Embed Size (px)

Citation preview

uniCredit Ghana Limited

Annual ReportFor The Year Ended 31 December 2015

Page

1

2

3

4

6 - 7

8

9 - 11

12

13

14 – 15

16

17

18

19

21 – 56

Contents Corporate Information

Misson, Vision & Values

Corporate Information

Board of Directors

Chairman’s Statement Executive Committee

Chief Executive’s Statement Directors’ Report Statement of Directors’ Responsibilities Independent Auditor’s Report Statement of Pro�t or Loss and Other Comprehensive Income Statement of Financial Position Statement of Changes in Equity Statement of Cash Flow Notes to the Financial Statements

Contents

uniCredit 2015 Annual Report | 01

About UsuniCredit Ghana Limited is one of the leading Savings & Loans Companies in Ghana, licensed by the Bank of Ghana (BoG) under the Non-Bank Financial Institutions Act 2008 (Act 774). The company is headquartered at No. 3 North Ridge Lane, Accra within the capital’s cosmopolitan arena. Since 2007, the footprints of uniCredit on the �nancial and banking landscape of Ghana have been progressively distinct, currently with eighteen (18) fully-networked branches in four (4) regions of Ghana.

uniCredit envisions becoming the most e�cient and e�ective Savings and Loans Company operating in the SME Banking market. In furtherance of this, we seek to provide our esteemed customers with convenient, tailored and reliable banking products and services through our state-of-the-art IT infrastructure and dedicated team of professionals deployed across all our branches. We o�er a range of personal, business and institutional �nancial solutions that are designed to deliver optimum value to our customers.

uniCredit is also committed to distinguishing itself through excellence, as is evidenced by its listing on the 2014 Ghana Club 100 as a member of the prestigious group of the current top 100 companies in Ghana. This recognition of the institution’s performance validates its focus on ensuring both productivity and operational vigilance to secure our customers’ interests.

With an ongoing branch expansion drive and the recent launch of its electronic banking suite, uniCredit gives you several reasons to own any of our deposit and credit products. We keep to our brand promise in going the extra mile to delight you, our esteemed customer, through a responsive and proactive approach to handling your business needs. Other services provided to our clients include:

Our sta� are ably-equipped to address your banking concerns and guide you towards the realisation of your personal and business �nancial goals. At uniCredit, we are ready to grow with you.

uniCredit…Your Caring Partner

SME & Personal BankingBusiness Advisory ServicesBusiness PlanningFinancial PlanningCash Flow Forecasts

Corporate Information

02 | uniCredit 2015 Annual Report

MISSIONTo develop Financial Products and Services and make them easily accessibleto our target market.

VISIONTo be the most e�cient and e�ectiveSavings & Loans Company operatingin the SME Banking Market.

CORE VALUES Caring Flexibility E�ciency Integrity Teamwork Accountability Professionalism

Misson, Vision & Core Values

uniCredit 2015 Annual Report | 03

Mr. Frank Oppong-Yeboah ChairmanMr. Samuel Sakyi-Hyde Chief Executive O�cerMrs. Akosua Du�uor Executive DirectorDr. Kwabena Du�uor II Non-Executive DirectorMrs. Boatemaa D. Barfour-Awuah Non-Executive DirectorMr. Simeon Tawiah Non-Executive DirectorMr. Benjamin Ofori Non-Executive DirectorMr. Anthony Marshall Arpoh Esq. Secretary

Mr. Samuel Sakyi- Hyde Chief Executive O�cerMrs Akosua Du�uor Executive DirectorMr. P. V. Yeboah-Asiamah General ManagerMr. Daniel Osei Head, Finance & AdministrationMr. Seth Ofori- Larbi Head, Internal Control

Deloitte and Touche Chartered Accountants 4 Liberation Road P. O. Box GP 453 Accra

Anthony Marshall Arpoh P. O. Box GP 18729, Accra. uniCredit Ghana Limited No. 3 North Ridge Lane North Ridge P. O. Box GP 18729, Accra. uniBank (Ghana) Limited

Directors:

Executive Committee:

Auditors:

Solicitor:

Registered O�ce:

Bankers:

Corporate Information

Board of Directors

Mr. Simeon TawiahNon-Executive Director

Mrs. BoatemaaD. Barfour-AwuahNon-Executive Director

Dr. Kwabena Du�uor IINon-Executive Director

Mr. Benjamin Kwame OforiNon-Executive Director

Mr. AnthonyMarshall Arpoh Esq.Secretary

Mrs. Akosua Du�uorExecutive Director

Mr. Samuel Sakyi-HydeChief Executive O�cer

Mr. Frank Oppong-YeboahChairman

04 | uniCredit 2015 Annual Report

Chairman’s Statement

Distinguished Shareholders,on behalf of the Board of Directors and Management of uniCredit Ghana Limited, it is my pleasure to welcome you to the 3rd Annual General Meeting of your Company; and present to you the Annual Report and Financial Statements for the �nancial year ended 31st December, 2015. The Company’s �nancial performance remained stable within the context of a competitive and challenging environment.

Operating EnvironmentThe Ghanaian economy in 2015 remained resilient despite the severe energy crisis, domestic and external debt burdens, and macroeconomic volatility. During the year, the government embarked on a stabilisation programme with the International Monetary Fund to address the increasingly unsustainable �scal and current account imbalances. This sought to restrain and prioritise public expenditure, increase tax revenue and strengthen the e�ectiveness of the central bank’s monetary policy. The issuance of a $1 billion Eurobond also helped to support the currency, cover the budget and rollover short-term debt.

Over the medium term, the economy is projected to recover with a real GDP growth of 5.4% in 2016 and 5.8% in 2017 anchored on higher oil and gas production, increased private sector and public infrastructure investments, as well as an improved macroeconomic framework. Ghana continues to enjoy a relatively favourable political risk pro�le, and the upcoming 2016 election is expected to be peaceful. It is also the expectation that

the government will ensure strong �scal discipline in order to remain within budget de�cit targets during this period. The macroeconomic highlights for 2015 indicated GDP growth at 4.1%. Real GDP is projected at 5.4% in 2016 in anticipation of increasing oil production and improvement in the electricity generation shortfall. Various strategies have been outlined in the 2016 budget to increase the revenue generation capacity of the government and reduce the country’s rising debt burden. In that regard, a new Income Tax Act 2015 (Act 896) came into force on 1st January 2016. The Act seeks to among others simplify the income tax regime, improve tax compliance and impose other new taxes. It also seeks to change the tax rate of some of the existing taxes in the country, and it is expected to yield additional revenue equivalent to 0.3% of GDP.

2015 Operating ResultsYour Company, uniCredit Ghana Limited, recorded a Pro�t before Tax of GH¢9,468,660.00 and Pro�t after Tax of GH¢8,240,901.00. Net Operating Income increased by 43% and Current Operating Expenses grew by 33%. Shareholders’ Funds increased substantially from GH¢30,321,844.00 to GH¢70,933,745.00, representing a signi�cant progression of 134%.

DividendThe Board does not intend to recommend any dividend to shareholders. In furtherance of continuously delivering value to shareholders, the Board of Directors recommends that the income surplus balance be ploughed back into company operations.

Mr. Frank Oppong-YeboahChairman

06 | uniCredit 2015 Annual Report

Changes in Capital StructureIn the year under review, shareholders injected additional GH¢32.37 million to increase our stated capital from GH¢17.49 million at the beginning of the year to GH¢49.86 million at the end of the year. The Board, Management and Sta� are most grateful to you, our dear shareholders, for your �nancial contributions that propelled the Company’s �nancial performance and expansion to the success attained.

Corporate GovernanceOur Company is committed to ensuring e�ective corporate governance and sound risk management practices which are of fundamental importance in the industry. The adherence to good corporate governance principles continues to be the mainstay of our operations, thereby helping us to maintain consistency and rigour in our decision-making processes. The Companies Act, 1963 (Act 179); Non-Bank Financial Institutions Act, 2008, (Act 774); the Anti-Money Laundering Act, 2008 (Act 749); and the Anti-Money Laundering Regulations, 2011(LI 1987) provide us with the regulatory framework for ensuring e�ective corporate governance and an e�cient compliance regime.

Outlook for the Year 2016The year 2016 is an election year and as always with Ghana's political stability and deepening democracy, I am sure that the

elections will be held peacefully. uniCredit Ghana Limited is highly con�dent in the future of Ghana, given the strong economic potential of the country and its sustained peaceful governance.

For uniCredit Ghana Limited, the year 2016 will be a year of transformation for new systems and processes to be put in place with the aim of increasing our market share and achieving sustained organic growth. We are very optimistic about the future of our Company.

AcknowledgementsOn behalf of the Board of Directors, we wish to thank each and every Shareholder; our cherished Customers; and other Stakeholders for the �rm con�dence and support demonstrated over the years. I would also like to express my sincere gratitude to our employees at all levels for their contribution to the growth and pro�ts we made in 2015.

We are con�dent that TOGETHER we will continue to build uniCredit Ghana Limited into a more pro�table business and record a considerable increase in its market share by our next Annual General Meeting.

Thank you for your attention.

Frank Oppong-YeboahChairman

For the year ended 31 December 2015

Chairman’s Statement

uniCredit 2015 Annual Report | 07

Executive Committee

08 | uniCredit 2015 Annual Report

P.V. Yeboah-AsiamahGeneral Manager

Mrs. Akosua Du�uorExecutive Director

Seth Ofori- LarbiHead, Internal Control

Daniel OseiHead, Finance and Admin.

Mr. Samuel Sakyi- HydeChief Executive O�cer

IntroductionI am delighted to present to you, our dear shareholders, the performance of your Company for the �nancial year ended 31st December 2015. The operating economic environment in the year 2015 was challenging, but in spite of these challenges I am pleased to inform you that your Company rea�rmed the strength of our business model to deliver yet another sterling performance.

A number of challenges characterised the operating environment in 2015, and these included; the severe power crisis which persisted for the most part of the year, with measures put in place by the government to ease the burden materialising a few months to the end of the year. The depreciation of the Cedi was steep during the �rst half of 2015 but recovered to close the year at 15.7% as compared to 31.3% in 2014. The falling prices of commodities including oil, cocoa and gold on the international markets also adversely impacted the Ghanaian economy.

In addition, the Central Bank merged the policy rate with the reverse repo rate during the year and also increased the policy rate to 26% from 21% at the end of 2014. Global economic activity remained subdued during the review period driven mainly by slower growth prospects in China and other emerging market economies.

Financial PerformanceThe New Dawn Strategy which was introduced in 2014 was adhered to in the year 2015. As a result, your Company delivered

a strong �nancial performance consistent with our performance over the years in spite of intense competition and a tough operating environment. This is evidenced by a pro�t before tax of GH¢9.46 million compared to GH¢4.26million in the previous year. Most of our business lines recorded growth, which is re�ective of our deliberate e�orts to create sustainable value and a focused implementation of our New Dawn Strategy.

The total asset base of the Company grew by 61.24% during the year from GH¢203.6 million in 2014 to GH¢328.4 million in 2015. Customer deposits increased by 49.58%, due to gains from our expanded branch network and deliberate deposit mobilisation e�orts during the period. We maintained a continuous focus on enhancing the quality of relationship management, credit monitoring and recoveries to e�ectively manage the quality of our loan book. That notwithstanding, speci�c and challenging advances were adequately provided for and recovery measures put in place. Our capital adequacy ratio remained relatively high at 30.75% arising out of our Tier I funding and increased earnings in 2015. We will leverage our strong capital position to sustain planned future development of our business.

Operational PerformanceTo improve the Company’s accessibility, we have broadened the Company’s delivery channels and diversi�ed its market o�ering, as evidenced by the expanded branch network to include Dr. Mensah- Kumasi, Ridge, Kasoa, Kokomlemle,Kantamanto Central and Agbogbloshie branches to enhance our retail franchise. In

uniCredit 2015 Annual Report | 09

Chief Executive’s StatementMr. Samuel Sakyi-HydeChief Executive O�cer

For the year ended 31 December 2015

Chief Executive’s Statement

order to reduce customer tra�c and activity in our banking halls and to further improve upon our customer services, we have also initiated the process of introducing Automated Teller Machine (ATM) products and services. As at the end of the year 2015, �ve (5) ATM machines had been procured for installation at vantage business o�ces. New Products and Services

TOTAL ASSETS TOTAL DEPOSITS

300.000

250.000

200.000

150.000

100.000

50.000

02011 2012 2013 2014 2015

350.000

300.000

250.000

200.000

150.000

100.000

50.000

2011 2012 2013 2014 20150

Total Assets

Total Deposits

Loans & Advances

Investments

Shareholders Funds

Pro�t before Tax

Pro�t after Tax

Return on Equity

78,12064,46937,47218,804

7,1254,1492,623

37.0%

104,73089,93557,62725,045

9,3022,5611,781

20.0%

156,835123,201

82,10339,86818,406 2,998 2,294

12.5%

203,672162,630

86,734.00 73,488.00 30,321.00

4,262.00 3,216.00

10.6%

328,406243,261

101,597.00 139,857.00

70,933.00 9,468.00 8,240.00

11.6%

2011GH¢ '000

2012GH¢ '000

2013GH¢ '000

2014GH¢ '000

2015GH¢ '000

SUMMARY OF COMPANY'S PERFORMANCE OVER THE PAST FIVE YEARS

10 | uniCredit 2015 Annual Report

LOANS & ADVANCES SHAREHOLDERS FUND

120.000

100.000

80.000

60.000

40.000

20.000

2011 2012 2013 2014 20150

80.000

70.000

60.000

50.000

40.000

10.000

20.000

30.000

02011 2012 2013 2014 2015

PROFIT BEFORE TAX PROFIT AFTER TAX

2011 2012 2013 2014 2015

10.000

6,0007,0008,0009,000

5,000

4,1494,000

1,0002,0003,000

0

2,561 2,998

4,262

9,468

2011 2012 2013 2014 2015

6,000

7,000

8,000

9,000

5,000

4,000

1,000

2,000

3,000

0

1,7812,294

3,216

8,240

2,623

The year 2015 saw the development of new products and services as well as revamping some existing products in line with customer needs and competitive insights. The “EazzLife” consumer asset �nance product was launched to enable our current and potential customers acquire an array of vital home and electronic appliances such as LED TVs, washing machines, etc. and make �exible payments over a period of twelve (12) months. Another product developed was the “Smart Personal Loan”, a same-day loan for salaried workers. This product is available to account and non-account holders of uniCredit.

Head O�ce In the spirit of breaking new grounds with our New Dawn Strategy, I am very pleased to inform you that our corporate head o�ce has been relocated to a plush, ultra-modern facility at North Ridge, Accra. This relocation has enhanced the visibility of the uniCredit brand and made it synonymous with vibrancy and distinction.

ConclusionOn behalf of the Board, I would like to appreciate our customers for their continued patronage of our products and services and our shareholders for their unwavering support to the Company’s Board, Management team and the business as a whole. Finally, I would also like to thank our talented employees for their continued commitment and dedication to the Company. Ladies and Gentlemen, I am con�dent that with your continued support, 2016 will be a tremendously successful year.

Thank you and God bless us all.

Samuel Sakyi-HydeChief Executive O�cer

For the year ended 31 December 2015

Chief Executive’s Statement

uniCredit 2015 Annual Report | 11

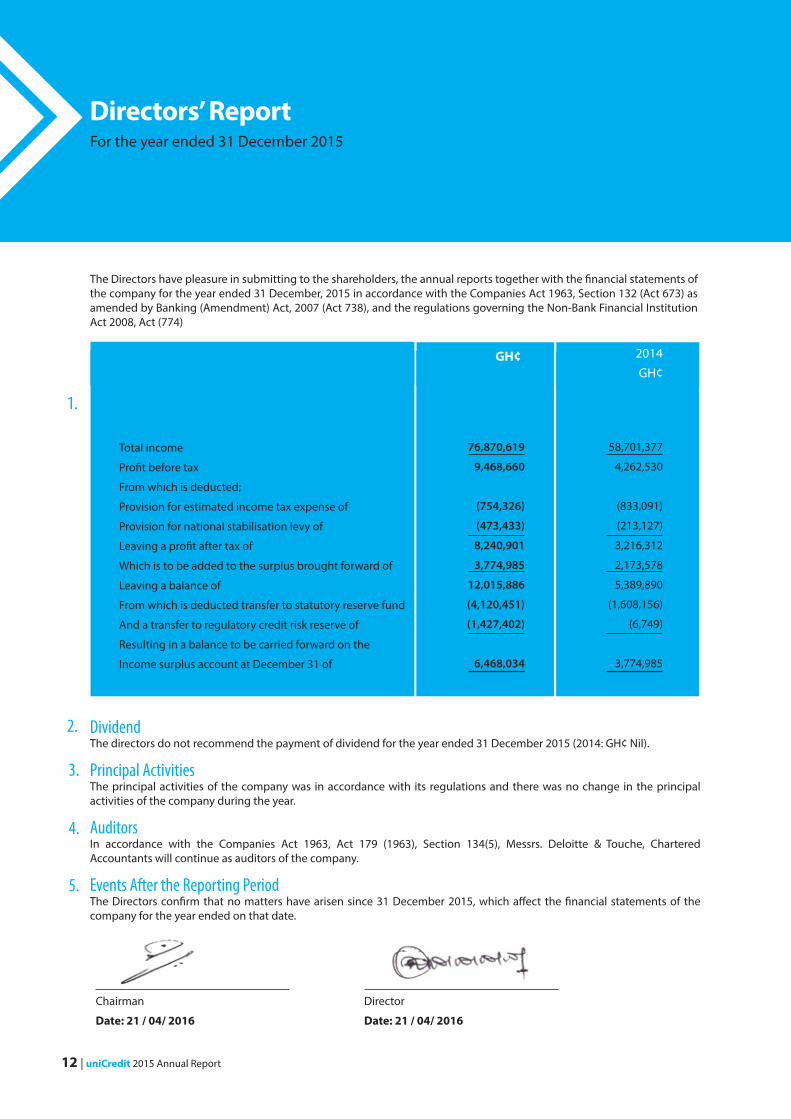

The Directors have pleasure in submitting to the shareholders, the annual reports together with the �nancial statements of the company for the year ended 31 December, 2015 in accordance with the Companies Act 1963, Section 132 (Act 673) as amended by Banking (Amendment) Act, 2007 (Act 738), and the regulations governing the Non-Bank Financial Institution Act 2008, Act (774)

DividendThe directors do not recommend the payment of dividend for the year ended 31 December 2015 (2014: GH¢ Nil).

Principal ActivitiesThe principal activities of the company was in accordance with its regulations and there was no change in the principal activities of the company during the year.

AuditorsIn accordance with the Companies Act 1963, Act 179 (1963), Section 134(5), Messrs. Deloitte & Touche, Chartered Accountants will continue as auditors of the company.

Events After the Reporting PeriodThe Directors con�rm that no matters have arisen since 31 December 2015, which a�ect the �nancial statements of the company for the year ended on that date.

Total income

Pro�t before tax

From which is deducted;

Provision for estimated income tax expense of

Provision for national stabilisation levy of

Leaving a pro�t after tax of

Which is to be added to the surplus brought forward of

Leaving a balance of

From which is deducted transfer to statutory reserve fund

And a transfer to regulatory credit risk reserve of

Resulting in a balance to be carried forward on the

Income surplus account at December 31 of

76,870,619

9,468,660

(754,326)

(473,433)

8,240,901

3,774,985

12,015,886

(4,120,451)

(1,427,402)

6,468,034

58,701,377

4,262,530

(833,091)

(213,127)

3,216,312

2,173,578

5,389,890

(1,608,156)

(6,749)

3,774,985

Result

Chairman

Date: 21 / 04/ 2016

Director

Date: 21 / 04/ 2016

2015 GH¢ 2014

GH¢

2.

1.

3.

4.

5.

For the year ended 31 December 2015

Directors’ Report

12 | uniCredit 2015 Annual Report

For the year ended 31 December 2015

Statement ofDirectors’ Responsibilities

The directors are responsible for preparing �nancial statements for each �nancial year which give a true and fair view of the state of a�airs of the company at the end of the �nancial year and of the pro�t and loss of the company for that year. In preparing those �nancial statements the directors are required to:

The directors are responsible for ensuring that the company keeps accounting records which disclose with reasonable accuracy, at any time , the �nancial position of the company and which enables them to ensure that the �nancial statements comply with the Companies Code, 1963 (Act 179). They are also responsible for taking such steps as are reasonably open to them to safeguard the assets of the company and to prevent and detect fraud and other irregularities.

The above statement which should be read in conjunction with the statement of the auditors’ responsibilities set out on page 6 is made with a view to distinguishing for shareholders the respective responsibilities of the directors and the auditors, in relation to the �nancial statements.

Select suitable accounting policies and apply them consistently;

Make judgments and estimates that are reasonable and prudent;

State whether applicable accounting standards have been followed, subject to any material departures disclosed and explained in the �nancial statements; and

Prepare the �nancial statements on the going concern basis unless it is inappropriate to presume that the company will continue in business.

uniCredit 2015 Annual Report | 13

Independent Auditors’ Report tothe Members of uniCredit Ghana Limited

Report on the Financial StatementsWe have audited the accompanying �nancial statements of uniCredit Ghana Limited on pages 11 to 52 which comprise the statement of �nancial position as at 31 December, 2015, income statement, statement of changes in equity and statement of cash �ows for the year then ended, together with the summary of signi�cant accounting policies and other explanatory notes, and have obtained all information and explanations which, to the best of our knowledge and belief, were necessary for the purposes of our audit.

Directors’ Responsibility for the Financial StatementsThe Directors are responsible for the preparation and fair presentation of these �nancial statements in accordance with International Financial Reporting Standards and the Companies Code, 1963 (Act 179). This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of �nancial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s ResponsibilityOur responsibility is to express an opinion on these �nancial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance as to whether the �nancial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the �nancial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the �nancial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the �nancial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the e�ectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the �nancial statements.

We believe that the audit evidence we have obtained is su�cient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the company has kept proper accounting records and the �nancial statements are in agreement with the records in all material respects and given in the prescribed manner, information required by the Companies Act, 1963 (Act 179), and the Banking Act, 2004 (Act 673), as amended by the Banking (Amendment) Act, 2007 (Act 738). The �nancial statements is fairly presented in all material respect of the �nancial position of the company as at 31 December 2015, and of its �nancial performance, cash �ows for the year then ended and are drawn up in accordance with the International Financial Reporting Standards (IFRS).

14 | uniCredit 2015 Annual Report

Independent Auditors’ Report tothe Members of uniCredit Ghana Limited

Report on Other Legal and Regulatory Requirements

The Companies Code, 1963 (Act 179) requires that in carrying out our audit we consider and report on the following matters. We con�rm that:

We have obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purposes of our audit;

In our opinion proper books of account have been kept by the company, so far as appears from our examination of those books; and

The balance sheet (statement of �nancial position), the pro�t and loss (statement of pro�t or loss and other comprehensive income) of the company are in agreement with the books of account.

i.

ii.

iii.

the accounts give a true and fair view of the state of a�airs of the �nancial institution;

we were able to obtain all the information and explanation required for the e�cient performance of our duties; and

the �nancial institution’s transactions were within its authorised powers.

Deloitte & ToucheLicence No. ICA/F/2015/129Chartered AccountantsAccra, GhanaFelix Nana SackeyPractising Certi�cate: Licence No. ICAG/P/1131

29th April, 2016

i.

ii.

iii.

The Non-Bank Financial Institutions Act, 2008 Act 774), Section 23 and the Banking Act, 2004 (Act 673), Section 78 (2) requires that we state certain matters in our report. We hereby state that:

uniCredit 2015 Annual Report | 15

2015 2014Notes GH¢

GH¢

Interest income 5 76,870,619 58,197,981

Interest expense 6 (32,421,243 ) (23,969,888)

Net interest income 44,449,376 34,228,093

Fees and commission income 7 5,101,642 502,566

Other operation income 8 57,157 830

Operating income 49,608,175 34,731,489

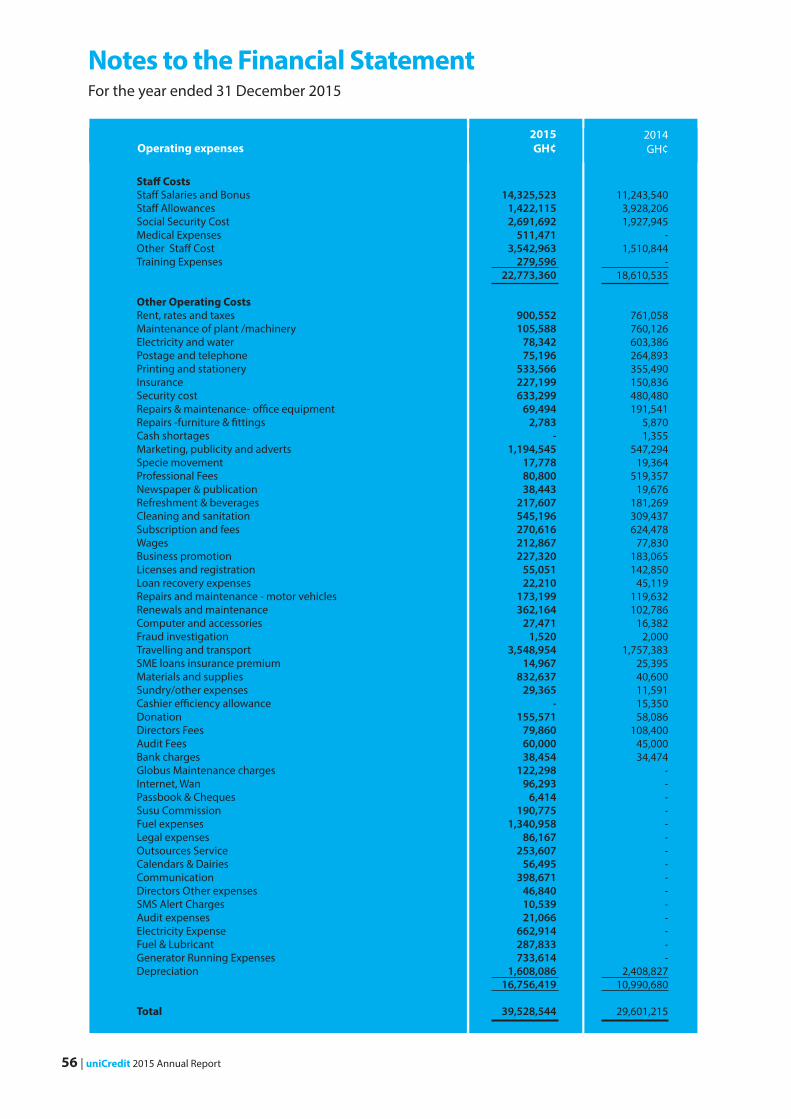

Operating expenses 9 (39,528,544) (29,601,215)

Operating Pro�t before charge for creditimpairment loss 10,079,631 5,130,274

Credit impairment loss 11 (610,971) (867,744)

Pro�t before taxation 9,468,660 4,262,530

Taxation 12 a (754,326) (833,091)

National �scal stabilisation levy 12d (473,433) (213,127)

Pro�t for the year 8,240,901 3,216,312

Other comprehensive income -

-

Total comprehensive income 8,240,901 3,216,312

The accompanying notes form an integral part of these �nancial statements.

Statement of Pro�t or Lossand Other Comprehensive IncomeFor the year ended 31 December 2015

16 | uniCredit 2015 Annual Report

Cash & Bank balances

Held-to maturity �nancial assets

Loans & advances to customers

Other assets

Property, plant and Equipment

Intangible assets

Current tax asset

Total assets

Liabilities

Customer deposits

Other liabilities

Current tax liability

National �scal stabilisation levy

Deferred tax liability

Total liabilities

Stated Capital

Capital Surplus

Statutory Reserve Funds

Regulatory Credit Risk Reserve

Income Surplus

Total shareholders' funds

Total liabilities and shareholders' funds

13

14

15

16

17

18

12c

19

20

12c

12d

12e

21

22

23

24

25

25,300,195

139,857,355

101,597,730

35,302,818

24,851,581

1,232,105

264,333

328,406,117

243,261,892

13,560,998

-

282,459

367,024

257,472,372

49,861,981

5,309,447

6,985,067

2,309,217

6,468,034

70,933,745

328,406,117

7,906,362

73,488,390

86,734,842

21,426,995

14,114,750

986

-

203,672,325

162,630,365

9,623,056

12,853

109,755

974,452

173,350,481

17,490,981

5,309,447

2,864,616

881,815

3,774,985

30,321,844

203,672,325

Chairman

Date: 21 / 04/ 2016

Director

Date: 21 / 04/ 2016

The accompanying notes form an integral part of these �nancial statements.

2015 GH¢

2014 GH¢NotesAsset

For the year ended 31 December 2015

Statement of Financial Position

uniCredit 2015 Annual Report | 17

Bala

nce

at J

anua

ry 1

Reta

ined

Pro

�t fo

r the

yea

r

Tran

sact

ion

with

Ow

ners

Add

ition

al C

apita

l Int

rodu

ced

Tran

sfer

s w

ithin

Equ

ityTr

ansf

er to

Sta

tuto

ry R

eser

ve F

und

Tran

sfer

to /(

from

) Reg

ulat

ory

cred

it ris

k re

serv

eBa

lanc

e at

Dec

embe

r 31

17,4

90,9

81-

32,3

71,0

00

-

-49

,861

,981

5,30

9,44

7 - - -

-5,

309,

447

2,86

4,61

6 - -

4,12

0,45

1

-6,

985,

067

881,

815 - - -

1,42

7,40

22,

309,

217

3,77

4,98

58,

240,

901 -

(4,1

20,4

51)

(1,4

27,4

02)

6,46

8,03

4

30,3

21,8

448,

240,

901

32,3

71,0

00

-

-70

,933

,745

Stat

edCa

pita

lG

H¢

2015

Capi

tal

Surp

lus

GH

¢

Stat

utor

y Re

serv

esG

H¢

Cred

it R

isk

Rese

rve

GH

¢

Inco

me

Surp

lus

GH

¢To

tal

GH

¢

Bala

nce

as a

t 1 Ja

nuar

y Pr

o�t f

or th

e ye

arTr

ansa

ctio

ns w

ith o

wne

rsAd

ditio

nal C

apita

l Int

rodu

ced

Tran

sfer

s w

ithin

equ

ityTr

ansf

er to

Sta

tuto

ry R

eser

ve F

und

Tran

sfer

to/(

from

) Reg

ulat

ory

cred

it ris

k re

serv

eBa

lanc

e as

at 3

1 D

ecem

ber

8,79

0,98

1 -

8,70

0,00

0

-

17,4

90,9

81

5,30

9,44

7 - -

-

5,30

9,44

7

1,25

6,46

0 - -

1,60

8,15

6

-2,

864,

616

875,

066 - -

6,

749

881,

815

2,17

3,57

83,

216,

312 -

(1,6

08,1

56)

(

6,74

9)3,

774,

985

18,4

05,5

323,

216,

312

8,70

0,00

0 -

-

30,3

21,8

44

Stat

edCa

pita

lG

H¢

2014

Capi

tal

Surp

lus

GH

¢

Stat

utor

y Re

serv

esG

H¢

Cred

it R

isk

Rese

rve

GH

¢

Inco

me

Surp

lus

GH

¢To

tal

GH

¢

For t

he y

ear e

nded

31

Dec

embe

r 201

5

Stat

emen

t of C

hang

es in

Equ

ity

uniC

redi

t 201

5 A

nnua

l Rep

ort |

18

Pro�t before tax

Adjustment for:

Depreciation and amortisation

Charge for Credit Impairment

Interest in Suspense

Pro�t on Disposal of Fixed Assets

Operating Pro�t Before Working Capital Changes

Changes in held-to-maturity �nancial assets

Change in advances

Change in other assets

Change in other investments

Change in Customer Deposits

Change in creditors and accruals

Cash from operating activities

Tax Paid

Net Cash from operating activities

Cash �ows from investing activities

Purchase of Property, Plant & Equipment

Purchase of intangible assets

Proceeds from sale of Property & Equipment

Net Cash used in Investing Activities

Cash �ows from �nancing activities

Changes in borrowings

Increase Stated Capital

Net Cash from Financing Activities

Net Increase in cash and cash equivalents

Cash & cash equivalents at beginning of year

Cash & cash equivalents at end of period

Cash and cash equivalent

Cash in hand

Bank balance

9,468,660

1,608,086

610,971

7,299,843

(57,157)

18,930,403

(66,368,965)

(22,773,702)

(13,875,823)

-

80,631,527

3,937,942

481,382

(1,939,669)

(1,458,287)

(12,496,954)

(1,407,682)

385,756

(13,518,880)

-

32,371,000

32,371,000

17,393,833

7,906,362

25,300,195

8,594,621

16,705,574

25,300,195

4,262,530

2,408,827

867,744

(54,438)

(830)

7,483,833

(33,620,174)

(5,444,730)

(7,519,044)

2,468,495

39,429,630

626,769

3,424,779

(1,181,966)

2,242,813

(3,780,777)

-

1,606

(3,779,171)

(5,000,000)

8,700,000

3,700,000

2,163,642

5,742,720

7,906,362

4,823,262

3,083,100

7,906,362

2015 GH¢

2014 GH¢Cash �ows from operating activities

Statement of Cash FlowsFor the year ended 31 December 2015

uniCredit 2015 Annual Report | 19

Reporting EntityuniCredit Ghana Limited was incorporated as a limited liability company and domiciled in Ghana under the Company’s Act of 1963 (Act 179) in 1995. It was granted a license to operate as a �nancial institution in 1984 in accordance with the Banking Law of 1989 (PNDC Law 225).

uniCredit Ghana Limited is a non-bank �nancial institution which has been in operation since 1995. The Institution was formerly called Kantamanto Savings and Loans Co. Ltd, but had a change of name in June 2007. The ownership of the Institution changed in April 2005. The Institution is headquartered at No. 3 North Ridge Lane, North Ridge,Accra.

The primary focus of uniCredit is to provide �nancial services that are speci�cally tailored to the needs of personal customers and micro, small and medium scale enterprises.

Summary of Signi�cant Accounting PoliciesThe signi�cant accounting policies adopted by uniCredit Ghana Limited under the International Financial Reporting Standards (IFRSs) are set out below:

Statement of ComplianceThe �nancial statements of the Institution have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

Basis of PreparationThe �nancial statements have been prepared on a historical cost basis, except for the following material items in the statement of �nancial position:

Functional and Presentation CurrencyThese �nancial statements are presented in Ghana cedi, which is the Institution’s functional currency. Except as otherwise indicated, �nancial information presented in Ghana cedi has been rounded to the nearest one Ghana cedi.

Preparation of the Financial StatementsThe preparation of �nancial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Company’s accounting policies. Changes in assumptions may have a signi�cant impact on the �nancial statements in the period the assumptions changed. Management believes that the underlying assumptions are appropriate. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are signi�cant to the �nancial statements are disclosed in Note 4.

Income and Statement of Cash FlowsThe Company has elected to present a single statement of pro�t or loss and other comprehensive income and presents its expenses by function of expense method.

The Company reports cash �ows from operating activities using the indirect method. Interest received is presented within investing cash �ows; interest paid is presented within operating cash �ows.

assets and liabilities held for trading are measured at fair value;

�nancial instruments designated at fair value through pro�t or loss are measured at fair value;

investments in equity instruments are measured at fair value;

other �nancial assets not held in a business model whose objective is to hold assets to collect contractual cash �ows or whose contractual terms do not give rise solely to payments of principal and interest are measured at fair value; and

available-for-sale �nancial assets are measured at fair value.

1.

2.

2.1

2.2

uniCredit 2015 Annual Report | 21

For the year ended 31 December 2015

Notes to the Financial Statement

Revenue RecognitionRevenue is recognised to the extent that it is probable that the economic bene�ts will �ow to the Institution and the revenue can be reliably measured, regardless of when the payment is being made. Revenue is measured at the fair value of the consideration received or receivable, taking into account contractually de�ned terms of payment and excluding taxes or duty. The Institution assesses its revenue arrangements against speci�c criteria in order to determine if it is acting as principal or agent. The Institution has concluded that it is acting as a principal in all of its revenue arrangements. The following speci�c recognition criteria must also be met before revenue is recognised:

Our revenues are primarily derived from the following sources: (1) interest income on loans issued to clients; (2) commission and fees on providing �nancial advisory services: and (3) other revenues which are ancillary to our operations. Generally, revenues are recognised when the services have been rendered. The following is a description of the composition of our revenues: InterestInterest income and expense are recognised in pro�t or loss using the e�ective interest method. The e�ective interest rate is the rate that exactly discounts the estimated future cash payments and receipts through the expected life of the �nancial asset or liability (or, where appropriate, a shorter period) to the carrying amount of the �nancial asset or liability. When calculating the e�ective interest rate, the Institution estimates future cash �ows considering all contractual terms of the �nancial instrument, but not future credit losses.

The calculation of the e�ective interest rate includes all transaction costs and fees and points paid or received that are an integral part of the e�ective interest rate. Transaction costs include incremental costs that are directly attributable to the acquisition or issue of a �nancial asset or liability.Interest income and expense presented in the statement of comprehensive income include:

Interest income and expense on all trading assets and liabilities are considered to be incidental to the Group’s trading operations and are presented together with all other changes in the fair value of trading assets and liabilities in net trading income.

Commission and Fees Fees and commission income and expense that are integral to the e�ective interest rate on a �nancial asset or liability are included in the measurement of the e�ective interest rate. Other fees and commission income, including account servicing fees, investment management fees, sales commission, placement fees and syndication fees, are recognised as the related services are performed. When a loan commitment is not expected to result in the draw-down of a loan, the related loan commitment fees are recognised on a straight-line basis over the commitment period. Other fees and commission expense relate mainly to transaction and service fees, which are expensed as the services are received.

Net Trading Income Net trading income comprises gains less losses related to trading assets and liabilities, and includes all realised and unrealised fair value changes, interest, dividends and foreign exchange di�erences.

2.3

interest on �nancial assets and �nancial liabilities measured at amortised cost calculated on an e�ective interest basis;

the e�ective portion of fair value changes in qualifying hedging derivatives designated in cash �ow hedges of variability in interest cash �ows, in the same period that the hedged cash �ows a�ect interest income/expense;

the ine�ective portion of fair value changes in qualifying hedging derivatives designated in cash �ow hedges of interest rate risk; and

fair value changes in qualifying derivatives, including hedge ine�ectiveness, and related

For the year ended 31 December 2015

Notes to the Financial Statement

The principal accounting policies are set out below:

22 | uniCredit 2015 Annual Report

Net Income from Other Financial Instruments at Fair Value through Pro�t or LossNet income from other �nancial instruments at fair value through pro�t or loss relates to non-trading derivatives held for risk management purposes that do not form part of qualifying hedge relationships, �nancial assets mandatorily measured at fair value through pro�t or loss other than those held for trading, and �nancial assets and liabilities designated at fair value through pro�t or loss. It includes all realised and unrealised fair value changes, interest, dividends and foreign exchange di�erences.

DividendsRevenue is recognised when the Institution’s right to receive the payment is established.

Taxes

Current Income TaxCurrent income tax assets and liabilities for the current period are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount those that are enacted or substantively enacted, at the reporting date in the countries where the Institution operates and generates taxable income.

Current income tax relating to items recognised directly in equity is recognised in equity and not in the statement of pro�t or loss. Management periodically evaluates positions taken in the tax returns with respect to situations in which applicable tax regulations are subject to interpretation and establishes provisions where appropriate.

Deferred TaxDeferred tax is provided using the liability method on temporary di�erences at the reporting date between the tax bases of assets and liabilities and their carrying amounts for �nancial reporting purposes. Deferred tax liabilities are recognised for all taxable temporary di�erences, except:

Deferred tax assets are recognised for all deductible temporary di�erences, carry forward of unused tax credits and unused tax losses, to the extent that it is probable that taxable pro�t will be available against which the deductible temporary di�erences, and the carry forward of unused tax credits and unused tax losses can be utilised, except:

The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that su�cient taxable pro�t will be available to allow all or part of the deferred tax asset to be utilised. Unrecognised deferred tax assets are reassessed at each reporting date and are recognised to the extent that it has become probable that future taxable pro�ts will allow the deferred tax asset to be recovered. Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the year when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the reporting date.

2.4

Where the deferred tax liability arises from the initial recognition of goodwill or of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, a�ects neither the accounting pro�t nor taxable pro�t or loss.

In respect of taxable temporary di�erences associated with investments in subsidiaries, associates and interests in joint ventures, where the timing of the reversal of the temporary di�erences can be controlled and it is probable that the temporary di�erences will not reverse in the foreseeable future.

Where the deferred tax asset relating to the deductible temporary di�erence arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, a�ects neither the accounting pro�t nor taxable pro�t or loss.

In respect of deductible temporary di�erences associated with investments in subsidiaries, associates and interests in joint ventures, deferred tax assets are recognised only to the extent that it is probable that the temporary di�erences will reverse in the foreseeable future and taxable pro�t will be available against which the temporary di�erences can be utilised.

For the year ended 31 December 2015

Notes to the Financial Statement

uniCredit 2015 Annual Report | 23

Deferred tax relating to items recognised outside pro�t or loss is recognised outside pro�t or loss. Deferred tax items are recognised in correlation to the underlying transaction either in other comprehensive income or directly in equity.

Deferred tax assets and deferred tax liabilities are o�set if a legally enforceable right exists to set o� current tax assets against current income tax liabilities and the deferred taxes relate to the same taxable entity and the same taxation authority. Tax bene�ts acquired as part of a business combination, but not satisfying the criteria for separate recognition at that date, would be recognised subsequently if new information about facts and circumstances changed. The adjustment would either be treated as a reduction to goodwill (as long as it does not exceed goodwill) if it is incurred during the measurement period or in pro�t or loss.

Value Added Tax and National Health Insurance Levy (Vat & Nhil)Revenues, expenses and assets are recognised net of the amount of VAT & NHIL, except:

Non-current Assets Held For Sale and Discontinued OperationsNon-current assets and disposal Companies classi�ed as held for sale are measured at the lower of their carrying amount and fair value less costs to sell. Non-current assets and disposal Companies are classi�ed as held for sale if their carrying amounts will be recovered principally through a sale transaction rather than through continuing use. This condition is regarded as met only when the sale is highly probable and the asset or disposal Institution is available for immediate sale in its present condition. Management must be committed to the sale, which should be expected to qualify for recognition as a completed sale within one year from the date of classi�cation.

Property, plant and equipment and intangible assets once classi�ed as held for sale are not depreciated or amortised.

Property, Plant and EquipmentProperty, plant and equipment is stated at cost, net of accumulated depreciation and/or accumulated impairment losses, if any. Such cost includes the cost of replacing component parts of the property, plant and equipment and borrowing costs for long-term construction projects if the recognition criteria are met.

When signi�cant parts of property, plant and equipment are required to be replaced at intervals, the Institution derecognises the replaced part, and recognises the new part with its own associated useful life and depreciation. Likewise, when a major inspection is performed, its cost is recognised in the carrying amount of the plant and equipment as a replacement if the recognition criteria are satis�ed. All other repair and maintenance costs are recognised in the statement of pro�t or loss as incurred. The present value of the expected cost for the decommissioning of the asset after its use is included in the cost of the respective asset if the recognition criteria for a provision are met.

Land and buildings are measured at cost less accumulated depreciation on buildings and impairment losses recognised. Valuations are performed with su�cient frequency to ensure that the fair value of a revalued asset does not di�er materially from its carrying amount.

Any revaluation surplus is recognised in other comprehensive income and accumulated in equity in the asset revaluation reserve, except to the extent that it reverses a revaluation decrease of the same asset previously recognised in the statement of pro�t or loss, in which case the increase is recognised in the statement of pro�t or loss. A revaluation de�cit is recognised in the statement of pro�t or loss, except to the extent that it o�sets an existing surplus on the same asset recognised in the asset revaluation reserve.

Where the taxes and levies incurred on a purchase of assets or services are not recoverable from the taxation authority, in which case the taxes are recognised as part of the cost of acquisition of the asset or as part of the expense item as applicable.

Receivables and payables are stated with the amount of taxes and levies include the net amount of taxes and levies recoverable from, or payable to, the taxation authority is included as part of receivables or payables in the statement of �nancial position.

2.5

2.6

For the year ended 31 December 2015

Notes to the Financial Statement

24 | uniCredit 2015 Annual Report

Depreciation is calculated on a straight-line basis over the estimated useful lives of the assets as follows:

An item of property, plant and equipment and any signi�cant part initially recognised is derecognised upon disposal or when no future economic bene�ts are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the di�erence between the net disposal proceeds and the carrying amount of the asset) is included in the statement of pro�t or loss when the asset is derecognised. The assets’ residual values, useful lives and methods of depreciation are reviewed at each �nancial year end and adjusted prospectively, if appropriate.

LeasesThe determination of whether an arrangement is, or contains, a lease is based on the substance of the arrangement at the inception date, whether ful�llment of the arrangement is dependent on the use of a speci�c asset or assets or the arrangement conveys a right to use the asset, even if that right is not explicitly speci�ed in an arrangement. For arrangements entered into prior to 1 January 2011, the date of inception is deemed to be 1 January 2011 in accordance with the IFRS 1.

The Institution as a lesseeFinance leases which transfer to the Institution substantially all the risks and bene�ts incidental to ownership of the leased item, are capitalised at the commencement of the lease at the fair value of the leased property or, if lower, at the present value of the minimum lease payments. Lease payments are apportioned between �nance charges and reduction of the lease liability so as to achieve a constant rate of interest on the remaining balance of the liability. Finance charges are recognised in �nance costs in the statement of pro�t or loss. A leased asset is depreciated over the useful life of the asset. However, if there is no reasonable certainty that the Institution will obtain ownership by the end of the lease term, the asset is depreciated over the shorter of the estimated useful life of the asset and the lease term.

Operating lease payments are recognised as an operating expense in the statement of pro�t or loss on a straight-line basis over the lease term.

The Institution as a lessorLeases in which the Institution does not transfer substantially all the risks and bene�ts of ownership of the asset are classi�ed as operating leases. Initial direct costs incurred in negotiating an operating lease are added to the carrying amount of the leased asset and recognised over the lease term on the same bases as rental income. Contingent rents are recognised as revenue in the period in which they are earned.

Borrowing CostsBorrowing costs directly attributable to the acquisition, construction or production of an asset that necessarily takes a substantial period of time to get ready for its intended use or sale are capitalised as part of the cost of the respective assets. All other borrowing costs are expensed in the period they occur. Borrowing costs consist of interest and other costs that an entity incurs in connection with the borrowing of funds.

Freehold landBuildingsLeasehold premisesPlant and machineryMotor vehiclesComputersO�ce equipmentFurniture and �ttings

Nil2%

10%20%20%

33.33%20%20%

2.7

2.8

For the year ended 31 December 2015

Notes to the Financial Statement

uniCredit 2015 Annual Report | 25

2.9

2.10

2.11

i.

Investment PropertiesInvestment properties are measured initially at cost, including transaction costs. Subsequent to initial recognition, investment properties are stated at fair value, which re�ects market conditions at the reporting date. Gains or losses arising from changes in the fair values of investment properties are included in the statement of pro�t or loss in the period in which they arise. Fair values are evaluated annually by an accredited external, independent valuer, applying a valuation model recommended by the International Valuation Standards Committee. Investment properties are derecognised when either they have been disposed of or when the investment property is permanently withdrawn from use and no future economic bene�t is expected from its disposal. The di�erence between the net disposal proceeds and the carrying amount of the asset is recognised in the statement of pro�t or loss in the period of derecognition.

Transfers are made to or from investment property only when there is a change in use. For a transfer from investment property to owner-occupied property, the deemed cost for subsequent accounting is the fair value at the date of change. If owner-occupied property becomes an investment property, the Institution accounts for such property in accordance with the policy stated under property, plant and equipment up to the date of change.

Intangible AssetsIntangible assets acquired separately are measured on initial recognition at cost. The cost of intangible assets acquired in a business combination is their fair value as at the date of acquisition. Following initial recognition, intangible assets are carried at cost less accumulated amortisation and accumulated impairment losses, if any. Internally generated intangible assets, excluding capitalised development costs, are not capitalised and expenditure is re�ected in the statement of pro�t or loss in the year in which the expenditure is incurred.

The useful lives of intangible assets are assessed as either �nite or inde�nite. Intangible assets with �nite lives are amortised over their useful economic lives and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The amortisation period and the amortisation method for an intangible asset with a �nite useful life is reviewed at least at the end of each reporting period. Changes in the expected useful life or the expected pattern of consumption of future economic bene�ts embodied in the asset is accounted for by changing the amortisation period or method, as appropriate, and are treated as changes in accounting estimates. The amortisation expense on intangible assets with �nite lives is recognised in the statement of pro�t or loss in the expense category consistent with the function of the intangible assets.

Intangible assets with inde�nite useful lives are not amortised, but are tested for impairment annually, either individually or at the cash-generating unit level. The assessment of inde�nite life is reviewed annually to determine whether the inde�nite life continues to be supportable. If not, the change in useful life from inde�nite to �nite is made on a prospective basis. Gains or losses arising from derecognition of an intangible asset are measured as the di�erence between the net disposal proceeds and the carrying amount of the asset and are recognised in the statement of pro�t or loss when the asset is derecognised.

Financial Instruments —Initial Recognition and Subsequent Measurement

Financial Assets

Initial Recognition and MeasurementFinancial assets within the scope of IAS 39 are classi�ed as �nancial assets at fair value through pro�t or loss, loans and receivables, held-to-maturity investments, available-for-sale �nancial assets, or as derivatives designated as hedging instruments in an e�ective hedge, as appropriate. The Institution determines the classi�cation of its �nancial assets at initial recognition.

All �nancial assets are recognised initially at fair value plus, in the case of assets not at fair value through pro�t or loss, directly attributable transaction costs.

For the year ended 31 December 2015

Notes to the Financial Statement

26 | uniCredit 2015 Annual Report

Purchases or sales of �nancial assets that require delivery of assets within a time frame established by regulation or convention in the marketplace (regular way trades) are recognised on the trade date, i.e., the date that the Institution commits to purchase or sell the asset.

The Institution’s �nancial assets include cash and short-term deposits, trade and other receivables, loans and other receivables, quoted and unquoted �nancial instruments and derivative �nancial instruments.

Subsequent MeasurementThe subsequent measurement of �nancial assets depends on their classi�cation as follows:

Financial Assets at Fair Value through Pro�t or LossFinancial assets at fair value through pro�t or loss include �nancial assets held for trading and �nancial assets designated upon initial recognition at fair value through pro�t or loss. Financial assets are classi�ed as held for trading if they are acquired for the purpose of selling or repurchasing in the near term. This category includes derivative �nancial instruments entered into by the Institution that are not designated as hedging instruments in hedge relationships as de�ned by IAS 39. Derivatives, including separated embedded derivatives are also classi�ed as held for trading unless they are designated as e�ective hedging instruments. Financial assets at fair value through pro�t and loss are carried in the statement of �nancial position at fair value with changes in fair value recognised in �nance income or �nance costs in the statement of pro�t or loss.

The Institution has not designated any �nancial assets upon initial recognition as at fair value through pro�t or loss.

The Institution evaluates its �nancial assets held for trading, other than derivatives, to determine whether the intention to sell them in the near term is still appropriate. When the Institution is unable to trade these �nancial assets due to inactive markets and management’s intention to sell them in the foreseeable future signi�cantly changes, the Institution may elect to reclassify these �nancial assets in rare circumstances. The reclassi�cation to loans and receivables, available-for-sale or held to maturity depends on the nature of the asset. This evaluation does not a�ect any �nancial assets designated at fair value through pro�t or loss using the fair value option at designation.

Derivatives embedded in host contracts are accounted for as separate derivatives and recorded at fair value if their economic characteristics and risks are not closely related to those of the host contracts and the host contracts are not held for trading or designated at fair value though pro�t or loss. These embedded derivatives are measured at fair value with changes in fair value recognised in the statement of pro�t or loss. Reassessment only occurs if there is a change in the terms of the contract that signi�cantly modi�es the cash �ows that would otherwise be required.

Loans and ReceivablesLoans and receivables are non-derivative �nancial assets with �xed or determinable payments that are not quoted in an active market. After initial measurement, such �nancial assets are subsequently measured at amortised cost using the e�ective interest rate method (EIR), less impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is included in �nance income in the statement of pro�t or loss. The losses arising from impairment are recognised in the statement of pro�t or loss in �nance costs.

Held-to-maturity InvestmentsNon-derivative �nancial assets with �xed or determinable payments and �xed maturities are classi�ed as held-to-maturity when the Institution has the positive intention and ability to hold them to maturity. After initial measurement, held-to-maturity investments are measured at amortised cost using the e�ective interest method, less impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is included in �nance income in the statement of pro�t or loss. The losses arising from impairment are recognised in the statement of pro�t or loss in �nance costs.

For the year ended 31 December 2015

Notes to the Financial Statement

uniCredit 2015 Annual Report | 27

Available-for-sale Financial InvestmentsAvailable-for-sale �nancial investments include equity and debt securities. Equity investments classi�ed as available-for-sale are those, which are neither classi�ed as held for trading nor designated at fair value through pro�t or loss. Debt securities in this category are those which are intended to be held for an inde�nite period of time and which may be sold in response to needs for liquidity or in response to changes in the market conditions.

After initial measurement, available-for-sale �nancial investments are subsequently measured at fair value with unrealised gains or losses recognised as other comprehensive income in the available-for-sale reserve until the investment is derecognised, at which time the cumulative gain or loss is recognised in other operating income, or determined to be impaired, at which time the cumulative loss is reclassi�ed to the statement of pro�t or loss in �nance costs and removed from the available-for-sale reserve. Interest income on available-for-sale debt securities is calculated using the e�ective interest method and is recognised in pro�t or loss.

The Institution evaluates its available-for-sale �nancial assets to determine whether the ability and intention to sell them in the near term is still appropriate. When the Institution is unable to trade these �nancial assets due to inactive markets and management’s intention to do so signi�cantly changes in the foreseeable future, the Institution may elect to reclassify these �nancial assets in rare circumstances. Reclassi�cation to loans and receivables is permitted when the �nancial assets meet the de�nition of loans and receivables and the Institution has the intent and ability to hold these assets for the foreseeable future or until maturity. Reclassi�cation to the held-to-maturity category is permitted only when the entity has the ability and intention to hold the �nancial asset accordingly.

For a �nancial asset reclassi�ed out of the available-for-sale category, any previous gain or loss on that asset that has been recognised in equity is amortised to pro�t or loss over the remaining life of the investment using the EIR. Any di�erence between the new amortised cost and the expected cash �ows is also amortised over the remaining life of the asset using the EIR. If the asset is subsequently determined to be impaired, then the amount recorded in equity is reclassi�ed to the statement of pro�t or loss.

DerecognitionA �nancial asset (or, where applicable a part of a �nancial asset or part of a group of similar �nancial assets) is derecognised when:

When the Institution has transferred its rights to receive cash �ows from an asset or has entered into a pass-through arrangement, and has neither transferred nor retained substantially all of the risks and rewards of the asset nor transferred control of it, the asset is recognised to the extent of the Institution’s continuing involvement in it.

In that case, the Institution also recognises an associated liability. The transferred asset and the associated liability are measured on a basis that re�ects the rights and obligations that the Institution has retained.

Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the Institution could be required to repay.

The rights to receive cash �ows from the asset have expired.

The Institution has transferred its rights to receive cash �ows from the asset or has assumed an obligation to pay the received cash �ows in full without material delay to a third party under a ‘pass-through’ arrangement; and either (a) the Institution has transferred substantially all the risks and rewards of the asset, or (b) the Institution has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

For the year ended 31 December 2015

Notes to the Financial Statement

28 | uniCredit 2015 Annual Report

Impairment of Financial AssetsThe Institution assesses at each reporting date whether there is any objective evidence that a �nancial asset or a group of �nancial assets is impaired. A �nancial asset or a group of �nancial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event has an impact on the estimated future cash �ows of the �nancial asset or the group of �nancial assets that can be reliably estimated. Evidence of impairment may include indications that the debtors or a group of debtors is experiencing signi�cant �nancial di�culty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other �nancial reorganisation and where observable data indicate that there is a measurable decrease in the estimated future cash �ows, such as changes in arrears or economic conditions that correlate with defaults.

Financial Assets Carried at Amortised CostFor �nancial assets carried at amortised cost, the Institution �rst assesses whether objective evidence of impairment exists individually for �nancial assets that are individually signi�cant, or collectively for �nancial assets that are not individually signi�cant. If the Institution determines that no objective evidence of impairment exists for an individually assessed �nancial asset, whether signi�cant or not, it includes the asset in a group of �nancial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be, recognised are not included in a collective assessment of impairment.

If there is objective evidence that an impairment loss has been incurred, the amount of the loss is measured as the di�erence between the assets carrying amount and the present value of estimated future cash �ows (excluding future expected credit losses that have not yet been incurred). The present value of the estimated future cash �ows is discounted at the �nancial asset’s original e�ective interest rate. If a loan has a variable interest rate, the discount rate for measuring any impairment loss is the current e�ective interest rate.

The carrying amount of the asset is reduced through the use of an allowance account and the amount of the loss is recognised in the statement of pro�t or loss. Interest income continues to be accrued on the reduced carrying amount and is accrued using the rate of interest used to discount the future cash �ows for the purpose of measuring the impairment loss. The interest income is recorded as part of �nance income in the statement of pro�t or loss. Loans together with the associated allowance are written o� when there is no realistic prospect of future recovery and all collateral has been realised or has been transferred to the Institution. If, in a subsequent year, the amount of the estimated impairment loss increases or decreases because of an event occurring after the impairment was recognised, the previously recognised impairment loss is increased or reduced by adjusting the allowance account. If a future write-o� is later recovered, the recovery is credited to �nance costs in the statement of pro�t or loss.

Available-For-Sale Financial InvestmentsFor available-for-sale �nancial investments, the Institution assesses at each reporting date whether there is objective evidence that an investment or a group of investments is impaired.

In the case of equity investments classi�ed as available-for-sale, objective evidence would include a signi�cant or prolonged decline in the fair value of the investment below its cost. ‘Signi�cant’ is evaluated against the original cost of the investment and ‘prolonged’ against the period in which the fair value has been below its original cost. Where there is evidence of impairment, the cumulative loss — measured as the di�erence between the acquisition cost and the current fair value, less any impairment loss on that investment previously recognised in the statement of pro�t or loss — is removed from other comprehensive income and recognised in the statement of pro�t or loss. Impairment losses on equity investments are not reversed through the statement of pro�t or loss; increases in their fair value after impairments are recognised directly in other comprehensive income.

ii.

uniCredit 2015 Annual Report | 29

For the year ended 31 December 2015

Notes to the Financial Statement

In the case of debt instruments classi�ed as available-for-sale, impairment is assessed based on the same criteria as �nancial assets carried at amortised cost. However, the amount recorded for impairment is the cumulative loss measured as the di�erence between the amortised cost and the current fair value, less any impairment loss on that investment previously recognised in the statement of pro�t or loss.

Future interest income continues to be accrued based on the reduced carrying amount of the asset, using the rate of interest used to discount the future cash �ows for the purpose of measuring the impairment loss. The interest income is recorded as part of �nance income. If, in a subsequent year, the fair value of a debt instrument increases and the increase can be objectively related to an event occurring after the impairment loss was recognised in the statement of pro�t or loss, the impairment loss is reversed through the statement of pro�t or loss.

Financial Liabilities

Initial recognition and measurementFinancial liabilities within the scope of IAS 39 are classi�ed as �nancial liabilities at fair value through pro�t or loss, loans and borrowings, or as derivatives designated as hedging instruments in an e�ective hedge, as appropriate. The Institution determines the classi�cation of its �nancial liabilities at initial recognition.

All �nancial liabilities are recognised initially at fair value and, in the case of loans and borrowings, carried at amortised cost. This includes directly attributable transaction costs.

The Institution’s �nancial liabilities include trade and other payables, bank overdrafts, loans and borrowings, �nancial guarantee contracts, and derivative �nancial instruments.

Subsequent MeasurementThe measurement of �nancial liabilities depends on their classi�cation as follows:

Financial liabilities at fair value through pro�t or lossFinancial liabilities at fair value through pro�t or loss include �nancial liabilities held for trading and �nancial liabilities designated upon initial recognition as at fair value through pro�t or loss. Financial liabilities are classi�ed as held for trading if they are acquired for the purpose of selling in the near term. This category includes derivative �nancial instruments entered into by the Institution that are not designated as hedging instruments in hedge relationships as de�ned by IAS 39. Separated embedded derivatives are also classi�ed as held for trading unless they are designated as e�ective hedging instruments.

Gains or losses on liabilities held for trading are recognised in the statement of pro�t or loss.

The Institution has not designated any �nancial liabilities upon initial recognition as at fair value through pro�t or loss.

Loans and BorrowingsAfter initial recognition, interest bearing loans and borrowings are subsequently measured at amortised cost using the e�ective interest rate method. Gains and losses are recognised in the statement of pro�t or loss when the liabilities are derecognised as well as through the e�ective interest rate method (EIR) amortisation process.

Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is included in �nance costs in the statement of pro�t or loss.

iii.

For the year ended 31 December 2015

Notes to the Financial Statement

30 | uniCredit 2015 Annual Report

DerecognitionA �nancial liability is derecognised when the obligation under the liability is discharged or cancelled or expires.

When an existing �nancial liability is replaced by another from the same lender on substantially di�erent terms, or the terms of an existing liability are substantially modi�ed, such an exchange or modi�cation is treated as a derecognition of the original liability and the recognition of a new liability, and the di�erence in the respective carrying amounts is recognised in the statement of pro�t or loss.

O�setting of Financial InstrumentsFinancial assets and �nancial liabilities are o�set and the net amount reported in the statement of �nancial position if, and only if, there is a currently enforceable legal right to o�set the recognised amounts and there is an intention to settle on a net basis, or to realise the assets and settle the liabilities simultaneously.

Fair Value of Financial InstrumentsThe fair value of �nancial instruments that are traded in active markets at each reporting date is determined by reference to quoted market prices or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs.

For �nancial instruments not traded in an active market, the fair value is determined using appropriate valuation techniques. Such techniques may include using recent arm’s length market transactions; reference to the current fair value of another instrument that is substantially the same; a discounted cash �ow analysis or other valuation models.

InventoriesInventories are valued at the lower of cost and net realisable value.

Net realisable value is the estimated selling price in the ordinary course of business, less estimated costs of completion and the estimated costs necessary to make the sale.

Impairment of Non-�nancial AssetsThe Institution assesses at each reporting date whether there is an indication that an asset may be impaired. If any indication exists, or when annual impairment testing for an asset is required, the Institution estimates the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or cash-generating unit’s (CGU) fair value less costs to sell and its value in use and is determined for an individual asset, unless the asset does not generate cash in�ows that are largely independent of those from other assets or Institution’s of assets.

Where the carrying amount of an asset or CGU exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount. In assessing value in use, the estimated future cash �ows are discounted to their present value using a pre-tax discount rate that re�ects current market assessments of the time value of money and the risks speci�c to the asset. In determining fair value less costs to sell, recent market transactions are taken into account, if available. If no such transactions can be identi�ed, an appropriate valuation model is used. These calculations are corroborated by valuation multiples, quoted share prices for publicly traded subsidiaries or other available fair value indicators.

The Institution bases its impairment calculation on detailed budgets and forecast calculations which are prepared separately for each of the Institution’s cash-generating units to which the individual assets are allocated. These budgets and forecast calculations are generally covering a period of �ve years. For longer periods, a long term growth rate is calculated and applied to project future cash �ows after the �fth year.

Impairment losses of continuing operations, including impairment on inventories, are recognised in the statement of pro�t or loss in those expense categories consistent with the function of the impaired asset, except for a property previously revalued where the revaluation was taken to other comprehensive income. In this case, the impairment is also recognised in other comprehensive income up to the amount of any previous revaluation.

2.12

2.13

v.

iv.

For the year ended 31 December 2015

Notes to the Financial Statement

uniCredit 2015 Annual Report | 31