Embed Size (px)

Citation preview

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 1/12

Why Accounting for Uncertainty and Risk can Improve Final

Decision-Making in Strategic Open Pit Mine Evaluation

L A Martinez1

ABSTRACT

The objectives of this paper are two-fold. First, it will show whatproblems can arise when single estimated values are substituted for adistribution of values when evaluating an open pit mine project in the faceof uncertainty. Secondly, it will show how the ability to deal withuncertainty and risk in mine project evaluation can have a significantimpact on the owners’ and stakeholders’ investment decision-making. Herea new mine evaluation framework, the integrated valuation/ optimisationframework (named IVOF), is introduced as an alternative tool for mineproject evaluation where uncertainty and risk are incorporated in theevaluation process.

INTRODUCTION

A new era is coming for the mining industry. An era where mineplanners, mining engineers and mine analysts, not only ask themselves the question, ‘What if ...?’ when evaluating theirrespective mine, but also want to know what is the effect of these‘What if ...?’ uncertainties on their project evaluation process, aswell as the best strategies to follow when facing either an adverseor a favourable condition.

Using intuition, it is logical to be asking these ‘What if ... ?’questions when evaluating a mine project. The reason for this isthat normally a mine project has a long-term operating life andthose of us that are involved in mine project evaluation are awarethat the future brings uncertainty. It is within this environmentthat mine analysts have to manage the level of uncertainty of their projects, so they can make decisions based on rational anddisciplined thought.

Even though it is getting more common to see projectmanagers making final decisions based on an expected minevalue and a sort of interval of confidence, where the risk/ potential for future losses/opportunities are assumed to becovered, there is still some reliance from most of them inworking with a given expected mine value number.

One of the common arguments the author has observed forusing just one number for making final decisions is that it is asimple process, ie if it is greater than zero or not. Conversely,decisions based on a distribution are not straightforward andfurther analysis, such as conditional simulation, scenario analysisand risk analysis, need to be made.

Another common argument the author has listened to is that it isnot worth the trouble of making decisions based on risk analysis

when the final results will not differ much from the single‘expected’ value. Indeed, a mine evaluation process based on risk analysis is more costly and time demanding than an evaluationprocess based on single estimates.

The previous arguments clearly indicate that the mainproblems for which uncertainty and risk are normally neglectedfrom the mine evaluation process are due to:

• lack of knowledge about the differences between makingdecisions based on expectations resulting from either a singleor a distribution of values, especially when working withcomplex processes such as the mine evaluation process; and

• lack of an appropriate mine evaluation framework that is ableto include the ‘What if ... ?’ uncertainties into the mineevaluation process appropriately and within a reasonabletime frame.

Consequently, the objective of this paper is two-fold:

1. it shows what problems can arise when single estimatedvalues are substituted for a distribution of values whenevaluating an open pit mine project in the face of uncertainty, and

2. it shows how the ability to deal with uncertainty and risk inmine project evaluation can have a significant impact on theowners’and stakeholders’ investment decision-making.

To achieve this, the paper explores and describes the mainsources of uncertainty of a mine project evaluation process. Thepaper will then show what problems can arise when singleestimated values are substituted for a distribution of values whenevaluating an open pit mine project in the face of uncertainty.Section 4 introduces a new mine evaluation framework, namedIVOF, as an alternative technology for mine project evaluationwhere uncertainty and risk are seen as allies when evaluating anopen pit mine project. At the end of the paper, two practicalexamples of how uncertainty and risk can be used fordecision-making in mine project evaluation are presented whenevaluating a gold and a coal mine project.

MAIN SOURCES OF UNCERTAINTY IN MINEPROJECT EVALUATION

As mentioned in the introduction, mine projects are complexbusinesses that demand a constant assessment of risk. This isbecause the value of a mine project is typically influenced bymany underlying economic and physical uncertainties, such asmetal prices, metal grades, costs, schedules, quantities andenvironmental issues, among others, which are not known withabsolute certainty. This section explores the main sources of uncertainty arising at the beginning of a mine project.

Uncertainty in orebody modelling

In the prefeasibility stage of a mining project, the geology andore distribution in the mineral deposit are estimated from theinformation derived from the exploration drilling samples. Sincethe information obtained from the samples is not representativeof the entire (3D) ore deposit, the geology of the ore depositrepresents one of the most critical sources of technical uncertaintyin a mine operation. One consequence of this lack of informationis the misclassification of resources, where economic ore can bedispatched to the waste dump and non-economic ore can be sent tomill.

To minimise the misclassification of resources, estimationtechniques based on stochastic models, eg kriging and conditionalsimulation techniques, are commonly used to estimate thegeological information at non-sampled locations. This is done byinterpolating the data from the few exploration samples.

Uncertainty in metal prices and costs

Another important source of uncertainty which has a criticalimpact on open pit mine project evaluation is that associated with

Project Evaluation Conference Melbourne, Vic, 21 - 22 April 2009 113

1. MAusIMM, Managing Consultant – Integrated Mine Optimisation,Gemcom Software Australia-Asia Pty Ltd, Level 6, 280 AdelaideStreet, Brisbane Qld 4000. Email: [email protected]

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 2/12

the economic environment where the mine project is developed.Within this economic environment, future metal prices and costsare the most important factors of uncertainty.

The price of the metal is the real cash-settlement thatrepresents the equilibrium or non-equilibrium of the metalmarket. Since this market is based on demand, supply and otherfactors, such as speculation, news events and dividend payouts(Fanning and Parekh, 2004; Case and Fair, 1989; Taylor, Moosa

and Cowling, 2000), uncertainty on future metal prices arisesbecause of two main factors:

1. the lack of exact knowledge of those factors leading to theincrease/decrease in metal supply and demand, and

2. the practices that producers or consumers perform in the faceof powerful speculative and political motives (MacAvoy,1988).

In the mining industry, metal prices are normally modelled asthe average price of the last three years, especially for thosecommodities whose price is listed on open markets, such asprecious and base metals (Rendu, 2006). Even though the use of single commodity price makes comparison between companieseasy, preventing the use of excessively optimistic prices, it is alsorecognised that it could be misleading when evaluating mining

projects. For example, an overestimated metal price may result ina favourable rate of return for a project, which is otherwisedoubtful, and conversely, an underestimated metal price may resultin an unfavourable return for the project, which is otherwiseprofitable.

Costs are another source of uncertainty when evaluating anopen pit mine project. The reason for this is that the economicevaluation component of the feasibility study is based oninformation that provides an answer to the question, ‘what is it going to cost?’ (Gentry and O’Neil, 1984). Since estimation of capital and operating costs is an important requirement for open

pit mine evaluation, uncertainty in costs arises due to the lack of the engineering or economic information at the beginning of themine project. Simply put, mining companies do not know withabsolute certainty today how much they will be able to spendtomorrow, let alone next month or even next year (Camus, 2002).

Uncertainty and risk in open pit mine planningand design

The complete process of planning and designing an open pitmine consists of two principal stages:

1. mine design, where the ultimate pit limits are found andcontoured; and

2. production scheduling, where the sequence of extractionover time and consequently the cash flow of the project areplanned and analysed respectively (see Figure 1).

The ultimate pit limit is the widest possible boundaries withinwhich all the subsequent mine planning works are performedwhile maximising total cumulative net present value (seeEquation 1). Production scheduling, on the other hand, is thedevelopment of a sequence of depletion schedules leading fromthe initial condition of the deposit to the ultimate pit limits.

Depending on the duration of the scheduling periods, productionscheduling can be classified as long-term or short-term scheduling.

Since both the ultimate pit and the production schedulingdepend directly on the orebody model and future metal price andcosts, uncertainty and risk in open pit mine planning and designarise due to the uncertain nature of the underlying variables thattake part in the designing and planning process. In this context,the allocation of the physical limits of both the ultimate pit andlong-term production sequence on the orebody model turns into acomplex and uncertain process.

114 Melbourne, Vic, 21 - 22 April 2009 Project Evaluation Conference

L A MARTINEZ

Surface

Waste

Not

economical

ore

Surrounding

material

Not

economical

ore

Surrounding

material

Ore

Waste

Surface

Waste

Non

economical

ore

Surrounding

material

Non

economical

ore

Surrounding

material

1

2

3

Ore

Waste

Ore

Surface

1

Surrounding

material

1 First Pushback

abc

d

a

Ore

Waste

a bc

d

Ultimate Pit

First Cutback

( A ) ( B )

( C ) ( D )

FIG 1 - Schematic representation of: (A) orebody and the ultimate pit; (B) long-term scheduling composed of the ultimate pit and cut-backs 1,

2 and 3; (C) short-term scheduling for cut-back 1, where a, b, c, and d represent the extraction sequence; and (D) plan view of the short-term

scheduling for cut-back 1, where a, b, c and d represent the extraction sequence (adapted from Martinez, 2003).

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 3/12

The ‘flaw of averages ’ in mine project evaluation

Traditionally, mine organisations use various types of quantitative methods to estimate profit and loss associated witha proposed mine project. Among all these measures of profitability, the net present value (NPV), which is based on thediscounted cash flow (DCF) technique (see for exampleBenninga, 2000), is the most widely used in the mining industry.This is because it recognises the time value of money andaccounts for risk via an adjusted discount rate, R (seeEquation 1), giving the mine analyst a tool for making financialinvestment and dividend decisions. More formally, the NPVtechnique consists of subtracting the capital investment (CapInv)incurred at the beginning of the mining project (assumed to beperiod t 0), from the sum of the present value of the expected netcash flows ( { } E CF t ) generated throughout the operating life (t =1,2,..,T ) of the open pit mine project:

{ } NPV

E CF

RCapInvt

t t

T

=+

−=∑

( ).

11

(1)

In practice, the expected cash flows generated at eachproduction period, t = 1,2,..,T are estimated using expected

values for the underlying variables such as the metal price, S t ,production costs, Cost t and metal quantity, qt , produced, ie:

{ } { } { } { } E CF E q E S E Cost t t t t = × −( ), (2)

One consequence of using expected values when estimatingcash flows is that the resulting NPV value is also assumed to bean expected value, which, as it will shown later on, may not bereflecting the real project’s value leading to incorrect decisions.

Although some variations of the discounted cash flow (DCF)technique, such as scenario analysis, have been developed to givemine analysts the flexibility of including different scenarios inthe mine evaluation process, they still suffer the same problem of the DCF, ie instead of working with the uncertain variables, these

techniques work with a single estimated value

2

for each scenario,relying on the adjusted discount rate, R, to account for risk anduncertainty in the entire mine project.

The problem with evaluation techniques based on the DCF isthat in cases involving uncertainty and non-linear processes,in our case the mine optimisation/evaluation process, singleestimate values are often of little use because of their lack of accuracy in describing an uncertain process. In other words, asit is shown in Figure 2, serious trouble can arise when a singlenumber is substituted for a distribution of probabilities. That is, if the expected value, E{X}, of the uncertainty variable, X , is inputinto the non-linear process F (.), the resulting output, F(E{X}),will not be the same as the expected value of the resultingoutputs, E{F(X)}, generated by inputting the entire distribution of values, ie F ( E { X }) ≠ E {F ( X )}.

Professor Savage, from Stanford University, refers to thisproblem as ‘the flaw of averages’3 (Savage, 2002a, 2002b, 2003),

which states that plugging average values of uncertain inputs intoa non-linear process does not result in the average value of theprocess, ie F ( E { X }) ≠ E {F ( X )}. He explains this concept withthe following example (see Figure 3):

Consider the state of a drunk, wandering back and forth on a busy highway. His average position is the centreline of the highway.Therefore the state of the drunk at his average position is alive. However, it is clear that theaverage state of the drunk is dead.

An analogous situation happens when evaluating a mineproject using traditional mine evaluation techniques that arebased on the DCF. That is, when evaluating a mine project it iscommon to use expected single values for representing all themine variables4 that are input into the non-linear mineoptimisation process (Martinez, 2003; Dimitrakopoulos, 1998).The final output of this practice is a single estimated value foreach of the project indicators, such as projected revenues andexpenses, grades, metal quantities and mining and processingcosts, among others, which are assumed to be the average valuesto be obtained. Although, it is common to perform a sensitivity

analysis that uses spider and tornado diagrams to obtain a sort of

Project Evaluation Conference Melbourne, Vic, 21 - 22 April 2009 115

WHY ACCOUNTING FOR UNCERTAINTY AND RISK CAN IMPROVE FINAL DECISION-MAKING

x1

x2

x3

xn

…

E {x} F() F(E {x})

x1

x2

x3

xn

…

E {F(x)}F()

F(x1)

F(x2)

F(x3)

F(xn)

…

Uncertain Input VariablesNon-linear Process

Final Results

FIG 2 - Scheme showing that ‘average inputs do not always yield

average outputs’ when dealing with uncertainty and non-linear

processes.

FIG 3 - A sobering example of the flaw of averages (from

Savage, 2003).

2. Observe that a single estimate in the context of a financial andengineering statement is a single number, often an average orexpected value, used to represent the value of an uncertain quantitysuch as the average metal grade of the deposit, the price of the metaland future mine revenues or expenses, among others. An uncertainquantity is normally represented by a probability distribution, or a bargraph, which represents the relative likelihood of various outcomes.

3. Also known in finance as the Jensen’s inequality, which states thatbecause the value of a project, x , is a random variable and the optionvalue, OV , on the project is a convex function of the project value,then, OV E X E OV X ( { }) { ( )}≠ .

4. Examples of these input variables are the orebody model, metalprices, costs and recoveries.

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 4/12

interval of confidence for the final mine revenues, traditionalmine evaluation techniques ignore any possible realisticfluctuations in revenue or expense due to the existing uncertaintyof the different input variables over time and corresponds to theassumption that the drunken guy will be always walking on thecentre line (see Figure 3).

The problem is that even though sensitivity analysis issupposed to account for variations in the different input

variables, it assumes that these changes will happen in a linearfashion, ie the same change will occur at each production period,which is not true. See for example Figure 3, where the yellowdashed lines represent the ±10 per cent confidence interval that issupposed to account for the drunk’s trajectory deviation from thecentral line. As observed in the figure, this confidence intervaldoes not give a realistic representation of the drunk’s trajectory.Another limitation of sensitivity analysis is that it ignoresdependence structure between the underlying variables that takepart in a mine evaluation process performing changes in anisolated fashion, ie changes to a specific variable are performedkeeping the other ones constant.

In the case of a mining project, metal grade variations willoccur at different locations of the orebody model, but following aspecific correlation structure, ie changes at different locations

will be generated following a specific correlation structure,which is a non-linear process. Similarly, metal prices will alsovary at each production period but at different rates. Thus, it isimportant to be cautious when making decisions based on asensitivity analysis, since it could lead to spurious description of the current financial situation of the mining project.

One of the techniques that has been widely accepted as aunified approach to dealing with uncertainty is the Monte CarloSimulation technique (Glasserman, 2004; Chan and Wong,2006). This is because instead of hiding behind a single best‘estimate’ this technique quantifies uncertainty by sampling theprobability distribution of the uncertain variable while trackingthe resulting outputs. However, despite its benefits when dealingwith uncertainty, the application of the Monte Carlo technique tothe mine evaluation problem is not straightforward. The reason

for this is that the mine optimisation process is a 3D complex,non-linear procedure where the uncertainties of the inputvariables are of different natures. For example, the uncertainty of the orebody model could be classified as static (Martinez, 2007)since it depends on the geology of the deposit that is uncertain;not because it changes over time, but because of the limited data(eg drill hole data) obtained for its quantification5. On the otherhand, the uncertainty of future metal prices can be classified asdynamic because it depends on the international metal market,which is affected by different mechanisms such as offer, demandand speculation and which varies over time. Furthermore,besides the nature of the sources of uncertainty, a mineevaluation process also depends on plans that are based onphysical designs, such as the ultimate pit and cut-back limits thatobey technical constraints such as the production scheduling.

A ROAD TO IMPROVE – APPLYING A NOVELINTEGRATED MINE EVALUATION FRAMEWORK

THAT ACCOUNTS FOR UNCERTAINTY AND RISK

Different techniques have been developed to overcome thecomplexity of the mine evaluation problem. Although some of

them have been shown to be very efficient in dealing with aspecific part of the problem, none of them have been able tosolve the complete problem, ie considering all sources of uncertainty. The reason that current techniques cannot solveappropriately the mine problem is that these techniques havebeen developed in isolation. That is, mine evaluation techniques,such as the upside/downside potential (Martinez, 2003;Dimitrakopoulos, Martinez and Ramazan, 2004), developed todeal with technical uncertainties, such as the orebody model, donot account for the uncertainty of economic variables. Similarly,mine valuation techniques, such as real options, that deal witheconomic uncertainties, such as metal prices, do notappropriately account for technical uncertainty.

The integrated valuation/optimisation framework (IVOF)(Martinez, 2009) is a novel mine evaluation framework, which isable to account for uncertainty and risk when evaluating a mineproject. In this context, the IVOF sees the mine evaluationproblem as a multistage solution where the problem is brokendown into a set of simple building blocks. One important featureof the IVOF process is that the flexibility to close the mine projectat any production period – if operational and economic conditionsare adverse – is considered as an embedded option of theevaluation process. Accordingly, the IVOF is seen as a new

technology, which not only extends current state-of-the-art mineevaluation techniques to incorporate uncertainty and risk, but atechnology where the planning, designing and valuation of a mineproject is performed using the existing uncertainty and risk. Thatis the IVOF technology sees uncertainty and risk as allies insteadof enemies.

To solve the mine evaluation problem, the IVOF technologyuses an extension of the least-squares Monte Carlo simulation(Longstaff and Schwartz, 2001; Gamba, 2003), which consists of applying Monte Carlo simulation technique within a stochasticdynamic approach, while obeying the open pit mine productionand scheduling constraints. In this context, at each productionperiod t = {t0 = 0,t1 = ∆t,...,tT = T∆t} the value of an open pitmine project is defined as the sum of the maximum cash flow,CF

t

, generated during the production period, t and the maximumbetween the continuation value, Φt+∆t and stopping value, Πt+∆t, ie:

Vt(Qt, St) = [ ] [ ]{ }max ( , ; max , ,*

*

g t

t t t t t t CF q S g +

Φ Π (3)

where:

qt is the available ore reserves at the beginning of period, t

qt and S t are the ore production rate and the metal price,respectively

Observe in Equation 3 that the maximisation of the cash flow,

CF t , is performed in respect to an optimum cut-off grade, gt

*

.The continuation value, Φt + ∆t, is defined as the expected6 value

of the mine operation if continuing (producing) operatingthroughout period (t + ∆t ):

{ }Φ ∆ ∆ ∆ ∆t t t t t t t t t r

E V Q S S =+ + + +1

1( )( , ) ,* (4)

While the stopping value, Πt + ∆t, is defined as the sum of thesalvage value (SVal) of the mine operation obtained from sellingall real assets, such as equipment and mine/processing facilitiesand the closure costs (Clc) incurred during period (t + ∆t ), ie:

{ }Π

∆ ∆t t t t t r E SVal Clc S =

+ +

+

1

1( )( ) .* (5)

116 Melbourne, Vic, 21 - 22 April 2009 Project Evaluation Conference

L A MARTINEZ

5. It is possible to minimise the uncertainty of an orebody model bytaking samples on a very small grid. However, this procedure willresult in a non-profitable project because the high cost incurred in thedata collection.

6. In this paper, E t *{.} is the conditional expectation with respect to the

unique risk neutral probability, which can also be denoted with

E E t t * *{.} { }= ⋅ ς , where ς t is the available information at period t .

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 5/12

So, the decision rule for closing the mine project at anyproduction period is if:

Φt+∆t ≤ Πt+∆t (6)

Observe that Equations 5 and 6 uses the riskless discount rate,r , instead of the aggregated risk adjusted discount rate R > r ,which is normally used when using the DCF technique. This

feature is indeed one important property of the IVOF technology,which consists of accounting for risk at the source of uncertaintyrather than at the cash flow stage. This property can be bettervisualised in Figures 4 to 7. As observed in Figure 4, traditionaltechniques based on the DCF rely on an aggregated risk adjusteddiscount rate, R, to account for the entire uncertainty and risk of a mine project. In other words, the aggregated discount rate is the‘atlas’ holding the entire mine project performance. Since theestimation of an aggregate discount rate that accounts for theentire uncertainty and risk of a mine project is not an easy task,its estimation could result either in an overestimated discountrate that will reduce the project value (see Figure 5) or anunderestimated discount rate, which will not be able to supportthe heavy load of risk inherent in the mine project leading it to its

collapse (see Figure 6). Contrary to the DCF technique, as shownin Figure 7, the IVOF includes the technical and economic risk atthe source of uncertainty – ie at the project stage – allowing themine analyst to avoid the difficult task of estimating an

aggregated discount rate that accounts for these uncertainties. Inthis case a smaller discount rate, r free ≤ r < R, that accounts fortime value of money, represented by the risk-free discount rate,r free and other external uncertainties such as politic risk, is usedinstead. Observe that if the uncertainty of the project is resolvedin its totality, then the discount rate, r , will equal the risk freediscount rate that only accounts for the value of money over

time.The final result obtained from the IVOF process is an adjusted

or extended net present value ( ENPV ), which is composed of thesimple net present value ( NPV ) of the project, calculated withrespect to the riskless rate of return, of certainty equivalent cashflows, and the added value, FVal, resulting from all possibleoperational and managerial flexibility, such as optimising cut-off grades and closing the mine in the face of future adverseconditions. That is:

ENPV NPV FVal FVal

= + >

; 0

NPV; FVal = 0 (7)

Observe in Equation 7 that due to the value of flexibility beingdefined as the value of the option to implement a specific

Project Evaluation Conference Melbourne, Vic, 21 - 22 April 2009 117

WHY ACCOUNTING FOR UNCERTAINTY AND RISK CAN IMPROVE FINAL DECISION-MAKING

FIG 5 - Traditional mine evaluation techniques can overestimate the

discount rate, which will minimise the mine project’s value.

FIG 6 - Traditional mine evaluation techniques can underestimate

the discount rate, which will not be able to support the heavy load

of risk of a mine project, leading it to its collapse.

FIG 7 - IVOF perspective of mine project evaluation under

uncertainty and risk. In this case the estimation of the discount

rate, r (represented here as the atlas holding the entire mine

project risk), is not a difficult task since it does not account for

technical and economic risk since they are accounted at their

source of uncertainty.

FIG 4 - Traditional mine evaluation process where the aggregate

discount rate is considered as the atlas holding the entire risk and

uncertainty of a mine project.

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 6/12

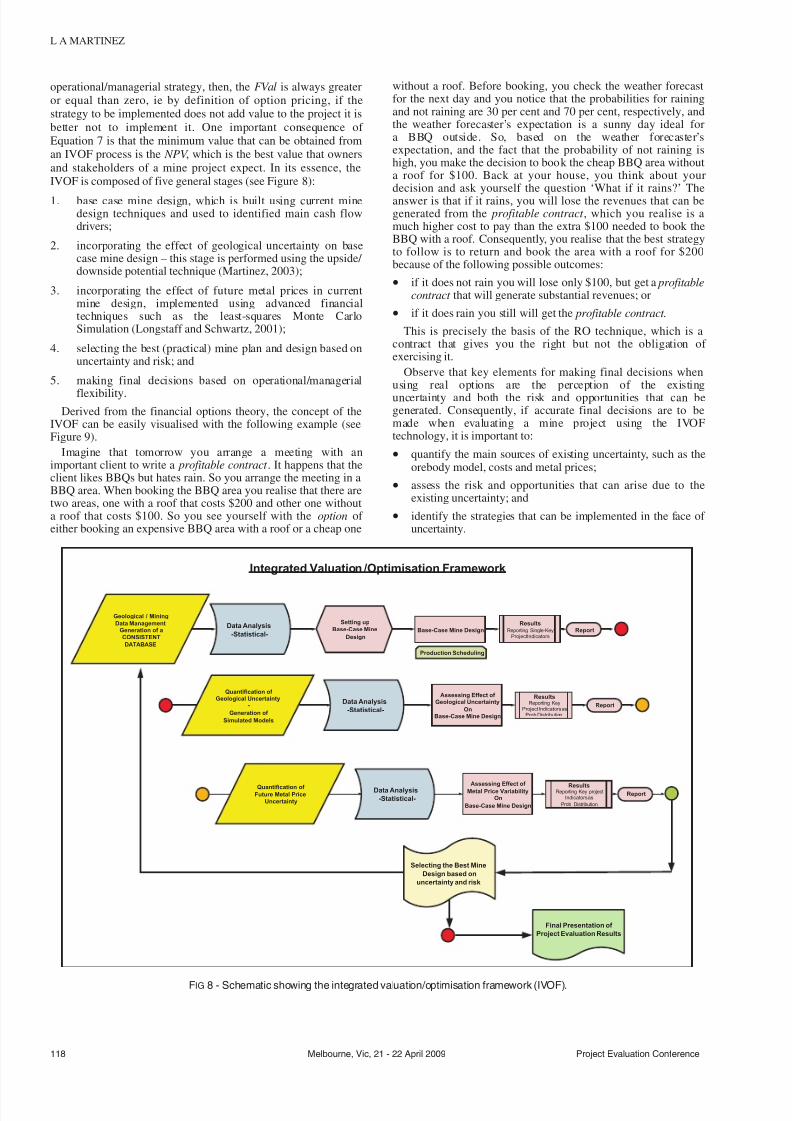

operational/managerial strategy, then, the FVal is always greateror equal than zero, ie by definition of option pricing, if thestrategy to be implemented does not add value to the project it isbetter not to implement it. One important consequence of Equation 7 is that the minimum value that can be obtained froman IVOF process is the NPV , which is the best value that ownersand stakeholders of a mine project expect. In its essence, theIVOF is composed of five general stages (see Figure 8):

1. base case mine design, which is built using current minedesign techniques and used to identified main cash flowdrivers;

2. incorporating the effect of geological uncertainty on basecase mine design – this stage is performed using the upside/ downside potential technique (Martinez, 2003);

3. incorporating the effect of future metal prices in currentmine design, implemented using advanced financialtechniques such as the least-squares Monte CarloSimulation (Longstaff and Schwartz, 2001);

4. selecting the best (practical) mine plan and design based onuncertainty and risk; and

5. making final decisions based on operational/managerial

flexibility.Derived from the financial options theory, the concept of the

IVOF can be easily visualised with the following example (seeFigure 9).

Imagine that tomorrow you arrange a meeting with animportant client to write a profitable contract . It happens that theclient likes BBQs but hates rain. So you arrange the meeting in aBBQ area. When booking the BBQ area you realise that there aretwo areas, one with a roof that costs $200 and other one withouta roof that costs $100. So you see yourself with the option of either booking an expensive BBQ area with a roof or a cheap one

without a roof. Before booking, you check the weather forecastfor the next day and you notice that the probabilities for rainingand not raining are 30 per cent and 70 per cent, respectively, andthe weather forecaster’s expectation is a sunny day ideal fora BBQ outside. So, based on the weather forecaster’sexpectation, and the fact that the probability of not raining ishigh, you make the decision to book the cheap BBQ area withouta roof for $100. Back at your house, you think about yourdecision and ask yourself the question ‘What if it rains?’ Theanswer is that if it rains, you will lose the revenues that can begenerated from the profitable contract , which you realise is amuch higher cost to pay than the extra $100 needed to book theBBQ with a roof. Consequently, you realise that the best strategyto follow is to return and book the area with a roof for $200because of the following possible outcomes:

• if it does not rain you will lose only $100, but get a profitablecontract that will generate substantial revenues; or

• if it does rain you still will get the profitable contract.

This is precisely the basis of the RO technique, which is acontract that gives you the right but not the obligation of exercising it.

Observe that key elements for making final decisions whenusing real options are the perception of the existinguncertainty and both the risk and opportunities that can begenerated. Consequently, if accurate final decisions are to bemade when evaluating a mine project using the IVOFtechnology, it is important to:

• quantify the main sources of existing uncertainty, such as theorebody model, costs and metal prices;

• assess the risk and opportunities that can arise due to theexisting uncertainty; and

• identify the strategies that can be implemented in the face of uncertainty.

118 Melbourne, Vic, 21 - 22 April 2009 Project Evaluation Conference

L A MARTINEZ

Geological / Mining

Data ManagementGeneration of a

CONSISTENT

DATABASE

Base-Case Mine DesignResults

Reporting Single-KeyProject Indicators

Quantification of Geological Uncertainty

-

Generation of

Simulated Models

Assessing Effect of Geological Uncertainty

OnBase-Case Mine Design

ResultsReporting Key

Project Indicators asProb Distribution

Quantification of Future Metal Price

Uncertainty

Assessing Effect of Metal Price Variability

On

Base-Case Mine Design

ResultsReporting Key project

Indicators as

Prob Distribution

Report

Final Presentation of

Project Evaluation Results

Integrated Valuation /Optimisation Framework

Production Scheduling

Selecting the Best Mine

Design based on

uncertainty and risk

Data Analysis

-Statistical-

Setting up

Base-Case Mine

Design

Data Analysis

-Statistical-

Data Analysis

-Statistical-

Report

Report

FIG 8 - Schematic showing the integrated valuation/optimisation framework (IVOF).

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 7/12

TWO CASE STUDIES SHOWING WHYACCOUNTING FOR RISK AND UNCERTAINTY

IMPROVE FINAL DECISION-MAKING

To show how the inclusion of uncertainty and risk can be of

benefit when evaluating a mine project, this section shows theevaluation process of two mine projects, a disseminated goldmine and a coal mine, using the IVOF technology.

The case of a gold mine project evaluation

In this section, a disseminated gold open pit mine project isplanned, designed and evaluated under geological (in situ metalgrade) and economical (metal price) uncertainties. The mainquestions that management is trying to answer are the following:

• What is the value of the mine using traditional mineevaluation techniques?

• What is the effect of both in situ metal grade variability andmetal price uncertainty on key project indicators?

• What is the effect of including the option to close the mine

project, if future economic and technical conditions areadverse, on the mine value?

As observed in Figure 10, the geological data available forthis project consists only of drill holes composite data (seeFigure 10a) that contains information about gold grades (ingrams), rock type – oxide, mixed-transitional, primary and thewallrock considered as sterile (see Figure 10b), and geotechnicalzones (composed of eight zones) (see Figure 10c). Figure 10d isshowing the variogram map used to build the estimated goldgrade orebody model using the ordinary kriging technique, asshown in Figure 10e.

The relevant financial and technical parameters available forthe evaluation process are shown in Table 1. As observed in thetable, the production period is considered to be of one year, themill capacity is 2 Mt per year and mining capacity is 9 Mt orrock per year. The expected gold price is 27.5 A$/g. Slope angles

are specified for each geotechnical zone and processing costsand recoveries are specified for each rock type. Furthermore,corporate uses a yearly risk-free discount rate of r = 5 per cent

Project Evaluation Conference Melbourne, Vic, 21 - 22 April 2009 119

WHY ACCOUNTING FOR UNCERTAINTY AND RISK CAN IMPROVE FINAL DECISION-MAKING

The opportunity to write a profitable project Humm ..Thecheap or the expensive one? The expected weather is a sunny day – the cheap one

But...WHAT IF IT RAINS? – You lose the project

Better book the expensive BBQ area with a roof: If it is either a rainy or sunny day you still have your Profitable Project.

FIG 9 - A simple explanation of the real options concept – the profitable contract signed on a BBQ area.

Parameter description Value

Assumed production period (years) 1Expected gold price (A$/g) 27.5

Expected selling cost (A$/g) 0.6875

Discount rate 12%

Time cost/peiod (A$ M) 1.5

Mill capacity/period (Mt) 2

Maximum mine capacity/period (Mt) 9

Processing cost – oxide rock (A$/t) 15.39

Processing cost – transitional rock (A$/t) 16.66

Processing cost – primary rock (A$/t) 16..9

Recovery – oxide rock 94%

Recovery – transitional rock 94%

Recovery – primary rock 90%

Slope angle – zone 1 (degrees) 52%

Slope angle – zone 2 (degrees) 57%

Slope angle – zone 3 (degrees) 50%

Slope angle – zone 4 (degrees) 48%

Slope angle – zone 5 (degrees) 45%

Slope angle – zone 6 (degrees) 50%

Slope angle – zone 7 (degrees) 55%

Slope angle – zone 8 (degrees) 60%

TABLE 1Table showing some of the financial and technical parameter

values used to evaluate the gold mine project.

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 8/12

while the real annual (WACC) adjusted discount rate is RWACC =12 per cent. Mining costs and processing costs are included inthe orebody model as varying for each production bench androck type, respectively. Additional information indicated that nostockpiles are considered in the analysis and that the requiredmining width for mining machinery is 40 m. At the end of themining operation, the corporate office has estimated a salvagevalue of A$60 M.

Figure 11 summarises the results of planning, designing andevaluating the gold mine project using traditional mineevaluation methods based on the DCF – the resulting design iscalled the base case design. As observed in the figure, the goldmine project is composed of an ultimate pit and the long-term

production scheduling, composed of four production periods. Inthis case, the Gold mine project is expected to have an operatinglife of around 3.5 years, where the mill target will be achievedduring the first 3.5 years. The mine is also expected to producearound 5.5 M, 6 M, 5 M and 3.5 M of grams of gold during thefirst, second, third and fourth year, with expected average gradesof 2.9, 3.2, 2.6 and 3.4 g/t, respectively. The results also indicatethat mining costs and selling costs are expected to be highduring the first three years (around A$30 M), with mining costsreaching a peak during the second year (A$35 M). Processingcost is seen to remain constant, around A$30 M, throughout theoperating mine life. The expected cash flows to be generated arearound A$75 M, A$65 M, A$50 M and A$40 M, for the first,

120 Melbourne, Vic, 21 - 22 April 2009 Project Evaluation Conference

L A MARTINEZ

Composite drill hole Data Rock type

Geotechnical zones

Variography

Estimated (OK) orebody

Model

(A)(B)

(C) (D)

(E)

FIG 10 - Scheme showing the available geological data: (A) east view of the gold mine project drill hole composite data set showing the

topography of the deposit (developed in Surpac™); (B) orebody model showing the oxide, transitional and primary rock types (developed in

Surpac™); (C) north-east view of the gold mine deposit showing the eight geotechnical zones (developed in Surpac™); (D) variogram

analysis performed on the gold mine deposit (Surpac™ – geostatistical tools); and (E) south-east view of the estimated gold grade orebodymodel. In this case the ordinary kriging technique (Surpac™ – geostatistical tools) was used for generating this model.

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 9/12

second, third and fourth production periods, respectively, givinga total (current) expected value of around A$230 M. A sensitivityanalysis indicates that a ±10 per cent variation in metal prices

will generate variation in the mine value to A$300 M (+10 percent) and A$200 M (-10 per cent).

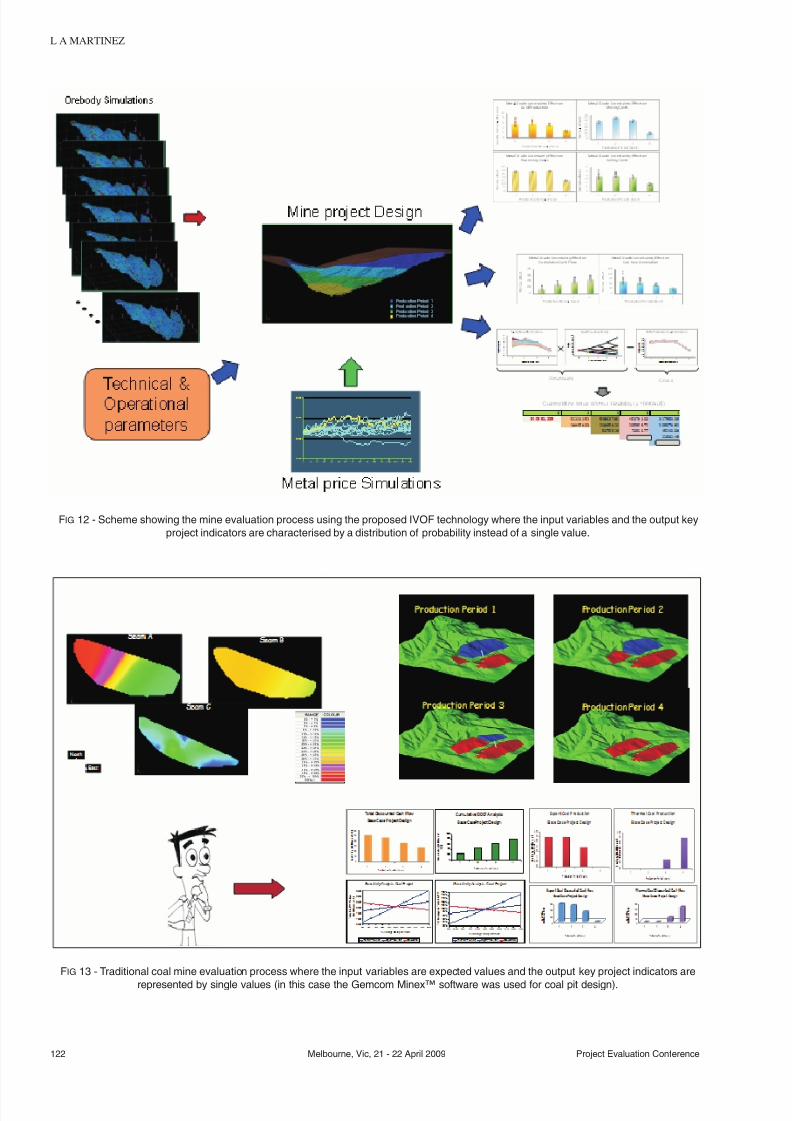

Conversely with traditional techniques, the IVOF processaccounts for the uncertainty of the input variables as well as itseffect on key project indicators (see Figure 12). In this specificcase, the in situ gold grade variability and the future gold priceuncertainty, as well as the option to close the mine if futuretechnical and economic conditions are not favourable, wereaccounted for when evaluating the gold mine project. The resultsindicate the gold mine project is likely to generate, on average, avalue of A$341 M, which is almost A$100 M more than theresults obtained from the DCF analysis. Furthermore, the resultsalso indicate that the strategy to follow is to close the mine inyear three if gold prices go down to A$11.18/g, or to close inyear four if gold prices go down to A$8.28/g.

The case of a multiseam coal mine projectevaluation

In this section, a multi (three) seam open pit coal mine project isplanned, designed and evaluated under geological (in situ ashgrade variability) and economical (coal price) uncertainties. Themain questions that management is trying to answer are thefollowing:

• What is the value of the mine using traditional mineevaluation techniques?

• What is the effect of both in situ metal grade variability andmetal price uncertainty on key project indicators?

As observed in Figure 13, the coal mine design, composed of pit limits, in-pit and out-pit dumps and production schedulingwere built using input economic data – in this case, coal prices

for thermal and export coal as well as mine and processing costsand the estimated ash variability for each seam. Similar to thegold mine project, the result of using estimates for the input

variables result in single estimates of the final project indicators,in this case coal production and cash flows.

Figure 14 shows that the inclusion of the in situ ash variability,as well as the uncertainty in future coal prices, result in thedistribution of probabilities for final project indicators such ascoal production per period and per product, ie export andthermal, as well as their respective cash flows. As shown in thefigure, the final NPV is also characterised by its distribution of probability (in this case shown as a cumulative distributionfunction) from where the mine planner is able to see therisk/potential of falling down/going up the estimated (static)mine value.

CONCLUSION

Throughout this paper, it has been shown that the mineevaluation problem is not easy to solve, but certainly notimpossible to achieve. Furthermore, this paper has shown thatwhen dealing with projects that carry uncertainty, the use of single estimates values could mislead final decision-making,turning a favourable rate of return to a project, which isotherwise doubtful or an unfavourable return for the project,which is otherwise profitable. Quantified uncertainty and risk analysis/management were shown to be powerful tools for themine analyst when evaluating a mine project in the face of uncertainty. The reason for this is that quantified uncertainty andrisk analysis give the mine planner/analyst a realistic range of thefinal outcomes, giving them the flexibility to react to either anadverse or a favourable condition and to implement the bestoperational and managerial strategy that are able to takeadvantage of the opportunities, while mitigating the risk forlosses.

Project Evaluation Conference Melbourne, Vic, 21 - 22 April 2009 121

WHY ACCOUNTING FOR UNCERTAINTY AND RISK CAN IMPROVE FINAL DECISION-MAKING

FIG 11 - Traditional mine evaluation process where the input variables are expected values and the output key project indicators are

represented by single values.

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 10/12

122 Melbourne, Vic, 21 - 22 April 2009 Project Evaluation Conference

L A MARTINEZ

FIG 12 - Scheme showing the mine evaluation process using the proposed IVOF technology where the input variables and the output key

project indicators are characterised by a distribution of probability instead of a single value.

FIG 13 - Traditional coal mine evaluation process where the input variables are expected values and the output key project indicators are

represented by single values (in this case the Gemcom Minex™ software was used for coal pit design).

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 11/12

In this context, the integrated valuation/optimisation framework (IVOF) is seen as a new technology suitable for mine projectevaluation since it integrates uncertainty and risk. One importantcharacteristic of the IVOF is that it extends existing state-of-the-art mine valuation/optimisation techniques to solve the mine

evaluation problem in a tractable and practical fashion. Oneadvantage of the IVOF is that it is a generic framework that canbe adapted to any mine project such as coal and iron ore, amongothers. Another advantage of the IVOF is that because of itstractability it can allow any optimisation process to be includedin the evaluation process.

In summary, throughout this paper it has been shown that aproject evaluation process that accounts for uncertainty and risk will deliver the following:

• an estimated value with its respective risk profile given by itsprobability distribution

• a map of the technical and economic mine project indicatorperformance where data deficient and high risk areas will beidentified (eg high-grade variability, limited geotechnical

design confidence, etc);• the ability to assess the risk and benefits of key project

interventions such as different equipment fleet, different plandesign and steeper slope angles; and

• the ability to identify and assess realistic and practicalstrategic operational and managerial decisions of mineclosure, expansion or temporal stop, among others.

The final results indicates that the incorporation of uncertaintyand risk into the mine evaluation process gives a more realisticoverview of the performance of the key mine project indicatorsthroughout its operating life and, consequently, about its currentmarket value.

A final comment is related to the importance of doing moreresearch and development for building new tools that can

account for uncertainty and risk in mine project evaluation.

Although some of the existing technology can be adapted toperform an IVOF process, currently it is not possible to performan appropriated (complete) mine project evaluation analysis dueto the lack of tools. For example, the well-accepted technologyfor open pit mine design that is based on the Lerchs-Grossmannalgorithm (Lerchs and Grossmann, 1965) deals only withdeterministic orebody models (as shown in Figure 2). All that wecan do is just adapt it to deal with a stochastic model but in aninappropriate and unpractical fashion. Another example is thelack of practical tools for dealing with multivariate stochasticprocesses, such as a multimetal mine projects.

REFERENCES

Benninga, S, 2000. Financial Modelling, 622 p (The MIT Press: London).

Camus, J P, 2002. Management of Mineral Resources – Creating Value inthe Mining Business, 107 p (Society for Mining, Metallurgy andExploration Inc: Littleton).

Case, K E and Fair, R C, 1989. Principles of Microeconomics, 610 p(Prentice-Hall: Englewood Cliffs).

Chan, N H and Wong, H Y, 2006. Simulation Techniques in Financial Risk Management , 220 p (Wiley-Interscience).

Dimitrakopoulos, R, 1998. Conditional simulation algorithms formodelling orebody uncertainty in open pit optimisation, International Journal of Surface Mining, Reclamation and Environment , 12:173-179.

Dimitrakopoulos, R, Martinez, L A and Ramazan, S, 2004. Optimisingopen pit design with simulated orebodies and Whittle Four-X: Amaximum upside/minimum downside approach, in ProceedingsOrebody Modelling and Strategic Mine Planning (eds: RDimitrakopoulos and S Ramazan), pp 243-248 (The AustralasianInstitute of Mining and Metallurgy: Melbourne).

Fanning, S and Parekh, J, 2004. Stochastic processes and theirapplications to mathematical finance, The Maryland MathematicsDepartment (working) 31 p.

Gamba, A, 2003. Real options valuation: A Monte Carlo approach,

Faculty of Management, University of Calgary (working) 40 p.

Project Evaluation Conference Melbourne, Vic, 21 - 22 April 2009 123

WHY ACCOUNTING FOR UNCERTAINTY AND RISK CAN IMPROVE FINAL DECISION-MAKING

FIG 14 - Scheme showing the coal mine evaluation process using the proposed IVOF technology, where the input variables and the output

key project indicators are characterised by a distribution of probability instead of a single value.

7/18/2019 Why accounting for uncertainty and risk can improve final.pdf

http://slidepdf.com/reader/full/why-accounting-for-uncertainty-and-risk-can-improve-finalpdf 12/12

Gentry, D W and O’Neil, T J, 1984. Mine Investment Analysis, 510 p(Society for Mining, Metallurgy and Exploration: Littleton).

Glasserman, P, 2004. Monte Carlo Methods in Financial Engineering,596 p (Springer).

Lerchs, H and Grossmann, L, 1965. Optimum design of open-pit mines,in CIM Transactions, LXVIII, pp 17-24.

Longstaff, F A and Schwartz, E, 2001. Valuing American options bysimulation: A simple least-squares approach, Review of FinancialStudies, 14:113-147.

MacAvoy, P W, 1988. Explaining Metal Prices: Economic Analysis of Markets in the 1980s and 1990s, 132 p (Kluwer Academic: Boston).

Martinez, L, 2003. Can quantification of geological risk improve open pitmine design? masters thesis (unpublished), W H Bryan MiningGeology Research Centre, The University of Queensland, Brisbane,168 p.

Martinez, L A, 2007. Orebody modelling and mine project evaluation:Estimation versus simulation – A practical viewpoint, in 33rd International Symposium on Applications of Computers and Operation Research in Mineral Industry (APCOM), Santiago, vol 1,pp 721-728.

Martinez, L A, 2009. Designing, planning and evaluating a gold mineproject under in situ metal grade and future metal price uncertainties,in Proceedings Orebody Modelling and Strategic Mine Planning(ed: R Dimitrakopoulos), pp 225-234 (The Australasian Institute of Mining and Metallurgy: Melbourne).

Rendu, J-M, 2006. Reporting mineral resources and mineral reserves inthe United States of America, in Proceedings Sixth International Mining Geology Conference (ed: S Dominy), pp 11-19 (TheAustralasian Institute of Mining Metallurgy: Melbourne).

Savage, S, 2002a. The flaw of averages, Harvard Business Review,80:20-22.

Savage, S, 2002b. Letter to the US Securities and Exchange Commission[online]. Available from:<http://www.sec.gov/rules/proposed/s71602/savage1.htm >[Accessed: 27 December 2008]

Savage, S, 2003. Decision Making with Insight , p 368 (Duxbury).

Taylor, J, Moosa, I and Cowling, B, 2000. Micro Economics, p 508 (JohnWiley & Sons).

124 Melbourne, Vic, 21 - 22 April 2009 Project Evaluation Conference

L A MARTINEZ