Embed Size (px)

Citation preview

Asia Pan-Asia Strategy

2 August 2011

Asia Equities Daily Focus Today's research headlines Asian Edition

Deutsche Bank AG/Hong Kong

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 146/04/2011.

Periodical

Asian Index Closings EQUITIES Close 1D Chg %Chg

SHSZ300 2977.72 0.19 -4.81 HSCEI 12540.40 1.35 -1.20 HSI 22663.37 0.99 -1.62 TWSE 8701.38 0.66 -3.02 KOSPI 2172.31 1.83 5.92 FSSTI 3215.27 0.82 0.79 KLCI 1558.01 0.59 2.57 SENSEX 18314.33 0.64 -10.70 NIFTY 5516.80 0.64 -10.07 SET 1144.14 0.94 10.79 JCI 4193.44 1.52 13.23 PCOMP 4550.53 1.04 8.32 ASX200 4497.80 1.65 -5.21 FOREX (vs US$) Close 1D Chg YTD %Chg Rmb 6.43 0.05 2.69 HK$ 7.79 0.05 -0.22 NT$ 28.81 0.16 1.70 Won 1050.70 0.32 7.17 S$ 1.20 0.17 6.79 M$ 2.94 0.88 4.11 Rupee 44.08 0.26 1.43 Baht 29.71 0.17 1.18 Rupiah 8464.00 0.47 6.29 Peso 41.97 0.41 4.37 A$ 1.10 -0.25 7.15

Source: Bloomberg Finance LP

Latest Commodity Prices COMMODITIES Close 1D %Chg YTD %Chg West Texas 94.88 -0.86 3.83 Brent 116.48 -0.28 23.52 CRB 341.41 -0.20 2.59 Copper 440.40 -1.57 -0.80 Gold (Spot) 1620.60 -0.45 14.06 Alum. (LME) 2624.00 -0.53 6.24 Baltic Dry 1264.00 -1.10 -28.71

Source: Bloomberg Finance LP

DB CORPORATE ACCESS

DB Access Taiwan Biotechnology Corporate Day - Taipei 8/10 DB Access Philippines Corporate Days - LDN 9/12 - 13 DB Access Malaysia and Singapore Corporate Day - SG 9/14 - 15 DB Access Taiwan Conference 2011 - Taipei 11/7 - 8 DB Access Korea Conference 2011 - Seoul 11/10 - 11 DB Access Indonesia Conference 2011 - Jakarta 11/29 - 12/1 DB Access China Conference 2012 - Beijing 1/9 - 11 DB Access Asia Conference 2012 - Singapore 5/28 - 30

Research Team

Carissa Szeto Equity Focus (+852) 2203 6171 [email protected]

Co

mp

any

Glo

bal

Mar

kets

Res

earc

h

TOP STORIES HSBC Holdings (0005.HK),HKD76.55 Hold Price Target HKD97.00

1H11 results preview Tracy YuPage 6

Hang Seng Bank (0011.HK) HKD123.60 Buy Price Target HKD150.00

1H11 results; strong capital and return of conservatism

Sophia LeePage 7

ESTIMATE & TARGET PRICE CHANGES

Asustek (2357.TW),TWD248.00 Buy Price Target TWD260.00

Ex-dividend target price adjustment Kc Kao

Page 8

Ace Hardware Indonesia (ACES.JK),IDR3,400.00 Buy Price Target IDR3,550.00

In-line 2Q11 with net profit +34% YoY, but rising SG&A costs

Reggy Susanto

Page 9

Ace Hardware Indonesia (ACES.JK),IDR3,400.00 Buy Price Target IDR3,550.00

Impact & preview of competitor: Do It Best Pongs Home Center

Reggy Susanto

Page 10

Astra Int'l (ASII.JK),IDR71,650.00 Buy Price Target IDR86,500.00

Raising automotive forecasts Rachman Koeswanto Page 11

BRI (BBRI.JK) IDR7,200 Buy Price Target IDR9,100

Banking on micro; upgrading target price to Rp9,100

Raymond Kosasih Page 12

United Tractors (UNTR.JK),IDR27,550.00 Buy Price Target IDR32,800.00

Raising heavy equipment forecasts Rachman Koeswanto Page 13

Dynasty Ceramic (DCC.BK) THB52.00 Hold Price Target THB51.50

Maintaining Hold for better demand next year

Sansanee Srijamjuree Page 14

MCOT (MCOT.BK) THB High yield dividend play Monchai Mokaranuraksa Page 15

Thai Union Frozen (TUF.BK),THB59.25 Buy Price Target THB62.00

Strong outlook re-affirmed (revised) Chalinee Congmuang Page 16

STRATEGY/ECONOMICS

Asia Economics Daily China July PMI stronger than expected

Kaushik DasPage 17

Global Commodities Daily

US growth recession Adam Sieminski Page 21

2 August 2011 Strategy Asia Equities Daily Focus

Page 2 Deutsche Bank AG/Hong Kong

ADDITIONAL RESEARCH DB CONFERENCE/CORPORATE DAY

DB Access Taiwan Biotechnology Corporate Day - Taipei 8/10

China TMT Daily More app factoids; also, SINA, 0700.HK

Alan Hellawell III

Page 23DB Access Philippines Corporate Days - LDN 9/12 - 13

Alternative Energy China announced a national on-grid tariff for solar PV

Eric ChengPage 24

DB Access Malaysia and Singapore Corporate Day - SG 9/14 - 15 DB Access Taiwan Conference 2011 - Taipei 11/7 - 8

China Prop Weekly Monitor

Sales volume continue to rebound in Tier-1 cities

Tony TsangPage 25

DB Access Korea Conference 2011 - Seoul 11/10 - 11 DB Access Indonesia Conference 2011 - Jakarta 11/29 - 12/1 DB Access China Conference 2012 - Beijing 1/9 - 11 Mandarin Oriental

(MOIL.SI),USD2.10 Hold NA

Solid 1H11 results Karen TangPage 26 D B Access Asia Conference 2012 - Singapore 5/28 - 30

NDRs Sohu.com Inc (SOHU.OQ) USD90.10 Hold NA

2Q beat; 3Q margin weak Alex YaoPage 27

Singapore Exchange (SGX:SP) - SG 8/3 Indocement Tunggal Prakarsa (INTP IJ) - SG 8/3 Pacific Basin (2343 HK) - HK 8/4 - 5 SAP AG (SAPG DE) - HK 8/4, SG 8/5, KUL 8/8 WPG Holdings

(3702.TW),TWD51.50 Buy Price Target TWD62.00

Solid 2Q11 results and 3Q11 outlook Jessica ChangPage 28

Hutchison Whampoa (0013 HK) - HK 8/5 China Overseas Grand Oceans Group (0081 HK) - HK 8/5Hutchison Port Holdings Trust (HPHT SP) - HK 8/8 Lifestyle International Holdings (1212HK) - HK 8/9 -10 Dongbu Insurance

(005830.KS),KRW53,700.00 Buy Price Target KRW68,000.00

Strong fundamentals lead the industry Francis Yim

Page 29Pearson Plc (PSON LN) - SHA 8/10, PEK 8/11, HK 8/12 China Overseas Land Investment Ltd (688 HK) - HK 8/10 & 12 Lianhua Supermarket (980HK) - Conf. call 8/11 PT Kalbe Farma (KLBF IJ) - HK 8/11 - 12 SJM Holdings (0880 HK) - HK 8/11 - 12

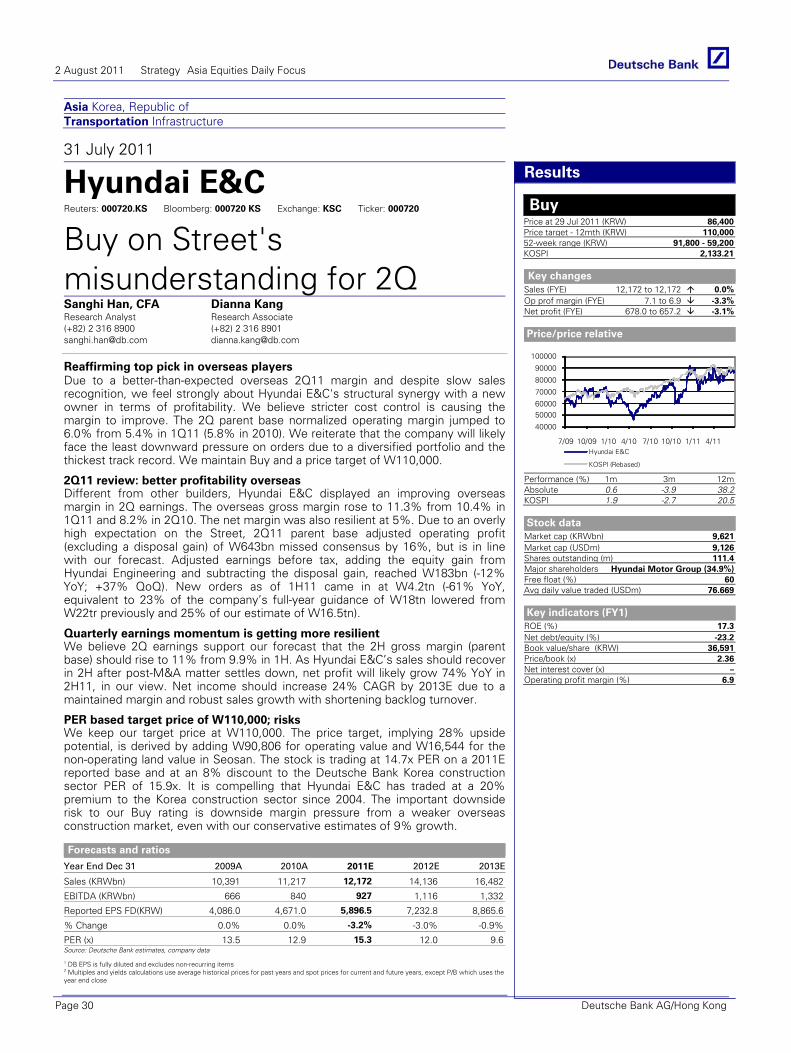

Hyundai E&C (000720.KS),KRW85,500.00 Buy Price Target KRW110,000.00

Buy on Street's misunderstanding for 2Q

Sanghi Han

Page 30 NEW: PCCW (0008 HK) - HK 8/15 - 16, SG 8/19 ComfortDelGro Corporation - SG 8/16 CapitaMalls Asia (CMA SP) - HK 8/18 - 19 China State Construction Int'l Holdings (3311 HK) - HK 8/22 PT Charoen Pokphand Indonesia (CPIN IJ) - SG 8/23

Korea Autos Carmakers' domestic sales up 6%, global sales up 10% YoY

Sanjeev RanaPage 31

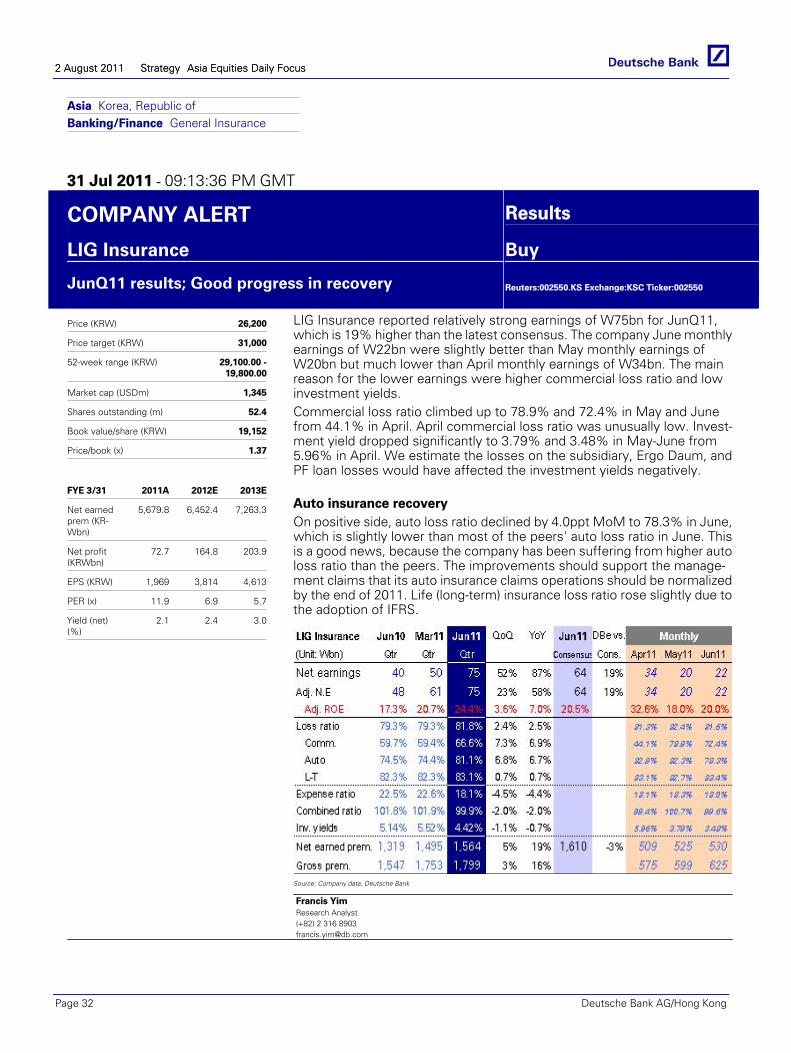

LIG Insurance (002550.KS),KRW27,050.00 Buy Price Target KRW31,000.00

JunQ11 results; Good progress in recovery

Francis Yim

Page 32

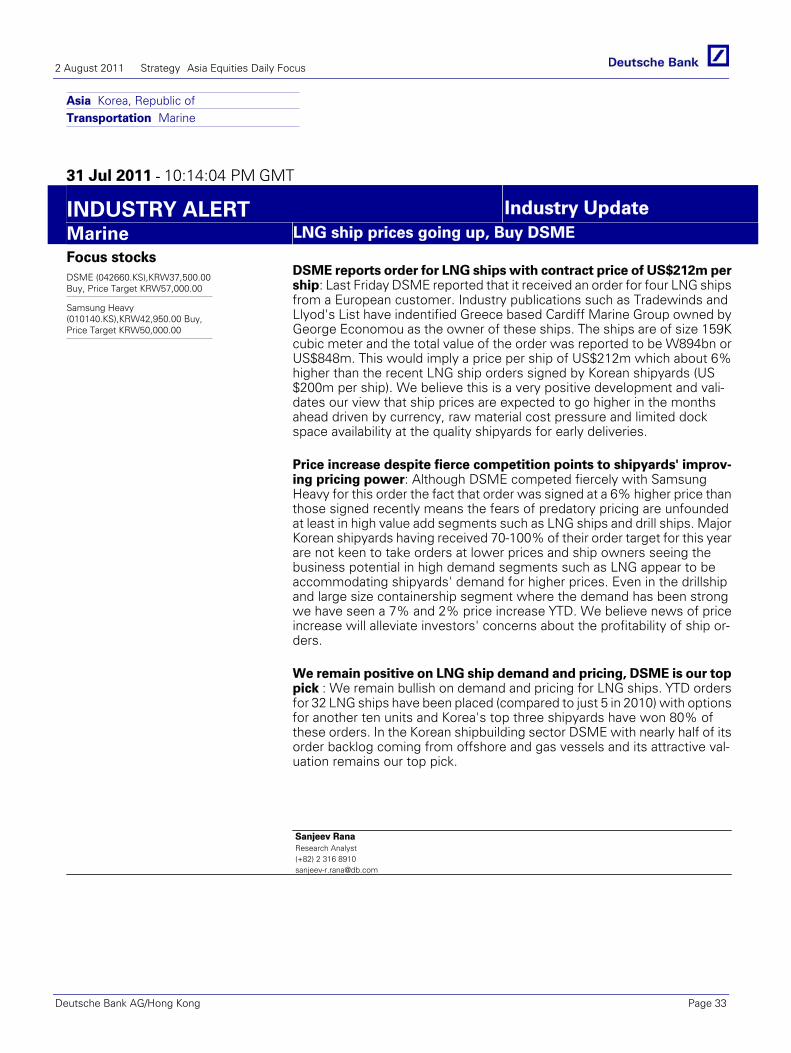

Marine LNG ship prices going up, Buy DSME

China Longyuan Power (0916 HK) - HK 8/25 Franshion Properties - SG 8/25 - 26 China Rongsheng Heavy Industries Group (1101 HK) - SG 9/1 - 2 AIA Group Ltd (1299 HK) - SG 9/13

Sanjeev RanaPage 33

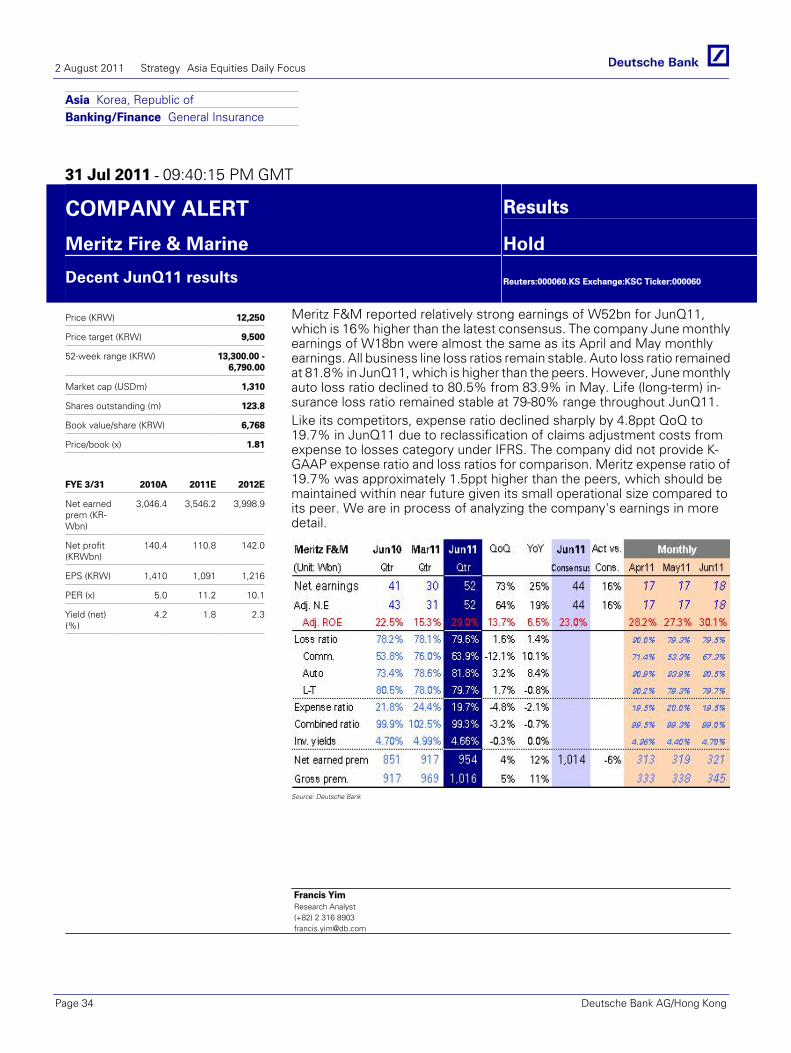

Meritz Fire & Marine (000060.KS),KRW12,100.00 Hold Price Target KRW9,500.00

Decent JunQ11 results

P T Summarecon Agung (SMRA IJ) - HK 9/26

DB ANALYST/SALES ROADSHOWS Francis Yim

Page 34

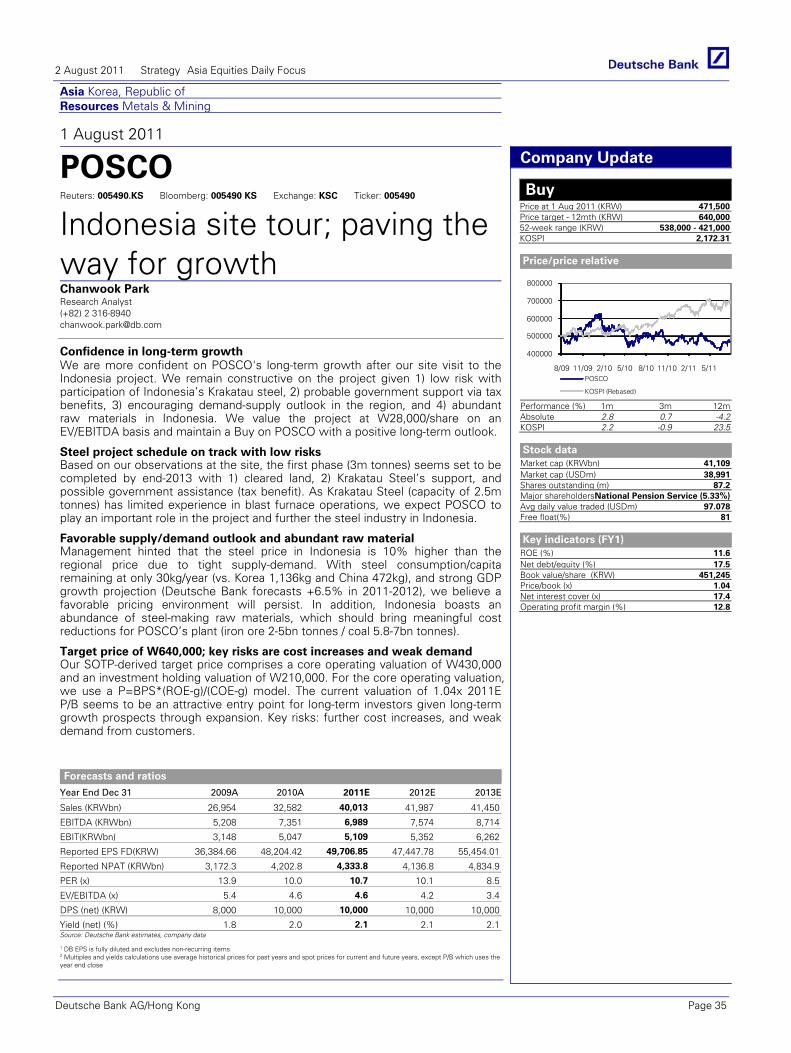

POSCO (005490.KS) KRW471,500 Buy Price Target KRW640,000

Indonesia site tour; paving the way for growth

Eugene Yeoh: 2H11 Small Mid Cap - SG 8/2 James Kan & Johnson Wan : HK/China Coal & Cement - PEK 8/3 - 4, SHA 8/5 Joelian Tseng : Taiwan Market - HK 8/4 - 5, SG 8/15 -16Judy Zhang : China Banking - SHA 8/10

Chanwook Park Page 35

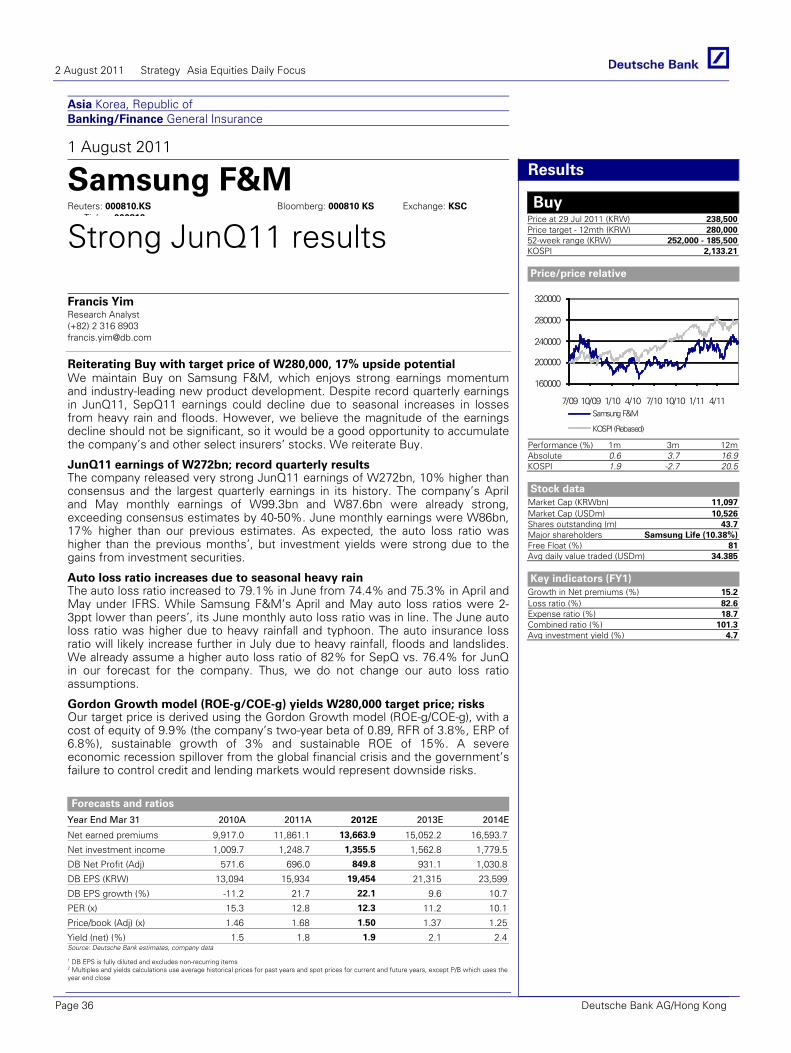

Samsung F&M (000810.KS),KRW239,500.00 Buy Price Target KRW280,000.00

Strong JunQ11 results

NEW: Abhay Laijawala: India Strategy/Metals & Minings - SG 8/11 - 12 John Kim : Korean Telecommunications - HK 8/18

Francis Yim

Page 36

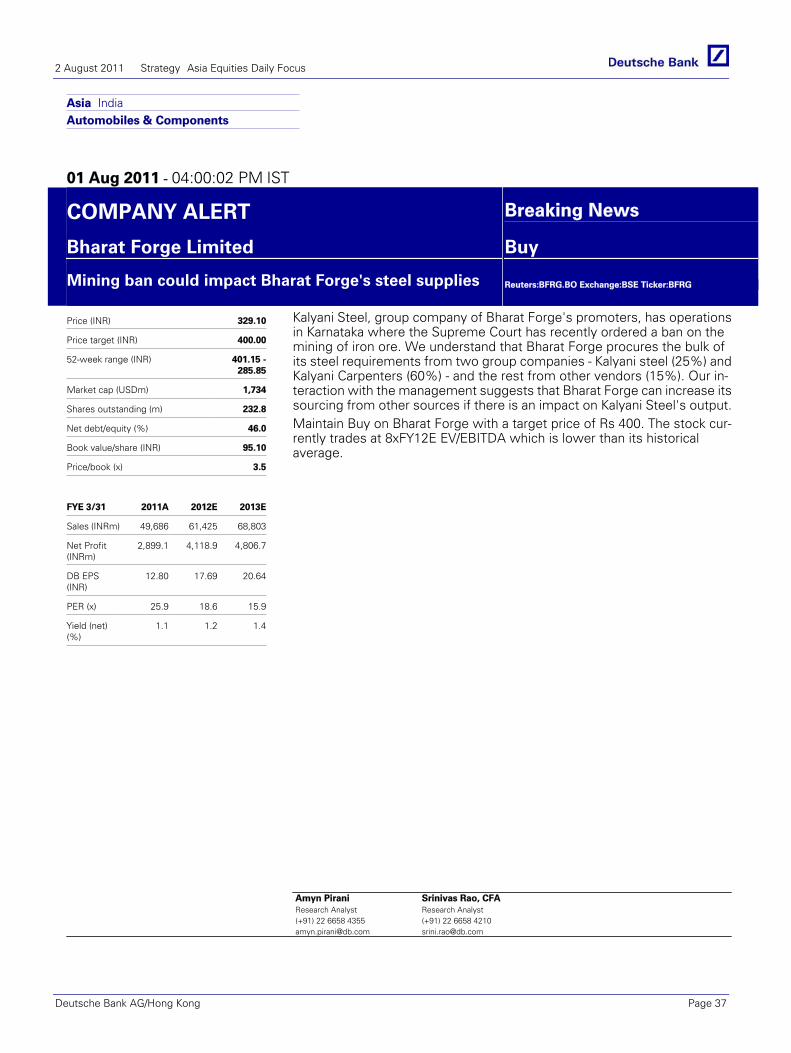

Bharat Forge Limited (BFRG.BO),INR315.80 Buy Price Target INR400.00

Mining ban could impact Bharat Forge's steel supplies

DB INTERNATIONAL PRODUCT ROADSHOWS

BAE Systems PLC (BA LN) - SG 8/2 Ben Fidler: Aerospace & Defence - HK 8/11, SG 8/12

Amyn Pirani

Page 37

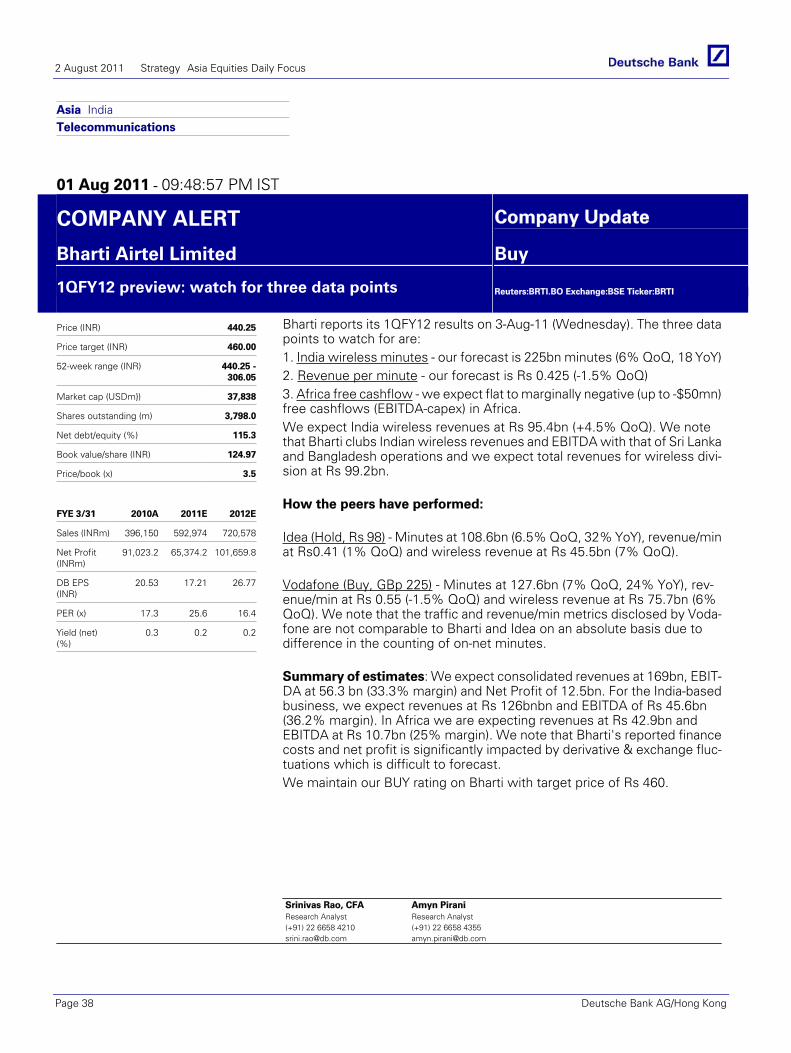

Bharti Airtel Limited (BRTI.BO) INR440.25 Buy Price Target INR460.00

1QFY12 preview: watch for three data points

Reinaldo Santana & Renata Coutinho: LatAm Retail - SG 8/29, HK 8/30, PEK 8/31, SEL 9/1 Matt Spick: Banks Northern Europe - SG 9/1 Elaine Dunphy: Pan European Oil & Gas - HK 9/14, SG 9/15 Warwick Okines : UK Retailers General - SG 9/16

Srinivas RaoPage 38

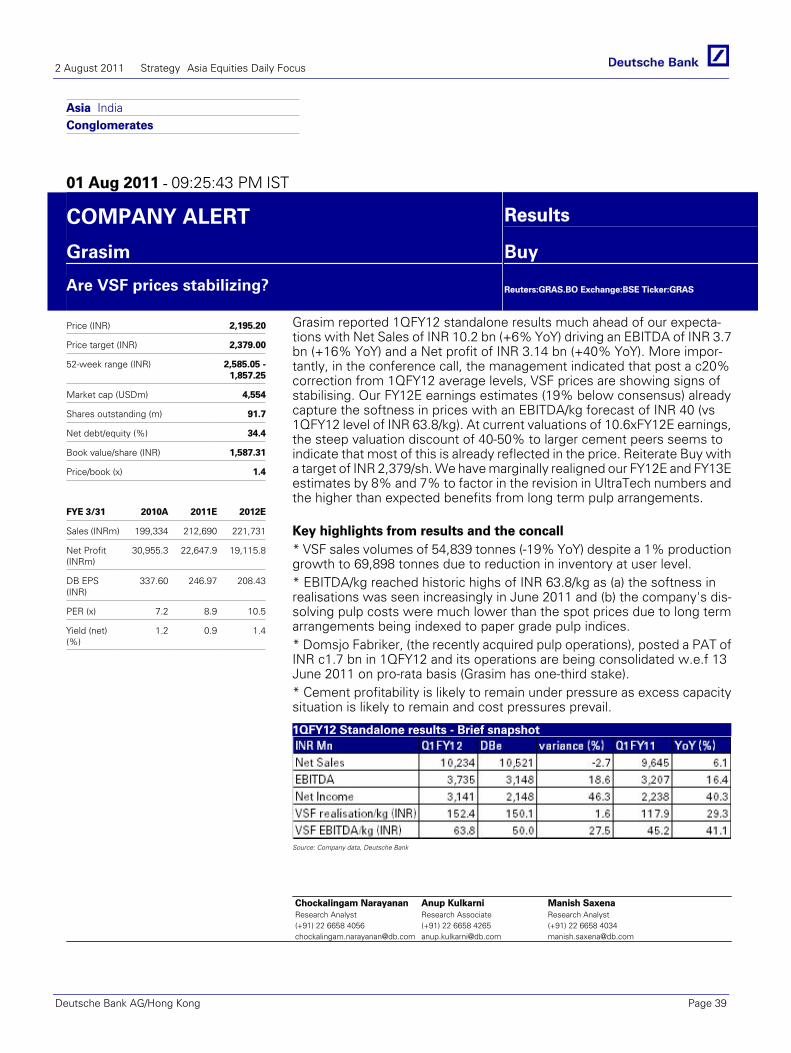

Grasim (GRAS.BO) INR2,195.20 Buy Price Target INR2,379.00

Are VSF prices stabilizing? Chockalingam Narayanan Page 39

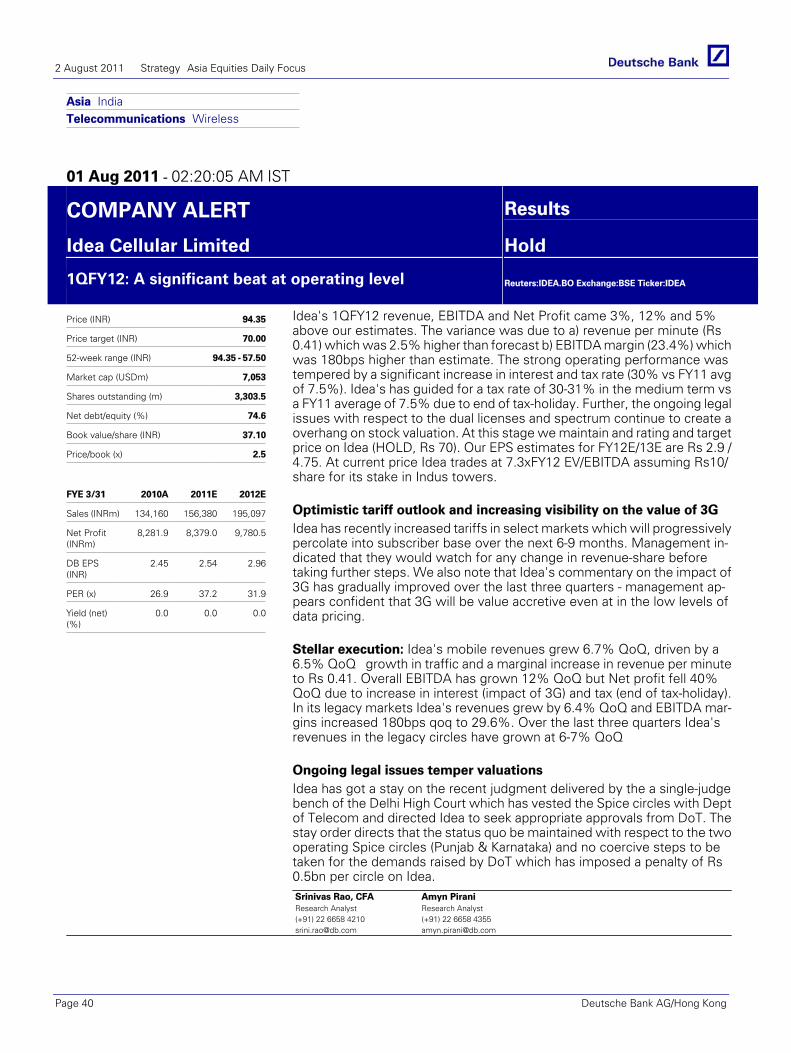

Idea Cellular Limited (IDEA.BO),INR98.25 Hold Price Target INR70.00

1QFY12: A significant beat at operating level

Srinivas RaoPage 40

Mahindra & Mahindra (MAHM.BO),INR730.55 Buy Price Target INR780.00

July 2011 volumes: strong numbers; unlike its peers

Srinivas Rao

Page 41

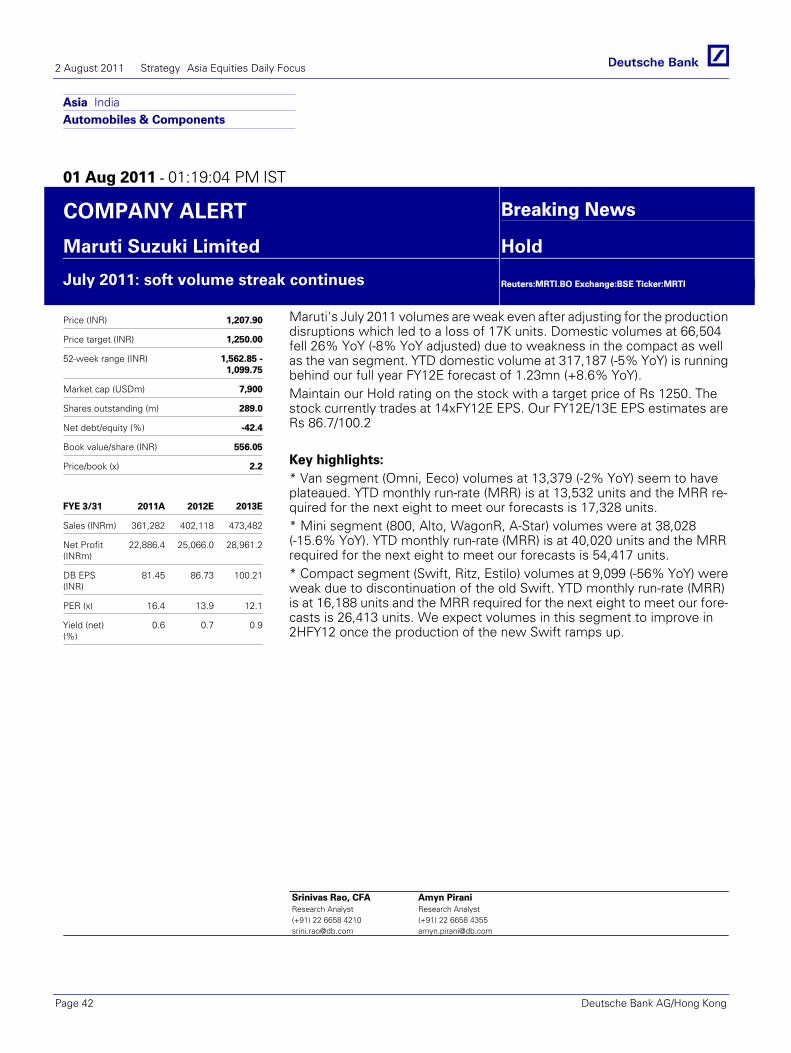

Maruti Suzuki Limited (MRTI.BO),INR1,208.75 Hold Price Target INR1,250.00

July 2011: soft volume streak continues

Srinivas Rao

Page 42

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 3

ADDITIONAL RESEARCH (cont’) Shree Cement (SHCM.BO) INR1,789.60 Hold Price Target INR1,712.00

Low pricing power with North Indian cement players-how long?

Chockalingam Narayanan Page 43

Steel Authority of India (SAIL.BO),INR119.95 Buy Price Target INR185.00

1Q'FY12 - Earnings disappoint on higher costs

Abhay Laijawala Page 44

Tata Motors Ltd (TAMO.BO) INR960.30 Buy Price Target INR1,365.00

July 2011: another month of slowdown in heavy truck volumes

Srinivas Rao

Page 45

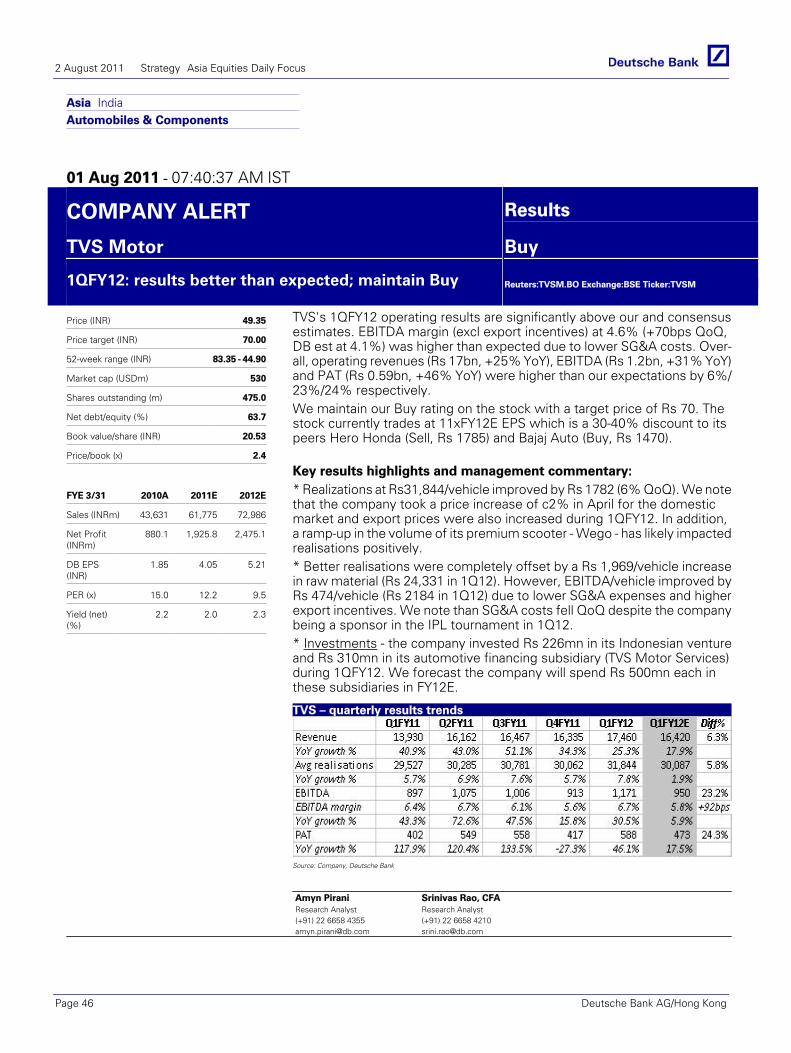

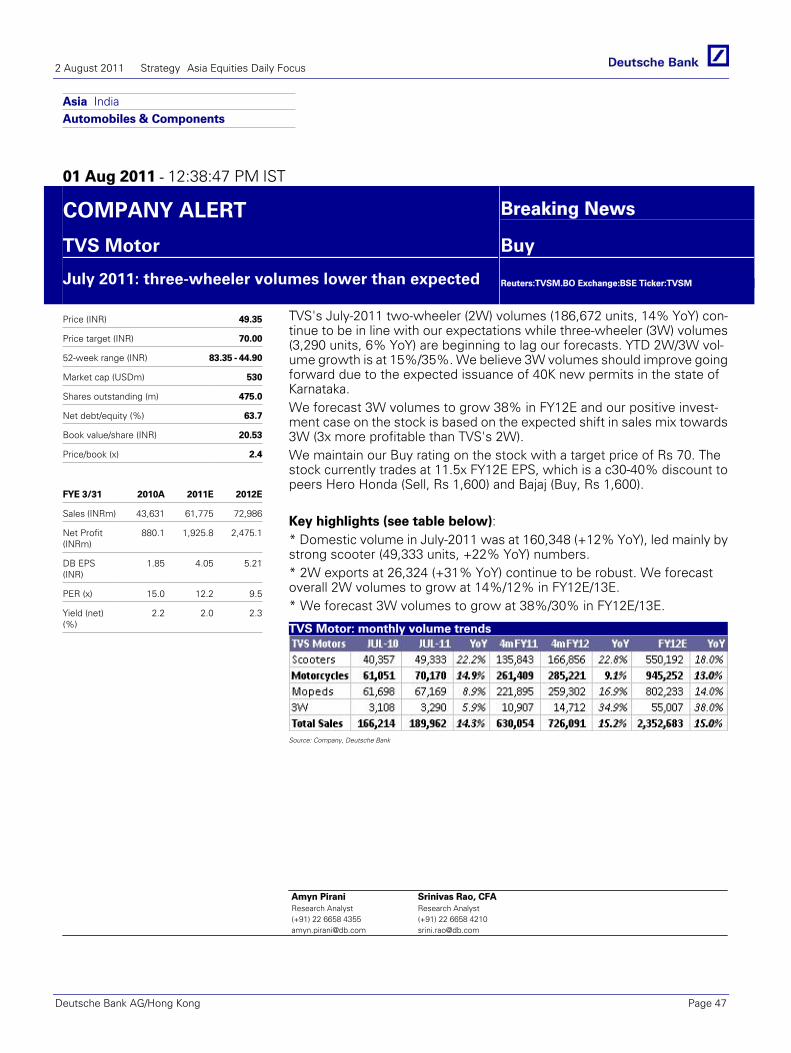

TVS Motor (TVSM.BO),INR53.45 Buy Price Target INR70.00

1QFY12: results better than expected; maintain Buy

Amyn PiraniPage 46

TVS Motor (TVSM.BO),INR53.45 Buy Price Target INR70.00

July 2011: three-wheeler volumes lower than expected

Amyn PiraniPage 47

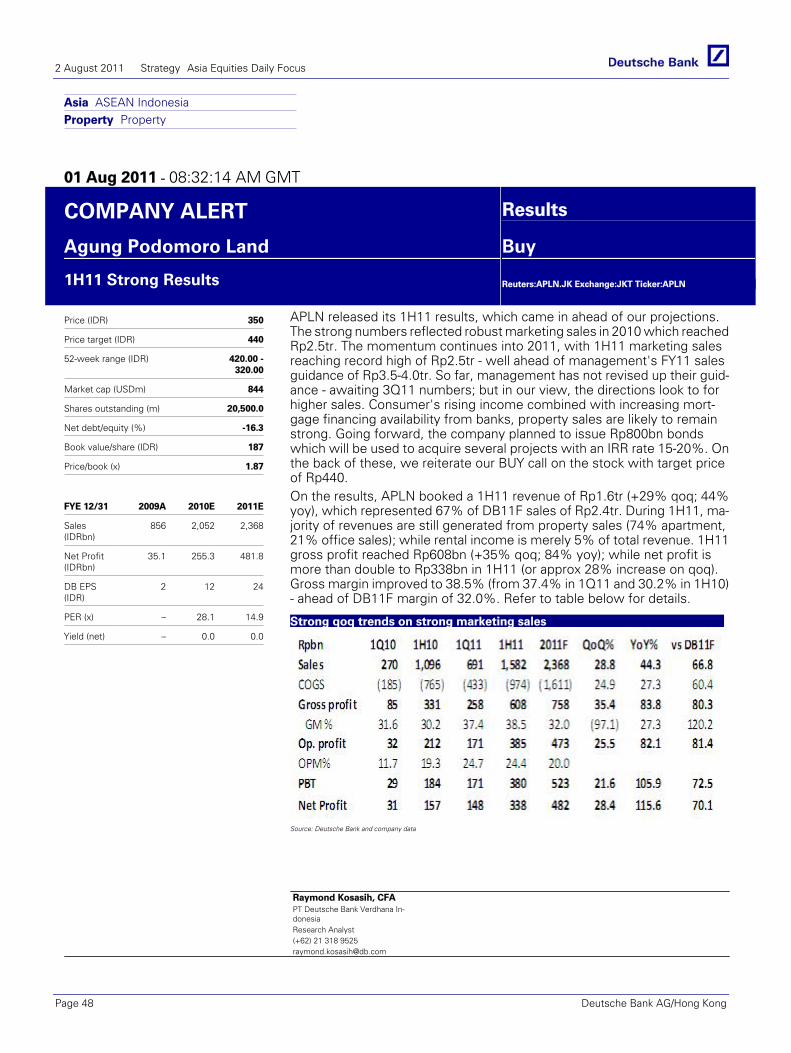

Agung Podomoro Land (APLN.JK),IDR390.00 Buy Price Target IDR440.00

1H11 Strong Results Raymond Kosasih Page 48

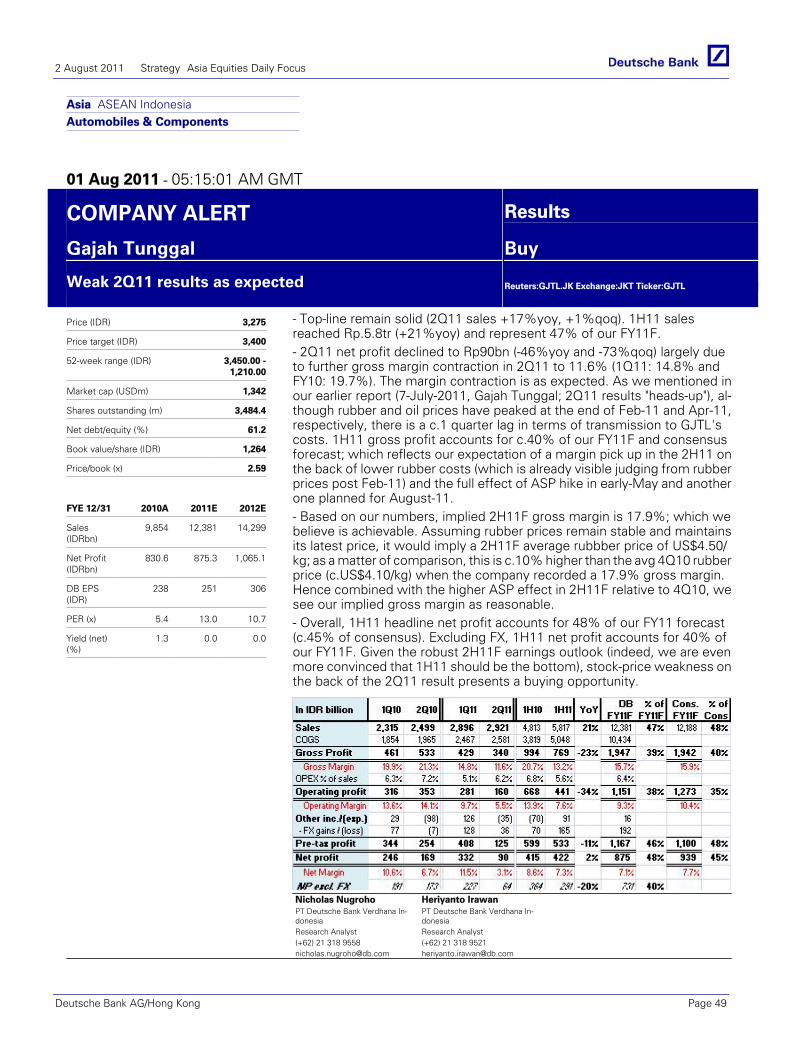

Gajah Tunggal (GJTL.JK),IDR3,125.00 Buy Price Target IDR3,400.00

Weak 2Q11 results as expected Nicholas Nugroho Page 49

Harum Energy (HRUM.JK) IDR9,700 Buy Price Target IDR11,000

2Q11 results; still largely tracking our forecast

Cherie KhoengPage 50

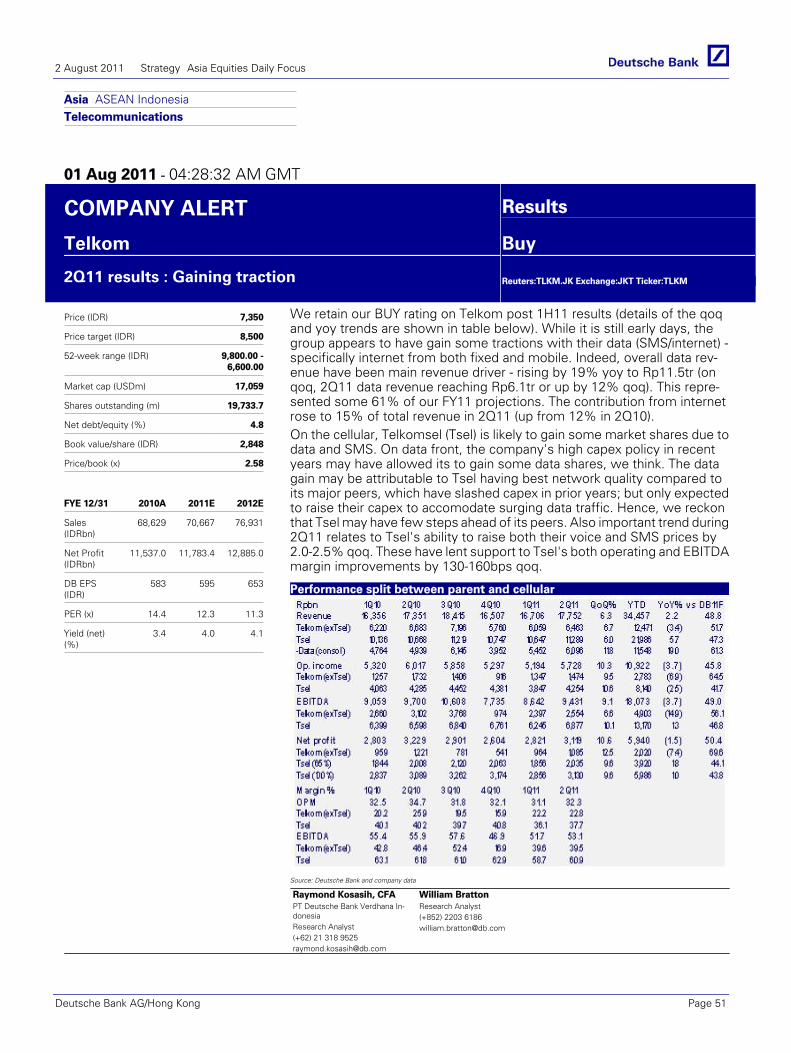

Telkom (TLKM.JK),IDR7,500.00 Buy Price Target IDR8,500.00

2Q11 results : Gaining traction Raymond Kosasih Page 51

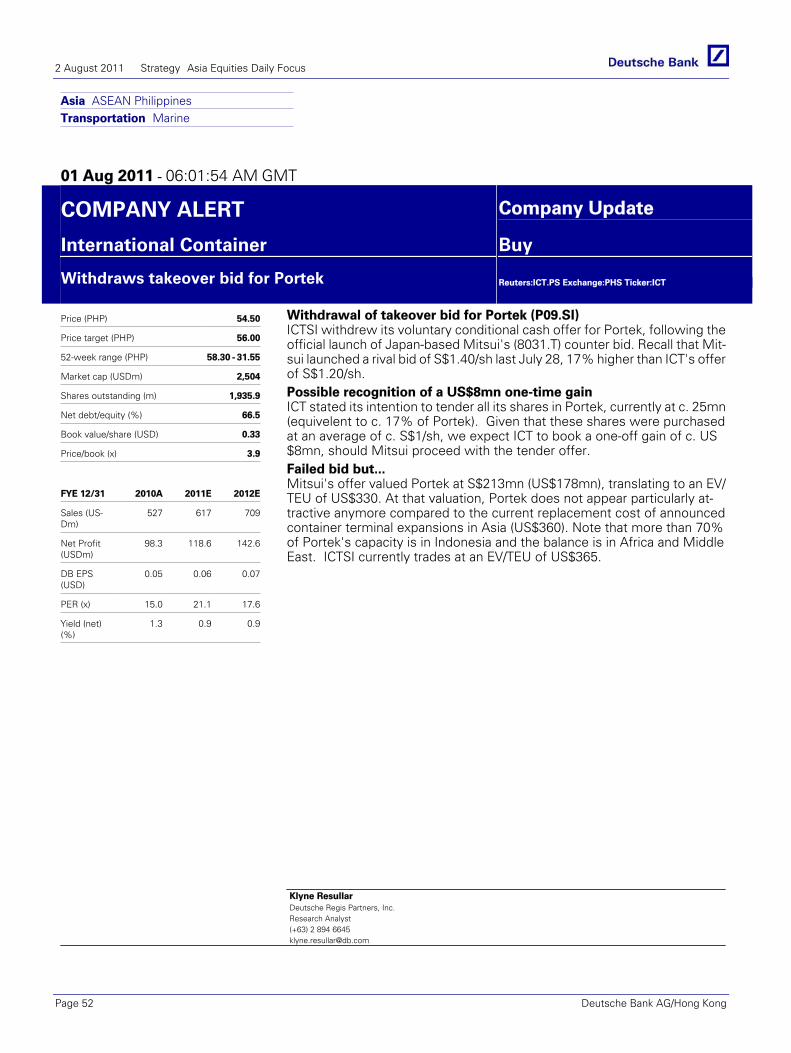

International Container (ICT.PS),PHP56.00 Buy Price Target PHP56.00

Withdraws takeover bid for Portek Klyne ResullarPage 52

SM Prime Holdings (SMPH.PS),PHP11.58 Hold Price Target PHP12.84

1H11 net profit up 14%, generally in line

Carl Sy

Page 53

Krung Thai Bank (KTB.BK),THB20.90 Buy Price Target THB25.00

KTB analyst meeting - affirmed positive outlook intact

Worawat Saisuphatphol Page 54

GLOBAL RESEARCH Pioneer (6773.T),¥413 Buy Price Target ¥530

Targeting renewed growth; upgrading rating to Buy (revised)

Yasuo NakanePage 55

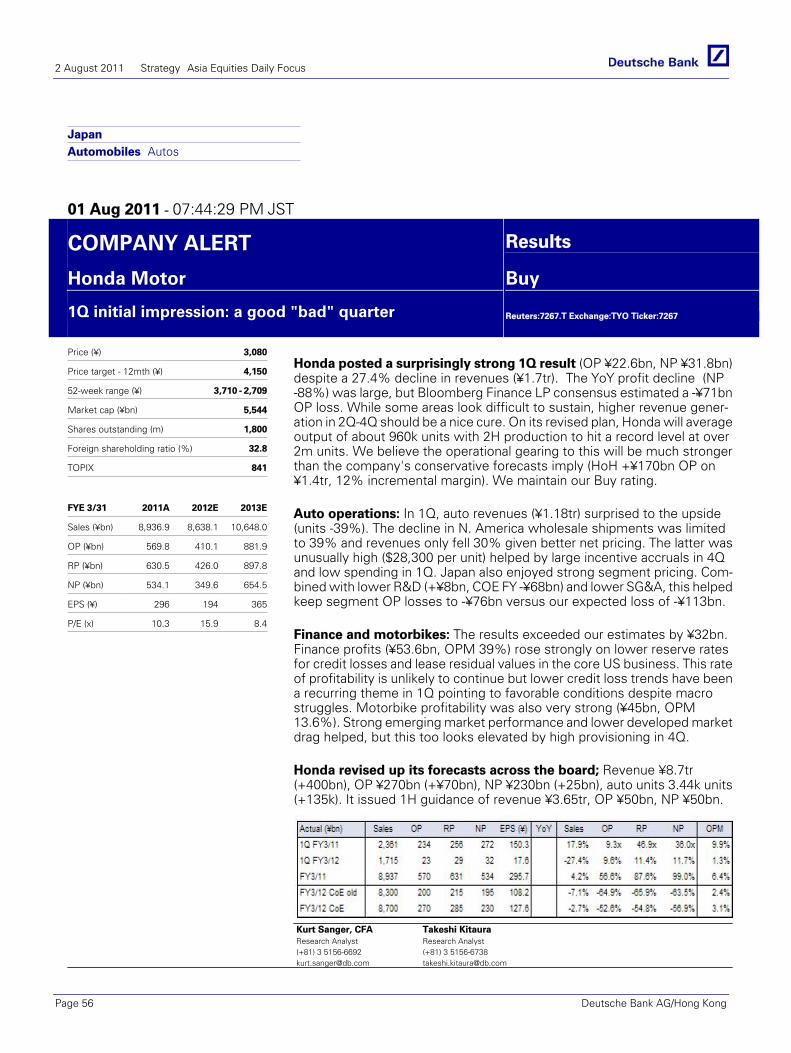

Honda Motor (7267.T),¥3,125 Buy Price Target ¥4,150

1Q initial impression: a good "bad" quarter

Kurt SangerPage 56

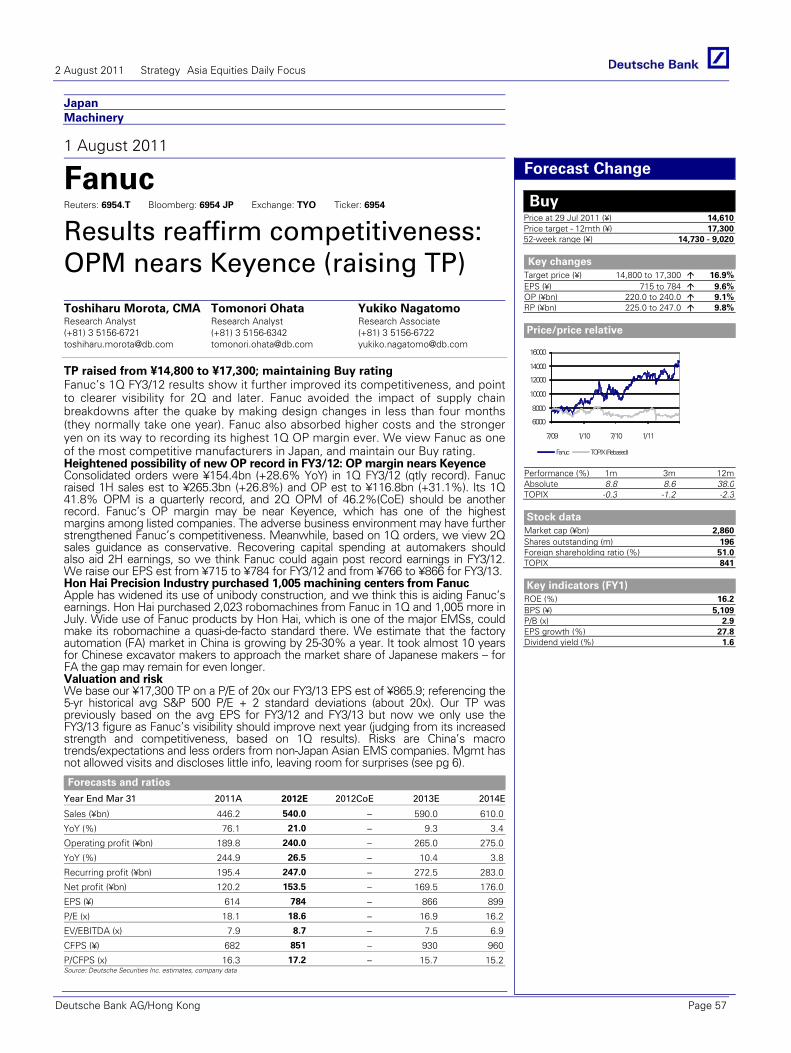

Fanuc (6954.T),¥15,280 Buy Price Target ¥17,300

Results reaffirm competitiveness: OPM nears Keyence (raising TP)

Toshiharu Morota Page 57

The notes and reports contained in this Daily are all excerpts of previously published documents. Please refer to the published notes on our web site for details on risks, valuations and earnings changes

2 August 2011 Strategy Asia Equities Daily Focus

Page 4 Deutsche Bank AG/Hong Kong

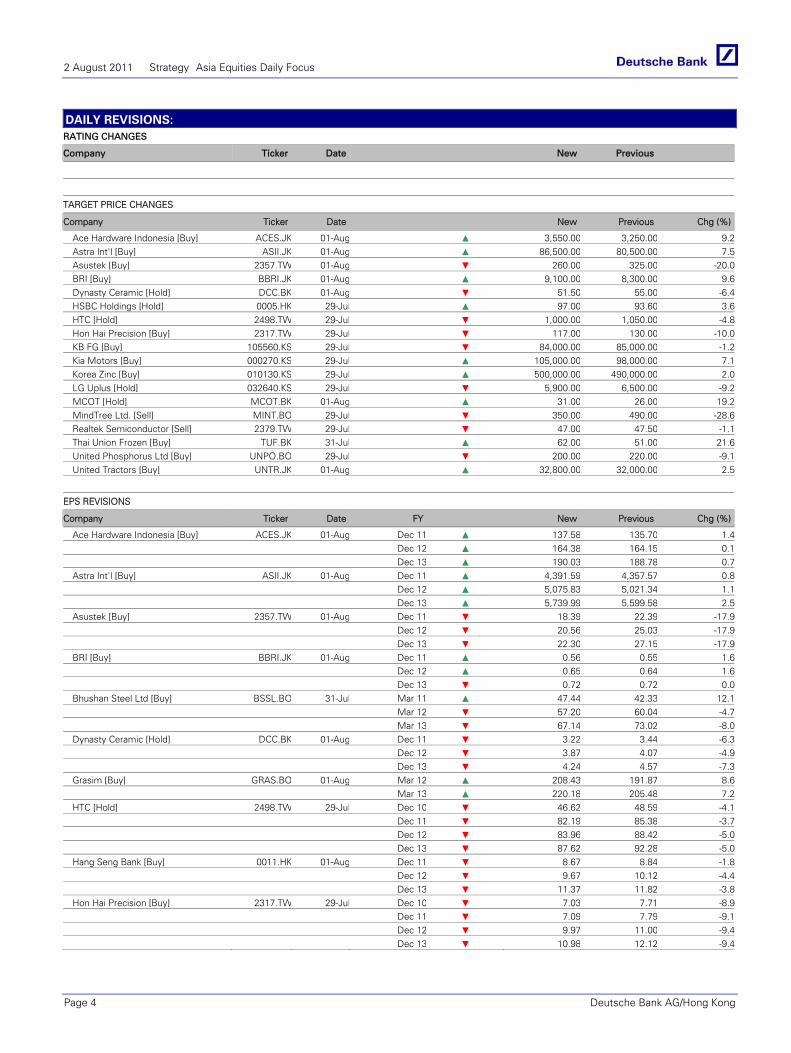

DAILY REVISIONS: RATING CHANGES

Company Ticker Date New Previous

TARGET PRICE CHANGES

Company Ticker Date New Previous Chg (%)

Ace Hardware Indonesia [Buy] ACES.JK 01-Aug ▲ 3,550.00 3,250.00 9.2Astra Int'l [Buy] ASII.JK 01-Aug ▲ 86,500.00 80,500.00 7.5Asustek [Buy] 2357.TW 01-Aug ▼ 260.00 325.00 -20.0BRI [Buy] BBRI.JK 01-Aug ▲ 9,100.00 8,300.00 9.6Dynasty Ceramic [Hold] DCC.BK 01-Aug ▼ 51.50 55.00 -6.4HSBC Holdings [Hold] 0005.HK 29-Jul ▲ 97.00 93.60 3.6HTC [Hold] 2498.TW 29-Jul ▼ 1,000.00 1,050.00 -4.8Hon Hai Precision [Buy] 2317.TW 29-Jul ▼ 117.00 130.00 -10.0KB FG [Buy] 105560.KS 29-Jul ▼ 84,000.00 85,000.00 -1.2Kia Motors [Buy] 000270.KS 29-Jul ▲ 105,000.00 98,000.00 7.1Korea Zinc [Buy] 010130.KS 29-Jul ▲ 500,000.00 490,000.00 2.0LG Uplus [Hold] 032640.KS 29-Jul ▼ 5,900.00 6,500.00 -9.2MCOT [Hold] MCOT.BK 01-Aug ▲ 31.00 26.00 19.2MindTree Ltd. [Sell] MINT.BO 29-Jul ▼ 350.00 490.00 -28.6Realtek Semiconductor [Sell] 2379.TW 29-Jul ▼ 47.00 47.50 -1.1Thai Union Frozen [Buy] TUF.BK 31-Jul ▲ 62.00 51.00 21.6United Phosphorus Ltd [Buy] UNPO.BO 29-Jul ▼ 200.00 220.00 -9.1United Tractors [Buy] UNTR.JK 01-Aug ▲ 32,800.00 32,000.00 2.5

EPS REVISIONS

Company Ticker Date FY New Previous Chg (%)

Ace Hardware Indonesia [Buy] ACES.JK 01-Aug Dec 11 ▲ 137.58 135.70 1.4 Dec 12 ▲ 164.38 164.15 0.1 Dec 13 ▲ 190.03 188.78 0.7Astra Int'l [Buy] ASII.JK 01-Aug Dec 11 ▲ 4,391.59 4,357.57 0.8 Dec 12 ▲ 5,075.83 5,021.34 1.1 Dec 13 ▲ 5,739.99 5,599.58 2.5Asustek [Buy] 2357.TW 01-Aug Dec 11 ▼ 18.39 22.39 -17.9 Dec 12 ▼ 20.56 25.03 -17.9 Dec 13 ▼ 22.30 27.15 -17.9BRI [Buy] BBRI.JK 01-Aug Dec 11 ▲ 0.56 0.55 1.6 Dec 12 ▲ 0.65 0.64 1.6 Dec 13 ▼ 0.72 0.72 0.0Bhushan Steel Ltd [Buy] BSSL.BO 31-Jul Mar 11 ▲ 47.44 42.33 12.1 Mar 12 ▼ 57.20 60.04 -4.7 Mar 13 ▼ 67.14 73.02 -8.0Dynasty Ceramic [Hold] DCC.BK 01-Aug Dec 11 ▼ 3.22 3.44 -6.3 Dec 12 ▼ 3.87 4.07 -4.9 Dec 13 ▼ 4.24 4.57 -7.3Grasim [Buy] GRAS.BO 01-Aug Mar 12 ▲ 208.43 191.87 8.6 Mar 13 ▲ 220.18 205.48 7.2HTC [Hold] 2498.TW 29-Jul Dec 10 ▼ 46.62 48.59 -4.1 Dec 11 ▼ 82.19 85.38 -3.7 Dec 12 ▼ 83.96 88.42 -5.0 Dec 13 ▼ 87.62 92.28 -5.0Hang Seng Bank [Buy] 0011.HK 01-Aug Dec 11 ▼ 8.67 8.84 -1.8 Dec 12 ▼ 9.67 10.12 -4.4 Dec 13 ▼ 11.37 11.82 -3.8Hon Hai Precision [Buy] 2317.TW 29-Jul Dec 10 ▼ 7.03 7.71 -8.9 Dec 11 ▼ 7.09 7.79 -9.1 Dec 12 ▼ 9.97 11.00 -9.4 Dec 13 ▼ 10.98 12.12 -9.4

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 5

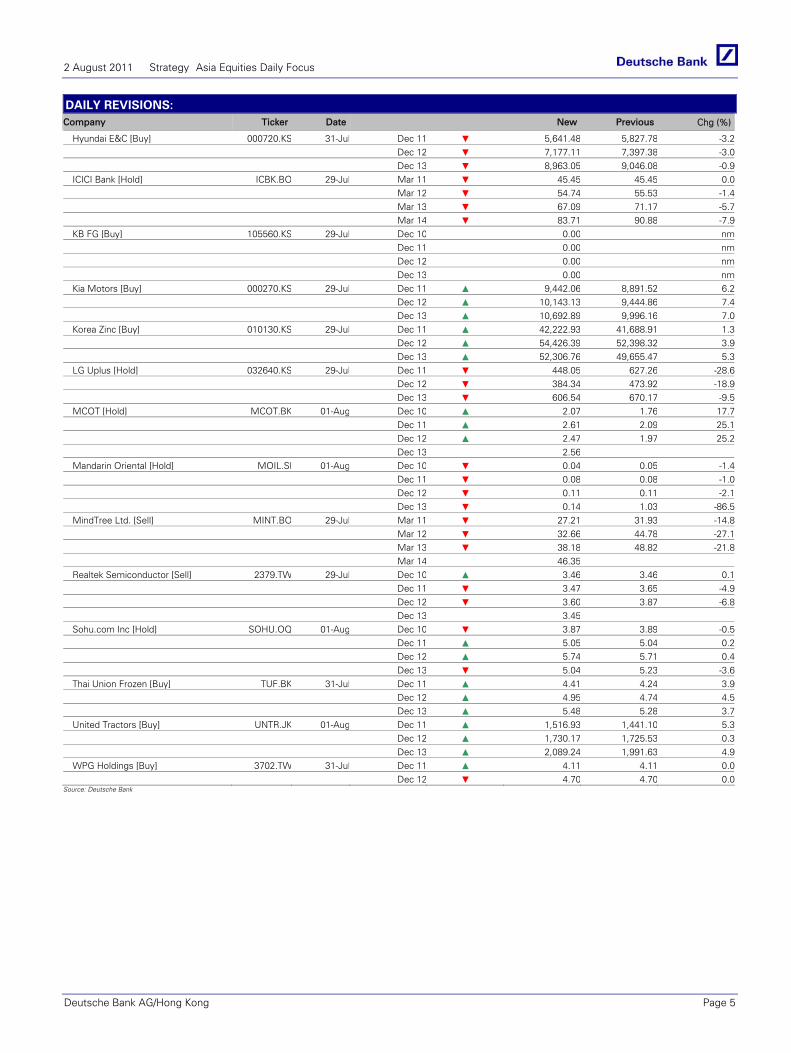

DAILY REVISIONS: Company Ticker Date New Previous Chg (%)

Hyundai E&C [Buy] 000720.KS 31-Jul Dec 11 ▼ 5,641.48 5,827.78 -3.2 Dec 12 ▼ 7,177.11 7,397.38 -3.0 Dec 13 ▼ 8,963.05 9,046.08 -0.9ICICI Bank [Hold] ICBK.BO 29-Jul Mar 11 ▼ 45.45 45.45 0.0 Mar 12 ▼ 54.74 55.53 -1.4 Mar 13 ▼ 67.09 71.17 -5.7 Mar 14 ▼ 83.71 90.88 -7.9KB FG [Buy] 105560.KS 29-Jul Dec 10 0.00 nm Dec 11 0.00 nm Dec 12 0.00 nm Dec 13 0.00 nmKia Motors [Buy] 000270.KS 29-Jul Dec 11 ▲ 9,442.06 8,891.52 6.2 Dec 12 ▲ 10,143.13 9,444.86 7.4 Dec 13 ▲ 10,692.89 9,996.16 7.0Korea Zinc [Buy] 010130.KS 29-Jul Dec 11 ▲ 42,222.93 41,688.91 1.3 Dec 12 ▲ 54,426.39 52,398.32 3.9 Dec 13 ▲ 52,306.76 49,655.47 5.3LG Uplus [Hold] 032640.KS 29-Jul Dec 11 ▼ 448.05 627.26 -28.6 Dec 12 ▼ 384.34 473.92 -18.9 Dec 13 ▼ 606.54 670.17 -9.5MCOT [Hold] MCOT.BK 01-Aug Dec 10 ▲ 2.07 1.76 17.7 Dec 11 ▲ 2.61 2.09 25.1 Dec 12 ▲ 2.47 1.97 25.2 Dec 13 2.56 Mandarin Oriental [Hold] MOIL.SI 01-Aug Dec 10 ▼ 0.04 0.05 -1.4 Dec 11 ▼ 0.08 0.08 -1.0 Dec 12 ▼ 0.11 0.11 -2.1 Dec 13 ▼ 0.14 1.03 -86.5MindTree Ltd. [Sell] MINT.BO 29-Jul Mar 11 ▼ 27.21 31.93 -14.8 Mar 12 ▼ 32.66 44.78 -27.1 Mar 13 ▼ 38.18 48.82 -21.8 Mar 14 46.35 Realtek Semiconductor [Sell] 2379.TW 29-Jul Dec 10 ▲ 3.46 3.46 0.1 Dec 11 ▼ 3.47 3.65 -4.9 Dec 12 ▼ 3.60 3.87 -6.8 Dec 13 3.45 Sohu.com Inc [Hold] SOHU.OQ 01-Aug Dec 10 ▼ 3.87 3.89 -0.5 Dec 11 ▲ 5.05 5.04 0.2 Dec 12 ▲ 5.74 5.71 0.4 Dec 13 ▼ 5.04 5.23 -3.6Thai Union Frozen [Buy] TUF.BK 31-Jul Dec 11 ▲ 4.41 4.24 3.9 Dec 12 ▲ 4.95 4.74 4.5 Dec 13 ▲ 5.48 5.28 3.7United Tractors [Buy] UNTR.JK 01-Aug Dec 11 ▲ 1,516.93 1,441.10 5.3 Dec 12 ▲ 1,730.17 1,725.53 0.3 Dec 13 ▲ 2,089.24 1,991.63 4.9WPG Holdings [Buy] 3702.TW 31-Jul Dec 11 ▲ 4.11 4.11 0.0 Dec 12 ▼ 4.70 4.70 0.0

Source: Deutsche Bank

Asia Hong Kong Banking/Finance Banks

29 July 2011

HSBC Holdings Reuters: 0005.HK Bloomberg: 5 HK Exchange: HKG Ticker: 0005

1H11 results preview

Tracy Yu Research Analyst (+852) 2203 6191 [email protected]

Jason Napier, CFA Research Analyst (+44) 20 754-74433 [email protected]

Sophia Lee, CFA Research Analyst (+852) 2203 6226 [email protected]

9.15am UK time, 4.15pm HK time, Monday 1 Aug 2011 HSBC reports results at 9.15am UK time or 4.15pm HK time on Mon 1 Aug. We expect PBT ex debt FV of US$11bn, or US$5.5bn for 2Q11 in line with 1Q11. We forecast core tier 1 ratio of 11.0%, EPS and DPS of 19cps and 9cps. We have cut our expectations for loan losses (Asia and North America) and the group tax rate, seeing our 11e, 12e and 13e EPS upgraded by 13%, 5% and 5% respectively. Our SOTP-driven target price rises to HK$97.0 from HK$93.6. We maintain our Hold rating as we expect HSBC to perform in line with MSCI Asia-ex JP Fin Index.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Net profit (USDm) 12,187.8 15,854.4 17,708.0 19,934.9 22,304.9

EPS (USD) 0.34 0.73 0.90 1.05 1.16

EPS growth (%) -39.4 21.1 8.7 10.2 9.6

PER (x) 33.7 14.0 11.1 9.4 8.6

Price/book (x) 1.56 1.28 1.18 1.12 1.05

DPS (net) (USD) 0.34 0.36 0.40 0.44 0.48

Yield (net) (%) 3.7 3.5 4.1 4.5 4.8

ROE (%) 5.1 9.4 10.9 12.2 12.7Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Results

Hold Price at 28 Jul 2011 (HKD) 77.35Price target - 12mth (HKD) 97.0052-week range (HKD) 91.75 - 74.75HANG SENG INDEX 22,571

Key changes

Price target 93.60 to 97.00 3.6%Provisioning (FYE) 12,088.6 to 10,914.9 -9.7%Net int margin (FYE) 2.61 to 2.55 -2.4%Net profit (FYE) 14,876.9 to 15,993.2 7.5%

Price/price relative

60

70

80

90

100

7/09 10/09 1/10 4/10 7/10 10/10 1/11 4/11HSBC Holdings

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute 2.5 -8.4 -4.4HANG SENG INDEX 2.3 -5.2 7.0

Stock data

Market cap (HKDm) 1,395,385Market cap (USDm) 179,071Shares outstanding (m) 17,756.4Major shareholders –Free float (%) 100Avg daily value traded (USDm) 214.9

Key indicators (FY1)

ROE (%) 10.9Loan/deposit ratio (%) 78.0Book value/share (USD) 8.39Price/book (x) 1.2NPL/total loans (%) 3.3Net int margin (%) 2.55

Margin, loan losses, costs, restructuring and run-off With HSBC's liquid balance sheet and capital strength taken for granted, we expect the focus on results day to be (i) net interest margin (stable through last year ex-BSM – will very rapid loan growth YTD see this lower in 2Q11?), credit quality (sustainability of low losses in high-book-growth Asia, trajectory for improvement in NA), and group restructuring (cost and breadth of cost cutting, magnitude of sold earnings in US cards and other non-core businesses).

Lower impairments, tax rate drives EPS upgrade, TP to HK$97.0, Hold Lower loan losses and lower tax rate in particular, see our 11e, 12e and 13e adj. EPS estimates rise by 13%, 5% and 5%. This leaves HSBC trading at 9.3x 2012 and 1.5x 2011 TNAV, as shown in Figure 6. Our target price is derived by sum of the parts, and increases to HK$97.0 from HK$93.6 driven by the EPS upgrades. We maintain our Hold rating on the stock as the strong business prospects in Asia are offset by growth concerns in the western markets.

Valuation and risks Our TP is derived by sum of the parts, and increases to HK$97.0 from HK$93.6 driven by the EPS upgrades. Share price upside risk derives from better than expected top line momentum, most likely driven by global markets or interest rate sensitivity. Downside risk derives from rising loan losses and weaker than expected margin and cost conditions in PFS and GBM in particular. (See page 6 for details).

2 August 2011 Strategy Asia Equities Daily Focus

Page 6 Deutsche Bank AG/Hong Kong

Asia Hong Kong Banking/Finance Banks

1 August 2011

Hang Seng Bank Reuters: 0011.HK Bloomberg: 11 HK Exchange: HKG Ticker: 0011

1H11 results; strong capital and return of conservatismSophia Lee, CFA Research Analyst (+852) 2203 6226 [email protected]

Tracy Yu Research Analyst (+852) 2203 6191 [email protected]

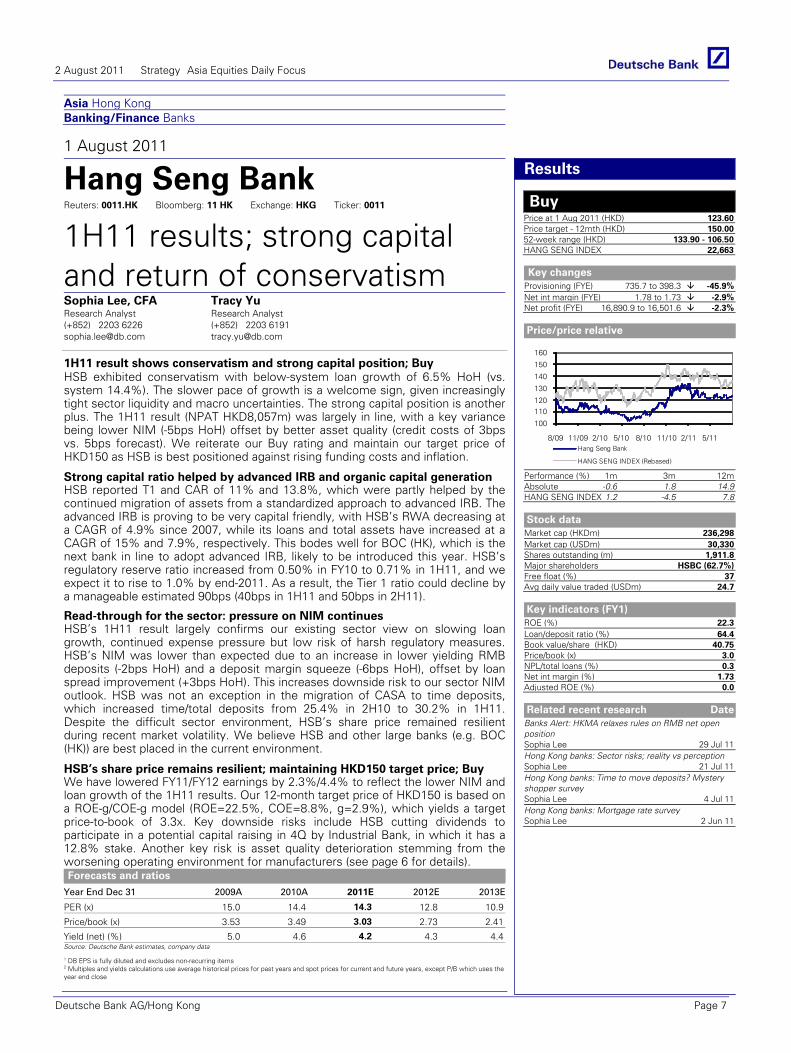

1H11 result shows conservatism and strong capital position; Buy HSB exhibited conservatism with below-system loan growth of 6.5% HoH (vs. system 14.4%). The slower pace of growth is a welcome sign, given increasingly tight sector liquidity and macro uncertainties. The strong capital position is another plus. The 1H11 result (NPAT HKD8,057m) was largely in line, with a key variance being lower NIM (-5bps HoH) offset by better asset quality (credit costs of 3bps vs. 5bps forecast). We reiterate our Buy rating and maintain our target price of HKD150 as HSB is best positioned against rising funding costs and inflation.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

PER (x) 15.0 14.4 14.3 12.8 10.9

Price/book (x) 3.53 3.49 3.03 2.73 2.41

Yield (net) (%) 5.0 4.6 4.2 4.3 4.4Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Results

Buy Price at 1 Aug 2011 (HKD) 123.60Price target - 12mth (HKD) 150.0052-week range (HKD) 133.90 - 106.50HANG SENG INDEX 22,663

Key changes

Provisioning (FYE) 735.7 to 398.3 -45.9%Net int margin (FYE) 1.78 to 1.73 -2.9%Net profit (FYE) 16,890.9 to 16,501.6 -2.3%

Price/price relative

100

110120

130

140

150

160

8/09 11/09 2/10 5/10 8/10 11/10 2/11 5/11Hang Seng Bank

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute -0.6 1.8 14.9HANG SENG INDEX 1.2 -4.5 7.8

Stock data

Market cap (HKDm) 236,298Market cap (USDm) 30,330Shares outstanding (m) 1,911.8Major shareholders HSBC (62.7%)Free float (%) 37Avg daily value traded (USDm) 24.7

Key indicators (FY1)

ROE (%) 22.3Loan/deposit ratio (%) 64.4Book value/share (HKD) 40.75Price/book (x) 3.0NPL/total loans (%) 0.3Net int margin (%) 1.73Adjusted ROE (%) 0.0

Related recent research Date

Banks Alert: HKMA relaxes rules on RMB net open position Sophia Lee 29 Jul 11Hong Kong banks: Sector risks; reality vs perception Sophia Lee 21 Jul 11Hong Kong banks: Time to move deposits? Mystery shopper survey Sophia Lee 4 Jul 11Hong Kong banks: Mortgage rate survey Sophia Lee 2 Jun 11

Strong capital ratio helped by advanced IRB and organic capital generation HSB reported T1 and CAR of 11% and 13.8%, which were partly helped by the continued migration of assets from a standardized approach to advanced IRB. The advanced IRB is proving to be very capital friendly, with HSB’s RWA decreasing at a CAGR of 4.9% since 2007, while its loans and total assets have increased at a CAGR of 15% and 7.9%, respectively. This bodes well for BOC (HK), which is the next bank in line to adopt advanced IRB, likely to be introduced this year. HSB’s regulatory reserve ratio increased from 0.50% in FY10 to 0.71% in 1H11, and we expect it to rise to 1.0% by end-2011. As a result, the Tier 1 ratio could decline by a manageable estimated 90bps (40bps in 1H11 and 50bps in 2H11).

Read-through for the sector: pressure on NIM continues HSB’s 1H11 result largely confirms our existing sector view on slowing loan growth, continued expense pressure but low risk of harsh regulatory measures. HSB’s NIM was lower than expected due to an increase in lower yielding RMB deposits (-2bps HoH) and a deposit margin squeeze (-6bps HoH), offset by loan spread improvement (+3bps HoH). This increases downside risk to our sector NIM outlook. HSB was not an exception in the migration of CASA to time deposits, which increased time/total deposits from 25.4% in 2H10 to 30.2% in 1H11. Despite the difficult sector environment, HSB’s share price remained resilient during recent market volatility. We believe HSB and other large banks (e.g. BOC (HK)) are best placed in the current environment.

HSB’s share price remains resilient; maintaining HKD150 target price; Buy We have lowered FY11/FY12 earnings by 2.3%/4.4% to reflect the lower NIM and loan growth of the 1H11 results. Our 12-month target price of HKD150 is based on a ROE-g/COE-g model (ROE=22.5%, COE=8.8%, g=2.9%), which yields a target price-to-book of 3.3x. Key downside risks include HSB cutting dividends to participate in a potential capital raising in 4Q by Industrial Bank, in which it has a 12.8% stake. Another key risk is asset quality deterioration stemming from the worsening operating environment for manufacturers (see page 6 for details).

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 7

Asia TaiwanTechnology Hardware & Equipment

01 Aug 2011 - 08:23:06 AM CST

COMPANY ALERT Forecast Change

Asustek Buy

Ex-dividend target price adjustment

Reuters:2357.TW Exchange:TAI Ticker:2357

Price (TWD) 232.00

Price target (TWD) 260.00

52-week range (TWD) 310.50 -210.00

Market cap (USDm) 5,125

Shares outstanding (m) 752.8

Net debt/equity (%) -38.7

Book value/share (TWD) 154.94

Price/book (x) 1.50

FYE 12/31 2010A 2011E 2012E

Sales(TWDm)

321,251 327,800 374,240

Net Profit(TWDm)

16,487.6 13,975.1 15,621.9

DB EPS(TWD)

7.60 18.39 20.56

PER (x) 33.2 12.6 11.3

Yield (net)(%)

1.5 4.0 4.4

We have adjusted Asustek's target price to NT$260 (from NT$330) to reflectthe change in shares to 760m (from 624m) and 11E-12E EPS changes to NT$18.4-NT$20.6 (from NT$22.4-NT$25) due to the stock dividend issued in3Q11.We do not change our 11E-13E net income estimates or valuationmethod for Asustek.Our NT$260 price target is based on SOTP valuation: NT$218 for Asustek'score business (12x target P/E and 2012E brand EPS of NT$18.2, in line withthe company's mid-cycle valuation), NT$21 for its Pegatron holdings (basedon Asustek's holding of 24% and Pegatron's current share price) and NT$21 for excess cash (based on 35% of Asustek's NT$43bn net cash).Key risks for Asustek include: 1) failure to expand NB market share, owingto less-competitive products and weaker channel relations; 2) higher-than-expected costs associated with new projects (e.g. tablet PC), which couldlead to a lower-than-expected operating margin; 3) higher-than-expectediPad cannibalization effect, which could lead to lower netbook/NB ship-ments; 4) slower-than-expected NB outsourcing trend, which could lead tolower operating margins.

Kc Kao, MBAResearch Analyst(+886) 2 2192 [email protected]

Ivy LeeResearch Analyst(+886) 2 2192 [email protected]

2 August 2011 Strategy Asia Equities Daily Focus

Page 8 Deutsche Bank AG/Hong Kong

Asia ASEAN IndonesiaConsumer Retail/Wholesale Trade

01 Aug 2011 - 08:01:54 AM GMT

COMPANY ALERT Company Update

Ace Hardware Indonesia Buy

In-line 2Q11 with net profit +34% YoY, but rising SG&Acosts

Reuters:ACES.JK Exchange:JKT Ticker:ACES

Price (IDR) 3,450

Price target (IDR) 3,550

52-week range (IDR) 3,550.00 -1,770.00

Market cap (USDm) 696

Shares outstanding (m) 1,715,000.0

Net debt/equity (%) -34.5

Book value/share (IDR) 664

Price/book (x) 5.20

FYE 12/31 2010A 2011E 2012E

Sales(IDRbn)

1,690 2,238 2,677

Net Profit(IDRbn)

177.9 232.1 281.9

DB EPS(IDR)

105 138 164

PER (x) 18.0 25.1 21.0

Yield (net)(%)

0.5 1.5 0.6

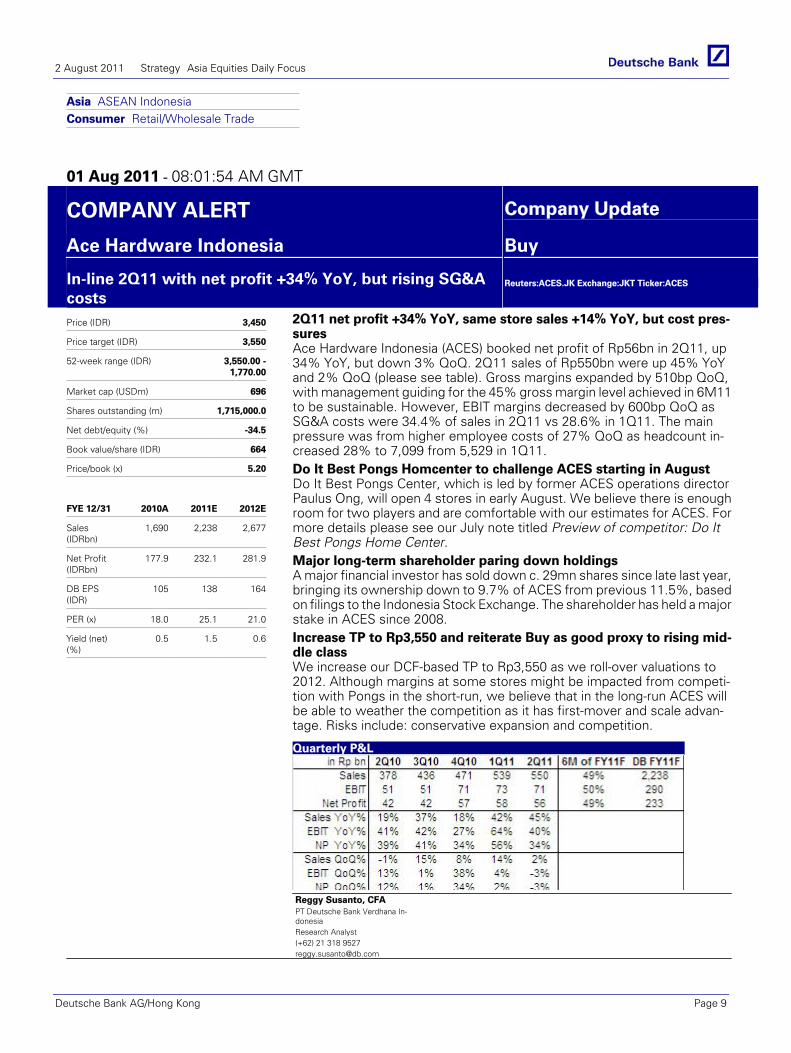

2Q11 net profit +34% YoY, same store sales +14% YoY, but cost pres-suresAce Hardware Indonesia (ACES) booked net profit of Rp56bn in 2Q11, up34% YoY, but down 3% QoQ. 2Q11 sales of Rp550bn were up 45% YoYand 2% QoQ (please see table). Gross margins expanded by 510bp QoQ,with management guiding for the 45% gross margin level achieved in 6M11to be sustainable. However, EBIT margins decreased by 600bp QoQ asSG&A costs were 34.4% of sales in 2Q11 vs 28.6% in 1Q11. The mainpressure was from higher employee costs of 27% QoQ as headcount in-creased 28% to 7,099 from 5,529 in 1Q11.Do It Best Pongs Homcenter to challenge ACES starting in AugustDo It Best Pongs Center, which is led by former ACES operations directorPaulus Ong, will open 4 stores in early August. We believe there is enoughroom for two players and are comfortable with our estimates for ACES. Formore details please see our July note titled Preview of competitor: Do ItBest Pongs Home Center. Major long-term shareholder paring down holdingsA major financial investor has sold down c. 29mn shares since late last year,bringing its ownership down to 9.7% of ACES from previous 11.5%, basedon filings to the Indonesia Stock Exchange. The shareholder has held a majorstake in ACES since 2008.Increase TP to Rp3,550 and reiterate Buy as good proxy to rising mid-dle classWe increase our DCF-based TP to Rp3,550 as we roll-over valuations to2012. Although margins at some stores might be impacted from competi-tion with Pongs in the short-run, we believe that in the long-run ACES willbe able to weather the competition as it has first-mover and scale advan-tage. Risks include: conservative expansion and competition.

Quarterly P&L

Source: Deutsche Bank and company data

Reggy Susanto, CFAPT Deutsche Bank Verdhana In-donesiaResearch Analyst(+62) 21 318 [email protected]

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 9

Asia ASEAN IndonesiaConsumer Retail/Wholesale Trade

01 Aug 2011 - 09:54:06 AM GMT

COMPANY ALERT Company Update

Ace Hardware Indonesia Buy

Impact & preview of competitor: Do It Best Pongs HomeCenter

Reuters:ACES.JK Exchange:JKT Ticker:ACES

Price (IDR) 3,450

Price target (IDR) 3,550

52-week range (IDR) 3,550.00 -1,770.00

Market cap (USDm) 696

Shares outstanding (m) 1,715,000.0

Net debt/equity (%) -34.5

Book value/share (IDR) 664

Price/book (x) 5.20

FYE 12/31 2010A 2011E 2012E

Sales(IDRbn)

1,690 2,238 2,677

Net Profit(IDRbn)

177.9 232.1 281.9

DB EPS(IDR)

105 138 164

PER (x) 18.0 25.1 21.0

Yield (net)(%)

0.5 1.5 0.6

Preview of Do It Best Pongs Home CenterWe had the privilege of having Paulus Ong, the founder and namesake ofPongs Home Center, give us a preview of his store. Mr. Paulus previouslyspent the past 10 years at Ace Hardware Indonesia, most recently as thedirector in charge of sales operation, distribution and store expansion. Heaims to open 4 Pongs stores in the first week of August and be c. 9% ofACES's store space by year-end. All of the Pongs stores scheduled to beopened will be in a vicinity of an existing ACES store. Pongs aims to open40 stores by 2015 vs the 67 that we expect ACES to have by that time(please see table).However, Mr. Paulus made clear that his aim was to growtogether with ACES, and not to compete aggressively, as he believes thereis enough room for two players.Pongs Home Center to provide "More Brands, More Choices"Pongs's main point of differentiation will be to offer a more diverse rangeof brands than ACES at competitive prices. They will aim to offer 65,000SKUs from 1,000 brands. The product categories will be similar to ACES,but will also include furniture, which is being done by ACES's sister com-pany Informa, and toys, which is being done by ACES's subsidiary ToysKingdom.Background of Paulus OngMr. Paulus entered ACES as a General Manager in 2001, when there were8 stores, and was appointed as Operations Director in 2005, when therewas 12 stores. During his time as a director, revenues grew nearly 5x as hespearheaded the opening of 34 stores.Maintain Buy on ACESWe believe that ACES's long-term prospects remain attractive as we be-lieve there is enough room for growth even with two players. ACES man-agement remains confident of margins and expansion prospects even inthe face of direct competition.

Comparison of Do It Best Pongs Home Center and ACES

Source: Deutsche Bank and company data

Reggy Susanto, CFAPT Deutsche Bank Verdhana In-donesiaResearch Analyst(+62) 21 318 [email protected]

2 August 2011 Strategy Asia Equities Daily Focus

Page 10 Deutsche Bank AG/Hong Kong

Asia ASEAN IndonesiaConglomerates

01 Aug 2011 - 06:41:44 AM GMT

COMPANY ALERT Forecast Change

Astra Int'l Buy

Raising automotive forecasts

Reuters:ASII.JK Exchange:JKT Ticker:ASII

Price (IDR) 70,500

Price target (IDR) 86,500

52-week range (IDR) 75,000.00 -46,500.00

Market cap (USDm) 33,568

Shares outstanding (m) 4,048.4

Net debt/equity (%) 35.4

Book value/share (IDR) 15,354

Price/book (x) 4.59

FYE 12/31 2010A 2011E 2012E

Sales(IDRbn)

129,991 152,253 171,350

Net Profit(IDRbn)

14,366.0 17,778.7 20,548.8

DB EPS(IDR)

3,549 4,392 5,076

PER (x) 13.2 16.1 13.9

Yield (net)(%)

2.7 1.4 1.7

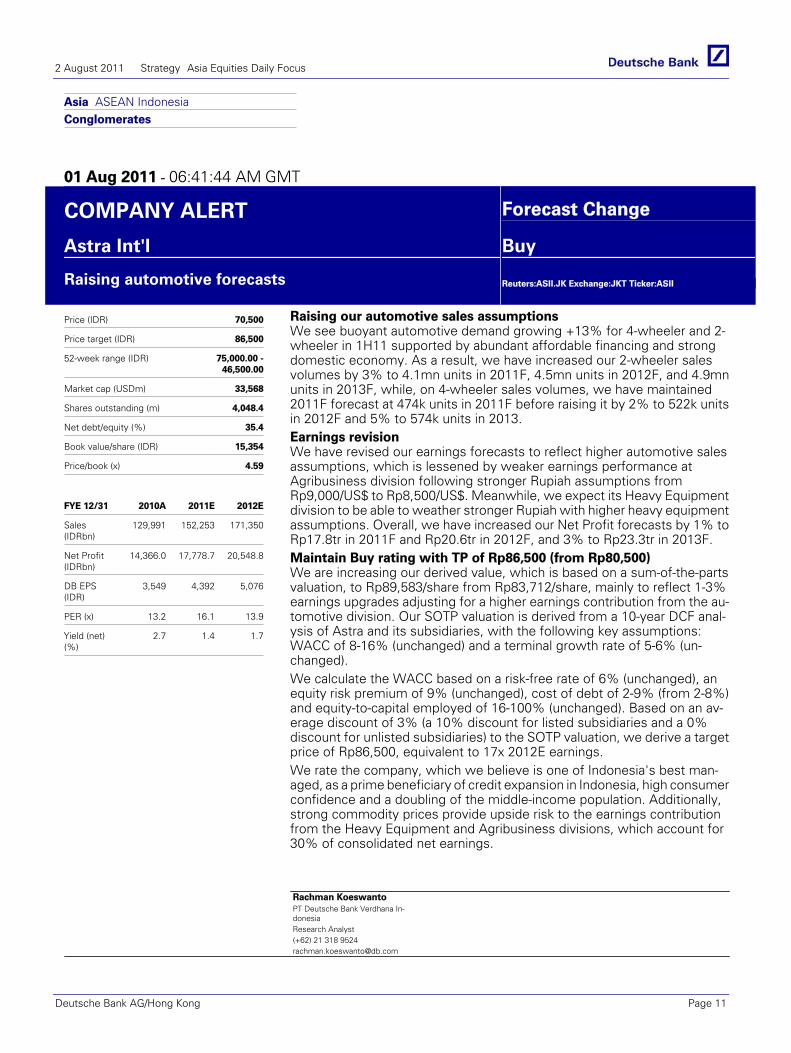

Raising our automotive sales assumptionsWe see buoyant automotive demand growing +13% for 4-wheeler and 2-wheeler in 1H11 supported by abundant affordable financing and strongdomestic economy. As a result, we have increased our 2-wheeler salesvolumes by 3% to 4.1mn units in 2011F, 4.5mn units in 2012F, and 4.9mnunits in 2013F, while, on 4-wheeler sales volumes, we have maintained2011F forecast at 474k units in 2011F before raising it by 2% to 522k unitsin 2012F and 5% to 574k units in 2013.Earnings revisionWe have revised our earnings forecasts to reflect higher automotive salesassumptions, which is lessened by weaker earnings performance atAgribusiness division following stronger Rupiah assumptions fromRp9,000/US$ to Rp8,500/US$. Meanwhile, we expect its Heavy Equipmentdivision to be able to weather stronger Rupiah with higher heavy equipmentassumptions. Overall, we have increased our Net Profit forecasts by 1% toRp17.8tr in 2011F and Rp20.6tr in 2012F, and 3% to Rp23.3tr in 2013F.Maintain Buy rating with TP of Rp86,500 (from Rp80,500)We are increasing our derived value, which is based on a sum-of-the-partsvaluation, to Rp89,583/share from Rp83,712/share, mainly to reflect 1-3%earnings upgrades adjusting for a higher earnings contribution from the au-tomotive division. Our SOTP valuation is derived from a 10-year DCF anal-ysis of Astra and its subsidiaries, with the following key assumptions:WACC of 8-16% (unchanged) and a terminal growth rate of 5-6% (un-changed).We calculate the WACC based on a risk-free rate of 6% (unchanged), anequity risk premium of 9% (unchanged), cost of debt of 2-9% (from 2-8%)and equity-to-capital employed of 16-100% (unchanged). Based on an av-erage discount of 3% (a 10% discount for listed subsidiaries and a 0%discount for unlisted subsidiaries) to the SOTP valuation, we derive a targetprice of Rp86,500, equivalent to 17x 2012E earnings.We rate the company, which we believe is one of Indonesia's best man-aged, as a prime beneficiary of credit expansion in Indonesia, high consumerconfidence and a doubling of the middle-income population. Additionally,strong commodity prices provide upside risk to the earnings contributionfrom the Heavy Equipment and Agribusiness divisions, which account for30% of consolidated net earnings.

Rachman KoeswantoPT Deutsche Bank Verdhana In-donesiaResearch Analyst(+62) 21 318 [email protected]

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 11

Asia ASEAN Indonesia Banking/Finance

1 August 2011

BRI Reuters: BBRI.JK Bloomberg: BBRI IJ Exchange: JKT Ticker: BBRI

Banking on micro; upgrading target price to Rp9,100Raymond Kosasih, CFA PT Deutsche Bank Verdhana Indonesia Research Analyst (+62) 21 318 9525 [email protected]

Arinta Harsono PT Deutsche Bank Verdhana Indonesia Research Analyst (+62) 21 318 9519 [email protected]

Back to basics; raising target price raised to Rp9,100; maintaining Buy A key message from 1H11 results is the bank's renewed focus on micro loans as a source of growth, which is consistent with our view (refer to 'BRI - Capital preservation and better earnings visibility', 2 March). The bank has accelerated micro expansions, with micro unit opening targets doubling to 200 and Teras rising from 600 to 700. This will not only support the bank's financial de-leveraging (hence preserving its capital), but also should maintain its high ROAE. We retain Buy and are raising our target price to Rp9,100 (using 2012F book as a reference).

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Provisioning (IDRbn) 5,798.9 7,917.4 7,334.8 8,801.8 10,757.8

Pre-prov profit (IDRbn) 15,547 22,673 24,492 28,895 33,024

Net profit (IDRbn) 7,308.3 11,472.4 13,725.6 16,074.5 17,812.6

EPS (IDR) 296.42 465.23 556.60 651.85 722.34

EPS growth (%) 22.6 56.9 19.6 17.1 10.8

PER (x) 10.5 10.0 12.9 11.0 10.0

Price/book (x) 3.5 3.5 3.7 2.9 2.3

Yield (net) (%) 4.1 2.3 1.6 1.9 1.8

ROE (%) 29.5 35.9 32.4 29.3 25.9Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Company Update

Buy Price at 1 Aug 2011 (IDR) 7,200Price target - 12mth (IDR) 9,10052-week range (IDR) 7,200 - 4,525Jakarta Comp. Index 4,193.44

Key changes

Price target 8,300.00 to 9,100.00 9.6%Provisioning (FYE) 7,606.5 to 7,334.8 -3.6%Net int margin (FYE) 9.23 to 9.23 0.0%Net profit (FYE) 13,509.1 to 13,725.6 1.6%

Price/price relative

3000

4000

5000

6000

7000

8000

8/09 11/09 2/10 5/10 8/10 11/10 2/11 5/11BRI

Jakarta Comp. Index (Rebased)

Performance (%) 1m 3m 12mAbsolute 7.5 11.6 45.5Jakarta Comp. Index 6.8 9.8 36.6

Stock data

Market cap (IDRbn) 177,550Market cap (USDm) 20,882Shares outstanding (m) 24,659.7Major shareholders The govt of Indonesia (56%)Free float (%) 44Avg daily value traded (USDm) 23.822

Key indicators (FY1)

ROE (%) 32.4Loan/deposit ratio (%) 80.7Book value/share (IDR) 1,951.17Price/book (x) 3.7NPL/total loans (%) 2.9Net int margin (%) 9.2Adjusted ROE (%) 0.0

Enhancing micro capacity BRI continues to rely on micro finance as a source of earnings growth. It continues to make investments to enhance micro-lending capacity. Management has guided for an acceleration of channel expansions to 200 (from 100) for micro units and to 700 (from 600) for Teras in 2011. Assuming lending capacity of Rp20bn, this should imply Rp125tr lending capacity (or a 65% upside).

Back to basics One of our key investment theses for BRI relates to its back-to-basics strategy of focusing its loan growth on high-yield and low-risk-weighting micro (and consumer) loans. Both now account for 52% of total loan book, up from a low of 45% in 2008. This implies 2008-1H11 2.5-year CAGR of 25% (an acceleration from 22% for 2005-08). This should reduce capital charges, thereby minimizing capital risks. Moreover, NPL risks also should decline.

Raising target price to Rp9,100 Despite the stock’s recent performance, we retain our Buy rating. We derive our TP based on a (ROE-g)/(COE-g) method. Risks are higher opex and NPL formation as well as and lower loan growth and asset yields (see pages 4 and 5 for details).

2 August 2011 Strategy Asia Equities Daily Focus

Page 12 Deutsche Bank AG/Hong Kong

Asia ASEAN IndonesiaAutomobiles & Components

01 Aug 2011 - 05:18:41 AM GMT

COMPANY ALERT Forecast Change

United Tractors Buy

Raising heavy equipment forecasts

Reuters:UNTR.JK Exchange:JKT Ticker:UNTR

Price (IDR) 27,300

Price target (IDR) 32,800

52-week range (IDR) 27,700.00 -18,400.00

Market cap (USDm) 11,977

Shares outstanding (m) 3,730.1

Net debt/equity (%) -3.1

Book value/share (IDR) 6,995

Price/book (x) 3.90

FYE 12/31 2010A 2011E 2012E

Sales(IDRbn)

37,324 47,698 55,653

Net Profit(IDRbn)

3,872.9 5,658.3 6,453.8

DB EPS(IDR)

1,038 1,517 1,730

PER (x) 18.7 18.0 15.8

Yield (net)(%)

2.4 2.5 2.9

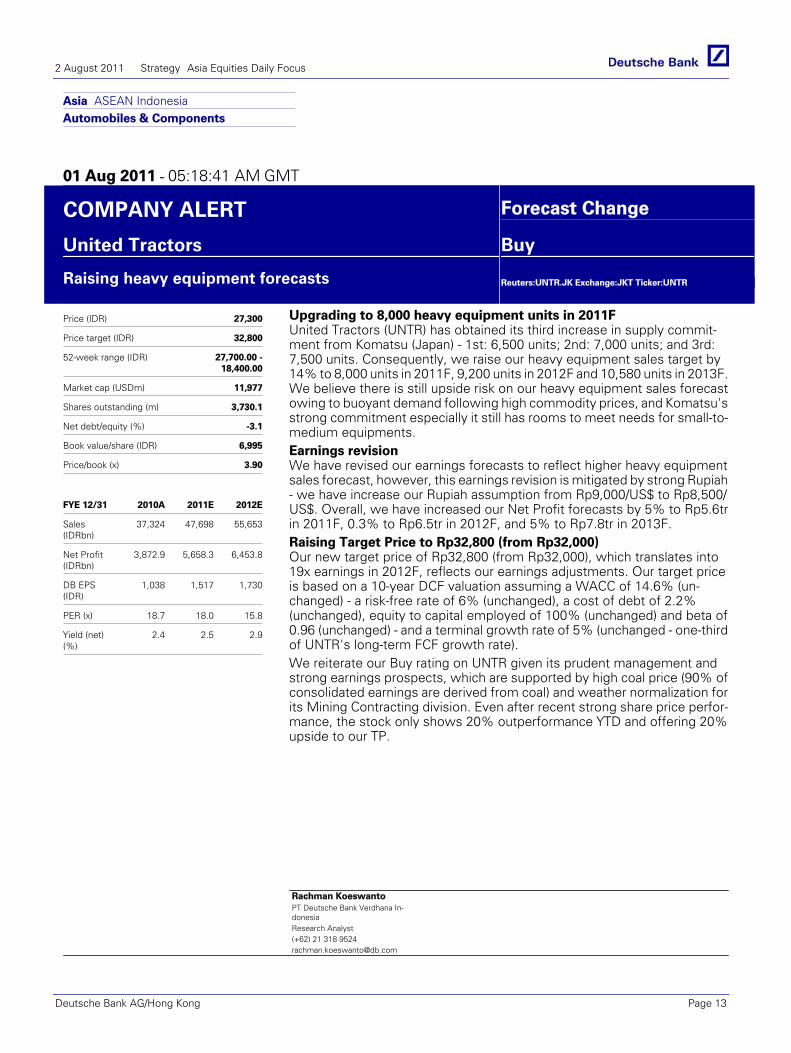

Upgrading to 8,000 heavy equipment units in 2011FUnited Tractors (UNTR) has obtained its third increase in supply commit-ment from Komatsu (Japan) - 1st: 6,500 units; 2nd: 7,000 units; and 3rd:7,500 units. Consequently, we raise our heavy equipment sales target by14% to 8,000 units in 2011F, 9,200 units in 2012F and 10,580 units in 2013F.We believe there is still upside risk on our heavy equipment sales forecastowing to buoyant demand following high commodity prices, and Komatsu'sstrong commitment especially it still has rooms to meet needs for small-to-medium equipments.Earnings revisionWe have revised our earnings forecasts to reflect higher heavy equipmentsales forecast, however, this earnings revision is mitigated by strong Rupiah- we have increase our Rupiah assumption from Rp9,000/US$ to Rp8,500/US$. Overall, we have increased our Net Profit forecasts by 5% to Rp5.6trin 2011F, 0.3% to Rp6.5tr in 2012F, and 5% to Rp7.8tr in 2013F.Raising Target Price to Rp32,800 (from Rp32,000)Our new target price of Rp32,800 (from Rp32,000), which translates into19x earnings in 2012F, reflects our earnings adjustments. Our target priceis based on a 10-year DCF valuation assuming a WACC of 14.6% (un-changed) - a risk-free rate of 6% (unchanged), a cost of debt of 2.2%(unchanged), equity to capital employed of 100% (unchanged) and beta of0.96 (unchanged) - and a terminal growth rate of 5% (unchanged - one-thirdof UNTR's long-term FCF growth rate).We reiterate our Buy rating on UNTR given its prudent management andstrong earnings prospects, which are supported by high coal price (90% ofconsolidated earnings are derived from coal) and weather normalization forits Mining Contracting division. Even after recent strong share price perfor-mance, the stock only shows 20% outperformance YTD and offering 20%upside to our TP.

Rachman KoeswantoPT Deutsche Bank Verdhana In-donesiaResearch Analyst(+62) 21 318 [email protected]

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 13

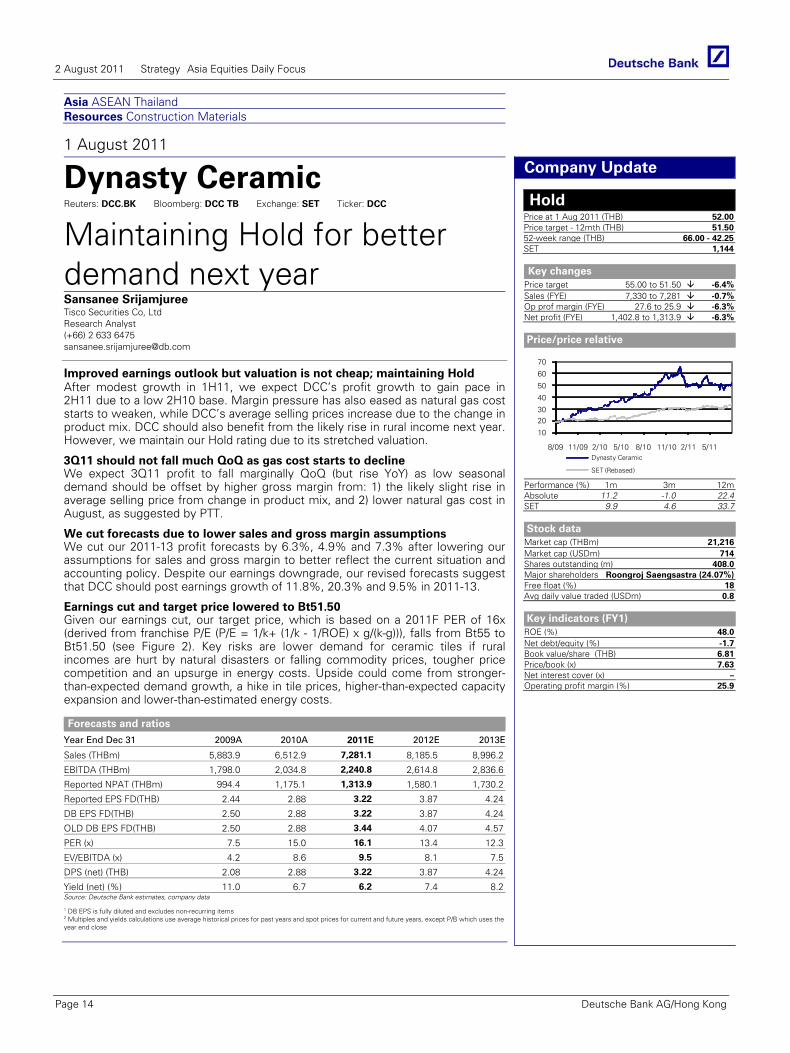

Asia ASEAN Thailand Resources Construction Materials

1 August 2011

Dynasty Ceramic Reuters: DCC.BK Bloomberg: DCC TB Exchange: SET Ticker: DCC

Maintaining Hold for better demand next year Sansanee Srijamjuree Tisco Securities Co, Ltd Research Analyst (+66) 2 633 6475 [email protected]

Improved earnings outlook but valuation is not cheap; maintaining Hold After modest growth in 1H11, we expect DCC’s profit growth to gain pace in 2H11 due to a low 2H10 base. Margin pressure has also eased as natural gas cost starts to weaken, while DCC’s average selling prices increase due to the change in product mix. DCC should also benefit from the likely rise in rural income next year. However, we maintain our Hold rating due to its stretched valuation.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (THBm) 5,883.9 6,512.9 7,281.1 8,185.5 8,996.2

EBITDA (THBm) 1,798.0 2,034.8 2,240.8 2,614.8 2,836.6

Reported NPAT (THBm) 994.4 1,175.1 1,313.9 1,580.1 1,730.2

Reported EPS FD(THB) 2.44 2.88 3.22 3.87 4.24

DB EPS FD(THB) 2.50 2.88 3.22 3.87 4.24

OLD DB EPS FD(THB) 2.50 2.88 3.44 4.07 4.57

PER (x) 7.5 15.0 16.1 13.4 12.3

EV/EBITDA (x) 4.2 8.6 9.5 8.1 7.5

DPS (net) (THB) 2.08 2.88 3.22 3.87 4.24

Yield (net) (%) 11.0 6.7 6.2 7.4 8.2Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Company Update

Hold Price at 1 Aug 2011 (THB) 52.00Price target - 12mth (THB) 51.5052-week range (THB) 66.00 - 42.25SET 1,144

Key changes

Price target 55.00 to 51.50 -6.4%Sales (FYE) 7,330 to 7,281 -0.7%Op prof margin (FYE) 27.6 to 25.9 -6.3%Net profit (FYE) 1,402.8 to 1,313.9 -6.3%

Price/price relative

10

2030

40

50

60

70

8/09 11/09 2/10 5/10 8/10 11/10 2/11 5/11Dynasty Ceramic

SET (Rebased)

Performance (%) 1m 3m 12mAbsolute 11.2 -1.0 22.4SET 9.9 4.6 33.7

Stock data

Market cap (THBm) 21,216Market cap (USDm) 714Shares outstanding (m) 408.0Major shareholders Roongroj Saengsastra (24.07%)Free float (%) 18Avg daily value traded (USDm) 0.8

Key indicators (FY1)

ROE (%) 48.0Net debt/equity (%) -1.7Book value/share (THB) 6.81Price/book (x) 7.63Net interest cover (x) –Operating profit margin (%) 25.9

3Q11 should not fall much QoQ as gas cost starts to decline We expect 3Q11 profit to fall marginally QoQ (but rise YoY) as low seasonal demand should be offset by higher gross margin from: 1) the likely slight rise in average selling price from change in product mix, and 2) lower natural gas cost in August, as suggested by PTT.

We cut forecasts due to lower sales and gross margin assumptions We cut our 2011-13 profit forecasts by 6.3%, 4.9% and 7.3% after lowering our assumptions for sales and gross margin to better reflect the current situation and accounting policy. Despite our earnings downgrade, our revised forecasts suggest that DCC should post earnings growth of 11.8%, 20.3% and 9.5% in 2011-13.

Earnings cut and target price lowered to Bt51.50 Given our earnings cut, our target price, which is based on a 2011F PER of 16x (derived from franchise P/E (P/E = 1/k+ (1/k - 1/ROE) x g/(k-g))), falls from Bt55 to Bt51.50 (see Figure 2). Key risks are lower demand for ceramic tiles if rural incomes are hurt by natural disasters or falling commodity prices, tougher price competition and an upsurge in energy costs. Upside could come from stronger-than-expected demand growth, a hike in tile prices, higher-than-expected capacity expansion and lower-than-estimated energy costs.

2 August 2011 Strategy Asia Equities Daily Focus

Page 14 Deutsche Bank AG/Hong Kong

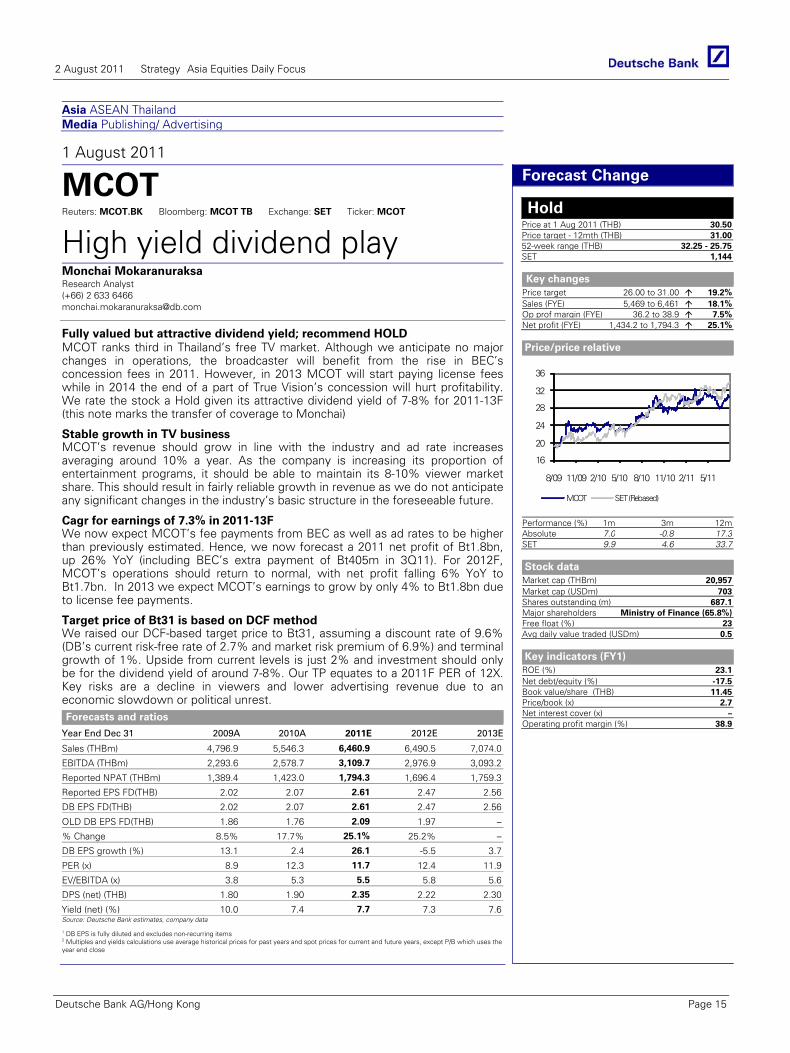

Asia ASEAN Thailand Media Publishing/ Advertising

1 August 2011

MCOT Reuters: MCOT.BK Bloomberg: MCOT TB Exchange: SET Ticker: MCOT

High yield dividend play Monchai Mokaranuraksa Research Analyst (+66) 2 633 6466 [email protected]

Fully valued but attractive dividend yield; recommend HOLD MCOT ranks third in Thailand’s free TV market. Although we anticipate no major changes in operations, the broadcaster will benefit from the rise in BEC’s concession fees in 2011. However, in 2013 MCOT will start paying license fees while in 2014 the end of a part of True Vision’s concession will hurt profitability. We rate the stock a Hold given its attractive dividend yield of 7-8% for 2011-13F (this note marks the transfer of coverage to Monchai)

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (THBm) 4,796.9 5,546.3 6,460.9 6,490.5 7,074.0

EBITDA (THBm) 2,293.6 2,578.7 3,109.7 2,976.9 3,093.2

Reported NPAT (THBm) 1,389.4 1,423.0 1,794.3 1,696.4 1,759.3

Reported EPS FD(THB) 2.02 2.07 2.61 2.47 2.56

DB EPS FD(THB) 2.02 2.07 2.61 2.47 2.56

OLD DB EPS FD(THB) 1.86 1.76 2.09 1.97 –

% Change 8.5% 17.7% 25.1% 25.2% –

DB EPS growth (%) 13.1 2.4 26.1 -5.5 3.7

PER (x) 8.9 12.3 11.7 12.4 11.9

EV/EBITDA (x) 3.8 5.3 5.5 5.8 5.6

DPS (net) (THB) 1.80 1.90 2.35 2.22 2.30

Yield (net) (%) 10.0 7.4 7.7 7.3 7.6Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Forecast Change

Hold Price at 1 Aug 2011 (THB) 30.50Price target - 12mth (THB) 31.0052-week range (THB) 32.25 - 25.75SET 1,144

Key changes

Price target 26.00 to 31.00 19.2%Sales (FYE) 5,469 to 6,461 18.1%Op prof margin (FYE) 36.2 to 38.9 7.5%Net profit (FYE) 1,434.2 to 1,794.3 25.1%

Price/price relative

16

20

24

28

32

36

8/09 11/09 2/10 5/10 8/10 11/10 2/11 5/11

MCOT SET (Rebased)

Performance (%) 1m 3m 12mAbsolute 7.0 -0.8 17.3SET 9.9 4.6 33.7

Stock data

Market cap (THBm) 20,957Market cap (USDm) 703Shares outstanding (m) 687.1Major shareholders Ministry of Finance (65.8%)Free float (%) 23Avg daily value traded (USDm) 0.5

Key indicators (FY1)

ROE (%) 23.1Net debt/equity (%) -17.5Book value/share (THB) 11.45Price/book (x) 2.7Net interest cover (x) –Operating profit margin (%) 38.9

Glo

bal

Mar

kets

Res

earc

h

Stable growth in TV business MCOT’s revenue should grow in line with the industry and ad rate increases averaging around 10% a year. As the company is increasing its proportion of entertainment programs, it should be able to maintain its 8-10% viewer market share. This should result in fairly reliable growth in revenue as we do not anticipate any significant changes in the industry’s basic structure in the foreseeable future.

Cagr for earnings of 7.3% in 2011-13F We now expect MCOT’s fee payments from BEC as well as ad rates to be higher than previously estimated. Hence, we now forecast a 2011 net profit of Bt1.8bn, up 26% YoY (including BEC’s extra payment of Bt405m in 3Q11). For 2012F, MCOT’s operations should return to normal, with net profit falling 6% YoY to Bt1.7bn. In 2013 we expect MCOT’s earnings to grow by only 4% to Bt1.8bn due to license fee payments.

Target price of Bt31 is based on DCF method We raised our DCF-based target price to Bt31, assuming a discount rate of 9.6% (DB’s current risk-free rate of 2.7% and market risk premium of 6.9%) and terminal growth of 1%. Upside from current levels is just 2% and investment should only be for the dividend yield of around 7-8%. Our TP equates to a 2011F PER of 12X. Key risks are a decline in viewers and lower advertising revenue due to an economic slowdown or political unrest.

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 15

Asia ASEAN Thailand Consumer Food & Beverage

1 August 2011

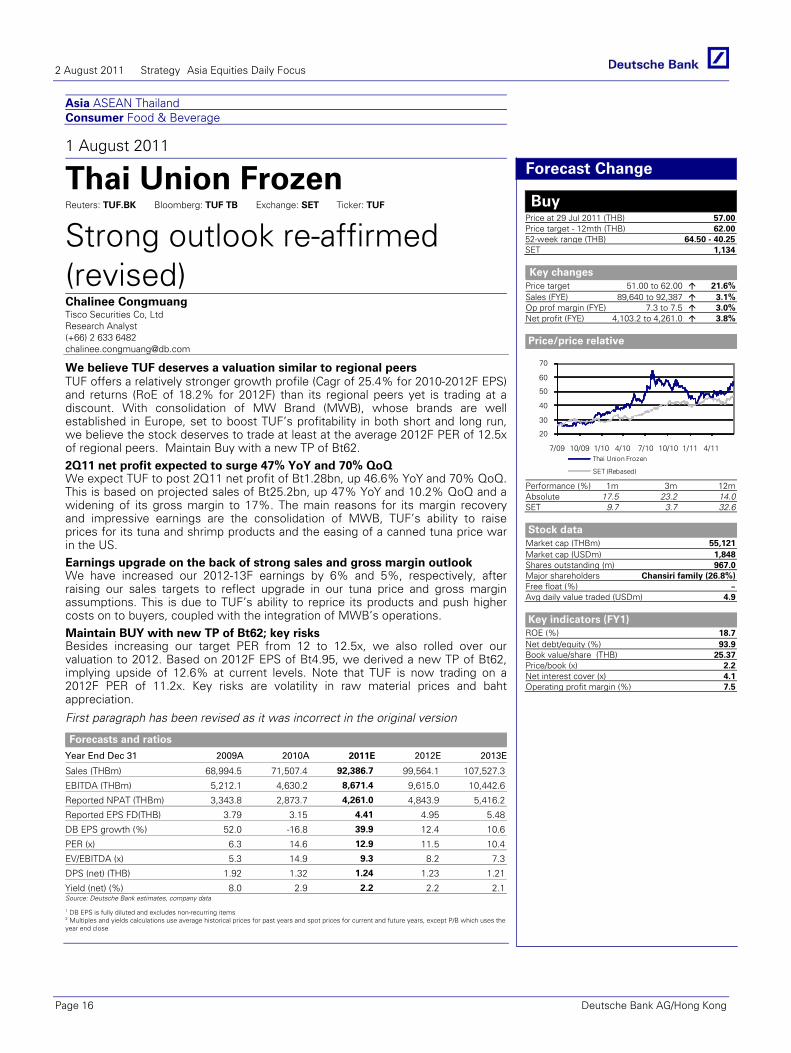

Thai Union Frozen Reuters: TUF.BK Bloomberg: TUF TB Exchange: SET Ticker: TUF

Strong outlook re-affirmed (revised) Chalinee Congmuang Tisco Securities Co, Ltd Research Analyst (+66) 2 633 6482 [email protected]

We believe TUF deserves a valuation similar to regional peers TUF offers a relatively stronger growth profile (Cagr of 25.4% for 2010-2012F EPS) and returns (RoE of 18.2% for 2012F) than its regional peers yet is trading at a discount. With consolidation of MW Brand (MWB), whose brands are well established in Europe, set to boost TUF’s profitability in both short and long run, we believe the stock deserves to trade at least at the average 2012F PER of 12.5x of regional peers. Maintain Buy with a new TP of Bt62.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (THBm) 68,994.5 71,507.4 92,386.7 99,564.1 107,527.3

EBITDA (THBm) 5,212.1 4,630.2 8,671.4 9,615.0 10,442.6

Reported NPAT (THBm) 3,343.8 2,873.7 4,261.0 4,843.9 5,416.2

Reported EPS FD(THB) 3.79 3.15 4.41 4.95 5.48

DB EPS growth (%) 52.0 -16.8 39.9 12.4 10.6

PER (x) 6.3 14.6 12.9 11.5 10.4

EV/EBITDA (x) 5.3 14.9 9.3 8.2 7.3

DPS (net) (THB) 1.92 1.32 1.24 1.23 1.21

Yield (net) (%) 8.0 2.9 2.2 2.2 2.1Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Forecast Change

Buy Price at 29 Jul 2011 (THB) 57.00Price target - 12mth (THB) 62.0052-week range (THB) 64.50 - 40.25SET 1,134

Key changes

Price target 51.00 to 62.00 21.6%Sales (FYE) 89,640 to 92,387 3.1%Op prof margin (FYE) 7.3 to 7.5 3.0%Net profit (FYE) 4,103.2 to 4,261.0 3.8%

Price/price relative

20

30

40

50

60

70

7/09 10/09 1/10 4/10 7/10 10/10 1/11 4/11Thai Union Frozen

SET (Rebased)

Performance (%) 1m 3m 12mAbsolute 17.5 23.2 14.0SET 9.7 3.7 32.6

Stock data

Market cap (THBm) 55,121Market cap (USDm) 1,848Shares outstanding (m) 967.0Major shareholders Chansiri family (26.8%)Free float (%) –Avg daily value traded (USDm) 4.9

Key indicators (FY1)

ROE (%) 18.7Net debt/equity (%) 93.9Book value/share (THB) 25.37Price/book (x) 2.2Net interest cover (x) 4.1Operating profit margin (%) 7.5

2Q11 net profit expected to surge 47% YoY and 70% QoQ We expect TUF to post 2Q11 net profit of Bt1.28bn, up 46.6% YoY and 70% QoQ. This is based on projected sales of Bt25.2bn, up 47% YoY and 10.2% QoQ and a widening of its gross margin to 17%. The main reasons for its margin recovery and impressive earnings are the consolidation of MWB, TUF’s ability to raise prices for its tuna and shrimp products and the easing of a canned tuna price war in the US. Earnings upgrade on the back of strong sales and gross margin outlook We have increased our 2012-13F earnings by 6% and 5%, respectively, after raising our sales targets to reflect upgrade in our tuna price and gross margin assumptions. This is due to TUF’s ability to reprice its products and push higher costs on to buyers, coupled with the integration of MWB’s operations. Maintain BUY with new TP of Bt62; key risks Besides increasing our target PER from 12 to 12.5x, we also rolled over our valuation to 2012. Based on 2012F EPS of Bt4.95, we derived a new TP of Bt62, implying upside of 12.6% at current levels. Note that TUF is now trading on a 2012F PER of 11.2x. Key risks are volatility in raw material prices and baht appreciation.

First paragraph has been revised as it was incorrect in the original version

2 August 2011 Strategy Asia Equities Daily Focus

Page 16 Deutsche Bank AG/Hong Kong

Asia

1 August 2011

Asia Economics Daily

China July PMI stronger than expected

Michael Spencer, Ph.D Chief Economist, Asia (+852) 2203 8303 [email protected]

Jun Ma, Ph.D Chief Economist, Greater China (+852) 2203 8308 [email protected]

Taimur Baig, Ph.D Chief Economist, India (+65) 6423 8681 [email protected]

Juliana Lee Senior Economist (+852) 2203 8312 [email protected]

Kaushik Das Economist (+91) 22 6658 4909 [email protected]

Eco

no

mic

s

HIGHLIGHTS

China – July PMI stronger than expected; cost pressure eases further Indonesia – CPI inflation eases to 4.6%yoy in July, slightly below expectation; Exports growth surprises to the upside in

June South Korea – Inflation surprises to the upside in July; Trade surplus widens sharply in July, led by high exports growth Thailand – Headline and core Inflation remains stable in July India – Trade deficit narrows in June, led by weaker imports growth Hong Kong – Retail sales growth accelerates further in June, but fails to meet expectations Sri Lanka – CPI inflation accelerates to 7.5%yoy in July, broadly in line with our expectation

NEWS IN BRIEF

CHINA PMI (July). China's manufacturing PMI came at 50.7 in July, slightly below the June reading of 50.9. This is better than the consensus forecast of 50.2, especially when taking into account the unfavorable seasonality for July. In addition, the continued decline in the input price index reinforces our view that CPI inflation will fall in H2 this year.

The upside surprises mainly came from a small rebound in new orders (51.1 in July vs. 50.7 in June) and employment (50.5 vs. 50.2). This suggests that the demand situation is stabilizing even with the seasonal weakness.

However, several aspects of the PMI report showed continued weakness. First, the PMI of small enterprises remained very low (at 46.4 in July vs. 45.2 in June), suggesting that credit tightening, RMB appreciation, cost pressure and sluggish external demand continue to pose challenges to the operating environment in the SME sectors, especially those engaged in export production. Second, inventory destocking continued, as the input and output inventory indices declined further (by 1ppt and 1.8ppts in July respectively).

Sector-wise, the PMI profile is broadly the same as last month - the strongest numbers are seen in food and beverage (60.8 and 57.3) and the weakest in textile (44.4) and transportation equipment (44.3, as the modest recovery in auto sales was offset by the rail accident).

(continued on next page…)

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 17

As for outlook, we expect the PMI to begin its modest recovery from August (to 51), and will gradually trend upwards to 53-54 (similar to historical average) by mid-Q4. The key factors that should help improve the PMI outlook in Q4 include: 1) the end of the inventory destocking; 2) the easing of power shortage; 3) some relaxation in credit, especially for SMEs (note that the State Council is now drafting a new set of policies to support SMEs); 4) the acceleration in public housing construction; and 5) a recovery in auto demand.

Another point to note in the PMI report is that the input price index fell further to 56.3 in July from 56.7 in June, the fourth consecutive monthly decline. This reinforces our expectation that PPI inflation will be falling in H2 this year, and thus help containing CPI inflation (especially non-food inflation) going forward. We estimate that non-food inflation will hover around only 0.1% mom in the remainder of this year, thanks to the benefits of monetary tightening in the past 18 months and the stabilization of global commodities prices. We forecast that yoy CPI inflation will fall to 6.2% yoy in July (to be released on August 9), down from 6.4% in June (the peak in the current inflation cycle). By November and December, yoy CPI inflation will likely decline to or even below 4%.

INDONESIA CPI Inflation (July). Headline inflation moderated further in July to 4.6%yoy, down sharply from 5.5% in June, broadly in line with our expectations. However, note that on a mom (nsa) basis, inflation pressure accelerated in July compared to June (+0.7% vs. +0.6%), led primarily by a sharp jump in food prices (+1.8%mom; 5.2%yoy). Price pressures were also visible in components such as transport (+0.2%mom), processed food (+0.4%mom) and education (+1.0% mom). We expect inflation pressure to sustain on a mom basis in the next couple of months due to Ramadan festival. However, favorable base effect will guide yoy inflation lower in the second half (well below 6%); hence, we don't expect any rate hike from BI at least until Q4.

External Trade (June). Exports growth accelerated to a sixteen month high of 49.3%yoy in June, up from 44.9% in May and was well above the consensus (45.0%) as well as our (42.5%) expectation. This was largely driven by oil and gas, exports of which rose at a faster pace of 88.9% in June vs. 71.9% in May, mainly benefitting from rising international oil prices. Also, non-oil & gas exports witnessed a strong growth of 42.1% (38.7% in May) during the month. Meanwhile, imports growth slowed sharply to 28.3% in June, down from 48.6% in May. The trade surplus for the month of June stood broadly stable at USD3.3bn (USD3.4bn in May).

SOUTH KOREA CPI Inflation (July). CPI inflation rose to 4.7%yoy in July, up from 4.4% in June and was above consensus as well as our expectation 4.4% and 4.5% respectively. This upward surprise was mainly led by food items, inflation of which touched 10% in July, after rising 8.5% in June. Also, transport inflation rose at a faster pace of 7.3% in July, as compared to 6.4% in June. On the other hand, housing inflation remained stable at 5.2% in July. Meanwhile, the core inflation rate rose further in July, to 3.8% from 3.7% in June, reflecting underlying demand-pull pressure. We expect headline inflation to remain above 4% until late Q3, before easing to about 3.5% in Q4. On the policy front, we expect the Bank of Korea to deliver only two more 25bps rate hikes in the coming 18 months, taking the policy rate to 3.75% beyond 2012. With inflation rising faster than expected and drawing more public complaints, the political weight on the monetary policy has tilted in favour of a rate hike by end of this quarter, though the BoK may consider rate hike in August as well.

External Trade (July). Exports growth accelerated to 27.3%yoy in July, up from 13.6% (revised) growth reported in June and was well above our (18.0%) as well as consensus (17.1%) expectation. This strong growth was led by volatile vessels exports, which grew sharply by 22.8% in July vs. 35.2% decline in June. Also, exports of petroleum products (91.1% in July vs. 58.1% in June) and metal products (34.1% vs. 20.1%) posted a strong growth during the month. In contrast, exports of electric/electronic products declined by 1.1% in July from 1.6% growth reported in June. By destination, shipments to China grew by 19.4% in July vs. 16.7% growth in June, while exports to US slowed from 11.6% to 1.9% during the month. With imports growth slowing from 27.5% to 24.8% in June, the trade surplus widened sharply to USD 7.2bn in June, from USD2.8bn in May.

THAILAND CPI Inflation (July). Headline inflation remained unchanged at 4.1%yoy in July, broadly in line with our as well consensus expectation of 4.2%. By category, food inflation moderated further in July, to 7.2% from 7.8% in June, led by falling vegetable/fruits prices. In contrast transport (3.7% in July vs. 3.5% in June) inflation rose further in July, suggesting sustained pressure from rising international oil prices. Meanwhile, core inflation too remained broadly stable at 2.6% in July, suggesting temporary pull back in domestic demand. We expect core inflation to head higher, rising above the BoT's upper tolerance

2 August 2011 Strategy Asia Equities Daily Focus

Page 18 Deutsche Bank AG/Hong Kong

level of 3% for the remainder of the year. On the policy front, we expect two more 25bps rate hikes in 2H, with the next one (25bps) in August.

INDIA External trade (June). As expected, exports growth eased to 46.4%yoy (USD29.2bn) in June, from 56.9% in May. Also, imports posted a weaker growth of 42.5% (USD36.9bn) in June, as compared to 54.1% in May. With relatively lower imports growth as compared to exports, the trade deficit narrowed sharply in June, to USD7.8bn from USD15.0bn in May. Within the segment, non-oil imports growth slowed to 47.8% from 71.0% in May, while, oil imports rose at a faster pace of 30.1% in June, as compared to 18.6% in May.

HONG KONG Retail Sales (June). Retail sales (volume) growth was up 22.2%yoy in June compared to 21.1% (revised) in May, but was somewhat weaker than our (24.5%) as well as consensus (24.4%) estimate. Even in value terms, retail sales posted a strong growth of 28.8% in June vs. 27.8% in May. During second quarter of this year, retail sales in volume terms rose by 21.8%, higher than 16.3% growth reported in Q1. We expect strong retail sales growth to continue in the second half, led by sharp rise in tourism income.

SRI LANKA CPI Inflation (July). Consumer price inflation accelerated to 7.5%yoy in July, up from 7.1% in June, broadly in line with our expectation (7.3%) while being above the consensus estimate of 7.1%. This upward surprise was mainly on account of higher transportation inflation in July compared to June (10.1%yoy vs. 6.3%yoy). Clothing (14.5%yoy in July vs. 13.4% in June), housing (4.8% vs. 3.7%) and health (3.3% vs. 1.6%) inflation also edged higher during the month. In contrast, food inflation moderated to 9.3%yoy, from 10.1% in June. Our forecasts show that headline CPI inflation has already peaked in April at 8.8% and should trend lower in the remaining part of 2011 (to about 5.0% by end-December 2011), assuming no further external shocks. We expect headline CPI inflation to average 7% in 2011. Core inflation, in our view, should also gradually ease to around 6.5% by end-December 2011. Given this inflation outlook, we think that CBSL will not want to hike policy rates anytime soon, though continuing to remain vigilant, so as to ensure that demand side inflation pressures remain under control.

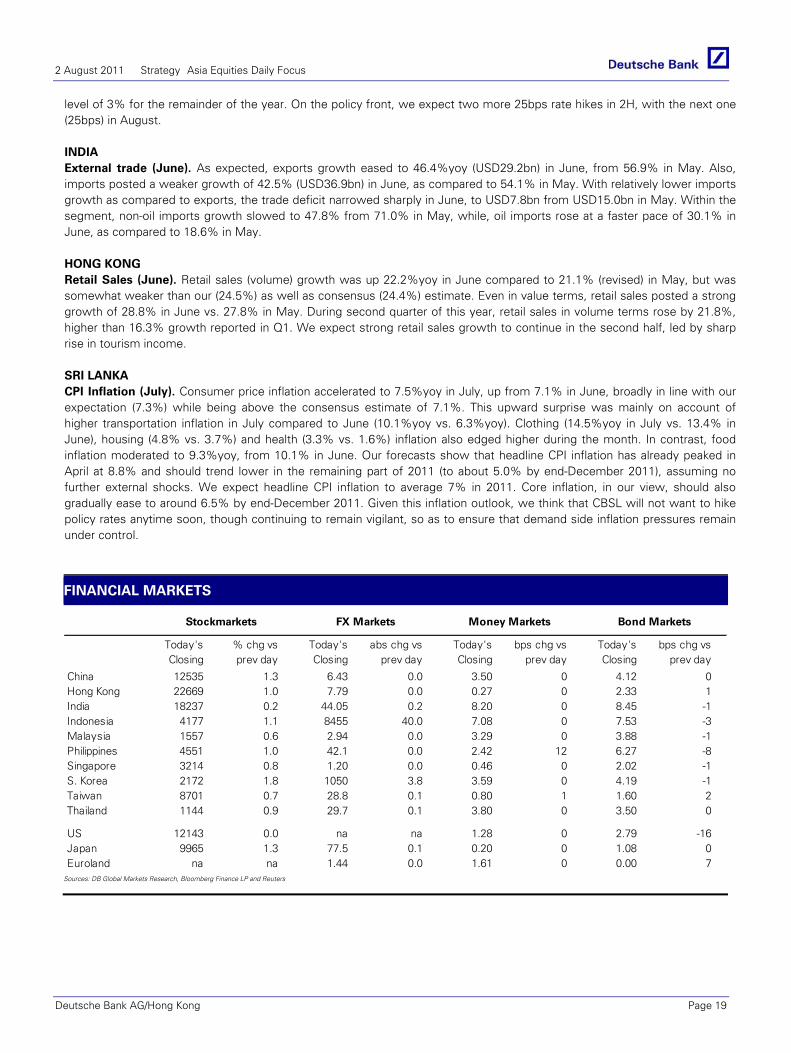

FINANCIAL MARKETS

Today's % chg vs Today's abs chg vs Today's bps chg vs Today's bps chg vsClosing prev day Closing prev day Closing prev day Closing prev day

China 12535 1.3 6.43 0.0 3.50 0 4.12 0Hong Kong 22669 1.0 7.79 0.0 0.27 0 2.33 1India 18237 0.2 44.05 0.2 8.20 0 8.45 -1Indonesia 4177 1.1 8455 40.0 7.08 0 7.53 -3Malaysia 1557 0.6 2.94 0.0 3.29 0 3.88 -1Philippines 4551 1.0 42.1 0.0 2.42 12 6.27 -8Singapore 3214 0.8 1.20 0.0 0.46 0 2.02 -1S. Korea 2172 1.8 1050 3.8 3.59 0 4.19 -1Taiwan 8701 0.7 28.8 0.1 0.80 1 1.60 2Thailand 1144 0.9 29.7 0.1 3.80 0 3.50 0

US 12143 0.0 na na 1.28 0 2.79 -16Japan 9965 1.3 77.5 0.1 0.20 0 1.08 0Euroland na na 1.44 0.0 1.61 0 0.00 7

Stockmarkets FX Markets Money Markets Bond Markets

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 19

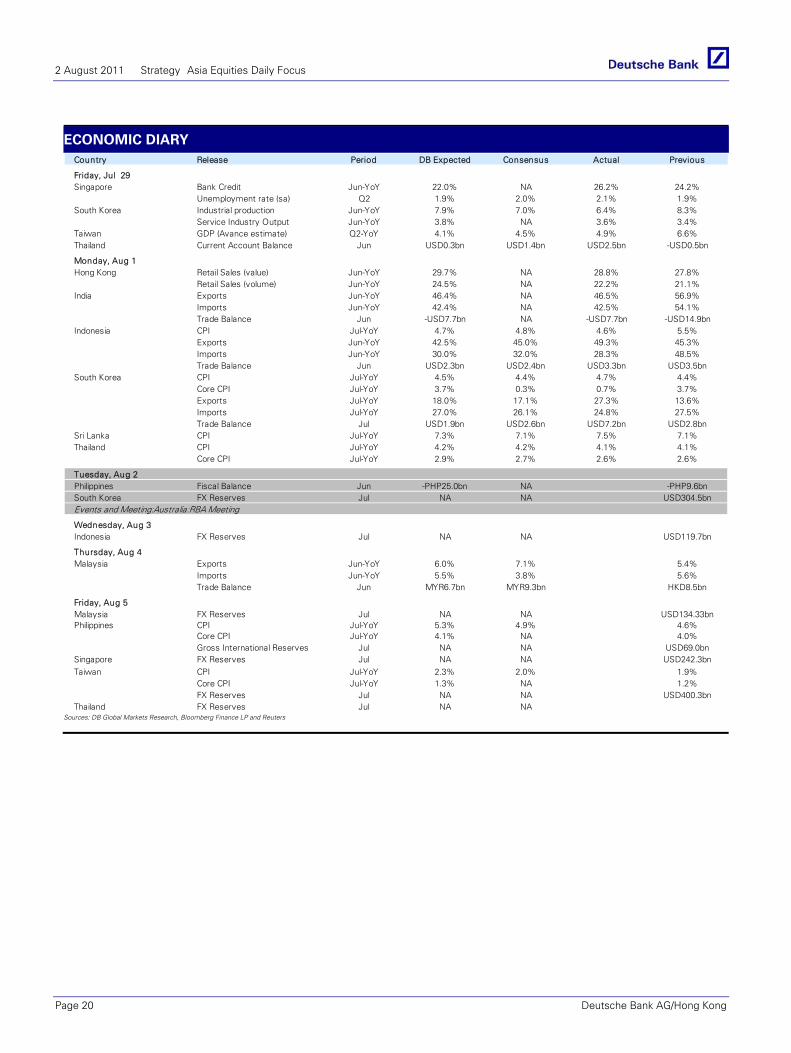

ECONOMIC DIARY Country Release Period DB Expected Consensus Actual Previous

Friday, Jul 29Singapore Bank Credit Jun-YoY 22.0% NA 26.2% 24.2%

Unemployment rate (sa) Q2 1.9% 2.0% 2.1% 1.9%South Korea Industrial production Jun-YoY 7.9% 7.0% 6.4% 8.3%

Service Industry Output Jun-YoY 3.8% NA 3.6% 3.4%Taiwan GDP (Avance estimate) Q2-YoY 4.1% 4.5% 4.9% 6.6%Thailand Current Account Balance Jun USD0.3bn USD1.4bn USD2.5bn -USD0.5bn

Monday, Aug 1Hong Kong Retail Sales (value) Jun-YoY 29.7% NA 28.8% 27.8%

Retail Sales (volume) Jun-YoY 24.5% NA 22.2% 21.1%India Exports Jun-YoY 46.4% NA 46.5% 56.9%

Imports Jun-YoY 42.4% NA 42.5% 54.1%Trade Balance Jun -USD7.7bn NA -USD7.7bn -USD14.9bn

Indonesia CPI Jul-YoY 4.7% 4.8% 4.6% 5.5%Exports Jun-YoY 42.5% 45.0% 49.3% 45.3%Imports Jun-YoY 30.0% 32.0% 28.3% 48.5%Trade Balance Jun USD2.3bn USD2.4bn USD3.3bn USD3.5bn

South Korea CPI Jul-YoY 4.5% 4.4% 4.7% 4.4%Core CPI Jul-YoY 3.7% 0.3% 0.7% 3.7%Exports Jul-YoY 18.0% 17.1% 27.3% 13.6%Imports Jul-YoY 27.0% 26.1% 24.8% 27.5%Trade Balance Jul USD1.9bn USD2.6bn USD7.2bn USD2.8bn

Sri Lanka CPI Jul-YoY 7.3% 7.1% 7.5% 7.1%Thailand CPI Jul-YoY 4.2% 4.2% 4.1% 4.1%

Core CPI Jul-YoY 2.9% 2.7% 2.6% 2.6%

Tuesday, Aug 2Philippines Fiscal Balance Jun -PHP25.0bn NA -PHP9.6bnSouth Korea FX Reserves Jul NA NA USD304.5bnEvents and Meeting:Australia:RBA Meeting

Wednesday, Aug 3Indonesia FX Reserves Jul NA NA USD119.7bn

Thursday, Aug 4Malaysia Exports Jun-YoY 6.0% 7.1% 5.4%

Imports Jun-YoY 5.5% 3.8% 5.6%Trade Balance Jun MYR6.7bn MYR9.3bn HKD8.5bn

Friday, Aug 5Malaysia FX Reserves Jul NA NA USD134.33bnPhilippines CPI Jul-YoY 5.3% 4.9% 4.6%

Core CPI Jul-YoY 4.1% NA 4.0%Gross International Reserves Jul NA NA USD69.0bn

Singapore FX Reserves Jul NA NA USD242.3bnTaiwan CPI Jul-YoY 2.3% 2.0% 1.9%

Core CPI Jul-YoY 1.3% NA 1.2%FX Reserves Jul NA NA USD400.3bn

Thailand FX Reserves Jul NA NASources: DB Global Markets Research, Bloomberg Finance LP and Reuters

2 August 2011 Strategy Asia Equities Daily Focus

Page 20 Deutsche Bank AG/Hong Kong

Global 1 August 2011

Global Commodities DailyUS growth recession

Co

mm

od

itie

s

The Day Ahead

Time(EST) Country Event Previous Market View

03:55 Germany PMI Manufacturing (July) 52.1 52.1

04:00 EZ PMI Manufacturing (July) 50.4 50.4

05:00 EZ Unemployment Rate (June) 9.9% 9.9%

10:00 US ISM Manufacturing(July) 55.3 55

Overview

Real GDP in Q2 for the US rose just 1.3%, as personal consumption virtually stalled (+0.1% vs. +2.1% previously). The prior quarters were revised down as well. In light of the softer first half performance, our US economics team lowered their estimate of Q3 GDP by a full percentage point to 2.5%; and reduced Q4 from 4.3% to 3.0%. This could reduce US oil demand growth for 2H 2011 by some 200kb/d from prior forecasts. The US EIA, for example, has been expecting growth of about 100kb/d YoY, and lower GDP could turn that into -100kb/d.

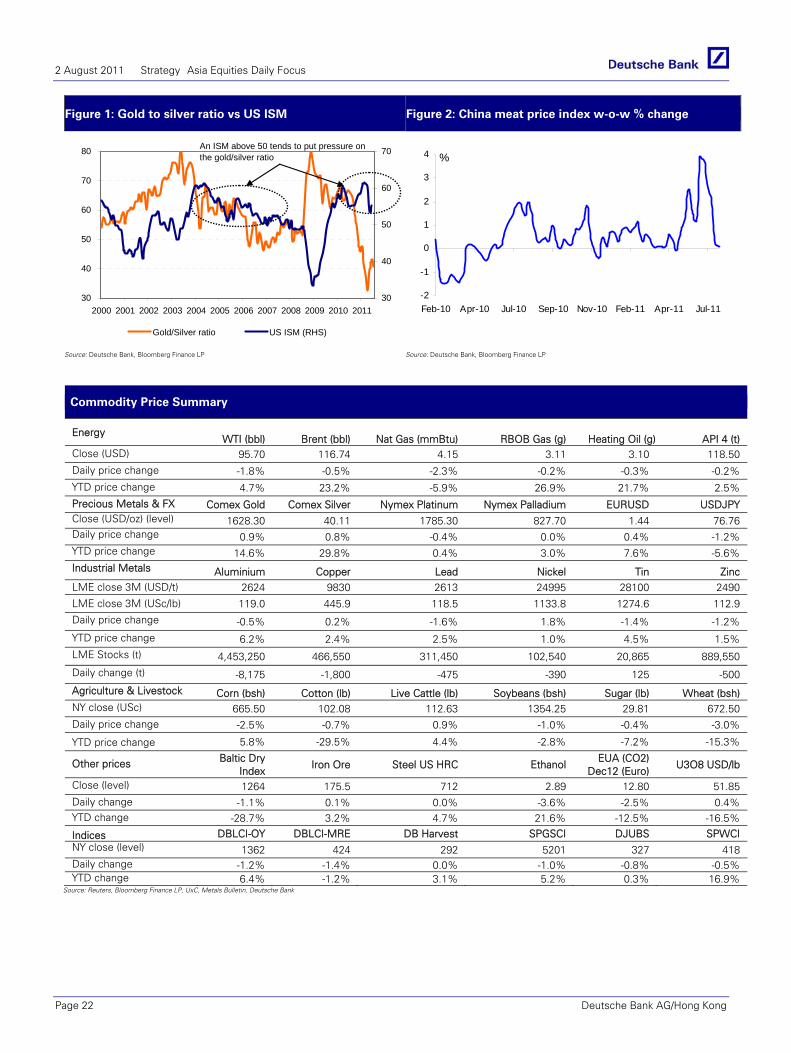

Gold advanced to fresh record highs on Friday as the weak macro data from the US raised concerns about a sub-par economic recovery. The USD weakness and worries about US debt downgrades also reinforced the price rally- with no progress made Friday on the US debt ceiling law. The next key data release for the complex will be today’s US ISM report. Historically when the US ISM is above 50, the gold to silver ratio has trended lower, Figure 1.

The industrial metals complex remains vulnerable to the ebb and flow of market anxiety towards European and US debt outlook. China released its manufacturing PMI for July this morning, which fell to a 28 month low of 50.7 from 50.9 in June. We believe the market will turn its attention to the outlook for China inflation (next release on Aug 9th), which holds the key to monetary policy and hence industrial metals demand. Latest data from the Ministry of Commerce showed a moderation in food inflation and specifically pork prices, Figure 2. We expect the decline in inflation will allow the authorities to switch policy emphasis away from inflation towards supporting growth.

China’s Henan province, the country’s largest aluminium producing region, may face power cuts. We commented in the daily previously that that recent heat wave has resulted in a considerable increase in electricity consumption. Daily electricity generation was 8.15% higher compared to last year’s peak daily output. According to Reuters, aluminium smelters could face cuts of up to 20% of normal supplies and extend into mid-September if the hot weather persists. In addition to tight energy market, a potential cut in export rebate for aluminium products from 11% to 7% could reduce net exports and provide support for aluminium prices in our view.

Looking at today’s calendar, in Eurozone market will focus on manufacturing PMI and unemployment rate for July. In the US, ISM will provide important guidance on manufacturing activity. Non-farm payroll report will be released towards the end of this week.

Commodities & Global Markets

Commodities News In Brief

• China produced about 19.5m tonnes of crude steel, equivalent to 1.95mn tonnes per day, down by 0.3% from the first ten days of this month, according to the China Iron & Steel Association.

• Japan’s crude oil imports in June fell 4.4% to 3.05mn barrels per day from a year earlier

• China’s inbound shipments of soybeans are forecast to drop to 3.2mn tonnes in August from 5mn tonnes projected this month, the Ministry of Commerce said.

• Sugar exports from India may be as much as 4mn tonnes in the year beginning Oct.1, according to six producers and traders in a Bloomberg News survey. That compares with an estimated 2.1mn tonnes this year, according to the Indian Sugar Mills Association.

Global Markets News In Brief

• Japan Housing Starts (YoY) fell to 5.8% in Jun from 6.4%.

• Germany Retail Sales increased to 6.3% from -2.5% (MoM) in June, while fell (YoY) to -1% vs 3.1%.

• UK Nationwide Housing Prices n.s.a (YoY) increased to -0.4% from -1.1% in July, while increased to 0.2% vs 0% (MoM).

• US GDP QoQ rose at a 1.3% annual rate following a 0.4% gain in Q1.

• US Chicago PMI fell to 58.8 points in July, down from 61.1in June.

• US U.of Michigan confidence fell to 63.7 from 71.5 in June.

• China leading index fell to 101.76 from 101.92 (MoM) in June.

• China PMI Manufacturing fell to 50.7 in July from 50.9 in June.

Event Risks

• Germany PMI Services on August 3 • EZ Retail Sales on August 3 • US MBA Mtg. Applications on August 3 • US Factory Orders on August 3 • US non-farm payroll on August 5

Research Team Adam Sieminski Xiao Fu Research Analyst Research Analyst (1) 20 2662 1624 (44) 20 7547 1558 [email protected] [email protected]

2 August 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 21

Figure 1: Gold to silver ratio vs US ISM Figure 2: China meat price index w-o-w % change

30

40

50

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 201130

40

50

60

70

Gold/Silver ratio US ISM (RHS)

An ISM above 50 tends to put pressure on the gold/silver ratio

-2

-1

0

1

2

3

4

Feb-10 Apr-10 Jul-10 Sep-10 Nov-10 Feb-11 Apr-11 Jul-11

%

Source: Deutsche Bank, Bloomberg Finance LP Source: Deutsche Bank, Bloomberg Finance LP

Commodity Price Summary

Energy WTI (bbl) Brent (bbl) Nat Gas (mmBtu) RBOB Gas (g) Heating Oil (g) API 4 (t)

Close (USD) 95.70 116.74 4.15 3.11 3.10 118.50 Daily price change -1.8% -0.5% -2.3% -0.2% -0.3% -0.2% YTD price change 4.7% 23.2% -5.9% 26.9% 21.7% 2.5% Precious Metals & FX Comex Gold Comex Silver Nymex Platinum Nymex Palladium EURUSD USDJPY Close (USD/oz) (level) 1628.30 40.11 1785.30 827.70 1.44 76.76 Daily price change 0.9% 0.8% -0.4% 0.0% 0.4% -1.2% YTD price change 14.6% 29.8% 0.4% 3.0% 7.6% -5.6% Industrial Metals Aluminium Copper Lead Nickel Tin Zinc LME close 3M (USD/t) 2624 9830 2613 24995 28100 2490

LME close 3M (USc/lb) 119.0 445.9 118.5 1133.8 1274.6 112.9

Daily price change -0.5% 0.2% -1.6% 1.8% -1.4% -1.2%

YTD price change 6.2% 2.4% 2.5% 1.0% 4.5% 1.5% LME Stocks (t) 4,453,250 466,550 311,450 102,540 20,865 889,550

Daily change (t) -8,175 -1,800 -475 -390 125 -500

Agriculture & Livestock Corn (bsh) Cotton (lb) Live Cattle (lb) Soybeans (bsh) Sugar (lb) Wheat (bsh) NY close (USc) 665.50 102.08 112.63 1354.25 29.81 672.50 Daily price change -2.5% -0.7% 0.9% -1.0% -0.4% -3.0%

YTD price change 5.8% -29.5% 4.4% -2.8% -7.2% -15.3%

Other prices Baltic Dry Index

Iron Ore Steel US HRC Ethanol EUA (CO2)

Dec12 (Euro) U3O8 USD/lb

Close (level) 1264 175.5 712 2.89 12.80 51.85 Daily change -1.1% 0.1% 0.0% -3.6% -2.5% 0.4% YTD change -28.7% 3.2% 4.7% 21.6% -12.5% -16.5%

Indices DBLCI-OY DBLCI-MRE DB Harvest SPGSCI DJUBS SPWCI NY close (level) 1362 424 292 5201 327 418 Daily change -1.2% -1.4% 0.0% -1.0% -0.8% -0.5% YTD change 6.4% -1.2% 3.1% 5.2% 0.3% 16.9%

Source: Reuters, Bloomberg Finance LP, UxC, Metals Bulletin, Deutsche Bank

2 August 2011 Strategy Asia Equities Daily Focus

Page 22 Deutsche Bank AG/Hong Kong

Asia China Technology

1 August 2011

China TMT Daily More app factoids; also, SINA, 0700.HK

(Please click through to the .pdf version of this document for a full overview of today's

news and views.)

Periodical

TOP CHINA TMT PICKS Company Rating Target Price AsiaInfo-Linkage Buy USD 26.30 China Telecom Buy HKD 5.70 ZTE Buy HKD 35.65

CHINA TMT STOCKS Company Rating Close Price 1D% 3M%

TELCOS as on 29/07China Comm Service Buy 3.9 -1.3 -16.9China Mobile Hold 77.6 -0.3 8.6China Telecom Buy 5.1 -1.4 13.4China Unicom Buy 15.5 -1.0 -1.8 INTERNET/ONLINE GAMING Alibaba.com Hold 10.9 -0.9 -21.2Baidu Buy 157.1 -0.8 5.8Ctrip.com Int'l Hold 46.1 0.3 -5.4Netease.com Buy 50.5 0.2 2.5Shanda Hold 35.0 -0.3 -27.6Shanda Games Hold 6.0 -3.7 -19.9Sina Corp Hold 108.1 -2.7 -19.8Sohu.com Hold 90.1 1.4 -14.8Tencent Buy 202.8 -1.1 -8.2 TECHNOLOGY AsiaInfo-Linkage Buy 15.3 -4.1 -19.2ChinaCache Buy 7.7 -1.3 -54.3Foxconn Int'l Hldgs Hold 3.6 -1.7 -22.5SouFun Buy 20.8 -0.3 -9.8Synnex Technology Buy 74.0 -2.4 1.2ZTE Buy 24.4 -0.8 -12.9 Indices Close 1D% 3M% as on 29/07HSI 22440.3 -0.6 -5.4HSCEI 12373.6 -1.2 -6.3Nasdaq 2756.4 -0.4 -4.1Sources: DB, Bloomberg Finance LP

CALENDAR OF EVENTS

Research Team

Alan Hellawell III Research Analyst (+852) 2203 6240 [email protected]

Eva Leung, CFA Research Analyst (+852) 2203 6190 [email protected]

FEATURE:

71% of freemium game transactions spent on in-app purchases cost under $10 We continue our discussion of the previous TMT daily around the topic of “Free” apps vs. paid apps with some additional updates. As profiled in an earlier Daily, mobile application analytics firm Flurry in a report released in May revealed that games drove 75% of revenue generated among the top 100 grossing iOS apps, of which 65% were generated from freemium games. Flurry recently conducted another study which analyzed how 3.5m consumers spent their money across top iOS and Android freemium games. Flurry organized the data into three price buckets representing the amount of money spent on freemium games: from $0.99 - $10, from $10 - $20, and over $20. Interestingly, about 71% of all transactions were under $10, 16% involved spending of between $10 to $20, and 13% for greater than $20. The average amount spent per transaction was $14.

The "over $20 in-app" price bracket generated half of the total revenues in freemium games Flurry data further showed that within the “under $10” bucket, most transactions clustered at the $9.99 level, followed by $4.99, and finally $0.99. An interesting question that arose was that why do consumers spend $0.99 less than 2% of the time in freemium games when this price point is so popular among premium games? Company analysts suggest that freemium gamers have a different mindset in deciding whether or not to spend. Flurry data showed that about 3% of consumers will spend on freemium games, and that a deeper commitment to the games will drive more spending. Additionally, the study revealed that high-end of the spending spectrum drove up the $14 average price point. Over 5% of all purchases were for amounts greater than $50, which were comparable to the price point of top console and PC games sold at retail shops.