Embed Size (px)

Citation preview

Unofficial Informal Business Discussion Minutes Tuesday, October 6, 2015 – 3:00 PM

Present: Charlotte J. Nash, Jace Brooks, John Heard Absent: Lynette Howard, Tommy Hunter

1. County Administration Economic Development: Georgia Law Presentation Dan McRae of Seyfarth Shaw, LLP presented information related to economic development tools available under Georgia law. No Official Action Taken.

Economic Development Tools Under Georgia Law

Daniel M. McRae, Partner Seyfarth Shaw LLP 1075 Peachtree Street, N.E. Suite 2500 Atlanta, GA 30309 404.888.1883 [email protected] danmcrae.com

Oct. 2015

STATE, LOCAL, AND FEDERAL

POLICIES

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

STATE

• GEORGIA IS COMPETITIVE IN ATTRACTING ECONOMIC DEVELOPMENT PROJECTS

• STATE INCENTIVES REFLECT STATE PRIORITIES AND POLITICAL AND FISCAL REALITIES

• OTHER STATES HAVE MANY OF THE SAME INCENTIVES

• STAND-OUT GEORGIA INCENTIVES ARE PRIMARILY CASH GRANTS (WHEN AVAILABLE) AND, IN ITS SECTOR, THE GEORGIA ENTERTAINMENT INDUSTRY INVESTMENT ACT ("FILM TAX CREDIT")

3 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

LOCAL

• LOCAL POLICIES ARE MORE REFLECTIVE OF LOCAL PRIORITIES

• LOCAL INCENTIVES ARE CONSTRAINED BY LOCAL RESOURCES

• FOREMOST LOCAL INCENTIVE IS PROPERTY TAX "ABATEMENT"

• OTHERS: COMMUNITY GRANTS, IN-KIND (LAND, SITE PREPARATION, ETC.)

4 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

FEDERAL

• FEDERAL PROGRAMS ARE DENSER, SLOWER, AND MORE DIFFICULT TO ACCESS

• RECENT POLICY CHANGES HAVE RE-ALIGNED SOME KEY PROGRAMS TO WORK BETTER WITH AREAS TARGETED BY THOSE PROGRAMS

• EXAMPLES- • EB-5 IMMIGRANT INVESTOR CAPITAL- FOR RURAL

AND HIGH UNEMPLOYMENT COMMUNITIES • NEW MARKETS TAX CREDITS- FOR LOW INCOME

COMMUNITIES

5 |

TARGETED INCENTIVES

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

LOCAL INCENTIVES

ALPHARETTA HAS DONE A GOOD JOB OF ASSEMBLING A BASKET OF STATE AND LOCAL INCENTIVES THAT IS PARTICULARLY ATTRACTIVE TO TECHNOLOGY COMPANIES

7 |

Source: http://growalpharetta.com/site-selectors/incentives/

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

GEORGIA INCENTIVES

8 |

AMONG ALL OF THE AVAILABLE INCENTIVES ON THE STATE LEVEL, ALPHARETTA HIGHLIGHTS THOSE THAT ARE MOST INTERESTING TO TECHNOLOGY COMPANIES

Source: http://growalpharetta.com/site-selectors/incentives/

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

LOCAL INCENTIVES

9 |

ALPHARETTA ALSO HAS DEVELOPED ITS OWN MENU OF LOCAL INCENTIVES

THIS IS "BONDS FOR TITLE" FOR PROPERTY TAX "ABATEMENT"

Source: http://growalpharetta.com/site-selectors/incentives/

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

CASH IS THE BEST INCENTIVE

10 |

A COMMUNITY GRANT PROGRAM HAS TO BE PROPERLY STRUCTURED IN ORDER TO AVOID VIOLATING THE PROHIBITION OF "GIFTS AND GRATUITIES" IN THE GEORGIA CONSTITUTION.

Source: http://growalpharetta.com/site-selectors/incentives/

AIMING HIGHER

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

CREATING A DESTINATION

Here are some case studies that show what can happen when the goal is attracting a cluster of businesses instead of a single economic development prospect.

12

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

TECH SQUARE PHASE 1

13

The Development Team Developer(s) Georgia Institute of Technology Jones Lang LaSalle (development manager) Designer(s) Thompson, Ventulett, Stainback & Associates

Economic Development Tool employed: Special zoning

Source: ULI (2008)

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

TECH SQUARE PHASE 2

14

"Atlanta real estate company Portman Holdings LLC will develop a $300 million mixed-use project and high-performance computing center for Georgia Tech in Midtown’s Technology Square." Source: Atlanta Business Chronicle

Source: Atlanta Business Chronicle

Economic Development Tools Sought: • Property tax

"abatement" • Others

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

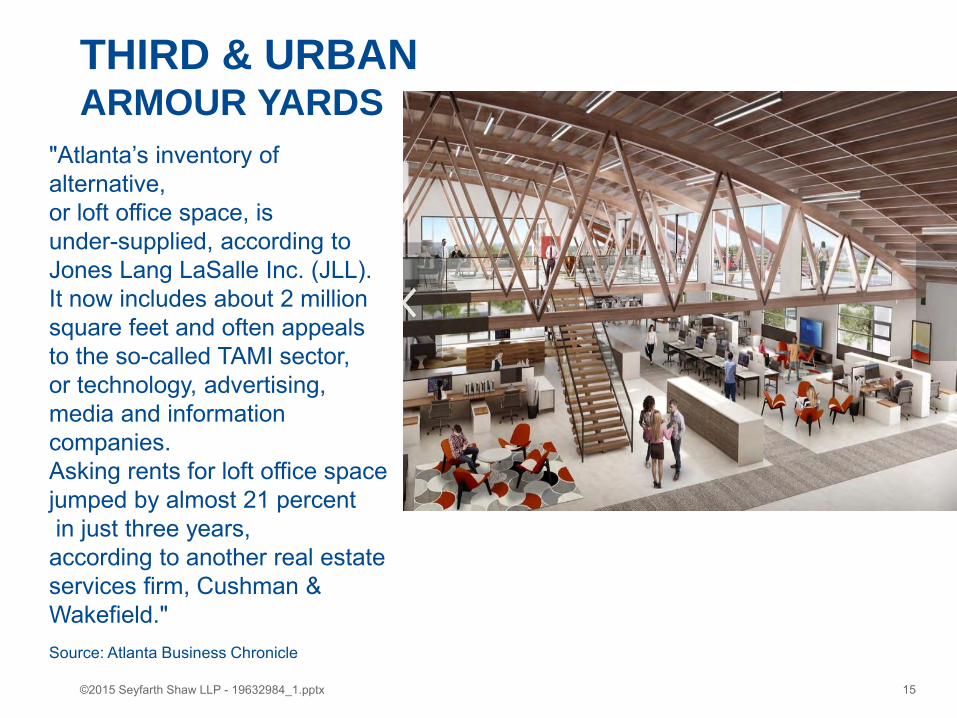

THIRD & URBAN ARMOUR YARDS

15

"Atlanta’s inventory of alternative, or loft office space, is under-supplied, according to Jones Lang LaSalle Inc. (JLL). It now includes about 2 million square feet and often appeals to the so-called TAMI sector, or technology, advertising, media and information companies. Asking rents for loft office space jumped by almost 21 percent in just three years, according to another real estate services firm, Cushman & Wakefield." Source: Atlanta Business Chronicle

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

THIRD & URBAN ARMOUR YARDS

16

"Its plans include converting the warehouses into loft offices, bringing in a coffee shop, and trying to land at least two chef-driven restaurants. It also wants to add a music venue, and it wouldn’t be surprising if Smith’s Olde Bar — which may have to relocate from its longtime home on Piedmont Avenue — takes a hard look at the project."

Source: Atlanta Business Chronicle

Note that the project is really a mixed use development, although it does not include a multifamily component. "Live, work, play, shop" is a success driver in most mixed use projects. Also note that the project's office component is "alternative", favored by millennials and other tech industry workers.

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

CARTER & ASSOCIATES 715 PEACHTREE

17

"I think the building can play an interesting role for tech firms coming out of the ATDC,” said Matt Delicata, a vice president with Carter, referring to the Advanced Technology Development Center, an incubator for startups at Tech Square." Source: Atlanta Business Chronicle

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

ENVIRONMENT- BUSINESS

18

Note that another success driver of the Carter 715 Peachtree project is the presence nearby of "investment and development catalysts." These include "Tech Square, where Cousins Properties Inc. is developing a $200 million headquarters for NCR Corp. and Portman Holdings plans a $300 million project for Georgia Tech including a 600,000-square foot tower anchored by a High Performance Computing Center. A $200 million Emory Proton Therapy Center is also underway near 715 Peachtree just north of Emory University Hospital Midtown." Source: Atlanta Business Chronicle

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

ENVIRONMENT- DEMOGRAPHIC

19

ATTRACTING THE TYPE OF WORKFORCE THAT IS NEEDED CAN DRIVE LOCATION- AND RELOCATION- DECISIONS. "NCR joins firms such as fellow technology company Worldpay in announcing an in-town shift, adding momentum to a trend of businesses looking to locate in urban areas and near transit links to appeal to younger workers. “Given the global shortage of certain IT and technology positions, it makes all the sense in the world to me that NCR would move almost onto Georgia Tech’s campus,” said Ken Ashley, an executive director at real estate services firm Cushman & Wakefield." Source: Dayton Daily News

BUT TRADITIONAL INCENTIVES CONTINUE TO MATTER: "The city of Atlanta is offering a $3.2 million grant to be paid out of its reserve fund to induce the [NCR] move. That, however, could be just a small part of a local incentives package that could include property tax breaks through a complicated bond and lease-purchase arrangement." Source: Dayton Daily News

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

ENVIRONMENT- PHYSICAL

20

Many mixed-use projects today are challenged by environmental issues typical of in-fill locations. It is important for a County Board of Tax Assessors to be ready and willing to harmonize the property tax credits available for remediation under the brownfield program with property tax savings under a "bonds for title" property tax "abatement" program. A local policy that provides that harmony is an incentive all by itself. Successful programs can lead to mixed-use projects on brownfield sites, of which Atlantic Station is a prime example.

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

NEW INCENTIVES

THE FOREGOING HIGHLIGHTS A COUPLE OF ISSUES THAT ECONOMIC DEVELOPMENT RESEARCH PARTNERS, WHICH HAS BEEN CALLED THE "THINK TANK" OF THE INTERNATIONAL ECONOMIC DEVELOPMENT COUNCIL, HAS CALLED "NEW INCENTIVES"

21 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

BROWNFIELD REMEDIATION

"Brownfields—contaminated former industrial sites—cost American cities millions in lost tax revenues every year. Remediating these lands increases property values and inner-city employment, while supporting smart growth. More than ever, economic developers are redeveloping brownfields for industry use rather than for housing. Economic developers in Philadelphia, for example, are connecting brownfield policy explicitly to business attraction. Reusing brownfields for industry takes advantage of existing infrastructure and lower standards for clean-up compared to those required for housing."

22 |

Source: EDRP "New Incentives" paper

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

HUMAN CAPITAL ATTRACTION AND DEVELOPMENT

"The availability and quality of talented labor is a critical factor in the success of every business—and every community. Today, economic developers are increasingly focusing incentives on talent attraction and development. FastStart, the ‘silver bullet’ in Louisiana's success in the site selection wars, provides responsive, customized training to relocating companies. Kansas Rural Opportunity Zones give student loan relief to workers who relocate to rural counties."

23 |

Source: EDRP "New Incentives" paper

GWINNETT'S TOOLS-

A COMMENTARY

LOOK FOR THE COMMENTARY HERE

©2015 Seyfarth Shaw LLP - 19632984_1.pptx 25

IMPORTANT FOR ECONOMIC DEVELOPMENT PROJECTS WITH STREET AND ROAD NEEDS, SINCE LOCAL AUTHORITIES ARE CONSTITUTIONALLY EXCLUDED FROM STREET AND ROAD UNDERTAKINGS INVOLVING LOCAL GOVERNMENTS

©2015 Seyfarth Shaw LLP - 19632984_1.pptx 26

OPPORTUNITY- REVISE AND ADD FLEXIBILITY

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

WHAT COMPANIES WANT TO NEGOTIATE

• Depending on the incentives structure, some or all of the following issues will be negotiable-

• The percentage and duration of the abatement

• What property is eligible • Whether existing investment and/or

investment already on the tax digest (not always the same) can be included

• The start date and treatment of any CIP (Construction in Progress)

12

"FLEXIBILITY" IMPLIES THE ABILITY TO NEGOTIATE

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

WHAT TO NEGOTIATE • Depending on the incentives

structure, some or all of the following issues will be negotiable-

• Goals (typically jobs created or retained, and investment to be made)

• Clawbacks • Post-closing compliance

• Reporting and auditing • More

• project-specific issues

THE COMPANY WILL WANT- • CONSERVATIVE GOALS

• SAFETY MARGIN • CURE RIGHTS

• FORCE MAJEURE RIGHTS • LIMITED ACCOUNTABILITY

PERIOD • LIMIT TIMES

ACCOUNTABILITY TESTED • UNCONDITIONAL/

AUTOMATIC PURCHASE OPTION

13

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

FOCUS ON PILOTs • DEPENDING ON ABATEMENT STRUCTURE

USED, PROPERTY MIGHT ACTUALLY NOT BE SUBJECT TO PROPERTY TAX • IN USUFRUCT (NONTAXABLE LEASE)

STRUCTURE • IF PROPERTY ISN’T TAXABLE, THEN SOME

DOORS OPEN • 100% ABATEMENT, OR • PAYMENTS IN LIEU OF TAXES (PILOT

PAYMENTS) • CONTRACTUAL PILOT PAYMENTS ARE

OUTSIDE NORMAL PROPERTY TAX RULES • SO, THEY ARE GOVERNED BY CONTRACT

(PILOT AGREEMENT) • "PILOT RESTRICTION ACT" MIGHT ALSO

APPLY 14

GWINNETT COUNTY HAS

HISTORICALLY USED THE

LEASEHOLD VALUATION METHOD OF

"ABATEMENT", NOT USUFRUCTS

©2015 Seyfarth Shaw LLP - 19632984_1.pptx 30

TADs ARE A REDEVELOPMENT TOOL, WHICH CAN BE IMPORTANT

IN ECONOMIC DEVELOPMENT WHEN CREATING A DESTINATION

©2015 Seyfarth Shaw LLP - 19632984_1.pptx 31

OZ can be an important tool when

locating/relocating a technology/TAMI

company to an urban environment

©2015 Seyfarth Shaw LLP - 19632984_1.pptx 32

• Like OZ except requires 5 jobs

minimum • Important incentive

DO THESE TOOLS FIT THE

TOOLBOX?

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

PUBLIC/PRIVATE PARTNERSHIPS P3

34 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

PUBLIC/PRIVATE PARTNERSHIPS (P3)

• ARE VERY POPULAR NOW • ONE OF THE EARLIEST SUCCESS STORIES IN

GEORGIA WAS IN HENRY COUNTY! • THE MERCER PROJECT

• SATELLITE ACADEMIC BUILDING • GRADUATE DEGREES

35

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

THE MERCER PROJECT

• THE HENRY COUNTY DEVELOPMENT AUTHORITY (HCDA) ACTED AS PROJECT MANAGER

• HCDA WAS ALSO CONDUIT FOR ISSUANCE OF TAX-EXEMPT BONDS • NO HCDA OR COUNTY RESPONSIBILITY FOR REPAYMENT • BONDS ARE BEING REPAID BY LEASE OF PROJECT TO

MERCER FOUNDATION • COUNTY PROVIDED LAND VIA GROUNDLEASE • CHOATE CONSTRUCTION PAID CONSTRUCTION

COSTS AND WAS REPAID OUT OF BOND PROCEEDS • "DESIGN-BUILD-FINANCE" P3 MODEL

36

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

CONTRACT REVENUE BONDS

37 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

Contract Revenue Bonds structure

38

• REVENUE BONDS FOR NEW FALCONS STADIUM

• REVENUE WAS PLEDGE OF PORTION OF CITY'S HOTEL/MOTEL TAXES (HMT)

• THIS WAS "PASS THROUGH" STRUCTURE

• CITY'S LIABILITY LIMITED TO HMT COLLECTIONS

Source: City of Atlanta

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

EB-5 IMMIGRANT INVESTOR CAPITAL

39 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx 40

BASIC RULE

FOR A $500,000 INVESTMENT IN A TARGETED EMPLOYMENT AREA THAT CREATES AT LEAST 10 DIRECT, INDIRECT OR INDUCED JOBS, A FOREIGN INVESTOR WILL GET A "GREEN CARD"

• Something called a "Regional Center" raises the capital and is the conduit .

• Capital is raised on a per project basis via a Private Placement Memorandum.

• Per investor requirement is $1 million, unless project is located in a Targeted Employment Area.

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

THE REGIONAL CENTER IS THE CONDUIT

• REGIONAL CENTER (RC) • EB-5 investment can be made by an investor on a stand-

alone basis, or through a USCIS-designated Regional Center (RC)

• RCs are the norm • Each investor’s investment must create at least 10 jobs

(direct, indirect and induced) • If the investment is stand-alone, indirect/induced jobs are not

counted • RCs use an economic model to calculate and substantiate job

creation • Models that are used are subject to USCIS approval

41

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

NEW MARKETS TAX CREDITS (NMTC)

42 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

BASIC RULE

THE PROJECT TYPICALLY NETS SUB DEBT ("FORGIVABLE LOAN") EQUAL TO 20%-25% OF THE NMTC ALLOCATION

• Something called a "CDE" holds the allocation of credits and is the conduit.

• Ultimate NMTC benefit should be calculated net of costs and any applicable taxable income on exit.

• Both the Development Authority of Fulton County and Invest Atlanta have CDEs 43

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

CLOSE TO HOME EXAMPLE

Meredian Bioplastics, Inc. (Meredian) is a green technology company that uses byproducts of the timber and agricultural industry to create bioplastics.Meredian utilized NMTC financing to acquire new equipment and expand from their previous facility to a 190,000 square-foot industrial, office and research facility in Bainbridge, Georgia. The continued success and growth of Meredian is vital to the economic health of the city of Bainbridge, and the new facility has brought significant investment into a low-income community in rural Georgia. Source: Meredian

NMTC Allocation $27.5 million

NMTC proceeds $8.6 million

Total Project Costs $38.7 million

1

2

3

44

CONCLUSION

45

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

OBSERVATIONS ON GWINNETT COUNTY

• GWINNETT COUNTY TODAY IS VERY DIFFERENT COMPARED TO GWINNETT COUNTY A FEW YEARS AGO

• SO IS THE WORLD AT LARGE • GWINNETT COUNTY HAS THE OPPORTUNITY TO

BOTH TARGET DESIRED COMPANIES INDIVIDUALLY AND TO CREATE DESTINATIONS THAT WILL ATTRACT CLUSTERS OF COMPANIES

46 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

OBSERVATIONS ON GWINNETT COUNTY

• GWINNETT COUNTY ALREADY HAS THE BASIC ECONOMIC DEVELOPMENT TOOLS

• INCREASED FLEXIBILITY WOULD BE DESIRABLE IN GWINNETT COUNTY'S ECONOMIC DEVELOPMENT ORDINANCE

• ADDITIONAL FINANCIAL INCENTIVES COULD BE EFFECTIVE IF RESOURCES AND LOCAL POLICY PERMIT

• ACCESSING THE EB-5 AND NMTC PROGRAMS COULD PAY OFF FOR GWINNETT COUNTY

47 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

OBSERVATIONS ON GWINNETT COUNTY

• CREATING A DESTINATION OFFERS A HIGHER UPSIDE BUT IS MORE DIFFICULT • THINGS TO CONSIDER-

• "NEW INCENTIVES" • CONNECTIVITY TO RESEARCH UNIVERSITIES • POSSIBLE P3 OPPORTUNITIES • USE OF REDEVELOPMENT TOOLS • LEVERAGE EXISTING BUILDINGS THROUGH

REPURPOSING/ADAPTIVE REUSE • PARTNER WITH EXPERIENCED, FOCUSED DEVELOPMENT

TEAMS • AGGRESSIVE FINANCIAL INCENTIVES WITHIN THE

DESTINATION, AT LEAST INITIALLY

48 |

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

OBSERVATIONS ON GWINNETT COUNTY

GWINNETT COUNTY HAS "THE RIGHT STUFF" TO ACCOMPLISH ITS GOALS

49 |

MORE INFORMATION

50

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

QUESTIONS?

If you have any questions or comments on this presentation, please do not hesitate to let me know.

Daniel M. McRae, Partner Seyfarth Shaw LLP

1075 Peachtree Street, N.E. Suite 2500

Atlanta, GA 30309 404.888.1883

404.892.7056 fax [email protected]

danmcrae.com

51

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

ON THE WEB

• MY WHITE PAPERS ON ECONOMIC DEVELOPMENT AND OTHER TOPICS CAN BE DOWNLOADED

at http://danmcrae.com/whitepapers • DAILY (ALMOST DAILY) UPDATES ON

• FACEBOOK http://facebook.com/danmcrae68 • LINKEDIN http://linkedin.com/in/danmcrae2 • TWITTER @McRaeDan

35

©2015 Seyfarth Shaw LLP - 19632984_1.pptx

SCOPE

This presentation is a quick-reference guide for elected and appointed officials and their staffs, company executives and managers, economic developers, participants in the real estate and financial industries, and their advisors. The information in this presentation is general in nature. Various points which could be important in a particular case have been condensed or omitted in the interest of readability. Specific professional advice should be obtained before this information is applied to any particular case. Any tax information or written tax advice contained herein is not intended to be and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on the taxpayer. (The foregoing legend has been affixed pursuant to U.S. Treasury Regulations governing tax practice.)

53