Embed Size (px)

Citation preview

Verstehen. Handeln.

Volatility Risk

Premium: Stylized Facts and

Portfolio Implications

CBOE Risk Management

Conference Europe 2015

Geneva, Switzerland

Dr. Bernhard Brunner

01

Stylized Facts about Volatility and Volatility Risk Premium

2

Volatility Risk Premium compared to Equity Risk Premium

Volatility risk premium follows the same logic as equity risk premium but is much more attractive over the last 15 years

Equities

Math Interpretation

Investment Realized return over a time

period (e.g. 1 year)

Riskfree (or low risk)

opportunity cost

Riskfree rate over the same

period (e.g. money market)

Risk premium Equity risk premium

(return over money market)

(Equity-)Volatility

Math Interpretation

Realized variance over a

time period (e.g. 1 year)

Implied variance over the

same period

Variance risk premium

-40%

-20%

0%

20%

40%

60%

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

-40%

-20%

0%

20%

40%

60%

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

18%

82% 41%

59% ø 1.6% ø 3.9%

Source: Bloomberg and risklab. Based on EuroStoxx50 and VSTOXX data over the period 01.01.2000-31.08.2015. For further information please see the risklab disclaimer at the end of the presentation.

Equity risk premium Variance risk premium

3

4

The Distribution of Volatility Risk Premium is Skewed!

Distribution of the variance premium:

Manage downside risk when harvesting volatility risk premium

Source: Bloomberg and risklab. Based on EuroStoxx50 and VSTOXX data over the period 01.01.2000-31.08.2015. For further information please see the risklab disclaimer at the end of the presentation.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-19

%

-15

%

-11

%

-7%

-3%

1%

5%

9%

13

%

17

%

21

%

25

%

29

%

33

%

37

%

18% occurrence of losses 82% occurrence of gains

5

Components of Volatility Risk Premium

Additional risk

premium,

depending on

the steepness

of the volatility

smile/skew

Volatility risk

premium

=

Realized

volatility

–

Implied

volatility

Risk premium,

depending on

implied volatility

of at-the-money

options Realized volatility

(e.g. over 30 days)

Implied atm Volatility

(e.g. over 30 days)

Implied Volatility

(e.g. over 30 days)

Volatility risk premium consists of two components:

1 atm = at the money

Received via sale of

Variance Swaps

(held to expiry)

Received via

sale of (delta

hedged) atm

Options

(„Gamma“)

approx. 2/3 of the

historical

realized

volatility risk

premium

approx. 1/3 of the

historical

realized

volatility risk

premium

*

*

Source: Bloomberg and risklab. Based on EuroStoxx50 and VSTOXX data over the period 01.01.2000-31.08.2015. For further information please see the risklab disclaimer at the end of the presentation.

1

Conclusion naive investment approach through rolling of future

contracts

Significant impact of implied volatility

Effect can be reduced by overlapping investments:

What is different between Equity and Volatility Risk Premium?

Equities Volatility

Risk Premium Equity Risk Premium Volatility Risk Premium

Derivative to

capture premium e.g. equity future variance swap

Influencing factors equity return, interest rate, (possibly dividends) implied volatility, realized volatility or (equity return)²

Sensitivity

analysis

0,00%

0,02%

0,04%

0,06%

0,08%

0,0%

0,5%

1,0%

1,5%

1 5 9 13 17 21 25 29 0

0,2

0,4

0,6

0,8

1 5 9 13 17 21 25 29

equity return +1%

rates +1%

Impact on risk premium over 30 days

(equity return +1%)²

implied

volatility +1%

Impact on risk premium over 30 days very low impact!

0

0,2

0,4

0,6

0,8

1 5 9 13 17 21 25 29

Impact on risk premium assuming daily (overlapping) investments

(equity return +1%)²

implied volatility +1%

6

Source: risklab. For further information please see the risklab disclaimer at the end of the presentation.

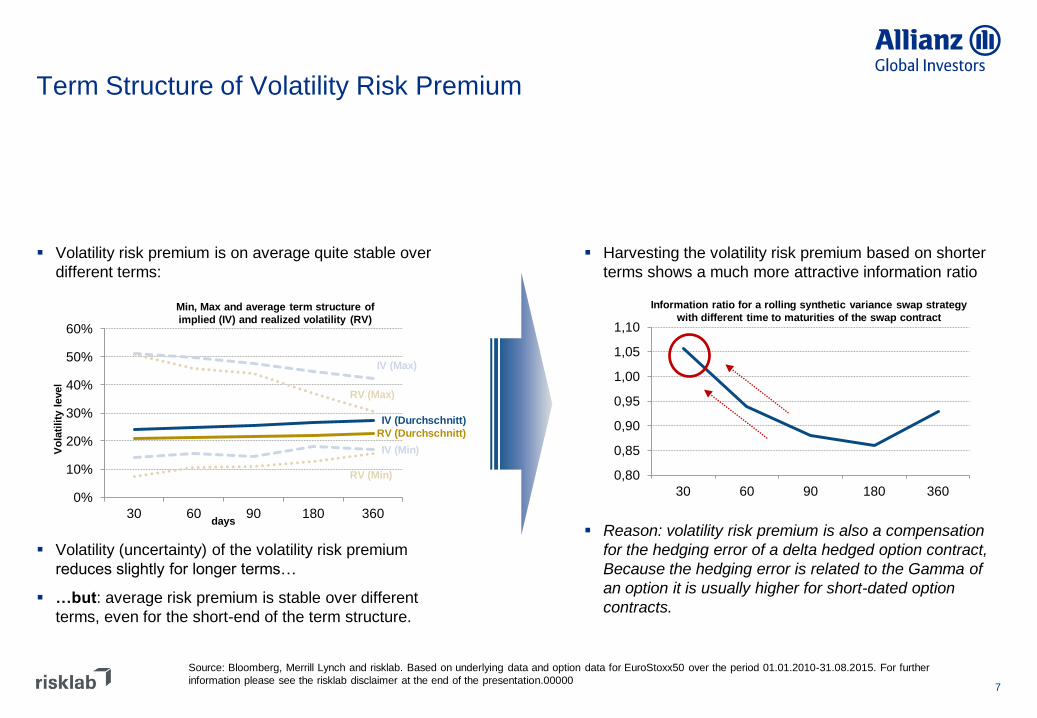

Term Structure of Volatility Risk Premium

Volatility risk premium is on average quite stable over

different terms:

Volatility (uncertainty) of the volatility risk premium

reduces slightly for longer terms…

…but: average risk premium is stable over different

terms, even for the short-end of the term structure.

Harvesting the volatility risk premium based on shorter

terms shows a much more attractive information ratio

Reason: volatility risk premium is also a compensation

for the hedging error of a delta hedged option contract,

Because the hedging error is related to the Gamma of

an option it is usually higher for short-dated option

contracts.

0,80

0,85

0,90

0,95

1,00

1,05

1,10

30 60 90 180 360

Information ratio for a rolling synthetic variance swap strategy

with different time to maturities of the swap contract

7

0%

10%

20%

30%

40%

50%

60%

30 60 90 180 360

IV (Durchschnitt)

RV (Durchschnitt)

RV (Min)

RV (Max)

IV (Max)

IV (Min)

Min, Max and average term structure of

implied (IV) and realized volatility (RV)

days

Vo

lati

lity

level

Source: Bloomberg, Merrill Lynch and risklab. Based on underlying data and option data for EuroStoxx50 over the period 01.01.2010-31.08.2015. For further

information please see the risklab disclaimer at the end of the presentation.00000

-15%

-10%

-5%

0%

5%

10%

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

-40%

-20%

0%

20%

40%

60%

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Volatility Risk Premium for different Asset Classes Equities and FX

0,80

0,85

0,90

0,95

1,00

1,05

1,10

30 60 90 180 360

1,50

2,00

2,50

3,00

3,50

4,00

30 60 90 180 360

Volatility risk premium

European equities

Eurostoxx50

Information ratio for a rolling synthetic variance swap strategy

with different time to maturities of the swap contract Volatility risk premium over 30 days

Volatility risk premium

FX

USD/EUR

76%

24% ø 3.4% IR 1.06

73%

27% ø 1.1% IR 3.67

Source: Bloomberg, Merrill Lynch and risklab. Based on underlying data and option data for EuroStoxx50 and USD/EUR over the period 01.01.2004-31.07.2015. For further

information please see the risklab disclaimer at the end of the presentation.

-30%

-20%

-10%

0%

10%

20%

30%

40%

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

1,60

1,80

2,00

2,20

2,40

2,60

30 60 90 180 360

0,50

0,55

0,60

0,65

0,70

0,75

0,80

0,85

30 60 90 180 360

Volatility Risk Premium for different Asset Classes Commodities: Gold and Oil

Volatility risk premium

Commodities

Gold

Information ratio for a rolling synthetic variance swap strategy

with different time to maturities of the swap contract Volatility risk premium over 30 days

Volatility risk premium

Commodities

Oil

70%

30% ø 1.9% IR 0.80

73%

27% ø 3.7% IR 2.49

Source: Bloomberg, Merrill Lynch and risklab. Based on underlying data and option data for Gold and Oil over the period 01.01.2004-31.07.2015. For further information please see

the risklab disclaimer at the end of the presentation.

-30%

-20%

-10%

0%

10%

20%

20

10

20

11

20

12

20

13

20

14

20

15

-8% -6% -4% -2% 0% 2% 4% 6% 8%

10%

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

0,50

0,70

0,90

1,10

1,30

1,50

1,70

1,90

30 60 90 180 360

1,00

1,10

1,20

1,30

1,40

1,50

1,60

1,70

1,80

30 60 90 180 360

Volatility Risk Premium for different Asset Classes Rates and Credit

Volatility risk premium

Rates

US Treasuries 10y

Information ratio for a rolling synthetic variance swap strategy

with different time to maturities of the swap contract Volatility risk premium over 30 days

Volatility risk premium

Credit

US HY Corporate

65%

35% ø 0.4% IR 1.24

85%

15% ø 3.9% IR 1.69

Source: Bloomberg, Merrill Lynch and risklab. Based on underlying data and option data for US Treasuries and US HY Corporate over the period 01.01.2010-31.07.2015. For further

information please see the risklab disclaimer at the end of the presentation.

Further Characteristics of Volatility …

1. In contrast to other asset classes, volatility does not pay interest or dividends

2. Volatility always returns to its long-term mean (mean reversion effect)

3. Volatility tends to jump (usually when the stock market slumps), followed by lengthier downward trends

4. Volatility forms volatility clusters (regimes)

11

10

20

30

40

50

60

70

80

90

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

VS

TO

XX

in

%

Long-term

average (2)

(3) (3)

(4)

Source: Bloomberg and risklab. EuroStoxx50 and VSTOXX data over the period 01.01.2000-31.08.2015. For further information please see the risklab disclaimer at the

end of the presentation.

… and their Effect on Volatility Risk Premium …

Observation:

Stable and attractive risk premium across all

volatility regimes

-30%

-10%

10%

30%

-30% -20% -10% 0% 10% 20% 30%

0%

20%

40%

60%

-30% -20% -10% 0% 10% 20% 30%

Volatility Cluster (regimes):

Observation:

Strong increase in volatilities negatively impacts the

volatility risk premium

In contrast, a decrease in volatility makes risk

premium even richer

Sensitivity to volatility (regime-switch):

Volatility Risk Premium

Volatility Risk Premium

Imp

lied

Vo

lati

lity

C

han

ge i

n I

mp

lied

Vo

lati

lity

Source: Bloomberg and risklab. EuroStoxx50 and VSTOXX data over the period 01.01.2000-31.08.2015. For further information please see the risklab disclaimer at the end of the

presentation.

Volatility risk premium is richer in a high volatility

environment but its volatility (uncertainty) is also

higher, et vice versa

… are especially attractive when considered together

Ho

he

Vo

latilit

ät

Nie

dri

ge

Vo

latilit

ät

4. 3.

4.

Langfristiges

Mittel

Erwartete Prämie ist niedrig aber

Unsicherheit der Prämie ist

ebenfalls niedrig

Verringerung der Prämie durch

Anstieg der Volatilität

1.Erwartete Prämie ist hoch aber

Unsicherheit der Prämie ist

ebenfalls hoch

Erhöhung der Prämie durch

Abnahme der Volatilität

1.

2.

3.

4.

2.

Mean-reversion effect causes the impact of increasing and decreasing volatilities to cancle out

and enables a stable harvesting of an attractive risk premium over a full volatility cycle

hig

h v

ola

tili

ty

low

vo

lati

lity

long-term

average

1.

3.

4.

2.

risk premium is expected to

be significant but risky

risk premium increases

further through decrease in

market volatilities

risk premium decreases

through increase in market

volatilities

risk premium is expected to

be low but stable (less risky)

Stylized Facts of Volatility and its Risk Premium have to be considered

• Sell volatility (short volatility) Volatility risk premium is negative

• Only variance swaps are able to fully exploit the volatility risk premium Significant part of the risk premium is

related to the steepness of volatility skew

• Focus on shorter end of risk premium term structure Risk premium is more attractive over

shorter time periods

• Consider overlapping investments and reduce timing effects Significant impact of implied volatility when

entering into a new trade

• Adjust exposure according to the current volatility regime Risk/return-ratio depends on the current

volatility regime (cluster)

• Further adjustment of exposure under consideration of the full volatility cycle Mean-reversion effect introduces volatility

cycles

• Include risk management components to reduce significant downside risk when volatility jumps

Volatility often jumps which negatively impacts risk premium

e.g

. riskla

b V

aria

nce P

rem

ium

Tra

din

g

(VP

T) In

dex (B

B: R

LA

BV

PT

<In

dex>

)

Alte

rnativ

e B

eta

A

ltern

ativ

e S

mart B

eta

02

Harvesting Volatility Risk Premium in a Portfolio Context

15

Correlation Analysis Equities

Correlation < 0.5

0.5 ≤ Correlation ≤ 0.75

Correlation > 0.75

Non-Linear Correlation to Equities:

Diversification benefits in normal market periods but correlation increases in market downturns

Source: Bloomberg and risklab.

EuroStoxx50 Index data and VPT Index

data over the period 01.01.2000-

31.08.2015. For further information

please see the risklab disclaimer at the

end of the presentation.

Correlation Analysis Fixed Income

Correlation < 0.5

0.5 ≤ Correlation ≤ 0.75

Correlation > 0.75

Negligible Correlation to Fixed Income:

Diversification benefits in all markets and particularly in rising interest rate markets

Source: Bloomberg and risklab. JPM

Government Bond Index data and VPT

Index data over the period 01.01.2000-

31.08.2015. For further information

please see the risklab disclaimer at the

end of the presentation.

Correlation Analysis Commodities

Correlation < 0.5

0.5 ≤ Correlation ≤ 0.75

Correlation > 0.75

Low Correlation to Commodities:

Diversification benefits in nearly all markets but beware of commodity crisis

Correlation < 0.5

0.5 ≤ Correlation ≤ 0.75

Correlation > 0.75 Source: Bloomberg and risklab.

Bloomberg Commodity Index data and

VPT Index data over the period

01.01.2000-31.08.2015. For further

information please see the risklab

disclaimer at the end of the

presentation.

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

5,0%

5,5%

4% 9% 14% 19% 24%

Retu

rn

Risk (CVaR, 1y, 95%)

SAA SAA Including Volatility

31%

38% 5%

26%

Fixed Income

Equities

Commodities

Volatility

Volatility as an Asset Class improves Risk/Return-

Characteristics of a Portfolio

50%

43%

7%

Fixed Income

Equities

Commodities

45% 28%

4% 23%

Diversification benefits in a portfolio context:

Replacing equities with volatility reduces risk, replacing fixed income with volatility adds return

Source: Bloomberg and risklab. Robust optimization using based on risklab analytics framework. For further information please see the risklab disclaimer at the end of the presentation.

Disclaimer

Investing involves risk. The value of an investment and the income from it may fall as well as rise and investors may not get back the full amount invested.

The volatility of fund unit prices may be increased or even strongly increased. Past performance is not a reliable indicator of future results. If the currency in which the past

performance is displayed differs from the currency of the country in which the investor resides, then the investor should be aware that due to the exchange rate fluctuations the

performance shown may be higher or lower if converted into the investor’s local currency.

Back-testings and hypothetical or simulated performance data has many inherent limitations only some of which are described as follows:

It is designed with the benefit of hindsight, based on historical data, and does not reflect the impact that certain economic and market factors might have had on the decision-making

process, if a client’s portfolio had actually been managed. No back-testings, hypothetical or simulated performance can completely account for the impact of financial risk in actual

performance.

It does not reflect actual transactions and cannot accurately account for the ability to withstand losses.

The information is based, in part, on hypothetical assumptions made for modeling purposes that may not be realized in the actual management of portfolios.

No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used in achieving the returns have been stated or fully considered.

Assumption changes may have a material impact on the model returns presented. The back-testing of performance differs from actual portfolio performance because the investment

strategy may be adjusted at any time, for any reason.

Investors should not assume that they will experience a performance similar to the back-testings, hypothetical or simulated performance shown. Material differences between back-

testings, hypothetical or simulated performance results and actual results subsequently achieved by any investment strategy are possible.

This is for information only and not to be construed as a solicitation or an invitation to make an offer, to conclude a contract, or to buy or sell any securities. The products or securities

described herein may not be available for sale in all jurisdictions or to certain categories of investors. This is for distribution only as permitted by applicable law and in particular not

available to residents and/or nationals of the USA. The investment opportunities described herein are not guaranteed. The views and opinions expressed herein, which are subject to

change without notice, are those of the issuer and/or its affiliated companies at the time of publication. The data used is derived from various sources, and assumed to be correct and

reliable, but it has not been independently verified; its accuracy or completeness is not guaranteed and no liability is assumed for any direct or consequential losses arising from its

use, unless caused by gross negligence or willful misconduct. The conditions of any underlying offer or contract that may have been, or will be, made or concluded, shall prevail.

Contact the issuer electronically or via mail at the address indicated below for a free copy of the sales prospectus, the incorporation documents, the latest annual and semi-annual

financial reports and the key investor information document in English. Please read these documents - which are solely binding - carefully before investing.

This is a marketing communication. Issued by risklab GmbH, www.risklab.com, a wholly owned subsidiary of Allianz Global Investors Holding GmbH. risklab GmbH is a limited liability

company, incorporated in Germany, with its registered office at Seidlstrasse 24-24a, D-80335 Munich, authorized and regulated by Bundesanstalt für Finanzdienstleistungsaufsicht

(www.bafin.de). The duplication, publication, or transmission of the contents, irrespective of the form, is not permitted.

The risklab brand name is used according to the trademark license agreement between risklab GmbH, Seidlstrasse 24-24a D-80335 Munich, Germany (licensee) and Algorithmics

Trademarks LLC, having its principal place of business at 1209 Orange St., Wilmington, Delaware, USA and Algorithmics Incorporated, having its principal place of business at 185

Spadina Ave., Toronto, Ontario, Canada (licensor). risklab is not affiliated with RMS® or RISKLINK®. The following names are registered trademarks of risklab GmbH: risklab

Dynamic Surplus Return Management™, risklab Variance Premium Trading Index™, risklab Commodity Variance Premium Trading Index™, risklab Variance Premium Trading

Stable Index™, risklab Commodities 4 Seasons Index™, risklab Commodities 4 Seasons Long Short Index™.

20

Understand. Act.

Thank You!