Embed Size (px)

Citation preview

What We Know:

The Global economy will shrink by 3% this year

Loss to GDP could amount to $9 trillion

2

GDP Growth Projections

The COVID-19 health crisis will have a severe impact on economic activity in 2020

Source: IMF, World Economic Outlook, April 2020

3

GDP Growth Projections

Source: Oxford Economics / Haver Analytics

World GDP

Global GDPQ4 2019=100

Worldwide trade will plummet 11% this year

5

Goods Trade Barometer

Source: World Trade Organization, WTO Trade Barometers, May 20, 2020

World Merchandise Trade Volume, 2000-2022

Below trend

Above trend

Most governments will be heavily indebted from expensive emergency relief measures

7

General GovernmentDebt to GDP Ratio In select OECD countries

Source: IMF

Source: Committee for a Responsible Federal Budget, Congressional Budget Office

US Debt to GDP before Coronavirus

8

Debt to GDP Ratio Forecast

NEDA Source: Committee for a Responsible Federal Budget, Congressional Budget Office

U.S. jobless claims have surpassed 40 million people

10

United States Initial Jobless Claims

Week ended May 23

Source: TRADINGECONOMICS.COM | U.S DEPARTMENT OF LABOURNEDA

11

NEDA

U.S Unemployment Rate

Source: Committee for a Responsible Federal Budget, Congressional Budget Office

Steep short-term decline in FDI

Top 5,000 MNEs which account for lion’s share of FDI: downward revisions of 2020 earnings estimates of 30% due to COVID-19. Hardest hit:

COVID-19 Impact on Global FDI

-208%Energy & basic materials

-116%Airlines

-47%Automotive Industry

-41%Hotels, Restaurants / Leisure

Source: UNCTAD, Investment Trends Monitor, March 2020

Downward pressure on FDI could be -30% to -40% during 2020-2021

COVID-19 Affects on MNEs by April, 2020

Source: World Bank Group, 2019-2020 Global Investment Competitiveness Report

14

NEDA

Continued self-isolation and depressed spending against a potential resurgence of the virus

Respondents who agree that…(%) “The worst of the coronavirus is still ahead”As of April 2020

BCG: COVID-19 BCG Perspectives, Version 8: May 8, 2020

Consumers starting to display more optimistic outlook

NEDA BCG: COVID-19 BCG Perspectives, Version: 24 April, 2020

US Consumer SentimentSome willingness to resume activities post lockdown, but not to pre-crisis level even with treatment

What We Don’t Know:

Greater protection/Reshoring of strategic supply chains and less reliance on imports

Lack of supply chain visibility

Source: BCI, 2019

Pre COVID-19 Learning:

Reshore: creation of favourable business conditions, skilled workforce and incentivesBCG Study (2002 – 2014) of major factors impacting manufacturing location decisions

• Increased wages: china’s wages rose 15-20% per year at the average Chinese factory

• Fluctuating currency value: the Chinese yuan increased in value by 35% against the USD

• Labor productivity: measured as the gains in output per manufacturing worker

• Reduction of energy costs from 2002 – 2014, especially in energy dependent industries such as iron, steel and chemicals

Historically US manufacturers struggled to maintain cost and productivity advantages

US shifted focus to complex, high-value products and industries

• Others closed US-based factories or sought cost savings by offshoring

• Shortly after China joined the WTO (2001) a large exodus of US manufacturers occurred

Supply chain dynamics have changed• By 2010 cost savings began to erode

(increases in labor and transportation costs)• Hidden costs: monitoring and QC, protection

of IP and lengthy supply chains

Potential Cumulative Reshored Jobs

Scenario Description Source Jobs

ReshoredCumulative Total Jobs

Using TCI analysis Reshoring initiative 500,000 1,000,000

If Chinese Wage Trends continue at 18% a year Boston Consulting Group 1,000,000 2,000,000

Adoption of better U.S training, increased process improvements & competitive tax rates

Federal Government’s Advanced Manufacturing Partnership 2,000,000 4,000,000

End of foreign currency manipulation Almost all manufacturing groups 3,000,000 6,000,000

Source: IEDC

22

Strategies to consider for our recovery

• Investment weary• Net Income & Revenue focus• Regionalization• Re-evaluate value chains / subsegments• Increased automation / digitization

Stakeholders know that capital investment and job creation results will be lower than expected this year.

Most Important KPI for EDOs: Adjustment to your strategy in an

efficient and effective manner?

All companiesReduction in investment and FDI

Revised EDO strategy+ =

23

Strategies to consider for our recovery - Companies• Reshoring manufacturing/supply chain• +1 sourcing strategy• Near shoring supply chain• Mitigating risk in existing supply chains / de-coupling from China• Increase in data driven and AI powered decision-making

• Massive investments in technology• Massive investment in digitization• Massive investment in skills update (Industry 4.0)• Worker productivity and output• Availability of finance

• Employee safety measures• “Work from home” is here to stay• The footprint for office real estate will change• Remote and virtual working models will proliferate

24

Strategies to consider for our recovery - EDOs

• Verify that industry and geographic targets are still viable• Re-assess your budget• Keep your stakeholders in the loop• Engage in concerted BR&E Activity• Re-visit your value proposition • Ensure that your mix of marketing collaterals are adapted to today’s reality• Strengthen cooperation

• Now is NOT the time to cease business development activities• Virtual conferences• Augmented and Virtual Reality• Digital/virtual meetings and site tours• Digital marketing• Seize new opportunities from changing FDI (huge capacity requirements

for potential reshoring)

Tracking OpportunitiesDr. Nadine Jeserich

26

Intro

Tracking growth industries,

Workforce, business planning and technology development

retain and support?create opportunities beyond 2020?

27

2020 employment by sector so far

Source: U.S Bureau of Labor Statistics.

Sectoral trends mostly well known by now –leisure/hospitality, retail

Employment change by industry, April 2020, seasonally adjusted, 3 month net change

28

Manufacturing production trendsIndustry Group NAICS MAR-APR

2020APR ‘19-APR’20

Natural gas 2212 10.7 11.1COVID Computer and electronic products 334 -5 0.2COVID Paper 322 -2.6 -1.5MIXED Electrical equipment, appliances, and components 335 -6 -5.4MIXED Food, beverage, and tobacco products 311.2 -7.1 -6.7MIXED Electric 2211 -3.3 -6.7MIXED Mining 21 -6.1 -7.5MIXED Chemicals 325 -5.1 -7.7MIXED Wood products 321 -9 -7.9MIXED Plastics and rubber products 326 -11 -13.2MIXED Machinery 333 -11 -14.4MIXED Fabricated metal products 332 -11.3 -14.9RISK Nonmetallic mineral products 327 -16.3 -18.5RISK Petroleum and coal products 324 -18.5 -22.1RISK Furniture and related products 337 -20.6 -24.5RISK Primary metals 331 -20.4 -27RISK Printing and support 323 -21.2 -27.6RISK Textile and product mills 313.4 -20.7 -28.7RISK Apparel and leather 315.6 -24.1 -34.5RISK Aerospace and miscellaneous transportation equipment 3364-9 -21.6 -34.9RISK Motor vehicles and parts 3361-3 -71.7 -79.3

••

•

Source: US Census Bureau, Industrial production index

29

Niche sectors that have fared well through 2019 and so far into 2020

IT – research – consulting – training⁃ Software⁃ Data processing⁃ Internet publishing⁃ Customer computer programming services / 5415⁃ Management and human resource consulting⁃ R&D⁃ Marketing research⁃ Business, computer, and management training 6114

Medical devices / supplies and pharma

Plastic products

Packaged nonperishablefood and snacks

Computer & peripheralequipment, wireless equipment

30

Supply chain strength

March supply chain disruptions were being reported in 9% 17% 24% 38%

North America Japan & Korea Europe China(9% for U.S. supply chains,

6% for supply chains elsewhere in North America)

of respondents each of respondents of respondents

Source: Institute for Supply Management

31

Trickle effects of foreign supply chain collapses:

TOTAL $347.3 BILLION

Primary sources of intermediate goods for the US

Source: USITC

Canada18%

China10%

Mexico7%

Ireland7%

Japan5%

Germany5%

Other48%

32

Extent of reliance on international supply chains

Share of foreign value added in electronics exports was around 10% for the United States,

companies came to a standstill!

33

And not just electronics

Source: OECD TiVA, Bloomberg Economics

A dependency on China manufacturing and/or Chinese suppliers

• Vulnerability ranges across industry sectors example - China sourcing viewpoint Electronics & electrical is likely the highest risk sector globally

Source: BCG, 2020

35

Likelihood of Reshoring Due to Coronavirus Outbreak

54% of respondents chose Likely, Very Likely or Extremely Likelyoptions on reshoring.

Source: Thomas Industrial Survey (n-1,073)

36

Reshoring trends

⁃ 2018 Tariff impacts prepared some industries and companies

⁃ Some imports were shifted to other South-East Asia locations: Furniture/Toys

⁃ Others to Canada and Mexico: chemicals, metals, car parts

Source: USTIC; The Economist

Change in share of US imports between Jul-Dec 2017 and Jul-Dec 2019, percentage points

37

Reshoring Interest by IndustryLikely to Extremely Likely to Reshore Production/Sourcing

Source: ThomasNet April 2020 COVID-19’s Impact on North American Manufacturers

38

Reshoring destinations

Most likely reshoring destination: Pennsylvania, Wisconsin, Texas

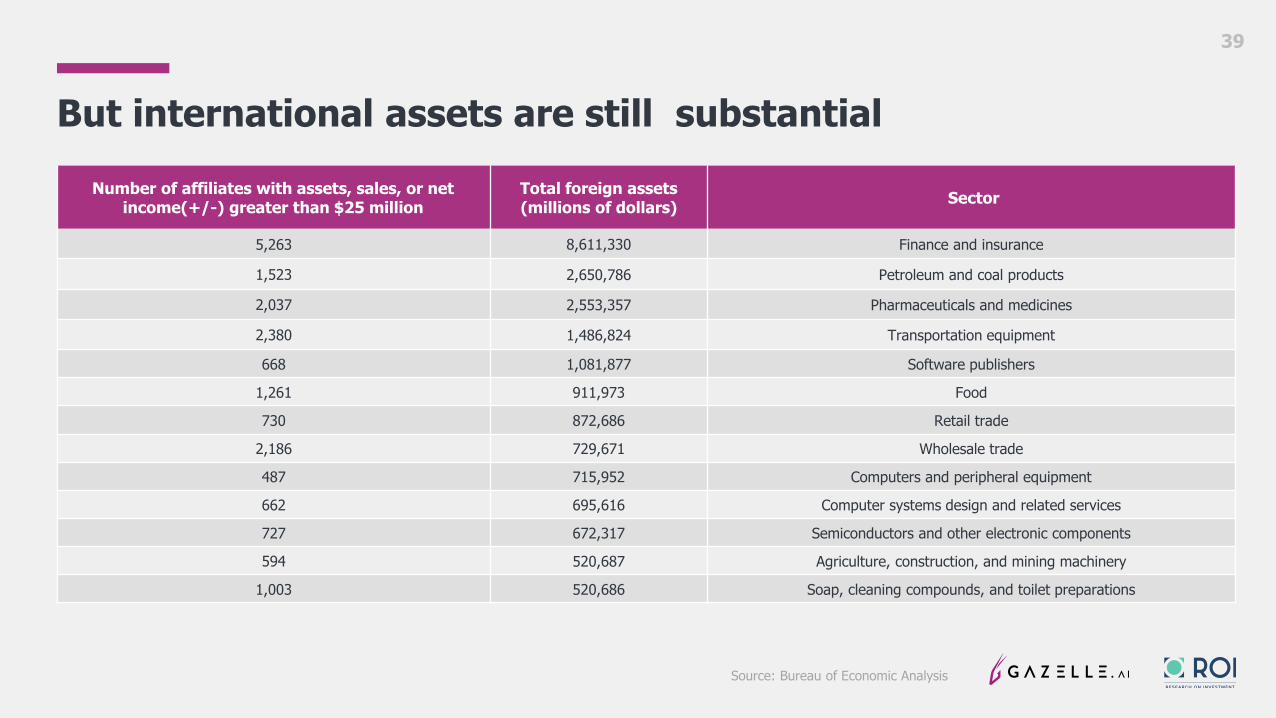

39

But international assets are still substantialNumber of affiliates with assets, sales, or net

income(+/-) greater than $25 millionTotal foreign assets(millions of dollars) Sector

5,263 8,611,330 Finance and insurance

1,523 2,650,786 Petroleum and coal products

2,037 2,553,357 Pharmaceuticals and medicines

2,380 1,486,824 Transportation equipment

668 1,081,877 Software publishers

1,261 911,973 Food

730 872,686 Retail trade

2,186 729,671 Wholesale trade

487 715,952 Computers and peripheral equipment

662 695,616 Computer systems design and related services

727 672,317 Semiconductors and other electronic components

594 520,687 Agriculture, construction, and mining machinery

1,003 520,686 Soap, cleaning compounds, and toilet preparations

Source: Bureau of Economic Analysis

40

Accelerating technologies

Those part of new normal and technology acceleration

• Distancing measures & reshoring trends = automation & robotics & AI/cloud computing needs• Remote work becoming permanent part of the economy• Health IT

41

Top Sectors for VC investment, 2017-Q1 2020

Source: PwC / CB insights MoneytreeTM Report Q1 2020

Bottom lineOpportunities Potential Risk

Medtech Transportation & Logistics Airlines

Pharma/Biotech High-tech Leisure/tourism

Online retail Machinery & Equipment Automotive

Software/AI/IT Consumer Electronics Offline retail

Online platforms Construction Energy & chemicals

Telecom services Plastics Apparel

Automation Wood

Aerospace

Defense

43

NEDA competitiveness

Where does theNorth east fit in?

NEDA

NEDA Economic Situation – Unemployment Claims

Unemployment Compensation Claims as a Percentage of the Civilian Workforce

⁃ Initial and Continuing Regular Unemployment Claims as a Percentage of the Civilian Labor Force, May 23, 2020

Source: Tax Foundation

NEDA

NEDA Economic Situation -Business Applications w Planned Wages

46

NEDA competitiveness• Widespread expertise

in Electronic components / Communications equipment

• => Robotics / automation / IoT => including upgrading Warehousing and distribution as a key distribution hub for the US

Supplier dense regions Integrator employment Supplier employment

Columbus, OH 358 4993

New York-Newark-Jersey City, NY-NJ-PA 121 1071

San Jose-Sunnyvale-Santa Clara, CA 76 580

Boston-Cambridge-Newton, MA-NH 287 1781

Grand Rapids-Wyoming, MI 389 2123

Birmingham-Hoover, AL 81 250

Pittsburgh, PA 190 525

Los Angeles-Long Beach-Anaheim, CA 564 949

Minneapolis-St. Paul-Bloomington, MN-WI 849 1416

Dallas-Fort Worth-Arlington, TX 152 228

Philadelphia-Camden-Wilmingon, PA-NJ-DE-MD 254 356

Source: Leigh & Kraft, Regional Studies vol. 52(2018)

47

Metalworking : custom/contract manufacturing – the supply chain for all manufacturing!Companies look for regional with manufacturing history and skilled trades and robust upskilling and automation programs

Source: Gazelle.ai

California19%

New York8%

Michigan7%

Ohio6%

New Jersey 6%Pennsylvania

6%Texas4%

Massachusetts4%

Florida4%

Connecticut4%

Illinois4%

Other28% Precision Manufacturing

Hubs

48

Reshoring opportunities

Transportation access

Ecosystem:of course

Skilled workforce: was often a reason for moving abroad

Have to be cost effective: competitive labor, real estate/construction costs, low-cost electricity

Pharma& medical device hotspots

Nationalhotspotsfor lifesciencesR&D

51

But cost competitive alternative

0 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000 7,000,000 8,000,000 9,000,000 10,000,000

New YorkTexas

CaliforniaWashington

MassachusettsNew Jersey

FloridaIllinois

PennsylvaniaVermontColorado

ConnecticutNorth Carolina

MinnesotaMaryland

New HampshireMaine

DelawareRhode Island

Indiana

Property & Utility Costs for Typical Biopharma Project

Property Utility

Project: 350 employee, 247,570 ft² of Industrial space, 24,757 ft² of Office space

Source: fDibenchmark

52

Accelerating technologies

• Education⁃ remote learning software⁃ virtual training⁃ lots of startup opportunities not just for big cities

post-secondary education hubs are in the Northeast based on job shares

7/10 statesTOP Edtech Ecosystems to Watch

Source: Startup Genome

53

NEDA competitiveness

• Fit of targets with local communities• Carve out subsectors most suitable but play into regional strength and story• And pursuing sectors that will be relevant to a wider cross-section of

regional communities • More diversified economies are always more resilient!

Economic RecoveryKirsten McGregor, Principal SAGAX Associates, LLC

55

Phases of Recovery

1.2.3.4.5.

56

Disruption & Response

• Solving the Immediate Impacts

• Focus on the responding to the disruption

• Ongoing simultaneously with COVID 19

• Set the foundation for Recovery

57

Intermediate & Long-Term Recovery

• Initiatives • Events • Policies• Strategies• Plans

58

Building Recovery Capacity

• Sustainable & Transparent Oversight• Subject Matter Experts• Dedicated interagency recovery staff• Coordination for all levels of government• Stakeholder engagement

59

Economic Impact Assessment

• Required for most grant applications • Preexisting Vulnerabilities• Disruption Impact assessments• Quantitative Data• Qualitative Data

60

FundingInvestment Priorities

• Priority Projects• Federal Funding• Leveraging Resources• State and Local Funding• Philanthropic Resources• Tracking Funding

(Grants Management)

Strategy• Priority Projects• Coordinated Approach• Champion• Appropriate Resources• Grant Applications

Leveraging Resources• State and Local Funding• Philanthropic Funding• COVID Federal

Appropriations• Non-COVID Federal Funding

61

Recovery Action Plans & Strategies • Start with an Action Plan to identify your top

economic recovery concerns and develop a road map for solutions

• Continue to support your community with initiatives and evolving policies during the recovery process

• Encourage clear and coordinated messaging • Develop a coordinated and updated economic

vision• Create a recovery strategy that provides in-depth

analysis and long-term inter-coordinated

QUESTIONS?