Embed Size (px)

Citation preview

www.bermudacaptive.bm JUN 2 - 4, 2014

Implementing Modern Portfolio Theory (MPT) by optimizing portfolios along the efficient frontier

Implementing Modern Portfolio Theory (MPT) by optimizing portfolios along the efficient frontier

Session

Moderator:

• Carl Terzer, Founder and Principal, CapVisor Associates, LLC

Panelists:

• Max Kozlov, Chartered Financial Analyst, Director, BlackRock

• Brian Dooley, CFA, Senior Portfolio Manager, Lines Overseas Management

• Stacy Apter, Director, Global Benefits Financing and Asset Management, The Coca-Cola Company

• Panelists– Bryan Dooley, CFA, Senior Portfolio Manager, Lines

Overseas Management– Max Kozlov, CFA, Director, Blackrock– Stacy Apter, Director- Global Benefits Financing and Asset

Management, The Coca Cola Company

• Moderator– Carl Terzer, Principal, CapVisor Associates, LLC

Presenters

• Definitions and Concept introduction

• Optimizing captive portfolios using Modern Portfolio Theory

• Implementation– active vs. passive management– manager selection

• Case Study: Coca Cola

Agenda

Client Portfolio Optimization Efficient Frontier Analysis

• Efficient Frontier line represents the best possible risk/reward portfolio combinations available in the marketplace• Reallocating assets to a portfolio combination that lies on the efficient frontier optimizes performance for any risk/reward combinations, i.e. increasing return at the same risk level (up arrow) or reducing portfolio risk for the same return (left arrow)

100% US Govt.

Int. Gov. Credit

Core Fixed Income

90% Core FI; 10% S&P 500

75% Core FI & 25% S&P 500

“Unoptimized” Client Portfolio

The Importance of Strategic Asset Allocation Optimization

Sources: Ibbotson and Kaplan entitled "Does Asset Allocation Policy Explain 40%, 90% or 100% of Performance?" (2000).

Determinants of long term investment results

Correlation Matrix

Quantitative criterion….Finding Superior RISK-ADJUSTED, AFTER TAX PERFORMANCE

Performance vs. benchmark (rolling YTD, one, three, five year periods)

Modern Portfolio Theory (MPT) statistical evaluation• Alpha –measures managers risk adjusted performance

• Beta- measures manager’s systemic risk

• R-squared - comparison measurement of managers returns to market index

• Standard deviation –measures managers return dispersion or variance

• Tracking error –measures how closely manager tracks index returns

• Sharpe ratio –measures manager’s excess return over risk – free rate of return

• Sortino ratio - Sharpe ratio refinement which differentiates harmful volatility from volatility in general by replacing standard deviation with downside deviation in denominator

• Up-market capture ratio -measures manager’s performance in up markets relative to index

• Down-market capture ratio –opposite of up-market capture ratio• Batting average –measures manager’s ability to meet or beat market consistently• And many more statistical risk-adjusted performance measurements

Universe Comparison Tool

Developing Input Assumptions

•1. Historic data extrapolation: past = future

•2. Ibbotson method, or “build-up” method

•3. Reverse optimization — grapes from wine

•4. Enterprise-wide optimization

•Goal: To create sensible assumptions, and sensible results

MPT - Historic Returns

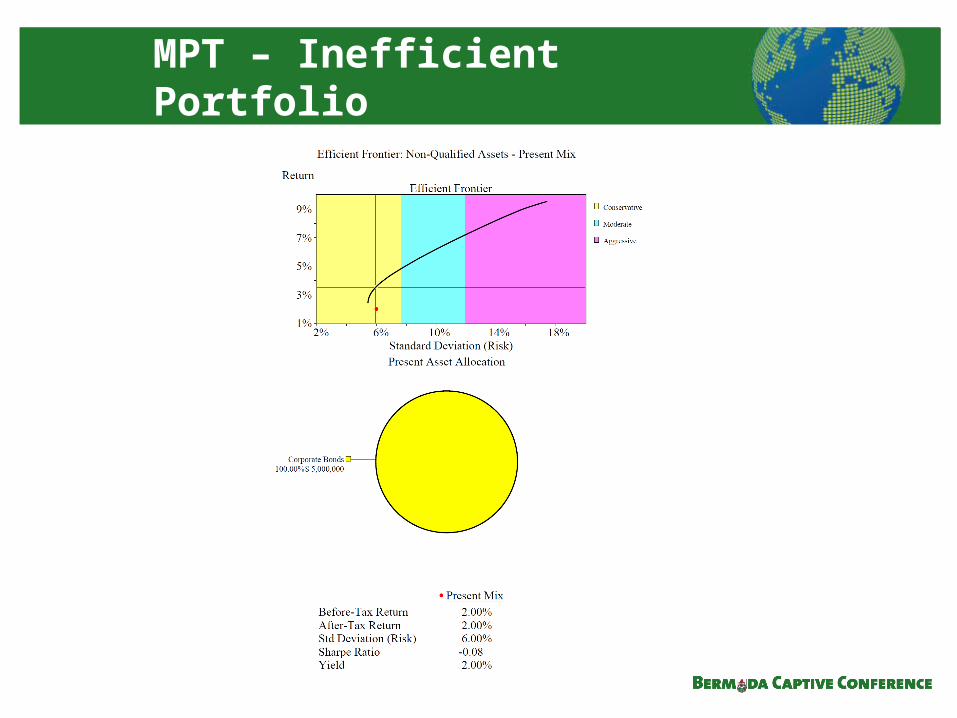

MPT – Inefficient Portfolio

MPT – Optimized Portfolio

MPT – Expected Return Ranges

MPT – Implementation Considerations

• Benchmarking

• Passive versus active strategies

• Frequency of rebalancing

• Strategic versus tactical positioning

• Use of range or targets

• ETF’s and indexing tactics

• Market timing and fund flows

Implementation strategy – presents risk-return tradeoff

Total risk %

Active risk %

Exp

ecte

d a

lph

a %

•When implementing their asset allocation strategy with active managers, investors seek alpha and experience active risk

Exp

ecte

d t

ota

l re

turn

s %

+1

+3

+2

-3

-1

-2

Active/indexed mix and the risk-control “dial”

•Allocations to indexing and enhanced indexing serve to control active risk in the pool

•At moderate plan active risk budgets, enhanced indexing replaces indexing, since it confers alpha and adds little additional risk

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Index 100 71 42 14 0 0 0 0

Enhanced index 0 18 36 54 46 29 13 0

Active 0 11 22 32 54 71 87 100

Active risk budget %

Manager Selection

Evaluating Investment Managers using the 5 P’s

1. Products (Solutions)2. Philosophy3. Process4. People5. Price (Value)

What is an index ETF?

Familiar ground…best of both worlds Two great investment ideas brought together

DiversifiedTradable during the

day

Diversified funds that trade like

stocks

ETFs

StockLike a

Mutual Fund

Like a stock Trading flexibility intraday on the exchange

Long or short

Options frequently available

Like an index fund Constructed to track benchmark indexes

Low expense ratios

Low turnover

What sets ETFs apart? The creation / redemption process enables the

unique benefits of ETFs such as liquid access and tax efficiency

With short sales, an investor faces the potential for unlimited losses as the security's price rises. There can be no assurance that an active trading market for shares of an ETF will develop or be maintained. Transactions in shares of the iShares Funds will result in brokerage commissions and will generate tax consequences. iShares Funds are obliged to distribute portfolio gains to shareholders. Diversification may not protect against market risk or loss of principal.

Benefits of iShares ETFs

ETF units and underlying assets can be lent out to potentially offset holding costs

ETFs offer a cost-effective route to diversified market exposure Ability to estimate in advance the total cost of ownership using ETFs with far

higher degree of certainty than with futures ETFs are not subject to additional operational costs when managing risk,

settlement and reporting that other derivative products require

ETFs are listed on exchanges and can be traded at any time the market is open Pricing is continuous throughout the day

ETFs offer two sources of liquidity1. Traditional liquidity measured by secondary market trading volume 2. The liquidity of the underlying assets via the creation and redemption process

ETFs offer immediate exposure to a basket or group of securities for diversification through a single trade

Broad range of asset classes, including equities, bonds, commodities, investment themes, etc.

Securities lending

Flexibility

Cost- effectiveness

Transparency

Diversification

Liquidity

There can be no assurance that an active trading market for shares of an ETF will develop or be maintained. Diversification may not protect against market risk or loss. Buying and selling shares of iShares Funds will result in brokerage commissions. There is no guarantee that there will be borrower demand for shares of the iShares Funds, or that securities lending will generate any level of income. Distributions paid out of the Fund's net investment income, including income from securities lending, if any, are taxable to investors as ordinary income.

* Pension premium written in 2011 = $659 M.

Coca-Cola Captives at a Glance

Consolidated Group

Corporate Pension Plans

Solvency Capital

Reserves Reinsurance

Contract

Coca-Cola

CCRSLCoca-Cola Reinsurance Services Limited

Dividends

Premium

Annuity Contract

Fronter

Premium less

charges

Capital Contribution

Focusing on Pensions:Nature of the Transaction

Pension Captive Objectives

• Centralized Company control of investment strategies

• Consistent and rigorous Company management of investment risk

• Gain efficiencies on managing larger pools of assets

• Manage surplus risk

• Eliminates duplicative roles by plans; collapsing into one committee

• Positive accounting impact for fully funded plans

Pension Investments - What Do We Hope to Achieve?

• Greater diversification, reducing risk without foregoing returns

• Framework positioned to better access opportunities in the market

• Accomplished by:Move to Global versus U.S./non-U.S.Creating specific allocation to Emerging MarketsDeveloping broader mandates to managers to effectively

invest across different investments based on opportunities and market cycles (eg. diversified credit)

TCCC’s Global Investment Beliefs

Investment Risk Premia

Equity investors demand a higher return to

compensate them for uncertain future earnings

of the business accruing to shareholders

Equity Risk Premium

Investors that lend money to borrowers should

demand a higher return for the uncertainty of

repayment

Credit Risk Premium

Investors should demand a higher return

to compensate them for an illiquid investmentIlliquidity Risk Premium

Skilled investment managers should be able

to outperform the average and generate “alpha”Skill Risk Premium

Investors demand an incremental return for

agreeing to receive payments in nominal

terms (as opposed to inflation-linked)

Inflation Risk Premium

Investors demand an incremental return for

agreeing to delay payment until longer into the

future

Term Risk Premium

We believe that current market conditions

offer an investor an incremental return in

holding select foreign currencies over the

medium term.

Currency Risk Premium

Investors who are providing insurance

to another party should expect to be rewardedInsurance Risk Premium

26

Our portfolio construction framework is based on each asset class providing exposures to certain investment risk premia that offer incremental returns over cash

Broadening exposures to multiple investment risk premia is a way to achieve diversification

All asset classes may have exposure to the skill risk premium based on the level and conviction of the active management provided by the investment manager’s process

All exposures noted are representative, actual exposure to return drivers will depend on the specific guidelines of a given mandate

Return Driver Portfolio Construction Framework

Illustrative Asset Classes Equity Credit Illiquidity Insurance Inflation Term Currency

Public equities (Global, US, etc.)

Diversified credit

EM debt

EM currency

Reinsurance/Vol./Commodities

Hedge Funds

Private equity

Core real estate

Core infrastructure

Global sovereign credit

Global corporate credit

US Equity – Large/Mid

Before After

US Equity – Small

Non-US Equity

Global Equity (large cap)

Emerging Market Equity

Long Duration Bonds

High Yield Bonds

Reinsurance

Bank Loans

Structured Products (ABS/MBS)

Dedicated Emerging Market Debt

Hedge Funds

Private Equity

Real Estate / Infrastructure

What do the changes look like?

Impact of Diversification

Model PortfolioExample before

Change

Year 10 EROA 8.8% 9.7%

Standard Deviation (%p.a.) 10.4% 15.3%

Year 1 VaR95 -9.1% -16.1%

Year 1 CVaR95 -17.0% -29.4%

Portfolio Equity Beta 0.53 0.62

Investment Strategy

Challenges: Open Plans – Organizational

belief in the value of pensions for employees

Need for Growth of Assets Desire for global consistency

in pension portfolio construction

Beliefs: Diversify by Risk

Premia, Not Asset Class Value of Active

Management Willingness to Give Up

Liquidity

Resources: Extremely High

Governance Global Reach Asset Mass Willingness to Be

Different Long Time Horizon

Key Findings Diversified return seeking allocation away from majority equities into alternative risk premia

(reinsurance, diversified credit) and high conviction active managers in addition to less liquid alternatives (real estate, infrastructure, timber)

Focus on management of global governance for all pension trusts gives senior management better feel for goals and objectives as well as ability to maintain global risk consistency (and manager structure) where appropriate.

Important information regarding iShares ETFs

• The iShares Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

• "The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Cohen & Steers Capital Management, Inc., European Public Real Estate Association (“EPRA® ”), FTSE International Limited (“FTSE”), India Index Services & Products Limited, JPMorgan Chase & Co., MSCI Inc., Markit Indices Limited, Morningstar, Inc., The NASDAQ OMX Group, Inc., National Association of Real Estate Investment Trusts (“NAREIT”), New York Stock Exchange, Inc., Russell Investment Group or S&P Dow Jones Indices LLC, nor are they sponsored, endorsed or issued by Barclays Capital Inc. None of these companies make any representation regarding the advisability of investing in the Funds. BlackRock is not affiliated with the companies listed above.

• Neither FTSE nor NAREIT makes any warranty regarding the FTSE NAREIT Real Estate 50 Index, FTSE NAREIT Residential Plus Capped Index, FTSE NAREIT Industrial/Office Capped Index or FTSE NAREIT All Mortgage Capped Index; all rights vest in NAREIT. Neither FTSE nor NAREIT makes any warranty regarding the FTSE EPRA/NAREIT Developed Real Estate ex-US Index, FTSE EPRA/NAREIT Developed Europe Index or FTSE EPRA/NAREIT Developed Asia Index; all rights vest in FTSE, NAREIT and EPRA. All rights in the FTSE Developed Small Cap ex-North America Index vest in FTSE. “FTSE®” is a trademark of London Stock Exchange Group companies and is used by FTSE under license."

• ©2014 BlackRock. All rights reserved. iSHARES and BLACKROCK are registered trademarks of BlackRock. All other marks are the property of their respective owners.

Not FDIC Insured • No Bank Guarantee • May Lose Value

Required disclosures

Important information regarding iShares ETFs• Carefully consider the iShares Funds’ investment objectives, risk factors, and charges and expenses

before investing. This and other information can be found in the Funds’ prospectuses, and, if available, summary prospectuses, which may be obtained by calling 1-800-iShares (1-800-474-2737) or by visiting www.iShares.com. Read the prospectus carefully before investing.

• Investing involves risk, including possible loss of principal.

• Bonds and bond funds will decrease in value as interest rates rise and are subject to credit risk, which refers to the possibility that the debt issuers may not be able to make principal and interest payments or may have their debt downgraded by ratings agencies. High yield securities may be more volatile, be subject to greater levels of credit or default risk, and may be less liquid and more difficult to sell at an advantageous time or price to value than higher-rated securities of similar maturity. An investment in the Fund(s) is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Securities with floating or variable interest rates may decline in value if their coupon rates do not keep pace with comparable market interest rates.

• When comparing stocks or bonds and iShares Funds, it should be remembered that management fees associated with fund investments, like iShares Funds, are not borne by investors in individual stocks or bonds. The annual management fees of iShares Funds may be substantially less than those of most mutual funds. Buying and selling shares of iShares Funds will result in brokerage commissions, but the savings from lower annual fees can help offset these costs.

• In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Securities focusing on a single country, narrowly focused investments (including REIT, preferred stock, factor and floating rate note funds), and investments in smaller companies may be subject to higher volatility. The iShares Minimum Volatility ETFs may experience more than minimum volatility as there is no guarantee that the underlying index's strategy of seeking to lower volatility will be successful.

![3 KEPIC의 현황과 적용 [호환 모드]20KEPIC%C... · mpt 2 asme ptc 2용어정의와상수 mpt 4.2asme ptc 4.2 미분기 mpt 4.3asme ptc 4.3 공기예열기 mpt 12.3asme ptc](https://img.dokumen.tips/doc/110x75/5aac75367f8b9a693f8d1890/3-kepic-20kepiccmpt-2-asme-ptc-2.jpg)