Embed Size (px)

Citation preview

TRACTEBEL ENGINEERING S.A. Avenue Ariane, 7 – 1200 Brussels - BELGIUM tel. +32 2 773 99 11 - fax +32 2 773 99 00 [email protected] tractebel-engie.com TECHNICAL NOTE

Our ref.: EASTNSI/4NT/0512397/000/02

TS:Imputation: P.008903/0004

Client:

Project:

02 2017 02 16 FIN *P. Henneaux *M. Bons

*L. Charlier *E. Haesen

*S. Ouziaux *J. Dubois

01 2016 12 09 FIN *P. Henneaux *L. Charlier *S. Ouziaux *J. Dubois

00 2016 11 18 FIN *P. Henneaux *L. Charlier *J. Dubois

REV. YY/MM/DD STAT. WRITTEN VERIFIED APPROVED VALIDATED

* This document is fully electronically signed on 2017 02 24.TRACTEBEL ENGINEERING S.A. – registered office: Avenue Ariane 7 – 1200 Brussels - BELGIUM VAT:BE 0412 639 681 – RMP/RPR Brussels: 0412 639 681 – Bank account - IBAN: BE74375100843707 – BIC/SWIFT: BBRUBEBB

European Commission

Study on electricity infrastructure developments in Central and South EasternEurope

FINAL REPORTSubject:

Comments:More information on the European Union is available on the Internet (http://www.europa.eu).

Luxembourg: Publications Office of the European Union, 2016

ISBN: 978-92-79-63919-7

Catalogue number: MJ0716069ENN doi: 10.2833/706948

© European Union, 2016

Reproduction is authorised provided the source is acknowledged.

The study has been carried out for the European Commission and expresses the opinion of the organisation having undertaken them. To this end, it does not reflect the views of the European Commission, TSOs, project promoters and other stakeholders involved. The European Commission does not guarantee the accuracy of the information given in the study, nor does it accept responsibility for any use made thereof

EASTNSI/4NT/0512397/000/02 2017 02 16 3/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

EUROPEAN COMMISSION – DIRECTORATE-GENERAL FOR ENERGY ENERGY/B1/2015-572 – STUDY ON ELECTRICITY INFRASTRUCTURE DEVELOPMENTS IN CENTRAL AND SOUTH EASTERN EUROPE FINAL REPORT

TABLE OF CONTENTS

1. INTRODUCTION ................................................................................................................... 5

2. ANALYSIS OF EXISTING PCIS ............................................................................................ 8

2.1. List of interconnection projects and groups ......................................................... 8

2.2. Detailed groups and internal reinforcements ...................................................... 10

2.2.1. Group I (AT/DE) ........................................................................................... 10 2.2.2. Group II (AT/IT) ........................................................................................... 11 2.2.3. Group III (AT/IT) .......................................................................................... 12 2.2.4. Group IV (BG/EL) ........................................................................................ 12 2.2.5. Group V (BG/RO) ........................................................................................ 13 2.2.6. Group VI (SI/HU/HR) ................................................................................... 15 2.2.7. Group VII (IL/CY/EL) ................................................................................... 16 2.2.8. Group VIII (CZ/DE) ...................................................................................... 17 2.2.9. Group IX (DE/PL) ........................................................................................ 18 2.2.10. Group X (DE/PL) ......................................................................................... 19 2.2.11. Group XI (SK/HU) ........................................................................................ 20 2.2.12. Group XII (SK/HU) ....................................................................................... 21 2.2.13. Group XIII (IT/ME) ....................................................................................... 22 2.2.14. Group XIV (IT/SI) ......................................................................................... 22 2.2.15. Group XV (RO/RS) ...................................................................................... 23

2.3. CBA of interconnection projects .......................................................................... 24

2.3.1. Short-term groups ........................................................................................ 25 2.3.2. Mid-term groups .......................................................................................... 25 2.3.3. Long-term groups ........................................................................................ 26

2.4. Analysis of interconnection levels ....................................................................... 27

2.5. Ranking of groups ................................................................................................. 28

2.5.1. Short-term groups ........................................................................................ 29

EASTNSI/4NT/0512397/000/02 2017 02 16 4/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2.5.2. Mid-term groups .......................................................................................... 29

2.6. Conclusions ........................................................................................................... 30

3. ANALYSIS OF BARRIERS AND CORRESPONDING RECOMMENDATIONS ................... 32

3.1. Overview of delayed PCIs ...................................................................................... 33

3.2. Longlist of barriers ................................................................................................ 36

3.3. Experiences of project promoters ........................................................................ 37

3.4. Major barriers ......................................................................................................... 42

3.4.1. Organisational issues at the permitting authority ......................................... 42 3.4.2. Difficulties related to the EIA ........................................................................ 44 3.4.3. Public consultation and opposition ............................................................... 45 3.4.4. Financing ..................................................................................................... 45

3.5. Need for actions ..................................................................................................... 47

3.5.1. Existing measures ....................................................................................... 47 3.5.2. New measures and recommendations ........................................................ 52

4. ASSESSMENT OF FURTHER INTEGRATION ................................................................... 55

4.1. Methodology ........................................................................................................... 55

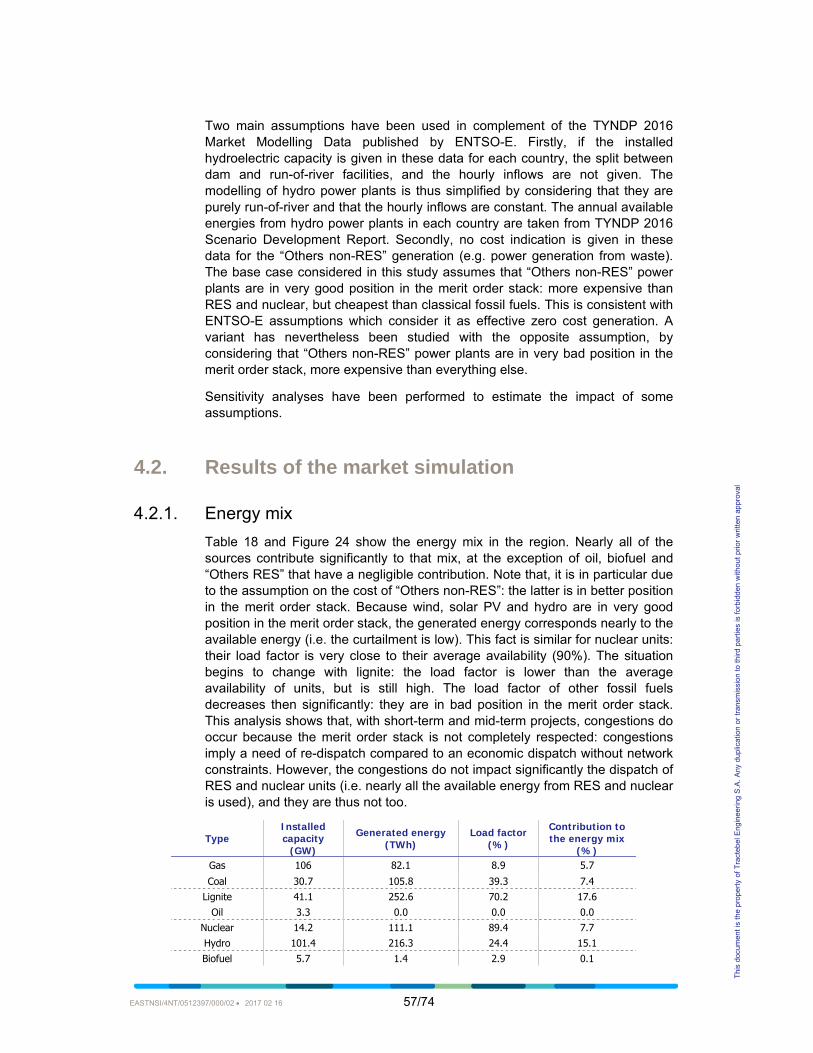

4.2. Results of the market simulation .......................................................................... 57

4.2.1. Energy mix .................................................................................................. 57 4.2.2. Zonal marginal electricity prices and major bottlenecks ............................... 59

4.3. Sensitivity analyses ............................................................................................... 62

4.3.1. Impact of internal constraints in Germany and Italy ..................................... 62 4.3.2. Impact of load-generation vision .................................................................. 63 4.3.3. Impact of generation assumptions ............................................................... 64 4.3.4. Summary of the main congested interconnections ...................................... 65

4.4. Need of further integration in the region .............................................................. 66

5. CONCLUSIONS .................................................................................................................. 67

ANNEX A: LITERATURE ........................................................................................................... 69

ANNEX B: CASE STUDIES ....................................................................................................... 70 PCI cluster 3.4.......................................................................................................... 70 PCI cluster 3.8.......................................................................................................... 71 PCI cluster 3.15 ........................................................................................................ 73

EASTNSI/4NT/0512397/000/02 2017 02 16 5/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

1. INTRODUCTION

In 2002, the European Council in Barcelona agreed on "the target for Member States of a level of electricity interconnections equivalent to at least 10% of their installed production capacity by 2005”. This target, expressed in terms of Net Transfer Capacity (NTC), was reiterated by the European Council in May 2013. In May 2014, the Commission proposed to extend the current 10% electricity interconnection target to 15% by 2030 while taking into account the cost aspects and the potential of commercial exchanges in the relevant regions. The European Council Conclusions requested that the EC, supported by the Member States, takes measures in order to ensure the achievement of a minimum target of 10% of existing electricity interconnections, as a matter of urgency, and no later than 2020 at least for Member States which have not yet attained a minimum level of integration in the internal energy market.

Despite the original target date of 2005, as indicated in Table 1, twelve Member States had still not met the 10% target as of 2014, including three of the five largest power systems in Europe.

The TEN-E Regulation1 identifies 4 priority electricity corridors (in its Annex I) which aim to identify Projects of Common Interest that support the achievement of internal market, sustainability and security of supply. In particular, the TEN-E Regulation identifies the NSI East Electricity priority corridor comprising Member States from Central Eastern and South Eastern Europe. For this purpose, in the second PCI list (Regulation (EU) 2016/89), 42 (out of 108) PCIs in the electricity sector belong to the NSI East Electricity corridor. However, this corridor shows a high degree of delay of PCI implementation, especially for financing and permitting issues.

Member States below 10% interconnection level

IE 9%

IT 7%

RO 7%

PT 7%

EE 4%

LT 4%

LV 4%

UK 6%

ES 3%

PL 2%

CY 0%

MT 0%

Table 1: Interconnection levels for electricity in 2014 for Member States below the 10% level

Source: ENTSO-E, Scenario Outlook and Adequacy Forecast 2014, as reported in COM(2015)82 final

1 Regulation (EU) 347/2013

EASTNSI/4NT/0512397/000/02 2017 02 16 6/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

The objective of this study is thus to provide an in-depth analysis of the electricity infrastructure developments in that region (especially the need of new interconnections), to understand the barriers (administrative, permitting, regulatory and financing aspects) towards the deployment of these projects, and to provide recommendations to progress on PCIs deployment in this region.

As shown in Figure 1, the NSI East region gathers 13 countries that are analysed in details in the frame of this study: Italy, Hungary, Romania, Germany, Slovenia, Bulgaria, Poland, Croatia, Cyprus, Slovakia, Greece, Czech Republic and Austria. In addition, the cross-borders with Energy Community contracting parties2 (Serbia, Bosnia and Herzegovina, Montenegro, FYR of Macedonia, and Albania) are also considered.

Figure 1: Geographical Scope of the study

The first step of the study is the assessment of existing Projects of Common Interest in the region and the way they address the specific bottlenecks in the electricity networks of the region. A key element of the study is the detailed analysis of the impact of each PCI on EU energy policies such as RES integration and Internal Energy Market completion. For this purpose, Chapter 2 reviews existing Cost Benefit Analysis (CBA) of PCIs in the region and drafts a prioritised project list to guarantee that a further integration in the region brings substantial socioeconomic benefits. This list focuses on short-term and mid-term

2 At the exception of Kosovo and Moldova.

EASTNSI/4NT/0512397/000/02 2017 02 16 7/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

interconnection projects, i.e. projects that are expected to be fully commissioned by 2025.

On the basis of this draft prioritised list, Chapter 3 investigates the delays and the barriers relevant for the deployment of the most important electricity infrastructure projects in Central and South Eastern Europe. This analysis of the barriers forms the basis of a proposal for a set of actions to overcome the obstacles identified.

The last step of the study is the assessment of the need for further integration in the region after the implementation of projects included in the prioritised list. Chapter 4 thus studies the expected remaining bottlenecks at the horizon 2030.

EASTNSI/4NT/0512397/000/02 2017 02 16 8/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2. ANALYSIS OF EXISTING PCIS

2.1. List of interconnection projects and groups

The first part of the study is the identification and the analysis of main electricity interconnection projects in the region. The considered list of interconnection projects is based on the list of PCIs, but is limited to projects increasing the transfer capacities between different countries. Therefore, this list of interconnection projects includes cross-border projects and internal reinforcements that increase transfer capacities between different countries, but does not include internal reinforcements that increase transfer capacities inside a specific country.

Figure 2: Map of groups of interdependent interconnection projects that will be analysed

In South-East and Central-East regions, for the 13 countries studied in this project, the analysis of Commission Delegated Regulation (EU) 2016/89 shows that 38 PCIs lead to an increase of cross-border transfer capacities3. These projects can be grouped in 15 groups of interdependent projects. Note that one of these groups gathers two co-dependent PCIs (3.16.1 and 3.17). Table 2 and Figure 2 show these groups. The ones indicated in red are the short-term groups (commissioning expected before 2020) while the one in orange and green are mid-term (commissioning expected between 2020 and 2025) and long-term (commissioning expected between 2025 and 2030) groups. The commissioning dates considered for this classification are the commissioning dates of the latest PCI of each group, as estimated by the PCI fiches of October

3 Internal projects without impact on cross-border transfer capacities such as the ones related to some of the internal German lines as well as storage projects are out of the scope of this study.

EASTNSI/4NT/0512397/000/02 2017 02 16 9/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2015 (latest version of the PCI fiches at the beginning of this study)4. Indeed, the expected increase of the interconnection capacity as estimated by ENTSO-E will be reached only when all projects of the group will be commissioned.

Group ID

Group Name Corresponding PCIs

Cross-border PCIs

I Interconnection Austria – Germany, between St. Peter (AT) and Isar (DE) 3.1.1, 3.1.2 3.1.1

II Interconnection Austria – Italy, between Lienz (AT) and Veneto region (IT) 3.2.1, 3.2.2 3.2.1

III Interconnection Austria – Italy, between Wurmlach (AT) and Somplago (IT) 3.4 3.4

IV Interconnection Bulgaria – Greece, between Maritsa East 1 (BG) and N. Santa (EL)

3.7.1, 3.7.2, 3.7.3, 3.7.4 3.7.1

V Capacity increase between Bulgaria and Romania (Black Sea Corridor)

3.8.1, 3.8.4, 3.8.5 -

VI Interconnection Croatia – Hungary – Slovenia, between Zerjavenec (HR) / Heviz (HU) and Cirkovce (SI)

3.9.1, 3.9.2, 3.9.3, 3.9.4 3.9.1

VII Interconnection Israel – Cyprus – Greece (Euroasia

Interconnector) between Hadera (IL), Kofinou (CY) and Korakia (EL)

3.10.1, 3.10.2, 3.10.3 3.10.1, 3.10.2

VIII Capacity increase between Czech Republic and Germany (Czech North South Corridor)

3.11.1, 3.11.2, 3.11.3, 3.11.4,

3.11.5 -

IX Interconnection Germany – Poland (GerPol Power Bridge), between Eisenhuttenstadt (DE) and Plewiska (PL)

3.14.1, 3.14.2, 3.14.3 3.14.1

X Interconnection Germany – Poland (GerPol Improvements), between Vierraden (DE) and Krajnik (PL) 3.15.1, 3.15.2 3.15.1

XI Double interconnection Hungary – Slovakia, between

Gabcikovo (SK) and Gonyu (HU) and between Sajovanka (HU) and Rimavska Sobota (SK)

3.16.1, 3.17 3.16.1, 3.17

XII Interconnection Hungary – Slovakia, between Kisvarda area (HU) and Velké Kapusany (SK) 3.18.1 3.18.1

XIII Interconnection Italy – Montenegro, between Villanova (IT) and Lastva (ME) 3.19.1 3.19.1

XIV Interconnection Italy – Slovenia, between Salgareda (IT) and Divaca-Bericevo region (SI) 3.21 3.21

XV Interconnection Romania – Serbia (Mid Continental East Corridor), between Resita (RO) and Pancevo (RS)

3.22.1, 3.22.2, 3.22.3, 3.22.4 3.22.1

Table 2 : List of groups of interconnection projects that will be analysed

4 Note that the PCI fiches were updated during this study (June 2016). This classification remains valid when

considering that update, except for Group XII: it is rescheduled for 2029 while it was initially planned for 2021. Moreover, expected commissioning dates given by ENTSO-E (in the TYNDP) and by ACER (in the annual report on PCI progress) might slightly differ. That will be discussed in the next chapters.

EASTNSI/4NT/0512397/000/02 2017 02 16 10/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2.2. Detailed groups and internal reinforcements

Because several fundamental characteristics of groups (e.g. their costs and their contribution to the NTC increase between two countries and so the benefits they bring to the system), rely on internal reinforcements, the identification of these internal reinforcements is required. Some internal reinforcements are already identified in the PCI list for PCIs forming part of a cluster. Other internal reinforcements are identified in the TYNDP: a project in the draft TYNDP 2016 package can gather several investment items that have to be realised in total to achieve a desired effect. A group linked to a particular PCI can thus gather projects beyond the ones that are part of the relevant cluster of interdependent PCIs in the second PCI list (Commission Delegated Regulation (EU) 2016/89). This section analyses thus internal reinforcements needed in order to take advantage of the full potential of PCIs.

2.2.1. Group I (AT/DE) Group I is an interconnection Austria – Germany. It consists mainly in a new 380 kV double circuit OHL between St. Peter (AT) and Isar (DE), including 110 km of new line in Germany5, 61 km of new circuit on an existing line, new 380 kV switchgears (in Altheim, Simbach, Pirach and St. Peter), new 380/220 kV transformers (substations Altheim and St. Peter) and a fourth circuit on the line between Isar and Ottenhofen. This project corresponds to the PCI 3.1.1 and the investment item 47.212 in the draft TYNDP2016. According to the draft TYNDP2016, the NTC increase between Austria and Germany will be 2900 MW (in both directions), if the following internal reinforcements are performed as well:

Upgrade of existing line St. Peter – Salzburg from 220 kV to 380 kV and new double circuit 380 kV line (replacement of the existing 220 kV lines on an optimized route) between Salzburg and Tauern (PCI 3.1.2 & draft TYNDP2016 investment item 47.216)6,

Upgrade of existing 220 kV line Westtirol – Zell-Ziller (105 km) and erection of an additional 220/380 kV transformer (PCI 2.1 & draft TYNDP2016 investment item 47.219),

Upgrade of the existing overhead line between Vöhringen (DE) and Westtirol (AT) to 380 kV (draft TYNDP2016 investment item 47.689).

This group is considered to be a “Mid-term group”, because the forecasted commissioning date of the latest PCI, PCI 3.1.2, is 2023. Figure 3 shows the electrical grid in the region of Group I. The cluster 3.1 contained initially PCI 3.1.3, the upgrade of the 220 kV line between St. Peter and Ernsthofen to 380 kV, but this line is now commissioned.

5 This is an AC line, so it is not directly affected by the recent German legislation giving priority of underground

cabling for new HVDC projects. 6 These internal lines are both necessary to be commissioned to get full advantage of the increase of the

interconnection capacity provided by the cross-border and to establish the 380-kV-Ring in Austria.

EASTNSI/4NT/0512397/000/02 2017 02 16 11/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Figure 3: Regional grid map of Group I (AT-DE), from ENTSO-E Transmission System Map.

2.2.2. Group II (AT/IT) Group II is an interconnection Austria – Italy. It consists mainly in the reconstruction of the existing 220-kV interconnection line as 380-kV line, between Lienz (AT) and the Veneto region (IT), of about 100-150 km (approximately 35 km in Austria, and the rest in Italy), along an optimized route, which minimizes the environmental impact. This project corresponds to the PCI 3.2.1 and the investment item 26.63 in the draft TYNDP2016.

According to the TYNDP2016, the NTC increase will be 1000 MW in the direction Italy → Austria and 1100 MW in the direction Austria → Italy, if the following internal reinforcements are performed as well:

New 380 kV OHL between Lienz and Obersielach (PCI 3.2.2 & draft TYNDP2016 investment item 26.218) with a length of approximately 190 km7,

New 380/220/132 substation at Volpago (draft TYNDP2016 investment item 26.1039).

This group is considered to be a “Mid-term group”, because the forecasted commissioning date of the latest project, PCI 3.2.2, is 2025. Figure 4 shows the electrical grid in the region of Group II.

7 This project is also the last part of the planned 380-kV-Ring, which is the backbone of Austrian electricity supply.

EASTNSI/4NT/0512397/000/02 2017 02 16 12/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Figure 4: Regional grid map of Group II & Group III (AT-IT) , from ENTSO-E Transmission System Map.

2.2.3. Group III (AT/IT) Group III is an interconnection Austria – Italy. It consists mainly in the construction of a new 220 kV AC OHL (merchant line) of 40 km, between Wurmlach/Greuth (AT) and Somplago (IT). It is a third party project (i.e. not promoted by the TSOs) promoted by Alpe Adria Energia SpA. This project corresponds to the PCI 3.4 and the investment item 210.1380 in the draft TYNDP2016. The draft TYNDP2016 indicates additionally that the project includes a 300 MW PST, located in Austria.

According to the draft TYNDP2016, the NTC increase between Austria and Italy will be 150 MW (in both directions) and no internal reinforcement is needed. This group is considered to be a “Short-term group”, because the forecasted commissioning date of PCI 3.4 is 2019. Figure 4 here above shows the electrical grid in the region of Group III.

2.2.4. Group IV (BG/EL) Group IV is an interconnection Bulgaria – Greece. It consists mainly in the construction of a new 400 kV AC OHL (single circuit), between Maritsa East 1 (BG) and N. Santa (EL), with a length of approximately 151 km (29 km in Greece and 122 km in Bulgaria). This project corresponds to the PCI 3.7.1 and the investment item 142.256 in the draft TYNDP2016.

According to the draft TYNDP2016, the NTC increase will be 850 MW in the direction Bulgaria → Greece and 400 MW in the direction Greece → Bulgaria, if the following internal reinforcements are performed as well:

New single circuit 400 kV OHL (in parallel to the existing one) between Maritsa East 1 and Plovdiv (PCI 3.7.2 & draft TYNDP2016 investment item 142.257),

EASTNSI/4NT/0512397/000/02 2017 02 16 13/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

New single circuit 400 kV OHL (in parallel to the existing one) between Maritsa East 1 and Maritsa East 3 (PCI 3.7.3 & draft TYNDP2016 investment item 142.258),

New 400 kV OHL between Maritsa East 1 and Burgas (PCI 3.7.4 & draft TYNDP2016 investment item 142.262).

This group is considered to be a “Mid-term group”, because the forecasted commissioning date of the latest PCIs, PCI 3.7.1 and PCI 3.7.4, is 2021. Figure 5 shows the electrical grid in the region of Group IV.

Figure 5: Regional grid map of Group IV (BG-EL) , from ENTSO-E Transmission System Map.

2.2.5. Group V (BG/RO) Group V consists in increasing the transfer capacity between Bulgaria and Romania (Black Sea Corridor) by performing internal reinforcements in both countries. It corresponds to the PCI project 3.8 and gathers the following PCIs:

New single circuit 400 kV OHL (in parallel to the existing one) of 140 km between Varna and Burgas in Bulgaria (PCI 3.8.1 & draft TYNDP2016 investment item 138.800),

New double circuit 400 kV OHL of 159 km between Cernavoda and Stalpu (with 1 circuit derivation in/out in substation Gura Ialomitei) in Romania (PCI 3.8.4 & draft TYNDP2016 investment item 138.273),

New double circuit 400 kV OHL (one circuit wired) of 137.5 km between Smardan and Gutinas in Romania (PCI 3.8.5 & draft TYNDP2016 investment item 138.275).

According to the draft TYNDP2016, the NTC increase will be 1350 MW in the direction Romania → Bulgaria and 800 MW in the direction Bulgaria → Romania, if the following internal reinforcements are performed as well:

EASTNSI/4NT/0512397/000/02 2017 02 16 14/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

New single circuit 400 kV OHL (139 km) between Suceava and Gadalin in Romania (draft TYNDP2016 investment item 138.276) 8,

Upgrade of the existing 220 kV OHL Stalpu – Teleajen – Brazi to 400 kV (continuation of the line between Cernavoda and Stalpu), and corresponding upgrade of the Stalpu substation (draft TYNDP2016 investment item 138.715).

This group is considered to be a “Mid-term group”, because the forecasted commissioning date of the latest PCI, PCI 3.8.1, is 2022. Figure 6 shows the electrical grid in the region of Group V.

Figure 6: Regional grid map of Group V (BG-RO) , from ENTSO-E Transmission System Map.

8 It corresponded previously to the PCI 3.8.6, but is no longer considered as PCI because the contribution to the NTC

contribution was not enough.

EASTNSI/4NT/0512397/000/02 2017 02 16 15/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2.2.6. Group VI (SI/HU/HR) Group VI is an interconnection Croatia – Hungary – Slovenia. It consists mainly in the connection of the existing substation of Cirkovce (SI) to one circuit of the existing Heviz (HU) – Zerjavinec (HR) double circuit 400 kV OHL by erecting a new 80 km double circuit 400 kV OHL in Slovenia. It will result in two new cross-border circuits: Heviz (HU) – Cirkvoce (SI) and Cirkvoce (SI) – Zerjavenec (HR). This project corresponds to the PCI 3.9.1 and the investment item 141.223 in the draft TYNDP2016.

According to the draft TYNDP2016, the NTC increase will be 1350 MW in the direction Romania → Bulgaria and 800 MW in the direction Bulgaria → Romania., if the existing 220 kV lines of the corridor Divaca-Bericevo-Podlog-Cirkovce in Slovenia are upgraded to 400 kV (PCIs 3.9.2, 3.9.3, 3.9.4 & draft TYNDP2016 investment item 141.225).

This group is considered to be a “Long-term group”, because the forecasted commissioning date of the latest PCIs, PCI 3.9.3 and PCI 3.9.4, is 20269. Note that the commissioning date of PCI 3.9.1 is already 2019, which means that the internal reinforcements needed to reach the expected increase of interconnection capacity is foreseen be commissioned 7 years after the interconnection itself. Figure 7 shows the electrical grid in the region of Group VI.

Figure 7: Regional grid map of Group VI (SI-HU-HR) , from ENTSO-E Transmission System Map.

9 It must be noted that the draft TYNDP2016 considers that the expected commissioning year of that project is 2021

(“on time”), which is contradictory with the PCI implementation fiche.

EASTNSI/4NT/0512397/000/02 2017 02 16 16/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2.2.7. Group VII (IL/CY/EL) Group VII is an interconnection Israel – Cyprus – Greece (Creta and mainland). It is called the “EuroAsia Interconnector”. It consists in two international HVDC interconnections and one national HVDC interconnection:

A new HVDC interconnection (final capacity: 2000 MW) of 330 km between Hadera (Israel) and Vasilikos (Cyprus), corresponding to the PCI 3.10.1 and the draft TYNDP2016 investment item 219.1407,

A new HVDC interconnection (final capacity: 2000 MW) of 880 km between Vasilikos (or Kofiniou) (Cyprus) and Korakia (Creta – Greece), corresponding to the PCI 3.10.2 and the draft TYNDP2016 investment item 219.1409,

A new HVDC interconnection (final capacity: 2000 MW) of 310 km between Korakia (Creta) and Athens in Greece, corresponding to the PCI 3.10.3 and the draft TYNDP2016 investment item 219.1410.

According to the draft TYNDP2016, the NTC increase will be 2000 MW (in both directions). However, the anticipated deployment of the complete HVDC system is divided of two stages: the first stage aims at having a capacity of 1000 MW on the axis Israel – Cyprus – Greece (Creta and mainland), while the second stage will allow to reach a capacity of 2000 MW. The first stage is anticipated to be completed in four steps:

Step 1: interconnection of Israel and Cyprus by an HVDC power transmission system of 500 MW (converter stations of 500 MW, but a pair of cables for a capacity up to 1000 MW),

Step 2 : interconnection of Attica and Crete by an HVDC power transmission of 1000 MW,

Step 3: upgrade of the HVDC power transmission system between Israel and Cyprus to 1000 MW (upgrade of converter stations),

Step 4: interconnection of Crete and Cyprus by an HVDC power transmission of 1000 MW.

This group is considered to be a “Mid-term group”, because the forecasted commissioning date of the second stage of the latest PCI, PCI 3.10.2, is 2022. Figure 8 shows the electrical grid in the region of Group VII.

EASTNSI/4NT/0512397/000/02 2017 02 16 17/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Figure 8: Regional grid map of Group VII (IL-CY-EL) , from ENTSO-E Transmission System Map.

2.2.8. Group VIII (CZ/DE) Group VIII consists in increasing the transfer capacity between the Czech Republic and Germany (Czech North South Corridor) by performing internal reinforcements in Czech Republic. It corresponds to the PCI project 3.11 and gathers the following PCIs:

New 400 kV substation in Vítkov with 400/110kV transformers (in addition to the existing 220 kV substation), new 400 kV substation in Vernerov with 400/110kV transformers, and new double circuit 400 kV OHL of 75 km between Vernerov and Vitkov (PCI 3.11.1 & draft TYNDP2016 investment items 200.306, 200.307 and 200.308),

New double circuit 400 kV OHL of 86 km between Vitkov and Prestice (PCI 3.11.2 & draft TYNDP2016 investment item 200.309),

Extension and upgrade of the existing substation 400/110kV in Kocin, and addition of a second circuit of 115.8 km to an existing single circuit 400 kV line between Prestice and Kocin (PCI 3.11.3 & draft TYNDP2016 investment items 35.311 and 35.315),

Extension and upgrade of the existing substation 400/110kV in Mirovka and new double circuit 400 kV OHL of 26.5 km between Kocin and Mirovka (PCI 3.11.4 & draft TYNDP2016 investment items 200.312 and 35.313),

New double circuit 400 kV OHL between Mirovka and the substation “V413” in Czech Republic (draft TYNDP2016 investment item 200.314),

Addition of a second circuit to an existing single circuit 400 kV line of 88.5 km between Mirovka and Cebin (PCI 3.11.5 & draft TYNDP2016 investment item 35.316).

According to the draft TYNDP2016, the NTC increase between the Czech Republic and Germany should be 500 MW (in both directions).

This group is considered to be a “Long-term group”, because the forecasted commissioning date of the latest PCI, PCI 3.11.5, is 2029. Figure 9 shows the electrical grid in the region of Group VIII.

EASTNSI/4NT/0512397/000/02 2017 02 16 18/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Figure 9: Regional grid map of Group VIII (CZ-DE) , from ENTSO-E Transmission System Map.

2.2.9. Group IX (DE/PL) Group IX is an interconnection Germany – Poland (GerPol Power Bridge).This project was completely redefined in the draft TYNDP2016 compared to the TYNDP2014 and is now called “GerPol Power Bridge II” (project 229 of the draft TYNDP2016). It consists in the following investments:

Construction of new 400/220kV substations in Zielona Góra and in Gubin, with PSTs (draft TYNDP2016 investment items 229.1272 and 229.1274),

Indentation to the double circuit 400 kV line Baczyna – Plewiska to form the new routes Baczyna – Zielona Góra and Zielona Góra – Plewiska (draft TYNDP2016 investment items 229.1270 and 229.1271),

New double circuit 400 kV between Zielona Góra and Gubin (draft TYNDP2016 investment item 1273),

New double circuit 400 kV cross-border line between Gubin (PL) and Eisenhuettenstadt (DE) (draft TYNDP2016 investment item 1275),

According to the draft TYNDP2016, these investments correspond functionally to PCI 3.14.1, and the NTC increase in 2030 will be 1500 MW in the direction Poland → Germany and 0 MW in the direction Germany → Poland.

This group is considered to be a “Long-term group”, because the forecasted commissioning date of the latest PCI, PCI 3.14.1, is 2030. Figure 10 shows the electrical grid in the region of Group IX.

EASTNSI/4NT/0512397/000/02 2017 02 16 19/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Figure 10: Regional grid map of Group IX (DE-PL) , from ENTSO-E Transmission System Map.

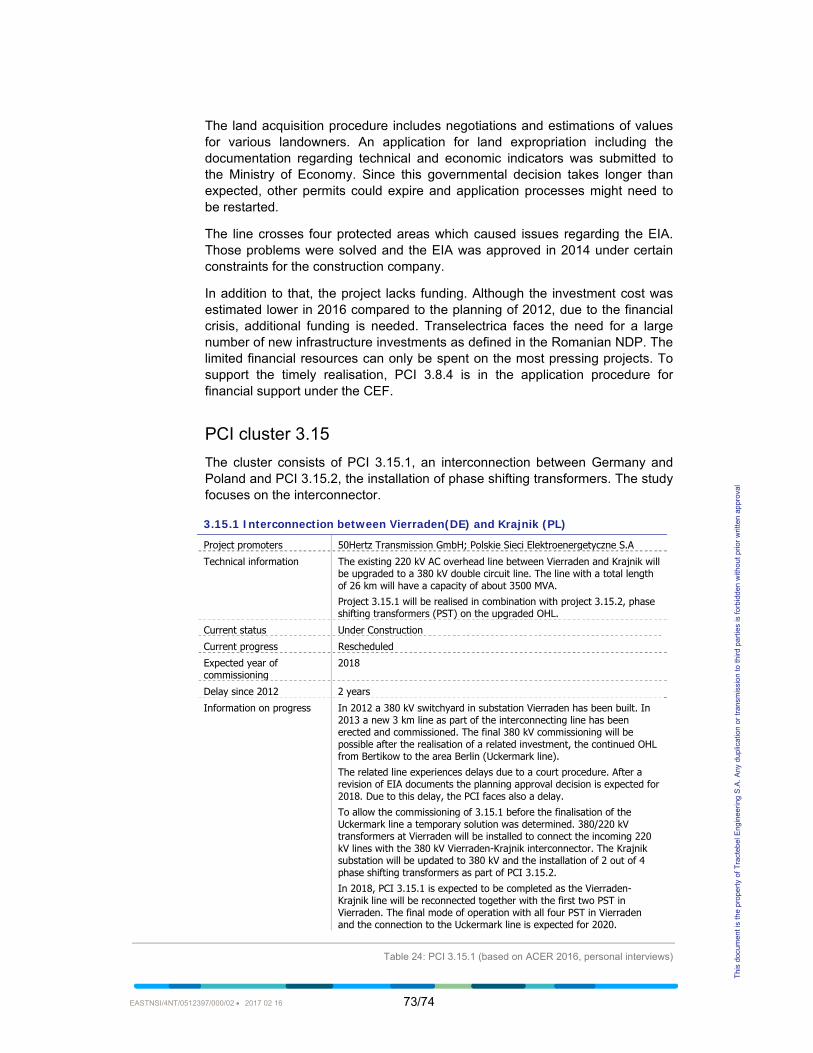

2.2.10. Group X (DE/PL) Group X is an interconnection Germany – Poland (GerPol Improvements). It consists mainly in the upgrade of the existing 220 kV line of 26 km between Vierraden and Krajnik to a double circuit 380 kV OHL10. In addition, the Krajnik substation must be upgraded. This project corresponds to the PCI 3.15.1 and the draft TYNDP2016 investment items 94.139 and 94.796.

According to the draft TYNDP2016, the NTC increase between Germany and Poland will be 1500 MW in the direction Poland → Germany and 500 MW in the direction Germany → Poland, if Phase Shifter Transformers (PSTs) are installed in Vierraden and in Mikulowa (PCI 3.15.2 & draft TYNDP2016 investment items 94.992 and 94.799). Indeed, the existing 220 kV line between Vierraden and Krajnik could be switched to 400 kV only after the PSTs have been installed on both existing interconnectors.

10 This is an AC line, so it is not directly affected by the recent German legislation giving priority of underground

cabling for new HVDC projects.

EASTNSI/4NT/0512397/000/02 2017 02 16 20/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

This group is considered to be a “Short-term group”, because the forecasted commissioning date of the latest PCIs, PCI 3.15.1 and PCI 3.15.2, is 2017, according to the latest PCI fiches (June 2016). However, the draft TYNDP2016 indicates that delays are expected on several investment items. If the PSTs are already installed in Mikulowa (June 2016), the upgrade of the line between Vierraden and Krajnik and the commissioning of PSTs in Vierraden is postponed to 2018, due to permit granting reasons on 50Hertz side. Moreover, the upgrade of the Krajnik substation is rescheduled to 2020. The overall project is thus planned to operate in final shape by 2020. Figure 11 shows the electrical grid in the region of Group X.

Figure 11: Regional grid map of Group X (DE-PL) , from ENTSO-E Transmission System Map.

2.2.11. Group XI (SK/HU) Group XI is a double interconnection Hungary – Slovakia (New SK-HU interconnection – phase 1). It consists mainly in a new double circuit 400 kV line of between Gabcikovo (SK) and Gonyu (HU) and a new double circuit 400 kV line between Rimavska Sobota (SK) and Sajoivanka. This double project corresponds to PCIs 3.16 and 3.17 and to the draft TYNDP2016 investment items 48.214 and 48.695. They are grouped together because they are co-dependent. PCI 3.16 includes also the erection of a new switching station Gabcikovo next to the existing one.

According to the draft TYNDP2016, the NTC increase will be 2400 MW in the direction Slovakia → Hungary and 950 MW in the direction Hungary → Slovakia, if the following internal reinforcement is performed as well:

Installation of a second 400/120 kV transformer and 2×70 MVAr shunt reactors in station Sajoivanka (draft TYNDP2016 investment items 48.696 and 48.697).

EASTNSI/4NT/0512397/000/02 2017 02 16 21/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

This group is considered to be a “Short-term group”, because the forecasted commissioning date of the latest PCIs, PCI 3.16.1, PCI 3.16.3 and PCI 3.17, is 2018. However, according to the draft TYNDP2016, the expected commissioning date is now 2019. Figure 12 shows the electrical grid in the region of Group XI.

Figure 12: Regional grid map of Group XI (SK-HU) , from ENTSO-E Transmission System Map.

2.2.12. Group XII (SK/HU) Group XII is an interconnection Hungary – Slovakia (New SK-HU interconnection – phase 2). It consists in a new double circuit 400 kV line between Kisvarda area (HU) and Velké Kapusany (SK). This project corresponds to the PCI 3.18.1 and to the draft TYNDP2016 investment item 54.720.

According to the draft TYNDP2016, the NTC increase will be 300 MW in the direction Hungary → Slovakia and 250 MW in the direction Slovakia → Hungary.

This group is considered to be a “Mid-term group”, because the initial forecasted commissioning date of PCI 3.18.1 was 2021, according to the PCI fiche of October 2015. However, the draft TYNDP2016 and the latest PCI fiche (June 2016) indicate that this project is rescheduled to 2029. Figure 13 shows the electrical grid in the region of Group XII.

Figure 13: Regional grid map of Group XII (HU-SK) , from ENTSO-E Transmission System Map.

EASTNSI/4NT/0512397/000/02 2017 02 16 22/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2.2.13. Group XIII (IT/ME) Group XIII is an interconnection Italy – Montenegro. It consists mainly in a new 1200MW 500kV HVDC subsea interconnection cable of 375 km between Villanova (IT) and Lastva (ME) and corresponding converter stations. This project corresponds to the PCI 3.19.1 and draft TYNDP2016 investment item 28.70.

According to the draft TYNDP2016, the NTC increase between Italy and Montenegro will be 1200 MW (in both directions), if a new 400 kV substation in Lastva is constructed and connected to the existing 400 kV line between Podgorica 2 (ME) and Trebinje (BA) (draft TYNDP2016 investment item 28.624).

This group is considered to be a “Short-term group”, because the forecasted commissioning date of PCI 3.19.1 is 2018. Figure 14 shows the electrical grid in the region of Group XIII.

Figure 14: Regional grid map of Group XIII (IT-ME) , from ENTSO-E Transmission System Map.

2.2.14. Group XIV (IT/SI) Group XIV is an interconnection Italy – Slovenia. It consists in a new HVDC underground cable with a length of about 150-200 km between Salgareda (IT) and Divaca-Bericevo region (SI) with a capacity of 1000 MW. This project corresponds to the PCI 3.21 and the draft TYNDP2016 investment item 150.616.

According to the draft TYNDP2016, the NTC increase between Italy and Slovenia will be 950 MW in both directions Additionally, PCI 3.21 is highly dependent on the realization of Cluster 3.9 (part of Group VI): PCIs 3.9.1 and 3.9.2 will be necessary to get full advantage of the increase of the interconnection capacity provided by the cross-border line11.

This group is considered to be a “Mid-term group”, because the forecasted commissioning date of PCI 3.21 is 2022. Figure 15 shows the electrical grid in the region of Group XIV.

11 Note that PCIs 3.9.1 and 3.9.2 should be commissioned in 2019 and 2021, respectively, so before PCI 3.21.

EASTNSI/4NT/0512397/000/02 2017 02 16 23/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Figure 15: Regional grid map of Group XIV (IT-SL) , from ENTSO-E Transmission System Map.

2.2.15. Group XV (RO/RS) Group XV is an interconnection Romania – Serbia (Mid-Continental East corridor). It consists mainly in a new double circuit 400 kV OHL of 131 km (63 km on Romanian side and 68 km on Serbian side) between Resita (RO) and Pancevo (RS). This project corresponds to the PCI 3.22.1 and the draft TYNDP2016 investment item 144.238.

According to the draft TYNDP2016, the NTC increase between Romania and Serbia will be will be 950 MW in the direction Romania → Serbia and 750 MW in the direction Serbia → Romania:

New 400 kV substation at Resita and new 400 kV OHL of 116 km between Portile de Fer and Resita in Romania (PCI 3.22.2 & draft TYNDP2016 investment items 144.701 and 144.269),

Upgrade of existing double circuit 220 kV lines Resita-Timisoara-Sacalaz-Arad to double circuit 400 kV lines and replacement of the 220 kV Timisoara substation with 400 kV substation in Romania (PCIs 3.22.3 and 3.22.4 & draft TYNDP2016 investment items 144.270 and 144.705).

This group is considered to be a “Mid-term group”, because the forecasted commissioning date of the latest PCIs, PCI 3.22.3 and PCI 3.22.4, is 2022. Figure 16 shows the electrical grid in the region of Group XV.

EASTNSI/4NT/0512397/000/02 2017 02 16 24/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Figure 16: Regional grid map of Group XV, from ENTSO-E Transmission System Map.

2.3. CBA of interconnection projects

This section provides a synthesis of costs and benefits of groups of interconnection projects listed in the previous section estimated by the draft TYNDP2016. For this analysis, Vision 3 is chosen as a reference, but main results are also given for the others visions. In the TYNDP 2016, the Net Present Value (NPV) is estimated from the cost and the yearly benefit of each project. In accordance with “ENTSO-E Guidelines for Cost Benefit Analysis of Grid Development Projects”, a real discount rate of 4% for 25-year lifetime and a residual value equal to zero were used.

Note that the CBA is performed on each group defined in the previous section, in its entirety (including internal reinforcements), and not on individual PCIs12. Indeed, a PCI alone cannot be used to its full potential without the adequate internal reinforcements that are included in its group. For the sake of clarity, interconnection groups are divided in the three temporal categories according to their implementation schedule, using as a reference the commissioning dates of the PCI fiches (in line with the methodology reported in the previous section): short-term, mid-term and long-term groups.

12 Note that, in order to become a PCI, a project must contribute also significantly to sustainability and security of

supply, according to the TEN-E Regulation, Art. 4.2. These benefits are not entirely captured by the SEW indicator used in the ENTSO- E methodology and they need a separate evaluation.

EASTNSI/4NT/0512397/000/02 2017 02 16 25/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2.3.1. Short-term groups Table 3 shows the CBA of short-term groups according to the draft TYNDP2016, using Vision 3 for the annual benefits, the NPV and the IRR.

The impact on the Socio-Economic Welfare (SEW) of Group III and of Group XI is negligible, but their costs are low. Therefore, their NPVs are around zero. On the contrary, Group X and Group XI increase significantly the SEW and display globally high NPVs and IRRs. Their NPVs are in a similar range. However, Group X has a low cost (85 M€) and annual benefits are only slightly lower than this cost. Therefore, the IRR is huge (more than 70%). On the contrary, Group XIII has a high cost (more than €1 billion) and annual benefits much smaller than this cost (between 100 M€ and 200 M€). It entails an IRR much lower, between 5% and 15%.

Group ID Cost (M€) Annual benefits (M€/year)

NPV (M€) IRR (%)

III (AT/IT) 60 [0,10] [-60,96] ]-∞,16.3]

X (DE/PL) 85 [60,80] [852,1165] [70.6,94.1]

XI (SK/HU) [74,90] [0,10] [-90,82] ]-∞,12.9]

XIII (IT/ME) [1181,1311] [100,181] [251,1631] [5.7,14.8]

Table 3: Economic Analysis of Short-Term Interconnection Groups, draft TYNDP2016 Vision 3

Table 4 shows the annual benefits and the NPVs for Vision 1, Vision 2 and Vision 4. Groups III and XI are not really sensitive to the load/generation vision: theirs NPVs stay close to 0 in each case. Group X displays a higher sensitivity, but the NPV stays very much positive for each vision. Group XIII is very sensitive: if the NPV is between €251 million and €1.9 billion for Vision 2, it is between €-1 billion and €381 million for Vision 4.

Group ID Annual benefits – V1

(M€/year)

NPV – V1 (M€)

Annual benefits – V2

(M€/year)

NPV – V2 (M€)

Annual benefits – V4

(M€/year)

NPV – V4 (M€)

III (AT/IT) [0,10] [-60,96] [0,20] [-60,252] [0,10] [-60,96]

X (DE/PL) [180,200] [2727,3039] [120,160] [1790,2415] [60,80] [852,1165]

XI (SK/HU) [0,10] [-90,82] [0,10] [-90,82] [0,10] [-90,82] XIII (IT/ME) [90,190] [95,1787] [100,200] [251,1943] [20,100] [-999,381]

Table 4: Economic Analysis of Short-Term Interconnection Groups, draft TYNDP2016 Visions 1, 2 & 4

2.3.2. Mid-term groups Table 5 shows the CBA of mid-term groups according to the draft TYNDP2016, using Vision 3 for the annual benefits, NPV and IRR.

EASTNSI/4NT/0512397/000/02 2017 02 16 26/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Groups II, IV, XIV and XV display negative NPV: the annual benefits they bring are low compared to their cost. The annual benefits of Group V are moderate, which leads to a low but positive NPV. Group I displays NPV of several billions of Euros, but there is an important relative uncertainty on annual benefits. Finally, Group VII leads to a huge NPV, between €9 billion and €14 billion. Nevertheless, it must be noted that no details about the origin of the high benefits computed by ENTSO-E is given in the TYNDP.

Group ID Cost (M€) Annual benefits (M€/year)

NPV (M€) IRR (%)

I (AT/DE) [1000,1500] [150,270] [843,3218] [8.8,26.9]

II (AT/IT) [615,815] [0,40] [-815,10] ]-∞,4.2]

IV (BG/EL) [178,198] [0,10] [-198,-22] ]-∞,2.8]

V (BG/RO) [258,338] [30,50] [131,523] [7.4,19.1]

VII (IL/CY/EL) 4247 [860,1160] [9188,13875] [20.0,27.2]

XIV (IT/SI) 870 [10,30] [-714,-401] [-7.9,-1.1]

XV (RO/RS) [151,201] [0,10] [-201,5] ]-∞,4.3]

Table 5: Economic Analysis of Mid-Term Interconnection Groups, draft TYNDP2016 Vision 3

Table 6 shows the annual benefits and the NPVs for Vision 1, Vision 2 and Vision 4. The sensitivity to the load/generation vision is low for Group II and Group VII. Group I displays NPVs around 0 but with a large variance for Vision 1 and Vision 2, but high NPVs for Vision 3 and Vision 4. Group IV displays NPVs around 0 for Vision 1 and Vision 3, but a NPV of several hundreds of M€ for Vision 2 and around €1 billion for Vision 4. Group V displays NPV constantly positive, but ranging from €131 million to around €4.6 billion. Group XIV has positive NPVs for Vision 1 and Vision 2, but negative NPVs for Vision 3 and Vision 4. Finally, Group XV displays positive NPVs, except for Vision 3, where the NPV is around 0.

Group ID Annual benefits – V1

(M€/year)

NPV – V1 (M€)

Annual benefits – V2

(M€/year)

NPV – V2 (M€)

Annual benefits – V4

(M€/year)

NPV – V4 (M€)

I (AT/DE) [60,100] [-563,562] [20,160] [-1188,1500] [110,250] [218,2906]

II (AT/IT) [20,40] [-503,10] [10,50] [-659,166] [0,20] [-815,-303] IV (BG/EL) [10,20] [-42,134] [20,40] [114,447] [60,100] [739,1384] V (BG/RO) [70,90] [756,1148] [40,60] [287,679] [230,310] [3255,4585]

VII (IL/CY/EL) [560,760] [4501,7626] [490,670] [3408,6220] [1050,1290] [12156,15905] XIV (IT/SI) [60,120] [67,1005] [80,140] [380,1317] [10,30] [-714,-401] XV (RO/RS) [80,100] [1049,1411] [50,70] [580,943] [50,70] [580,943]

Table 6: Economic Analysis of Mid-Term Interconnection Groups, draft TYNDP2016 Visions 1, 2 & 4

2.3.3. Long-term groups Table 7 shows the CBA of long-term groups according to the draft TYNDP2016, using Vision 3 for the annual benefits, the NPV and the IRR. Economic benefits brought by Group VI are low compared to its cost and its NPV is negative. Benefits brought by Group XII are also small, but given its low cost, it leads to a NPV around 0. The annual benefits brought by Group VIII are also much lower, but it leads nevertheless to a NPV of several hundreds of M€. Finally, Group IX has a moderate cost and brings important annual benefits compared to that cost (approximately the half). Consequently, its NPV is around €1 billion and the IRR is of several tens of percent.

EASTNSI/4NT/0512397/000/02 2017 02 16 27/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Group ID Cost (M€) Annual benefits (M€/year)

NPV (M€) IRR (%)

VI (SI/HU/HR) 345 [0,20] [-345,-33] ]-∞,3.1]

VIII (CZ/DE) [231,347] 40 [278,394] [10.6,17.0]

IX (DE/PL) [150,250] [70,90] [844,1256] [27.9,60.0]

XII (SK/HU) [57,69] [0,10] [-69,99] ]-∞,17.2]

Table 7: Economic Analysis of Long-Term Interconnection Groups, draft TYNDP2016 Vision 3

Table 8 shows the annual benefits and the NPV for Vision 1, Vision 2 and Vision 4. Group VI is quite sensitive on the Vision: benefits are much higher for Vision 1 and Vision 2 than for Vision 3 and Vision 4. It is the opposite for Group VIII and Group IX: benefits are lower in Vision 1 and in Vision 2. Finally, Group XII is insensitive to the load/generation vision.

Group ID Annual benefits – V1

(M€/year)

NPV – V1 (M€)

Annual benefits – V2

(M€/year)

NPV – V2 (M€)

Annual benefits – V4

(M€/year)

NPV – V4 (M€)

VI (SI/HU/HR) [70,90] [749,1061] [70,90] [749,1061] [20,40] [-33,280]

VIII (CZ/DE) [10,30] [-191,238] 20 [-35,81] [40,60] [278,706] IX (DE/PL) [0,10] [-250,6] [0,10] [-250,6] [90,130] [1156,1881] XII (SK/HU) [0,10] [-69,99] [0,10] [-69,99] [0,10] [-69,99]

Table 8: Economic Analysis of Long-Term Interconnection Groups, draft TYNDP2016 Visions 1, 2 & 4

2.4. Analysis of interconnection levels

Table 9 shows the current interconnection levels (2016) of the 13 countries of the NSI East electricity corridor the interconnection levels that they will have in 2020 if no additional interconnection is developed and the additional export capacity needed to reach the 10% target in 2020. Numbers are taken from the 2015 ENTSO-E “Scenario Outlook & Adequacy Forecast”. Five countries/regions are expected to be below this target in 2020 with their current export capacity: Cyprus, Germany, Italy, Poland and Romania. If small increases of export capacity (less than 1 GW) are sufficient for Cyprus and Romania to reach the target, large increases are needed for Poland, Germany and Italy (approximately 2.7 GW, 5 GW and 7 GW).

EASTNSI/4NT/0512397/000/02 2017 02 16 28/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Country

Current export

capacity (GW)

Current generating

capacity (GW)

Current interconnection

level (%)

2020 generating

capacity (GW)

2020 interconnection

level if no change (%)

Additional export capacity needed to reach 10% in

2020 (GW) AT 7 25 28.0 28 25.0 0

BG 1.6 13.7 11.7 12.9 12.4 0 CY 0 1.7 0.0 1.9 0.0 0.2 CZ 5.5 21.5 25.6 20.2 27.2 0 DE 15.6 195.5 8.0 215.1 7.3 5.9 EL 1.9 17.8 10.7 18.9 10.1 0 HR 2.6 4.7 55.3 5.8 44.8 0 HU 2.5 8 31.3 9.4 26.6 0 IT 4.5 122.1 3.7 122.9 3.7 7.8 PL 1.6 37.9 4.2 42.9 3.7 2.7 RO 2.5 21.1 11.8 25.3 9.9 0.1 SI 3.2 3.6 88.9 4.1 78.0 0 SK 2.7 7.6 35.5 8.6 31.4 0

Table 9: Analysis of interconnection levels in 2016 and in 202013

2.5. Ranking of groups

The ranking of groups focuses on short-term and mid-term projects and is based on the following criteria:

The CBA of each group, as presented in the previous section (average value and range of the NPV),

The role of the projects in achieving the EC 10% target of interconnection for each country,

The investment costs (expensive projects are less likely to be developed in priority),

The risks in terms of environment or public acceptance, due to the main characteristics of the project: overhead line or underground cable (the specific impact of the project on the environment is not studied).

13 Note that, for some countries, the expected generating capacity in 2020 is less than the 2016 value (e.g. BG, CZ),

or only slightly higher (e.g. IT). It is due to a decommissioned capacity larger than the expected new capacity.

EASTNSI/4NT/0512397/000/02 2017 02 16 29/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

2.5.1. Short-term groups Among short-term groups, Group X (IT/ME) and Group XIII (IT/ME) have quasi-constantly positive economic indicators. An exception occurs for Group XIII in draft TYNDP2016 Vision 4. Group X will increase by 1.5 GW the interconnection level of Poland and by 0.5 GW the interconnection level of Germany which are foreseen to be below the 10% target at 2020 horizon. The investment cost is moderate (around €150 million), which implies that the financial risk is small, and the environmental impact is small (upgrade of an existing line and addition of PSTs in existing substations). Even if its investment cost is much higher than other projects (around €1 billion), Group XIII will increase significantly the interconnection level of Italy (by 1-1.2 GW) which is well below the 10% target, and, because it consists mainly in an undersea HVDC cable, no major public opposition is expected. Therefore, because economic indicators are systematically positive for Group X and these groups are equivalent on others aspects, Group X is ranked number 1 and Group XIII is ranked number 2.

The two remaining groups, Group III (AT/IT) and Group XI (SK/HU) bring small annual benefits, which leads to unclear economic indicators: in some cases, theirs NPVs are positive, but, in others cases, they are negative. Group III does not bring a positive NPV, its cost is low and it helps to increase the interconnection level of Italy. Group XI (SK/HU) has a moderate investment cost (around €100 million) and does not increase the interconnection level of countries below the 10% target. Moreover, it will have a non-negligible environmental impact (new overhead line) and it could suffer from public opposition. Therefore, Group III is ranked number 3 and Group XI is ranked number 4.

Rank Group ID

1 X (DE/PL)

2 XIII (IT/ME) 3 III (AT/IT) 4 XI (SK/HU)

Table 10: Ranking of Short-Term Interconnection Groups

2.5.2. Mid-term groups Among mid-term groups, Group IV (BG/EL) and Group V (BG/RO) have usually high NPVs and moderate investment costs. Group V has a systematically positive NPV (which is not the case for Group V) and has a positive impact on the interconnection level of Romania, expected to be slightly below the 10% in 2020 without any new interconnection. These two groups are however expected to have significant environmental impacts: new OHL are built on several hundreds of kilometres. Therefore, despite an investment cost slightly higher for Group V, the latter is ranked number 5 and Group IV is ranked number 6.

Among remaining groups, Group I (AT/DE) increases significantly (by 2.3 GW) the interconnection level of Germany, which is foreseen to be below the 10% target at 2020 horizon. Moreover, it is the only one to have both good economic indicators and a significant contribution on the export capacity of a country needing a large increase of its interconnection level. Despite a significant investment cost (around €1 billion) and non-negligible environmental impact

EASTNSI/4NT/0512397/000/02 2017 02 16 30/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

(new overhead lines), this group is thus ranked number 7. Note that Germany is part of three others priority electricity corridors, the “Northern Seas Offshore Grid” and the “North-South Electricity Interconnections in Western Europe”, and the “BEMIP” electricity corridors: others PCIs not analysed in this report can help to increase the interconnection level of Germany.

Two groups with quasi-consistently positive NPVs remain: Group VII (IL/CY/EL) and Group XV (RO/RS). Group XV has a moderate investment cost (between €130-220 million), a non-negligible environmental impact (new overhead lines) and is ranked number 8. Group VII should have a positive NPV but could display a negative NPV under some circumstances and its investment cost is important. Moreover, the benefits will strongly rely on the exchanges with a third-party country, Israel, and thus on its energy mix evolution, which is quite uncertain from a European point of view. Therefore, it is ranked number 9. Note that the CBA was performed for the 2000 MW version, after completion of stage 2 of this EuroAsia interconnector. The CBA of stage 1 only could be better, because the benefits of an increase of the interconnection capacity between different regions are usually higher when the existing interconnection capacity is low. The two remaining groups, Group II (AT/IT) and Group XIV (IT/SI), display negative NPV in Vision 3 and are thus not ranked. Note that Group II has an average NPV negative in all Visions, while Group XIV brings significant economic benefits (and thus a positive NPV) in Vision 1 and in Vision 2.

Rank Group ID

5 V (BG/RO)

6 IV (BG/EL) 7 I (AT/DE) 8 XV (RO/RS) 9 VII (IL/CY/EL)

Not ranked II (AT/IT), XIV (IT/SI)

Table 11: Ranking of Mid-Term Interconnection Groups

2.6. Conclusions

This section aimed at synthetizing the CBA analyses proposed by ENTSO-E in the draft TYNDP2016 for all PCI projects allowing for increasing transfer capacities between the countries (i.e. while excluding projects with a purely national scope -e.g. internal grid reinforcements in Germany, despite having a significant cross border benefit, or storage projects) in South-East and Central-East regions. For the 13 Member States studied in this project, 38 PCIs leading to an increase of cross-border transfer capacities were considered, while being grouped into 15 groups of interdependent projects

EASTNSI/4NT/0512397/000/02 2017 02 16 31/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

The draft TYNDP 2016 showed that most of the projects foreseen at short-term and mid-term time horizons have a positive Net Present Value (under the assumption of considering a real discount rate of 4% for 25-year lifetime and a residual value equal to zero). Such a positive NPV is moreover quite robust to the load-generation visions considered. This means that these projects will lead to an increase of social welfare in the South East and Central-East Regions. This increase of Social Welfare can be explained by a better use of Renewable Energy Sources (reduction of curtailment)14 within the countries and by an optimized economic dispatch resulting from the increase of transfer capacities.

Moreover, a lot of these projects allow for increasing the level of electricity interconnections of countries which do not currently meet the objective of least 10% of their installed production capacity. This is especially the case of projects

at Polish borders (Germany-Poland: Groups IX and X) at Romanian borders (Bulgaria Romania: Group V) at Italian borders (Austria-Italy: Groups II and III but also Italy-Slovenia:

Group XIV and Italy-Montenegro: Group XIII) at Cyprus borders (Greece-Cyprus-Israel: Group VII) Regarding the long-term projects, the ranges of expected NPVs for these projects are quite large. Because they evolve in an uncertain environment (i.e. the evolution of the load and the generation mix during the decade 2020-2030 is highly uncertain), it is difficult to assess their exact role in the future European system. These projects are discussed in section 4 dedicated to the assessment of further integration. The question of internal constraints in Germany and in Italy is also discussed in this fourth section. But before assessing the options for further integration of South East and Central-East Regions, the next section aims at analysing the barriers for implementation of short-term and long-term PCI projects and at proposing recommendations for mitigating these barriers.

14 Note that the reduction of RES curtailment is not directly included as such in the SEW, but it avoids the use of

more expensive generation (i.e. RES have a quasi-null marginal cost while classical units have a non-negligible marginal cost) and, thus, leads to a lower generation cost.

EASTNSI/4NT/0512397/000/02 2017 02 16 32/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

3. ANALYSIS OF BARRIERS AND CORRESPONDING RECOMMENDATIONS

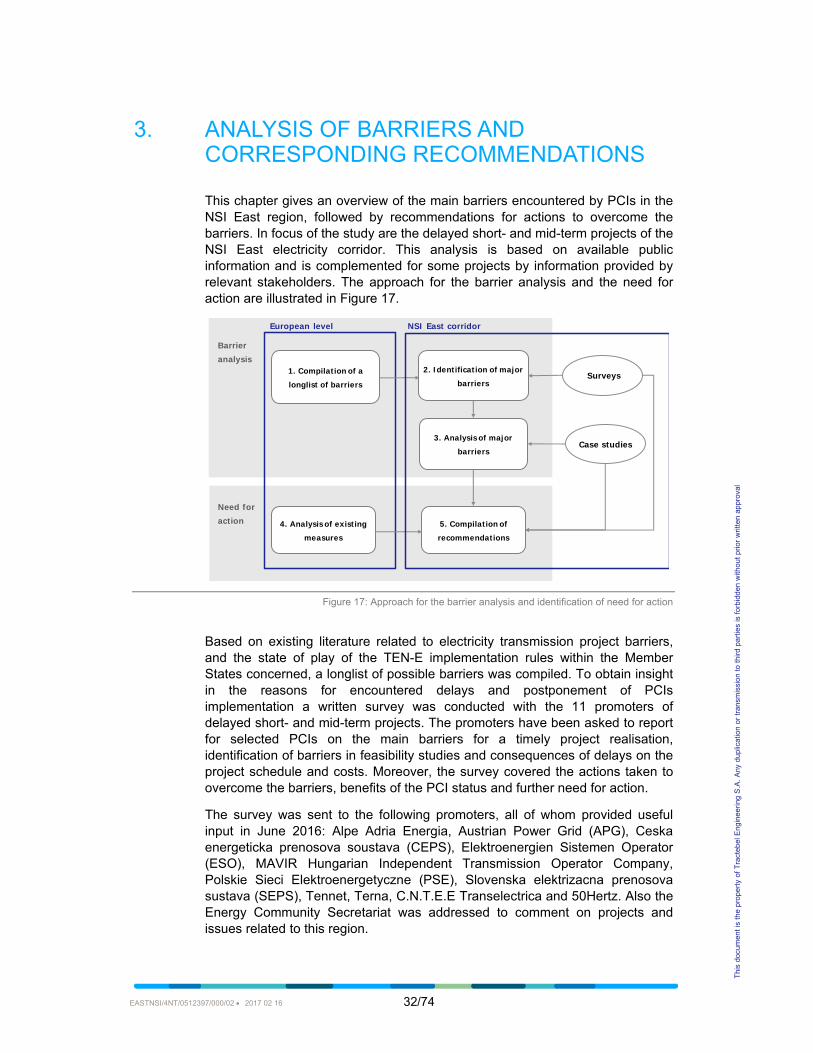

This chapter gives an overview of the main barriers encountered by PCIs in the NSI East region, followed by recommendations for actions to overcome the barriers. In focus of the study are the delayed short- and mid-term projects of the NSI East electricity corridor. This analysis is based on available public information and is complemented for some projects by information provided by relevant stakeholders. The approach for the barrier analysis and the need for action are illustrated in Figure 17.

Figure 17: Approach for the barrier analysis and identification of need for action

Based on existing literature related to electricity transmission project barriers, and the state of play of the TEN-E implementation rules within the Member States concerned, a longlist of possible barriers was compiled. To obtain insight in the reasons for encountered delays and postponement of PCIs implementation a written survey was conducted with the 11 promoters of delayed short- and mid-term projects. The promoters have been asked to report for selected PCIs on the main barriers for a timely project realisation, identification of barriers in feasibility studies and consequences of delays on the project schedule and costs. Moreover, the survey covered the actions taken to overcome the barriers, benefits of the PCI status and further need for action.

The survey was sent to the following promoters, all of whom provided useful input in June 2016: Alpe Adria Energia, Austrian Power Grid (APG), Ceska energeticka prenosova soustava (CEPS), Elektroenergien Sistemen Operator (ESO), MAVIR Hungarian Independent Transmission Operator Company, Polskie Sieci Elektroenergetyczne (PSE), Slovenska elektrizacna prenosova sustava (SEPS), Tennet, Terna, C.N.T.E.E Transelectrica and 50Hertz. Also the Energy Community Secretariat was addressed to comment on projects and issues related to this region.

1. Compilation of a

longlist of barriers

European level NSI East corridor

2. Identification of major

barriers

3. Analysis of major

barriers

5. Compilation of

recommendations

4. Analysis of existing

measures

Barrier

analysis

Need for

action

Surveys

Case studies

EASTNSI/4NT/0512397/000/02 2017 02 16 33/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

As an outcome of the survey evaluation, major barriers in the NSI East region were identified. To gain further insight into those barriers three projects were selected for further review in the form of case studies. For the review of these case studies a number of relevant parties were contacted via in-depth telephone interviews. These interviews covered topics, related to a specific PCI as well as to PCI implementation experiences in general. The interviews covered the status and recent progress of the PCIs, detailed information on the projects specific barriers as well as barriers related to the PCI implementation and further need for action.

The interviews were conducted with representatives of the following organisations during August/September 2016: Alpe Adria Energia, Autorita Energia, Bundesnetzagentur, E-Control, ESO, Nature And Biodiversity Conservation Union (NABU), Transelectrica and 50Hertz.

The feedback of the survey, the interviews and own analysis of existing measures to overcome the barriers resulted in a proposal for actions to further facilitate PCI implementation in the NSI East region. These recommendations are given in Chapter 3.5.

A first outcome of the barrier analysis and survey feedback was presented to the NSI East Regional Group in October 2016, with the opportunity for all members to provide additional views in writing.

While the longlist of barriers and the existing measures are regarded on a European level, the analysis of barriers and the respective recommendations refer in particular to the NSI East region.

3.1. Overview of delayed PCIs

A first overview focuses on all PCIs analysed in Chapter 2. The current project status (under consideration, planned but not yet in permitting, permitting, under construction) as well as the current progress (on time, rescheduled, delayed) were identified for those 38 projects on the list as seen in Table 12. The ACER 2015 PCI implementation monitoring report is taken as reference as it makes a comparison with 2012 which represents the development since the entry into force of Regulation (EU) 347/2013.

Current status Progress over the past years

Total

On time Rescheduled Delayed

Under consideration 1 2 - 3

Planned, but not yet in permitting

11 2 1 14

Permitting 6 4 9 19

Under construction - 1 1 2

Total 18 9 11 38

Table 12: Comparison of status (2015) and progress (2012 to 2015) for PCIs in the region (based on ACER 2015)

EASTNSI/4NT/0512397/000/02 2017 02 16 34/74

This

doc

umen

t is

the

prop

erty

of T

ract

ebel

Eng

inee

ring

S.A

. Any

dup

licat

ion

or tr

ansm

issi

on to

third

par

ties

is fo

rbid

den

with

out p

rior w

ritte

n ap

prov

al

Out of the 38 PCIs in focus, 18 projects were on time, 9 had been rescheduled and 11 were delayed. Looking at the current progress, one can distinguish between the projects in planning phase (under consideration, planned but not yet in permitting) and execution phase (permitting, under construction). 17 out of the 38 PCIs are still in planning. 21 are already in execution. Of these 21 projects in execution, only six are on time. Ten projects are delayed and five were rescheduled.

The ACER 2016 PCI implementation monitoring report focuses on progress since 2015. Compared to the 2015 report, five of the delayed projects and four of the rescheduled projects experienced a new delay in 2015. Also two other projects that were on time faced delays in this year as well.