Embed Size (px)

Citation preview

VANTAGE HSA Part of an integrated CDHC solution

• A Vantage Health Savings Account helps you contain your costs, empower your employees and keep your benefits package competitive in today's environment of rising costs and changing rules. When combined with another consumer-directed health care (CDHC) plan such as a Flexible Spending Account, you can maximize the value of your benefits package to employees and multiply your savings. And with the Vantage Benefits Card, you can set custom stacking rules to allow employees to access funds from several CDHC accounts with one card.

WHAT IS AN HSA HSAs are tax-advantaged medical savings accounts available to taxpayers who are enrolled in an HSA-qualified high-deductible health plan. The funds contributed to the account are not subject to federal income tax at the time of deposit. Unused amounts in one year can be carried over to following years and added to subsequent contributions.HDHP Minimum Required Deductibles:• Self-only: $1,200• Family: $2,400HDHP Out-of-Pocket Maximum:• Self-only: $6,050• Family: $12,100 HSA Contribution Limits:• Individual (self-only HDHP): $3,100 • Family: $6,250

HOW THE HSA WORKS • With a Health Savings Account (HSA), you may either contribute

all or a portion of your health plan deductible into a tax-advantage savings account, within certain limits. And like an individual retirement account (IRA), your HSA investment earnings are tax-deferred. Funds remain tax-free provided you use them to pay for qualified medical expenses. And better yet, funds may grow annually allowing you to save for future medical expenses.

• When you enroll in a Vantage HSA, accessing your funds is simple! You’ll receive an HSA Visa debit card to use anywhere Visa is accepted for qualified medical expenses.

• After you open your account, your deposits will earn interest in an FDIC-insured custodial account. As you accumulate assets in your HSA, you will be provided access to numerous investment options.

VANTAGE ADVANTAGE FOR HSA

Trust Vantage's Expertise• Convenience. Our HSA provides easy employee access via the Vantage

Benefits Card for point-of-sale swipes and our intuitive self-service website for ongoing account management. We also offer online, fax and mail disbursement requests.

• Compliance. Our team of legal experts helps ensure your HSA plan is fully compliant with all applicable laws, including those that are still evolving due to health care reform.

• Focus. Vantage's online self-service portal and customer service phone center work together to answer your employees' questions, so you can focus on your core business functions.

• Experience. Trust our experienced providers of human resources and benefits administration to manage your HSA program.

• Cost-effectiveness. You pay no annual or renewal fees, only monthly fees for participating employees. Plus, there are no hidden account or transaction fees for your employees.

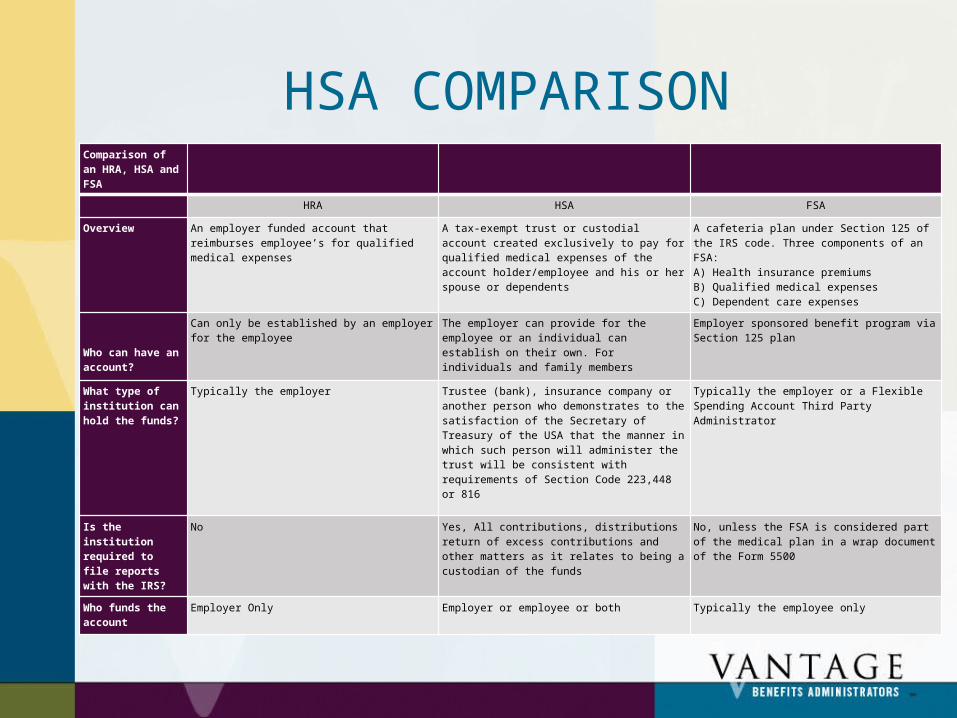

HSA COMPARISONComparison of an HRA, HSA and FSA

HRA HSA FSA

Overview

An employer funded account that reimburses employee’s for qualified medical expenses

A tax-exempt trust or custodial account created exclusively to pay for qualified medical expenses of the account holder/employee and his or her spouse or dependents

A cafeteria plan under Section 125 of the IRS code. Three components of an FSA:A) Health insurance premiumsB) Qualified medical expensesC) Dependent care expenses

Who can have an account?

Can only be established by an employer for the employee

The employer can provide for the employee or an individual can establish on their own. For individuals and family members

Employer sponsored benefit program via Section 125 plan

What type of institution can hold the funds?

Typically the employer Trustee (bank), insurance company or another person who demonstrates to the satisfaction of the Secretary of Treasury of the USA that the manner in which such person will administer the trust will be consistent with requirements of Section Code 223,448 or 816

Typically the employer or a Flexible Spending Account Third Party Administrator

Is the institution required to file reports with the IRS?

No Yes, All contributions, distributions return of excess contributions and other matters as it relates to being a custodian of the funds

No, unless the FSA is considered part of the medical plan in a wrap document of the Form 5500

Who funds the account

Employer Only Employer or employee or both Typically the employee only

HSA COMPARISONComparison of an HRA, HSA and FSA

HRA HSA FSA

Who owns the moneys in these accounts

The employer The employee The unused funds revert back to the employer at the end of the plan year.“Use it or lose it rule”

Can these dollars be used for retirement income?

No, as there is technically no value to the employee once they leave the employer

Yes No, “use it or lose it rule”

Can these dollars be rolled over?

No, as there is technically no value to the employee once they leave the employer

Yes, within 60 days No, “use it or lose it rule”

How Is money withdrawn?

Employer or TPA reimburses Book of checks or debit card Check or debit card

High Deductible Health Plan(HDHP) required

No Yes- minimum of $1,200 for individual $2,400 for families

No

HSA COMPARISONComparison of an HRA, HSA and FSA

HRA HSA FSA

Eligibility Employee who meets employer's defined eligibility criteria

Eligible employee/individual covered by HDHP and no other non-HDHP coverage

Employee who meets employer's eligibility criteria

FICA savings Yes Yes/No Yes

Maximum contribution

No maximum. Employer may impose a maximum, but there is no IRS limitation.

For 2012Individual - $3,050Family - $6,150.

No IRS maximum on Health FSA IRS has a maximum for Dependent Care of $5,000.00 per plan year

Tax deductibility --employee

Contribution has no impact on current year earned income

Employee contributions are pretax if offered through a Section 125 Plan or tax deductible (through IRS Form 1040) if contributions are made independent from employer

Employee contributions are pretax

Taxation of accumulated earnings

Tax-free if assets are held in a tax-exempt trust Tax-free N/A

HSA COMPARISONComparison of an HRA, HSA and FSA

HRA HSA FSA

Qualified retiree insurance premiums

Retiree health insurance, including qualified LTC Limited None

Non-medical withdrawals

Not allowed Yes, but will be included in gross income and subject to 10% excise tax, unless made after death, disability or age 65

Not allowed

Carryover from year to year

Yes Yes No

Portable after termination

Yes, only if employee elects COBRA under group health plan

Yes, employees may take funds with them when they leave

No

HSA FAQ’S • What are qualified medical expenses?• Your HSA can be used to pay for qualified medical expenses that apply

toward your deductible. Additionally, you can pay for qualified medical expenses that your health plan doesn't cover. (For a complete list of qualified medical expenses, please refer to Section 213(d) of the Internal Revenue Service Code.)

• How do I access the funds in my HSA?• Using your funds is simple. You’ll receive a Visa debit card that can be used

anywhere Visa is accepted, such as your doctor's office and pharmacy. Checks will also be available on request.

• Can I use my debit cards to obtain cash?• Yes. Your debit card will work at any ATM. You can also use your debit card

to obtain cash from a bank teller. • I only have the debit card, and my doctor doesn't accept Visa. How

do I pay?• Pay your doctor with a check or cash from your personal checking or

savings account, and then reimburse yourself from your HSA by obtaining cash.

HSA FAQ’S • Who do I call if my debit card is lost or stolen?• Call the Vantage HSA customer service center at 1-888-581-9787,

Monday - Friday, 8 a.m. to 6 p.m. (Central Time). • Can I write checks from my HSA account?• A check request form and signature card will be mailed to you with

your debit card. If you’d like to receive checks, simply return the completed form and signature card to Vantage. You’ll receive your checks within 10 - 15 business days. To cover the cost of check processing, there is a $1.25 charge for each check you write.

• Are there any forms I need to file to be reimbursed for medical expenses?

• No. You pay for medical expenses with your debit card, or by writing a check if you have chosen that option.

HSA FAQ’S • What happens if I don't spend all the funds in my HSA by the end

of the year?• Unused funds rollover from year to year. • What is the minimum amount I can contribute to my Vantage HSA?• You must contribute at least $20 per month to your HSA. • Who can contribute to my Vantage HSA?• HSA contributions can be made by any eligible individuals. For an

employer-sponsored HSA, the employee, the employer or both may contribute to the HSA. Family members may also make contributions to an HSA for another family member as long as the other family member is eligible and covered under the high- deductible health plan.

• How do I contribute funds to my HSA in addition to my monthly contribution?

• You will be mailed deposit coupons once your HSA is established. Simply mail your check and coupon to Vantage at the address provided.

HSA FAQ’S • In the event that I marry or have children, how do I change the

amount of my contribution?• Call the Vantage HSA customer service center at 1-888-581-9787, Monday-

Friday, 8 a.m. to 6:00 p.m. (Central Time). • Are there any tax forms that I need to use in preparing my taxes

at year-end?• Yes. Similar to IRAs, each January you will be sent a 1099 Form for any

distributions made from the HSA during the calendar year. If the contributions were made by you or your employer through an employer plan, those contributions will be reported on your W-2 issued by your employer.

• What if I change jobs?• Call the Vantage HSA customer service center at 1-888-581-9787, Monday-

Friday, 8 a.m. to 6:00 p.m. (Central Time). • What happens if I‘m no longer participating in a high-deductible

health plan?• You can continue to spend any funds in your HSA to pay for qualified

medical expenses. However, you can no longer contribute to your HSA.

HSA FAQ’S • How I can check the balance of my HSA?• You can view the balance of your HSA online at

www.vantagebenefits.com, or by calling 1-888-581-9787. • What if I need assistance or have questions about

my HSA?• Call the Vantage HSA customer service center at 1-888-

581-9787, Monday - Friday, 8 a.m. to 6:00 p.m. (Central Time).

• In the event of my death, what happens to my HSA funds?

• In case of death, remaining HSA funds shall be forwarded to your designated beneficiary or beneficiaries as indicated on your Vantage HSA Enrollment Form.