Embed Size (px)

Citation preview

PRE-FEASIBILITY STUDY

TOMATO PASTE PLANT

Pakistan Horticulture Development & Export BoardMinistry of Commerce, Government of Pakistan

126 Y, Commercial Area, Phase III, DHA, Lahore

Feasibility study for Tomato Past Plant

1 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

1. INTRODUCTION

Agriculture

Agriculture sector is the backbone of Pakistan’s economy employing about 45 % of thework force. Nature has blessed Pakistan with an ideal climate for growing a large varietyof vegetables and fruits. According to rough estimates about 30%-40% ofvegetables/fruits are wasted due to negligence and lack of cold chain / processingfacilities, which could convert them into non-perishable form, permitting itstransportation and storage without wastage. With the spread of education, change inhabits of populace, growth in working women force and increase in per capita income &urbanization, the demand for processed vegetable/fruit products is increasingprogressively.

Tomato Outlook

Tomato is a rich source of vitamin A & C and is cultivated over vast area of land in theworld. It has its origin from Themistition, city of Mexico where it was named asTomatile. Then its cultivation started in Central America and subsequently shifted toEurope. In Indo-Pak sub continent, its utility is growing year by year resulting into moredemand/cultivation. It is popular due to its color, taste & food value. Tomato has longbeen processed into Ketchup in Italy, Turkey, Greece, USA and European countries. It isused in large quantity at household and restaurants in the shape of tomato juice, tomatopuree and paste. These products are also gaining popularity in Pakistan.

Tomato, like other vegetables/fruits is a perishable commodity and has a shorter shelf lifein normal temperature. Therefore, problems are faced in the supply chain due tonon-existence of a cold chain system in the country which results in losses of product anddrastic price variations. Tomato Paste provides a way out with extremely positiveoutcome both commercially and financially. Indeed, tomato consumption by the foodprocessing industry revolves around the availability of user friendly intermediate productslike tomato paste, puree, ketchup and sauces.

Products, such as tomato paste/puree have potential demand with local fruit/vegetableprocessors as well as the retail market. Establishment of tomato processing facilities inthe country can contribute in reducing the dependence of local industry on importedtomato paste. The paste is currently being imported mainly from China, Iran and Turkey.About 2,400 tons of tomato paste was imported during the year 2005-2006. In Pakistan,

Feasibility study for Tomato Past Plant

2 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

business opportunities in processing of vegetables and fruit products are yet to be fullyexploited.

Opportunity Rationale

Vegetables/Fruits processing industry, in general, is showing signs of healthy growth withexpanding product range and increased acceptability in the local market. Favorablenatural environment, increasing population, rising demand for processed vegetables andfruits, and relatively lower labour cost are some of the factors that can contribute towardssustained growth rate in this particular sector. Tomato is one of the most popularvegetables in the world. The derivatives of tomato like paste, juice, ketchup, etc. arewidely used in kitchens all around the world. With the increasing affluence of the world,its demand has increased very rapidly resulting in wide scale development of tomatoindustry for production of tomato paste/puree. Rise of the fast food industry in thecountry is also having a significant impact on the demand for tomato and fruit products. Itis expected that this trend will continue in the near future and the consumption of tomatowill increase.

Tomato ketchup industry is just another example of the success for the Pakistanicompanies which grew from its very humble beginning to the position of a player in theleague. The future also looks very bright with developing local and export marketsaround.

Per capita consumption is still very low as compared to developed countries. Forexample, US consumption of tomato paste per capita is 30 kg per year, EU countriesconsume 15 kg per capita, and Turkey consumes 1 Kg Per capita. As compared to thesefigures, per capita consumption in Pakistan is negligible. It shows that there is still bigpotential for demand from the local market, which is expected to rise with the passage oftime.

Economic Size of Plant

A tomato paste and pulp processing plant can be designed with a wide range of optimalprocessing capacity and product mix. However, it is suggested that the smallest viableeconomic processing unit should have 3 tons of tomato processing capacity per hour.Processing plant used for the purpose of this study will have annual processing capacityof 10,800 tons of tomato yielding 2,160 tons of tomato paste. The proposed plant willhowever, be capable to process upto 5 tons of tomato per hour.

Feasibility study for Tomato Past Plant

3 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

2. RAW MATERIAL

Raw Material Requirements

The raw materials required for a tomato processing unit are:

Fresh Tomatoes.Preservative including Glacier Citric Acid, Potassium Met bisulphate or SodiumBenzoate.

Packaging Requirements

Packing requirements for the end consumers are:

Retail Customers: Tin Packs, Pouch Packs and Glass BottlesProcessors: Large Plastic ContainersHotel Industry: Large Tin Packs, Plastic DrumsAseptic pack in drums for foreign processors/bulk consumers

In the initial stage, the unit will start with bulk supply to processors/ hotel industry and would gradually move into retail sales. Export markets would be explored in later stage.

Availability of Raw Material

Small-scale farmers and wholesale market commission agents in vegetable & fruitmarkets are the major suppliers of raw material in the local processing industry. Tomato(the primary raw material), salt, preservatives etc. (secondary raw materials) are availablelocally. Metal containers, pouches and glass bottles (Packing material) are also availablelocally. Aseptic packs are normally imported and cost very high. Aseptic packing is usedfor obtaining long shelf life for products without preservatives and is used for exportpurposes.

Feasibility study for Tomato Past Plant

4 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

Availability Period of Tomato in Pakistan

The data regarding availability period of tomatoes in Pakistan, is given in the following table:

Tomato Crop Calendar

Season Date for release of crop

Kharif Ist FebruaryRabi Ist August

Provinces / Months JAN FEB

MAR APR MA

Y JUN JUL AUG SEP OCT NOV DEC

B a l u c h i s t a n(Kharif)Baluchistan (Rabi)SindPunjab N.W.F.P.(Kharif)N.W.F.P.(Rabi)

Production/Price of Tomatoes

Following table shows the province wise and overall yearly production of tomatoes in Pakistan.

Year Punjab Sind NWFP Baluchistan Pakistan % IncreaseProduction of Tomatoes (Tones)

2000-01 60,752 32,930 139,993 35,080 268,755 -2001-02 62,226 32,838 146,207 52,841 294,112 9.432002-03 65,199 35,011 148,274 57,806 306,290 4.142003-04 63,956 35,722 157,495 155,613 412,786 34.772004-05 63,710 33,968 146,871 181,660 426,209 3.252005-06 64,588 48,326 161,599 193,633 468,146 9.84

(Source: Ministry of Food Agriculture & Livestock’s)

Pakistan produced 468,146 tons tomatoes in 2005-06 which was 75 % more than theproduction in the year 2000-01. The growth in tomato production was normal till year2002-2003. But there was un-precedented increased of 35 % during 2003-04 ascompared to the last year. The main reason behind this was the extra ordinary productionof tomatoes in Baluchistan, as.it produced almost three times more tomatoes than the last

Feasibility study for Tomato Past Plant

5 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

year’s production. In 2005-2006, out of total tomato production, 41% was in Balochistan,35 % in NWFP, 14 % in Punjab and 10 % in Sind.

Tomato is cultivated throughout the Pakistan. Previously N.W.F.P. was the main tomatogrowing province which used to contribute nearly 50% of total national production up till2003-04. Since 2004-05, Balochistan province is the leading producer of tomato inPakistan. The share of Balochistan’s production has increased from 13 % in 2000-2001 to41 % in the year 2005-2006. The main reasons are the growth in the development ofagriculture-able area, development of agricultural infrastructure, availability of water andfavourable Government policies.

Following tables shows the yearly average prices of tomato that prevailed in the country.

Yearly Average Tomato Price (Rs.)/40 kgYear Punjab Sind NWFP Balochistan

2000-01 412.08 313.83 435.50 405.082001-02 515.33 299.42 400.75 437.172002-03 348.25 188.17 304.42 295.082003-04 574.83 371.92 481.67 516.332004-05 729.80 423.70 715.10 634.502005-06 556.08 365.10 475.50 466.90

(Source: Ministry of Food Agriculture & Livestock’s)

The price of tomato is lowest in the province of Sind followed by the province ofBalochistan while it is highest in Punjab. Lower price in Sind is due to the consumerbehavior and supply factor as tomato from whole of the Pakistan is sent to Karachi (Sind)being a main consumption hub of agriculture produce due to concentrated population.

Top ten tomato producing districts of Pakistan for the year 2005-06

District RANK* Province Hectares Tonnes Tonnes/Hectare

%age ofTotal

ProductionKilla Saifullah 3 Balochistan 6,488 85,473 13.17 18.26 Swat 8 NWFP 5,752 65,374 11.37 13.96 Nasirabad 1 Balochistan 1,569 27,918 17.79 5.96Barkhan 2 Balochistan 1,605 22,187 13.82 4.74Badin 10 Sindh 3,520 20,876 5.93 4.46Jaffarabad 6 Balochistan 1,340 15,990 11.93 3.42Malakand 7 NWFP 1,070 12,553 11.73 2.68Tank 5 NWFP 835 10,430 12.49 2.23Dir Lower 4 NWFP 772 10,073 13.05 2.15Mohmand Agency 9 NWFP 1,220 8,545 7.00 1.83

*Rank with respect to yield

Feasibility study for Tomato Past Plant

6 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

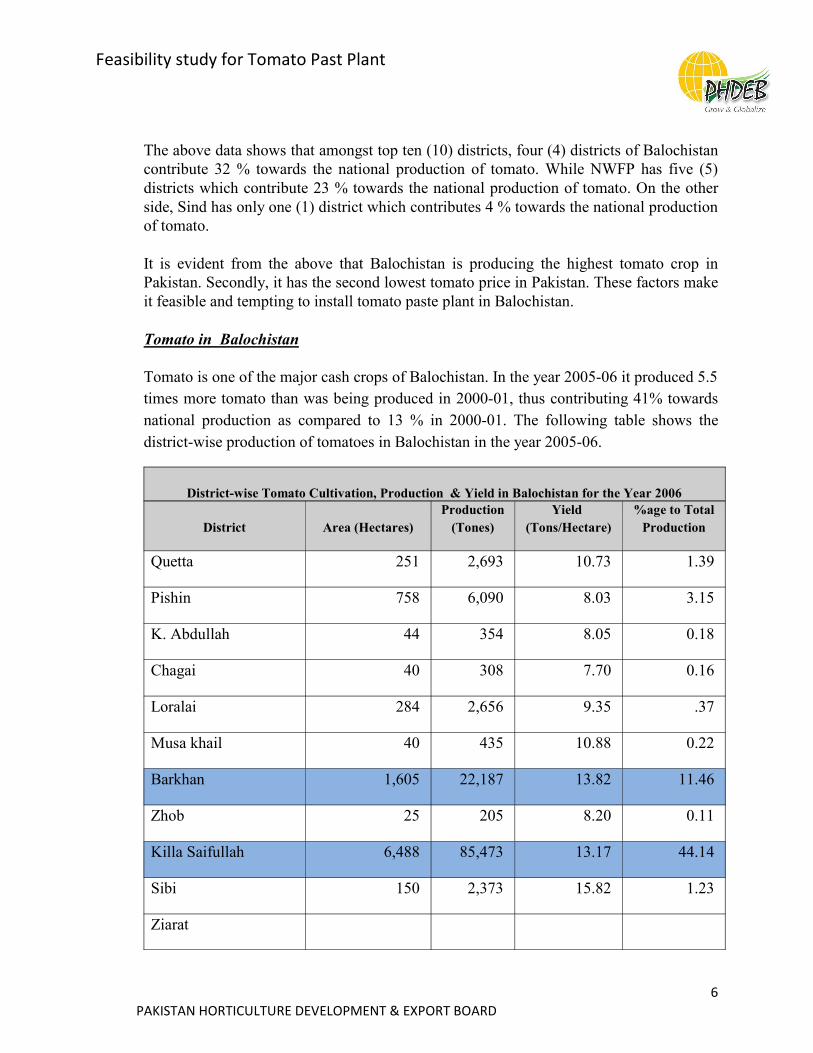

The above data shows that amongst top ten (10) districts, four (4) districts of Balochistancontribute 32 % towards the national production of tomato. While NWFP has five (5)districts which contribute 23 % towards the national production of tomato. On the otherside, Sind has only one (1) district which contributes 4 % towards the national productionof tomato.

It is evident from the above that Balochistan is producing the highest tomato crop inPakistan. Secondly, it has the second lowest tomato price in Pakistan. These factors makeit feasible and tempting to install tomato paste plant in Balochistan.

Tomato in Balochistan

Tomato is one of the major cash crops of Balochistan. In the year 2005-06 it produced 5.5times more tomato than was being produced in 2000-01, thus contributing 41% towardsnational production as compared to 13 % in 2000-01. The following table shows thedistrict-wise production of tomatoes in Balochistan in the year 2005-06.

District-wise Tomato Cultivation, Production & Yield in Balochistan for the Year 2006

District Area (Hectares)Production

(Tones)Yield

(Tons/Hectare)%age to Total

Production

Quetta 251 2,693 10.73 1.39

Pishin 758 6,090 8.03 3.15

K. Abdullah 44 354 8.05 0.18

Chagai 40 308 7.70 0.16

Loralai 284 2,656 9.35 .37

Musa khail 40 435 10.88 0.22

Barkhan 1,605 22,187 13.82 11.46

Zhob 25 205 8.20 0.11

Killa Saifullah 6,488 85,473 13.17 44.14

Sibi 150 2,373 15.82 1.23

Ziarat

Feasibility study for Tomato Past Plant

7 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

Kohlu 22 342 15.55 0.18

Dera Bughti

Nasirabad 1,569 27,918 17.79 14.42

Jaffarabad 1,340 15,990 11.93 8.26

Bolan 400 5,240 13.10 2.71

Jhal Magsi 27 354 13.11 0.18

Kalat 117 1,014 8.67 0.52

Mastung 125 1,065 8.52 0.55

Khuzdar 825 6,945 8.42 3.59

Awaran 213 1,534 7.20 0.79

Kharan 218 1,671 7.67 0.86

Lasbela 620 6,456 10.41 3.33

Turbat 173 2,027 11.72 1.05

Panjgoor 37 275 7.43 0.14

Gwadar 4 28 7.00 0.01

Total 15,375 193,633 12.59 100

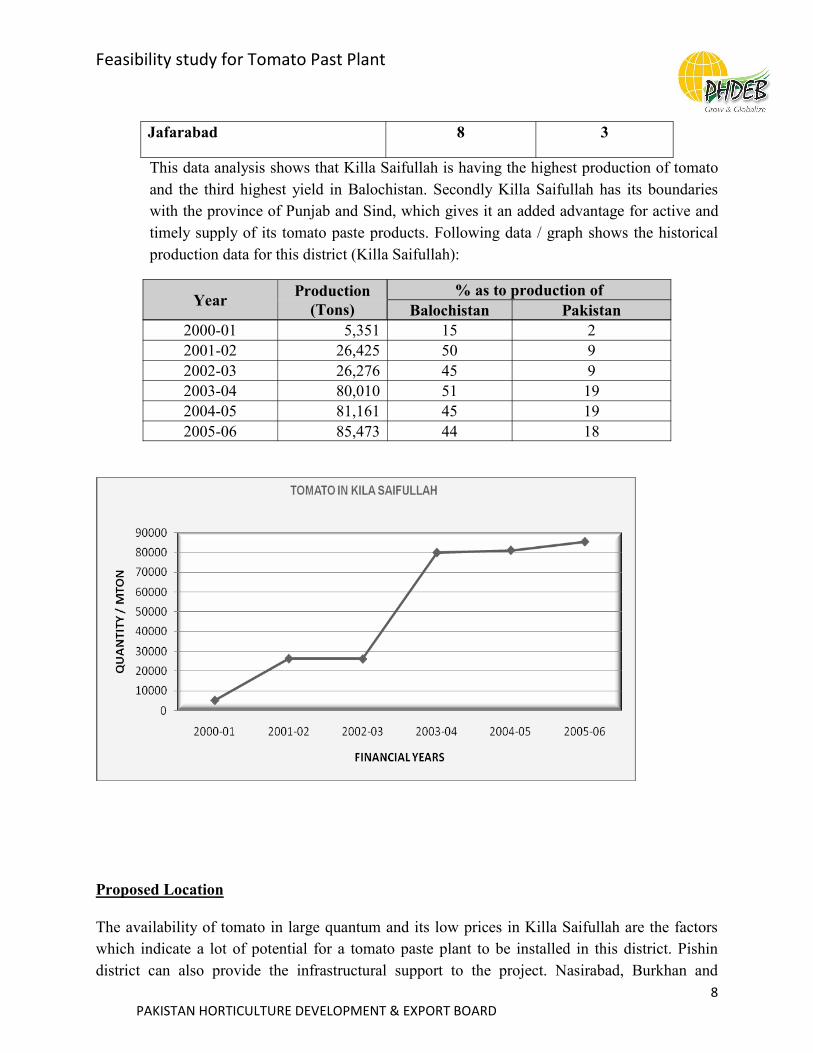

The above table shows that the following four districts contribute 3/4th of the totalproduction in Balochistan and 1/3rd of the total production in Pakistan.

District% As To Production Of

Baluchistan Pakistan

Killa Saifullah 44 18

Nasirabad 14 6

Barkhan 12 5

Feasibility study for Tomato Past Plant

8 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

Jafarabad 8 3

This data analysis shows that Killa Saifullah is having the highest production of tomatoand the third highest yield in Balochistan. Secondly Killa Saifullah has its boundarieswith the province of Punjab and Sind, which gives it an added advantage for active andtimely supply of its tomato paste products. Following data / graph shows the historicalproduction data for this district (Killa Saifullah):

Year Production(Tons)

% as to production ofBalochistan Pakistan

2000-01 5,351 15 22001-02 26,425 50 92002-03 26,276 45 92003-04 80,010 51 192004-05 81,161 45 192005-06 85,473 44 18

Proposed Location

The availability of tomato in large quantum and its low prices in Killa Saifullah are the factorswhich indicate a lot of potential for a tomato paste plant to be installed in this district. Pishindistrict can also provide the infrastructural support to the project. Nasirabad, Burkhan and

Feasibility study for Tomato Past Plant

9 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

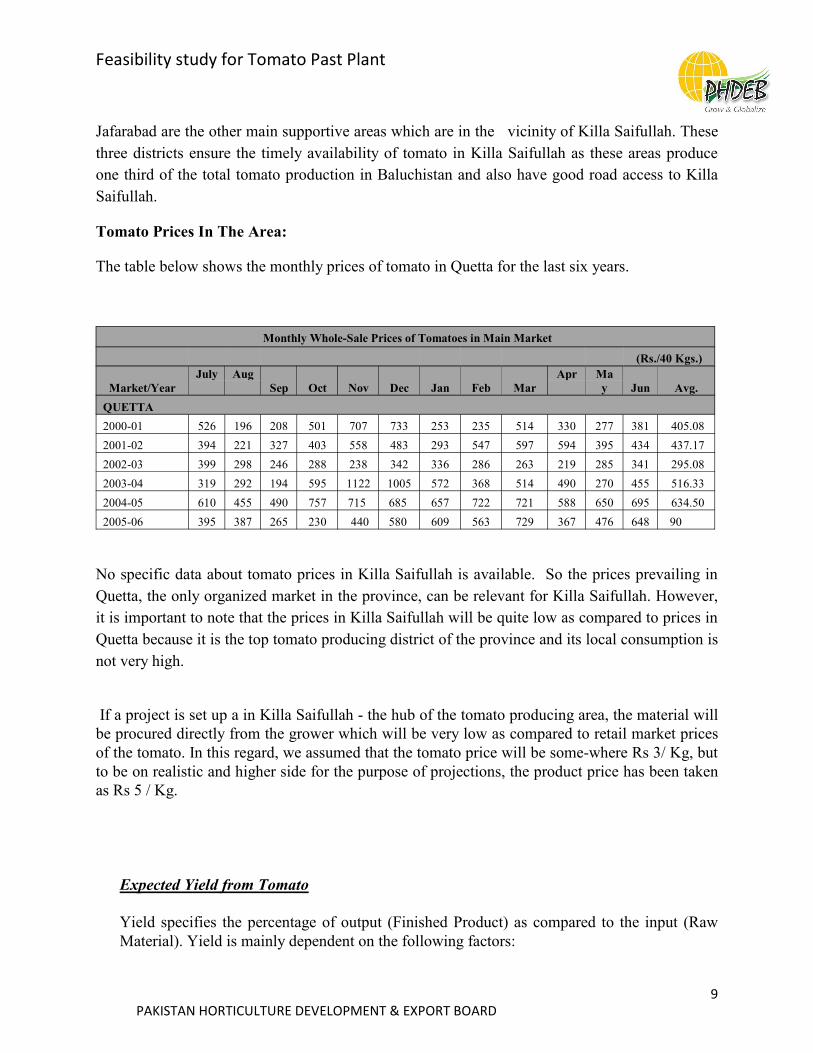

Jafarabad are the other main supportive areas which are in the vicinity of Killa Saifullah. Thesethree districts ensure the timely availability of tomato in Killa Saifullah as these areas produceone third of the total tomato production in Baluchistan and also have good road access to KillaSaifullah.

Tomato Prices In The Area:

The table below shows the monthly prices of tomato in Quetta for the last six years.

Monthly Whole-Sale Prices of Tomatoes in Main Market

(Rs./40 Kgs.)

Market/YearJuly Aug

Sep Oct Nov Dec Jan Feb MarApr Ma

y Jun Avg.QUETTA2000-01 526 196 208 501 707 733 253 235 514 330 277 381 405.082001-02 394 221 327 403 558 483 293 547 597 594 395 434 437.172002-03 399 298 246 288 238 342 336 286 263 219 285 341 295.082003-04 319 292 194 595 1122 1005 572 368 514 490 270 455 516.332004-05 610 455 490 757 715 685 657 722 721 588 650 695 634.502005-06 395 387 265 230 440 580 609 563 729 367 476 648 90

No specific data about tomato prices in Killa Saifullah is available. So the prices prevailing inQuetta, the only organized market in the province, can be relevant for Killa Saifullah. However,it is important to note that the prices in Killa Saifullah will be quite low as compared to prices inQuetta because it is the top tomato producing district of the province and its local consumption isnot very high.

If a project is set up a in Killa Saifullah - the hub of the tomato producing area, the material willbe procured directly from the grower which will be very low as compared to retail market pricesof the tomato. In this regard, we assumed that the tomato price will be some-where Rs 3/ Kg, butto be on realistic and higher side for the purpose of projections, the product price has been takenas Rs 5 / Kg.

Expected Yield from Tomato

Yield specifies the percentage of output (Finished Product) as compared to the input (RawMaterial). Yield is mainly dependent on the following factors:

Feasibility study for Tomato Past Plant

10 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

1. Strict quality control on raw material and production processes.2. Type of plant3. Processing methodology

Normal yield from Tomato Paste is 20 %. Fresh tomatoes are available almost throughout theyear in Pakistan.

Feasibility study for Tomato Past Plant

11 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

3. TOMATO PASTE PRODUCT

TOMATO PRODUCTS

Tomatoes and tomato products have always been a natural part of human diet. Everyoneappreciates their red color and juicy taste. Recent research also indicates that processed tomatoesare good for human health due to a high content of lycopene. Last twenty years have witnessedan explosion of new and refined tomato products. Purées and passata have become majorproducts together with the more classical ketchup, tomato paste and chilli sauces. Driven by theinterest for ethnic food, there has also been a growing market for speciality sauces with particles,e.g. salsas with pepper and onions and a wide variety of tasty dip sauces. The variety of productsin this market is already large, and is expected to increase in the future with more and morecooking recipe products.

Major products of processed tomatoes include tomato paste, puree, tomato sauces, ketchup,whole canned tomatoes and juices.

TOMATO PASTE is the main product of processed tomatoes which is used as a raw material tomake ketchup, sauces and other tomato related products.

Processors of tomato paste usually sell to re-packaging companies which add different additivesto make specialized retail products such as ketchup, sauces and juices. Tomato paste is also usedas tomato substitute in restaurants, hotels and individual households.

4. PRODUCTION PROCESS

Detailed Production Process

The production process will involve the following steps:

Washing

Fresh tomatoes arriving at the plant in trucks are unloaded into a collection channel (also knownas flume), a stainless steel or cement duct into which a quantity of water 3 to 5 times higher thanthe amount of unloaded tomato is continuously pumped. For example, a 10 tons/hour raterequires at least 30m3/hour of water.

Sorting

This water flow carries the tomatoes onto the roller elevator, which then conveys them to thegrading station. The delivery trucks park-up alongside the flume and, while the trailerscontaining the tomatoes are being tilted towards it, an operator, using a special tube, pipes a vastquantity of water inside the truck, so that the tomatoes can flow out from the special 50 x 50cm

Feasibility study for Tomato Past Plant

12 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

opening. In this way the tomatoes and the water will be gradually feed into the flume withoutgetting damaged.

The tomatoes then arrive at the grading station, after having been rinsed under a clean waterspraying system (preferably drinking water). Here the staff removes the green, damaged andexcessively small tomatoes which are placed on a reject conveyor (or an auger) and thencollected in a large box or directly inside a truck to be taken away.

Chopping/ Crushing

The tomatoes suitable for processing are transported to the chopping station (a hammer mill or aspecial mono-pump provided with pre-feeding screw) where they are chopped (broken andpulped).

Pre Heating

The pulp is pre-heated to 65-75°C for Cold Break processing or to 85-98°C for Hot Breakprocessing. The main control panel on the evaporator regulates the pre-heating temperature.

Pulping & Refining

The heated tomato pulp (fiber, juice, skin and seeds) is then conveyed via a special pump to anextraction unit composed of two operating stations: a pulper and a refiner, equipped with twosieves having different sized meshes. The first sieve processes solid pieces up to 1 mm, while therefiner processes solid pieces up to 0.6 mm, depending on the type of sieve fitted on the machine

(the manufacturer can supply sieves with different sized holes if necessary). Two products comeout of the extraction unit: refined juice for concentration and waste for disposal. The averageextractor yield varies according to different factors: the pulp’s temperature (a higher temperaturewill mean an increased juice yield), the variety of tomatoes treated, the type of sieve fitted, therotation speed and the shape of the rotor on each dejuicing body unit. On average, however, theyield is about 95%. For example, if the extractor is fed with 100 kg of hot pulp, it will produce95 kg of juice and 5 kg of waste. In addition, there is also a hypothetical product waste of about1-3% from the grading stations. Therefore, 100 kg of tomatoes unloaded from the trucks willproduce about 93-94 kg of juice to be concentrated. At this point the refined juice is collected ina large tank with an agitator which constantly feeds the evaporator. This tank is equipped withmaximum and minimum level indicators-adjusters which control the pump supplying juice to theevaporator.

Evaporation/Concentration

The juice in this storage tank is fed to the evaporator which automatically regulates juice intakeand finished concentrate output; the operator only has to set the Brix value on the evaporator’scontrol panel; during normal working conditions, the evaporator does not require any furtherregulations. The juice inside the evaporator passes through different stages where itsconcentration level will gradually increase until the required density is obtained in the final stageor “finisher”. Here the tomato paste is automatically extracted via a pump controlled by anelectronic refractometer.

Feasibility study for Tomato Past Plant

13 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

The entire concentration process (evaporation) takes place under vacuum conditions and at lowtemperatures, significantly below 100°C. Product circulation inside the various concentrictubular exchangers is carried out by special stainless steel pumps which are designed to ensurethat the product is conveyed inside the exchanger tubes at a speed of over 1.2 m/sec to avoid“flash evaporation” thus avoiding to get burnt. This means it is possible to process for extensiveperiods without having to shut down the machine.

Evaporator output is measured in liters of evaporated water per hour while concentrating tomatojuice with an initial 5°Brix concentration and producing tomato paste double concentrate at 30°Brix. All the tomato juice evaporators are designed according to these parameters. Theevaporative capacity of tomato juice concentrators is greatly influenced by the viscosity level. Ifthe tomato paste has a low Bostwick value, then the concentrator’s output level will also be low;on the other hand, a higher Bostwick value means an increased output level. It is thereforefundamental to know if the productivity data supplied by a manufacturer refers to HB or CBfinished products.

Aseptic Filing & Packaging

The concentrate is sent from the evaporator directly inside the aseptic system tank. From here itis pumped at high pressure inside the aseptic sterilizer-cooler and then to the aseptic filler, whereit is filled into pre-sterilized aseptic bags housed in metal drums. The sterilization temperatureand the holding time vary according to the product’s PH value. Generally speaking, a product

with a pH value equal to or less than 4.2 could have a sterilization temperature of 115°Cmeasured at the end of the holding section, and a holding time of at least 60-90 seconds. On theother hand, if the pH value is greater than 4.2, it is advisable to acidify the product in order tobring it to about 4.1, improving taste and final product quality.

The sterilized tomato paste is cooled down to about 35-38°C before being piped intopre-sterilized aluminum bags housed in special metal or plastic bins via a special aseptic filler.The packaged concentrate can be kept up to 24 months depending on its pH value and ambientconditions.

Storing

When storing for over 12 months, it is however advisable to conserve it in refrigerated cells,more to reduce oxidization, which could cause darkening than to protect the product’s asepticquality.

Feasibility study for Tomato Past Plant

14 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

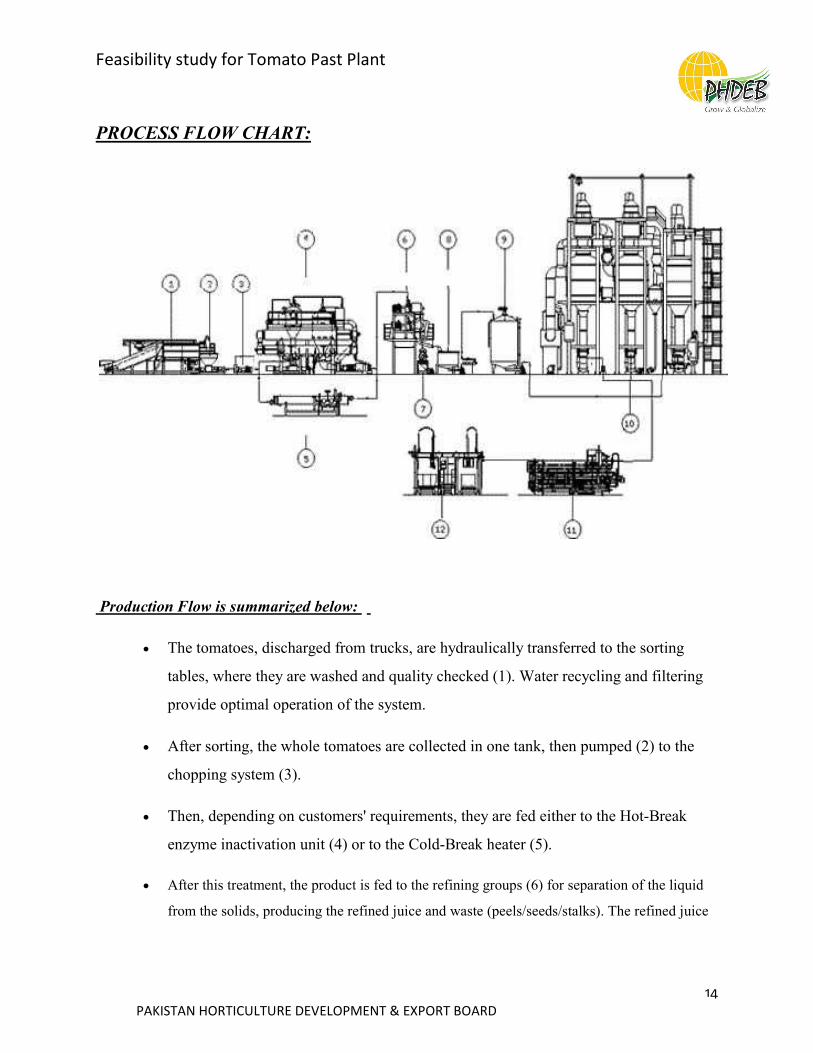

PROCESS FLOW CHART:

Production Flow is summarized below:

The tomatoes, discharged from trucks, are hydraulically transferred to the sorting

tables, where they are washed and quality checked (1). Water recycling and filtering

provide optimal operation of the system.

After sorting, the whole tomatoes are collected in one tank, then pumped (2) to the

chopping system (3).

Then, depending on customers' requirements, they are fed either to the Hot-Break

enzyme inactivation unit (4) or to the Cold-Break heater (5).

After this treatment, the product is fed to the refining groups (6) for separation of the liquid

from the solids, producing the refined juice and waste (peels/seeds/stalks). The refined juice

Feasibility study for Tomato Past Plant

15 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

is collected in a tank (8) while the waste is treated to recover the remaining part of the juice

still present (7).

Both the product collection (8) and the storage tanks (9) feed the evaporator

continuously by means of centrifugal pumps.

The concentration phase allows, during the evaporating process (10), production of

concentrated products with different Brix characteristics.

UHT sterilizing treatment (ultra high temperature) and cooling (11).

Aseptic filling into flexible bags, with a capacity of up to 1,500 l (12).

HOT BREAK is a method where in tomatoes/selected fruits are heated by passing through asteam heated tubular heater. This method gives better yield of pulp having higher viscositywithout being separated into juice & pulp. This process also kills microorganism.

COLD BREAK is a method where tomatoes are not heated to get the pulp. The pulp obtainedthrough Cold Break process is of lower quality when compared to pulp obtained by Hot Break.

End product could be stored either in tin packing or in aseptic bags of 200 kg. For the purposesof our feasibility study, we recommend aseptic packing in the bags of 200 kg because ofinvolvement of cost factor, storing capacity and other allied factors.

As regards the end use, there is no hard and fast rule for hot process or cold process. Generally,hot process is preferred as it gives a better aroma, better yield and is in use for production ofprocessed product by the Industry. Hot-Break is considered a better method because it givesbetter yield and aroma.

5. MARKET ANALYSIS

International trend

1. Tomato Processing Industry:

Feasibility study for Tomato Past Plant

16 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

Tomato is one of the most popular vegetable in the world. The derivatives of tomato likepaste, juice, ketchup, etc. are widely used in almost all the world kitchens. With the increasingaffluence of the world, its demand has increased very rapidly resulting in wide scaledevelopment of tomato industry.

a) World Tomato Paste Export

Total export market of tomato paste is around 2 billion US $ (fiscal year 2005) and this shows43 % increase from year 2003 and 27% from 2004.

Feasibility study for Tomato Past Plant

17 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

Top Ten Exporters of Tomato Paste in the World

(Figures in tons)Country 2003 2004 2005China 436,880 527,800 558,250Italy 465,000 416,818 415,000Spain 123,556 160,000 180,000Turkey 184,923 165,000 155,000Greece 80,000 135,000 135,000Portugal 121,228 115,000 125,000Brazil 19,288 14,217 14,500Israel 6,150 8,950 7,000Mexico 6,790 6,800 6,800France 3,450 5,000 5,000

China is the leading exporter of tomato paste followed by Italy, Spain and Turkey. Italy is notonly the top exporter but it is also the top importer of tomato paste. It imports a big quantity fromChina, re-packs the paste and sells most to Africa and Middle East.

Competition has intensified as world exports of fresh tomatoes from key suppliers have beenincreasing in recent years. It is noteworthy that some of the major exporters of fresh tomatoes arealso major importers. Over the last decade, China’s exports of tomato products have grownimmensely.

b) World Tomato Paste Import

While the leading importers of the tomato paste are Germany, Italy, England, Japan and France.These countries have imported approximately US$ 500 million paste in 2003. As per theinternational figures, there has been growth of 20% -25% in tomato paste consumption.Tomato/Fruits processing industry is one of the largest growing industries in the world due to theconsumption habits and life style.

Potential Markets

Local Market:

According to estimates, about 95% of the indigenous tomato based processed products (puree,paste, pulps, jams, jelly and juices) are sold in the local market. The proposed project has verywide market for processors, hotel industry and retail sellers of tomato paste.

Feasibility study for Tomato Past Plant

18 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

The target market of tomato paste/puree and pulp is as follows:

Food processors like Mitchell’s Fruit, Shezan International, Ahmed Foods, Shangrila Foods,

Rafhan Best Foods, National Foods, Tops Fruit, and Salman Food

Hotels like PC, Avari, Holiday Inn, Shelton, Marriot etc.

Fast Food / Chinese Restaurants like McDonald, Pizza Hut, KFC, Salt & Pepper etc.

Working women / Households

It is gathered that Food processors are major consumers of tomato paste in the country. Someof these companies meet their requirements (fully or partially) through in-house production oftomato paste/pulp while others depend on the following outside sources:

1. Import from paste manufacturing countries

2. Local cottage industry paste manufacturers

Tomato Paste Imported in Pakistan

“Trade Competitiveness Map” of International trade Center Geneva Switzerland,Pakistan reports tomato paste imports in Pakistan over the last five years as follows:

Years 2005-06 2004-05 2003-04 2002-03 2001-02US $ (000) 1,450 1,040 469 490 354

Note: As per the organization (ITC), the reported data is discrepant up-to the extent of 26%. asper the independent sources of the organization as Pakistan’s reported import of tomato pasteis not reported completely and actual is on the higher side. The above data is after removal ofdiscrepancy.

Based on the above data, it is concluded that demand of tomato paste in Pakistan is increasingat rapid growth rate.

Tomato Paste Produced by Cottage Industry:

There are some individual / cottage industry units working in Pakistan which are makingtomato paste/pulp and selling it to re-packaging companies which add different additives likevinegar, sugar, salt and spices to make specialized retail products such as ketchup, sauces andjuices. The supply is not sufficient and of desired quality. The yield of cottage industry

Feasibility study for Tomato Past Plant

19 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

supplies is low. One kg paste of the proposed plant will be equal to about 2.8 kg of the tomatopaste produced by the cottage industry.

The tomato paste so purchased is of lower brix and quality which gives low yield in ketchupprocess. Its price range is Rs. 25- 35/kg. Interestingly, due to un-availability of thetomato/paste (at economical price), some people use pulp of other materials like carrots andpumpkins by mixing it with 15 – 20% tomato paste.

Retail Supply of Tomato Paste:

As stated earlier, major portion of the produce is sold as intermediary product and only a smallportion is processed and sold as tomato paste in the retail market. Only the leading foodprocessors like Mitchell have branded products in the market while imported paste is also soldon leading Departmental Stores. Size of this market segment is estimated at 100-200 MT perannum. Due to restricted size of this market, the study has been based on bulk packing.

Local Market Demand Development:

Local demand can be created for the sale of tomato paste. In Pakistan tomato is an importantingredient of our food. Especially all the continental food stuff is made of fresh tomato. Mostof the time, around 4 -6 months during the year, tomato becomes very expensive. It rangesfrom Rs. 35 to 120 per Kg. During this period, tomato paste can replace the tomato for thecooking ingredient. One kg of tomato paste is as good as 5 Kgs of fresh tomato.

Current & Future Demand in Local Market:

Establishment of a tomato paste plant in the country can significantly reduce the dependenceof local ketchup industry / hotels on imported paste and thus save valuable foreign exchange.The paste is currently being imported mainly from China, Iran and Turkey. Around 2400 MTof tomato paste was imported during the year 2005-2006.

The current estimated consumption of tomato paste/pulp in the country is around 4,000-4,500

tons as detailed below:

Food Processing Industry = 3,000-3,200 MT

Hotels & Restaurants = 800-1,000 MT

House Hold = 200 – 300 MT

The demand for tomato paste in near future is expected to increase at around 15% per annum.

Feasibility study for Tomato Past Plant

20 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

In the local market, tomato paste is available at whole sales level but in small bottle and tinpacks. The whole sales market rate for the tomato past is as follows:

1. 1 Kg Packing Rs.80 – Rs. 1202. 500Gms Rs. 55- Rs. 70 3. 450 Gms Rs. 30- Rs. 454. 300 – 330 Gms Rs. 25 – Rs. 40

Export Market:

There is great potential of tomato paste in Afghanistan, Middle East, Far East, EuropeanCountries, USA etc. As per the latest survey of Afghanistan Investment Support Agency(AISA) in 2006-07, currently there is a huge demand for tomato paste, Jams, Jellies,marmalades products. In the recent years the Afghani culture and eating habits of people arechanging. Local demand for fruit juices is booming, but presently juices and tomato paste arebeing imported. Market research indicates that there is a market of USD 16-22 million for fruitjuices and USD 8-16 million in tomato paste. Pakistani Investors in the food and beverageprocessing sector can capitalize on this large and adjacent consumer market.

6. PLANT & MACHINERY

There are no local manufacturers which have experience of manufacturing tomato paste plants.Secondly, the plant & equipment for food industry is to be made from special steel. Therefore,the project is based on imported machinery. Imported Plants of Italian, Chinese and Indian originare available. The detail on the machinery is annexed.

Government has exempted plant and machinery, operated by power of any description as animported or purchased locally by a registered person to be used for the manufacture of taxablegoods by the registered person on the basis of certain requirements. The exemption policy hasbeen notified in the SRO 987 (1)/1999 dated August 31, 1999. Further exemption is alsoavailable in respect of Income Tax & Sales Tax at the time of import with a view to start thetaxable activity after the trial run. There is no period bar to start the production.

Plant Utilization:

For Tomato Paste/Pure, the installed production capacity is to be kept idle for seven (7) monthsin a year. In order to run the operations for the whole year, the only way out of this dilemma isdiversification, in which, other fruit products can replace tomato during those idle months.

Feasibility study for Tomato Past Plant

21 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

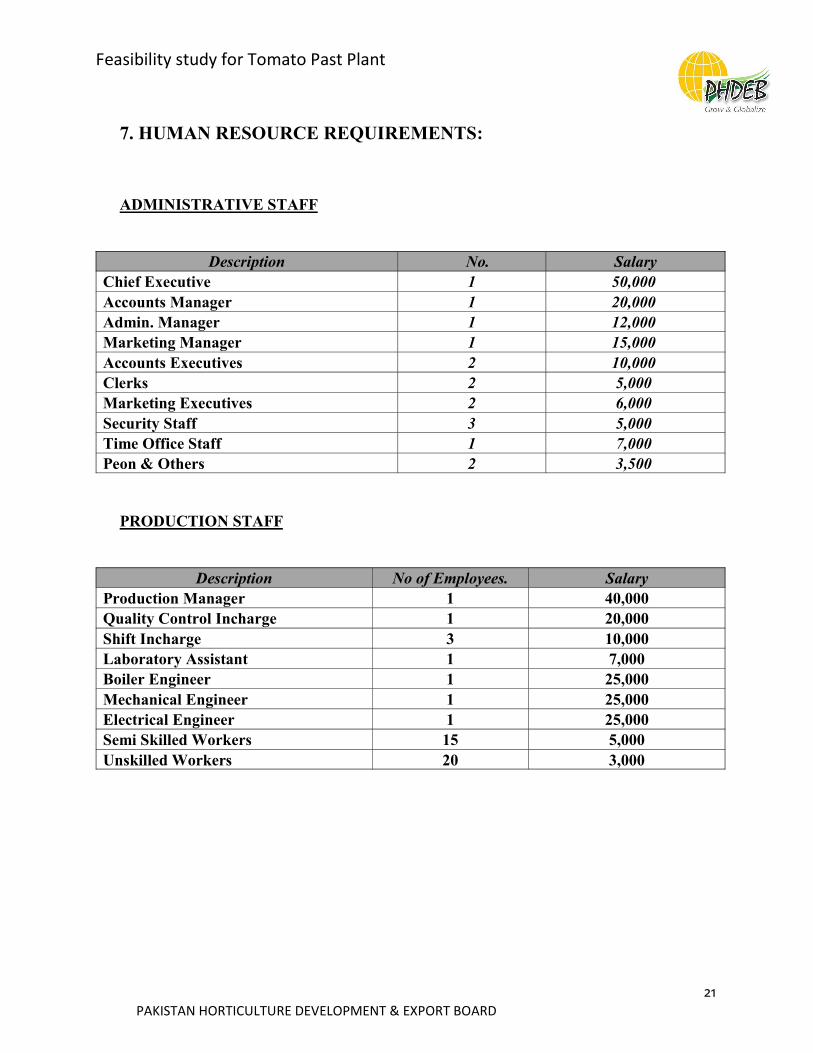

7. HUMAN RESOURCE REQUIREMENTS:

ADMINISTRATIVE STAFF

Description No. SalaryChief Executive 1 50,000 Accounts Manager 1 20,000 Admin. Manager 1 12,000 Marketing Manager 1 15,000 Accounts Executives 2 10,000 Clerks 2 5,000 Marketing Executives 2 6,000 Security Staff 3 5,000 Time Office Staff 1 7,000 Peon & Others 2 3,500

PRODUCTION STAFF

Description No of Employees. SalaryProduction Manager 1 40,000Quality Control Incharge 1 20,000Shift Incharge 3 10,000Laboratory Assistant 1 7,000Boiler Engineer 1 25,000Mechanical Engineer 1 25,000Electrical Engineer 1 25,000Semi Skilled Workers 15 5,000Unskilled Workers 20 3,000

Feasibility study for Tomato Past Plant

22 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

8. PROJECT COST

Cost Heads Local Imported Total

Land & Development 3,900 -

3,900

Building & Civil Works 15,125 -

15,125

Plant & Machinery 1,500 80,000

81,500

Erection and Installation 2,790 -

2,790

Furniture & Fixture 650 -

650

Vehicles 2,200 -

2,200

Pre-Production Expenses 2,000 -

2,000

Contingencies 9,663 -

9,663

Total Fixed Cost 37,828 80,000

117,828

Net Initial Working Capital 5,247 -

5,247

Total Project Cost 43,075 80,000

123,075

Feasibility study for Tomato Past Plant

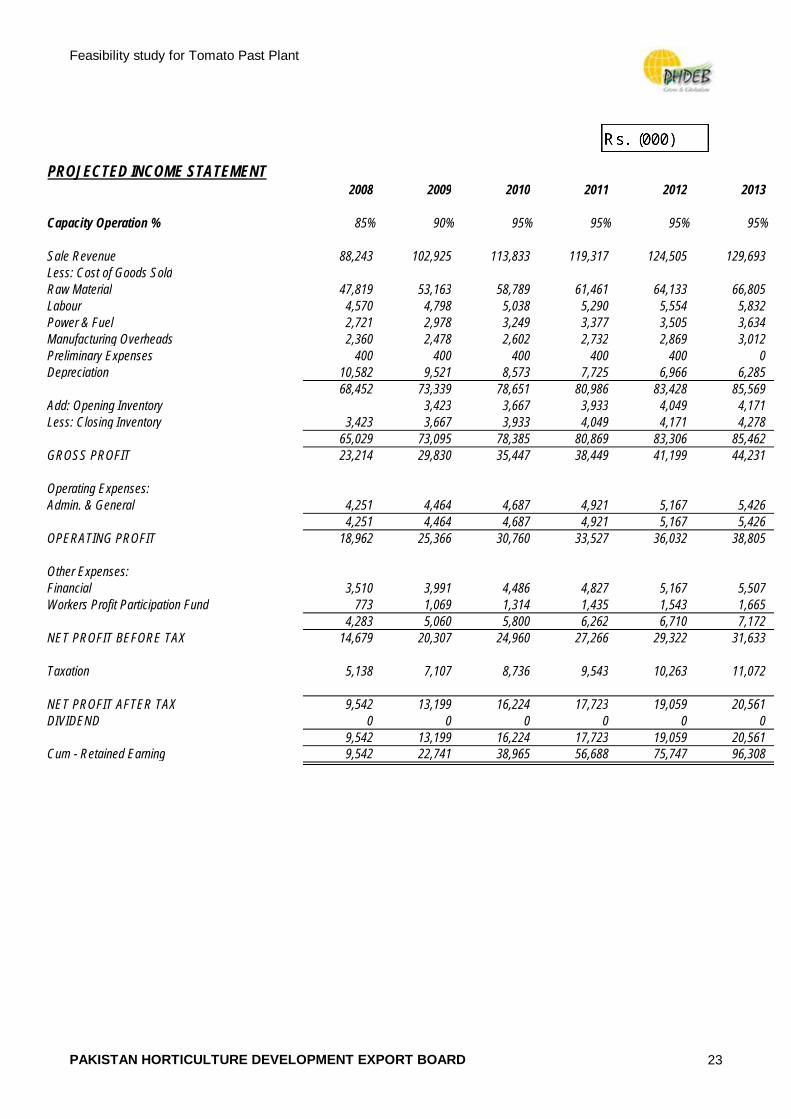

PROJECTED INCOME STATEMENT2008 2009 2010 2011 2012 2013

Capacity Operation % 85% 90% 95% 95% 95% 95%

Sale Revenue 88,243 102,925 113,833 119,317 124,505 129,693Less: Cost of Goods SoldRaw Material 47,819 53,163 58,789 61,461 64,133 66,805Labour 4,570 4,798 5,038 5,290 5,554 5,832Power & Fuel 2,721 2,978 3,249 3,377 3,505 3,634Manufacturing Overheads 2,360 2,478 2,602 2,732 2,869 3,012Preliminary Expenses 400 400 400 400 400 0Depreciation 10,582 9,521 8,573 7,725 6,966 6,285

68,452 73,339 78,651 80,986 83,428 85,569Add: Opening Inventory 3,423 3,667 3,933 4,049 4,171Less: Closing Inventory 3,423 3,667 3,933 4,049 4,171 4,278

65,029 73,095 78,385 80,869 83,306 85,462GROSS PROFIT 23,214 29,830 35,447 38,449 41,199 44,231

Operating Expenses:Admin. & General 4,251 4,464 4,687 4,921 5,167 5,426

4,251 4,464 4,687 4,921 5,167 5,426OPERATING PROFIT 18,962 25,366 30,760 33,527 36,032 38,805

Other Expenses:Financial 3,510 3,991 4,486 4,827 5,167 5,507Workers Profit Participation Fund 773 1,069 1,314 1,435 1,543 1,665

4,283 5,060 5,800 6,262 6,710 7,172NET PROFIT BEFORE TAX 14,679 20,307 24,960 27,266 29,322 31,633

Taxation 5,138 7,107 8,736 9,543 10,263 11,072

NET PROFIT AFTER TAX 9,542 13,199 16,224 17,723 19,059 20,561DIVIDEND 0 0 0 0 0 0

9,542 13,199 16,224 17,723 19,059 20,561Cum - Retained Earning 9,542 22,741 38,965 56,688 75,747 96,308

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 23

Feasibility study for Tomato Past Plant

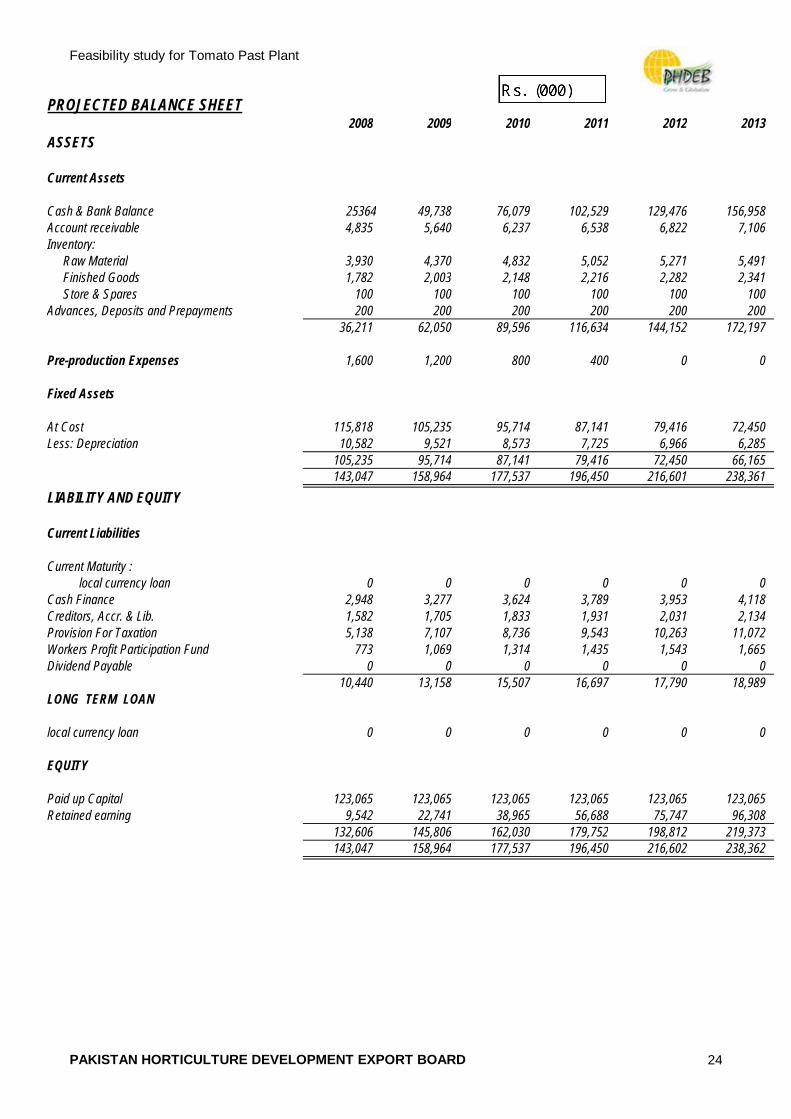

PROJECTED BALANCE SHEET2008 2009 2010 2011 2012 2013

ASSETS

Current Assets

Cash & Bank Balance 25364 49,738 76,079 102,529 129,476 156,958Account receivable 4,835 5,640 6,237 6,538 6,822 7,106Inventory: Raw Material 3,930 4,370 4,832 5,052 5,271 5,491 Finished Goods 1,782 2,003 2,148 2,216 2,282 2,341 Store & Spares 100 100 100 100 100 100Advances, Deposits and Prepayments 200 200 200 200 200 200

36,211 62,050 89,596 116,634 144,152 172,197

Pre-production Expenses 1,600 1,200 800 400 0 0

Fixed Assets

At Cost 115,818 105,235 95,714 87,141 79,416 72,450Less: Depreciation 10,582 9,521 8,573 7,725 6,966 6,285

105,235 95,714 87,141 79,416 72,450 66,165143,047 158,964 177,537 196,450 216,601 238,361

LIABILITY AND EQUITY

Current Liabilities

Current Maturity : local currency loan 0 0 0 0 0 0Cash Finance 2,948 3,277 3,624 3,789 3,953 4,118Creditors, Accr. & Lib. 1,582 1,705 1,833 1,931 2,031 2,134Provision For Taxation 5,138 7,107 8,736 9,543 10,263 11,072Workers Profit Participation Fund 773 1,069 1,314 1,435 1,543 1,665Dividend Payable 0 0 0 0 0 0

10,440 13,158 15,507 16,697 17,790 18,989LONG TERM LOAN

local currency loan 0 0 0 0 0 0

EQUITY

Paid up Capital 123,065 123,065 123,065 123,065 123,065 123,065Retained earning 9,542 22,741 38,965 56,688 75,747 96,308

132,606 145,806 162,030 179,752 198,812 219,373143,047 158,964 177,537 196,450 216,602 238,362

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 24

Feasibility study for Tomato Past Plant

PROJECTED CASH FLOW2008 2009 2010 2011 2012 2013

OPERATING ACTIVITIES

Operating Profit 18,962 25,366 30,760 33,527 36,032 38,805 Add: Depreciation 10,582 9,521 8,573 7,725 6,966 6,285Preliminary Expenses 400 400 400 400 400 0

29,944 35,288 39,734 41,653 43,398 45,090Working capital changes:

(Increase)/decrease in Stores & Spares (100) 0 0 0 0 0(Increase)/decrease in Stock in Trade (5,712) (660) (607) (288) (286) (279)(Increase)/decrease in Acc. Rec. (4,835) (804) (598) (301) (284) (284)(Increase)/decrease in Advances,Deposits and Prepayments (200) 0 0 0 0 0Increase/(decrease)Creditors,Accrued and Other Liabilities 1,290 83 87 69 72 75Net Working Capital Changes (9,558) (1,382) (1,118) (519) (499) (488)

Cash Generated From Operations 20,387 33,906 38,616 41,134 42,899 44,602

Financial Charges Paid (3,218) (3,951) (4,445) (4,798) (5,139) (5,479) Dividend Paid - - - - - - W.P.P.F - (773) (1,069) (1,314) (1,435) (1,543) Income tax - (5,138) (7,107) (8,736) (9,543) (10,263) NET CASHFLOW FROM OPERATING 17,169 24,044 25,994 26,286 26,783 27,317

INVESTING ACTIVITIES:

Fixed Assets Acquired (115,818) 0 0 0 0 0Long Term Investments 0 0 0 0 0 0Preliminary Expenses (2,000) 0 0 0 0 0NET CASHFLOW FROM INVESTING (117,818) 0 0 0 0 0

FINANCING ACTIVITIES:

Demand Finance Acquired/(Paid) 0 0 0 0 0 0Cash Finance 2,948 329 347 165 165 165Capital Introduced 123,065 0 0 0 0 0Directors Loan 0 0 0 0 0 0NET CASHFLOW FROM FINANCING 126,013 329 347 165 165 165

NET INCREASE/(DECREASE) IN CASH 25,364 24,374 26,341 26,450 26,947 27,482OPENING CASH&CASH EQUIVALENTS 0 25,364 49,738 76,079 102,529 129,476CLOSING CASH&CASH EQUIVALENTS 25,364 49,738 76,079 102,529 129,476 156,958

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 25

Feasibility study for Tomato Past Plant

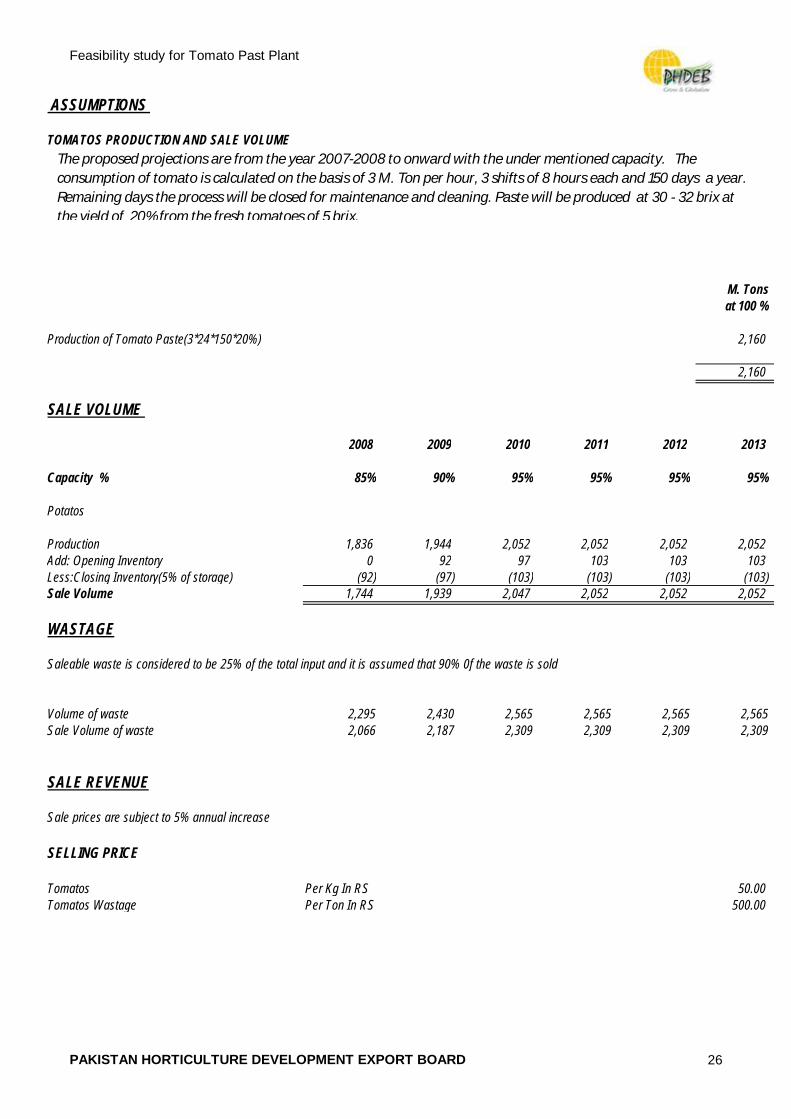

ASSUMPTIONS

TOMATOS PRODUCTION AND SALE VOLUME

M. Tonsat 100 %

Production of Tomato Paste(3*24*150*20%) 2,160

2,160 SALE VOLUME

2008 2009 2010 2011 2012 2013

Capacity % 85% 90% 95% 95% 95% 95%

Potatos

Production 1,836 1,944 2,052 2,052 2,052 2,052Add: Opening Inventory 0 92 97 103 103 103Less:Closing Inventory(5% of storage) (92) (97) (103) (103) (103) (103)Sale Volume 1,744 1,939 2,047 2,052 2,052 2,052

WASTAGE

Saleable waste is considered to be 25% of the total input and it is assumed that 90% 0f the waste is sold

Volume of waste 2,295 2,430 2,565 2,565 2,565 2,565 Sale Volume of waste 2,066 2,187 2,309 2,309 2,309 2,309

SALE REVENUE

Sale prices are subject to 5% annual increase

SELLING PRICE

Tomatos Per Kg In RS 50.00Tomatos Wastage Per Ton In RS 500.00

The proposed projections are from the year 2007-2008 to onward with the under mentioned capacity. The consumption of tomato is calculated on the basis of 3 M. Ton per hour, 3 shifts of 8 hours each and 150 days a year. Remaining days the process will be closed for maintenance and cleaning. Paste will be produced at 30 - 32 brix at the yield of 20% from the fresh tomatoes of 5 brix.

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 26

Feasibility study for Tomato Past Plant

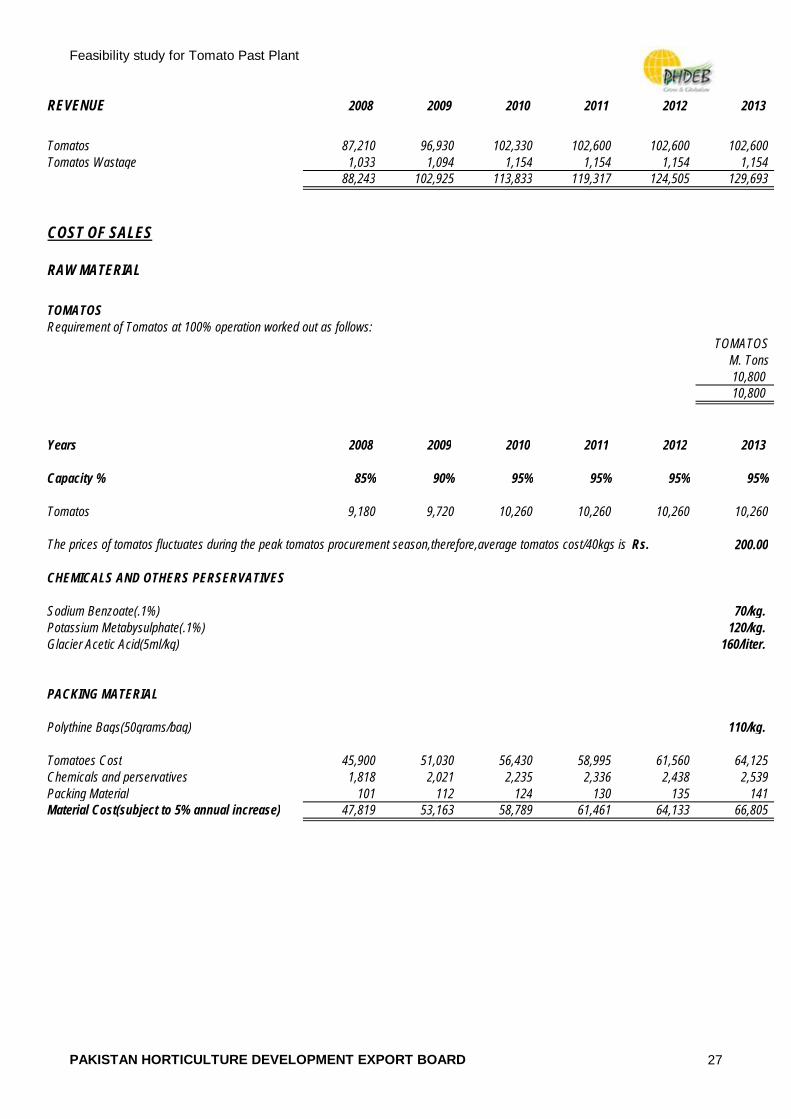

REVENUE 2008 2009 2010 2011 2012 2013

Tomatos 87,210 96,930 102,330 102,600 102,600 102,600 Tomatos Wastage 1,033 1,094 1,154 1,154 1,154 1,154

88,243 102,925 113,833 119,317 124,505 129,693

COST OF SALES

RAW MATERIAL

TOMATOSRequirement of Tomatos at 100% operation worked out as follows:

TOMATOSM. Tons10,80010,800

Years 2008 2009 2010 2011 2012 2013

Capacity % 85% 90% 95% 95% 95% 95%

Tomatos 9,180 9,720 10,260 10,260 10,260 10,260

The prices of tomatos fluctuates during the peak tomatos procurement season,therefore,average tomatos cost/40kgs is Rs. 200.00

CHEMICALS AND OTHERS PERSERVATIVES

Sodium Benzoate(.1%) 70/kg.Potassium Metabysulphate(.1%) 120/kg.Glacier Acetic Acid(5ml/kg) 160/liter.

PACKING MATERIAL

Polythine Bags(50grams/bag) 110/kg.

Tomatoes Cost 45,900 51,030 56,430 58,995 61,560 64,125 Chemicals and perservatives 1,818 2,021 2,235 2,336 2,438 2,539 Packing Material 101 112 124 130 135 141 Material Cost(subject to 5% annual increase) 47,819 53,163 58,789 61,461 64,133 66,805

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 27

Feasibility study for Tomato Past Plant

LABOURLabour requirement of the proposed project is given below

Salary Description No. Salary Per Annum

Production Manager 1 40,000 480 Quality Control Incharge 1 20,000 240 Shift Incharge 3 10,000 360 Laboratory Assistant 1 7,000 84 Boiler Engineer 1 25,000 300 Mechanical Engineer 1 25,000 300 Electrical Engineer 1 25,000 300 Semi Skilled Workers 15 5,000 900 Unskilled Workers(5Months) 20 3,000 300

160,000 3,264 Add: Fringe benefit 40% 1,306

4,570

Years 2008 2009 2010 2011 2012 2013

Labour Cost subject to 5% annual increase 4,570 4,798 5,038 5,290 5,554 5,832

POWER AND FUEL

Connecting Load kW 100Load Required KW 80

Fixed charges Rs.352 per kW per month.

Energy Charges Per Unit

Energy Cost(1.15+1.97)/2 1.56Fuel adjustment & Duty 0.18Additional Surcharge(1.89+2.08)/2 1.99Surcharge10.4% 0.30

4.02

Fixed Charges 422Variable Energy Charges at 100% capacity 2,704

Power Cost Subject to 5% annual increase 2008 2009 2010 2011 2012 2013

Fixed 422 422 422 422 422 422 Variable 2,299 2,556 2,826 2,955 3,083 3,212

2,721 2,978 3,249 3,377 3,505 3,634

WATER

No water charges are assumed for the proposed project as it will be taken from tube well sunk domestically.

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 28

Feasibility study for Tomato Past Plant

OTHER MANUFACTURING OVERHEAD

Repair and Maintenance

These have been taken @ 1 % of the plant and machinery& building in first year subject to 5% increase in subsequent years

2008 2009 2010 2011 2012 2013

Repair and Maintenance 961 1,009 1,060 1,113 1,168 1,227

Stores and Spares

These have been taken @ 1% of the plant and machinery in first year subject to 5% increase in subsequent years

Stores and Spares 810 851 893 938 985 1,034

Insurance Charges

These have been taken @ 0.50 of the assets subject to 5%annul increase

Insurance Charges 589 619 649 682 716 752

TOTAL 2,360 2,478 2,602 2,732 2,869 3,012

DEPRECIATION SCHEDULE

Description Cost Other Total Rate Cost Cost %

Land 3,900 - 3,900 0Factory building 15,125 1,470 16,595 5Plant and Machinery 83,780 8,143 91,923 10Furniture, Fixture and Utilities 1,200 - 1,200 10Vehicles 2,200 - 2,200 20

106,205 9,613 115,818

Other Cost

Contingencies 9,6139,613

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 29

YEAR WISE DEPRECIATION (Rs. 000)

Years Factory Plant & Furniture Vehicle TotalBuilding Machinery

1 830 9,192 120 440 10,582 2 788 8,273 108 352 9,521 3 749 7,446 97 282 8,573 4 711 6,701 87 225 7,725 5 676 6,031 79 180 6,966 6 642 5,428 71 144 6,285 7 610 4,885 64 115 5,674 8 579 4,397 57 92 5,126 9 550 3,957 52 74 4,633 10 523 3,561 46 59 4,190

6,659 59,871 782 1964 69,275

ADMINISTRATIVE AND GENERAL EXPENSES

Employees Salary(Rs.000)

Description No. Salary Salary Per Month Per Annum

Chief Executive 1 50,000 600Accounts Manager 1 20,000 240Admin. Manager 1 12,000 144Marketing Manager 1 15,000 180Accounts Executives 2 10,000 240Clerks 2 5,000 120Marketing Executives 2 6,000 144Security Staff 8 5,000 480Time Office Staff 1 7,000 84Peon & Others 3 3,500 126

133,500 2,358Add: Fringe Benefit @ 40% 943

3,301

2008 2009 2010 2011 2012 2013

Employees Salary Subject to 5% annual increase 3,301 3,466 3,640 3,822 4,013 4,213

General Expenses

Travelling (Including Marketing) 400Printing and Stationery 150Telecommunication 300Others 100

950

General Expenses Subject to 5% annual increase 950 998 1047 1100 1155 1212

Total Admin. & General Expenses 4,251 4,464 4,687 4,921 5,167 5,426

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 30

Feasibility study for Tomato Past Plant

FINANCIAL EXPENSES

Financial Charges:

2008 2009 2010 2011 2012 2013

Cash Finance 2,510 2,791 3,086 3,227 3,367 3,507 Other 1,000 1,200 1,400 1,600 1,800 2,000

3,510 3,991 4,486 4,827 5,167 5,507

Cash Finance:

Cash finance is proposed to be financed by Bank @ 14%

PROFIT PARTICIPATION FUND

These fund have been taken at a rate of 5% of the net profit before tax

TAXES

Tax at the rate of 35% of profit has been calculated on local sale

PAKIST AN HORT ICULT URE DEVELOPMENT EXPORT BOARD 31

Feasibility study for Tomato Past Plant

32 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

9. FINANCIAL INDICATORS

Present Value (at 15%) = Rs 130.138 million

Pay Back Period = 5.15 years

IFRR = 16.32 %

IERR = 28.03 %

Employment = 60 Nos

Break Even Capacity = 77 %

Feasibility study for Tomato Past Plant

33

APPENDIX - I

LIST OF PLANT & MACHINERY

Lift/Elevator

Washer

Feasibility study for Tomato Past Plant

34 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

Drum brush fruit washer is suitable for fruits like tomato and carrots which requiresaccurate cleaning;

surfing washer is for cleaning and selection of common fruits .This machine is alsouseful for apples, pears, and oranges and so on..

Technical Data:

Capacity(t/h) 5 10 15

Water Consumption(kw) 0.6 1.1 1.5

Dimension 4850X1480X2000(10T/H)

Crusher

Feasibility study for Tomato Past Plant

35 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

This machine is applicable for various fruits and vegetables.

Technical Data:

Capacity (t/h) 3 10

Power( KW) 3.7 5.5

Dimension (mm) 1100X750X1200 1350X1100X1450

Feasibility study for Tomato Past Plant

36

Preheating Machine

Multi-tube preheating machine is use to pasteurize the crushed products and to protectthe original colour,and to soften the products meanwhile.

Max capacity:3000KG/H

tubular board cover structure

heat exchange area: 3.5~4.0 m2

input at mormal tempreture,output tempreture around 80~85 ℃ adjustable

steam consumption: 300~500KG/H

dimension: 1700*500*1400 (longth * width * highth)

Feasibility study for Tomato Past Plant

37 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

Pulping Machine

The machine is applicable for pulping, peeling and deseeding of tomato, apricot etc.

Technical Data:

Capacity (T/H) 3 5 8 20

BladeSpeed(rpm) 525 960 960 2200

Power (KW) 5.5 11 18.5 18.5

Screening size 0.6,0.8,1.1 2.0,0.6 1.1,0.8,0.6 0.5

Dimension(MM)

1300X1200X1200 2000X1400X1800 2000X1700X2300 1800X700X1900

Feasibility study for Tomato Past Plant

38 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

Juice Extractor

The new invented belt juice extrator is widely applicable for fruit/vegetablesjuicing.This machine is featured with high quality , good automazition and highyeild-out.The capacity range is 3~20T/H.

The machine is applicable for juicing from tomato,orange,gringer,apple,pineapple etc.

capacity( T/h) 3

power( KW) 4

spiral speed( rpm) 400

dimmension (mm) 1560×450×1340

Feasibility study for Tomato Past Plant

39

Decanter

DECANTER TYPE V SERIES

DECANTER TYPE P SERIES

1、Liquid Collector 2、Liquid Level 3、External 4、Spiral 5、Feed Pipe6、Screw Feeder 7、Drum 8、Antierosion Busbings 9、Solid Discharge 10、Reduction

Feasibility study for Tomato Past Plant

40 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

outlet of concentrated tomato process extract

Disk Centrifuge

Skimming Separator

TECHNOLOGICAL DATA

Milk skimmingcapacity

2000 l/h Operating water PHvalue

6.5-7.5

Clarification andstandardization

5000l/h Motor power 6.5 kw

Solids chambercapacity

2.0 l Voltage 3 × 380/660

Bowl speed 11000 r.p.m Auxiliary Voltage 24 Ac

Maximum product 1.1 kg/dm3 Frequency 50 Hz

Feasibility study for Tomato Past Plant

41 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

density

Maximum sludgedensity

1.35 kg/dm3 Electric system Three phase withearth

Maximum producttemperature

+90 ℃ Motor and electricpanel protection level

IP55

Minimum producttemperature

+3 ℃ Noise 76 ± 2 dBA

Minimum feedingpressure foroperating water

2 bar

Operating waterconsumption (eachdischarge)

10 l

Net weight470kg

Operating watertotal hardness

≤ 6 dH Dimensions(L × W ×H)

1150 × 800 × 1150

Vaccum Concentrator

Feasibility study for Tomato Past Plant

42

Tube In Tube Sterilizer

Multi-tube coaxial heat exchangers have been successful used in food preservation for many years. They are particularlysuitable for sterilizing and/or cooling products having low and medium viscosity with the use of steam, hot and cold water

Feasibility study for Tomato Past Plant

44

Sterilizing And Bulk Aseptic Filler

Filling process, which include bag opening, filling, weighting, and bag closing, isaccomplished at aseptic condition. Thanks to the aseptic technology, the ASEPTICFILLER is particularly suitable for fruit or vegetable juice, concentrates and purees,beverage original and medicine.

Model DWZ-1-200 DWZ-2-200 DWZ-2-50

Filling heads 1 2 2

Bag capacity5 -500L

(adjustable)

5 -500L

(adjustable)

5 -50L

(adjustable)

Filling speed

( bags/h )

6-12

(Bag capacity: 200L )

12-20

(Bag capacity: 200L )

80-100

(Bag capacity: 25L

Feasibility study for Tomato Past Plant

44 PAKISTAN HORTICULTURE DEVELOPMENT & EXPORT BOARD

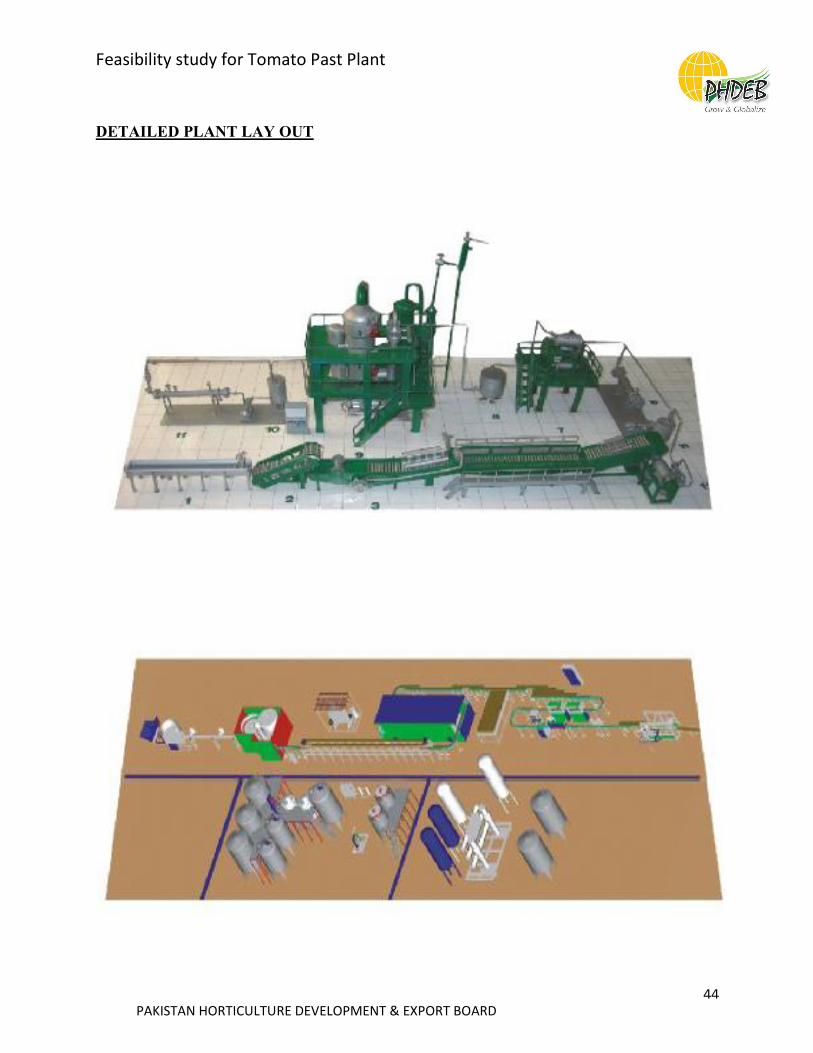

DETAILED PLANT LAY OUT