Embed Size (px)

Citation preview

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

Indexed & Listed at: Ulrich's Periodicals Directory ©, ProQuest, U.S.A., EBSCO Publishing, U.S.A., Cabell’s Directories of Publishing Opportunities, U.S.A.

as well as inOpen J-Gage, India [link of the same is duly available at Inflibnet of University Grants Commission (U.G.C.)] Registered & Listed at: Index Copernicus Publishers Panel, Poland

Circulated all over the world & Google has verified that scholars of more than 1388 Cities in 138 countries/territories are visiting our journal on regular basis.

Ground Floor, Building No. 1041-C-1, Devi Bhawan Bazar, JAGADHRI – 135 003, Yamunanagar, Haryana, INDIA

www.ijrcm.org.in

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

ii

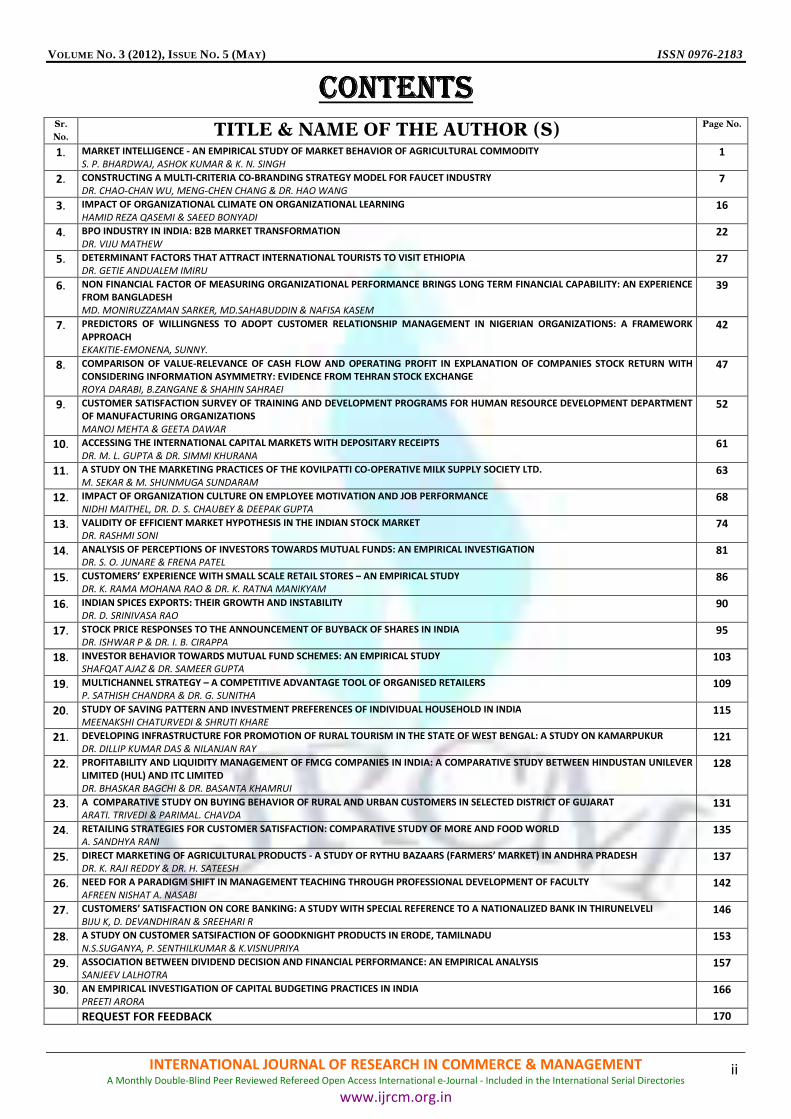

CONTENTSCONTENTSCONTENTSCONTENTS

Sr.

No. TITLE & NAME OF THE AUTHOR (S) Page No.

1. MARKET INTELLIGENCE - AN EMPIRICAL STUDY OF MARKET BEHAVIOR OF AGRICULTURAL COMMODITY

S. P. BHARDWAJ, ASHOK KUMAR & K. N. SINGH

1

2. CONSTRUCTING A MULTI-CRITERIA CO-BRANDING STRATEGY MODEL FOR FAUCET INDUSTRY

DR. CHAO-CHAN WU, MENG-CHEN CHANG & DR. HAO WANG

7

3. IMPACT OF ORGANIZATIONAL CLIMATE ON ORGANIZATIONAL LEARNING

HAMID REZA QASEMI & SAEED BONYADI

16

4. BPO INDUSTRY IN INDIA: B2B MARKET TRANSFORMATION

DR. VIJU MATHEW

22

5. DETERMINANT FACTORS THAT ATTRACT INTERNATIONAL TOURISTS TO VISIT ETHIOPIA

DR. GETIE ANDUALEM IMIRU

27

6. NON FINANCIAL FACTOR OF MEASURING ORGANIZATIONAL PERFORMANCE BRINGS LONG TERM FINANCIAL CAPABILITY: AN EXPERIENCE

FROM BANGLADESH

MD. MONIRUZZAMAN SARKER, MD.SAHABUDDIN & NAFISA KASEM

39

7. PREDICTORS OF WILLINGNESS TO ADOPT CUSTOMER RELATIONSHIP MANAGEMENT IN NIGERIAN ORGANIZATIONS: A FRAMEWORK

APPROACH

EKAKITIE-EMONENA, SUNNY.

42

8. COMPARISON OF VALUE-RELEVANCE OF CASH FLOW AND OPERATING PROFIT IN EXPLANATION OF COMPANIES STOCK RETURN WITH

CONSIDERING INFORMATION ASYMMETRY: EVIDENCE FROM TEHRAN STOCK EXCHANGE

ROYA DARABI, B.ZANGANE & SHAHIN SAHRAEI

47

9. CUSTOMER SATISFACTION SURVEY OF TRAINING AND DEVELOPMENT PROGRAMS FOR HUMAN RESOURCE DEVELOPMENT DEPARTMENT

OF MANUFACTURING ORGANIZATIONS

MANOJ MEHTA & GEETA DAWAR

52

10. ACCESSING THE INTERNATIONAL CAPITAL MARKETS WITH DEPOSITARY RECEIPTS

DR. M. L. GUPTA & DR. SIMMI KHURANA

61

11. A STUDY ON THE MARKETING PRACTICES OF THE KOVILPATTI CO-OPERATIVE MILK SUPPLY SOCIETY LTD.

M. SEKAR & M. SHUNMUGA SUNDARAM

63

12. IMPACT OF ORGANIZATION CULTURE ON EMPLOYEE MOTIVATION AND JOB PERFORMANCE

NIDHI MAITHEL, DR. D. S. CHAUBEY & DEEPAK GUPTA

68

13. VALIDITY OF EFFICIENT MARKET HYPOTHESIS IN THE INDIAN STOCK MARKET

DR. RASHMI SONI

74

14. ANALYSIS OF PERCEPTIONS OF INVESTORS TOWARDS MUTUAL FUNDS: AN EMPIRICAL INVESTIGATION

DR. S. O. JUNARE & FRENA PATEL 81

15. CUSTOMERS’ EXPERIENCE WITH SMALL SCALE RETAIL STORES – AN EMPIRICAL STUDY

DR. K. RAMA MOHANA RAO & DR. K. RATNA MANIKYAM

86

16. INDIAN SPICES EXPORTS: THEIR GROWTH AND INSTABILITY

DR. D. SRINIVASA RAO

90

17. STOCK PRICE RESPONSES TO THE ANNOUNCEMENT OF BUYBACK OF SHARES IN INDIA

DR. ISHWAR P & DR. I. B. CIRAPPA

95

18. INVESTOR BEHAVIOR TOWARDS MUTUAL FUND SCHEMES: AN EMPIRICAL STUDY

SHAFQAT AJAZ & DR. SAMEER GUPTA

103

19. MULTICHANNEL STRATEGY – A COMPETITIVE ADVANTAGE TOOL OF ORGANISED RETAILERS

P. SATHISH CHANDRA & DR. G. SUNITHA

109

20. STUDY OF SAVING PATTERN AND INVESTMENT PREFERENCES OF INDIVIDUAL HOUSEHOLD IN INDIA

MEENAKSHI CHATURVEDI & SHRUTI KHARE

115

21. DEVELOPING INFRASTRUCTURE FOR PROMOTION OF RURAL TOURISM IN THE STATE OF WEST BENGAL: A STUDY ON KAMARPUKUR

DR. DILLIP KUMAR DAS & NILANJAN RAY

121

22. PROFITABILITY AND LIQUIDITY MANAGEMENT OF FMCG COMPANIES IN INDIA: A COMPARATIVE STUDY BETWEEN HINDUSTAN UNILEVER

LIMITED (HUL) AND ITC LIMITED

DR. BHASKAR BAGCHI & DR. BASANTA KHAMRUI

128

23. A COMPARATIVE STUDY ON BUYING BEHAVIOR OF RURAL AND URBAN CUSTOMERS IN SELECTED DISTRICT OF GUJARAT

ARATI. TRIVEDI & PARIMAL. CHAVDA

131

24. RETAILING STRATEGIES FOR CUSTOMER SATISFACTION: COMPARATIVE STUDY OF MORE AND FOOD WORLD

A. SANDHYA RANI 135

25. DIRECT MARKETING OF AGRICULTURAL PRODUCTS - A STUDY OF RYTHU BAZAARS (FARMERS’ MARKET) IN ANDHRA PRADESH

DR. K. RAJI REDDY & DR. H. SATEESH

137

26. NEED FOR A PARADIGM SHIFT IN MANAGEMENT TEACHING THROUGH PROFESSIONAL DEVELOPMENT OF FACULTY

AFREEN NISHAT A. NASABI 142

27. CUSTOMERS’ SATISFACTION ON CORE BANKING: A STUDY WITH SPECIAL REFERENCE TO A NATIONALIZED BANK IN THIRUNELVELI

BIJU K, D. DEVANDHIRAN & SREEHARI R 146

28. A STUDY ON CUSTOMER SATSIFACTION OF GOODKNIGHT PRODUCTS IN ERODE, TAMILNADU

N.S.SUGANYA, P. SENTHILKUMAR & K.VISNUPRIYA 153

29. ASSOCIATION BETWEEN DIVIDEND DECISION AND FINANCIAL PERFORMANCE: AN EMPIRICAL ANALYSIS

SANJEEV LALHOTRA 157

30. AN EMPIRICAL INVESTIGATION OF CAPITAL BUDGETING PRACTICES IN INDIA

PREETI ARORA 166

REQUEST FOR FEEDBACK 170

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

iii

CHIEF PATRONCHIEF PATRONCHIEF PATRONCHIEF PATRON PROF. K. K. AGGARWAL

Chancellor, Lingaya’s University, Delhi

Founder Vice-Chancellor, GuruGobindSinghIndraprasthaUniversity, Delhi

Ex. Pro Vice-Chancellor, GuruJambheshwarUniversity, Hisar

PATRONPATRONPATRONPATRON SH. RAM BHAJAN AGGARWAL

Ex.State Minister for Home & Tourism, Government of Haryana

Vice-President, Dadri Education Society, Charkhi Dadri

President, Chinar Syntex Ltd. (Textile Mills), Bhiwani

COCOCOCO----ORDINATORORDINATORORDINATORORDINATOR DR. SAMBHAV GARG

Faculty, M. M. Institute of Management, MaharishiMarkandeshwarUniversity, Mullana, Ambala, Haryana

ADVISORSADVISORSADVISORSADVISORS DR. PRIYA RANJAN TRIVEDI

Chancellor, The Global Open University, Nagaland

PROF. M. S. SENAM RAJU Director A. C. D., School of Management Studies, I.G.N.O.U., New Delhi

PROF. M. N. SHARMA Chairman, M.B.A., HaryanaCollege of Technology & Management, Kaithal

PROF. S. L. MAHANDRU Principal (Retd.), MaharajaAgrasenCollege, Jagadhri

EDITOREDITOREDITOREDITOR PROF. R. K. SHARMA

Professor, Bharti Vidyapeeth University Institute of Management & Research, New Delhi

COCOCOCO----EDITOREDITOREDITOREDITOR DR. BHAVET

Faculty, M. M. Institute of Management, MaharishiMarkandeshwarUniversity, Mullana, Ambala, Haryana

EDITORIAL ADVISORY BOARDEDITORIAL ADVISORY BOARDEDITORIAL ADVISORY BOARDEDITORIAL ADVISORY BOARD DR. RAJESH MODI

Faculty, YanbuIndustrialCollege, Kingdom of Saudi Arabia

PROF. SANJIV MITTAL UniversitySchool of Management Studies, GuruGobindSinghI. P. University, Delhi

PROF. ANIL K. SAINI Chairperson (CRC), GuruGobindSinghI. P. University, Delhi

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

iv

DR. SAMBHAVNA Faculty, I.I.T.M., Delhi

DR. MOHENDER KUMAR GUPTA Associate Professor, P.J.L.N.GovernmentCollege, Faridabad

DR. SHIVAKUMAR DEENE Asst. Professor, Dept. of Commerce, School of Business Studies, Central University of Karnataka, Gulbarga

MOHITA Faculty, Yamuna Institute of Engineering & Technology, Village Gadholi, P. O. Gadhola, Yamunanagar

ASSOCIATE ASSOCIATE ASSOCIATE ASSOCIATE EDITORSEDITORSEDITORSEDITORS PROF. NAWAB ALI KHAN

Department of Commerce, Aligarh Muslim University, Aligarh, U.P.

PROF. ABHAY BANSAL Head, Department of Information Technology, Amity School of Engineering & Technology, Amity

University, Noida

PROF. V. SELVAM SSL, VIT University, Vellore

DR. N. SUNDARAM Professor, VITUniversity, Vellore

DR. PARDEEP AHLAWAT Reader, Institute of Management Studies & Research, MaharshiDayanandUniversity, Rohtak

S. TABASSUM SULTANA Associate Professor, Department of Business Management, Matrusri Institute of P.G. Studies, Hyderabad

TECHNICAL ADVISORTECHNICAL ADVISORTECHNICAL ADVISORTECHNICAL ADVISOR AMITA

Faculty, Government M. S., Mohali

MOHITA Faculty, Yamuna Institute of Engineering & Technology, Village Gadholi, P. O. Gadhola, Yamunanagar

FINANCIAL ADVISORSFINANCIAL ADVISORSFINANCIAL ADVISORSFINANCIAL ADVISORS DICKIN GOYAL

Advocate & Tax Adviser, Panchkula

NEENA Investment Consultant, Chambaghat, Solan, Himachal Pradesh

LEGAL ADVISORSLEGAL ADVISORSLEGAL ADVISORSLEGAL ADVISORS JITENDER S. CHAHAL

Advocate, Punjab & Haryana High Court, Chandigarh U.T.

CHANDER BHUSHAN SHARMA Advocate & Consultant, District Courts, Yamunanagar at Jagadhri

SUPERINTENDENTSUPERINTENDENTSUPERINTENDENTSUPERINTENDENT SURENDER KUMAR POONIA

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

v

CALL FOR MANUSCRIPTSCALL FOR MANUSCRIPTSCALL FOR MANUSCRIPTSCALL FOR MANUSCRIPTS Weinvite unpublished novel, original, empirical and high quality research work pertaining to recent developments & practices in the area of

Computer, Business, Finance, Marketing, Human Resource Management, General Management, Banking, Insurance, Corporate Governance

and emerging paradigms in allied subjects like Accounting Education; Accounting Information Systems; Accounting Theory & Practice; Auditing;

Behavioral Accounting; Behavioral Economics; Corporate Finance; Cost Accounting; Econometrics; Economic Development; Economic History;

Financial Institutions & Markets; Financial Services; Fiscal Policy; Government & Non Profit Accounting; Industrial Organization; International

Economics & Trade; International Finance; Macro Economics; Micro Economics; Monetary Policy; Portfolio & Security Analysis; Public Policy

Economics; Real Estate; Regional Economics; Tax Accounting; Advertising & Promotion Management; Business Education; Management

Information Systems (MIS); Business Law, Public Responsibility & Ethics; Communication; Direct Marketing; E-Commerce; Global Business;

Health Care Administration; Labor Relations & Human Resource Management; Marketing Research; Marketing Theory & Applications; Non-

Profit Organizations; Office Administration/Management; Operations Research/Statistics; Organizational Behavior & Theory; Organizational

Development; Production/Operations; Public Administration; Purchasing/Materials Management; Retailing; Sales/Selling; Services; Small

Business Entrepreneurship; Strategic Management Policy; Technology/Innovation; Tourism, Hospitality & Leisure; Transportation/Physical

Distribution; Algorithms; Artificial Intelligence; Compilers & Translation; Computer Aided Design (CAD); Computer Aided Manufacturing;

Computer Graphics; Computer Organization & Architecture; Database Structures & Systems; Digital Logic; Discrete Structures; Internet;

Management Information Systems; Modeling & Simulation; Multimedia; Neural Systems/Neural Networks; Numerical Analysis/Scientific

Computing; Object Oriented Programming; Operating Systems; Programming Languages; Robotics; Symbolic & Formal Logic and Web Design.

The above mentioned tracks are only indicative, and not exhaustive.

Anybody can submit the soft copy of his/her manuscript anytime in M.S. Word format after preparing the same as per our submission

guidelines duly available on our website under the heading guidelines for submission, at the email addresses:

[email protected]@ijrcm.org.in.

GUIDELINES FOR SUBMISSION OF MANUSCRIPTGUIDELINES FOR SUBMISSION OF MANUSCRIPTGUIDELINES FOR SUBMISSION OF MANUSCRIPTGUIDELINES FOR SUBMISSION OF MANUSCRIPT

1. COVERING LETTER FOR SUBMISSION:

DATED: _____________

THE EDITOR

IJRCM

Subject: SUBMISSION OF MANUSCRIPT IN THE AREA OF .

(e.g. Finance/Marketing/HRM/General Management/Economics/Psychology/Law/Computer/IT/Engineering/Mathematics/other, please specify)

DEAR SIR/MADAM

Please find my submission of manuscript entitled ‘___________________________________________’ for possible publication in your journals.

I hereby affirm that the contents of this manuscript are original. Furthermore, it has neither been published elsewhere in any language fully or partly, nor is it

under review for publication elsewhere.

I affirm that all the author (s) have seen and agreed to the submitted version of the manuscript and their inclusion of name (s) as co-author (s).

Also, if my/our manuscript is accepted, I/We agree to comply with the formalities as given on the website of the journal & you are free to publish our

contribution in any of your journals.

NAME OF CORRESPONDING AUTHOR:

Designation:

Affiliation with full address, contact numbers & Pin Code:

Residential address with Pin Code:

Mobile Number (s):

Landline Number (s):

E-mail Address:

Alternate E-mail Address:

NOTES:

a) The whole manuscript is required to be in ONE MS WORD FILE only (pdf. version is liable to be rejected without any consideration), which will start from

the covering letter, inside the manuscript.

b) The sender is required to mention the following in the SUBJECT COLUMN of the mail:

New Manuscript for Review in the area of (Finance/Marketing/HRM/General Management/Economics/Psychology/Law/Computer/IT/ Engineering/Mathematics/other, please specify)

c) There is no need to give any text in the body of mail, except the cases where the author wishes to give any specific message w.r.t. to the manuscript. d) The total size of the file containing the manuscript is required to be below 500 KB.

e) Abstract alone will not be considered for review, and the author is required to submit the complete manuscript in the first instance.

f) The journal gives acknowledgement w.r.t. the receipt of every email and in case of non-receipt of acknowledgment from the journal, w.r.t. the submission

of manuscript, within two days of submission, the corresponding author is required to demand for the same by sending separate mail to the journal.

2. MANUSCRIPT TITLE: The title of the paper should be in a 12 point Calibri Font. It should be bold typed, centered and fully capitalised.

3. AUTHOR NAME (S) & AFFILIATIONS: The author (s) full name, designation, affiliation (s), address, mobile/landline numbers, and email/alternate email

address should be in italic & 11-point Calibri Font. It must be centered underneath the title.

4. ABSTRACT: Abstract should be in fully italicized text, not exceeding 250 words. The abstract must be informative and explain the background, aims, methods,

results & conclusion in a single para. Abbreviations must be mentioned in full.

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

vi

5. KEYWORDS: Abstract must be followed by a list of keywords, subject to the maximum of five. These should be arranged in alphabetic order separated by

commas and full stops at the end.

6. MANUSCRIPT: Manuscript must be in BRITISH ENGLISH prepared on a standard A4 size PORTRAIT SETTING PAPER. It must be prepared on a single space and

single column with 1” margin set for top, bottom, left and right. It should be typed in 8 point Calibri Font with page numbers at the bottom and centre of every

page. It should be free from grammatical, spelling and punctuation errors and must be thoroughly edited.

7. HEADINGS: All the headings should be in a 10 point Calibri Font. These must be bold-faced, aligned left and fully capitalised. Leave a blank line before each

heading.

8. SUB-HEADINGS: All the sub-headings should be in a 8 point Calibri Font. These must be bold-faced, aligned left and fully capitalised.

9. MAIN TEXT: The main text should follow the following sequence:

INTRODUCTION

REVIEW OF LITERATURE

NEED/IMPORTANCE OF THE STUDY

STATEMENT OF THE PROBLEM

OBJECTIVES

HYPOTHESES

RESEARCH METHODOLOGY

RESULTS & DISCUSSION

FINDINGS

RECOMMENDATIONS/SUGGESTIONS

CONCLUSIONS

SCOPE FOR FURTHER RESEARCH

ACKNOWLEDGMENTS

REFERENCES

APPENDIX/ANNEXURE

It should be in a 8 point Calibri Font, single spaced and justified. The manuscript should preferably not exceed 5000 WORDS.

10. FIGURES &TABLES: These should be simple, crystal clear, centered, separately numbered &self explained, and titles must be above the table/figure. Sources of

data should be mentioned below the table/figure. It should be ensured that the tables/figures are referred to from the main text.

11. EQUATIONS:These should be consecutively numbered in parentheses, horizontally centered with equation number placed at the right.

12. REFERENCES: The list of all references should be alphabetically arranged. The author (s) should mention only the actually utilised references in the preparation

of manuscript and they are supposed to follow Harvard Style of Referencing. The author (s) are supposed to follow the references as per the following:

• All works cited in the text (including sources for tables and figures) should be listed alphabetically.

• Use (ed.) for one editor, and (ed.s) for multiple editors.

• When listing two or more works by one author, use --- (20xx), such as after Kohl (1997), use --- (2001), etc, in chronologically ascending order.

• Indicate (opening and closing) page numbers for articles in journals and for chapters in books.

• The title of books and journals should be in italics. Double quotation marks are used for titles of journal articles, book chapters, dissertations, reports, working

papers, unpublished material, etc.

• For titles in a language other than English, provide an English translation in parentheses.

• The location of endnotes within the text should be indicated by superscript numbers.

PLEASE USE THE FOLLOWING FOR STYLE AND PUNCTUATION IN REFERENCES:

BOOKS

• Bowersox, Donald J., Closs, David J., (1996), "Logistical Management." Tata McGraw, Hill, New Delhi.

• Hunker, H.L. and A.J. Wright (1963), "Factors of Industrial Location in Ohio" Ohio State University, Nigeria.

CONTRIBUTIONS TO BOOKS

• Sharma T., Kwatra, G. (2008) Effectiveness of Social Advertising: A Study of Selected Campaigns, Corporate Social Responsibility, Edited by David Crowther &

Nicholas Capaldi, Ashgate Research Companion to Corporate Social Responsibility, Chapter 15, pp 287-303.

JOURNAL AND OTHER ARTICLES

• Schemenner, R.W., Huber, J.C. and Cook, R.L. (1987), "Geographic Differences and the Location of New Manufacturing Facilities," Journal of Urban Economics,

Vol. 21, No. 1, pp. 83-104.

CONFERENCE PAPERS

• Garg, Sambhav (2011): "Business Ethics" Paper presented at the Annual International Conference for the All India Management Association, New Delhi, India,

19–22 June.

UNPUBLISHED DISSERTATIONS AND THESES

• Kumar S. (2011): "Customer Value: A Comparative Study of Rural and Urban Customers," Thesis, Kurukshetra University, Kurukshetra.

ONLINE RESOURCES

• Always indicate the date that the source was accessed, as online resources are frequently updated or removed.

WEBSITE

Garg, Bhavet (2011): Towards a New Natural Gas Policy, Political Weekly, Viewed on January 01, 2012 http://epw.in/user/viewabstract.jsp

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

39

NON FINANCIAL FACTOR OF MEASURING ORGANIZATIONAL PERFORMANCE BRINGS LONG TERM

FINANCIAL CAPABILITY: AN EXPERIENCE FROM BANGLADESH

MD. MONIRUZZAMAN SARKER

SR. LECTURER

SCHOOL OF BUISNESS & ECONOMICS

UNITED INTERNATIONAL UNIVERSITY

DHAKA, BANGLADESH

MD.SAHABUDDIN

RESEARCH OFFICER

THE FEDERATION OF BANGLADESH CHAMBERS OF COMMERCE AND INDUSTRY (FBCCI)

DHAKA, BANGLADESH

NAFISA KASEM

LECTURER

FACULTY OF BUSINESS ADMINISTRATION

UNIVERSITY OF DEVELOPMENT ALTERNATIVE

DHAKA, BANGLADESH

ABSTRACT This paper deals with the measurement of organizational performance (MOP) and tries to highlight that Non-Financial factor of measuring organizational

performance brings long term financial capability. An endeavor has been made to present the problems associated with the financial indicators of performance

and how Non-Financial Indicators (NFI) help in decision making. Both importance of NFIs in Bangladeshi context and consequences of ignorance NFIs have been

discussed to find out the evidence of Non-Financial factors impact. Finally, this paper suggests that using the NFIs which linked to factors such as corporate

strategy, value drivers, organizational objectives and the competitive environment.

KEYWORDS Measurement of Organizational Performance (MOP); Non Financial Indicators (NFIs); Organizational Performance (OP).

INTRODUCTION easuring of organizational performance is an important factor for the organization itself and the stakeholders of the organization. It is not always an

easy job to do. Measurement of OP is always linked with organizational missions, goals and objectives. Choosing performance measure is a challenge.

Performance measurement systems play a key role in developing strategy, evaluating the achievement of organizational objectives and compensating

managers. Yet many managers feel traditional financially oriented systems no longer work adequately.

From A recent survey of U.S. financial services, companies found that most of the companies were not satisfied with their measurement systems that have been

used right now. They believed that there were too much emphasis on financial measures such as earnings and accounting returns and little emphasis given on

drivers of value such as customer and employee satisfaction, innovation and quality.

In response to that, companies are now implementing new performance measurement systems. For example, A third of the financial services companies, made

a major change in their performance measurement system during the past two years and 39% of the companies, plan a major change within two years.

As a result of the Inadequacies in financial performance measures, innovations ranging from non-financial indicators of "intangible assets" and "intellectual

capital" to "balanced scorecards" of integrated financial and non-financial measures had made. This article discusses the advantages of non-financial

performance measures and offers suggestions for implementation.

OBJECTIVES AND METHODOLOGY OF THE STUDY As the competition among the competitors has been increased, this Competition forces every organization to increase their performance and profit but

somehow it is not possible to achieve both of these objectives due to the misconception of organizational performance. In most of the cases, organization

emphasizes on financial record as an indicator of performance, As financial record is the final outcome of any performance which cannot be modified within

current year so new indicator must be needed. So, here we have tried to emphasis on Non-Financial indicator to measure organizational performance so that

organization can learn lessons and take act in the current year to achieve financial success. To establish this concept, we have collected secondary information

from the various different kinds of published journals, articles, and books related with the analysis. This study is exploratory in nature and based on secondary

information. For the reliability of this study, we have given emphasis on the practical knowledge and expert opinions about the organizational performance.

PROBLEMS ASSOCIATED WITH THE FINANCIAL INDICATORS OF PERFORMANCE By tradition, firm often uses financial indicators of performance to measure the success of the organization. Researcher Kaplan (1983) has identified three main

probable consequences for the high-tech diversified manufacturing industries that are still practicing traditional cost based reporting system. These are:

USE-TYPE: Traditional cost reports use of arbitrary cost allocation schemes and there is no link between products, different processes or indirect cost that they

create. Therefore, without reliable picture of what different processes really cost, management is unable to see the connection between decisions and their

effects on the cost.

RELEVANCE-TYPE: The system fails to develop quality control that ensures customer satisfaction and factor productivity measure or fails to highlight opportunity

costs. Further it also fails to provide answers to the manager for some basic questions like- what takes up the time of production planning staff, the right amount

of resources is in the place etc.

CONTROL-TYPE: The traditional cost report also fails to consider the Non-Financial factors that need to measure the efficiency of customer’s service. Therefore,

this system subsidize low-volume, customized product, at the cost of high volume standard products in manufacturing industry (O’Guin 1991). So, the system

under-cost is the complex products and consequently creates a control- type problem for the firm. Many researchers have found that there is an impact of Non-

Financial Indicators (NFIs) on the decision making process in achieving the organizational target (Smith, 1994; Green-Singleton 1993).

M

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY)

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENTA Monthly Double-Blind Peer Reviewed Refereed Open Access International e

NON-FINANCIAL INDICATORS IN DECISION MAKINGNowadays In the area of operation management, Non

manufacturing firms. In the strategy of new control measure, NFIs can help a firm to maintain consistency with goals and obje

internal and external factors that are required to achieve the firm’s target (Ber

three types of failures such as, Use-types, relevance-type, and control

decision of value, facilitated evaluation and control measure of a firm (Smith 1994).Most significant reasons for the use of NFIs are that i

innovation, Quality, satisfying customer and production efficiency (Singleton,G.B,19993).

Now-a-days, it is not just an issue of financial justification for the firm

efficiency and growth in comparing with competitors. Therefore, the firm should be willing to invest capital

on the operational efficiency of the firm. Chalos (1992) identifies various NFIs to measure the operation control, which is s

FIGURE 1: NON

Source: Chalos I (1992), Managing cost in manufacturing. Prentice Hall, New York.

The above point understands a company's value drives, the factors that create stakeholder value. Once known, these factors de

contribution to long-term success and so how to translate corporate objectives into measures that guide managers' actions

one of the Important Factors largely influences the success of the organization and the following costs such

PREVENTION COSTS: The costs of all activities specifically designed to prevent poor quality from products or services. Examples are the costs o

review, quality planning, supplier capability surveys, process capability evaluations, quality

education and training.

APPRAISAL COSTS: Appraisal costs are the costs associated with measuring, evaluating or auditing products or services to assure conformance to

standards and performance requirements. These include the costs of incoming and source inspection/test of purchased material, in

inspection/test, product, process or service audits, and calibration of measuring and test equipment, associated supplies a

FAILURE COSTS: The costs resulting from products or services are not conforming to requirements or customer/user needs. Failure costs are di

internal and external failure categories. Internal Failure Costs:

to the customer. Examples are the costs of scrap, rework, re

after delivery or shipment of the product — and during or after the furnishing of a service

complaints, customer returns, warranty claims, product recalls.

The above all costs can be controlled and managed during the operational year of any firm and firm can build a strong interna

financial gain at the end.

IMPORTANCE OF NFIS IN BANGLADESHI CONTEXTIf we try to solve the following questions, all answers will emphasis on NFIs.

a) Why do the government firms turn into private firm?

b) Why do the government firms face huge financial loss every year?

c) Why are the performances of government firm becoming weaker day by day?

d) Why are the private firms gaining huge financial benefits?

The main reasons behind the poor performance of government are that they don’t emphasis the Non

Satisfaction, Time Management, Inventory, and Product De

2. Studies show that here in Bangladesh, most of the firms particularly in manufacturing want to gain financial benefit immed

force them to emphasis financial measurement. Because of too much emphasis on financial measure, it forces the organizations

which lead them to accept loss at the end of the competitive market. Noapara (Jessore, Bangladesh)

around 15 cement factories established a decade ago in a full swing but after a few years only 5 of them are survived. Most o

to make immediate profits force them to increase their production without considering standard quality and the ultimate effect is very logical that they are

bound to shut down all factory due to lack of market confidence.

Raw Material

Scrap

Cost

Quality

Inventory

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENTBlind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

FINANCIAL INDICATORS IN DECISION MAKING Nowadays In the area of operation management, Non-Financial indicators (NFIs) are receiving recognition among the practitioners

manufacturing firms. In the strategy of new control measure, NFIs can help a firm to maintain consistency with goals and obje

internal and external factors that are required to achieve the firm’s target (Berlin and Brimson, 1988). It was found that the negative consequences of the above

type, and control-type could be overcome by the use of NFIs.Thus it has been argued that NFIs improve the

ue, facilitated evaluation and control measure of a firm (Smith 1994).Most significant reasons for the use of NFIs are that i

innovation, Quality, satisfying customer and production efficiency (Singleton,G.B,19993).

s not just an issue of financial justification for the firm-owners. It is also an issue of increasing firm’s image, market share, customer loyalty,

efficiency and growth in comparing with competitors. Therefore, the firm should be willing to invest capital to meet customer’s expectations that largely depend

on the operational efficiency of the firm. Chalos (1992) identifies various NFIs to measure the operation control, which is s

FIGURE 1: NON-FINANCIAL PERFORMANCE MEASUREMENT

Source: Chalos I (1992), Managing cost in manufacturing. Prentice Hall, New York.

The above point understands a company's value drives, the factors that create stakeholder value. Once known, these factors de

term success and so how to translate corporate objectives into measures that guide managers' actions

one of the Important Factors largely influences the success of the organization and the following costs such as:

The costs of all activities specifically designed to prevent poor quality from products or services. Examples are the costs o

review, quality planning, supplier capability surveys, process capability evaluations, quality improvement, team meetings, quality improvement projects, quality

Appraisal costs are the costs associated with measuring, evaluating or auditing products or services to assure conformance to

performance requirements. These include the costs of incoming and source inspection/test of purchased material, in

inspection/test, product, process or service audits, and calibration of measuring and test equipment, associated supplies a

The costs resulting from products or services are not conforming to requirements or customer/user needs. Failure costs are di

Internal Failure Costs: Failure costs occurring prior to delivery or shipment of the product, or the furnishing of a service,

to the customer. Examples are the costs of scrap, rework, re-inspection, re-testing, material review, downgrading, External Failure Costs:

and during or after the furnishing of a service — to the customer. Examples are the costs of processing, customer

complaints, customer returns, warranty claims, product recalls.

The above all costs can be controlled and managed during the operational year of any firm and firm can build a strong interna

IMPORTANCE OF NFIS IN BANGLADESHI CONTEXT following questions, all answers will emphasis on NFIs.

Why do the government firms turn into private firm?

Why do the government firms face huge financial loss every year?

Why are the performances of government firm becoming weaker day by day?

private firms gaining huge financial benefits?

The main reasons behind the poor performance of government are that they don’t emphasis the Non-Financial factor like

Satisfaction, Time Management, Inventory, and Product Development. Here a model of ultimate effects of ignorance of NFIs are tried to show below in figure

2. Studies show that here in Bangladesh, most of the firms particularly in manufacturing want to gain financial benefit immed

force them to emphasis financial measurement. Because of too much emphasis on financial measure, it forces the organizations

which lead them to accept loss at the end of the competitive market. Noapara (Jessore, Bangladesh) Industrial area can be one of the best examples where

around 15 cement factories established a decade ago in a full swing but after a few years only 5 of them are survived. Most o

increase their production without considering standard quality and the ultimate effect is very logical that they are

bound to shut down all factory due to lack of market confidence.

Operation Control

Inventory

Turns

Space

Quality

Quality

Defects

Rework

Product

Diversity

Volume

Overhead

Time

Switch over

Cycle

Downtime

Scheduling

Utilization

ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT Included in the International Serial Directories

40

Financial indicators (NFIs) are receiving recognition among the practitioners of the diversified

manufacturing firms. In the strategy of new control measure, NFIs can help a firm to maintain consistency with goals and objectives and measurement of both

lin and Brimson, 1988). It was found that the negative consequences of the above

type could be overcome by the use of NFIs.Thus it has been argued that NFIs improve the

ue, facilitated evaluation and control measure of a firm (Smith 1994).Most significant reasons for the use of NFIs are that it deals with causes like

owners. It is also an issue of increasing firm’s image, market share, customer loyalty,

to meet customer’s expectations that largely depend

on the operational efficiency of the firm. Chalos (1992) identifies various NFIs to measure the operation control, which is shown below figure:

The above point understands a company's value drives, the factors that create stakeholder value. Once known, these factors determine which measures

term success and so how to translate corporate objectives into measures that guide managers' actions. As a matter of fact, Quality cost is

The costs of all activities specifically designed to prevent poor quality from products or services. Examples are the costs of new product

improvement, team meetings, quality improvement projects, quality

Appraisal costs are the costs associated with measuring, evaluating or auditing products or services to assure conformance to quality

performance requirements. These include the costs of incoming and source inspection/test of purchased material, in-process and final

inspection/test, product, process or service audits, and calibration of measuring and test equipment, associated supplies and materials

The costs resulting from products or services are not conforming to requirements or customer/user needs. Failure costs are divided into

ior to delivery or shipment of the product, or the furnishing of a service,

External Failure Costs: Failure costs occurring

to the customer. Examples are the costs of processing, customer

The above all costs can be controlled and managed during the operational year of any firm and firm can build a strong internal position which will lead them to

Financial factor like Total Quality Management Customer

. Here a model of ultimate effects of ignorance of NFIs are tried to show below in figure -

2. Studies show that here in Bangladesh, most of the firms particularly in manufacturing want to gain financial benefit immediately after investments which

force them to emphasis financial measurement. Because of too much emphasis on financial measure, it forces the organizations to ignore Non-Financial factors

Industrial area can be one of the best examples where

around 15 cement factories established a decade ago in a full swing but after a few years only 5 of them are survived. Most of the firms take loan from bank and

increase their production without considering standard quality and the ultimate effect is very logical that they are

Time

Switch over

Cycle

Downtime

Scheduling

Utilization

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY)

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENTA Monthly Double-Blind Peer Reviewed Refereed Open Access International e

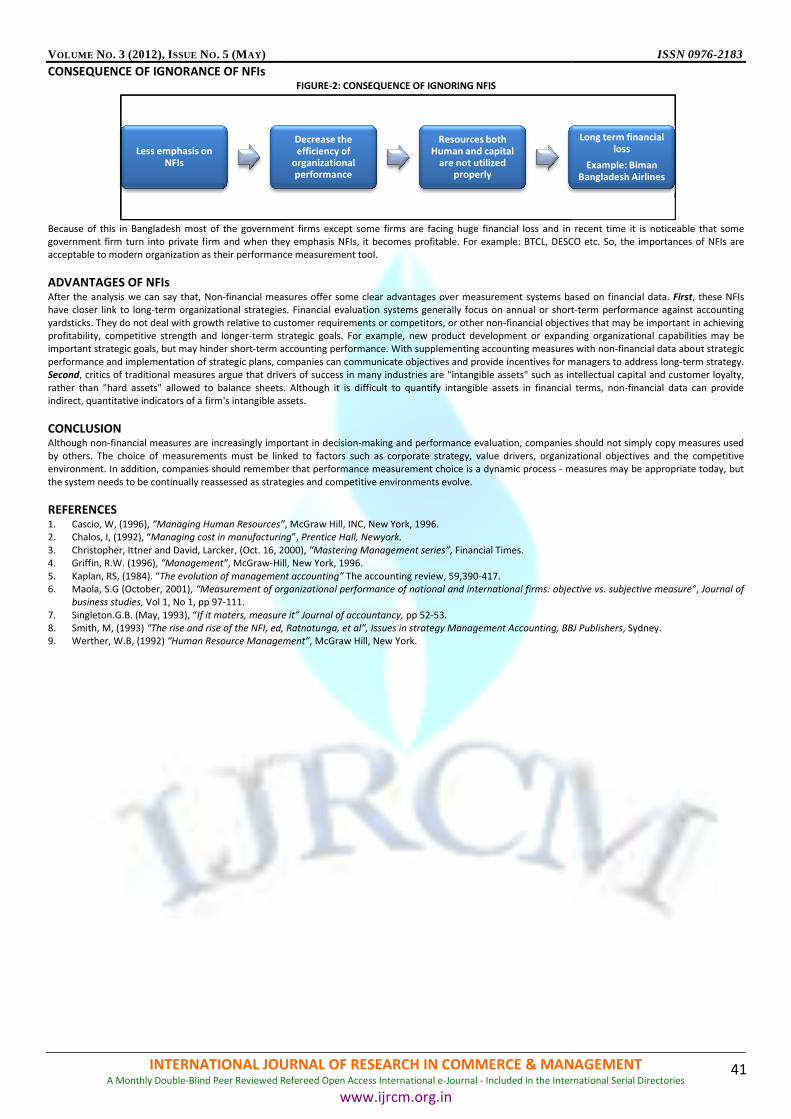

CONSEQUENCE OF IGNORANCE OF NFIs

Because of this in Bangladesh most of the government firms except some firms are facing huge financial loss and in recent tim

government firm turn into private firm and when they emphasis NFIs, it becomes profitable. For example

acceptable to modern organization as their performance measurement tool.

ADVANTAGES OF NFIs After the analysis we can say that, Non-financial measures offer some clear advantages over measurement systems based on financial data.

have closer link to long-term organizational strategies. Financial evaluation systems generally focus

yardsticks. They do not deal with growth relative to customer requirements or competitors, or other non

profitability, competitive strength and longer-term strategic goals. For example, new product development or expanding organizational capabilities may be

important strategic goals, but may hinder short-term accounting performance. With supplementing accounting measures with non

performance and implementation of strategic plans, companies can communicate objectives and provide incentives for managers t

Second, critics of traditional measures argue that drivers of success in many industrie

rather than "hard assets" allowed to balance sheets. Although it is difficult to quantify intangible assets in financial term

indirect, quantitative indicators of a firm's intangible assets.

CONCLUSION Although non-financial measures are increasingly important in decision

by others. The choice of measurements must be linked to factors such as corporate strategy, value drivers, organizational objectives and the competitive

environment. In addition, companies should remember that performance measurement choice is a dynamic process

the system needs to be continually reassessed as strategies and competitive environments evolve.

REFERENCES 1. Cascio, W, (1996), “Managing Human Resources”, McGraw Hill, INC, New York, 1996.

2. Chalos, I, (1992), “Managing cost in manufacturing

3. Christopher, Ittner and David, Larcker, (Oct. 16, 2000),

4. Griffin, R.W. (1996), “Management”, McGraw-Hill, New York, 1996.

5. Kaplan, RS, (1984). “The evolution of management accounting”

6. Maola, S.G (October, 2001), “Measurement of organizational performance of national and int

business studies, Vol 1, No 1, pp 97-111.

7. Singleton.G.B. (May, 1993), “If it maters, measure it” Journal of accountancy,

8. Smith, M, (1993) “The rise and rise of the NFI, ed, Ratnatu

9. Werther, W.B, (1992) “Human Resource Management”

Less emphasis on NFIs

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENTBlind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

FIGURE-2: CONSEQUENCE OF IGNORING NFIS

Because of this in Bangladesh most of the government firms except some firms are facing huge financial loss and in recent tim

government firm turn into private firm and when they emphasis NFIs, it becomes profitable. For example: BTCL, DESCO etc. So, the importances of NFIs are

acceptable to modern organization as their performance measurement tool.

financial measures offer some clear advantages over measurement systems based on financial data.

term organizational strategies. Financial evaluation systems generally focus on annual or short

yardsticks. They do not deal with growth relative to customer requirements or competitors, or other non-financial objectives that may be important in achieving

term strategic goals. For example, new product development or expanding organizational capabilities may be

term accounting performance. With supplementing accounting measures with non

performance and implementation of strategic plans, companies can communicate objectives and provide incentives for managers t

, critics of traditional measures argue that drivers of success in many industries are "intangible assets" such as intellectual capital and customer loyalty,

rather than "hard assets" allowed to balance sheets. Although it is difficult to quantify intangible assets in financial term

ve indicators of a firm's intangible assets.

financial measures are increasingly important in decision-making and performance evaluation, companies should not simply copy measures used

linked to factors such as corporate strategy, value drivers, organizational objectives and the competitive

environment. In addition, companies should remember that performance measurement choice is a dynamic process - measures may be appropriate today, but

the system needs to be continually reassessed as strategies and competitive environments evolve.

, McGraw Hill, INC, New York, 1996.

Managing cost in manufacturing”, Prentice Hall, Newyork.

, (Oct. 16, 2000), “Mastering Management series”, Financial Times.

Hill, New York, 1996.

The evolution of management accounting” The accounting review, 59,390-417.

“Measurement of organizational performance of national and international firms: objective vs. subjective measure”

If it maters, measure it” Journal of accountancy, pp 52-53.

“The rise and rise of the NFI, ed, Ratnatunga, et al”, Issues in strategy Management Accounting, BBJ Publishers

“Human Resource Management”, McGraw Hill, New York.

Decrease the efficiency of

organizational performance

Resources both Human and capital

are not utilized properly

ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT Included in the International Serial Directories

41

Because of this in Bangladesh most of the government firms except some firms are facing huge financial loss and in recent time it is noticeable that some

: BTCL, DESCO etc. So, the importances of NFIs are

financial measures offer some clear advantages over measurement systems based on financial data. First, these NFIs

on annual or short-term performance against accounting

financial objectives that may be important in achieving

term strategic goals. For example, new product development or expanding organizational capabilities may be

term accounting performance. With supplementing accounting measures with non-financial data about strategic

performance and implementation of strategic plans, companies can communicate objectives and provide incentives for managers to address long-term strategy.

s are "intangible assets" such as intellectual capital and customer loyalty,

rather than "hard assets" allowed to balance sheets. Although it is difficult to quantify intangible assets in financial terms, non-financial data can provide

making and performance evaluation, companies should not simply copy measures used

linked to factors such as corporate strategy, value drivers, organizational objectives and the competitive

measures may be appropriate today, but

ernational firms: objective vs. subjective measure”, Journal of

nga, et al”, Issues in strategy Management Accounting, BBJ Publishers, Sydney.

Long term financial loss

Example: Biman Bangladesh Airlines

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

42

REQUEST FOR FEEDBACK

Dear Readers

At the very outset, International Journal of Research in Commerce and Management (IJRCM) acknowledges

& appreciates your efforts in showing interest in our present issue under your kind perusal.

I would like to request you to supply your critical comments and suggestions about the material published

in this issue as well as on the journal as a whole, on our E-mails i.e. [email protected] or

[email protected] for further improvements in the interest of research.

If you have any queries please feel free to contact us on our E-mail [email protected].

I am sure that your feedback and deliberations would make future issues better – a result of our joint

effort.

Looking forward an appropriate consideration.

With sincere regards

Thanking you profoundly

Academically yours

Sd/-

Co-ordinator

VOLUME NO. 3 (2012), ISSUE NO. 5 (MAY) ISSN 0976-2183

INTERNATIONAL JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT A Monthly Double-Blind Peer Reviewed Refereed Open Access International e-Journal - Included in the International Serial Directories

www.ijrcm.org.in

I