Embed Size (px)

Citation preview

WESTPAC FIXED INCOME INVESTORFIXED INCOME INVESTOR PRESENTATIONPRESENTATION FOR THE SIX MONTHS ENDED 31 MARCH 2014 UNLESS OTHERWISE STATED EUROPEAN ROADSHOW MAY 2014

Disclaimer

The material contained in this presentation is intended to be general background information on Westpac Banking Corporation (“Westpac”) and its activities. It does not constitute a prospectus, offering memorandum or offer of securities. It should not be reproduced, distributed or transmitted to any person without the consent of Westpac and is not intended for distribution in any jurisdiction in which such distribution would be contrary to local law or regulation.

This presentation is directed only at persons who (i) have professional experience in matters relating to investments; or (ii) are persons falling within Article 49(2)(a) to (d) (“high net worth companies, unincorporated associations etc.”) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 (as amended); or (iii) are outside the United Kingdom (all such persons together being referred to as “relevant persons”). This document must not be acted on or relied on by persons who are not relevant persons.

The information is supplied in summary form and is therefore not necessarily complete. Also, it is not intended that it be relied upon as advice to investors or potential investors, who should consider seeking independent professional advice depending upon their specific investment objectives, financial situation or particular needs. The material contained in this presentation may include information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information.

All amounts are in Australian dollars unless otherwise indicated.

Financial information in this presentation may be presented on a cash earnings basis. Cash earnings is a non-GAAP measure. Refer to Westpac’s Interim 2014 Results (incorporating the requirements of Appendix 4D) for the half year ended 31 March 2014 available at www.westpac.com.au for details of the basis of preparation of cash earnings. Refer to Appendix 1 for a reconciliation of reported net profit to cash earnings.

I f ti t i d i th i ibl th h th b it ti d i thi t ti d t f t f th t ti l ifi ll t t th t th i f tiInformation contained in or otherwise accessible through the websites mentioned in this presentation does not form part of the presentation unless we specifically state that the information is incorporated by reference thereby forming part of the presentation. All references in this presentation to web sites are inactive textual references and are for information only.

Disclosure regarding forward-looking statements

This presentation contains statements that constitute “forward-looking statements” within the meaning of Section 21E of the US Securities Exchange Act of 1934. The forward-looking statements include statements regarding our intent, belief or current expectations with respect to our business and operations, market conditions, results of operations and financial condition, including, without limitation, future loan loss provisions, indicative drivers, forecasted economic indicators and performance metric outcomes.

We use words such as ‘will’, ‘may’, ‘expect’, 'indicative', ‘intend’, ‘seek’, ‘would’, ‘should’, ‘could’, ‘continue’, ‘plan’, ‘probability’, ‘risk’, ‘forecast’, ‘likely’, ‘estimate’, ‘anticipate’, ‘believe’, or similar words to identify forward-looking statements. These statements reflect our current views with respect to future events and are subject to change, certain risks, uncertainties and assumptions which are, in many instances, beyond our control and have been made based upon management’s expectations and beliefs concerning future developments and their potential effect upon us. Should one or more of the risks or uncertainties materialise, or should underlying assumptions prove incorrect, actual results may vary materially from the expectations described in this presentation. Factors that may impact on the forward-looking statements made include those described in the section entitled ‘Risk factors’ in Westpac’s Interim Financial Report for the half year ended 31 March 2014 available at www.westpac.com.au. When relying on forward-looking statements to make decisions with respect to us, investors and others should carefully consider such factors and other uncertainties and events We are under no obligation and do not intend to update any forward looking statementsinvestors and others should carefully consider such factors and other uncertainties and events. We are under no obligation, and do not intend, to update any forward-looking statements contained in this presentation.

Westpac Group | May 2014 | European Investor Roadshow 2

INDEXINDEX 1H14 HIGHLIGHTS 4 AUSTRALIAN HOME LENDING 20 ECONOMICS 28ECONOMICS 28SECURED FUNDING 40 ADDITIONAL INFORMATION 50 APPENDICES 60APPENDICES 60

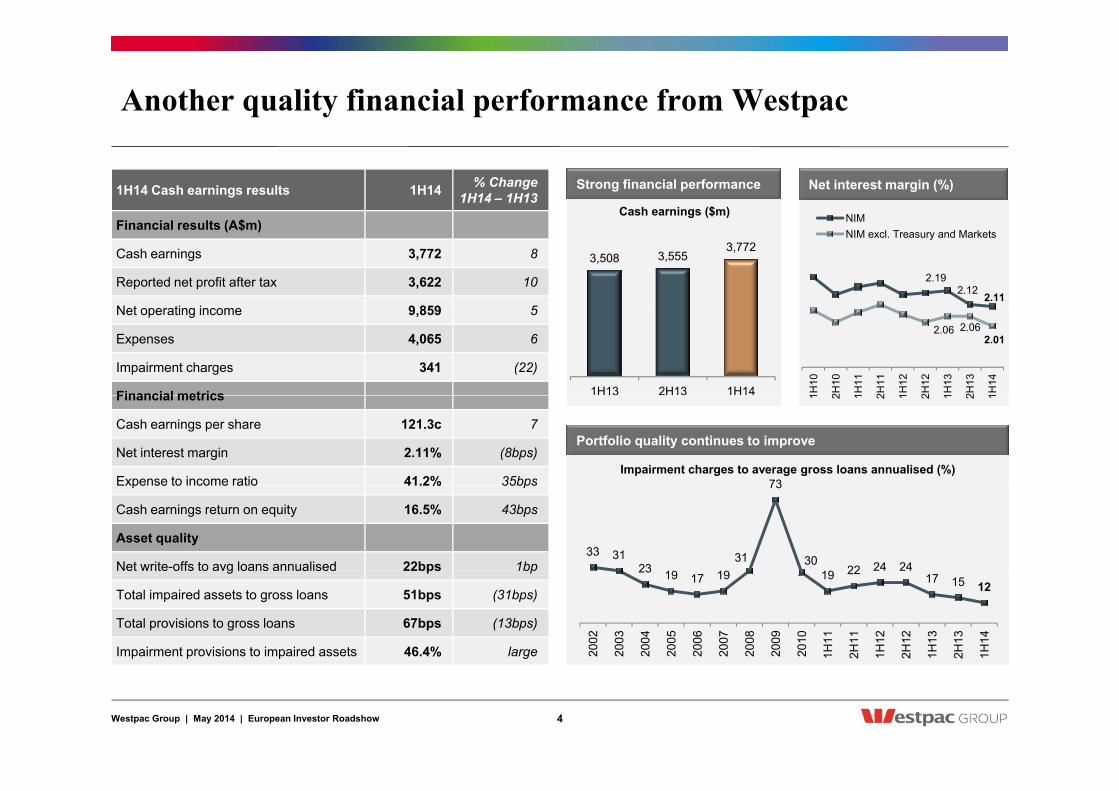

Another quality financial performance from Westpac

1H14 Cash earnings results 1H14 % Change 1H14 – 1H13

Strong financial performance

Cash earnings ($m) NIM

Net interest margin (%)

Financial results (A$m)

Cash earnings 3,772 8

Reported net profit after tax 3,622 10

N t ti i 9 859 5

3,508 3,555 3,772

g ($ )

2.19 2.12 2.11

NIMNIM excl. Treasury and Markets

Net operating income 9,859 5

Expenses 4,065 6

Impairment charges 341 (22)

Financial metrics 1H13 2H13 1H14

2.06 2.06 2.01

1H10

2H10

1H11

2H11

1H12

2H12

1H13

2H13

1H14

73

Financial metrics

Cash earnings per share 121.3c 7

Net interest margin 2.11% (8bps)

Expense to income ratio 41.2% 35bps

Portfolio quality continues to improve

Impairment charges to average gross loans annualised (%)

1 2 1 2 1 2 1 2 1

33 31 23 19 17 19

31

73

30 19 22 24 24

17

Expense to income ratio 41.2% 35bps

Cash earnings return on equity 16.5% 43bps

Asset quality

Net write-offs to avg loans annualised 22bps 1bp 19 17 19 19 17 15 12

2002

2003

2004

2005

2006

2007

2008

2009

2010

1H11

2H11

1H12

2H12

1H13

2H13

1H14

Total impaired assets to gross loans 51bps (31bps)

Total provisions to gross loans 67bps (13bps)

Impairment provisions to impaired assets 46.4% large

Westpac Group | May 2014 | European Investor Roadshow 4

Westpac has clear strategic priorities...

Remain strong ...managed in a balanced way Remain strong

T t d th Strength A strong company

Capital within preferred range

Target stable funding

Return Maintain discipline Maintain strong ROE Maintain dividend path

Targeted growth

Target stable funding ratio >75%

Growth Investment driven

Productivity Sector leading

Customer relationships

Investment drivenHigher growth in target segments, including Deposits, Asia, SME, Trade and Natural Resources

Sector leadingMaintain expense to

income ratio below peers

Materially simplify

One team

Westpac Group | May 2014 | European Investor Roadshow 5

Strategy delivering growth in targeted areas

Customer deposits ($bn)

Westpac RBB St George

Customer numbers (#m) Aust. housing growth vs system (times)

348 360 383 389 6.13 6.17 6.22

3 22 3 26 3.55

Westpac RBB St.George

0.8x 0.7x

0.8x 0.9x

2H12 1H13 2H13 1H14

3.22 3.26

1H13 2H13 1H143Q13 4Q13 1Q14 2Q14

FUA FUM

2H12 1H13 2H13 1H14

FUA2 and FUM3 ($bn)

Life in-force premiums General gross written premiums

Insurance premiums ($m)

Asia Australia

WIB trade finance volumes ($bn)

1H13 2H13 1H143Q13 4Q13 1Q14 2Q14

89 97

104 108

68 76

86 93 601 635 685 734

General gross written premiums

3.3 3.9

5.5

7.1

2H12 1H13 2H13 1H14

186 198 218 227

2H12 1H13 2H13 1H14 2H12 1H13 2H13 1H14

Westpac Group | May 2014 | European Investor Roadshow 6

1 RBA Financial Aggregates March 2014. 2 Funds under administration. 3 Funds under management.

Strong portfolio of brands s

Westpac Retail & Business Banking Australian retail and business

• 1H14 cash earnings $1,251m • Up 10% on 1H13

Westpac Retail &

Contribution to Cash Earnings (%)

All comparisons to 1H13

ncia

l Ser

vice

s Australian retail and business banking for consumers, SMEs and commercial customers under the Westpac brand

• Strong franchise; lending up 4%, deposits up 8%, as the division tilts to growth

St.George Banking Group Australian retail and business

• 1H14 cash earnings $772m • Up 12% on 1H13

33

10

2 3

Westpac Retail & Business Banking St.George Banking Group BT Financial Group

Westpac Institutional

stra

lian

Fina

n banking under the St.George, BankSA, Bank of Melbourne and RAMS brands

p• Each brand contributing positively;

solid revenue growth; decline in impairment charges

BT Financial Group Wealth division with $82bn funds

d d $107b

• 1H14 cash earnings $438m • Up 21% on 1H13

20

12 20

Bank Westpac New Zealand

Westpac Pacific

Group (inc. Treasury)

nal

Au under management and $107bn funds under administration at 31 March 2014

p• Funds management earnings up 28%;

strong insurance flows in life and general insurance

Westpac Institutional Bank L di A t l i i tit ti l

• 1H14 cash earnings $752m D 4% 1H13

Market share at 31 March 2014 (%)

Australia

Inst

itutio

n Leading Australasian institutional bank, with branches and representative offices in Australia, NZ, US, UK and Asia

• Down 4% on 1H13• Underlying business continues to

perform well; customer revenue up 3%; strong contribution from markets businesses

Household deposit market share1 23%

Housing credit market share2 23%

Business credit market share2 19%

Wealth platforms market share3 20%

NZ

Westpac New Zealand Banking and wealth services to consumers, businesses and institutions in New Zealand

• 1H14 cash earnings NZ$432m • Up 17% on 1H13 • Improving asset quality driving lower

impairment charges; lending up 6%, deposits up 8%

Wealth platforms market share 20%

New Zealand

Household deposit market share4 21%

Consumer lending market share4 20%

Westpac Group | May 2014 | European Investor Roadshow 7

1 APRA Banking Statistics. 2 Reserve Bank of Australia. 3 Plan for Life December 2013, All Master Funds Admin. 4 Reserve Bank of New Zealand.

Improving balance sheet momentum

Net loans ($bn)

Housing Total credit Business

Australian private sector credit growth (% ann)

10

15

20

25 Housing Total credit Business

f/cs end '15

521 16 7 4

11 6 565

-10

-5

0

5

J 94 J 98 J 02 J 06 J 10 J 14

1H13 Aust. Housing

Aust. Business

Aust. Personal &

other

NZ (A$) Overseas 1H14

Up 8%

Customer deposits ($bn)

Sources: RBA, Westpac Economics Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14 other

Customer deposits at 1H14 (%)

15 % income

Australian household savings rate (% income)

360 383 389

U 8%

42

18

25

6

9

12

1H13 2H13 1H14

Up 8%15

Term deposits Savings

Online Transaction -3

0

3

Dec-89 Dec-93 Dec-97 Dec-01 Dec-05 Dec-09 Dec-13

Westpac Group | May 2014 | European Investor Roadshow 8

Sources: ABS, Westpac Economics

Setting Westpac apart – Domestic customer focus, efficiency and balance sheet strength, y g

Total income by geography1 (%)

Clear focus on Australia and New Zealand Brands supporting targeted growth

Australian Financial Services

Wealth penetration2 leads sector (%)

Brands rank #1 and # 3

10

15

9 8

2 17

4 15 Asia, Pacific,

Europe & Americas

New Zealand

Total income by geography (%) Australian Financial Services

21.9%

16 1%

19.5% WRBB

SGB

P 1

Brands rank #1 and # 3

88 67

87 76

Westpac Peer 1 Peer 2 Peer 3

Australia Westpac NZ WIB

16.1%

14.1% 14.3%

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14

Peer 1

Peer 2

Peer 3

47 0

Westpac Peer 1 Peer 2 Peer 3

Expense to income ratio3 (%) Impairment charges to average loans annualised3 (bps)

Leader in efficiency Risk management a competitive advantage

Common equity ratio3 (APRA Basel III) (%)

Capital level strong relative to peers

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14

41.2

44.3 42.6

47.0

12

21

16 20

( p )

8.8 8.3 8.5 8.6

Westpac Peer 1 Peer 2 Peer 3 Westpac Peer 1 Peer 2 Peer 3 Westpac Peer 1 Peer 2 Peer 3

Westpac Group | May 2014 | European Investor Roadshow

1 Source: Company Annual Reports. Westpac, Peer 1 and Peer 3 as at 30 September 2013. Peer 2 as at 30 June 2013. 2 See Appendix 4 for Wealth penetration metrics definition and provider details 3. Source: Company reports. Westpac , Peer 1 and Peer 3 as at 31 March 2014, Peer 2 as at 31 December 2013.

9

Fully harmonised common equity tier 1 capital ratio at the upper end of global peersupper end of global peers

Global peer comparison of Basel III pro-forma common equity tier 1 capital ratios1 (%)

15.0 14.7

13.9 13.6

12.8

11.9 11.9 11.8 11.4 11.3 11.1 10.9 10.7 10.5 10.5 10.5 10.4 10.4 10.4 10.3 10.3

10 010.0 9.8 9.7 9.7 9.5 9.5 9.3 9.3 9.1 9.0 8.9 8.8 8.8 8.6 8.6 8.3 8.1 8.3 8.1 7.9

SE

B

Ban

k

rdea

DnB

UB

S

DB

S

CB

C

Ban

k

CB

A

tpac

nley

nder

a H

K

AN

Z

roup

NA

B

atix

is

Ban

k

Ban

k

oyds

ribas

eral

e

argo

Ban

k

ank

BV

A

CIB

C

clay

s

treal

Nov

a …

BK

IR

Ban

k

ncia

l

corp

RB

S

bank

e S

A

pula

r

SU

N

pula

r

BE

N

S

Dan

ske

B

Nor D U D

OC

Mac

quar

ie B C

Wes

t

Mor

gan

Sta

San

tan

Bank

of C

hina

A

Citi

gr N

Na

Han

g Se

ng B

Dah

Sin

g B Llo

BN

P P

ar

Soc

iete

Gen

e

Wel

ls F

a

Deu

tsch

e B

Roy

al B

a

BB C

Barc

Ban

k of

Mon

t

Ban

k of

N B

TD B

PNC

Fin

an

US

Banc R

Com

mer

zb

Cre

dit A

gric

ole

Banc

o Po

p S

Banc

o Po

p B

Westpac Group | May 2014 | European Investor Roadshow 10

1 Company data, Credit Suisse estimates (based on latest reporting data as at April 2014. Australian banks based on 1H14 results.

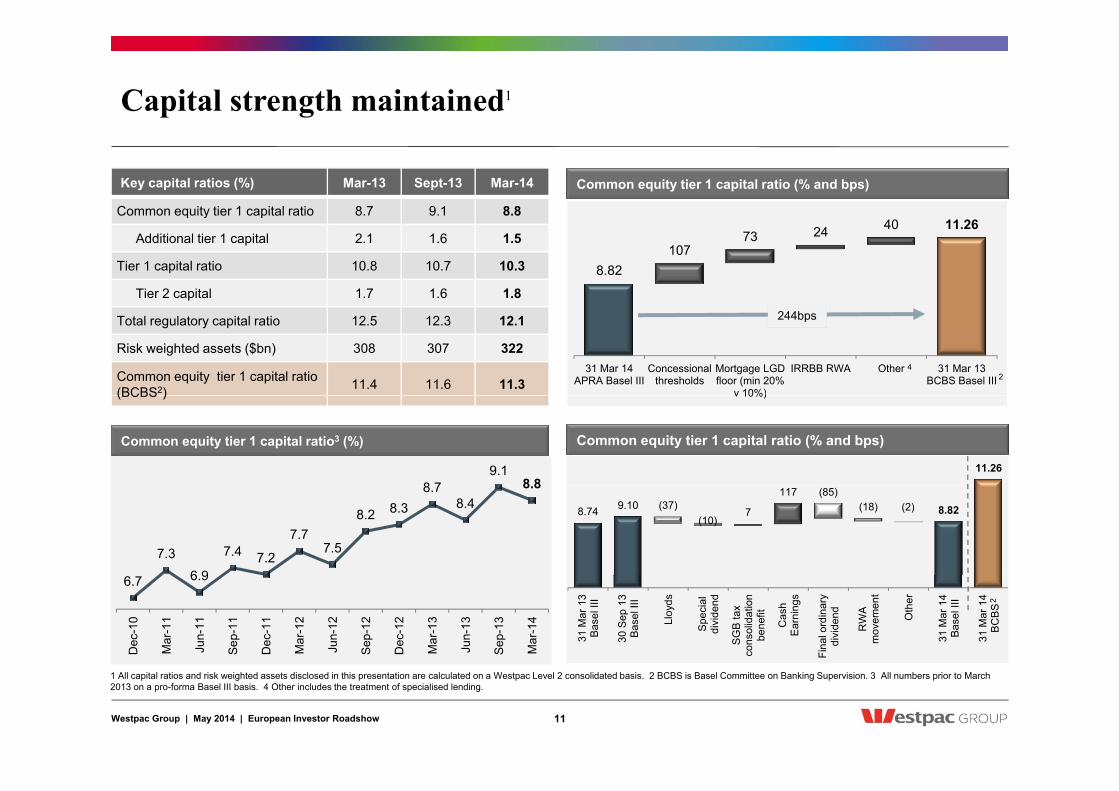

Capital strength maintained1

Key capital ratios (%) Mar-13 Sept-13 Mar-14

Common equity tier 1 capital ratio 8.7 9.1 8.8

Common equity tier 1 capital ratio (% and bps)

q y p

Additional tier 1 capital 2.1 1.6 1.5

Tier 1 capital ratio 10.8 10.7 10.3

Tier 2 capital 1.7 1.6 1.8 8.82

107 73 24 40 11.26

Total regulatory capital ratio 12.5 12.3 12.1

Risk weighted assets ($bn) 308 307 322

Common equity tier 1 capital ratio (BCBS2) 11.4 11.6 11.3

31 Mar 14 APRA Basel III

Concessional thresholds

Mortgage LGD floor (min 20%

v 10%)

IRRBB RWA Other 31 Mar 13 BCBS Basel III

244bps

2 4

(BCBS ) v 10%)

8 79.1

8 8

Common equity tier 1 capital ratio3 (%) Common equity tier 1 capital ratio (% and bps)

11.26

7.3 6 9

7.4 7.2

7.7 7.5

8.2 8.3 8.7

8.4 8.8

8.74 9.10 7

117

8.82 (37) (10)

(85) (18) (2)

6.7 6.9

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Mar

-14

31 M

ar 1

3

B

asel

III

30 S

ep 1

3

B

asel

III

Lloy

ds

Spe

cial

di

vide

nd

SG

B ta

x co

nsol

idat

ion

bene

fit

Cas

h

Ear

ning

s

Fina

l ord

inar

y di

vide

nd

RW

A

mov

emen

t

Oth

er

31 M

ar 1

4 B

asel

III

31 M

ar 1

4

BC

BS

2

Westpac Group | May 2014 | European Investor Roadshow 11

1 All capital ratios and risk weighted assets disclosed in this presentation are calculated on a Westpac Level 2 consolidated basis. 2 BCBS is Basel Committee on Banking Supervision. 3 All numbers prior to March 2013 on a pro-forma Basel III basis. 4 Other includes the treatment of specialised lending.

Capital well positioned for D-SIB capital requirement

Westpac’s capital base • On 23 December 2013, APRA issued an information paper which

– Identified the four major Australian banks as domestic systemically important

12.1% Total regulatory

capital ratio

1 8% / $5 7b Ti 2

banks (D-SIB)

– Provided detail of the additional higher loss absorbency requirements for D-SIB as a buffer

• D-SIB requirement of 1% is to be met by common equity tier 1 capital (CET1)

I l t ti f th D SIB i th h t i f th it l ti

1.5% / $4.8bn AT1

1.8% / $5.7bn Tier 2

8.0 % Regulatory minimum (effective Jan 2016)

• Implementation of the D-SIB is through an extension of the capital conservation buffer (CCB) effectively increasing the buffer above regulatory minimums

• The CCB and D-SIB buffer will commence on 1 January 2016

• Westpac is currently reviewing its preferred capital range (effective Jan 2016)

8.8% $28.5bn

Common Equity Tier 1

3.5% D-SIB HLA + Capital

Conservation Buffer

Requirement Common Equity Tier 1 Total Capital APRA

Implementation

Minimum 4.5% 6.0% 8.0% 1 Jan 2013

Capital Conservation Buffer (CCB) 2.5% 1 Jan 2016

D-SIB requirement 1.0% 1 Jan 2016

Countercyclical Buffer 0% - 2.5% 1 Jan 2016

4.5% Common Equity

Tier 1

APRA regulatory minimums Westpac 1H14

Countercyclical Buffer 0% 2.5% 1 Jan 2016

Total Capital Requirement 8.0%-10.5% 9.5%-12.0% 11.5%-14.0%

Leverage Ratio 3% 1 Jan 2018

Westpac Group | May 2014 | European Investor Roadshow 12

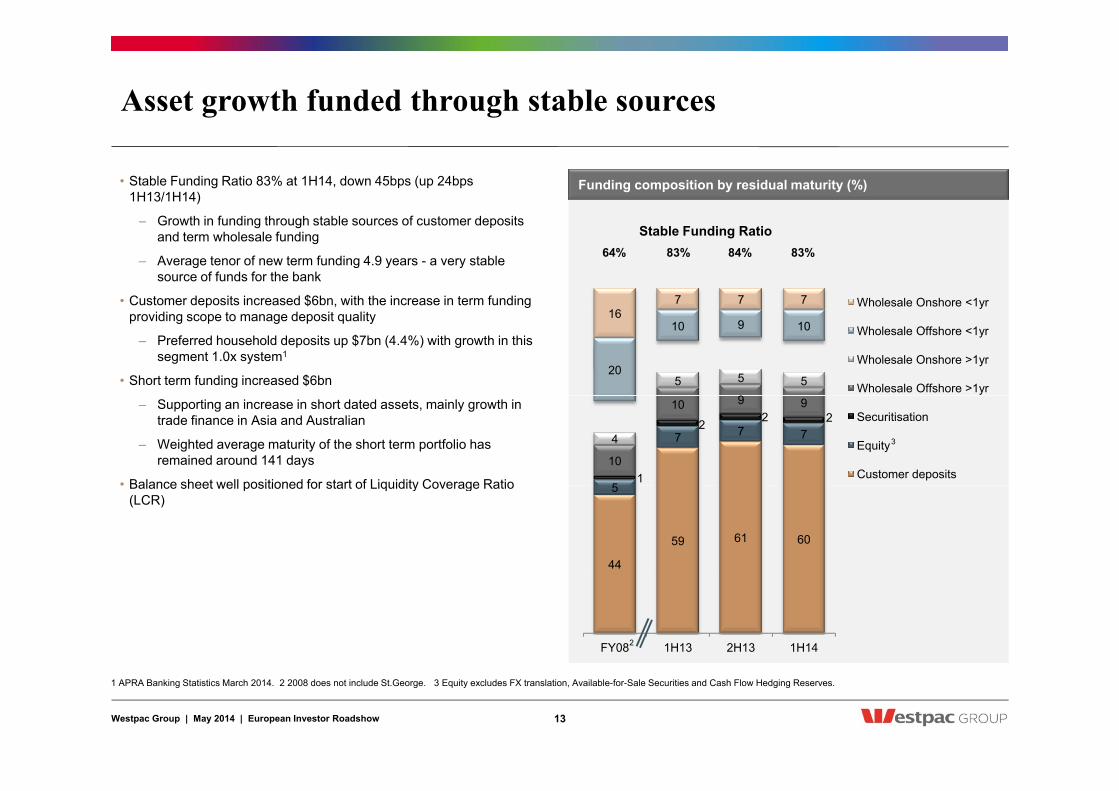

Asset growth funded through stable sources

Funding composition by residual maturity (%) • Stable Funding Ratio 83% at 1H14, down 45bps (up 24bps 1H13/1H14)

G th i f di th h t bl f t d it

7 7 7 Wholesale Onshore <1yr

Stable Funding Ratio 64% 83% 84% 83%

– Growth in funding through stable sources of customer deposits and term wholesale funding

– Average tenor of new term funding 4.9 years - a very stable source of funds for the bank

• Customer deposits increased $6bn, with the increase in term funding

95 5 5

20

10 9 10 16

Wholesale Onshore 1yr

Wholesale Offshore <1yr

Wholesale Onshore >1yr

Wholesale Offshore >1yr

p $ , gproviding scope to manage deposit quality

– Preferred household deposits up $7bn (4.4%) with growth in this segment 1.0x system1

• Short term funding increased $6bn

3

5

7 7 7

1

2 2 2

10

10 9 9

4

Securitisation

Equity

Customer deposits

3

– Supporting an increase in short dated assets, mainly growth in trade finance in Asia and Australian

– Weighted average maturity of the short term portfolio has remained around 141 days

• Balance sheet well positioned for start of Liquidity Coverage Ratio

44

59 61 60

5 • Balance sheet well positioned for start of Liquidity Coverage Ratio (LCR)

FY08 1H13 2H13 1H14 2

Westpac Group | May 2014 | European Investor Roadshow 13

1 APRA Banking Statistics March 2014. 2 2008 does not include St.George. 3 Equity excludes FX translation, Available-for-Sale Securities and Cash Flow Hedging Reserves.

Strong liquidity position maintained

Liquid assets ($bn) • $127bn in unencumbered liquid assets held at 31 March 2014

– Securities are eligible for repo with a central bank and proposed

45 54 58

Self securitisation

Private securities d t

127 126

111

Committed Liquidity Facility (CLF)

– Sufficient to cover all short term debt outstanding (including long term debt with a residual maturity less than one year)

• Westpac is well positioned for the introduction of the LCR

APRA ill l th LCR th h APS210 f 1 J 2015

36 44 43

108

38

30 28 26

and government guaranteed paper

Cash, government and semi-government bonds

45 1

– APRA will apply the LCR through APS210 from 1 January 2015

– The LCR is intended to improve the resilience of banks against potential short-term stress

– It requires banks to hold 100% of their net cash outflows over a 30-day horizon in High Quality Liquid Assets (HQLA)

7 FY08 1H13 2H13 1H14 Short term

outstanding debt 1H14 3

2

y g y q ( )

– In addition, APRA has stated that a suitable buffer would be in the range of 10-15% of net cash outflows

• As insufficient HQLA are available in Australia to meet the LCR requirement, a CLF will be provided by APRA and the RBA

– The CLF allows banks to access a specified amount of liquidity (approved by APRA) through repo arrangements with the RBA, for a 15bps fee

– The CLF is available only to address a shortage of HQLA in Australian dollars

– APRA has yet to finalise the CLF limit for Westpac

Westpac Group | May 2014 | European Investor Roadshow 14

1 Private securities include Bank paper, RMBS, and Supra-nationals. 2 2008 does not include St.George. 3 Includes long term wholesale funding with a residual maturity less than 1 year.

New term issuance well diversified

Covered Bond Hybrid Senior Govt Guaranteed Sub Debt

Term debt issuance and maturity profile1,2 ($bn)

Short term funding3,4 ($bn)

Lowest short term funding of peers

153 170

17 18 21

24

Covered Bond Hybrid Senior Govt Guaranteed Sub Debt

Issuance Maturities

24 23 2022

33

25 23 20

43 45

g ($ )Short term funding to total funding including equity3,4 (%)

108 119

Westpac Peer 1 Peer 2 Peer 3FY09 FY10 FY11 FY12 FY13 1H14 2H14 FY15 FY16 FY17 FY18 >FY18

15 2022

11

20

es pac ee ee ee 3

Issued ($bn)

Remaining capacity (8% cap &

Australian covered bond issuance5

% Capacity utilised

1H14 new term issuance composition1 (%)

By type By tenor By currency

16

26 25

29

Remaining capacity (8% cap & overcollateralisation) ($bn) 49

43 36

40

58 22

11 4 5

39

32

23 4 2

5

24

52

19

1 Based on residual maturity and FX spot currency translation. Includes all debt issuance with contractual maturity greater than 13 months, excluding US Commercial Paper. 2 Contractual maturity date for hybrids and callable subordinated instruments

15 20 14 19

16

Peer 1 Peer 2 Peer 3 Westpac Peer 1 Peer 2 Peer 3 Westpac

Senior unsecured Covered bonds RMBS ABS Subordinated debt

39

AUD USD EUR JPY Other 2 Years 3 Years

5 Years >5 years

Westpac Group | May 2014 | European Investor Roadshow 15

1 Based on residual maturity and FX spot currency translation. Includes all debt issuance with contractual maturity greater than 13 months, excluding US Commercial Paper. 2 Contractual maturity date for hybrids and callable subordinated instruments is the first scheduled conversion date or call date for the purposes of this disclosure. Perpetual sub-debt has been included in >FY18 maturity bucket. Maturities exclude securitisation amortisation. 3 Includes long term wholesale funding with a residual maturity less than 1 year. 4 Short term funding includes Central Bank deposits and long term wholesale funding with a residual maturity less than 1 year. Source: Westpac, Company reports. Westpac and Peer 1 as at 31 March 2014, Peer 2 as at 31 December 2013 and Peer 3 as at 30 September 2013. 5 Sources: Westpac, APRA Banking Statistics March 2014.

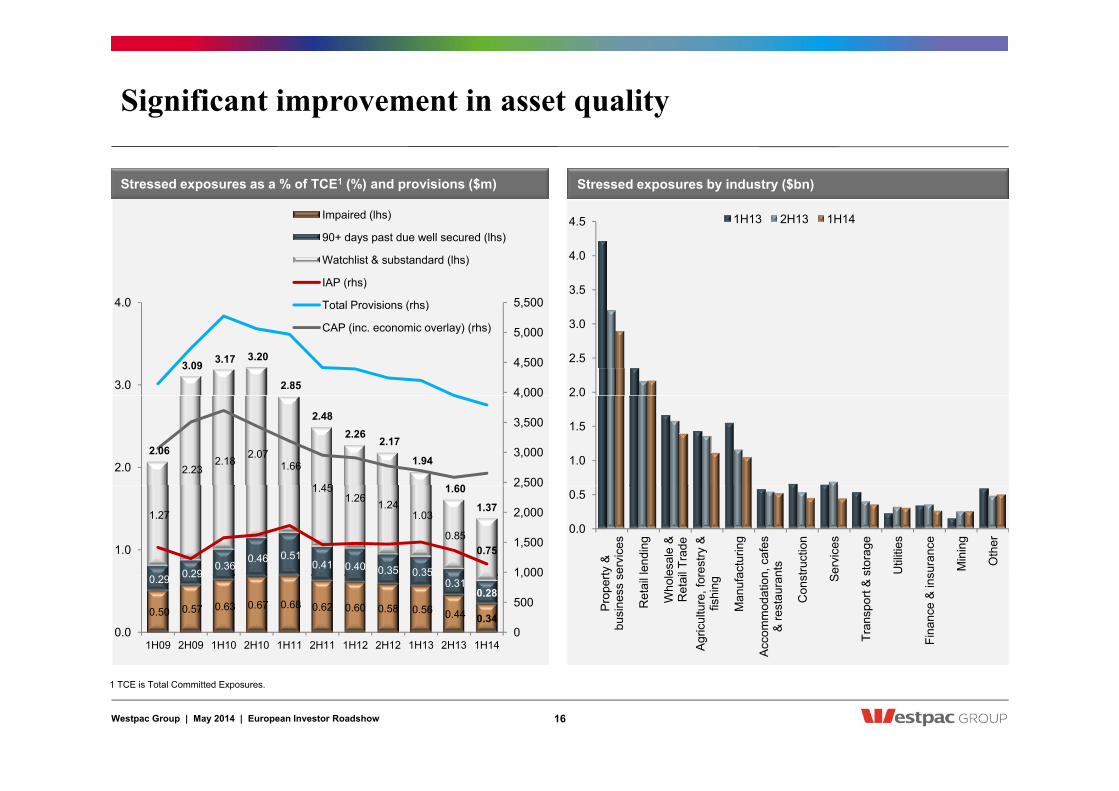

Significant improvement in asset quality

Impaired (lhs)

Stressed exposures as a % of TCE1 (%) and provisions ($m) Stressed exposures by industry ($bn)

1H13 2H13 1H14

5,5004.0

Impaired (lhs)

90+ days past due well secured (lhs)

Watchlist & substandard (lhs)

IAP (rhs)

Total Provisions (rhs)3.5

4.0

4.5 1H13 2H13 1H14

3.09 3.17 3.20

2.85 4,000

4,500

5,000

5,500

3.0

4.0 Total Provisions (rhs)

CAP (inc. economic overlay) (rhs)

2.0

2.5

3.0

2.23 2.18 2.07

1.66

1 45

2.06

2.48 2.26

2.17

1.94

1 60 2,500

3,000

3,500

4,000

2.0 1.0

1.5

2.0

0 29 0.36

0.46 0.51 0.41 0.40 0.35 0.35

1.27

1.451.26 1.24

1.03

0.85 0.75

1.60

1.37

1,000

1,500

2,000

2,500

1.0

0.0

0.5

ty &

se

rvic

es

lend

ing

esal

e &

il

Trad

e re

stry

&

actu

ring

n, c

afes

nt

s

truct

ion

Ser

vice

s

stor

age

Util

ities

sura

nce

Min

ing

Oth

er

0.50 0.57 0.63 0.67 0.68 0.62 0.60 0.58 0.56 0.44 0.34

0.29 0.29 0.35 0.31

0.28

0

500

1,000

0.0 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14

Prop

ert

busi

ness

s

Ret

ail

Who

leR

etai

Agr

icul

ture

, for

fishi

ng

Man

ufa

Acc

omm

odat

ion

& re

stau

ran

Con

s S

Tran

spor

t & s

Fina

nce

& in

s

Westpac Group | May 2014 | European Investor Roadshow 16

1 TCE is Total Committed Exposures.

Australian mortgage delinquencies at low levels

Delinquencies

• Sustained period of low interest rates and a continued conservative h t d bt b b h t d t dit

90+ Past Due Total 90+ First Home Buyer

Australian mortgages delinquencies and loss rates (%)

approach to debt by borrowers has supported very strong credit quality

• 90+ days delinquencies remain low at 50bps, down 3bps (down 8bps 1H13/1H14)

• 30+ days delinquencies 128bps, up 8bps (down 15bps 1H13/1H14) 2.0

3.0

90+ Investor 30+ Past Due

Loss Rates

y q p , p p ( p )reflecting normal seasonal trends for the first half

Properties in possession

• Properties in possession 189 at March 2014, down from 353 at September 2013 (248 at March 2013)

-

1.0

Sep

-08

Dec

08

Mar

-09

Jun

09

Sep

-09

Dec

09

Mar

-10

Jun

10

Sep

-10

Dec

10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

• Represents <2bps of the portfolio

Loss rates

• Portfolio losses of $45m represent an annualised loss rate of 2bps (net of insurance claims1)

S S S S D S D S D

1.5 ALL NSW/ACT VIC/TAS

Australian mortgage 90+ days delinquencies (%)

• Loss rates remain very low by international standards due to sound underwriting standards, high levels of borrower equity, mortgage insurance and active collections strategies

0.5

1.0

QLD WA SA/NT

0.0 M

ar-0

9

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Westpac Group | May 2014 | European Investor Roadshow 17

1 Mortgage insurance claims 1H14 $3m (2H13 $14m, 1H13 $10m).

High quality Australian mortgage portfolio

Australian housing portfolio 1H13 Balance

2H13 Balance

1H14 Balance

1H14 Flow1

T t l tf li ($b ) 321 9 328 5 338 0 33 1100 1H14 drawdowns LVR at origination

Australian housing loan-to-value (LVR) ratios (%)

Total portfolio ($bn) 321.9 328.5 338.0 33.1

Owner-occupied (%) 48.1 47.9 47.6 47.7

Investment property loans (%) 42.2 43.1 44.0 49.2

Portfolio loan/line of credit (%) 9.7 9.0 8.4 3.1

V i bl t / Fi d t (%) 85 / 15 81 / 19 84 / 16 76 / 2450 60 70 80 90 Portfolio LVR at origination

Portfolio dynamic LVR 2,3,4

Variable rate / Fixed rate (%) 85 / 15 81 / 19 84 / 16 76 / 24

Low Doc (%) 5.2 4.7 4.2 1.0

Proprietary channel (%) 58.2 58.0 55.3 55.7

First Home Buyer (%) 11.7 11.4 10.9 7.6

M t i d (%) 24 4 23 3 22 2 13 50

10 20 30 40

0<=60 60<=70 70<=80 80<=90 90<=95 95+Mortgage insured (%) 24.4 23.3 22.2 13.5

1H13 2H13 1H14

Average LVR at origination (%) 69 69 69

Average dynamic2,3,4 LVR (%) 48 46 47

0<=60 60<=70 70<=80 80<=90 90<=95 95+

50

Australian banking system Total portfolio (all brands)

8

Australian housing portfolio by State (%)

Average LVR of new loans5 (%) 70 72 72

Average loan size ($’000) 219 221 223

Customers ahead on repayments, including offset accounts2,6 (%)

70 71 73

20

30

40

50 Total portfolio (all brands)1H14 drawdowns (all brands)

( )

Actual mortgage losses (net of insurance)7 ($m) 52 43 45

Actual mortgage loss rate

annualised (bps) 3 3 2 -

10

20

NSW & ACT VIC & TAS QLD WA SA & NT

Westpac Group | May 2014 | European Investor Roadshow 18

1 Flow is all new mortgage originations total settled amount originated during the 6 month period ended 31 March 2014 and includes RAMS. 2 Excludes RAMS. 3 Dynamic LVR represents the loan-to-value ratio taking into account the current outstanding loan balance, changes in security value and other loan adjustments. 4 Property valuation source Australian Property Monitors. 5 Average LVR of new loans is based on rolling 6 month window for each half year period. 6 Customer loans ahead on payments exclude equity/line of credit products as there are no scheduled payments. 7 Mortgage insurance claims 1H14 $3m (2H13 $14m, 1H13 $10m). 8 ABA Cannex February 2014.

Mortgage customers continuing to repay ahead of schedule

• Australian mortgage customers continue to display a cautious approach to debt levels, taking advantage of historically low mortgage rates to pay down debt

Australian home loan customers ahead on repayments1,2 (%) Mar-13 rates to pay down debt

– Including mortgage offset account balances, 73% of customers are ahead of scheduled payments, with 21% of these being more than 2 years ahead

– Excluding mortgage offset account balances, 56% of Australian t t h d f h d l d t 30

40

50

Sep-13Mar-14 Mar-14 inc. mortgage offset accounts

Ahead on repayments

exc. mortgage offset accounts

mortgage customers are ahead of scheduled payments

• Sound underwriting criteria underpin the Group’s very low level of residential mortgage arrears and losses

• Credit policies are broadly aligned across brands and all credit decisions are made by the Westpac Group, regardless of the

0

10

20

Behind On Time < 1 Month < 1 Year < 2 Years > 2 Years y gorigination channel

• Loan serviceability assessments include an interest rate buffer, adequate surplus test and discounts to certain forms of income (e.g. dividends, bonus or rental income)

• Westpac has a minimum assessment rate often referred to as a floor 15 2 (6 7) 20 8

Aust. mortgage offset account balances ($bn) Australian mortgage1 balance growth ($bn)

• Westpac has a minimum assessment rate, often referred to as a floor rate, currently set at 6.80% p.a. across all brands

• In the current interest rate environment, the minimum assessment rate is at least 185bps higher than the standard lending rate

312.5 31.9

15.2

321.5

(6.7) (15.1) (12.8) (3.5)

20.8

2H13

New

lend

ing

Red

raw

/ In

tere

st/fe

es

Con

tract

re

paym

ents

Acc

eler

ated

re

paym

ents

Pro

perty

sal

es &

ot

her r

unof

f

Ext

erna

l re

finan

ce

1H14

1H09

2H

09

1H10

1H

11

2H11

1H

12

2H12

1H

13

2H13

1H

14

Westpac Group | May 2014 | European Investor Roadshow 19

1 Excludes RAMS. 2 Customer loans ahead on payments exclude equity loans/line of credit products as there is no scheduled principal payments. ‘Behind’ is more than 30 days past due. ‘On time’ includes up to 30 days past due.

AUSTRALIANAUSTRALIAN HOME LENDINGHOME LENDING

Housing activity responding to lower rates

'upgraders' ex refinancing investor finance first home buyers

Housing finance approvals: value of housing finance ($bn/mth)

current 2008 09 2001 02 1996 97

Housing credit: rate cut cycles compared (index)

8

10

12

8

10

12 AUDbn/mth AUDbn/mth

upgraders , ex-refinancing investor finance first home buyers

140

150

160

140

150

160

Index* Index* current 2008-09 2001-02 1996-97

1990-93 1987-88 1983-84

*index based to 100 in month prior to first rate cut last 5yrs

0

2

4

6

0

2

4

6

F b 92 F b 97 F b 02 F b 07 F b 1290

100

110

120

130

90

100

110

120

130

0 3 6 9 12 15 18 21 24 27 thSources: RBA, Westpac Economics.

Feb-92 Feb-97 Feb-02 Feb-07 Feb-12Sources: ABS, Westpac Economics.

0 3 6 9 12 15 18 21 24 27 months

140 140 index index Sydney Perth Melbourne Brisbane

40 40 % %

%income required to service mortgage of 75% median dwelling all regions

deteriorate

House affordability: all dwellings (%) Dwelling prices: Australia capital cities (index)

110

120

130

110

120

130

25

30

35

25

30

35

of 75% median dwelling, all regions

long run avg

improve

10yr avg

90

100

110

90

100

110

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 10

15

20

10

15

20

Mar-79 Mar-84 Mar-89 Mar-94 Mar-99 Mar-04 Mar-09 Mar-14

estimates based on capital cities prior to 1993

Westpac Group | May 2014 | European Investor Roadshow 21

Sources: RP Data-Rismark, Residex, ABS, RBA, Westpac Economics. Sources: RP Data-Rismark, Residex, Westpac.

Australian housing market fundamentals sound

Australia Sydney Melbourne

Rental vacancy rates (%)

population dwelling stock*

Population versus dwelling stock (annual average change ‘000)

6 6

Australia Sydney Melbourne

400

population dwelling stock

* net of demolitions – implied by Census data to 2006; Westpac

% ’000 %

4

5

4

5 investor housing

300

350

3 3 200

250

1

2

1

2

50

100

150

0 0 Mar-84 Mar-89 Mar-94 Mar-99 Mar-04 Mar-09 Mar-14

0

50

1950s 1960s 1970s 1980s 1990s 2000s last 3 years

Westpac Group | May 2014 | European Investor Roadshow 22

Sources: REIA, Westpac Economics.

Sources: ABS, Westpac Economics.

A more cautious approach to household leverage by Australian households by Australian households

accumulated savings since Jun 07

Australian households: debt to income ratio (%)

debt serv ratio (mortgagors lagged 6mths rhs) arrears rate (lhs)*

Pressure easing on existing borrowers (%)

160

180

160

180

% %

accumulated savings since Jun-07

total (gross) debt

housing debt

total debt net of deposits*

trend since Jun-07 2 0

2.2 24

% %

debt serv ratio (mortgagors, lagged 6mths, rhs) arrears rate (lhs)

*% of securitised loans in arrears, by value, including self-securitised loans WBC

forecasts

120

140

160

120

140

160

*direct holdings of cash and deposits

1.6

1.8

2.0

20

22 forecasts

60

80

100

60

80

100 –25pts since peak

1.2

1.4

16

18

20

40

20

40

= 52.9%

~20pts elsewhere? 0.8

1.0

12

14

-20

0

Mar-77 Mar-87 Mar-97 Mar-07 -20

0

0.4

0.6

Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14 10

12

Westpac Group | May 2014 | European Investor Roadshow 23

Sources: ABS, RBA, Westpac. Sources: ABS, RBA, Standard & Poor's, Westpac Economics.

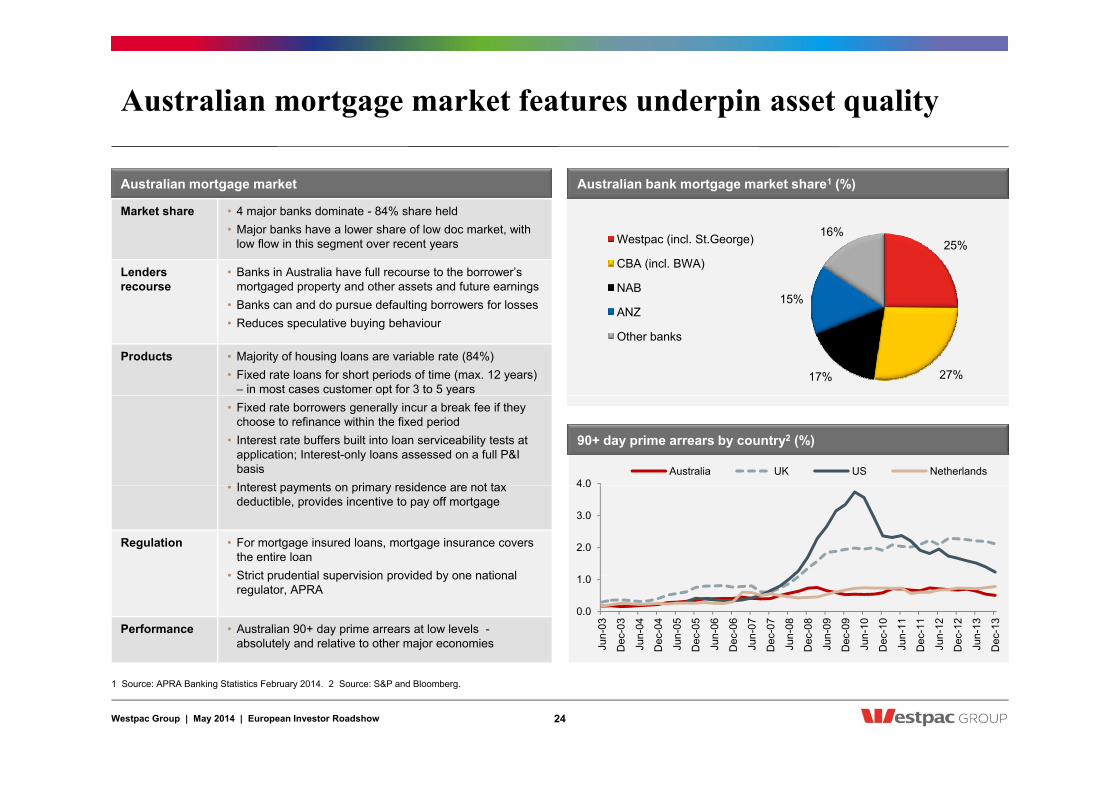

Australian mortgage market features underpin asset quality

Australian mortgage market

Market share • 4 major banks dominate - 84% share held

Australian bank mortgage market share1 (%)

j• Major banks have a lower share of low doc market, with

low flow in this segment over recent years

Lenders recourse

• Banks in Australia have full recourse to the borrower’s mortgaged property and other assets and future earnings

• Banks can and do pursue defaulting borrowers for losses

25%

15%

16% Westpac (incl. St.George)

CBA (incl. BWA)

NAB • Banks can and do pursue defaulting borrowers for losses• Reduces speculative buying behaviour

Products • Majority of housing loans are variable rate (84%) • Fixed rate loans for short periods of time (max. 12 years)

– in most cases customer opt for 3 to 5 years27% 17%

ANZ

Other banks

90+ day prime arrears by country2 (%)

• Fixed rate borrowers generally incur a break fee if they choose to refinance within the fixed period

• Interest rate buffers built into loan serviceability tests at application; Interest-only loans assessed on a full P&I basis Interest payments on primary residence are not tax 4 0

Australia UK US Netherlands • Interest payments on primary residence are not tax

deductible, provides incentive to pay off mortgage

Regulation • For mortgage insured loans, mortgage insurance covers the entire loan

• Strict prudential supervision provided by one national

2.0

3.0

4.0

• Strict prudential supervision provided by one national regulator, APRA

Performance • Australian 90+ day prime arrears at low levels - absolutely and relative to other major economies

0.0

1.0

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Westpac Group | May 2014 | European Investor Roadshow 24

1 Source: APRA Banking Statistics February 2014. 2 Source: S&P and Bloomberg.

Australian investment property portfolio performing well

• Investment property loans (IPLs) 44% of Westpac’s Australian mortgage portfolio

• 46% of IPL loans originated at 75-80% LVR to 50 Owner Occupied IPL

Loan-to-value ratio at origination1 (%)

25 Owner Occupied IPL

Applicants by gross income band1 (%)

• 46% of IPL loans originated at 75-80% LVR, to maximise tax benefits and avoid mortgage insurance costs

• Majority of IPLs are interest-only, however the actual amortisation profile closely tracks the principal and interest portfolio 20

30

40

50 p

10

15

20

25 Owner Occupied IPL

IPL average dynamic LVR1 51%

– 41% of interest-only IPL customers ahead on repayments

• Compared to owner-occupied applicants, IPL applicants on average are older, have higher incomes and higher credit scores

S ifi di li i l IPL i

0

10

0-60

60-7

0

70-7

5

75-8

0

80-8

5

85-9

0

90-9

5

95-9

7

97+

0

5

0<=5

0

50<=

75

75<=

100

00<=

125

25<=

150

50<=

200

00<=

500

500<

=1m

1m+

• Specific credit policies apply to IPLs to assist risk mitigation, including

– Holiday apartments subject to tighter acceptance requirements

– Additional LVR restrictions apply to single industry towns

All Non IPL

90+ days delinquency by customer type1 (%) IPL1 portfolio (%)

By customer type

7 10 12 15 20 5

Loss rates1 (bps)

11.0 industry towns

• IPL delinquency performance historically better than portfolio average

– At 1H14, IPL 90+ days delinquencies were 39bps compared to 50bps for total portfolio

IPL losses $22m1 in 1H14 representing an 0.5

1.0

Non-IPLMix (IPL & Owner Occ.) Multi (More than 1 IPL) Single IPL

28

25

48 2.2 3.1 1.2

l o . o

2

• IPL losses $22m1 in 1H14, representing an annualised loss rate of 3bps

• Self-managed Super Fund balances a very small part of the portfolio, at <1% of Australian mortgage balances

0.0

0.5

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Single IPL Mix (IPL & Owner Occ.) Multi (>1 IPL)

1H14

tota

lpo

rtfol

io

1H14

IPL

portf

oli o

1H14

Ow

ner O

cc.

portf

olio

1992

tota

l por

tfolio

(last

rece

ssio

n)

Westpac Group | May 2014 | European Investor Roadshow 25

1 Excludes RAMS. 2 The average number of securities for multi-IPL customers is two.

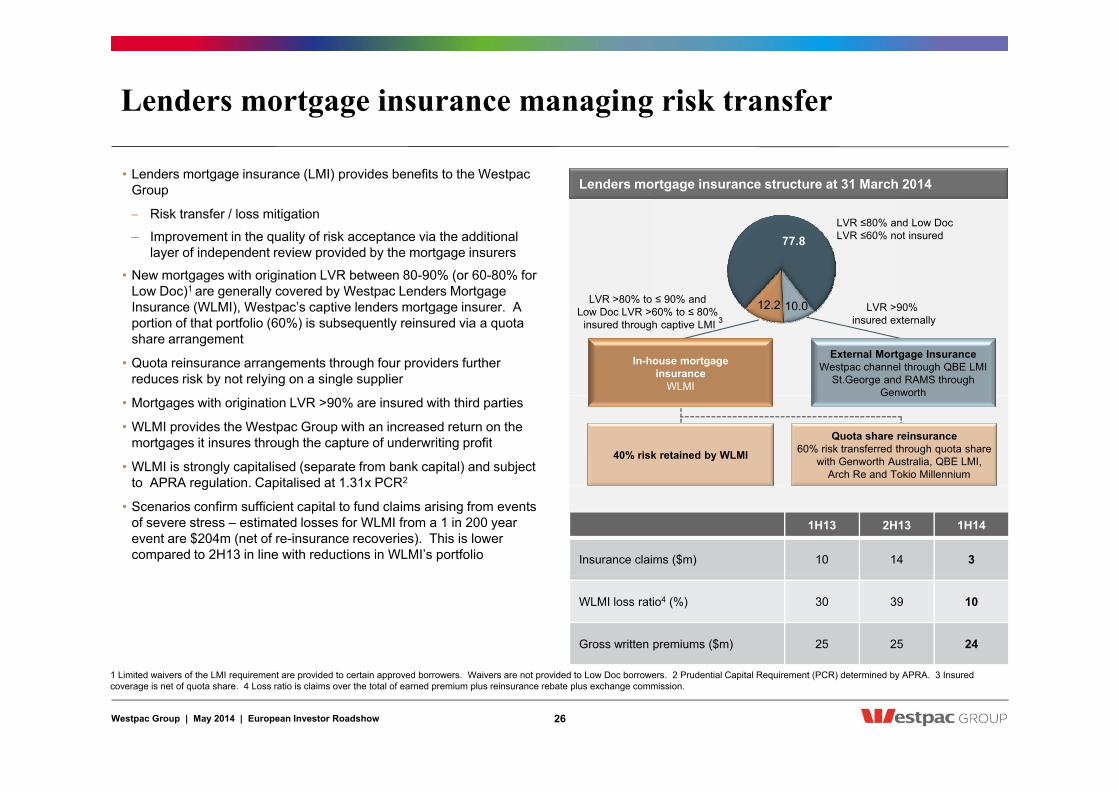

Lenders mortgage insurance managing risk transfer

Lenders mortgage insurance structure at 31 March 2014 • Lenders mortgage insurance (LMI) provides benefits to the Westpac

Group

– Risk transfer / loss mitigation

77.8

10 012 2LVR >80% to ≤ 90% and LVR >90%

LVR ≤80% and Low Doc LVR ≤60% not insured

Risk transfer / loss mitigation

– Improvement in the quality of risk acceptance via the additional layer of independent review provided by the mortgage insurers

• New mortgages with origination LVR between 80-90% (or 60-80% for Low Doc)1 are generally covered by Westpac Lenders Mortgage Insurance (WLMI) Westpac’s captive lenders mortgage insurer A 10.012.2Low Doc LVR >60% to ≤ 80%

insured through captive LMI LVR >90%

insured externally 3 Insurance (WLMI), Westpac s captive lenders mortgage insurer. A portion of that portfolio (60%) is subsequently reinsured via a quota share arrangement

• Quota reinsurance arrangements through four providers further reduces risk by not relying on a single supplier

In-house mortgage insurance

WLMI

External Mortgage Insurance Westpac channel through QBE LMI

St.George and RAMS through Genworth

40% risk retained by WLMI

• Mortgages with origination LVR >90% are insured with third parties

• WLMI provides the Westpac Group with an increased return on the mortgages it insures through the capture of underwriting profit

• WLMI is strongly capitalised (separate from bank capital) and subject to APRA regulation Capitalised at 1 31x PCR2

Quota share reinsurance 60% risk transferred through quota share

with Genworth Australia, QBE LMI, Arch Re and Tokio Millennium

Genworth

1H13 2H13 1H14

Insurance claims ($m) 10 14 3

to APRA regulation. Capitalised at 1.31x PCR

• Scenarios confirm sufficient capital to fund claims arising from events of severe stress – estimated losses for WLMI from a 1 in 200 year event are $204m (net of re-insurance recoveries). This is lower compared to 2H13 in line with reductions in WLMI’s portfolio

WLMI loss ratio4 (%) 30 39 10

Gross written premiums ($m) 25 25 24

Westpac Group | May 2014 | European Investor Roadshow 26

1 Limited waivers of the LMI requirement are provided to certain approved borrowers. Waivers are not provided to Low Doc borrowers. 2 Prudential Capital Requirement (PCR) determined by APRA. 3 Insured coverage is net of quota share. 4 Loss ratio is claims over the total of earned premium plus reinsurance rebate plus exchange commission.

Mortgage portfolio stress testing outcomes

Australian mortgage portfolio stress testing as at 31 March 2014

Key assumptions Stressed scenario

• Westpac regularly conducts a range of portfolio stress tests as part of its regulatory and risk management activities

Th A t li t tf li t t ti i t d Key assumptions Stressed scenario

Current Year 1 Year 2 Year 3

Portfolio size ($bn) 338 326 320 318

• The Australian mortgage portfolio stress testing scenario presented represents a severe recession and assumes that significant reductions in consumer spending and business investment lead to six consecutive quarters of negative GDP growth, resulting in a material increase in unemployment and nationwide falls in property and other asset prices

Unemployment rate (%) 5.8 11.6 10.6 9.4

Interest rates (cash rate, %) 2.5 1.25 1.25 1.25

House prices (% change cumulative) 0.0 -13.0 -22.4 -26.2

p

• Estimated Australian housing portfolio losses under stress conditions are manageable and within the Group’s risk appetite and capital base

– Cumulative total losses of $2.2bn over three years for the uninsured portfolio ( g )

Annual GDP growth (%) 2.8 -3.9 -0.2 1.7

Key outcomes

Stressed losses (bps) 2 26 32 7

uninsured portfolio

– Cumulative claims on LMI, both WMLI and external insurers, of $765m over the three years

• Westpac’s captive mortgage insurer, Westpac Lenders Mortgage Insurance (WLMI), separately conducts stress testing to ensure it is ( p )

(net of LMI recoveries)1,2 2 26 32 7sufficiently capitalised to cover mortgage claims arising from a stressed mortgage environment

• Preferred capital ranges incorporate buffers at the Westpac Group level that consider the combined impact on the mortgage portfolio and WLMI of severe stress scenarios

Westpac Group | May 2014 | European Investor Roadshow 27

1 Assumes 30% of LMI claims will be rejected in a stressed scenario. 2 Stressed loss rates are calculated as a percentage of mortgage exposure at default.

ECONOMICSECONOMICS

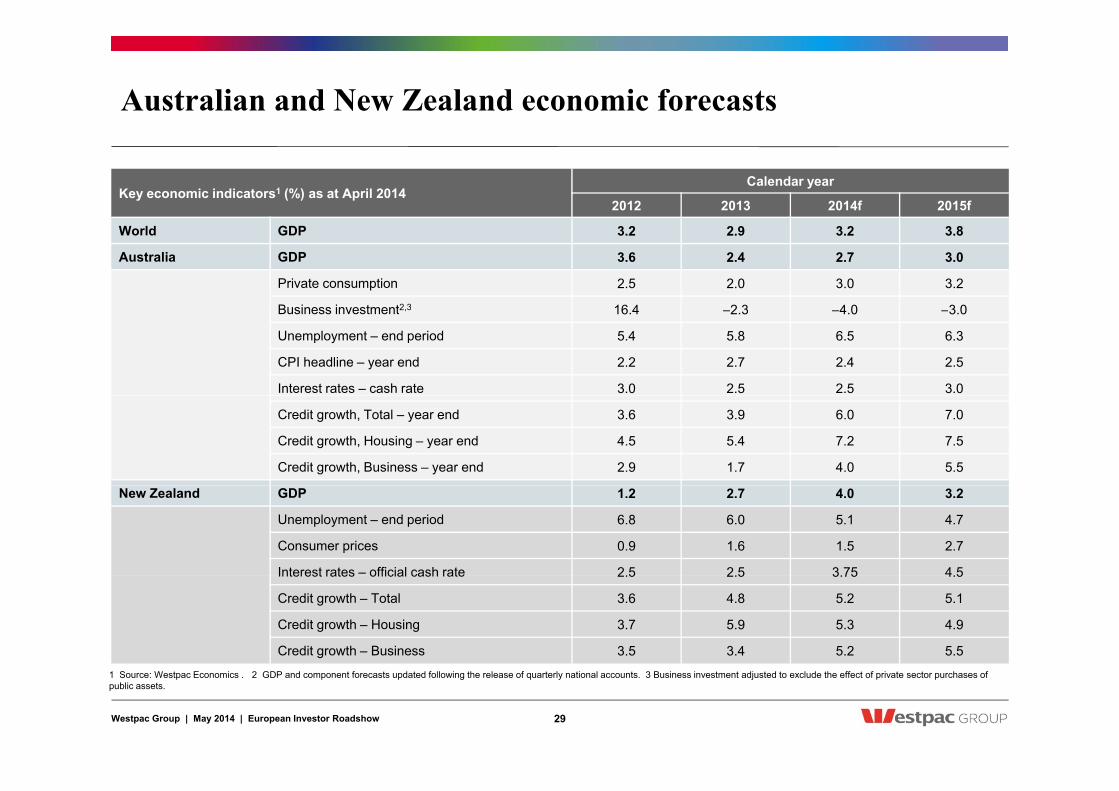

Australian and New Zealand economic forecasts

Key economic indicators1 (%) as at April 2014 Calendar year

2012 2013 2014f 2015f

World GDP 3.2 2.9 3.2 3.8

Australia GDP 3.6 2.4 2.7 3.0

Private consumption 2.5 2.0 3.0 3.2

B i i t t2 3 16 4 2 3 4 0 3 0Business investment2,3 16.4 –2.3 –4.0 –3.0

Unemployment – end period 5.4 5.8 6.5 6.3

CPI headline – year end 2.2 2.7 2.4 2.5

Interest rates – cash rate 3.0 2.5 2.5 3.0

Credit growth, Total – year end 3.6 3.9 6.0 7.0

Credit growth, Housing – year end 4.5 5.4 7.2 7.5

Credit growth, Business – year end 2.9 1.7 4.0 5.5

New Zealand GDP 1.2 2.7 4.0 3.2

Unemployment – end period 6.8 6.0 5.1 4.7

Consumer prices 0.9 1.6 1.5 2.7

Interest rates – official cash rate 2 5 2 5 3 75 4 5Interest rates official cash rate 2.5 2.5 3.75 4.5

Credit growth – Total 3.6 4.8 5.2 5.1

Credit growth – Housing 3.7 5.9 5.3 4.9

Credit growth – Business 3.5 3.4 5.2 5.5

Westpac Group | May 2014 | European Investor Roadshow 29

1 Source: Westpac Economics . 2 GDP and component forecasts updated following the release of quarterly national accounts. 3 Business investment adjusted to exclude the effect of private sector purchases of public assets.

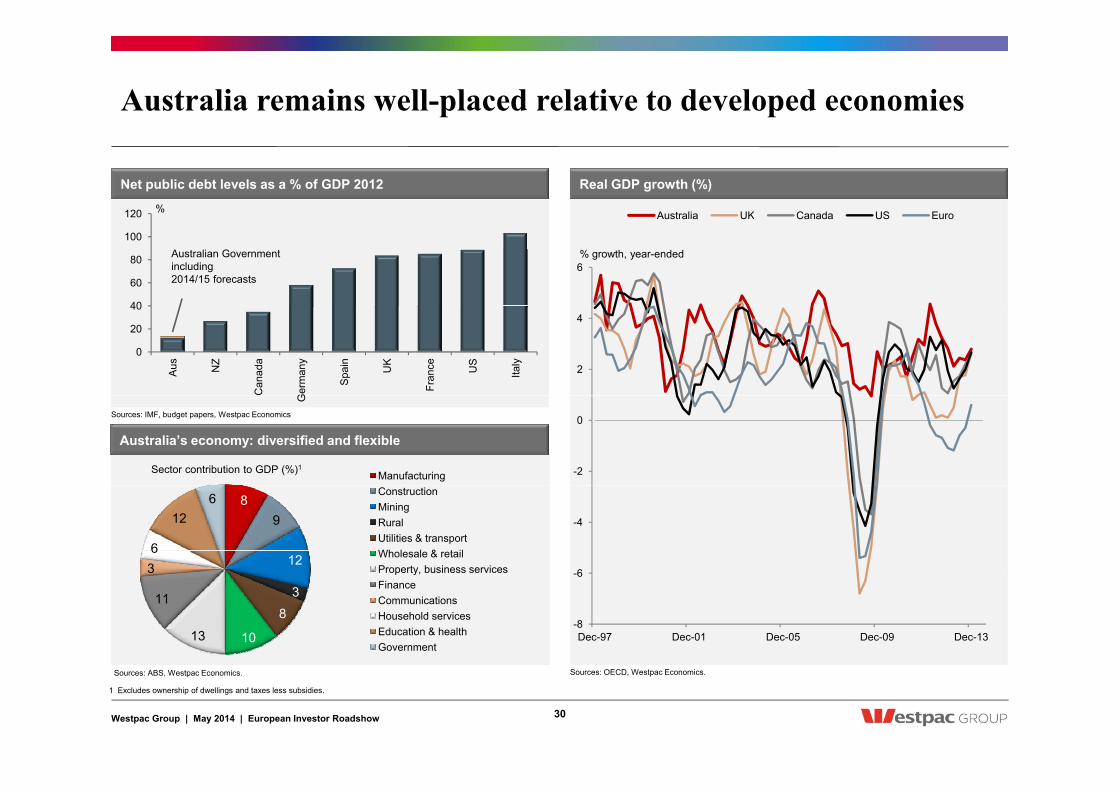

Australia remains well-placed relative to developed economies

Net public debt levels as a % of GDP 2012

120 % Australia UK Canada US Euro

Real GDP growth (%)

40

60

80

100

120

Australian Government including 2014/15 forecasts

6

Australia UK Canada US Euro

% growth, year-ended

0

20

40

Aus

NZ

Can

ada

Ger

man

y

Spa

in

UK

Fran

ce

US

Italy

2

4

Manufacturing

Australia’s economy: diversified and flexible

Sector contribution to GDP (%)1

Sources: IMF, budget papers, Westpac Economics .

G

-2

0

8 9

12 3 6

12 6 Construction

Mining Rural Utilities & transport Wholesale & retail Property, business services -6

-4

3 8

10 13

11 Finance Communications Household services Education & health Government

-8

6

Dec-97 Dec-01 Dec-05 Dec-09 Dec-13

Westpac Group | May 2014 | European Investor Roadshow

1 Excludes ownership of dwellings and taxes less subsidies.

30

Sources: ABS, Westpac Economics. Sources: OECD, Westpac Economics.

Australia’s economic transition from mining to non-mining

Australian growth mix: Contributions to GDP growth (%)

2012 2013 2014f 2015f mining CAPEX

Investment: share of Australian economy (% of GDP)

4 4

ppts

2012 2013 2014f 2015f

ann%

14 14 % of GDP % of GDP

mining, CAPEX

housing investment

business investment (ex mining)

f/cs end 2015

2

3

2

3

10

12

10

12 2015

1 1

6

8

6

8

-1

0

-1

0

* includes housing

2

4

2

4

-2 -2 Consumer* Mining inv. Business

investment Net Exports GDP

0

2

0

2

Dec-89 Dec-93 Dec-97 Dec-01 Dec-05 Dec-09 Dec-13

Westpac Group | May 2014 | European Investor Roadshow 31

Sources: ABS, Westpac Economics. Sources: ABS, Westpac Economics.

Commodity cycle evolves

itt d i t t (lh ) bulks* (lhs) exchange traded* (rhs)

Committed Australian projects and mining investment ($bn) Commodity prices (index)

120 300

$bn $bn

committed investment (lhs)

BREE* most likely projection

mining capital expenditure (rhs)

350

680

index index

bulks* (lhs) exchange traded* (rhs)

Westpac forecasts

80

100

200

250 *Bureau of Resources and Energy Economics

300

480

580

60 150 250

380

480

20

40

50

100

150

200

180

280

*b lk i l d i d l

0 0 2002/03 2006/07 2010/11 2014/15 2018/19

100 80 Apr-03 Apr-05 Apr-07 Apr-09 Apr-11 Apr-13

*bulks includes iron ore and coal. exchange traded includes rural, crude oil, base metals & gold.

Westpac Group | May 2014 | European Investor Roadshow 32

Sources: BREE, ABS, Westpac Economics. Sources: Westpac Economics, Bloomberg, ABS.

Cash rate expected to remain stable at 2.50%; AUD expected to trend lower over medium termAUD expected to trend lower over medium term

Australia UK Canada US Euro fair value band* AUD/USD actual & forecast

Australian dollar (AUD/USD) Major countries’ policy rates (%)

8

Australia UK Canada US Euro

%

1.20 1.20

USD USD

fair value band AUD/USD actual & forecast

*based on commodity prices, 2yr swap spread, and external debt

Fore-t

6

7

1.00

1.10

1.00

1.10 and external debt casts

4

5

0.80

0.90

0.80

0.90

latest: 0.92

1

2

3

0 50

0.60

0.70

0 50

0.60

0.70

0

1

Apr-07 Apr-08 Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14 0.40

0.50

0.40

0.50

Apr-91 Apr-95 Apr-99 Apr-03 Apr-07 Apr-11 Apr-15

Westpac Group | May 2014 | European Investor Roadshow

Sources: RBA, OECD, Westpac Economics. Sources: RBA, Westpac Economics.

33

Labour market showing some signs of improvement in early 2014

household services mining ‘000

in early 2014

Australia Canada UK US Euro

Unemployment rates (%) Cumulative change in industry employment (‘000)

200

300

400

500 construction goods distribution 000

14

Australia Canada UK US Euro

%

-200

-100

0

100

Mar 09 Mar 10 Mar 11 Mar 12 Mar 13 Mar 1410

12

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14

8

business services public admin manufacturing other ‘000

Cumulative change in industry employment (‘000)

Sources: ABS, Westpac Economics

4

6

100

200

300

400

500

2 Mar-98 Mar-02 Mar-06 Mar-10 Mar-14 -200

-100

0

100

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14

Westpac Group | May 2014 | European Investor Roadshow

Sources: OECD, Westpac Economics.

34

Sources: ABS, Westpac Economics

Credit growth picking up at a modest pace

Australian private sector credit growth (% ann)

Consumer (lhs) Business * (rhs) Housing Total credit Business

Business confidence and consumer confidence (net balance)

30 130

net bal. net bal.

Consumer (lhs) Business (rhs)

monthly 25 25

Housing Total credit Business

% ann % ann

f/cs end '1

10

20

110

120

15

20

15

20 '15

-10

0

90

100

5

10

5

10

30

-20

70

80

* rebased to avg 0 -5

0

-5

0

-40

-30

60

70

Apr-02 Apr-06 Apr-10 Apr-14 -10 -10

Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14

Westpac Group | May 2014 | European Investor Roadshow 35

Sources: Westpac MI, NAB, Westpac Economics. Sources: RBA, Westpac Economics

Chinese growth remains a positive for Australia

• As a $US7 trillion economy, China grew at 10%. As a $US10 trillion economy, Westpac expects China to grow at 7%

Represents an equivalent incremental contribution to global absorptive

Real GDP %ann 2012 2013 2014f 2015f

China 7.7 7.7 7.3 7.6 • Represents an equivalent incremental contribution to global absorptive

capacity, at higher levels of energy, protein, metal and consumer goods demand per head

• Were China to slow immediately to a 5% pace (a big downside shock that we do not envisage), it would still double its 2012 size by 2025

• Chinese authorities have shown a clear commitment to maintaining growth35 35

% of 2012 GDP % of 2012 GDP

8% CAGR

Chinese real GDP increments: 4 scenarios (% of 2012 GDP)

• Chinese authorities have shown a clear commitment to maintaining growth above 7% but will be less tolerant of strong credit driven expansions – the double digit growth rates that have featured regularly over the past 20 years are now unlikely to occur

• Australia’s economic linkages with China continue to grow, led by trade

– China now accounts for over 25% of Australia’s exports 25

30

25

30

8% CAGR

History & 7% CAGR

6% CAGR

5% CAGR

China now accounts for over 25% of Australia s exports

– Investment, tourism and migration flows also significant. Tourism arrivals from China are now 11% of all arrivals, with a CAGR of 13.1% between 2005 and 2013, against total arrivals growing at 1.9%. China was Australia's third largest source of foreign direct investment in the latest financial year. 15

20

15

20

• Australia will continue to benefit as Chinese households progressively expand their living standards and their consumption basket

5

10

5

10

0 0 1993 1998 2003 2008 2013 2018 2023 2028

Westpac Group | May 2014 | European Investor Roadshow 36

Source: Westpac Economics.

Chinese growth remains a positive for Australia

% 1980 2000 2010

China’s share of selected elements of world activity (%)

10

15

20

25 1980 2000 2010

0

5

10

Household consumption

Gross fixed capital formation

Exports Imports Manufacturing value added

Construction value added

Services value added

PPP GDP Nominal USD GDP

CO2 emissions Energy use 1 1 2 3

60 % GDP 2000 2007 2011 Ex China, nominal national

accounts basis for goods and

Sources: UN, IMF, IEA, Westpac Economics. All national accounts related shares are in 2005 constant US dollars. 1 Goods & services. 2 From fossil fuel combustion. 3 Total primary energy supply.

800 800 index index Total imports

Crude oil

Chinese imports – total and key primary products (index) Major countries nominal export shares (% GDP)

30

40

50

accounts basis for goods and services. For China, goods only, value-added estimates.

300

400

500

600

700

300

400

500

600

700 Crude oilIron ore Food

Value of total imports and food and volume of non-food raw materials.

0

10

20

AUD FRA DEU JPY KRW SEK TKL GBP USD BRL INR CNY 0

100

200

300

0

100

200

300

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

Westpac Group | May 2014 | European Investor Roadshow 37

Source: CEIC, Westpac Economics. Source: CEIC, OECD, Westpac Economics, Dragonomics.

A strong economic picture in New Zealand

• The New Zealand economy is experiencing a strong upturn driven by earthquake-related construction activity, last year’s rise in house prices a four decade high in the terms of trade and buoyant % %

New Zealand GDP growth and forecast (%)

prices, a four decade high in the terms of trade, and buoyant business investment activity. Annual economic growth is expected to peak at around 4%.

• Post-earthquake reconstruction in Canterbury is now in full swing, and residential construction activity is also ramping up in Auckland.

Th t i t ti t k d ti i fl ti 23 4 5 6 7

23 4 5 6 7

Westpac forecast

• The strong economy is starting to provoke domestic inflation pressures – construction costs in particular are starting to rise.

• Rising interest rates and the unwind of the Canterbury rebuild are expected to cause slower economic growth over the second half of this decade. -3

-2 -1 0 1 2

-3 -2 -1 0 1 2

1999 2001 2003 2005 2007 2009 2011 2013 2015 20171999 2001 2003 2005 2007 2009 2011 2013 2015 2017Source: Statistics NZ, Westpac Economics

1.6 1.6 $bn $bn

Earthquake-related construction activity in Christchurch ($bn)

0.8

1.0

1.2

1.4

0.8

1.0

1.2

1.4 Residential

Commercial

Infrastructure

Estimate Forecast

0.0

0.2

0.4

0.6

0.0

0.2

0.4

0.6

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Westpac Group | May 2014 | European Investor Roadshow 38

Source: Westpac Economics

New Zealand housing market beginning to slow

• House price inflation peaked at 10% in 2013, but is now slowing. Westpac is forecast 5.5% house price inflation in 2014, and 1% in 2015 3030

ann % ann %

New Zealand house price inflation (annual %)

2015.

• Since 1 October 2013 the Reserve Bank has required banks to limit high-LVR lending to just 10% of total new mortgage lending. Turnover of smaller houses fell sharply, and house prices stagnated in early-2014. However, there is tentative evidence that prices have subsequently resumed their upward trajectory.

10

20

30

10

20

30

Westpac forecast

subsequently resumed their upward trajectory.

• Higher fixed mortgage rates are also affected the housing market. Financial markets moved last year to price in a substantial OCR hiking cycle.

• Offsetting these negative forces, net immigration is booming. The rate of population growth is expected to rise to rise to 1 6% in 2014

-20

-10

0

-20

-10

0

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017rate of population growth is expected to rise to rise to 1.6% in 2014, up from 0.7% in 2012.

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017Source: QV, Statistics NZ, Westpac Economics

9%

New Zealand Official Cash Rate (%)

4 5 6 7 8

Westpac forecast

0 1 2 3

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Westpac Group | May 2014 | European Investor Roadshow 39

Source: RBNZ, Westpac Economics

SECURED FUNDINGSECURED FUNDINGCOVERED BONDS AND SECURITISATION

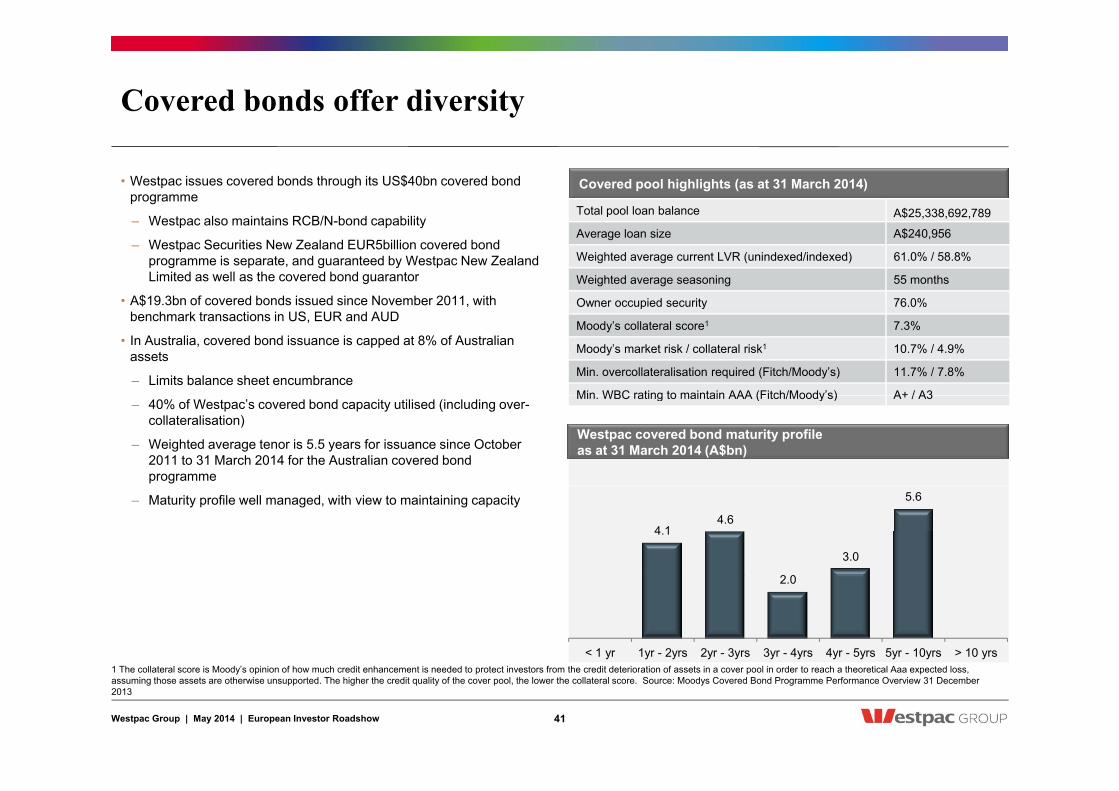

Covered bonds offer diversity

• Westpac issues covered bonds through its US$40bn covered bond programme

W t l i t i RCB/N b d bilit

Covered pool highlights (as at 31 March 2014)

Total pool loan balance A$25,338,692,789– Westpac also maintains RCB/N-bond capability

– Westpac Securities New Zealand EUR5billion covered bond programme is separate, and guaranteed by Westpac New Zealand Limited as well as the covered bond guarantor

• A$19.3bn of covered bonds issued since November 2011, with

p A$25,338,692,789

Average loan size A$240,956

Weighted average current LVR (unindexed/indexed) 61.0% / 58.8%

Weighted average seasoning 55 months

Owner occupied security 76.0%$ ,benchmark transactions in US, EUR and AUD

• In Australia, covered bond issuance is capped at 8% of Australian assets

– Limits balance sheet encumbrance

Owner occupied security 76.0%

Moody’s collateral score1 7.3%

Moody’s market risk / collateral risk1 10.7% / 4.9%

Min. overcollateralisation required (Fitch/Moody’s) 11.7% / 7.8%

Min WBC rating to maintain AAA (Fitch/Moody’s) A+ / A3– 40% of Westpac’s covered bond capacity utilised (including over-

collateralisation)

– Weighted average tenor is 5.5 years for issuance since October 2011 to 31 March 2014 for the Australian covered bond programme

Min. WBC rating to maintain AAA (Fitch/Moody s) A+ / A3

Westpac covered bond maturity profile as at 31 March 2014 (A$bn)

– Maturity profile well managed, with view to maintaining capacity

4.1 4.6

2 0

3.0

5.6

2.0

< 1 yr 1yr - 2yrs 2yr - 3yrs 3yr - 4yrs 4yr - 5yrs 5yr - 10yrs > 10 yrs

Westpac Group | May 2014 | European Investor Roadshow 41

1 The collateral score is Moody’s opinion of how much credit enhancement is needed to protect investors from the credit deterioration of assets in a cover pool in order to reach a theoretical Aaa expected loss, assuming those assets are otherwise unsupported. The higher the credit quality of the cover pool, the lower the collateral score. Source: Moodys Covered Bond Programme Performance Overview 31 December 2013

Westpac Covered Bond Programme

Issuer Westpac Banking Corporation

Issuer rating AA-/Aa2/AA- by S&P / Moody’s / Fitch

Format Legislative Covered Bond

Covered Bond rating Aaa / AAA by Moody’s / Fitch

Programme size US$40 billion

M t it ti S ft d H d B ll tMaturity options Soft and Hard Bullet

Covered Bond Guarantor Westpac Covered Bond Trust, a special purpose vehicle (trust)

Covered Bond Guarantee Covered Bond Guarantor has guaranteed payments of interest and principal under the Covered Bonds Covered Bond Guarantee secured over the Mortgage Loans and its other assets (limited in recourse to its assets)

LVR cap in asset coverage test 80% (subject to indexation)

Asset percentage Subject to rating agency requirements programme maximum 95%Asset percentage Subject to rating agency requirements, programme maximum 95%

Collateral Prime Australian residential mortgages

Listing London Stock Exchange

Westpac Group | May 2014 | European Investor Roadshow 42

Programme features

Structure Covered Bonds are issued by Westpac, backed by an unconditional and irrevocable guarantee by the Covered Bond Guarantor (the “CBT Guarantor”), which is limited in recourse to the assets in the Westpac Covered Bond T tTrust

Security

Security comprises a pool of Australian residential mortgages which meet the eligibility criteria (the “cover pool”). It also includes certain other assets such as cash and investments (subject to legislative and rating agency limits). Mortgages in the cover pool sold to the CBT Guarantor to ensure that covered bondholders have a priority claim over the cover pool in the event of Issuer insolvencyover the cover pool in the event of Issuer insolvency

Prior to service of a Notice to Pay on the CBT Guarantor, an Asset Coverage Test will be run monthly to ensure the CBT Guarantor has sufficient assets to support the outstanding covered bonds. Defaulted loans will have nil value applied to them and remaining loans adjusted by the Asset Percentage. The Asset Percentage will be confirmed by

Overcollateralisation pp g j y g g y

the rating agencies quarterly and is subject to a maximum of 95%, which represents a minimum level of overcollateralisation of just over 5%.

Following service of a Notice to Pay on the CBT Guarantor, an Amortisation Test is run monthly to ensure the CBT Guarantor has sufficient assets to meet the covered bond obligations

Asset Monitor

PricewaterhouseCoopers monitors the calculation of the Asset Coverage Test and the Amortisation Test on at least an annual basis.

They also provide the asset monitor reporting requirements in relation to the legislation on at least a six monthly basis This includes verification of the asset register and provision of any other information APRA requiresbasis. This includes verification of the asset register and provision of any other information APRA requires

Hedging The Total Return Swap and Covered Bond Swap will be used to hedge any exposure of the CBT Guarantor to interest rate and currency risks

Westpac Group | May 2014 | European Investor Roadshow 43

Westpac cover pool

At the time of sale, each loan: Total pool loan balance1 A$25 338 692 789

Covered Bond Pool eligibility criteria Covered pool loan statistics as at 31 March 2014

• Is denominated and payable only in AUD in Australia

• Is secured by a mortgage that constitutes a first ranking Australian mortgage (second allowed as long as first held with the CBT Guarantor)

• Is secured by a mortgage over a property which has erected on it a residential dwelling

Total pool loan balance1 A$25,338,692,789

Number of loans 105,159

Average loan size A$240,956

residential dwelling

• Was approved and originated by the seller in the ordinary course of business

• Is a loan under which the outstanding principal balance owed by the borrower is not more than AUD$2,000,000

• Is a loan under which the relevant borrower is required to repay the loan

Max loan size A$2,000,000

Weighted average current LVR (unindexed) 61%

Weighted average current LVR (indexed) 58.8%

within 30 years of the relevant cut-off date

• Is not a delinquent mortgage or a defaulted loan and no legal demand has been served on the relevant borrower in respect of a payment on the loan

• The sale of an interest in, or the sale of an interest in any related security, does not contravene or conflict with any law

Mortgage Insured 14.8%

90 day + arrears 0.01%

Weighted average seasoning 55 months• The relevant borrower is a resident of Australia

• Not a loan with an interest only payment period of >10 years

• The related mortgage has been or will be stamped

• Where applicable, all progress drawings have been made by the borrower d th id ti l d lli h b l t d d

g g g

Weighted average remaining term to maturity 274 months

Weighted average interest rate 5.3%

and the residential dwelling has been completed; and

• The borrower has made at least one monthly payment or two fortnightly payments in respect of the loan

Fixed / floating split (by bal) 18.6% / 81.4%

Interest only (by bal) 26.9%

Owner occupied security 76.0%

Westpac Group | May 2014 | European Investor Roadshow 44

1 Pool loan balance excludes cash balances of A$4,661,307,211. Loans included in the cover pool are currently only originated by Westpac Retail and Business Banking.

Cover pool statistics as at 31 March 2014

Loan to value ratio by balance (%)

40 Current LVR (unindexed) Current LVR (indexed)

Geographic distribution by state

Northern20

30

40 Current LVR (unindexed) Current LVR (indexed)

Queensland $3,466.0m, 13.6%

Western Australia $3,309.8m, 13.1% South Australia

$1,256.6m, 5.0%

NorthernTerritory $258.0m,

1.0%

0

10

0 50% 50 55% 55 60% 60 65% 65 70% 70 75% 75 80% 80 100% > 100%

Portfolio seasoning

Victoria $6 839 9m

New South Wales $9,227.7m, 36.4%

$1,256.6m, 5.0%

Australian Capital Territory

$676.0m, 2.7%

0-50% 50-55% 55-60% 60-65% 65-70% 70-75% 75-80% 80-100% > 100%

18 00020,000 30 % of pool by balance (lhs)

$6,839.9m 27%

Di t ib ti b i V l f l (A$ ) % of pool by

Tasmania $304.5m, 1.2%

6,000 8,000 10,00012,00014,00016,00018,000

10

15

20

25 Number of loans (rhs)

Distribution by region Value of loans (A$m) % of pool by value

Metropolitan 19,835 78.3%

Non-Metropolitan 5,503 21.7%

0 2,000 4,000

-

5

< 6Mth

6 mths -

1yr

1yr - 2yrs

2yrs - 3yrs

3yrs - 4yrs

4yrs - 5yrs

5yrs - 6yrs

6yrs - 7yrs

7yrs - 8yrs

8yrs - 9yrs

9yrs - 10yrs

> 10 yrs

Westpac Group | May 2014 | European Investor Roadshow 45

Cover pool statistics as at 31 March 2014 (cont.)

% of pool (lhs) Number of loans (rhs)

Mortgage principal balance distribution Interest rate split (%)

10 000

15,000

20,000

25,000

30,000

10

15

20

25

30 % of pool (lhs) Number of loans (rhs)

18.6

Fixed

-

5,000

10,000

-

5

10

0-10

0K

00-2

00k

200-

300k

300-

400k

400-

500k

500-

750k

750k

-1m

m -

1.5m

> 1.

5m

81.4

Floating

Years to maturity (legal) Interest only expiry date remaining period

1 2 3 4 5 7 1m

100 000100% of pool by balance (lhs) Number of loans (rhs) % of interest only loans by balance (lhs) Number of loans (rhs)

30 00040,000 50,000 60,000 70,000 80,000 90,000 100,000

30 40 50 60 70 80 90

100

4,000

6,000

8,000

10,000

20

30

40

0 10,000 20,000 30,000

- 10 20 30

< 1 yr 1yr - 5yrs 5yrs - 10yrs > 10 yrs 0

2,000

-

10

< 6 mths 6 mths - 1yr

1yr - 2yrs 2yrs - 3yrs 3yrs - 4yrs 4yrs - 5yrs > 5 yrs

Westpac Group | May 2014 | European Investor Roadshow 46

Securitisation an important part of the Group’s funding

• Securitisation is an important part of the Group’s funding

A$11 5bn in outstanding issuance at 31

Westpac has been a consistent RMBS issuer

Original RMBS and ABS issuance by calendar year (A$bn)– A$11.5bn in outstanding issuance at 31 March 2014, represents 2% of the Group’s total funding, mostly RMBS issuance

– Provides additional diversity to funding and investor base

8.3 7 8 9

10 WST Crusade

Westpac re opensWestpac re opens

A$1.2bn Auto ABS in Dec 2012 - first for a major Australian bank

A$1.2bn Auto ABS in Dec 2012 - first for a major Australian bank

WST Trust Series 2013-1, A$2.1bn in Feb 2013, and WST Trust 2013-2 in Oct

WST Trust Series 2013-1, A$2.1bn in Feb 2013, and WST Trust 2013-2 in Oct

Original RMBS and ABS issuance by calendar year (A$bn)

and investor base

– Only major Australian bank to have an active Auto ABS capability

– Westpac’s RMBS and Auto ABS transactions have been well supported b th A t li d ti k t 1 9

7.0

2.0

4.4 4.4

5.7 5.7 5.9

1 2 3 4 5 6

Westpac re-opens domestic RMBS market with first major bank deal since 2009

Westpac re-opens domestic RMBS market with first major bank deal since 2009

2013 $A2.252013 $A2.25

by the Australian domestic market, as well as offshore investors

• Westpac has outstanding securitisation transactions under both the WST and Crusade programmes

1.9 2.01.11.0 1.2 1.0

- 1

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Minimal changes to Lloyd’s Bella securitisations Minimal changes to Lloyd’s Bella securitisations Post St.George merger Post St.George merger – Westpac Securitisation Trust (WST)

Programme is Westpac’s programme for securitising Westpac-originated residential mortgages

– Crusade Programme is Westpac’s

Following the completion of the acquisition of Capital Finance Australia Limited ("CFAL") and the Bella securitisations on 31 December 2013 as part of acquisition of Lloyds Banking Group’s Australian business, it is intended that the only changes to the existing Bella securitisations will be: • The interest rate swaps have been novated to Westpac Banking

Following the completion of the acquisition of Capital Finance Australia Limited ("CFAL") and the Bella securitisations on 31 December 2013 as part of acquisition of Lloyds Banking Group’s Australian business, it is intended that the only changes to the existing Bella securitisations will be: • The interest rate swaps have been novated to Westpac Banking

• Securitisation management and execution integrated into one team

• Crusade RMBS Programme is currently in run off

• Crusade ABS platforms and

• Securitisation management and execution integrated into one team

• Crusade RMBS Programme is currently in run off

• Crusade ABS platforms and gvehicle for securitising St.George originated residential mortgages and auto loans

– Bella securitisation programme acquired 31 December 2013

The interest rate swaps have been novated to Westpac Banking Corporation

• The Trust Manager has been replaced with Westpac Securitisation Management Limited ("WSM"). WSM also manages Westpac's WST RMBS programme, the Crusade ABS (auto) programme and Westpac's covered bond programme

The interest rate swaps have been novated to Westpac Banking Corporation

• The Trust Manager has been replaced with Westpac Securitisation Management Limited ("WSM"). WSM also manages Westpac's WST RMBS programme, the Crusade ABS (auto) programme and Westpac's covered bond programme

pinfrastructure utilised for Auto ABS

• New securitisation RMBS pools currently sourced solely from Westpac originated mortgage pools

pinfrastructure utilised for Auto ABS

• New securitisation RMBS pools currently sourced solely from Westpac originated mortgage pools

Westpac Group | May 2014 | European Investor Roadshow 47

WST RMBS performance

Key pool comparison statistics (issuance)

WST WST WST WST WST WST WST

High quality product

All WST transactions backed by prime residential mortgages

Consistently outperforms both the Australian Prime SPIN Index

Consistent pool characteristics and

2013-2 2013-1 2012-1 2011-3 2011-2 2011-1 2009-1