Embed Size (px)

Citation preview

Business white paper

Virtual TVStep up to industry challenges in virtualization and cloud

Table of contents

1 A consumer-driven shift

2 The new market scenario

3 A changing market triggers new challenges

4 Business imperatives to position in this market

5 Organizational challenges

6 Capabilities to manage the transformation

7 Providing tangible benefits

7 A solution that works

11 Implementation strategies

12 Conclusion

13 HP enables business transformation for the CME industry

14 About the authors

Business white paper | Virtual TV

1

Business white paper | Virtual TV

The TV Industry is changing at the fastest pace in its history. It is poised at the edge of a radical transformation toward digital. This shift in consumer-usage patterns is providing several implications for players confronted with more complexity in managing content inside their organizations and delivering it across networks. Players that lag behind in adopting cloud solutions put future growth at risk as hardware legacy solutions cannot follow this demand of increased flexibility.

A consumer-driven shift

Catalyst of the transformation is a plethora of connected devices with increasingly larger screens. The falling costs of devices, coupled with the availability of broadband connections, has accelerated the penetration of smart TVs, smartphones, over-the-top (OTT) sticks, tablets, connected set-top boxes and game consoles in households.

With so many connected screens and digital content delivered over Internet protocol (IP), consumers have learned how to take full control of the viewing experience.

Content is increasingly watched on all devices, wherever at home or on the go. Deferred-video watching is getting increasingly popular in broadband homes as consumers decide when to watch live content. With network personal video recorders (nPVRs), users can schedule their favorite programs, record, and watch them later on any device.

This shift in consumer-usage patterns will result in a new market scenario that will have several implications for broadcasters and communications service providers.

Figure 1. Key market data

90%

*Source: Strategy Analytics

10Bconnected devices that are

video enabledby 2020* by 2015*

>

*Source: eMarketer

23%increase of time spent with

mobile devicesby 2014*

*Source: Forrester

*Source: Cisco

of global internet tra c will be video

by 2017*

46%of millennials in the US said

they typically watch TV

time-shifted

2

Digitalization of content enables broadcasters to provide a long list of content so that a library called “all films ever made” could soon be a reality. Consumers, however, are not interested in infinite content as they expect it tailored to their recommendations and preferences.

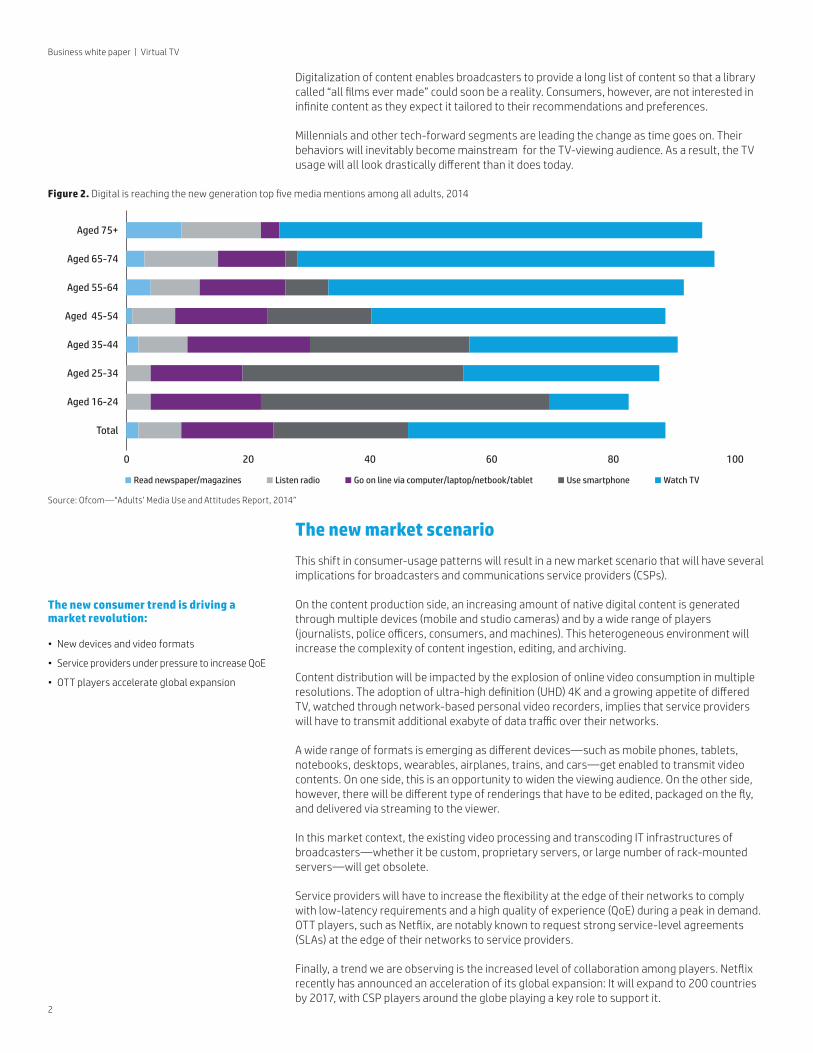

Millennials and other tech-forward segments are leading the change as time goes on. Their behaviors will inevitably become mainstream for the TV-viewing audience. As a result, the TV usage will all look drastically different than it does today.

Business white paper | Virtual TV

Figure 2. Digital is reaching the new generation top five media mentions among all adults, 2014

0 20 40 60 80 100

Total

Aged 16-24

Aged 25-34

Aged 35-44

Aged 45-54

Aged 55-64

Aged 65-74

Aged 75+

Read newspaper/magazines Listen radio Go on line via computer/laptop/netbook/tablet Use smartphone Watch TV

Source: Ofcom—“Adults’ Media Use and Attitudes Report, 2014”

The new market scenario

This shift in consumer-usage patterns will result in a new market scenario that will have several implications for broadcasters and communications service providers (CSPs).

On the content production side, an increasing amount of native digital content is generated through multiple devices (mobile and studio cameras) and by a wide range of players (journalists, police officers, consumers, and machines). This heterogeneous environment will increase the complexity of content ingestion, editing, and archiving.

Content distribution will be impacted by the explosion of online video consumption in multiple resolutions. The adoption of ultra-high definition (UHD) 4K and a growing appetite of differed TV, watched through network-based personal video recorders, implies that service providers will have to transmit additional exabyte of data traffic over their networks.

A wide range of formats is emerging as different devices—such as mobile phones, tablets, notebooks, desktops, wearables, airplanes, trains, and cars—get enabled to transmit video contents. On one side, this is an opportunity to widen the viewing audience. On the other side, however, there will be different type of renderings that have to be edited, packaged on the fly, and delivered via streaming to the viewer.

In this market context, the existing video processing and transcoding IT infrastructures of broadcasters—whether it be custom, proprietary servers, or large number of rack-mounted servers—will get obsolete.

Service providers will have to increase the flexibility at the edge of their networks to comply with low-latency requirements and a high quality of experience (QoE) during a peak in demand. OTT players, such as Netflix, are notably known to request strong service-level agreements (SLAs) at the edge of their networks to service providers.

Finally, a trend we are observing is the increased level of collaboration among players. Netflix recently has announced an acceleration of its global expansion: It will expand to 200 countries by 2017, with CSP players around the globe playing a key role to support it.

The new consumer trend is driving a market revolution:

• New devices and video formats

• Service providers under pressure to increase QoE

• OTT players accelerate global expansion

3

A changing market triggers new challenges

Players in the market should recognize their legacy infrastructures are not able to keep pace with consumer expectations. In short, they are becoming obsolete. Taking a defensive strategy is a risky bet, as opting for the status quo will have clear business impacts.

Business white paper | Virtual TV

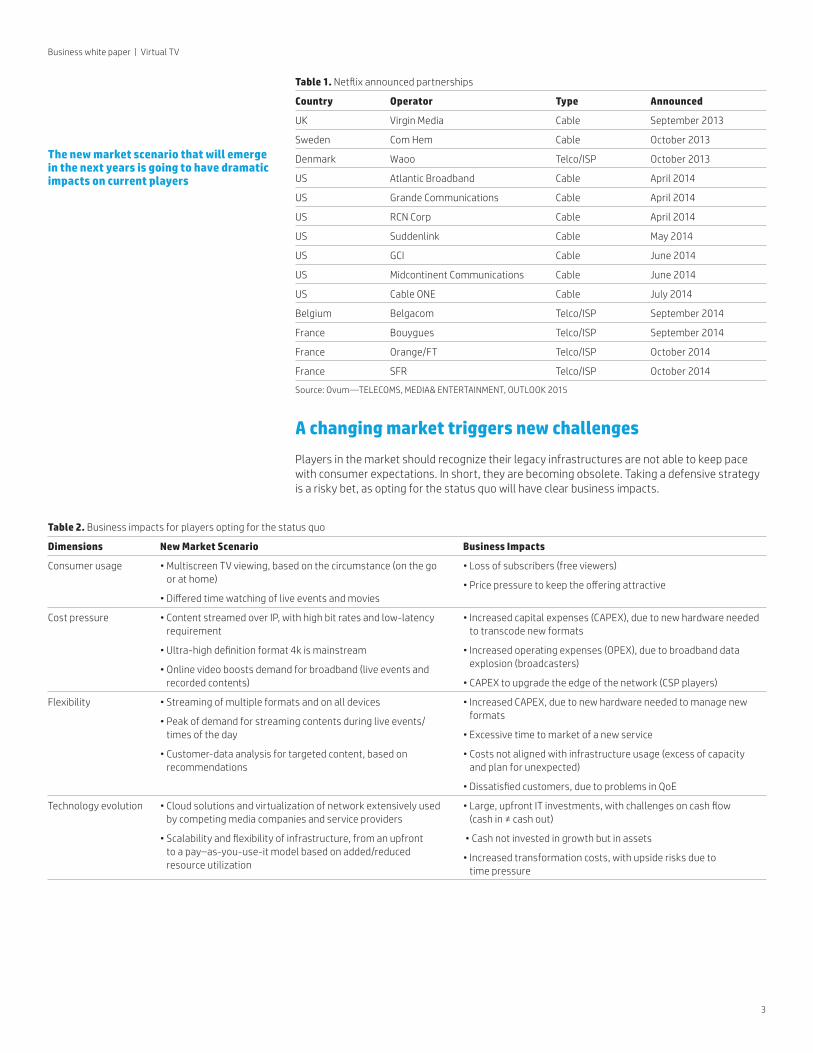

Table 1. Netflix announced partnerships

Country Operator Type Announced

UK Virgin Media Cable September 2013

Sweden Com Hem Cable October 2013

Denmark Waoo Telco/ISP October 2013

US Atlantic Broadband Cable April 2014

US Grande Communications Cable April 2014

US RCN Corp Cable April 2014

US Suddenlink Cable May 2014

US GCI Cable June 2014

US Midcontinent Communications Cable June 2014

US Cable ONE Cable July 2014

Belgium Belgacom Telco/ISP September 2014

France Bouygues Telco/ISP September 2014

France Orange/FT Telco/ISP October 2014

France SFR Telco/ISP October 2014

Source: Ovum—TELECOMS, MEDIA& ENTERTAINMENT, OUTLOOK 2015

Table 2. Business impacts for players opting for the status quo

Dimensions New Market Scenario Business Impacts

Consumer usage • Multiscreen TV viewing, based on the circumstance (on the go or at home)

• Differed time watching of live events and movies

• Loss of subscribers (free viewers)

• Price pressure to keep the offering attractive

Cost pressure • Content streamed over IP, with high bit rates and low-latency requirement

• Ultra-high definition format 4k is mainstream

• Online video boosts demand for broadband (live events and recorded contents)

• Increased capital expenses (CAPEX), due to new hardware needed to transcode new formats

• Increased operating expenses (OPEX), due to broadband data explosion (broadcasters)

• CAPEX to upgrade the edge of the network (CSP players)

Flexibility • Streaming of multiple formats and on all devices

• Peak of demand for streaming contents during live events/ times of the day

• Customer-data analysis for targeted content, based on recommendations

• Increased CAPEX, due to new hardware needed to manage new formats

• Excessive time to market of a new service

• Costs not aligned with infrastructure usage (excess of capacity and plan for unexpected)

• Dissatisfied customers, due to problems in QoE

Technology evolution • Cloud solutions and virtualization of network extensively used by competing media companies and service providers

• Scalability and flexibility of infrastructure, from an upfront to a pay–as-you-use-it model based on added/reduced resource utilization

• Large, upfront IT investments, with challenges on cash flow (cash in ≠ cash out)

• Cash not invested in growth but in assets

• Increased transformation costs, with upside risks due to time pressure

The new market scenario that will emerge in the next years is going to have dramatic impacts on current players

4

The advent of the cloud is shifting data residing on physical devices—such as computers, mobile devices, set-top boxes, and pay TV cards—toward all digital solutions. We expect that by 2020, more than 80% of the content-related data will be stored in the cloud and accessible from everywhere.

Broadcasters and CSPs are moving toward cloud computing and virtualization programs. Successful studios, publishers, telcos, and cable operators are leveraging cloud services to archive, manage, distribute and transform content across the production value chain. This leads to an optimization IT resources during peals in demand due to an allocation of capabilities based on traffic requirements.

Sharing resources within the organization reduces operating costs and cost structures can be rationalized by delegating business operations to other partners.

Content delivery is already experiencing cloud options. Standards, such as the framework for interoperable media services (FIMS) which is adopted for easier cross-media, multi-platform delivery. Video transcoding and optimization of media experiences via adaptive bitrate streaming for delivery to TVs, PCs, and mobile devices are increasingly managed on virtual machines operating on OpenStack. These solutions enable full flexibility and scalability.

Content management in the cloud is an emerging trend. Archive and live production environment still rely on specialty hardware and dedicated serial digital interfaces (SDIs)—making it the most critical application for broadcasters. The lowest latencies and highest throughput and reliability are required in managing this step of the value chain, which explains why those proven technologies still dominate. Regardless of this, packet-based networks are continuously improving; 10 gigabit Ethernet (gigE) is getting more affordable, while 40 gigE and 100 gigE are on the way.

Business imperatives to position in this market

Based on our discussions with media companies and service providers, a set of strategic priorities needs to be addressed to succeed in this market. It is not just a matter of addressing one or two. The new market demands a laser focus on addressing all business imperatives to get a stake out of this scenario.

•Content—Ensure content is delivered on all devices, in all formats, and with a high quality of experience for the viewer (broadcasters, CSPs).

•Customer lifetime value—Improve the average revenue per user (ARPU) and reduce the churn by offering freemium services, such as a network personal video recorder, and offer customized content to lock in the viewer (broadcasters, CSPs).

•Innovation—Get the agility to test new ways to monetize content and business models, with a fail-early, fail-fast approach and without committing to an upfront cash outflow (broadcasters, CSPs).

•Online advertising—Optimize the monetization of online advertising by increasing the inventory and tailoring advertising to the viewer (broadcasters, CSPs)

•Operationalefficiency—Ensure full scalability while rationalizing the organization, processes, and IT infrastructures in a new context in which hundreds of virtual machines and software need to be configured/maintained (broadcasters, CSPs).

Turning these imperatives into action requires an infrastructure that scales with demand and manages the desired level of flexibility while keeping costs under control. In a highly competitive market, context with aggressive OTT players saving capital and operational expenditures is key.

To achieve these goals, according to the latest Infonetics Research survey, chief technology officers (CTOs) intend to apply new strategies for CAPEX and OPEX reduction. A faster time to market and flexibility in setting up new services are also key for adopting a virtualized environment and cloud-computing technology.

Business white paper | Virtual TV

The strategic priorities need to be mapped on new operational, functional and network capabilities

5

Organizational challenges

This shift toward virtual environments has profound implications from an organizational point of view.

In particular, broadcasters, which traditionally were relying on engineers, will have to reshape their skillsets as they get exposed for the first time to an IT world.

For them, rationalizing the organization is a must as their services have become multichannel and multidevice. All players will have to be able to deliver content over different delivery chains—such as satellite, digital terrestrial television (DTT), digital subscriber line (DSL), Windows, and mobile operating systems (iOS, Android).

Broadcasters have been historically structured with separate teams working on the different media channels, each team adopting different technologies. We see a tendency to organize teams vertically in the value chain. For example, there are separate teams for the headend, DRM, delivery and video player, and user interface—all working independently from the delivery channel.

Business white paper | Virtual TV

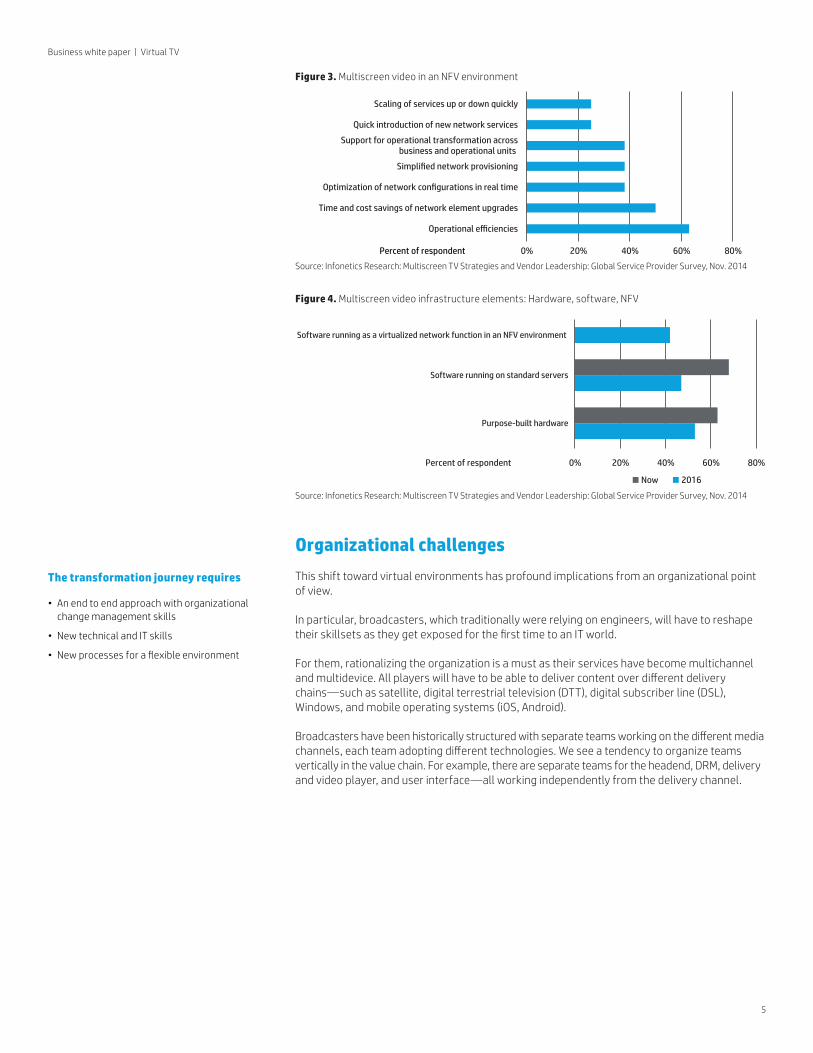

Figure 3. Multiscreen video in an NFV environment

0% 20% 40% 60% 80%

Operational efficiencies

Time and cost savings of network element upgrades

Optimization of network configurations in real time

Simplified network provisioning

Support for operational transformation acrossbusiness and operational units

Quick introduction of new network services

Scaling of services up or down quickly

Percent of respondent

Source: Infonetics Research: Multiscreen TV Strategies and Vendor Leadership: Global Service Provider Survey, Nov. 2014

Figure 4. Multiscreen video infrastructure elements: Hardware, software, NFV

0% 20% 40% 60% 80%

Purpose-built hardware

Software running on standard servers

Software running as a virtualized network function in an NFV environment

Now 2016

Percent of respondent

Source: Infonetics Research: Multiscreen TV Strategies and Vendor Leadership: Global Service Provider Survey, Nov. 2014

The transformation journey requires

• An end to end approach with organizational change management skills

• New technical and IT skills

• New processes for a flexible environment

6

The transformation journey toward a virtualized and cloud architecture requires an end-to-end approach with organizational change management skills, along with technical (IT and media) implementation skills. Typically, there is a pushback from operations as the responsibility gets more horizontal, transferring additional work to IT staff. Usually, changes are not only limited to new responsibilities. They also include new processes and a proactive acceptance of working in more flexible environments. In terms of skills, there is a need to create new ones in the IT software (OpenStack, for example). In a fully virtualized environment, the roles of the teams are normally split in this way:

• Infrastructure operations team—Takes care of virtual machines, profiles, blades, configuration maintenance and all the network-related activities.

• Operations team—Handles video services: sources, provisioning, video processing, outputs redundancy, and app failover.

Capabilities to manage the transformation

The transformation journey implies there is a need for new capabilities. While some players, such as OTT and broadcasters, are focused on storage, CSPs will have to find efficient solutions to deliver content over IP. All players will recognize the need to have the following capabilities:

ScalabilityFor operators offering only linear TV, there is no question to scale up, as the only thing that can be added is the number of channels aired. Digital content is being delivered over IP toward an audience with increasingly different expectations. Viewers, now with more and more devices, are looking for on-demand solutions, which require a fully scalable infrastructure. Single standard servers can be deployed to run concurrent applications—such as live and video on demand (VoD) transcoding, digital rights management (DRM) encryption, file packaging, and streaming. These apps add the desired level of scalability.

FlexibilityThe trend of putting more structured information at the edge of the network is accelerating. The ETSI mobile edge contracting is coordinating the needs for a new technology infrastructure at the edge of the network. This will enable innovative business models and supports content-driven applications, with caching and low latency running in open ecosystem.

CSPs are evolving their networks to enable content to be delivered through network functions virtualization (NFV) instead of static routing. A virtual content delivery network (vCDN) infrastructure adjusts resources to unexpected changes in demand. NFV and SDN virtualize the network functions, meaning that the end points of the network adapt when traffic increases at a given location. Content distribution is optimized from one end point to the other by changing the routing patterns and by triggering new end points as traffic increases. Content is picked up where it is closest to destination (caching), and traffic routing is optimized. Virtual CDNs also enable players to share resources with other players or CDN providers as well.

AnalyticsAll players need capabilities to turn customer data into relevant insights having an impact on research and development (R&D), marketing, and post-sales processes. These data will have to be positioned in the cloud. In the past, the few available data were stored in user devices. These data may be used and shared outside the organization, but first of all, there is a need to have the tools to render the data.

The Fidelity index will increase if players provide a one-stop shop that provides a complete experience targeted to the single viewer’s preferences. The big question is who owns the data: It could be network owner (CSP) or the broadcaster that is the interface with the viewer.

Business white paper | Virtual TV

CSPs and media players need to a new set of capabilities to manage the position into the new market

7

Providingtangiblebenefits

The implementation of a virtualized infrastructure is associated with tangible benefits. These can be divided into three core areas: hardware independence, business agility, and CAPEX and OPEX savings.

Hardware independenceThe implementation of a virtualized infrastructure means there is a decoupling of applications from the underlying hardware. This enables the introduction of latest blades seamlessly as the existing software licenses and the software video can be used on standard servers. Furthermore, this solution enables adjusting the output/channel capacity via code-efficiency enhancements without changing hardware.

Business agilityVirtual environments have the ability to automatically spawn additional instances for load spikes and short-lived events. A further element of agility is the lead time to commission new machines (from hours to minutes), machine reboot (from >30min to <5min), and the disaster recovery (from days to hours). Business agility includes:

• Enhanced monitoring and management tools

• Faster deployment of services on unified infrastructure

• New monetization opportunities and the ability to test innovative services due to shorter software innovation cycles

CAPEX/OPEXThe robust sharing of hardware among apps turns into massive savings. On the CAPEX side, the main savings derive from reduced network connectivity, switch ports and cables, and the space needed to host the infrastructure. Lower power consumption—due to more efficient cooling combined with a need for a less specialized and smaller admin and operations staff size—turns into tangible OPEX savings. In short, the density and ability to pack a huge amount in processing power in a chassis enable the same transcoding functions while reducing the footprint and the cost per stream. This translates into a reduced total cost of ownership.

Business white paper | Virtual TV

Table 3. TCO drivers

CAPEX TCO impact OPEX TCO impact

Cost/channel of encoding: HW High Infrastructure management and administration staffing High

Cost/channel of encoding: SW High Video services ops team staffing High

Virtualization software (hypervisor) Medium SLA (product support and ProServ) Medium

Network Infrastructure components Medium Initial installation/integration Medium

Network ports Medium Power Medium

Virtualization management SW (centralized infra management)

Low Cooling Medium

Blade system management SW Low Rack space (facility) Medium

A solution that works

The next-generation infrastructure consists of storage, network functions, and computing virtualization. The target architecture objective is to balance the adoption of solutions that improve storage capabilities and take into account the limitation of the network capacity. It is enabled by a software-defined video architecture that enables the acquisition, elaboration, and transmission of multiple terabits of data per second, with low-latency throughput and fast network connectivity.

The implementation of a virtualized infrastructure is associated with tangiblebenefits.Thesecanbedividedinto three core areas: hardware standardization, CAPEX and OPEX savings, and business agility.

8

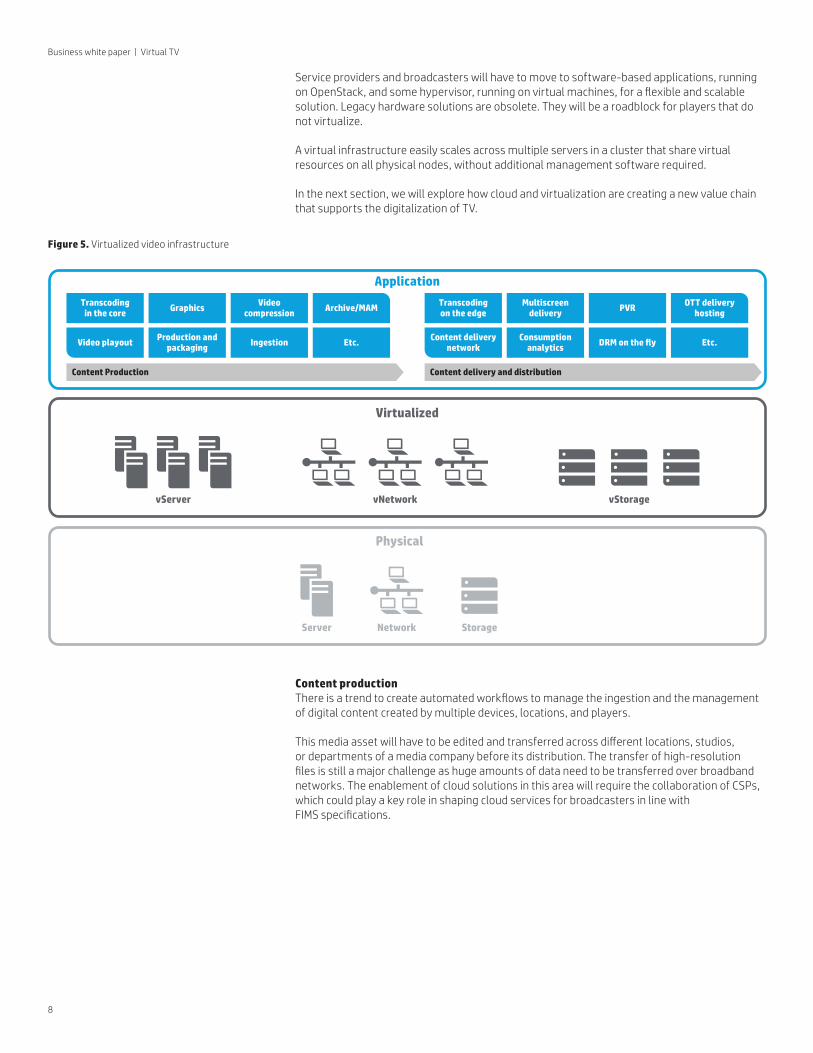

Service providers and broadcasters will have to move to software-based applications, running on OpenStack, and some hypervisor, running on virtual machines, for a flexible and scalable solution. Legacy hardware solutions are obsolete. They will be a roadblock for players that do not virtualize.

A virtual infrastructure easily scales across multiple servers in a cluster that share virtual resources on all physical nodes, without additional management software required.

In the next section, we will explore how cloud and virtualization are creating a new value chain that supports the digitalization of TV.

Business white paper | Virtual TV

Transcodingin the core Graphics Video

compression Archive/MAM

Video playout Production andpackaging Ingestion Etc.

Transcodingon the edge

Multiscreendelivery PVR OTT delivery

hosting

Content deliverynetwork

Consumptionanalytics DRM on the fly Etc.

Application

Virtualized

vServer vNetwork vStorage

Physical

Server Network Storage

Content delivery and distributionContent Production

Figure 5. Virtualized video infrastructure

Content productionThere is a trend to create automated workflows to manage the ingestion and the management of digital content created by multiple devices, locations, and players.

This media asset will have to be edited and transferred across different locations, studios, or departments of a media company before its distribution. The transfer of high-resolution files is still a major challenge as huge amounts of data need to be transferred over broadband networks. The enablement of cloud solutions in this area will require the collaboration of CSPs, which could play a key role in shaping cloud services for broadcasters in line with FIMS specifications.

9

A shift to a fully digital content creation will generate thousands of terabytes of data for films, television shows, and other content. This huge amount of data must be optimized to reduce volumes, without having an impact on the quality of experience. It has to be secured for a long time while being quickly accessible, retrievable, and protected.

The next-generation video production infrastructure combines corporate media asset management (MAM), workflow, archives, and a reliable and secure media cloud infrastructure. A cloud media platform provides an on-demand capability—from content creation and management to distribution and monitoring—enabling:

• Less complexity by leveraging cloud-based services

• Fast deployment—much faster than developing in-house

• Comprehensive and secure storage of media assets and subscriber information

• Quick and easy discovery of relevant content for operators and consumers

• A better business model—operating expenses instead of capital expenditures

This enables an end-to-end digital workflow that can break down the barriers between production teams and other business units. By adopting a service-oriented architecture (SOA) approach and cloud technologies in the production processes, it is possible to decouple operations from dedicated applications and infrastructures. This enables content to be easily shared across the company s ecosystem, including partners. Further, integrated business intelligence and analytics tools can measure content performance, track user activity, and optimize the consumer experience.

The architecture should be designed, keeping in mind two main points:

• Throughput instead of capacity matter: This impacts costs of the infrastructure as fast disks and highly power consumptions storage should be always online.

• Latency more than bandwidth: This impacts collaboration concurrent actions over a distributed environment.

It is important to plan the architecture by evaluating all the dimensions early in the design, such as networking, storage, capacity, sustained throughput, computing power, and software licenses. Granted, this initial outlay generates extra costs at the beginning. That said, the planning builds the foundation to mitigate or avoid future cost explosions. Better yet, this planning brings benefits once the long-awaited features are finally available as a simple software license acquisition.

Video transcodingThe conversion and compression of video and audio data to enable content on all devices create an extremely compute-intensive process. The shift from the advanced video coding (AVC) industry standard for video transcoding toward a new standard—called H.265 high efficiency video coding (HEVC)—will reduce bandwidth requirements by as much as 60%. It, however, will increase the processing effort by 10X. The emerging UHD 4K format will require additional compute resources.

Software-defined, video-processing platforms optimizing transcoding and caching are available for deployment on-premises or in the cloud. Built on OpenStack, these virtual machines offer a modular, pluggable, and extensible architecture for video transcoding. They optimize media experiences via adaptive bitrate streaming for delivery to TVs, PCs, and mobile devices.

A single server can run concurrent applications—such as live and video on demand (VoD) transcoding, digital rights management (DRM) encryption, file packaging, and streaming. In addition, such a solution can easily scale across multiple servers in a cluster, all sharing virtual resources.

Business white paper | Virtual TV

Business agility includes:

• Enhanced monitoring and management tools

• Faster deployment of services on unified infrastructure

• New monetization opportunities and the ability to test innovative services due to shorter software innovation cycles

10

Business white paper | Virtual TV

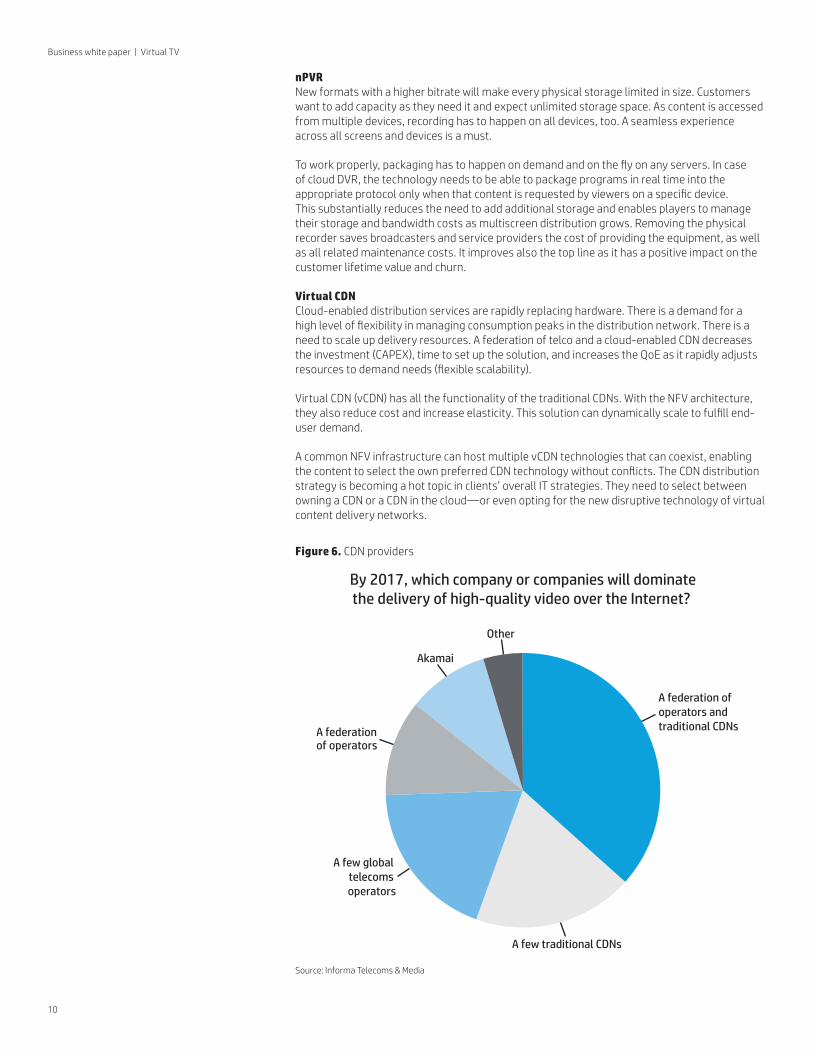

Figure 6. CDN providers

By 2017, which company or companies will dominatethe delivery of high-quality video over the Internet?

Other

Akamai

A few traditional CDNs

A few global telecoms operators

A federationof operators

A federation of operators and traditional CDNs

Source: Informa Telecoms & Media

nPVRNew formats with a higher bitrate will make every physical storage limited in size. Customers want to add capacity as they need it and expect unlimited storage space. As content is accessed from multiple devices, recording has to happen on all devices, too. A seamless experience across all screens and devices is a must.

To work properly, packaging has to happen on demand and on the fly on any servers. In case of cloud DVR, the technology needs to be able to package programs in real time into the appropriate protocol only when that content is requested by viewers on a specific device. This substantially reduces the need to add additional storage and enables players to manage their storage and bandwidth costs as multiscreen distribution grows. Removing the physical recorder saves broadcasters and service providers the cost of providing the equipment, as well as all related maintenance costs. It improves also the top line as it has a positive impact on the customer lifetime value and churn.

Virtual CDNCloud-enabled distribution services are rapidly replacing hardware. There is a demand for a high level of flexibility in managing consumption peaks in the distribution network. There is a need to scale up delivery resources. A federation of telco and a cloud-enabled CDN decreases the investment (CAPEX), time to set up the solution, and increases the QoE as it rapidly adjusts resources to demand needs (flexible scalability).

Virtual CDN (vCDN) has all the functionality of the traditional CDNs. With the NFV architecture, they also reduce cost and increase elasticity. This solution can dynamically scale to fulfill end-user demand.

A common NFV infrastructure can host multiple vCDN technologies that can coexist, enabling the content to select the own preferred CDN technology without conflicts. The CDN distribution strategy is becoming a hot topic in clients’ overall IT strategies. They need to select between owning a CDN or a CDN in the cloud—or even opting for the new disruptive technology of virtual content delivery networks.

11

The major benefits for telco and media players with vCDN are:

• Economic impact: Enable the next order of magnitude in terms of scale, supporting the shift from traditional TV to OTT TV.

• Elasticity: CDN can be deployed dynamically to fulfill end-user demands.

• Multiplicity: Different vCDN technologies can coexist and run in the same NFV infrastructure.

• TV service bundling: This includes TV middleware, nPVR, video analytics, and content management systems.

SecurityThe proliferation of mobile, as well as machine–to-machine devices, has created a heterogeneous ecosystem of devices running on different architectures, not all certified. Key is to secure the edge of the network and the cloud. Regarding piracy, nPVR can ensure more control than set-top boxes as the file can be digitally protected and is not resident on a physical device. In terms of reliability, when the viewer stores the content, the viewer expects it to be stored correctly. If not, there will be a negative user experience. Finally, as not all devices support all DRM, there is an increasing need to adapt digital rights on the fly.

Implementation strategies

The move toward NFV implies a reorganization of the hardware located in the core and on the edge. Once fully implemented, the NFV orchestrator enables a high level of agility in deploying network resources, such as caching, vCDN, routing, and more.

Without a clear adoption strategy, there is the serious risk to incur into a costly transformation with negative impacts on the overall return on investment (ROI). To minimize the risk and achieve tangible results, we suggest a two-step approach in moving toward the virtualization journey:

• The first step transforms the edge of the network. The adoption of standard servers and software running in virtual environment enabled resources to be shared among different applications, based on peaks in demand.

• In the second step, a NFV director is set up to orchestrate the virtualized network functions to optimize the video delivery.

A near-future evolution is the integration of NFV with analytics systems to trigger proactive reactions in a real-time mode, turning the network infrastructure configuration for video delivery.

The setup of a virtualized architecture can be done with different models, each having strategic implications, advantages, and disadvantages:

In-house Setting up everything in-house implies having hardware, software, and required human resources managing the virtual infrastructure inside the organization. The advantage of this solution is that it grants full control to the organization, using the infrastructure and eliminating most of the dependencies that typically arise when external partners are involved. It is not only a matter of having only full control of daily operations, but more importantly, it is a long-term strategic choice as the organization acquires a set of core capabilities (HR skills and processes). The disadvantage is that it requires a significant investment of financial resources and time to set up.

Business white paper | Virtual TV

The architecture virtualization can be managed with a direct control of the infrastructure or by external partners

12

Managed services In this option, the infrastructure is located in the premises of the organization. Servers and software are fully owned by the organization. The maintenance and management are put in the hands of an external partner that will follow the defined SLAs. This option requires a limited amount of investment. In addition, it can be implemented faster, as there is no need to source the required IT skills that may not be in the organization. Typically, it is the preferred option for starting up new initiatives, as it minimizes initial risks by shifting a large burden of the complexity to an external entity.

The journey toward a virtual environment can happen in two progressive phases. Players can initially opt for managed services and then decide to ramp up the commitment by opting for an in-house solution.

Conclusion

A generational shift is accelerating the consumption of digital TV, wherever at home or on the go. This digitalization enables broadcasters to provide a long list of content so that a library called “all films ever made” could soon be reality.

The innovation of format and resolution (UHD 4K) and the appetite of different experience of TV watching through network-based personal video recorders (nPVR) imply that CSPs have to transmit additional exabyte of data traffic over their networks, sustaining quality of service and experience.

If they want to keep the pace of customer expectations, all the players in this market— content producers, broadcasters, and CSPs—need to establish new partnerships, exploring the new capabilities that cloud solutions and virtualization approach can grant into the media market segment.

While players such as OTT players and broadcasters are focused on cloud storage, CSPs will have to find efficient solutions to deliver content over a virtualized infrastructure.

Nowadays, the main areas of virtualization are content production, video transcoding, nPVR and vCDN that are leveraging new disruptive technologies, such as NFV.

A virtual infrastructure easily scales across multiple servers in a cluster that shares virtual resources on all physical nodes, without additional management software required.

This next-generation infrastructure is the result of storage, network functions, and computing virtualization. The target architecture objective is to balance the adoption of solutions that enable increased storage capabilities, with the limitation of the network capacity. The performances required for acquisition, elaboration, and transmission of huge amounts of data with low-latency throughput and high network speed are enabled by the software layer.

The implementation of a video-virtualized infrastructure is associated with tangible benefits that can be divided into three core areas: hardware independence, business agility, and CAPEX and OPEX savings.

Without a clear adoption strategy, there is the serious risk to incur a costly transformation, which impacts the overall return on investment. To minimize the risk and achieve tangible results, we suggest a two-step approach in the virtualization journey. The first step consists in transforming the edge of the network. The second involves orchestrating the virtualized network functions through an NFV director.

Business white paper | Virtual TV

13

HP enables business transformation for the CME industry

HP CME assists the world’s top communications and media companies to transform their customers’ experiences and exceed business objectives of cost efficiency, innovation, and increasing revenues. HP CME draws upon more than 30 years of hands-on telecom industry experience and proven leadership in combining network and IT technologies. HP CME business consulting practice SCS delivers a comprehensive suite of industry business consulting services designed to transform a CSP from a technology-centric business to a customer-centric business by offering:

• CME industry thought-leader business consultants—leveraging global reach with local capabilities

• A proven track record of defining and executing business transformation to large CSPs, worldwide

• A portfolio of consulting services that can be combined and customized to meet key business objectives

• A proven methodology to guide and orchestrate a completely customized transformation strategy on any scale

• A model-based approach that attacks problems in a systematic way, synchronizing interdependencies between operations, organization, and technology”

Business white paper | Virtual TV

• Hardware independency• Dedicated and virtualized server implementations• Cloud and managed services• Full IP production• TV everywhere

• Mobile devices and apps• Video virtualized functions on the edge (transcoding, CDN, etc.)• Third-party video service brokerage

• Network function virtualization• Network analytics• Second-generation cloud computing technologies with standards

Broadcasters’drivers and

tends

Cloud andvirtualization

technology trends

CSP drivers and trends

Virtual videoinfrastructureand TV cloud

solutions

Figure 7. Virtualized video infrastructure and cloud TV

Rate this documentShare with colleagues

Sign up for updates hp.com/go/getupdated

HP Industry Advisory Program is a unique HP Solution Consulting Services program that delivers innovative thought leadership to address clients’ key business issues. The program is built on the global knowledge, expertise, and experience of our industry business consultants. It incorporates proven HP methodologies, industry frameworks, and intellectual capital to deliver true business value through a collaborative, social media-based environment.

Learn more athp.com/go/scs

About the authors

Alessandro PugliaAlessandro Puglia has more than 10 years of consulting and industry experience, helping clients improve their performance by addressing strategic and operational issues. In his career, Puglia served top players across communications and media industry as a business consultant, applying advanced subject-matter knowledge in complex business issues, and identifying and executing their IT strategies.

Max Ferdinand BaldelliMax F. Baldelli is a strategy consultant with extensive CME industry experience, helping clients in managing new strategic initiatives and transformation projects. In his career, Baldelli supported top players operating in the communications and media industry in evaluating opportunities and executing business strategies. His core focus and experience are in linking user needs with technology solutions.

Alberto Curcio Alberto Curcio is a solution-oriented professional with a business, technical, and communications background. Curcio has a special interest in the new frontier of telecommunication business consulting methodologies with heterogeneous worldwide experience. His core focus and experience are in the analysis and design of business processes, business management consulting, IT strategy development, and conceptual design.

Business white paper | Virtual TV

© Copyright 2015 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. The only warranties for HP products and services are set forth in the express warranty statements accompanying such products and services. Nothing herein should be construed as constituting an additional warranty. HP shall not be liable for technical or editorial errors or omissions contained herein.

4AA5-7335ENW, March 2015