Embed Size (px)

Citation preview

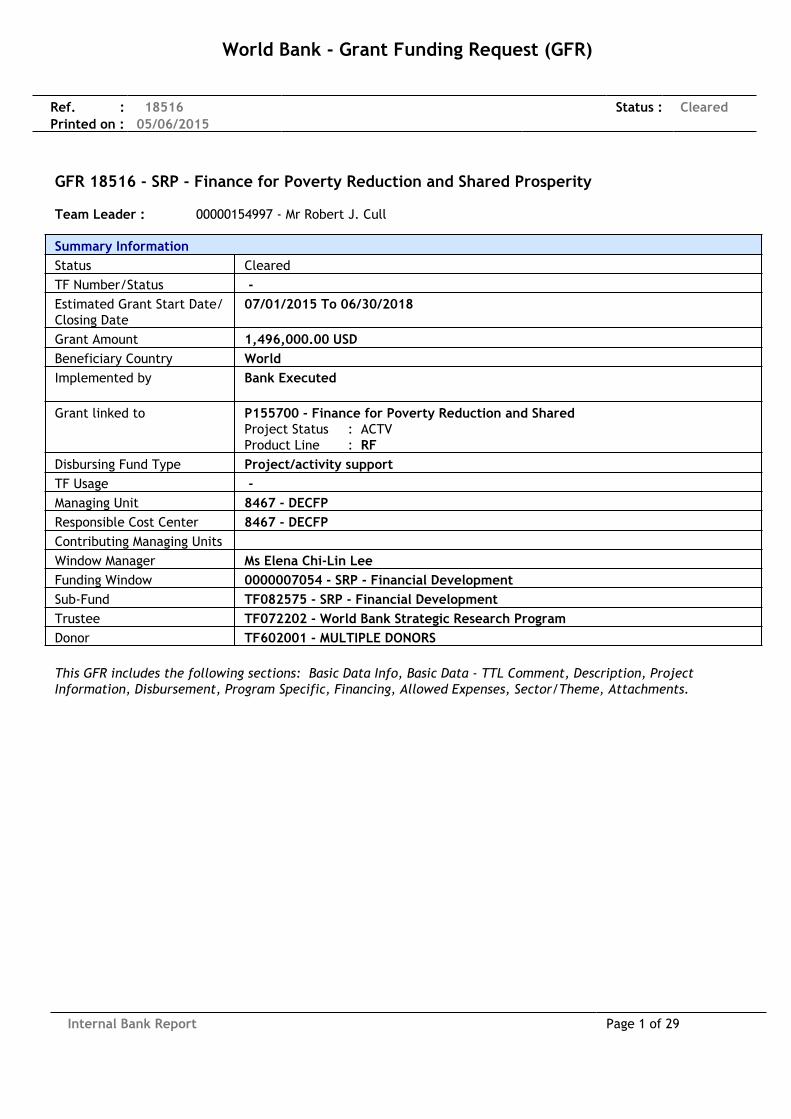

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

GFR 18516 - SRP - Finance for Poverty Reduction and Shared Prosperity

Team Leader : 00000154997 - Mr Robert J. Cull

Summary InformationStatus ClearedTF Number/Status - Estimated Grant Start Date/Closing Date

07/01/2015 To 06/30/2018

Grant Amount 1,496,000.00 USD Beneficiary Country WorldImplemented by Bank Executed

Grant linked to P155700 - Finance for Poverty Reduction and SharedProject Status : ACTVProduct Line : RF

Disbursing Fund Type Project/activity supportTF Usage - Managing Unit 8467 - DECFPResponsible Cost Center 8467 - DECFPContributing Managing UnitsWindow Manager Ms Elena Chi-Lin LeeFunding Window 0000007054 - SRP - Financial DevelopmentSub-Fund TF082575 - SRP - Financial DevelopmentTrustee TF072202 - World Bank Strategic Research ProgramDonor TF602001 - MULTIPLE DONORS

This GFR includes the following sections: Basic Data Info, Basic Data - TTL Comment, Description, ProjectInformation, Disbursement, Program Specific, Financing, Allowed Expenses, Sector/Theme, Attachments.

Internal Bank Report Page 1 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

Comments/Requests by TTL

DESCRIPTION

1. What is the Development Objective (or main objective) of this Grant?

The objective of this grant proposal is to generate new knowledge on how financial development and financialinclusion impact economic growth and income inequality. Through both channels, finance can potentially have aneffect on reducing poverty and boosting shared prosperity, the twin goals that the World Bank Group has set out foritself. In particular, the research from this program will provide new micro-level evidence on (1) the linkagesbetween finance and growth, (2) the contribution of finance to risk and volatility both on the domestic andinternational front, which can have implications for economic growth and for the income and welfare of the poor, (3)the links between financial development and inclusion with income inequality, and (4) the nature of financialproducts better tailored to the needs of the poor which can impact shared prosperity.

2. Summary description of Grant financed activities

The proposed program has two main components: (A) research related to the role of finance in spurring growth #including its role in mitigating or amplifying income shocks and crises # and thereby reducing poverty, and (B)research on how financial inclusion can contribute to reducing inequality and improving shared prosperity, and howthe poor use financial services.

Conceptually, the themes under the two research components are deeply interlinked, as finance may actsimultaneously on two or more of the dimensions of interest. For example, in addition to their adverse growthimpact, crises often have major distributional effects detrimental to the poor. Hence, if finance helps avert crises, itmay promote not only growth but also equity. The same happens if finance helps promote growth intensive inunskilled employment, or if enhanced financial inclusion helps entrepreneurship and thereby growth.

A. The proposed work on the links between finance and income growth will address two broad sets of questions:

(A.1) What is the micro-evidence on the linkages between finance and growth? There has been extensive research, atthe Bank and outside, on the finance-growth nexus, employing an aggregate empirical perspective. In comparison,the microeconomic evidence, especially from poor countries, has been much less studied. In addition, the emphasisfrom the aggregate perspective has been on the growth effects of broad measures of financial development, whereasthe use of financial services at the firm level is the focus here. In particular, this part of the proposed program willuse microeconomic data to assess a number of key questions: How does access to finance affect firm sales,employment, investment and productivity? Does the nature of financing (short versus long term, domestic versusforeign currency) matter? Does usage of financial services disproportionately benefit the most productive firms? Doesit lead to an increase in the productivity of incumbents, to entry of higher-productivity firms, and/or to exit oflow-productivity ones? Is the answer different for large firms and SMEs? What are the effects of FDI on theperformance of both source and destination firms and sectors? Finally, how does firm performance respond tochanges in the institutional framework shaping the supply of finance?

(A.2) Volatility and financial crises represent major obstacles to sustained growth and poverty reduction, as shown bythe experience of many countries over the last quarter century. Moreover, aside from their growth effects, volatilityand risk are themselves detrimental to welfare, especially for the poor, who have limited opportunities to hedgeconsumption risk. In this regard, financial development and financial policies can play a dual role # if properlymanaged, they help diversify risk and cushion adverse shocks; if not, they can contribute to the propagation ofturbulence and make the financial system itself a source of instability and crises. The proposed research will assess

Internal Bank Report Page 2 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

this dual role of finance. It will examine the contribution of finance to risk and volatility, both on the domestic andthe international front. On the domestic side, the program will examine issues such as: How is bank risk priced? Whatis the role of debt maturity structure in mitigating and managing bank risk? To what extent do private borrowingdecisions internalize their contribution to aggregate risk? On the international side, the research will likewiseexamine the role of financial integration for the management of risk. Financial integration opens new possibilities forinternational risk diversification, but it also facilitates the international propagation of financial turbulence. In thisarea, the research will examine how increasing financial openness has changed the risks faced by low-incomecountries, their success in exploiting new opportunities for diversification of income and consumption risk, and therole of global institutional investors in the propagation of shocks.

B. On the finance-inequality channel, the proposed research will likewise address two broad sets of issues:

(B.1) Similar to the research on the finance-growth nexus, a number of studies have documented the links betweenfinancial development, poverty levels, and income equality from an aggregate perspective. In contrast, the proposedresearch will employ micro-data to document the links between the use of financial services and income distribution,both globally and for low income countries, specifically. The questions to be addressed include: What is the role offinancial development and inclusion in shaping the dynamics of income inequality along the path to development?Related to this, what is the empirical relationship between financial inclusion, as measured at the individual or firmlevel, and overall income inequality? Does financial inclusion contribute to shared prosperity?

(B.2) Natural questions arise as to the nature of financial services available to the poor, and whether existingfinancial products need to be better tailored to satisfy their needs and promote poverty reduction and boost sharedprosperity. Micro-level studies will therefore describe the financial products that the poor and excluded (like femalesand SMEs) use, and how they benefit from the use of those products. The studies will address questions about specificfinancial products and pertinent regulations affecting their use, such as: How do households use informal finance?How does resort to formal and informal finance evolve over the business cycle? What are the consequences forhouseholds of using informal finance? How do financial regulations (in particular related to consumer protection)enhance (or impede) the supply of financial products matching the needs of the poor? What is the quality ofinformation provided by financial institutions to low-income customers when choosing among credit and savingsproducts? Do financial institutions offer the poor the products best suited to meet their needs, in particular as itrelates to cost and intended usage? A group of studies will, in fact, vary the terms of the financial productsthemselves to assess their suitability to the needs of the poor in terms of the structure of microcredit contracts.Finally, the proposal also includes the collection and analysis of data on the poor#s use of financial products viafinancial capability and consumer protection surveys in Haiti and Rwanda.

3. (Optional question) What can/has been done to find an alternative source of financing, i.e. instead of a Bankadministered Grant?

The researchers are using Bank budget to pay for their time but unfortunately there are very limited alternativesources of funding that can be used to pay to hire research assistants, conduct field experiments or surveys, and buydata. Hence, support from SRP would be crucial to the success of the proposed research activities.

4. What are the main risks related to the Grant financed activity ? Are there any potential conflicts of interest forthe Bank? How will these risks/conflicts be monitored and managed?

This is a research program proposal and, consequently, it is susceptible to the risks inherent to any research activity:i) datasets that researchers plan to work with may turn out to be unavailable, or of insufficient quality; ii) researchlinked to World Bank operations gets delayed when the projects themselves experience delays or changes; and iii)new ideas or research emerge suggesting that the planned approaches need to be changed. We can confidentlymanage and mitigate these risks in several key ways. The most important is to take a portfolio approach to research,

Internal Bank Report Page 3 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

whereby we allow for some projects to drop out and others to get added along the way as events transpire, whilemaintaining the emphasis on the core themes proposed. Second, we have a mix of projects at different stages, fromthose at the inception stage to those looking for funding to reach completion. Third, close involvement withoperations will help mitigate the risks of project delays, while identifying a range of potential datasets will helpmitigate the risks of any one dataset not being accessible or of high enough quality.

There are relatively few conflicts of interest in this work. Some of the research will investigate the impacts ofpolicies which the World Bank has advised or supported governments to implement. However, researchers retainindependence to report on the results, whatever they might be, and so we do not believe this is a constraint on thework.

SRP

1. How does (do) the objective(s) of this proposal align with the World Bank Group#s twin goals? What are the keythematic research questions (from the 2015 Call for Proposals) being addressed in this research?

As noted above, the research program has been explicitly designed to address how finance affects the achievementof the WBG#s twin goals (reduced poverty and boosting shared prosperity) in developing countries. To this end, theproposed work focuses on the impact of finance on the various factors contributing to those goals: income growth,increased stability of income and consumption, and reduced income inequality and enhanced inclusion of the poor.

2. Provide a literature review & explain study#s intellectual merit. For Program proposal (PP), provide detailedrationale for the selection of issues within an overarching topic and how it helps to address critical problemsfacing Bank clients/operations.

The relevant literature and the value added of particular components of the research will be discussed in Section 3below. We focus this section on detailing the rationale for the selection of issues to be covered within this programproposal and how it helps address critical problems facing Bank clients and operations.

Each individual project in this proposal is aligned with the core theme of this proposal: to examine the role of financein reducing poverty and boosting shared prosperity, the twin goals that the World Bank Group is pursuing. We believethat there is added value to be had through combining these together as a program proposal. Viewing this work as aprogram enables a more holistic view to be taken of the core questions of interest, with different projects helping toanswer complementary questions related to the core underlying themes. Moreover, it offers the opportunity tobenefit from synergies in learning across the projects. Projects in one country can learn from experiences in another,with the staggered timing of the different projects allowing lessons to be incorporated along the way, rather thanbeing drawn only ex post.

As is to be expected, we have to be selective in the coverage of countries and even in the specific topics we proposeto focus on within the large themes we are trying to cover. While priority is given to research activities focusing onlow-income countries, data considerations play a large role in how specific topics and countries were selected. Also,the particular questions being addressed within the broad themes are ones that researchers have an interest inworking on, in countries that the call is focused on, and that staff in operations have an interest in collaborating on.We have chosen not to include work on a couple of sub-questions within the call that were not of interest toresearchers and staff within the World Bank.

3. Describe analytic design & methodology. Individual Proposal: elaborate on hypotheses, conceptual framework,data; PP: describe broad research design, components, and how they#re linked & coherently contribute to theoverall objective.

As noted above, our broad research program has two main components (A) research related to the role of finance inspurring growth # including its role in mitigating or amplifying income shocks and crises # and thereby reducing

Internal Bank Report Page 4 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

poverty, and (B) research on how financial inclusion can contribute to reducing inequality and improving sharedprosperity, and how the poor use financial services. Below we provide a detailed account of the proposedsubcomponents within (A) and (B). We describe in each case the relevant literature and the value added by eachproject. We also describe the methodology and data to be used and provide information on the projected outputs andthe dissemination strategy.

A. FINANCE AND GROWTH

I. Micro evidence on the linkages between finance and growth (firm level studies)

I.1 Financial Frictions, Entry Barriers, and the Size Distribution of Firms

The project seeks to investigate the properties of the size distribution of firms in low income countries in order toshed light on plausible types of distortions that are dragging productivity growth and misallocating resources in theseeconomies. Is it the case that obstacles to firm creation and high-growth entrepreneurship are the main drivers of thelack of productivity growth in these economies? Or is it that distortions to post-entry size, such as those generated byfinancial frictions, are the biggest constraint? These questions relate intimately with the World Bank#s twin goals, byidentifying promising avenues for reform and policy improvements that could unleash private sector development,create jobs, and reduce poverty.

Two bodies of literature exist investigating, independently, the effects of barriers to firm entry and the effects ofallocative distortions. Regarding the former, the work of Barseghyan and Di Ceccio (2011), develops a theory withendogenous entry and operations decisions of firms, and show that reducing entry barriers from the highest decile inthe entry cost distribution (measured by the World Bank's Doing Business Database) to the level in the lowest decilewould generate a 75% increase in TFP and GDP per worker. Similar findings where obtained by Moscoso Boedo andMukoyama (2012), with a methodology that also takes into account the effects of entry barriers on the size of theinformal sector. The literature investigating the macroeconomic effects of allocative distortions is more dense, butthe spirit of it is well summarized in Hsieh and Klenow (2009). The authors develop a methodology to identify suchdistortions from firm-level data, and find that, in China and India, the withdrawal of such distortions and there-allocation of resources as in the US could yield TFP gains of up to 60 %. This proposal seeks to develop aframework to think jointly about the two type of distortions, and to devise a strategy that appeals to firm level datato identify the most binding type of constraint.

The approach is to build upon widely used theories of firm size, entry, and exit, incorporating two type of distortions:1) taxes to the entry of new firms, and 2) taxes to the firm size, that operate through the cost of capital or the costof labor. From a macroeconomic point of view, both types of distortions will reduce GDP. However, they#ll carry verydifferent implications for the firm size distribution. We shall exploit these differences to then go to firm-level dataand try to identify the nature of the most binding distortion affecting the economy in question. Preliminary resultsshow, for example, that entry barriers seem to be the most prevalent in Kenya, where a typical manufacturing plantsize is about 60 employees, while financial frictions seem to be more disruptive in Ghana, where average firm size isless than 10 workers. More broadly, the team has currently gained access to firm censuses from the followingcountries: Kenya, Ghana, Ethiopia, Cameroon, Peru, China, and India. The country coverage allows us to put theperformance of low income countries in context with relatively more developed economies. The team expects toexpand the number of countries under study throughout the duration of the project.

The main output of this project will be a paper detailing the results of the research. The aim is to publish the work ina top journal in the finance field. The findings of this research will be disseminated via presentations at academicinstitutions, as well as international organizations.

I.2. Access to Finance and Firm Employment

An extensive literature exists exploring the impact of finance on economic growth both at the macro and micro (firm)

Internal Bank Report Page 5 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

level. In contrast, fewer studies have examined the impact of finance on jobs. The majority of papers on the subjecthave focused on data from individual developed countries: the US (Benmeleck, Bergman and Seru, 2011;Duygan-Bump et al., 2011; Greenstone and Mas, 2012; Chowdorow-Reich, 2013) and France (Bertrand et al., 2007).There are few papers that have relied on cross-country data, either at the firm level (Aterido et al, 2011; Cull andXu, 2011) or at the industry level (Pagano and Pica, 2012). But, with the exception of Aterido et al. 2011, the existingpapers have looked at the impact of the aggregate level of financial development as opposed to analyzing morespecifically how measures of access to finance affect employment. This distinction is important because access tofinance is not the same as financial development. Financial systems can be considered developed because the volumeof credit to GDP is high but access to finance might still be low if credit is allocated only among few firms.

The objective of this research is to use firm level data to analyze how access to finance affects firms# employmentand, in particular, investigate whether there is a differential impact for MSMEs, which tend to be more commonlycredit constrained. We plan to use two firm level datasets to analyze the link between finance and employment.First, we will use data from ORBIS, a commercial database distributed by Bureau van Dijk. We will focus on thosefirms that report data on employment. Furthermore, we will restrict our analysis to developing countries whichreport data on 5 or more firms. Overall, the data we use from ORBIS includes information for close to 2 million firmsoperating across 46 developing countries. The data covers the period 2005-2011. One advantage of using ORBIS is thatit includes large and small, listed and unlisted firms. Also, these data allow us to identify the amount of financing(short and long-term) received by firms. Second, we will use World Bank Enterprise Survey (ES) data to analyze howfirms# access to finance affects firm level employment growth. This dataset contains information on 52,329 firmsoperating in 70 countries. We will restrict our analysis to countries with two or more surveys over the course of theperiod 2002-2014, so that we can control for country fixed effects.

To identify a causal link from finance to employment growth we will adopt two main strategies. First, we will use adifference-in-difference approach where we will compare the impact of finance on employment growth acrossindustries that are more versus less dependent on external sources of finance. This follows the strategy proposed byRajan and Zingales (1998). However, while they have used this strategy to assess how country level financial depthaffects industry output growth, in this case we use it to study how firm access to finance affects firm employmentgrowth. Second, instead of directly analyzing the impact of finance on employment, we will examine what happensto employment for firms in countries that undertake financial infrastructure reforms that are intended to increasethe supply of credit such as the introduction of credit bureaus or collateral registries relative to firms that are incountries that do not introduce such reforms. In particular, we plan to analyze the impact of the introduction ofcredit bureaus in Armenia (2007), Bolivia (2004), Bosnia-Herzegovina (2001), Bulgaria (2005), Croatia (2007), CzechRepublic (2002), Ecuador (2005), Georgia (2005), Honduras (2002), Kazakhstan (2006), Kenya (2008), Kyrgyzstan(2003), Macedonia (2011), Moldova (2011), Nicaragua (2005), Poland (2001), Romania (2004), Russia (2006), Rwanda(2010), Serbia (2004), Slovakia (2004), Slovenia (2008), Uganda (2009), Ukraine (2007), Uzbekistan (2005) andcollateral registries in Albania (2001), Bosnia-Herzegovina (2005), Croatia (2007), Georgia (2010), Guatemala (2009),Kyrgyzstan (2002), Moldova (2003), Peru (2006), Romania (2000), Rwanda (2009), Serbia (2006), Slovakia (2003),Tajikistan(2004), Ukraine (2005) and Vietnam (2004).

Given the work of Love, Martinez Peria and Singh (2014) and Martinez Peria and Singh (2014) that shows thatcollateral registries and credit bureaus improve firms# access to finance, we seek to use these financial access eventsthat we can assume are independent of firm employment and demand for finance to investigate the impact offinance on employment.

We expect to produce a paper that will be submitted to the working paper series and to an academic journal. We alsoplan to disseminate this work via blogs and via presentations at academic and policy conferences.

I.3. Access to Finance and Gazelles

Entrepreneurship and job creation remain one of the most hotly debated issues in understanding countries# growthpatterns. In very early work, Birch (1994) suggested that most jobs are created by #gazelles#, fast-growing firms thatare not necessarily young or small. But trying to identify ex-ante which firms grow to be gazelles remains elusive.

Internal Bank Report Page 6 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

The objective of this project is to focus on the early life-cycle of firms and identify firms that may be classified asgazelles and see if we can predict which firms are likely to be gazelles based on their initial conditions. To answerthis question, we proceed in three steps. First we use India census data from the Annual Survey of Industries (ASI)consisting of a panel of firms from 2001-2010. We restrict the sample to firms born during this period and identifywhich of these young firms experience periods of high growth. We then focus on the starting conditions of these firms# their size, location, industry, and capital structure # to see if we can predict which young firms are gazelles.

Second, we use data on public and private limited companies in India from the Prowess database over the period1994-2010. While these firms tend to be larger than the firms in the ASI dataset, the advantage of the Prowessdatabase is that we have access to a more comprehensive set of firm characteristics including ownership structure,details on management, and public listing status. In particular, we are able to exploit the collapse of the Indian IPOmarket in 1997 as an exogenous shock to capital to identify how capital constraints are associated with gazelleformation.

Third, we will use cross-country panel firm-level data from Worldscope to investigate the relationship betweeninstitutions, financial development and ability of firms to grow fast across different sectors of the economy. Thereare a lot of unanswered questions, for example, are gazelles really as important in developing countries as they havebeen shown to be in the US?

We expect to produce a paper that will be submitted to the working paper series and to an academic journal. We alsoplan to disseminate this work via blogs and via presentations at academic and policy conferences.

I.4 Efficiency and Financial Risks of SMEs in China

Traditionally studies of SMEs rely on firm-level evidence (see, for example Beck, Demirguc-Kunt, and Maksimovic,2005, and Beck, Demirguc-Kunt, Laeven, and Maksimovic, 2006). However, the sampling frame for SMEs tends toleave out many micro and unregistered firms since they are not in the sampling universe (as determined by thestatistics bureau, the tax bureau or the chamber of commerce). This literature also leaves open a number ofunanswered questions: for example, how is SME finance related to the entrepreneurs# household characteristics suchas wealth, the structure of the household, and the wealth of other family members that do not own businesses?

This project aims to add to the literature in several ways. First, by using a representative and large household survey,this research will document the characteristics of a representative set of SMEs in China, document the sample#s sizedistribution and investigate how access to finance by SMEs is related to entrepreneurs# characteristics. The researchwill also investigate how collateral affects access to finance and the relative reliance on formal and informal finance.At the same time, the research will assess whether Chinese SMEs are efficient and what hinders their growth.Specific questions include: Given the same amount of credit, do they create more jobs and profits than larger firms?What share of SMEs are financially insolvent (i.e., with negative net assets)? And what are the determinants offinancial insolvency for SMEs?

The project will examine these questions using the Chinese Household Finance Survey (CHFS) data, which containsroughly 4,000 households owning SMEs (out of 28,000 households), and provides basic profiles of thesehousehold-owned businesses. For comparison groups, researchers will also use the Annual Survey of Industrial Firms(ASIF), which has around 200,000 firms per year and covers large and medium-sized non-state firms and allstate-owned firms in China. The research will also rely on the 2005 firm census, which covers all registered firms inChina.

The research will be conducted jointly with two researchers from the Southwestern University of Finance andEconomics (SWUFE) in China. By working with SWUFE (a university located in China#s less developed Western Region)and especially with two of its junior researchers, the project will also help strengthen that institution#s researchcapacity.

As output for this project, we expect to produce one working paper that will eventually be published in an academic

Internal Bank Report Page 7 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

journal. We will also write blogs and may publish in Chinese media for wider dissemination of the results.

I.5. Firm Financing and Growth Dynamics

Since the 1990s, capital markets around the world have witnessed a period of rapid development and intenseactivity. Yet, much needs to be learned about how firms have used that expansion to obtain new financing, and towhat extent the prosperity observed in capital markets has been translated into prosperity for all types of firms.

This research seeks to examine which and how many firms from different regions of the developing world obtaincapital market financing of different types. We also plan to study whether there are differences in the financing indomestic and international markets and in equity and bond financing. We plan to pay particular attention to theextent to which the financing is long term versus short term, or in domestic and foreign currency, as well as whichmarkets provide different types of financing for different types of firms. We will explore whether firms that obtainmore long-term financing invest more or become less vulnerable to shocks. We will also study whether the financingchanges during crises. We will compare the performance of firms across different regions. In particular, we plan toanalyze the growth performance of those firms as they raise capital. Though very basic, researchers have not fullyaddressed these issues.

This research will complement several papers and reports that argue that large firms are the ones that access capitalmarkets (Harris and Raviv, 1991; Myers, 2003) but which have so far offered no systematic documentation of howmany firms access equity and bond markets across countries, and whether more firms have accessed those markets asthe capital market activity has expanded worldwide. This research will also contribute to the extensive debate onwhether and how capital markets influence economic growth. Although the size of capital markets and the liquidityof secondary stock markets are positively associated with aggregate growth (Levine and Zervos, 1996, 1998;Demirguc-Kunt and Maksimovic, 1998; Henry, 2000; Beck and Levine, 2004; Bekaert et al., 2005; Levine, 2005),researchers have not determined whether the activity in primary markets is associated with growth at the firm level.There is also a debate on whether capital market development can expand access to finance, loosen financingconstraints, and disproportionately boost the growth of small, capable firms (Demirguc-Kunt and Levine, 2001; Myers,2003; Stein, 2003; Ayyagari et al., 2013). If for most countries, only a few large firms issue securities and then growrapidly, one can conclude that capital market development around the world has not, in general, involved smallerfirms issuing securities to fuel growth. The benefits for smaller firms might be indirect, as larger firms use capitalmarkets to obtain financing and free up resources for smaller firms. As securities markets across countries develop,the extensive margin among listed firms might expand, so that smaller firms could participate more in these markets.Finally, this project will inform a large separate debate on whether developing countries can borrow long term, andwhether firms can use foreign markets to extend their maturity (Gozzi et al., 2015).

This research will contribute to the various strands of the literature discussed above by using a large internationaldataset on firm-level domestic and international issuances of equities and bonds since the 1990s, matched withdifferent firm attributes. By using the data on issuance activity, this research will study how many firms and whichfirms issue equity and bonds, and for the latter the maturity of their borrowing. Moreover, by combining the issuanceof these two instruments with balance sheet information, the research will shed new light on the behavior of assets,sales, and employment when firms of different sizes issue securities. The data on firm capital raising activity comefrom the Thomson Reuters Security Data Corporation (SDC) Platinum database, which provides transaction-levelinformation on new issuances of common and preferred equity and publicly and privately placed bonds with anoriginal maturity of more than one year. To examine the performance of issuing and non-issuing firms, we will use amatched dataset on security issuances from SDC Platinum with firm-level balance sheet information from the Orbis(Bureau van Dijk) database. We plan to document different patterns for different developing country regions,something that is missing from the analysis and that will be useful to policy makers.

As outputs, we expect to produce at least two working papers and related publications. This work will be widelydisseminated in conferences, meetings with policy makers, as well as blogs and other outlets geared to the moregeneral public.

Internal Bank Report Page 8 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

I.6. The Effects of Low Returns on Savings and Indivisible Investment on Investment Levels in Developing Countries

This project aims to assess the impact of a low interest rate environment on small firms in countries with limitedaccess to credit. In developing countries, a large share of output is produced by small firms that must accumulateretained earnings to finance indivisible investment projects. Understanding how the constraints on these firmsinteract with low saving rates is crucial for assessing the policy gains from providing high-return stores of value,either through financial development or through monetary policy. This topic is of particular relevance to relativelylow-income households, as they are more likely to be self-employed or owners of small firms.

In his book #Money and Capital in Economic Development# (1973), McKinnon suggests that, in countries with limitedfinancial development, small and growing firms may be net savers rather than net borrowers: absent access to credit,firms must accumulate retained earnings to finance indivisible investment projects. This suggests that a low interestrate environment may be harmful (rather than helpful) for growth. In recent work Eden and Nguyen (2014) develop aquantifiable model in which inflation, by lowering the real rate of return on nominal savings, lowers investment insmall firms. The calibration conducted by the authors suggests that this mechanism may be quantitatively importantfor understanding investment in small firms.

Furthermore, a parallel macro literature pioneered by Caballero, Farhi and Gourinchas (AER, 2008) points at twostylized facts: first, interest rates are low and declining; second, while neoclassical growth models would predict thatemerging and developing economies should be net borrowers, many are net savers.

The proposed project will relate these two sets of issues. First, it will aim at quantifying the extent to whichindivisibilities at the micro level can help account for aggregate saving behavior on the macro level. Second, it willaim to quantify the effects of low interest rates on growth in developing countries, with a focus on small firms.

The proposed project will consist of a quantifiable model and a careful calibration. The model will build onmicrofoundations along the lines of Eden and Nguyen (2014), in which firms with incomplete access to credit maychoose to finance indivisible investment projects with retained earnings. In this environment, the firm#s demand forsavings would depend on the size of the indivisible investment relative to its profits. These parameters will becalibrated using firm-level data such as the World Banks Enterprise Surveys, together with price-level data from ICP.

The firm-level analysis will be embedded in a macroeconomic environment with global financial markets. Theaggregate demand for savings will be calibrated using moments relating to the size distribution of firms and theiraccess to finance. The hypotheses are: (a) indivisibilities at the firm level and financial underdevelopment may bequantitatively relevant in understanding the aggregate demand for saving in emerging and developing economies; and(b) a low interest rate environment reduces investment and growth in some low-income countries.

The expected output for this project is a research paper which will be circulated as a working paper and submittedfor publication. This project will be disseminated by a working paper and possible publication in an academic journaland seminar and conference presentations both in academia and in policy institutes.

I.7. Institutional Investors, Stock Prices, and Capital Allocation

Stock prices aggregate information about firms# fundamentals from many market participants. This information isuseful for decision makers, i.e. capital providers, customers, regulatory authorities and firm managers. Ideally, thisinformation should convey valuable signals about productivity and performance. In turn, stock markets are expectedto promote long-term growth, not only by providing equity financing for firms, but also by directing capital towardthe most productive projects.

While there is a large body of research studying the real effects of equity markets, most of this literature has focusedon the U.S. and little is known about the informational role of stock prices in low- and middle-income countries. Thisresearch seeks to close this gap. In particular, we seek to study stock price informativeness in developing countries(i.e. whether stock prices reflect information about firms# fundamentals), and the extent to which equity markets

Internal Bank Report Page 9 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

improve capital allocation and firms# outcomes. Additionally, given the growing role of non-bank financialinstitutions, the research will study whether institutional investors improve information production in equity marketsand whether their presence is beneficial for capital allocation and firms# performance.

In developing countries equity ownership tends to be highly concentrated. In such cases, institutional investorseffectively become corporate insiders, increasing the information asymmetry with other retail investors. Thispotentially reduces liquidity and is detrimental for information aggregation. Also, in smaller financial markets,domestic institutional investors are more likely to have strong ties to local publicly traded companies, whetherdirectly or indirectly (e.g. they might belong to the same economic group or the firm might receive lending through abank member of the same financial conglomerate as the institutional investor). Such relationships can be additionalsources of asymmetric information. In these cases, stock prices might be more opaque and less likely to reflectfundamentals.

This project will study the sensitivity of firms# investment to stock prices, and test whether investment decisions aremore efficient when stock prices reflect more private information. Furthermore, we will test for the determinants ofinformation in stock prices and analyze whether the presence of institutional investors is beneficial for informationproduction.

Data for this project will come from the following three sources: (i) Compustat Global for balance sheet data andprice information of publicly traded companies. (ii) Enterprise Surveys for private firm-level data. (iii) FactsetOwnership Database (former Lionshares) which provides worldwide equity ownership data at the fund/firm/quarterlevel.

The main results from this research will be presented in a paper. We expect to disseminate the results via policynotes, blog postings and seminar presentations, both academic and policy oriented.

I.8 Institutional Investors and the Expansion of Firm Finance

Many countries have tried to promote broader access to finance by developing their institutional investor bases. Butto what extent do institutional investors help expand the financing opportunities of firms and countries? Do domesticand foreign investors behave differently? What are the effects of benchmarks and other industry factors in theirportfolio allocations? Does participation in common benchmarks have an effect on the cost of capital of firms andcountries? Does it affect the ability to raise funds from institutional investors?

This research plans to analyze to what extent when firms from developing countries become part of commonbenchmark indexes, their cost of capital goes down and their ability to raise funds increases. The opposite mightoccur when firms are dropped from those indexes. The work will also study to what extent this effect comes from ashift in the demand for assets by institutional investors that these benchmark changes entail, which are notdetermined by the actions of those firms.

Aside from documenting how the cost of capital changes when the benchmark effects are implemented, we will usesome new exogenous methodological changes in broadly used benchmark indexes to test the direction of causality ofthese effects. These changes have affected companies across the world, and developing countries faced largereallocations of capital when those changes were implemented. As the amounts of passive investments haveincreased over time, the magnitude and timing of the effects also seem to have changed. The effects have becomelarger and stronger when the effects are implemented, relative to when they are announced (which were morecommon in previous research, as in Hau 2011).

One important advantage of using benchmarks is that they allow us to test how they affect the allocation of domesticand international savings and the cost of capital to firms. Benchmarks have become popular and are frequently usedby institutional investors to help alleviate agency problems. Benchmarks allow the underlying investors andsupervisors to evaluate and discipline fund managers on a short-run basis using, for example, the tracking error of thefund (the deviation of its returns from the benchmark returns). To the extent that the investment strategy of these

Internal Bank Report Page 10 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

funds is pinned down by the composition of their benchmark indexes (#benchmarks#), changes in the weights that apopular benchmark gives to different firms can trigger a similar rebalancing among the funds that track it and resultin sizeable movements in portfolio allocations and the amounts invested in each company. Furthermore, because agrowing number of mutual funds follow benchmarks more passively as a way to cut costs, increase transparency, andprovide simple investment vehicles, the importance of benchmarks has risen over time.

Benchmarks are also appealing to analyze because they are adjusted frequently and are subject to significantexogenous revisions that are clear, anticipated (after they have been announced), and large (entailing changes in theassets included, changes in the loading of each asset or country, and reclassification of countries across benchmarks).Thus, we are able to test the causality from benchmarks changes to mutual fund portfolio changes. These effects areindependent of any buy-and-hold effect that benchmarks might have on mutual fund allocations. Large benchmarkchanges such as country upgrades and downgrades can have systemic effects on capital allocations and asset prices.Moreover, they can lead to counterintuitive movements, including declining prices during upgrades, as well as inflowsand higher prices in countries with deteriorating fundamentals. By linking different countries in the same portfolio,benchmark changes can trigger reallocations across countries in that portfolio, connecting countries that mightotherwise be disconnected (e.g., Qatar and U.A.E. with Argentina, Kuwait, Nigeria, and Pakistan in the MSCI FrontierMarkets Index or Brazil, Russia, India, and China in the MSCI BRIC Index).

To conduct the research we plan to compile a novel dataset of detailed portfolio asset-level allocations acrosscountries by a large number of international mutual funds that we will match with the allocations of the benchmarksthey follow. We will also obtain information about the exogenous methodological changes that occurred in thesebenchmarks and trace the effects on the firms, as well as the mechanism behind those changes by studying thebehavior of mutual funds around those episodes.

The outputs from this project will be at least a working paper and a related publication. This work will be widelydisseminated in conferences, meetings with policy makers, as well as blogs and other outlets geared to the moregeneral public.

II. Volatility and risk

II.1 Domestic market evidence

II.1.a. Monitoring and Short-term Debt

The ability to raise long term debt is critical in funding housing, infrastructure, and long-term corporate projects.Issues surrounding costs and availability of long-term financing are therefore important from a developmentperspective, and are of significant interest to policymakers, development institutions and donors. There has beengreater need for policy guidance and discussion in the aftermath of the global financial crisis, which has constrainedthe supply of long-term funding and increased its costs. This research will contribute to the policy debate onlong-term finance, by empirically analyzing the impact of corporate governance and its interaction with country levelinstitutional structures on the use of long-term debt.

Short-term debt exposes firms to credit supply shocks and liquidity risk (Diamond 1991, Titman 1992, He and Xiong2012, Gopalan, Song and Yerramilli 2014). But, past research also suggests that leverage and debt maturity structurechoices could be effective in mitigating agency conflicts (Grossman and Hart 1982, Jensen 1986, Stulz 1990, and Hartand Moore 1995). Good corporate governance and independent boards are also expected to be effective in mitigatingagency problems (Bhagat, Carey, and Elson 1999, Yermack 1996, Gompers, Ishii, and Metrick 2003, Klein 2002). Inaddition, the law and finance literature suggests that the extent to which debt contracts can be used to mitigateagency problems depends on the institutional environment, and in particular the laws surrounding creditor andinvestor rights and the quality of enforcement of these laws (La Porta et al. 1998 and 2000, Diamond 2004, Burkart etal. 2003). Given the tradeoff between monitoring benefits and liquidity risk associated with short-term debt, weconjecture that firms with better governance will choose higher amounts of short-term debt in institutionalenvironments where the monitoring benefits of short term debt outweigh its costs. In particular, when creditors can

Internal Bank Report Page 11 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

impose substantial costs on managers and the firm during distress, boards and shareholders should employ greateramounts of short-term debt so that the managers are exposed to external monitoring by the market when it is moreeffective. This is the main contribution of the project.

We will analyze the firm level relationship between measures of governance and use of short-term debt in regressionsusing country fixed effects. We will then examine how this relationship covaries with measures of creditor andinvestor rights. We will confirm the cross-country results by examining changes around corporate governance reformsthat have been implemented over the sample period through a diff-in-diff approach.

The project will produce an academic paper, which will be submitted to the World Bank Policy Research WorkingPaper Series and to a peer reviewed finance journal. The authors will engage the community of academics, regulatorsand policy makers by presenting the project#s findings at conferences and symposia. The authors will alsodisseminate the main findings via the #All about Finance# blog.

II.1.b Bank Debt Pricing, Systemic and Idiosyncratic Risk

In the policy debate about reforming the existing capital adequacy framework to reflect systemic risk contributions,questions about the role of market discipline have received insufficient attention. This project examines howinvestors price systemic and idiosyncratic default risk in the debt of financial institutions. We show that in thepresence of implicit guarantees that are triggered in the event of multiple failures, investors price idiosyncratic butnot systematic risk. The results from this project shed light on the effectiveness of market discipline in the presenceof sector-wide implicit guarantees and will have important policy implications. In particular, the project#s findingsare useful for understanding potentially unintended consequences of a collective guarantee provided to the financialsystem.

The effects of too-systemic-to-fail government guarantees are an active topic of investigation amongst bothacademic and policy makers (see Kroszner 2013 and Strahan 2013 for reviews). This project contributes to thisliterature by examining the pricing implications of sector-wide implicit guarantees. If the implicit guarantee takeseffect only if banks fail at the same time, then they will have incentives to take on correlated risks (Acharya, Engleand Richardson 2012; Acharya and Yorulmazer 2007) so as to increase the value of the implicit guarantee. Investorswill then price in idiosyncratic but not systematic risk, since the guarantee will only take effect if a bank fails whenothers are failing at the same time. If the guarantee applies only to large banks, systematic risk would be pricednegatively for larger banks and positively for smaller banks. We will empirically examine these pricing implications inthe cross-section of corporate bonds.

The project will have a theoretical and an empirical section. First, we will build a model examining the pricingimplications of sector-wide guarantees. Second, we will examine the model#s predictions in the cross-section ofcorporate bonds.

In particular, we will model the pricing implications of an implicit government guarantee that is triggered in theevent of multiple bank failures. In standard asset pricing models, the idiosyncratic risk of an individual firm is notpriced. Asset prices and risk premiums are determined by exposures to systematic risk factors. But, if there is animplicit guarantee that gets triggered when there is a large systematic shock, then the pricing of idiosyncratic risk isnot clear. For instance, if a bank fails when no others are failing then the bank will not receive the state guarantee.If, on the other hand it fails when others are failing, it will receive a guarantee. The former is more likely when abank has more idiosyncratic risk. The latter is more likely if a bank has more systematic risk exposures. With animplicit sector-wide guarantee idiosyncratic risk will be priced and the impact of systematic risk exposures on pricewill be subdued, whereas only systematic risk would be priced without the guarantee. If the guarantee is for certainsectors of the economy, such as the financial sector, then we should see differences across sectors in the pricing ofsystematic risk in the debt markets.

In the second part of the analyses, we intend to test the model#s key pricing implications in the corporate bondmarket using the empirical model in Campbell and Taksler (2003) and Gopalan, Song and Yerramilli (2012). In

Internal Bank Report Page 12 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

particular we will compute systematic and idiosyncratic components of credit risk for firms that have corporate bondsoutstanding. We will then examine how each component of credit risk is priced for financial institutions andcompared to companies in other sectors.

The project will produce an academic paper, which will be submitted to the World Bank Policy Research WorkingPaper Series and to a peer reviewed finance journal. The authors will engage the community of academics, regulatorsand policy makers by presenting the project#s findings at conferences and symposia. The authors will alsodisseminate the main findings via the #All about Finance# blog.

II.1.c Social competition and excessive risk taking: evidence from lab experiments

Over-borrowing by firms and households can lead to financial instability and financial crises,This research studies, in a lab experiment setting, how social competition worsens the over-borrowing problem indeveloping countries. This fits the Bank#s agenda on shared prosperity, because financial crises hurt the poorseverely.

Financial crises have attracted a large amount of research (see Hsu, 2013 for a comprehensive review). Recently,research has looked into different sources for over-borrowing. Korinek (2015) and Bianchi (2011) argue that agentsover-borrow because they do not realize the macro-financial instability they contribute to by their borrowing. Theliterature has not considered the social competition aspect of over-borrowing, probably because it is difficult toincorporate social competition into traditional models of macroeconomics. One innovation of this project is that wewill be able study the issue in a lab experiment setting.

Using the framework laid out by Korinek (2015) and a series of incentivized lab experiments, this research will testthe observation that competitive preferences distort risk-taking in the market. We will do this by eliciting risk takingbehavior in two treatments: when returns to risk taking are public versus when returns are private. The difference inbehavior across these treatments is due to competitive behavior. In addition, we will also consider a treatment whenthe highest return from risk taking is rewarded (to mimic rewards to successful entrepreneurs). Next, we implementa series of Tobin-taxes under both the public and private borrowing conditions to determine the tax rate that bringsborrowing/risk taking to socially optimal levels.

The expected output will be two working papers that will be sent to the WB Policy Research Working Paper Series andeventually to academic journals. We also plan to disseminate the work via blogs and presentations at academic andpolicy seminars and conferences.

II.2. Integration, Globalization, and the Transmission of Shocks

II.2.a. Institutional Investors and the Transmission of Shocks

Foreign institutional investors are the dominant players in most equity markets. They represent 70% of totalinstitutional stock ownership in developed economies and 93% in emerging economies. These international investorsprovide an important source for firms# financing and are vital drivers of economic growth. However, their presence isalso a potential source of financial instability. More precisely, through their portfolio rebalancing they mightpropagate shocks across industries, markets and countries. In turn, companies which rely on equity financing are thensusceptible to foreign shocks and might become financially constrained as liquidity dries up. Financial instability canhave widespread and severe consequences, slowing long-term growth and disproportionately affecting the poor(Prasad, et al., 2007; Laursen and Mahajan, 2005).

This project seeks to study how different types of international institutional equity investors react to shocks andwhether their behavior affects the transmission of crisis events across countries. In particular, we seek to answerthree research questions. First, how volatile are foreign institutional equity investments across countries? Second,which types of institutional investors help transmit crises and which ones tend to mitigate the transmission of shocks?Third, what was the behavior of different types of institutional investors during the global crisis and the ensuing

Internal Bank Report Page 13 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

sovereign debt crisis?

While the literature argues that the supply side of funds and, in particular, the actions of fund managers areimportant in the transmission of shocks, detailed evidence on how institutional investors behave in theirinternational investments is rather limited. To our knowledge, there are no comprehensive studies on the role ofdifferent types of international institutional investors in transmitting shocks. Due to data availability, most studieshave focused on the behavior of mutual funds. However, not all types of institutional investors face the same type ofincentives and monitoring as mutual funds. For example, portfolio decisions within insurance companies anddefined-benefit pension funds are most likely driven by maturity matching while hedge funds anddefined-contribution pension funds are typically motivated by short term objectives resulting from marketmonitoring. In this sense, some institutional investors are likely to play a stabilizing role in equity markets duringcrisis times while others might help propagate shocks.

The data for this study will come from the Factset Ownership Database (former Lionshares). This database providesequity ownership data worldwide at the fund/firm/quarter level. This covers equity holdings by funds collectedglobally from fund reports, regulatory authorities (e.g., 13F reports in the United States), fund associations indifferent countries, and directly from the fund management companies. That is, for each public company, thedatabase presents quarterly information on holdings by institutional investors such as banks, insurance companies,investment companies, pension funds, hedge funds, venture capital and sovereign wealth funds. We will useDatastream for additional firm level information (earnings, stock prices, etc.).

The main results from this research will be presented in a paper. We also expect to disseminate the results via policynotes, blog postings and seminar presentations, both academic and policy oriented.

II.2.b Equity Market Integration and the Covariance of Stock Returns

Equity markets constitute a significant source of firms# long-term financing. However, in many developing economies,stock markets are still small, illiquid and highly fragmented. A common policy recommendation to overcome suchlimitations and to promote financial development is the integration of stock markets and the promotion ofcross-border investments and listing of securities. In theory, financial integration should enhance competition,improve efficiency and productivity, and facilitate the flow of information. More importantly, issuing firms fromotherwise small markets are exposed to a larger set of investors, potentially increasing their ability to raise muchneeded long term funds.

Stock market integration can be achieved in many ways. For example, via regional stock exchanges or through theharmonization of regulation and the standardization of both security deposits systems and settlement systems acrossseveral countries. Harmonization of stocks markets is a costly task and in many cases requires a strong politicalcommitment. One of the trade-offs between financial market development through stock market integration is theadditional exposure to foreign shocks, which might harm financial stability. More precisely, integrated stock marketsmight be more prone to propagate shocks across firms, industries and across countries. In turn, companies that relyon equity financing are then susceptible to foreign shocks that are not necessarily related to their business model.Such spillover effects are likely to manifest themselves through higher covariance of stock returns in excess offundamentals.

This research will study stock return co-movement and trading volume before and after recent experiences of stockmarket integration in developing countries (e.g. the Central African Stock Exchange, BVMAC, the Latin AmericanIntegrated Market, MILA, among several others). In particular we seek to answer questions such as does thecovariance of stock returns increase for listed firms across these markets? What industries and markets are moreexposed to foreign shocks following the stock market integration? Does trading activity increase for publicly tradedfirms after stock market integration?

There is extensive work documenting stock returns co-movement in excess of fundamentals. However, most of thisliterature has focused on within country experiences in well-developed stock markets. This research will study price

Internal Bank Report Page 14 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

co-movement between the stocks in markets that underwent regional integration efforts. We seek to shed light onthe potential impact for financial stability resulting from equity market integration.

The data for this study will come from Datastream. Datastream provides global coverage of daily stock priceinformation and periodic fundamental information for listed companies. The main results from this research will bepresented in a paper. We expect to disseminate the results via policy notes, blog postings and seminar presentations,both academic and policy oriented.

II.2.c International Capital Flows to Small and Poor Countries

International capital flows and, in particular, foreign direct investment (FDI) have risen substantially over time. Aspart of this process, developing countries are increasingly participating in these flows by not only receiving a largeramount of funds but also making investments abroad, in both developed and developing countries. This is relevantbecause FDI allows countries to attract more capital, diversify their sources of funds, diversify the risk of theirinvestments, and transfer technology between the source and target countries and firms, upstream and downstream.Still, relatively little is known about the extent to which capital actually flows into and out of poor countries (fromand to other poor countries or rich ones), and how the developing country firms and sectors that receive and sendthose investments perform when they engage in international financial transactions.

The work in this area plans to exploit novel bilateral data to study a series of related questions using different levelsof aggregation, from country-level to firm-level data. In particular, we plan to study three aspects of FDI: (i) Wheredo the international capital flows to small and poor countries come from? Has this changed over time? Are small andpoor countries also exporting more capital over time? To where? Are the South-South transactions increasing? (ii)When firms engage in foreign direct investment, how do they perform? Do they gain expertise by investing in othercountries? Similarly, how do the firms that receive the investments behave? Do they acquire expertise from thesource firm? Does this change depend on whether the target and source firms are from the South or the North, orfrom countries with particular expertise as manifested in their exports? (iii) Is capital flowing to firms in all sectors ofthe economy? Is it flowing to the firms in the sectors in which a country has a comparative advantage, like theprimary sector? Or is it going to firms in the sectors in which the sending country has a comparative advantage? Doinvestments in a specific sector allow firms to subsequently specialize and increase production in that sector?

These questions are associated with several recent discussions in the literature and are important for developmentpolicy making because capital flows represent a significant share of the financial resources available to developingcountries for investment and growth. Moreover there is a growing interest in whether the financial connections of theSouth are with more technologically advanced nations or with similar nations in the South, and how thosetechnological transfers work.

Since the early 1990s, countries in the South have been growing fast relative to those in the North and, by now, theycapture an important share of the world#s economic activity. Although the vast literature on capital flows argues thatfinancial flows have increased over time, it has not studied how important the South is as recipient and source ofcapital flows for different types of countries, nor how large the financing among South countries is. This is becausemost of the literature on capital flows relies on the flows of each country to and from the rest of the world.

A separate strand of the literature analyzes the effects of FDI and the performance of firms around the FDI activity.But this literature tends to be concentrated on particular countries and focuses on the firm receiving the FDI. To ourknowledge, there is no study using the most recent data and analyzing the effect of FDI on the target and sourcefirms. For example, North India#s Tata group might have benefited from acquiring Britain#s Jaguar, while it might notget similar benefits when investing in firms from less developed countries. With the data we have, we would be ableto conduct that type of analysis. Moreover, we would be able to analyze whether the effects differ depending onwhere the firms are located and the expertise of the countries involved. In fact, there is some debate about whetherthe investments from the North and the South have different effects (Holmes et al., 2013).

In a separate debate, little is known about the cross-country sectoral allocation of capital and about the specific

Internal Bank Report Page 15 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

channels or motives through which capital flows might be linked to trade flows in different sectors. In fact,cross-border investments and exports might be connected from incentives at the firm level (Greenaway and Kneller,2007; Alfaro and Charlton, 2009). To address whether investments and exports are related, sectoral data help to shednew light. The most disaggregated level at which the links between financial and trade flows have been studied so faris the country-pair level, pooling both exports and imports. The sector-level data we plan to use for this researchrepresents a major step forward, which can yield highly relevant information for academics and policymakersregarding the link between trade and financial flows.

To conduct the different analyses we will use bilateral data on FDI. We will construct new types of descriptivestatistics and expand on the analysis in the literature. We will use firm-level transaction data on mergers andacquisitions (M&A) from Thomson Reuters# SDC Platinum and on (announced) greenfield investments from theFinancial Times# FDI Markets. For comparison, we will also analyze syndicated loans from Thomson Reuters# SDCPlatinum transaction-level data. We will match the data on FDI with data from Orbis to analyze the performance offirms around the FDI activity. For some countries we might get access to census data. To study which sectors thefinancial flows go to and whether they go to countries whose firms have expertise in those sectors, we will use tradedata. In particular, we will match the data above on foreign investments and syndicated loans at the sector levelwith sector-level trade information from Comtrade.

As outputs, we expect at least two working papers and related publications. This work will be widely disseminated inconferences, meetings with policy makers, as well as blogs and other outlets geared to the more general public.

II.2.d Financial Integration, Risk Sharing, and the Stability of Consumption in Developing Countries

Over the last quarter-century, financial openness and financial integration have risen across the world. Barriers tointernational financial flows have been sharply reduced, or dismantled altogether, in advanced economies, emergingmarkets, and more recently also in #frontier markets#, with the latter including a number of poor countries andAfrican economies. Cross-border financial flows have correspondingly experienced large increases in most countries.

In a context of incomplete financial markets, these developments could be interpreted as expanding the menu oftradable assets and /or reducing the costs of trading existing assets. From a theoretical perspective, this in turnshould widen countries# opportunities to diversify their idiosyncratic income risk and thereby improve consumptionrisk-sharing. Other things equal, this should result in a welfare-enhancing increase in the stability of households#consumption streams. Because consumption is much more volatile in developing than in advanced countries, itfollows that the former would stand to gain the most from financial globalization. However, earlier empiricalassessments (starting with, e.g., Kose et al., 2006) failed to find evidence that the era of financial globalization hadled to increased consumption stability outside advanced countries # if anything, the finding was that the volatility ofconsumption had been on the rise.

Related to this, a long-standing line of research (dating back to Obstfeld, 1994 and Lewis, 1996) has focused onquantifying the extent of international consumption risk-sharing, by assessing the international correlation ofconsumption, or through regressions of consumption on domestic income and global (or average) consumption(Sorensen et al., 2007, Kose et al., 2009). Strictly speaking, the empirical tests performed by this literature assessthe null hypothesis of perfect risk-sharing across the world. Once the null is rejected (as it almost invariably is), thetests are uninformative about the extent of risk sharing actually taking place. Further, they implicitly (or explicitly,as in Crucini, 1999 and Asdrubali and Kim, 2008) assume that the degree of international risk sharing is the same inall countries, an assumption that is clearly inappropriate when both rich and poor countries are included in theanalysis.

The purpose of this research is to examine the patterns of consumption volatility during the financial globalizationera, provide an assessment of the degree of consumption risk sharing across countries and over time, and examinethe contribution of international financial integration to those trends. The research will pay particular attention tothe similarities and, especially, the differences between rich and poor countries. The specific questions to beaddressed will include:

Internal Bank Report Page 16 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

# How has the volatility of consumption evolved during the globalization era? What are the differences andsimilarities between rich and poor countries? Have common (global) shocks become a more prevalent source ofconsumption fluctuations? To what extent do observed changes in the international correlation of consumptionreflect changes in the correlation of national consumption with national income, and changes in the internationalcorrelation of incomes? What is the degree of consumption risk-sharing in different countries? Does it varysystematically with the level of development?

# How does risk-sharing relate to de iure and de facto measures of financial openness (such as those derived fromChinn and Ito, 2008, and Lane and Milesi-Ferretti, 2010)? Does such a relation differ between rich and poor countries?Does the composition of foreign assets and liabilities (e.g., FDI vs debt) matter? What is the role of other potentiallyrelevant policy and structural factors # e.g., real openness, the exchange rate regime, fiscal institutions, and thecommodity-intensity of production?

# Assessments of consumption risk-sharing may be distorted by consumption inertia (Fuhrer and Klein, 2006) andborrowing constraints (Asdrubali and Kim, 2008). The latter ingredient is particularly prevalent in poor countries, andtheory suggests that it should have been significantly affected by the rising degree of international financialopenness. Does bringing these factors into the empirical analysis affect the conclusions regarding risk-sharingpatterns and the role of financial integration?

The research methodology will be based on the estimation of static and dynamic factor models (Bai and Ng 2003,2007; Stock and Watson, 2005) to identify the common and idiosyncratic components of consumption and real incomeusing a large sample of countries. To assess the spillovers across countries, we will also estimate models in the styleof the spatial dynamic panel data (SDPD) model considered by Yu, De Jong and Lee (2008). In addition, to provide astructural interpretation for the assessment of risk-sharing across countries, we will estimate an extended version ofCrucini#s (1999) model, allowing for heterogeneous degrees of risk-sharing and, to the extent feasible, consumptioninertia and hand-to-mouth consumers.

We expect that the proposed work will yield valuable insights regarding what poor countries can expect fromincreasing financial openness, as well as policy conclusions regarding how to manage the process of financialintegration # e.g., the effects of alternative forms of financial integration in terms of asset and liability composition,and the potential role of other policies and reforms accompanying financial integration.

The research will generate at least two papers, which we will issue as working papers and, after suitable revision,submit for journal publication. The main results will be disseminated with presentations at academic and policyevents, as well as blog posts and presentations to Bank staff.

FINANCE AND INEQUALITY

III. Documenting the link between finance and inequality

III.1. The Distributional and Macroeconomic Implications of Financial Development: A Quantitative Analysis

A rooted conjecture in the area of development economics is that the process of convergence from low to high levelsof income implies a #Kuznets curve#, that is a period of increased income inequality until the transformations in theeconomy start to spread out over the entire income distribution. This research seeks to provide a benchmark for theexpected evolution of income inequality generated by the development of financial markets. Having some sort oftheoretical benchmark is important for evaluating the observed patterns of income distribution of a country overtime, or a group of countries at a point in time. This is also an important ingredient for guiding the direction of policyinstruments aimed at correcting for deviations from the expected paths of inequality. Clearly, these contributions arealigned with the bank#s twin goals of reducing poverty and fostering shared prosperity.

There is a growing literature seeking to understand the role of financial development for economic development.Well known studies in the area are Buera, Kaboski, and Shin (2011), Moll (2014), and Midrigan and Xu (2014).

Internal Bank Report Page 17 of 29

World Bank - Grant Funding Request (GFR)

Ref. : 18516 Status : Cleared Printed on : 05/06/2015

However, most of this literature focuses on understanding differences in levels of income across countries. Thecontribution of this proposal is to shift the focus to understanding development dynamics, and characterizingpatterns of income inequality along those development paths.

The approach in the proposal is a structural one. We shall develop a theoretical framework with multidimensionalheterogeneity across individuals that will act as the source of income inequality. Specifically, there will beheterogeneity across individual's entrepreneurial ability to operate firms, there will be heterogeneity of incomebetween entrepreneurs and wage earners, there will be inequality due to frictions in the labor market that lead toequilibrium unemployment, and there will be variation in wealth accumulation and capital income resulting fromagents' consumption saving decisions. The proposal also contemplates coming back to the data and refining the typeof insights we try to infer from the evidence. For example is it the case that a temporary increase in inequality isalways necessary for entrepreneurs to increase saving rates and bridge the capital deepening gap?

The main output from this research will be a working paper of publishable quality in a top journal in the field. Thiswork will also be disseminated via presentations at academic institutions, as well as international organizations.

III.2 Inequality, Inadequate Finance, and Alternative Coping Mechanisms

Rising inequality is a top challenge faced by China and many developing countries. Inequality in household incomeand asset ownership has been shown to be much more serious than previously thought in the Chinese context (Surveyand Research Center for China Household Finance, 2013). The Chinese Household Finance Survey (CHFS) provides anexcellent data set for better understanding inequality in China. It provides detailed information on wealth, income,and transfers (both private and from government). Since the data are representative at the provincial level, we canalso calculate regional inequality.

This research seeks to describe the basic patterns of inequality in China and to explore the role played by access (orlack thereof) to finance as a determinant of regional inequality in the country. While a handful of studies have lookedat the relationship between finance and inequality (Clarke, Xu and Zou 2006 and Beck, Demirguc-Kunt and Levine2007), using the Chinese data has the advantage of holding the legal system and culture constant. Moreover, we willalso investigate whether trust affects inequality, whether access to finance or trust is more important, and whetherthere is a complementary relationship between trust and access to finance (Guiso, Sapienza and Zingales, 2004).Intuitively, trust should help the poor in obtaining finance (Knack and Keefer, 1997) and thus make pro-poor growthmore likely.