Embed Size (px)

Citation preview

Commercial Finance

Rick WolfertVice Chairman, Commercial Finance

A Recognized Leader in Commercial Finance

Managed Assets: $39 Billion

Large and loyal customer base

- Over 57,000

2,450 employees- Large direct sales force: ~400

Preeminent brand - 98 years of middle market lending

experience - Superior risk underwriting experience

and skill

Global scope- Operating in over 30 countries

Data as of September 30, 2006.

Broad Portfolio of Scaled Businesses in Attractive Markets

Commercial Finance Group

Commercial Services Business CapitalComm, Media & Entertainment

Commercial Real EstateConstruction

Equipment FinanceEnergy

HealthcareMergers and Acquisitions

Sponsor Finance

Aerospace

Rail

Commercial Aircraft

Business Aircraft

Aerospace and Defense FinanceCommercial Credit

Commercial Services Int’l

Commercial Services Asia

Commercial Services Europe

Trade Finance Transportation Finance Corporate FinanceNet Revenue: $331 Million Net Income: $129 Million ROE: 26%

Net Revenue: $266 Million Net Income: $182 Million ROE: 17%

Net Revenue: $603 Million Net Income: $240 Million ROE: 16%

Net Revenue: $1.2 BillionNet Income: $551MillionROE: 17.9%

Syndicated Loan Group

Data as of or for the nine months ended September 30, 2006.

Clear Traction in Executing the New Strategy

33%Efficiency Ratio

$12.5 BillionVolume

$1.2 BillionNet Revenue

17.9%ROE

0.16%Net Charge-offs

3.23%Net Margin

$39 BillionManaged Assets

$551 MillionNet Income

vs. 20052006

28%

290 bps

220 bps

59%

15%

26 bps

9 bps

22%Challenges

Aggressive market pricing

Liberal credit structures

Accomplishments

Successfully launched customer-centric, market-focused growth strategy

Attracted over 150 top commercial finance professionals

Enhanced state-of-the-artrisk management system

Executed well on new growth initiatives

Data as of or for the nine months ended September 30.

1995-2006: A Dramatically Changed Competitive Landscape

Banks consolidating and moving up-market

Disrupted client relationships

Shifting middle market and industry strategies

Banking Commercial Finance

1995-2006: A Dramatically Changed Competitive Landscape

Banks consolidating and moving up-market

Disrupted client relationships

Shifting middle market and industry strategies

Banking Commercial Finance

Revenue

Where We Compete

Junk B-

$10M

$50M

$1B

$100B+

B+ BB- BBB AAA

Credit Rating

Middle Market~$1.8 Trillion

Finance Companies

Local Banks

Large Banks

Investment Banks

Hedge Funds

Finance CompaniesRegional Banks

Hedge Funds

Positioned for Global Growth

Aerospace global headquarters opened in Dublin, 2005

Expanding European factoring platform – German Factoring acquisition Q2 2006

Fortifying Asian expansion – New Singapore Aerospace office Q4 2006

AtlantaBostonCharlotteChicagoDallas

North AmericaShanghaiSingaporeHong Kong

$930 Billion

LondonDublinFrankfurt

Europe

$330 Billion

$420 Billion

Asia-Pacific

$147 Billion

HoustonLos AngelesNew YorkTempeToronto

$410 Billion

Loans

EquipmentFinance

$750 Billion$1.34 TrillionMarket $330 Billion

$183 Billion

Market-Focused Model Driving Organic Growth

Relationship Managers• Industry thought leaders• Consultative approach• Develop / manage CIT relationship• Coordinate execution

Equipment Finance& Leasing

Factoring

Asset Based Lending

Corporate Finance

Structured / Project Finance

M&A Advisory

Commercial Real Estate Advisory & Finance

Products and Services Target Industries

Communications, Media & Entertainment

Construction

Retail

Healthcare

Energy

Aerospace

Rail

Private Equity Sponsors Intermediaries Financial

Institutions

Channel Partners

HedgeFunds

Syndicated Loan Group

SponsorFinance

Capital Markets

Healthcare

Energy

Europe

Sales

EquipmentFinance

CommercialReal Estate

M&AAdvisory

CommercialServices

Canada

Risk

Communications, Media & Entertainment

Business Capital

Construction

Aerospace

Rail

Performance Driven by Strong Talent

2002 2003 2004 2005 2006 (E)

New Strategy is Driving Strong Originations Growth

CAGR: ~40%

CAGR: 6%

Q4

9 months

New Business Volume($ Billions)

8.19.1

8.2

11.412.5

7.8

Cross-Selling Strategy is Working

Tremendous growth in referral activity in 2006

Incentive compensationdrives behaviors

Lowest cost origination lever

2005 20069 mos.

$228

$967

22 72Transactions

Cross-Sell Volume($ Millions)

YTD324%

An Originations Powerhouse

$12.5 Billion Booked YTD

InvestmentVehicles

$9.3 Billion 2007 Initiative$3.2 Billion

CapitalMarkets

SyndicationsBalance Sheet

$61 Billion Proposed YTD

0

500

1,000

1,500

0

500

1,000

1,500

Driving Non-Spread Revenue and Improving Earnings Mix

Revenue Composition($ in Millions)

20029 mos.

20039 mos.

20049 mos.

20059 mos.

20069 mos.

Spread Non-Spread (NSR)

NSR Growth22%

Owned Credit Losses(% of Average Finance Receivables)

Best-in-Class Risk Management

660 person risk team lead by seasoned veterans

Sophisticated systems provide ‘early warning detection’

State-of-the-art risk-adjusted pricing discipline

Risk philosophy driven by diversification and supportedby strong collateral positions

Risk Management Expertise

0.25%0.16%

Risk-Adjusted Margin(% of Average Earning Assets)

20069 mos.

20059 mos.

2.75% 3.11%

20069 mos.

20059 mos.

Model Designed to Deliver Earnings Through All Cycles

Strong Economy

Acquisition Finance

Growth Capital

Mergers and Acquisitions

Real Estate

Construction

Competitors enter,margins decline

Down Cycle

Factoring

Restructuring

DIP Financing

Distressed Debt

Advisory Services

Competitors exit, margins improve

What do Middle Market Customers Really Want?

Understand their business

Stand with them through cycles

Deliver solutions for complex financing needs

Respond quickly and always deliver on commitments

Limited

How We Win in the Middle Market

RelationshipOrientation

StructuringExpertise

Middle Market Advisory Capabilities

Agility

Direct Access toDecision Makers

Broad ProductOffering

Long-Term Commitmentto Middle Market

Deep & Dedicated IndustryFocus / Expertise

Banks FinanceCompanies

HedgeFunds

Limited

Limited

Limited

Limited

Business Overview

Trade Finance Corporate FinanceTransportation Finance

Trade Finance: Commercial Services

#1 factoring position in the U.S.- ~$45 Billion volume

Average client relationship - Over 10 years

Actively cross-selling insurance, commercial credit and M&A

International expansion- Following our clients to Europe

and Asia

Factoring Volume($ Billions)

27.8 27.5

38.242.3

32.7

2002 2003 2004 2005 20069 mos.

CAGR: 12%

Transportation Finance: Rail

Youngest major fleet in the industry

- Average age of 10 years versus industry average of 19 years

#3 franchise position with over100,000 car fleet

Over 99% utilization rate

Smart bolt-on acquisitions

Attractive pricing on renewals

Favorable railcar delivery positions with manufacturers in 2007 / 2008

Managed Assets ($ Billions)

1.82.4 2.6

3.53.8

2002 2003 2004 2005 20069 mos.

CAGR: 22%

Transportation Finance: Aerospace

#3 franchise position

40 years of industry experience

Over 120 customers

International platform: over 80% of aircraft are outside North America

Modern, fuel efficient fleet

Commercial Aircraft: Over $2 trillion requirement for aircraft financing in the next 20 years

Business Aircraft: $156 billion of aircraft deliveries in the next 10 years

Aerospace and Defense Finance: Supply chain finance

4.2 4.85.5

6.77.1

2002 2003 2004 2005 2006

Managed Assets($ Billions)

9 mos.

CAGR: ~15%

Corporate Finance

6.5 6.7 7.48.7

10.4

2002 2003 2004 2005 20069 mos.

Leveraging industry expertise, specialty lending acumen, balance sheet and capital market capabilities

Focused ‘One CIT’ approachto channel partners

Collaborative deal teams driving organic growth

Advisory services enhance capabilities and fee revenue

Expanding lead generation through Piper Jaffray alliance

New Business Volume($ Billions)

Sponsor-Backed Transactions

2005 2006 9 mos.

Number of Deals 196 262

Lead Deals 15 40

Commitments $4.0 B $7.3 B

Fundings $2.2 B $4.0 B

CAGR: ~30%

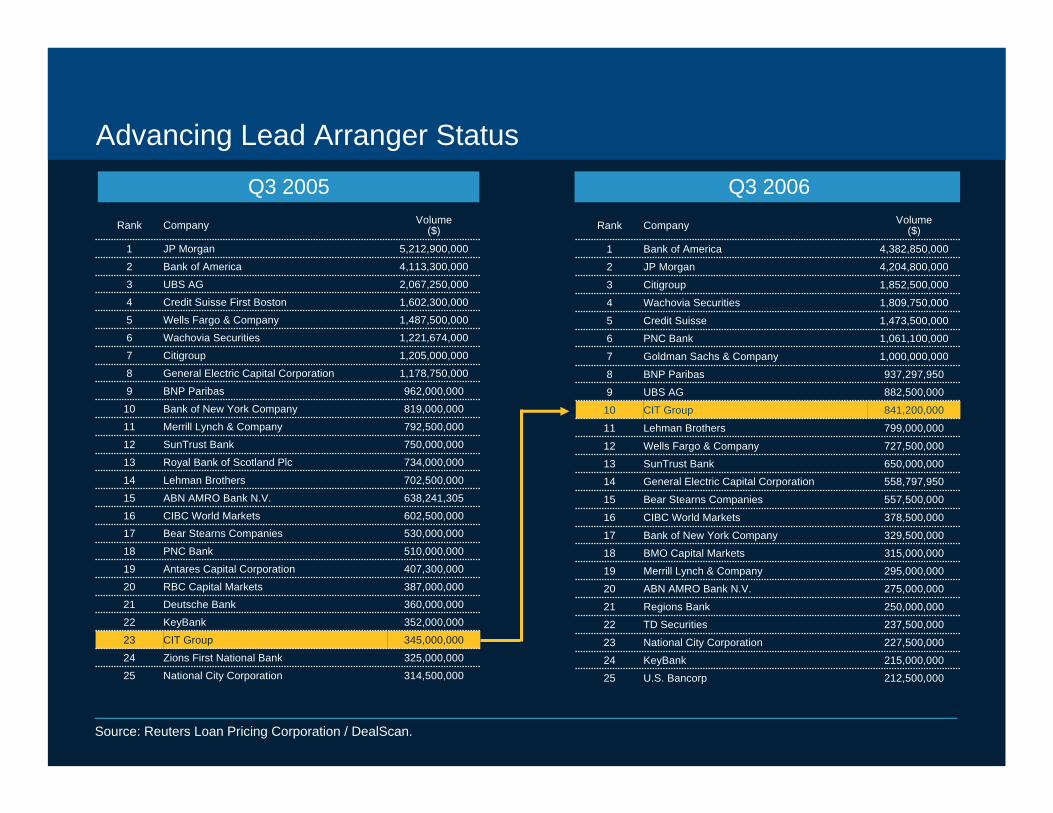

Advancing Lead Arranger Status

Q3 2005

314,500,000National City Corporation25

325,000,000Zions First National Bank24

345,000,000CIT Group23

352,000,000KeyBank22

360,000,000Deutsche Bank21387,000,000RBC Capital Markets20

407,300,000Antares Capital Corporation19

510,000,000PNC Bank18

Volume($)CompanyRank

530,000,000Bear Stearns Companies17602,500,000CIBC World Markets16

638,241,305ABN AMRO Bank N.V.15

702,500,000Lehman Brothers14

734,000,000Royal Bank of Scotland Plc13

750,000,000SunTrust Bank12

792,500,000Merrill Lynch & Company11

819,000,000Bank of New York Company10

962,000,000BNP Paribas9

1,178,750,000General Electric Capital Corporation8

1,205,000,000Citigroup7

1,221,674,000Wachovia Securities6

1,602,300,000Credit Suisse First Boston4

1,487,500,000Wells Fargo & Company5

2,067,250,000UBS AG3

4,113,300,000Bank of America2

5,212,900,000JP Morgan1

Source: Reuters Loan Pricing Corporation / DealScan.

Q3 2006

212,500,000U.S. Bancorp25

215,000,000KeyBank24

227,500,000National City Corporation23

237,500,000TD Securities22

250,000,000Regions Bank21

275,000,000ABN AMRO Bank N.V.20

295,000,000Merrill Lynch & Company19

315,000,000BMO Capital Markets18

Volume($)CompanyRank

329,500,000Bank of New York Company17

378,500,000CIBC World Markets16

557,500,000Bear Stearns Companies15

558,797,950General Electric Capital Corporation14

650,000,000SunTrust Bank13

727,500,000Wells Fargo & Company12

799,000,000Lehman Brothers11

841,200,000CIT Group10

882,500,000UBS AG9

937,297,950BNP Paribas8

1,000,000,000Goldman Sachs & Company7

1,061,100,000PNC Bank6

1,809,750,000Wachovia Securities4

1,473,500,000Credit Suisse5

1,852,500,000Citigroup3

4,204,800,000JP Morgan2

4,382,850,000Bank of America1

New Strategic Initiatives are Growth Engines for the Future

Q1 2005 Q2 2005 Q3 2005 Q4 2005 Q1 2006 Q2 2006 Q3 2006 Q4 2006 2007

Overall Investment vs. Return($ Millions)

Investment phase

Revenue positive

Healthcare

Mergers & Acquisition

Commercial Real Estate

Capital Markets

Global Sponsor

Syndicated Loan

Energy

Aerospace & Defense Finance

International Trade Finance

Commercial Credit

Business Capital Restructuring

StructuredEquipment Finance

New Strategic Initiatives are Growth Engines for the Future

Overall Investment vs. Return($ Millions)

Q1 2005 Q2 2005 Q3 2005 Q4 2005 Q1 2006 Q2 2006 Q3 2006 Q4 2006 2007-50

-30

-10

10

30

50

70

90

110

130

150

Q1 2005 Q2 2005 Q3 2005 Q4 2005 Q1 2006 Q2 2006 Q3 2006

ExpenseRevenue

Net Revenue

Healthcare Vertical Driving Growth

Healthcare as a growth engineLaunched industry vertical in 2005Hired best-in-class teamOrganized sales force around large healthcare sub-segments

2005 Healthcare Financings:~$170 Billion

Managed Assets($ Billions)

Dec 2004 Dec 2005 Sep 2006

0.5

1.5

2.5

Hospitals Dental Physician Practices

Speciality Pharma / Meditech Outpatient

Long Term Care Managed Care

Life Sciences Vendor

31%

5%16%5%

16%

9%

12%6%

CAGR: 144%

Healthcare - Rapid Payback on Investment

0

10

20

30

40

50

60

Q1 2005 Q2 2005 Q3 2005 Q4 2005 Q1 2006 Q2 2006 Q3 20060

20

40

60

80

100

120

140

160

180

Revenues Expenses Efficiency Ratio

Accelerating Productivity

($ Millions) Efficiency Ratio (%)

Building Scale Through Bolt-On Acquisitions

Trade Finance Transportation Finance

Rail Fleet(Railcars)

German Factoring 166

SunTrust 864

Factoring Assets($ Millions)

Corporate Finance

Healthcare Finance Assets($ Millions)

HBCC 515 PLM 5,845

DJ Joseph 2,100

Bombardier 15,000

Acquisitions are a core competencyAccretive from inception

All are tracking at or above plan

Construction: Transformation Success Story

Refocused on core strategy

Restructured the business- $11 million cost take-out

- 106 headcount reduction

Re-deployed sales force

Effective use of capital markets distribution capabilities

The result:- Improved front-end and

operational efficiency

- Sales productivity morethan doubled

- Achieving ROE hurdle rate

$28 MNon-Spread Revenue

$1.2 BVolume

15.1%ROE

27.2%Efficiency Ratio

$32 MNet Income 66%

23%

30%

1,098bps

667bps

20069 mos.

20059 mos.

VS.

Investment Phase in Growth Initiatives is Nearly Complete

Funded 25% by exiting slow-growth / low-return businesses

Rigorous focus on productivity and expense management

Platforms built without incurring goodwill

5%

95%

80%

20% Back-end

Front-end

Majority of investment has been…

Focused on the Front-End

Cost and Revenue Correlated

Fixed

Variable

134

101

(33)

Investment Restructuringsavings

Net Investment

Investment for Growth($ Millions)

Balancing Size of Sales Force with Productivity

275

Sep2005

20%

==++

28

32%

37

59%

12.1

7.6

Sales Force Size* Sales Productivity($ Millions)

Volume*

($ Billions)

Sep2006

20059 mos.

20069 mos.

20059 mos.

20069 mos.

330

* Excludes Trade Finance volume and headcount.

14.4%16.0% 16.8% 16.8% 17.2%

18.5% 18.0%

2,0973,087 2,705

3,5313,065

4,568 4,892

Q1 2005 Q2 2005 Q3 2005 Q4 2005 Q1 2006 Q2 2006 Q3 2006

Delivering Strong Growth and Returns

ProfitabilityDrivers

Record new business volumesStable risk-adjusted marginsIncreasing levels of fee incomeStrong credit quality

Volume ($ Millions) ROE

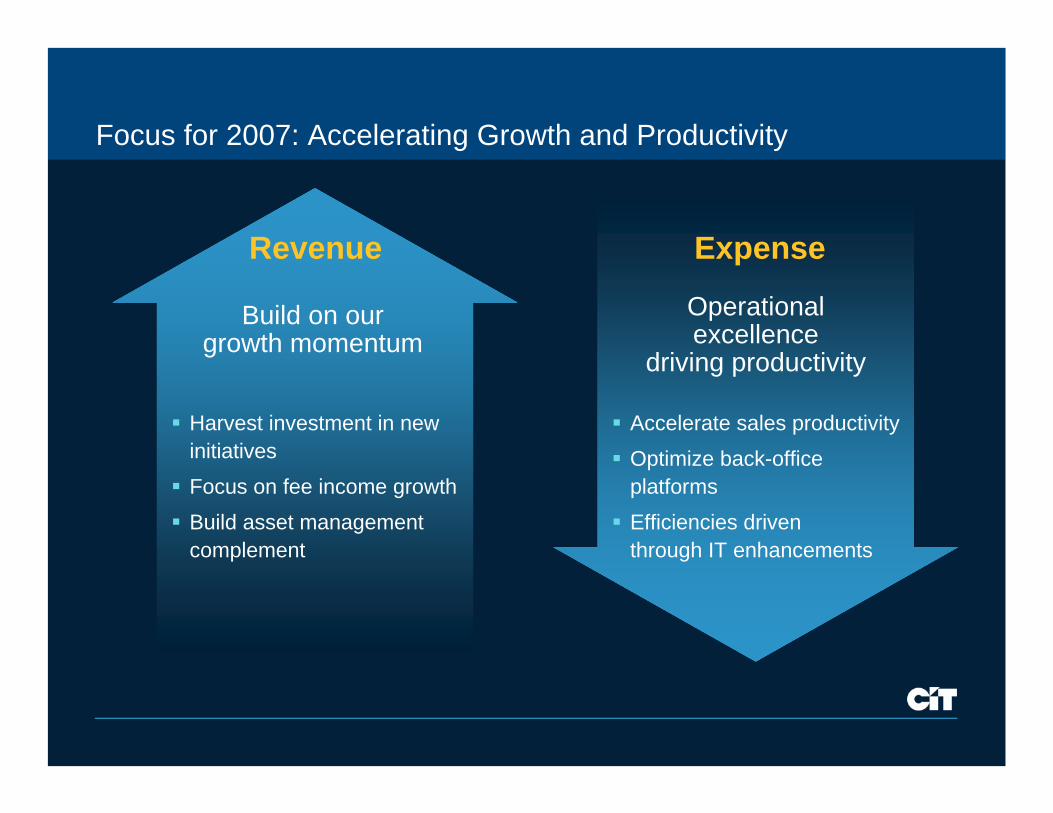

Focus for 2007: Accelerating Growth and Productivity

Harvest investment in new initiatives

Focus on fee income growth

Build asset management complement

Build on our growth momentum

Operationalexcellence

driving productivity

Accelerate sales productivity

Optimize back-office platforms

Efficiencies driventhrough IT enhancements

Revenue Expense

Commercial Finance Panel

Gregg Smith M&A

Jim HudakCommunications, Media & Entertainment

Flint BeseckerHealthcare

Healthcare Team Leads with Trusted Advisor Approach

Top 5 healthcare leaders have over 100 years of industry experience

Applies intellectual capital to drive value for clients

Healthcare is huge market representing 16% of GDP

Added 289 new relationships in past 12 months

Sole Lead Arranger

$55,000,000

Senior Secured Credit Facility

Supporting the Acquisition of Tarrant Dialysis Centers by US Renal

$47,100,000

Senior Secured Credit Facilities

Acquisition Finance

Relationship Case Study

Widely respected middle market private equity firm with long standing healthcare

investment track record

4 Closed lead mandate financings in 20063 Pending commitments due to fund2 Buy-side advisory engagements

CIT Healthcare is preferred source for private equity firm’s activities Sole Lead Arranger

M&A Advisory Team Executes Mandates Across CIT’s Platform

Over 90 opportunities have been reviewed:

have acquired

September 2006

and

Sanus Holdings, LLC

®®

The undersigned initiated the transaction and acted as exclusivefinancial advisor to Arcapita Inc. and Sanus Holdings, LLC

Common Characteristics

A leading distributorof women’s apparel

®®

Exclusive sell-side advisor

PROJECTYELLOW JACKET

In Process

Aerospace & Defense (1)Communication, Media & Entertainment (14)Consumer Products (5)Diversified Industrials (20)

Energy (5)Healthcare (30)Rail (1)Retail & Apparel (15)

Long-term relationships

Leverage CIT’s balance sheet

Deep industry expertise

CIT initiated

Case Studies

Communications, Media & EntertainmentValidation of Industry Vertical Strategy

Strategic Group with Great Growth and New Potential

Industry experts with long term relationships in each sub-vertical

Deliver multiple products for a total financing solution

Expanded into contiguous areas -Sports and Entertainment

Repositioned team for stronger underwritings and lead positions

27 co-lead or sole lead arranger transactions to date in 2006

Proof of Concept

Sole Arranger, Administrative Agent

and Acquisition Advisor

First Lien Revolving Line of Credit, First Lien Term Loan B and Second Lien Term Loan used for acquisition

Casino and hotel operator

$222,000,000

Sole Arranger, Administrative Agent

and Acquisition Advisor

First Lien Revolving Line of Credit, First Lien Term Loan B and Second Lien Term Loan used for acquisition

First Lien Revolving Line of Credit, First Lien Term Loan B and Second Lien Term Loan used for acquisition

Casino and hotel operator

$222,000,000

Administrative Agent (Senior)

Documentation Agent (Mezzanine)

Revolving line of credit and mezzanine facility for the purpose of film production

Successful genre film label

$212,500,000

Administrative Agent (Senior)

Documentation Agent (Mezzanine)

Revolving line of credit and mezzanine facility for the purpose of film production

Successful genre film label

$212,500,000

219

780

2005 2006

Syndication Volume($ Millions)

250%

10.2

24.6

2005 2006

Fee Income($ Millions) 140%

0.7

1.5

2005 2006

Volume($ Billions) 114%

Commercial Finance

Improved go-to-market synergiesFocus on major growth opportunitiesGreatly enhanced fee income generationEnhanced risk management – domain expertiseScalable modelDeliver consistently through all cycles

Benefits

Market and industry focusedCustomer-centricEnd-to-end solutionsRelationship drivenEnables cross-sellingOriginate and distribute model

The Right Modelat the Right Time

Industry expertise valuedCapital expenditures increasingComplex and growing financing needsFragmented competitive landscapeGlobal scope

Focus on Large and Attractive Markets