Embed Size (px)

Citation preview

The opinions expressed in this presentation are those of the speaker. The International Foundationdisclaims responsibility for views expressed and statements made by the program speakers.

Update on the Multiemployer Pension Reform Act (MPRA)

James K. Estabrook, Esq.ShareholderLindabury, McCormick, Estabrook & Cooper, P.C.Westfield, New Jersey

Randy G. DeFrehnExecutive DirectorNational Coordinating Committee for Multiemployer Plans (NCCMP)Washington, D.C.

Kevin J. McCaffrey, CEBSPresidentTeamsters Local 707Hempstead, New York

PO1-1

Nuts and Bolts of MPRA

• Strengthening pension benefit guaranty corporation

• Modifications to multiemployer rules– Amendments to Pension Protection Act of

2006

• Multiemployer plan mergers and partitions • Remediation measures for deeply troubled

plans

PO1-2

Strengthening PBGC

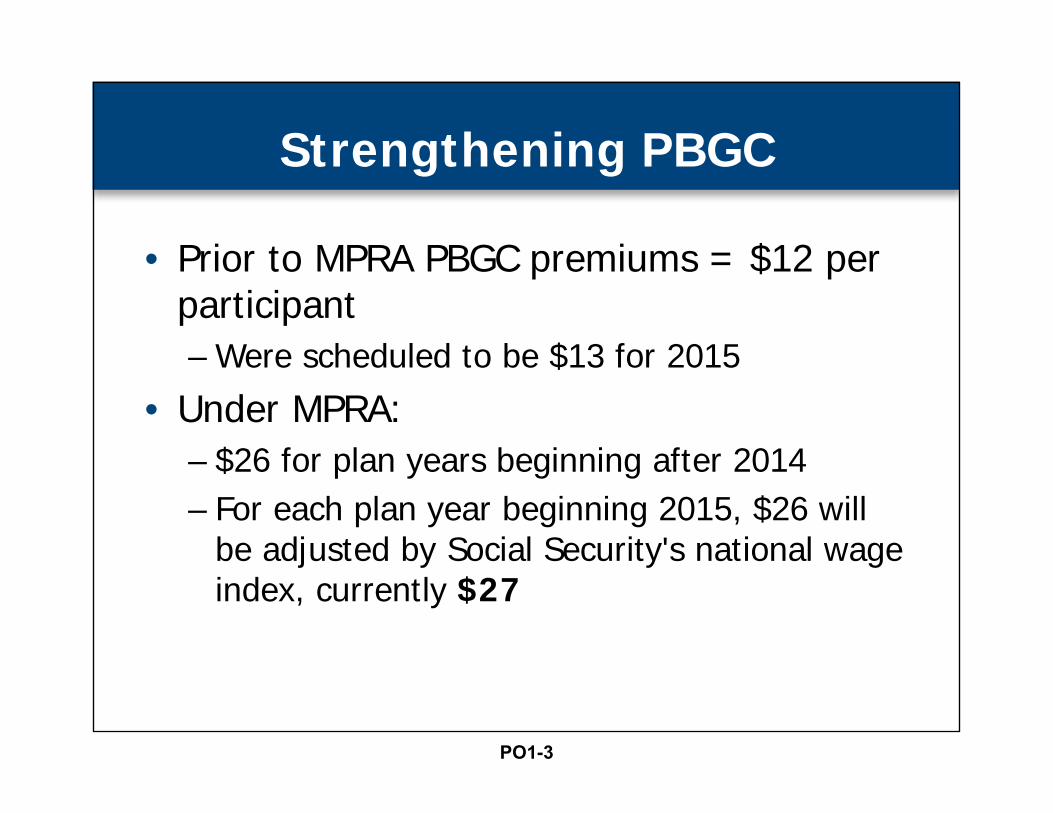

• Prior to MPRA PBGC premiums = $12 per participant– Were scheduled to be $13 for 2015

• Under MPRA:– $26 for plan years beginning after 2014– For each plan year beginning 2015, $26 will

be adjusted by Social Security's national wage index, currently $27

PO1-3

Strengthening PBGC

• Prior to MPRA, when PBGC determined its assets from multiemployer-fund premiums exceeded current needs, could request Treasury to invest such amounts in obligations issued or guaranteed by United States

• Under MPRA, minimum pools of assets must be held in noninterest-bearing accounts before further investments are made:– For fiscal year 2016 = $108,000,000– For fiscal year 2017 = $111,000,000– For fiscal year 2018 = $113,000,000– For fiscal year 2019 = $149,000,000; and– For fiscal year 2020 = $296,000,000

PO1-4

Strengthening PBGC

• PBGC’s financial assistance must be proportionately withdrawn from noninterest-bearing accounts and its other invested accounts

• PBGC required to report to Congress analyzing whether new MPRA premiums were sufficient

• Report issued June 17, 2016, reflects multiemployer program had a net deficit of $52.3 billion at end of 2015 ($54.2 billion/liabilities and $1.9 billion/assets) with a 50% chance of being insolvent by 2024 and 90% chance of being insolvent by 2028

• President’s 2017 budget proposal supports greater authority to PBGC to set premiums and raise $15 billion in next 10 years

PO1-5

Amendments to Pension Protection Act of 2006

• Repeal of sunset of PPA funding rules• Ten technical corrections:

1. Election to be in Critical Status2. Clarification of rule for emergence from Critical Status 3. Endangered Status not applicable if no additional action is

required4. Correct Endangered Status funding improvement plan target

funded percentage5. Conforming Endangered Status and Critical Status rules during

funding-improvement and rehabilitation plan adoption periods

PO1-6

Amendments to Pension Protection Act of 2006

6. Corrective plan schedules when parties fail to adopt in bargaining

7. Repeal of reorganization rules for multiemployer plans8. Disregard of certain contribution increases when

calculating withdrawal liability9. Guarantee for pre-retirement survivor annuities under

multiemployer pension plans10. Required disclosure of multiemployer plan information

PO1-7

PBGC Assistance for Multiemployer Fund Mergers

• If boards of trustees request a merger, PBGC may act to promote and facilitate merger if it determines transaction is good for participants of at least one fund and is not reasonably expected to be adverse to overall interests of participants of any of the funds

PO1-8

PBGC Assistance for Multiemployer Fund Mergers

• Such facilitation may include:– Training– Technical assistance– Mediation – Communication with stakeholders– Support with related requests to other government

agencies

• MPRA resurrects participant and plan sponsor advocate

PO1-9

PBGC Assistance for Multiemployer Fund Mergers

• PBGC may provide financial assistance to merged Fund if:– One or more of funds involved is in “critical

and declining status”– PBGC reasonably expects that financial

assistance will reduce its expected long-term loss with respect to the Funds involved

PO1-10

PBGC Assistance for Multiemployer Fund Mergers

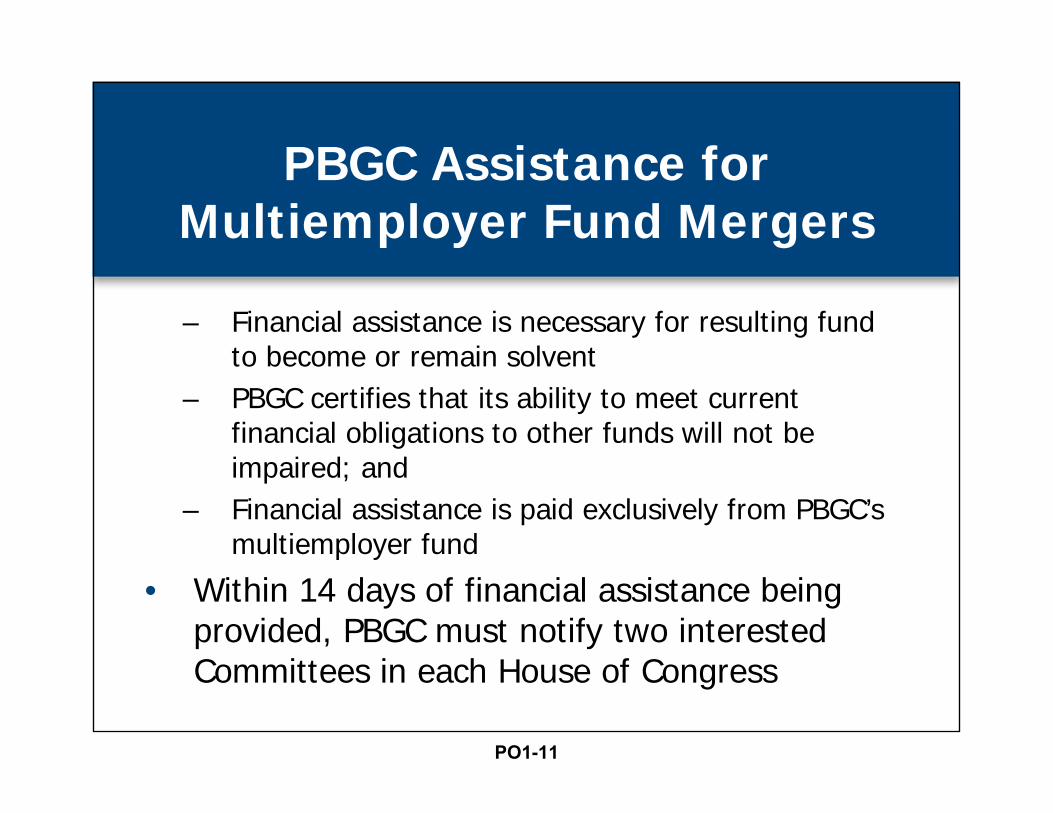

– Financial assistance is necessary for resulting fund to become or remain solvent

– PBGC certifies that its ability to meet current financial obligations to other funds will not be impaired; and

– Financial assistance is paid exclusively from PBGC’s multiemployer fund

• Within 14 days of financial assistance being provided, PBGC must notify two interested Committees in each House of Congress

PO1-11

Partitions of Eligible Multiemployer Funds

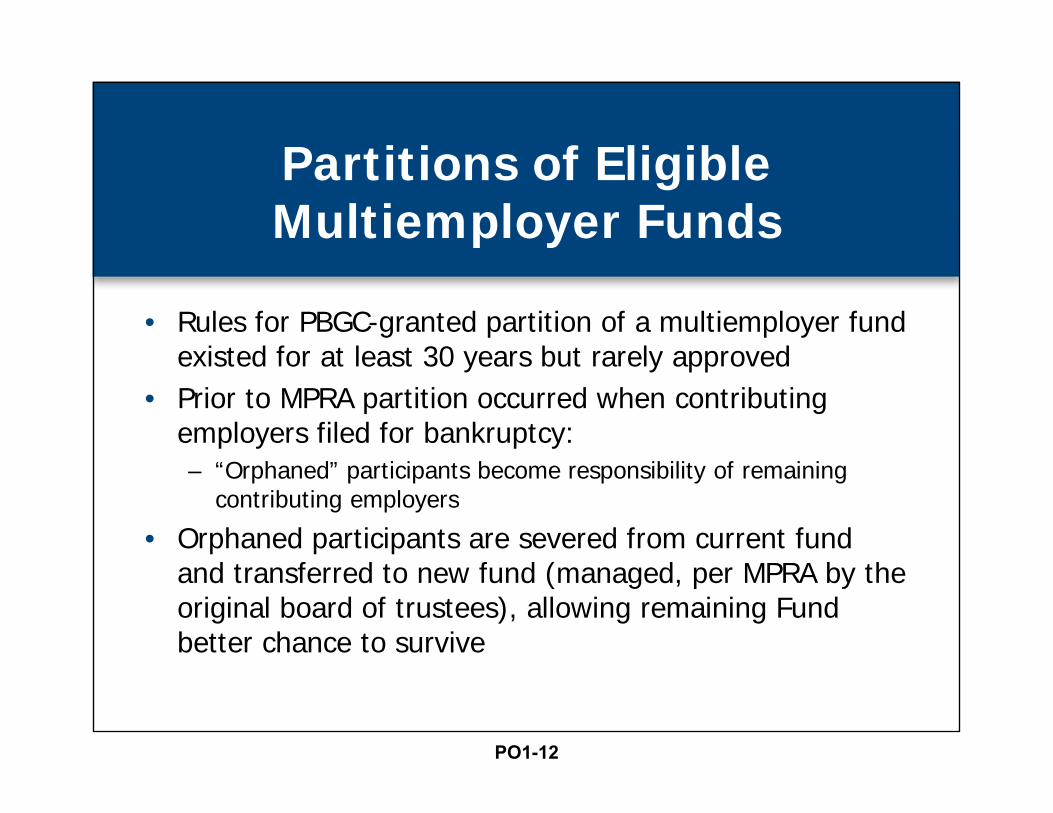

• Rules for PBGC-granted partition of a multiemployer fund existed for at least 30 years but rarely approved

• Prior to MPRA partition occurred when contributing employers filed for bankruptcy:– “Orphaned” participants become responsibility of remaining

contributing employers

• Orphaned participants are severed from current fund and transferred to new fund (managed, per MPRA by the original board of trustees), allowing remaining Fund better chance to survive

PO1-12

Partitions of Eligible Multiemployer Funds

• MPRA encourages partitions under following conditions:– Fund is in “critical and declining” status– Trustees have taken all reasonable measures

to avoid insolvency (including maximum allowed reductions of PPA’s adjustable benefits)

PO1-13

Partitions of Eligible Multiemployer Funds

– Partition will reduce PBGC’s expected long-term loss with respect to the fund and is necessary for fund to remain solvent

– PBGC certifies to Congress that such partition will not impair PBGC’s future ability to serve multiemployer community

– Paid exclusively from PBGC’s multiemployer-fund– Fund created by partition order will pay no more than

PBGC-guaranteed benefits; and – Partition transfers from original fund to new fund minimum

amount of liabilities necessary for original fund to remain solvent

PO1-14

Partitions of Eligible Multiemployer Funds Application

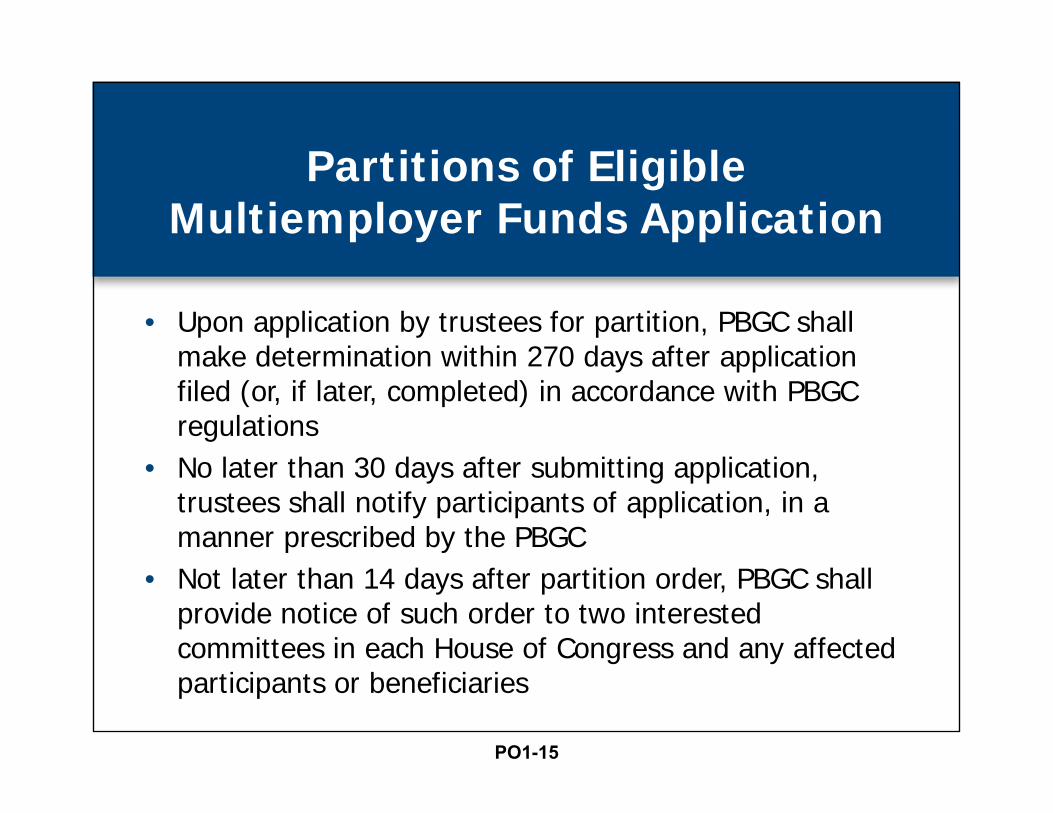

• Upon application by trustees for partition, PBGC shall make determination within 270 days after application filed (or, if later, completed) in accordance with PBGC regulations

• No later than 30 days after submitting application, trustees shall notify participants of application, in a manner prescribed by the PBGC

• Not later than 14 days after partition order, PBGC shall provide notice of such order to two interested committees in each House of Congress and any affected participants or beneficiaries

PO1-15

Partitions of Eligible Multiemployer Funds Operation

• If employer withdraws from fund that was partitioned– Within 10 years then withdrawal liability computed with respect to both

Funds involved– After 10 years then withdrawal liability computed only with respect to

original fund that was partitioned

• New fund pays benefits up to PBGC's benefit guarantees• Original fund pays any excess between what it had promised and

what new fund pays• For ten years after partition, original fund pays PBGC premiums for

both funds• If benefit improvement is adopted within 10 years of partition then

original fund makes restorative payments to PBGC, to be paid with premiums

PO1-16

Current StatusPBGC Assistance for Multiemployer Fund Mergers Partitions of Eligible

Multiemployer Funds

• Merger– No public information to date that PBGC has provided

any financial assistance to merge plans where one is in critical and declining status

• Partitions– Road Carriers—Local 707 Pension Fund, sought

partition under MPRA. Denied because in the PBGC’s opinion, the application failed to demonstrate that the plan would remain solvent following a partition

PO1-17

Remediation Measures forDeeply Troubled Plans

• New Zone Status—“Critical and Declining Status”– In Critical Status meeting any one or more

of the four tests– Projected to become insolvent within

• Current plan year or any of 14 succeeding plan years, or• Current plan year or any of 19 succeeding plan years if ratio of

inactive participants to active participants exceeds 2 to 1 or if funded percentage of the plan is less than 80%

– In making projections, plan actuary is to (i) assume that each employer in compliance with the rehabilitation plan will remain so for the entire rehabilitation period, and (ii) reflect prior benefit suspensions that are still in effect

PO1-18

Remediation Measures forDeeply Troubled Plans

• Duty of Disclosure and Reporting– Annual Funding Notice, issued no later than 120 days after

beginning of plan year, amended to provide• Status is “Critical and Declining”• Projected date of insolvency• Clear statement that insolvency may result in benefit reduction• Statement describing whether trustees have taken legally permitted

actions to prevent insolvency

– Annual Certification of Funded Status, issued no later than 90 days after beginning of plan year

• 41 plans listed in Critical and Declining Status on DOL site

PO1-19

Remediation Measures forDeeply Troubled Plans

• “Benefit Suspension”– Means, the temporary or permanent reduction of any

current or future payment obligation of the plan to any participant or beneficiary whether or not in pay status at the time of suspension

– Length of the suspension is the earlier of (i) when the Trustees provide a benefit improvement for those not in pay status; or (ii) the suspension of benefits expires by its own terms

PO1-20

Remediation Measures forDeeply Troubled Plans

• Conditions for Suspension– Plan actuary certifies that the plan will avoid

insolvency indefinitely assuming the proposed suspension of benefits and that they will continue until they expire by their own terms

– Trustees determine, through a written record, that the plan is projected to become insolvent unless benefits are suspended even though all reasonable measureshave been taken, and continue to be taken, to avoid insolvency

PO1-21

Remediation Measures for Deeply Troubled Plans

Factors that may be considered, in writing, in determining whether all reasonable measures to avoid insolvency have been and continue to be taken during benefit suspension:

• Current and past contribution levels• Levels of benefit accruals (including any

prior reductions in the rate of benefit accruals)

• Prior reductions (if any) of adjustable benefits

• Prior suspension (if any) of benefits• The impact on plan solvency of the

subsidies and ancillary benefits available to active participants

• Compensation levels of active participants relative to employees in the participants’ industry generally

• Competitive and other economic factors facing contributing employers

• The impact of benefit and contribution levels on retaining active participants and bargaining groups under the plan

• The impact of past and anticipated contribution increases under the plan on employer attrition and retention levels

• Measures undertaken by the Trustees to retain or attract contributing employers

PO1-22

Remediation Measures forDeeply Troubled Plans

• Limitations on Suspension– Monthly benefit of any participant may not be reduced below

110% of monthly benefit guaranteed by PBGC– No suspension of benefits based on disability– Limited percentage suspension for participants age 75 to 80– No suspension for participants who attained age 80 at time of

suspension

• Effective date of suspension of benefits cannot be before the effective date of partition

• Any suspension of benefits, in the aggregate, shall be reasonably estimated to achieve, but not materially exceed, the level that is necessary to avoid insolvency

PO1-23

Limitations on Suspension

Suspension must be “equitably distributed” across participant population, taking into account one or more of the following factors

• Age and life expectancy• Length of time in pay status• Amount of benefit • Type of benefit: survivor, normal

retirement, early retirement• Extent to which participant or beneficiary is

receiving a subsidized benefit• Extent to which participant or beneficiary

has received post-retirement benefit increases

• History of benefit increases and reductions• Years to retirement for active employees

• Any discrepancies between active and retiree benefits

• Extent to which active participants are reasonably likely to withdraw support for the plan, accelerating employer withdrawals from the plan and increasing the risk of additional benefit reductions for participants in and out of pay status

• Extent to which benefits are attributed to service with an employer that failed to pay its full withdrawal liability

PO1-24

Remediation Measures forDeeply Troubled Plans

• Approval process• Application to Treasury for approval, in consultation with

PBGC and DOL, that satisfies the criteria for conditions, limitations, benefit improvements and notice for suspension

• Thirty days after receipt of application Treasury shall, (i) publish notice in Federal Register soliciting comments, and (ii) publish the application on the Treasury website

PO1-25

Remediation Measures forDeeply Troubled Plans

• Approve or deny application within 225 days of submission. Deemed approved unless within 225 days Treasury notifies trustees that they failed to satisfy one of the criteria. Treasury must detail specific reasons for rejection.

• Trustees must concurrently provide notice to participants, beneficiaries, union and contributing employers detailing factors considered and estimate of impact on each participant. Model Notice provided by Treasury.

PO1-26

Remediation Measures forDeeply Troubled Plans

• Participant Ratification Required• Approved suspension must be submitted to vote of

participants and beneficiaries of the plan by Treasury no later than 30 days after its approval on ballot supplied by trustees

• Suspension goes into effect following vote unless a majority of all participants and beneficiaries of the plan vote to reject the suspension

• Treasury can override negative vote within 90 days if plan is a “systemically important plan”– Plan that PBGC projects will need assistance in excess of $1

billion (indexed) if suspensions are not implemented

PO1-27

Remediation Measures for Deeply Troubled Plans

• Judicial review• Trustees may seek judicial review only after application

for suspension is denied• Judicial review of approval of suspension may only be

brought after final Treasury authorization– No temporary injunction unless convincing likelihood plaintiff will

prevail on merits– Participants and beneficiaries do not have a cause of action

under title– Statute of limitations is one year

PO1-28

Remediation Measures forDeeply Troubled Plans

• Special Rules– Benefit improvements, while any suspension of benefits under

the plan remain in effect, are subject to separate “equitable distribution” rules

– Plans with 10,000 or more participants must select a retiree representative no later than 60 days prior to trustees’ submission to Treasury

• Must be a participant in pay status• Duty is to advocate for retired/deferred vested participants and

beneficiaries• Plan shall pay all expenses including legal and actuarial support

– Benefit reductions or suspension while in critical and declining status are disregarded for withdrawal liability purposes unless the withdrawal occurs more than 10 years after the effective date of the benefit suspension

PO1-29

Multiemployer PensionReform Act of 2014

Regulations• IRS Final Regulations, Section 1.432(e)(9), Suspension

of Benefits under the Multiemployer Pension Reform Act of 2014 (April 28, 2016)

• IRS Revenue Procedure 2016-27, Application Procedures for Approval of Benefit Suspensions for Certain Multiemployer Defined Benefit Pension Plans under §432(e)(9) with Model Notice, Power of Attorney and Checklist

PO1-30

Multiemployer PensionReform Act of 2014

• PBGC Interim Final Rule on Partitions of Eligible Multiemployer Plans with Model Notice as amended by Final Rule (12/23/15)

• PBGC Proposed Rule on Mergers and Transfers Between Multiemployer Plans (6/6/16)

PO1-31

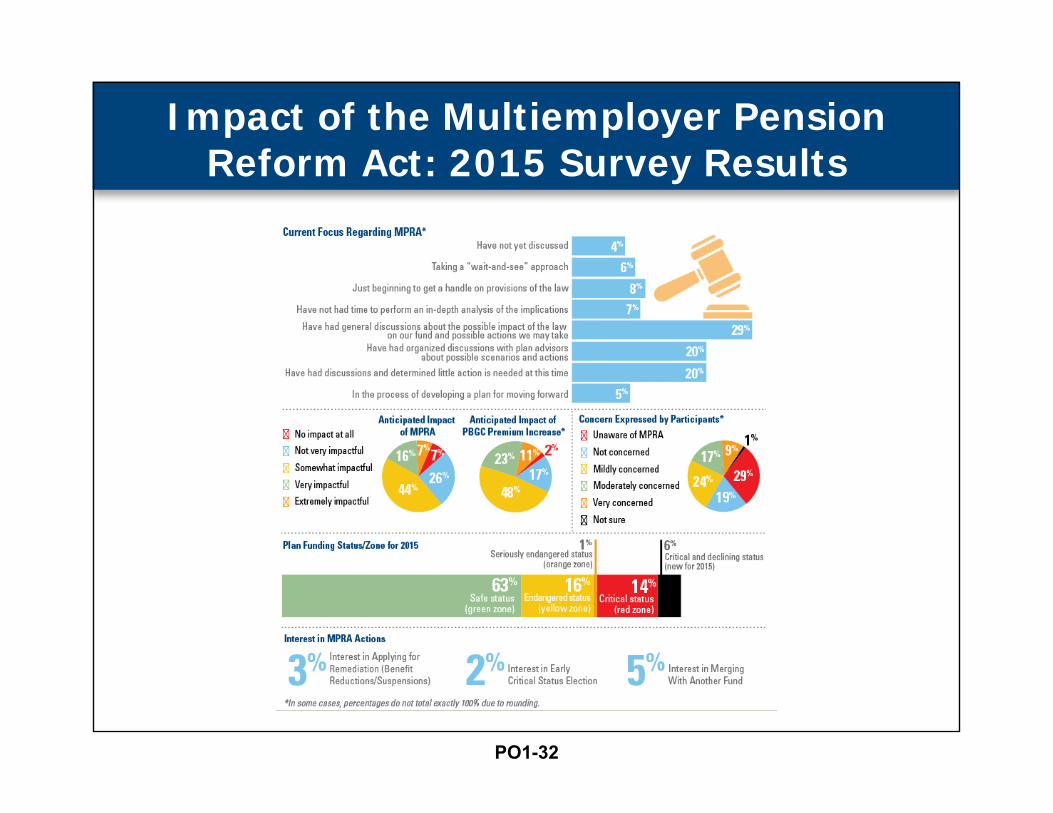

Impact of the Multiemployer Pension Reform Act: 2015 Survey Results

PO1-32

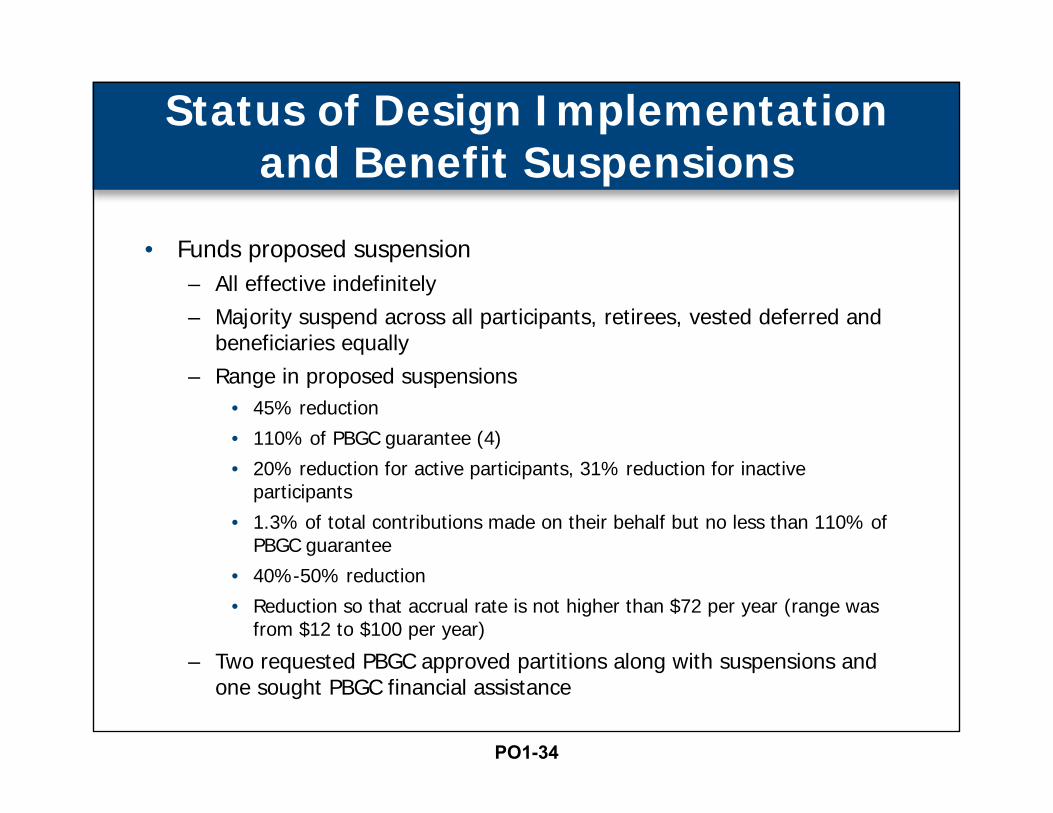

Status of Design Implementation and Benefit Suspensions

• Ten funds have filed for approval to suspend pension benefits

• Three have been denied, none approved, seven still under review– Ironworkers Local 16 Pension Fund (11/3/16)– Road Carriers—Local 707 (6/24/16)– Teamsters Central States Southeast and Southwest Areas

(5/6/16)• Two were withdrawn and resubmitted

– Ironworkers Local 17 Pension Fund (7/29/16)– Teamsters Local 469 Pension Fund (3/31/16)

PO1-33

Status of Design Implementation and Benefit Suspensions

• Funds proposed suspension– All effective indefinitely– Majority suspend across all participants, retirees, vested deferred and

beneficiaries equally– Range in proposed suspensions

• 45% reduction

• 110% of PBGC guarantee (4)

• 20% reduction for active participants, 31% reduction for inactive participants

• 1.3% of total contributions made on their behalf but no less than 110% of PBGC guarantee

• 40%-50% reduction

• Reduction so that accrual rate is not higher than $72 per year (range was from $12 to $100 per year)

– Two requested PBGC approved partitions along with suspensions and one sought PBGC financial assistance

PO1-34

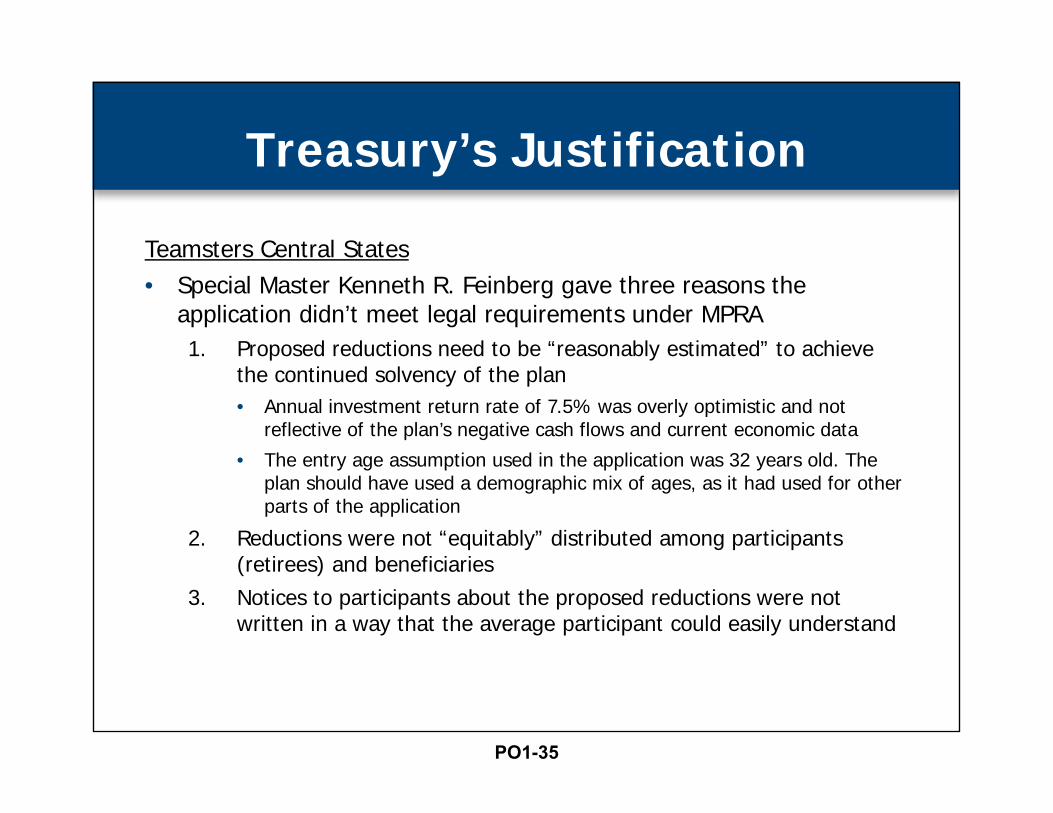

Treasury’s Justification

Teamsters Central States• Special Master Kenneth R. Feinberg gave three reasons the

application didn’t meet legal requirements under MPRA1. Proposed reductions need to be “reasonably estimated” to achieve

the continued solvency of the plan• Annual investment return rate of 7.5% was overly optimistic and not

reflective of the plan’s negative cash flows and current economic data

• The entry age assumption used in the application was 32 years old. The plan should have used a demographic mix of ages, as it had used for other parts of the application

2. Reductions were not “equitably” distributed among participants (retirees) and beneficiaries

3. Notices to participants about the proposed reductions were not written in a way that the average participant could easily understand

PO1-35

Alternatives are Unacceptable

• With PBGC’s projected insolvency, participants in plans unable to survive face even greater uncertainty– Absent significant premium increases or restructuring of the

guaranty program PBGC will exhaust its reserves within the next 10 years

– Benefits will be paid from cash flows—Projected to be as low as 10% of statutory amounts

– Magnitude of projected increases will overwhelm system and will almost certainly cause employers to follow single employer “flight”

– Alternatives include restructured premium and/or guaranty formulae, alternative risk pooling, and/or PBGC intervention to prevent shifting of risk

PO1-36

Websites

https://www.ifebp.org/news/featuredtopics/MPRA/Pages/default.aspx

https://blog.ifebp.org/index.php/central-states-benefit-reduction-application-denied-now-what

PO1-37

Key Takeaways

• MPRA’s intent has been mischaracterized– Objective is to allow plans to PRESERVE benefits above

PBGC guaranty levels

• Guidance on MPRA is a “work in progress”– Treasury’s last minute change regarding ROI made

Central States’ application moot

• Numerous funds are currently analyzing and/or preparing Treasury submissions

• With the election behind us decisions are more likely to be based on merit

• Absent enacted and signed bailout legislation, MPRA will still provide participants in critical and declining status plans with the greatest long-term retirement income security

PO1-38

2017 Educational ProgramsPensions

63rd Annual Employee Benefits Conference October 22-25, 2017Las Vegas, Nevadawww.ifebp.org/usannual

Trustees and Administrators InstitutesFebruary 20-22, 2017

Lake Buena Vista (Orlando), FloridaJune 26-28, 2017

San Diego, Californiawww.ifebp.org/trusteesadministrators

Certificate of Achievement in Public Plan Policy (CAPPP®)Part I and Part II, June 13-16, 2017

San Jose, CaliforniaPart II Only, October 21-22, 2017

Las Vegas, Nevadawww.ifebp.org/cappp

Related Reading

2016 Retirement Plans Facts | Item #9060 Visit one of the on-site Bookstore locations or see www.ifebp.org/bookstore for more books.

PO1-39

![[4830-01-p] DEPARTMENT OF THE TREASURY€¦ · Public Law 109-280 (120 Stat. 780 (2006)) (PPA ’06) and amended by the Multiemployer Pension Reform Act of 2014, Division O of the](https://img.dokumen.tips/doc/110x75/5f030e377e708231d4075062/4830-01-p-department-of-the-treasury-public-law-109-280-120-stat-780-2006.jpg)