Embed Size (px)

Citation preview

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 1

Using single source data to precisely target and measure advertising’s

impact on sales to drive ROI

WAIC Conference – May 1, 2014 Nielsen Catalina Solutions

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 2

What we’ll cover

• Purchaser-centric approach

• Single source data

• Buyergraphics vs. demographics

• Driving retail sales and ROAS

• Case studies

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 3

Nielsen Catalina Solutions (NCS)Combining strengths of two industry leaders

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 4

TV Watch Data Nielsen Media Data +Millions of computer screens, Televisions, mobile phones

Buy Data Catalina Frequent Shopper Card Data

Nielsen Homescan All-Outlet DataClient Proprietary Sales Data

70 MM HH

ANONYMOUS SINGLE SOURCE HHs

WATCH

Matching what consumers watch and buy

Single Source

Households

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 5

STB4.3 MM

Households

Catalina FSD70 MM Households

HomeScan

100,000

NPM + MM

37,000

1.4 Million

NCS TV Single Source: Big, Smart Data

Quality = Scale & Representivity

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 6

Online portals & publishers

~100 MM HH

Catalina FSD70 MM HH

HomeScan

100,000

NOL100,000

16 Million

NCS Digital Single Source: Big, Smart Data

Quality = Scale & Representivity

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 7

Survey = Claimed Single Source

Households Demographics

Life Stage & Lifestyle

Increase in Data Precision

“Place an X by the product if youhave used it in the last 6 months”

ACTUAL CONSUMER RETAIL SALES DATA+ ACTUAL TV VIEWING

Survey BasedPurchaser

vs.

Single source provides greatest precision & ROAS

Single Source

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 8

47% of the brand’s volume reached by demographic target 53% of the brand’s volume is outside

the demographic target

BRANDVOLUME

53%

Today’s reality…demographic approach can miss over half your buyers

WOMEN

25-54 47%

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 9

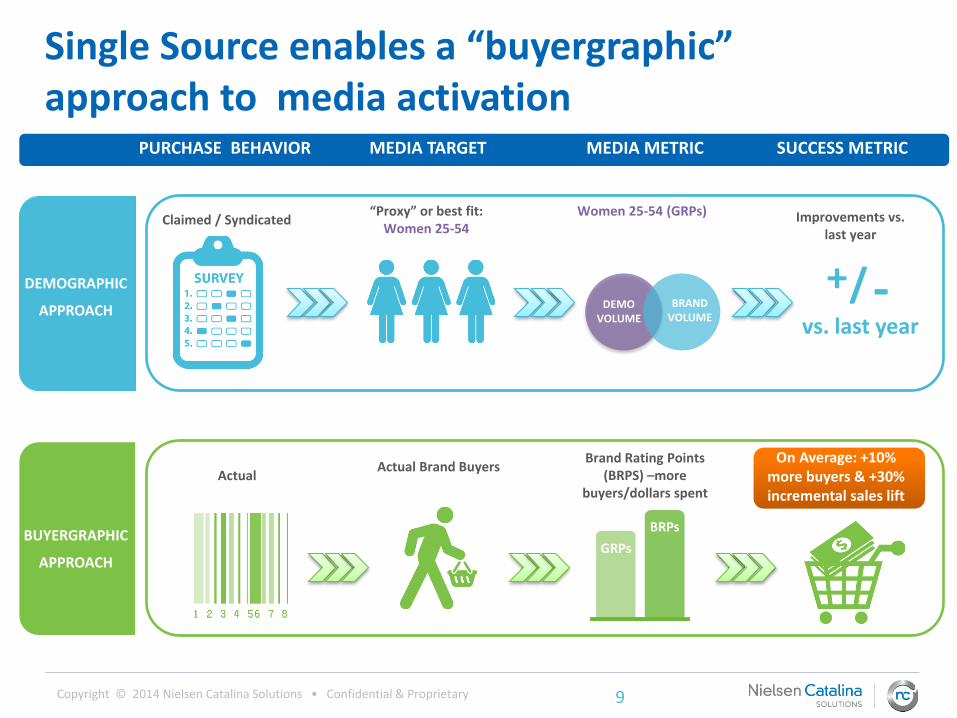

DEMOGRAPHIC

APPROACH

MEDIA TARGET

“Proxy” or best fit:Women 25-54

PURCHASE BEHAVIOR

Claimed / Syndicated

MEDIA METRIC

Women 25-54 (GRPs)

SUCCESS METRIC

Improvements vs. last year

BUYERGRAPHIC

APPROACH

Actual Brand BuyersActual

Brand Rating Points (BRPS) –more

buyers/dollars spent

On Average: +10%more buyers & +30% incremental sales lift

DEMOVOLUME

BRANDVOLUME

+ -/vs. last year

Single Source enables a “buyergraphic”approach to media activation

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 10

ASSESSDELIVERY

Post-buy analysis basedon purchasers

OPTIMIZEPLAN

Buyergraphics identify buyer-rich media for plans/allocations

SUPPORTACTIVATION

Support agency planning/buying

systems

SalesEffect

Studies

MEASURE SALES IMPACT

AdVantics™

Based onpurchase behavior

DEFINEAUDIENCE

Continuous Media Optimization Process

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 11

Case Studies

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 12

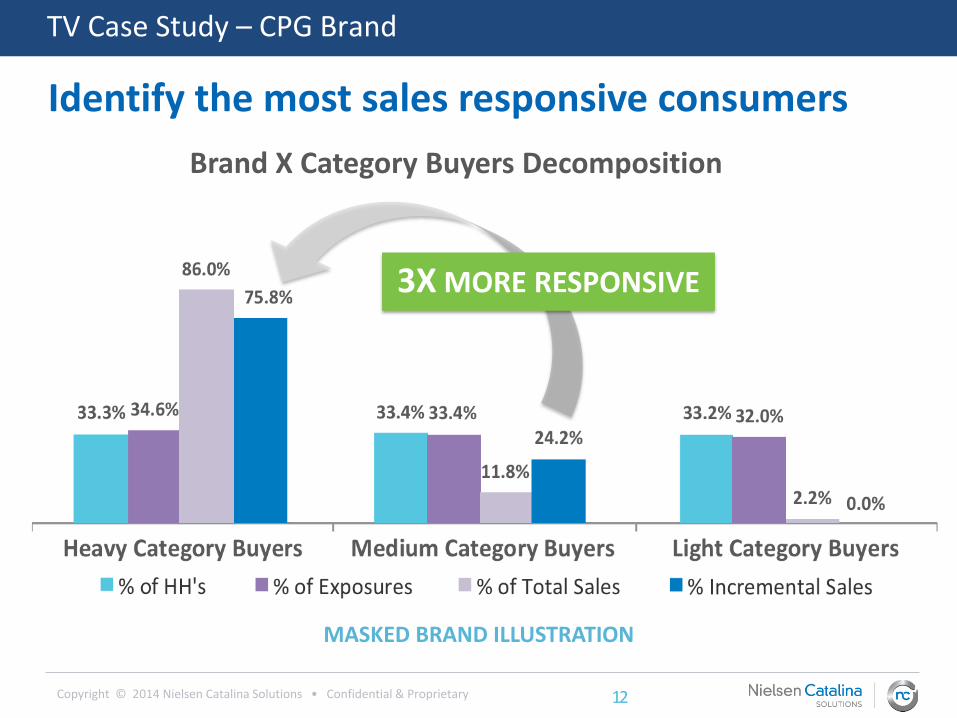

MASKED BRAND ILLUSTRATION

Brand X Category Buyers Decomposition

3X MORE RESPONSIVE

TV Case Study – CPG Brand

Identify the most sales responsive consumers

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 13

13%

TV Case Study – CPG Brand

TV-driven incremental sales increased by 20%

OriginalDemographic Based

$13,276 MM

Brand A

Original

20%

OptimizedBuyer Based

$15,931 MM

Optimized

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 14

Buyergraphic Optimization

BRAND X BUYERS

# Network Rating

1 ABC Family 0.51

2 E! 0.50

3 TBS 0.42

3 HGTV 0.42

5 TNT 0.37

6 WEtv 0.34

7 A&E 0.32

8 TLC 0.31

9 Bravo 0.29

10 Food Network 0.28

11 Lifetime 0.25

185 index

80% FEMALE

Source: Nielsen Media Research AdViews (4Q 2012-2Q 2013)

DemographicSelection

WOMEN 18-49

# Network Rating

1 TBS 0.57

2 ABC Family 0.47

3 A&E 0.43

3 TNT 0.43

5 TLC 0.38

6 Bravo 0.36

7 HGTV 0.35

7 Lifetime 0.35

9 Food Network 0.34

10 BET 0.29

11 E! 0.27

Case Study – TV Network

Finding Brand X buyers on Cable Networks

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 15

TV Case Study – CPG

TV campaign increased sales by >10%

Actual ROASD

EPLO

Y M

EDIA

CO

NTI

NU

OU

S M

EDIA

OP

TIM

IZA

TIO

N

Three strong Buyer Segments identified

Original

Network NBC CBS

HH GRP’s 2.9 3.0

Buyer Index

67 79

Har

ry’s

La

w

Ho

w I

Met

You

r M

oth

er67

79

TV schedule under-delivered buyer segments

Revised

Network NBC CBS

HH GRP’s 3.6 5.7

Buyer Index

126 108

The

Off

ice

Surv

ivo

r:O

ne

Wo

rld

126

108

Programs were shifted to reach buyers

Bu

yer

Segm

ent

A

Bu

yer

Segm

ent

B

~210 index

~400 index

Bu

yer

Segm

ent

C

~175 index

Buyer Index

> 10% Incremental Lift in

TV Driven Sales

Ori

gin

alD

emo

grap

hic

Bas

ed

Op

tim

ize

dB

uye

r B

ased

>10%

ID HIGH POTENTIAL BUYER SEGMENTS

OPTIMIZE MEDIA TO REACH BUYERS

MEASURE RESULTS

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 16

TV Case Study: Multiple CPG Brands

Marketing Situation:

• BRAND LOYALTY was DECLINING

• PURCHASE ON DEAL was INCREASING

• TV ROI was DECLINING

Problem: How to improve the TV ROI across entire Brand portfolio?

needs graphic design work

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 17

Buyergraphic targets were developed for each brand. Existing TV inventory was reallocated to better match programs with targets

Brands Original TV Target NCS Buyer-Based Target

Brand A A 25 – 39 Heavy Buyers of Brands w/ Similar Flavor and Type

Brand B A 35 – 49 Heavy Buyers of Competitive Brands

Brand C A 18 – 34 Heavy Buyers of Brands w/ Similar Flavor

Brand D A 18 – 34 Heavy Buyers of Category

Brand E M 25 – 34 Category Switchers

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 18

Media Results: 21% more BRPs were delivered to the entire brand portfolio after re-allocation

4,466 4,4664,989

6,046

Original Delivery NCS Re-AllocationGRPs BRPs

Q2 2013 National TV Inventory Re-Allocation

+21% BRPs

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 19

BRAND A BRAND B BRAND C BRAND D BRAND E

Q2 Original Delivery BRPs Q2 NCS Re-Allocation BRPs

% Increase 38% 22% 58% 32% 17%

Media Results: Each brand delivered more buyers after re-allocation

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 20

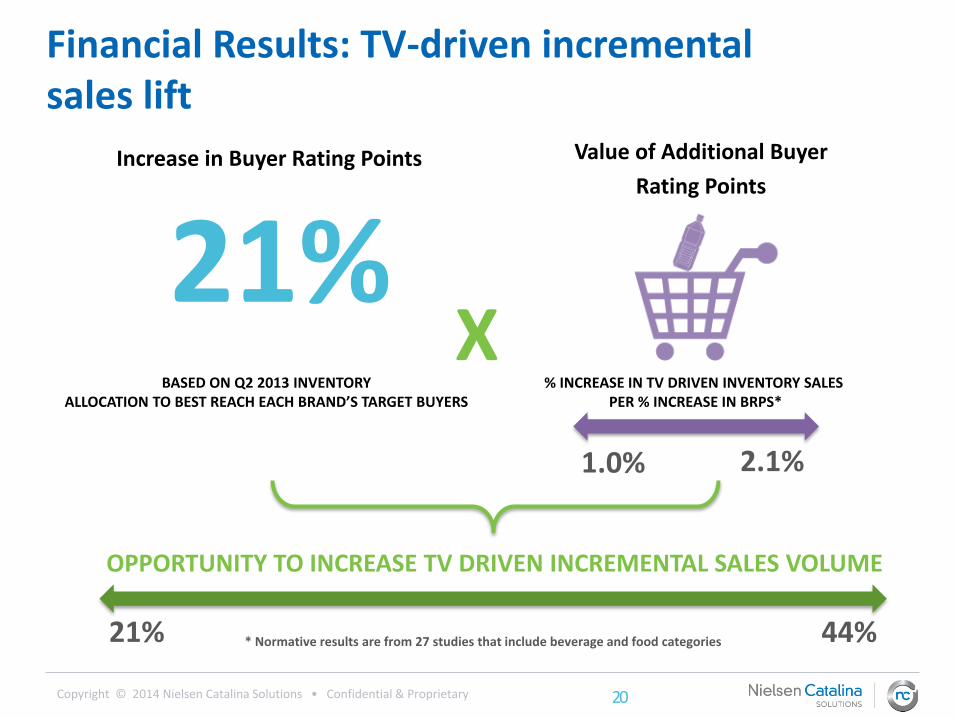

Financial Results: TV-driven incrementalsales lift

* Normative results are from 27 studies that include beverage and food categories

X

21% 44%

OPPORTUNITY TO INCREASE TV DRIVEN INCREMENTAL SALES VOLUME

Value of Additional Buyer

Rating Points

1.0% 2.1%

% INCREASE IN TV DRIVEN INVENTORY SALESPER % INCREASE IN BRPS*

Increase in Buyer Rating Points

21%BASED ON Q2 2013 INVENTORY

ALLOCATION TO BEST REACH EACH BRAND’S TARGET BUYERS

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 21

What’s driving sales?

TV

TV Driven Sales for Brand

BrandIncremental Sales due to

TV (MM)

% Increase in BRPs

Range in Incremental Sales Gain

(MM)

LowRange

HighRange

Brand A $21.9 38% $8.3 $11.8

Brand B $18.5 22% $4.1 $7.1

Brand C $25.8 40% $10.3 $14.4

Brand D $71.8 32% $22.9 $34.5

Brand E $2.7 17% $0.5 $0.9

Total Portfolio $140.7 $46.1 $68.7

Financial Results: Annual incremental sales increased $46MM – $69MM using buyerbased TV targeting

---

Marketing Mix

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 22

$43.5MMMedia

Spending

7,690HH GRPs

90%Reach

$199MM Incremental Sales$4.57 ROAS

4.5% Sales Uplift

ImpactExecution

NCS Holiday Campaign Sales Effect Measurement

TV Case Study – Retailer

TV campaign drove retailer’s sales at holiday

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 23

Digital Case Study – Ad Payback

Online Ads generate $3 for every $1 spend on advertising using purchaser information

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 24

Radio Case Study – Ad Payback

Radio is effective for driving sales!

Radio Payback per $1 Ad Investment

Ratio of incremental sales revenue per thousand to advertising cost per thousand = PaybackSource: Nielsen Catalina Solutions, Radio Ad Norms 2014

$11.15

Retail A

$6.21

All - Category Average

$1.81Breakfast Bar

$7.33Snacks A $4.17

Beer

$3.81Soft Drink A

$4.33Snacks B $23.21

Retail B

$1.38Soft Drink B

$3.12Candy

$1.97Soft Drink C

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 25

Compilation of 1,000+ studies across multiple categories

Control Exposed

+24%

Control Exposed

+22%

NCS Purchase-based Targeted Campaign

NCS Purchase-based Targeted Campaign

Case Study Compilation – Digital and TV

TV CampaignAverage Dollars Per Household

Control

+18%

Exposed

Digital CampaignAverage Dollars Per Household

Control

+17%

Exposed

Non-NCS Targeted Campaign

Demo-Targeted Campaign

NCS “buyergraphics” ~30% incremental retail sales lift

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 26

Single source data with purchaser-based targetscan drive sales and increase ROAS for all media

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 27

Final Thoughts --

TBD

TBD

TBD

TBD

Copyright © 2014 Nielsen Catalina Solutions • Confidential & Proprietary 28

Thank you!To learn more, contact:

Leslie [email protected]

www.ncsolutions.com