Embed Size (px)

Citation preview

www.goncm.com/mouwww.goncm.com/mountainntain

user: ncmwbmountain password: user: ncmwbmountain password: skilift8skilift8

FHA BasicsFHA BasicsKay A. Cleland, DE, CRMS, CML, Kay A. Cleland, DE, CRMS, CML,

CAMB Education ChairCAMB Education Chair

Table of ContentsTable of Contents FHA – General InformationFHA – General Information Benefits of FHABenefits of FHA MCAWMCAW Limits/LTV’s/Investment/Max.Loan Amt/MIPLimits/LTV’s/Investment/Max.Loan Amt/MIP Closing CostClosing Cost Loan ApplicationLoan Application IncomeIncome AssetsAssets CreditCredit RatiosRatios PurchasePurchase Rate & Term RefinanceRate & Term Refinance Cash Out RefinanceCash Out Refinance Streamline RefinanceStreamline Refinance Appraisal Appraisal FHA Checklist FHA Checklist

FHAFHA

FHA = Federal Housing Administration is an FHA = Federal Housing Administration is an agency of the Department of Housing and Urban agency of the Department of Housing and Urban Development (HUD)Development (HUD)

1934 Began helping borrowers1934 Began helping borrowers 1983 HUD established DE (Direct Endorsement)1983 HUD established DE (Direct Endorsement) FHA helps borrowers who cannot meet the FHA helps borrowers who cannot meet the

down payment requirements of conventionaldown payment requirements of conventional FHA does not make loans – they insure themFHA does not make loans – they insure them Most FHA loans are pooled into GNMA = Most FHA loans are pooled into GNMA =

Mortgage Backed Securities and then sold in the Mortgage Backed Securities and then sold in the Secondary MarketSecondary Market

http://www.hud.govhttp://www.hud.gov

FHA FHA FHA insures:FHA insures:

Single Family Detached – Full Doc only Single Family Detached – Full Doc only No Non-Owner occupied (except Streamline No Non-Owner occupied (except Streamline

w/out appraisal)w/out appraisal)

Owner Occupied – primary residenceOwner Occupied – primary residence Borrower may not purchase more than 1 SFD Borrower may not purchase more than 1 SFD

Exception: Borrower is relocating & reestablishing Exception: Borrower is relocating & reestablishing Increase in Family SizeIncrease in Family Size Vacating jointly owned property Vacating jointly owned property Nonoccupying Co-borrowerNonoccupying Co-borrower See See

hud.govhud.gov

FHAFHA

HUD has guidelines that the underwriter HUD has guidelines that the underwriter must meet. If they go outside of the must meet. If they go outside of the guidelines it must be completely guidelines it must be completely documented and the loan may not get documented and the loan may not get insured by HUD. If guidelines are insured by HUD. If guidelines are followed HUD will issue a Mortgage followed HUD will issue a Mortgage Insurance Certification.Insurance Certification.

DE Underwriter has a CHUMs # which DE Underwriter has a CHUMs # which identifies them with HUD. They are identifies them with HUD. They are audited.audited.

UNDERWRITINGUNDERWRITING

Automated Underwriting Automated Underwriting Approve (findings w/ credit report)Approve (findings w/ credit report) Refer (denied)Refer (denied)

Manual Underwriting Manual Underwriting When submitting file include the Refer When submitting file include the Refer

findings & Creditfindings & Credit >585 fico >585 fico Nontraditional Credit = No fico and No Nontraditional Credit = No fico and No

Credit Credit

Basic FHA ProgramsBasic FHA Programs

Section Section

203 (b) 203 (b) Basic 1-4 Family Mortgage Basic 1-4 Family Mortgage InsuranceInsurance

203 (k) 203 (k) Rehabilitation Loans Rehabilitation Loans 234234 CondominiumCondominium 251251 Adjustable Rate Mortgages Adjustable Rate Mortgages

CAIVRSCAIVRS

Credit Alert Interactive Voice Response Credit Alert Interactive Voice Response SystemSystem FHA Connection FHA Connection

Delinquent Debt/Foreclosure – GovernmentDelinquent Debt/Foreclosure – Government Must come back with “A” = GoodMust come back with “A” = Good If comes back with “B” = Bad – Cannot do If comes back with “B” = Bad – Cannot do

loanloan CAIVRS # must be written on MCAWCAIVRS # must be written on MCAW

The FHA ConnectionThe FHA Connection https://entp.hud.gov/clashttps://entp.hud.gov/clas Must process using FHA ConnectionMust process using FHA Connection

Request Case numbers Request Case numbers Case Query to check a case numberCase Query to check a case number UFMIP due UFMIP due Inspector AssignmentsInspector Assignments Appraisal InformationAppraisal Information Case CancellationsCase Cancellations CAIVRSCAIVRS

Homeownership Centers Homeownership Centers (HOC)(HOC) DenverDenver

(AR, CO, IA, KS, LA, MO, MN, MT, NE, (AR, CO, IA, KS, LA, MO, MN, MT, NE, NM, ND, OK, SD, TX, WI, WY, UT)NM, ND, OK, SD, TX, WI, WY, UT)

General Questions 1-800-225-5342 or emailGeneral Questions 1-800-225-5342 or [email protected]@custhelp.com or or FHA Resource Center (www.hud.gov)FHA Resource Center (www.hud.gov)

Premium Problems = Mortgage Insurance Premium Problems = Mortgage Insurance Accounting & Servicing Division 703-235-8117Accounting & Servicing Division 703-235-8117

Neighborhood Watch – Check DelinquencyNeighborhood Watch – Check Delinquency

BENEFITS of FHABENEFITS of FHA Lower Down PaymentLower Down Payment Automated Underwriting/ Refers = Manual Automated Underwriting/ Refers = Manual

UnderwriteUnderwrite Cashout Refinance to 95% Cashout Refinance to 95% Rate & Term Refinance – P/O Seasoned 2Rate & Term Refinance – P/O Seasoned 2ndnd

Streamline Refinance (fha to fha) no income or Streamline Refinance (fha to fha) no income or assetsassets

Maximum financing on 2-4 unit propertiesMaximum financing on 2-4 unit properties No Income LimitationsNo Income Limitations Less Cash from BorrowerLess Cash from Borrower No prepayment penalty No prepayment penalty

BENEFITS of FHABENEFITS of FHA

Credit is more lenientCredit is more lenient No Reserve RequirementNo Reserve Requirement Qualifying Ratios 31/43%Qualifying Ratios 31/43% Gifts are permitted for entire down Gifts are permitted for entire down

payment & closing costpayment & closing cost ARMS with caps of 1/5ARMS with caps of 1/5 Upfront MIP may be financed on top Upfront MIP may be financed on top

of Max.Loan Amt.of Max.Loan Amt.

BENEFITS of FHA Cont’dBENEFITS of FHA Cont’d Seller Contributions – Up to 6% Seller Contributions – Up to 6% FHA loans are assumable (must qualify)FHA loans are assumable (must qualify) 401k Loans – Not counted as liabilities401k Loans – Not counted as liabilities Streamlines (Don’t look at income/assets)Streamlines (Don’t look at income/assets) HUD doesn’t require operating income HUD doesn’t require operating income

statements on 3-4 unit propertiesstatements on 3-4 unit properties FHA is not just for 1FHA is not just for 1stst time homebuyers time homebuyers Can use non profit programs-Nehemiah,etc.Can use non profit programs-Nehemiah,etc.

(5013c nonprofit organization – registered)(5013c nonprofit organization – registered)

Mortgage Credit Analysis Mortgage Credit Analysis Worksheet (MCAW)Worksheet (MCAW)

The MCAW = FHA / 1008 = Conventional.The MCAW = FHA / 1008 = Conventional.““The MCAW comes from your processing The MCAW comes from your processing software – as you complete the application software – as you complete the application and GFE it completes the MCAW. (Calyx, and GFE it completes the MCAW. (Calyx, Byte, Encompass, Contour,etc.)Byte, Encompass, Contour,etc.)

Purchase Money Purchase Money 92900-PUR92900-PUR RefinanceRefinance 92900-WS92900-WS

The following information is used to complete a The following information is used to complete a MCAW. Your software will print this form.MCAW. Your software will print this form.

MCAW MCAW Mortgage Credit Analysis Mortgage Credit Analysis

WorksheetWorksheet

MCAWMCAW

MCAWMCAW

FHA County LimitsFHA County Limits The Base loan amount cannot exceed the county The Base loan amount cannot exceed the county

limit (See Chart on www.hud.gov)limit (See Chart on www.hud.gov)Ex. ColoradoEx. ColoradoAdamsAdams 1 family1 family $308,270$308,270ArapahoeArapahoe $308,370$308,370BroomfieldBroomfield $308,370$308,370DouglasDouglas $308,370$308,370El PasoEl Paso $247,000$247,000JeffersonJefferson $308,370$308,370MesaMesa $200,160$200,160

https://entp.hud.gov/idapp/htl/hicostlook.cfm https://entp.hud.gov/idapp/htl/hicostlook.cfm

Loan Amount CalculationLoan Amount Calculation

Appraised value or purchase price Appraised value or purchase price which ever is less divided by the which ever is less divided by the loan amount = LTV.loan amount = LTV.

Appraised Value/Purchase = Appraised Value/Purchase = $100,000 $100,000

95% ltv = $95,000 Loan Amount 95% ltv = $95,000 Loan Amount $5,000 down$5,000 down

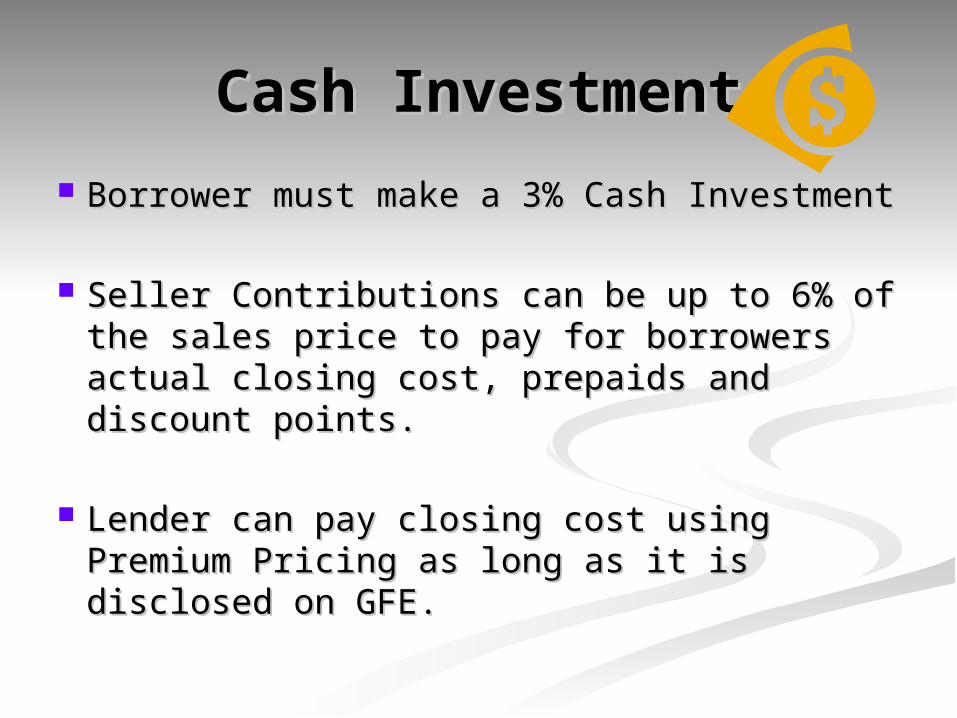

Cash InvestmentCash Investment

Borrower must make a 3% Cash Borrower must make a 3% Cash Investment Investment

Seller Contributions can be up to 6% of the Seller Contributions can be up to 6% of the sales price to pay for borrowers actual sales price to pay for borrowers actual closing cost, prepaids and discount points.closing cost, prepaids and discount points.

Lender can pay closing cost using Premium Lender can pay closing cost using Premium Pricing as long as it is disclosed on GFE.Pricing as long as it is disclosed on GFE.

Mortgage Insurance Mortgage Insurance Premium (MIP)Premium (MIP)

Required on ALL FHA loans regardless of Required on ALL FHA loans regardless of LTVLTV

Insurance is collected by the Lender and Insurance is collected by the Lender and paid to FHA who in turn assist the lenders in paid to FHA who in turn assist the lenders in the event of default.the event of default.

Upfront MIP (not collected on condo’s-234c)Upfront MIP (not collected on condo’s-234c) Multiply the base loan amount by factor (1.50%) Multiply the base loan amount by factor (1.50%) Can be paid in cash at closing by buyer or sellerCan be paid in cash at closing by buyer or seller Financed 100% into the mortgage amountFinanced 100% into the mortgage amount

Mortgage Insurance Mortgage Insurance Premium (MIP)Premium (MIP)

Annual MIPAnnual MIP Multiply the base loan amount by appropriate Multiply the base loan amount by appropriate

factor.factor. Annual MIP is collected in monthly installments.Annual MIP is collected in monthly installments. Loan Amount x factor divided by 12 = monthlyLoan Amount x factor divided by 12 = monthly

.50% mortgage term >15 years.50% mortgage term >15 years

.25% mortgage term of <=15 years & LTV >=90%.25% mortgage term of <=15 years & LTV >=90%

.0% mortgage term of <=15 years & LTV <90%.0% mortgage term of <=15 years & LTV <90%

.0 for all streamline refi’s closed before July 7,1991.0 for all streamline refi’s closed before July 7,1991

Cancellation of Annual MIP Cancellation of Annual MIP 203(b) 203(b) For all mortgages >15 years the annual For all mortgages >15 years the annual

MIP will be MIP will be cancelled when the LTV cancelled when the LTV reaches 78% provided the reaches 78% provided the borrower borrower has paid the annual MIP for at least 5 has paid the annual MIP for at least 5 yrs.yrs.

For mortgages <=15 years, the annual For mortgages <=15 years, the annual MIP will be cancelled when the LTV MIP will be cancelled when the LTV reaches 78%reaches 78%

Mortgage Insurance Mortgage Insurance Premium (MIP)Premium (MIP)

Allowable Closing CostAllowable Closing Cost All cost including Paid Outside of Closing All cost including Paid Outside of Closing

(POC) must be itemized on the HUD I.(POC) must be itemized on the HUD I. Whenever “Actual Costs” are allowed, it Whenever “Actual Costs” are allowed, it

is expected that they do not exceed what is expected that they do not exceed what is reasonable and customary for the area. is reasonable and customary for the area. Must be exact charge. Credit is $16 must Must be exact charge. Credit is $16 must show $16 not $20show $16 not $20

GFEGFE must be accurate & include all must be accurate & include all charges or underwriter will not be able to charges or underwriter will not be able to use which will result in you paying fees. use which will result in you paying fees. (See GFE)(See GFE)

GFEGFEGood Faith EstimateGood Faith Estimate

Complete and Accurate Complete and Accurate Exact Fees Exact Fees

Must be prepared and sent out to Must be prepared and sent out to borrower within 3 days of initial borrower within 3 days of initial applicationapplication

Seller ConcessionsSeller Concessions

Up to 6% of the sales price towards:Up to 6% of the sales price towards: Actual closing costs, prepaids and Actual closing costs, prepaids and

discount pointsdiscount points

From Interested Third Parties:From Interested Third Parties: SellerSeller Builder Builder

Premium PricingPremium Pricing

Brokers/Lenders may pay borrower’s Brokers/Lenders may pay borrower’s allowable closing costs and/or allowable closing costs and/or prepaidsprepaids

Closing Cost that may be Closing Cost that may be chargedcharged

to the Borrower & included to the Borrower & included in acquisitionin acquisition

Appraisal (to appraiser)Appraisal (to appraiser) Attorney fee (3rd party)Attorney fee (3rd party) Credit Report (actual fee-make sure you have the bills to back it up)Credit Report (actual fee-make sure you have the bills to back it up) Deposit VerificationsDeposit Verifications Doc Preparation (3Doc Preparation (3rdrd party) party) Flood CertFlood Cert Inspection Fee (to appraiser)Inspection Fee (to appraiser) Tax StampsTax Stamps Orig. Fee – 1% of base loan amount w/out mipOrig. Fee – 1% of base loan amount w/out mip TermiteTermite R.E. broker feesR.E. broker fees Recording fees Recording fees Repairs (if required by appraiser)Repairs (if required by appraiser) Energy Efficient itemsEnergy Efficient items SurveySurvey Water and Sewer test Water and Sewer test Title examination feeTitle examination fee Title insuranceTitle insurance Home Inspection fee (up to $200)Home Inspection fee (up to $200)

Closing Cost that may be Closing Cost that may be chargedcharged

to the Borrower & not to the Borrower & not included in acquisitionincluded in acquisition

Discount PointsDiscount Points Prepaid itemsPrepaid items Lock in or Commitment feesLock in or Commitment fees Non-realty items or personal Non-realty items or personal

property itemsproperty items

Loan ApplicationLoan Application Source of Funds Source of Funds

Gift, checking/savings, selling itemsGift, checking/savings, selling items Details of Transaction must be complete for the Details of Transaction must be complete for the

underwriter to understand what you wantunderwriter to understand what you want 2 Year Job history – Must match documentation2 Year Job history – Must match documentation

Must include telephone #’s & AddressesMust include telephone #’s & Addresses Liabilities – List allLiabilities – List all Assets – List allAssets – List all Income – Accuracy & VerificationIncome – Accuracy & Verification 2 Year Residency – Must have documentation2 Year Residency – Must have documentation

Loan ApplicationLoan Application All parties must sign and date applicationAll parties must sign and date application

Loan Originator must sign & date w/companyLoan Originator must sign & date w/company Must have all required FHA disclosuresMust have all required FHA disclosures HMDA information must be completedHMDA information must be completed HUD Addendum must be attached to HUD Addendum must be attached to

initial and final Applicationinitial and final Application Addendum verifies on their form that all Addendum verifies on their form that all

information is true and correct information is true and correct Must be signed and dated by all partiesMust be signed and dated by all parties Contains appraisal & occupancy certificationsContains appraisal & occupancy certifications Initial 1003 Addendum the 1Initial 1003 Addendum the 1stst two pages must two pages must

be fully completed and signed. Broker signs be fully completed and signed. Broker signs page 1 / Borrower signs page 2page 1 / Borrower signs page 2

Income – TypesIncome – TypesFull Doc Only (Cannot do Stated)Full Doc Only (Cannot do Stated)

Salary / Hourly Salary / Hourly CommissionsCommissions Self EmployedSelf Employed Overtime / Bonus Overtime / Bonus Social Security / DisabilitySocial Security / Disability Rental IncomeRental Income

Salary / HourlySalary / Hourly

2 Full Year History – Same Line of Work 2 Full Year History – Same Line of Work - 2 Years W-2’s - 2 Years W-2’s - 30 Day Current Paystubs- 30 Day Current Paystubs - Verbal Verification of Employment- Verbal Verification of Employment

INCOME CALCULATIONSINCOME CALCULATIONS Hourly Hourly = Rate x Hours x 52 divided by 12= Rate x Hours x 52 divided by 12 Salaried/Weekly = Rate x 52 divided by 12Salaried/Weekly = Rate x 52 divided by 12 Salaried/Bi-Weekly = Bi-Weekly x 26 divided by 12Salaried/Bi-Weekly = Bi-Weekly x 26 divided by 12 Salaried/Semi Monthly = Semi Monthly x 24 Salaried/Semi Monthly = Semi Monthly x 24

divided by 12divided by 12

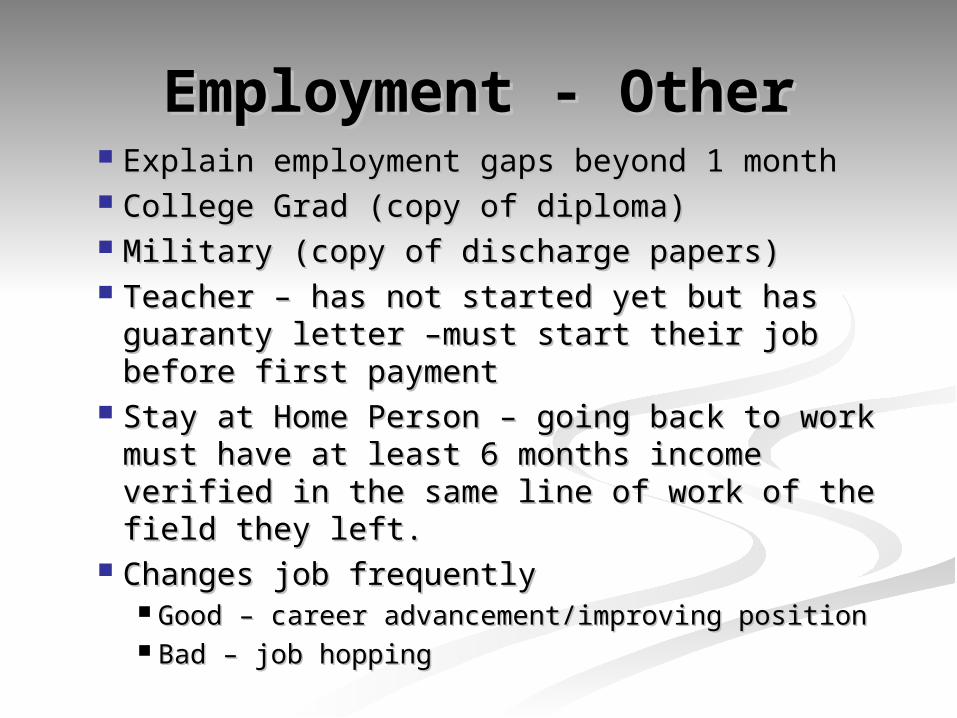

Employment - OtherEmployment - Other Explain employment gaps beyond 1 monthExplain employment gaps beyond 1 month College Grad (copy of diploma)College Grad (copy of diploma) Military (copy of discharge papers)Military (copy of discharge papers) Teacher – has not started yet but has Teacher – has not started yet but has

guaranty letter –must start their job before guaranty letter –must start their job before first paymentfirst payment

Stay at Home Person – going back to work Stay at Home Person – going back to work must have at least 6 months income verified must have at least 6 months income verified in the same line of work of the field they left.in the same line of work of the field they left.

Changes job frequently Changes job frequently Good – career advancement/improving positionGood – career advancement/improving position Bad – job hoppingBad – job hopping

CommissionsCommissions

2 Full Year History – Same Line2 Full Year History – Same Line - 2 Years COMPLETE Tax Returns with - 2 Years COMPLETE Tax Returns with

ALL Schedules ALL Schedules

(Establish earnings trend)(Establish earnings trend)

- Average 24 MonthsAverage 24 Months- Need copies of tax returns to determine Need copies of tax returns to determine

nonreimbursable expenses – DEDUCT from nonreimbursable expenses – DEDUCT from incomeincome

Self EmployedSelf Employed

2 Full Year History – Same Line2 Full Year History – Same Line - 2 Years COMPLETE Tax Returns with - 2 Years COMPLETE Tax Returns with

ALL Schedules ALL Schedules - K1’s = How Much OwnershipK1’s = How Much Ownership

If owns more than 25% than we If owns more than 25% than we need to have fullneed to have full

BusinessTax Returns BusinessTax Returns - Need YTD P & L’s (unaudited)- Need YTD P & L’s (unaudited)

- Average 24 Months- Average 24 Months

Overtime / BonusOvertime / Bonus

2 Year History – Continuance 2 Year History – Continuance Average Past 2 Years Average Past 2 Years

Cannot use bonus as income & Cannot use bonus as income & downpayment downpayment

- Average 24 Months- Average 24 Months

SocialSecurity/SocialSecurity/Disability/RetirementDisability/Retirement

S.S./DisabilityS.S./Disability = Must have Awards Letter = Must have Awards Letter Proof of Receipt – Past 12 monthsProof of Receipt – Past 12 months Must show continuance for as least 3 yearsMust show continuance for as least 3 years

115% Gross Up Amt. x 115%115% Gross Up Amt. x 115% RetirementRetirement = continuance for 3 years = continuance for 3 years

Need Awards Letter or Letter from Need Awards Letter or Letter from former employer or W-2s or Tax Returns or former employer or W-2s or Tax Returns or Copies of Canceled Checks for 12 monthsCopies of Canceled Checks for 12 months

Rental IncomeRental Income

Copies of Tax Returns and/or Leases Copies of Tax Returns and/or Leases Use Net Rental Income Use Net Rental Income If 2 units –owner occ.-want to use 2If 2 units –owner occ.-want to use 2ndnd unit unit

rental income – Can use 91% of total rent rental income – Can use 91% of total rent off 1 yr.lease.off 1 yr.lease.

If Bought after last Tax Return filedIf Bought after last Tax Return filed Use income documented from verification Use income documented from verification

source x 75% minus PITIsource x 75% minus PITI If Owned for One Full YearIf Owned for One Full Year

Can use Tax Return-Schedule E averageCan use Tax Return-Schedule E average

Child Support / AlimonyChild Support / Alimony

If want to use as income If want to use as income Must continue for at least 3 years Must continue for at least 3 years Need copy of divorce decreeNeed copy of divorce decree Proof of ReceiptProof of Receipt

- Cancelled Checks (12 months)- Cancelled Checks (12 months)

- Court Doc’s (if pmt goes through - Court Doc’s (if pmt goes through the courts)the courts)

- Bank Deposits (12 months)- Bank Deposits (12 months)

- Tax Returns- Tax Returns

ASSETS - Sources of ASSETS - Sources of FundsFunds

Deposits on Sales ContractsDeposits on Sales Contracts Copy of Cancelled Check Copy of Cancelled Check Copy of Check & Bank StatementsCopy of Check & Bank Statements

Checking & Savings AccountsChecking & Savings Accounts VOD (Verification of Deposit)VOD (Verification of Deposit) Bank Statements – 2 MonthsBank Statements – 2 Months

Large Deposits – Must ProveLarge Deposits – Must Prove

Cash On Hand (NOT Acceptable)Cash On Hand (NOT Acceptable)

Sources of FundsSources of Funds 401 K’s – Can only count 60% in assets401 K’s – Can only count 60% in assets Stocks – Current Statement (w/in 30 days)Stocks – Current Statement (w/in 30 days) Proceeds from Sale of Home – HUD IProceeds from Sale of Home – HUD I Sale of Personal Property – ProofSale of Personal Property – Proof

Appraisal to show worth / Blue Book ValueAppraisal to show worth / Blue Book Value Bill of SaleBill of Sale

Gifts – Gift Letter Gifts – Gift Letter Must Prove Donorability Must Prove Donorability Verification w/withdrawal from acct. & depositVerification w/withdrawal from acct. & deposit Gifts – Non profit & equity – only need gift Gifts – Non profit & equity – only need gift

letter & HUD Iletter & HUD I

Credit HistoryCredit History

Late or Slow Pays – Last 12 monthsLate or Slow Pays – Last 12 months Bankruptcy – 2 Years Discharged & Bankruptcy – 2 Years Discharged &

No Delinquency since No Delinquency since Foreclosure – 3 Years from time of Foreclosure – 3 Years from time of

foreclosure & must have re-foreclosure & must have re-established credit established credit

Minor credit > 2 years Not an issue Minor credit > 2 years Not an issue but may need explanationbut may need explanation

Judgments, Collections – Must be paid Judgments, Collections – Must be paid off & explainedoff & explained

Credit HistoryCredit History No Established Credit History – Use No Established Credit History – Use

Alternative Credit = Electric Bill, Phone Alternative Credit = Electric Bill, Phone Bill, Insurance Bill, Gas Bill, Cable Bill, Bill, Insurance Bill, Gas Bill, Cable Bill, Water Bill (anything showing 12 month Water Bill (anything showing 12 month payment history) payment history)

Alternative Credit does not replace bad Alternative Credit does not replace bad creditcredit

Recent Debts – Must be explained & use Recent Debts – Must be explained & use of funds may need to be verified.of funds may need to be verified.

Inquiries – Are the borrowers increasing Inquiries – Are the borrowers increasing their credit risk – Need explanationtheir credit risk – Need explanation

QUALIFYING RATIO’SQUALIFYING RATIO’S

Top Ratio Top Ratio Monthly Housing Expense divided by Monthly Housing Expense divided by

Gross Monthly Income = Gross Monthly Income = Housing RatioHousing Ratio Bottom RatioBottom Ratio

Total Monthly Housing Expenses + Total Monthly Housing Expenses + Total Monthly Debt Payments Total Monthly Debt Payments (Liabilities) divided by Gross Monthly (Liabilities) divided by Gross Monthly Income = Income = Total Expense RatioTotal Expense Ratio

31 / 4331 / 43

PURCHASEPURCHASEReal Estate ContractReal Estate Contract

Real Estate Contract must be dated & Real Estate Contract must be dated & contain all parties original signaturescontain all parties original signatures

Contract must permit FHA financing and Contract must permit FHA financing and contain the terms of the financingcontain the terms of the financing

All changes must be initial by all partiesAll changes must be initial by all parties Must contain the address & legal of propertyMust contain the address & legal of property Home Inspection disclosure Home Inspection disclosure must be dated must be dated

prior to orprior to or on contract dateon contract date. Borrower has . Borrower has right to an inspection and can finance up to right to an inspection and can finance up to $200 in their loan. (lender does not need a $200 in their loan. (lender does not need a copy of the inspection)copy of the inspection)

For Your ProtectionFor Your ProtectionGet a Home InspectionGet a Home Inspection

U.S. Department of Housing and Urban Development (HUD)

Federal Housing Administration (FHA)

OMB Approval No: 2502-0538 (exp. 06/30/2006)

For Your Protection: Get a Home Inspection

Name of Buyer (s) _________________________________________________________________________________________________________

Property Address _________________________________________________________________________________________________________

_________________________________________________________________________________________________________

Why a Buyer Needs a Home Inspection

A home inspection gives the buyer more detailed information about the overall condition of the home prior to purchase. In a home inspection, a qualified inspector takes an in-depth, unbiased look at your potential new home to: evaluate the physical condition: structure, construction, and

mechanical systems; identify items that need to be repaired or replaced; and estimate the remaining useful life of the major systems,

equipment, structure, and finishes.

Appraisals are Different from Home Inspections

An appraisal is different from a home inspection. Appraisals are for lenders; home inspections are for buyers. An appraisal is required to:

estimate the market value of a house; make sure that the house meets FHA minimum property

standards/requirements; and make sure that the house is marketable.

FHA Does Not Guarantee the Value or Condition of your Potential New Home If you find problems with your new home after closing, FHA can not give or lend you money for repairs, and FHA can not buy the home back from you.

Radon Gas Testing

The United States Environmental Protection Agency and the Surgeon General of the United States have recommended that all houses should be tested for radon. For more information on radon testing, call the toll-free National Radon Information Line at 1-800-SOS-Radon or 1-800-767-7236. As with a home inspection, if you decide to test for radon, you may do so before signing your contract, or you may do so after signing the contract as long as your contract states the sale of the home depends on your satisfaction with the results of the radon test.

Be an Informed Buyer

It is your responsibility to be an informed buyer. Be sure that what you buy is satisfactory in every respect. You have the right to carefully examine your potential new home with a qualified home inspector. You may arrange to do so before signing your contract, or may do so after signing the contract as long as your contract states that the sale of the home depends on the inspection.

I/we understand the importance of getting an independent home inspection. I/we have considered this before signing a contract with the seller for a home. Furthermore, I/we have carefully read this notice and fully understand that FHA will not perform a home inspection nor guarantee the price or condition of the property.

______ I/We choose to have a home inspection performed.

I/We choose not to have a home inspection performed.

X X

Signature & Date Signature & Date

Purchase ContractPurchase Contract Amendatory Clause (escape clause) – If the Amendatory Clause (escape clause) – If the

appraisal comes in low the borrowers can get appraisal comes in low the borrowers can get their money back and it also states that there their money back and it also states that there are no side agreements.are no side agreements.

Real Estate Certification – All parties certify Real Estate Certification – All parties certify that all terms and conditions are true & no that all terms and conditions are true & no other agreements exist.other agreements exist.

How the contract is set up is how you do the How the contract is set up is how you do the loan. Ex. Seller paying $2000 – should show loan. Ex. Seller paying $2000 – should show Seller is paying prepaids, discount points, Seller is paying prepaids, discount points, closing cost. The last thing you use is closing closing cost. The last thing you use is closing cost because the borrower can finance some cost because the borrower can finance some into the loan.into the loan.

Purchase ContractPurchase Contract

Non-realty items can not be included Non-realty items can not be included in the purchase price – get them off in the purchase price – get them off of the contract. Ex. Pool tables, of the contract. Ex. Pool tables, riding lawn mowers, pool riding lawn mowers, pool equipment, etc. equipment, etc.

MC-11 – Things that we want to get MC-11 – Things that we want to get off of the contract.off of the contract.

If earnest money – Need copy of the If earnest money – Need copy of the cancelled check.cancelled check.

Mortgage Amount Mortgage Amount CalculationCalculation

(This is FHA’s calculation)(This is FHA’s calculation) Low Closing Cost StateLow Closing Cost State

CO,WY,UT,OR,CACO,WY,UT,OR,CA Property Value $50,000 or <Property Value $50,000 or < 98.75%98.75% Property Value $50,000-$125,000 97.65%Property Value $50,000-$125,000 97.65% Property Value >$125,000Property Value >$125,000 97.15%97.15%

High Closing Cost StateHigh Closing Cost State ND,SD,MN,KSND,SD,MN,KS Property Value $50,000 or <Property Value $50,000 or < 98.75%98.75% Property Value >$50,000Property Value >$50,000 97.75%97.75%

Purchase Example – High Purchase Example – High Cost StateCost State11stst Calculation - Statutory Investment Calculation - Statutory Investment

$ $ 100,000100,000 _Sales Price _Sales Price ++1,0001,000 _Borrower Paid Closing Cost_Borrower Paid Closing Cost==101,000101,000 _Total Acquisition _Total Acquisition 3,0003,000 _Required Investment (3%)_Required Investment (3%)$101,000 total acq. - $3,000 = $101,000 total acq. - $3,000 = $98,000$98,000

22ndnd Calculation – Maximum Mortgage Calculation – Maximum Mortgage$100,000$100,000 _Lesser of Sales/Appraised_Lesser of Sales/AppraisedX 97.75 X 97.75 __fha factorfha factor==$97,750$97,750 _Max Mortgage_Max Mortgage

Actual Base Loan Amt. is the lower of Calc 1 or Actual Base Loan Amt. is the lower of Calc 1 or 2 which would be $98,000 vs. $97,750. 2 which would be $98,000 vs. $97,750. Base Loan Amt. is $97,750Base Loan Amt. is $97,750

Purchase Example – High Purchase Example – High Cost StateCost State

Cont’dCont’d$$3,250 3,250 _Actual Down Payment _Actual Down Payment

(Total Acq. Of $101,000 – Max. (Total Acq. Of $101,000 – Max. Mortgage of $97,750 = $3,250)Mortgage of $97,750 = $3,250)

+________ Prepaids & Discount paid by +________ Prepaids & Discount paid by borrowerborrower

=________ Total Down Payment / Funds =________ Total Down Payment / Funds needed to needed to close loan close loan

Purchase Example – High Purchase Example – High Cost StateCost State

$97,750 $97,750 Base Loan Amount Base Loan Amount

X 1.5X 1.5 MIP FactorMIP Factor

=$1,466.25=$1,466.25 MIP MIP

$97,750 (base) + $1,466 (mip) = $97,750 (base) + $1,466 (mip) = $99,216 $99,216 Total Loan Amount Total Loan Amount

Mip is $1,466.25 but cents must be paid in Mip is $1,466.25 but cents must be paid in cash at closing. Cannot be financed.cash at closing. Cannot be financed.

RATE & TERM RefinanceRATE & TERM Refinance

Why do a full blown Rate & Term Why do a full blown Rate & Term Refinance?Refinance?

Present loan is not an FHA Present loan is not an FHA Deleting a borrowerDeleting a borrower Paying off a first & a seasoned second w/ Paying off a first & a seasoned second w/

max ltv of 97%max ltv of 97%

RATE & TERM RefinanceRATE & TERM Refinance“How to Calculate the Loan “How to Calculate the Loan

Amount”Amount”11stst Calculation Calculation $ $ 100,000100,000 _Appraised Value _Appraised Value X 97.75%X 97.75% _fha factor (high cost)_fha factor (high cost)= $97,750= $97,750

22ndnd Calculation Calculation $90,000$90,000 _Existing 1_Existing 1stst lien/Payoff lien/Payoff+$2,000+$2,000 _Seasoned 2_Seasoned 2ndnd Mortgage/Payoff Mortgage/Payoff+$1,000+$1,000 _Closing Cost_Closing Cost+$900+$900 _Discount Points_Discount Points+$1,000+$1,000 _Prepaids (Interest/Hazard/Tax)_Prepaids (Interest/Hazard/Tax)=$94,900=$94,900 TotalTotalActual Base Loan Amt. is the lower of Calc 1 or Actual Base Loan Amt. is the lower of Calc 1 or

2 which would be $97,750 vs. $94,900. 2 which would be $97,750 vs. $94,900. Base Loan Amt. is $94,900Base Loan Amt. is $94,900

Rate & Term RefinanceRate & Term Refinance

$94,900 $94,900 Base Loan Amount Base Loan Amount

X 1.5X 1.5 MIP FactorMIP Factor

=$1,423.50=$1,423.50 MIP MIP

$94,900 (base) + $1,423 (mip) = $94,900 (base) + $1,423 (mip) = $96,323 $96,323 Total Loan Amount Total Loan Amount

Mip is $1,423.50 but cents must be paid in Mip is $1,423.50 but cents must be paid in cash at closing. Cannot be financed.cash at closing. Cannot be financed.

Cash Out RefinanceCash Out Refinance

Appraised Value x 85% = Appraised Value x 85% = Maximum Maximum Base Mortgage Base Mortgage

Payoff + Closing Costs + Discount Payoff + Closing Costs + Discount Points + Prepaids + Total amount of Points + Prepaids + Total amount of any debts to be paid off and/or amount any debts to be paid off and/or amount of funds buyers wishes = Total Amount of funds buyers wishes = Total Amount of Base Loanof Base Loan

Appraisal is required on a Cash Out Appraisal is required on a Cash Out RefinanceRefinance

Cash Out RefinanceCash Out Refinance100,000100,000 Appraised Value Appraised Value

X 85%X 85%

=85,000=85,000 Mortgage Amount Mortgage Amount

$85,000$85,000 Base Loan Amount Base Loan Amount

X 1.5X 1.5 MIP FactorMIP Factor

=$1,275=$1,275 MIPMIP

$85,000 (base) + $1,275 (mip) = $85,000 (base) + $1,275 (mip) = $86,275 $86,275 Total Loan AmountTotal Loan Amount

STREAMLINE Refinance STREAMLINE Refinance Current mortgage must be FHA insuredCurrent mortgage must be FHA insured Mortgage to be refinanced must be current Mortgage to be refinanced must be current If new base loan amount exceeds original If new base loan amount exceeds original

base loan amount, a credit report is required base loan amount, a credit report is required New Loan Amount cannot exceed statutory New Loan Amount cannot exceed statutory

limitslimits Property was acquired w/out credit review a Property was acquired w/out credit review a

6 month seasoning requirement applies 6 month seasoning requirement applies MIP refund worksheet is requiredMIP refund worksheet is required Evidence of social security is required Evidence of social security is required Original case number is needed to order a Original case number is needed to order a

new case numbernew case number

Streamline Refinance Streamline Refinance Cont’dCont’d

No Cash back is allowed – not even $1No Cash back is allowed – not even $1 Income / Assets do not need to be verifiedIncome / Assets do not need to be verified If appraisal – underwriter can require If appraisal – underwriter can require

repairsrepairs Subordination of 2Subordination of 2ndnd liens are allowed liens are allowed Rate must always be reducedRate must always be reduced Term can be reduced, however the P&I Term can be reduced, however the P&I

can only increase up to $50can only increase up to $50 If P&I increases over $50 a full blown If P&I increases over $50 a full blown

refinance is requiredrefinance is required Loan terms are 15, 25 or 30 years Loan terms are 15, 25 or 30 years

Streamline Refinance Streamline Refinance Cont’dCont’d

W/Out an appraisal, the term of the mortgage is W/Out an appraisal, the term of the mortgage is lesser of 30 years or the unexpired term of the lesser of 30 years or the unexpired term of the mortgage plus 12 years. (how many years mortgage plus 12 years. (how many years remaining & add 12 or 30)remaining & add 12 or 30)

Credit qualifying streamlines require verificationsCredit qualifying streamlines require verifications If the refi is an ARM to a fixed rate, the rate on the If the refi is an ARM to a fixed rate, the rate on the

new loan cannot be > than 2% above the current new loan cannot be > than 2% above the current ARM rate.ARM rate.

If the refi is a fixed rate to an ARM, the rate of the If the refi is a fixed rate to an ARM, the rate of the new mortgage is at least 2% below the rate of the new mortgage is at least 2% below the rate of the current mortgagecurrent mortgage

If the refi is an ARM to ARM, an immediate pmt If the refi is an ARM to ARM, an immediate pmt reduction must occur & the max rate on the new reduction must occur & the max rate on the new mortgage can not exceed the rate on the mortgage can not exceed the rate on the oldmortgage being refinanced.oldmortgage being refinanced.

Streamline w/o AppraisalStreamline w/o Appraisal11stst Calculation Calculation$91,500$91,500 _ Original Loan Amt. (Note)_ Original Loan Amt. (Note)

22ndnd Calculation Calculation $90,000$90,000 _Existing 1_Existing 1stst lien/Payoff (can only lien/Payoff (can only

include 1 month’s interest) include 1 month’s interest)+$1,000+$1,000 _Closing Cost_Closing Cost+$900+$900 _Discount Points_Discount Points+$1,000+$1,000 _Prepaids (Interest/Hazard/Tax)_Prepaids (Interest/Hazard/Tax)-$900-$900 _MIP Refund (netting authorization)_MIP Refund (netting authorization)=$92,000=$92,000 TotalTotal

Actual Base Loan Amt. is the lower of Calc 1 or 2 which Actual Base Loan Amt. is the lower of Calc 1 or 2 which would be $91,500 vs. $92,000. Base Loan Amt. is would be $91,500 vs. $92,000. Base Loan Amt. is $91,500$91,500

Streamline w/o AppraisalStreamline w/o Appraisal

$91,500 $91,500 Base Loan Amount Base Loan Amount

X 1.5X 1.5 MIP FactorMIP Factor

=$1,372.50=$1,372.50 MIP MIP

$91,500 (base) + $1,372 (mip) = $91,500 (base) + $1,372 (mip) = $92,872 $92,872 Total Loan Amount Total Loan Amount

MIP is $1,372.50 but cents must be paid in MIP is $1,372.50 but cents must be paid in cash at closing. Cannot be financed.cash at closing. Cannot be financed.

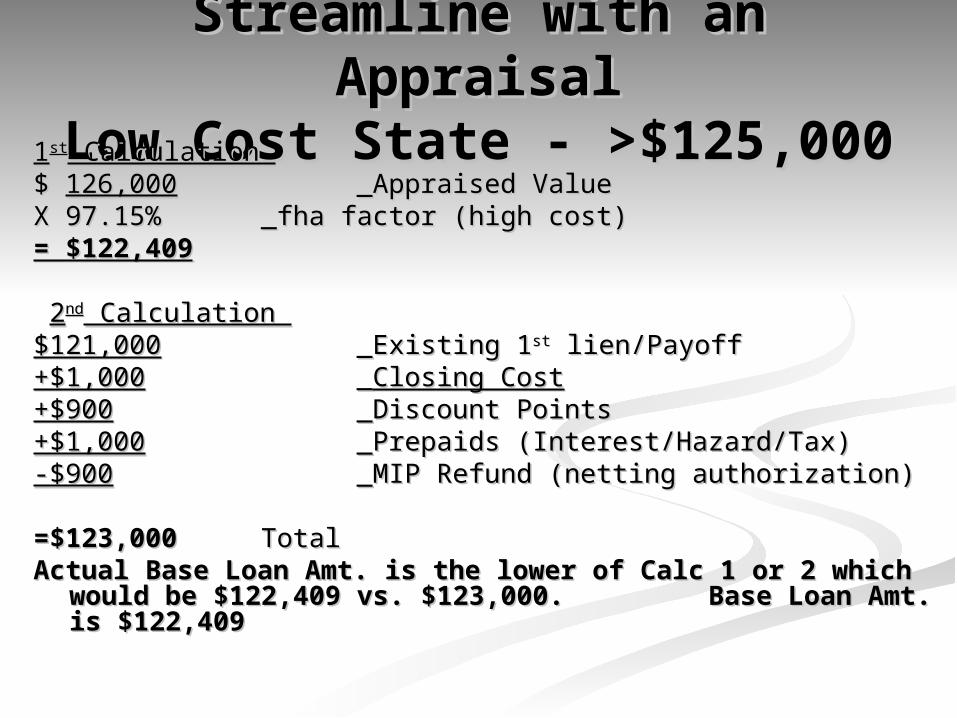

Streamline with an Streamline with an AppraisalAppraisal

Low Cost State - >$125,000Low Cost State - >$125,00011stst Calculation Calculation $ $ 126,000126,000 _Appraised Value _Appraised Value X 97.15%X 97.15% _fha factor (high cost)_fha factor (high cost)= $122,409= $122,409

22ndnd Calculation Calculation $121,000$121,000 _Existing 1_Existing 1stst lien/Payoff lien/Payoff+$1,000+$1,000 __Closing CostClosing Cost+$900+$900 _Discount Points_Discount Points+$1,000+$1,000 _Prepaids (Interest/Hazard/Tax)_Prepaids (Interest/Hazard/Tax)-$900-$900 _MIP Refund (netting authorization)_MIP Refund (netting authorization)

=$123,000=$123,000 TotalTotalActual Base Loan Amt. is the lower of Calc 1 or 2 which Actual Base Loan Amt. is the lower of Calc 1 or 2 which

would be $122,409 vs. $123,000. Base Loan Amt. is would be $122,409 vs. $123,000. Base Loan Amt. is $122,409$122,409

Streamline with an Streamline with an AppraisalAppraisal

$122,409 $122,409 Base Loan Amount Base Loan Amount

X 1.5X 1.5 MIP FactorMIP Factor

=$1,836.13=$1,836.13 MIP MIP

$122,409 (base) + $1,836 (mip) = $122,409 (base) + $1,836 (mip) = $124,245 Total Loan Amount $124,245 Total Loan Amount

Mip is $1,836.13 but cents must be paid in Mip is $1,836.13 but cents must be paid in cash at closing. Cannot be financed.cash at closing. Cannot be financed.

APPRAISALAPPRAISAL-When do you need -When do you need

anan Appraisal on an FHA Loan?Appraisal on an FHA Loan?

Rate & Term RefinanceRate & Term Refinance Cash Out RefinanceCash Out Refinance PurchasePurchase FHA Streamline with appraisalFHA Streamline with appraisal

Including all costIncluding all cost If your new payment is not decreasing by $50If your new payment is not decreasing by $50

Streamline without appraisalStreamline without appraisal New Base mortgage including all cost New Base mortgage including all cost

financed/rolled in cannot exceed the original financed/rolled in cannot exceed the original notenote

APPRAISALAPPRAISAL Used by the Lender to determine the Used by the Lender to determine the

property value property value Must be performed by an FHA approved Must be performed by an FHA approved

appraiser – see appraiser list on hud.govappraiser – see appraiser list on hud.gov VC sheet (Valuation Condition-Notice to VC sheet (Valuation Condition-Notice to

Lender) must be attached and it is the Lender) must be attached and it is the brokers responsibility to clear all conditionsbrokers responsibility to clear all conditions

The Homebuyer Summary must be signed The Homebuyer Summary must be signed by the appraiser and borrowers at least 5 by the appraiser and borrowers at least 5 business days prior to closing.business days prior to closing.

An fha appraisal is good for 6 monthsAn fha appraisal is good for 6 months A case # and appraisal request must be A case # and appraisal request must be

done thru the FHA Connection & then the done thru the FHA Connection & then the broker must fax the request to the broker must fax the request to the appraiser.appraiser.

APPRAISALAPPRAISAL A satisfactory termite inspection is required on A satisfactory termite inspection is required on

all loans except streamline refinancesall loans except streamline refinances If repairs are required it is the brokers If repairs are required it is the brokers

responsibility to make sure complete and responsibility to make sure complete and inspectedinspected

Well and septic inspections are required, if app.Well and septic inspections are required, if app. A property that has been resold within 91 days A property that has been resold within 91 days

is not eligible for FHAis not eligible for FHA A property that has been resold within 91-180 A property that has been resold within 91-180

days must have 2 FHA appraisals to support the days must have 2 FHA appraisals to support the value value

FHA CHECKLISTFHA CHECKLIST

Purchase / Rate & Term Purchase / Rate & Term StreamlineStreamline

Fha StreamlineFha Streamline FHA Streamline Checklist (FHA to FHA)FHA Streamline Checklist (FHA to FHA) No Income / No Asset Required / No Credit Report unless loan amount exceeds original loan amount-just No Income / No Asset Required / No Credit Report unless loan amount exceeds original loan amount-just

need mortgage historyneed mortgage history _____ Loan Application _____92900A _____92900B _____Assumption/Release of Liability _____ Loan Application _____92900A _____92900B _____Assumption/Release of Liability _____Complete, accurate, signed and dated by all parties _____Complete, accurate, signed and dated by all parties _____ Final Loan Application _____Final Good Faith Estimate (Match MCAW)_____ Final Loan Application _____Final Good Faith Estimate (Match MCAW) _____Complete, accurate, signed and dated by all parties_____Complete, accurate, signed and dated by all parties _____ Disclosure Package – All required disclosure within 3 days of application_____ Disclosure Package – All required disclosure within 3 days of application _____T-I-L _____ECOA _____Informed Customer Choice _____ Initial GFE handwritten_____T-I-L _____ECOA _____Informed Customer Choice _____ Initial GFE handwritten _____ Right to Receive an Appraisal _____ Borrowers Authorization _____ Servicing Disclosure_____ Right to Receive an Appraisal _____ Borrowers Authorization _____ Servicing Disclosure _____ Case # with netting authorization and previous case information_____ Case # with netting authorization and previous case information _____ Hawk Alert _____Social Security Validation_____ Hawk Alert _____Social Security Validation _____ Current Payoff = principal + 1 months interest + mip payment_____ Current Payoff = principal + 1 months interest + mip payment _____ Note on current loan _____ HUD I on current loan_____ Note on current loan _____ HUD I on current loan _____ MCAW (Mortgage Credit Analysis Worksheet) _____ Complete and Accurate _____ MCAW (Mortgage Credit Analysis Worksheet) _____ Complete and Accurate _____ Current Mortgage rating – from origination date of mortgage or 12 month minimum _____ Current Mortgage rating – from origination date of mortgage or 12 month minimum _____ Mortgage must be current in the month closed or payment made _____ Mortgage must be current in the month closed or payment made _____ One Repository Credit Report (when new loan amount exceeds old loan amount)_____ One Repository Credit Report (when new loan amount exceeds old loan amount) _____ Appraisal, if required _____ Appraisal logging from HUD Connection _____ Appraisal, if required _____ Appraisal logging from HUD Connection _____ USPS (Validation of zip code under USPS.com)_____ USPS (Validation of zip code under USPS.com) _____ Flood Certification – NCM orders – broker’s responsibility to verify prior to closing_____ Flood Certification – NCM orders – broker’s responsibility to verify prior to closing _____ Lock _____Not expired before disbursement date _____ Loan Amount _____ Rate _____ Term _____ Lock _____Not expired before disbursement date _____ Loan Amount _____ Rate _____ Term _____ Manila file folder _____ Acco fastened down on right side _____ Clearly marked FHA STREAMLINE_____ Manila file folder _____ Acco fastened down on right side _____ Clearly marked FHA STREAMLINE Loan must close in the month of underwriting or must be re-approved thru underwriting.Loan must close in the month of underwriting or must be re-approved thru underwriting. **Required to CLOSE** - Fax all required documentation to the Closing Department at NCM. **Required to CLOSE** - Fax all required documentation to the Closing Department at NCM. _____ Closing Request (complete) Set the Closing 48 hours from Approved to Fund_____ Closing Request (complete) Set the Closing 48 hours from Approved to Fund _____ Homeowners Insurance – correct loan amount / premium / dates_____ Homeowners Insurance – correct loan amount / premium / dates _____ Title Commitment _____ Title Commitment _____ Title company email address _____ Title company email address _____ Final Good Faith Estimate_____ Final Good Faith Estimate www.goncm.com/mountainwww.goncm.com/mountain The information is provided for business and professional uses only and is not to be provided to a consumer or the public. This The information is provided for business and professional uses only and is not to be provided to a consumer or the public. This

information is provided to assist real estate professionals and is not an advertisement to extend consumer credit as defined by information is provided to assist real estate professionals and is not an advertisement to extend consumer credit as defined by Section 226.2 of Regulation Z. Programs, interest rates and fees are subject to change without notice. Section 226.2 of Regulation Z. Programs, interest rates and fees are subject to change without notice.

A Division of National City Bank A Division of National City Bank 11/11/0511/11/05

THE ENDTHE END

THANK YOU FOR YOUR THANK YOU FOR YOUR BUSINESS!BUSINESS!

National City Mortgage National City Mortgage