1

Abhijit Bhattacharya Chief Financial Officer Philips Healthcare

Accelerating Healthcare

2

Forward-looking statements This document and the related oral presentation, including responses to questions following the presentation, contain certain forward-looking statements with respect to the financial condition, results of operations and business of Philips and certain of the plans and objectives of Philips with respect to these items. Examples of forward-looking statements include statements made about our strategy, estimates of sales growth, future EBITA and future developments in our organic business. By their nature, these statements involve risk and uncertainty because they relate to future events and circumstances and there are many factors that could cause actual results and developments to differ materially from those expressed or implied by these statements. These factors include, but are not limited to, domestic and global economic and business conditions, developments within the euro zone, the successful implementation of our strategy and our ability to realize the benefits of this strategy, our ability to develop and market new products, changes in legislation, legal claims, changes in exchange and interest rates, changes in tax rates, pension costs and actuarial assumptions, raw materials and employee costs, our ability to identify and complete successful acquisitions and to integrate those acquisitions into our business, our ability to successfully exit certain businesses or restructure our operations, the rate of technological changes, political, economic and other developments in countries where Philips operates, industry consolidation and competition. As a result, Philips’ actual future results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors that could cause future results to differ from such forward-looking statements, see the Risk management chapter included in our Annual Report 2013.

Third-party market share data Statements regarding market share, including those regarding Philips’ competitive position, contained in this document are based on outside sources such as specialized research institutes, industry and dealer panels in combination with management estimates. Where information is not yet available to Philips, those statements may also be based on estimates and projections prepared by outside sources or management. Rankings are based on sales unless otherwise stated.

Use of non-GAAP Information In presenting and discussing the Philips Group financial position, operating results and cash flows, management uses certain non-GAAP financial measures. These non-GAAP financial measures should not be viewed in isolation as alternatives to the equivalent IFRS measures and should be used in conjunction with the most directly comparable IFRS measures. A reconciliation of such measures to the most directly comparable IFRS measures is contained in our Annual Report 2013. Further information on non-GAAP measures can be found in our Annual Report 2013.

Use of fair-value measurements In presenting the Philips Group’s financial position, fair values are used for the measurement of various items in accordance with the applicable accounting standards. These fair values are based on market prices, where available, and are obtained from sources that are deemed to be reliable. Readers are cautioned that these values are subject to changes over time and are only valid at the balance sheet date. When quoted prices or observable market data are not readily available, fair values are estimated using appropriate valuation models and unobservable inputs. Such fair value estimates require management to make significant assumptions with respect to future developments, which are inherently uncertain and may therefore deviate from actual developments. Critical assumptions used are disclosed in our Annual Report 2013. Independent valuations may have been obtained to support management’s determination of fair values. All amounts in millions of euro’s unless otherwise stated; data included are unaudited. Financial reporting is in accordance with the accounting policies as stated in the Annual Report 2013, unless otherwise stated.

Important information

3

1. Our strategy is aligned to industry mega trends

2. Delivery of Healthcare solutions key to our future

3. Our ‘self help’ is a strong driver of financial performance

4. Key takeaways

Agenda

4

The Philips Business System, our repeatable system to unlock and deliver value

Philips Group Strategy

Manage our portfolio with granular value creation plans and resource allocation

Philips Capabilities, Assets and Positions

Leverage our unique strengths and assets to drive global scale and local relevance across our portfolio

Philips Excellence

Be a learning organization that delivers with speed and excellence to our customers, applying a growth and performance culture

Philips Path-to-Value

Create value to our customers and shareholders in a repeatable manner

5

Mega trends create great opportunities for profitable growth

Sources: World health organization, Agriculture and Agri-food Canada, OECD observer

• Around 65% of deaths globally are due to chronic and non-communicable diseases

• World’s population of people 60 years+ doubled since 1980; forecast to reach 2 billion by 2050

• Growing and aging population with more chronic diseases

• Growing demand for integral value-based healthcare solutions

• Imaging systems for diagnostics and therapy

• Patient care for hospital and home

• Clinical Informatics & consulting services

Mega Trends

Sizeable Opportunities

Our Business Domains

6

Philips Healthcare What we do. Where we are.

Philips Healthcare

€9.6 Billion sales in 2013

36,000+ People employed worldwide in 100 countries

450+ Products & services offered in over 100 countries

8% of sales invested in R&D in 2013

Geographies1

North

America

Other Mature

Geographies

42% 12% 25%

Growth

Geographies2

Western

Europe

21%

1 Based on sales last 12 months March 2014 2 Growth geographies are all geographies excluding USA, Canada, Western Europe, Australia, New Zealand, South Korea, Japan and Israel

Businesses1

36% 14% 23% 27%

Home

Healthcare

Solutions

Customer

Services

Patient Care

& Clinical

Informatics

Imaging

Systems

7

Healthcare constitutes an important part of the Philips Group Last twelve months

1 Excluding Central sector (IG&S) 2 EBITA adjustments based on the following gains/ charges: for Healthcare EUR 63M, Consumer Lifestyle EUR (12)M and Lighting EUR (104)M

Net Operating CapitalSales

100% = EUR 22.4B1 100% = EUR 13.2B1100% = EUR 2.7B1, 2

Adjusted EBITA

Healthcare

ConsumerLifestyle

Lighting

Healthcare

ConsumerLifestyle

Lighting

19%

29%

52%42%

37%

21%

56%

10%

34%

ConsumerLifestyle

Lighting

Healthcare

8

1. Our strategy is aligned to industry mega trends

2. Delivery of Healthcare solutions key to our future

3. Our ‘self help’ is a strong driver of financial performance

4. Key takeaways

Agenda

9

Philips Healthcare Guiding Statement

We are dedicated to creating the future of health care and saving lives. We develop innovative solutions across the continuum of care in partnership with clinicians and our customers to improve patient outcomes, provide better value and expand access to care.

10

Redefining the delivery of care as a solutions partner

• 15-year alliance with sales value of more than $300 million

• Teaming up Healthcare and Lighting to win a major customer

• End2End: Solutions, services, clinical education, consulting, roadmap, operational efficiency

• Philips will provide consulting services to streamline planning, maintenance and education across GRMC sites

• Alliance includes full breadth of our solutions under a single, consistent payment structure

Alliance with Georgia Regents Medical Center for a first-of-its-kind healthcare delivery model in the United States

11

Redefining the delivery of care as a solutions partner

Partnering with the Stockholm County and Karolinska University Hospital to meet future demands of healthcare

• Karolinska will develop new care pathways by integrating patient care, clinical research and education

• Philips will provide access to state-of-the-art imaging systems equipment and services for 14 years for 600-bed new hospital site to be opened in late 2016, at predictable costs

• Managed equipment services include the procurement, system integration and maintenance, including those of other vendors, to ensure optimal delivery of care

• Strong focus on innovation, education and collaboration, including establishment of a research and innovation hub

12

Leadership positions and customer satisfaction rates

Market position

Customer satisfaction

Sleep therapy

Respiratory care

Home monitoring

telecare North America

NPS Lifeline and Home

Oxygen Ventilation

North America

Home Healthcare Solutions

#1

#1

#1

Imaging Systems

Interventional X-Ray cardiovascular

Image-Guided interventions

Ultrasound worldwide

Overall Best in KLAS performance

leader in Imaging

Overall system performance

IMV ServiceTrak NPS

IntelliSpace Portal Advanced

Visualization KLAS Category Leader

CT, MR Ingenia, and Ultrasound iU22

Best in KLAS Product Awards

Frost & Sullivan APAC and India

Medical Imaging Company of the year

#1

#1

Patient Care and Clinical Informatics

Patient monitoring

AEDs1

Digital telemetry

Non-invasive ventilation

Cardiology Imaging

North America

NPS Patient Monitoring -

North America, UK, Germany

and India

#1

#1

#1

#1

#1

#1

#1

#2

#1

#1

#1

Sources: COCIR, NEMA, Market Intelligence Estimate, IMV rated ServiceTrak, Frost and Sullivan, Business group market insights, InMedica Global Patient Monitoring study 2013, MRG Global Ventilator study 2013, MRG Global Healthcare Informatics 2013. 1IDR: #1 for China, France, Germany, UK and US combined

#1

#1

13

1. Our strategy is aligned to industry mega trends

2. Delivery of Healthcare solutions key to our future

3. Our ‘self help’ is a strong driver of financial performance

4. Key takeaways

Agenda

14

Accelerate! drives operational excellence, agility and customer centricity across Healthcare

• Innovation investments in Hospital to Home, Image-Guided Intervention & Therapy, Informatics Solutions & Systems, Value Segment, and Consulting

• Market investments in China, Latin America, India, and ASEAN

Culture

Customer centricity

End2End

Operating model

Resource to win

• Simplified organization, increasing spans of control and removing two layers • Improve sales force productivity with Sales Support Centers, Customer

Relationship Management system, and digital tools

• Culture champions team focused creating a growth and performance culture around customer centricity, innovation, inspiration, and operational excellence

• Healthcare leaders trained in Accelerate Leadership Program

• Three-fold increase in total revenue covered by End2End programs with 40% of revenues to be covered by 2014

• Improve time-to-market of new solutions supported by clinical evidence

• Overhauled our Go-to-Market model in the US focusing on the largest opportunities, with significant investments in supporting infrastructure

• Upgrading our marketing capabilities

15

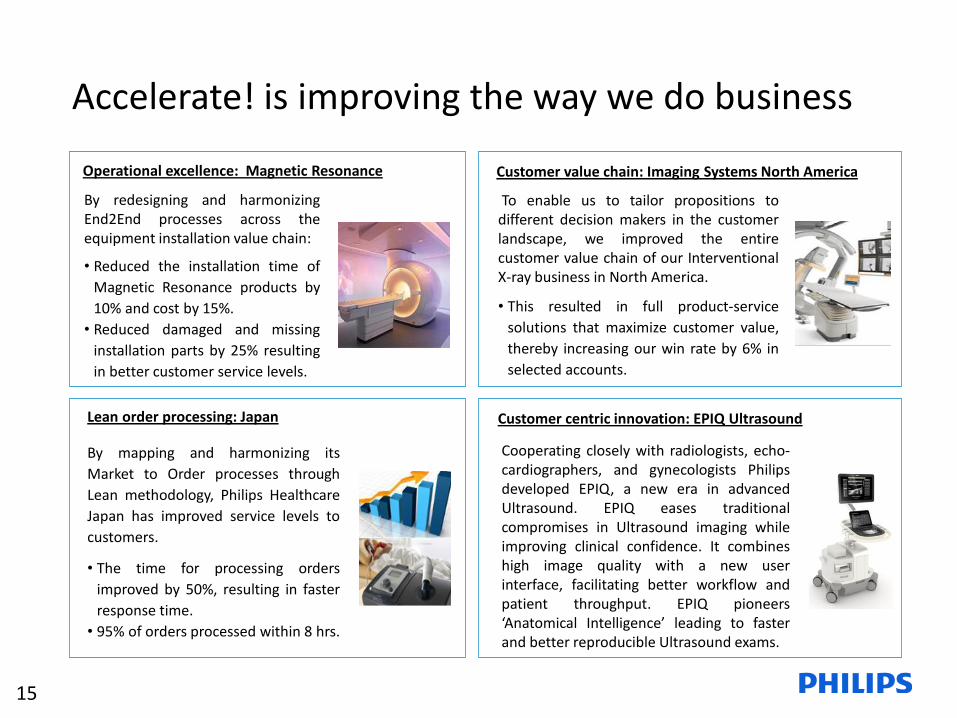

Accelerate! is improving the way we do business

Operational excellence: Magnetic Resonance

By redesigning and harmonizing End2End processes across the equipment installation value chain:

• Reduced the installation time of

Magnetic Resonance products by

10% and cost by 15%.

• Reduced damaged and missing

installation parts by 25% resulting

in better customer service levels.

To enable us to tailor propositions to different decision makers in the customer landscape, we improved the entire customer value chain of our Interventional X-ray business in North America.

• This resulted in full product-service

solutions that maximize customer value,

thereby increasing our win rate by 6% in

selected accounts.

Customer value chain: Imaging Systems North America

Customer centric innovation: EPIQ Ultrasound

Cooperating closely with radiologists, echo-cardiographers, and gynecologists Philips developed EPIQ, a new era in advanced Ultrasound. EPIQ eases traditional compromises in Ultrasound imaging while improving clinical confidence. It combines high image quality with a new user interface, facilitating better workflow and patient throughput. EPIQ pioneers ‘Anatomical Intelligence’ leading to faster and better reproducible Ultrasound exams.

Lean order processing: Japan

By mapping and harmonizing its

Market to Order processes through

Lean methodology, Philips Healthcare

Japan has improved service levels to

customers.

• The time for processing orders

improved by 50%, resulting in faster

response time.

• 95% of orders processed within 8 hrs.

16

Accelerate! is changing Healthcare top to bottom

2013….. Performance

Box

• Strong OIT and sales growth

• Successful market launches

• Investments in R&D and growth geographies

• Industrial footprint in growth geographies

• Strategies to address market headwinds in Southern Europe and Japan

• BMC1 performance management

Val

ue

ROIC

2011 Performance

Box Gro

wth

ROIC

Laying the foundation to improve performance

Transform Philips through Accelerate! • Value delivery from past acquisitions

• Upgraded marketing capabilities

• Sales force productivity

• Created performance and growth culture

• Increase value segment portfolio in Imaging

• Continue to close gap in co-leadership in Imaging

• Consulting services business

Gro

wth

2012 Performance

Box

• Operational excellence through Accelerate!

• Return on investment on growth and innovation investments

• Reduced overhead, cost of complexity

• Leveraged industrial footprint in growth geographies

• Gained share, extended leadership in Patient Care and Clinical Informatics

• International growth and improved patient interface market position in Home Healthcare Solutions

Accelerating performance improvement

Gro

wth

ROIC

1 BMC = Business Market Combination

2011 – 2013 Accelerating performance improvement

• Invested in Industrial footprint in growth geographies

• Reduced overhead and complexity

• BMC1 performance management implemented

• Gained share, extended leadership in Patient Care and Clinical Informatics

• Operating margins & Inventory management improved

• Improved patient interface market position in the Sleep business

• Upgraded marketing capabilities

• Culture change gaining strong traction

• Philips Business System being implemented

17 1 Including restructuring and acquisition-related charges 2 SG&A = Selling, General & Administrative Expense Note – Financials in 2011 and 2012 revised for the adoption of IAS19R

Philips Healthcare has made steady progress since 2011, but there is much more to come

18 1 Philips calculates ROIC % as: EBIAT / NOC; 2011 ROIC has been adjusted to exclude the impairment of goodwill charge taken in 2011

Solid improvement in ROIC Margin expansion and NOC management driving 300bps y-o-y improvement in 2013

19

Transform to become an Excellent company

Expand global leadership positions

Initiate new growth engines

• Healthcare Transformation Services

• Hospital to Home

• Digital health platform

• What else can we provide the 80-year-old woman

living in her home?

• Across the continuum of care

• Ubiquitous monitoring

• Ultrasound everywhere

• Sleep and breathe better

• Expand value solutions

• Image-guided interventional therapy (IGIT)

• Compliance

• Improve quality everywhere with Philips Excellence

• Close the profitability gap to competitors

• Accelerate! & implement the PBS

Next steps on our Path-to-Value

20

1. Our strategy is aligned to industry mega trends

2. Delivery of Healthcare solutions key to our future

3. Our ‘self help’ is a strong driver of financial performance

4. Key takeaways

Agenda

21

Key takeaways

• Health care industry is dynamic, changing, and profitable

• We made good progress on performance improvements in 2013

• Accelerate! continues to unlock significant value, with the 2016 targets as the next step on our path to value, and more to come thereafter

• Our cultural change is making us more customer centric, agile and entrepreneurial, while embedding integrity in everything we do

• While 2014 is a challenging year, we are making good progress towards reaching our 2016 targets

22

Recommended