Embed Size (px)

Citation preview

Analysts

Tongxin Xian Qiaochu Geng [email protected] [email protected]

Jiangliang Chen Qiao Huang [email protected] [email protected]

Wells Fargo & Company is the fourth largest bank holding company in the United States, with $1.5 trillion assets, $1.1 trillion deposits and $170 billion stockholders’ equity by the end of fiscal year 2013.i Wells Fargo & Co. is a diversified community based financial services and bank holding company, which operates mainly in the United States with partial business in other countries. It has three main operating segments, including Community Banking, Wholesale Banking and Wealth, and Brokerage and Retirement.ii The Community Banking segment is focused on individual customers and small businesses. The company provides diversified financial products and services, such as borrowing and lending, and issuing debit cards and mortgages to its customers. It was the second largest issuer of debit cards in the U.S. in 2013. For the fiscal year ended 12/31/2013, Wells Fargo net income rose 16% to $31,878 million.

Stock Performance Highlights 52 week High $53.17 52 week Low $43.41 Beta Value 0.86 Average Daily Volume 14.8 M

Share Highlights Market Capitalization $276.86 B Shares Outstanding 5.22 B Book Value per share $31.57 EPS (12/31/2013) $3.89 P/E Ratio 13.01 Dividend Yield 2.60% Dividend Payout Ratio 29%

Company Performance Highlights ROA 1.51% ROE 13.38% Revenue $82.28 B

WFC Exhibits Potential Strength

With the continuing improvement of the economy, Wells Fargo had a progressive increase in its net income in 2013. Its net income rose 16% to $21,878 million. The 16% growth mainly results from decreases in expenses, especially provisions for credit losses and non-interest expenses. We expect that Wells Fargo’s net income will increase at least 5% in 2014 along with the growth of loans and deposits. Wells Fargo generated revenue of $83.8 billion in 2013, 51.09% of which was from interest income and 48.91% of which was from non-interest income. The composition of the source of revenue reflects a well-diversified business model, which largely reduced Wells Fargo’s unsystematic risk. We believe the proportion of non-interest income as the percentage of total revenue will increase in next 3 to 5 years because of the increase in trust & investment fees, mortgage banking, and insurance fees.

The economy is recovering from the crisis and customers have more resources to pay off their credits. The October Consumer Confidence Survey result showed a new recovery high at 94.5, which indicates better consumer perceptions of employment, business condition and income, and also showed a stronger consumer spending and loaning. Wells Fargo had a $19.2 billion customer loans increase in 2013. The rise in customer loans largely results from increasing consumer confidence, which we believe will maintain its high level in the next 3 years. As the second largest issuers of debit cards in the U.S. in 2013, Wells Fargo has great growing potential.

The U.S. Housing Market is slowly recovering from the crisis. By 10/20/2014, the median house price in the United State rose by 7.7% from last year.iii Wells Fargo will benefit from the current home price trend because about 20% of Wells Fargo’s earning assets are real estate 1-4 family first mortgages. The rise in home prices will allow Wells Fargo to release more mortgage loans and generate more interest income in 2014. One Year Stock Performance

Financial Ratios

Loan-to-deposit Ratio 0.77Debt to Equity 7.93%

Important disclosures appear on the last page of this report.

Company Overview

Krause Fund Research

Financials Banking

Recommendation: Buy

Wells Fargo & Co. (NYSE: WFC)

Current Price $53.44Target Price $59.69-61.54

Source from: Yahoo! Finance iv

Page 2

Executive Summary

We recommend to buy Wells Fargo & Company at this time based on our economic, industry, and company analysis. We predict the GDP will continue to increase in 2015 and the unemployment rate will decrease. Based on our prediction and analysis, these factors influence the consumer confidence to increase. With a consumer purchasing power increase, people will borrow more money from banks in order to spend more. As the world’s biggest bank and number one lender to small business in the U.S., Wells Fargo’s loan business will continue growing. Our analysis shows the interest rate will increase in 2015, which will help Wells Fargo grow its profit as more loans are given out.

Economic Analysis

Gross Domestic Product Real Gross Domestic Product, GDP, is one of the most important economic factors to measure the well-being of an economy. GDP defined as the output of goods and services produced by the labor and property located in the Unites States within a specific time period. V Many analysts and economists use it as an indicator to gauge a nation’s standard of living because it represents the size of the nation’s economy. We think GDP is a very essential economic factor for the finance sector because the Federal Reserve often uses GDP as a benchmark to adjust its monetary policy, which will have a huge impact on the financial services industry.

According to the Federal Reserve’s projection, the GDP will increase around 3.0%-3.2% in 2015. Historically, GDP gradually recovered from the recession with 2.5% increases. Also, GDP continued growing during the first three quarters of 2014. From our opinion, we partially agree with the Federal Reserve’s projection. We believe it will increase 3.0% in the future six months, slightly decreased from the actual GDP in third quarter 3.5%. We predict that GDP will increase around 2.7%-3.0% in the future 2-3 years.

Continue growing GDP will have positive impacts on the financial service sector. As the big economic environment is turning into a better situation, the consumer’s purchasing power will increase and consumer confidence will increase at the same time. With the increase of consumer spending, people tend to borrow more money from banks and credit companies, which speed up the development of the financial industry.

Source from: Federal Reserve vi

Source from: Federal Reserve vii

Unemployment Rate Unemployment rate is the earliest indicator of economic trends released each month. We think unemployment rate is very important because a high unemployment rate will lower the development speed of the country and lower the nation’s spending power, which will prevent people from borrowing money from banks.

Based on the data from the Bureau of Labor Statistics, the number of unemployment rate has been volatile during the years. Since 2009, the unemployment rate showed a downtrend and decreased by nearly 1.0% each year. According to the Federal Reserve, the unemployment rate will stay around 5.4%-5.7% in 2015 and keep from 5.2% to 5.5% in the long run. We partially agree with the forecast given by the Federal Reserve. We predicted that the unemployment rate will keep around 5.8% in the future six month and decrease to 5.6%-5.8% in the future 2-3 years.

We believe a lower unemployment rate will be beneficial to the financial service sector because people tend to spend more money when they have a job. The consumer spending will increase when the unemployment rate decreases. Strong purchasing power will lead to more loans and money borrowing that will increase the business of banks and credit companies.

Source from: Bureau of Labor Statisticsviii

Page 3

Source from: Bureau of Labor Statistics ix

Consumer Confidence Index The consumer confidence index is based on a random consumer confidence survey provided by The Conference Board. The index that has base year 1985 equal to 100 point and measures U.S. consumers’ optimism and sentiment. Consumer Confidence Index (CCI) increased from last year’s range 58.43 to 82.13 to current year’s 78.3 to 94.48 after adjusting the seasonal effect, even reached the highest point at October as 94.48 after economic crisis of 2008.x Financial sector, the uptrend of CCI is benefiting the financial sector, especially for the consumer finance industry.

Sources from: Factset dataxi

The table above shows the CCI data from 2007 to September, 2014. As higher consumption optimism which dramatically increased from the depression, we expect that the consumer confidence will continue being optimistic and reach 100 to 110 that is similar to the point before crisis. Also, the uphill data, which means higher consumer expenditures, gives the consumer finance industry a positive effect.

New Housing Starts and Mortgage Rates New housing starts is a very important factor because the housing market controls 4% of GDP that indicates consumer’s house purchasing power. More new housing starts represent higher consumer spending and confidence to the market.

30-year fixed mortgages rate is the most important driver of the new housing starts. From the historical price, the mortgage rate had a downtrend from 1990 and fluctuated a little during the years. The mortgage rate increased 15% since 2012 and stayed at 4.211% in 2014. The rebound of the mortgage rate in 2012 cause housing price to go increase. In 2015, we predict the mortgage rate will stay around 4.5%-4.75%. In the future 2-3 years, we expect the mortgage to increase to 5.5%-6.0%. Lower mortgage rate will

stimulate consumers to purchase more houses and spend more money, which would increase the loan business of banks and credit companies.

Source from: Freddiemac xii

Industry Analysis

Market and Competition Since the 2008 financial crisis, the diversified financial services industry recovered well with the huge support from the government and market development. A low unemployment rate, a low interest rate and increasing GDP have positive impacts on the market and they speed up the industry growth. To be general, borrowing and lending, the debit card issue and loan mortgage for customers contribute to the whole market most.

The diversified financial services industry is highly competitive and intense. Based on Porter’s five forces we conclude three main reasons to explain the current situation in the industry: the bargaining power of suppliers and buyers, threat of substitutes and entrants, and rivalry of competition. The diversified financial services industry is one of the most important industries in the financial services sector because it covers business from personal level to institution level of lending-based services. The power of the diversified financial services industry as a supplier is very strong because it mainly provides financial services, does conventional banking operations and offer loans to small or medium corporations. Also, as a buyer, the diversified financial services industry plays an important role due to its strong purchasing power.

The threat from substitutes and new entrants is very obvious. Many companies outside the industry are trying to get in and share wealth. For example, an insurance company can easily start its loan business and take away some market share that belongs to original loan banks. Also, companies like Google and Apple have started to introduce their own electronic wallets that will take away from the financial services market. However, with strict regulation and capital requirement, new entrants cannot easily survive. Customers value companies’ name and prefer old banks that provide wide range of services.

Page 4

For rivalry of competitions, the competition within the industry is very intense. Companies try to introduce new services and provide better products that fit customers’ demand. At the same time companies in the industry are trying to form into a group while works against the pressure from the government and competitors outside of the industry.

Industry Trends and Recent Development

Federal Reserve Polices The current situation of Federal Reserve policy is complicated and changes during time. It is very hard for investors to predict what the Fed is going to do next and make rational investment decisions. However, with the historically low interest rates, banks and other financial service-related companies still generate revenue and move the market.

According to the newest report released by the Federal Reserve in November, all depository institutions must hold a percentage of certain types of deposits in a Federal Reserve Bank as vault cash.xiii Also, depository institutions must report to Feds regularly about their deposits and other reservable liabilities situations.xiv For the deposits, the Federal Reserve will pay a certain amount of interest rate to the banks. This action keeps part of the bank assets liquid so they can be used in case of emergencies.

Along with keeping the cash liquid, the Federal Reserve decided to still keep low interest rates in 2015 around 0- 0.25%.xv The Federal Reserve is trying to use low interest rates to maximize employment and keep the market stable. In the long run, the Federal Reserve decided to slowly rise the interest rate, which is a good sign for Wells Fargo. With the rising of the interest rate, Wells Fargo’s banking business will increase and its profit margin will increase as well. Also, Federal Reserve purchased a large number of long-term Treasury securities to make the financial market move and grow in a stable pace.

Stress test In March, a stress test revealed the newest test results. In the report, Federal Reserve tested 30 total financial companies and only one company, Zions Bancorp, failed to meet the 5% top-tier capital threshold. The stress test examined the banks anti-pressure liability under a big financial crisis. The test scenario included the real GDP becoming -4.6%, unemployment rate turn to peak level at 11.3%, home prices reach -26% and 10-year treasury yield reach 1.6%. xvi The annual stress test helped the Federal Reserve to make sure big banks have enough assets to deal with crisis. Also, it makes sure the financial industry is able move the market when the crisis is coming.

Based on the test results, we have a strong belief the financial industry will perform well if there is an economic downturn. The best performers in the test include Bank of New York Mellon and State Street Corporation. The lowest performers included Bank of American and JPMorgan Chase. xviiThe results showed Wells Fargo performed well under the hypothetical scenario because it hits 8.2% tier 1

common ratio. It means wells Fargo will still have the ability to repurchase and pay dividends during an economic downturn.

Before the Stress test, the Federal Reserve rejected five banks’ capital plan including Citigroup. The Fed said Citigroup’s plan did not provide the accurate number that how much it will lose in a severe economic downturn. xviii

In addition, the Feds is not satisfied with the capital plan submit by Bank of America and Goldman Sachs and asked these two banks resubmit their plans. Wells Fargo’s performance is highly rated by Feds because the company is working its best to adjust new regulation and maximize shareholder’s equity. Wells Fargo’s capital plan shows the company is going to pay its dividends to 0.35 per share and repurchase additional 350 million shares in the next year.

The figure shows the tier 1 common ratio results of the stress tests:

Source from: Forbesxix

Peer competition As Warren Buffet’s favorite bank and Berkshire Hathaway’s largest equity holding stock, Wells Fargo occupies a competitive position in the industry. According to the newest report released this May, Wells Fargo is the only bank that had positive shares that grow by 8% among its peers. Other big banks like JPMorgan Chase decreased 8% of its share, Citigroup decreased 11% of its share and Bank of America decreased 7%.Xx That main reason of Wells Fargo’s success is its old fashioned operation method, which includes mortgage lending, credit cards, debits cards, deposits and loans business. These traditional banking businesses helped Wells Fargo generate a large amount of profits.

Page 5

Source from: our own valuation and Buzz.Moneyxxi

Company Analysis

Company Business Description Wells Fargo & Company was founded in 1956 in San Francisco, California. The company is the fourth largest bank holding company in the United States, with $1.5 trillion in assets, $1.1 trillion in deposits and $170 billion stockholders’ equity by the end of fiscal year 2013.xxii Wells Fargo & Co is a diversified community based financial services and bank holding company, which operates mainly in the United States with partial business in other countries. It has three main operating segments, including Community Banking, Wholesale Banking, and Wealth, Brokerage and Retirement.xxiii Community Banking focuses on individual customers and small businesses. The company provides diversified financial products and services, such as borrowing and lending, and issuing debit cards and mortgages to its customers. It was the second largest issuer of debit cards in the U.S. in 2013.

Source from: Nilson Report xxiv

As its name reflects, the Wholesale Banking segment deals with larger institutional customers across the country. The Wealth, Brokerage and Retirement segment focuses more on financial services such as investment advisory. Community banking consists of nearly 60% of Wells Fargo & Company’s total revenue.xxv

Corporate Strategy All the business strategies that Wells Fargo has are in order to achieve its core vision, which is to satisfy all of its customers’ financial needs, help customers succeed financially, and be recognized as the premier financial services company in its market.xxvi The primary business strategy that Wells Fargo has is increasing the number of its financial products and providing high-quality financial products and services to satisfy its customers’ needs.xxvii

Cross-selling enables Wells Fargo to maximize the profit from each customer and increases its customer loyalty through offering customers the products and services they need, when they need them, to help them succeed financially.

Wells Fargo use technology to personalize service to customers.

Wells Fargo has a Customer-Centric business strategy- “We start with what the customer needs, not with what we want to sell.”xxviii

Financial Summary Along with the thriving of the whole economy and the financial industry, Wells Fargo had a strong year with a 16 percent increase in its net income, reaching $21.9 billion. It generated $83.3 billion in revenue in fiscal year 2013 and increased its diluted earnings per common share by 16 percent to $3.89. Wells Fargo increased its loans and deposits in 2013. The total loans at the end of 2013 were $825.8 billion and the total deposits reached a record of $1.1 trillion. Wells Fargo divides its loans into a commercial segment and a customer segment. In 2013, the commercial segment loans had a $20.7 billion increase and customer loans had a $19.2 billion increase. xxix The strong financial performance in 2013 made Wells Fargo the most profitable U.S. bank and it ranked as the world’s most valuable bank by market capitalization. xxx

Products and Services Community Banking Community banking offers consumers and small businesses with diversified financial products and services, such as investment, insurance, mortgage and home equity loans, and trust services. The community banking segment includes retail banking, small business banking, regional banking, and Wells Fargo Home Lending business units. xxxi

The community banking segment generated $12.7 billion in net income in 2013, increased 21% compared to 2012. However, its revenue decreased $3.1 billion by 6 percent compared with $53.4 billion in 2012. The increase in net income mainly results from the decrease in provision of credit losses and non-interest expenses.

We believe the consumer loans will increase by 4.2% and the commercial loans will increase by 3.8% in 2014. We think that

Page 6

consumer loans will increase because consumer confidence was increasing during year 2014. On October 28th, consumer confidence reached 94.5, which reflects consumers’ optimism in the outlook of both jobs and incomes that will boost personal consumption and increase loans. We believe that mortgages and automobile loans will increase by 5% and credit cards and other loans will increase by 2% and 3% respectively.

Wholesale Banking Wholesale banking includes Middle Market Commercial Banking, Government and Institutional Banking, Corporate Banking, Commercial Real Estate, Treasury Management, Corporate Trust and Assets Management. Wholesale Banking reported a 5% increase in net income of $8.1 billion in 2013 compared to net income of $7.8 billion in 2012. The increase in net income also comes from the decrease in provision of credit loss and strong growth in asset backed finance, asset management capital markets and corporate banking. xxxii

We believe wholesale banking will continue to grow because real estate mortgages, real estate construction and commercial and industrial loans will continue to grow as the result of the growing economy. We expect commercial and industrial loans and real estate mortgage loans to increase by 4% in 2014.

Wealth, Brokerage and Retirements Wealth, Brokerage and Retirement provides a full range of financial advisory services to clients. Services includes wealth management solutions (financial planning, private banking, credit, investment management, and fiduciary services.)xxxiii

Wealth, Brokerage and Retirements reported a net income of $1.7 billion in 2013, up 29% from 2012. The increase in net income results from improvement in credit quality and growth in loan balance.

We forecast that the Wealth, Brokerage and Retirement segment will have a slight increase in 2014. We expect the insurance fee to increase by 2% and the trust and investment fees to increase by 6.8% in 2014.

(Source from: Wells Fargo Annual Report 2013)xxxiv

Marketing Strategy Wells Fargo has a core vision in building strong and life-time relationships with its customers. Therefore increasing financial products is a key of its marketing strategy. Cross-selling strategy and extending services geographically accelerate Wells Fargo’s ability to gain more new customers.

Analysis of Recent Earnings Release On October 14th, 2014, Wells Fargo released its 3rd quarter earnings report, which showed a continuing growth in both net income and diluted earnings per share compared to the prior year.

Net income of $5.7 billion, up 3% from third

quarter 2013 Diluted earnings per share up 3% to $1.02 from prior

year Revenue of $21.2 billion, up 4% ROA of 1.4% and ROE of 13.10%

The good financial performance in the 3rd quarter results from strong loan and deposit growth in 3rd quarter, 2014. The company did well in reducing and controlling its noninterest expenses. The efficiency ratio was 57.7 percent in third quarter 2014, decreased by 0.2% compared to 57.9 percent in the previous quarter. The continued improvement in credit quality helps the company maintain its loan losses at historical lows. The company only released $300 million from the allowance for credit losses, which reflects a better expectation of future economy. The net charge-offs were $668 million in third quarter 2014, decreased by $307 million from third quarter, 2013. Wells Fargo declared $3.6 billion of common stock dividend and net share repurchase including $1.0 billion forward share repurchase expected to settle in fourth quarter, 2014. We believe with the strong economic growth, Wells Fargo will continue to increase its net income and dividend in fourth quarter, 2014.

Competition Analysis The diversified financial industry within the financial sector is highly correlated with the S&P 500 index, which has strong performance in 2013. The competition within the industry is highly competitive. The main competitors of Wells Fargo include U.S. Bancorp, Bank of American Corporation, JPM Chase &Co., and CitiGroup Inc.

Key statistics comparison between WFC and its competitors: (For Fiscal Year 2013)

Source from: Retrieved from Bloomberg, Comparative Analytics, Relative Valuationxxxv

Page 7

As the comparison table above states, Wells Fargo has the highest market capitalization among its competitors. Both its Return on Equity and Return on Assets ratios are above the average of its competitors. We believe Wells Fargo is very competitive among its peers because Wells Fargo has a relatively high net interest margin, which accounts for its high net income level. In addition, Wells Fargo has a high dividend yield of 2.62%, which is very attractive to most investors. The current and forward economic outlook is very positive. With the recovery of economy and improvement in the housing market, we believe Wells Fargo can boost its profitability by increasing its loans and deposits. In addition, Wells Fargo’s reputation was not severely damaged during the financial crisis between 2008 and 2012. As a result, it has a competitive advantage compared to its competitors.

Below is the one year stock price performance comparison of five companies.

Even though the diversified financial industry is relatively mature and intensely competitive, Wells Fargo has a unique advantage among its competitors. The cross-selling business strategy provides appropriate products and services to the right customers. The cross-selling strategy allows Wells Fargo to maximize the profit from each customer and increases its customer loyalty through enhancing the connections between the company and its customers. The focus on technological development is a competitive advantage for Wells Fargo because it helps Wells Fargo develop a better customer database and personalize products to its customers.

Dividends Payout Plan Dividends payout plan is restricted by the regulatory policies as well as capital guidelines. As a financial holding and bank holding company, Wells Fargo & Company’s capital actions are regulated under the New Capital Rule forced by the Federal Reserve. The Dodd-Frank Act enforces straightforward capital ratios that must be achieved by all bank holding companies, including Wells Fargo & Company. In March 2014, the Federal Reserve released the report of “Supervisory Stress Test Methodology and Results” projected minimum Tier 1 common ratio for all bank holding companies from quarter 4, 2014 to quarter 4, 2015. Among 30 participants, Wells Fargo & Company generated a projected Tier 1 common ratio of 8.2%. This ratio might be low because it just reaches the median performance among 30 participants.

Exhibit below is Wells Fargo’s dividend history from 2004 to 2014

Source from: Wells Fargo, Stock Price and Dividendxxxvii

Wells Fargo currently has a dividend payout ratio of 29%. The approved capital plan of Wells Fargo & Company includes an increase of 350 million additional share buybacks in 2014. In addition, dividend per share increases by 16.7% from 0.30 cents per share in 2013 to 0.35 cents per share in 2014.xxxviii According to this modest capital plan, we value the stock of Wells Fargo & Company because it focuses on its stabilities and holds a conservative strategy. We project that the dividend payout ratio will rise to 33% in 2014 because of Wells Fargo’s modest capital plan and better future credit quality.

Government Regulation The diversified financial industry is heavily regulated by the Office of the Comptroller of Currency, the Federal Reserve Board and the Federal Deposit Insurance Corporation (FDIC). Regulations can help and hurt Wells Fargo at the same time. Basel capital and liquidity standards and FRB guidelines and rules require Wells Fargo to have higher capital reserve, which will limit Wells Fargo’s reinvestment and retain activities. After the financial crisis in 2008, Wells Fargo and other financial institutions were subjected to a series of new regulations, such as new minimum capital reserve for companies’ subsidiaries. The regulatory environment will have significant influence on the dividend payout policies, the type of assets to invest in and other financing and investing activities.

The increasing trend of Wells Fargo’s Equity/Asset ratio is strong evidence that Wells Fargo has made most necessary adjustments for the new regulations. From our valuation model, Wells Fargo currently has 13.15% of return on equity in 2013 and the ROE ratio will decrease to 12.81% as a result of the FDIC’s new regulation that requires banks to hold more capital reserves and the type of risky assets that banks can invest in. However, we believe the government regulation on capital reserves and interest rates will ease in three to five years along with the recovery of the economy. Therefore, the Return on Equity will start to increase in year 2017 and beyond.

Catalysts for Growth/Change A robust recovering economy could be a catalyst for

growing earnings for Wells Fargo & Company. Since Wells Fargo & Company adopts conservative growth strategy; we

Source from: Yahoo! Financexxxvi

Page 8

believe if the economy is really recovering rather than only nominal indicators, Wells Fargo & Company would benefit from its recent stable performances. In addition, with the improvement in consumer confidence and unemployment, we expect a strong growth in commercial loans, consumer loans and interest-bearing deposits. Wells Fargo can increase its net interest margin by increasing its loans and deposits in 2014.

The brand of Wells Fargo & Company is another strong catalyst for its growth. Among the other big four banks in the U.S. (JPMorgan Chase, Bank of America, Citigroup, U.S. Bank), Wells Fargo & Company has the smallest asset size. However, it has the largest market capitalization ($264.2 billions) among the big four banks.xxxix As we can see, Wells Fargo & Company is a valuable investment decision.

S.W.O.T. Analysis Strengths/Opportunities

Wells Fargo has a powerful brand name and a highly recognized logo- the horse. The company has a great reputation among customers and good marketing and business strategy.

As the second largest bank in deposits, home mortgage servicing, and debit cards, WFC has a strong dividend and total payout ratio, and those ratios continue to grow.

Wells Fargo is not highly exposed to the global market, so it can prevent some currency risk and other international trade risks.

The company’s core value is people, both customers and employees. Wells Fargo has over 265,000 employeesxl. The company contributes to different volunteer works and pay back to its communities.

Weakness/ Threats WFC has less exposure to global business compared to

other financial companies, which might lose some good investment opportunities.

The financial industry is relatively mature, stable and highly competitive. Compared to Discover, and Citi Bank, Wells Fargo’s credit reward program is less attractive. There are threats of product substitution by other commercial banks

As the largest U.S mortgage lender, Wells Fargo is restricted by Federal policies. Changes in government regulation and the Federal Reserve rate will have influence on Wells Fargo’s business model.

Valuation Summary

We valued Wells Fargo under multiple valuation models, including Discounted Cash Flow/ Economic Profit model, Dividend Discount model and Relative model. Results are shown below:

We are confident in our Discounted Cash Flow Model because it reflects most of our assumptions compared to other models. We think the Dividend Discount Model is also reliable because Wells Fargo has a relative stable dividend payout ratio around 30%. As long as the growth rate of the dividend is not reasonable, the Dividend Discount Model can give us a conservative price forecast. The results from relative multiple models show Wells Fargo’s stock is greatly overvalued. We recognize there is a lot of bias in estimation of comparable firms’ future multiples and it is hard to track and analyze the differences between multiples across firms. For that reason, we think the relative multiple model’s results are not reliable.

Assumptions

Revenue Decomposition As a financial company, Wells Fargo’s revenue is largely driven by its interest income, which results from different interest-bearing earning assets. We segment interest-bearing earning assets into five main categories: Federal funds sold and other short investments, Trading Assets, Investment Securities, Loans, and Others.

Our key assumption under revenue decomposition is the growth of each earning assets and funding resources’ interest rate. In Wells Fargo’s own revenue decomposition table, they use the average balance of each earning assets, therefore they can maintain a stable interest rate across different years. In our revenue decomposition model, we use the same amount on the balance sheet for each earning assets due to lack of Wells Fargo’s daily transaction data. Since we have every earning assets’ balance, in order to get the interest income for each earning assets, the key assumption we have to make is the interest rate.

We expect the interest rate on Real estate 1-4 family first mortgage loan will increase to 4% in 2014 due to the increasing price of house and personal income. We also projected the interest rate of commercial and industrial loans increase to 3.75% in 2014 because of the improvement in economy. The increase in interest and non-interest bearing expense offset the increase in commercial and consumer loans’ interest income. In our revenue decomposition, loans weight more than 70 percent of interest-bearing earning assets that generate interest income. Consumer loans count around two third of total loans with estimated interest income of $22,792 million in 2014. The commercial loans will have estimated interest income of $14,335 million in 2014.

Dividend Discount Model Wells Fargo has relatively stable and consistent dividend payout to its shareholders. It paid $5,953 million in dividend in 2013 and has a dividend payout ratio of 29 percent. We assume the dividend declared per common share will increase to 1.40 in 2014, which can push up the dividend payout ratio to 33 percent. When calculating the intrinsic value by using the DDM model, we get a target price of $59.94. We think this price will be very close to the fair price because the assumption of dividend growth and dividend payout is conservatively reasonable.

Dividend Discount Model $59.94 Discounted Cash Flow/Economic Profit $61.78

Relative P/B $40.38Relative P/E (EPS 2014) $50.55Relative P/E (EPS 2015) $49.06

Page 9

Relative Multiple Models We select Bank of America Corporation, JPMorgan Chase & Co, CitiGroup, and U.S. Bancorp as Wells Fargo’s comparable firms because they are in the same industry and they are the five biggest banks in the United States. Besides the five banks, we also select Morgan Stanley and Goldman Sachs Group, Inc. as Wells Fargo’s comparable firms because some of Wells Fargo’s investment segment business overlapped with those two companies’ business.

The result from relative multiple model shows that Wells Fargo is largely overvalued now. The relative price over book model give us $ 40.38 and the relative P/E (EPS 2014) give us $50.55. We are not very confident in our relative multiple model because we believe Wells Fargo should be trade at a premium.

We believe the government regulation will change in a positive way for financial institutions along with the economy’s recovery in the future. Compared to other financial institutions, Wells Fargo has its relative advantage. Because it did not suffer a great loss and retained its great reputation during the financial crisis, therefore it can grow its deposits and loans at a faster rate than other financial institutions whose reputation was severely damaged during the financial crisis.

Moreover, we believe the future competition among financial institutions will be largely driven by technology. Since Wells Fargo has been dedicated in developing its technology-based products and services, we expect Wells Fargo can be traded at a premium.

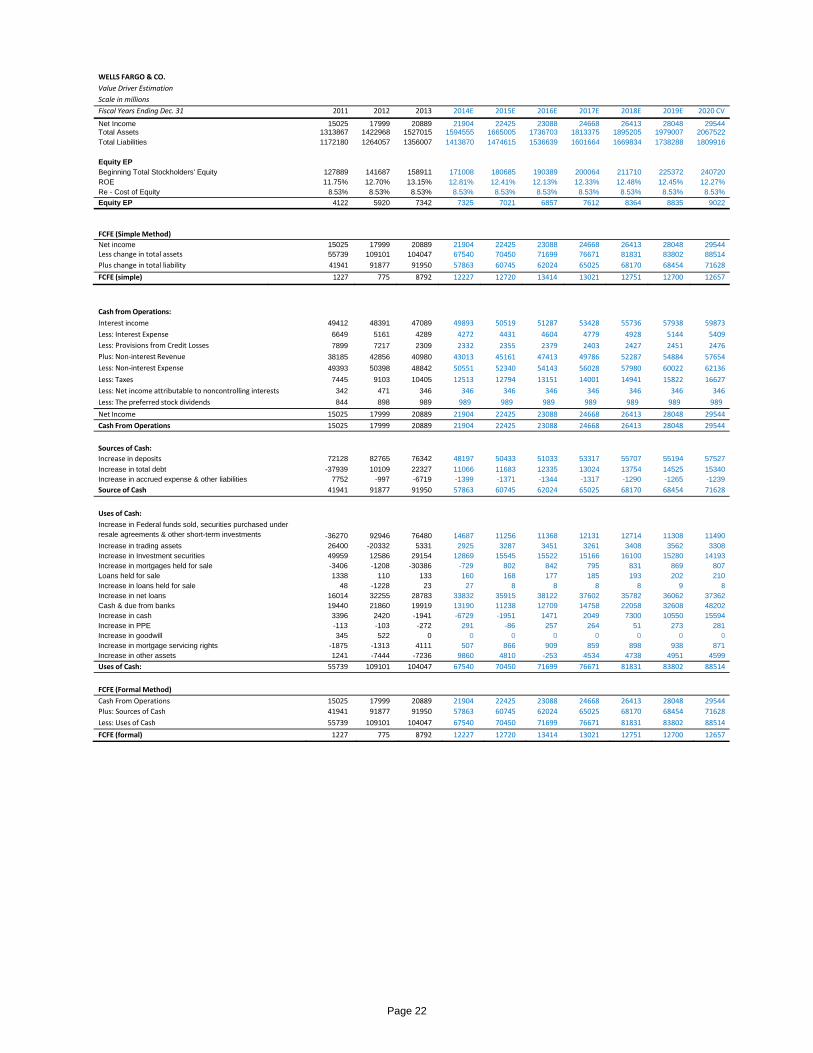

DCF and EP Models We believe DCF and EP models are the most accurate forecasts because DCF and EP model covered all of our key assumptions, which is relatively conservative and realistic. The most important assumptions in the calculation of DCF and EP models are cost of equity and FCFF. Details about assumption of cost of equity are shown below. The DCF and EP models give us the highest intrinsic price, $61.78. We think the price in DCF/ EP models is reasonable because considering the diversified business models and the stable growth that WFC has, we expected the stock price to grow in the future.

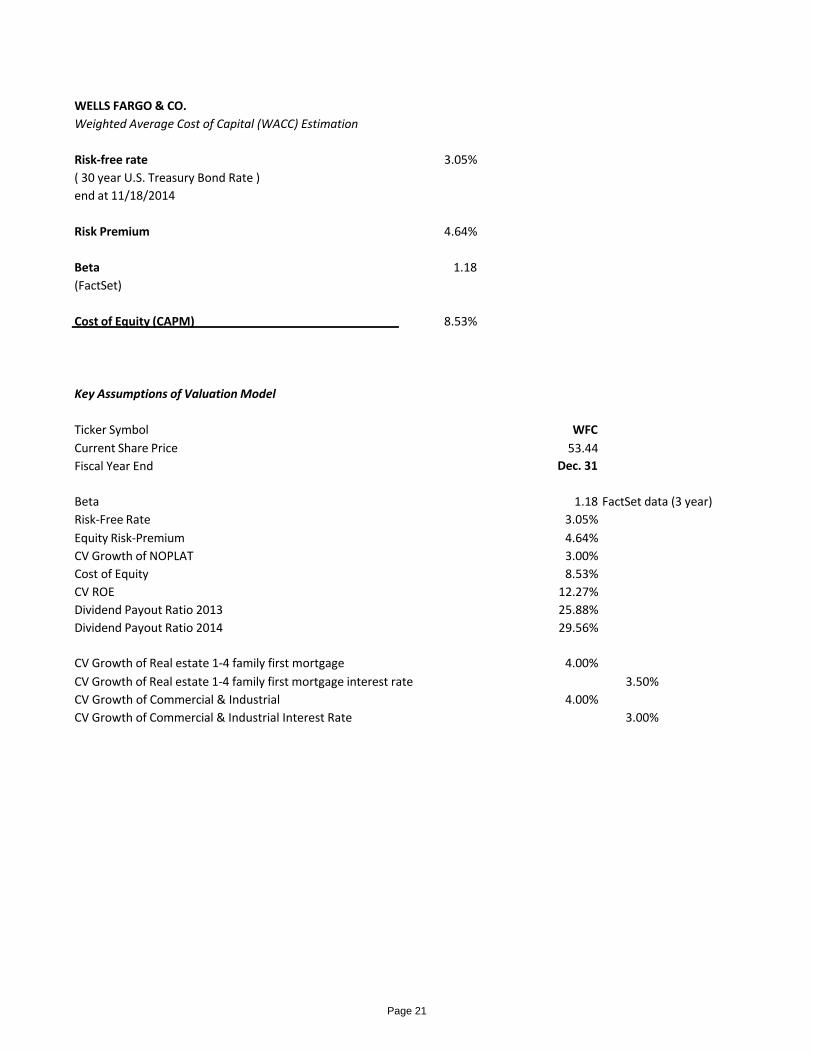

Cost of Equity As a financial firm, we use the cost of equity to forecast the future price instead of weighted average cost of capital. We use the Capital Asset Pricing Model to calculate the cost of equity. For the risk-free rate, we used 30-year long-term US Treasury Bond rate because it is the least risky investment, even it doesn’t match our forecast horizon. For the equity risk premium, we used the geometric average premiums because it considers the compounding of returns over the long horizon. For the equity beta, we first looked at the Bloomberg WFC raw beta, which is 0.98. We also looked up on Yahoo! Finance, the beta they have for WFC is 0.86.

However, after we compare Wells Fargo’s historical beta and its volatility level, we finally decided to use beta of 1.18 from FactSet.

Sensitivity Analysis

We understand that the assumptions we made in out models will have different levels of impact on the intrinsic value. It is hard to accurately predict the future stock price. Therefore, we develop a sensitivity analysis to analyze those key assumptions’ impact on our intrinsic value under different scenarios, including the best case, the worst case and the realistic case. We put the target price in the top-left corner in the data table. Since we are most confident in our Discounted Cash Flow model, we use the partial year adjusted price from the Discount Cash Flow model in this sensitivity analysis.

Beta & CV Growth

The first sensitivity analysis tests the impact of beta and continuing value of growth on price. Beta is an important element in terms of calculating cost of equity. The continuing value of the growth rate is also essential in the calculation of both DCF and DDM models. Increase in beta will lower the price. When the beta increased from 1.18 to 1.23 by +0.05, the price decreased $2.57. Compared to beta, continuing value of growth has less impact on price. For instance, +0.05 increase in continuing value of growth will only rise $0.31 of the price. Beta measures a stock’s volatility, the degree to which its price fluctuates in relation to the S&P 500.xli Therefore, if the S&P 500 index and Wells Fargo is doing well, the beta will decrease, and vice versa.

CV ROE & CV Growth

The second sensitivity analysis evaluates the impact of continuing value of Return on Equity and continuing value of growth on Price. Return on Equity is an essential factor for financial company because it measures financial companies’ profitability and it is one of the key assumptions in the DDM model. Both the continuing value of growth and the continuing value of ROE have a slight influence on price.

Page 10

(A 0.25% increase will result in a less than $0.30 change in price.) Return on Equity is calculated by the net income divided by shareholders’ equity. Therefore, if Wells Fargo continues to have growth in its net income and continues to manage its stock buyback and dividend payout programs appropriately, its ROE can grow in a stable rate.

CV ROE & Cost of Equity

We also test the effect of the cost of equity and continuing value of ROE on price. Cost of equity is a crucial factor in calculating of DDM and DCF/EP model. As we expected, cost of equity has significant influence on price. A 0.25 increase in cost of equity from 8.53% to 8.78% can lower price by $2.91. The cost of equity is calculated by using the CAPM, therefore, it is important for the company to manage their risk and reduce its volatility. The overall well-being of the economy and government’s Q1 policies will influence the risk-free rate, and then influence the cost of equity’s value in our model.

CV Growth of Real estate 1-4 family first mortgage interest rate & CV Growth of Real estate 1-4 family first mortgage

In the fourth sensitivity analysis, we test continuing value of growth of Real estate 1-4 family mortgage and its interest rate. Consumer loans count for about 30% of Wells Fargo’s total assets. Real estate 1-4 family mortgage has the largest proportion in consumer loans. Therefore, we think it is important to test the impact of Real estate 1-4 family mortgage on price. As we expected, change in interest rate significantly influences the price. For example, +0.50% increase(from 3.50% to 4.00%) in continuing value growth of real estate 1-4 family first mortgage interest rate will result a positive change in price by $2.64. The U.S. housing market is slowing recovery from the subprime mortgage crisis. During the past 3 years, the strict government regulation and rising interest rates have limited the growth of the housing market. With the economy’s recovery, we believe the government regulation will slowly ease in the next 5 years. We expect the demand for real estate mortgages to increase in the next 5 years as a result of increasing in jobs and income. The real estate 1-4 family mortgage interest rate will increase along with the increase in mortgage demand.

CV Growth of Commercial & Industrial interest rate & CV Growth of Commercial & Industrial

Lastly, we evaluate the impact of a continuing value of growth of commercial & industrial and its interest rate. Total commercial loans weighs about 25% of Wells Fargo’s total assets. More than half proportion of total commercial loans is commercial & industrial. Therefore, it is important to evaluate commercial & industrial loans. As the test result shows above, the change in continuing growth of commercial & industrial balance slightly influences price (+0.25% change from 4.00% to 4.25% results only $0.02 change in price). Compared to growth in commercial & industrial loan’s balance, growth in the interest rate of the commercial & industrial loans has a stronger impact on the price (+0.25% change from 3.00% to 3.25% results nearly $1 change in price). We predict that the demand of commercial and industrial loans will increase during the following 3 to 5 years as a result of strong performance of the economy and the market. Therefore, the growth in demand in commercial and industrial loans will boost its interest rate to 3.75% in 2014. Based on the sensitivity analysis, it is important for Wells Fargo to make and manage its interest rates on loans because change in those interest rates will largely influence its price performance.

Page 11

Important Disclaimer

This report was created by students enrolled in the Security Analysis (6F:112) class at the University of Iowa. The report was originally created to offer an internal investment recommendation for the University of Iowa Krause Fund and its advisory board. The report also provides potential employers and other interested parties an example of the students’ skills, knowledge and abilities. Members of the Krause Fund are not registered investment advisors, brokers or officially licensed financial professionals. The investment advice contained in this report does not represent an offer or solicitation to buy or sell any of the securities mentioned. Unless otherwise noted, facts and figures included in this report are from publicly available sources. This report is not a complete compilation of data, and its accuracy is not guaranteed. From time to time, the University of Iowa, its faculty, staff, students, or the Krause Fund may hold a financial interest in the companies mentioned in this report.

i Wells Fargo & Company (2013). From 10-K 2013, Page 1. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013_10K.pdf>

ii FactSet Research Systems. (n.d.). Wells Fargo & Company, Retrieved November 18, 2014, from FactSet database.

iii October 2014 Real Estate Data. (2014, November 13). Retrieved November 18, 2014, from <http://www.realtor.com/data-portal/realestatestatistics>

iv Yahoo! Finance. Retrieved November 18, 2014, from <http://finance.yahoo.com/echarts?s=WFC+Interactive#%7B %22range%22%3A%221y%22%2C%22scale%22%3A%22l inear%22%7D>

v Pritzker, P., Doms, M., & Moyer, B. (2014, October 1). Measuring the Economy-A Primer on GDP and the National Income and Product Accounts. Retrieved November 18, 2014, from <http://www.bea.gov/national/pdf/nipa_primer.pdf>

vi Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, June 2014. (2014, June 18). Retrieved November 18, 2014, from <http://www.federalreserve.gov/monetarypolicy/files/fomcpr ojtabl20140618.pdf>

vii Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, June 2014. (2014, June 18). Retrieved November 18, 2014, from <http://www.federalreserve.gov/monetarypolicy/files/fomcpr ojtabl20140618.pdf>

viii Unemployment rate down to 6.1 percent in June: The Economics Daily: U.S. Bureau of Labor Statistics. (2014,

July 8). Retrieved November 18, 2014, from <http://www.bls.gov/opub/ted/2014/ted_20140708.htm#tab- 1>

ix Unemployment rate down to 6.1 percent in June: The Economics Daily: U.S. Bureau of Labor Statistics. (2014, July 8). Retrieved November 18, 2014, from <http://www.bls.gov/opub/ted/2014/ted_20140708.htm#tab- 1>

x Bloomberg L.P. (2014) CONCCONF Index 01/01/13 to 11/1/14. Retrieved November 18, 2014 from Bloomberg database

xi FactSet Research Systems. (n.d.). Wells Fargo & Company, Retrieved November 18, 2014, from FactSet database.

xii 30-Year Fixed-Rate Mortgages since 1971. (n.d.). Retrieved November 18, 2014, from <http://www.freddiemac.com/pmms/pmms30.htm>

xiii Press Release. (2014, November 13). Retrieved November 18, 2014, from <http://www.federalreserve.gov/newsevents/press/bcreg/201 41113a.htm>

xiv Press Release. (2014, November 13). Retrieved November 18, 2014, from <http://www.federalreserve.gov/newsevents/press/bcreg/201 41113a.htm>

xv Current FAQsInforming the public about the Federal Reserve. (2014, November 3). Retrieved November 18, 2014, from <http://www.federalreserve.gov/faqs/money_12849.htm>

xvi Wells Fargo & Company, Annual Company –Run Stress Test Results. (2014, March 20). Retrieved November 18, 2014, from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/stress-test-results-2014.pdf>

xvii Touryalai, H. (2014, March 20). Stress Test Results: Big Banks Look Healthier As 29 of 30 Pass, Zions Fails. Retrieved November 18, 2014, from <http://www.forbes.com/sites/halahtouryalai/2014/03/20 /stress-test-results-big-banks-look-healthier-as-29-of-30- pass-zion-fails/>

xviii Gandel, S. (2014, March 26). Citi and four other banks stumble in Fed stress tests. Retrieved November 18, 2014, from <http://fortune.com/2014/03/26/citi-and-four-other- banks-stumble-in-fed-stress- tests/?utm_content=buffer38fa8&utm_medium=social&utm_ source=facebook.com&utm_campaign=buffer/>

Page 12

xix Touryalai, H. (2014, March 20). Stress Test Results: Big Banks Look Healthier As 29 of 30 Pass, Zions Fails. Retrieved November 18, 2014, from <http://www.forbes.com/sites/halahtouryalai/2014/03/20 /stress-test-results-big-banks-look-healthier-as-29-of-30- pass-zion-fails/>

xx Monica, P. (2014, March 20). Warren Buffett's favorite bank -- Wells Fargo -- isn't like the others - The Buzz - Investment and Stock Market News. Retrieved November 18, 2014, from <http://buzz.money.cnn.com/2014/05/20/wells-fargo-stock/>

xxi Monica, P. (2014, March 20). Warren Buffett's favorite bank -- Wells Fargo -- isn't like the others - The Buzz - Investment and Stock Market News. Retrieved November 18, 2014, from <http://buzz.money.cnn.com/2014/05/20/wells-fargo-stock/>

xxii Wells Fargo & Company (2013). From 10-K 2013, Page 1. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013_10K.pdf>

xxiii FactSet Research Systems. (n.d.). Wells Fargo & Company, Business Description, Retrieved November 18, 2014, from FactSet database.

xxiv Charts & Graphs Archive. (2014, November 1). Retrieved November 18, 2014, from <http://www.nilsonreport.com/publication_chart_and_graphs _archive.php?1=1&year=2014>

xxv FactSet Research Systems. (n.d.). Wells Fargo & Company, Segments, Retrieved November 18, 2014, from FactSet database.

xxvi Wells Fargo & Company. (2014). Annual report 2013. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013-annual-report.pdf>

xxvii Wells Fargo & Company. (2014). Annual report 2013. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013-annual-report.pdf>

xxviii Wells Fargo Strategy. (1999, January 1). Retrieved November 18, 2014, from <https://www.wellsfargo.com/invest_relations/vision_values/ 6>

xxix Wells Fargo & Company. (2014). Annual report 2013. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013-annual-report.pdf>

xxx Wells Fargo & Company. (2014). Annual report 2013. Page 3. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013-annual-report.pdf>

xxxi Wells Fargo & Company. (2014). Annual report 2013. Page 44. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013-annual-report.pdf>

xxxii Wells Fargo & Company. (2014). Annual report 2013. Page 44. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013-annual-report.pdf>

xxxiii FactSet Research Systems. (n.d.). Wells Fargo & Company, Comparative Statistics, Retrieved November 18, 2014, from FactSet database.

xxxiv Wells Fargo & Company. (2014). Annual report 2013. Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013-annual-report.pdf>

xxxv Bloomberg L.P. (2014) Relative Valuation. Retrieved November 18, 2014 from Bloomberg database

xxxvi Yahoo! Finance. Retrieved November 18, 2014, from <http://finance.yahoo.com/echarts?s=WFC+Interactive#%7B %22range%22%3A%221y%22%2C%22scale%22%3A%22l inear%22%2C%22comparisons%22%3A%7B%22USB%22 %3A%7B%22color%22%3A%22%23cc0000%22%2C%22 weight%22%3A1%7D%2C%22JPM%22%3A%7B%22color %22%3A%22%23009999%22%2C%22weight%22%3A1% 7D%2C%22C%22%3A%7B%22color%22%3A%22%23ff0 0ff%22%2C%22weight%22%3A1%7D%2C%22BAC%22% 3A%7B%22color%22%3A%22%239900ff%22%2C%22wei ght%22%3A1%7D%7D%7D >

xxxvii Stock Price and Dividends. (n.d.). Retrieved November 18, 2014, from <https://www.wellsfargo.com/invest_relations/dividend>

xxxviii Wells Fargo (WFC) Plans Modest Dividend, Buyback Increase Following CCAR Results. (2014, March 26). Retrieved November 18, 2014, from <http://www.streetinsider.com/Dividend Hike/Wells Fargo (WFC) Plans Modest Dividend, Buyback Increase Following CCAR Results/9319992.html>

xxxix Morris, P. (2014, May 27). 1 More Reason Warren Buffett Owns $23 Billion of Wells Fargo Inc. Retrieved November 18, 2014, from <http://www.fool.com/investing/general/2014/05/27/1-more- reason-warren-buffett-owns-23-billion-of-we.aspx>

Page 13

xl Wells Fargo & Company (2013). From 10-K 2013, Retrieved from <https://www08.wellsfargomedia.com/downloads/pdf/invest _relations/2013_10K.pdf>

xli Beta: Measuring a Stock?s Volatility |Growth Stocks and Beta. (n.d.). Retrieved November 18, 2014, from <http://www.zacks.com/education/articles.php?id=58>

Page 14

WELLS FARGO & CO. Revenue Decomposition Scale in millions

Fiscal Years Ending Dec. 31 2011 2012 2013 2014E 2015E 2016E 2017E 2018E 2019E 2020 CV

Earning assets Federal funds sold, securities purchased under resale agreements and other short‐ term investments

345

378

489

685

719

753

790

828

862

896

Trading assets 1463 1380 1406 1578 1712 1783 1848 1915 1985 2047

Investment Securities: Total available‐for ‐sale securities 9107 8757 8819 9259 9781 10301 10810 11351 11861 12336

Loans: Commercial: Commercial and industrial 6894 6981 6807 7691 7466 7210 6921 7198 7486 7785

Real estate mortgage 4163 4411 4147 4177 4054 4518 5012 5187 5343 5503

Real estate construction 1055 894 784 693 676 659 735 811 835 860

Lease Financing 976 921 738 713 702 789 745 767 790 814

Foreign 941 984 946 1061 1026 1072 1255 1160 1200 1242

Total Commercial 14029 14191 13422 14335 13924 14248 14667 15123 15655 16205

Consumer: Real estate 1‐4 family first mortgage 11090 10671 10716 10857 10687 10473 10945 11383 11838 12311

Real estate 1‐4 family junior lien mortgage 3926 3457 3013 2844 2894 2960 3071 3169 3248 3313

Credit card 2794 2885 3083 3385 3369 3359 3374 3501 3571 3549

Automobile 3555 3390 3365 3494 3641 3382 3657 3835 4155 4321

Other revolving credit and installment 1908 1923 2019 2212 2506 2699 2901 3237 3334 3434

Total consumer 23273 22326 22196 22792 23098 22873 23947 25125 26145 26929

Total Loans 37302 36517 35618 37127 37022 37121 38614 40248 41800 43134

other 548 587 723 746 770 795 820 836 853 870

Held‐to‐maturity securities 0 0 22 405 426 447 467 488 510 530

Mortgages held for sale 1644 1825 1290 1170 1221 1273 1321 1371 1422 1469

Loans Held for sale 58 41 13 13 13 14 15 15 16 17

Total Earning Assets 50467 49485 48380 50984 51664 52487 54685 57052 59310 61299

Funding Resource Deposits: Interest‐bearing checking 40 19 22 25 26 27 29 30 31 33

Market rate and other savings 836 592 450 492 516 541 567 594 621 649

Savings certificates 995 782 559 581 641 704 738 773 808 844

Other time deposits 268 225 194 229 241 252 264 277 290 303

Deposits in foreign offices 136 109 112 116 113 110 115 120 126 132

Total interest‐bearing deposits 2275 1727 1337 1444 1538 1634 1713 1795 1876 1960

short‐term borrowing 94 94 71 84 87 90 93 96 99 103

Long‐term debt 3978 3110 2585 2433 2493 2551 2608 2662 2821 2991

Other liabilities 316 245 307 312 314 329 366 375 347 356

Total interest‐bearing liabilities 6663 5176 4300 4272 4431 4604 4779 4928 5144 5409

Total funding sources 6663 5176 4300 4272 4431 4604 4779 4928 5144 5409

Page 15

WELLS FARGO & CO. Income Statement Scale in millions

Fiscal Years Ending Dec. 31 2011 2012 2013 2014E 2015E 2016E 2017E 2018E 2019E 2020 CV

Interest Income Interest income on trading assets

1440

1358

1376

1578

1712

1783

1848

1915

1985

2047

Interest income on securities available for sale 8475 8098 8116 9259 9781 10301 10810 11351 11861 12336 Interest income on mortgages held for sale 1644 1825 1290 1170 1221 1273 1321 1371 1422 1469 Interest income on loans held for sale 58 41 13 13 13 14 15 15 16 17 Interest income on loans 37247 36482 35571 37127 37022 37121 38614 40248 41800 43134 Other interest income 548 587 723 746 770 795 820 836 853 870

Total interest income 49412 48391 47089 49893 50519 51287 53428 55736 57938 59873 Interest Expense Interest expenses on deposits

2275

1727

1337

1444

1538

1634

1713

1795

1876

1960

Interest expenses on short-term borrowings 80 79 60 84 87 90 93 96 99 103 Interest expenses on long-term debt 3978 3110 2585 2433 2493 2551 2608 2662 2821 2991 Other interest expense 316 245 307 312 314 329 366 375 347 356

Total interest expense 6649 5161 4289 4272 4431 4604 4779 4928 5144 5409 Net interest income 42763 43230 42800 45622 46088 46683 48649 50808 52794 54463 Provision for credit losses 7899 7217 2309 2332 2355 2379 2403 2427 2451 2476

Net interest income after provision for credit losses 34864 36013 40491 43289 43732 44304 46246 48382 50343 51988 Noninterest Income Service charges on deposit accounts

4280

4683

5023

5375

5751

6153

6584

7045

7538

8066

Trust & investment fees 11304 11890 13430 14343 15319 16391 17538 18801 20155 21626 Card fees 3653 2838 3191 3319 3451 3589 3733 3864 3999 4139 Other fees 4193 4519 4340 4492 4649 4812 4980 5130 5284 5442 Mortgage banking 7832 11638 8774 9125 9490 9822 10166 10522 10837 11162 Insurance 1960 1850 1814 1850 1887 1925 1964 2003 2043 2084 Net gains from trading activities 1014 1707 1623 1672 1722 1773 1818 1863 1910 1958 Net gains (losses) on debt securities available for sale 54 (128) (29) (29) (29) (29) (29) (29) (29) (29) Net gains (losses) from equity investments 1482 1485 1472 1501 1531 1562 1593 1625 1658 1691 Operating leases 524 567 663 673 683 693 704 714 725 736 Other non-interest income 1889 1807 679 693 706 721 735 750 765 780

Total noninterest income 38185 42856 40980 43013 45161 47413 49786 52287 54884 57654 Noninterest Expense Salaries expense

14462

14689

15152

15834

16546

17274

18034

18810

19619

20443

Commission & incentive compensation 8857 9504 9951 10548 11181 11796 12445 13129 13851 14613 Employee benefits expense 4348 4611 5033 5285 5549 5826 6118 6424 6745 7082 Equipment expense 2283 2068 1984 2024 2064 2105 2148 2190 2234 2279 Net occupancy expense Operating leases expense Core deposit and other intangibles

3011 -

1880

2857 -

1674

2895 -

1504

2895

1519

2895

1534

2895

1550

2895

1565

2895

1581

2895

1597

2895

1612 FDIC & other deposit assessments 1266 1356 961 971 980 990 1000 1010 1020 1030 Other non-interest expenses 13286 13639 11362 11476 11590 11706 11823 11942 12061 12182

Total non-interest expenses 49393 50398 48842 50551 52340 54143 56028 57980 60022 62136 Income (loss) before income tax expense 23656 28471 32629 35752 36553 37574 40004 42688 45205 47506 Income tax expense 7445 9103 10405 12513 12794 13151 14001 14941 15822 16627

Net income (loss) before non-controlling interests 16211 19368 22224 23239 23760 24423 26003 27748 29383 30879 Net income attributable to non-controlling interests (342) (471) (346) (346) (346) (346) (346) (346) (346) (346)Net income attributable to Wells Fargo 15869 18897 21878 22893 23414 24077 25657 27402 29037 30533

Less: Preferred stock dividends and other 844 898 989 989 989 989 989 989 989 989Net income (loss) applicable to common stock 15025 17999 20889 21904 22425 23088 24668 26413 28048 29544

Per share information Net earnings (loss) per share - basic

2.85

3.4

3.89

4.19

4.33

4.49

4.82

5.18

5.51

5.80

Dividends declared per common share 0.48 0.88 1.15 1.40 1.65 1.95 1.95 1.95 1.95 1.95 Year end shares outstanding 5263 5266 5257 5198 5153 5125 5108 5098 5092 5090

Dividend pay 2526 4634 6046 7278 8512 9991 9957 9938 9926 9923

Page 16

WELLS FARGO & CO. Common Size Income Statement Scale in millions

Fiscal Years Ending Dec. 31 2011 2012 2013 2014E 2015E 2016E 2017E 2018E 2019E 2020 CV

Interest Income Interest income on trading assets 0.11% 0.10% 0.09% 0.10% 0.10% 0.10% 0.10% 0.10% 0.10% 0.10%Interest income on securities available for sale 0.65% 0.57% 0.53% 0.58% 0.58% 0.58% 0.59% 0.59% 0.59% 0.59%Interest income on mortgages held for sale 0.13% 0.13% 0.08% 0.07% 0.07% 0.07% 0.07% 0.07% 0.07% 0.07%Interest income on loans held for sale 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Interest income on loans 2.83% 2.56% 2.33% 2.33% 2.22% 2.14% 2.13% 2.12% 2.11% 2.09%Other interest income 0.04% 0.04% 0.05% 0.05% 0.05% 0.05% 0.05% 0.04% 0.04% 0.04%Total interest income 3.76% 3.40% 3.08% 3.13% 3.03% 2.95% 2.95% 2.94% 2.93% 2.90%Interest Expense Interest expenses on deposits 0.17% 0.12% 0.09% 0.09% 0.09% 0.09% 0.09% 0.09% 0.09% 0.09%Interest expenses on short-term borrowings 0.01% 0.01% 0.00% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.00%Interest expenses on long-term debt 0.30% 0.22% 0.17% 0.15% 0.15% 0.15% 0.14% 0.14% 0.14% 0.14%Other interest expense 0.02% 0.02% 0.02% 0.02% 0.02% 0.02% 0.02% 0.02% 0.02% 0.02%Total interest expense 0.51% 0.36% 0.28% 0.27% 0.27% 0.27% 0.26% 0.26% 0.26% 0.26%Net interest income 3.25% 3.04% 2.80% 2.86% 2.77% 2.69% 2.68% 2.68% 2.67% 2.63%Provision for credit losses 0.60% 0.51% 0.15% 0.15% 0.14% 0.14% 0.13% 0.13% 0.12% 0.12%Net interest income after provision for credit losses 2.65% 2.53% 2.65% 2.71% 2.63% 2.55% 2.55% 2.55% 2.54% 2.51%Noninterest Income Service charges on deposit accounts 0.33% 0.33% 0.33% 0.34% 0.35% 0.35% 0.36% 0.37% 0.38% 0.39%Trust & investment fees 0.86% 0.84% 0.88% 0.90% 0.92% 0.94% 0.97% 0.99% 1.02% 1.05%Card fees 0.28% 0.20% 0.21% 0.21% 0.21% 0.21% 0.21% 0.20% 0.20% 0.20%Other fees 0.32% 0.32% 0.28% 0.28% 0.28% 0.28% 0.27% 0.27% 0.27% 0.26%Mortgage banking 0.60% 0.82% 0.57% 0.57% 0.57% 0.57% 0.56% 0.56% 0.55% 0.54%Insurance 0.15% 0.13% 0.12% 0.12% 0.11% 0.11% 0.11% 0.11% 0.10% 0.10%Net gains from trading activities 0.08% 0.12% 0.11% 0.10% 0.10% 0.10% 0.10% 0.10% 0.10% 0.09%Net gains (losses) on debt securities available for sale 0.00% -0.01% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Net gains (losses) from equity investments 0.11% 0.10% 0.10% 0.09% 0.09% 0.09% 0.09% 0.09% 0.08% 0.08%Operating leases 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04%Other non-interest income 0.14% 0.13% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04%Total noninterest income 2.91% 3.01% 2.68% 2.70% 2.71% 2.73% 2.75% 2.76% 2.77% 2.79%Noninterest Expense Salaries expense 1.10% 1.03% 0.99% 0.99% 0.99% 0.99% 0.99% 0.99% 0.99% 0.99%Commission & incentive compensation 0.67% 0.67% 0.65% 0.66% 0.67% 0.68% 0.69% 0.69% 0.70% 0.71%Employee benefits expense 0.33% 0.32% 0.33% 0.33% 0.33% 0.34% 0.34% 0.34% 0.34% 0.34%Equipment expense 0.17% 0.15% 0.13% 0.13% 0.12% 0.12% 0.12% 0.12% 0.11% 0.11%Net occupancy expense 0.23% 0.20% 0.19% 0.18% 0.17% 0.17% 0.16% 0.15% 0.15% 0.14%Operating leases expense 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Core deposit and other intangibles 0.14% 0.12% 0.10% 0.10% 0.09% 0.09% 0.09% 0.08% 0.08% 0.08%FDIC & other deposit assessments 0.10% 0.10% 0.06% 0.06% 0.06% 0.06% 0.06% 0.05% 0.05% 0.05%Other non-interest expenses 1.01% 0.96% 0.74% 0.72% 0.70% 0.67% 0.65% 0.63% 0.61% 0.59%Total non-interest expenses 3.76% 3.54% 3.20% 3.17% 3.14% 3.12% 3.09% 3.06% 3.03% 3.01%Income (loss) before income tax expense 1.80% 2.00% 2.14% 2.24% 2.20% 2.16% 2.21% 2.25% 2.28% 2.30%Income tax expense 0.57% 0.64% 0.68% 0.78% 0.77% 0.76% 0.77% 0.79% 0.80% 0.80%Net income (loss) before non-controlling interests 1.23% 1.36% 1.46% 1.46% 1.43% 1.41% 1.43% 1.46% 1.48% 1.49%Net income attributable to non-controlling interests -0.03% -0.03% -0.02% -0.02% -0.02% -0.02% -0.02% -0.02% -0.02% -0.02%Net income attributable to Wells Fargo 1.21% 1.33% 1.43% 1.44% 1.41% 1.39% 1.41% 1.45% 1.47% 1.48%

Less: Preferred stock dividends and other 0.06% 0.06% 0.06% 0.06% 0.06% 0.06% 0.05% 0.05% 0.05% 0.05%Net income (loss) applicable to common stock 1.14% 1.26% 1.37% 1.37% 1.35% 1.33% 1.36% 1.39% 1.42% 1.43%

Page 17

WELLS FARGO & CO. Balance Sheet Scale in millions

Fiscal Years Ending Dec. 31 2011 2012 2013 2014E 2015E 2016E 2017E 2018E 2019E 2020 CV

Assets Cash & due from banks 19440 21860 19919 13190 11238 12709 14758 22058 32609 48203

Federal funds sold, securities purchased under resale agreements & other short- term investments 44367 137313 213793 228480 239735 251103 263234 275948 287257 298747 Trading assets 77814 57482 62813 65738 69025 72476 75738 79146 82707 86016 Investment securities available for sale 222613 235199 252007 264555 279467 294324 308861 324305 338898 352454 Investments securities held-to-maturity - - 12346 12667 13300 13965 14593 15250 15936 16574 Total Investment securities 222613 235199 264353 277222 292767 308289 323455 339555 354835 369028 Mortgages held for sale 48357 47149 16763 16034 16835 17677 18473 19304 20173 20979 Loans held for sale 1338 110 133 160 168 177 185 193 202 210 Loans: Commercial & industrial 167216 187759 197210 205098 213302 221834 230708 239936 249534 259515 Real estate mortgage 105975 106340 107100 111384 115839 120473 125292 129677 133567 137574 Real estate construction 19382 16904 16747 17333 18026 18838 19591 20277 20885 21512 Other real estate mortgage Lease financing 13117 12424 12034 12395 12767 13150 13544 13951 14369 14800 Foreign commercial 39760 37771 47665 49333 51307 53615 55760 57990 60020 62121

Total commercial loans 345450 361198 380756 395544 411242 427910 444895 461831 478375 495522 Consumer: real estate 1-4 family first mortgage 228894 249900 258497 271422 284993 299243 312709 325217 338226 351755 Consumer: real estate 1-4 family junior lien mortgage 85991 75465 65914 67232 68913 70980 73110 74572 76064 77585 Consumer: credit card 22836 24640 26870 27407 27956 28515 29085 29667 30260 30865 Consumer: automobile 43508 45998 50808 53348 56016 58817 61463 63922 66479 69138 Consumer: other revolving credit & installments 42952 42373 42954 44243 45570 46937 48345 49795 51289 52828

Total consumer loans 424181 438376 445043 463653 483447 504491 524712 543173 562317 582170 Total loans 769631 799574 825799 859196 894689 932402 969607 1005004 1040693 1077693 Less Allowance for loan losses 19372 17060 14502 14067 13645 13236 12839 12453 12080 11717

Net loans 750259 782514 811297 845129 881044 919166 956769 992551 1028613 1065975 Mortgage servicing rights-measured at fair value 12603 11538 15580 16034 16835 17677 18473 19304 20173 20979 Mortgage servicing rights-amortized 1408 1160 1229 1283 1347 1414 1478 1544 1614 1678 Premises & equipment, net 9531 9428 9156 9447 9361 9618 9883 9934 10207 10488 Goodwill 25115 25637 25637 25637 25637 25637 25637 25637 25637 25637 Other assets 101022 93578 86342 96202 101012 100760 105294 110032 114983 119583

Total assets 1313867 1422968 1527015 1594555 1665005 1736703 1813375 1895206 1979008 2067522

Liabilities Noninterest-bearing deposits 244003 288207 288117 296761 305663 314833 324278 334007 344027 354348 Interest-bearing deposits 676067 714628 791060 830613 872144 914007 957879 1003857 1049031 1096237

Total deposits 920070 1002835 1079177 1127374 1177807 1228840 1282157 1337864 1393057 1450585 Short-term borrowings 49091 57175 53883 55769 57721 59741 61832 63996 66236 68554 Accrued expenses & other liabilities 77665 76668 69949 68550 67179 65835 64519 63228 61964 60725 Long-term debt 125354 127379 152998 162178 171909 182223 193156 204746 217031 230052

Total liabilities 1172180 1264057 1356007 1413870 1474615 1536639 1601664 1669834 1738288 1809916

Equity Wells Fargo stockholders' equity:

Preferred stock 11431 12883 16267 16267 16267 16267 16267 16267 16267 16267 Common stock (net par and additional paid-in capital) 64888 68938 69432 70166 71320 72529 73779 75068 76390 77745 Retained earnings 64385 77679 92361 101487 110200 118797 129308 141782 155904 171525 Cumulative other comprehensive income (loss) 3207 5650 1386 1386 1386 1386 1386 1386 1386 1386 Treasury stock (2744) (6610) (8104) (8276) (8425) (8544) (8647) (8737) (8820) (8896) Unearned ESOP shares (926) (986) (1200) (1212) (1224) (1236) (1249) (1261) (1274) (1287)

Total Wells Fargo stockholders' equity 140241 157554 170142 179819 189523 199198 210844 224506 239854 256741 Noncontrolling interests 1446 1357 866 866 866 866 866 866 866 866

Total equity 141687 158911 171008 180685 190389 200064 211710 225372 240720 257607 Total Liabilities and equity 1313867 1422968 1527015 1594555 1665005 1736703 1813375 1895206 1979008 2067522

Page 18

WELLS FARGO & CO. Common Size Balance Sheet (as a percentage of total assets) Scale in millions

Fiscal Years Ending Dec. 31 2011 2012 2013 2014E 2015E 2016E 2017E 2018E 2019E 2020 CV

Assets Cash & due from banks 1.48% 1.54% 1.30% 0.83% 0.67% 0.73% 0.81% 1.16% 1.65% 2.33% Federal funds sold, securities purchased under resale agreements & other short-term investments 3.38% 9.65% 14.00% 14.33% 14.40% 14.46% 14.52% 14.56% 14.52% 14.45% Trading assets 5.92% 4.04% 4.11% 4.12% 4.15% 4.17% 4.18% 4.18% 4.18% 4.16% Investment securities 16.94% 16.53% 17.31% 17.39% 17.58% 17.75% 17.84% 17.92% 17.93% 17.85% Mortgages held for sale 3.68% 3.31% 1.10% 1.01% 1.01% 1.02% 1.02% 1.02% 1.02% 1.01% Loans held for sale 0.10% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% Loans: Commercial & industrial 12.73% 13.19% 12.91% 12.86% 12.81% 12.77% 12.72% 12.66% 12.61% 12.55% Real estate mortgage 8.07% 7.47% 7.01% 6.99% 6.96% 6.94% 6.91% 6.84% 6.75% 6.65% Real estate construction 1.48% 1.19% 1.10% 1.09% 1.08% 1.08% 1.08% 1.07% 1.06% 1.04% Other real estate mortgage Lease financing 1.00% 0.87% 0.79% 0.78% 0.77% 0.76% 0.75% 0.74% 0.73% 0.72% Foreign commercial 3.03% 2.65% 3.12% 3.09% 3.08% 3.09% 3.07% 3.06% 3.03% 3.00%

Total commercial loans 26.29% 25.38% 24.93% 24.81% 24.70% 24.64% 24.53% 24.37% 24.17% 23.97% Consumer: real estate 1-4 family first mortgage 17.42% 17.56% 16.93% 17.02% 17.12% 17.23% 17.24% 17.16% 17.09% 17.01% Consumer: real estate 1-4 family junior lien mortgage 6.54% 5.30% 4.32% 4.22% 4.14% 4.09% 4.03% 3.93% 3.84% 3.75% Consumer: credit card 1.74% 1.73% 1.76% 1.72% 1.68% 1.64% 1.60% 1.57% 1.53% 1.49% Consumer: automobile 2.85% 3.01% 3.33% 3.35% 3.36% 3.39% 3.39% 3.37% 3.36% 3.34% Consumer: other revolving credit & installments 3.27% 2.98% 2.81% 2.77% 2.74% 2.70% 2.67% 2.63% 2.59% 2.56%

Total consumer loans 32.28% 30.81% 29.14% 29.08% 29.04% 29.05% 28.94% 28.66% 28.41% 28.16% Total loans 58.58% 56.19% 54.08% 53.88% 53.73% 53.69% 53.47% 53.03% 52.59% 52.12% Less Allowance for loan losses 1.47% 1.20% 0.95% 0.88% 0.82% 0.76% 0.71% 0.66% 0.61% 0.57%

Net loans 57.10% 54.99% 53.13% 53.00% 52.92% 52.93% 52.76% 52.37% 51.98% 51.56% Mortgage servicing rights-measured at fair value 0.96% 0.81% 1.02% 1.01% 1.01% 1.02% 1.02% 1.02% 1.02% 1.01% Mortgage servicing rights-amortized 0.11% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% 0.08% Premises & equipment, net 0.73% 0.66% 0.60% 0.59% 0.56% 0.55% 0.54% 0.52% 0.52% 0.51% Goodwill 1.91% 1.80% 1.68% 1.61% 1.54% 1.48% 1.41% 1.35% 1.30% 1.24% Other assets 7.69% 6.58% 5.65% 6.03% 6.07% 5.80% 5.81% 5.81% 5.81% 5.78%

Total assets 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Liabilities Noninterest-bearing deposits 18.57% 20.25% 18.87% 18.61% 18.36% 18.13% 17.88% 17.62% 17.38% 17.14% Interest-bearing deposits 51.46% 50.22% 51.80% 52.09% 52.38% 52.63% 52.82% 52.97% 53.01% 53.02%

Total deposits 70.03% 70.47% 70.67% 70.70% 70.74% 70.76% 70.71% 70.59% 70.39% 70.16% Short-term borrowings 3.74% 4.02% 3.53% 3.50% 3.47% 3.44% 3.41% 3.38% 3.35% 3.32% Accrued expenses & other liabilities 5.91% 5.39% 4.58% 4.30% 4.03% 3.79% 3.56% 3.34% 3.13% 2.94% Long-term debt 9.54% 8.95% 10.02% 10.17% 10.32% 10.49% 10.65% 10.80% 10.97% 11.13%

Total liabilities 89.22% 88.83% 88.80% 88.67% 88.57% 88.48% 88.33% 88.11% 87.84% 87.54%

Equity Wells Fargo stockholders' equity:

Preferred stock 0.87% 0.91% 1.07% 1.02% 0.98% 0.94% 0.90% 0.86% 0.82% 0.79% Common stock (net additional paid-in capital) 4.94% 4.84% 4.55% 4.40% 4.28% 4.18% 4.07% 3.96% 3.86% 3.76% Retained earnings 4.90% 5.46% 6.05% 6.36% 6.62% 6.84% 7.13% 7.48% 7.88% 8.30% Cumulative other comprehensive income (loss) 0.24% 0.40% 0.09% 0.09% 0.08% 0.08% 0.08% 0.07% 0.07% 0.07% Treasury stock -0.21% -0.46% -0.53% -0.52% -0.51% -0.49% -0.48% -0.46% -0.45% -0.43% Unearned ESOP shares -0.07% -0.07% -0.08% -0.08% -0.07% -0.07% -0.07% -0.07% -0.06% -0.06%

Total Wells Fargo stockholders' equity 10.67% 11.07% 11.14% 11.28% 11.38% 11.47% 11.63% 11.85% 12.12% 12.42% Noncontrolling interests 0.11% 0.10% 0.06% 0.05% 0.05% 0.05% 0.05% 0.05% 0.04% 0.04%

Total equity 10.78% 11.17% 11.20% 11.33% 11.43% 11.52% 11.67% 11.89% 12.16% 12.46% Total Liabilities and equity 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

WELLS FARGO & CO. Historical Cash Flow Statement Scale in millions

Fiscal Years Ending Dec. 31 2011 2012 2013

Cash Flows from Operating Activities Net income before noncontrolling interests Adjustment to reconcile net income to net cash provided by operating activities:

Provision for credit losses

16,211

7,899

19,368

7,217

22,224

2,309

Change in fair value of MSRs (residential) & MHFS carried at fair value (295) (2,307) (3,229) Depreciation & amortization 2,208 2,807 3,293 Other net losses (gains) 3,273 (3,661) (9,384) Preferred shares released to ESOP 959 - - Stock option compensation expense 529 1,698 1,920 Excess tax benefits related to stock option payments (79) (226) (271)

Originations of MHFS (345,099) (483,835) (317,054) Proceeds from sales of & principal collected on mortgages originated for sale 298,524 421,623 311,431 Originations of LHFS (5) (15) - Proceeds from sales of and principal collected on LHFS 11,833 9,383 575 Purchases of LHFS Net change in:

Trading assets

(11,723)

35,149

(7,975)

105,440

(291)

43,638

Loans originated for sale Deferred income taxes

- 3,573

- (1,297)

- 4,977

Accrued interest receivable (401) 293 (13) Accrued interest payable (362) (84) (32) Other assets, net (11,529) 2,064 4,693 Other accrued expenses & liabilities, net 3,000 (11,953) (7,145)

Net cash flows from operating activities 13,665 58,540 57,641 Cash Flows from Investing Activities Net change in:

Federal funds sold, securities purchased under resale agreements & other short-term investments 36,270 (92,946) (78,184) Available-for-sale securities:

Proceeds from sales of securities available-for-sale 23,062 5,210 2,837 Prepayments & maturities of securities available-for-sale 52,618 59,712 50,737 Purchases of securities available for sale (121,235) (64,756) (89,474)

Held-to-maturity securities: Paydowns & maturities of held-to-maturity securities - - 30 Purchases of held-to-maturity securities - - (5,782)

Nonmarketable equity investments: Sales proceeds of nonmarketable equity investments - - 2,577 Purchases of nonmarketable equity investments - - (3,273)

Loans: Loans originated by banking subsidiaries, net of p (35,686) (50,420) (43,744) Proceeds from sales (including participations) of 6,555 6,811 7,694 Purchases (including participations) of loans (8,878) (9,040) (11,563) Principal collected on nonbank entities' loans 9,782 25,080 19,955 Loans originated by nonbank entities (7,522) (23,555) (17,311)

Net cash acquired from (paid for) acquisitions (353) (4,322) - Proceeds from sales foreclosed assets Proceeds from sales of foreclosed assets & short sales

10,655 -

9,729 -

- 11,021

Net cash from purchases & sales of MSRs (155) 116 407 Other investing activities, net (157) (1,509) 581

Net cash flows from investing activities (35,044) (139,890) (153,492) Cash Flows from Financing Activities Net change in:

Deposits

72,128

82,762

76,342

Short term borrowings (6,231) 7,699 (3,390) Long-term debt:

Proceeds from issuance of long-term debt

11,687

27,695

53,227 Long-term debt repayment (50,555) (28,093) (25,423)

Preferred stock: Proceeds from issuance of preferred stock Redemption of preferred stock Cash dividends - preferred

2,501

- (844)

1,377

- (892)

3,145

- (1,017)

Common stock: Proceeds from issuance of stock warrants Proceeds from issuance of common stock

-

1,296

-

2,091

-

2,224 Common stock repurchased (2,416) (3,918) (5,356) Cash dividends paid on common stock (2,537) (4,565) (5,953)

Common stock warrants repurchased (2) (1) - Excess tax benefits related to stock option payments Purchase of Prudential's noncontrolling interest Net change in noncontrolling interests

79 -

(331)

226 -

(611)

271 -

(296) Other financing activities, net - - 136

Net cash flows from financing activities 24,775 83,770 93,910 Net change in cash & due from banks 3,396 2,420 (1,941)

Cash & due from banks at beginning of year 16,044 19,440 21,860

Cash & due from banks at end of year 19,440 21,860 19,919

Supplement cash flow disclosures: Cash paid for interest

7,011

5,245

4,321

Cash paid for income taxes 4,875 8,024 7,132

Page 19

WELLS FARGO & CO. Forecast Cash Flow Statement Scale in millions

Fiscal Years Ending Dec. 31 2014E 2015E 2016E 2017E 2018E 2019E 2020 CV

Cash Flows from Operating Activities Net income before noncontrolling interests Adjustment to reconcile net income to net cash provided by operating activities:

Impairment of mortgage

23,239

(507)

23,760

(866)

24,423

(909)

26,003

(859)

27,748

(898)

29,383

(938)

30,879

(871)Originations of MHFS Proceeds from sales of & principal collected on mortgages originated for sale

729

(802)

(842)

(795)

(831)

(869)

(807)

Trading assets (2,925) (3,287) (3,451) (3,261) (3,408) (3,562) (3,308)Loans originated for sale (27) (8) (8) (8) (8) (9) (8)Other assets, net (9,860) (4,810) 253 (4,534) (4,738) (4,951) (4,599)Other accrued expenses & liabilities, net (1,399) (1,371) (1,344) (1,317) (1,290) (1,265) (1,239)

Net cash flows from operating activities 9,250 12,616 18,122 15,228 16,573 17,790 20,045Cash Flows from Investing Activities Net change in:

Federal funds sold, securities purchased under resale agreements & other short-term investments (14,687) (11,256) (11,368) (12,131) (12,714) (11,308) (11,490)Change in investment securities (12,869) (15,545) (15,522) (15,166) (16,100) (15,280) (14,193)Change in Premises& equipment, net (291) 86 (257) (264) (51) (273) (281)

Change in Net Loans (33,832) (35,915) (38,122) (37,602) (35,782) (36,062) (37,362)Net cash flows from investing activities (61,679) (62,629) (65,270) (65,164) (64,647) (62,923) (63,327)

Cash Flows from Financing Activities Net change in:

Deposits 48,197 50,433 51,033 53,317 55,707 55,194 57,527Short term borrowings 1,886 1,952 2,020 2,091 2,164 2,240 2,318

Long-term debt: 9,180 9,731 10,315 10,933 11,589 12,285 13,022Cash paid for preferred stock dividend (989) (989) (989) (989) (989) (989) (989)Cash paid for dividend (7,278) (8,512) (9,991) (9,957) (9,938) (9,926) (9,923)