Embed Size (px)

Citation preview

TRID: TILA/RESPA Integrated Disclosures Dan Hanson, Executive Vice President of National Production

2

Texan Proverb

A Kodak Moment

Raymond Depardon, Kodak Picture Spot, California, Los Angeles, 1982

3

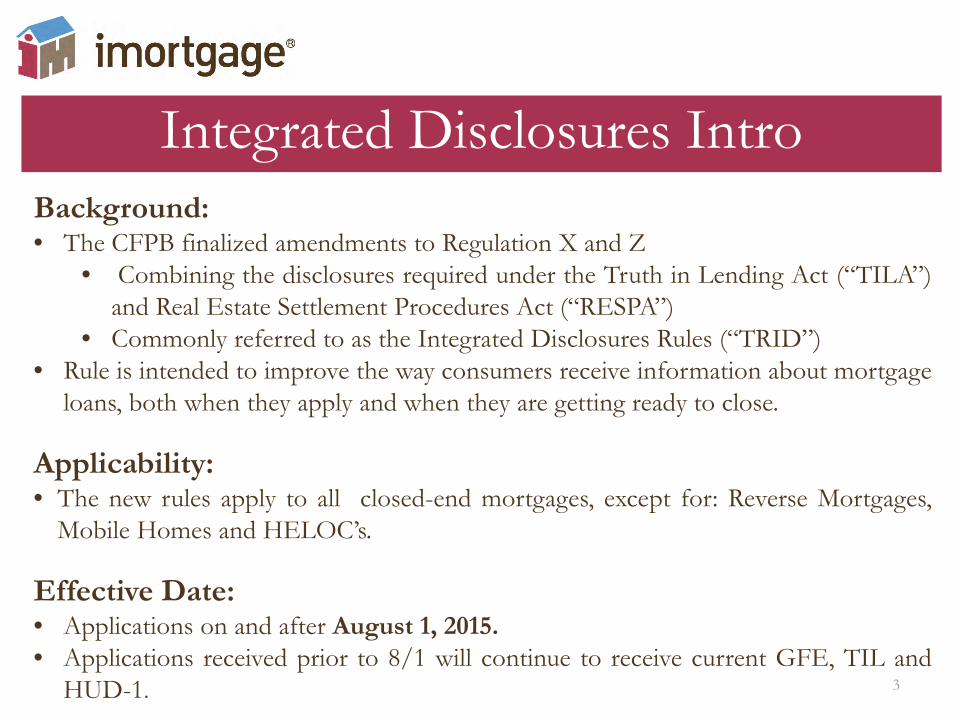

Integrated Disclosures Intro Background: • The CFPB finalized amendments to Regulation X and Z

• Combining the disclosures required under the Truth in Lending Act (“TILA”) and Real Estate Settlement Procedures Act (“RESPA”)

• Commonly referred to as the Integrated Disclosures Rules (“TRID”) • Rule is intended to improve the way consumers receive information about mortgage

loans, both when they apply and when they are getting ready to close.

Applicability: • The new rules apply to all closed-end mortgages, except for: Reverse Mortgages,

Mobile Homes and HELOC’s.

Effective Date: • Applications on and after August 1, 2015. • Applications received prior to 8/1 will continue to receive current GFE, TIL and

HUD-1.

4

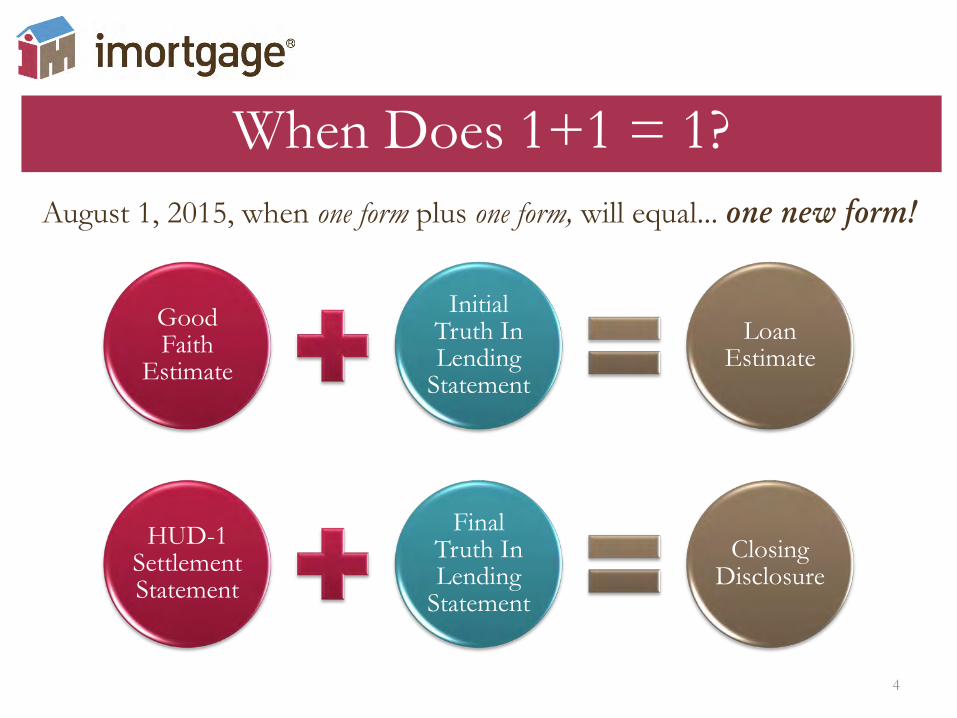

When Does 1+1 = 1? August 1, 2015, when one form plus one form, will equal... one new form!

Good Faith

Estimate

Initial Truth In Lending

Statement

Loan Estimate

HUD-1 Settlement Statement

Final Truth In Lending

Statement

Closing Disclosure

5

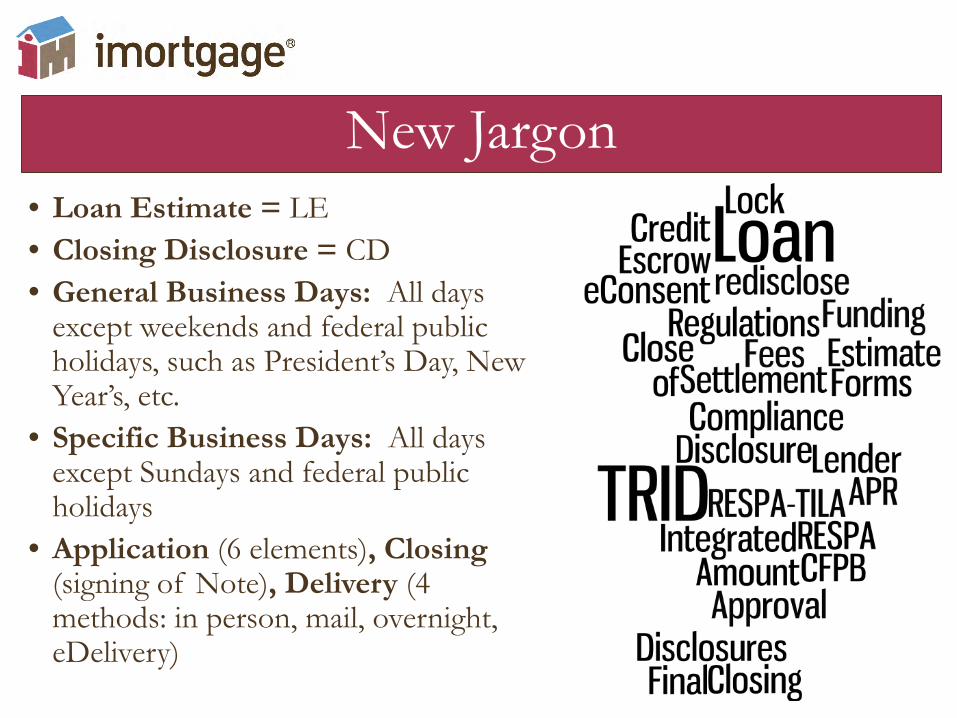

• Loan Estimate = LE • Closing Disclosure = CD • General Business Days: All days

except weekends and federal public holidays, such as President’s Day, New Year’s, etc.

• Specific Business Days: All days except Sundays and federal public holidays

• Application (6 elements), Closing (signing of Note), Delivery (4 methods: in person, mail, overnight, eDelivery)

New Jargon

6

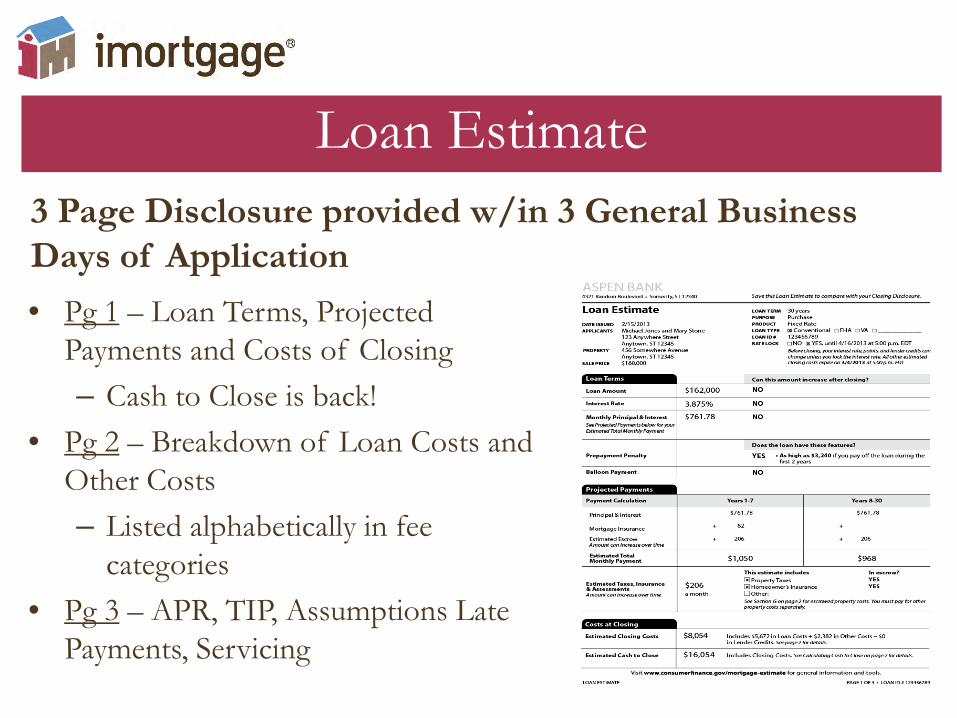

• Pg 1 – Loan Terms, Projected Payments and Costs of Closing – Cash to Close is back!

• Pg 2 – Breakdown of Loan Costs and Other Costs – Listed alphabetically in fee

categories • Pg 3 – APR, TIP, Assumptions Late

Payments, Servicing

Loan Estimate 3 Page Disclosure provided w/in 3 General Business Days of Application

7

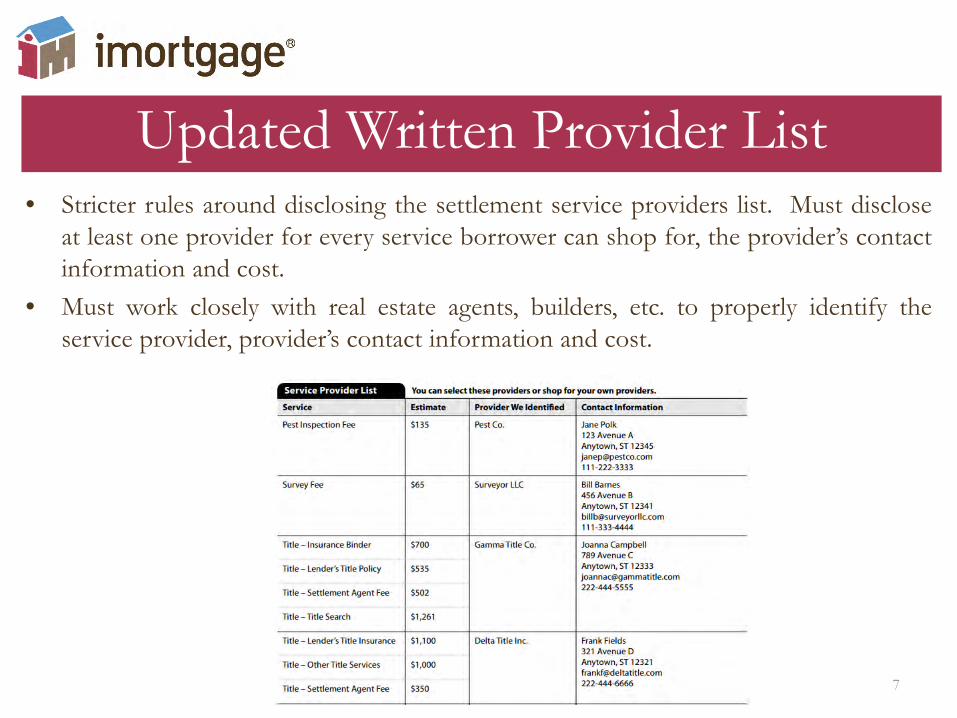

• Stricter rules around disclosing the settlement service providers list. Must disclose at least one provider for every service borrower can shop for, the provider’s contact information and cost.

• Must work closely with real estate agents, builders, etc. to properly identify the service provider, provider’s contact information and cost.

Updated Written Provider List

8

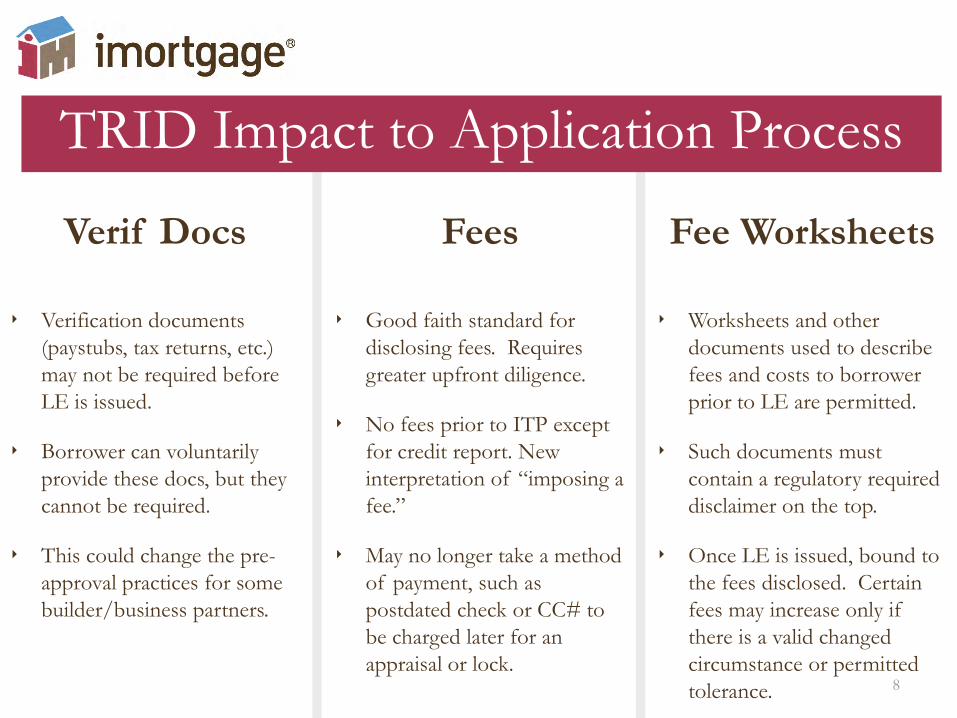

Verif Docs

‣ Verification documents (paystubs, tax returns, etc.) may not be required before LE is issued.

‣ Borrower can voluntarily provide these docs, but they cannot be required.

‣ This could change the pre-approval practices for some builder/business partners.

Fees

‣ Good faith standard for disclosing fees. Requires greater upfront diligence.

‣ No fees prior to ITP except for credit report. New interpretation of “imposing a fee.”

‣ May no longer take a method of payment, such as postdated check or CC# to be charged later for an appraisal or lock.

Fee Worksheets

‣ Worksheets and other documents used to describe fees and costs to borrower prior to LE are permitted.

‣ Such documents must contain a regulatory required disclaimer on the top.

‣ Once LE is issued, bound to the fees disclosed. Certain fees may increase only if there is a valid changed circumstance or permitted tolerance.

TRID Impact to Application Process

9

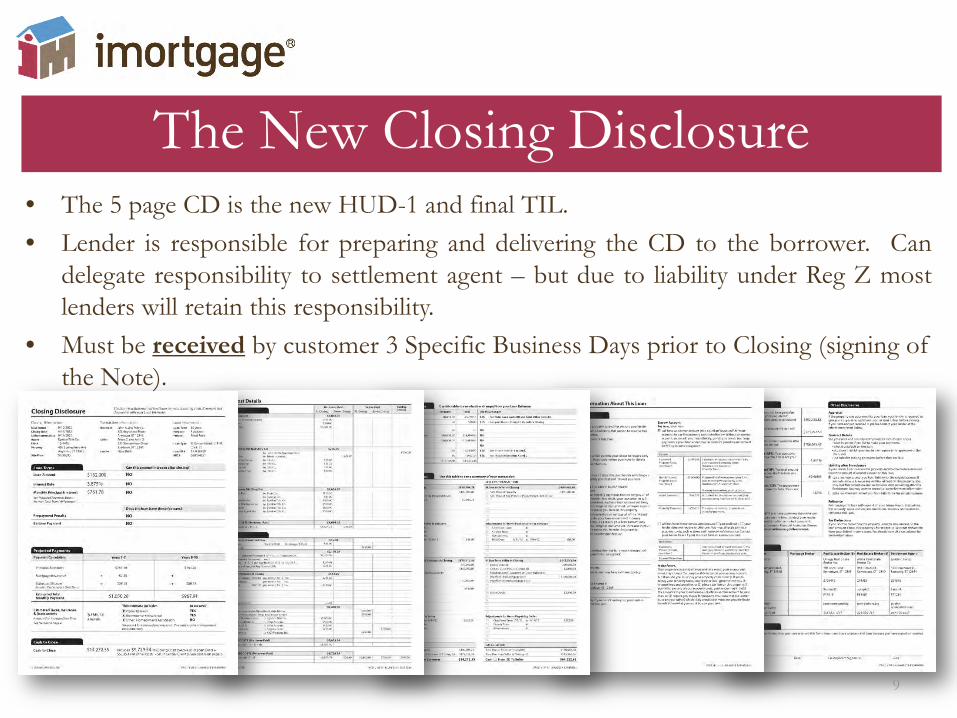

• The 5 page CD is the new HUD-1 and final TIL. • Lender is responsible for preparing and delivering the CD to the borrower. Can

delegate responsibility to settlement agent – but due to liability under Reg Z most lenders will retain this responsibility.

• Must be received by customer 3 Specific Business Days prior to Closing (signing of the Note).

The New Closing Disclosure

10

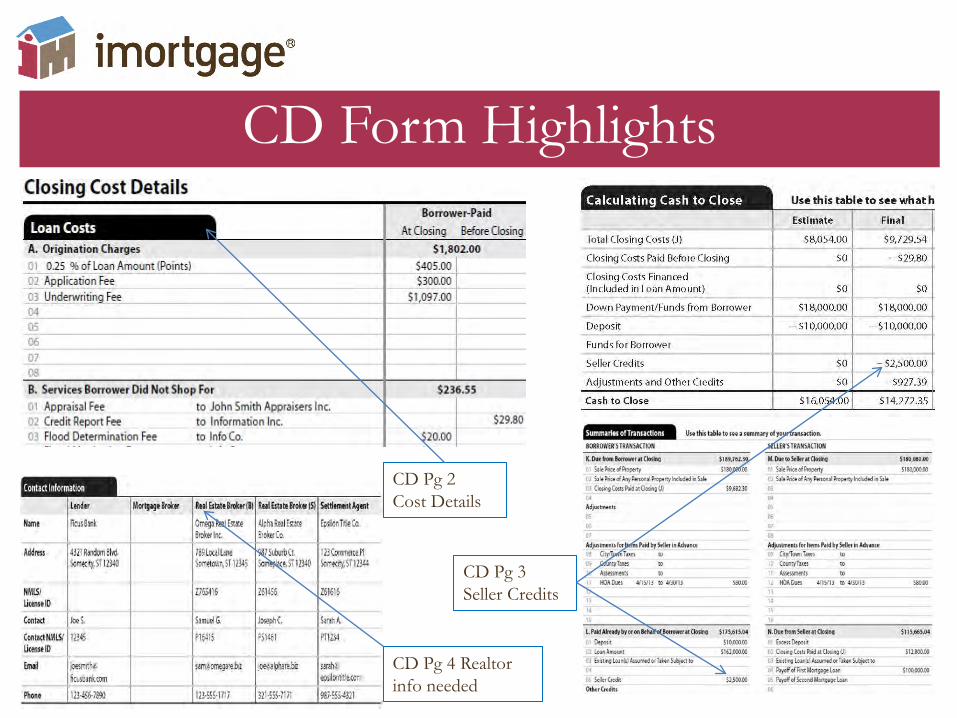

CD Form Highlights

CD Pg 4 Realtor info needed

CD Pg 3 Seller Credits

CD Pg 2 Cost Details

11

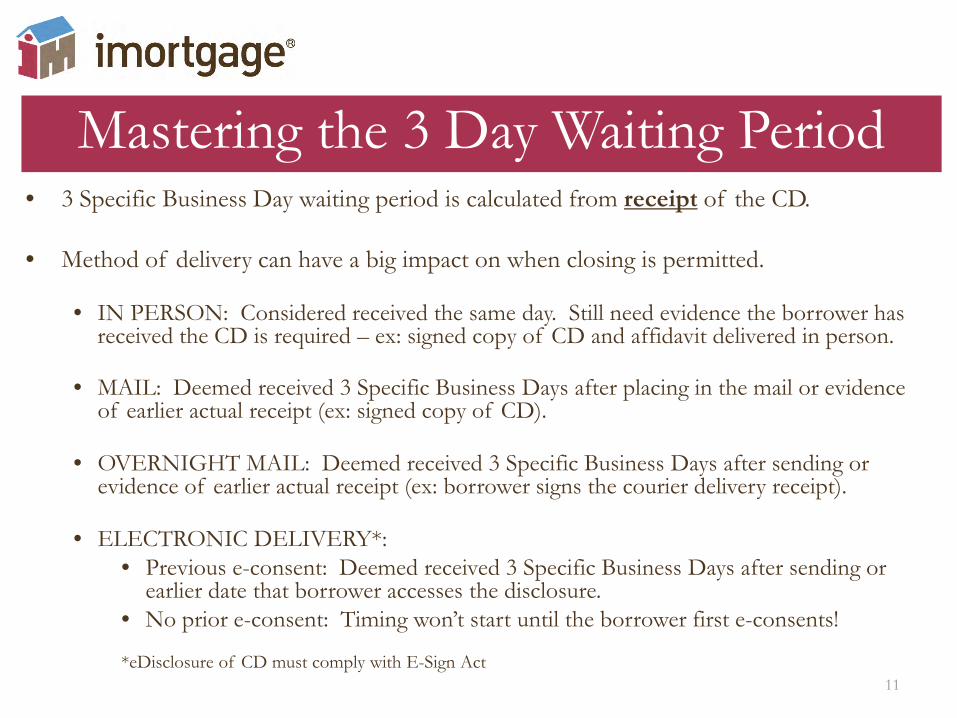

• 3 Specific Business Day waiting period is calculated from receipt of the CD.

• Method of delivery can have a big impact on when closing is permitted. • IN PERSON: Considered received the same day. Still need evidence the borrower has

received the CD is required – ex: signed copy of CD and affidavit delivered in person.

• MAIL: Deemed received 3 Specific Business Days after placing in the mail or evidence of earlier actual receipt (ex: signed copy of CD).

• OVERNIGHT MAIL: Deemed received 3 Specific Business Days after sending or evidence of earlier actual receipt (ex: borrower signs the courier delivery receipt).

• ELECTRONIC DELIVERY*: • Previous e-consent: Deemed received 3 Specific Business Days after sending or

earlier date that borrower accesses the disclosure. • No prior e-consent: Timing won’t start until the borrower first e-consents! *eDisclosure of CD must comply with E-Sign Act

Mastering the 3 Day Waiting Period

12

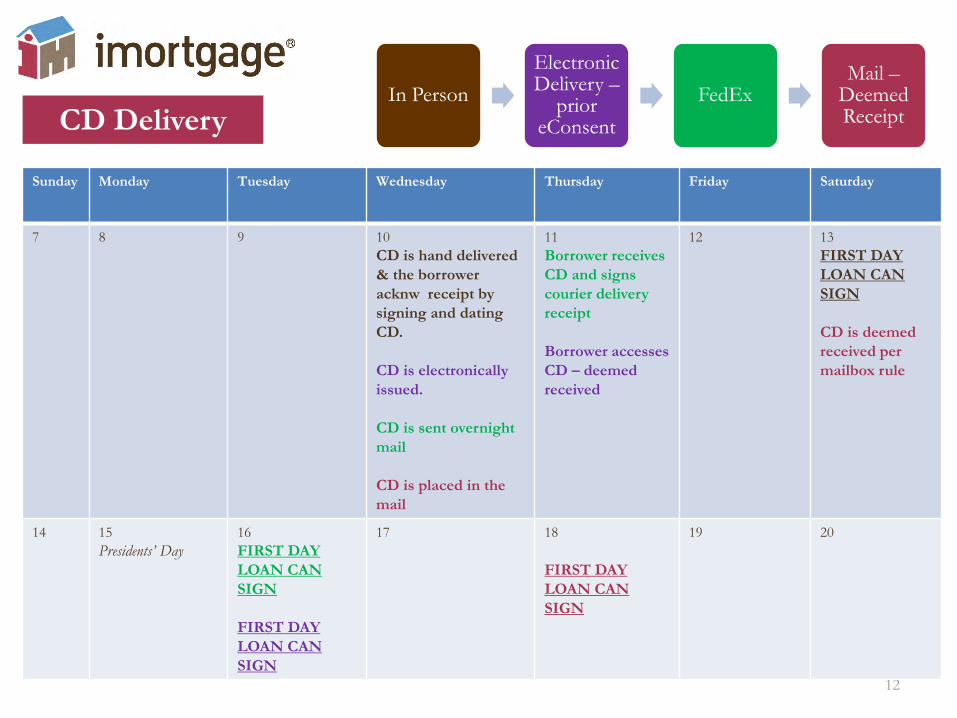

Sunday Monday Tuesday Wednesday Thursday Friday Saturday

7 8 9 10 CD is hand delivered & the borrower acknw receipt by signing and dating CD. CD is electronically issued. CD is sent overnight mail CD is placed in the mail

11 Borrower receives CD and signs courier delivery receipt Borrower accesses CD – deemed received

12 13 FIRST DAY LOAN CAN SIGN CD is deemed received per mailbox rule

14 15 Presidents’ Day

16 FIRST DAY LOAN CAN SIGN FIRST DAY LOAN CAN SIGN

17

18 FIRST DAY LOAN CAN SIGN

19 20

In Person Electronic Delivery –

prior eConsent

FedEx Mail –

Deemed Receipt CD Delivery

13

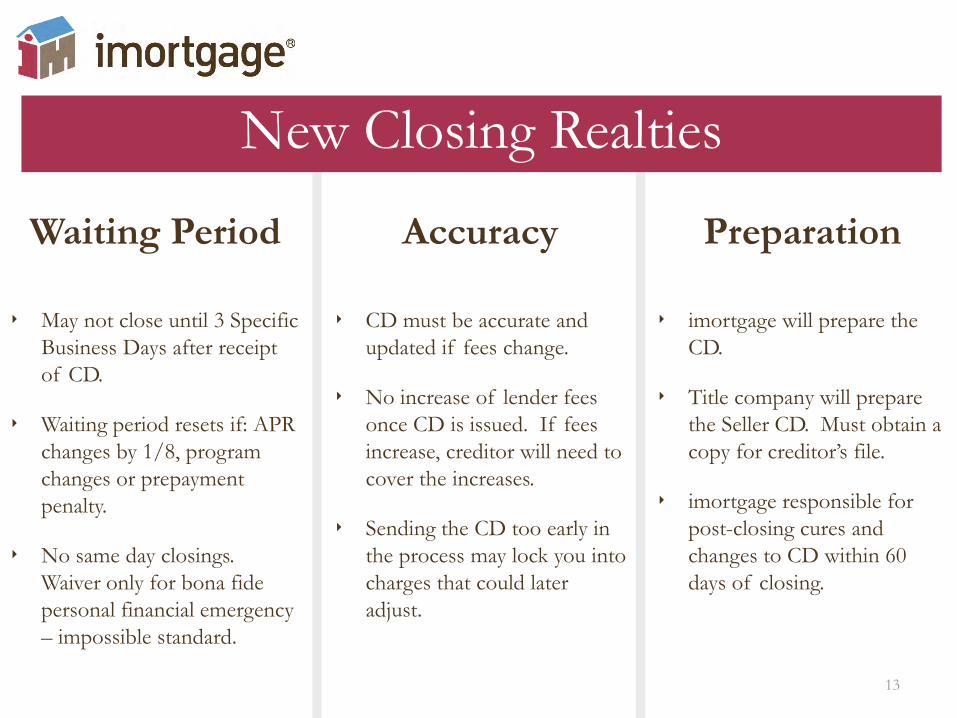

Waiting Period

‣ May not close until 3 Specific Business Days after receipt of CD.

‣ Waiting period resets if: APR changes by 1/8, program changes or prepayment penalty.

‣ No same day closings. Waiver only for bona fide personal financial emergency – impossible standard.

Accuracy

‣ CD must be accurate and updated if fees change.

‣ No increase of lender fees once CD is issued. If fees increase, creditor will need to cover the increases.

‣ Sending the CD too early in the process may lock you into charges that could later adjust.

Preparation

‣ imortgage will prepare the CD.

‣ Title company will prepare the Seller CD. Must obtain a copy for creditor’s file.

‣ imortgage responsible for post-closing cures and changes to CD within 60 days of closing.

New Closing Realties

14

Texan Proverb

“If you can’t change your fate, change your attitude.”

Maya Angelou

Timing Is Everything

Life in the Fast Lane

15

Accurate COE

Early CTC

Vendor Portal

eDelivery

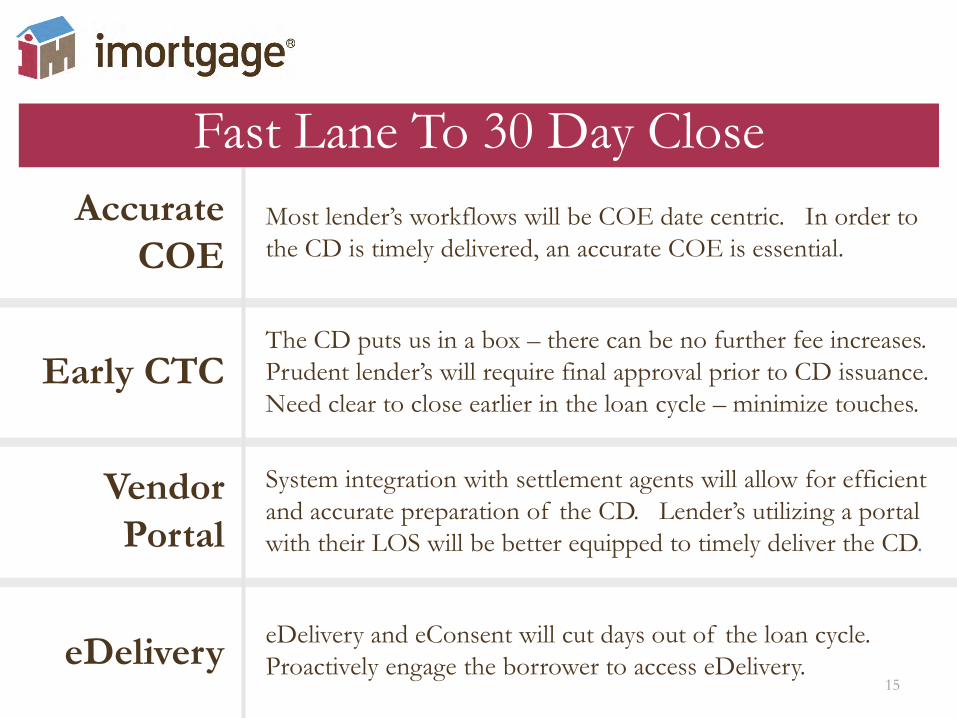

Most lender’s workflows will be COE date centric. In order to the CD is timely delivered, an accurate COE is essential.

The CD puts us in a box – there can be no further fee increases. Prudent lender’s will require final approval prior to CD issuance. Need clear to close earlier in the loan cycle – minimize touches.

System integration with settlement agents will allow for efficient and accurate preparation of the CD. Lender’s utilizing a portal with their LOS will be better equipped to timely deliver the CD.

eDelivery and eConsent will cut days out of the loan cycle. Proactively engage the borrower to access eDelivery.

Fast Lane To 30 Day Close

16

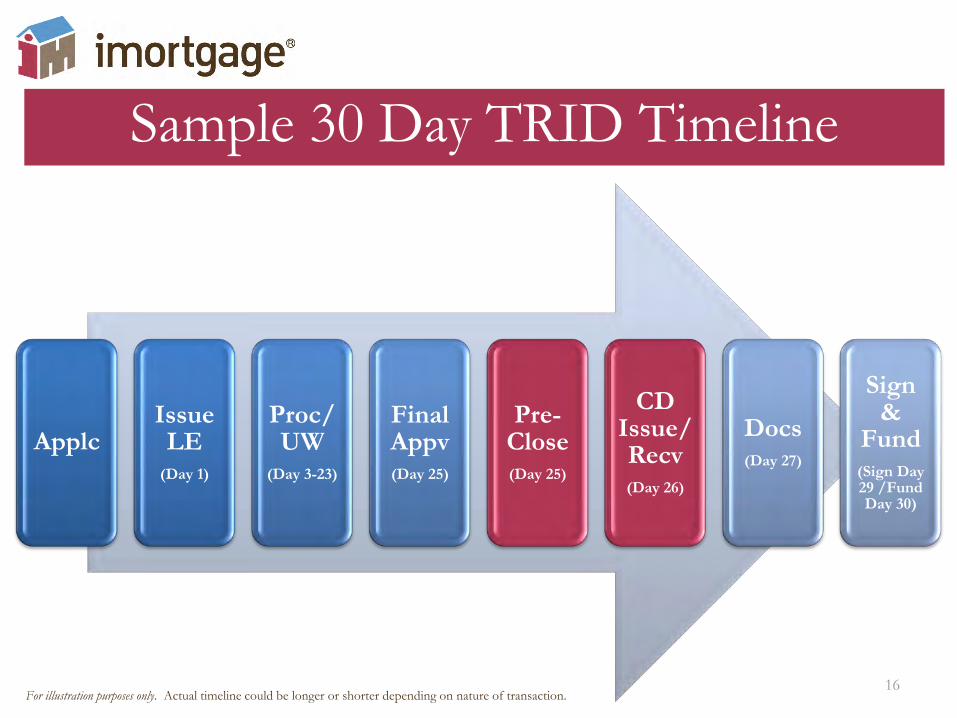

Applc Issue LE

(Day 1)

Proc/UW

(Day 3-23)

Final Appv (Day 25)

Pre-Close (Day 25)

CD Issue/Recv (Day 26)

Docs (Day 27)

Sign &

Fund (Sign Day 29 /Fund Day 30)

Sample 30 Day TRID Timeline

For illustration purposes only. Actual timeline could be longer or shorter depending on nature of transaction.

17

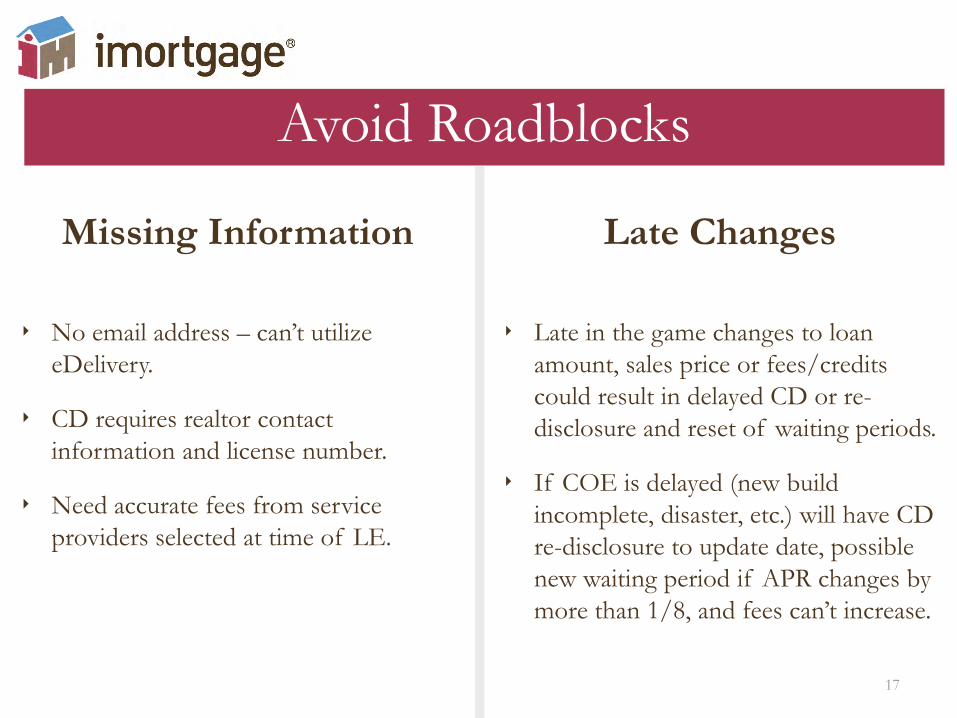

Missing Information Late Changes

‣ No email address – can’t utilize eDelivery.

‣ CD requires realtor contact information and license number.

‣ Need accurate fees from service providers selected at time of LE.

‣ Late in the game changes to loan amount, sales price or fees/credits could result in delayed CD or re-disclosure and reset of waiting periods.

‣ If COE is delayed (new build incomplete, disaster, etc.) will have CD re-disclosure to update date, possible new waiting period if APR changes by more than 1/8, and fees can’t increase.

Avoid Roadblocks

18

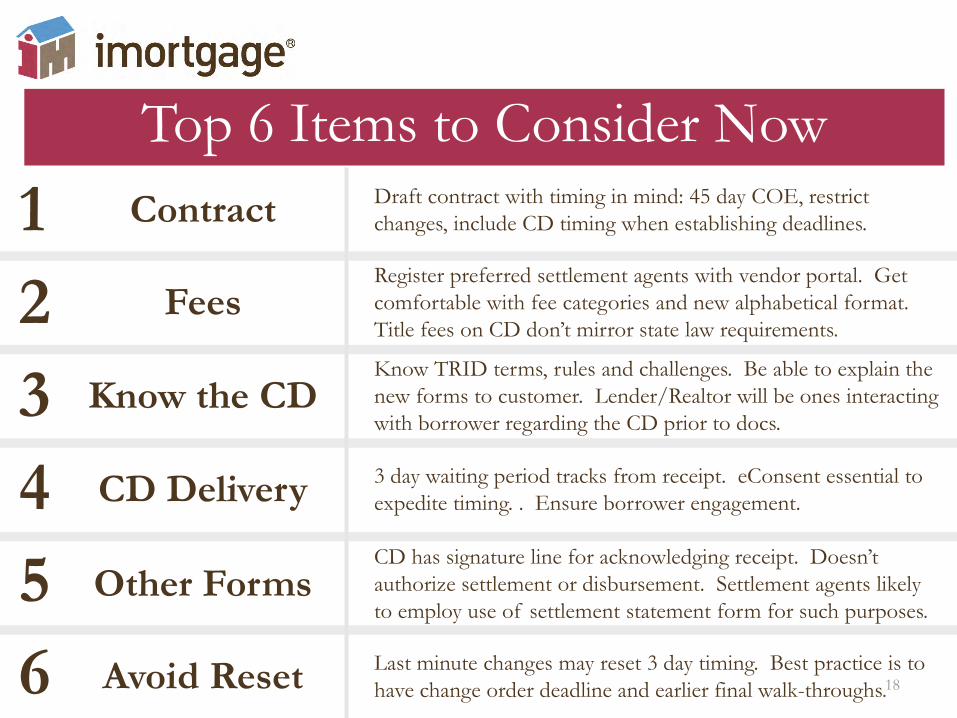

Contract Draft contract with timing in mind: 45 day COE, restrict changes, include CD timing when establishing deadlines.

Fees Register preferred settlement agents with vendor portal. Get comfortable with fee categories and new alphabetical format. Title fees on CD don’t mirror state law requirements.

Know the CD Know TRID terms, rules and challenges. Be able to explain the new forms to customer. Lender/Realtor will be ones interacting with borrower regarding the CD prior to docs.

CD Delivery 3 day waiting period tracks from receipt. eConsent essential to expedite timing. . Ensure borrower engagement.

Other Forms CD has signature line for acknowledging receipt. Doesn’t authorize settlement or disbursement. Settlement agents likely to employ use of settlement statement form for such purposes.

Avoid Reset Last minute changes may reset 3 day timing. Best practice is to have change order deadline and earlier final walk-throughs.

1 2 3 4 5 6

Top 6 Items to Consider Now

19

Texan Proverb

“If you can’t change your fate, change your attitude.”

Maya Angelou

Communicate, Coordinate, Collaborate

20

Texan Proverb

TRID TILA/RESPA Integrated Disclosures

imortgage is ready for August 1st!

For educational purpose only. loanDepot.com, LLC dba imortgage is licensed by the Alabama Consumer Credit, License 21189; AZ Department of Financial Institutions, Mortgage Banker 0924173; CA Department of Business Oversight under California Residential Mortgage Lending Act, 4131040; CO Department of Regulatory Agencies, Division of Real Estate, Registered Mortgage Company; FL Office of Financial Regulations, Mortgage Lender Servicer MLD903; GA Department of Banking and Finance, Residential Mortgage Licensee 24020; ID Department of Finance, Broker/Lender MBL-7650; NC Commissioner of Banks, Mortgage Lender L-147367; NM Financial Institutions Division of the Regulation and Licensing Department, as a Mortgage Loan Company; NV Department of Business and Industry - Division of Mortgage Lending, Mortgage Banker 3646; OR Division of Finance and Corporate Securities, Mortgage Lender ML-4972; SC State Board of Financial Institutions, Mortgage Lender/Servicer MLS-174457; TN Department of Financial Institutions, Residential Mortgage Licensee 110371; TX Department of Savings and Mortgage Lending under a Mortgage Banker Registration; VA Bureau of Financial Institutions, Broker/Lender MC-5431; WA State Department of Financial Institutions, Consumer Loan Company CL174457; WY Division of Banking, Mortgage Lender/Broker License 2092. Corporate NMLS 174457. All rights reserved. Updated 04/02/2015

DAN HANSON EXECUTIVE VICE PRESIDENT OF NATIONAL PRODUCTION EMAIL: [email protected]