Embed Size (px)

Citation preview

Uniq plcNo.1 Chalfont Park

Gerrards Cross

Buckinghamshire

SL9 0UN

United Kingdom

Telephone +44 (0) 1753 276000

Facsimile: +44 (0) 1753 276019

www.uniq.com

Un

iq A

nn

ual R

epo

rt an

d A

ccou

nts 2010

Annual Report and Accounts 2010

Designed and produced by Addison www.addison.co.uk

Printed in the UK by Pureprint, Environmental Management System ISO 14001 accredited and Forest Stewardship Council (FSC) chain of custody certified.

This report is printed utilising vegetable-based inks on Revive 50 White Silk which is produced with 50% recycled fibre from both pre- and post-consumer sources, together with 50% ECF (Elemental Chlorine Free) fibre from well-managed forests independently certified according to the rules of the Forest Stewardship Council.

FreshnessInnovationQuality

Uniq produces freshly prepared chilled food for major retailers and has market-leading positions in Desserts and Food to Go. Our high-quality and innovative products aim to delight our customers.

Desserts

£312mTotal revenue 2010

Food to Go

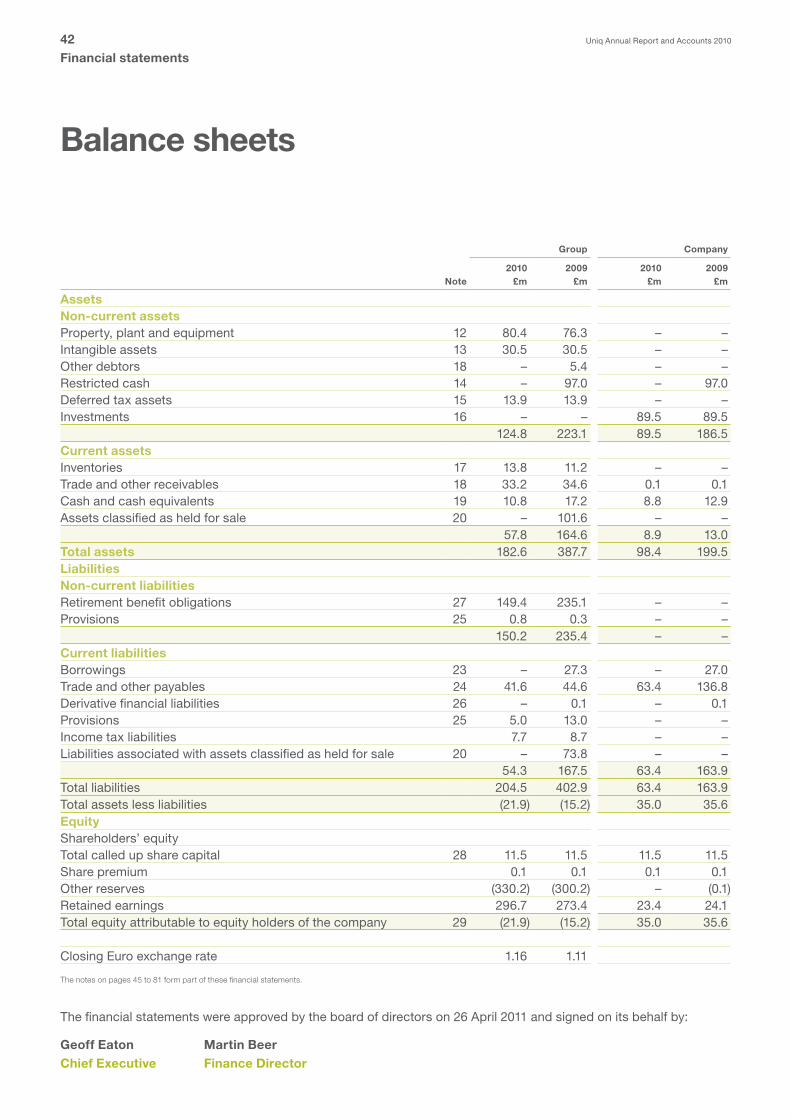

Financial statementsIndependent Auditors’ report 38Group income statement 40Group statement of comprehensive income 41Balance sheets 42Group statement of changes in equity 43Cash flow statements 44Notes to the financial statements 45 Other informationFive year record 82Shareholder information 83

ContentsFinancial highlights 01 Directors’ reportChairman’s statement 02Chief Executive’s statement 04Market overview 06Business review 08Financial review 16Principal risks 20Directors’ responsibilities 21Board of directors 22Report of the directors 24Corporate governance 27Remuneration report 32

£155m2010 revenue

We are an innovative, market-leading manufacturer of premium and everyday freshly prepared pot desserts, a flexible and niche supplier of quality, differentiated yogurt and a state-of-the-art producer of fresh chocolate desserts made exclusively for Cadbury.

£157m2010 revenue

We are the Number One sandwich and wrap supplier to M&S, the winner of multiple sandwich retailer of the year, and the UK’s second largest producer of dressed salads.

Uniq Annual Report and Accounts 2010 Uniq Annual Report and Accounts 2010

01Financial highlights

• Revenueup6.8%*• Tradingprofitbeforecentralcostsup88%• Businessperformancerecognisedthorugh

customerawards• StrongmomentumcontinuesinFoodtoGo

• Balancesheettransformedondeliveryofinnovativepensionsolutionin2011

• SuccessfuladmissiontoAIM• Dessertsreviewidentifiesprofitable

growthopportunityfordefinedmarkets

• M&SbestdessertsupplieroverChristmas• M&SNPDrangeoftheyear(minis)• Highesteversinglesandwichproduction

atNorthampton–6.5munits• 24%increaseinsalesatSpalding• 58NPDproductslaunchedduringtheyear• 99.97%servicelevelinSpaldingduringthe

WorldCup

*adjusted for 53rd week in 2010

2010£m

2009£m

Continuing operations

Revenue 311.9 287.2Tradingoperatingprofitbeforesignificantitems 8.3 4.4Groupcostsbeforesignificantitems (4.2) (6.3)Operating profit/(loss) before significant items 4.1 (1.9)Significantitemsbeforetax (2.4) (0.7)Financeexpense(excludingpension-related) (1.4) (4.6)Incometax – (0.4)Net profit/(loss) before pension-related finance expense 0.3 (7.6)Pensionrelatedfinanceexpense (11.5) (11.3)Loss after tax (11.2) (18.9)

Profit/(loss)fromdiscontinuedoperations 35.4 (2.0)Profit/(loss) for the year 24.2 (20.9)

Key performance indicators % %

Revenuegrowth 6.8% 0.2%Grossmargin 15.3% 14.2%Operatingmargin 1.3% (0.7%)

Financial highlights for the year ended 31 December 2010

Highlights

Key achievements

Financial results

Further information can be found at www.uniq.com

Post period update

UniqAnnualReportandAccounts2010

UniqAnnualReportandAccounts201002Directors’ report

I am pleased to report a continued improvement in the performance of the business, with an operating profit before significant items of £4.1m in 2010 compared to a loss of £1.9m in 2009. Turnover showed good growth, with sales of £312m representing an increase of nearly 7% on 2009’s sales figure of £292m (adjusted for 53rd week).

Althoughthesefiguresprovidestrongevidencethatthe

board’sstrategyoftransformingthecompanyintoa

high-qualityUK-focusedprivatelabelbusinesshasbeen

successful,itbecameincreasinglyclearduring2010that

thespeedandscaleofoureffortscouldnotmeetthe

growingdemandsofourpensionliabilities.Theboard

thereforecontinuedtoseekasolutiontoourpension

fundingsituationandon9February2011,thecompany

reachedagreementwiththeTrusteeoftheUniqPension

Schemeonthetermsofarestructuringofthecompany.

Thisreleasedthecompanyfromitsobligationstothedefined

benefitsectionofthePensionSchemeinexchangefora

90.2%equitystakeinthecompany,withcurrentshareholders

retaininga9.8%stakeinthecompany.

Whilethecontextforthisdecisionissetoutinmoredetail

below,theoutcomeisthatUniqcannowlookforwardto

afutureinwhichitsmanagementcandevelopthepotential

ofitsbusinesseswithouttheconstraintsimposedbyour

pensionsituation.Althoughtheboardunderstandsthat

thiswillhavecausedshareholdersconsiderableconcern,

weareconfidentthatouractionisintheirbestinterests

andthebestlong-terminterestsofallstakeholders.

Uniqhasastrong,well-runbusinessdeliveringthequality,

innovationandconsistencythatourcustomersdemand,

inmarketsthatoffermultipleopportunities.AsChief

ExecutiveGeoffEatonoutlinesinhisstatementonpages

4and5,webelievethatUniqisnow,finally,inaposition

tocapitaliseonthesestrengths.

The context for restructuringUniqevolvedoutoftheUnigateGroupwhich,atitspeak

duringthe1980s,wasamultinationalconglomeratewithover

30,000employeesintheUK,EuropeandNorthAmerica.

Unigatehadaverylargedefinedbenefitpensionplanwith

over40,000members(includingactivemembers,deferred

membersandpensioners)intheUK.WhenUnigatesoldits

‘flagship’dairybusinessin2000,theremainingbusiness

changeditsnametoUniqplc.Underthetermsofthis

transactionUniqplcretainedtheresponsibilityformembers

ofthedairybusinessintheUniqPensionFund.

InMay2001,Uniqdemergeditslogisticsbusiness,

Wincantonplc.TheUniqPensionFundwassplitroughly

inhalfandUniqwasleftwithapensionscheme(known

astheUniqPensionScheme)ofapproximately21,000

membersbutwithamuchsmallerbusiness,interms

ofassets,withwhichtosupportthepensionscheme.

Board strategyIn2006,theboardrecognisedthatUniqwasnota‘pan-

Europeangroup’butanumberofseparatebusinesses

withdistinctmarketsandchallenges.Theboardadopted

astrategyintendedtotransformthebusinessandaddress

thepensiondeficit.ThroughthesaleoftheBelgiansalads

businessin2006andtheFrenchStHubertspreads

businessin2007(totalproceeds£288m),thegroup

wasabletosetaside£87minasecureaccount

tooffsetsubstantiallythedeficitatthattimeinitsmain

UKPensionFund.Theremainingcashrepaiddebtand

providedfundstosupporttherecoveryoftheretained

businesses,whichwereatthattimeincurring

substantiallosses.

Alignmentofthegroup’sbusinesseswiththeircustomers

andmarketswastackledthroughdecentralisingthe

organisationtoallowmanagementtoactfasterand

moreeffectively.Majormilestoneswereachievedin

eachofthegroup’sdivisions,withrecoveryevident

throughoutthebusiness.

Pension funding However,turbulenceinworldfinancialmarketsduring

2008resultedinasharpincreaseintheUKpension

deficit.Theneedtostrengthenthegroup’sbusinesses

becamemoreurgent.Accordingly,theboarddecided

tomodifyitsrecoveryplanand,inparticular,pursue

consolidationopportunitiesinFranceandNorthern

Europe–tocreatevaluethroughjointventureorsale

ofthosebusinesses–andfocusitsresourceson

strengtheningitsbusinessesintheUK.

Chairman’s statementFoundations for the future

03Directors’ report

Chairman’s statement

UniqAnnualReportandAccounts2010

Thebusinessesweresoldinearly2010andtheproceeds

fromtheirsalewereusedtosupportthegrowthofthe

UKbusinessandtoassistthegroupinitstriennial

fundingdiscussionswiththePensionSchemeTrustee.

Pension liabilitiesOnanIAS19accountingvaluationbasis,thepensiondeficit

asat31December2010was£142.1m.Onabuy-outbasis

(whichassumestheliabilitieshavebeenboughtoutbyan

insurancecompany),thenetdeficitwas£430m.

Thescaleofthisdeficitnegativelyimpactedthemarket

valueofthecompany.Theboardthereforeconsideredall

possiblefundingoptionsforthePensionScheme,allof

whichwouldhaveinvolvedafundamentalimpactonthe

long-termfutureofthegroupandonshareholdervalue.

Aspartoftriennialscheme-specificfundingdiscussions,

whichbeganinMarch2009betweenthecompanyandthe

Trustee,along-termfundingproposalwasdevelopedand

wasdescribedinlastyear’sannualreportandaccounts.

ItwasrejectedbythePensionsRegulatoron16July2010.

Restructuring solutionOn9February2011,thecompanyreachedagreement

withtheTrustee,thePensionsRegulatorandthePension

ProtectionFundonthetermsofarestructuringofthe

company.ThisSchemeofArrangementwasapproved

bytheshareholderson25February2011andsanctioned

bytheCourton18March2011.Inexchangefora90.2%

equitystakeinthecompany,withcurrentshareholders

retaininga9.8%stakeinthecompany,andafinal

paymentof£14mtothePensionFund,therestructuring

releasedthecompanyfromitsobligationstothedefined

benefitsectionoftheUniqPensionFund.Followingthis

restructuringthecompanysuccessfullyappliedforthe

sharestoberelistedonAIMasfrom1April2011.

DividendTheboardhasdecidedthatitisnotappropriatetopay

adividendtoshareholdersfor2010(2009:£nil).However,

followingthepensionrestructuringtheDirectorsintend

topaydividendswhenitisappropriatetodoso.

OutlookItisagreatcredittoChiefExecutiveGeoffEatonand

hismanagementteamthat,despiteaperiodofsuch

uncertaintyandthechallengeofcreatingandimplementing

thepensionsolution,theyhavecontinuedtofocuson,

andachieve,thetransformationofthebusiness.

Profitabilityhasbeenrestored,strongcustomerrelationships

establishedandtheflexible,innovativeprocessesthat

ourmarketsdemandareinplaceandalreadybeginning

toshowresults.Inspiteofthis,thenewyearhasthrown

upfurtherchallengeswithfurtherrawmaterialprice

inflation,increasinglyintensecompetitionandlossof

businessinDessertsbeingnotifiedbeforetheimplementation

ofthepensionsolution.Iwouldliketocongratulateall

managementandstaffatUniqfortheirunstintingefforts,

whichwefullyexpecttomaintaintheimprovedperformance

ofyourcompanydespitethechallengingenvironment.

Furthermore,thecomprehensivereviewofourDesserts

business,announcedinJanuary,hasbeencompleted

andaplanhasbeenapprovedthatisexpectedtodeliver

sustainableimprovementinprofitability.

John WarrenChairman 26April2011

“ We are confident that our action is in the long-term interests of all stakeholders and will give Uniq the opportunity to repay their commitment.”

UniqAnnualReportandAccounts201004Directors’ report

Chief Executive’s statement Delivering the full potential of your business

Having addressed our legacy issues and completed our transformation into a UK-focused, high-quality Desserts and Food to Go producer, I believe we are now able to deliver the full potential of the business.

Ourinvestmentinpeople,processesandproductsover

thelasttwoyearsmeansweareinastrongpositionto

meetthechallengesandopportunitiesourchosenmarkets

present.Thishasbeendemonstratedbyourimproving

performancethisyear,whichwasdrivenbyourstrong

managementteamsandtheirabilitytoefficientlytranslate

theirmarketinsightsintoattractiveandinnovativeproducts

thatmeetthedemandsofbothcustomersandconsumers.

Withtherightfoundationsnowinplace,Ibelievewecan

consolidateourgrowth,optimiseourreturnoninvestments

andraiseprofitabilitytowardsindustrystandardmargins.

Asbefitsabusinessthatis,inmanyways,startingafresh,

Iwouldliketotakethisopportunitytolayouttoinvestors

andallstakeholdersourvisionforthefuture:themarket

opportunitiesweface;thestrategythatwillenableusto

addresstheseopportunities;andthetargetsbywhichwe

willmeasurehowsuccessfulweareindoingso.

VisionOuraimistobethemostrespectedfreshprepared

foodcompanyintheUKforinnovation,serviceand

qualityasjudgedbyourcustomers,suppliers,

employeesandshareholders.

Our opportunities and strengthsWeservelargeandgrowingmarkets,withinwhichthere

aremultipleopportunitiesanddriversofdemand:forexample,

convenience,eatingoutofhomeandonthemove,healthy

eating,andcaféculture.Byinvestinginunderstanding

consumersandinnovatingtocreatearegularpipeline

ofnewproductsweareabletobenefitfromthisgrowth.

Strongmarketpositionsgiveusthescaletoensurewecan

attractandretainhighlycapableteamsandmakeefficient

useofassets.Wesupplyover65%ofthesandwichesfor

ourlargestcustomer,weareamarket-leadingsupplierof

premiumdesserts,wearetheexclusiveproduceroffresh

Cadburychocolatedessertsandwearethenumbertwo

supplierinpreparedsalads.

Weservicecustomerswhoareinvestingingrowth

andwehavethepotentialtoincreaseourshareof

theirbusiness–wearehighlyfocusedandwederive

competitiveadvantagefromunderstandingand

consistentlymeetingourcustomers’needs.

Wehaveanefficientcapitalstructurethatwillsupport

investment.Ourreturnoninvestmentwillbeenhanced

bysignificanttaxassets–wewillnotpaytaxonour

profitfortheforeseeablefuture.

Wehaveanexperiencedandcapablemanagement

teamthathascometogetherduringfiveyearsof

restructuring,turnaroundanduncertaintyand,having

alreadydeliveredsomesuccess,isappropriately

incentivisedandcommittedtodrivegrowthfurther,

unfetteredbythelegaciesofthepast.

Ourproductrangesincludebothpremiumandvalue

productsandareappropriatelytiered.Ourflexibility

andabilitytoinnovatemeanthatwecanquickly

adaptourproductrangestoreflecttheeconomic

circumstancesofconsumers.

Performance reviewDessertsOurDessertsstrategybegantoshowrealresults

thisyear.Newandrefreshedproductrangesatboth

ourMinsterleyandEvercreechsites,alliedwiththe

investmentswehavemadeinthebusinessoverthe

lasttwoyears,droveastrongerperformanceand

establishedUniqastheplacetogoforinnovative

high-qualityprivatelabelproducts.

Immediatelyfollowingthissuccesswewereforcedto

pushthroughapriceincreasefollowingtheincrease

increamcostswhichhaverisenby80%overthelast

twoyears.Thisnotonlyhadanadverseimpacton

somecustomerrelationshipsbutalsoledtoachange

inconsumerbehaviourashigherpricepointsresulted

inswitchingtootherproducts.Followingtheyearend

wewerenotifiedofthelossof£10mofDessertssales

partlyasaresultofthesefactorsandpartlyreflecting

theuncertaintiescausedbythepensionposition.

UniqAnnualReportandAccounts2010 05Directors’ report

Chief Executive’s statement

Desserts reviewOnthebackofthedisturbancecausedbytheprice

increaseandasaresultofthedecisiontodiscontinue

cottagecheeseproductionatEvercreechweconducted

acomprehensivereviewofourDessertsbusiness.

OurDessertsbusinesssuppliesfourdistinctsub-sectors

ofthedessertsmarket;premiumdesserts,Cadbury

chocolatedesserts,yoghurtandeverydaydesserts.

Threeofthesesub-sectorsareeitherprofitableor

ontracktoachieveprofitability,whilethelossesare

concentratedineverydaydesserts.Asaresultof

theDessertsreviewwehaveapprovedthefollowing

profitimprovementplans:

• TousethespacefreedupatEvercreechbythe

discontinuanceofcottagecheeseproductionto

investinfurthergrowingourpremiumdesserts

business–whichgrewby21%in2010.

• ToimplementambitiousgrowthplansforCadbury

dessertsforwhichwehaveidentifiedconsiderable

potential.Weneedtosecuresupportforthese

plansfromourpartners.

• Tocontinuetobuildourcapabilityandcustomer

baseforourpremium,differentiatedyoghurtbusiness

atMinsterley,withsupportfromM&S.

• Toimplementaplantosignificantlyreducetheoverheads

andcostsineverydaydessertsandworkwithour

customerstoaddressthemarketneedswhileensuring

thatwestopthelossesinthissub-sector.

Food to GoAtNorthampton,weextendedourten-yeargrowthrecord

in2010,successfullyimplementingtheincreasedsandwich

volumeswonfromM&Ssupplierconsolidation.Newand

relaunchedproductrangeshelpedustonotonlytake

advantageofgrowingnichemarketssuchashealthyeating

andcaféculture,buttowinprestigiousawardsandfurther

strengthenourrelationshipwithourprincipalcustomer,

M&S.Northamptoncontinuestosetthestandardforlean,

flexibleandcreativeprocesses,supportedbybothstrong

managementandafullyengagedworkforce.InSalads,

ourSpaldingsiteincreasedvolumesaswetookonlast

year’snewbusinesswins,helpingtodriveefficiencieswhile

successfullymaintainingexceptionallyhighqualityand

servicelevels.Althoughoversupplyinthemarketcontinued

tosqueezemargin,theSaladsbusinessremainswellpositioned

tobenefitstronglyfromanysupplierconsolidation.

Geoff EatonChief Executive26April2011

Our strategy We will achieve growth by:

• �Empoweringourbusinessessothattheyhavethespeedandflexibilitytomeettheneedsofourcustomersinafast-movingandcompetitivemarket-place.Atthesametime,wewillleverageourcombinedscaletosupportourbusinessesandenhanceourgrowthopportunities

• Creatingnewopportunitiesbydeliveringoutstandingservicewiththehigheststandardsofqualityandefficiencydayindayout

• Meetingtheneedsofourcustomersandconsumersthroughinnovationthatsatisfiesthedemandsofgrowingandever-changingmarkets

• �Investinginourpeople,processes,equipmentandfacilitiesandcontinuouslyimprovingeverythingwedo

• Workinginpartnershipwithourkeysuppliersandcustomerstoachievethemosteffectivesupplychaincapableofdeliveringaddedvaluetooursharedconsumers

Our targets and key performance indicators:

• Weaimtodeliverorganicgrowthofover5%ayear• Ourtradingprofitmarginshoulddeliveranoverall

returnonsalesofover5%• Ourreturnoninvestmentshoulddeliverdouble-digit

returnsandexceedourweightedaveragecostofcapital• Wewilladoptaprogressivedividendpolicywitha

long-termtargetdividendcoverofthreetimes• Wewillmaintainanappropriatecapitalstructure

withtotalnetdebtnomorethanthreetimesEBITDA

Our key actions to deliver our strategy:

• WewillcontinuetodrivegrowthinourSandwichbusiness• WewillconsolidateourrecoveryinSaladsandthen

buildourcapabilitiesforlong-termgrowth• Wewillbuildonoursuccessfulinnovationinpremium

dessertsandyoghurt,seektoimplementanambitiousgrowthstrategyforCadburychocolatedessertsandsignificantlyreducecostsandimproveefficiencytostopthelossesineverydaydesserts

UniqAnnualReportandAccounts201006Directors’ report

Market overviewAs the economy recovered in 2010, consumers traded up but continued to demand value.

Onereasonforchilledconveniencefoodsalesoutperforming

thewidermarketplaceis‘treating’.Whilehouseholds

facedwithconstrainedincomegrowthandhighertaxation

havecutbackonspending,theyarestillattractedby

non-essentialtreatswhilecarryingouttheirroutine

foodshopping.

Healthwasalsoakeytrend.The2010Datamonitor

ConsumerSurveyshowedtheextenttowhichconsumers

believethattasteshouldnotcomeattheexpenseof

nutrition.Indeed,62%ofconsumersattachedmore

importancetofindingproductsthatcombinedthese

attributesthantheydidtwoyearsago.

Premium v ValueConsumerappetiteappearsnottohavebeenfundamentally

changedbytherecession,andthedemandforpremium

rangesre-asserteditself,particularlyinthesecondhalf

oftheyear.Cost-consciousconsumershave,however,

beenhelpedtowardtheserangesbypromotionalactivity.

Asthegraphillustrates,demandforpremiumtiers

returnedtogrowthinthefinalquarterof2010,while

demandforvalueproductscontinuedtoslowacross

themarketplace.

Input pricesAwidevarietyoffactors,rangingfromadverseweather

conditionsandrisingglobaldemandtohigherenergy

pricesandmarketspeculation,ledtoincreasedinput

pricesin2010.Thiswasparticularlynoticeableinthe

secondhalfoftheyearastheworldeconomicrecovery

accelerated,pushingupdemand.

Uniq’sinputpricesrose3.8%intheyeartoDecember

2010,whileinthebroaderUKeconomytheConsumer

PricesIndex(CPI)roseby3.7%*andtheRetailPrices

Index(RPI)wasup4.8%*inthesameperiod.

Our marketThebroadmarketinwhichUniqoperatesistheUKfresh

andchilledfoodssector.Thishadatotalvalueof£37bn

in2010,representinganincreaseof3.1%on2009.

ThemajorityofUniq’soutputfalls,however,withinone

segmentofthismarket:chilledconveniencefoods.

Thisgrewmorestrongly,withsalesup5%in2010at

£7.5bn.Asthissegmentisdominatedbythemajor

retailers’ownbrandsandUniqisprimarilyaproducer

ofprivatelabel/ownbrandproductsforthemajor

retailers,theoutperformanceofchilledconvenience

foodsishighlyencouraging.

Formorespecificinformationaboutthemarketsub-sectors

inwhichweoperate,seebelow.

TrendsOneofthekeytrendsin2010wasconsumersshopping

aroundtofindgood-qualityproductsthatalsomettheir

valuerequirements.Thisprovedapositiveinfluencefor

privatelabel,whichcanoftenofferconsumerssignificant

savingswhencomparedtobrandedproducts.Acomparison

ofthe2009and2010DatamonitorConsumerSurveys

showsthattherewasasignificantincreaseintheproportion

ofconsumerssayingthatprivatelabelwasofequal,ifnot

better,qualitythanbrandedproducts.Thisabilityofprivate

labelproductstomeetboththevalueandqualitydemands

ofconsumersdrovegrowthin2010.Indeed,research

publishedbyNielsenin2010showsthatprivatelabels

nowaccountfor47%ofallvolumesoldintheUK

retailchannel.

Anothertrendwasthegrowthof‘mealdeal’bundles,where

shoppersbuyamenuofproductsforadiscountedprice.

Thislendsitselfwelltothe‘mixandmatch’versatilityof

chilledconveniencefood,includingdessertsandsalads.

Ithasparticularresonanceinthecurrenteconomicclimate,

whereshopperscansavemoneybyeatingathomerather

thangoingouttoarestaurant.

Total Grocers Year-on-Year % changes

Economy

Premium

Feb2010

Jun Oct Feb2011

Nov2009

50

40

30

20

10

0

-10

-20Total Grocers Year-on-Year % changes

Economy

Premium

Feb2010

Jun Oct Feb2011

Nov2009

50

40

30

20

10

0

-10

-20

Top 5 raw materials Price movement for 2010

Dairy

Ingredients

Fruit and Conserves

Vegetables

Confectionery

%

01 02 03 04 05 06 07 08 09 10 11 12

15

10

5

0

-5

-10

-15

Source: Uniq

Top 5 raw materials Price movement for 2010

Dairy

Ingredients

Fruit and Conserves

Vegetables

Confectionery

%

01 02 03 04 05 06 07 08 09 10 11 12

15

10

5

0

-5

-10

-15

Source: Uniq

UniqAnnualReportandAccounts2010 07Directors’ reportMarket overview

Althoughtheinflationarytrend,drivenlargelybymajor

globalfactors,wasevidentacrossalmostallUniq’s

purchasingcategories,individualinputpricesalso

behavedaccordingtotheirownspecificdrivers.

Creamprices,forexample,rosefarmoresharplythan

averageinputpricesasanumberoffactorsfundamentally

alteredthebalanceofdemandandsupplyinthemarket.

Highbutterpricesledtomorecreambeingboughtby

butterproducers,reducingtheavailabilitytothose,

likeUniq,whouseitforotherdairy-basedproducts.

*Source: Office for National Statistics

Desserts marketThetotalchilleddessertsmarket(whichincludesyogurts)

grewby3.0%to£2.4bnduring2010,withvolumes

remainingflat.However,yoghurtsrepresentlessthan

10%ofUniq’stotaldessertsproduction.Inchilledpot

desserts,whichrepresentthevastmajorityofUniq’s

sales,themarketgrewmorestrongly,rising4.8%by

valuein2010.Withinthedessertsmarket,triflesales

remainedunchangedin2010,yoghurtsalesedged

upby2.4%andcheesecakegrewstronglyby13.2%.

About75%ofUniq’sdessertsoutputisprivatelabel

andthemajorityofthisisforM&S,whichstrengthened

itspositionasadestinationstorefordesserts,

registeringincreasedsalesbybothvalueandvolume.

Source: Kantar World panel w/e 26/12/10

Food to Go marketTheFoodtoGomarketisworth£16.8bnandgrewby

12.4%in2010.Ofthis,approximately20%issoldby

themajorretailers,forwhomUniqprovideprivatelabel

products.TheyearsawoverallFoodtoGosalesrevenue

growingaheadofvolume,asretailerschangedtheir

rangestoincludemorepremiumlinesandconsumers

tradedup,buyingfewerlowervalueproducts.

Convenienceiskeyinthe‘onthego’market,and

increasingnumbersofoutletopeningshavecontributed

totheaccelerationinsalesgrowth.Sandwichesrepresent

approximately22.3%oftheentireFoodtoGomarketand

totalsandwichsalesgrewby6.6%,withvolumeup3.2%.

InSalads,whichrepresentsapproximately1.5%ofthe

FoodtoGomarket,salesincreasedby9.3%ofvalue,

onvolumesup5.0%.

UniqAnnualReportandAccounts201008Directors’ report

• Investment programme impacted by market volatility

• Highly successful new product launches• Desserts review establishes clear path

to profitability

Asthemarketleaderinchilledpotdesserts,Uniq

operatesfromtwosites.MinsterleyproducesCadbury

chocolatedesserts,premiumdifferentiatedyoghurt

andprivatelabelpremiumandeverydaydesserts;and

Evercreechproducespremiumdessertsandisexiting

cottagecheese.Bothsiteshavealongheritageof

supplyingdairy-basedproductsintoamarketthat

hasbeenchallengingforanumberofyears.

Ourcustomers,themajorretailers,andtheend

consumer,demandfreshlypreparedhigh-quality,

great-tastingproductsthatareattractiveandinnovative.

Investmentduringtheyearinareassuchasnewconcept

development,newproductionlines,packingequipment

andmoreconvenientpackformatshasenabledusto

launchmorethan58newproductsin2010.Thesewere

extremelywellreceivedbyourcustomersandby

consumers,insomecasestheinitialdemandbeing

morethandoubleourexpectation.Ourconsumerinsight

andtechnicalexpertiseenabledustodevelopexciting

newproductsforfast-growingnichemarkets,including

breakfastyoghurtsforCostaCoffeeandminidesserts

forM&SCaféandFoodontheMove.Thiswasrecognised

duringtheyearwhenwereceivedtheM&S‘Innovatorof

theYear’award.

Sales up 1.5%* to £155mLosses reduced by 6.9% to £2.7m

Oursuccesshasbeenachieveddespiteastrong

headwindfromrawmaterialinflation,driveninparticular

bywholesalecreamcostswhichhaverisenbyaround

80%overthelasttwoyearsasaresultofshortageof

supplyandhighdemandfromtheContinent.Whilewe

wereabletosuccessfullynegotiatepriceincreaseswith

ourcustomerstoreflectourgrowingcosts,thisinevitably

hadanimpactonvolumesascustomersandconsumers

remainhighlysensitivetoprice.

DuringtheyearArlainvestedinnewcottagecheesecapacity

atitsnewdairyandanumberofourcustomerswereableto

securelowerpricesandswitchedtheirsupply.Consequently,

wedecidedtodownscalecottagecheeseproductionand

plantoexitthismarketin2011.Thegrowthdeliveredinour

premiumdessertsbusinessin2010allowedustotransfer

manyoftheemployeesfromcottagecheesetodessertsand

weintendtousethevacatedspacetofacilitatefurther

growthinpremiumdesserts.

PerformanceTherestructuringofourDessertsbusinessin2009–

throughconsolidationfromthreesitestotwo,thecreation

ofanewconsumerandinnovation-ledstrategyandthe

reinforcementofourmanagementcapabilitythrougha

numberofexperiencedhirestokeypositions–startedto

showresultsin2010.Despitetheimpactofcoldweatherin

thebusyChristmastradingperiod,salesheldupwellinthe

fourthquarterandwepostedanoverallsalesincreaseof

1.5%*in2010,achievingrevenueof£155m.Althoughrising

rawmaterialcostsandalossofshareinthecottagecheese

markethadanadverseeffectonoverallperformance,

wewereabletoreducelossesovertheyearby6.9%.

Site review – MinsterleyAtourMinsterleysiteourfocuswasonrestimulating

growthinoureverydaydessertscategoriessuchastrifle,

whereweholdamarket-leadingposition.Toachievethis

weredevelopedallourrecipesandpackagingformatsin

accordancewithourconsumerresearch.Asaresult,we

investedinnewtechnologytogiveusgreaterflexibility

inthenumberofpotsperpackandthespeedatwhich

theycouldbepacked.Thisprocesswassuccessful,but

growthwasheldbackbypriceincreasesasaresultof

higherrawmaterialcosts.

Business review:Desserts

UniqAnnualReportandAccounts2010 09Directors’ report

Business review | Desserts

Ourco-packagreementwithMüllertoproduce

Cadburybrandeddessertssawconsiderableinvestment

tobuildcapacity,resultinginastate-of-the-art,highly

efficientfacility.Althoughtheanticipatedvolumesdid

notmaterialiseduring2010wearewellpositionedto

workwithourpartnersonfutureopportunities.

Inyoghurtswesuccessfullydevelopedanewrange

ofproductsforM&Sandwonnewbusinesstoprovide

Costawithanexcitingrangeofyoghurtproducts.

Site review – EvercreechOurEvercreechsiteproducesaround70%ofitsoutput

forM&S(increasingto100%followingtheplanned

withdrawalfromcottagecheesesupply),andhas

benefitedbothfromM&S’sstrongperformancein

dessertsandfrominvestingtofurthermatchtheretailer’s

commitmenttoqualityandinnovation.Asaresult,

arangeofnewproductswasdevelopedduring2010

thatincluded‘minis’(small-sizeddessertsdesigned

tobeeatenonthemoveorasexcusableindulgence),

confectionery(dessertsbasedonpopularsweets)andthe

extraspecialchocolate‘jinglebell’Christmasdessert,

deliveringgrowthof19%inpremiumdesserts.

Successfulinnovationwasachievedthrougha

combinationofmarketinsight,high-qualityin-house

chefs,smartandflexibleproductiontechniquesand

ahighlyengagedandcommittedworkforce.Thiswas

demonstratedbyourwinningbothaninnovationand

acollaborationawardfromM&Sduringtheyear.

Asdetailedabove,ourstrongperformancewasoffset

byrisinginputpricesandfallingdemandforcottage

cheeseasanewentrantcameintothemarket.

Byworkingcloselywithourcustomerswewereable

tonegotiatepriceincreasestoreflectrisingcosts.

* All comparisons to sales growth from prior year are adjusted to reflect the additional 53rd week in 2010.

New product development

How minis made their markIn2010Uniqhelpedtodevelopatotallynewconceptindesserts–themini:abite-sizeddessertthatlookedandtastedgreat,butwassmallenoughtoeatonthemoveand‘guiltfree’.

• Marketinsightteamidentifiesagapinthemarket• Uniqworkwithcustomertodeveloptheconcept• Across-functionalteamisbroughttogetherto

delivertheconcept• Equipmentdesignedtodeliversmall‘shots’

ofdessert• Productionstarts• Operatorsapplyleantechniquestoachieve

requiredefficiencies• Productsreachstores,demandrisesrapidly• Increasecapacitytomeetdemand• Salesreach£5m

Technical excellence

Meeting demand at ChristmasWhenourMinsterleysitewasaskedtotakeovertheproductionofM&S’shighlysuccessfulinside-outtrifle,itmeantquicklyrisingtothechallengeofacomplexandtechnicallydemandingprocess.Aproductdevelopmentteamwasrapidlyassembled,anewproductionlinewasdesignedandlaidout,andtrialswerecarriedouttodeterminethelabourteamrequired.Asaresult,all14,000unitsofinside-outtrifleweredeliveredintimeforChristmas.

UniqAnnualReportandAccounts201010Directors’ report

Business review:Food to Go

• Over 100m sandwiches produced during 2010• Share of M&S sandwich market rose to over 65%• Strong cost management

AstheleadingsupplierofsandwichestoM&Sand

theUK’snumbertwosupplierofprepareddressed

salads,Uniq’sFoodtoGooperationsarelocatedat

Northampton(sandwiches)andSpalding(dressed

salads).Eachisrunbyitsownmanagementteam

buttheysharemanyingredientsandprocesses.

FoodtoGoisafast-movingbusinessinwhichcustomers

andconsumersexpectfresh,enticingproductsthatare

availablewhenevertheywantthem.Volumesgoupor

downonadailybasisaccordingtotheweather,time

ofyearoroccasion.Inordertoservicethismarket

successfullyUniqworkswithitscustomers,themajor

retailers,tofullyunderstandwhatconsumerswant

andtodevelopproductsthatmeetandexceedtheir

expectations.Todeliverthese,thefinestandfreshest

ingredientsmustbesourced,prepared,packagedand

despatchedbothquicklyandtothehighestpossible

standard.Thischallengerequireshighlydisciplined

management,acreativeflairforfood,technical

excellenceandafullyengagedworkforcewiththe

flexibilitytodealwithdifferinglevelsofdemand.

PerformanceDrivenbybothorganicgrowthandtheassimilationof

newbusinesswins,salesgrewby13%*to£157min

2010.Profitsroseby51%to£11m,supportedbythe

economiesofscaleachievedthroughhighervolumes,

processefficienciesandthesuccessofnewproduct

launchesintogrowingmarkets.

Sales up 13%* at £157m Profits up 51% at £11m

Site review – NorthamptonFollowingM&S’sdecisionlastyeartoreducethenumber

ofitssandwichsuppliersfromthreetotwo,Uniq’s

Northamptonsitewasabletosecuresignificantnew

business.Duringtheyear,transferoftheremainingnew

linesandvolumeswassuccessfullycompletedwithout

interruptiontoproductionoranynegativeimpacton

quality.ThishelpedustoachieveourhighesteverM&S

sandwichshareduringtheyear.

Ourdedicationtoservice,qualityandtastewasfurther

recognisedbyanumberofawards.WeassistedM&S

towinSandwichMultipleRetaileroftheyear2010,

TheLunch!MultipleRetaileroftheYearAward2010

andwonthe2010BestLowFatRange.Theseawards

alsodemonstratedthestrengthofourrelationship

withM&S,whichstretchesbackover30years.

HighlightsofourworkwithM&Sthisyearinclude:

• TherelaunchoftheFoodontheMovesandwichoffer

tomakeboththeindividualproductsandtherange

moreattractiveandeasierforcustomerstonavigate

• Thedevelopmentofanewsofterfresherbreadfor

alloursandwiches

• ThecontinuingsuccessofthenewSimplyFuller

Longerrange

• Successfullylaunchingnewproductsforthe

fast-growingM&SCaférange

• RelaunchofthepremiumGastropubsandwich

inabagrange.

Wehavecontinuedtoalignouractivitieswiththe

M&SPlanAagendabydeveloping,forexample,an

innovativeschemetousecoldairfromoutsideto

coolourproductionfacilities.

Ofthe£15mnewbusinesswonfromM&S,£10m

wastakenonlastyearandtheremaining£15mwas

transferredthisyear.Inaddition,weachieved£6mof

organicgrowth,drivenbynewproductsandrelaunches

intogrowingmarkets.ThelossoftheSupplairshort-haul

flightsbusiness,asreportedinlastyear’sannualreport,

hadanegativesalesimpactduring2010of£5m.Headline

growthfromthenewbusinesswinswassupportedbya

strongunderlyingperformance,particularlyinthesecond

halfoftheyearasconsumerconfidenceandnew

productlaunchesboostedsales.Likemanyfood

UniqAnnualReportandAccounts2010 11Directors’ report

Business review | Food to Go

producersweexperiencedrawmaterialspriceinflation

duringtheyear.Wewereabletomeettheseincreased

costsbyfindingefficienciesinourbusinessand,where

possible,agreeingpriceincreaseswithourcustomers.

Site review – SpaldingUniq’sSpaldingsiteproducesprivatelabelprepared

dressedsaladsformajorretailersandfoodservice

companies.Themainproductareasarepotatosalad,

coleslawandpastaandvarietysalads.Itslocationin

Lincolnshiremeansitcansourceoverhalfitsfreshsalad

ingredientsfromwithina70-mileradius.Itscommitment

toitscustomers,longheritageintheregionandhighly

efficientmanagementprocesseshavemadeittheUK’s

secondlargestsupplierinthemarket.

TheCo-operativebusinesswinreportedinlastyear’s

annualreportwassuccessfullyservicedduringtheyear.

Weinvestedinincreasedmayonnaiseproductionand

storagecapacityatSpaldingtocopewiththeincreased

volumeandpeakdemand.Ourreputationforservice,

qualityandinnovationhelpedustogrowoursaleswith

allthemajorretailersweserve,andpostanoverallsales

increaseof24%*byvaluefor2010.Successfulproduct

innovation,particularlyingrowingnichemarketssuch

asentertainingathome,wereachievedthroughcareful

marketresearch,consumerinsightandcloseworking

withourcustomers.

However,themarketcontinuedtosufferfromoversupply

in2010,makingitdifficulttogrowmarginalongside

sales.Thisalsomadeitmorechallengingtopasson

inflationarycoststoourcustomers.Althoughthesewere

relativelylowduringthefirstpartoftheyear,finalquarter

inflationgrewmoresharplyandweexpectthistrend

tocontinueinto2011.

Thesignificantprogresswehavemadeduringtheyearin

furtherimprovingefficiencyhashelpedustomaintainour

competitivepositionandachieveprofitabilityinchallenging

markets.Actionstakensuchassmarterbuying,increased

labourefficiencies,reducedwasteandenergyuse,and

moreagilesupplychainshaveallcontributedtostrongly

positioningourbusinessinahighlycompetitivemarket.

* All comparisons to sales growth from prior year are adjusted to reflect the additional 53rd week in 2010.

Growing markets

– Café cultureUKCafésalesareworth£5bn,withM&SCaféthesixthlargestoperatorinthemarket.Thethreelargestcoffeeshops(Costa,StarbucksandCaffeNero)comefromthebrandedcoffeeshopsector.Thebrandedcoffeeshopmarketgrewby12.9%lastyearto£1.9bn.M&Soperatesinthenon-specialistsectorwhichisshowingthefastestoutletgrowth.Asthesupplierofmorethan90%ofM&SCaféchilledsavouryproducts,wearewellpositionedtobenefit.Itisaverydiscerningandfast-movingmarketthatrequiresattractive,greattastingproductswithhigh-quality,freshingredients.WorkingcloselywithM&S,wecarriedoutcarefullytailoredconsumerresearch,anddevelopednewlinesin2010.Asaresult,Uniq’ssalesinthiscategorygrewby12%during2010.

Flexible production

– winning the World CupSuccessinFoodtoGomeansbeingabletoadaptquicklyandefficientlytorapidlychangingdemand.Summerisalwaysthebusiesttimefordressedsalads,buttheWorldCupaddedfurtherdemandforourlargesharingpacksofpastasaladsandcoleslaw,withcustomerordersspikingby50%.NotonlywasourSpaldingsiteabletofullymeetthisdemand,theydidsowithoutanynegativeimpactontheiraverage99.97%servicequalityrate.

CSR VisionWe are committed to the sustained

well-being of our Business, our People, our Partners and our Environment. Our honest

intent is to be socially, ethically and environmentally responsible in everything we do. We will always seekto understand and comply with the appropriate legaland regulatory requirements and go beyond this todrive sustainability through 5 key pillars delivered

through engaged site teams

Our peopleand culture

Vision

Engagement

FareShare

Values

Training/Development

Employee/Wellbeing

Charity

Local Health and Safety Water Customers

Waste Suppliers

Energy NGOs

Packaging Regulatory

Refrigeration Experts

Transport

Food Safety

Healthy

Ourcommunity

Our health,safety andwellbeing

Ourenvironment

Ourbusinesspartners

Uniq Annual Report and Accounts 201012Directors’ report

Corporate Social Responsibility

Our aimWe seek to actively engage all

employees in our vision and wish

to create a culture where everyone

brings all their talent and commitment

to drive our success every day.

Summary of what we are doing: • A clear vision and set of values

which we live every day

• Investment in capability and

growth through training and

development

• Cultural surveys to measure

engagement and drive action

to improve

• A fair deal and a stake in success

Progress

3 of the 4 sites have undertaken baseline cultural surveys with a high engagement of 83%.

Continued roll out of the Uniq Learning System.

Employee absence reduction across the group.

Long-term promises

Continued improvement and engagement in the process, with increasing scores, making Uniq a great place to work.

Talent identification and succession planning.

Sustained low employee absence.

Our governanceUniq is a devolved organisation and

the principal accountability for CSR

rests with the Managing Directors

of each of our operating sites. As an

ethical food producer we recognise

that the management of social,

ethical and environmental issues

requires everyone’s engagement.

Our People and Culture

Guidance is provided by recognised

advisers, endorsed by the CSR forum,

who report annually to the Uniq Board.

We aim to follow the standards of the

Global Reporting Initiative (GRI) in

our key activities and in future reporting.

The group, and all the associated sites,

work within four guiding principles:

• Shared responsibility

• Honesty and accountability

• Sustainable progress

• Demonstrable compliance

Uniq Annual Report and Accounts 2010 13Directors’ report

Business review | CSR

Progress

In 2010 the group was involved in 44 charity/community giving projects (Financial and in-kind). This included sending products to FareShare to feed the homeless.

Numbers of local resident complaints were down on previous years.

Long-term promises

The promise is to increase our involvement for the good of charities we support.

The group aims to be good neighbours, reducing our negative impact on the local community.

Our aimOur commitment is to make positive

contributions to our local community

through employment, education,

good neighbourliness and support

of local causes.

Summary of what we are doing:Principle areas of activity are; community

engagement and charitable giving

to both local and national charities.

We attempt to mitigate our noise and

transport environmental impacts at

all times.

Case Study: Employeecultural surveysDuring 2009 and 2010, the group

rolled out a detailed employee cultural

survey, covering topics such as

engagement, great place to work,

fairness, etc. The aim was to provide

objective data, from which we can

improve and make Uniq a great place

to work and a workplace of choice.

Case Study: Uniq LearningSystem (ULS) In order to enhance the skills

and knowledge of our employees,

Uniq embarked on a learning

journey. This involved undertaking

a skills need analysis, writing

and rolling out competence based

learning units. These are verified,

by the departmental and

site-based assessors.

A member of Northampton’s staff said: ‘It has helped me develop myself, reduce waste and do a better job… it makes us feel we do worthwhile work.’

The group has also supported FareShare in helping feed the vulnerable in our community. Two sites support their local air ambulances.

Case Study: Minimising noise impact at MinsterleyThe site has in the past received a

significant number of noise complaints

relating to steam valve pressure relief

systems. On investigation, it was found

that they were venting and creating a

noise issue. Most of the offending valves

have been replaced, thereby reducing

complaints by 50% since 2008.

Case Study: Local community support at EvercreechEvercreech have engaged with their

local community; running fun-days,

sponsoring school crossing patrols

and being present at farm shop

open days. The site has also been

involved at the local Bath & West

Agricultural Show.

Our Community

Uniq Annual Report and Accounts 201014Directors’ reportBusiness review | CSR

Our aimWe believe good environmental

practice is good business practice.

We are committed to environmental

sustainability in setting ambitious

goals in six key impact areas: waste,

water, energy, packaging, refrigeration

and transport. We will engage our

employees in lean manufacturing

systems to deliver our and our

customers environmental goals.

Our Environment

Summary of what we are doing: Examples include:• Water: We use less and investigate

ways of using recycled water

and using less water in our

cooling systems.

• Waste: Implementing lean

manufacturing across the group

and diversion of waste away

from landfill.

• Energy: Reduction in consumption

using schemes such as; low energy

lighting, free winter cooling, bio-diesel

extraction from effluent, leak

reduction and lagging campaigns.

• Packaging: We are working towards

the use of recycled packaging in our

packaging, target lower weights

and reduce excessive packaging.

• Transport: Implementing green

car travel policies.

Case Study: Reduction of waste to landfill at Spalding and MinsterleySpalding have already reached

<1% waste to landfill, with Minsterley

going from 80% (January 2009),

to 7% waste to landfill in November

2010. At Minsterley, this has been

achieved by segregation and diversion

of product to animal feed and

utilisation of waste to energy facilities.

Progress

Landfill waste across the group has reduced to 29.2% from 38.2% (2009).

Zero Waste to Landfill by 2015, across the group.

Total energy consumption has reduced to 1136KWhr/Tonne of finished product from 1213 KwHrs/Te (2009), giving a 6% reduction.

20% Reduction in Energy (KWHrs per tonne) in 2015 from 2007 baseline.

Continual packaging weight reduction and recyclability.

Minimise CO2 transport and business miles,by maximising use of video conferencing.

No HCFCs in use in the group by 2015.

The group has reduced water consumption in 2010 to 8.4m3/tonne of finished product, from a 2009 figure of 9.2m3, giving a 9% reduction.

20% reduction in water use by 2015 from 2007 baseline. A number of sites have already achieved this target.

Long-term promises

Case Study: Free Coolingat NorthamptonNorthampton have managed to

change their refrigeration equipment

to allow them to take advantage of

cool winter external temperatures.

To this end, the refrigeration is

provided by cool air taken from

outside the factory.

Case Study: Investigation of alternative technologyThe Spalding site is investigating the

use of wind turbines. This is a long

journey which analyses bat and

bird migration patterns over several

seasons, to decrease the impact on

their numbers. The use of renewable

energy is seen as a way forward

within Uniq. Meanwhile, Minsterley

is investigating the use of anaerobic

digestion (AD), to make methane and

subsequently electricity from

it’s waste.

Uniq Annual Report and Accounts 2010 15Directors’ report

Business review | CSR

Our aimIs to engage and collaborate with all

our internal and external stakeholders

to ensure we continually optimise

our ethical performance.

Summary of what we are doing: • We are working with suppliers

and using auditable databases

(SEDEX) to ensure our critical

suppliers are working to

recognised ethical standards.

• Our sites are SEDEX compliant

• We are working with key customers,

to understand their needs, in order

to build improving internal standards.

• We are working with key external

advisers, and regulators to ensure

improvement and understanding.

Our Business Partners

Our aimWe are committed to ensuring that

we provide and maintain a safe place

of work and help our people make

informed health choices. We will

continue to innovate healthy options

and market leading safe products

for our customers.

Summary of what we are doing: Uniq are improving workplace safety

by decreasing the number and severity

of incidents. We have improved the

provision of healthier meals and

nutritional advice and have promoted

active lifestyles at home and work.

Food safety is embedded in the way

we work and we continue to achieve

a year on year improvement.

Uniq is actively supporting our

customers’ health agendas by

increasing the range of healthy and

wholesome options available to

the retailers and end consumer.

The aim is to increase the healthier

food options.

Our Health, Safety and Wellbeing

Progress

Critical suppliers SEDEX registered 75%.

Progress

Reportable Accident rate down to 713/100,000 employees from 849 (2009), both are much below the food industry average (1,350).

All sites scored grade A in the British Retailer Consortium Audit.

Long-term promises

100% of critical suppliers by end 2011.

Long-term promises

Strive to zero Health & Safety Executive reportable accidents.

Enhanced external CSR communications (e.g. website, CSR annual report).

Year on year improvement in food safety.

Case Study: The benefits ofhealth surveillance at SpaldingTo raise awareness on National

Diabetes day occupational health at

Spalding ran a screening programme

for staff and employees. As a result,

a number of individuals were

identified to be possibly suffering

from the condition and were advised

to seek further medical advice.

Case Study: ROSPA Gold Awards All sites in the group have undergone

a fantastic transformation in safety

performance in recent years.

Northampton have been awarded

a ROSPA Gold Award for the past

6 years. This places them amongst

the best safety performers within

the food industry.

Uniq Annual Report and Accounts 201016Directors’ report

Financial review 2010

This financial review covers the activities of the group

for the 12 months ended 31 December 2010. The group

completed the disposals of its overseas businesses

realising funds to settle its outstanding borrowings which

were paid off in full at the end of the year. In March 2011

the group completed a debt for equity swap with its

pension fund, releasing the group from its onerous

liabilities to the pension fund. As this was not completed

until 2011, the results for 2010 are not affected by this

restructuring. However, we have included a proforma

balance sheet and restated profit before tax statement

at the end of this section to illustrate the significant

impact of the deal.

Revenue for continuing operations was up 6.8% on the

prior year (adjusted for 53rd week). The operating result

before significant items for the group moved from £1.9m

loss to £4.1m profit.

Group costsGroup costs represent the cost of running the parent

company and the head office at Gerrards Cross. As a

result of the downsizing of the group, we have reduced

the size of the head office reducing costs to £4.2m in

the year, a saving of £2.1m over last year.

Finance costsThis is split into three types of costs: operational, pension

related and accounting.

Operational finance charges include bank interest and

amortisation of bank fees and are related to the ongoing

operations of the business. Operations finance charges

for 2010 were £1.7m which was £1.7m lower than the

previous year due to the reduction of borrowings on the

realisation of overseas operations. During the year, as

part of our agreement with the pension fund, we were

required to hold surplus funds in a separate Disposal

Reinvestment account rather than pay down our outstanding

debt with the bank. This caused finance charges to be

higher than they would otherwise have been.

Pension finance charges cover two items: net pension

interest that is charged as part of IAS19 and interest

earned on the secure account. IAS19 pension interest

is a reflection of the balance of pension assets and liabilities

and is set at the beginning of the year. The net charge for

2010 was increased over the prior year due to the pension

fund de-risking its asset base to gilts. The pension interest

charge for 2011 will be significantly smaller due to the removal

of the main pension fund from the group in March 2011.

Interest earned relates to the income on the secure account

balance of £97m which was lower year-on-year due to

lower interest rates. This balance, with accrued interest,

was paid over to the pension fund in October 2010.

Accounting finance charges are other finance items and

are generally non-cash. In 2010, this was a net income of

£0.3m compared to a charge of £1.2m in 2009 and relates

to foreign exchange differences on cash balances across

the group.

Significant items Significant items are those items of financial performance

which because of size or incidence, require separate

disclosure. The net significant item for continuing operations

in 2010 was a charge of £2.4m. This included £1.9m of

costs in relation to the closure of our cottage cheese site

at Evercreech (£1.5m of asset impairment and £0.4m of

redundancy costs); £0.3m of redundancy costs and £0.1m

of asset impairment incurred due to the downsizing of

the group head office; £2.7m of costs in relation to the

pension solution and a credit of £2.6m in relation to

the Wincanton settlement.

We have incurred a significant level of costs in exploring

and implementing an acceptable solution for our pension

fund liability. Some of these costs have been incurred in

2010 but we expected to incur further costs of approximately

£3.1m in 2011 as the solution is completed. We reached a

full and final settlement of our litigation with Wincanton in

February 2011 which resulted in us making a final payment

of £2.3m. The provision we were holding for this litigation

Uniq Annual Report and Accounts 2010 17Directors’ reportFinancial review

at £4.9m was in excess of the final payment and therefore

the balance of the provision has been released.

Carrying Value of MinsterleyAt the year end we assessed the balance sheet carrying

value of Minsterley (£48.4m) by carrying out an impairment

review. This review indicated, on the basis of the expected

cashflows in the group’s budgets and strategy plans, that

assets were adequately supported by the future cash flows

and no impairment was required. Since the year end, the

group has carried out a detailed review of the Desserts

operations in the light of recent profit performance and

announced sales losses. The revised plans for Minsterley

are dependent upon securing support from our customers.

Should this support not be forthcoming, the carrying

value may not be supportable.

TaxationThere is no tax charge in the year for continuing operations

although the group made a profit after discontinued items,

as brought forward losses have been used where possible

to mitigate any tax exposures. The group has substantial

tax losses (£83m), unclaimed capital allowances (£214m)

and future tax relief for pension contributions (£73m)

brought forward. These tax attributes exclude the losses

that have been created through additional contributions

as part of the debt for equity swap with the pension fund

in 2011. The growth and strategy of the business will

accelerate the use of these losses.

Discontinued operationsDiscontinued operations include businesses which were

disposed of during the year. The disposal of the Northern

European operations was completed in the first half of

2010: the Netherlands businesses on 9 January and the

German/Poland businesses on 21 April. The results of

these businesses have been included in the group up to

the date of disposal.

Profit after tax and before significant items for the discontinued

businesses was £3.2m. Total significant items were a credit of

£32.2m which includes a charge of £0.7m for onerous leases

on group properties offset by £32.9m of profit on disposal of

the businesses. The profit on disposal includes a credit of

£30.3m relating to foreign exchange gains previously credited

to reserves which have been recycled to the profit and loss

account on disposal.

Summary results2010

£m2009

£m

UK trading operating profit 8.3 4.4Group costs (4.2) (6.3)Operating profit/(loss) before significant items 4.1 (1.9)Finance costs (excluding pension related) (1.4) (4.6)Profit/(loss) before significant items 2.7 (6.5)Significant items (2.4) (0.7)Pension finance costs (11.5) (11.3)Loss before tax (11.2) (18.5)Tax charge – (0.4)Loss from continuing operations (11.2) (18.9)Discontinued items net of tax 35.4 (2.0)Profit/(loss) attributable to shareholders 24.2 (20.9)Basic profit/(loss) per share 21.3p (18.4)p

Funds flow2010

£m

Operating profit 4.1Depreciation and amortisation 9.9 EBITDA 14.0Net capital expenditure (15.0)Increase in working capital (4.0)Continuing operating cash flow (5.0)Provisions and significant items (3.1)Tax (1.1)Discontinued operations 26.8Pension contributions (0.9)Other (1.9)Total funds flow 14.8Opening net debt (4.0)Closing net cash 10.8

Uniq Annual Report and Accounts 201018Directors’ report

Funds flowDuring the year the continuing group had a £5.0m operating

cash outflow. This includes £15.0m spend on capital

expenditure of which £10.6m related to the completion of

the Desserts project at the Minsterley site. Working capital

outflow for continuing operations in the year was £4.0m

which reflects the increased pressure from suppliers. During

the year the continuing group spent £3.1m on provisions and

significant items: £1.3m related to restructuring costs in

Desserts and £1.8m related to group head office restructuring

and pension legacy costs. The provision balance at the

year end of £5.8m includes £2.3m which was paid in final

settlement to Wincanton in February 2011, £1.3m in relation

to overseas disposals, £1.2m for onerous leases on

properties, £0.3m relating to Desserts restructuring costs

and £0.7m of pension legacy fees. Tax payments of £1.1m in

the year relate to tax assessed on the disposal of St Hubert

which was completed in 2008. Net cash received from

discontinued operations of £26.8m represents the total cash

flow of the discontinued businesses to the date of disposal

plus the proceeds from disposals after payment of disposal

costs. Pension contributions relate to payments made to the

Pension Trustee to fund transfers out and pension costs

and interest costs of £1.5m reflect the level of borrowings

maintained through the year. Total funds flow for the year

was £14.8m.

Working capital and credit insuranceAs noted in previous years, the group has experienced

significant pressure from suppliers on payment terms

and rates due to the withdrawal of credit insurance on

the company and the impact of the pension deficit on

the group’s balance sheet. This has resulted in a further

worsening of the group’s working capital position and

a cash outflow. Having completed the pension deal,

the group expects to be able to improve the availability

of credit insurance through discussions with relevant

insurers and therefore return to more normal trading

terms with its suppliers.

FundingOpening net debt at the beginning of the year was £4.0m

including £6.1m of net cash in the discontinued businesses.

The disposal of these businesses gave rise to cash proceeds

which, in accordance with a previous agreement with

the pension fund, were placed in a separate Disposal

Reinvestment account during the period of negotiation

with the pension fund to find a final solution. We maintained

our borrowings and the net cash in Disposal Reinvestment

account until 31 December 2010 when our bank facility

expired and all borrowings were repaid in full. Net cash

at the year end after payment of borrowings was £10.8m.

We have negotiated a new bank facility with Lloyds

TSB which was conditional on completing the debt for

equity swap with the pension fund. This process was

completed on 22 March 2011 and the new bank facility

became available. This new facility provides for a £15m

term loan, amortising at £3m each year for three years

with a lump sum repayment at the end of the facility,

and a £10m revolving credit facility to fund working

capital requirements.

PensionsThe group operates a main UK scheme and a number

of other small pension funds including an unfunded

overcap scheme, medical benefits provision and small

legacy scheme.

The IAS19 deficit on the main UK scheme at the beginning

of the year was £227.8m which was reduced significantly

during the year by the payment of the monies in the secure

account of £97.6m. Other movements on the deficit include

£29.4m return on assets and £40.5m relating to the unwinding

of the liabilities. There was no service charge as the

scheme was closed to further accrual in 2009. The closing

deficit was £142.1m (excluding a provision of £3.4m for

scheme expenses).

Post balance eventsPensions – update for 2011In March 2011, the group completed a deal to swap the

debt owed to its pension fund for equity in the company.

This deal has removed the main UK pension deficit from

the balance sheet of the group but as this deal was

completed in 2011, this is not reflected in these financial

statements. To illustrate the significant impact that this

deal will have on the group, a proforma Balance Sheet is

shown in the table opposite. The profit before tax (shown

opposite) has been restated as if the pension fund had

not existed throughout the financial year.

Significant VAT recoveryIn March 2011, the group recovered £2.6m from HMRC

in relation to various claims under the Fleming ruling.

This repayment consisted of £1.0m of VAT recovery and

£1.6m of interest on the claim. The group is continuing

to claim further amounts under the Fleming ruling.

Uniq Annual Report and Accounts 2010 19Directors’ reportFinancial review

Proforma Balance Sheet – Effect of the Pension Deal

£m 2010Adj

(note 1)Pro

forma

AssetsNon-current assetsProperty, plant and equipment 80.4 80.4 Intangible assets 30.5 30.5 Deferred tax assets 13.9 13.9

124.8 124.8 Current assetsInventories 13.8 13.8 Trade and other receivables 33.2 33.2 Cash and cash equivalents 10.8 (3.3) 7.5

57.8 54.5 Total assets 182.6 179.3 LiabilitiesNon-current liabilitiesBorrowings – 11.0 11.0Retirement benefit obligations 149.4 (145.6) 3.8 Provisions 0.8 0.8

150.2 15.6 Current liabilitiesBorrowings – 3.0 3.0 Trade and other payables 41.6 41.6 Provisions 5.0 5.0 Income tax liabilities 7.7 7.7

54.3 57.3 Total liabilities 204.5 72.9 Total assets less liabilities (21.9) 106.4EquityShareholders’ equityTotal called up share capital 11.5 (10.3) 1.2 Share premium 0.1 64.5 64.6 Other reserves (330.2) (330.2) Retained earnings 296.7 74.1 370.8 Total equity (21.9) 106.4

Note 1 – The adjustments reflect the issue of shares by the parent company at the closing price on 16 March 2011 to the pension fund in exchange for the cancellation of the IAS19 pension deficit and the payment of £14m as a final contribution to the pension fund, funded by the new bank facility.

Restated Profit before tax – Effect of the Pension Deal

£m 2010Adj

(note 2) Restated

Continuing operationsRevenue 311.9 311.9Cost of sales (264.3) (264.3)Gross profit 47.6 47.6Distribution expenses (18.3) (18.3)Administrative expenses (25.2) (25.2)Operating profit before significant items 4.1 4.1Significant items (2.4) 2.7 0.3Operating profit after significant items 1.7 2.7 4.4Net pension interest (12.1) 12.1 –Finance income 1.2 (0.6) 0.6Finance expenses (2.0) (2.0)Net finance changes (12.9) 11.5 (1.4)(Loss)/profit before tax (11.2) 14.2 3.0

Note 2 – The adjustments reflect the removal of the significant cost in relation to the management of the group’s pension fund, the pension interest charge and the finance income related to the monies previously held in the secure account for the benefit of the pension fund from 1 January 2010.

Business performance measurementThe group measures its performance using a series of

KPIs, both financial and non-financial. The financial KPIs

are: sales growth; gross margin percentage; operating

profit percentage and return on capital. The non-financial

KPIs vary according to business unit.

Senior management are remunerated by bonuses

based on group and divisional financial performance

and in 2010, by delivery of the pension solution

and by share incentives, more details of which

are included in the remuneration report.

Financial riskThe group is subject to financial risks, but has

procedures and controls in place to mitigate

these risks. The group’s major financial risks

can be split as follows:

Market risk – Market risk can be broken down into

currency risk and interest rate risk. The group

has formal procedures and policies to mitigate

these risks.

Credit risk – The majority of the group’s customers

are large, established retail organisations with a good

credit record. As a result the group does not have

significant concentrations of credit risk.

Liquidity risk – During 2010 the group operated

within its banking facility which expired at the end

of December 2010. A new bank facility of £25m has

been negotiated and was available for use by the

group from March 2011. Liquidity risk remains low

due for the group due to formal procedures and

policies to manage cash resources.

Martin BeerFinance Director26 April 2011

Uniq Annual Report and Accounts 201020Directors’ report

Principal risks

This section updates what the board believes are the most significant risks and uncertainties which are specific to Uniq’s businesses.

Minsterley profitabilityMinsterley has a history of losses and has not generated a

profit in any reporting period since the site was acquired in

2005. In 2009, the Paignton site was closed and volume was

successfully consolidated into the Minsterley site. In the last

five years, there have been investments in the infrastructure,

service and quality at the Minsterley site and financial results

have improved significantly.

Management recognises the recovery of profitability

of the Minsterley site has taken longer than expected.

The site serves four sub-sectors of the market: Cadbury

chocolate desserts, premium differentiated yoghurt,

premium and everyday desserts. The Cadbury, yoghurt

and premium dessert sub-sectors are either profitable or

on track to achieve profitability, while the site losses are

all concentrated in the everyday desserts sub-sector.

The Desserts review has approved a series of steps

to address and stop the losses in everyday desserts.

Minsterley produces Cadbury desserts under a co-packing

agreement. Additional capacity has been successfully installed

and the Cadbury manufacturing facility at Minsterley is highly

efficient. However, the anticipated growth has not yet

materialised and there are ongoing discussions with the

customer regarding the terms of the co-packing agreement.

There is a risk that Cadbury volumes could continue to decline,

or that the co-packing agreement could be amended or

terminated. Any of these outcomes could have an adverse

impact on the group’s operations and its financial condition.

CustomersThe group is heavily dependent on a limited number of

significant grocery retailers in the UK and one major retailer,

M&S, represents over half of the group’s sales. In line with

industry practice, the majority of Uniq’s UK sales are made by

means of short-term standard purchase orders rather than

long-term contracts. In recent years, the major multiple

retailers have increased their share of the UK grocery market

and price competition between those retailers has intensified.

This price competition has led the major multiple retailers

to seek lower prices from their suppliers. Uniq has created

a decentralised, entrepreneurial business structure to

enable it to get closer to its customers and to mitigate

this risk. However, there can be no assurance that Uniq’s

customers will continue to purchase its products at

current volumes, at current pricing or on current terms.

The credit insurance market and the creditworthiness of the group and its customersAs is common in the food industry, many suppliers use

credit insurance to reduce the risk of exposure to the group.

The credit extended by suppliers is an important part of

the group’s funding. Over the last few years, the level of

insurance available to the group’s suppliers has significantly

reduced, owing to a general tightening of credit insurance

and the perceived extent of the group’s UK pension deficit.

The removal of the pension deficit will create the necessary

conditions for credit insurance cover to be reinstated and

therefore, in time, this risk will reduce.

Weather and seasonalitySales of some products, such as salad products, are

materially affected by unseasonable weather and seasonality.

Sales can be materially increased or reduced as a result

of weather fluctuations and seasonality.

InnovationThe group operates in competitive markets and in fast moving

sectors of the food industry. Its success is dependent on

anticipating changes in consumer preferences, including

dietary and nutritional concerns and on successful new

product development and product relaunches in response

to such changes in consumer behaviour. The group’s future

results will depend on its ability successfully to identify,

develop, manufacture, market and sell new or improved

products in these changing markets.

Changes in the cost and availability of raw materialsThe group purchases its raw materials, many of which

are commodities, from numerous suppliers. There are

a number of factors affecting the price of these raw

materials, such as quality, availability, demand, weather

conditions, currency fluctuations, agricultural policies

and political instability. Many of these raw materials are

subject to potentially significant price fluctuations.

The group will generally not be a sufficiently large buyer

to have any control over these prices and may be unable

to pass on such price increases to its customers in

whole or part or without a period of delay.

21Uniq Annual Report and Accounts 2010

Directors’ report

Directors’ responsibilities

The directors are responsible for preparing the Annual Report and the group and parent company financial statements in accordance with applicable law and regulations.

Company law requires the directors to prepare group and

parent company financial statements for each financial

year. Under that law they are required to prepare the

group financial statements in accordance with IFRSs as

adopted by the EU and applicable law and have elected

to prepare the parent company financial statements on

the same basis.

Under company law the directors must not approve the

financial statements unless they are satisfied that they give

a true and fair view of the state of affairs of the group and

parent company and of their profit or loss for that period.

In preparing each of the group and parent company

financial statements, the directors are required to:

• select suitable accounting policies and then apply

them consistently;

• make judgements and estimates that are reasonable

and prudent;

• state whether they have been prepared in accordance

with IFRSs as adopted by the EU; and

• prepare the financial statements on the going

concern basis unless it is inappropriate to presume

that the group and the parent company will

continue in business.

The directors are responsible for keeping adequate

accounting records that are sufficient to show and

explain the parent company’s transactions and disclose

with reasonable accuracy at any time the financial

position of the parent company and enable them to

ensure that its financial statements comply with the

Companies Act 2006. They have general responsibility

for taking such steps as are reasonably open to them

to safeguard the assets of the group and to prevent

and detect fraud and other irregularities.

Under applicable law and regulations, the directors

are also responsible for preparing a Directors’ Report

and a Directors’ Remuneration Report that complies

with that law and those regulations.

The directors have also decided to prepare voluntarily

a Corporate Governance Statement as if the company

were required to comply with the Listing Rules and the

Disclosure Rules and Transparency Rules of the Financial

Services Authority in relation to those matters.

The directors are responsible for the maintenance

and integrity of the corporate and financial information

included on the company’s website. Legislation in the

UK governing the preparation and dissemination of

financial statements may differ from legislation in

other jurisdictions.

We confirm that to the best of our knowledge:

• the financial statements, prepared in accordance

with the applicable set of accounting standards,

give a true and fair view of the assets, liabilities,

financial position and profit or loss of the company

and the undertakings included in the consolidation

taken as a whole; and

• the directors’ report includes a fair review of the

development and performance of the business

and the position of the issuer and the undertakings

included in the consolidation taken as a whole,

together with a description of the principal risks

and uncertainties that they face.

Geoff EatonChief Executive

Martin BeerFinance Director26 April 2011

Martin BeerFinance director

John WarrenChairman

Geoff Eaton Chief executive

Uniq Annual Report and Accounts 201022Directors’ report

John WarrenChairman * † ‡ //

Joined the board in 2007, served as Interim Chairman from 25 June 2009 and appointed Chairman on 14 April 2010. He is also chairman of the audit committee and the pension committee. He was formerly finance director of United Biscuits plc and WH Smith plc. He is a fellow of the Institute of Chartered Accountants in England and Wales and is a non-executive director of The Rank Group plc, Bovis Homes Group plc and Spectris plc.

Geoff Eaton Chief executive ‡ //

Joined the board as chief executive in 2005. He was formerly chief executive of ISIS Research from 2001 to 2004. Prior to that he spent 13 years with Tomkins plc where he held a number of senior executive roles including executive director at RHM in the UK, executive vice-president at Gates Corporation in the US and head of corporate development for the Tomkins Group. He is a chartered accountant, having qualified with Arthur Andersen.

Martin Beer Finance director //Appointed to the board in 2002 as finance director. He is a chartered accountant, having qualified with Price Waterhouse. He has been with the group since 1990 in various financial roles, including finance director of Unigate Dairies for five years.

Belinda Gooding Non-executive director * † ‡

Joined the board in 2006. She is chief executive of Roots & Wings, a trustee of Chelsea Physic Garden and a non-executive director of Strutt & Parker. She was formerly chief executive of 2 Save Energy Ltd, a non-executive director of Biloxi Southern Foods, Sir Hans Sloane chocolates and Pet’s Kitchen and chief executive of Duchy Originals Ltd from 2000 to 2007. Prior to that she spent ten years in marketing roles with Mars (Masterfoods) and was group marketing director of Dairy Crest Group plc.

Board of directors and senior management

Dr Matthew Litobarski Non-executive director

Belinda GoodingNon-executive director

Stephen DraiseyManaging director

Andrew McDonaldGeneral counsel and company secretary

23Uniq Annual Report and Accounts 2010

Directors’ reportBoard of directors

Dr Matthew Litobarski Non-executive director * † ‡