life of the asset and the lessee will not be liable for its full

value. The lessor or the original manufacturer or supplier will assume the residual risk.

This type of lease is normally only used when the asset has a probable resale value, for

instance, aircraft or vehicles.

The most common form of operating lease is known as contract hire. Essentially, this gains

the customer the use of the asset together with added services. A very common example

of an asset on contract hire would be a fleet of vehicles.

Advantages of Leasing

Car leasing provides the option of making no down payment, although you must still make

the first month's payment and any registration fees. Some promotional lease deals require

a down payment to get the deal.

Since monthly lease payments are lower than with buying, you get to drive a new vehicle

every two to four years, depending on the term length of your lease.

Most people like to lease for a term that coincides with the length of the manufacturer's

warranty coverage so that if something goes wrong with the car, the repairs are always

covered.

Most car leases require little or no down payment, which makes getting into a new car

more affordable and frees up your cash for other things. However, you can choose to

make a down payment, or trade in your old vehicle, to lower your monthly payment

amount.

With leasing, the headaches of selling a used car are eliminated. When your lease ends,

you simply turn it back to the leasing company and walk away, unless you decide to buy it

or trade it.

Disadvantages of Leasing

If you must terminate your lease before the end of your contract, the cost is usually very

high, much higher than might be expected.

The trade-off for low monthly lease payments is that you typically do not build ownership

or trade-in value in your leased vehicle. However, it is fairly common that the market

value of a vehicle at lease-end is higher than the purchase option price specified in the

lease contract, which means you may have some equity trade value.

If you exceed the mileage allowance in your lease contract, you will be charged for the

extra miles at a specified per-mile rate. A large mileage excess could result in a hefty

charge, even at a reasonable per-mile rate.

29

PQP/7B/Jan 2013

If you return a leased vehicle at lease-end with excessive dents, scratches, or unrepaired

accident damage, you will be charged — because those damages reduce the vehicle's

value. Most lease companies clearly specify what is considered "excessive" so that you'll

know if you should get it repaired before returning your vehicle. Get the repairs done

yourself before you return the vehicle and avoid being charged.

b) i)

Sales for Period 7 were significantly above budget by favourable £100,000. However, the

cumulative to date figures show that sales had in fact been below budget. The increase for

Period 7 has reduced this adverse variance/shortfall to £80,000. If this trend continues

then by the end of the year, overall sales should exceed budget by £200,000. However,

additional strategies to increase sales may be required if overall profit margins are to be

maintained at 8%.

Direct Cost of Sales are naturally higher when sales are higher and it is possibly easier to

understand the trend by calculating direct costs as a %age of Sales i.e. Direct costs x 100.

Sales

Budget Actual

Period 7 280/500 x 100 56.0% 322/600 x 100 53.66%

Cumulative to

date 1960/3500 x 100 56.0% 1951/3420 x 100 57.05%

Forecast for year 3500/6000 x 100 58.33% 3850/6200 x 100 62.10%

The forecast for direct costs was original set at 56%, but this has increased to 57.05% and

is now predicted to be 62.10%. This is now forecast for the year as a whole as adverse by

£350,000, i.e. additional direct costs are anticipated.

However, period 7 direct costs are not consistent with this trend showing an adverse

variance of £42,000, and the directors may need to investigate the variance further to

establish if this is related to some peculiarity in sales mix or as a result of savings from bulk

buying, which has reduced costs.

Factory overheads were un-favourable in period 7, adverse by £11,000) although

cumulative the variance shows a favourable figure of £20,000. Overall the forecast for the

year shows an adverse variance of £50,000, i.e. additional costs not included in budget.

Again the directors may need to investigate this trend, as the budget may not have included

inflationary increases correctly.

Administration and selling costs are also adverse by £1,000 with a cumulative

favourable variance of £20,000. This predicts an overall favourable variance of £173,000.

It would appear that considerable economies are planned and have already commenced.

Operating profits have improved for Period 7 by a favourable figure = £46,000 although

the cumulative figure is still adverse by £11,000. This shows an overall improving trend but

the forecast for the year remains as adverse £27,000 i.e. profits will not be as high as

anticipated. This is confirmed by the Profit margin, which has fallen from the budget figure

of 8% to an overall margin of 7.3%. The directors would be advised to request more

frequent variance reporting (maybe weekly) so that tighter control on costs can be

maintained.

30

PQP/7B/Jan 2013

ii) When deciding to give a qualified opinion, auditors must objectively take into consideration

uncertainties about the outcome of future events, and their potential financial effect.

The auditors may give a qualified opinion if they disagree with the treatment or disclosure

of an item in the financial statements, and in the opinion of the auditors, the effect of this

does not give a true and fair view.

Disagreements may arise on:

The use of an inappropriate accounting treatment or disclosure

The actual accounts or facts included

Failure to comply with accounting requirements

A limitation on the scope of the auditors examination i.e. the quality and type of

evidence provided or insufficient evidence

Not all accounting records being made available

Directors preventing a ‘testing’ procedure requested by the auditors e.g. to verify the

stock take.

This was the least popular question choice and candidates did not appear prepared to deal with a

question about budget analysis, which was disappointing.

Part a) was generally well answered as candidates could explain the advantages and

disadvantages of Hire Purchase v Leasing. However, weaker candidates either prepared a ‘list’

and/or did not provide detailed explanations which were required for full marks.

Part b) required an explanation of the cause of each variance based on the current period; the

cumulative figures and the year. Weaker candidates did not identify the variance as

adverse/favourable and many simply repeated the information given, gaining few marks.

Explanations were vague using terms such as ‘down/up’ or jargon (slipping away) which made it

difficult to award marks. No candidates attempted to calculate %age of sales and did not appear

to be prepared for a question of this nature.

Part b) required an understanding of the auditor’s role when giving a qualified opinion, and again

only the more well prepared gave fully developed explanations and examples.

31

PQP/7B/Jan 2013

7. a) The accountant for James Scriven Ltd has prepared the following aged debtor analysis.

As credit manager, you have to decide what bad debts to write off and then calculate

the new provision for doubtful debts.

Aged debtor analysis at 31 December 2012

Age of debt

Debtor Total

debt

Less than

1 month

1-2

months

2-3

months

3-4

months

Over 4

months

Peter Lounds

Ltd 4,200.80 2,000.00 1,800.40 210.30 189.20

Zandra Smith 750.43 750.43

D S Cox 3,900.00 1450.26 2250.70 199.00

Softseat Ltd 580.67 340.67 240.00

P Bond 2,622.20 900.00 1,220.00 200.40 292.12 9.62

T F Day 780.00 340.60 439.40

B G Moon 169.23 121.23 48.00

Total 13,002.53 4,812.09 5,758.50 410.80 821.99 1,199.05

The company’s credit policy is:

To write off as bad debts all debts over 4 months old

Make a specific provision for debts over £200 and between 3 and 4 months old

Make a general provision of 3% of the remaining debtors.

TASK

a) i) Showing your workings, calculate the new provision for doubtful debts.

(3 marks)

You have also been provided with the following additional information:

In 2011, a debt owed by Quality Furnishings Ltd was written of as a bad debt.

On 31 March 2012, £101.34 (including VAT at standard rate) was received in final

settlement of the debt.

The provision for bad debts at 1 January 2012 was £340.

ii) Using both the relevant aged debtor analysis and this additional information, prepare

the following accounts:

Bad debts

Provision for doubtful debts

Bad debts recovered

Quality Furnishings Ltd for 2012 only. (7 marks)

iii) If gross profit was £192,000 and expenses £78,000 before the above adjustments,

showing your workings calculate the revised net profit. (3 marks)

32

PQP/7B/Jan 2013

b) The accountant informs you that he has extracted a trial balance, but this does not agree

and he has placed the difference in a suspense account.

The following errors have been identified:

£35 discount allowed to Forest Ltd has been debited to their account

Purchases of goods for £910 from Drystone Brothers posted to their account in error

as £700

Sales account has been overcast by £70

A sales invoice for £245 has been entered in Clair & Sons account as £385

TASK

i) Make appropriate journal entries to rectify these errors. (4 marks)

ii) Draft the suspense account after the above errors have been corrected showing the original

balance. (3 marks)

Question aims

To test the candidate’s ability to:

Calculate the bad debts to be written off from an analysis of balances outstanding

Calculate the provision for doubtful debts using the same analysis

Prepare a provision for doubtful debts account

Prepare a bad debts account, including a bad debt recovered

Prepare a debtors account

Recalculate the net profit after writing off bad debts and making a new provision for

doubtful debts

Use the journal to correct errors in a trial balance

Use a suspense account to identify differences in trial balance.

Suggested answer

a) i) The new provision for doubtful debts is as follows:

Bad debts written off: 750.43 + 199.00 + 240.00 + 9.62 = 1,199.05

Remaining debtors: 13002.53 – 1199.05 = 11,803.48

Specific provision (£340.67 + 292.12) 632.79

General provision (11,803.48 – 632.79 = 11709.69 x 3%) 335.12

Provision for doubtful debt 967.91

ii)

Bad debts account

Date Details Dr Cr Balance

Dec 31 Zandra Smith 750.43 750.43

D S Cox 199.00 949.43

Softseat Ltd 240.00 1,189.43

P Bond 9.62 1,199.05

Dec 31 Profit and loss 1,199.05 0

Provision for bad debts account

Date Details Dr Cr Balance

Jan 1 Balance (340.00)

Dec 31 Profit and loss 627.91 (967.91)

33

PQP/7B/Jan 2013

Bad Debts Recovered account

Date Details Dr Cr Balance

Mar 31 Quality Furnishings Ltd 84.45 (84.45)

Dec31 Profit and loss 84.45 0

Quality Furnishings Ltd account

Date Details Dr Cr Balance

Mar 31 Bad debts recovered 84.45 84.45

Mar 31 VAT 16.89 101.34

Mar 31 Bank 101.34 0

iii) Gross profit 192,000.00

Expenses:

Given 78,000.00

Increase in provision for doubtful debts 627.91

Bad debts (£1,199.05 - 84.45) 1,114.60

79,742.51

Net profit 112,257.49

b) i) Make appropriate journal entries to rectify these errors

Details Dr Cr

Suspense Account 70.00

Forest Ltd 70.00

Suspense Account 210.00

Drystone Brothers 210.00

Sales Account 70.00

Suspense Account 70.00

Suspense Account 140.00

Clair and Sons 140.00

34

PQP/7B/Jan 2013

ii) Draft the suspense account after the above errors have been corrected showing the original

balance.

Suspense Account

Dr Cr Balance

31 December Forest Ltd 70.00 70.00

Drystone Brothers 210.00 280.00

Sales 70.00 210.00

Clair & Sons 140.00 350.00

Trial balance difference

(missing figure). Also

accept as opening balance

350.00 0

This was not a particularly popular question choice and few candidates who attempted a

response achieved reasonable marks.

Part a) required calculations and more able candidates correctly identified bad and doubtful

debts, although the calculation of the bad debts adjustment resulting in a credit to P&L of £84.45

(net of VAT) was frequently shown including the VAT element. Whilst the more able candidates

correctly prepared the actual accounts, using ‘rolling balance’, few actually showed the fully

correct entries here. The bad debts account frequently showed only the total £1,199.05 without

the individual account details, which are required to complete the double entry. For Quality

Furnishings the debit for bad debt recovered was again show gross (i.e. including VAT) although

candidates did recognise the correct total paid to bank = credit £101.34. These errors affected

the calculation of the amended net profit figure, with few candidates including the £627.91

increase for the current year in the bad debts provision.

Part b) required journal entries and a suspense account, which should have been anticipated as

this is frequently examined. Whilst more able candidates gained max (or near max) marks for

this section, weaker candidates did not recognise that the £35 = x 2 (£70) to correct the posting

error whilst the adjustments for the other entries were frequently reversed. Some candidates

did not calculate the £140 transposition error, attempting to show all the entries to correct Clair

and Sons account, and getting quite confused! The suspense account was affected by the

answers to the first part of this section, and so only the better prepared candidates gained good

marks here.

37

PQP/7B/Jan 2013

8. Jenny Fisher set up a business selling unusual gifts and decorative items from a small

shop three years ago. The following account balances were brought forward on 1

January 2013.

Account Balance

Bank 240.21

VAT 86.00 owed by Customs and Excise

Discount allowed 25.12

Jones Stores 312.15 Dr

Tim Trainer 680.20 Cr

Sales 809.25

During the first two weeks of January 2013, the following transactions occurred:

January 2 Cash takings of £1,380 for the last week in December 2012 were banked.

January 3 A sales invoice for £900.00 excluding VAT was sent to Jones Stores for

goods supplied in December 2012.

January 4 A cheque for £650.00 was sent to Tim Trainer in full settlement of their

account. The balance remaining is to be treated as a discount.

January 4 A credit note for £22.60, excluding VAT, was sent to Jones Stores for goods

billed in error.

January 5 Jones Stores paid £300.00 in full settlement of the balance owing on 1st

January.

January 8 Purchased a computer costing £450.00 including VAT from PC Supplies to

help with the business accounts. Paid an initial deposit of 20%.

January 10 The VAT owed to Jenny at 1 January 2013 was paid by HM Customs &

Excise directly into the business bank account.

TASK

a) Open all the accounts that are necessary to record the above transactions and enter all

balances brought forward on 1 January 2013. (3 marks)

All credit balances must be shown in brackets.

b) Make the necessary entries in the relevant accounts to record the transactions,

including appropriate entries for discounts and VAT. (15 marks)

All credit balances must be shown in brackets.

c) Explain the principal difference between cash and credit sales. (2 marks)

Total 20 marks

38

PQP/7B/Jan 2013

Question aims

To test the candidate’s ability to:

Carry out double entry book-keeping to record sales, purchases and sales returns in

the ledger accounts

Calculate and record VAT

Record receipts and payments

Record discounts allowed and received

Record the purchase of fixed assets.

Explain the difference between cash and credit sales

Suggested answer

a) and b)

Account: Sales

Date Details Dr Cr Balance

Jan 1 Balance b/fwd 809.25 (809.25)

Jan 2 Cash Takings 1,150.00 (1,959.25)

Jan 3 Jones Stores 900.00 (2,859.25)

Account: Bank

Date Details Dr Cr Balance

Jan 1 Balance b/fwd 240.21 240.21

Jan 2 Cash Sales 1,380.00 1,620.21

Jan 4 Tim Trainer 650.00 970.21

Jan 5 Jones Stores 300.00 1,270.21

Jan 8 PC Supplies 90.00 1,180.21

Jan 10 VAT 86.00 1,266.21

Account: VAT

Date Details Dr Cr Balance

Jan 1 Balance b/fwd 86.00 86.00

Jan 2 Cash Sales 230.00 (144.00)

Jan 2 Credit Sales 180.00 (324.00)

Jan 4 Sales returns 4.52 (319.48)

Jan 8 PC Supplies 75.00 (244.48)

Jan 10 Bank 86.00 (330.48)

39

PQP/7B/Jan 2013

Account: Jones Stores

Date Details Dr Cr Balance

Jan 1 Balance b/fwd 312.15 312.15

Jan 2 Sales invoice 1080.00 1,392.15

Jan 4 Credit note 27.12 1,365.03

Jan 5 Bank 300.00 1,065.03

Jan 5 Discount allowed 12.15 1,052.88

Account: Tim Trainer

Date Details Dr Cr Balance

Jan 1 Balance b/fwd 680.20 (680.20)

Jan 4 Bank 650.00 (30.20)

Jan 4 Discount received 30.20 0

Account: Discount allowed

Date Details Dr Cr Balance

Jan 1 Balance b/fwd 25.12 25.12

Jan 4 Jones Stores 12.15 37.27

Account: Sales returns

Date Details Dr Cr Balance

Jan 4 Jones Stores 22.60 22.60

Account: Discount received

Date Details Dr Cr Balance

Jan 4 Tim Trainer 30.20 (30.20)

Account: PC Supplies

Date Details Dr Cr Balance

Jan 8 Computer 450.00 (450.00)

Jan 8 Bank (Deposit) 90.00 (360.00)

Account: Computers

Date Details Dr Cr Balance

Jan 8 PC Supplies 375.00 375.00

c) Cash sales are paid for immediately i.e. the customer will pay Jenny Fisher for goods at

the time of the sale. VAT if applicable will be included in the total amount charged to the

customer. Payment is generally in cash but could be cheque or any other acceptable

method.

Credit sales are where a regular customer (e.g. Jones Stores) has arranged for an account

with the supplier. This will be shown in the sales ledger which summarises the transactions

for a month. At the end of the month Jenny Fisher will send the customer a Statement of

Account, which summarises all the transactions, including VAT at the current rate. A

settlement discount may be allowed if the customer pays within a set period, e.g. within

seven days. The customer could pay by cash, cheque or BACS if arrangements have been

made with the supplier.

40

PQP/7B/Jan 2013

This was a fairly popular choice, and candidates achieved the full range of marks available.

Part a) was designed to test knowledge of the rules of double entry. This was generally well

done and some candidates achieved maximum marks although only the very well prepared

gained the additional mark for presentation. Some candidates did not appear to recognise the

requirement for continuous balance format, using ‘T’ accounts and/or not including any

balance total. Candidates are again reminded that every entry must have a date, narrative

and amount in the correct column, plus a running balance, to get the mark. All credit balances

must be bracketed. A few candidates used “rounding” for the entries, which is not appropriate

in the ledger account, as the totals must be correct, and show the actual balance. Although

the “own figure” rule was applied to give marks for the balance figure, using rounding lost

some candidates valuable marks. There are still a few students who don’t correctly apply the

double entry rules and weaker candidates “reversed” the Debit/Credit entries gaining no marks

and wasting time. The main errors were as follows:

Including £12.15 discount allowed in the Bank account, should be Jones Stores

Showing ‘Net’ figure of £360 for PC Supplies, should be Gross £450; Deposit £90

Ignoring VAT element of £75 on purchase of computer

Ignoring VAT element of £180 on cash sales

Showing cash sales gross = £1,380 (should be net of VAT = £1,150)

Creating a separate account for cash sales, which should be included in ‘sales’.

Showing the opening balance for the VAT account as a credit rather than a debit as was the

case in this question.

Part b) required candidates to explain the difference between cash and credit sales, which the

majority were able to deal with correctly.

---o0o---

Recommended