Embed Size (px)

Citation preview

Erasmus University RotterdamErasmus School of EconomicsAccounting, Auditing & ControlAccounting & AuditingMaster Thesis

The Impact of Audit Client Complexity on the Audit Fee: the Role of Auditor Industry Specialization

Date: 28 July 2014

Name: Jian Guo (328226)

Supervisor: Mr. E.A. de Knecht RA

Co-reader: Mr. R. van der Wal RA

AcknowledgementsThis thesis is written for the completion of the master program Accounting, Auditing and

Control at the Erasmus University of Rotterdam. It can be seen as the final assignment of my

scientific education and a starting point for my professional education to become a certified

public auditor in the Netherlands. Therefore, the research subject has been carefully chosen

that is embedded within the auditing theory: audit fee determination. The main motivation for

this topic is that it is highly relevant to the practice. Since there is not a clear guideline to

determine the level of audit fee, academic contribution of examining of audit fee determinants

can be really helpful towards existing literature about audit fee determination.

It has been an intensive period to conduct the research and to write the master thesis,

especially since the first time that I met my supervisor was eight weeks after handing in the

application form and thesis proposal, what normally takes around three weeks. Nevertheless, I

was able to finish the thesis and want to thank to several people who have supported me

during the time of writing the thesis.

First of all, I want to thank my supervisor, Mr. E.A. de Knecht RA, who has provided me lots

of valuable feedbacks and useful insights on a timely manner. The discussions with Mr. de

Knecht were very helpful to obtain a questioning mind and critical view. This was not only

helpful for my thesis, but also for my future career and life. Secondly, I want to thank EY

Rotterdam for providing me a stimulating environment to write my thesis. I especially want to

thank my supervisor at EY, Ms. Marloes de Vries RA, for giving me useful supports from

practical aspects of the audit professions in relation to my thesis subject. Last but not least, I

want to thank my parents, my girlfriend and my friends for their tremendous support during

the final period of my master program.

Jian Guo

Delft, July 2014

2

AbstractThis thesis examines whether the auditor industry specialization would influence the impact

of the audit client complexity on the audit fee. By using 10136 firm-years observations of

U.S. listed companies from 2007 up to and included 2013, the findings indicate that the audit

industry specialist fee premium exists for complex clients. In the supplemental tests, the

difference in the audit fee the among complex and noncomplex companies has been

confirmed to be statistically significant when controlling other fee determinants, consistent

with the conclusion that industry specialists require a higher fee for compensating the

education costs. When considered in conjunction with the prior research, this thesis provides

another approach to measure the audit client complexity. The results suggest that companies

of certain industries are more complex to audit due to their characteristic operations, and

thereby require more efforts from auditors to perform the audit and ask for a higher audit fee.

3

Table of Contents

1. Introduction 61.1 Background 61.2 Relevance 81.3 Objective 91.4 Research question 91.5 Methodology 101.6 Demarcation and Limitation 101.7 Structure 11

2. Theoretical Background 122.1 Introduction 122.2 Agency Theory 12 2.2.1 Information Asymmetry and Agency Costs 12 2.2.2 Financial Statements Audit and the Costs 132.3 The Role of the Public Auditor 14 2.3.1 Audit Services 14 2.3.2 Certified Public Accounting Firms 15 2.3.3 The BIG 4 Network and Its Impact 152.4 Audit fee 16 2.4.1 Audit Pricing Model 162.5 The Determinants of the Audit Fee 17 2.5.1 Client Size 17 2.5.2 Client Business Risk 18 2.5.3 Client Complexity 18 2.5.4 Auditor Specialization 192.6 Summary 20

3. Prior Research 223.1 Introduction 223.2 Common Determinants of Audit Fee 223.3 Audit Client Complexity 263.4 Auditor Industry Specialization 293.5 Hypotheses Development 313.6 Summary 32

4. Research Design 344.1 Introduction 344.2 Research Approaches in Accounting 34 4.2.1 Quantitative Researches 354.3 Research Methodology 354.3.3 Control Variables 384.4 Sample Collection 40

5. Results 43

4

5.1 Introduction 435.2 Assumptions for Regression Analysis 435.3 Mean Differences of Client Complexity and Industry Specialists 465.4 Association of Client Complexity and Industry Specialists 475.5 Analysis of the Investigation Concerning the Audit Client Complexity and the Auditor Industry

Specialization 48 5.5.1 Descriptive Statistics of the Regression Components 485.6 Interaction of Client Complexity and the Industry Specialists on the Audit Fee 505.7 Discussion 525.8 Summary 54

6. Conclusion 566.1 Introduction 566.2 Research Summary 566.3 Conclusions 566.4 Limitations 576.5 Suggestions for Further Research 58

References 59

Appendix 62

5

1. Introduction

1.1 Background

Nowadays, public auditors are accomplishing an indispensable role in the worldwide financial

markets. They ensure the quality of the company’s annual financial statements and enhance the

confidence of the public and the investors in the capital market. It is worth noting that, over the last

decades, several well-known financial scandals exist in which public auditors are jointly responsible.

Because of these scandals investors and stakeholders have paid huge prices. Consequently,

maintaining a high level of audit quality to prevent such a scandal from happening again in the future

should be the top priority to all audit firms.

Audit service provided by public auditors ‘is a professional service that improves the quality of

information for decision makers’ (Arens, Elder, & Beasley, 2013 p.8). High quality information

indicates that the firms’ annual financial statements are free of material misstatements, consequently,

presenting a firm’s financial position in a true and fair view. In return to the service, companies are

charged by the audit firms to compensate the effort from the public auditors, this is qualified as the

audit fee. Because every company has its unique settings and industry environment, among firms the

amount of audit fee varies.

In order to perform an audit, a certain amount of professional knowledge from public auditors is

required. It is not only the knowledge about how to design and implement the audit procedures, but

also specific knowledge regarding to the industry in which the client firm is operating. This industry

specific knowledge is particularly valuable for understanding their client business and its business

environment. Consequently, this specific knowledge can be qualified as the specialization of an audit

firm, which is not required by any regulations but which is essential for maintaining a high quality

audit engagement.

When preventing audit failures, the public auditor’s knowledge is crucial. Audit failure occurs when

the public auditors stated that a firm’s annual financial statement is free of material misstatements

when it is still contains material misstatements. Audit failure is one of the causes of the recent

financial scandals. Financial scandals like Enron, WorldCom, Ahold and Vestia had a huge negative

impact on the public confidence in the security markets. The involvement of public auditors in these

incidents creates both by the regulators and by the public concerns about the audit quality.

6

In response to the financial scandals of Enron and WorldCom, the U.S. government in 2002 passed the

Sarbanes-Oxley Act (SOx) with enhanced standards introduced to restore the confidence in the

security market. One essential implementation of SOx is included in Section 404 (hereafter: SOx 404):

Issuers are required to publish information in their annual reports concerning the scope and adequacy of the internal control structure and procedures for financial reporting. This statement shall also assess the effectiveness of such internal controls and procedures.

The registered accounting firm shall, in the same report, attest to and report on the assessment on the effectiveness of the internal control structure and procedures for financial reporting.

The main interpretation of SOx 404 is the requirement of the corporate managers and the public

auditors to report on the adequacy of the company’s internal control. Managers, as a part of the annual

report, are required to publish an internal control report and the public auditors need to express their

opinions about the effectiveness of the internal control structure of the firm. Consequently, in order to

assess a firm’s internal control, public auditors have to be equipped with even more specific

knowledge which enables them to have a better understanding about the firm and its industry.

Concerning some industries, performing a high quality audit only have audit procedure knowledge is

not sufficient. Due to the complexity of an industry, to judge the line items in the annual financial

statement it requires more specific knowledge. Typical operations within an industry or the

decentralization of operations to complete the audit would require significant more efforts from the

public auditors (Hay, Knechel, & Wong, 2006). For instance, it is well-known that the pharmaceutical

industry requires a high research and development intensity. Statement of Financial Accounting

Standards 2 suggested that ‘All research and development costs encompassed by this Statement shall

be charged to expense when incurred’. However, International Accounting Standard 38 ‘Intangible

Assets’ allows companies to capitalize development costs when it is able to produce probable future

economic benefits under certain criteria. Consequently, in order to judge whether the expectation of a

company is justified it requires the public auditors having a large amount of industry specific

knowledge. If auditors are not educated in judging the company’s expectation, for the evaluation to

maintain the level of the audit quality a third party should be involved. Alternatively, if public auditors

in this industry are specialized, they would perform this audit in a more efficiently way. Consequently,

to a certain extent, the complexity of an audit engagement relies on the specialization of the public

auditors.

When a group of public auditors are more specialized than the other, it is not surprising that the

charged fees are different as well. As signaled before, the audit fee is the compensation paid by firms

for the audit effort by the public auditors. A problem with the determination of audit fee is that no

clear guideline exists to follow. Concerning the determination of the audit fee, academicians have

7

developed a theoretical model. This model separated the fee into two components: audit production

and the present value of potential future costs associated with the current audit (Simunic, 1980). The

audit production is a function of the audit hours and the audit cost per hour. Concerning the specialists,

because they have an extra amount of knowledge to improve the efficiency of the audit the assumption

is that the needed audit hours are less than non-industry specialists. However, to compensate their

training investment specialists charge a higher fee per hour. Consequently, not is known whether an

increase in the specialization to ease the industry complexity could create an increase or decrease in

the audit fee.

Consequently, in improving the efficiency of an audit engagement particularly within relatively

complex industries, it is essential to realize that specialization can be highly valuable. Specialized

industry knowledge helps the public auditors ease the complexity of an audit and reduce their effort in

the audit production. Because it is not clear whether audit clients pay a fee premium for the audit

specialist, this thesis will investigate the correlated effect of specialization, generated to ease industry

complexity, on the audit fee.

1.2 Relevance

Audit fee is mostly determined prior an audit engagement. At the time of contracting, public auditors

should estimate the nature and the magnitude of the evidence needed to mitigate the uncertainty of an

audit failure. In the U.S, public firms report the expenses paid for auditing their financial statement in

their annual reports. However, it is still unclear what factors were used to determine the level of audit

fee. Besides, the determinants of the audit fee are not clear-cut in addition due to the corresponding

duty of the professional confidentiality within the public audit profession. Because of this feature, a

number of researches have been performed to determine what factors are systematically associated

with the audit fee.

Among the studies conducted, researchers confirmed that several factors with the audit fee are

systematically correlated. For instance, audit client size, complexity, the public auditor’s size, brand

names and specialization all showed a significant impact on the audit fee (Hay et al., 2006).

Complexity and specialization are both confirmed to be positively associated with the audit fee. In

prior researches, the proxy for complexity is mostly the number of subsidiaries (Hay et al., 2006). It is

suggested that subsidiaries would increase the complexities of transactions and consequently requires

more audit effort. However, this measurement of complexity is not associated with a particular

industry. A limitation of this approach is that it assumes that the complexity among industries is equal.

Since the complexity in addition varies due to the nature of an industry, this could create biased

results. The contribution of this thesis is an alternative way to measure the complexity. In addition,

when an industry is complex due to its required specialized knowledge, this complexity term becomes

8

a subjective matter. Additional tests in this thesis are going to investigate whether specialization could

influence the positive association of the complexity and the audit fee.

The approach is that the complexity of an audit due to the industry characteristics is subjective. The

level of complexity would decrease if public auditors do have industry specific knowledge comparing

with public auditors who do not have this knowledge. Specialized public auditors in addition are able

to perform the audit differently than non-specialists do. Consequently, the difference in audit effort

could cause a difference in the audit fee.

1.3 Objective

The purpose of this thesis is to determine whether specialization influences the correlation between the

complexity and the audit fee, if so, in which direction. As signaled in the previous section, the public

auditor’s specialization could be useful for certain complex industries. However, not is known whether

this amount of specialization could create an increase or a decrease in the audit fee.

Alternatively, because it serves as a cost concerning the public audit firms for training and educating

their staffs the audit fee may increase. Consequently, they may charge a specialist premium to

compensate these expenses. Besides, these specialized public auditors are more likely to provide

services in their specialized industry consequently acquiring expertise due to hands-on experiences.

Eventually, they may become the only provider of the high quality audit services within a particular

industry thereby enjoying a monopolistic position and provides it price-setting power which in

addition creates an increase in audit fee. Alternatively, when a public audit firm owns a large amount

of market share, the training costs can be spread to more clients. Since the non-specialists are facing

higher costs, at the same time, they are able to keep increasing their market share. Consequently, the

audit firm achieves economies of scales within this certain industry. To keep its competitive position

among other public audit firms it will reduce its audit fee eventually.

The results in this thesis would be useful for several groups. First, an alternative approach will use to

measure a firm’s complexity. This approach assumes that industry characteristics would increase the

complexity of a specific firm. This alternative measurement could create different implications for

prior researches. Second, to understand the development of their audit fee the outcome of the thesis

could be useful for corporate managers. Third, the audit firms could use the results as a suggestion to

whether or not develop a differentiation strategy with specialization.

The main purpose of this thesis is to provide researchers, auditors and audit clients more insights in the

determination of the audit fee.

9

1.4 Research question

In this study, the next research question will be answered:

Does the public auditor’s industry specialization influence the association between the audit fee and

the audit client complexity?

In order to provide thorough understanding of this topic, the next sub questions will be answered:

1. What is the function of the public auditor?

2. What is the content of the term client complexity?

3. What is the content of the term auditors industry specialization?

4. Why does the complexity drive up the audit fee?

5. Is auditor’s specialization really needed to perform an audit?

6. Is the audit fee for complex industry higher than for others?

1.5 Methodology

The level of the complexity would be measured as a dummy variable. Companies from a complex

industry received 1, otherwise 0. The level of specialization is measured as percentage of an industry

that is audited by a particular public audit firm; the audit firm with the market share of 15% or more

will be recognized as specialist.

Firstly, to ascertain that the audit fee is higher for complex industries, the audit fee for complex

industries and regular industries will be compared. Secondly, a test will be performed to assess

whether companies who used industry specialists are significantly paying more fee than

nonspecialists. Finally a regression test will perform with the audit fee as independent variable, the

complexity as dependent variable and the specialization as moderating variable.

During the research, other variables that could be a driver of the audit fee will be controlled. These

variables are: audit client size measured by total assets and total turnover, business risk as the

combination of certain financial ratios, geographical dispersion and previous auditor’s opinion.

1.6 Demarcation and Limitation

The sample is selected from the U.S. Audit Analysis database and Compustat; the results may

consequently be insignificant for other regions. Additionally, the audit fee data is only available for

public companies; the relation may only appear for public companies instead of all companies

including private companies. In addition, due to the availability of the data the time period is selected

after 2001. However, the implementation of SOx could drive up the audit fee.

10

The measurement of auditor specialization has its limitations as well. The specialization is measured at

the national level. Since it could be that one local office is much more specialized in a specific

industry than the other establishment from the same audit firm, this could create biased results The

reason behind this could be that due to the geographical locations of clients, it is more efficient to set

up a specialized office nearby the client. When measured at the national level, only the aggregated

specialization is taken into account.

1.7 Structure

Chapter 2 describes the theoretical backgrounds of the main concepts used in this thesis. The

theoretical background includes the role of the public auditor, the audit client complexity, the auditor’s

industry specialization and the confirmed determinants of the audit fee. The concepts will be explained

and their theoretical association will be presented.

Chapter 3 concentrated on the prior researches conducted in this topic. The most influential papers in

this topic will be presented. The thesis is mainly an extension of these papers. In addition in this

chapter the hypotheses will be developed.

Chapter 4 describes the research design and the sample selection. The research design mainly includes

the model construction and the way to measure the selected variables. Additionally, a description will

be given in which manner the sample was obtained.

Chapter 5 will analyze the results obtained from the sampling. This chapter focuses on the findings of

the results and to test the hypotheses.

Chapter 6 will present a summary of the thesis and the main conclusion derived from the results. And

the limitations and the suggestions will be given.

11

2. Theoretical Background

2.1 Introduction

In order to have a better understanding concerning the research question this chapter mainly aims at

introducing the theoretical frameworks used in this thesis. To clarify the role of public auditors

particularly to capital providers, the rise of the public audit profession will first be analyzed from the

perspective of the agency theory. This is fundamental for understanding the origination of the audit

fee. Besides, a brief description of the certified public auditing accounting firms will be presented

which is followed by a short description of the current audit market domination by the Big4 firms.

Since the Big4 firms are able to deliver high quality audits which are appreciated by most of the

clients, the level of audit fees may be not determined solely from a price competition. More

specifically, a differentiation strategy in specialization provides audit firms opportunities to increase

the fee. Finally y, the determination of audit fee is revealed from an academic view: the audit pricing

model of Simunic (1980). Based on this model, determinants of interests for this thesis will be

explained. These are the client size, the client business risks, the client complexity and the auditor

specialization.

2.2 Agency Theory

The agency theory is raised based on principal-agent relationship. The principal-agent relationship is a

widely applied theory. This thesis focuses only on the effects on stock exchange quoted companies.

As what the name suggested, the principal-agent relationship exists between two parties: the principal

and the agent of the principals. Concerning stock exchange quoted companies, the agent is the board

of management and the principals are shareholders who are the actual owners of the company. Agents

are recruited to represent the principals and perform on the principals’ behalf. Since the managers are

the leaders of the company, they, as agents, have more superior information than the actual owners

have. To a large extent, the revenue for the shareholders is dependent on the performance of the

managers. However, it happens quite frequently that managers have conflicting objectives and/or goals

than the shareholders have.

2.2.1 Information Asymmetry and Agency Costs

The main objective for the shareholders is to maximize their revenue. This could be achieved by hiring

managers with great managerial capacity. A company’s performance can be largely dependent on the

talents of the managers. Motivated managers with good management skills and rich experiences help

to increase the revenue for shareholders and maximize the company’s profit.

12

However, managers often have their own objectives that are different from the ones of the

shareholders and due to the information asymmetry they have the ability to act for their own interest.

When doing so, the shareholders’ value is not maximized. For instance, in order to enable shareholders

to receive more dividends, it is managers’ task to maximize the net income. However, academic

economic literature showed evidence that managers are only likely to increase the company’s net

income when their compensation will increase as well (Healy, 1985).

For shareholders, due to the information asymmetry between he managers and the shareholders in

general it is difficult to determine whether or not the managers are acting in their own interests.

Concerning the shareholders, several sources of information exist to obtain information of their

company. The most important information source remains the financial statements, which consist of a

balance sheet, income statement, cash flow statement and statement of owner’s equity. The purpose of

publishing financial statements is to present to the stakeholders the company’s financial information as

clearly and precisely as possible. The most important group of stakeholders is the company’s creditors

and the shareholders. They support the company by providing capitals and receive interests or

dividends as returns. Not surprisingly, to this group of capital providers it is essential to evaluate a

company’s potential to achieve its objectives and repay them in the future. When a company through

its financial statements communicates unreliable information, for capital providers it becomes even

more difficult to obtain real information. In that case they have to acquire reliable information on their

own. Consequently, they may require more return on their capital, which can be qualified as an

expenditure arisen from the agent-principal relation, and consequently increase the company’s

expenditures. This in turn will decrease a company’s ability to attract more capital and achieve its

objectives.

By providing reliable information by the company, because they do not need to acquire reliable

information on their own, the capital providers will use the presented information in full extend, which

could lower the required return. Additionally, regulators have established divers accounting guidelines

to improve the reliability of the published financial statements. Consequently, all published financial

statements have to adhere to standard guidelines provided like the General Accepted Accounting

Principles (GAAP) or the International Financial Reporting Standards (IFRS). To maintain the quality

of the published financial statements like has been signaled in the introduction chapter, regulators of

these standards are constantly updating their rules.

2.2.2 Financial Statements Audit and the Costs

As signaled before, it is crucial that the reported information on the financial statements are reliable

and accurately concerning the companies’ financial position. This is exactly the responsibility of the

13

public auditors: to ensure with reasonable assurance that a company’s financial statements present its

financial position in a true and fair view. It is commonly accepted and proved by researches that the

auditors’ name reputation (e.g. Big 4) is positively associated with the audit quality (Becker, DeFond,

Jiambalvo, & Subramanyam, 1998; Francis & Yu, 2009).

Companies invite public auditors to investigate their financial statements and in compensation pay

them the audit fees. It is essential to note that, even though the audit fee for the companies remains as

an expense the major concern when choosing an auditor (firm) is still the quality according to what is

suggested in the agent-principle theory. In other words, the amount of audit fee is not the main focus

of the company. Since it states that the level of the audit fee is not fully determined by a price

competition among audit firms, this assumption is crucial in this thesis. Suppose it was the case, the

main driver for the audit fee would be the competiveness within the audit industry, which would

decrease the validity of the determinants that in the academic literature are relevant to investigate the

audit fee.

2.3 The Role of the Public Auditor

This thesis is about financial statement auditing, consequently the definitions in n this paragraph are

applied for the financial statements audits.

2.3.1 Audit Services

2.3.1.1 Nature of Auditing

Arens et al., (2013, p.4) defines auditing as “the accumulation and evaluation of evidence about

information to determine and report on the degree of correspondence between the information and

established criteria”. In this definition two key terms exist: information and established criteria. To

ascertain the reported information is in accordance with the established criteria, auditors need to

collect evidence. The information that is being audited can be quantifiable information (e.g. financial

statements numbers) or qualified information (e.g. the efficiency of a firm’s operation). Based on the

collected evidence, auditors should be able to draw a conclusion about the quality of the reported

information based on their understanding of the established criteria, in other words, whether the

company’s financial statements present its company’s financial position in a true and fair view. The

results of that investigation are included in the audit report with the auditor’s opinion. Concerning

public auditors it is essential to remain independent from their client even though an economic bond

exists between the auditors and their clients, which is the audit fee.

2.3.1.2 Auditor’s Responsibilities

The main responsibility of the public auditors can be described as

14

‘Obtain reasonable assurance about whether the financial statements as a whole are free from

material misstatements, whether due to fraud or error, thereby enabling the auditor to express an

opinion on whether the financial statements are presented fairly, in all material respects, in

accordance with an applicable financial reporting framework.’ (Arens et al., 2013, p144)

The level of assurance can be qualified as a level of certainty that auditors have upon completion of

an audit. Auditing standards requires auditors to have reasonable assurance instead of absolute

assurance. The main reason an absolute assurance is not applicable is that auditors are not issuers of

the published financial statements. Consequently, they are not able to provide fully assurance. In

order to provide a reasonable assurance, a certain amount of professional knowledge is required. For

instance, in order to draw conclusions about the correctness of an account, auditors often have to

investigate samples. The sample selection procedures and its sizes are fully dependent on the

judgment of the auditors. An inadequate decision concerning the sample increases the associated risk

of the presence of a material misstatement in the published financial statements. Besides, certain

industries often have to deal with complex estimations, which form the auditor requires certain

industrial knowledge. Consequently, in order to realize a correct judgment auditors are required to

have a well-educated background.

2.3.2 Certified Public Accounting Firms

A certified public accounting firm (CPA firm) provides assurance and attestation services. Audit

services belong to the assurance services and are mostly the core business activities concerning a CPA

firms.

Concerning the most CPA firms, the organizational structure is Limited Liability Partnership (LLP),

which states that the firm is owned by one or more partners. The advantage of this organizational

structure is that partners are only personally liable for debt and obligations of their own acts and not

for the liabilities arising from other partners.

In the U.S., financial statements audits of all general companies are performed by CPA firms. In 2012,

in the US more than 45000 CPA firms exists with a range in size from 1 to 40000 staff (Arens et al.,

2013). In general, audit firms are categorized based on their revenue. The categories are: Big 4,

National, Regional and Large Local (Arens et al., 2013). Concerning this thesis, due to the availability

of data, the audit fee and the auditor’s specialization are mainly derived from Big4 CPA firms.

2.3.3 The BIG 4 Network and Its Impact

15

Currently, the audit market is predominant by the Big 4 firms. This has raised a much concerns about

the competition within the market which would in turn influences the audit quality. Consequently, in

order to maintain the audit quality, regulators have enhanced/set new regulations. For instance, audit

independence rules are set to limit the audit firms to provide other services to its audit client. Although

the intention of these rules is to maintain and improve the audit quality, they could potentially reduce

the number of available CPA firms for a client to choose from. Concerning companies that demand

high quality auditing services from Big4 firms, the limited choices available could create a lower

bargaining power (Porter, 1979). Consequently, the CPA firms may ask a higher compensation for

their audit effort. Consequently, a less competitive audit market increases the audit fee.

2.4 Audit fee

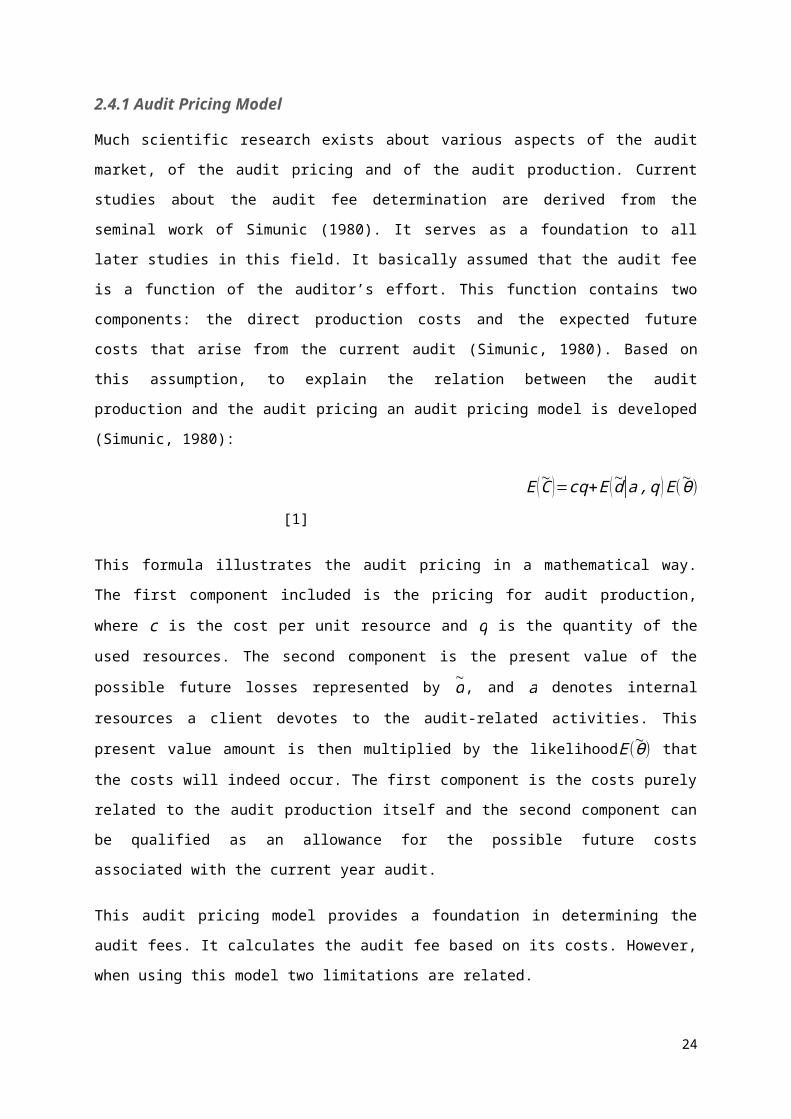

2.4.1 Audit Pricing Model

Much scientific research exists about various aspects of the audit market, of the audit pricing and of

the audit production. Current studies about the audit fee determination are derived from the seminal

work of Simunic (1980). It serves as a foundation to all later studies in this field. It basically assumed

that the audit fee is a function of the auditor’s effort. This function contains two components: the

direct production costs and the expected future costs that arise from the current audit (Simunic, 1980).

Based on this assumption, to explain the relation between the audit production and the audit pricing an

audit pricing model is developed (Simunic, 1980):

E (~C )=cq+E (~d|a , q ) E (~Ɵ)

[1]

This formula illustrates the audit pricing in a mathematical way. The first component included is the

pricing for audit production, where c is the cost per unit resource and q is the quantity of the used

resources. The second component is the present value of the possible future losses represented by ~d,

and a denotes internal resources a client devotes to the audit-related activities. This present value

amount is then multiplied by the likelihoodE(~Ɵ) that the costs will indeed occur. The first component

is the costs purely related to the audit production itself and the second component can be qualified as

an allowance for the possible future costs associated with the current year audit.

This audit pricing model provides a foundation in determining the audit fees. It calculates the audit fee

based on its costs. However, when using this model two limitations are related.

1) The cq part is only valid to predict the costs for the audit production if the audit quality of the

conducted audits performed would be at the same level as the assumed quality of the audit. This

assumed audit quality is mostly associated with the brand name of the audit firm. If it is not the

16

scenario, cost per unit resource is not able to capture the unit cost in a reliable way. Besides, the

E (~d|a ,q ) E(~Ɵ) part in addition would predict a wrong value if the perceived audit quality is not

the same as the assumed audit quality.

2) In order to determine the right amount of per unit cost the audit market should be competitive. If

the audit market is formed by monopolistic market players, they are able to ignore the pressure

from the competitors and consequently present to them the price-setting power.

These two limitations were confirmed by later researches. The quality of an audit can be affected by

many factors. It is nearly impossible for an audit firm to perform every audits at the same quality level

as assumed by their brand name (Francis, 2004). Besides, the audit market is predominating by the

Big4 accounting firms. The large market share would reduce the impact of a competitive market on

the audit fee. Consequently, a priori reasoning exists to believe that the audit costs model provided a

valid and reliable framework to predict the audit fee Simunic (1980). However, in practice it is

inappropriate.

Consequently, Simunic (1980) and other researchers had to found several factors that would

systematically influence the audit fee. They have chosen to link some client characteristics directly to

the audit fee and found that a certain amount of client characteristics are effective proxies to determine

the audit fee (Hay et al., 2006). Besides, researchers in addition found that auditor characteristics and

engagement attributes could influence the audit fee (Hay et al., 2006). Essentially, since these

characteristics would affect the audit fee either by the total audit hours or the audit cost per hour, the

audit pricing model by researchers is still used as a foundation to determinate the drivers for the audit

fees.

2.5 The Determinants of the Audit Fee

Several client characteristics exist that could influence the audit fee. Since they have a direct

association with the audit effort and the audit engagement risk, which will increase the total audit

hours, these determinants are essential. The most important characteristics are presented in the next

paragraphs.

2.5.1 Client Size

In determining the audit fee, the audit client size by far was confirmed to be one of the most

significant explanatory variables (Hay et al., 2006). The reason behind this is that in order to mitigate

the increased audit risk larger clients typically require more effort from the auditors. Based on this

argue, the audit fee per hour would remain at the same level regardless the size of the auditees. In the

17

study conducted by O’Keefe, Simunic, & Stein (1994) for investigating CPA firm’s use of different

grade of professionals and various client characteristics, they have found clear evidence that the audit

effort and the client size has a concave relation. The explanation for this concave relationship is that

the use of a relatively larger proportion of low-level professional auditors, consequently the

inexpensive personnel costs would create a little increase in the audit fee. However, the total audit

hours is still increasing with the size of the client which will create an increase in the audit fee.

The size of an auditee firm can be measured by multiple ways. The most used proxy is the amount of

the total asset (Hay et al., 2006). Another widely used variable is total sales. Because the lawsuits

against the auditors mostly arise from improper valuations, the amount of the total assets in addition

has consequences on the responsibilities of the auditors. Consequently, a firm with larger assets

requires more efforts from the auditors, consequently possessing a higher audit fee.

2.5.2 Client Business Risk

Besides the company size, business risk in addition is one of the major factors affecting the audit fee.

For instance, when a company endured financial losses a higher possibility will exists of bankruptcy,

which in turn creates a larger possibility of legal actions against the client and in addition against the

auditor. To prevent such a situation from happening, auditors have to perform more effort to mitigate

the risk and to avoid any lawsuits in the future (Arens et al., 2013). Francis & Simon (1987) found a

positive correlation between the audit risk and the audit fee. A survey study conducted by Bell et al.

(2001) further confirmed that such a correlation was caused by the related audit hours.

The client business risk can be measure in two ways, namely operational risk or financial risk. The

most used proxies to measure business risk are financial ratios to measure a company’s ability to pay

off its debt.

2.5.3 Client Complexity

Audit client complexity in addition could affect the audit fee. Since auditors need to have a good

understanding of their client’s company in order to develop an appropriate audit strategy (Arens et al.,

2013), complex clients would requires more efforts from auditors to fully understand their business

operations than less complex clients. In other words, the more complex a client, the more time-

consuming the audit procedure would be that could create a higher audit fee. Existing scientific

literature showed a positive correlation between the audit client complexity and the audit fee (Hay et

al., 2006).

18

The most used measurement for client complexity is the number of subsidiaries that a firm locally and

internationally owns. The argument for this proxy is that if a firm is complex, it in addition has more

diversified operations. Sandra & Patrick (1996) showed that auditors are likely to charge a higher fee

for complex clients. They have examined the Hong Kong audit market, and found that a company that

has more foreign subsidiaries is facing a variety of legislative requirements of disclosures.

Consequently, this requires more audit testing than companies with less foreign subsidiaries. When

more audit testing is needed, audit firms would add more manpower to complete the audit

engagement, which implies that the clients have to pay an additional charge for the audit engagement

(Simunic, 1980).

A company’s complexity is mostly due to its business, which is industrial specific. Consequently,

instead of the number of subsidiaries, the industry sector is another way of specifying company

complexity. Craswell & Taylor (1991) followed this method, examined the correlation between the

complexity of audit clients and the corresponding audit fees. They classified all companies into the

following groups

(1) natural resources, which have unique accounting problems with respect to the valuation of

mineral/oil reserves, income determination, and complex forward sales and hedging contracts;

(2) building suppliers and engineering firms, both of which are involved in multi-period

contracting which creates special accounting problems relating to cost capitalization and

income recognition;

(3) retailers, which have elaborate inventory systems and special revenue recognition issues

associated with sales returns and various types of customer financing and

(4) investment and financial services, which have complex contracts for financial instruments and

derivatives, large-scale EDP systems, and special regulatory accounting requirements.

This classification was based on the industry-level measurements of the systematic risk and the total

risk. In addition, Craswell, Francis, & Taylor (1995) used a similar classification for the complexity

and found that specialized auditors charge the complex clients a fee premium of 18% on average than

less complex industries.

2.5.4 Auditor Specialization

Based on the Porter's (1985) competitive strategy, an audit firm may choose for a differentiation

strategy to gain a sustainable competitive advantage over its competitors. For audit firms, one way to

achieve a competitive advantage is to obtain specializations in particular industries. This strategy is

used by many audit firms aiming to attract more clients (Mayhew & Wilkins, 2003). Because they

19

believe it increases the audit quality indeed this is appreciated by the audit clients (Klein & Leffler,

1981; Low, 2004; Owhoso, Messier, & Lynch, 2002).

The choice and the ability for audit firms to apply the specialization strategy is dependent on the type

of industry (Cahan, Godfrey, Hamilton, & Jeter, 2008; Cairney & Young, 2006). Cahan et al. (2008)

assert that the key driver for firms performing such a choice is the industry specific investment

opportunity. They showed that exploiting investment opportunity requires industry specific

knowledge, which an auditor may increase his competitive position.

Specialization in a particular industry enables a firm to increase its bargaining power against its

current and potential audit clients and in addition increases the premium charged comparing to their

less specialized competitors (Klein & Leffler, 1981; Porter, 1979). Besides, a specialized audit could

enjoy an increase in its reputation (DeAngelo, 1981), which permits them possessing a more

competitive advantage position and consequently increases its power, allowing them to charge a

higher premium. On the other hand, specialized auditors are able to work more efficiently and in

addition reduce the working hour needed. In addition, it is easier for them to achieve economic of

scales particularly in their specialized industry. Consequently, increased specialization in specific

industries may reduce a firm’s cost and provide the possibility of discounts in charging the audit fee

(Cairney & Young, 2006; Eichenseher & Danos, 1981). Summarizing, industry specialists have the

incentive and the ability to charge either a fee premium or discounts.

2.6 Summary

In the introduction of this thesis, several questions were formulated to provide a better understanding

of this thesis. This chapter has answered the first four questions. A brief summary of the answers is

provided below.

1. What is the function of a public auditor?

The role of a public auditor is to provide reasonable assurance that the published financial statements

of a company are free of material misstatements. Since an important group of financial statements

users is capital providers of the company, this is essential concerning the effectiveness of the capital

market.

2. What is the content of the term client complexity?

Client complexity can be qualified as an attribute from clients’ side to influence the audit fee.

Typically, client complexity is measured using the number of subsidiaries. Since the complexity

creates a more time-consuming audit, auditors usually charge a higher fee for complex clients.

20

In this thesis, client complexity will be measured based on the industry characteristics, which can be

implemented that some industries are systematically more difficult to audit than other industries.

3. What is the content of the term auditors’ industry specialization?

In order to increase its competitive position, audit firms can choose for a differentiation strategy.

Auditors’ specialization is one way to achieve it. When an auditor is specialized in a particular

industry, it will gain the ability to charge either a fee premium or discounts.

It is essential to note that this specialization is not mandatory in completing an audit engagement.

4. Why does the complexity will drive up the audit fee?

Because auditors need to spend more time to have a good understanding of the business, basically, a

complex company requires more efforts from the auditors. This process is essential concerning the

development of the audit strategy. Consequently, to compensate their efforts due to the complexity,

auditors will charge a fee premium.

21

3. Prior Research

3.1 Introduction

This thesis investigates the influence of the auditor’s industry specialization on the audit fee among

listed firms in the United States of America (U.S). In order to have a better understanding of the topic

in this chapter the determinants of the audit fee will be analyzed. Consequently, this will provide a

context in which the results of this thesis can be referred.

In this chapter, seven academic articles published during 1986 up to and included 2013 in great detail

will be presented. These articles possess either comparable research objective or methodology with

this thesis. By comparing with previous studies, it provides the possibility to explanation the

implications of the results in this thesis. A short summary of all articles is provided in appendix 1.

Simunic (1980) suggested investigating the direct determinants that significantly influences the audit

fee. This approach was applauded by researchers and services as the foundation concerning the study

of the audit fee. The next passage summarizes in which way this was applied in most audit fee studies.

“Typically, an estimation model is developed by regressing fees against a variety of measures

surrogating for attributes that are hypothesized to relate to audit fees, either negatively or positively”

(Hay et al., 2006, p. 146). This was illustrated in the next equation:

ln f i=b0+b1 ln A i+∑ bk gik+∑ be g ie+e i [2]

WhereLn fi = the audit fee (natural log)b0 = the interceptbn = the coefficientsLn Ai = the audit client size measure (natural log)ei = the error term

The other two groups of variables gik and gie are the potential fee drivers to be tested. All the articles

which will be presented in this chapter in their researches have used this.

3.2 Common Determinants of Audit Fee

3.2.1 Audit Client Size

Based on the audit pricing model, the audit client size is considered as the most important influential

factor on the audit fee. In fact, to ensure the validity of the results in the audit fee regression it is

22

always included as a control variable. In this section, two major articles studying the effect of the

client size on audit fees will be presented.

3.2.1.1 Palmrose (1986)

This paper by Palmrose (1986) was one of the earliest studies in the audit fee determinants. The main

research objective of Palmrose’s study was to detect whether the auditor’s size has a systematically

correlation with the audit fee. Additionally, Palmrose believes that a large sized client requires more

audit procedure and the increased audit effort would push up the audit fee to a higher level.

To test the assumption the study adopted a regression analysis. In this regression equation, the

dependent variable was the audit fee and the independent variables contain the client size, the number

of reports, the number of the audit locations, and the percentage reduction in the fees from the auditee

inputs, the ownership indicator variable, the report modification indicator, the industry specialist

indicator and the client industry indicator. However, the author did not specifically emphasize the

hypotheses in this paper.

The data was obtained from questionnaires which aimed at individuals ‘who were considered most

likely to be knowledgeable about the services of the public accounting firms’ (Palmrose, 1986, p.

102). The questionnaires were delivered to 1186 domestic public and non-public companies in the

U.S. during early November and mid-December 1981. Overall, there were 361 usable responses, at a

response rate of 30%, which is similar to the other survey studies performed regarding to audit fee

(Miller, 1978; Simunic, 1980).

The term LnAssets had a coefficient of .470 which was significant at α = .01. Among the independent

variables, the major explanatory variable in the pricing of the audit fee was the clients’ assets. This

result is in conformity with the prediction that the size of the audit client is significant positively

correlated with the audit fee.

3.2.1.2 Carson & Fargher (2007)

This study examined whether larger clients are charged with a higher fee. Their intuition was that

larger clients usually require more specialists to complete an audit engagement. Consequently, since

previous studies have showed that a specialization increases the premium charged (Ferguson, Francis,

& Stokes, 2003), increase the audit fee. Consequently, they expected that, to compensate the auditor’s

specialization, large clients would pay more audit fee. In this paper no hypotheses are signaled.

23

The data was collected based on the audit engagements performed in the year 1998, 1999 and in 2004

in Australia. The data from 1998 were used to test the research question. Since Price Waterhouse

Coopers and Lybrand merged in late 1997, which could potentially impacts their reputation and

pricing, the data from 1999 and 2004 was used as sensitivity analysis. The samples of 1998 and of

1999 were drawn from the Who Audits Australia database. This database contains the fees for audit

services and for non-audit services of the Australian listed companies. In addition, the sample

concerning 2004 was drawn from the University of New South Wales audit fee database.

The finding of this study showed that the clients located in the upper quintiles regarding to firm size

requires a significant higher audit fee. One explanation presented by the authors was that since their

auditors are designated the industry specialist larger clients are charged with a higher fee.

Consequently, the result was in conformity with the prediction that the audit fees are positively

correlated with the audit client size.

3.2.2 Auditors’ Business Risk

When determining the amount of audit fee, auditors should take the behavior of their client into

consideration. For instance, clients might be tempted to perform risky conducts to achieve their

objectives. These acts might create a wrong estimation of the accounting numbers. Since it is the

auditors’ responsibility to ensure that the annual financial statements are free of material

misstatements, risky conducts may increase the audit risk of the auditors. Consequently, auditors

would ask a compensation for the potential work needed to mitigate the audit risk. A number of

researches have examined whether a risky conduct of the audit clients could create a higher audit fee

(Bell et al., 2001; O’Keefe et al., 1994; Seetharaman, Gul, & Lynn, 2002). Since no consistent

measure exists of the term business risk, the results until now are mixed. In general, two possible

business risks exist which may affect the auditors. One is the current business risk that could cause

potential legal actions against the auditors in the future. For instance, auditors of risky clients face a

higher possibility of liability payments. However, a problem with this approach is that not a common

way exists to measure this possibility. Researchers exist who used a survey study to directly obtain the

auditors’ opinion about the influence of their perceived business risk on the audit fee (Bell et al.,

2001). The other possible business risk arises from misconducts that are not by definition illegal.

Based on the U.S. law those misconducts are totally legal and will not result in a misstated financial

statement (Lyon & Maher, 2005). However, they could harm the reputation of the audit firm

consequently decreases its attractiveness to existing and potential clients. To measure this type of

business risk researchers mostly use financial ratios (Seetharaman et al., 2002). In this section, based

on existing researches both types will be signaled.

24

3.2.2.1 Seetharaman, Gul and Lynn (2002)

Seetharaman, Gul and Lynn studied the effect of the litigation risks of auditors on the audit fee. They

assume that auditors would be in serious trouble if they underestimate their legal liability exposure.

Legal actions against auditors do not only create liability payments, it represents the poor quality of

the services (Palmrose, 1988). Litigation claims would reduce an audit firm’s reputation which could

cause current or potential clients leave the audit firm. Consequently,

“the threat from litigation makes it incumbent upon auditors to continually assess their exposure to

lawsuits and to incorporate that assessment into the planning and pricing of audit services”

(Seetharaman et al., 2002, p. 92).

A reason exists to assume that auditors will charge a premium for the potential consequences of the

client’s litigation risk. The authors have not specifically formulated any hypotheses.

As a proxy to measure the auditors’ litigation risks, Seetharaman et al. chose to use the number of

legal environments in which audit clients are operating. .With the increase of the legal environments,

the company faces variant financial reporting standards, which increases the possible litigation

exposure. For instance, the “antifraud provision of the Securities Exchange Act of 1934 have a

transnational jurisdiction applied, in particular, to non-US auditors (Seetharaman et al., 2002, p. 92).

In other words, when Non-US companies are willing to issue equity in the US stock exchanges, they

are exposed to the liabilities based on the American securities laws. Consequently, it is expected that if

the clients are facing different legal environments an increase in the audit fee exists.

In order to test the hypotheses stated before, the authors used a regression model to examine whether

the auditors of U.K. firms charge a fee premium for their clients accessing the U.S. capital markets.

The data used in this study was obtained from the Financial Times Extel Company Analysis database,

the Bank of New York ADR database and the Disclosure’s Global Access database. After excluding

banks concerning the period 1996 up to and included 1998 they collected in total 3666 observations.

The results of the study showed that the UK auditors indeed charge a higher fee when their non-US

oriented clients have accessed the American market. However, it is worth noting that the measure of

the business risk used in this study is similar to the complexity measures in other audit fee studies,

namely the number of subsidiaries. The only difference is that the subsidiaries used in this study have

to face different legal environments. Consequently, it cannot be determined whether the increase in the

audit fee is due to the complexity, e.g. number of subsidiaries, or due of the different legal

environments.

25

3.2.2.2 Lyon and Maher (2005)

Lyon & Maher (2005) studied another type of business risk: the legal misconducts and its association

with the audit fee. As a proxy for the client misconduct, they employed clients’ bribery payments to

high level government officials. A company bribes governmental officials to achieve its own business

objectives. In a country where bribery is common, companies have to follow the rule of the game no

matter whether they are willing too. Based on a legal perspective, in 1974 in the U.S. bribery

payments were not illegal In fact, the SEC included a voluntary disclose program to request companies

to report their questionable payments to the governmental officials. Consequently, nearly 200

companies did report their bribery payments which are mostly paid to government officials in

developing countries. Based on the financial reporting perspective, the act of paying these bribes was

not an accounting issue if the amount was reported correctly. Hence, since bribery did not create any

misstatements auditors have the choice to accept this item. However, the bribery scandals attract

widespread media attention and may harm the reputation of the audit firm. To cover themselves in this

situation, auditors may need to spare more efforts in their audit to ensure their opinions about the

company are correct. This consequently will drive up the audit fee.

The authors developed the next hypothesis to test their assumption:

Hypothesis 1

To clients who pay bribes to foreign government official’s auditors charge higher fees than to clients

who do not pay bribes to foreign government officials.

To test the hypothesis a cross-sectional audit fee regression model was employed. A dummy variable

was introduced which is equal to 1 if the company did report bribery, otherwise 0. Besides generally

used control variables including clients’ size, audit complexity and auditor-client risk sharing, several

variables in addition that are correlated with bribe and might directly affect the cost of an audit are

included. These are geographical dispersion, percentage of assets in developing countries and

corruption index.

Data from 82 companies registered with the SEC were obtained from the Paton Accounting Center at

the University of Michigan, SEC 10-K reports, Moody’s, and Compustat in 1974.

The results showed that auditors, even though the misconduct is not illegal and does not cause any

financial misstatements, do allege corporate misconduct as risky business, and ask a higher audit fee.

3.3 Audit Client Complexity

26

Among the signaled determinants before, researchers in addition expect that audit client complexity is

correlated with the audit fee. The reason is that a complex client to complete the audit procedures

concerning the auditor will be more time-consuming (Hackenbrack & Knechel, 1997; Simunic, 1980).

Consequently, a complex client should be charged with a higher amount of audit fee. However, the

measurement of the client complexity across studies is different. In general, two streams of complexity

measure exist. On one hand, researchers assume that the client company structure can cause the

complexity. They used the number of subsidiaries as the proxy to represent it, a company with more

subsidiaries has decentralized operations and consequently is more complex concerning the audit (Hay

et al., 2006). On the other hand, researchers assume that complexity can be qualified as an industry

characteristic, which implies that some industries are more complex to the audit than others.

Consequently, to assess the complexity they used the Standard Industrial Classification (SIC) codes. In

the next section, two articles of each stream will be presented.

3.3.1 Sandra & Patrick (1996)

To have a better understanding of the components of the audit fee , Sandra & Patrick (1996) studied

the audit market in Hong Kong. Client complexity was one of their major interests, which was

measured by the number of subsidiaries. They believe that a company with more subsidiaries has more

diversified operations hence requiring more hours to complete the audit.

The authors in total formulated 10 hypotheses to confirm the audit fee drivers found in U.S. and in

U.K. studies in addition are valid to Hong Kong markets. Since the hypothesis 6 has been developed to

test the influence of the client complexity on the audit fee. This hypothesis will be given:

Hypotheses 6

Audit fee is positively associated with the number of principal subsidiaries in the group.

In order to test these hypotheses, the authors adopted a regression model with audit fee as the

dependent variable and several fee drivers as independent variables. Unfortunately, the authors in their

paper did not provide their regression equation.

The sample used concerns companies listed on the Stock Exchange of Hong Kong Limited from the

year 1992 and 1993. Since it is required for all listed companies in Hong Kong to disclose the amount

of auditors’ fee, the authors are able to obtain the data from the annual financial reports included in the

database Hong Kong City Hall Library. Companies were excluded if (1) no audit fee was disclosed,

some foreign companies are not required to report the audit fees; and (2) if they are from the banking

industry. Consequently, there were 313 companies for the year 1992 and 396 companies for year 1993,

which represent 76% and 83% of the population concerning the two years, respectively.

27

This study has proved that a significant correlation exists between the number of subsidiaries and the

audit fee required which suggests that the complexity in the audit pricing process is relevant.

3.3.2 Craswell, Francis and Taylor (1995)

One of the purposes of the study by Craswell, Francis and Taylor is to investigate whether the audit

specialization premium asked are industry-specific. Their motivation is that some industries require

different accounting technologies than other general industries. The accounting technology refers to a

company’s accounting system and the selection and the application of accounting policies to report

their activities.

“Crucial accounting policy issues concern the recognition and measurement of assets, liabilities, and

income arising from the firm’s economic activity. To the extent accounting technology is industry-

specific rather than generic, the firm’s agency/contracting problems and their method of resolution

via accounting will also have unique industry features” (Craswell et al., 1995, p. 300)

Based on that concerning the audit some industries are relatively more complex. When auditing in

these industries auditors need to have more industry specific knowledge. Hence, to compensate their

training and education investment they will charge a higher fee. The authors in total have developed

three hypotheses. The three hypotheses are formulated as followed:

Hypothesis 1

In those industries not having specialist auditors, Big 8 auditors will have higher audit fees than non-

Big 8 auditors.

Hypothesis 2

In industries having specialist auditors, non-specialist Big 8 auditors wilt have higher audit fees than

non-Big 8 auditors.

Hypothesis 3

In those industries having auditor specialists, specialist Big 8 auditors will have higher audit fees than

non-specialist Big 8 auditors.

The sample used in this study was hand-collected from the annual reports of 1484 companies listed on

the Australia Stock Exchange in the year 1987. The authors have classified 23 industry groups

whereby 9 of them are labeled as complex which require industry specialists to perform the audit. Out

of the 1484 listed companies 911 companies are regarded as complex.

28

The results showed that the auditors of complex industries in comparing with other general industries

indeed charge a premium.

3.4 Auditor Industry Specialization

Auditor industry specialization in the scientific auditing literature is considered as a major subject.

These specialists are important due to their contribution to a higher audit quality. For instance, an

experiment by Solomon, Shields, & Whittington (1999) showed that relative to other industries the

industry specialists have more accurate predictions of the potential financial statement errors in their

industries. In addition, industry specialized auditors are able to constrain the use of earnings

management and consequently increase the quality of the published earnings. Balsam, Krishnan, &

Yang (2003) found that companies that are audited by industry specialists have lower discretionary

accruals and a higher earnings response coefficient, which implies that the industry specialists are able

to improve the quality of the earnings. Additionally, Carcello & Nagy (2004) reported that a negative

correlation exists between the industry specialists and financial fraud. Based on the additional

trainings needed and the potential benefits of the specialized auditors, a reason exists to assume that

specialization would create a higher audit fee.

Although many researches on the auditors’ specialization exist, the definition and the designation of

the specialized auditors among the researchers are still not unified. Most researchers followed the

definition communicated by Palmrose (1986) which stated that the largest, the second and the third

largest suppliers can be qualified as specialists in each industry. This definition basically relies on the

within-industry market share approach which considered that an auditor is to be industry specialists if

he has a significant part of market share in that industry. An alternative approach is based on the

within-firm portfolio, which stated that an auditor can be qualified as a specialist for industries that

have the largest portfolio shares within the audit firm. The rationale behind this approach is that to an

audit firm, industry with the largest portfolio share generates the most revenues hence attracts the most

attention as well as efforts within the audit firm.

Moreover, in addition studies exist that provided evidence that auditor industry specialization does not

increase the audit fee. For instance, to improve their bargaining position audit firms are able to choose

for a differentiation strategy however, this does not necessarily creates higher audit fee. Casterella,

Francis, Lewis, & Walker (2004) provided explanation to this issue. Additionally, to increase the cost

efficiency, industry specialist are able to achieve economies of scale, which in turn could decrease the

audit fee (Bills, Jeter, & Stein, 2013).

3.4.1 Casterella, Francis, Lewis, & Walker (2004)

29

Casterella, Francis, Lewis, & Walker (2004) used Porter (1985) analysis of the competitive strategy to

understand an auditor’s choice of becoming industry specialists. They assessed industry specialization

as a differentiation strategy of audit firms which provides them sustainable competitive advantage

over other auditors; hence permit them a stronger bargaining position. However, because of their size

and the related revenues this bargaining power is much weaker particularly to large clients.

Consequently, large firms have a stronger influence in negotiating their audit fees. Hence, the authors

of this paper expected that small clients are more likely to pay a fee premium for industry specialists

than large clients.

The authors did not provide the development of the hypotheses. In order to test their assumption, they

adopted a regression model with audit fee as dependent variable and several fee drivers as independent

fee variables. Companies audited by Big 6 auditors and have a SIC code below 6000 excluding

financial institutions were selected and a survey questionnaire was sent in which were requested the

total audit fee, the auditor tenure, the number of subsidiaries and the comments of the nonrecurring

events that might influence the audit fee. At a usable response rate of 21%, information from 651

companies was collected. In addition, auditors with 20 percent or more market share within an

industry are labeled as industry specialist and clients with total assets less than $ 123 million are

labeled as small clients.

The result was in conformity with their prediction: compare to non-specialists specialists do require a

higher audit fee, and this is only applicable to smaller companies. For large clients, companies not

only do not pay an industry premium, in addition when comparing with smaller firms their audit fee is

relatively less.

3.4.2 Bills, Jeter & Stein (2013)

The authors of this article assumed that the auditors’ industry specialization could create a decrease in

the audit fee. Their argument was that companies of certain industries contain stable operations over

time, which creates industry homogeneity and consequently are more easily to audit than other

industries. Consequently, to obtain cost based competitive advantages concerning auditors it is more

attractive to stay within those industries with a greater homogeneity. In addition to benefit from

economies of scale for auditors it is more likely to stay within these industries. Consequently, industry

homogeneity enables industry specialists requiring lower audit compensation. An essential limitation

is that, since the audit firm cost data are not publicly available, the cost based competitive advantages

cannot be observed. The authors are only able to test whether the industry homogeneity creates a

decrease in audit fee for industry specialists.

30

In order to test their argumentation, the authors developed the next hypotheses:

Hypothesis 1

As evidenced by relatively lower fees for audits in industries with homogeneous operations, industry

specialization results in cost efficiencies.

Hypothesis 2

As evidenced by relatively lower fees for audits in complex industries with homogenous operations

industry specialization results in cost efficiencies.

The term homogeneity is classified following the study by Cairney & Young (2006) which measured

homogeneity by using the correlation of the differences in the year-to-year operating expenses for

companies within an specific industry. Since concurrent economic conditions are resulting in a

homogeneous reported financial impact in a relative way this measure reflects the underlying

similarity of the companies’ operations (Cairney & Young, 2006).

The sample was collected using the Audit Analytics and the Compustat. After excluding financial

industries and observations with only one company within an industry, 23852 firm-year observations

exist between fiscal years 2004 up to and included 2009.

The results suggested that the industry specialist require a fee premium for clients from non-

homogenous industries, but charged an incrementally lower fee to clients from homogenous industries.

In the sensitivity test, the authors found no significant differences in the audit quality concerning both

industries.

3.5 Hypotheses Development

Based on the examined prior research, the next hypotheses are formulated.

Audit client complexity in this thesis will be used as a determinant for the audit fee. This can be

caused by many factors. One of them is the industry in which the audit clients are operating. For

instance, the virtue of some industries requires special accounting policies, which increases the

difficulty and the audit hours to complete the audit. Consequently, clients in a typical complex

industry would be charged with a higher audit fee than clients in other general industries. In order to

test this assumption, the next hypothesis is developed:

Hypothesis 1

Higher complexity of the auditee would cause higher audit fee

31

The amount of industry specific knowledge could create either higher or lower audit fee. Because they

provide their personnel with additional trainings and educations in order to obtain industry specific

knowledge, to cover the extra costs, the audit firms may charge their clients a higher audit fee. In

addition, by their valuable industry specialized knowledge, auditors could gain a competitive

advantage over their competitors, hence charging a higher fee. On the other hand, industry specific

knowledge in addition could create a lower audit fee. Since the auditors have more knowledge about

the client’s industry, they are able to recognize the industry specific audit risks at an earlier stage.

Additionally, industry specialists are more likely to attract potential clients from their specialized

industry and in the end achieve economies of scales, which comparing with non-specialists could

create a fee discount. Hence to test which one is the case, and which correlation is significant the next

hypotheses are developed.

Hypothesis 2a

Industry specific knowledge would cause a higher audit fee

Hypothesis 2b

Industry specific knowledge would cause a low audit fee

Based on the approach that audit clients’ complexity could create a higher audit fee, the industry

specific knowledge of the auditors could reduce the relative complexity and increase the audit

efficiency hence create a decreased audit fee particularly for complex clients. Consequently, the next

hypothesis was developed:

Hypothesis 3

Industry specific knowledge decreases the effect of auditee’s complexity on the audit fee

3.6 Summary

The chapter provided a short analysis of several studies concerning the audit fee determinants. All

articles used a similar regression analysis to examine their assumed fee drivers and the most of them

are confirmed to have a statistically significant influence on the audit fee. These confirmed

determinants are also used in this thesis as control variables to eliminate their effect with the audit fee.

However, there are several differences between the articles which will be highlighted subsequently.

These differences did not cause opposite conclusions but are worthwhile to mention in order to