Embed Size (px)

Citation preview

Understanding Monetary Policy and Financial Markets

Mahmood ul Hasan KhanAdditional DirectorEconomic Policy Review DepartmentState Bank of Pakistan

Monetary Policy: Concepts, Framework and Experience

2

Monetary Policy: Concepts, Framework and Experience

Monetary Policy

� A key component of economic policy

� Central banks are responsible for the formulation and implementation of MP.

� Policy actions taken by a central bank to change the monetary conditions in an economy.

3

conditions in an economy.

� Four key characteristics

1. Goals

2. Intermediate target

3. Instruments-policy options

4. Strategy/framework

Monetary Policy Goals

� Multiple objectives

� low inflation

� Support economic growth

� Equilibrium in the balance of payments, and

4

� Interest and exchange rate stability

� Single objective

� low and steady inflation

� Dual vs. hierarchical mandate

� Country Experience

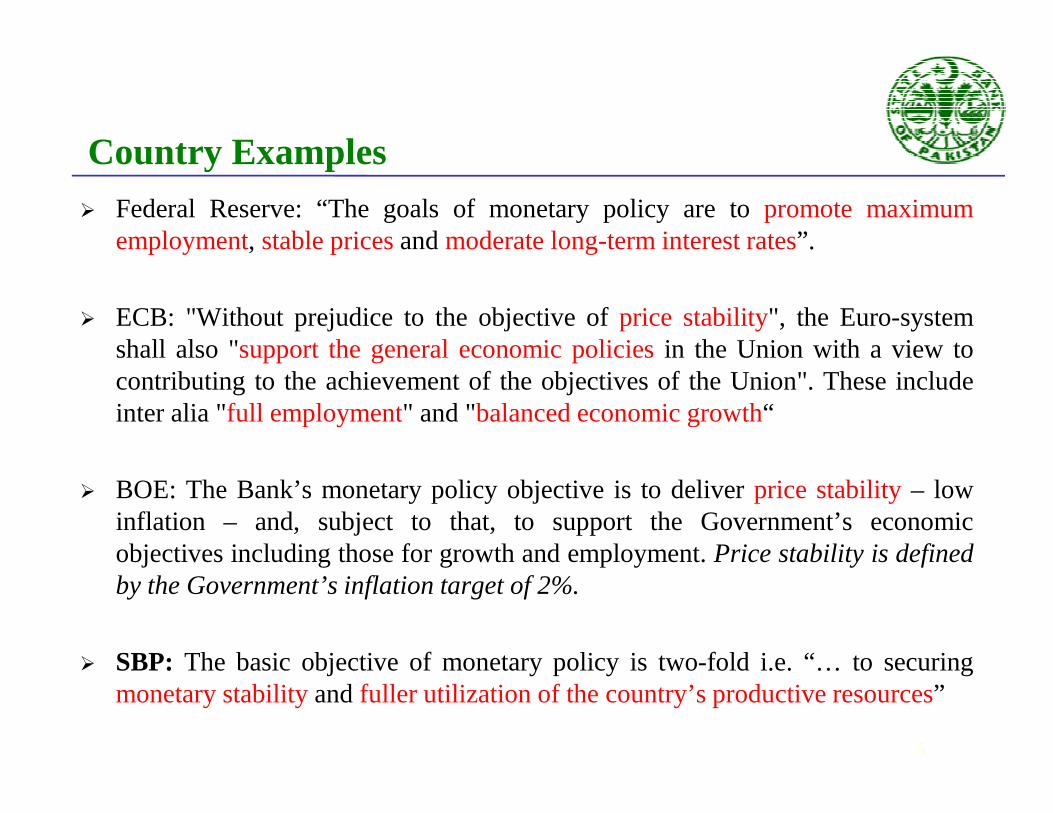

Country Examples� Federal Reserve: “The goals of monetary policy are topromote maximum

employment, stable pricesandmoderate long-term interest rates”.

� ECB: "Without prejudice to the objective ofprice stability", the Euro-systemshall also "support the general economic policiesin the Union with a view tocontributing to the achievement of the objectives of the Union". These includeinteralia "full employment" and"balancedeconomicgrowth“

5

interalia "full employment" and"balancedeconomicgrowth“

� BOE: The Bank’s monetary policy objective is to deliverprice stability– lowinflation – and, subject to that, to support the Government’s economicobjectives including those for growth and employment.Price stability is definedby the Government’s inflation target of 2%.

� SBP: The basic objective of monetary policy is two-fold i.e. “… tosecuringmonetary stabilityandfuller utilization of the country’s productive resources”

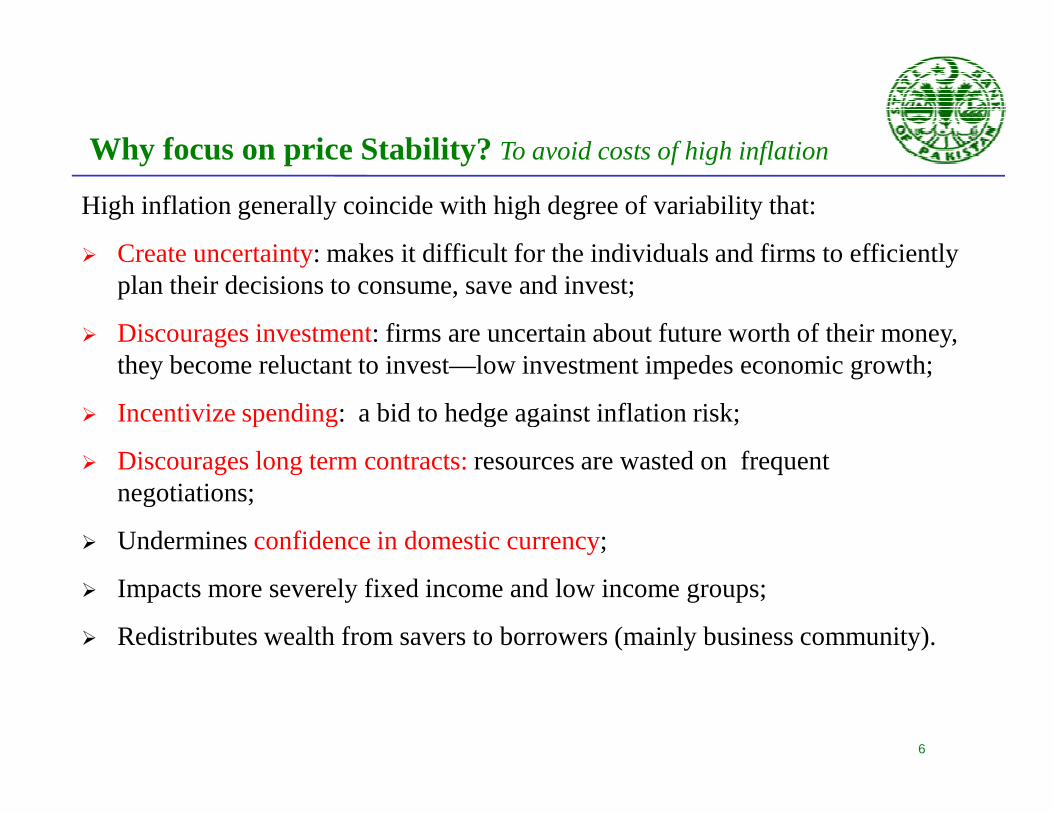

High inflation generally coincide with high degree of variability that:

� Create uncertainty: makes it difficult for the individuals and firms to efficiently plan their decisions to consume, save and invest;

� Discourages investment: firms are uncertain about future worth of their money, they become reluctant to invest—low investment impedes economic growth;

� Incentivize spending: a bid to hedge against inflation risk;

Why focus on price Stability? To avoid costs of high inflation

6

� Incentivize spending: a bid to hedge against inflation risk;

� Discourages long term contracts: resources are wasted on frequent negotiations;

� Undermines confidence in domestic currency;

� Impacts more severely fixed income and low income groups;

� Redistributes wealth from savers to borrowers (mainly business community).

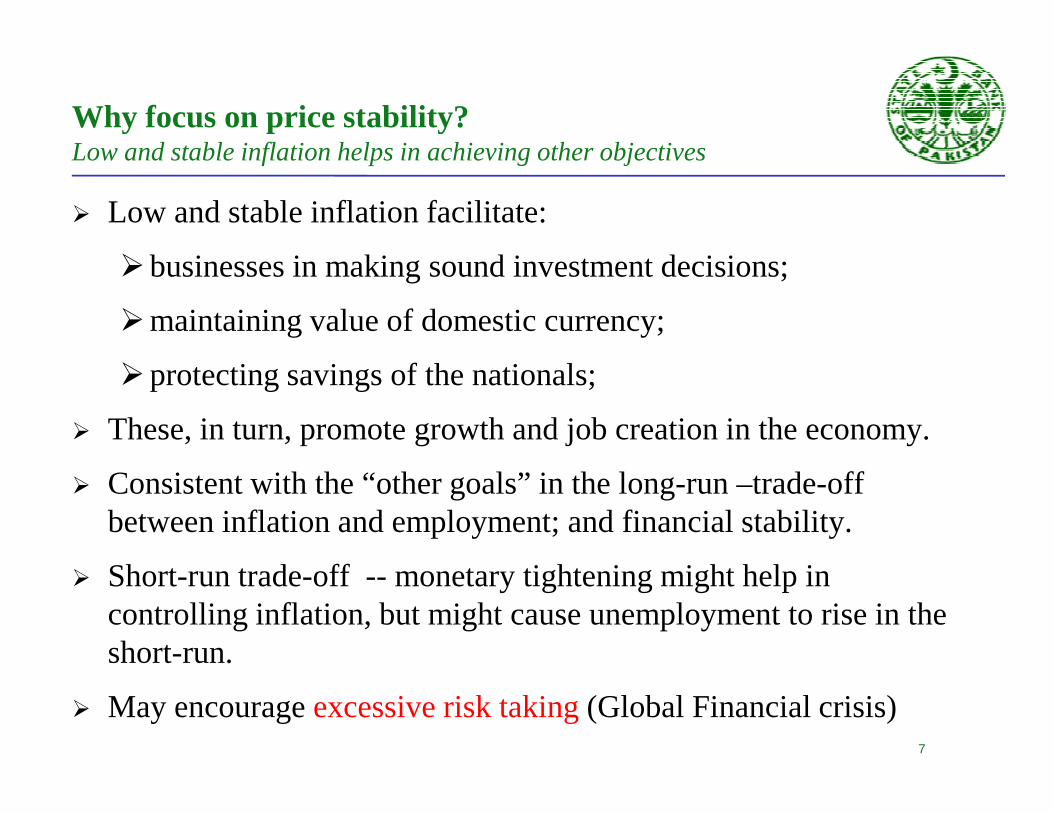

Why focus on price stability?Low and stable inflation helps in achieving other objectives

� Low and stable inflation facilitate:

�businesses in making sound investment decisions;

�maintaining value of domestic currency;

�protecting savings of the nationals;

� These, in turn, promote growth and job creation in the economy.

� Consistent with the “other goals” in the long-run –trade-off between inflation and employment; and financial stability.

� Short-run trade-off -- monetary tightening might help in controlling inflation, but might cause unemployment to rise in the short-run.

� May encourage excessive risk taking (Global Financial crisis)7

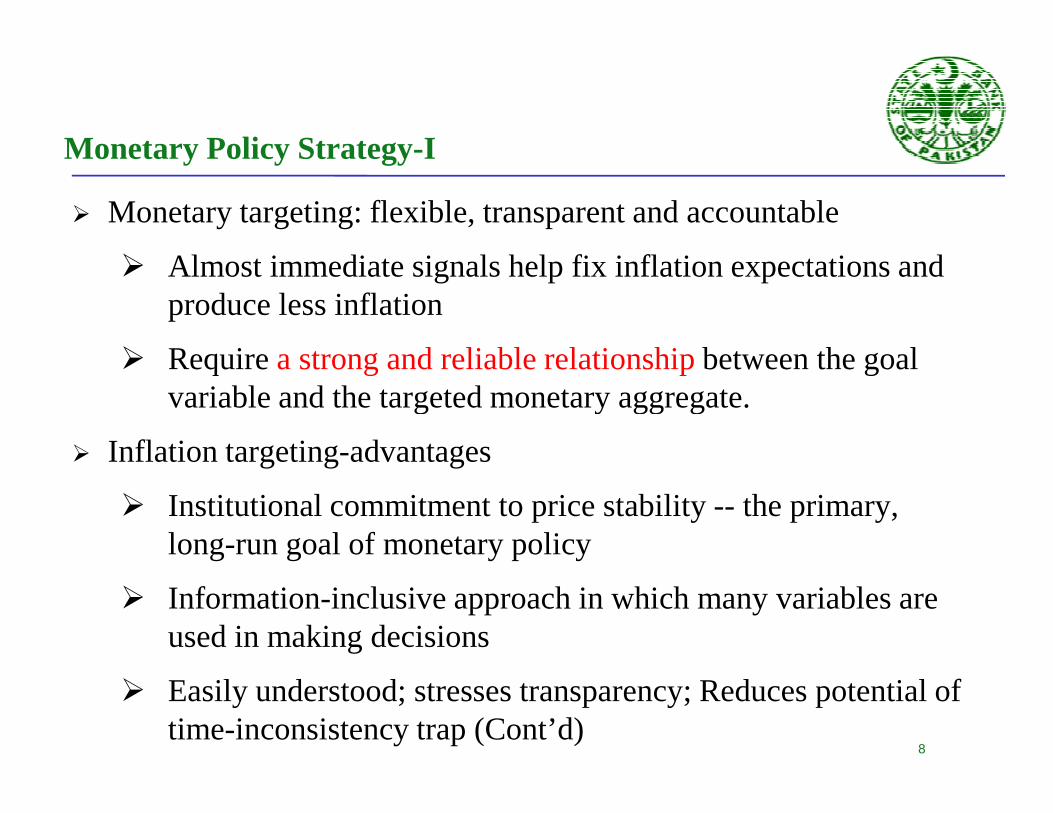

Monetary Policy Strategy-I

� Monetary targeting: flexible, transparent and accountable

� Almost immediate signals help fix inflation expectations and produce less inflation

� Require a strong and reliable relationship between the goal variable and the targeted monetary aggregate.variable and the targeted monetary aggregate.

� Inflation targeting-advantages

� Institutional commitment to price stability -- the primary, long-run goal of monetary policy

� Information-inclusive approach in which many variables are used in making decisions

� Easily understood; stresses transparency; Reduces potential of time-inconsistency trap (Cont’d)

8

Monetary Policy Strategy-II

� Inflation targeting - disadvantages

� Too much rigidity

� Potential for increased output fluctuations

� Implicit nominal anchor: Forward looking and preemptive

� Uses many sources of information

� Avoids time-inconsistency problem

� Demonstrated success

� Lack of transparency and accountability

� Strong dependence on the preferences, skills, and trustworthiness of individuals in charge

9

Tactics: Choosing Policy Instruments

� Tools /operating instruments

� Open market operations

� Reserve requirements

� Interest rates� Interest rates

� Can’t have interest-rate and aggregate targets - one or the other

� Criteria for choosing policy instrument

� Observable and Measurable

� Controllabile

� Predictable effect on Goals (MTM)

10

Market interest rate Structure

Monetary and Credit Aggregates

Asset Prices

Domestic Goods Prices

Aggregate Output

Monetary Policy Actions- Current- Expected

Aggregate Demand

Monetary transmission mechanism: a simplified view

11

Exchange Rate

Monetary Policy Objectives

Imported Goods Prices

Aggregate Prices

Key issue – Transmission lags and Uncertainty

� Stability of relationship; Data uncertainty; Model uncertainty; shocks; etc.

� Monetary management is both a science as well as an art, where a lot depends on judgment.

Monetary policy: experience of Pakistan

� Ultimate objective – Monetary stability; Soundness of the

financial system; Fuller utilization of country productive

resources

� Intermediate target – Inflation and assessment of monetary

12

Intermediate target – Inflation and assessment of monetary

aggregates.

� Operational target – money market overnight repo rate

� Indicators – yield curve/interest rate spreads, reserve money

etc.

� Instruments – policy rate, OMOs, CRR, SLR.

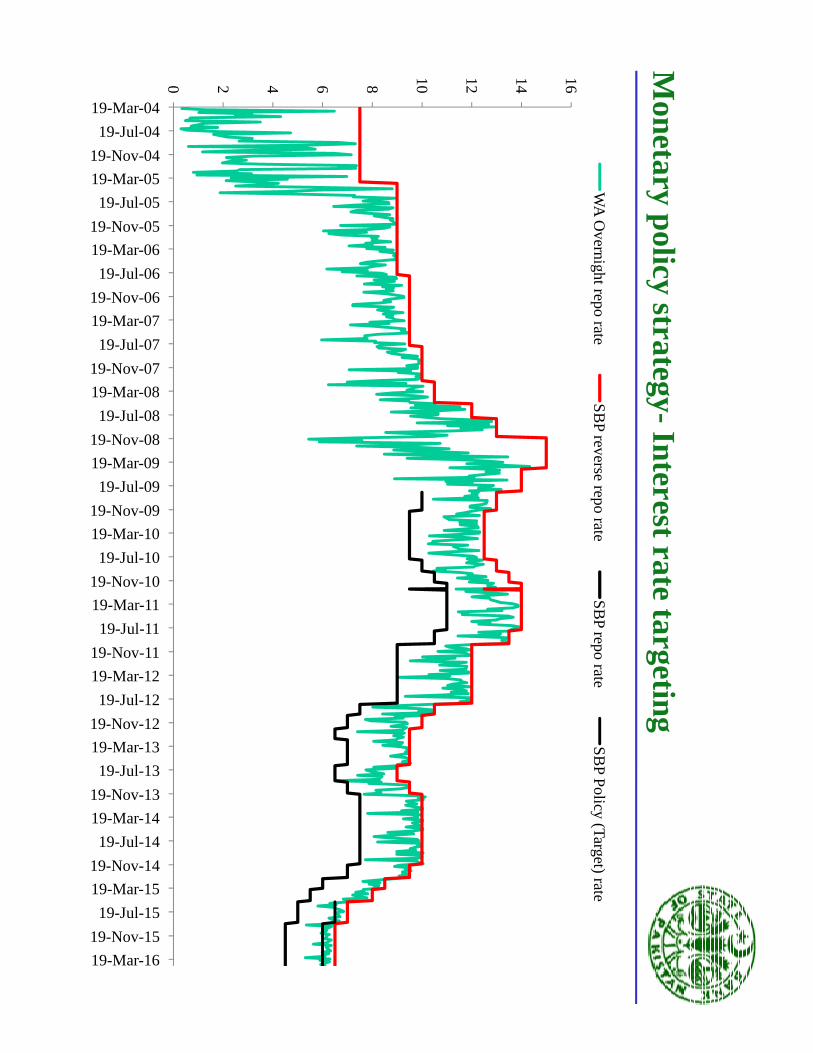

Monetary policy Instruments

In May 2015, SBP announced changes in the Monetary Policy Framework by introducing the SBP Target Rate..

Rates on standing facilities

� SBP Reverse Repo Rate (6.5 %); SBP Policy Rate (Target Rate -6.0 %); and SBP repo rate (4.5%)

13

Open Market Operations

� conducted regularly on Fridays and on need basis on other days.

Cash Reserve Ratio (CRR)

� 5% for demand liabilities (including less than 1 year time deposits);

� 5% as CRR and 15% special CRR on foreign currency deposits.

Statutory Liquidity Ratio (SLR)

� 19% for demand liabilities (including less than 1 year time deposits)

10 12 14 16

WA

Overnight repo rate

SB

P reverse repo rate

SB

P repo rate

SB

P P

olicy (Target) rate

Monetary policy strategy-Interest rate targeting

0 2 4 6 8

19-Mar-04

19-Jul-04

19-Nov-04

19-Mar-05

19-Jul-05

19-Nov-05

19-Mar-06

19-Jul-06

19-Nov-06

19-Mar-07

19-Jul-07

19-Nov-07

19-Mar-08

19-Jul-08

19-Nov-08

19-Mar-09

19-Jul-09

19-Nov-09

19-Mar-10

19-Jul-10

19-Nov-10

19-Mar-11

19-Jul-11

19-Nov-11

19-Mar-12

19-Jul-12

19-Nov-12

19-Mar-13

19-Jul-13

19-Nov-13

19-Mar-14

19-Jul-14

19-Nov-14

19-Mar-15

19-Jul-15

19-Nov-15

19-Mar-16

Monetary policy strategy

� Interest rate targeting: SBP adjusts the policy rate in the direction it deem necessary to control inflation close to its target;

� This has effects on other market interest rates, such as secondary market rates, KIBOR, that are used as benchmark for lending to businesses and households;

Decision is broadly based on the assessment of near-term � Decision is broadly based on the assessment of near-term inflation path and inflation expectations vis-à-vis announced inflation target;

� Demand pressuresin the economy: projections of key macroeconomic variables including reserve money, M2 and its major components, imports and exports, and current account balance; etc.

� Monetary Policy Committee in responsible for policy formulation

Monetary policy decision making process

� SBP’s Monetary Policy Committee responsible for the policy formulation.

� The MPC consists of Governor SBP (chairperson); three senior executives of the Bank; three members of the board; and three external members.

� At least six times a year to decide the monetary policy stance.

� Initial draft of MPS is circulated among the SBP’s senior management, to initiate Initial draft of MPS is circulated among the SBP’s senior management, to initiate debate and to get their feedback and suggestions.

� After incorporating comments, the draft MPS along with other information including Monetary Policy Information Compendium, Macroeconomic Outlook, etc. is sent to the MPC before the meeting.

� The decision is reached through consensus of the MPC.

� The decisions are announced through press conference by the Governor (in January and July) and through a press release on other four occasions.

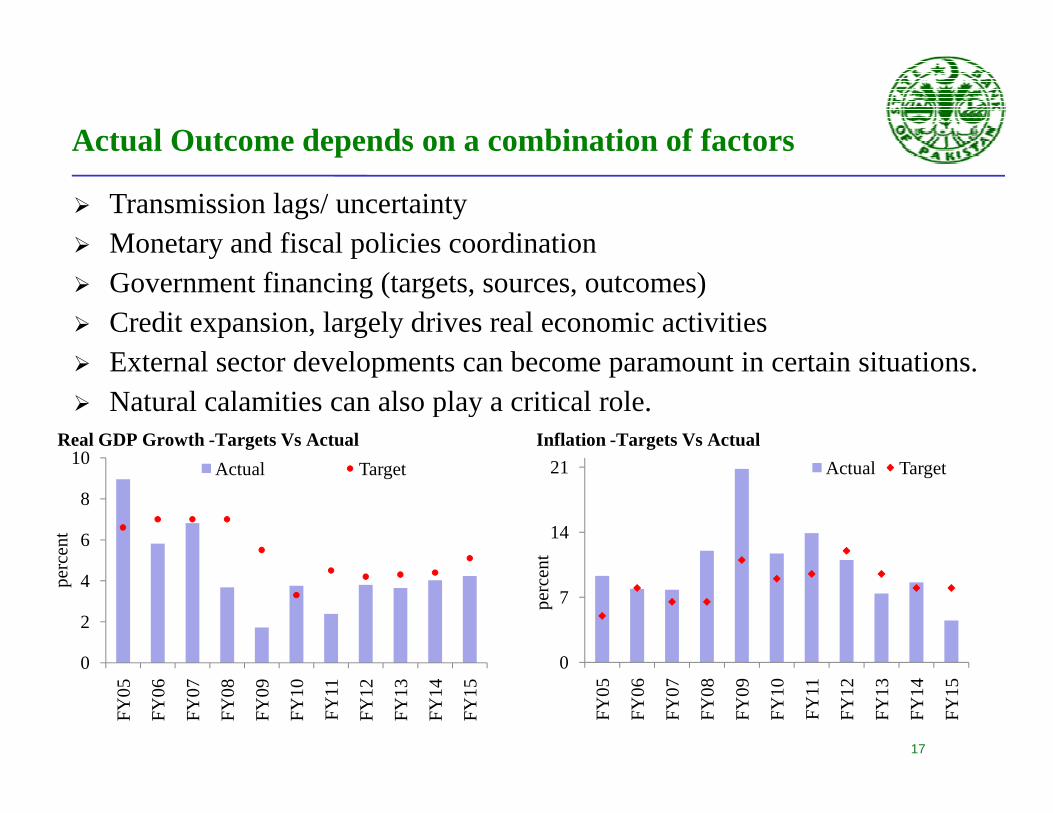

� Transmission lags/ uncertainty� Monetary and fiscal policies coordination � Government financing (targets, sources, outcomes)� Credit expansion, largely drives real economic activities� External sector developments can become paramount in certain situations.� Natural calamities can also play a critical role.

Actual Outcome depends on a combination of factors

17

0

7

14

21

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

per

cen

t

Actual Target

Inflation -Targets Vs Actual

0

2

4

6

8

10

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

per

cen

t

Actual Target

Real GDP Growth -Targets Vs Actual

� Natural calamities can also play a critical role.

Financial Markets: Fundamentals, and Experience

18

Monetary policy and Financial Markets

� Financial markets are central to monetary policy operations

� Monetary transmission depends on efficiency and structure of financial markets

� Interest rate deregulation-help in developing money markets � Interest rate deregulation-help in developing money markets and transmission thereof

� Financial liberalization- can alter transmission

Financial Instruments

Financial instruments are contracts that govern the transfer, use and repayment of funds

Two main classes of instruments:

� Money Market Instruments

� Capital Market Instruments

Money Market Instruments-I

� Money Market instruments characterized by maturities of less than 1 year

� Reissued frequently, tradable (liquid)

� Sound issuers (low credit risk)

� Used by many participants for:

� Financing operations (working capital)

� Cash and liquidity management

� Monetary policy and interest rate setting

Money Market Instruments-I

� Main instruments are issued by:

� Banks (CDs, CPs)

� Govt. (Treasury bills, repos)

� Corporate (Commercial Paper)� Corporate (Commercial Paper)

� Repurchase agreements (“repos”), a collateralized loan:

� Mostly done with govt securities

� Overnight, as well as open- and term-repos

� Key advantage: Lender obtains full ownership of security

Capital Market Instruments-I

� Longer term, more than 1 year maturity

� Three broad categories:

� Bonds� Bonds

� Equities

� Derivatives

Capital Market Instruments-Bonds

� Sometimes called fixed-income securities

� Promise a fixed stream of income, or a stream determined by formula (e.g. variable rate or indexed bonds)

� Coupons are generally semiannual and yield-to-maturity (YTM) is a good measure of returnis a good measure of return

� Government bonds usually provide a benchmark yield curve

� Corporate bonds are similar in structure, generally higher default risk (summarized by ratings ):

� Secured bonds (specific collateral)

� Unsecured bonds (debentures)

� Subordinated bonds (lower-seniority)

Capital Market Instruments- Equities

� Equities or common stocks, provide ownership in a company (with limited liability), including

� Residual claim on profits (dividends); no maturity

� Voting power (except for preferred shares)

� Mostly held for capital appreciation, and corporate control� Mostly held for capital appreciation, and corporate control

� Preferred stock has features of equities and bonds

� Promises fixed dividend

� But with discretion to postpone;

� Senior to common shares, but no vote/control

� Could be callable or convertible to common shares

Capital Market Instruments- Derivatives � Derivatives are instruments whose value depends on that of an

underlying security

� Forwards: agreement to exchange an asset at future time and given price

� Tailored according to requirement of customer

Traded OTC & Generally held to expiration� Traded OTC & Generally held to expiration

� Futures: same as forwards, except for:

� Standardized & traded in market(margins)

� Generally traded before expiration

� Swaps: agreement to exchange a series of cash flows or currency

� Options: right to buy or sell an asset at specified delivery (“strike”) price.

Financial Markets: a direct route

� Financial markets provide the direct finance route via issuance of financial instruments.

� Firms raise funds by issuing bonds or equities in the primary market

� Equity: IPO

� Bonds: public offering/private placement

� Trading of already-issued securities occurs in the secondary market

� No new funds raised

� Just a transfer of ownership/exposures (but quite relevant; liquidity)

Financial Markets by types

� Primary markets deal with all the standard problems of lending; underwriting done by investment bank

� Secondary Markets allow agents to “undo” a loan, sell asset to someone else

� Money Market� Money Market

� Capital Markets

� Debt and Equity Markets

� Foreign Exchange Markets

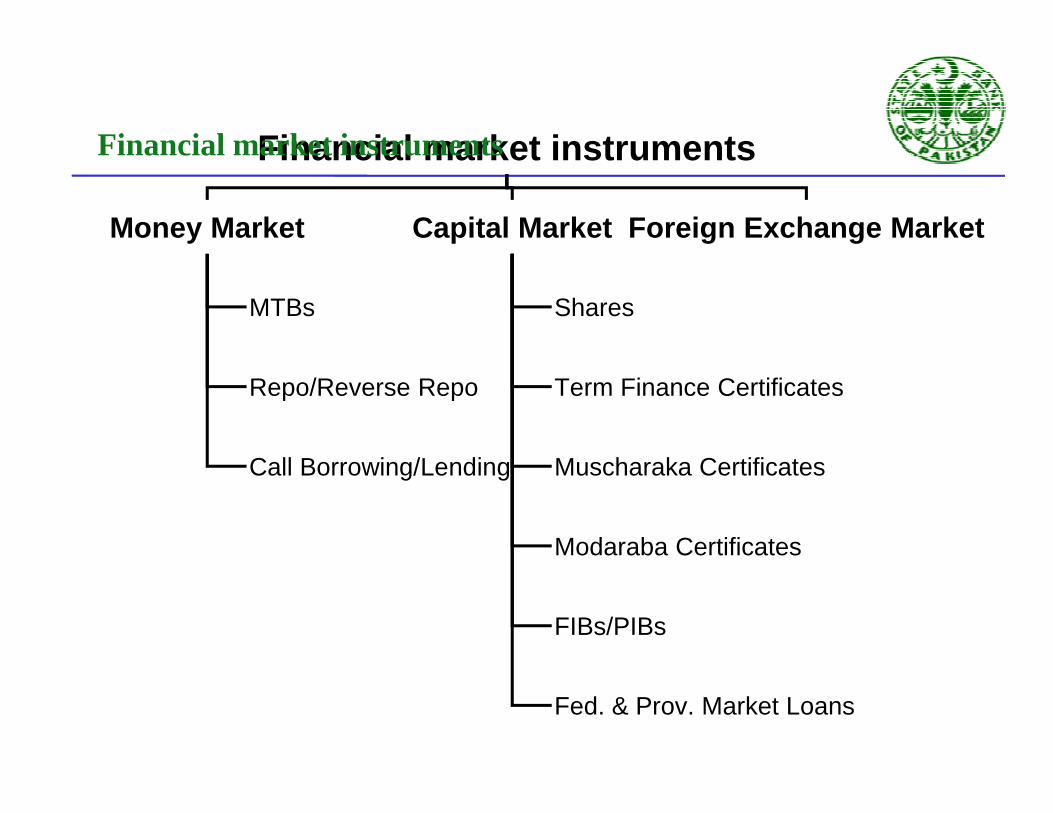

Financial market instruments

Money Market Capital Market Foreign Exchange Market

MTBs

Repo/Reverse Repo

Shares

Term Finance Certificates

Financial market instruments

Call Borrowing/Lending Muscharaka Certificates

Modaraba Certificates

FIBs/PIBs

Fed. & Prov. Market Loans

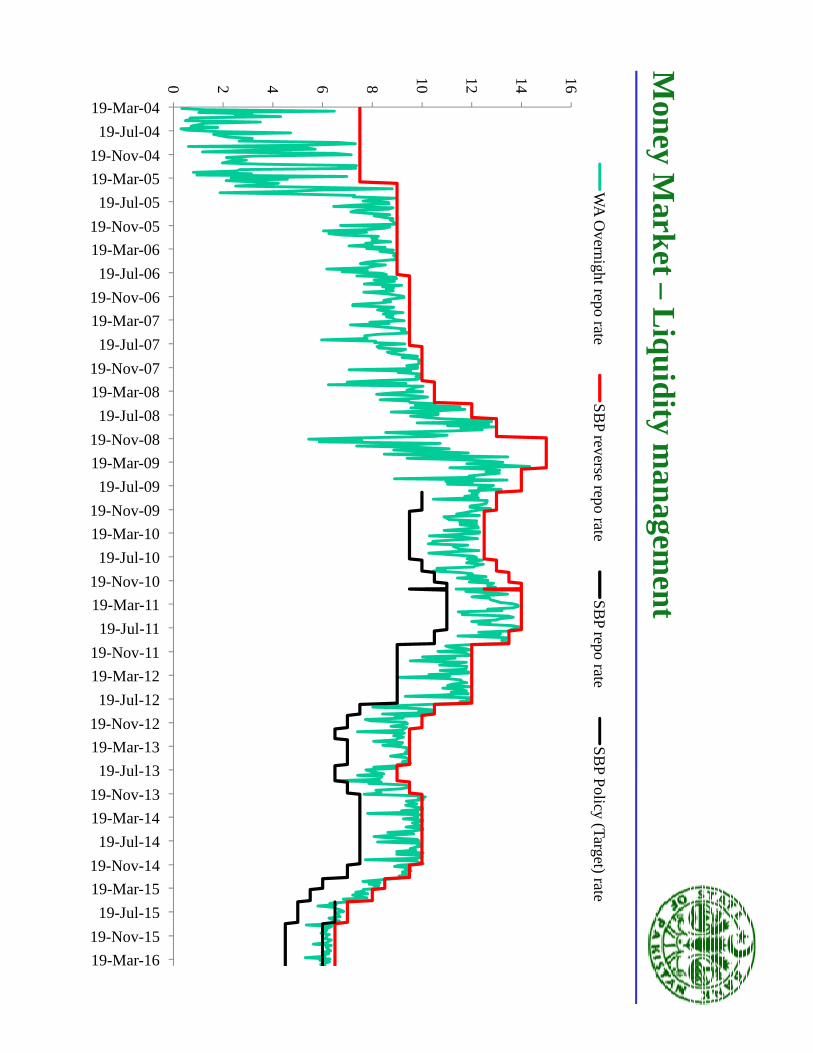

10 12 14 16

WA

Overnight repo rate

SB

P reverse repo rate

SB

P repo rate

SB

P P

olicy (Target) rate

Money M

arket –Liquidity m

anagement

0 2 4 6 8

19-Mar-04

19-Jul-04

19-Nov-04

19-Mar-05

19-Jul-05

19-Nov-05

19-Mar-06

19-Jul-06

19-Nov-06

19-Mar-07

19-Jul-07

19-Nov-07

19-Mar-08

19-Jul-08

19-Nov-08

19-Mar-09

19-Jul-09

19-Nov-09

19-Mar-10

19-Jul-10

19-Nov-10

19-Mar-11

19-Jul-11

19-Nov-11

19-Mar-12

19-Jul-12

19-Nov-12

19-Mar-13

19-Jul-13

19-Nov-13

19-Mar-14

19-Jul-14

19-Nov-14

19-Mar-15

19-Jul-15

19-Nov-15

19-Mar-16

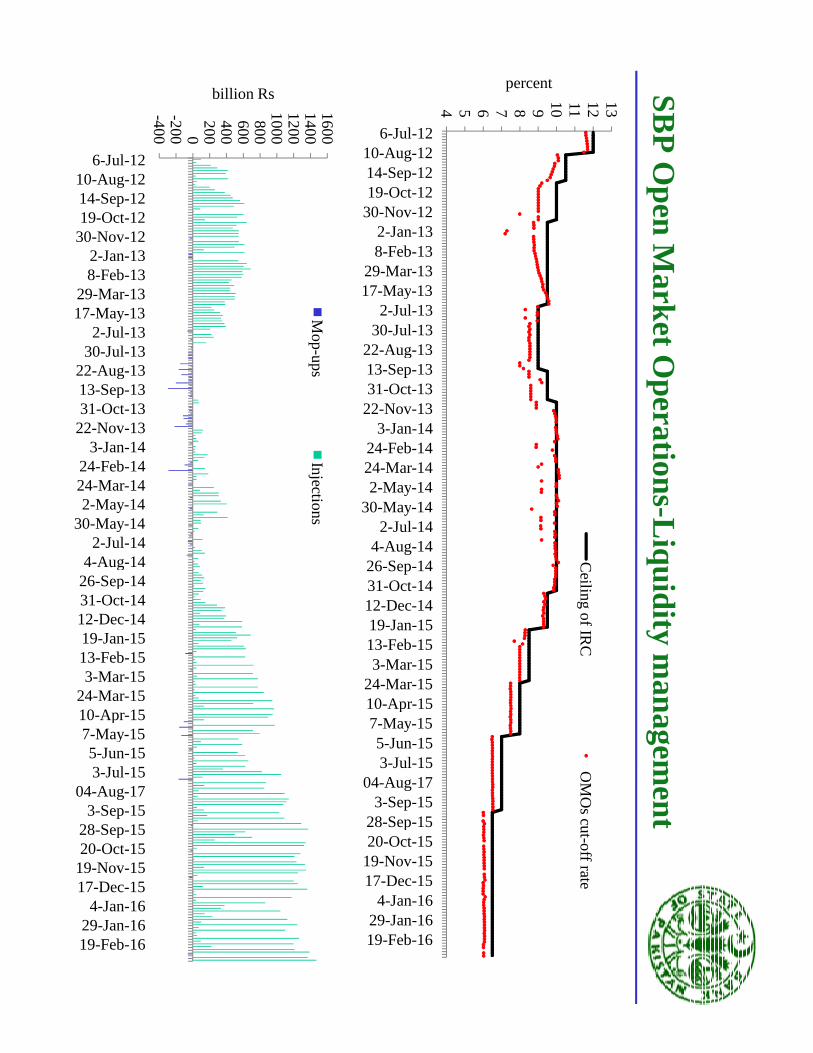

SB

P O

pen Market O

perations-Liquidity managem

ent

4 5 6 7 8 9 10 11 12 13

Jul-12Aug-12Sep-12Oct-12

Nov-12Jan-13Feb-13Mar-13May-13

Jul-13Jul-13

Aug-13Sep-13Oct-13

Nov-13Jan-14Feb-14Mar-14May-14May-14

Jul-14Aug-14Sep-14Oct-14Dec-14Jan-15Feb-15Mar-15Mar-15Apr-15

May-15Jun-15Jul-15

Aug-17Sep-15Sep-15Oct-15

Nov-15Dec-15Jan-16Jan-16Feb-16

percent

Ceiling of IR

CO

MO

s cut-off rate

6-Jul10-Aug14-Sep19-Oct

30-Nov2-Jan8-Feb

29-Mar17-May

2-Jul30-Jul

22-Aug13-Sep31-Oct

22-Nov3-Jan

24-Feb24-Mar2-May

30-May2-Jul

4-Aug26-Sep31-Oct12-Dec19-Jan13-Feb3-Mar

24-Mar10-Apr7-May5-Jun3-Jul

04-Aug3-Sep

28-Sep20-Oct

19-Nov17-Dec

4-Jan29-Jan19-Feb

-400-200 0200400600800

1000120014001600

6-Jul-1210-Aug-1214-Sep-1219-Oct-12

30-Nov-122-Jan-138-Feb-13

29-Mar-1317-May-13

2-Jul-1330-Jul-13

22-Aug-1313-Sep-1331-Oct-13

22-Nov-133-Jan-14

24-Feb-1424-Mar-142-May-14

30-May-142-Jul-14

4-Aug-1426-Sep-1431-Oct-1412-Dec-1419-Jan-1513-Feb-153-Mar-15

24-Mar-1510-Apr-157-May-155-Jun-153-Jul-15

04-Aug-173-Sep-15

28-Sep-1520-Oct-15

19-Nov-1517-Dec-15

4-Jan-1629-Jan-1619-Feb-16

billion Rs

Mop-ups

Injections

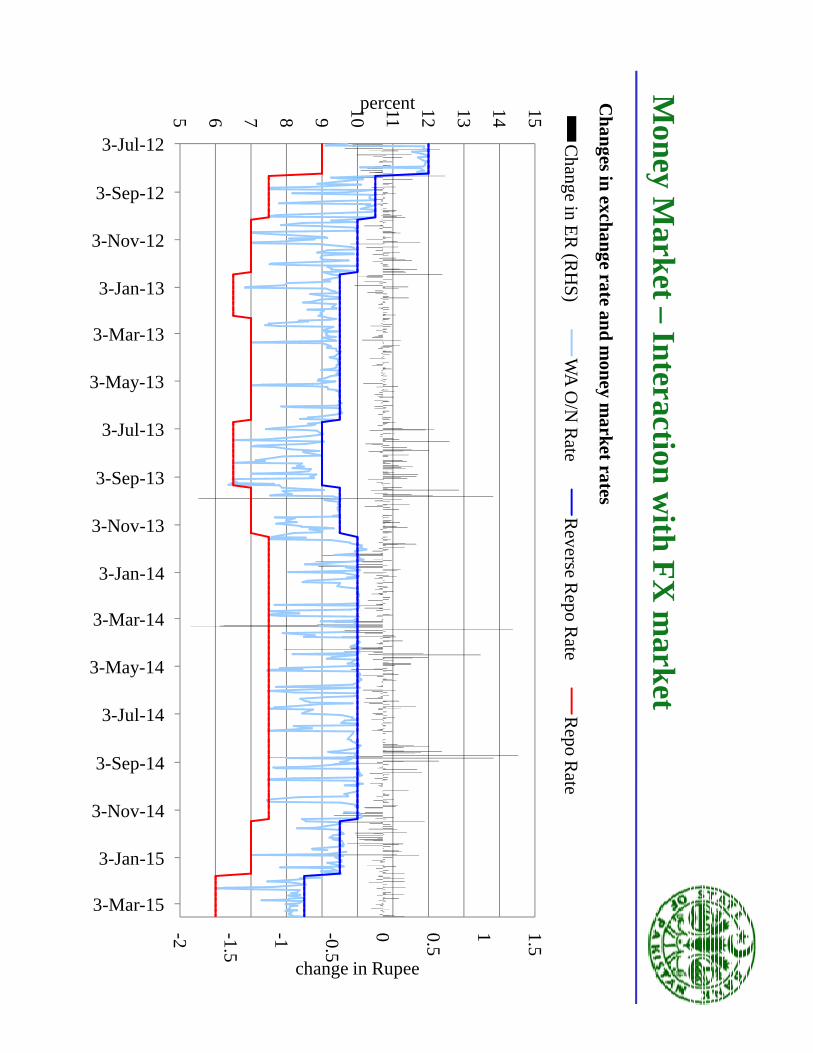

Money M

arket –Interaction w

ith FX

market

0.5

1 1.5

12

13

14

15

change in Rupee

percent

Ch

ang

e in E

R (R

HS

)W

A O

/N R

ateR

everse Rep

o R

ateR

epo

Rate

Changes in exchange rate and m

oneym

arket rates

-2 -1.5

-1 -0.5

0

5 6 7 8 9 10 11

3-Jul-12

3-Sep-12

3-Nov-12

3-Jan-13

3-Mar-13

3-May-13

3-Jul-13

3-Sep-13

3-Nov-13

3-Jan-14

3-Mar-14

3-May-14

3-Jul-14

3-Sep-14

3-Nov-14

3-Jan-15

3-Mar-15

change in Rupee

percent

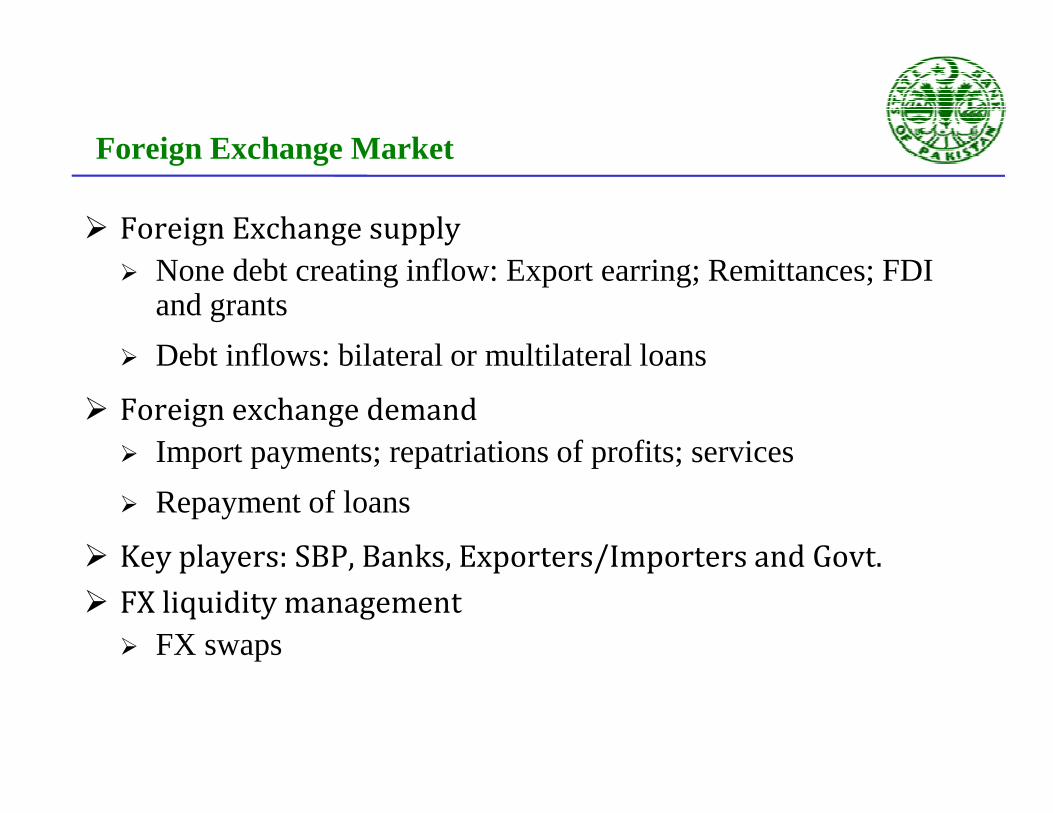

Foreign Exchange Market

� Foreign Exchange supply

� None debt creating inflow: Export earring; Remittances; FDI and grants

� Debt inflows: bilateral or multilateral loans

� Foreign exchange demand� Foreign exchange demand

� Import payments; repatriations of profits; services

� Repayment of loans

� Key players: SBP, Banks, Exporters/Importers and Govt.

� FX liquidity management

� FX swaps

Bonds Markets in Pakistan-I

� Bond market in Pakistan is fairly small

� Household investors: primarily invest in NSS

� Institutional investors: government and private bonds

� Prior to financial sector reforms of 1990s.

� No corporate bond market: not a single bond was issued by private sector;� No corporate bond market: not a single bond was issued by private sector;

� Not many companies were left after nationalization

� Private limited companies avoid any public disclosure

� Only Government bond market

� Privatization paved the way for private sector

� Prize Bonds-the most famous bond in the public

� Zero coupon, risk free instrument with lottery based returns

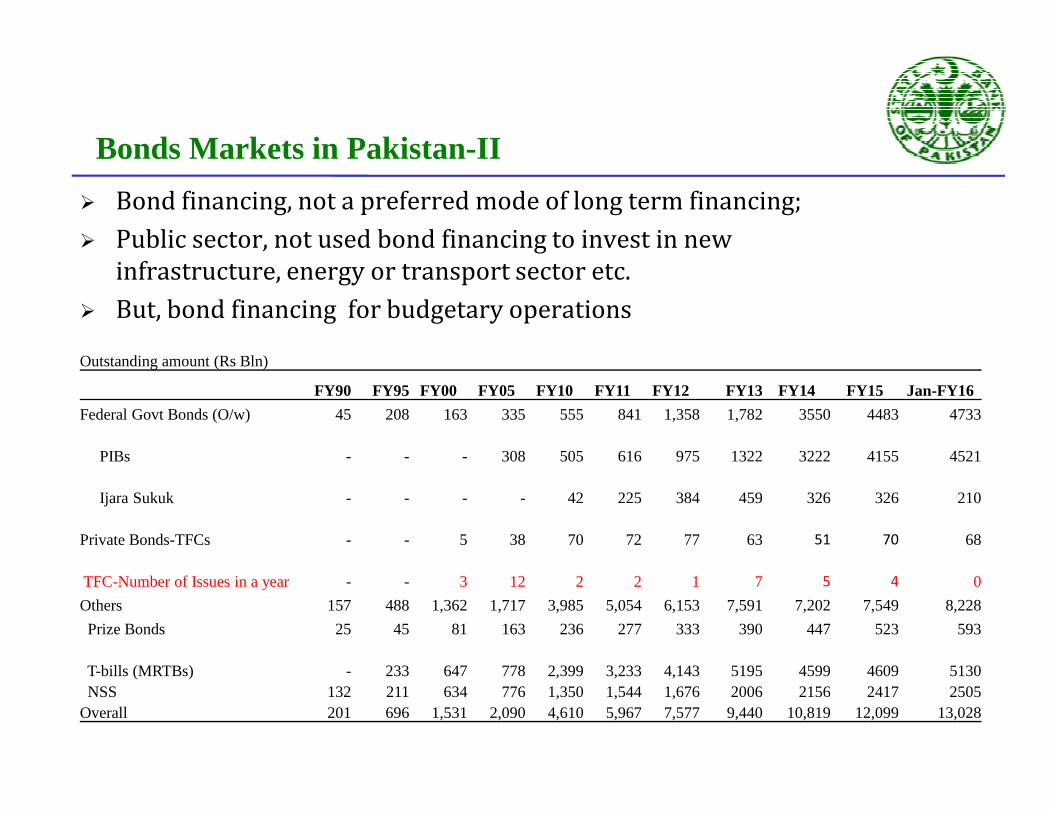

Bonds Markets in Pakistan-II

� Bond financing, not a preferred mode of long term financing;

� Public sector, not used bond financing to invest in new

infrastructure, energy or transport sector etc.

� But, bond financing for budgetary operations

Outstanding amount (Rs Bln)

FY90 FY95 FY00 FY05 FY10 FY11 FY12 FY13 FY14 FY15 Jan-FY16

Federal Govt Bonds (O/w) 45 208 163 335 555 841 1,358 1,782 3550 4483 4733Federal Govt Bonds (O/w) 45 208 163 335 555 841 1,358 1,782 3550 4483 4733

PIBs - - - 308 505 616 975 1322 3222 4155 4521

Ijara Sukuk - - - - 42 225 384 459 326 326 210

Private Bonds-TFCs - - 5 38 70 72 77 63 51 70 68

TFC-Number of Issues in a year - - 3 12 2 2 1 7 5 4 0

Others 157 488 1,362 1,717 3,985 5,054 6,153 7,591 7,202 7,549 8,228

Prize Bonds 25 45 81 163 236 277 333 390 447 523 593

T-bills (MRTBs) - 233 647 778 2,399 3,233 4,143 5195 4599 4609 5130NSS 132 211 634 776 1,350 1,544 1,676 2006 2156 2417 2505

Overall 201 696 1,531 2,090 4,610 5,967 7,577 9,440 10,819 12,099 13,028

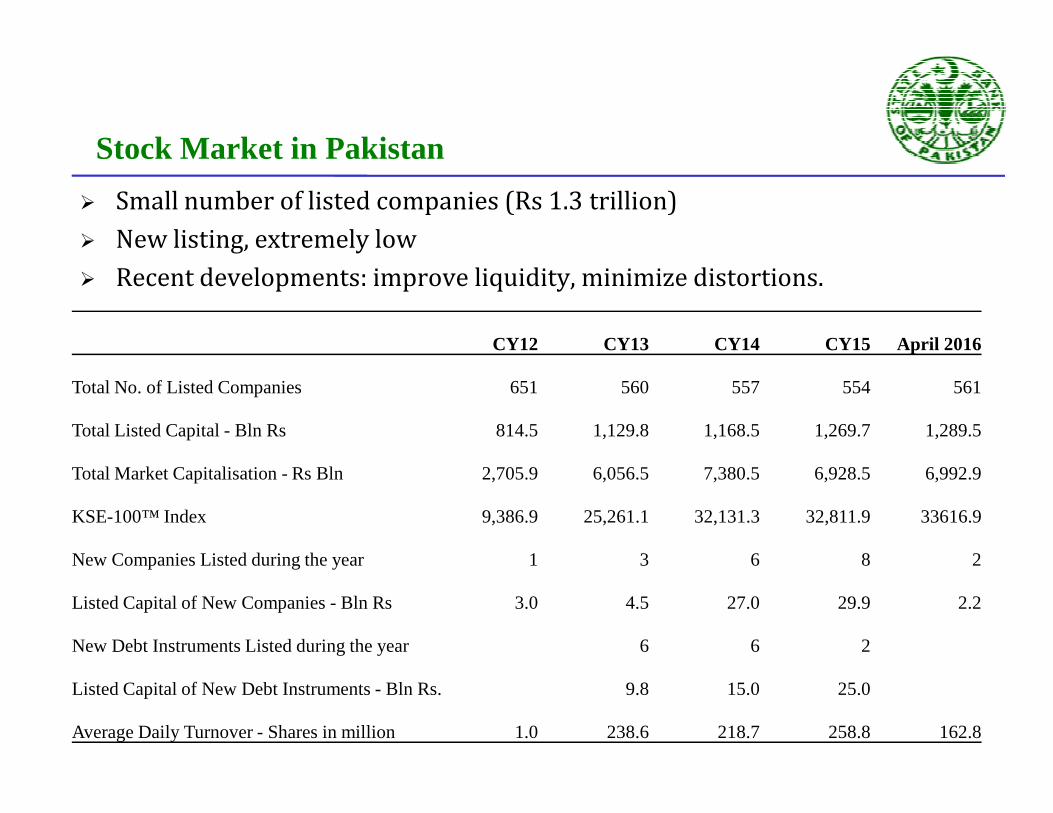

Stock Market in Pakistan

� Small number of listed companies (Rs 1.3 trillion)

� New listing, extremely low

� Recent developments: improve liquidity, minimize distortions.

CY12 CY13 CY14 CY15 April 2016

Total No. of Listed Companies 651 560 557 554 561

Total Listed Capital - Bln Rs 814.5 1,129.8 1,168.5 1,269.7 1,289.5

Total Market Capitalisation - Rs Bln 2,705.9 6,056.5 7,380.5 6,928.5 6,992.9

KSE-100™ Index 9,386.9 25,261.1 32,131.3 32,811.9 33616.9

New Companies Listed during the year 1 3 6 8 2

Listed Capital of New Companies - Bln Rs 3.0 4.5 27.0 29.9 2.2

New Debt Instruments Listed during the year 6 6 2

Listed Capital of New Debt Instruments - Bln Rs. 9.8 15.0 25.0

Average Daily Turnover - Shares in million 1.0 238.6 218.7 258.8 162.8

THANKS

37

THANKS

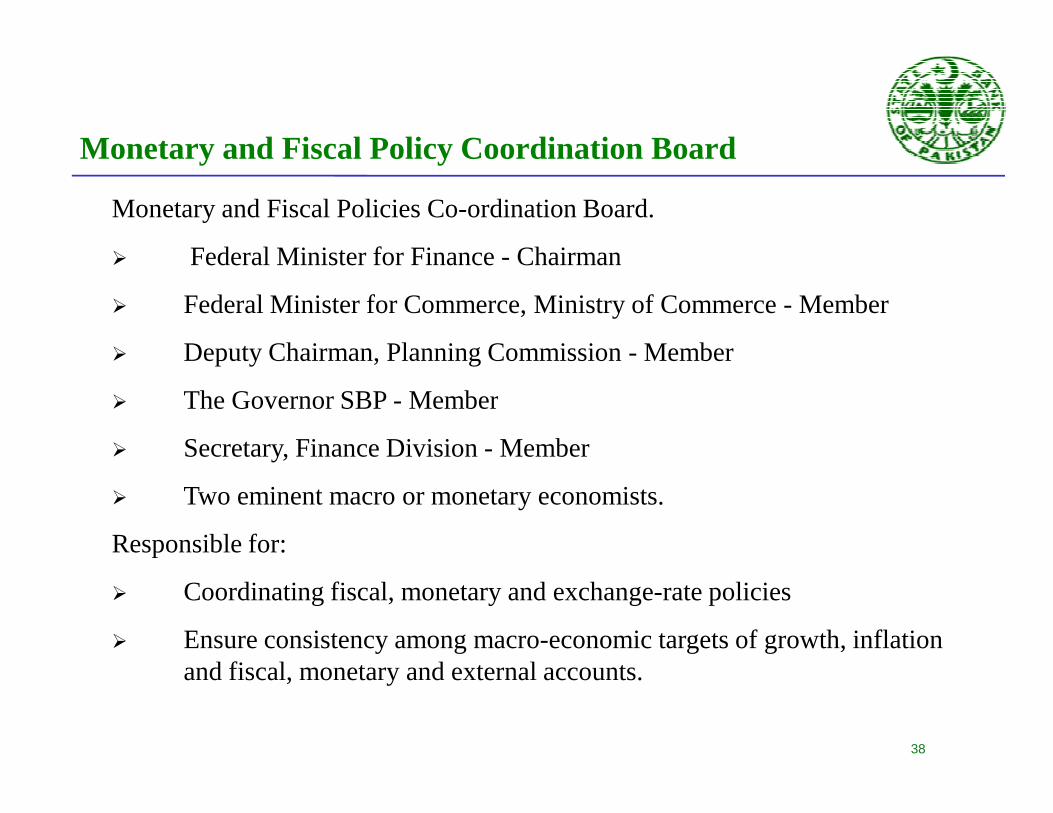

Monetary and Fiscal Policies Co-ordination Board.

� Federal Minister for Finance - Chairman

� Federal Minister for Commerce, Ministry of Commerce - Member

� Deputy Chairman, Planning Commission - Member

� The Governor SBP - Member

Monetary and Fiscal Policy Coordination Board

� The Governor SBP - Member

� Secretary, Finance Division - Member

� Two eminent macro or monetary economists.

Responsible for:

� Coordinating fiscal, monetary and exchange-rate policies

� Ensure consistency among macro-economic targets of growth, inflation and fiscal, monetary and external accounts.

38

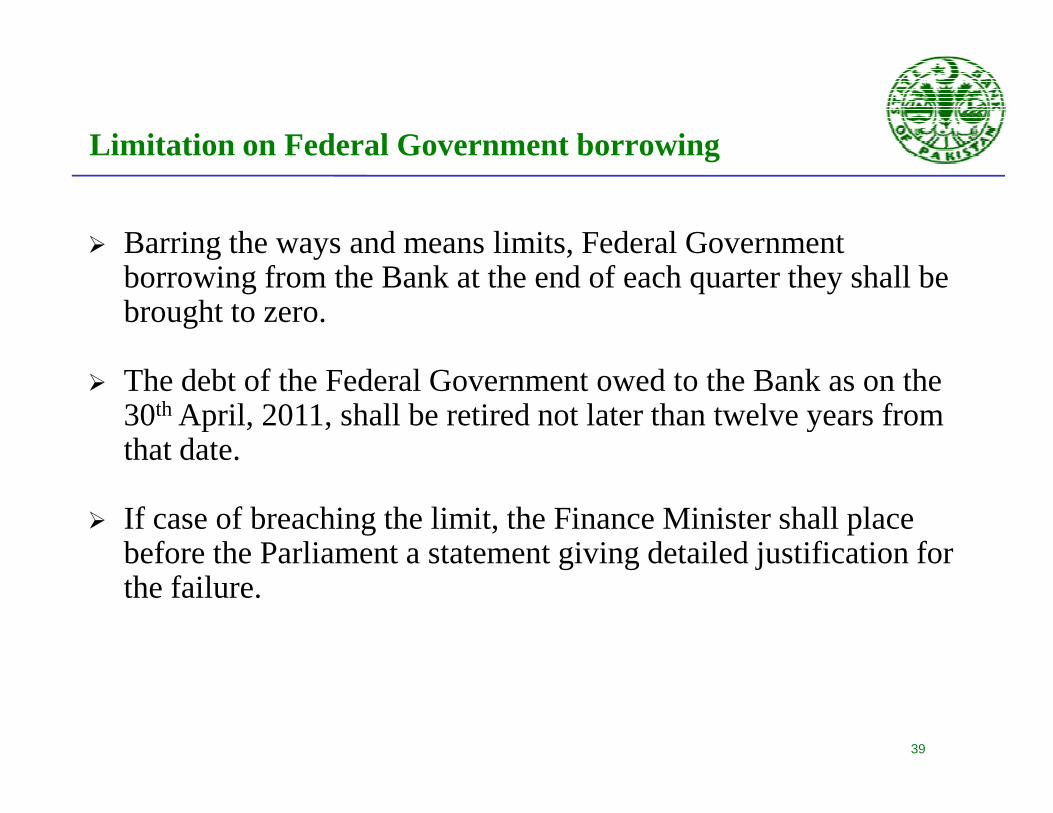

� Barring the ways and means limits, Federal Government borrowing from the Bank at the end of each quarter they shall be brought to zero.

� The debt of the Federal Government owed to the Bank as on the 30th April, 2011, shall be retired not later than twelve years from

Limitation on Federal Government borrowing

30th April, 2011, shall be retired not later than twelve years from that date.

� If case of breaching the limit, the Finance Minister shall place before the Parliament a statement giving detailed justification for the failure.

39