Embed Size (px)

Citation preview

Marshall Katz MS, CIC, LUTC, LIA, AAI 1

Welcome to MAIA’s

Errors & Omissions Streaming Class

It’ here somewhere?

•We will do 5 check-ins

•They will be random throughout

the session

• If you miss one, the session does

not count

• I will try and give you enough

time to log in

HousekeepingHousekeepingHousekeepingHousekeeping

Marshall Katz MS, CIC, LUTC, LIA, AAI 2

WARNING

• This class is a guide�

• A discussion

• Informational

• If your not the boss�ask before you make office changes

Why are we here?

• E & O carriers think it’s a good idea

• Discount on E & O policy

• A break in our routine to think about possible areas of concern

• Agency principals think it’s a good idea

• Talk about protecting the bottom line

• Talk about increasing the bottom line

• To put in place Quido Qbains “7P’s - The Power to Persuade Plenty of Prospects to Purchase our Product for a Profit”

Marshall Katz MS, CIC, LUTC, LIA, AAI 3

CE and E & O Certification

We will no longer be using E&O forms at E&O classes.

Participants CEU certificates will now serve this purpose.

Please let the participants know that:

1. The forms will no longer be used and

2. The CEU certificate will serve this purpose, and

3. As long as they attended in full, will receive a CEU certificate

via email after the class and

4. That processing can take up to 4 weeks

5. Keep them safe as duplicate requests will be charged

If you have any questions, please let me know.

Thank you

Heather Kramer

Keep for the future??

marshall

@insadv.com1. Copy of slides2. Follow-up3. Questions

Marshall Katz MS, CIC, LUTC, LIA, AAI 4

How do I get the most

out of this class?

�Get active.

�Get involved – Ask questions

There are no stupid questions.

�Think – About relating this topic to your

customers, your agency, your desk and

how you want to address the issues.

Are there any agency owners,

managers or supervisors present?

• What do you see as a big issue

today?

• What steps have you taken to

address them?

Marshall Katz MS, CIC, LUTC, LIA, AAI 5

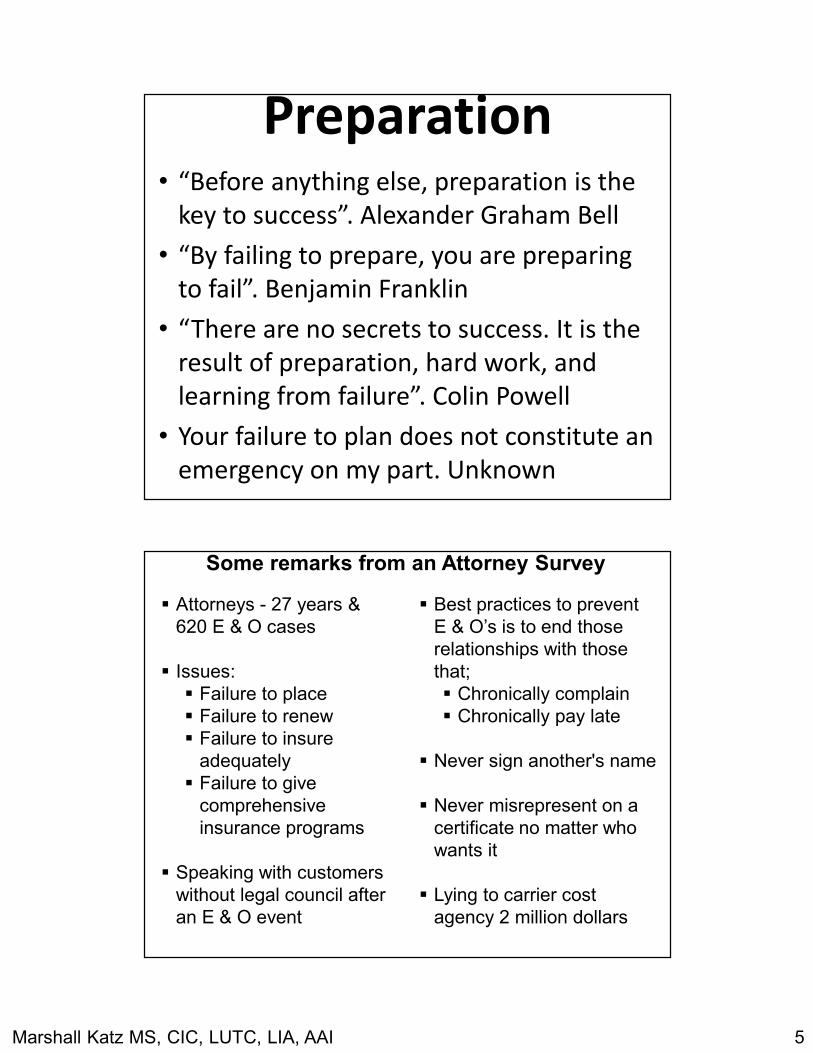

Preparation• “Before anything else, preparation is the

key to success”. Alexander Graham Bell

• “By failing to prepare, you are preparing

to fail”. Benjamin Franklin

• “There are no secrets to success. It is the

result of preparation, hard work, and

learning from failure”. Colin Powell

• Your failure to plan does not constitute an

emergency on my part. Unknown

Some remarks from an Attorney Survey

� Attorneys - 27 years & 620 E & O cases

� Issues:� Failure to place � Failure to renew� Failure to insure

adequately� Failure to give

comprehensive insurance programs

� Speaking with customers without legal council after an E & O event

� Best practices to prevent E & O’s is to end those relationships with those that;� Chronically complain� Chronically pay late

� Never sign another's name

� Never misrepresent on a certificate no matter who wants it

� Lying to carrier cost agency 2 million dollars

Marshall Katz MS, CIC, LUTC, LIA, AAI 6

Some remarks from an Attorney Survey

� Use electronic file keeping only – loose papers mean a loose ship

� Always keep signed documents

� Keep copies of all advertising and promotional materials

� Use risk exposure surveys by everyone in the organization

� Use a spreadsheet for coverage offerings and let customer choose what they desire

� If organization caters to foreign speaking customers have an interpreter and do not show any verbal or written biases against them

Does it matter?

Marshall Katz MS, CIC, LUTC, LIA, AAI 7

Time Wasters

Redundant System

OVERVIEW AND INTRODUCTION SECTION

Marshall Katz MS, CIC, LUTC, LIA, AAI 8

Contributing Factors to E & O’s

�Product changes

�Changing carrier relationships

�Lawyers

�Customer expectations

�Changing customer relationships

�Emerging exposures

�Consumer demands

Non AIB MAPDEFINITIONS "You" or "Your" - refers to a person shown as a named insured on the Coverage Selections Page and the person's spouse, civil partner or registered domestic partner or a person in a similar civil union or domestic partnership, if living in the same household. "Domestic partner" means a person living as a continuing partner with you and: (a) is at least 18 years of age and competent to contract; (b) is not a relative; and (c) shares with you the responsibility for each other's welfare, evidence of which includes:

(1) the sharing in domestic responsibilities for the maintenance of the household; or

(2) having joint financial obligations, resources, or assets; or (3) one with whom you have made a declaration of domestic partnership or

similar declaration with an employer or government entity. Domestic partner does not include more than one person, a roommate whether sharing expenses equally or not, or one who pays rent to the named insured.

Policy language can differ!

AIB MAPYou or Your – refers to the person(s) named in Item 1 of the Coverage Selections Page.

Marshall Katz MS, CIC, LUTC, LIA, AAI 9

Non AIB MAPHousehold Member - means anyone living in your household who is related to you by blood, marriage, civil union, registered domestic partnership, or similar union or partnership or adoption. This includes wards, step-children or foster children.

Policy language can differ!

AIB MAPHousehold Member – means anyone living in your household who is related to you by blood, marriage or adoption. This includes wards, step-children or foster children.

You have an MGA contract.

• Have you re-quoted all insureds with all carriers

• Does the aggregator provide a cheat sheet with all the differences between the carriers to make an intelligent decision on who to offer

–Some carriers may offer higher umbrella limits than others for UM/UIM

–Some carriers offer new forms that allow primary/non-contributory

Marshall Katz MS, CIC, LUTC, LIA, AAI 10

From a Recent Class

Liquor LiabilityOld policy had 3rd party coverage�new policy did not. Person fell outside the restaurant and became permanently injured.Agency did not give 3rd party coverage on new policy as the customers primary concern was policy pricing and the agency did not address the difference in writing.

Outbuilding Not InsuredBuilding was never picked up for the policyTotal loss to the $20,000 buildingNow the insureds attorney wants $60,000!

Professional Not Insured on New or Old PolicyCustomer bought professional cheaper from another agencyHad a claim originating from the old policyNew policy did not pick up prior actsOld policy never addressed adding tailOld agency held liable for claim

Phone call from agent.• Is there an issue with me writing the GL

and another agent writing the BAP

• Loading and unloading for one

–Do both carrier forms sync

–Will the customer get cancelled for

non-pay with other agent

–Get rewritten with a carrier with

language that creates a coverage gap

• Not good risk management for

customer or agency

Marshall Katz MS, CIC, LUTC, LIA, AAI 11

From: Utica Claims

Sent: Monday, January 13, 2014 9:50 AM

To: Ann Tobin

Subject: Re: Flood Claims Question

Ann, This is all the documentation we have regarding floods.

1) In 2012, we set up 16 flood related claims nationally. In 2012, we had no flood related losses in MA.

2) In 2013, we set up 20 flood related claims nationally. In 2013, we set up 1 flood related claim in MA.

3) We have set up ( in 2012 and 2013) 37 claims relating to hurricane Sandy for losses in NJ, NY and CT, and approx. 30 of those claims were flood related.

Senior E/O Claims SpecialistUtica National Insurance Group

Helpful Tools• Online RMV Manual: www.massagent.com

–All the things you need at a touch of the button

–Searchable data

–The RMV uses it

• www.roboform.com

–Automatically go to the logon page

–Automatically pre-fills your user name and password, then selects enter

–All you need is one password for all your logons☺

• Virtual Risk Consultant

Marshall Katz MS, CIC, LUTC, LIA, AAI 12

What About Plows for PL?

c. "Motor vehicles".

(1)This includes:

(a) Their accessories, equipment and parts; or

(b) Electronic apparatus and accessories designed to be operated solely by power from the electrical system of the "motor vehicle". Accessories include antennas, tapes, wires, records, discs or other media that can be used with any apparatus described above.

The exclusion of property described in (a) and (b) above applies only while such property is in or upon the "motor vehicle".

(2) We do cover "motor vehicles" not required to be registered for use on public roads or property which are:

(a)Used solely to service an "insured's" residence; or

(b)Designed to assist the handicapped;

ISO’s 1991/2000ISO’s 2011

• Does this expose unknowing customer?

• Does this expose the agency to an E & O claim when

another carrier in the office is more lenient?

• How have we let the customer know of this issue?

Marshall Katz MS, CIC, LUTC, LIA, AAI 13

From a thinking class participant:

This language is ambiguous at best. I see several scenarios

where this exclusion would apply. For example: Mom and dad

purchase a vehicle for their child while in college. They own it

and insure it in their name listing the child as principle

operator. The child graduates and moves to a new community.

Mom and dad allow the child to continue to use the vehicle

and the garaging is changed to the child's new address. The

child pays the mom and dad for the use of the vehicle which

includes any loan payment and insurance costs. The

exclusion is triggered by the final words, "for any

compensation" and applies since the child is no longer a

household member. Wouldn't the money paid to mom and

dad be considered "compensation" since the loan debt is

legally theirs? The policy has been rated correctly for the

exposure but this language seems to eliminate all coverage

except PIP.

Another example would be a grandparent

who owns a vehicle but no longer drives.

They allow the grandchild (non household

member) to "use" the vehicle and the

grandchild pays any additional cost of

insurance and pays to maintain the vehicle.

Maybe they even take her grocery

shopping as a "thank you". Is this also

considered "compensation"?

Marshall Katz MS, CIC, LUTC, LIA, AAI 14

And, an unmarried couple at one time

living together, the vehicle is registered and

owned by person 1 (since person 2 had

credit issues), driven primarily by person

2. Person 2 moves out (garaging is

changed) and agrees to pay all fees for the

vehicle when they separate. Is this

considered a leasing arrangement where

this exclusion would now apply? What

about divorce situations?

We are not a voluntary agent with …, but my initial

concern would be with MAIP policies. If the customer

has no choice in the company assignment and they

have previously been covered for the exposure, would

we be able to change their carrier assignment or

would this endorsement not apply to MAIP policies?

The bigger issue would be that agents are not always

aware of every policyholder's living arrangement and

we will never know what they do day to day. We do

however have an obligation to make sure they are

properly covered which in this case seems impossible.

If … is doing this now, it seems that others will adopt

similar endorsements.

Marshall Katz MS, CIC, LUTC, LIA, AAI 15

Is Lead Paint Liability Coverage desired?

1. Circle response above

2. Sign where indicated

3. Return in the envelope provided

YES, I have circled coverage desired, please invoice me.

NO, I do not want coverage.

__________ x_______________________________

date signature

Mrs. SlumlordMrs. SlumlordMrs. SlumlordMrs. Slumlord3/2/2014

These kind of projects make us money.

re: Identity Fraud Expenses Endorsement Available

Vermont Mutual Insurance Company has just made available a

new endorsement that can be added to your homeowners policy

for identity fraud expenses.

The endorsement costs $25.00 per year and can cover up to

$15,000 for “expenses” incurred (see enclosed sample

endorsement).

Please complete below and return in

the envelope provided:

__X_ YES, please add this to my policy and bill me separately

_____ NO, do not add this to my policy

_______ x____________________________

date signature

If you have any questions, please feel free to call.

Sincerely,

MarshallMarshallMarshallMarshallMarshall D Katz

Mr. ThanksalotMr. ThanksalotMr. ThanksalotMr. Thanksalot3/2/2014

Marshall Katz MS, CIC, LUTC, LIA, AAI 16

Little endorsement

• Costs $25.00 per year

• Mail to 1,000 customers

• 500 agree to buy it

• 500 X $25.00 = $12,500 new premium

• $12,500 X 20% = $2,500 new commission

• 1,000 letters cost $390.00 postage

• customers are better covered

• Added coverage will probably not be removed

• Agency gets compensated

Liquor and the ISO 2000/2011 HO Policy Forms

• Most companies have been saying no host coverage related to vehicle use.

• MPIUA now states there is none.

• Court agreed.

• How do you know what your carriers position is?

• How about asking each one?

Marshall Katz MS, CIC, LUTC, LIA, AAI 17

Massachusetts Property Insurance Underwriting Association (MPIUA) v. Berry, Lawrence, Mass.,

Homeowners Patrick Bernier and Julien Caron negligently served alcohol to David DiFrancesco, a guest in their home.

Under the influence, Difrancesco caused a motor vehicle accident, striking a car operated by Malcolm Berry, who sustained serious injuries. Berry sued Bernier and Caron and the court agreed with MPIUA (Bernier & Caron’s HO company) that the 2000 ISO form does not cover the exposure.

From The Standard

Auto Exclusion Applies In Social-Host Liability Case

To Do Tomorrow for 2000/11 HO

• Ask all of your carriers to develop an annual endorsement to cover liquor exposures for negligent supervision of a vehicle?

• Ask ISO to develop an annual endorsement to cover liquor exposures for negligent supervision of a vehicle?

• Ask RLI to develop an annual endorsement to cover liquor exposures for negligent supervision of a vehicle?

• Connect with N & D? They have an endorsement.

• Find a market for those already in a 2000/11 policy form�maybe excess & surplus 1991 form is better than any company with 2000/2011?

Marshall Katz MS, CIC, LUTC, LIA, AAI 18

Verdicts

In 1994 a New Mexico jury awarded

$2.9 million U.S. in damages to 81

year-old Stella Liebeck who suffered

third-degree burns to her legs, groin

and buttocks after spilling a cup of

McDonald's coffee on herself.

Questions:1. What were the limits on the policy?2. Was there an umbrella in play and what limits were

offered?

More

Jim was temporarily blind in one eye when hit by a golf ball on a golf course. Jim had just played out a par 3 hole and left the hole with 3 other players. Jim remembered that he left his 25-cent ball marker on the green and walked back on the green to get it. The foursome following had already hit a tee shot that was in flight when Jim got back on the green. The foursome yelled "fore" and the rest of the story was an insurance company payment to Jim for $106,000!

Bottom Line:Everyone should have a personal liability policy they can attach to when needed for coverage.

Marshall Katz MS, CIC, LUTC, LIA, AAI 19

Emerging Exposures•Mold

•Identity theft

•Kidnapping

•MAIP

•Computer Malpractice

•Replacement cost coverage for personal lines autos

•Building ordinance

•Divorce

•New exclusions on policies

•Flood as a peril on some commercial policies

Marshall Katz MS, CIC, LUTC, LIA, AAI 20

MAIP

• Tuesday agency called MAIP about someone with a DUI.

• Tuesday MAIP said to write application with Collision/Comp on the policy and the assigned company will determine if they will allow.

• Wednesday insured called the agency that Tuesday night all tires on their monster truck were slashed.

• What went wrong if agency has to pay the claim?

MAIP Sign-Off

• I fully understand that the application for the 2008 Ford Mustang must be assigned an insurance company by the MAIP (MA Assigned Insurance Plan).

• I also fully understand that any coverage chosen on the application must be approved by the assigned insurance company in writing and no oral or written representations made will alter that process.

___________ x_____________________

date signature

3/2/2014 Ms. Drunk BeyondbeliefMs. Drunk BeyondbeliefMs. Drunk BeyondbeliefMs. Drunk Beyondbelief

Marshall Katz MS, CIC, LUTC, LIA, AAI 21

Irene has her 2008 Corvette insured with company A and Robin has her 2008 Corvette insured with company B. They both collide while staring at an Aston Martin parked on the roadside. When they exchange information, Irene mentions that at least she will get the cost to replace her Corvette with no depreciation. Robin wants to know what agency is she with, as she does not have that coverage? Irene tells Robin that she is insured through the Special-cars Insurance Agency. Robin then says she is too�!!!!!!!

3/2/2014

Dear auto renewal:

Your auto policy is renewing shortly on your 2009 Mercedes. The agency wants to offer you a choice of coverage:

���� ABC Mutual (current company) insures your car on a depreciated value. Premium $850

���� DEF Mutual (new company) insures your car on a replacement (new) cost basis. Premium $950

Please select one above, sign and mail in the enclosed envelope within 30 days of the above date.

_______ x_______________

date signature

Marshall Katz MS, CIC, LUTC, LIA, AAI 22

Importance of Building Ordinance for Commercial Lines

An old funeral parlor building had a major fire and upon rebuilding they were required to construct a hydraulic lift to bring the “guest” from the basement to the viewing room (some new code). Well the policy they had did not cover building ordinance coverage and the funeral parlor ended up out of pocket for $100,000 in expenses not covered. How then does a funeral parlor and agent cover this loss? �Make sure the construction costs calculated for

the building is 100% to value �The Building Ordinance endorsement has been

added to the policy at the 100% total coverage limit.

Marshall Katz MS, CIC, LUTC, LIA, AAI 23

From November 2012 class

• Agency wrote home for $500,000 coverage A

• Fire loss $80,000

• Building inspector condemned home as unsafe leaving a $420,000 building ordinance loss

• Carrier paid $80,000 fire loss and $50,000 for building ordinance loss (10% of coverage A)

• Customer suing agency for $370,000 for not asking if the customer wanted the endorsement raising the 10% to 100%

• Endorsement comes in increments

$11.3 Million Award

• Defamation of character judgment

• From a blog site!!!

• How many customers have a personal/commercial blog that can create a legal obligation to another?

Marshall Katz MS, CIC, LUTC, LIA, AAI 24

Best Practices

• How does your agency operate?

• How do other agencies operate?

–In your area

–Across the country

• The better set-up..the lower the E & O loss ratio

• E & O carriers expect suits even when groundless. They do however watch for repeated causes of action; the same staff member causing them and the agencies remedy to curtail the suits.

CAUSES OF E & O LOSSES SECTION

Marshall Katz MS, CIC, LUTC, LIA, AAI 25

Causes of E & O Losses • Organizational Structure

• Lack of uniformity to practice and procedures

• Inadequate training

• Time constraints

• Chronic backlog

• Not hiring the right people

Boss

Commercial

Lines Mgr

Personal Lines

Mgr

Accounting Dept

Mgr

Sales

CSR

Sales

CSR

A/P

G/L

Vertical Structure

Horizontal Structure

Boss Sales CSR G/L

Michael Gerber: E Myth Series

Marshall Katz MS, CIC, LUTC, LIA, AAI 26

Why get licensed?P & C LA&H Adviser

To be legal when transacting insurance when no one licensed is present

To be legal when transacting insurance when no one licensed is present

To get paid for giving someone information to help their business; what about you?

Commissions Commissions Fee

Persistency Persistency Professional

Did I get the

best employee

for the

position?

Marshall Katz MS, CIC, LUTC, LIA, AAI 27

AGENTS’ AND BROKERS’ STANDARD OF CARE SECTION

State Law Issues

http://www.ifb.org

Focus Fraud Magazine

Good examples.

Competition may be in there?

Names names!

Magazine can be mailed to home or office.

Marshall Katz MS, CIC, LUTC, LIA, AAI 28

State Laws - more

• Misrepresentation

• False advertising

• Discrimination

• Defamation

• Rebating

• Larceny

• Perjury

• Fraud

Not good

Duties of Care

•Claims made by companies

•Claims made by customers

•Claims made by others

Marshall Katz MS, CIC, LUTC, LIA, AAI 29

Claims Made by Insurers

• Failure to pay attention to:

–Underwriting guidelines

–Agency contract

• Failure to disclose material facts

• Failure to act in best interest of insurer

• Failure to:

–Revise coverage when requested

–Cancel coverage when requested

Contractual Duties to Customers

• Failure to obtain coverage as requested*

• Failure to advise customer on issues

• Failure to identify exposures*

• Order take state issues!

*#1 E & O Cause depending on resource

Marshall Katz MS, CIC, LUTC, LIA, AAI 30

Agency Practices vs. Legal DutyCreating a duty where none previously existed

• Contacting late payers

• Contacting the bank for customers

• Carrying late paying customers with agency bill

accounts

• Notifying customers when license plates are

about to expire

• Calling about restoring coverage

– Motorcycles

– Campers

– Etc.

Do you or the agency create

a duty where none exists?

Claims Made by Others

• Certificate holders

• Mortgagees

• Lienholders

• 3rd parties

• Government

• Etc.

We don’t know

them…but will

have a

relationship to

them!

Marshall Katz MS, CIC, LUTC, LIA, AAI 31

November 2012 Class

• Carrier paid customer $18,000 after a total

• Customer went out and used the money to purchase another vehicle

• The bank on the 1st vehicle asked customer for the $13,000 loan balance

• The customer did not have it�

• So the bank received the money from the agency as they did not list the lienholder on the policy as they were listed on the RMV-1.

• 10/14/2009 06:20 PM Subject: Question Hi Caryn: I am an instructor with MAIA and I heard a statement made at class by a student that Massachusetts is an order taker state and that it is not the agents job to offer higher limits or coverage and that it is the insureds job to tell us what they want. This statement was made to them by an E & O attorney representing them on a claim.

• Perhaps the E & O attorney who was representing the student on the claim could shed more light on what he meant. Our counsel in MA have advised that the case law in MA states that an agent has a general duty to use skill, care and diligence to procure the requested insurance and that there is no duty to advise absent special circumstances. If asked, we would advise an agent in any state that they should make and save any records of discussions concerning increased limits or broader coverage.

• Caryn L. Mahoney | AVP | Claims & Liabilities Commercial Insurance | Swiss Re | Mailing address: Specialty Claims PO Box 29221, Shawnee Mission 66201, USADirect: (312) 821- 4238 Fax: (877) 880-1590 E-mail: [email protected]

http://www.swissre.com

•

Marshall Katz MS, CIC, LUTC, LIA, AAI 32

Account ReviewsThere are many sources of information available to agents

and brokers including:

�Physical inspections

�Interviews with key personnel

�Review of financial statements

�Review of contracts and agreements with vendors,

suppliers, landlords, tenants, and others for insurance

requirements

�Review of the customer’s advertising materials,

brochures, and website to gain a complete understanding

of the prospect’s operations

�Flow charts to analyze the basic processes of the

customer

�Surveys and checklists

Marshall Katz MS, CIC, LUTC, LIA, AAI 33

Marshall Katz MS, CIC, LUTC, LIA, AAI 34

Son

Last resort

1st he looks to household members

DadMaid

Hanover

Commerce

MetLife

Rear-

endedNot a HH Member

Uninsured / Underinsured

• You don’t own a car policy – you get your highest household members policy coverage

• You don’t own a car policy and don’t have a household member you get the vehicle you are in policy coverage

• You do own a car policy and in another auto – you get your highest policy limit

• You are in an owned auto – you get that policy limit

Marshall Katz MS, CIC, LUTC, LIA, AAI 35

Hit by another at-fault auto.

Do I have a policy?

No

Get highest HH member

policy

No HH member

Get auto I’m in coverage

Yes

Was I in my auto?

No

Get my highest

Yes

Get limit on that

auto

UM / UIM

$230,000 E & O

• Auto policy customer wants a motorcycle policy in her name

• Boyfriend is primary operator

• Boyfriend is step 9, bad credit

• Agency recommends and sells 250/500 limits on parts 3, 5 & 12 on the motorcycle policy

• Boyfriend is seriously hurt occupying motorcycle by an uninsured driver

• Boyfriend only collected the 20/40 he had on his own auto policy insured with a different agency

• Sued agent writing the motorcycle policy stating they did not inform him to increase his auto policy

• The agency lost

Marshall Katz MS, CIC, LUTC, LIA, AAI 36

A commercial one

• Agency wrote for many years a commercial auto policy with 20/40 U1 & U2 limits but 500/500 bodily injury liability

• Employee has friend in vehicle who gets hurt bad by an at fault driver with minimum limits

• They go back to the commercial auto policy for coverage because the friend lives alone and does not own a vehicle

• Agency gets sued for not having U1 & U2 limits the same as the bodily injury limits and loses because they have no proof they offered higher U1 & U2 limits

From Agency November 2012• Agency wrote husband 250/500 limits

• Another agency wrote wife 50/100 limits

• Each were “you’s” on their own policies

• Wife hit by uninsured driver and collected 50,000 from her policy

• Wife sued husbands agency for not having her as a named insured on his policy

• Problems:

– Carrier may not have listed wife as she is not a titled owner of husbands auto!

– Why didn’t wife have her car with the better agency in the 1st place?

– Why didn’t they sue the wife's agency for low limits?

Marshall Katz MS, CIC, LUTC, LIA, AAI 37

I got a call

I was asked to be an expert witness to

testify against an agency to help a law

firm collect an E & O claim

Homework:

1.Ask all of your auto carriers to do a book profile of all policies where the UM/UIM limits are lower than BI and get that information to you.

2.Look at umbrella polices that can give higher UM/UIM limits such as RLI through MAIA or companies I am told like Chartis?

3.Then sell high limits to everyone.

Do you offer Named Non-Owner Policies to those that don’t have an auto?

Some Issues:• No/not enough liability coverage on

vehicles driven• Lack of sufficient UM/UIM coverage• No physical damage coverage• Not being a “YOU”• Other

Marshall Katz MS, CIC, LUTC, LIA, AAI 38

Class Participant

• Boyfriend owns both cars

• Boyfriend is a you

• Girlfriend is listed operator

• They go on vacation and rent a car in boyfriends name and do or do not list girlfriend as driver

• Girlfriend has coverage only from rental agency

• MAP/PAP gives permissive users coverage for “YOUR AUTO” or “YOUR COVERED AUTO”

• Boyfriend has coverage for any auto on parts 4 and 5�girlfriend does not

• Girlfriend also has issues with parts 3, 6, 7, 8, 9, and 12

20/40 $47 30/70 $87 250/500 $358

20/50 $51 35/80 $105 500/500 $677

25/50 $65 50/100 $141

25/60 $69 100/300 $221

3/2/2014 Mr. Fraud WayMr. Fraud WayMr. Fraud WayMr. Fraud Way

$1,000,000 Umbrella Liability Coverage Desired? $150.00 Yes / No (co approval)

Marshall Katz MS, CIC, LUTC, LIA, AAI 39

I have read the above and have reviewed the associated costs for the various coverage's above and understand the circumstances should I not have the proper coverage after an accident or loss.quickpick

3/2/2014 x Mr. HighsdipMr. HighsdipMr. HighsdipMr. Highsdip

$150$225

Check oneAdditional autoReplacement auto – auto

replaced___________

Added to top of quickpick sheet

���

Check oneAdditional autoReplacement auto – auto replaced____________�� 2005 Nissan Xterra

�

Now everyone knows what transpired.�Customer signs off on it�Sales is clear to data entry person�Upload/Download is done right the first time

Marshall Katz MS, CIC, LUTC, LIA, AAI 40

Liability Sign Off

I also acknowledge and verify that a representative of

Good Humor Insurance Agency has explained to me

that in the event I am in an accident that is my fault,

where liability is undisputed and damages clearly

exceed my policy limits that I have chosen, my

insurance company may have to pay those policy limits

to the injured party(s) without obtaining a release of my

liability. In that event I may have continuing legal

exposure for additional damages. I also understand that

such payment of the policy limits by my insurance

company may release my insurance company from any

duty to, or continuing duty to, defend me in any lawsuit

filed for that accident.

_________________ x______________________________date signature

3/2/2014 Mr. IsueregularlyMr. IsueregularlyMr. IsueregularlyMr. Isueregularly

Vehicle Usage Affidavit (personal Lines)

customer name

policy number

I am aware of the following language in my policy: If you or someone on your behalf gives us

false, deceptive, misleading or incomplete information in any application or policy change request

and if such false, deceptive, misleading or incomplete information increases our risk of loss, we

may refuse to pay claims under any or all of the Optional Insurance Parts of this policy. Such

information includes the description and the place of garaging of the vehicles to be insured, the

names of all household members and customary operators required to be listed and the answers

given for all listed operators. We may also limit our payments to those amounts that we are

required to sell under Part 3 and Part 4 of this policy.

Operator name

%

95 Wagon 03 SUV

Mom 100

Dad 100

_________ x______________________________

date insured signature

I understand if the usage changes, I will notify the above insurance agency so that an

adjustment can be made to the policy. If I fail to notify the above insurance agency and a loss

takes place, the insurance company may act in accordance with the above paragraph.

80 Ford

100JR 5

Garaging Worchester Brighton Northampton

Marshall Katz MS, CIC, LUTC, LIA, AAI 41

Vehicle Usage Affidavit (commercial Lines)

customer name

policy number

I am aware of the following language in my policy: If you or someone on your behalf gives us

false, deceptive, misleading or incomplete information in any application or policy change request

and if such false, deceptive, misleading or incomplete information increases our risk of loss, we

may refuse to pay claims under any or all of the Optional Insurance Parts of this policy. Such

information includes the description and the place of garaging of the vehicles to be insured, the

names of all household members and customary operators required to be listed and the answers

given for all listed operators. We may also limit our payments to those amounts that we are

required to sell under Part 3 and Part 4 of this policy.

95 GMC 03 Chevy 07 SUV 08 Mercedes

Garaging

Farthest location driven to

_________ x______________________________

date insured signature

I understand if the usage changes, I will notify the above insurance agency so that an

adjustment can be made to the policy. If I fail to notify the above insurance agency and a loss

takes place, the insurance company may act in accordance with the above paragraph.

No Part 5 Optional Bodily Injury to Others Desired

I understand without this part to the auto policy I will not have any coverage:

1. For injury to guests

2. For injuries caused out of state

3. For injuries in Massachusetts on private ways and roads.

I may also lose driving privileges if I am in an accident out of state, and then lose my license in Massachusetts.

The agency then recommends not to drive any auto.

_________ x__________________

date signature

Iknowmorethanyou, MDIknowmorethanyou, MDIknowmorethanyou, MDIknowmorethanyou, MD3/2/2014

Marshall Katz MS, CIC, LUTC, LIA, AAI 42

Marshall Katz MS, CIC, LUTC, LIA, AAI 43

Marshall Katz MS, CIC, LUTC, LIA, AAI 44

xxxxMrs. GreathealthMrs. GreathealthMrs. GreathealthMrs. Greathealth

����

3/2/2014

Conditional Receipts• Coverage is conditional if insured

dies during the underwriting process

–Correct modal premium received

–All conditions (medical, etc.) have been done

–&

–Carrier would have approved the application as is.

Marshall Katz MS, CIC, LUTC, LIA, AAI 45

Life Insurance - more• All lines sold need to ask and get an answer

if the customer wants life insurance

Example

• Customer died not having life insurance

• Customers widow sued agency for not selling a policy to spouse

• Agency lost in court because they could not produce a declination of coverage offered signed by the customer

• This court case dictates a need for a process of getting the customer from one policy unit to another

THE CUSTOMER LIFE CYCLE SECTION

Marshall Katz MS, CIC, LUTC, LIA, AAI 46

Marketing & Selling Issues

• Failure to identify exposures

• Failure to ITV (insure to value)

• Failure to recommend higher limits

• Proposal errors

• Overstating policy benefits

Marshall Katz MS, CIC, LUTC, LIA, AAI 47

The Sump Pump Issue

• Agency had customer for 13 years

• Moved insured to 3 different companies

• Insured suffered a sump pump backup loss

• Insured did not have endorsement

• Agency contends insured did not tell them they had a sump pump

• Insured contends agency has a duty to ask if they have one

• Who do you side with?

Which is the best statement?

• The agency recommends carrying

100/300 bodily injury liability

coverage

• The agency recommends carrying

at least 100/300 bodily injury

liability coverage

Marshall Katz MS, CIC, LUTC, LIA, AAI 48

Confirm in writing – keep copy

Sometimes

• Certificate of mailing

–Pre-inspection notices

• Certified Mail Return Receipt

–Coverage issues

–Flood policy application & premium

–New applications to E & S & MGA markets

• Bulk mail to let everyone know…but

–Keep all documentation

–Copy of letters, receipt from PO, listing of all mailed with count

E & S Markets• Get copies of their license and E & O coverage

• Can it be placed 1st in the voluntary markets, if not

keep all rejections, guides, etc. as part of file

• Number all application pages 1 of 10, 2 of 10, etc.

• The quote form has important info:

–Earned premium

–Coverage deficiencies

• Get copies of the form and endorsements that will be

part of the new policy and review

• Is the carrier solvent?

• Have customer sign off on the E & S quote formI accept and understand the terms above.

_________ x______________________________

date signature3/2/2014 Ms. Dontinsureme

Marshall Katz MS, CIC, LUTC, LIA, AAI 49

FORM BR-7 AFFIDAVIT BY ASSURED Affidavit #______

I/We ____________ of_________ do hereby state that in ________20____, I/We directed______________my/our Insurance Broker to obtain insurance against certain risks as described herein. My/Our Insurance Broker informed us that the required insurance could not be obtained from, or would not be written by, companies licensed or admitted to transact business in the Commonwealth of Massachusetts.1/We, the Assured, was/were informed that the type and amount of insurance shown below could be obtained from certain

insurers not admitted to transact business in the commonwealth. I/We was/were further informed:

A. The surplus lines insurer with whom the insurance was placed is not licensed in this state and is not subject to

Massachusetts regulations.

B. In the event of the insolvency of the surplus lines insurer, losses will not be paid by the state insurance guaranty fund.

Signature by Assured_________________________________

Print name__________________________________________

Date_______________________________________________

THIS PORTION MUST BE COMPLETED AND SIGNED BY THE ORIGINAL BROKER

Name of Insured:___________________________________Address: ______________________________________________

Location of Property: _____________________________________________________________________________________

Description: ____________________________________________________________________________________________

Coverage: ______________________________________________________________________________________________

Limit: ___________________________________________Premium: ______________________________________________

I/We hereby verify that I/We explained the foregoing to the insured and it was acknowledged that he/she understood such.

SS/Fed. Tax ID ___________________________Signature__________________________________Date__________________

A copy of this affidavit must be kept in the original broker’s file and a copy must be given to the assured at the time said copy was completed by him/her.

Email from MAIA’s Attorney Dan Foley.

• Marshall,

• You can tell folks what the Commissioner has told us when we met with him on this matter as you referred to in your second paragraph. But certainly, the affidavit does present a legitimate issue, but that fact that in your condo example, the premium is less and the policy has extra bells and whistles in a specially designed program, this policy cannot be purchased in the voluntary market, so you can’t obtain coverage that meets the needs of your insured, so you can place it in the E&S market.

• It certainly would be nice if we could resolve the Affidavit issue however. At the meeting with the Commissioner, we did give him the affidavit that NJ uses that possibly could resolve this issue. Obviously, this issue is not at the top of the DOI’s priority list with everything else that is going on.

• Dan (Foley, MAIA)

Marshall Katz MS, CIC, LUTC, LIA, AAI 50

New Business Proposals

Applications

CUSTOMER PROPOSALS

• Insurance proposals can provide a wealth of

defense documentation, including:

– outlines coverage's offered

– highlights coverage limitations

– any insured requirements

– E&O coverage checklist

• Customer sign-offs acknowledging what was

discussed should be included

• It is also a good idea to have the customer initial

each page of the application and sign where

required

Marshall Katz MS, CIC, LUTC, LIA, AAI 51

PROPOSALS – CARRIER SYSTEMS

• Many agencies may present proposals

exactly as they are generated from carrier

underwriting systems.

• These proposals may not include

appropriate disclaimer information or an

area for customer sign-off.

• The agency may want consider adding a

supplemental page for both of these.

WAIVER FORMS

• Some states require acknowledgement

waivers to be signed for various coverage's

(i.e. – UM/UIM, earthquake, flood Acord 60)

• ACORD also offers some template forms.

• Carriers may specifically require waivers

when certain coverages are rejected.

• Waivers are important for E&O defense;

therefore, agencies need to determine

when a waiver is required.

Marshall Katz MS, CIC, LUTC, LIA, AAI 52

HE SAID VS. SHE SAID

•“The faintest ink

is stronger than

the most vivid

memory”

New Business• Use checklists (Big I)

• Sell the most liberal company offerings to all

• Have insured sign-off on coverage/declines

• Have insured sign the application and initial each page

• Check binding authority before binding

• Verify policy received is the one ordered

• Use transmittal when sending

• Don’t accept pre-dated checks or signatures

• Renewals s/b treated as new business

Marshall Katz MS, CIC, LUTC, LIA, AAI 53

Applications�Never sign on behalf of a customer

�Only have the customer sign (power of atty.?)

�Initial key points (Fraud Class)

�Advise customer to review whole application

�If mail application to new customer get it as a

notarized signature

�Establish a system to submit to carriers ASAP

�Date and time all – don’t accept early

dates/checks

�Use most restrictive company rules for all

Auto Situation

• Insured came into agency at 11:00 AM for new auto policy

• Insured called next day to report accident the day before that occurred at 10:00 AM

• Agency advised them no coverage because the application was taken 1 hour after

• Insured said they were in the agency at 9:00 AM, 1 hour before accident

• Court upheld claim as agency had no proof to support time

Marshall Katz MS, CIC, LUTC, LIA, AAI 54

No other operators

Not wanted

initials

Have the IT Department Fix App.

• If customer does not want something�the application should automatically trigger it

Customer stated not wanted

Remember anything we talk about applies to all linesS

Marshall Katz MS, CIC, LUTC, LIA, AAI 55

Agency did not place customer with a company that gave pollutant clean-up coverage for an outside oil tank. One of the companies in the office provided this coverage while the others did not.

Result was the agency writing a $28,000 check. They have a $50,000 E & O deductible.

Bruno’s Landscaping

1.Have an overall line of business list

2.Then have a drill down form and endorsement list by the specific line being written

Marshall Katz MS, CIC, LUTC, LIA, AAI 56

Personal Lines Checklist

Yes No

Auto insurance desired � �

Home, apartment or condo insurance desired � �

Umbrella liability insurance desired � �

Flood insurance desired � �

Life insurance desired � �

Named non-owner auto policy desired � �

Other insurance desired � �

Date 3/2/2014 Signature x Ms. Ms. Ms. Ms. SmoothoperatorSmoothoperatorSmoothoperatorSmoothoperator

�

�

�

�

�

�

�

Quotes - Management

Taken

Binder

Policy

Not Taken

Why

ReviewWhy make quotes a timewaster adding to a backlog of calls/emails not answered timely?Research why the customer did not buy?Research why the customer did not stay? Follow the money�is someone pocketing cash?Consider not taking cash payments?

Marshall Katz MS, CIC, LUTC, LIA, AAI 57

Endorsements• Changes need to be sent to carriers on

the most restrictive carrier timeline

• Need to have the “you” make the change

• Do not act on behalf of a 3rd party

• Enter data in management system

• Confirm change with insureds signature

• Use the contact to cross-sell

Drive Fax Deficiencyre:

Dear Dealer:

We have received a fax on the above customer.

We can not fax back the RMV1 and a binder for the following reasons:

���� Title or Certificate of Origin missing

���� Title or Certificate of Origin not signed

���� RMV1 missing

���� RMV1 not signed

���� Our customer did not contact us in advance. In an effort to protect our customer we have called our customer and as soon as they confirm purchase of the above vehicle we will fax the necessary forms back to you.

If you have any questions, please call.

Sincerely,

Only the “You” can say process it!

Marshall Katz MS, CIC, LUTC, LIA, AAI 58

“Replacement Business”

• Consider doing an exit interview with customer (the you)!

• Why?

–Customer is the only one that counts

–Take-over letter may be fraudulent

–Customer never intended to leave

–Customer changed their minds and wants to stay with you

–Customer only wanted a quote

• Consider only accepting LPR from the new writing agent for all lines

Builders Risk Sign-offProject: 100 Main St, Small-town, USA

I fully understand that any change orders have to be faxed or mailed to the agency to increase coverage on my policy. If I do not receive written confirmation from the agency or company, my policy does not include these change order additions and I will not be insured properly.

______ x__________________

date signature

3/2/2014 Mr. G. C. Contractor

Marshall Katz MS, CIC, LUTC, LIA, AAI 59

Claims

•Claims Handling� Doing nothing can upset customer

� Advise what:

� customer needs to do

� customer can expect from others

� Call them at regular intervals

� Look at all carriers for liability-Is there Umbrella

� Report all losses?

�Liability-ASAP

�Property-Is claim over deductible, will it be?

�Disaster Plan

Marshall Katz MS, CIC, LUTC, LIA, AAI 60

Claims - more

• Never indicate if claim will be paid

• Never talk customer out of placing a claim (93A – bad faith issues)

• Don’t give personal referrals to repair

• Monitor insureds for claims activity

• Practice fraud “red flags”

• Have a claims “how to” manual on how to handle for each line and carrier

• Never admit to carrier it was your error

• Consider calling E & O carrier early on

claimsI fully understand the following:

Insurance policies are intended to pay catastrophic losses like your house burning down or getting hit by a tornado, not for small losses. The agency encourages everyone to take a high deductible so that you can buy more catastrophic coverage and thereby not collect on small losses. Small collectible losses could cause:

1. Non-renewal of your policy

2. Lose loss-free credits, causing a premium increase

_______ x_________________

date signature

3/2/2014 Ms. Ms. Ms. Ms. SmallclaimsSmallclaimsSmallclaimsSmallclaims

Marshall Katz MS, CIC, LUTC, LIA, AAI 61

Renewals

Renewals need:• Proactive communication

• 60-120 days prior to renewal date

• Contact insured to review coverage

• Have an agenda to email, fax or mail them

• Envelopes need to indicate this is important

• Consider a specific renewal department

–Multi-tasking doesn’t work – great article

– http://techtips.steveanderson.com/2014/01/30/the-

myth-of-multitasking/

Marshall Katz MS, CIC, LUTC, LIA, AAI 62

RENEWALSSome areas of concern?

• Mono-line auto

• BAP with no PAP

• PAP s/b a BAP

• No auto coverage at all

• Low U1/U2/UM/UIM

limits

• Low PD / BI limits

• Low or no umbrella

coverage

• No review in forever…

• Etc.

• DP1 with MPIUA

• No liability coverage

for a DP policy

• Duplicate liability

coverage for a DP

policy

STAY WITHIN YOUR EXPERTISE

• Easy to say but hard to do when an opportunity

presents itself.

• When additional expertise may be needed:

– Complexity/scope of operations

– Number of locations

– International operations

– Large network of supply chain vendors

– Products and completed operations

– Familiarity with specialty coverage's

Marshall Katz MS, CIC, LUTC, LIA, AAI 63

Consider developing a specific

renewal department?

Why are forward thinking organizations creating

these departments?

• The staff working in them can concentrate on:

– The renewal process and the customer

– Up sell activities

– Cross sell activities

– Little distractions with walk-ins or phone calls

– Make it a profit center

Insurance Renewal Letter

Dear customer:The Massachusetts insurance policy has options and we wanted to make you aware of those and to give you the opportunity to change your renewal policy. Part 6 - Medical Payments coverage is now available with higher options. If you or those riding with you do not have any health coverage or have poor health coverage, then you may want an option below. Just select by circling the option desired, sign where highlighted and mail in the envelope provided.

_____ Yes, I have circled an

option desired

_____ No option desired

PART 6 MEDICAL

PAYMENTS

Limit Per

Person

Rate

$500 $13

750 19

1000 24

2000 45

5000

10,000

15,000

20,000

25,000

91

167

225

236

247

______ x______________________

date signature

Marshall Katz MS, CIC, LUTC, LIA, AAI 64

Motorcycle Insurance Renewal Letter contd.

Coverage options have also changed for those desiring to insure their motorcycle on a “Stated Amount Basis”. This means that you can have your motorcycle appraised and insured for that appraised amount, rather than the book value that does not take into account customization.

_____ I will mail an appraisal to your office to insure my motorcycle(s) to its proper value.

_____ I do not need anything other than book value. (to check your book value www.kbb.com)

______ x______________________date signature

Ms. Ms. Ms. Ms. RubbersidedownRubbersidedownRubbersidedownRubbersidedown

����

����

3/2/2014

Marshall Katz MS, CIC, LUTC, LIA, AAI 65

Marshall Katz MS, CIC, LUTC, LIA, AAI 66

Do the envelopes you use;Help the insured understand coverage?Help sell more coverage?Get noticed at the mailbox?

No return postageSno ones going to return your mailing.

Marshall Katz MS, CIC, LUTC, LIA, AAI 67

3/2/2014

Dear Pick-up or Van driver:

The MA auto policy only covers stock (factory) items. If you have dealer installed or other after market items and want them covered, please complete below. If you do not have any items, please also let us know.

Please complete and return within 30 days so that we may change your policy before the renewal. After 30 days the change may take effect after the renewal.

Do you have any of the following installed (include values)*:

���� Tool box $ ���� Cap $ ���� Raised Roof $

���� Bed liner $ ���� Camper body $ ���� Wheelchair Ramp $

���� Emergency lights $ ���� Plow $ ���� Electronics $

���� Spinners $ ���� Custom paint $

���� Other _______________________________________________

���� No added items to vehicle________ x_____________________

date signature

*If you have receipts mail them in with the form.

Commercial Property

Dear Customer:

Below is a list of properties that your policy with us currently covers. Please review, make adjustments where needed and return in the envelope provided.

Building Personal Property

Delete, Add, Other (explain)

200 Main $1,000,000 $500,000

500 Quincy $2,000,000 $1,000,000

17 Tpke. Rd. $5,000,000

3/2/2014 x Mr. Slumlord

Marshall Katz MS, CIC, LUTC, LIA, AAI 68

Condo Renewal Letter

Marshall Katz MS, CIC, LUTC, LIA, AAI 69

1. Some carriers are placing endorsements

on policies you may not be aware of

unless you review them.

2. Watch for the new ACV roof endorsement

seen on the ISO 2011 HO forms.

3. Watch for flood not covered in

comprehensive coverage on the BAP

4. Etc.

http://public records.netronline.com

Marshall Katz MS, CIC, LUTC, LIA, AAI 70

Only

click a

state

from

here

for no

fee

http://publicrecords.netronline.com

Marshall Katz MS, CIC, LUTC, LIA, AAI 71

Marshall Katz MS, CIC, LUTC, LIA, AAI 72

Bank closing faxdate: June 5, 2005

to: Betty Boopcompany: Aggravation Mortgage Core: Mr & Mrs Good customers, 200 Main St Yuppieville MAfrom: Marshall Katznumber of pages including cover sheet: 1

Please fax back the following for the above:

closing date: loan #:

Mortgagee clause:

Where should the agency fax the binder and paid receipt?Name:Phone:Fax number

Upon receipt of the above we will fax back a binder and paid receipt for the insurance.

Thank you for your cooperation and assistance.

Cancellations

• Companies usually issue, not the agency

• New MA Personal Auto Regulations

• Bad pay accounts

• Stuff not your responsibility (plate & license reminders)

• Tails on Claims Made Policies

Marshall Katz MS, CIC, LUTC, LIA, AAI 73

Cancellations - more

• Let customers know about payment plans

• Compare chronic late pays with claims

• Do not accept company payments

• Don’t accept cash

Marshall Katz MS, CIC, LUTC, LIA, AAI 74

1. Sent a separate one page notice by bulk mail to all customers that we

were stopping notifying that day

a. Didn’t want to miss anyone

b.Wanted the definitive line drawn in the sand

c. Didn’t want to continue the notices 1 more day

d.Could control the expense to 2 mailings and no more employee

time wasted on agency notices each day/week/month

2. Printed a list of current names and addresses it went to with a count

3. Scan all actual letters with names and addresses for future reference

in a bulk file

4. The post office then gives a receipt of how many pieces were mailed

to match our count

5. 30 days later do it one more time

6. Thinking back I would have liked an envelope that stated something

like “open immediately, important changes inside”

7. I wanted to handle separately from mailing policies, endorsements or

other items, so that it didn’t get muddied with other things

8. I already had a bulk mail permit for other mailings like newsletters,

calendars and the like

An agency asked me for thisS

Issues with carriers contacting late payers that are in cancel billing.

• Late payer gets cancelled now;

–Moved to different carrier

–Moved to different agency

–You write them from another agency

• Late payer thinks being notified is SOP

• They don’t get notified and start blaming someone�anyone

• Carriers shouldn't do what agencies stopped years ago

Marshall Katz MS, CIC, LUTC, LIA, AAI 75

Audits• Failure to disclose how policies work

and get cancelled for audit billing

• Review audit worksheets for accuracy

• How does the carrier operate on disputed audits

• Change current policy to reflect past audit performed

• Pro-forma’s ½ way through policy period to see if customer is on track

Workers Comp Quotedate

Name

Address

City state zip

Workers Compensation Policy Quote

effective date: upon approval by insurance company

DEPOSIT premium based on annual payroll of $(subject to audit by carrier)

limits of coverage/premium: circle coverage desired

100,000/500,000/100,000 500,000/500,000/500,000 1,000,000/1,000,000/1,000,000

$223.00 $275.00 $301.00

Umbrella policy desired (subject to approval)? Yes / No

$1,000,000 - $450 $2,000,000 - $550 $3,000,000 - $650

$4,000,000 - $750 $5,000,000 - $850

medical deductible credits (they are per employee injured - not incident)

None $500 - $3.00 $1,000 - $5.00 $2,000 - $7.00 $2,500 - $8.00 $5,000 - $12.00

We have had no known workers compensation losses for the past 3 years.

__________ x___________________________

date signature

Policy is auditable up to 3 years. This means the insurance company can ask for your payroll records up to 3 years back and adjust your deposit premium to a final premium. If your payroll becomes higher than above, it would be best to fax our office and adjust the premium as payroll increases on no longer than quarterly intervals.

Subject to policy conditions, exclusions, and company underwriting rules & rates.

3/2/2014 Ms. Ms. Ms. Ms. LowpayerLowpayerLowpayerLowpayer

Marshall Katz MS, CIC, LUTC, LIA, AAI 76

Opt-In/Out• Student from 01-21-09 E & O II class

• Had a self-employed accountant customer

• He suffered a crushed back and hands and couldn’t work

• $400,000 workers comp type injury

• None offered - yikes

“Those of you who know me well know that I have a passion for selling “clean”. Many of the “situations” that wind up with us could have been avoided if the salesperson had fully explained the terms of the sale, made sure that the benefits and features of their product or service matched the needs and wants of their customer exactly, and/or walked away from a customer that they knew was going to be a problem down the road.”

Rick Roberge – Manager of collections

Marshall Katz MS, CIC, LUTC, LIA, AAI 77

CERTIFICATES AND OTHER EVIDENCE OF INSURANCE

Certificates of Insurance

Should You Be Concerned?

2009 E&O Data

• 42% AI missing/wrong

• 24% misrepresentation

• 17% nonexistent

coverages

Corroboration

• City of Atlanta survey

• Agency consultant review

• Florida agency study

• AI endorsement not added$180,000

• Blanket AI endorsement$445,000

• 4,000 bogus certificates$10,290,000

• $150 MILLION claim?

• Average COI claim is $50,000

Marshall Katz MS, CIC, LUTC, LIA, AAI 78

Certificates & Evidence of Insurance

• Completed by a high level thinking person

• Use Acord form only and…

make no changes to the form!!!

• Acord has sued for copyright issues

• Less is more

• Some states call it a filed form and altering

it in any way is not allowed and/or illegal

• Send all pages to certificate holder

Certificates & Evidence of Insurance

�Send all to carrier – even if carrier

does not want (they have a delete key)

�New certificates no longer state

“endeavor”. Don’t use any that still

state “endeavor”. Outdated and don’t

have permission from Acord to use.

�Look at copyright issues page

Marshall Katz MS, CIC, LUTC, LIA, AAI 79

Certificates & Evidence of Insurance

• Consider agency font

• Consider printing so that they can not be

reproduced

• Claims frequency for E & O tends to be low but

severity tends to be high for these

• Use a fax or email system to get data for

certificate, verifies;

–Who requested it

–Who should be listed

–Appropriate contact data

Certificates & Evidence of Insurance

• Don’t misrepresent policies on certificate

• If asked for a 1 million auto limit on a

certificate and the insured has a 1 million CSL

on the auto, it is not necessary to show an

umbrella limit if the insured has one and it is

not requested.

• If asked for a 3 million auto limit and the

insured has an auto limit of 1 million and

umbrella limit of 5 million, the certificate must

show the full 5 million umbrella limit.

Marshall Katz MS, CIC, LUTC, LIA, AAI 80

New

WASHINGTON, D.C., Nov. 19, 2012 — The Independent Insurance Agents & Brokers of America (IIABA or the Big “I”) applauded the National Conference of Insurance Legislators (NCOIL) for adopting the “Certificates of Insurance Model Act” yesterday during NCOIL’s annual meeting in Point Clear, Ala.

Big “I” Applauds NCOIL’s Passage of Certificates of Insurance Model Act

Association has tirelessly worked to clarify and improve these important documents.

New on Certificates

“Many third parties exploit their marketplace leverage to demand the issuance of certificates that do not accurately reflect the underlying insurance policies, and the model is designed to eliminate such practices and ensure that certificates are utilized for their intended purpose.”

Marshall Katz MS, CIC, LUTC, LIA, AAI 81

New on CertificatesPerhaps most notably, the “Certificates of Insurance Model Act” prohibits a person from requesting the issuance of a certificate that has not been filed with insurance regulators or one that does not accurately reflect the underlying policy.This important element also enables insurance departments to issue cease and desist orders and assess fines against parties that request false or misleading certificates. Among other provisions, the model act also:

Get DOI to act on this!

New on Certificates• Prohibits a person from issuing a false or

misleading certificate or one that purports to alter, amend, or extend the coverage provided by the insurance policy,

• Prohibits the use of a certificate to warrant that a policy of insurance complies with the insurance or indemnification requirements of a contract, and

• Confirms that a certificate of insurance is not a policy and does not independently confer rights to its recipient.

Marshall Katz MS, CIC, LUTC, LIA, AAI 82

Acord Forms

• 75 - Binder for new business

• 27 - Evidence of Property Insurance (PL)

• 28 - Evidence of Commercial Property

– For association only

– E & O exposure if given to unit owner

• 24 – Certificate of Property Insurance

–For the unit owner or their mortgagee

• 25 – Certificate of Liability Insurance if mortgagee wants proof of liability coverage

File Documentation

Marshall Katz MS, CIC, LUTC, LIA, AAI 83

File Documentation

• Keep everything forever!!!!!!!

• Electronic imaging allows the documentation to be saved forever and later printed if needed

• Create an audit trail of what transpired

• Make appropriate back-up!!!

• One “system” for filing

• Data breach aware and controlled

• MA Recommended List

Risk Analysis and Exposure Identification

Marshall Katz MS, CIC, LUTC, LIA, AAI 84

Risk Analysis• Identify exposures(customer/agency)

• Analysis of frequency and severity

• Decide on risk management techniques

• Implement

• Monitor

http://vrc.iiaba.net/index1.asp

Marshall Katz MS, CIC, LUTC, LIA, AAI 85

Risk Management• Control

–Reduce – sprinklers, alarm, air bags

–Prevention – drivers ed., shovel, safety equipment

• Avoid – don’t do something

• Retain – don’t insure the exposure

• Transfer – insure, hold harmless

• Administer – get in motion

• Monitor

Marshall Katz MS, CIC, LUTC, LIA, AAI 86

Retain

Reduce

Transfer

Share

Avoid

Reduce

Retain

How often

How bad

Website/Social Media

• Who’s reviewing the content

• Someone relies on statements and we don’t even have a paying relationship with them

• How are people allowed to post on the blog

• Is there a waiver from the social media site

Marshall Katz MS, CIC, LUTC, LIA, AAI 87

ReviewWhat causes E & O pay-outs

• Placing inadequate coverage

• Renewing inadequate coverage

• Product changes not addressed

• Lack of account preparation

• Lack of follow-up

• Lack of signed documentation

• Inconsistent systems

• Time wasters (URA’s-Unwanted Repetitive Actions)

� Cancellation notice follow-up

� Cancel re-writes

� Quoting shoppers with no review

� Mortgage company issues

� Other areas that are not our responsibility

"The difficulties we experience

always illuminate the lessons we need most."

~ Author Unknown

1. How much you appreciate your other customers.

2. The holes in your business system that let them in.

3. How to improve your communication skills.

4. How to tighten up your systems to keep further headaches from occurring.

5. To be more selective with the customers you accept in the future.

6. Improve your conflict resolution skills.

7. How to improve the quality of what you do.

8. Improve your ability to say "no".

9. Who not to accept referrals from.

10. Be stronger in your beliefs of how you like to do business.

Marshall Katz MS, CIC, LUTC, LIA, AAI 88

“The better organized you are in the simple things, the more spontaneous and free you can be in the more important things.” ... Brian Tracy

Questions, comments and follow-up.

Keep for the future:

Marshall Katz MS, CIC, LUTC, LIA, AAI 89

Thank youfor being

heretoday!