Embed Size (px)

Citation preview

Vagabond Venture Oil Group

SEARCH FOR FOSSILSEARCH FOR FOSSIL

FUELSFUELS

Winter Term 2012

1

Geology in the news

Future Class?

Drilling Results - Economics

TODAY’S PLAN

2

Drilling Results - Geologic

GEOLOGY IN THE NEWSAustin American Statesman: February 25, 2012

Texas Supreme Court determination 08-0964: “Subsurface fresh water belongs to land owner and should be treated like oil and gas deposits which are owned by land owner of subsurface minerals”

Two land ownerships in TexasSurface land ownership: farms, ranches, homes, etc.

Subsurface land ownership: Oil and gas deposits

Rain water

Salt water

Hot salt water

Fresh Ground waterFresh water Soil

Brackish Ground water Fresh Ground water

Massive Edwards limestone Village Center

Berry Creek pond

Edwards limestoneWalnut layers

Glen Rose limestone

Trinity Sandstone

Rocks at Sun CityGeorgetown limestoneWilliams Dr. Front Gate

Georgetown limestone SR 195

Edwards limestoneComanche Peak layer

Edwards limestonePorus reef layers

Austin American Statesman: March 3, 2012

GEOLOGY IN THE NEWS

Fracking & horizontal drilling of new wells costing $1.5 million predicted to increase oil production by 2 million bbls/day

Problems: lack of water for fracking and local endangered lizard species

Gas and Oil Shale Plays: USA and Western CanadaWest Texas Oil Shale Play: Bone Springs Oil Shale

DISCLAIMERThe material you are about to see was

developed for the learning and enjoyment of the class participants.

The diagrams and numbers have been gathered from various sources to reflect the geologic and economic scenerios of the two locations, but neither is a real prospect and neither represents an

actual investment opportunity. 9

- Drilling resultsDrilling results- Return on investmentsReturn on investments

VAGABOND GROUPVAGABOND GROUP

2 OPPORTUNITIES2 OPPORTUNITIESOn-shore PennsylvaniaOn-shore PennsylvaniaOff-shore Gulf of MexicoOff-shore Gulf of Mexico

VAGABOND GROUPVAGABOND GROUP

2 OPPORTUNITIES2 OPPORTUNITIESOn-shore PennsylvaniaOn-shore PennsylvaniaOff-shore Gulf of MexicoOff-shore Gulf of Mexico

- Drilling resultsDrilling results- Return on investmentsReturn on investments

On-shore PennsylvaniaOn-shore Pennsylvania

On-shore: PennsylvaniaOn-shore: Pennsylvania

- TD @ 5,060’ in salt

- reached Marcellus shale @ 4,935’

- found 52’ Marcellus shale

On-shore: PennsylvaniaOn-shore: Pennsylvania

Is there

gas?Let’s look at the seismic & well

logs . . . .

On-shore: PennsylvaniaOn-shore: Pennsylvania

`MARCELLUSMARCELLUS

S N

4’ shaleno gas

56’ shale46’ gas

DISCOVERY

thickness ? gas ?

our prospect

52’ shaleno gas!

Why?

DRY HOLE!

DRY HOLE

On-shore: PennsylvaniaOn-shore: Pennsylvania

`

DISCOVERY

MARCELLUSMARCELLUS

S N

our prospect

1) no organic-rich deposits in our area of Marcellus

organic richnot organic rich

2) gas leaked out of Marcellus shale along fault

DRY HOLE

On-shore: PennsylvaniaOn-shore: Pennsylvania

`MARCELLUSMARCELLUS

S N

1) no organic-rich deposits in our area of Marcellus 2) gas leaked out of Marcellus shale along fault

our prospect

fault leaks

DRY HOLE!

DISCOVERYDRY HOLE

One million $ investor is broke!

Maxum Oil

CEO

On-shore: PennsylvaniaOn-shore: PennsylvaniaS N

our prospect

DRY HOLE!

One million $ investor is broke!

It’s not too late!

Upper Devonian Ohio Gas Shale

Rocks of Northeastern USA

extent of Ohio and related gas shales

Ladoga

Probable Extension of Ohio Gas Shale Play into IllinoisIn Illinois the Ohio Shale is Called the New Albany Shale

Your next investment?

VAGABOND GROUPVAGABOND GROUP

2 OPPORTUNITIES2 OPPORTUNITIESOn-shore PennsylvaniaOn-shore PennsylvaniaOff-shore Gulf of MexicoOff-shore Gulf of Mexico

- Drilling resultsDrilling results

Off-shore Gulf of MexicoOff-shore Gulf of Mexico

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

- TD @ 16,624’ in salt

- reached Wilcox sand @ 12,500’

- found 2,166’ sand

Looking at the seismic data. . . .

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

- discovered 520’ oil sands Let’

see!

saltWilcoxWilcox sandstones

sandstones

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

water ~6000’BE

ST

Wilcox Sandstone Reservoirs?our prospect

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

saltWilcoxWilcox sandstones

sandstones

water ~6000’

our prospect

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

11,500’ - top sand

16,000’ - base sand

12,500’12,500’

14,666’ - base sand14,666’ - base sand- & sand- & sand- fault- fault

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

16,000’ - base sand

12,500’12,500’

14,666’ - base sand14,666’ - base sand- & sand- & sand- fault- fault

16,604’ – top salt16,604’ – top salt

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

12,500’12,500’

14,666’ - base sand14,666’ - base sand- & sand- & sand- fault- fault

16,604’ – top salt16,604’ – top saltthickness of Wilcox sandthickness of Wilcox sand = 2,166’= 2,166’

12,500’ – top sand12,500’ – top sand

14,666’ - base sand14,666’ - base sand

Let’s look at the well log . . . .

where’s

the oil!

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

Presence of oil/gas

Reservoir Rocks(sandstones)

top sand: 12,500’ top sand: 12,500’

base sand: 14,666’ base sand: 14,666’

100’

520’

520 feet of ‘pay’

520 feet of ‘pay’

near base of sand!

near base of sand!

Off-shore: Gulf of MexicoOff-shore: Gulf of Mexico

??

520’ PAY520’ PAYnear base sandnear base sand

Lateral wellLateral well

Perhaps more pay?Perhaps more pay?

??

- Drilling resultsDrilling results- Return on investmentsReturn on investments

VAGABOND GROUPVAGABOND GROUP

2 OPPORTUNITIES2 OPPORTUNITIESOn-shore PennsylvaniaOn-shore PennsylvaniaOff-shore Gulf of MexicoOff-shore Gulf of Mexico

REMEMBER THE OFFSHORE BORDER DISPUTE?REMEMBER THE OFFSHORE BORDER DISPUTE?

33

OFFSHORE DEVELOPMENT OPTIONSOFFSHORE DEVELOPMENT OPTIONS

34

FPSOFPSO=FFloating, PProduction, SStorage, OOffloading (5840ft)

REMEMBER FPSO’S?REMEMBER FPSO’S?

35

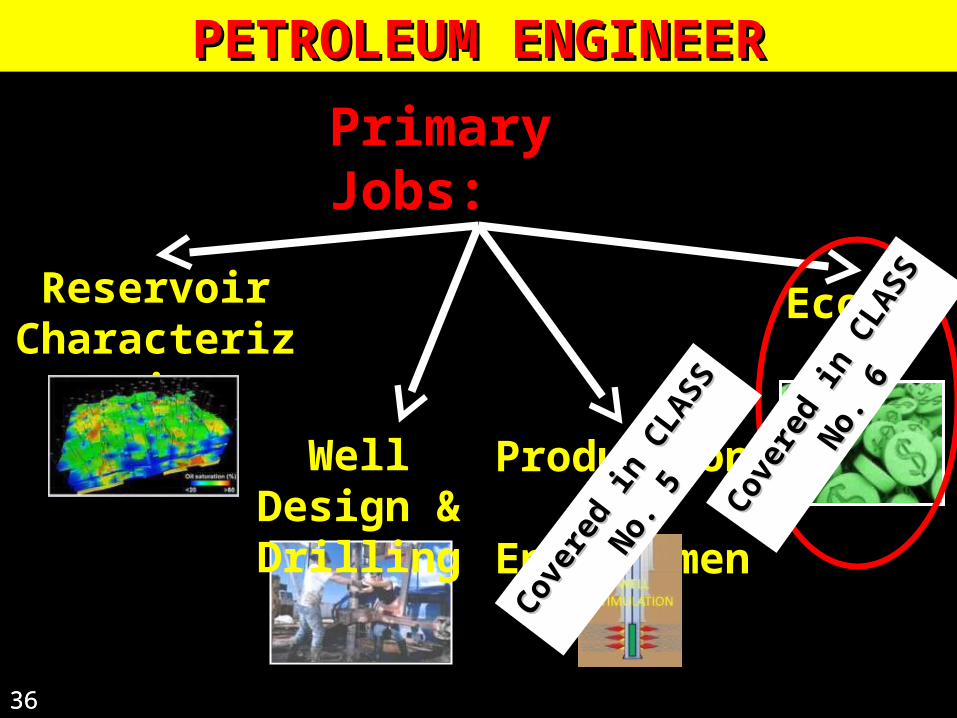

PETROLEUM ENGINEERPETROLEUM ENGINEER

36

Primary Jobs:

Reservoir Characterization

Production & Enhancements

Well Design & Drilling

36

EconomicAnalysis

Cove

red i

n CLA

SS N

o. 5

Cove

red i

n CLA

SS N

o. 5

Cove

red

in C

LASS

No.

6

Cove

red

in C

LASS

No.

6

37

Economic Analysis

OIL &GAS ECONOMICSOIL &GAS ECONOMICS

Oil PriceOil PriceOil PriceOil Price

Operating Operating &&

Investment Investment Cost Cost

Operating Operating &&

Investment Investment Cost Cost

Production Production RateRate

Production Production RateRate

38

RecoverabRecoverablele

ReservesReserves

RecoverabRecoverablele

ReservesReserves

Royalties Royalties &&

Working Working InterestInterest

Royalties Royalties &&

Working Working InterestInterest

O&G TaxO&G TaxAccountingAccountingO&G TaxO&G Tax

AccountingAccounting6 KEY FACTORS

IN O&G ECONOMIC ANALYSIS

OIL &GAS ECONOMICSOIL &GAS ECONOMICS

Technical• Worldwide

Reserves status

• Worldwide Production Capacity

• Refining Capacity

Political• OPEC’s Mood• Producing

country’s stability

• Balance of Power

Financial• Transaction

costs

Factors Affecting OIL PRICE

39

Economic• Worldwide

Supply & Demand

• Cost of Alternatives

OIL &GAS ECONOMICSOIL &GAS ECONOMICS

Selection• Quality of

seismic • Geologic &

Geophysical selection accuracy

Modeling• Recovery

Factor• Reservoir

modeling accuracy

Drive• Reservoir

drive mechanism

Factors AffectingRECOVERABLE

RESERVES

40

Physical Rock Properties

• Reservoir aerial extent

• Porosity• Permeabilit

y

OIL &GAS ECONOMICSOIL &GAS ECONOMICS

Downhole• Quality of

completions

Regulations• State

mandated allowables

ProductionFaciliities

• Capacity of Facilities

Factors AffectingPRODUCTION RATES

41

Reservoir• Rate of

Depletion• Byproducts

produced

OIL &GAS ECONOMICSOIL &GAS ECONOMICS

Royalties• Amount

paid to property owners

• Over-ride agreements

Factors AffectingROYALTIES &

WORKING INTEREST

42

Working Interest

• Major player or not

OIL &GAS ECONOMICSOIL &GAS ECONOMICS

Well Cost• Depth of

well• Amt of

logging• Byproducts

produced• Drilling

costs• Enhanced

recovery needed

Financial• Proximity to

market• Insurance

Costs

Operating• Disposal

Needed• Fuel costs• Personnel costs

& benefits

Factors AffectingOPERATING &

INVESTMENT COSTS

43

Production Facilities

• Design Efficiency

• Volume capacity

OIL &GAS ECONOMICSOIL &GAS ECONOMICS

Tax code is written specifically for O&G investing, is complex and must be handled by specialist

Factors AffectingO&G TAX

ACCOUNTING

44

OIL & GAS ECONOMICSOIL & GAS ECONOMICS

45

All of these factors result in an economic calculation to

determine the profitability of the project

The economic calculation is a called a

Net Present Value (NPV) calculation

NPV = ∑ (Income – Expense)*(1+DR)^t

The following examples will make this understandable…

OFFSHORE GOM, BAHA #2OFFSHORE GOM, BAHA #2

46

FUTURE PRODUCTION OFFSHOREFUTURE PRODUCTION OFFSHORE

47

SIMPLE NET PRESENT VALUESIMPLE NET PRESENT VALUE

48

OFFSHORE, GULF OF MEXICO, BAHA FIELD PRODUCING 100,000 BOPD INITIALLY

DECLINING EXPONENTIALLY OVER 10 YEARS

INFLATION DATA IS FROM

APRIL 1999 TO APRIL 2000

OTHER INVESTMENT RETURNSOTHER INVESTMENT RETURNS

52

STOCK DATA IS FROM APRIL 1999 TO APRIL

2000

OTHER INVESTMENT RETURNSOTHER INVESTMENT RETURNS

53

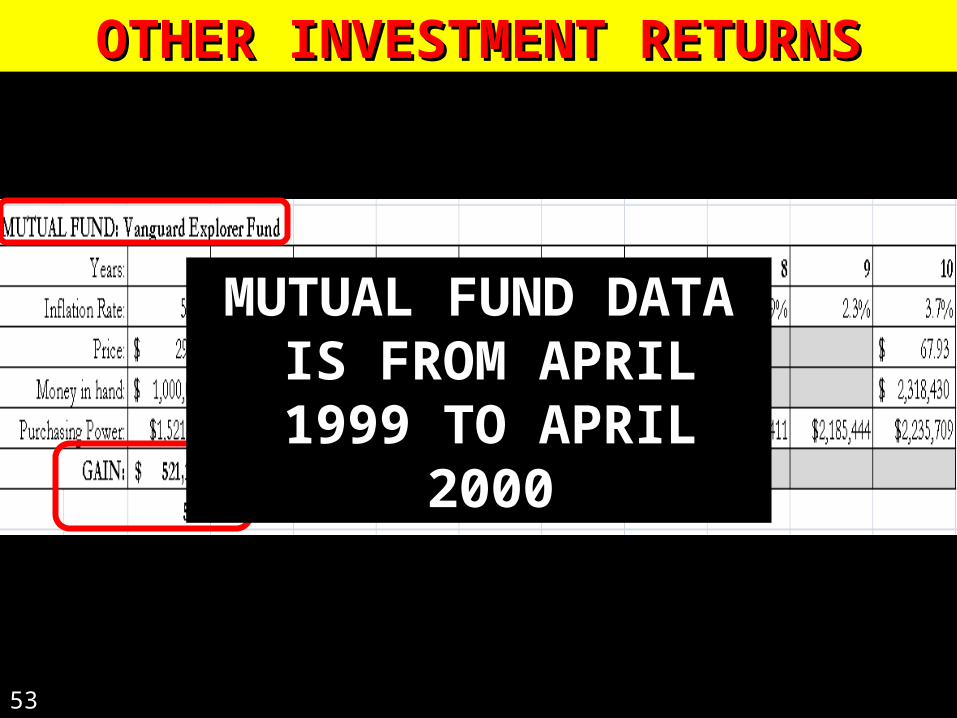

MUTUAL FUND DATA IS FROM APRIL 1999 TO

APRIL 2000

OTHER INVESTMENT RETURNSOTHER INVESTMENT RETURNS

54

INFLATION DATA IS FROM

APRIL 1999 TO APRIL 2000

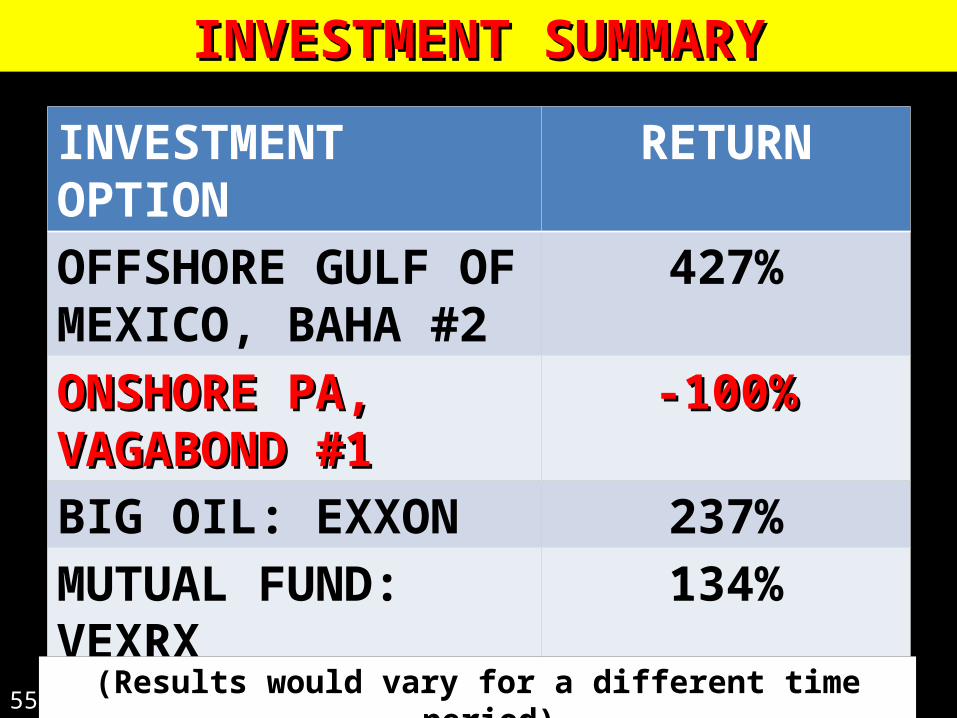

INVESTMENT SUMMARYINVESTMENT SUMMARY

55

INVESTMENT OPTION RETURNOFFSHORE GULF OF MEXICO, BAHA #2

427%

ONSHORE PA, ONSHORE PA, VAGABOND #1VAGABOND #1

-100%-100%

BIG OIL: EXXON 237%MUTUAL FUND: VEXRX 134%UNDER MATTRESSUNDER MATTRESS -11.4%-11.4%

(Results would vary for a different time period)

3 people made more than $5,000,000!$5,000,000!

‘Slim’ ‘Belle’s well’ Phyllis Dolich

PARTICIPANT RESULTSPARTICIPANT RESULTS% of Class% of Class Range of Range of ReturnsReturns

4%4% greater than greater than 5X5X the investmentthe investment

67%67% between between 2X to 5X 2X to 5X the investmentthe investment28%28% between between 1X to 2X1X to 2X the investment the investment1%1% ………………………………Lost it ALL!………………….Lost it ALL!………………….

VAGABOND OIL GROUPVAGABOND OIL GROUP

57

CONGRATSCONGRATSTo all theTo all the

Black Gold Black Gold Millionaires!Millionaires!

NEXT FALL?NEXT FALL?

Vagabonds Vagabonds TrampingTramping

the East African Riftthe East African Rift

EgyptEgypt

NEXT FALL?NEXT FALL?

Nile RiverNile River

Lake TanganyikaLake Tanganyika

The SerengetiThe Serengeti

Victoria FallsVictoria Falls

Zambezi RiverZambezi River

Mt KilimanjaroMt Kilimanjaro

Great Rift ValleyGreat Rift Valley

KenyaKenya

TanzaniaTanzania

ZimbabweZimbabwe

Hope to se

e you in September!

Hope to se

e you in September! EgyptEgypt

Thanks for the help . Thanks for the help . . .. .

Lynn LidelLynn LidelMargaret RaperMargaret Raper

THE ENDTHE ENDVAGABOND OIL GROUPVAGABOND OIL GROUP

61http://www.youtube.com/watch?v=Q9gGqNUxQ5Q

BOOKS/ARTICLES• Petroleum Geology, Exploration, Drilling, and Petroleum Geology, Exploration, Drilling, and

Production Production by Norman J. Hyne PhDby Norman J. Hyne PhD

• Money in the Ground Money in the Ground by John Orban, IIIby John Orban, III

• Let’s Talk Oil Deal Let’s Talk Oil Deal by John Orban, IIIby John Orban, III

• Economic Evaluation and Investment Decision Economic Evaluation and Investment Decision Methods Methods by Franklin J & John M. Stermoleby Franklin J & John M. Stermole

• Financial Accounting for Upstream Oil & Gas Financial Accounting for Upstream Oil & Gas ActivitiesActivities, Professional Development Institute, , Professional Development Institute, University of North TexasUniversity of North Texas

• Choosing a Perforation StrategyChoosing a Perforation Strategy, Schlumberger, Schlumberger

PERSONAL CONTACTS• Mike BeaumontMike Beaumont, Petroleum Engineer & , Petroleum Engineer &

Independent O&G Consultant, EuropeIndependent O&G Consultant, Europe

• David KarrsDavid Karrs, Petroleum Engineer, Chevron, , Petroleum Engineer, Chevron, USAUSA

• Bob GowerBob Gower, Finance & Accounting, Chevron, , Finance & Accounting, Chevron, Houston, TexasHouston, Texas

• Keith SeanardKeith Seanard, PE & Exploitation Mgr., Swift , PE & Exploitation Mgr., Swift Energy, Houston, TexasEnergy, Houston, Texas

• Frank KellyFrank Kelly, Petroleum Engineer, , Petroleum Engineer, Schlumberger, DubaiSchlumberger, Dubai

• Tako KoningTako Koning, Geologist & Independent O&G , Geologist & Independent O&G Consultant, West AfricaConsultant, West Africa

• Robin WrigleyRobin Wrigley, Independent O&G Consultant, , Independent O&G Consultant, UKUK

Petroleum Engineer - REFERENCESREFERENCES• http://www.observationsandnotes.blogspot.com/2009/04/http://www.observationsandnotes.blogspot.com/2009/04/

best-worst-10-years-in-stock-market.html best-worst-10-years-in-stock-market.html • http://www.glossary.oilfield.slb.com/default.cfm • http://www.123rf.com/search.php?

word=oil_well&start=60&searchopts=&itemsperpage=60

INTERNET

62

• http://observationsandnotes.blogspot.com/2009/03/http://observationsandnotes.blogspot.com/2009/03/average-annual-stock-market-return.html average-annual-stock-market-return.html • http://www.energyindustryphotos.com/

oilfield_blowout_photos_and_rig.htm • http://www.rigzone.com/news/article.asp?a_id=115612

OIL &GAS ECONOMICSOIL &GAS ECONOMICS

OPEC MEMBERSHIP

63

Saudi ArabiaSaudi Arabia IranIranAlgeriaAlgeria AngolaAngolaEcuadorEcuador IraqIraqKuwaitKuwait LibyaLibyaNigeriaNigeria QatarQatarUAEUAE VenezuelaVenezuela

Gabon & Indonesia are former members

WIND ENERGYWIND ENERGY

64

WIND ENERGYWIND ENERGY

65

1 natural gas well produces: 2,400,000 cu ft per day

Or 100,000 cu ft/hour

Natural gas has approx. 1,000 BTU per cu ft

Therefore 1 well produces: 100,000,000 BTU per hour

1 standard wind turbine produces: 6,824,284 BTU/hr(2.0 MW wind turbine)

Therefore, 1 well is equivalent to 14.7 wind turbines (in the amount of energy produced)

WIND ENERGYWIND ENERGY

66

6400 ft

8300 ft

15 turbines15 turbinesneedneed

1,220 acres1,220 acres

15 turbines15 turbinesneedneed

1,220 acres1,220 acres

• 1 well takes 5 acres5 acres to drill; 15 wind turbines need 1,220 acres

• Therefore, wind turbines need 244X as much space and 4X as many roads

• 1 well cost = $2.1 million; 15 wind turbines = $52.5 million

• Therefore, wind turbines are 25X more expensive for the same amount of energy

67

Select investment time period

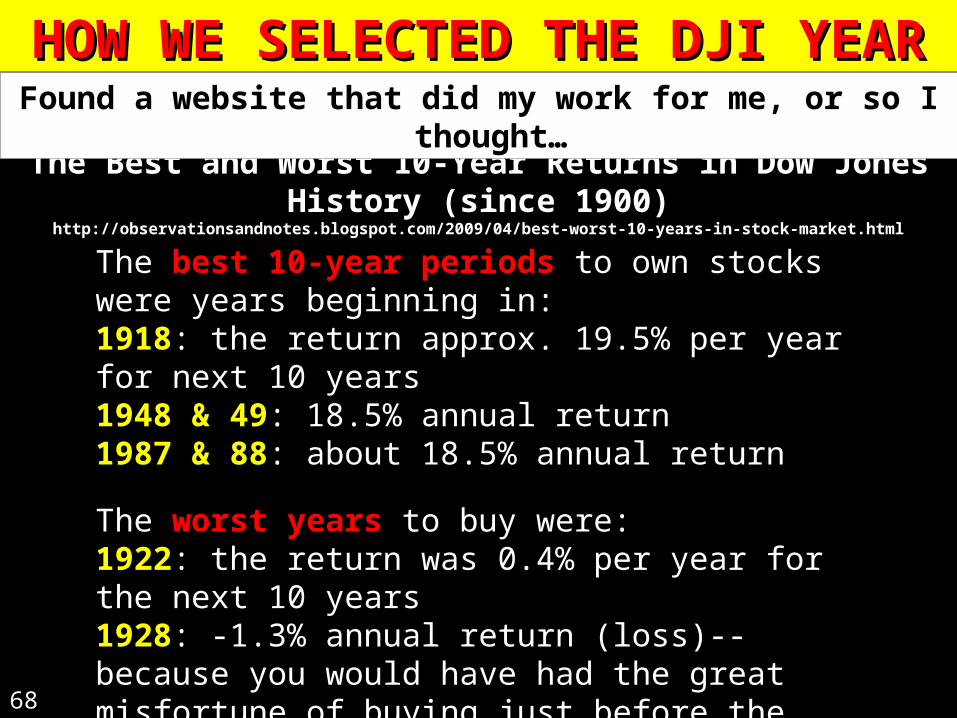

HOW WE SELECTED THE DJI YEARHOW WE SELECTED THE DJI YEAR

68

The best 10-year periods to own stocks were years beginning in:1918: the return approx. 19.5% per year for next 10 years 1948 & 49: 18.5% annual return 1987 & 88: about 18.5% annual return

The worst years to buy were:1922: the return was 0.4% per year for the next 10 years 1928: -1.3% annual return (loss)-- because you would have had the great misfortune of buying just before the 1929-1932 stock market crash. 1964: annual return of 0.3%

The Best and Worst 10-Year Returns in Dow Jones History (since 1900)http://observationsandnotes.blogspot.com/2009/04/best-worst-10-years-in-stock-market.html

Found a website that did my work for me, or so I thought…

HOW WE SELECTED THE DJI YEARHOW WE SELECTED THE DJI YEAR

69

Then used their chart to select years with average returns

HOW WE SELECTED THE DJI YEARHOW WE SELECTED THE DJI YEAR

70

But Exxon’s chart only goes back to 1970;Since most of Best/Worst years were before 1970, I

had to start over

DOW JONES INDUSTRIAL INDEX (‘70-’12)DOW JONES INDUSTRIAL INDEX (‘70-’12)

71http://finance.yahoo.com/charts#chart8:symbol=%5Edji;range=19700127,20120128;indicator=volume;charttype=line;crosshair=on;ohlcvalues=0;logscale=off

So, used the DJI chart from 1970 to present and selected 10 periods that gave a “normal”

distribution of possible returns

HOW WE SELECTED THE DJI YEARHOW WE SELECTED THE DJI YEAR

72 > > 12.512.5

%%

>4.0%< >4.0%< 12.5%12.5%

< < 4.0%4.0%

HOW WE SELECTED THE DJI YEARHOW WE SELECTED THE DJI YEAR

73

SORTED BY Order Picked out of Hat

Selection Start End Begin End 10 YR % Compd

Order Date Date Years Dow Dow Diff Return Annually

1 Jan-94 Jan-04 10.0 3636 10357 6721 184.8% 11.03%

2 Jan-99 Jan-09 10.0 9786 8447 -1339 -13.7% -1.46%

3 Jul-97 Jul-07 10.0 7945 13896 5951 74.9% 5.75%

4 Jan-85 Jan-95 10.0 1267 4158 2891 228.2% 12.61%

5 Jan-95 Jan-05 10.0 4157 10504 6347 152.7% 9.71%

6 Oct-89 Oct-99 10.0 2753 11497 8744 317.6% 15.36%

7 Apr-90 Apr-00 10.0 2881 10447 7566 262.6% 13.74%

8 Jan-02 Jan-12 10.0 10404 12980 2576 24.8% 2.24%

9 Jan-73 Jan-83 10.0 951 1130 179 18.8% 1.74%

10 Jan-87 Jan-97 10.0 2305 6583 4278 185.6% 11.06%

Don was asked to select a number from 1 to Don was asked to select a number from 1 to 10; he chose 7 10; he chose 7

74

O&G Economic Overview

75

Balancing RisksBalancing Risks

• 3000 Oil & Gas Companies in the USA3000 Oil & Gas Companies in the USA• 2 Key Attributes: 2 Key Attributes: Finding O&GFinding O&G & & Managing RiskManaging Risk

• What What riskrisk you say??.... you say??....

Company ACompany A StrengthStrength WeaknessWeakness

Company BCompany B WeaknessWeakness Strength Strength

Company CCompany C StrengthStrength StrengthStrength

76

Risk MitigationRisk Mitigation

Include table from Money in the Ground, page 212, figure

“To what extent can O&G Investments risks be avoided,

controlled or minimized?

From “Money in the Ground” by Orban

If you do:

• DUE DILIGENCE• PLANNING &• THOUGHTFUL

PREPARATIONYou can avoid:• 100% stupid mistakes• 80% of excessive drlg costs• 70% of excessive prod costs• Etc.

SIX PRINCIPLE ECONOMIC FACTORSSIX PRINCIPLE ECONOMIC FACTORS

77

(and attributes that cause (and attributes that cause riskrisk of that factor)of that factor)

• Price of oil (POO) Price of oil (POO) (OPEC’s “mood”, worldwide supply/demand, (OPEC’s “mood”, worldwide supply/demand, weather, market speculation, standby production capacity, political weather, market speculation, standby production capacity, political instabilities, refining capacity, etc.)instabilities, refining capacity, etc.)

• Recoverable Reserves (RR) Recoverable Reserves (RR) (reservoir aerial extent, thickness, (reservoir aerial extent, thickness, porosity, permeability, reservoir drive mechanism, etc.)porosity, permeability, reservoir drive mechanism, etc.)

• Production Rate (PR) Production Rate (PR) (State mandated Allowables, depletion (State mandated Allowables, depletion curve, byproducts produced, etc.)curve, byproducts produced, etc.)

• Operating & Investment Cost (OIC) Operating & Investment Cost (OIC) (depth of well, (depth of well, byproducts produced, proximity to market, steel supply/demand, type byproducts produced, proximity to market, steel supply/demand, type drilling contract, amount of logging done, volume capacity of producing drilling contract, amount of logging done, volume capacity of producing facilities, disposal issues, water and fuel source, insurance cost, etc.)facilities, disposal issues, water and fuel source, insurance cost, etc.)

SIX PRINCIPLE ECONOMIC FACTORSSIX PRINCIPLE ECONOMIC FACTORS

78

• Ownership: Working Interest, Royalties & Ownership: Working Interest, Royalties & Overrides (WI, ROY, OR) Overrides (WI, ROY, OR) (ownership subject to priority (ownership subject to priority overrides, calculating working interest in O&G properties is not overrides, calculating working interest in O&G properties is not straightforward as you might think)straightforward as you might think)

• Oil & Gas Accounting (TAX) Oil & Gas Accounting (TAX) (tax code is written specifically (tax code is written specifically for O&G investing, is complex and must be handled by specialist; for O&G investing, is complex and must be handled by specialist; accounting methods of successful efforts or full cost; handling of accounting methods of successful efforts or full cost; handling of depletion allowance, etc.)depletion allowance, etc.)

(and attributes that cause (and attributes that cause riskrisk to that factor)to that factor)

Distribution of USA Wells by ProductionDistribution of USA Wells by Production

77.4% of all USA Producing wells

produce less than

10 BOPD

35% of all USA Producing wells

produce between

0 & 1 BOPD

98.5% of all USA Producing wells produce

less than 100 BOPD

79

80

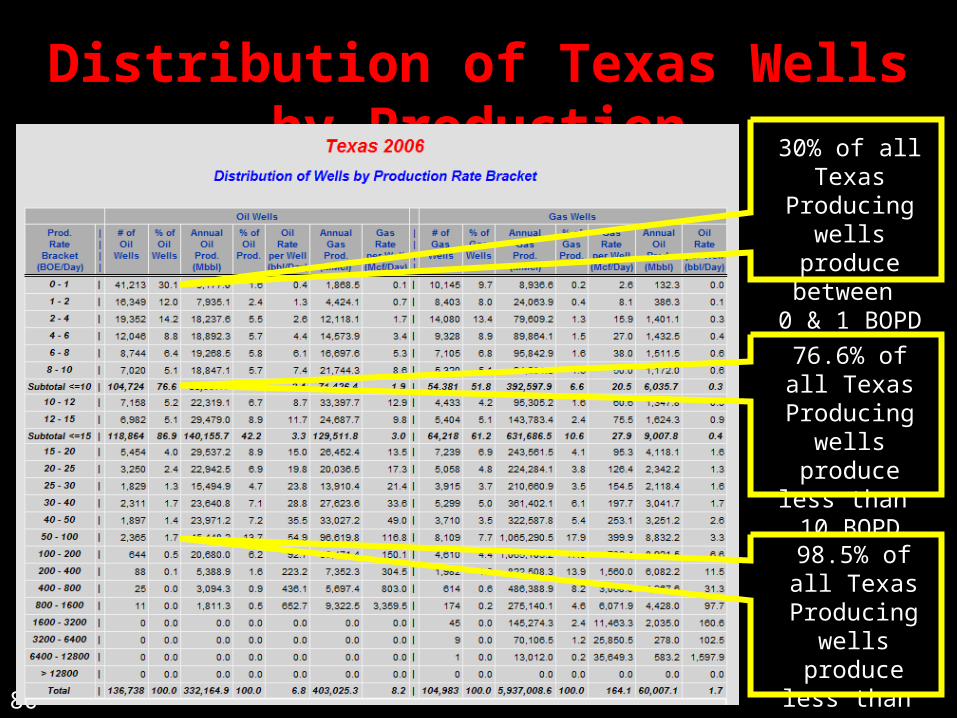

Distribution of Texas Wells by ProductionDistribution of Texas Wells by Production

76.6% of all Texas Producing

wells produce less than 10 BOPD

30% of all Texas Producing wells

produce between

0 & 1 BOPD

98.5% of all Texas

Producing wells produce less

than 100 BOPD

81

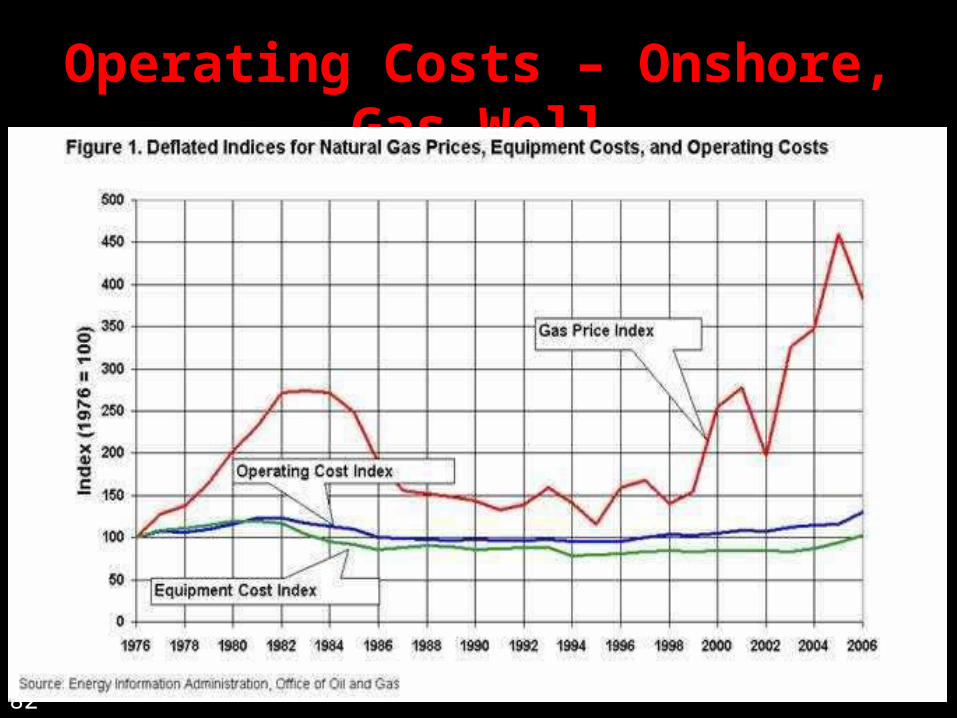

Operating Costs – Onshore, Oil WellOperating Costs – Onshore, Oil Well

82

Operating Costs – Onshore, Gas WellOperating Costs – Onshore, Gas Well

ECONOMIC ANALYSISECONOMIC ANALYSIS

83

• The bottomline in any financial investment The bottomline in any financial investment decision is what is the NPV (decision is what is the NPV (net present value of net present value of the cash flow streamthe cash flow stream) generated by this ) generated by this investmentinvestment

• NPV is therefore a combination of the six NPV is therefore a combination of the six principle factors in these generalized equations:principle factors in these generalized equations:

• RevenueRevenue = PR x POO x (WI+ROY-OR) = PR x POO x (WI+ROY-OR)

• CostsCosts = OIC x TAX adjusts = OIC x TAX adjusts

• NPVNPV = (Revenue – Costs) per period = (Revenue – Costs) per period discounted at some discount ratediscounted at some discount rate

ECONOMIC ANALYSISECONOMIC ANALYSIS

84

• In conjunction with NPV, modern risk analysis uses In conjunction with NPV, modern risk analysis uses Expected Value Theory for investing in a “pool” of Expected Value Theory for investing in a “pool” of propertiesproperties

• Example:Example:

(all costs in(all costs in

$1000’s)$1000’s)

• The cost of the “deal” should be no more than $150The cost of the “deal” should be no more than $150

Possible Outcomes

NPV Value

Probability of Outcome

Probability Weighted

Value

Successful WellSuccessful Well $1,000$1,000 10%10% $100$100

Successful WellSuccessful Well $250$250 20%20% $50$50

Dry HoleDry Hole $ 0$ 0 70%70% $ 0$ 0

Expected Expected Value Value $150$150

Very

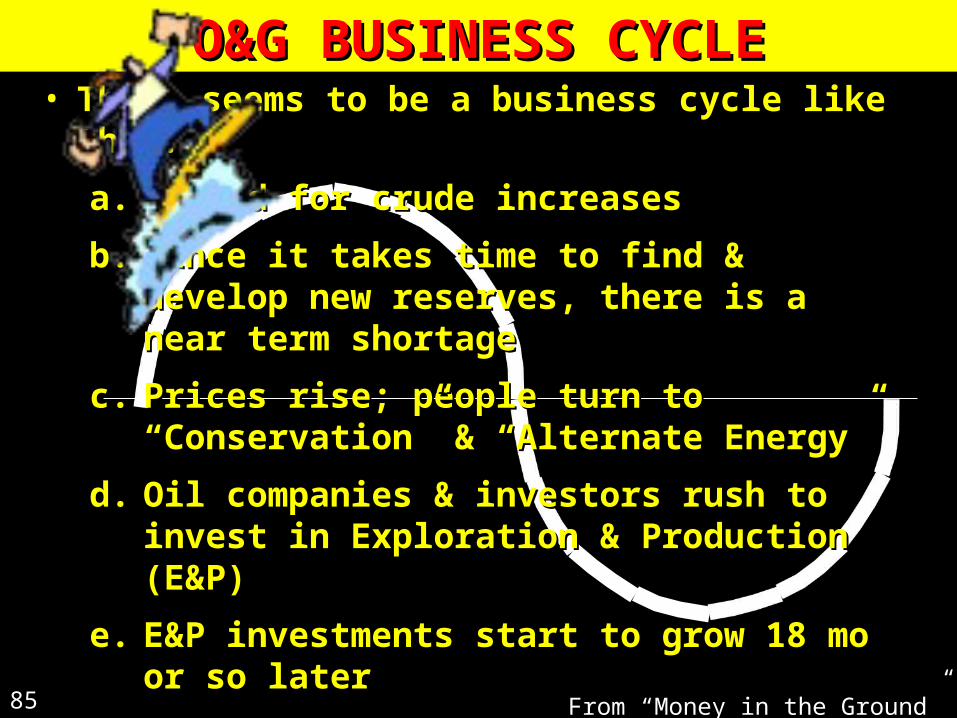

O&G BUSINESS CYCLEO&G BUSINESS CYCLE

85 From “Money in the Ground” by Orban

• There seems to be a business cycle like this:There seems to be a business cycle like this:

a.a. Demand for crude increasesDemand for crude increases

b.b. Since it takes time to find & develop new reserves, Since it takes time to find & develop new reserves, there is a near term shortagethere is a near term shortage

c.c. Prices rise; people turn to “Conservation” & Prices rise; people turn to “Conservation” & “Alternate Energy”“Alternate Energy”

d.d. Oil companies & investors rush to invest in Oil companies & investors rush to invest in Exploration & Production (E&P)Exploration & Production (E&P)

e.e. E&P investments start to grow 18 mo or so laterE&P investments start to grow 18 mo or so later

f.f. Supply floods the market, prices recede; people Supply floods the market, prices recede; people “forget” about conservation“forget” about conservation

g.g. Eventually, demand starts rising againEventually, demand starts rising again

ECONOMIC ANALYSISECONOMIC ANALYSIS

86

• In summary:In summary:• Oil & Gas investing is a risky businessOil & Gas investing is a risky business

• Understand the components of riskUnderstand the components of risk

• Invest with experienced, reputable companies with a Invest with experienced, reputable companies with a very good track record of both finding hydrocarbons and very good track record of both finding hydrocarbons and minimizing risksminimizing risks

• Use investment specialists as requiredUse investment specialists as required

• Catch the O&G business cycle at the right timeCatch the O&G business cycle at the right time

WHERE DID WEIRD IDEA COME FROM?WHERE DID WEIRD IDEA COME FROM?

88

Spotted the concept of an oil platform attacked on the web, of course. Built the idea

from there.