Embed Size (px)

Citation preview

A special information featureMonday, October 4, 2010 • THE GLOBE AND MAIL FPSC1

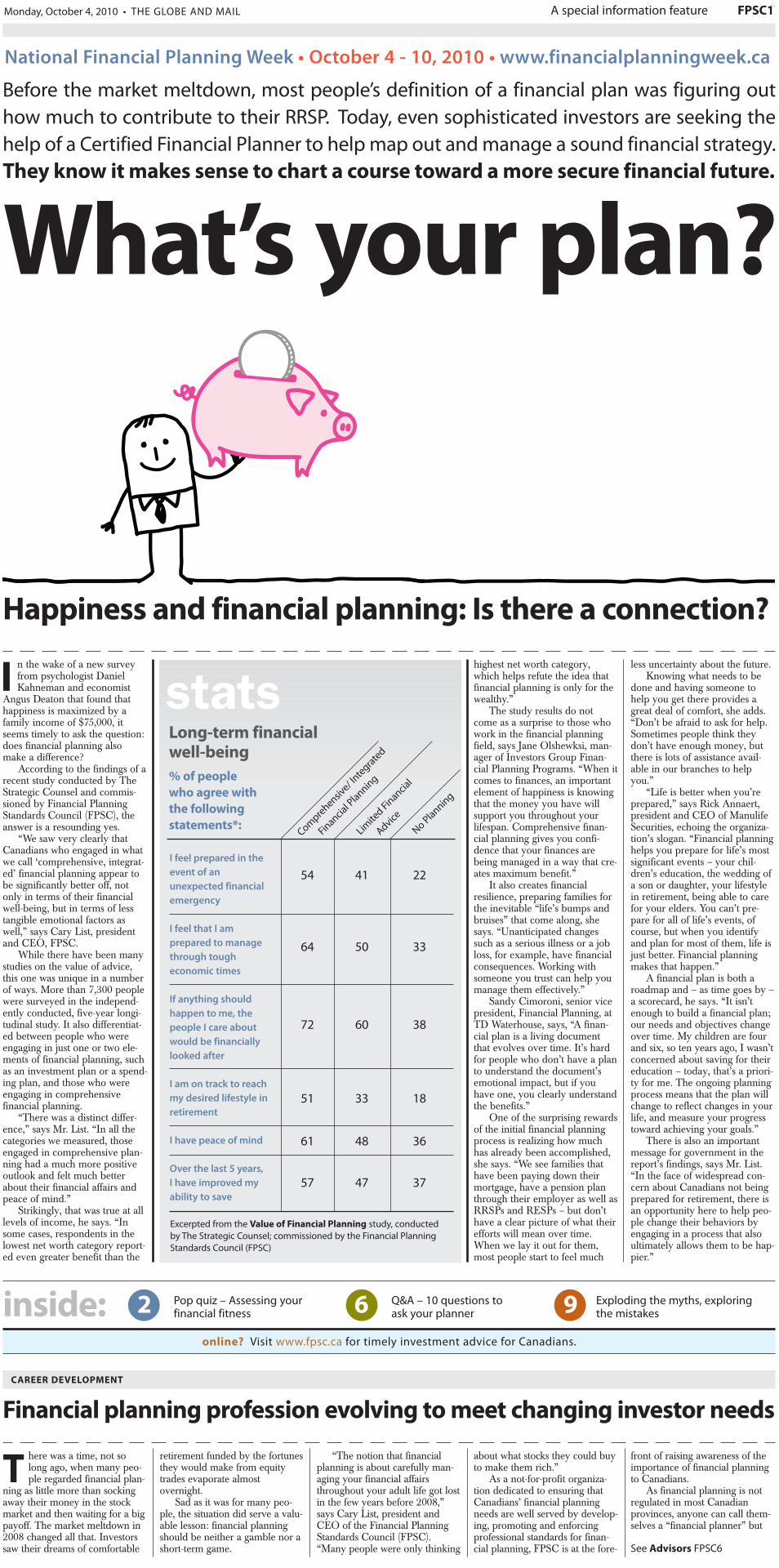

I n the wake of a new surveyfrom psychologist DanielKahneman and economist

Angus Deaton that found thathappiness is maximized by afamily income of $75,000, itseems timely to ask the question:does financial planning alsomake a difference?

According to the findings of arecent study conducted by TheStrategic Counsel and commis-sioned by Financial PlanningStandards Council (FPSC), theanswer is a resounding yes.

“We saw very clearly thatCanadians who engaged in whatwe call ‘comprehensive, integrat-ed’ financial planning appear tobe significantly better off, notonly in terms of their financialwell-being, but in terms of lesstangible emotional factors aswell,” says Cary List, presidentand CEO, FPSC.

While there have been manystudies on the value of advice,this one was unique in a numberof ways. More than 7,300 peoplewere surveyed in the independ-ently conducted, five-year longi-tudinal study. It also differentiat-ed between people who wereengaging in just one or two ele-ments of financial planning, suchas an investment plan or a spend-ing plan, and those who wereengaging in comprehensivefinancial planning.

“There was a distinct differ-ence,” says Mr. List. “In all thecategories we measured, thoseengaged in comprehensive plan-ning had a much more positiveoutlook and felt much betterabout their financial affairs andpeace of mind.”

Strikingly, that was true at alllevels of income, he says. “Insome cases, respondents in thelowest net worth category report-ed even greater benefit than the

highest net worth category,which helps refute the idea thatfinancial planning is only for thewealthy.”

The study results do notcome as a surprise to those whowork in the financial planningfield, says Jane Olshewksi, man-ager of Investors Group Finan-cial Planning Programs. “When itcomes to finances, an importantelement of happiness is knowingthat the money you have willsupport you throughout yourlifespan. Comprehensive finan-cial planning gives you confi-dence that your finances arebeing managed in a way that cre-ates maximum benefit.”

It also creates financialresilience, preparing families forthe inevitable “life’s bumps andbruises” that come along, shesays. “Unanticipated changessuch as a serious illness or a jobloss, for example, have financialconsequences. Working withsomeone you trust can help youmanage them effectively.”

Sandy Cimoroni, senior vicepresident, Financial Planning, atTD Waterhouse, says, “A finan-cial plan is a living documentthat evolves over time. It’s hardfor people who don’t have a planto understand the document’semotional impact, but if youhave one, you clearly understandthe benefits.”

One of the surprising rewardsof the initial financial planningprocess is realizing how muchhas already been accomplished,she says. “We see families thathave been paying down theirmortgage, have a pension planthrough their employer as well asRRSPs and RESPs – but don’thave a clear picture of what theirefforts will mean over time.When we lay it out for them,most people start to feel much

less uncertainty about the future.Knowing what needs to be

done and having someone tohelp you get there provides agreat deal of comfort, she adds.“Don’t be afraid to ask for help.Sometimes people think theydon’t have enough money, butthere is lots of assistance avail-able in our branches to helpyou.”

“Life is better when you’reprepared,” says Rick Annaert,president and CEO of ManulifeSecurities, echoing the organiza-tion’s slogan. “Financial planninghelps you prepare for life’s mostsignificant events – your chil-dren’s education, the wedding ofa son or daughter, your lifestylein retirement, being able to carefor your elders. You can’t pre-pare for all of life’s events, ofcourse, but when you identifyand plan for most of them, life isjust better. Financial planningmakes that happen.”

A financial plan is both aroadmap and – as time goes by –a scorecard, he says. “It isn’tenough to build a financial plan;our needs and objectives changeover time. My children are fourand six, so ten years ago, I wasn’tconcerned about saving for theireducation – today, that’s a priori-ty for me. The ongoing planningprocess means that the plan willchange to reflect changes in yourlife, and measure your progresstoward achieving your goals.”

There is also an importantmessage for government in thereport’s findings, says Mr. List.“In the face of widespread con-cern about Canadians not beingprepared for retirement, there isan opportunity here to help peo-ple change their behaviors byengaging in a process that alsoultimately allows them to be hap-pier.”

T here was a time, not solong ago, when many peo-ple regarded financial plan-

ning as little more than sockingaway their money in the stockmarket and then waiting for a bigpayoff. The market meltdown in2008 changed all that. Investorssaw their dreams of comfortable

retirement funded by the fortunesthey would make from equitytrades evaporate almostovernight.

Sad as it was for many peo-ple, the situation did serve a valu-able lesson: financial planningshould be neither a gamble nor ashort-term game.

“The notion that financialplanning is about carefully man-aging your financial affairsthroughout your adult life got lostin the few years before 2008,”says Cary List, president andCEO of the Financial PlanningStandards Council (FPSC).“Many people were only thinking

about what stocks they could buyto make them rich.”

As a not-for-profit organiza-tion dedicated to ensuring thatCanadians’ financial planningneeds are well served by develop-ing, promoting and enforcingprofessional standards for finan-cial planning, FPSC is at the fore-

front of raising awareness of theimportance of financial planningto Canadians.

As financial planning is notregulated in most Canadianprovinces, anyone can call them-selves a “financial planner” but

Long-term financialwell-being%of peoplewho agree withthe followingstatements*:

Excerpted from the Value of Financial Planning study, conductedby The Strategic Counsel; commissioned by the Financial PlanningStandards Council (FPSC)

online? Visit www.fpsc.ca for timely investment advice for Canadians.

I feel prepared in theevent of anunexpected financialemergency

I feel that I amprepared to managethrough tougheconomic times

If anything shouldhappen to me, thepeople I care aboutwould be financiallylooked after

I am on track to reachmy desired lifestyle inretirement

I have peace of mind

Over the last 5 years,I have improved myability to save

54 41 22

64 50 33

72 60 38

51 33 18

61 48 36

57 47 37

Comprehensive/Integrated

Financial Planning

Limited Financial

Advice

NoPlanning

stats

What’s your plan?

National Financial Planning Week • October 4 - 10, 2010 • www.financialplanningweek.ca

Financial planning profession evolving tomeet changing investor needs

Happiness and financial planning: Is there a connection?

inside: 2 6 9Q&A – 10 questions toask your planner

Exploding the myths, exploringthe mistakes

Pop quiz – Assessing yourfinancial fitness

CAREER DEVELOPMENT

See Advisors FPSC6

Before the market meltdown, most people’s definition of a financial plan was figuring outhow much to contribute to their RRSP. Today, even sophisticated investors are seeking thehelp of a Certified Financial Planner to helpmap out andmanage a sound financial strategy.They know itmakes sense to chart a course toward amore secure financial future.

G

A special information feature Monday, October 4, 2010 • THE GLOBE AND MAILFPSC2

A ccording to experts, get-ting your finances inorder can have a positive

effect on your stress levels, emo-tional well-being and social life.

Yet fewer than two in 10Canadians have worked with aprofessional to create a compre-hensive financial plan thataddresses their retirement, invest-ment, insurance, financial man-agement, estate and tax planningneeds.

The following tips can helpindividuals get their financialplans on a positive track.

Meet Your Life Goals, HavePeace of Mind, Feel Content.In a recent survey conducted byFinancial Planning StandardsCouncil, people with compre-hensive financial plans said they:

• Feel confident about theirretirement

• Feel they can take the vacationthey want, every year

• Have peace of mind• Feel content about the way

their life is going• Feel able to help family

members in times ofemergencies

Working with a certified pro-fessional to create a financialplan will give you unique strate-gies that may bring you closer toaccomplishing your life goals.And remember, a financial planisn’t about depriving yourself!It’s about balancing today’swants and needs with tomor-row’s demands – whatever they

Financial Planning Standards Council (FPSC) is a not-for-profitorganization dedicated to ensuring Canadians’ financial plan-ning needs are well served by developing, promoting andenforcing professional standards for financial planners, throughCFP certification, and raising awareness of the importance offinancial planning to Canadians.

FPSC licenses the Certified Financial Planner marks in Cana-da. With 18,000 licensed CFP professionals to date, FPSC is theforemost authority for the financial planning profession inCanada (in association with the IQPF in Quebec), continually

developing, delivering and enforcing the highest competenceand ethical standards. There are more than 117,000 individualswho have earned CFP certification in 23 countries around theworld.

Throughout its 13-year history and even now, FPSC continuesto face new challenges and adapt to the needs of Canadians:revising its governance structure, updating the CFP certificationprogram, establishing a national Financial PlanningWeek andworking with like-minded organizations to further mutuallybeneficial objectives.

pop quiz

This report was produced by RandallAnthony Communications Inc. (www.randallanthony.com) in conjunction with the advertising department of The Globe and Mail. Richard Deacon, National Business Development Manager, [email protected].

A financial plan starts by lookingat how you feel about yourmoney

How’s your financial fitness?

About FPSC

Take this short quiz now! Agree Disagree Not Sure

National Financial Planning Week • October 4 - 10, 2010 • www.financialplanningweek.ca

I rarely have problems meeting mymonthly financial obligations

I don’t worry about my financialsituation

I think I will be able to retire in thelifestyle I want

I feel I can take an annual vacation

I’m confident I can help my familyfinancially in emergencies

I feel on track to accomplishing thelife goals that are important to me

fpsc.ca

83% of Canadians with acomprehensive financial planfeel in control of their finances.

It’s the value of professional advice.

CFP®, CERTIFIED FINANCIAL PLANNER® and are trademarks owned outside the U.S. by Financial PlanningStandards Board Ltd. (FPSB). Financial Planning Standards Council is the marks licensing authority for the CFPmarks in Canada through agreement with FPSB. ©2010 Financial Planning Standards Council. All rights reserved.Statistics from FPSC’s Value of Financial Planning study, 2010. Copyright 2010 Financial Planning Standards Council. All rights reserved.

it’s time to get over‘‘getting by’’

A special information featureMonday, October 4, 2010 • THE GLOBE AND MAIL FPSC3

Q&A with Cary ListPresident and CEO,Financial Planning StandardsCouncil

A s the most influential stan-dards-setting body forfinancial planners, Finan-

cial Planning Standards Council(FPSC) stands at the forefront ofthe financial services industry.President and CEO Cary Listtalks about the council’s visionfor the future and its responsibili-ty for helping shape the financiallives of Canadians.

What role does FPSC play inprotecting and serving thepublic interest?Created in 1995 to professional-ize the financial industry and

impose rigorous ethical standards,we provide voluntary certificationto the financial planning commu-nity. We also monitor and disci-pline our members, serving bothas a regulator and ombudsmanon behalf of Canadians.

Currently, of the roughly70,000 active financial advisors in

Canada, almost 18,000 havereceived FPSC training and certi-fication. Each of these can legiti-mately call themselves financialplanners since they are qualifiedthrough a professional designa-tion, namely the Certified Finan-cial Planner® (CFP) certification.

It is this designation that setsCFP professionals apart from allother individuals holding them-selves out as financial advisors.

And obtaining this designationis no easy feat. Successful candi-dates must pass a rigorous seriesof lessons and exams, coveringthe technical, practical and ethical

aspects of financial planning.

What is one thing Canadiansneed to know about the finan-cial planning landscape inCanada?That it is fragmented, with toomany advisors claiming to besomething they are not. Yet,

despite this, we could still beentering a golden age for finan-cial planning.

The regulatory environmentmust recognize that financialplanning is separate and distinctfrom product-based advice. Thiswill help the financial industry asa whole, as well as its clients, tosupport and value comprehensiveplanning so that it can be integralto Canadians’ lives.

What is the biggest differencebetween an advisor who iscertified and one who is not?Because financial planning is stilla relatively new profession, thereare a lot of good advisors who arequalified but are not certified. Wewould like to change that.

One of the easiest thingsCanadians can do is to develop a

better understanding of creden-tials and licences of their advi-sors, as well as their approach,their values and commitment toprofessionalism.

By seeking out someone whohas earned CFP certification,you’re at least getting that extralayer of protection and assurance

that comes with an enhancedlevel of qualification.

That means an experiencedprofessional who has voluntarilystepped up to a higher standard,has agreed to be held account-able by an external third partyand is required to abide by estab-lished standards of practice and acode of ethics.

Why do you feel that financialplanning is so important toCanadians?I think there’s a great misconcep-tion that financial planning is justabout getting sound investmentadvice. It’s really much morethan that.

By accepting a piecemealapproach to financial planning,with the idea that doing some-thing is better than nothing, I’d

argue that Canadians are actuallyshort changing themselves.

Our research indicates thatthe benefits of financial planningare much more than simply theaccumulation of wealth. There isreal empirical evidence thatCanadians who engage in finan-cial planning are far better off

than those who don’t.Clients who utilize this type

of wide-ranging planning tend tohave a more optimistic outlookand are much more confidentwhen it comes to reaching theirgoals.

At the same time, advisorswho provide comprehensivefinancial planning have strongerrelationships, characterized byimproved levels of engagement,with their clients.

What then should Canadiansbe doing to improve theirfinancial literacy?Get started, right now.

Managing money is a life skillas important as language, readingand arithmetic. It is far easier toshape sound financial behaviourearlier in life than to try to

change it later on.Canadians of all ages need to

talk to CFP professionals in theircommunities about how effectiveplanning can help them makeresponsible financial decisionsthat balance today’s needs anddesires with tomorrow’sdemands.

Canadians benefit fromunderstanding thevalue of financial planning

National Financial Planning Week • October 4 - 10, 2010 • www.financialplanningweek.ca

...the benefits of financial planning are much more than simply the accumulation of wealth.There is real empirical evidence that Canadians who engage in financial planning are far betteroff than those who don’t. Clients who utilize this type of wide-ranging planning tend to have amore optimistic outlook and are much more confident when it comes to reaching their goals.

Investors Group mutual funds are available for purchase only through Investors Group Financial Services Inc. (a financial services firm in Québec) or Investors Group Securities Inc. (a financial planning firm in Québec),the principal distributors of Investors Group mutual funds. TM Trademarks owned by IGM Financial Inc. and licensed to its subsidiary corporations.

Visit www.investorsgroup.com orVisit www.investorsgroup.com orcallcall 1-888888-746746-63446344 to find an office near you.to find an office near you.

ALBERTAAlexandropoulos, NickAn, ThomasBaillie, GailBarr, RyanBaylis, KarenBeck, JordanBeler, PaulBerges, BlakeBey, ScottBidyk, KeithBilyk, AdamBrooks, DanaBuryn, BarbaraBylsma, RichardCadman, AmyCameron, BrendonCampbell, AnneCampbell, IreneCarreiro, Maria RoseChen, Guo HuaChiwetelu, RolandChoi, Young SukChong, HildyChrones, GeorgeClark, BrianCole, RobertCooper, DarrenCopot, ChristopherCrosland, KeithDe Weerd, JasonDean, BrookeDeRosa, DarrenDing, DerekDoerksen, KelleyDoyle, BenjaminDrouillard, AndreDupuis, ShawnDushenski, DelilahEgey-Samu, AronElkadri, MohammedEresman, JoelFarkas, BritniFeigs, ThomasFirth, MelissaFoff, PatrikFong, JennaForrest, ChristopherFriesen, ChristopherGagnon, JustinGee, MichaelGervais, ThomasGhuman, ShivcharanGiese, GregoryGiese, NinaGill, NicholasGolebiewski, WojtekGouliquer, JasminGraham, LanceHackman, ChelseaHarrison, MichaelHart, StephanieHeisler, NicolaHenry, JenniferHetherington, JenniferHilborn, JamesHolden, ScottHolz, GeorgeHosein, JoshuaHowell, BlairHowell, PrestonHsieh, Hui-WenInglis, EvanIppolito, Christopher

Jewell, RyanJohnson, JeanKakkar, PragyaKam, Wei TaoKellock, RayeleneKnorr, TarynKorte, ChrisKoshman, ChristinaKozakiewicz, AdamKruzel, DeniseLafitte, MikeLavers, PamLazzer, AndreaLeavitt, KennethLee, KathleenLin, AliceLittman, MyronLough, VictorLowry, ClarkMacDonald, StephenMacKenzie, AlexMahmood, AzharMalcolm, MichelleMamchur, MichaelMartin, MichaelMcCarville, ChristineMcKnight, BryceMead, GlenMejilla, Adam-OscarMelnyk, BrockMiller, GarryMoore, TaraMoulds, DavidMusic, KristinNadeau, WandaNessel, RobertNicoll, DerekOlsen, DaniellePalynchuk, KathrynParhar, DaneshPark, AlicePark, StephenPflanz, PaulPidhirniak, MichaelPilling, DavidPollock, ScottPower, PaulQuartly, DarcyRavndahl, SeanRawles, ChristopherReason, ErnestReid, SarahRichardson, JeremiahRietveld, LindaRobertson, BradleyRobertson, DonaldRobertson, ScottRupprecht, JoelSabey, ChristopherSabey, DahlinSaltykova, ValerieSanftleben, AmberSaulit, MarnieScherf, GregorySchonewille, JonathanSeitz, TheresaSharma, VinodShipley-Strickland, JulieShkwarok, ChristopherSidhu, RavinderSimcoe, SteveSmith, BrysonSpasova, PavlinaSteinman, Benjamin

Stier, RobinSwystun, SherriTaimuri, RoxanaThong, AlTraynor, JasonTrompetter, MichaelTrynchuk, Cheryl-LeeTucker, JosephVerma, AmitVoong, ShawnWachter, JensWagner, JosephWalbergs, ScottWan, DanielWard, JonathanWeir, KentWhite, KevinWilhelm, KimWilliams-Moir, ColleenWillmer, AshleyWoolley, GeorgeYam, MonaYetman, MaryGailZadrey, RaymondZhao, Siyang

BRITISH COLUMBIAAnders, DanAndersen, ShaneAng, CarmenAppelle, RobertArneja, NaveenArntson, DeneanArruda, LuciaAstaneh, EhsanBaker, SeanBaldonero, NadiaBarker, JohnBeckett, MatthewBehan, DonaldBensimhon, MikeBerg, GaryBerry, MarcusBessie, CraigBisset-Covaneiro, PhilipBoyd, Timothy ScottBrazier, BritaBrodie, CarlBuie, MatthewCalderwood, DarinCallaghan, MurrayCampos, ChristopherCastonguay, TomChan, Shirley Suk YeeChang, Yun JuiCharbonneau, SimoneCheetham, PaulChen, LinsonCheng, KuanCheng, XiCheng, Xu XiaCheung, RegineChou, PhillipChow, EdmondChow, RobertChu, MichaelClements, KevinCoburn, WilliamCook, JennaCorpuz, RyanCraig, DevinCrompton, StephenCutler, Michael

Deol, ShivDhillon, PrabhjotDhillon, SarahDiardichuk, DarrylDiep, HollyDiep, JamesDimter, MathiasDong, Jingru CynthiaDosanjh, StevenDykstra, DevonEdge, PeterErez, MichaelEsmail, KarimFairbotham, JamesFan, KaiFang, MingFarrow, IanFavaro, MichaelFerguson, JasonFitch, JonathanFleenor, BrandonFuller, SimonFung, EstherFung, KennyGandhi, MehulGangnes, JayGao, April Hong YangGibbons, AaronGilani, NaheedGleeson, PaulGlougie, JonathonGreen, AbbieHall, GeoffHansen, WayneHo, Kevin FrancisHodges, MikeHong, JeehoonHsieh, I-chen (Jenny)Hsu, GraceHuntley, DarrenHuston, DeanJansen, KirstenJefferson, LancelotJelic, JohnnyJohnston, BlaineJohnston, JohnJones, RichardJones, TammyJudd, StephenKang, XiuKastens, RainerKhakoo, AlykhanKidd, SusanKleinschmidt, TimKruchen, MariaLai, Kinson Kam HoLam, KelvinLatimer, RochelleLe, MichelleLeach, BobbieLee, Jae IkLepicq, BrianLeung, Hoi Yee FloraLewis, RachelLi, JieLi, MengLi, NanLi, Pak Yin WilliamLin, AdelineLin, Chao NanLin, WeiLong, StephenLouttit, StacieLuk, Alex

Lukawesky, StacyLumb, ThomasMacDougall, LyleMaddin, LauraMadokoro, TimothyMadunic, JosieMak, AuthranMarkham, TomMcEachen, RyanMcFadden, BryceMcQueen, DerekMeehan, Anne MarieMeisner, JoanneMiao, JingMoore-McCourt, TerryMurphy, PeterMurray, WilliamMutka, DavidNemec, JakobNg, KelvinNg, OI-ManNguyen, ChiNowak, MatthewNurani, LailaOkino, StaceyOuspenskaia, KseniaPalmer, CharlesPang, JacobPaquette, GarrettParikh, Madhuri (Margie)Patterson, ChristopherPeterson, KimPonte, RandyPregelj, StefanPresland, CarlRae-Arthur, LeslieRebagliati, RichardRedcliffe, ChrisReimer, JeannetteReynolds, TimothyRhee, DonaldRichmond, JamesRimell, DanielRoberts, KeithRockwell, MichaelRoutly, PhilipSaggi, SonikaSchellenberg, GordonSchmidt-Weinmar,

JohannesServiss, DustinSharp, LeonShen, VeronicaShen, Yea-SahSidhu, ManpreetSigaty, GeorgeSt. Pierre, CarolStafford, CampbellStark, BryanStewart, MichaelSturgess, ChristopherSzilagyi, DanielTalabis, Girlie GraceTate, StephenTay, Chun-YiTherriault, MarkTipton, DawnTrobridge, CarlyTse, Kelvin Kar OnValarao, Anna LizaVan Gaalen, JoelVan Limbeek, JohnVon Niessen, TeresaVu, Jennifer

Vukorep, CassandraWan, Janet Siu YingWang, Dan VivianWang, JianWang, MichaelWang, WeiWang, Xiao NingWhitehead, CliffWilson, TanyaWinzoski, Noreen GailWolthuizen, Wendy

CharleneWong, AshleyWong, BenWong, Chi FungWong, ClintonWong, CrystalXu, MengYang, Alvin Tzu-YangYang, JohnnyYang, ZheYang, ZhenYe, Wen JingYeung, EricYeung, JenyYoung, SunnyYu, LiliZanni, IvanZanotto, CarlaZhuang, FeiZhuang, Jin YunZinn, DanielZou, Shang

MANITOBAAnderson, ScottBarker, MichaelBrownlee, JasonBrugger, KevinCampbell, MatthewCampbell, StuartChabot, PaulChallis, RyanChambers, NanceChandler, EricaCunningham, Heatherde Muelenaere, JacquesDelisle, MichelleDoyle, JayEby, RobertEckert, PamelaFriesen, CoreyFriesen, JodiGougeon, DanielGryz, JohnHutton, MitchellKeller, StefanieKlassen, KatharinaKoensgen, JackieLam, HungLeavesley, DirkMacDonald, CraigMassey, KurtisMcArthur, PatrickMcDonald, OliveMcKee, ScottPaterson, CarolynPatton, LauraPhillips, GregoryPoapst, A. DouglasPodgurnycormier, KarenRodrigue, ChristopheSarna, Brad

Schillberg, IanSidey, MarshallSingh, HarmanpreetSkinner, TylerStephenson, JaredTyler, MichaelVogrig, Lucy (Lucia)

NEW BRUNSWICKBoudreau, MathieuBourgeois, AndreComeau, NadiaCouture, EricDupuis, MarleneGallant, Jean-PierreGodsoe, FrankMacKay, MichaelPrice, MatthewRowat, ShelleyShanks, GregVallée, MathieuWhite, Jeffery

NEWFOUNDLAND& LABRADORBarrett, IanBlackwood, RandolphHiscock, DerekLanger, LeighanneMurray, GregorySheppard, ScottShort, KimberleyStokes, Cyril

NOVA SCOTIABugden, TimCairney, BenjaminCasey, KevinCassis, NickolasCluett, RonCox, CoryDaigle, TrevorD’Eon, GillesFox, GregoryJenkins, DanielJohnston, NathanLeiper, AndrewMac Neil, DavidMacQueen, KennethMathers, NicholasNeynens, JoelNichol, SharonNowlan, TimothyRagbir, AnnScott, BrendaWilson, BradleyWilson, IanXu, Heju

ONTARIOAgius, DavidAgnew, JosephAjani, AlyAl-dabagh, TahaAlevizos, ConstantinosAlexander, RosannaAlves, FernandaAnand, HarvinderAntonio, JamesArdagh, Gregory

ioCongratulatioCongratulatioCongratulatio

President’sList

For each CFP Examination, FPSC honours the top performersas members of the President’s List. We are pleased torecognize the following individuals as members of thePresident’s List for the June 2010 CFP Examination:

Marion BurnOntario

Barbara BurynAlberta

Daniel CharlesQuebec

1st place:Florijan Papa, Ontario

2nd place (tie):Scott Lawrence, OntarioA. Douglas Poapst, Manitoba

Mathias DimterBritish Columbia

Benjamin EdwardsOntario

Dennis FieldOntario

It’s the value of professional advice.

Arena, StefanoArora, GurmeetAshton, LisaAujla, ShivinderAzzi, ZiadBajwa, SaeedBakharev, OlegBandayrel, AnnabelleBarbaro, MarioBarton, EricBazarca, TinaBeauchamp, PatrickBelo, MelbaBelsito, SandroBenedet, DerekBeniwal, RajeshBermel, ReneeBewick, JeffBirkbeck, DavidBlake, RyanBoonen, JustinBorman, BrandonBouck, DeborahBranco, MichaelBrettle, TraciBritton, WilliamBromley, ChristopherBrooks, Donna LynBrown, JoshuaBrown, SandraBrutto, MassimoBurn, MarionCalvert, IanCampanella, FabioCampbell, SpencerCampbell, TracyCampbell-Hawes, ShirleyCarney, JamesCarrière, GillesCarson, RobynCarter, AlexCarty, CrystalCarver, CharlesCaschera, MelissaChabot, StevenChambers, NealChan, Kaiser Kwong KitChan, MelindaChan, Vivian Ping ChingChang, IanChapman, JeffreyCherniavsky, AndrewCheung, SusannahChillman, DouglasChin, AmyChiu, CharlesChoudhury, SanjeevChow, Pik ChiChu, Mo WanChu, TerriChuchinnawat, ThitikornChugh, AtamChung, JohnChurch, EricChurch, Susan A.Clappison, CarlClarke, MatthewClarke, MichaelCochrane, LeahCockriell, KerryCoelho, JoeCoffey, StevenConnell, JohnathanCornacchia, Michael

Cote, MichaelCraig, CatherineDa Silva, RicardoDajo, BorisD’Alimonte, RobertDang, Tuyet Nhung

(Jennifer)Daniel, KevinDas, ChrisDe Boer, Waynede Hart, ChristopherDeering, SandraDefalco, DianeDekker, NinaDermo, StacyDesroches, MaryDeubry, TammieDhream, GurmeetDias, DennysDieleman, PeterDing, MansuDinino, TanyaDixit, JatinDomise, AndrayDonnell, PatrickDoucet, LukeDriscoll, BrianDryden, ChristopherD’Souza, NoelDunne, JamesDupree, AdamDupuis, DanielDurst, JonathanDziarski, GeorgeEdwards, BenjaminEdwards, TrevorEhgoetz, AndrewEllis, DouglasEnright, BrendanErauw, JeffreyEruysal, KamilFalcon, MarleneFarley, BrianFarr, SuzanneFarrow, StephanieFekete, VladField, DennisFociro, LaertFoley, DerrickFortino, JohnFowler, BonnieFranchino, AnthonyFraser, MaryFredericks, RonaldFurletti, PietroGal, GabrielGalloro, JosephGalluzzo, AnthonyGao, HejunGardner, AndrewGarofalo, ChrisGartner, MarthaGauld, GeoffreyGeorge, ShaunaGervais, LynneGiannotti, PeterGodbolt, FrederickGoodwin, DavidGordon, JeffGovier, TracyGrieco, VictorGrummett, PaulGuenther, SandraGuilfoyle, Blair

Guzman, BorisHaddon, HeatherHamilton, JustinHarness, JordannaHartviksen, KeelyHeard, RenaldoHeffron, MichaelHennebury, MattHildebrandt, MichaelHill, GrahamHillier, DavidHingorani, RichaHirtescu, SergiuHiscock, BrendaHo, BernardHolland, MichaelHolman, JaniceHolt, KirstenHoneyford, RichardHorner, PeterHouston, JayHowes, MichaelHowes, ShariHuether, John DavidHulshof, DavidHynes, TammyIncurvati, MatthewIqbal, Muhammad ZafarIrving, MiriamJackson, AtibaJackson, WayneJaehn-Kreibaum,

ChristianJankovics, MarekJankowski, JesseJefford, ChristopherJeon, Kyongtac DavidJones, CatherineJoseph, JollyKakkar, Anup (Bobby)Kalra, RajeshKalsi, RajvinderKamalinia, AydenKarfor, GregoryKatyal, SanjivKeleher, GeoffreyKeller, AnthonyKelley, StephenKennedy, ClaireKesteloot, JefferyKhalifa, AmiraKhanna, RajitKhullar, ParveenKirkham, NancyKirkland, AndrewKnapp, Lynda KayKnowles, SidneyKoehler, JasonKong, KammuiKortenaar, PeterKorzynska, EwelinaKrokker, KarlKrulisz, KatarzynaKubow, RobertKudsia, DevKukreja, ManojKumar, SunilKwan, Kin ShingLalonde, JulesLamba, HerpreetLass, CherylLauer, PaulLauwerier, CrystalLaw, Robert

Lawrence, RyanLawrence, ScottLawson, LeslieLe, LiemLeBar, HeatherLee, StephenLekas, AlexanderLeonard, TammyLeung, MichaelLeung, Yin Yee LouisaLewington, BrianLi, Guo HongLin, Yue ChanLinker, LindsayLinton, KellyLivingstone, DarrenLomas, KennethLongo, EnnioLoubert, BrianLowe, RyanMa, LiMa, ShouliMacanowicz, LolaMacMillan, WilliamMacri, VinceMadden, JohnMainella, AlexanderMakuyu, MartinMalachowska, MonikaMalik, ImranMalott, KellyManderville, KentMansour, KhaledMaple, SeanMaquiso-Montojo, Tess

MichelleMarchl, PeterMarks, ChristineMarquez, JosephMartin, KevinMartonfi, DanMassimiani, MarcelloMateus, CarlosMathew, JoseMatias, AllisonMatossian, HrantMatthews, EustanMatwey, DanielMcAdam, BoydMcCallan, CraigMcCanny, RosemaryMcLean, MitchellMcPhee, WilliamMichaud, PaulMilev, IvanMilne, AndrewMiron, DanielMitchell, CarolMiu, RonaldMoakler, JohnMoon, HyominMorris, CharleneMorrisey, SaraMorrison, JenniferMuriella, DavidMurphy, SusanMurray, DavidMuth, RalphNagy, RyanNanni, MatthewNaylor, NathanNear, JessicaNelson, JasonNephew, Steven

Newman, DeanNewman, Pauline (Paula)Nicholls, JulieNong, QuanxiO’Neill, KimberlyOsburn, DanaPacheco, AngeliquePaley, DeanPalisak, TomPalumbo, DomenicoPapa, FlorijanPark, Chi HwanPark, EllenPark, JustinPatani, NeelamPaton, AlanPenwarden, EdwardPereira, JasonPierre, PercyPiotrowski, WojciechPlayfair, WendyPoeta, DavidPoirier, Marc-AndrePoitras, Philip A.Polson, JohnPremdas, TracyPrior, RichardRai, GurjeetRaina, SameerRainville, RogerRaja, ElenaRalph, JannyRamsay, SuzanneRancourt, JustinRandhawa, TegbirRankin, AmandaRashid, AmirReale, BenjaminRecoskie, KimberleyRehal, Manpreet SinghReid, MarkRichardson, MichaelRichmond, DanielRipley, MicheleRitchie Vaisberg, RosalindRobinson, MarkRoung, JonathanRowe, MarkRoy, DuaneSabat, EdwardSaini, HarminderSammut, CharlesSantoro, StephenSarracini, DarcieSauve, MarnieSawhney, RainaSchacter, AdamScholl, JohnSchroeder, SarahSears, MatthewSeibel, KennethSequeira, ElaineSgro, FrankShah, DulariShanderuk, MichaelSharma, JatinderSharma, PeeyooshShaw, AllanSheridan, JamesSherman, ScottShoff, BruceShowers, LeslieSibbald, AnthonySimmons, Shannon

Simone, ChadSimpson, KariSinden, AlisonSinno, OmarSmith, LeslieSmith, NigelSmith, SheilaSnow, RonaldSolokhine, NonnaSoltis, JosephSomes, TamaraSoutar, RoderickSpeck, BradleySt. Jean, LeanneStade, KimberlySte.Croix, LesterSteele, NicholasSteele, NormanStulp, KevinSun, CuinanSwartz, EliSweeney Schenk, TraceySyla, Mary-annSzeto, Siu KwanTang, BinTaylor Kim, JillTenggardjaja, IanTenhunen, Diana RitaTenorio, JayTham, Pooi FongThompson, AnnThornton, CharlesTinio, AlfredoTomar, AlokTomona, SandraToy, HungTraballo, AlfredoTrajkovic, SlobodanTregunna, MichaelTruglia, GiuseppeTurner, KyleTyrovolas, KostasUrso, Stevenvan Gilst, BenjaminVan Graft, MarkVandergrift, ChristiaanVanGassen, EricVarga, MatthewVermeer, ChristineWahi, PankajWalas, JohnWalker, AndrewWalker, BrendaWalker, MichaelWalker, SarahWalsh, AdamWalsh, DanielWan, Wing Ching PatriciaWang, XukunWarren, JenniferWarren, KimberlyWaterman, BradWaters, JamesWeatherall, ToddWeaver, BrianneWeaver, HeidiWeber, ColleenWebster, GordonWegrzyn, DanielWei, ZhuoerWestall, JulieWestberg, RichardWhitehead, StewartWhiteside, Gareth

Williams, SharonWilson, JeffreyWilson, MichelleWismer, DavidWojtasik, RobbieWong, Chung WaiWong, JohnsonWu, Jia YingXithalis, EvangelosXu, Jia LongYeh, Cheng-ChiehYellenik, BarbaraYi, SeungYu, Yong GaoZacerkowny, TaliaZenta, PatrickZhang, GuoweiZhang, JinZhang, QianyueZhao, DanZhou, JunZhou, WeiZhu, QingshuangZhuleku, GentianZou, Alice Yan FeiZukiwski, Andrea

QUEBECAltro, MatthewCharles, DanielCleroux, RichardGhattas, HanyHarris, JasonKim, GeneLachance, MarcOliver, WilliamPalmer, DannySchultheiss, PhilippeZhang, Jun

SASKATCHEWANAmos, DeannaAnderson, BrendaBiehn, DouglasBonneteau, DarrenDuff, TracyHaanen, LisaHess, BarbaraHewson, TaylorHoesgen, RobertHogan, KellyLane, BrianLaRose, MeaghanLevesque, LukeOutram, LauriePoulton, JasonRein, JonathonRosenberger, DarrenRuston, AaronShaw, ScottShirkie, CamilleSmith, MelodySquires, SheilaSun, Xiao YanThompson, BruceUllah, RafiqueWozniak, Jack

OREGON, USASteele, Matthew

FINANCIAL PLANNING STANDARDS COUNCIL902-375 University Avenue, Toronto, ON M5G 2J5Telephone: 416.593.8587 Toll Free: 1.800.305.9886E-mail: [email protected] Website: www.fpsc.ca

CFP®,CERTIFIED FINANCIAL PLANNER® and are trademarks owned outside the U.S.by Financial Planning Standards Board Ltd.Financial Planning Standards Council is the markslicensing authority for the CFP Marks in Canada,through agreement with FPSB.© Copyright2010 Financial Planning Standards Council.All rights reserved.

onsonsonsons1,006 FutureCFP® Professionals!Financial Planning Standards Council (FPSC) is pleased to congratulate

the outstanding number of candidates who passed the June 2010 Certified

Financial Planner (CFP) Examination. They are now one step closer to joining

more than 17,500 CFP professionals across Canada and over 126,000

international colleagues who, through CFP certification, have met the

highest standards for competent and ethical service in financial planning.

Andrew GardnerOntario

Fredrick GodboltOntario

Derek HiscockNewfoundland & Labrador

Scott HoldenAlberta

Jules LalondeOntario

Herpreet LambaOntario

Alex MacKenzieAlberta

John MaddenOntario

Ryan McEachenBritish Columbia

David PillingAlberta

Richard PriorOntario

Jeannette ReimerBritish Columbia

Michael RichardsonOntario

Philippe SchultheissQuebec

Marshall SideyManitoba

Sheila SquiresSaskatchewan

Sherri SwystunAlberta

Bradley WilsonNova Scotia

A special information feature Monday, October 4, 2010 • THE GLOBE AND MAILFPSC6

National Financial Planning Week • October 4 - 10, 2010 • www.financialplanningweek.ca

I n the aftermath of significantchanges to financial remuner-ation structures international-

ly, Canadian investment industryexperts stress the importance ofan open and transparent flow ofinformation.

In the U.K. and Australia, thepractice of steering consumerstoward products associated withhefty commissions led industryregulators to ban commissionsoutright as of 2012, says NickCann, CFP and chief executive ofthe Institute of Financial Planningin the U.K.

In Canada, required trainingand regulations for licensedfinancial advisors provides pro-tection against similar transgres-sions, but Kevin Regan, execu-tive vice-president at InvestorsGroup, emphasizes that clearcommunication is also essential.

The commission system canalso mislead consumers intothinking that advice is free, saysMr. Cann. “They don’t thinkthey are paying for anythingbecause it is coming out of theproduct.”

One initiative designed toclarify remuneration here inCanada is Fund Facts, a new,plain-language documentdesigned specifically to help con-sumers quickly comprehend thevariety of fees and commissionsthey may pay for mutual funds.

“After two years of consult-ing with insiders and consumer

groups, the Canadian industryput together a salient summaryabout the mutual fund productswe are recommending,” Mr.Regan says.

Fund Facts will make itsdebut in the marketplace in early2011. The document, limited totwo pages, is exemplary of theindustry’s commitment to trans-parency and clarity, he says, andexplains sales charges, trailingcommissions and other fees injargon-free English.

But even the clearest docu-mentation will not replace theneed for clear communicationbetween advisors and consumers.

“The hallmark of any rela-tionship with a financial plannershould be openness and trust,”says Mr. Regan. “Clients need toask their financial planner notonly how they get paid, but alsofor an outline of their credentialsand experience. They should dis-cuss how often they will commu-nicate to review progress andupdate their financial plan. Theyshould think about their goals –short-, medium- and long-term —and make sure their plannerknows what they are.”

Industry aims for clear communication onfees, commissions

not everyone who refers to them-selves as a planner is certified.CFP certification provides assur-ance that the planner is commit-ted to internationally recognizedstandards of professional compe-tence, ethics and practice.

“There is a growing awarenessof financial planning as a distinctprofession, and a view of certifiedfinancial planners as trusted advi-sors qualified to guide clientsthrough the complexities of long-term planning,” says Mr. List.

FPSC’s efforts are bearingfruit: With 18,000 certified finan-cial planners, Canada’s CFP ratioper capita is one of the highest inthe world.

Martin Dupras, chairman ofthe board of directors of the Insti-tut québécois de planificationfinancière (IQPF), which grantsfinancial planning diplomas andestablishes rules concerning the

ongoing professional develop-ment of financial planners, agreesthat the economic crisis raisedconsumer awareness of the needfor professional financial planningadvice, but it also challengedfinancial planners to demonstratetheir worth.

“Generally, people are betterinformed about financial mattersthan they used to be, whichmeans financial planners need tobe providing advice and guidancethat goes well beyond what theirclients already know,” says Mr.Dupras.

In addition, he says, con-sumers are faced with a far morecomplex array of financial prod-ucts than were available just a fewyears ago, and choosing the rightmix to meet their needs can bevery challenging.

Noel Maye, CEO of FinancialPlanning Standards Board Ltd.(FPSB), a non-profit associationthat owns the CFP marks outside

the U.S. and establishes, upholdsand promotes worldwide profes-sional standards in financial plan-ning, says there has been a signifi-cant shift across the world inrecent years towards personalresponsibility for financial plan-ning.

“People are living longer,

which means they will spendmore years in retirement. Manyhave more assets than their par-ents may have had, but they alsohave more obligations, such aschildren’s education and the costof care for elderly parents,” saysMr. Maye.

At the same time, he says,

many governments around theworld are no longer able to pro-vide the social support for retire-ment that they may have done inthe past. This means people needto plan for their own financialfuture, and they are increasinglyturning to professional financialplanners for help.

Advisors from FPSC1

Financial planningprofession enters new era

10 Questions to AskYour PlannerThese questions will help you interview and evaluate several financial planners to find a competent,qualified professional with whom you feel comfortable and whose business style suits your financialneeds.

Don’t be afraid to ask these and any other questions you feel need a full and open answer. Anyprofessional will welcome them.

1. What are your qualifications?Ask the planner what her qualifications are to offer financial advice and if, in fact, she is a quali-fied planner. Ask what training she has successfully completed. Ask what steps she takes tokeep up with changes and developments in the financial planning field and the financial servic-es industry at large. Ask whether she holds any professional credentials or designations.

2. What experience do you have?Experience is an important consideration in choosing any professional. Ask how long the plan-ner has been in practice; inquire about what experience the planner has in dealing with peoplein similar situations to yours and whether he has any specialized training. Choose a financialplanner who has at least two years experience counselling individuals on their financial needs.

3. What services do you offer?The services a financial planner offers will vary and depend on her credentials, registration,areas of expertise and the organization for which she works. Some planners offer financial plan-ning advice on a range of topics but do not sell financial products. Others may provide adviceonly in specific areas such as estate planning or taxation. Those who sell financial products suchas insurance, stocks, bonds and mutual funds, or who give investment advice, must be regis-tered with provincial regulatory authorities and may have specialized designations in theseareas of expertise.

4. What is your approach to financial planning?The types of services a financial planner will provide vary from organization to organization.Some planners prefer to develop detailed financial plans encompassing all of a client’s financialgoals. Others choose to work in specific areas such as taxation, estate planning, insurance andinvestments. Ask whether the individual deals only with clients with specific net worth andincome levels, and whether the planner will help you implement the plan she develops or referyou to others who will do so.

5. Will you be the only person working with me?It is quite common for a financial planner to work with others in his organization to develop andimplement financial planning recommendations. Financial planners often work with other pro-fessionals, like lawyers and accountants. You may want to meet everyone who will be workingwith you.

6. Howwill I pay for your services?Your planner should disclose in writing how she will be paid for the services she will provide.Planners can be paid in several ways, including commission, salary and fee-for-service.

7. Howmuch do you typically charge?Although the amount you pay the planner depends on your particular needs, the financial plan-ner should be able to provide you with an estimate of possible costs based on the work to beperformed. Such costs would include the planner’s hourly rates or flat fees, or the percentage hewould receive as commission on products you may purchase as part of the financial planningrecommendations.

8. Could anyone besides me benefit from your recommendations?Ask the planner to provide you with a description of her conflicts of interest in writing, forinstance, any business relationship with the companies or ownership interest in any companythat supplies financial products sold by the planner and the planner's employer.

9. Are you regulated by any organization?Financial planners who sell financial products such as securities and insurance or who provideinvestment advice are regulated by provincial regulatory authorities and may also subscribe toa code of ethics through a professional association. Individuals in the accounting and legal pro-fessions are usually members of professional bodies that govern their fields. Planners who holdCFP® certification are subject to disciplinary proceedings of the Financial Planning StandardsCouncil, the body that enforces that CFP Code of Ethics.

It’s a fair question to ask if he has ever been the subject of disciplinary action by any regula-tory body or industry association. You can verify the answer by contacting the relevant organi-zation; some organizations have a searchable function on their websites, such as the Check aCFP Professional tool on the FPSC website.

Ask the financial planner whether he subscribes to a professional code of ethics such as theCertified Financial Planner Code of Ethics.

10. Can I have it in writing?Ask the planner to provide you with a written agreement that details the services that will beprovided. Keep this document in a secure place for future reference.

Adapted with permission from the Financial Planning Standards Council. For full details on theseimportant questions, please visit fpsccanada.org/10-questions-ask-your-planner online, orcall the Financial Planning Standards Council toll free at 1.800.305.9886.

q&a

“Generally, people are better informed about financial matters than they used to be, which meansfinancial planners need to be providing advice and guidance that goes well beyond what theirclients already know. In addition, consumers are faced with a far more complex array of financialproducts, and choosing the right mix to meet their needs can be very challenging.”

“Clients need to ask their financialplanner not only how they get paid,but also for an outline of theircredentials and experience.”

A special information featureMonday, October 4, 2010 • THE GLOBE AND MAIL FPSC7

T o raise awareness of theimportance of financialplanning and encourage

more Canadians to do financialplanning, CFP professionalsacross Canada are hosting Finan-cial Planning Week HealthCheck Ups in their communities.“We want to demonstrate thatfinancial planning can help alle-viate stress and help individualsand families chart a course. It’sabout so much more than simplyhow much you’re making onyour investments,” says TamaraSmith, vice president, Marketingand Consumer Affairs, FinancialPlanning Standards Council(FPSC).

The following CFPs will bejoining their colleagues fromCharlottetown, P.E.I., to Victoria,B.C., in providing complimenta-ry Financial Health Check Upsin their communities. For infor-mation about events in yourcommunity, please visitwww.financialplanningweek.ca/map/events.

Valerie Chaitan-White, CFP,The Next 30 YearsHeadingley, Manitoba“Individuals’ life plans shouldreflect their interests, while takinginto account all the forces thatimpact daily life. That is some-thing you cannot do if you onlytalk about money exclusively. I

find it disheartening to see peoplefairly close to retirement whoreally have little idea what theyare going to do with the nextstage of their life, and are not pre-pared for it in any way.”

Ms. Chaitan-White will beproviding financial planningcheckups at Headingley’s Munici-pal Library during Financial Plan-ning Week.

For more information, pleasevisit www.thenext30years.com.

Stephen Cox, CFP,Desjardins Financial SecurityIndependent NetworkHalifax, Nova Scotia“People tend to confuse financialplanning with investing, but it isso much more than that. At oursessions and webinars, we will betalking more about identifying lifegoals, and we use an individual’saaspirations to develop a financialroadmap for their life. Compre-hensive financial planningincludes several essential compo-nents beyond investing (or assetmanagement): retirement plan-ning; cash management; tax effi-ciency; risk assessment (like thepossibility of losing your job oryour ability to work); and ensur-ing that your estate is passed oneffectively to the people of yourchoice.

“I’ve been in the business forquite a few years and just about

every time I ask new clients tobring in a copy of their existingfinancial plan, I draw a blank.We’re hoping to rectify that a bitduring Financial PlanningWeek.”

For more information, pleasevisit www.stevecox.ca.

Pierre Ghorbanian, CFP,Retirement Compensation FundingToronto, OntarioNoting that life is never simplyabout money, Mr. Ghorbanianhas teamed up with Daniel Chi-ang, a respected holistic nutrition-ist at the nearby Inspired LifeHealth Centre, to provide whole-life checkups during FinancialPlanning Week.

“Improving your emotionaland physical health in a naturalway echoes the holistic approachwe use within our own practice.Participants will be asked to makea small donation to the Seeds ofHope Foundation, a local charitythat supports initiatives such asthe Alano Club, which counselsthose who are unemployed orotherwise facing a crossroads intheir lives.

“That is what financial plan-ning is really all about. We try toanticipate the unexpected anddevelop strategies to deal withchallenges when they do arrive.”

For more information, pleasevisit www.danforthcfp.ca.

Experts share insights and strategiesnationally during Financial PlanningWeek

Celebrate Financial PlanningWeekby assessing your financesAccording to the Financial Planning Standards Council, when itcomes to financial planning many Canadians simply don’tknow where to start. This Financial PlanningWeek, FPSCencourages you to take action, one step at a time.

• Keep your receipts and count up howmuch you spend on

the“little things”

• Create – and stick to – a weekly budget

• Help teach your children to save 10% and spend wisely

• Pay off a credit card

• Establish an emergency fund (three months is

recommended)

• Evaluate your employee benefits

• Develop a holiday spending budget

• Plan for year-end tax strategies now

• Invite a financial planner to speak at your workplace

• Review your insurance coverage

•Write down your financial goals and revisit them

periodically

• Calculate your net worth; update it annually to measure

your progress

For more information, please visitwww.fpsc.ca.

take action

National Financial Planning Week • October 4 - 10, 2010 • www.financialplanningweek.ca

fpsc.ca

76% of Canadians with a CertifiedFinancial Planner® professional feeltheir financial affairs are on track.

It’s the value of professional advice.

can change your financial situation.advicethe right kind of professional

CFP®, CERTIFIED FINANCIAL PLANNER® and are trademarks owned outside the U.S. by Financial PlanningStandards Board Ltd. (FPSB). Financial Planning Standards Council is the marks licensing authority for the CFPmarks in Canada through agreement with FPSB. ©2010 Financial Planning Standards Council. All rights reserved.Statistics from FPSC’s Value of Financial Planning study, 2010. Copyright 2010 Financial Planning Standards Council. All rights reserved.

TD Waterhouse Discount Brokerage, TD Waterhouse Financial Planning, and TD Waterhouse Private Investment Advice are divisions of TD Waterhouse Canada Inc., a subsidiary of The Toronto-Dominion Bank. TD Waterhouse Canada Inc. – Member CIPF. TD Waterhouse PrivateClient Services means The Toronto-Dominion Bank and its related companies that provide deposit, investment, loan, securities, trust and other products and services. TD Waterhouse is a trade-mark of The Toronto-Dominion Bank, used under license.

PRIVATE CLIENT SERVICESFINANCIAL PLANNINGDISCOUNT BROKERAGE 1-866-638-5321 WWW.TDWATERHOUSE.CA

Years ago they began a trip they’ll

spend a lifetime completing.

Talk to TD Waterhouse. Together we’ll create aretirement plan that will be ready when you are.

Not long ago, it seemed as if retirement was a lifetime away. Now it’s almost here, and

you’re looking to the future with excitement. At TD Waterhouse, we believe you deserve

to look ahead with confidence too. It’s why we work closely with you to create the right

retirement plan. One that may include wealth management services such as investment

and tax planning. Just as importantly, you’ll know that one-on-one advice, backed by a

team of investment professionals, is there to help ensure that financial opportunities are

seized and retirement dreams are realized.

Contact us today, and start getting ready for the retirement you’ve always wanted.

A special information featureMonday, October 4, 2010 • THE GLOBE AND MAIL FPSC9

National Financial Planning Week • October 4 - 10, 2010 • www.financialplanningweek.ca

W hen it comes to finan-cial planning, a fewcommon misunder-

standings may be keeping manyCanadians from getting the helpthey need to achieve peace ofmind today and their goals anddreams for the future.

Among the most prevalent,says Tina Tehranchian, CFP, abranch manager at Assante Capi-tal Management in RichmondHill, Ontario, is the idea that ahigh income is required to bene-fit, or even to save for retirement.“I’ve seen people with very highincomes who have much less insavings than families with much

more modest incomes,” she says.“Consistency is the key. Financialplanning is not only for thewealthy – in fact, it is a means tohelp you create wealth.”

Perhaps the most widespreadof all financial planning myths isthat it is just about investing ortax planning, says Al Nagy, CFP,a financial consultant withInvestors Group in Edmonton. “Ialways ask prospective clients ifthey have a financial plan inplace, and often they’ll hand mea list of investments.”

While it incorporates both ofthose realms, it is the comprehen-sive nature of financial planning

that makes it so valuable, evenfor individuals who want to man-age their own investments. “Theymay think that using the servicesof a financial planner will meanlosing control,” says Ms.Tehranchian. “But this can be acompletely collaborative process– while some individuals may beskilled at managing their owninvestments, they might not havethe ability to manage their owntax and estate planning.”

Another idea that leads usastray is that the responsibility forthe success of the financial planlies solely with the financial advi-sor. “No matter how good theadvice is, if the clients don’t acton it, nothing will happen,” shesays. “People hesitate to takeaction; or they may try to out-smart their financial advisor – it’sthe equivalent of signing up for agym membership and believingthat will be enough to get you fit.Financial planning is a two-waystreet – there is no way to getgood advice from your planner ifyou’re sharing incomplete infor-mation.”

One of the greatest surprisesfor individuals and families whoembark on the planning processis the process itself, says Mr.Nagy. “When I initially sit downwith people, typically at least onemember of the family says theyfind finances boring. But financialplanning is an emotional processthat helps you answer questionsabout life and life’s uncertainty.When they realize we’re reallytalking about achieving their lifegoals, they become completelyengaged.”

Commonmisunderstandings often preventpeople from taking the first step

Mistakes andmisconceptions aboutfinancial planningYou are the focus of the financial planning process. The resultsyou get from working with a financial planner are as muchyour responsibility as the planner’s. To achieve the best results,you will need to be informed about what you can realisticallyexpect from the financial planning process.

Many people don’t really understand the value of financialplanning. As a result, many people:

• Think financial planning is the same as investing

• Neglect to set measurable financial goals

• Neglect to evaluate their financial plan periodically

• Think financial planning is the same as retirement

planning

• Expect unrealistic returns on investments

• Are looking for a quick financial fix instead of a long-term

strategy

• Don’t understand that good professional planning advice

is largely dependent on good information from clients

• Believe financial planning is primarily tax planning

• Think they'll lose control over their decisions if they use

a planner

Adapted with permission from www.FPSC.caFor more information, please visitwww.fpsc.ca.

fyi

Manulife, Manulife Financial, Manulife Securities, the Manulife Financial For Your Future logo, the Block Design, the Four Cubes Design, and Strong Reliable Trustworthy Forward-thinking are trademarks of The Manufacturers Life InsuranceCompany and are used by it, and by its affiliates under license. Manulife Securities, consisting of Manulife Securities Incorporated, Manulife Securities Investment Services Inc., and Manulife Securities Insurance Inc., (carrying on business in BritishColumbia as Manulife Securities Insurance Agency), is one of Canada’s pre-eminent financial organizations. Manulife Securities provides a wide range of investment and insurance products and services to the clients of its independent advisors.Manulife Securities Incorporated is a licensed investment dealer, and a Member of the Investment Industry Regulatory Organization of Canada (“IIROC”). Manulife Securities Investment Services Inc. is a licensed mutual fund dealer, and a Member of theMutual Fund Dealers Association of Canada (“MFDA”). Insurance products and services are offered through Manulife Securities Insurance Inc.

At Manulife Securities, our advisors take great pride in their ability to get to

the heart of what really matters most to you. We understand that it’s not

just about the destination anymore - the journey is as equally important.

Tomorrow’s financial horizon is filled with opportunities and challenges.

The power of strong and reliable financial advice holds greater significance

when it comes to reaching your financial goals and dreams.

Our interest in your long-term financial strategy is the underlying

foundation of our values – it is the forefront of our commitment. Whether

you are looking for a fresh perspective or expert service, advice, and

experience, your Manulife Securities advisor is your partner – for your

future.

To find an advisor in your area, please visit www.manulifesecurities.ca

What’s on your horizon?

HOLLIE, AGE 8

How much money do youthink Mommy and Daddymake at their jobs? $20 or $50in 3 minutes.

Do you think $15 is a lot ofmoney? Not that much. It justcosts 15 loonies.

What is financial planning?Figuring out something thatworks. Like if the TV was broken,you’d need to get some screwsand plugs and plug them in.

What is a budget? A friend thathelps you all the time.

How old do you want to bewhen you buy your firsthouse?16 or 17.

CLAIRE, AGE 5

What does financial planningmean?To go and plant your garden.

How much does a housecost? $100.

LEANNE, AGE 8

What do you want to bewhen you grow up? An artist.

How much money do youthink an artist makes?Twenty dollars a day.

When do you think youpaents will retire?My mom already retired. Mydad thinks he will retire whenhe is 60.

A special information feature Monday, October 4, 2010 • THE GLOBE AND MAILFPSC10

I n children, a limited under-standing of money and theway it works is natural. But

there is ample evidence that alack of financial literacy is alsoundermining the well-being of

Canadian adults.“Canadians now owe $1.45

for every dollar of personal dis-posable income we’re earning,”says Patricia Lovett-Reid, CFP,vice president, TD Waterhouse

Canada Inc.. “We’re faced withmany choices every day. Most ofthose choices will have a smallimpact on our life, but some willbe very significant.”

Ms. Lovett-Reid, who has

four children ranging in age from22 to 26, says, “The attitudes andbehaviours of parents have ahuge influence on their children’sfinancial life. Canadians are livingbeyond their means, and if chil-dren see their parents being con-sumption-oriented, it’s natural forthem to fall into that tendency aswell.”

In addition to modelling effec-tive financial behaviour, parentscan also help their children devel-op skills by encouraging them tomanage money, in age-appropri-ate ways, as they grow up. “As aparent, you can create a fun andsafe learning environment forchildren so that their first experi-ence isn’t the credit card they getas a university student,” she says.

Whether you give your chil-dren an allowance or not, advisesMs. Lovett-Reid, it’s empoweringto develop an inclusive familystyle around decision-making.“When children help make fami-ly decisions, they begin to under-stand that there is only so muchdiscretionary income, and tounderstand the differencebetween what’s essential andwhat’s nice to have.”

That understanding is alsocritical for adult Canadians whohave fallen off track in terms ofachieving their financial goals oreven living within their means,she says, “I know people don’tlike budgets, but they work. Gothrough your statements tobecome clear on what expensesyou are obligated to pay andwhat is discretionary. Many peo-ple are shocked when they seethe numbers; as a result, theystart to do things differently.”

Many experts feel that ourgovernment also has an impor-

tant role to play in the develop-ment of financial literacy.

“Financial literacy is a lifeskill, ideally developed at ayoung age,” says Stephen Rot-stein, vice president, Policy andEnforcement, Financial PlanningStandards Council. “In our sub-missions to the Working Groupon Financial Literacy for Ontarioand to the Federal Task Force onFinancial Literacy, we’ve recom-mended the development of edu-cation policies that will help cre-ate financial literacy during theschool years.”

Effective financial literacyeducation requires teaching it as asocial science rather than a mathclass, says Mr. Rotstein. “Thefocus should be on the decision-making that goes into making abudget rather than simply on thenumbers.”

If financial literacy is taughteffectively in schools, he says, allstudents will be armed with theknowledge and tools they need tomake informed and effectivefinancial decisions. Just as impor-tant, “it will shape positive behav-iour early on, before detrimentalfinancial behaviours are instilled.We believe that financial literacyskills should be taught, in an age-appropriate way, starting as earlyin life as possible. The earlier chil-dren are taught, the more theycan improve on these skills andperfect them as they grow older.”

Those skills and behaviourshave the potential to significantlyenhance quality of life for Cana-dians. “People often look at finan-cial planning as denying your-self,” says Mr. Rotstein. “[Moreaccurately], it is the process ofmanaging your affairs to achieveyour life goals.”

Teaching financial literacy in schools a social imperative

National Financial Planning Week • October 4 - 10, 2010 • www.financialplanningweek.ca

From themouths of babes: insight into howwe think about finances and our futures

What do little kids think aboutmoney, its uses andwhere it comes from? Economies of scale aside,children reveal views not too distant from those of many adults.

Don’t buyanything for

a year.

100 dollars.That is a lotof money.

To quit your joband do whatever

you want.

Um...Five, four,

fifty thousanddollars.

What do you think you haveto do to save $25?

How much money do youneed to retire?

Do you know what it means to retire?

How much do you thinka house costs?

“When children help make familydecisions, they begin to understandthat there is only so much discre-tionary income, and to understandthe difference between what’s essen-tial and what’s nice to have.”

EDUCATION

NOAH, 4

Do you know what debt is?It’s when someone dies and goesto heaven.

Where do you get money?From a bank – they have lots ofmoney.

What is Retirement?Retirement is you’re tired but youget to rest a lot.

If you need money what doyou do? I ask Mom – she has lots!

How many credits cards doyour parents have?Umm ... a million?