Embed Size (px)

Citation preview

Asia Pan-Asia Strategy

18 January 2011

Asia Equities Daily Focus Today's research headlines Asian Edition

Deutsche Bank AG/Hong Kong

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

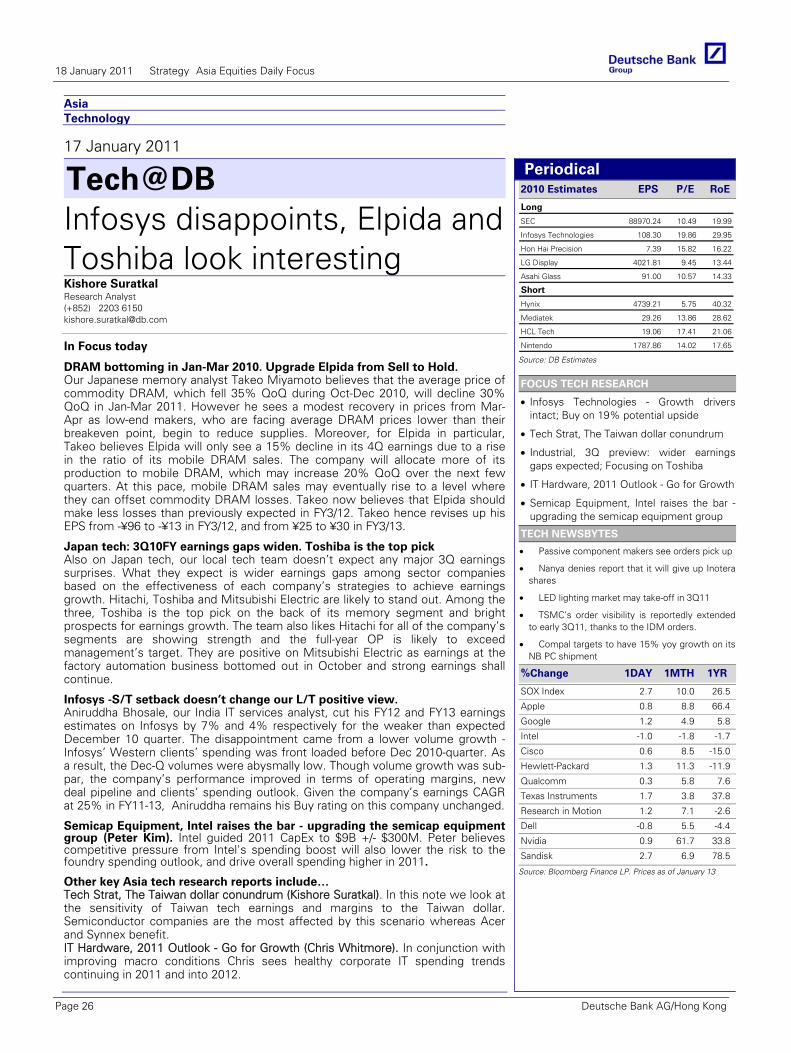

Periodical

Asian Index Closings EQUITIES Close 1D Chg %Chg

SHSZ300 2974.35 -3.80 -4.92 HSCEI 12938.05 -1.63 1.94 HSI 24156.97 -0.52 4.87 TWSE 8925.09 -0.53 -0.53 KOSPI 2099.85 -0.40 2.38 FSSTI 3238.63 -0.23 1.52 KLCI 1574.49 0.29 3.66 SENSEX 18882.25 0.12 -7.93 NIFTY 5654.75 0.00 -7.82 SET 1023.19 -0.88 -0.93 JCI 3535.73 -0.94 -4.53 PCOMP 4148.16 0.39 -1.26 ASX200 4763.10 -0.80 0.38 FOREX (vs US$) Close 1D Chg YTD %Chg Rmb 6.59 0.05 0.20 HK$ 7.78 -0.02 -0.03 NT$ 29.02 0.01 0.97 Won 1117.48 -0.28 0.76 S$ 1.29 -0.01 -0.36 M$ 3.06 -0.05 0.16 Rupee 45.52 -0.34 -1.79 Baht 30.57 -0.33 -1.67 Rupiah 9063.00 -0.10 -0.74 Peso 44.52 -0.66 -1.61 A$ 0.99 0.50 -2.89

Source: Bloomberg Finance LP

Latest Commodity Prices COMMODITIES Close 1D %Chg YTD %Chg West Texas 91.54 0.15 0.18 Brent 97.16 -0.97 3.03 CRB 333.06 0.00 0.08 Copper 440.35 0.84 -0.81 Gold (Spot) 1362.65 0.07 -4.09 Alum. (LME) 2472.00 -0.48 0.08 Baltic Dry 1439.00 0.07 -18.84

Source: Bloomberg Finance LP

DB CORPORATE ACCESS DB Access India Conference 2011 - Mumbai 3/7 - 9 DB Access Asia Conference 2011 - Singapore 5/23 - 26

Research Team

Carissa Szeto Equity Focus (+852) 2203 6171 [email protected] Ching-Li Teo, CFA Equity Focus (+852) 2203 6206 [email protected]

Co

mp

any

Glo

bal

Mar

kets

Res

earc

h

Nodita_ 1. 2.

TOP STORIES Malaysia Strategy Charging forward; Bullish Su-Yin Teoh Page 5

Siliconware Precision (2325.TW),TWD36.20 Buy Price Target TWD46.00

Structural turnaround in sight; upgrading to Buy Michael Chou Page 6

RECOMMENDATION CHANGES

Shinsegae (004170.KS) KRW 603,000 Hold Price Target KRW 660,000

No excitement expected; downgrading to Hold

Jihyun Song Page 7

Bursa Malaysia (BMYS.KL),MYR8.90 Hold Price Target MYR8.20

Turnover rebound; upgrade to Hold Andrew HillPage 8

ESTIMATE & TARGET PRICE CHANGES

Hengan Intl. (1044.HK),HKD61.25 Buy Price Target HKD69.50

Near-term hiccups; long term staying positive; maintain Buy

Mabel WongPage 9

PICC (2328.HK),HKD10.76 Sell Price Target HKD8.10

Group restructuring is still a dilutionrisk

Bob LeungPage 10

Axis Bank (AXBK.BO) INR 1,201.35 Buy Target Price INR 1,560.00

Profitability intact on pricing power &liquidity management

Dipankar Choudhury Page 11

Glenmark Pharma (GLEN.BO),INR347.55 Hold Price Target INR325.00

Traction in US but slower recoveryacross markets

Abhay Shanbhag Page 12

Steel Authority of India (SAIL.BO),INR157.15 Buy Price Target INR207.00

Revising estimates down but remainpositive

Abhay Laijawala Page 13

STRATEGY/ECONOMICS

Asia Economics Daily China RRR hike; Singapore inflation and trade

Michael Spencer Page 14

Asia Economics Monthly January Michael Spencer Page 17

Asia Real Exchange Rates November Indices Juliana Lee

Page 19

Global Commodities Daily Harsh weather and inflation Michael Lewis

Page 22

Commodities Outlook Michael LewisPage 24

Tech@DB Infosys disappoints, Elpida and Toshiba look interesting

Kishore Suratkal Page 26

18 January 2011 Strategy Asia Equities Daily Focus

Page 2 Deutsche Bank AG/Hong Kong

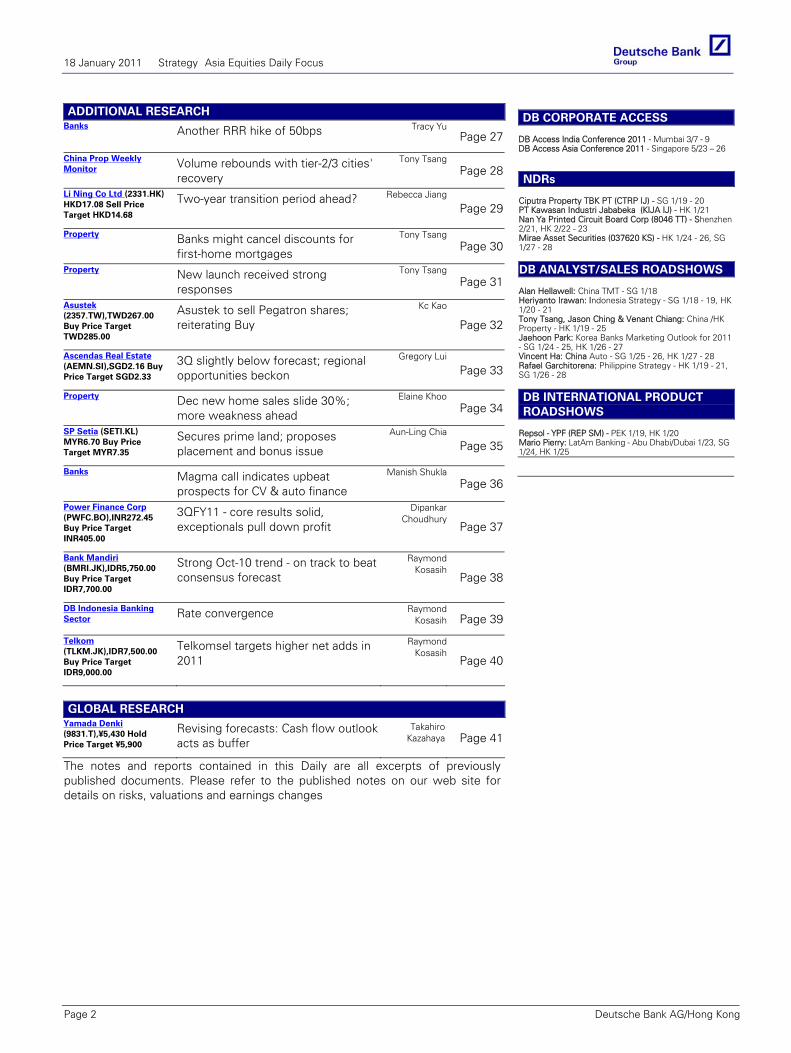

ADDITIONAL RESEARCH

Banks Another RRR hike of 50bps DB CORPORATE ACCESS

Tracy Yu Page 27

China Prop Weekly Monitor Volume rebounds with tier-2/3 cities'

recovery

DB Access India Conference 2011 - Mumbai 3/7 - 9 DB Access Asia Conference 2011 - Singapore 5/23 – 26

Tony Tsang Page 28

Li Ning Co Ltd (2331.HK) HKD17.08 Sell Price Target HKD14.68

Two-year transition period ahead?

NDRs Ciputra Property TBK PT (CTRP IJ) - SG 1/19 - 20

Rebecca Jiang

Page 29

Property Banks might cancel discounts for first-home mortgages

PT Kawasan Industri Jababeka (KIJA IJ) - HK 1/21 Nan Ya Printed Circuit Board Corp (8046 TT) - Shenzhen 2/21, HK 2/22 - 23 Mirae Asset Securities (037620 KS) - HK 1/24 - 26, SG 1/27 - 28

Tony Tsang Page 30

Property New launch received strong responses

DB ANALYST/SALES ROADSHOWS Tony Tsang Page 31

Asustek (2357.TW),TWD267.00 Buy Price Target TWD285.00

Asustek to sell Pegatron shares; reiterating Buy

Alan Hellawell: China TMT - SG 1/18 Heriyanto Irawan: Indonesia Strategy - SG 1/18 - 19, HK 1/20 - 21 Kc Kao

Page 32

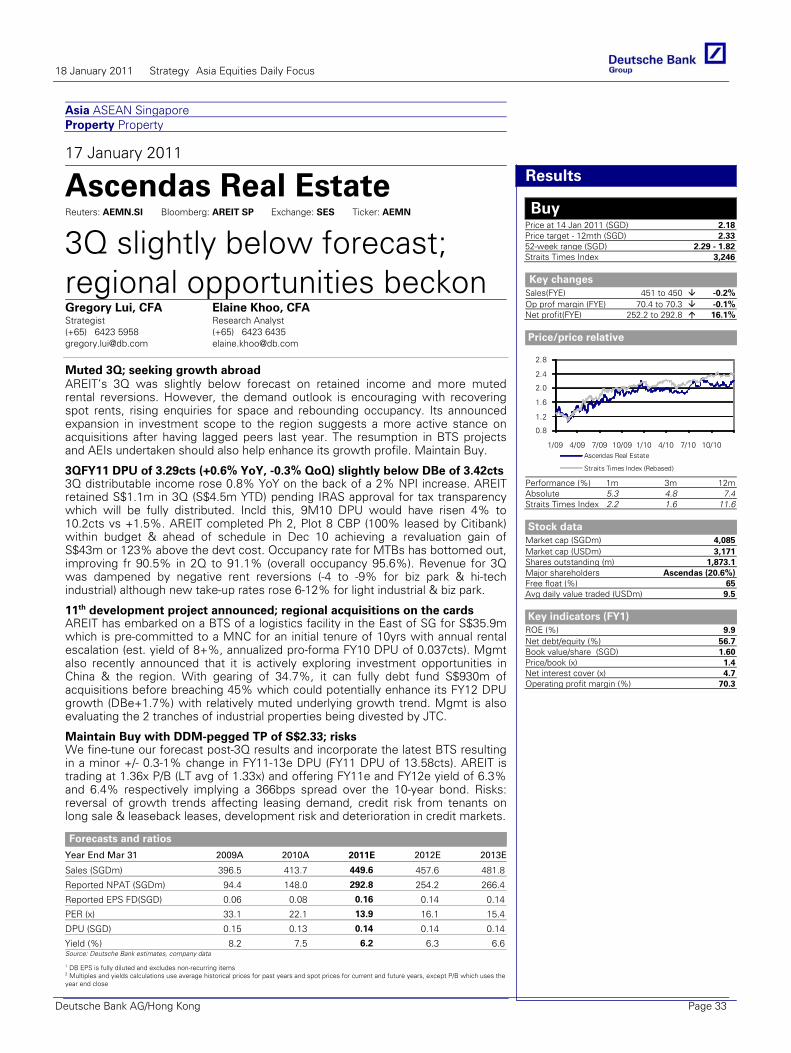

Ascendas Real Estate (AEMN.SI),SGD2.16 Buy Price Target SGD2.33

3Q slightly below forecast; regional opportunities beckon

Tony Tsang, Jason Ching & Venant Chiang: China /HK Property - HK 1/19 - 25 Jaehoon Park: Korea Banks Marketing Outlook for 2011 - SG 1/24 - 25, HK 1/26 - 27 Vincent Ha: China Auto - SG 1/25 - 26, HK 1/27 - 28 Rafael Garchitorena: Philippine Strategy - HK 1/19 - 21, SG 1/26 - 28

DB INTERNATIONAL PRODUCT ROADSHOWS

Gregory Lui

Page 33

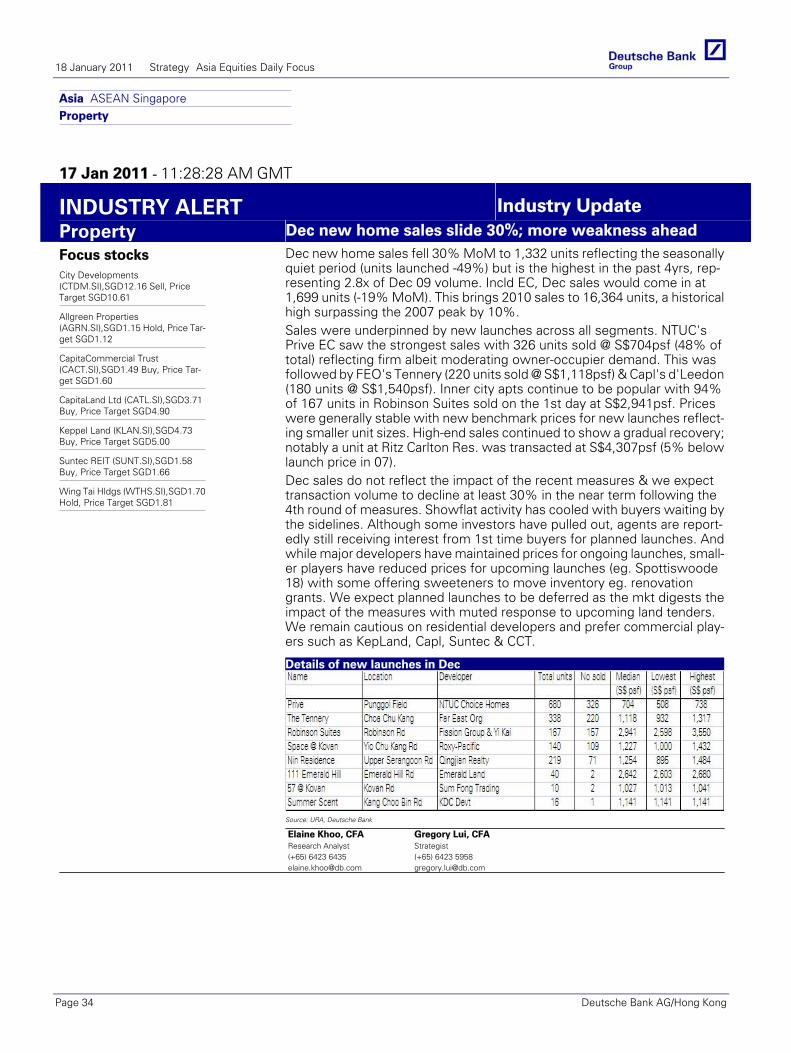

Property Dec new home sales slide 30%; more weakness ahead

Elaine Khoo Page 34

SP Setia (SETI.KL) MYR6.70 Buy Price Target MYR7.35

Secures prime land; proposes placement and bonus issue

Aun-Ling Chia

Page 35Repsol - YPF (REP SM) - PEK 1/19, HK 1/20

Mario Pierry: LatAm Banking - Abu Dhabi/Dubai 1/23, SG 1/24, HK 1/25

Manish Shukla Banks Magma call indicates upbeat prospects for CV & auto finance

Page 36

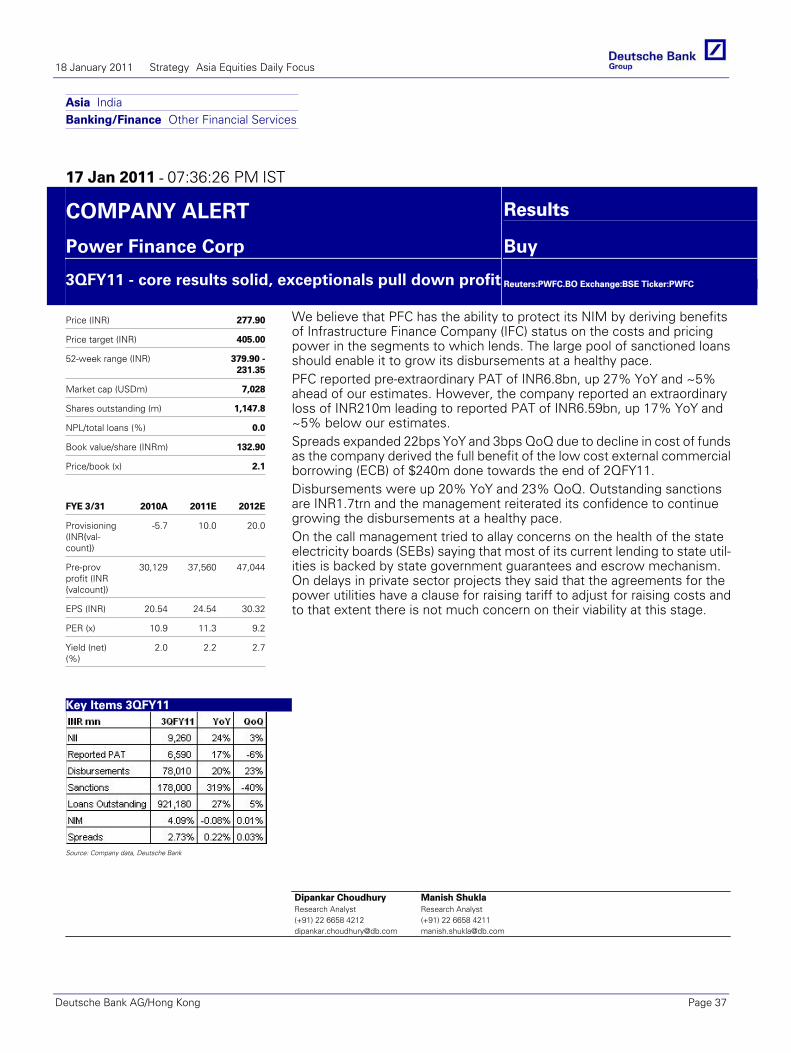

Power Finance Corp (PWFC.BO),INR272.45 Buy Price Target INR405.00

3QFY11 - core results solid, exceptionals pull down profit

Dipankar Choudhury

Page 37

Bank Mandiri (BMRI.JK),IDR5,750.00 Buy Price Target IDR7,700.00

Strong Oct-10 trend - on track to beat consensus forecast

Raymond Kosasih

Page 38

DB Indonesia Banking Sector Rate convergence Raymond

Kosasih Page 39

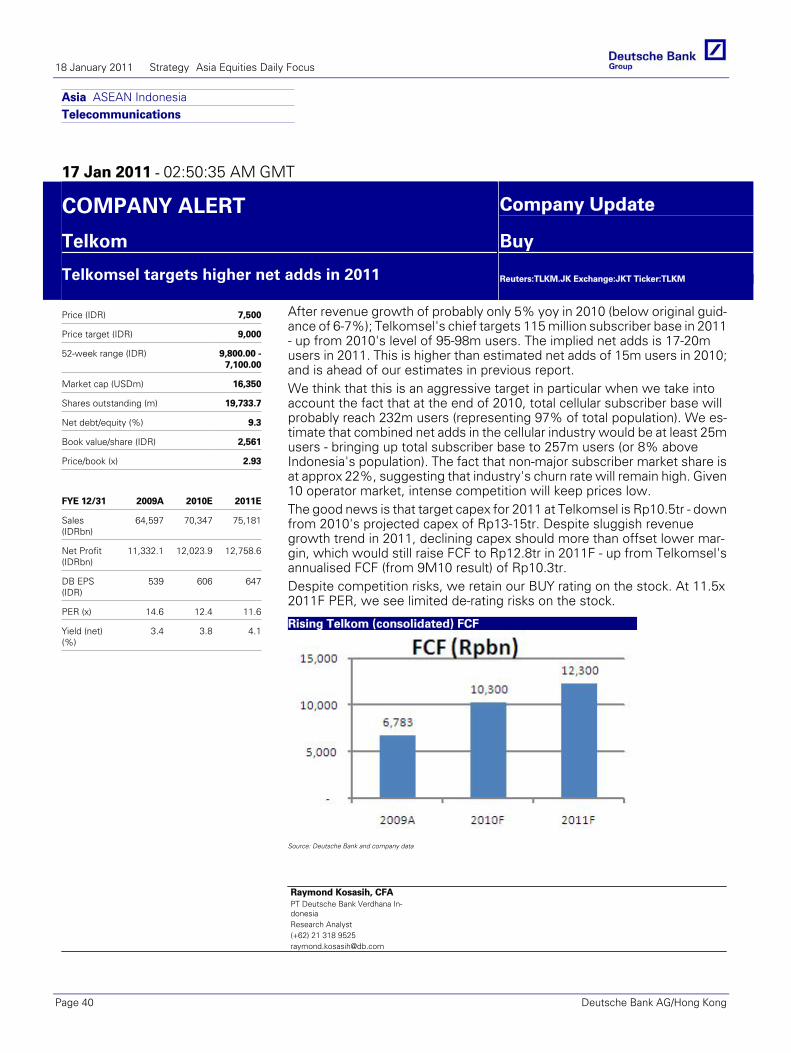

Telkom (TLKM.JK),IDR7,500.00 Buy Price Target IDR9,000.00

Telkomsel targets higher net adds in 2011

Raymond Kosasih

Page 40

GLOBAL RESEARCH

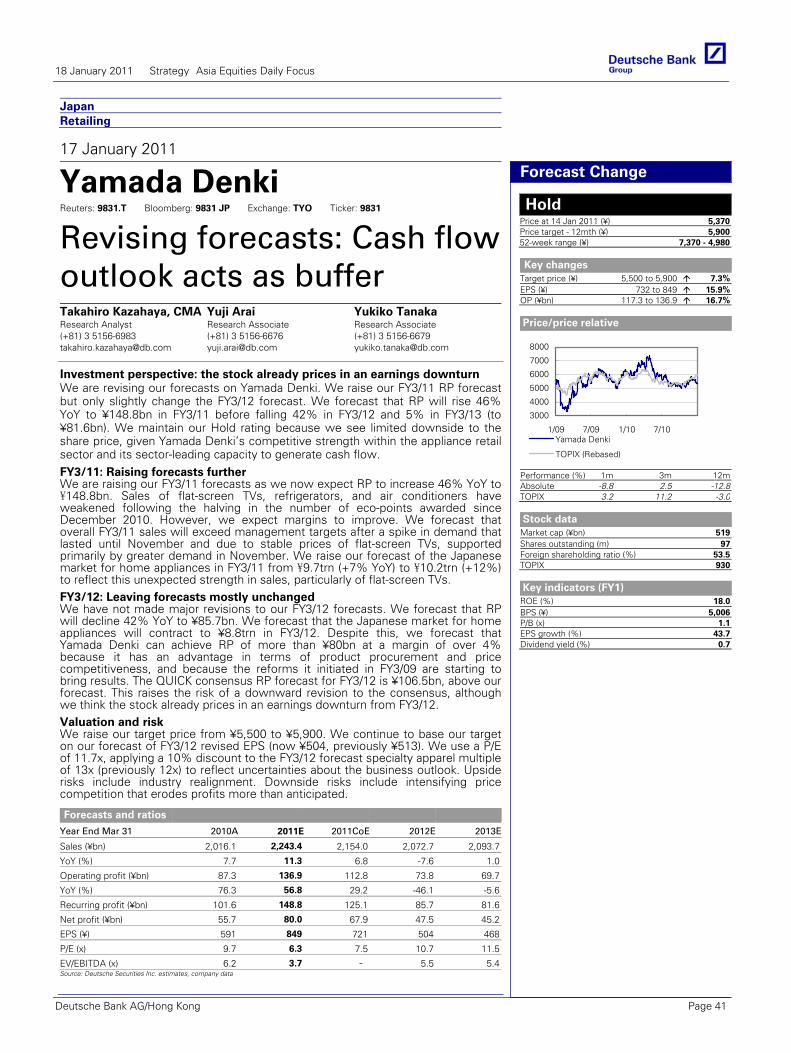

Yamada Denki (9831.T),¥5,430 Hold Price Target ¥5,900

Revising forecasts: Cash flow outlook acts as buffer

Takahiro Kazahaya Page 41

The notes and reports contained in this Daily are all excerpts of previously published documents. Please refer to the published notes on our web site for details on risks, valuations and earnings changes

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 3

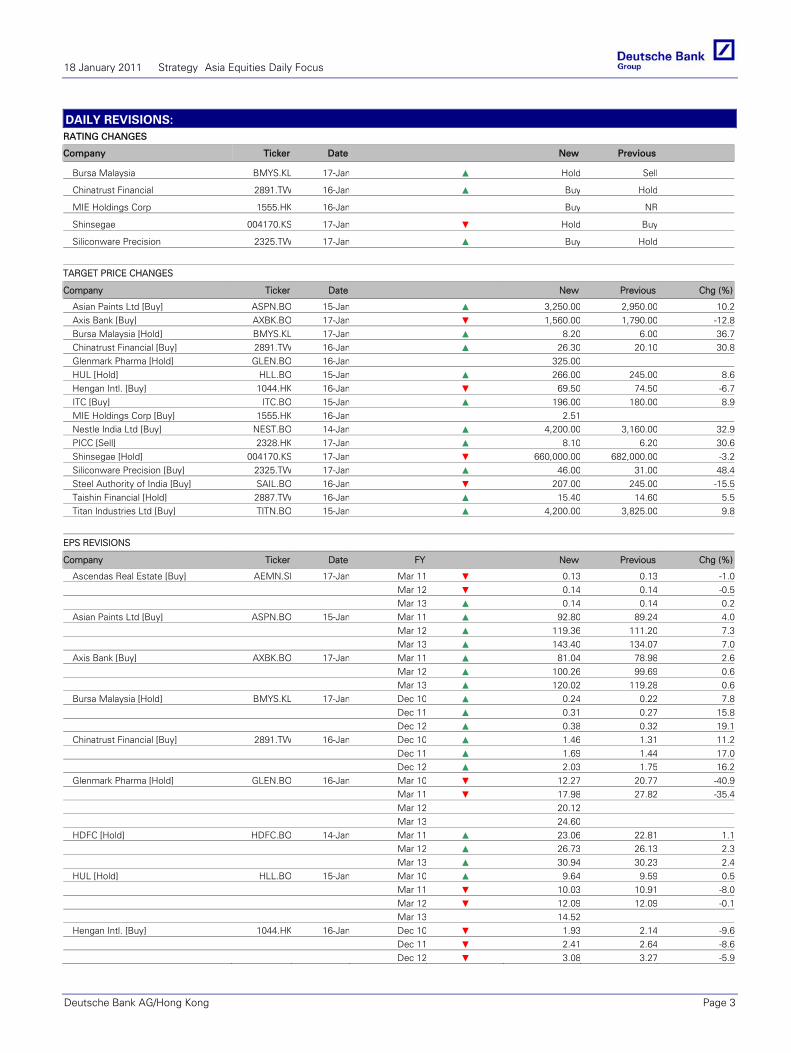

DAILY REVISIONS: RATING CHANGES

Company Ticker Date New Previous

Bursa Malaysia BMYS.KL 17-Jan ▲ Hold Sell

Chinatrust Financial 2891.TW 16-Jan ▲ Buy Hold

MIE Holdings Corp 1555.HK 16-Jan Buy NR

Shinsegae 004170.KS 17-Jan ▼ Hold Buy

Siliconware Precision 2325.TW 17-Jan ▲ Buy Hold

TARGET PRICE CHANGES

Company Ticker Date New Previous Chg (%)

Asian Paints Ltd [Buy] ASPN.BO 15-Jan ▲ 3,250.00 2,950.00 10.2Axis Bank [Buy] AXBK.BO 17-Jan ▼ 1,560.00 1,790.00 -12.8Bursa Malaysia [Hold] BMYS.KL 17-Jan ▲ 8.20 6.00 36.7Chinatrust Financial [Buy] 2891.TW 16-Jan ▲ 26.30 20.10 30.8Glenmark Pharma [Hold] GLEN.BO 16-Jan 325.00 HUL [Hold] HLL.BO 15-Jan ▲ 266.00 245.00 8.6Hengan Intl. [Buy] 1044.HK 16-Jan ▼ 69.50 74.50 -6.7ITC [Buy] ITC.BO 15-Jan ▲ 196.00 180.00 8.9MIE Holdings Corp [Buy] 1555.HK 16-Jan 2.51 Nestle India Ltd [Buy] NEST.BO 14-Jan ▲ 4,200.00 3,160.00 32.9PICC [Sell] 2328.HK 17-Jan ▲ 8.10 6.20 30.6Shinsegae [Hold] 004170.KS 17-Jan ▼ 660,000.00 682,000.00 -3.2Siliconware Precision [Buy] 2325.TW 17-Jan ▲ 46.00 31.00 48.4Steel Authority of India [Buy] SAIL.BO 16-Jan ▼ 207.00 245.00 -15.5Taishin Financial [Hold] 2887.TW 16-Jan ▲ 15.40 14.60 5.5Titan Industries Ltd [Buy] TITN.BO 15-Jan ▲ 4,200.00 3,825.00 9.8

EPS REVISIONS

Company Ticker Date FY New Previous Chg (%)

Ascendas Real Estate [Buy] AEMN.SI 17-Jan Mar 11 ▼ 0.13 0.13 -1.0 Mar 12 ▼ 0.14 0.14 -0.5 Mar 13 ▲ 0.14 0.14 0.2Asian Paints Ltd [Buy] ASPN.BO 15-Jan Mar 11 ▲ 92.80 89.24 4.0 Mar 12 ▲ 119.36 111.20 7.3 Mar 13 ▲ 143.40 134.07 7.0Axis Bank [Buy] AXBK.BO 17-Jan Mar 11 ▲ 81.04 78.98 2.6 Mar 12 ▲ 100.26 99.69 0.6 Mar 13 ▲ 120.02 119.28 0.6Bursa Malaysia [Hold] BMYS.KL 17-Jan Dec 10 ▲ 0.24 0.22 7.8 Dec 11 ▲ 0.31 0.27 15.8 Dec 12 ▲ 0.38 0.32 19.1Chinatrust Financial [Buy] 2891.TW 16-Jan Dec 10 ▲ 1.46 1.31 11.2 Dec 11 ▲ 1.69 1.44 17.0 Dec 12 ▲ 2.03 1.75 16.2Glenmark Pharma [Hold] GLEN.BO 16-Jan Mar 10 ▼ 12.27 20.77 -40.9 Mar 11 ▼ 17.98 27.82 -35.4 Mar 12 20.12 Mar 13 24.60 HDFC [Hold] HDFC.BO 14-Jan Mar 11 ▲ 23.06 22.81 1.1 Mar 12 ▲ 26.73 26.13 2.3 Mar 13 ▲ 30.94 30.23 2.4HUL [Hold] HLL.BO 15-Jan Mar 10 ▲ 9.64 9.59 0.5 Mar 11 ▼ 10.03 10.91 -8.0 Mar 12 ▼ 12.09 12.09 -0.1 Mar 13 14.52 Hengan Intl. [Buy] 1044.HK 16-Jan Dec 10 ▼ 1.93 2.14 -9.6 Dec 11 ▼ 2.41 2.64 -8.6 Dec 12 ▼ 3.08 3.27 -5.9

18 January 2011 Strategy Asia Equities Daily Focus

Page 4 Deutsche Bank AG/Hong Kong

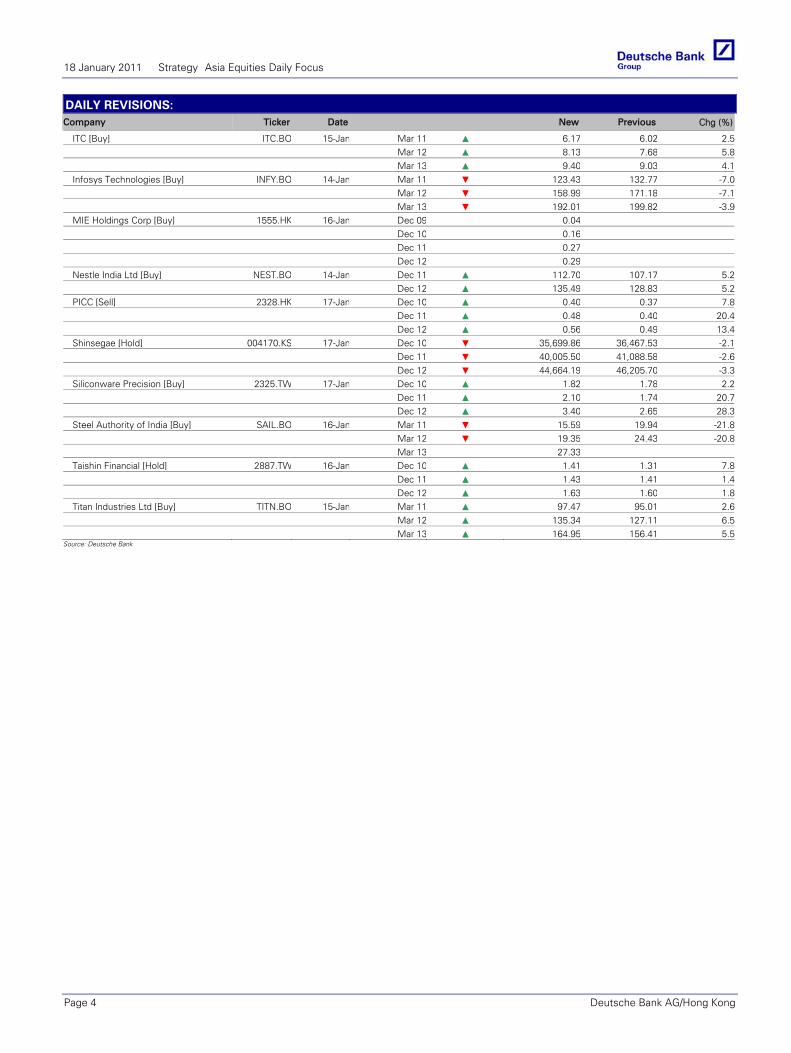

DAILY REVISIONS: Company Ticker Date New Previous Chg (%)

ITC [Buy] ITC.BO 15-Jan Mar 11 ▲ 6.17 6.02 2.5 Mar 12 ▲ 8.13 7.68 5.8 Mar 13 ▲ 9.40 9.03 4.1Infosys Technologies [Buy] INFY.BO 14-Jan Mar 11 ▼ 123.43 132.77 -7.0 Mar 12 ▼ 158.99 171.18 -7.1 Mar 13 ▼ 192.01 199.82 -3.9MIE Holdings Corp [Buy] 1555.HK 16-Jan Dec 09 0.04 Dec 10 0.16 Dec 11 0.27 Dec 12 0.29 Nestle India Ltd [Buy] NEST.BO 14-Jan Dec 11 ▲ 112.70 107.17 5.2 Dec 12 ▲ 135.49 128.83 5.2PICC [Sell] 2328.HK 17-Jan Dec 10 ▲ 0.40 0.37 7.8 Dec 11 ▲ 0.48 0.40 20.4 Dec 12 ▲ 0.56 0.49 13.4Shinsegae [Hold] 004170.KS 17-Jan Dec 10 ▼ 35,699.86 36,467.53 -2.1 Dec 11 ▼ 40,005.50 41,088.58 -2.6 Dec 12 ▼ 44,664.19 46,205.70 -3.3Siliconware Precision [Buy] 2325.TW 17-Jan Dec 10 ▲ 1.82 1.78 2.2 Dec 11 ▲ 2.10 1.74 20.7 Dec 12 ▲ 3.40 2.65 28.3Steel Authority of India [Buy] SAIL.BO 16-Jan Mar 11 ▼ 15.59 19.94 -21.8 Mar 12 ▼ 19.35 24.43 -20.8 Mar 13 27.33 Taishin Financial [Hold] 2887.TW 16-Jan Dec 10 ▲ 1.41 1.31 7.8 Dec 11 ▲ 1.43 1.41 1.4 Dec 12 ▲ 1.63 1.60 1.8Titan Industries Ltd [Buy] TITN.BO 15-Jan Mar 11 ▲ 97.47 95.01 2.6 Mar 12 ▲ 135.34 127.11 6.5 Mar 13 ▲ 164.95 156.41 5.5

Source: Deutsche Bank

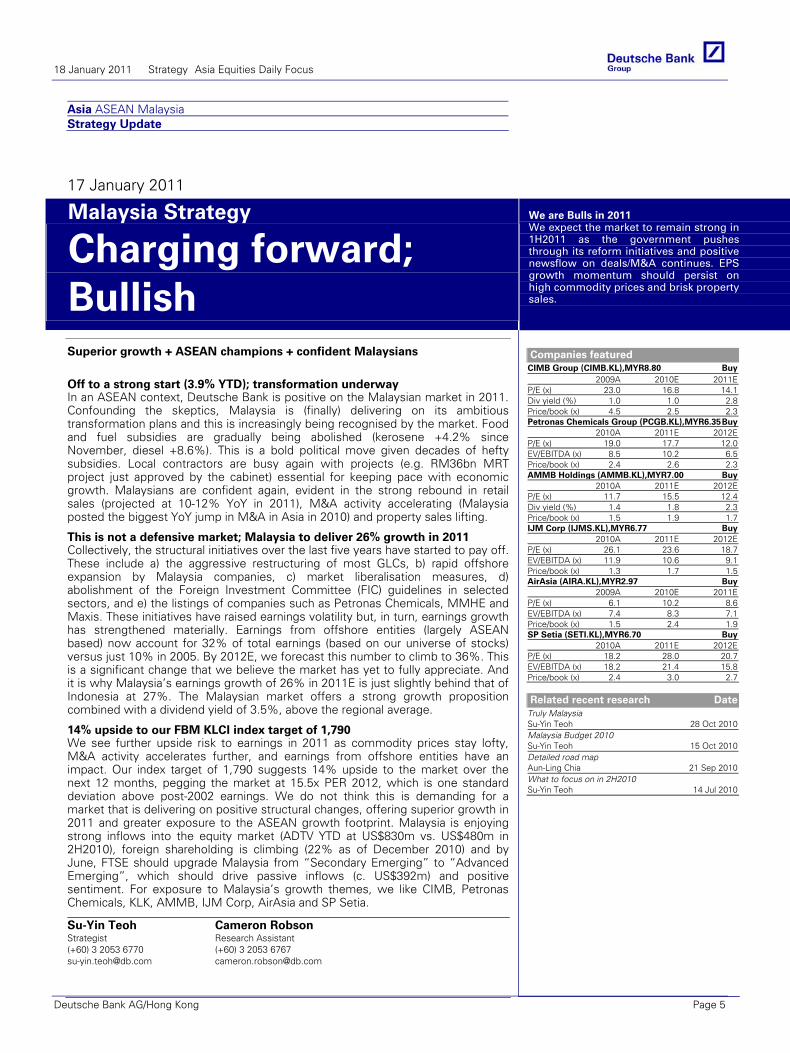

Asia ASEAN Malaysia Strategy Update

17 January 2011

Malaysia Strategy

Charging forward; Bullish

We are Bulls in 2011 We expect the market to remain strong in 1H2011 as the government pushes through its reform initiatives and positive newsflow on deals/M&A continues. EPS growth momentum should persist on high commodity prices and brisk property sales.

Superior growth + ASEAN champions + confident Malaysians

Su-Yin Teoh Strategist (+60) 3 2053 6770 [email protected]

Cameron Robson Research Assistant (+60) 3 2053 6767 [email protected]

Deutsche Bank AG/Hong Kong

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

Companies featured

CIMB Group (CIMB.KL),MYR8.80 Buy2009A 2010E 2011E

P/E (x) 23.0 16.8 14.1Div yield (%) 1.0 1.0 2.8Price/book (x) 4.5 2.5 2.3Petronas Chemicals Group (PCGB.KL),MYR6.35Buy

2010A 2011E 2012EP/E (x) 19.0 17.7 12.0EV/EBITDA (x) 8.5 10.2 6.5Price/book (x) 2.4 2.6 2.3AMMB Holdings (AMMB.KL),MYR7.00 Buy

2010A 2011E 2012EP/E (x) 11.7 15.5 12.4Div yield (%) 1.4 1.8 2.3Price/book (x) 1.5 1.9 1.7IJM Corp (IJMS.KL),MYR6.77 Buy

2010A 2011E 2012EP/E (x) 26.1 23.6 18.7EV/EBITDA (x) 11.9 10.6 9.1Price/book (x) 1.3 1.7 1.5AirAsia (AIRA.KL),MYR2.97 Buy

2009A 2010E 2011EP/E (x) 6.1 10.2 8.6EV/EBITDA (x) 7.4 8.3 7.1Price/book (x) 1.5 2.4 1.9SP Setia (SETI.KL),MYR6.70 Buy

2010A 2011E 2012EP/E (x) 18.2 28.0 20.7EV/EBITDA (x) 18.2 21.4 15.8Price/book (x) 2.4 3.0 2.7

Related recent research Date

Truly Malaysia Su-Yin Teoh 28 Oct 2010Malaysia Budget 2010 Su-Yin Teoh 15 Oct 2010Detailed road map Aun-Ling Chia 21 Sep 2010What to focus on in 2H2010 Su-Yin Teoh 14 Jul 2010

Off to a strong start (3.9% YTD); transformation underway In an ASEAN context, Deutsche Bank is positive on the Malaysian market in 2011. Confounding the skeptics, Malaysia is (finally) delivering on its ambitious transformation plans and this is increasingly being recognised by the market. Food and fuel subsidies are gradually being abolished (kerosene +4.2% since November, diesel +8.6%). This is a bold political move given decades of hefty subsidies. Local contractors are busy again with projects (e.g. RM36bn MRT project just approved by the cabinet) essential for keeping pace with economic growth. Malaysians are confident again, evident in the strong rebound in retail sales (projected at 10-12% YoY in 2011), M&A activity accelerating (Malaysia posted the biggest YoY jump in M&A in Asia in 2010) and property sales lifting.

This is not a defensive market; Malaysia to deliver 26% growth in 2011 Collectively, the structural initiatives over the last five years have started to pay off. These include a) the aggressive restructuring of most GLCs, b) rapid offshore expansion by Malaysia companies, c) market liberalisation measures, d) abolishment of the Foreign Investment Committee (FIC) guidelines in selected sectors, and e) the listings of companies such as Petronas Chemicals, MMHE and Maxis. These initiatives have raised earnings volatility but, in turn, earnings growth has strengthened materially. Earnings from offshore entities (largely ASEAN based) now account for 32% of total earnings (based on our universe of stocks) versus just 10% in 2005. By 2012E, we forecast this number to climb to 36%. This is a significant change that we believe the market has yet to fully appreciate. And it is why Malaysia’s earnings growth of 26% in 2011E is just slightly behind that of Indonesia at 27%. The Malaysian market offers a strong growth proposition combined with a dividend yield of 3.5%, above the regional average.

14% upside to our FBM KLCI index target of 1,790 We see further upside risk to earnings in 2011 as commodity prices stay lofty, M&A activity accelerates further, and earnings from offshore entities have an impact. Our index target of 1,790 suggests 14% upside to the market over the next 12 months, pegging the market at 15.5x PER 2012, which is one standard deviation above post-2002 earnings. We do not think this is demanding for a market that is delivering on positive structural changes, offering superior growth in 2011 and greater exposure to the ASEAN growth footprint. Malaysia is enjoying strong inflows into the equity market (ADTV YTD at US$830m vs. US$480m in 2H2010), foreign shareholding is climbing (22% as of December 2010) and by June, FTSE should upgrade Malaysia from “Secondary Emerging” to “Advanced Emerging”, which should drive passive inflows (c. US$392m) and positive sentiment. For exposure to Malaysia’s growth themes, we like CIMB, Petronas Chemicals, KLK, AMMB, IJM Corp, AirAsia and SP Setia.

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 5

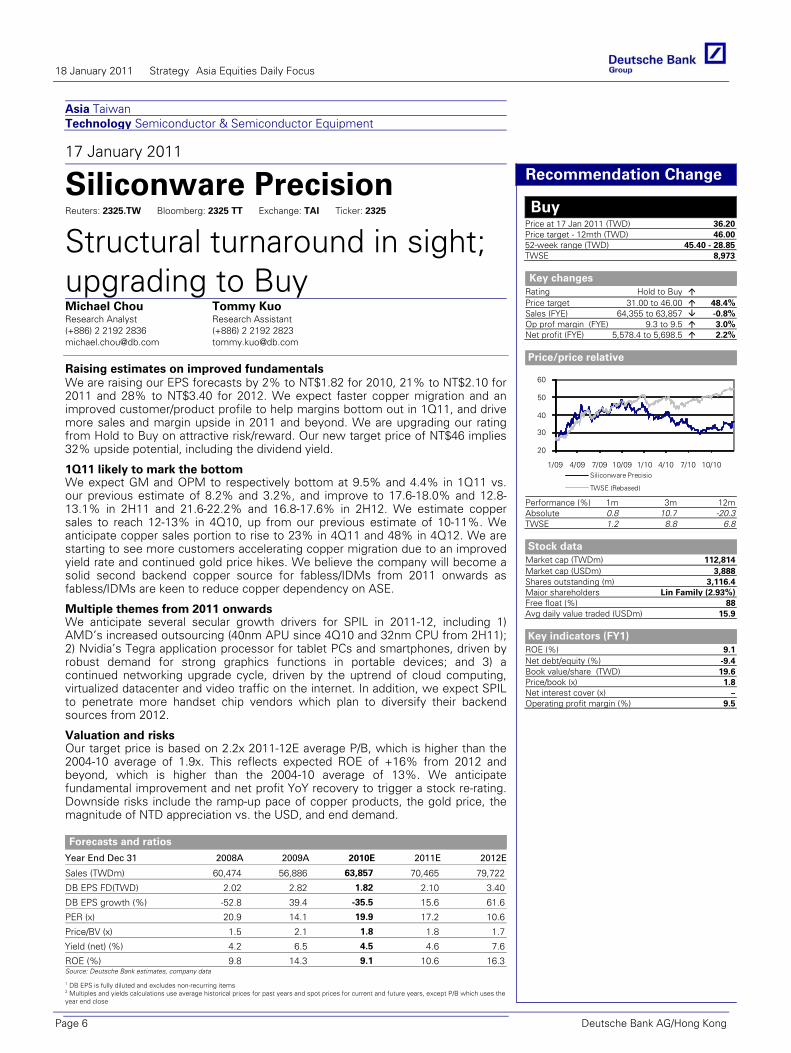

Asia Taiwan Technology Semiconductor & Semiconductor Equipment

17 January 2011

Siliconware Precision Reuters: 2325.TW Bloomberg: 2325 TT Exchange: TAI Ticker: 2325

Structural turnaround in sight; upgrading to Buy Michael Chou Research Analyst (+886) 2 2192 2836 [email protected]

Tommy Kuo Research Assistant (+886) 2 2192 2823 [email protected]

Raising estimates on improved fundamentals We are raising our EPS forecasts by 2% to NT$1.82 for 2010, 21% to NT$2.10 for 2011 and 28% to NT$3.40 for 2012. We expect faster copper migration and an improved customer/product profile to help margins bottom out in 1Q11, and drive more sales and margin upside in 2011 and beyond. We are upgrading our rating from Hold to Buy on attractive risk/reward. Our new target price of NT$46 implies 32% upside potential, including the dividend yield.

Forecasts and ratios

Year End Dec 31 2008A 2009A 2010E 2011E 2012E

Sales (TWDm) 60,474 56,886 63,857 70,465 79,722

DB EPS FD(TWD) 2.02 2.82 1.82 2.10 3.40

DB EPS growth (%) -52.8 39.4 -35.5 15.6 61.6

PER (x) 20.9 14.1 19.9 17.2 10.6

Price/BV (x) 1.5 2.1 1.8 1.8 1.7

Yield (net) (%) 4.2 6.5 4.5 4.6 7.6

ROE (%) 9.8 14.3 9.1 10.6 16.3Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Recommendation Change

Buy Price at 17 Jan 2011 (TWD) 36.20Price target - 12mth (TWD) 46.0052-week range (TWD) 45.40 - 28.85TWSE 8,973

Key changes

Rating Hold to Buy Price target 31.00 to 46.00 48.4%Sales (FYE) 64,355 to 63,857 -0.8%Op prof margin (FYE) 9.3 to 9.5 3.0%Net profit (FYE) 5,578.4 to 5,698.5 2.2%

Price/price relative

20

30

40

50

60

1/09 4/09 7/09 10/09 1/10 4/10 7/10 10/10Siliconware Precisio

TWSE (Rebased)

Performance (%) 1m 3m 12mAbsolute 0.8 10.7 -20.3TWSE 1.2 8.8 6.8

Stock data

Market cap (TWDm) 112,814Market cap (USDm) 3,888Shares outstanding (m) 3,116.4Major shareholders Lin Family (2.93%)Free float (%) 88Avg daily value traded (USDm) 15.9

Key indicators (FY1)

ROE (%) 9.1Net debt/equity (%) -9.4Book value/share (TWD) 19.6Price/book (x) 1.8Net interest cover (x) –Operating profit margin (%) 9.5

1Q11 likely to mark the bottom We expect GM and OPM to respectively bottom at 9.5% and 4.4% in 1Q11 vs. our previous estimate of 8.2% and 3.2%, and improve to 17.6-18.0% and 12.8-13.1% in 2H11 and 21.6-22.2% and 16.8-17.6% in 2H12. We estimate copper sales to reach 12-13% in 4Q10, up from our previous estimate of 10-11%. We anticipate copper sales portion to rise to 23% in 4Q11 and 48% in 4Q12. We are starting to see more customers accelerating copper migration due to an improved yield rate and continued gold price hikes. We believe the company will become a solid second backend copper source for fabless/IDMs from 2011 onwards as fabless/IDMs are keen to reduce copper dependency on ASE.

Multiple themes from 2011 onwards We anticipate several secular growth drivers for SPIL in 2011-12, including 1) AMD’s increased outsourcing (40nm APU since 4Q10 and 32nm CPU from 2H11); 2) Nvidia’s Tegra application processor for tablet PCs and smartphones, driven by robust demand for strong graphics functions in portable devices; and 3) a continued networking upgrade cycle, driven by the uptrend of cloud computing, virtualized datacenter and video traffic on the internet. In addition, we expect SPIL to penetrate more handset chip vendors which plan to diversify their backend sources from 2012.

Valuation and risks Our target price is based on 2.2x 2011-12E average P/B, which is higher than the 2004-10 average of 1.9x. This reflects expected ROE of +16% from 2012 and beyond, which is higher than the 2004-10 average of 13%. We anticipate fundamental improvement and net profit YoY recovery to trigger a stock re-rating. Downside risks include the ramp-up pace of copper products, the gold price, the magnitude of NTD appreciation vs. the USD, and end demand.

18 January 2011 Strategy Asia Equities Daily Focus

Page 6 Deutsche Bank AG/Hong Kong

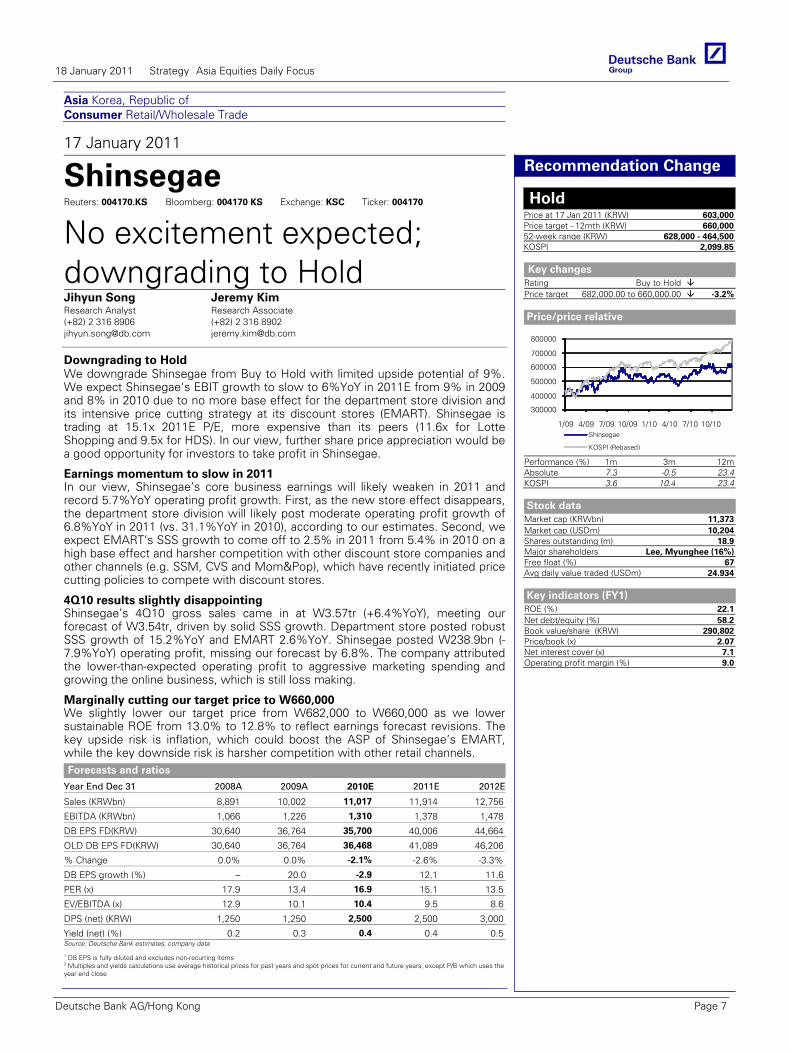

Asia Korea, Republic of Consumer Retail/Wholesale Trade

17 January 2011

Shinsegae Reuters: 004170.KS Bloomberg: 004170 KS Exchange: KSC Ticker: 004170

No excitement expected; downgrading to HoldJihyun Song Research Analyst (+82) 2 316 8906 [email protected]

Jeremy Kim Research Associate (+82) 2 316 8902 [email protected]

Downgrading to Hold We downgrade Shinsegae from Buy to Hold with limited upside potential of 9%. We expect Shinsegae's EBIT growth to slow to 6%YoY in 2011E from 9% in 2009 and 8% in 2010 due to no more base effect for the department store division and its intensive price cutting strategy at its discount stores (EMART). Shinsegae is trading at 15.1x 2011E P/E, more expensive than its peers (11.6x for Lotte Shopping and 9.5x for HDS). In our view, further share price appreciation would be a good opportunity for investors to take profit in Shinsegae.

Forecasts and ratios

Year End Dec 31 2008A 2009A 2010E 2011E 2012E

Sales (KRWbn) 8,891 10,002 11,017 11,914 12,756

EBITDA (KRWbn) 1,066 1,226 1,310 1,378 1,478

DB EPS FD(KRW) 30,640 36,764 35,700 40,006 44,664

OLD DB EPS FD(KRW) 30,640 36,764 36,468 41,089 46,206

% Change 0.0% 0.0% -2.1% -2.6% -3.3%

DB EPS growth (%) – 20.0 -2.9 12.1 11.6

PER (x) 17.9 13.4 16.9 15.1 13.5

EV/EBITDA (x) 12.9 10.1 10.4 9.5 8.6

DPS (net) (KRW) 1,250 1,250 2,500 2,500 3,000

Yield (net) (%) 0.2 0.3 0.4 0.4 0.5Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Recommendation Change

Hold Price at 17 Jan 2011 (KRW) 603,000Price target - 12mth (KRW) 660,00052-week range (KRW) 628,000 - 464,500KOSPI 2,099.85

Key changes

Rating Buy to Hold Price target 682,000.00 to 660,000.00 -3.2%

Price/price relative

300000

400000

500000

600000

700000

800000

1/09 4/09 7/09 10/09 1/10 4/10 7/10 10/10Shinsegae

KOSPI (Rebased)

Performance (%) 1m 3m 12mAbsolute 7.3 -0.5 23.4KOSPI 3.6 10.4 23.4

Stock data

Market cap (KRWbn) 11,373Market cap (USDm) 10,204Shares outstanding (m) 18.9Major shareholders Lee, Myunghee (16%)Free float (%) 67Avg daily value traded (USDm) 24.934

Key indicators (FY1)

ROE (%) 22.1Net debt/equity (%) 58.2Book value/share (KRW) 290,802Price/book (x) 2.07Net interest cover (x) 7.1Operating profit margin (%) 9.0

Co

mp

any

Glo

bal

Mar

kets

Res

earc

h

Earnings momentum to slow in 2011 In our view, Shinsegae’s core business earnings will likely weaken in 2011 and record 5.7%YoY operating profit growth. First, as the new store effect disappears, the department store division will likely post moderate operating profit growth of 6.8%YoY in 2011 (vs. 31.1%YoY in 2010), according to our estimates. Second, we expect EMART’s SSS growth to come off to 2.5% in 2011 from 5.4% in 2010 on a high base effect and harsher competition with other discount store companies and other channels (e.g. SSM, CVS and Mom&Pop), which have recently initiated price cutting policies to compete with discount stores.

4Q10 results slightly disappointing Shinsegae’s 4Q10 gross sales came in at W3.57tr (+6.4%YoY), meeting our forecast of W3.54tr, driven by solid SSS growth. Department store posted robust SSS growth of 15.2%YoY and EMART 2.6%YoY. Shinsegae posted W238.9bn (-7.9%YoY) operating profit, missing our forecast by 6.8%. The company attributed the lower-than-expected operating profit to aggressive marketing spending and growing the online business, which is still loss making.

Marginally cutting our target price to W660,000 We slightly lower our target price from W682,000 to W660,000 as we lower sustainable ROE from 13.0% to 12.8% to reflect earnings forecast revisions. The key upside risk is inflation, which could boost the ASP of Shinsegae’s EMART, while the key downside risk is harsher competition with other retail channels.

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 7

Asia ASEAN Malaysia Banking/Finance Exchanges

17 January 2011

Bursa Malaysia Reuters: BMYS.KL Bloomberg: BURSA MK Exchange: KLS Ticker: BMYS

Turnover rebound; upgrade to Hold Andrew Hill, CFA Research Analyst (+65) 6423 8507 [email protected]

Su-Yin Teoh Strategist (+60) 3 2053 6770 [email protected]

Upgrade to Hold Given the recent rebound in market activity we have upgraded earnings forecasts substantially and as a result raised our rating to Hold from Sell with a revised price target of RM8.20/share. Although we think valuation is not compelling, with a forward PE below its long-run average and strong turnover trends persisting into 2011 we suspect the share price will remain well supported.

Forecasts and ratios

Year End Dec 31 2008A 2009A 2010E 2011E 2012E

Net profit (MYRm) 104.4 101.6 132.8 176.5 220.0

EPS (MYR) 0.20 0.19 0.24 0.31 0.38

EPS growth (%) -56.9 -3.1 28.3 28.7 20.8

PER (x) 41.2 36.6 37.0 28.7 23.8

EV/EBITDA (x) 23.8 10.2 17.3 13.1 10.4

Yield (net) (%) 2.2 2.6 2.5 3.2 3.9Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Recommendation Change

Hold Price at 17 Jan 2011 (MYR) 8.97Price target - 12mth 8.2052-week range (MYR) 8.97 - 6.78KLSE COMPOSITE 1,570

Key changes

Rating Sell to Hold Price target 6.00 to 8.20 36.7%

Price/price relative

3

5

6

8

9

11

1/09 4/09 7/09 10/09 1/10 4/10 7/10 10/10Bursa Malaysia

KLSE COMPOSITE (Rebased)

Performance (%) 1m 3m 12mAbsolute 11.9 3.1 10.8KLSE COMPOSITE 3.9 4.9 21.3

Stock data

Market cap (MYRm) 4,717Market cap (USDm) 1,542Shares outstanding (m) 537.3Major shareholders CMDF (19.52%)Free float (%) 76Avg daily value traded (USDm) 3.6

Key indicators (FY1)

ROE (%) 15.6Net debt/equity (%) -137.6Book value/share (MYR) 1.58Price/book (x) 5.7Net interest cover (x) 306.9Operating profit margin (%) 45.4

Glo

bal

Mar

kets

Res

earc

h

EPS upgrades 8-19% on strong volumes Recent turnover trends in the Malaysian equity market have been particularly robust leading us to upgrade earnings by 8% for 2010e, 16% for 2011e and 19% for 2012e. From a 2010e base of RM1.6bn, we now assume average daily equity market turnover (ADT) of RM2.1bn in 2011e and RM2.5bn in 2012e. Our 2011e ADT reflects 22% growth in average market capitalisation and an increase in velocity to 37% from 34% in 2010.

Equity market turnover has rebounded substantially At RM2bn, December quarter average daily equity market turnover was up 35% QoQ bringing quarterly turnover to its highest level since the global financial crisis. And so far in 2011 volume trends have remained very strong. January turnover in the month-to-date is up 81% on pcp. If sustained this would represent a record month for January turnover and if maintained for the full year we estimate would imply a further 30% upside to our 2011e EPS. But turnover is inherently volatile and we suspect the current level of activity will not be maintained suggesting revisions risks are relatively evenly balanced, in our view.

Target price raised to RM8.20/share Following earnings revisions and a roll forward of our valuation we have raised our target price to RM8.20/share (from RM6/share) based on a three-stage DDM methodology, consistent with the methodology we employ for the closest listed peer SGX (SGXL.SI, Buy, S$10.50/share). Key assumptions are detailed in Figure 4 on page 4 and include beta 1.2, cost of equity 11% and terminal growth of 5%. At 28x one-year forward PE the stock is trading below its long term average 30x. Key sensitivity remains variations in equity market turnover. Main upside risk from further economic liberalization, potential tie-ups with regional exchanges, potential capital management and renewed offshore participation. Key downside risk is a slowdown in broader market activity.

18 January 2011 Strategy Asia Equities Daily Focus

Page 8 Deutsche Bank AG/Hong Kong

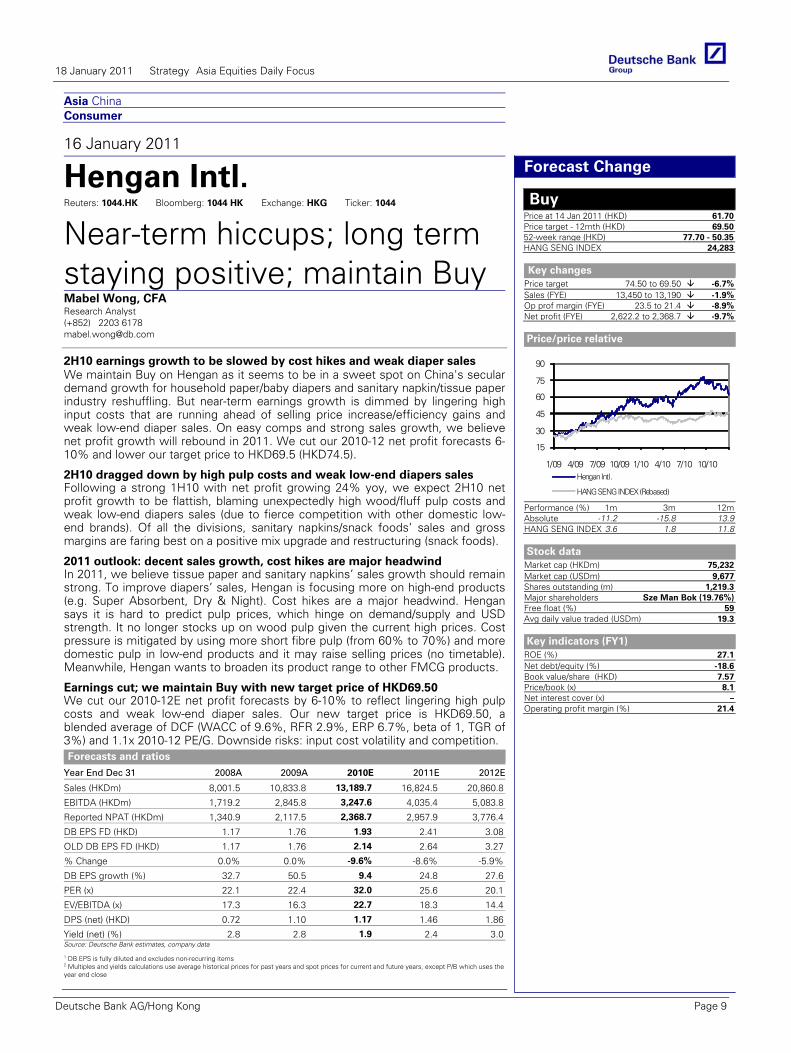

Asia China Consumer

16 January 2011

Hengan Intl. Reuters: 1044.HK Bloomberg: 1044 HK Exchange: HKG Ticker: 1044

Near-term hiccups; long term staying positive; maintain BuyMabel Wong, CFA Research Analyst (+852) 2203 6178 [email protected]

2H10 earnings growth to be slowed by cost hikes and weak diaper sales We maintain Buy on Hengan as it seems to be in a sweet spot on China's secular demand growth for household paper/baby diapers and sanitary napkin/tissue paper industry reshuffling. But near-term earnings growth is dimmed by lingering high input costs that are running ahead of selling price increase/efficiency gains and weak low-end diaper sales. On easy comps and strong sales growth, we believe net profit growth will rebound in 2011. We cut our 2010-12 net profit forecasts 6-10% and lower our target price to HKD69.5 (HKD74.5).

Forecasts and ratios

Year End Dec 31 2008A 2009A 2010E 2011E 2012E

Sales (HKDm) 8,001.5 10,833.8 13,189.7 16,824.5 20,860.8

EBITDA (HKDm) 1,719.2 2,845.8 3,247.6 4,035.4 5,083.8

Reported NPAT (HKDm) 1,340.9 2,117.5 2,368.7 2,957.9 3,776.4

DB EPS FD (HKD) 1.17 1.76 1.93 2.41 3.08

OLD DB EPS FD (HKD) 1.17 1.76 2.14 2.64 3.27

% Change 0.0% 0.0% -9.6% -8.6% -5.9%

DB EPS growth (%) 32.7 50.5 9.4 24.8 27.6

PER (x) 22.1 22.4 32.0 25.6 20.1

EV/EBITDA (x) 17.3 16.3 22.7 18.3 14.4

DPS (net) (HKD) 0.72 1.10 1.17 1.46 1.86

Yield (net) (%) 2.8 2.8 1.9 2.4 3.0Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Forecast Change

Buy Price at 14 Jan 2011 (HKD) 61.70Price target - 12mth (HKD) 69.5052-week range (HKD) 77.70 - 50.35HANG SENG INDEX 24,283

Key changes

Price target 74.50 to 69.50 -6.7%Sales (FYE) 13,450 to 13,190 -1.9%Op prof margin (FYE) 23.5 to 21.4 -8.9%Net profit (FYE) 2,622.2 to 2,368.7 -9.7%

Price/price relative

15

30

45

60

75

90

1/09 4/09 7/09 10/09 1/10 4/10 7/10 10/10Hengan Intl.

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute -11.2 -15.8 13.9HANG SENG INDEX 3.6 1.8 11.8

Stock data

Market cap (HKDm) 75,232Market cap (USDm) 9,677Shares outstanding (m) 1,219.3Major shareholders Sze Man Bok (19.76%)Free float (%) 59Avg daily value traded (USDm) 19.3

Key indicators (FY1)

ROE (%) 27.1Net debt/equity (%) -18.6Book value/share (HKD) 7.57Price/book (x) 8.1Net interest cover (x) –Operating profit margin (%) 21.4

2H10 dragged down by high pulp costs and weak low-end diapers sales Following a strong 1H10 with net profit growing 24% yoy, we expect 2H10 net profit growth to be flattish, blaming unexpectedly high wood/fluff pulp costs and weak low-end diapers sales (due to fierce competition with other domestic low-end brands). Of all the divisions, sanitary napkins/snack foods’ sales and gross margins are faring best on a positive mix upgrade and restructuring (snack foods).

2011 outlook: decent sales growth, cost hikes are major headwind In 2011, we believe tissue paper and sanitary napkins’ sales growth should remain strong. To improve diapers’ sales, Hengan is focusing more on high-end products (e.g. Super Absorbent, Dry & Night). Cost hikes are a major headwind. Hengan says it is hard to predict pulp prices, which hinge on demand/supply and USD strength. It no longer stocks up on wood pulp given the current high prices. Cost pressure is mitigated by using more short fibre pulp (from 60% to 70%) and more domestic pulp in low-end products and it may raise selling prices (no timetable). Meanwhile, Hengan wants to broaden its product range to other FMCG products.

Earnings cut; we maintain Buy with new target price of HKD69.50 We cut our 2010-12E net profit forecasts by 6-10% to reflect lingering high pulp costs and weak low-end diaper sales. Our new target price is HKD69.50, a blended average of DCF (WACC of 9.6%, RFR 2.9%, ERP 6.7%, beta of 1, TGR of 3%) and 1.1x 2010-12 PE/G. Downside risks: input cost volatility and competition.

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 9

Asia China Banking/Finance General Insurance

17 January 2011

PICC Reuters: 2328.HK Bloomberg: 2328 HK Exchange: HKG Ticker: 2328

Group restructuring is still a dilution risk Bob Leung Research Analyst (+852) 2203 6200 [email protected]

Rolling DCF model into 2011, raising target price to HK$8.10 without dilution We roll forward our normalized DCF valuation model for PICC to 2011 and raise our target price to HK$8.10 per share (assuming no capital-raising). We also raise our FY10E net profit by 11% due to faster-than-expected GWP growth of PICC’s motor insurance portfolio. Factoring in up to a 75bps rise in interest rates in 2011 and raising our premium growth target to 16%, we also raise our FY11E net profit by 32%.

Forecasts and ratios

Year End Dec 31 2008A 2009A 2010E 2011E 2012E

Net earned premiums 80,019.0 93,296.0 118,324.8 136,763.9 151,118.3

Underwriting income -2,605.0 -2,060.0 2,142.4 2,711.2 3,181.3

Net investment income 3,716.0 2,866.0 3,910.2 4,989.5 5,727.9

Net profit (CNYm) 47.0 1,640.0 4,433.2 5,318.1 6,229.5

DB EPS (CNY) 0.01 0.16 0.40 0.48 0.56

OLD DB EPS (CNY) 0.01 0.16 0.37 0.40 0.49

% Change 0.0% 0.0% 7.8% 20.4% 13.4%

DB EPS growth (%) – 1,535.7 148.6 20.0 17.1

PER (x) 508.7 28.6 22.9 19.1 16.3

Price/book (x) 2.1 3.2 3.9 3.2 2.7Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Forecast Change

Sell Price at 17 Jan 2011 (HKD) 10.76Price target - 12mth (HKD) 8.1052-week range (HKD) 12.24 - 6.57HANG SENG INDEX 24,157

Key changes

Price target 6.20 to 8.10 30.6%Net earned prem (FYE)109,452.7 to 118,324.8Underwriting inc (FYE) 1,892.7 to 2,142.4 13.2%Net profit (FYE) 4,111.6 to 4,433.2 7.8%

Price/price relative

2

46

8

10

12

14

1/09 4/09 7/09 10/09 1/10 4/10 7/10 10/10PICC

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute 0.9 -9.3 36.9HANG SENG INDEX 6.3 1.7 11.6

Stock data

Market Cap (HKDm) 119,888Market Cap (USDm) 15,421Shares outstanding (m) 11,142.0Major shareholders PICC Holdings (72%)Free Float (%) 18Avg daily value traded (USDm) 23.0

Key indicators (FY1)

ROE (%) 18.5Growth in Net premiums (%) 26.8Loss ratio (%) 66.7Expense ratio (%) 31.5Combined ratio (%) 98.2

Glo

bal

Mar

kets

Res

earc

h

Priced in 18% growth in next five years with forever underwriting profits Our DCF valuation currently assumes a forever strong combine ratio at 97.5% –98% with average long-term investment yield at 4%. With an effective tax rate of approximately 22%, PICC’s current stock price at HK$10.76 implies a self-sustained (without capital injection) 18% premium growth for the next five years. This is clearly unrealistic, in our view, given PICC’s solvency will most likely drop towards 100% as at December 2010 with the group debt-to-net equity ratio already more than 35%.

Group restructuring is a dilution risk, not a capital solution Even in the event of PICC’s parent group finally restructuring and seeking eventual listing (which is a complex and difficult event), this would not provide a solution to PICC’s capital needs without significant dilution to earnings. We estimate that PICC would now need up to Rmb8-11bn fresh equity capital (keeping the debt-to-net equity ratio below 35%) to sustain growth above 12-15% over the next three years if it is to maintain a solvency margin of more than 150%.

Downside risk to our valuation PICC’s stock price still trades over 3.3x our revised FY11 P/B. With a high debt-to-equity ratio, further dilution looks likely. We are already assuming forever strong underwriting profitability, which is unlikely, with increasing natural disasters. We maintain Sell with a downside risk to our valuation, where capital-raising is highly likely in 2011 to support growth. Strong A-share performance is an upside risk.

18 January 2011 Strategy Asia Equities Daily Focus 18 January 2011 Strategy Asia Equities Daily Focus

Page 10 Deutsche Bank AG/Hong Kong

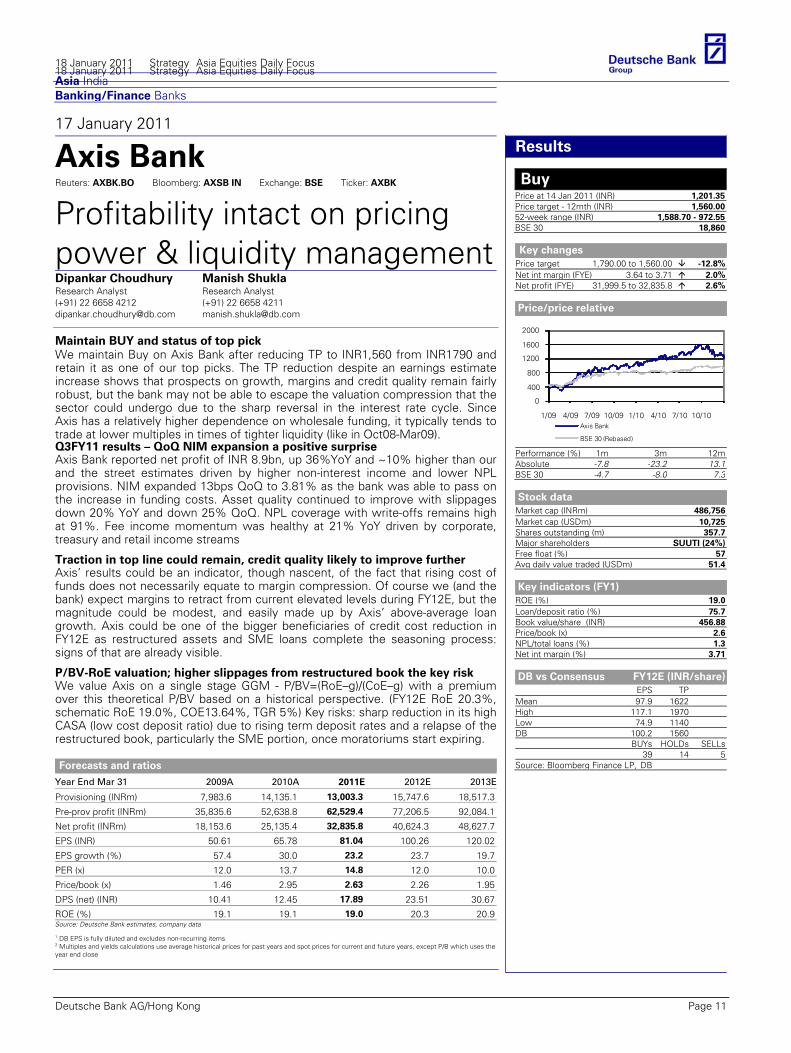

Asia India Banking/Finance Banks

17 January 2011

Axis Bank Reuters: AXBK.BO Bloomberg: AXSB IN Exchange: BSE Ticker: AXBK

Profitability intact on pricing power & liquidity managementDipankar Choudhury Research Analyst (+91) 22 6658 4212 [email protected]

Manish Shukla Research Analyst (+91) 22 6658 4211 [email protected]

Maintain BUY and status of top pick We maintain Buy on Axis Bank after reducing TP to INR1,560 from INR1790 and retain it as one of our top picks. The TP reduction despite an earnings estimate increase shows that prospects on growth, margins and credit quality remain fairly robust, but the bank may not be able to escape the valuation compression that the sector could undergo due to the sharp reversal in the interest rate cycle. Since Axis has a relatively higher dependence on wholesale funding, it typically tends to trade at lower multiples in times of tighter liquidity (like in Oct08-Mar09).

Forecasts and ratios

Year End Mar 31 2009A 2010A 2011E 2012E 2013E

Provisioning (INRm) 7,983.6 14,135.1 13,003.3 15,747.6 18,517.3

Pre-prov profit (INRm) 35,835.6 52,638.8 62,529.4 77,206.5 92,084.1

Net profit (INRm) 18,153.6 25,135.4 32,835.8 40,624.3 48,627.7

EPS (INR) 50.61 65.78 81.04 100.26 120.02

EPS growth (%) 57.4 30.0 23.2 23.7 19.7

PER (x) 12.0 13.7 14.8 12.0 10.0

Price/book (x) 1.46 2.95 2.63 2.26 1.95

DPS (net) (INR) 10.41 12.45 17.89 23.51 30.67

ROE (%) 19.1 19.1 19.0 20.3 20.9Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Results

Buy Price at 14 Jan 2011 (INR) 1,201.35Price target - 12mth (INR) 1,560.0052-week range (INR) 1,588.70 - 972.55BSE 30 18,860

Key changes

Price target 1,790.00 to 1,560.00 -12.8%Net int margin (FYE) 3.64 to 3.71 2.0%Net profit (FYE) 31,999.5 to 32,835.8 2.6%

Price/price relative

0

400

800

1200

1600

2000

1/09 4/09 7/09 10/09 1/10 4/10 7/10 10/10Axis Bank

BSE 30 (Rebased)

Performance (%) 1m 3m 12mAbsolute -7.8 -23.2 13.1BSE 30 -4.7 -8.0 7.3

Stock data

Market cap (INRm) 486,756Market cap (USDm) 10,725Shares outstanding (m) 357.7Major shareholders SUUTI (24%)Free float (%) 57Avg daily value traded (USDm) 51.4

Key indicators (FY1)

ROE (%) 19.0Loan/deposit ratio (%) 75.7Book value/share (INR) 456.88Price/book (x) 2.6NPL/total loans (%) 1.3Net int margin (%) 3.71

DB vs Consensus FY12E (INR/share)

EPS TPMean 97.9 1622High 117.1 1970Low 74.9 1140DB 100.2 1560

BUYs HOLDs SELLs39 14 5

Source: Bloomberg Finance LP, DB

Co

mp

any

Q3FY11 results – QoQ NIM expansion a positive surprise Axis Bank reported net profit of INR 8.9bn, up 36%YoY and ~10% higher than our and the street estimates driven by higher non-interest income and lower NPL provisions. NIM expanded 13bps QoQ to 3.81% as the bank was able to pass on the increase in funding costs. Asset quality continued to improve with slippages down 20% YoY and down 25% QoQ. NPL coverage with write-offs remains high at 91%. Fee income momentum was healthy at 21% YoY driven by corporate, treasury and retail income streams

Traction in top line could remain, credit quality likely to improve further Axis’ results could be an indicator, though nascent, of the fact that rising cost of funds does not necessarily equate to margin compression. Of course we (and the bank) expect margins to retract from current elevated levels during FY12E, but the magnitude could be modest, and easily made up by Axis’ above-average loan growth. Axis could be one of the bigger beneficiaries of credit cost reduction in FY12E as restructured assets and SME loans complete the seasoning process: signs of that are already visible.

P/BV-RoE valuation; higher slippages from restructured book the key risk We value Axis on a single stage GGM - P/BV=(RoE–g)/(CoE–g) with a premium over this theoretical P/BV based on a historical perspective. (FY12E RoE 20.3%, schematic RoE 19.0%, COE13.64%, TGR 5%) Key risks: sharp reduction in its high CASA (low cost deposit ratio) due to rising term deposit rates and a relapse of the restructured book, particularly the SME portion, once moratoriums start expiring.

18 January 2011 Strategy Asia Equities Daily Focus 18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 11

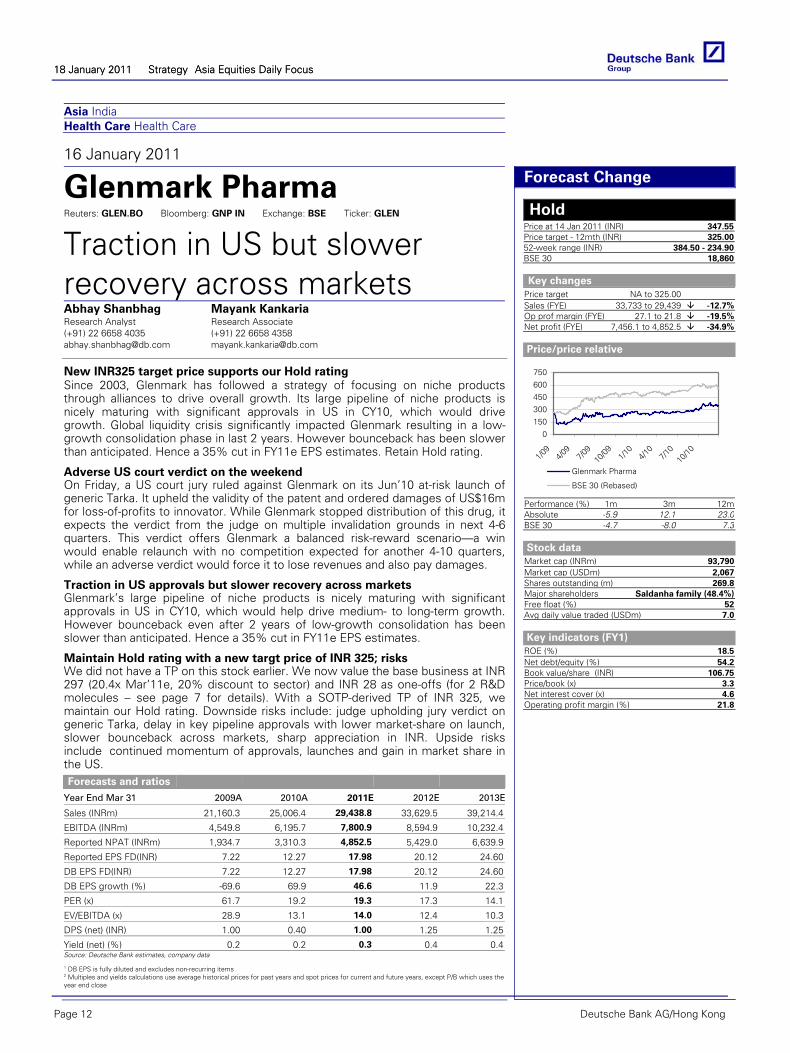

Asia India Health Care Health Care

16 January 2011

Glenmark Pharma Reuters: GLEN.BO Bloomberg: GNP IN Exchange: BSE Ticker: GLEN

Traction in US but slower recovery across marketsAbhay Shanbhag Research Analyst (+91) 22 6658 4035 [email protected]

Mayank Kankaria Research Associate (+91) 22 6658 4358 [email protected]

New INR325 target price supports our Hold rating Since 2003, Glenmark has followed a strategy of focusing on niche products through alliances to drive overall growth. Its large pipeline of niche products is nicely maturing with significant approvals in US in CY10, which would drive growth. Global liquidity crisis significantly impacted Glenmark resulting in a low-growth consolidation phase in last 2 years. However bounceback has been slower than anticipated. Hence a 35% cut in FY11e EPS estimates. Retain Hold rating.

Forecasts and ratios

Year End Mar 31 2009A 2010A 2011E 2012E 2013E

Sales (INRm) 21,160.3 25,006.4 29,438.8 33,629.5 39,214.4

EBITDA (INRm) 4,549.8 6,195.7 7,800.9 8,594.9 10,232.4

Reported NPAT (INRm) 1,934.7 3,310.3 4,852.5 5,429.0 6,639.9

Reported EPS FD(INR) 7.22 12.27 17.98 20.12 24.60

DB EPS FD(INR) 7.22 12.27 17.98 20.12 24.60

DB EPS growth (%) -69.6 69.9 46.6 11.9 22.3

PER (x) 61.7 19.2 19.3 17.3 14.1

EV/EBITDA (x) 28.9 13.1 14.0 12.4 10.3

DPS (net) (INR) 1.00 0.40 1.00 1.25 1.25

Yield (net) (%) 0.2 0.2 0.3 0.4 0.4Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Forecast Change

Hold Price at 14 Jan 2011 (INR) 347.55Price target - 12mth (INR) 325.0052-week range (INR) 384.50 - 234.90BSE 30 18,860

Key changes

Price target NA to 325.00 Sales (FYE) 33,733 to 29,439 -12.7%Op prof margin (FYE) 27.1 to 21.8 -19.5%Net profit (FYE) 7,456.1 to 4,852.5 -34.9%

Price/price relative

0

150

300450

600

750

1/09

4/09

7/09

10/09 1/1

04/1

07/1

010

/10

Glenmark Pharma

BSE 30 (Rebased)

Performance (%) 1m 3m 12mAbsolute -5.9 12.1 23.0BSE 30 -4.7 -8.0 7.3

Stock data

Market cap (INRm) 93,790Market cap (USDm) 2,067Shares outstanding (m) 269.8Major shareholders Saldanha family (48.4%)Free float (%) 52Avg daily value traded (USDm) 7.0

Key indicators (FY1)

ROE (%) 18.5Net debt/equity (%) 54.2Book value/share (INR) 106.75Price/book (x) 3.3Net interest cover (x) 4.6Operating profit margin (%) 21.8

Adverse US court verdict on the weekend On Friday, a US court jury ruled against Glenmark on its Jun’10 at-risk launch of generic Tarka. It upheld the validity of the patent and ordered damages of US$16m for loss-of-profits to innovator. While Glenmark stopped distribution of this drug, it expects the verdict from the judge on multiple invalidation grounds in next 4-6 quarters. This verdict offers Glenmark a balanced risk-reward scenario—a win would enable relaunch with no competition expected for another 4-10 quarters, while an adverse verdict would force it to lose revenues and also pay damages.

Traction in US approvals but slower recovery across markets Glenmark’s large pipeline of niche products is nicely maturing with significant approvals in US in CY10, which would help drive medium- to long-term growth. However bounceback even after 2 years of low-growth consolidation has been slower than anticipated. Hence a 35% cut in FY11e EPS estimates.

Maintain Hold rating with a new targt price of INR 325; risks We did not have a TP on this stock earlier. We now value the base business at INR 297 (20.4x Mar’11e, 20% discount to sector) and INR 28 as one-offs (for 2 R&D molecules – see page 7 for details). With a SOTP-derived TP of INR 325, we maintain our Hold rating. Downside risks include: judge upholding jury verdict on generic Tarka, delay in key pipeline approvals with lower market-share on launch, slower bounceback across markets, sharp appreciation in INR. Upside risks include �continued momentum of approvals, launches and gain in market share in the US.

18 January 2011 Strategy Asia Equities Daily Focus 18 January 2011 Strategy Asia Equities Daily Focus

Page 12 Deutsche Bank AG/Hong Kong

Asia India Resources Metals & Mining

17 January 2011

Steel Authority of India Reuters: SAIL.BO Bloomberg: SAIL IN Exchange: BSE Ticker: SAIL

Revising estimates down but remain positive Abhay Laijawala Research Analyst (+91) 22 6658 4205 [email protected]

Anuj Singla Research Analyst (+91) 22 6658 4172 [email protected]

Cutting estimates and TP on higher coking coal prices; maintain Buy Following the lower-than-expected 3Q’FY11 results and upward revision of our coking coal assumptions, we are cutting our earnings estimates for FY11 and FY12 by 22% and 21%, respectively. Consequently, we are cutting our target price by 15% to INR207. We remain excited over SAIL’s modernization program which is expected to improve SAIL’s profitability significantly, once its full benefits are harnessed. We expect the benefits of modernization to become apparent from FY13 - when the IISCO plant is progressively commissioned.

Forecasts and ratios

Year End Mar 31 2009A 2010A 2011E 2012E 2013E

Sales (INRm) 431,500.8 405,513.8 443,670.1 503,260.7 602,558.7

EBITDA (INRm) 84,082.0 90,798.3 92,062.7 115,139.9 165,622.9

Reported NPAT (INRm) 61,748.1 67,543.7 64,377.0 79,925.7 112,896.0

DB EPS growth (%) -18.1 9.4 -4.7 24.2 41.3

DB EPS FD(INR) 14.95 16.35 15.59 19.35 27.33

OLD DB EPS FD(INR) 14.95 16.35 19.94 24.43 –

% Change 0.0% 0.0% -21.8% -20.8% –

PER (x) 8.0 11.1 10.4 8.3 5.9

EV/EBITDA (x) 4.5 7.5 6.6 5.5 3.7

Yield (net) (%) 2.2 1.8 2.0 2.5 3.1Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Forecast Change

Buy Price at 14 Jan 2011 (INR) 161.35Price target - 12mth (INR) 207.0052-week range (INR) 256.35 - 161.35BSE 30 18,860

Key changes

Price target 245.00 to 207.00 -15.5%Sales (FYE) 480,621 to 443,670 -7.7%Op prof margin (FYE) 21.8 to 17.4 -20.2%Net profit (FYE) 82,342.4 to 64,377.0 -21.8%

Price/price relative

4080

120160200240280

1/09

4/09

7/09

10/09 1/1

04/1

07/1

010

/10

Steel Authority of I

BSE 30 (Rebased)

Performance (%) 1m 3m 12mAbsolute -11.6 -28.1 -32.9BSE 30 -4.7 -8.0 7.3

Stock data

Market cap (INRm) 666,440Market cap (USDm) 14,684Shares outstanding (m) 4,130.4Major shareholders Govt. of India (86%)Free float(%) 14Avg daily value traded (USDm) 14.4

Key indicators (FY1)

ROE (%) 18.0Net debt/equity (%) -15.0Book value/share (INR) 92.49Price/book (x) 1.7Net interest cover (x) 17.1Operating profit margin (%) 17.4

Coking coal availability and prices remain area of concern Until its modernization is complete, SAIL will remain an inefficient user of coking coal and hence its earnings remain more vulnerable - than its domestic peers - to sharp rises in coking coal prices. With coking coal constituting 73% of SAIL’s raw material costs and 44% of its operating costs, we estimate that for every US$10 increase in annual coking coal prices, SAIL’s FY12 EPS would decline by 3.2%. We confess that our earnings forecasts for FY12 may be at risk if coking coal availability is impacted or if prices rise more than our forecasts (US$274/tonne).

Stock price weakness over done; expect sharp earnings recovery in 4Q’FY11 SAIL’s stock price has been under pressure recently on account of the overhang of equity issuance and weak results. While 3Q’FY11 results were below our expectations, we remain confident of a sharp recovery in both margins and earnings in 4Q’FY11 on the back of resumption in global steel pricing momentum and improving volumes. The stock is currently trading at a valuation discount to its global peers and appears attractive, in our view.

Reiterate Buy with revised target price of INR207/share We have increased our target multiple to 7.2x, in line with the expansion of valuation multiples for global steel companies. Our target multiple is still at a 10% discount to CSN, steel company similar in profile with captive access to iron ore. Downside risks: appreciation in INR, delay in expansion/ modernization programme, escalation in coking coal prices (see p.8).

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 13

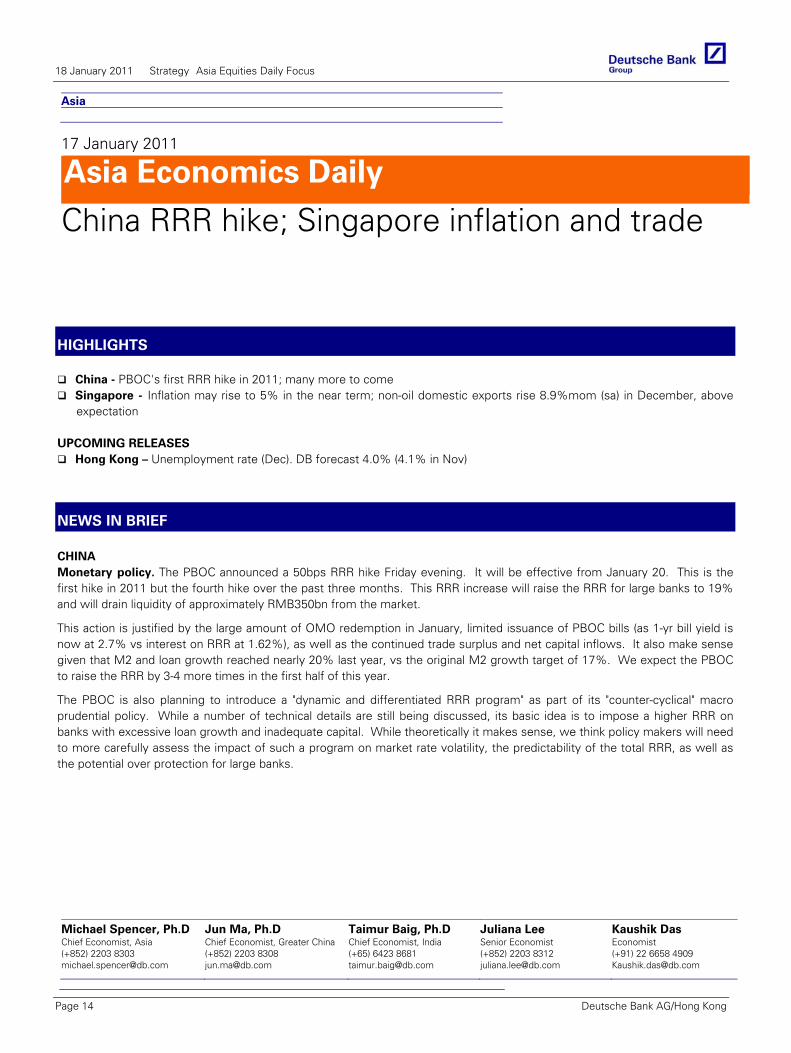

Asia

17 January 2011

Asia Economics Daily

China RRR hike; Singapore inflation and trade

Deutsche Bank AG/Hong Kong

Michael Spencer, Ph.D Chief Economist, Asia (+852) 2203 8303 [email protected]

Jun Ma, Ph.D Chief Economist, Greater China (+852) 2203 8308 [email protected]

Taimur Baig, Ph.D Chief Economist, India (+65) 6423 8681 [email protected]

Juliana Lee Senior Economist (+852) 2203 8312 [email protected]

Kaushik Das Economist (+91) 22 6658 4909 [email protected]

Mac

ro

Glo

bal

Mar

kets

Res

earc

h

Eco

no

mic

s

HIGHLIGHTS

China - PBOC's first RRR hike in 2011; many more to come Singapore - Inflation may rise to 5% in the near term; non-oil domestic exports rise 8.9%mom (sa) in December, above

expectation UPCOMING RELEASES

Hong Kong – Unemployment rate (Dec). DB forecast 4.0% (4.1% in Nov)

NEWS IN BRIEF

CHINA Monetary policy. The PBOC announced a 50bps RRR hike Friday evening. It will be effective from January 20. This is the first hike in 2011 but the fourth hike over the past three months. This RRR increase will raise the RRR for large banks to 19% and will drain liquidity of approximately RMB350bn from the market.

This action is justified by the large amount of OMO redemption in January, limited issuance of PBOC bills (as 1-yr bill yield is now at 2.7% vs interest on RRR at 1.62%), as well as the continued trade surplus and net capital inflows. It also make sense given that M2 and loan growth reached nearly 20% last year, vs the original M2 growth target of 17%. We expect the PBOC to raise the RRR by 3-4 more times in the first half of this year.

The PBOC is also planning to introduce a "dynamic and differentiated RRR program" as part of its "counter-cyclical" macro prudential policy. While a number of technical details are still being discussed, its basic idea is to impose a higher RRR on banks with excessive loan growth and inadequate capital. While theoretically it makes sense, we think policy makers will need to more carefully assess the impact of such a program on market rate volatility, the predictability of the total RRR, as well as the potential over protection for large banks.

18 January 2011 Strategy Asia Equities Daily Focus

Page 14 Deutsche Bank AG/Hong Kong

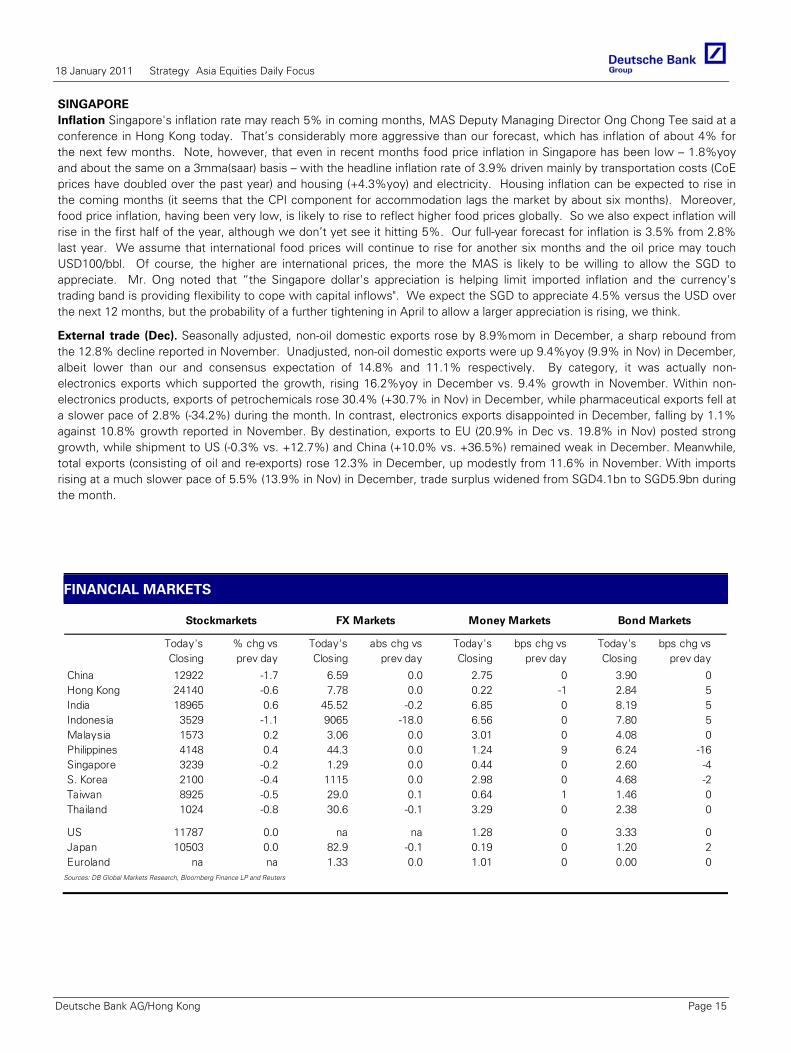

SINGAPORE Inflation Singapore's inflation rate may reach 5% in coming months, MAS Deputy Managing Director Ong Chong Tee said at a conference in Hong Kong today. That’s considerably more aggressive than our forecast, which has inflation of about 4% for the next few months. Note, however, that even in recent months food price inflation in Singapore has been low – 1.8%yoy and about the same on a 3mma(saar) basis – with the headline inflation rate of 3.9% driven mainly by transportation costs (CoE prices have doubled over the past year) and housing (+4.3%yoy) and electricity. Housing inflation can be expected to rise in the coming months (it seems that the CPI component for accommodation lags the market by about six months). Moreover, food price inflation, having been very low, is likely to rise to reflect higher food prices globally. So we also expect inflation will rise in the first half of the year, although we don’t yet see it hitting 5%. Our full-year forecast for inflation is 3.5% from 2.8% last year. We assume that international food prices will continue to rise for another six months and the oil price may touch USD100/bbl. Of course, the higher are international prices, the more the MAS is likely to be willing to allow the SGD to appreciate. Mr. Ong noted that “the Singapore dollar's appreciation is helping limit imported inflation and the currency's trading band is providing flexibility to cope with capital inflows". We expect the SGD to appreciate 4.5% versus the USD over the next 12 months, but the probability of a further tightening in April to allow a larger appreciation is rising, we think.

External trade (Dec). Seasonally adjusted, non-oil domestic exports rose by 8.9%mom in December, a sharp rebound from the 12.8% decline reported in November. Unadjusted, non-oil domestic exports were up 9.4%yoy (9.9% in Nov) in December, albeit lower than our and consensus expectation of 14.8% and 11.1% respectively. By category, it was actually non-electronics exports which supported the growth, rising 16.2%yoy in December vs. 9.4% growth in November. Within non-electronics products, exports of petrochemicals rose 30.4% (+30.7% in Nov) in December, while pharmaceutical exports fell at a slower pace of 2.8% (-34.2%) during the month. In contrast, electronics exports disappointed in December, falling by 1.1% against 10.8% growth reported in November. By destination, exports to EU (20.9% in Dec vs. 19.8% in Nov) posted strong growth, while shipment to US (-0.3% vs. +12.7%) and China (+10.0% vs. +36.5%) remained weak in December. Meanwhile, total exports (consisting of oil and re-exports) rose 12.3% in December, up modestly from 11.6% in November. With imports rising at a much slower pace of 5.5% (13.9% in Nov) in December, trade surplus widened from SGD4.1bn to SGD5.9bn during the month.

FINANCIAL MARKETS

Today's % chg vs Today's abs chg vs Today's bps chg vs Today's bps chg vsClosing prev day Closing prev day Closing prev day Closing prev day

China 12922 -1.7 6.59 0.0 2.75 0 3.90 0Hong Kong 24140 -0.6 7.78 0.0 0.22 -1 2.84 5India 18965 0.6 45.52 -0.2 6.85 0 8.19 5Indonesia 3529 -1.1 9065 -18.0 6.56 0 7.80 5Malaysia 1573 0.2 3.06 0.0 3.01 0 4.08 0Philippines 4148 0.4 44.3 0.0 1.24 9 6.24 -16Singapore 3239 -0.2 1.29 0.0 0.44 0 2.60 -4S. Korea 2100 -0.4 1115 0.0 2.98 0 4.68 -2Taiwan 8925 -0.5 29.0 0.1 0.64 1 1.46 0Thailand 1024 -0.8 30.6 -0.1 3.29 0 2.38 0

US 11787 0.0 na na 1.28 0 3.33 0Japan 10503 0.0 82.9 -0.1 0.19 0 1.20 2Euroland na na 1.33 0.0 1.01 0 0.00 0

Stockmarkets FX Markets Money Markets Bond Markets

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 15

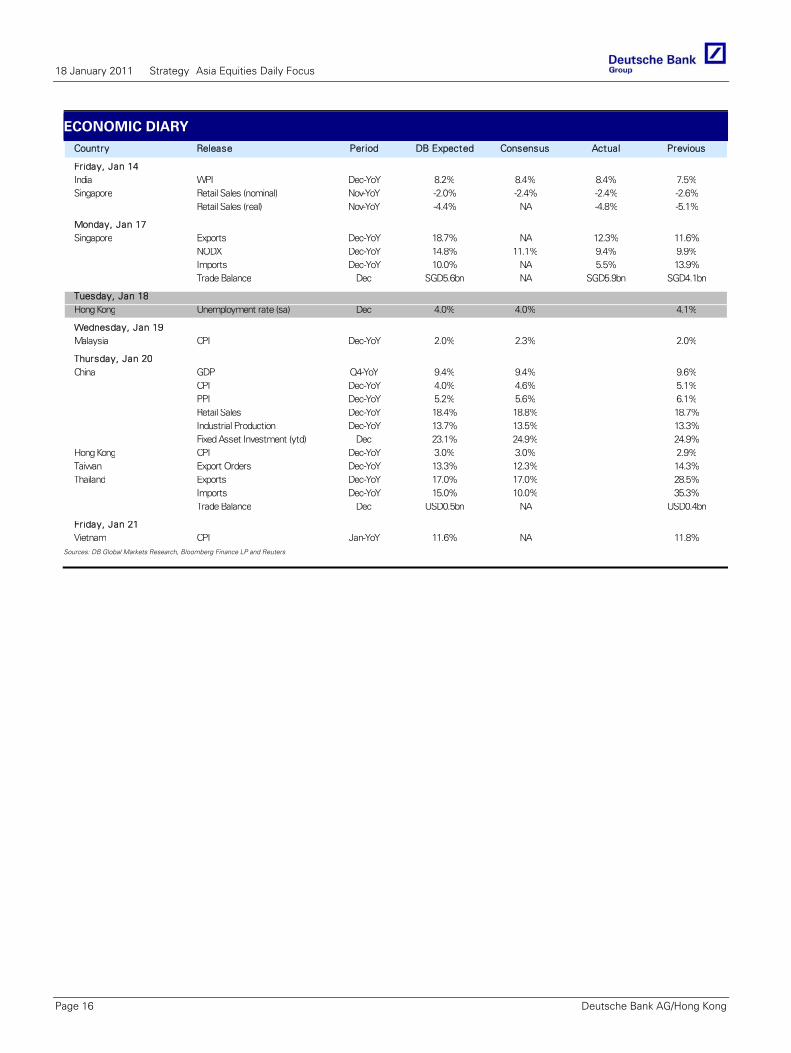

ECONOMIC DIARY Country Release Period DB Expected Consensus Actual Previous

Friday, Jan 14India WPI Dec-YoY 8.2% 8.4% 8.4% 7.5%Singapore Retail Sales (nominal) Nov-YoY -2.0% -2.4% -2.4% -2.6%

Retail Sales (real) Nov-YoY -4.4% NA -4.8% -5.1%

Monday, Jan 17Singapore Exports Dec-YoY 18.7% NA 12.3% 11.6%

NODX Dec-YoY 14.8% 11.1% 9.4% 9.9%Imports Dec-YoY 10.0% NA 5.5% 13.9%Trade Balance Dec SGD5.6bn NA SGD5.9bn SGD4.1bn

Tuesday, Jan 18Hong Kong Unemployment rate (sa) Dec 4.0% 4.0% 4.1%

Wednesday, Jan 19Malaysia CPI Dec-YoY 2.0% 2.3% 2.0%

Thursday, Jan 20China GDP Q4-YoY 9.4% 9.4% 9.6%

CPI Dec-YoY 4.0% 4.6% 5.1%PPI Dec-YoY 5.2% 5.6% 6.1%Retail Sales Dec-YoY 18.4% 18.8% 18.7%Industrial Production Dec-YoY 13.7% 13.5% 13.3%Fixed Asset Investment (ytd) Dec 23.1% 24.9% 24.9%

Hong Kong CPI Dec-YoY 3.0% 3.0% 2.9%Taiwan Export Orders Dec-YoY 13.3% 12.3% 14.3%Thailand Exports Dec-YoY 17.0% 17.0% 28.5%

Imports Dec-YoY 15.0% 10.0% 35.3%Trade Balance Dec USD0.5bn NA USD0.4bn

Friday, Jan 21Vietnam CPI Jan-YoY 11.6% NA 11.8%

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

18 January 2011 Strategy Asia Equities Daily Focus

Page 16 Deutsche Bank AG/Hong Kong

Asia

17 January 2011

Asia Economics Monthly January

Economics

Table of Contents Asia economic and financial forecasts ............... Page 2Overview ............................................................ Page 3China................................................................... Page 8Hong Kong........................................................ Page 10India .................................................................. Page 12Indonesia .......................................................... Page 16Malaysia............................................................ Page 18Philippines ........................................................ Page 20Singapore ......................................................... Page 22South Korea ...................................................... Page 24Taiwan .............................................................. Page 28Thailand ............................................................ Page 30Interest rate and inflation charts....................... Page 32Asian economic indicators ............................... Page 36

Research Team

Michael Spencer, Ph.D Chief Economist, Asia (+852) 2203 8305 [email protected]

Jun Ma, Ph.D Chief Economist, Greater China (+852) 2203 8308 [email protected]

Taimur Baig, Ph.D Chief Economist, India (+65) 6423 8681 [email protected]

Juliana Lee Senior Economist (+852) 2203 8312 [email protected]

Kaushik Das Economist (+91) 22 6658-4909 [email protected]

Eco

no

mic

s

OVERVIEW: International food prices are rising as fast as they did in 2007/08 and most economies in Asia appear likely to import this inflation. However, we do not expect a vigorous policy response to higher inflation.

CHINA: PMI and export growth moderated in December but our growth outlook for 2011 remains on track. Property tax will be rolled out in Chongqing and Shanghai soon. Fiscal policy will support public housing and tax cuts for individuals and services.

HONG KONG: A moderation in export growth this year should bring slower overall growth. Inflation is rising due to external and local (property) factors. Retail sales boom shows no signs of abating and could drive growth higher than expected.

INDIA: November IP growth pulled down sharply due to holiday and base effect; but other indicators of growth remain strong. Inflation risks have accentuated, with food prices soaring once again. The rise in global crude oil prices has complicated the government’s petroleum subsidy policy.

INDONESIA: Real activities remain robust, suggesting a 6%+ growth outlook; inflation has picked up considerably.

MALAYSIA: Subsidies are being removed gradually, so inflation is muted in the near-term. The external growth impulse is much weaker than it was for most of 2010 and domestic demand growth could slow sharply.

PHILIPPINES: Economic growth would likely be robust, but inflation will gradually rise. Global food and fuel prices could surge, causing a sharp rise in inflation.

SINGAPORE: Growth rebounds in Q4, but YoY growth will fall sharply until Q2. Some upside risk perhaps to growth from exports but similarly upside risk to inflation.

SOUTH KOREA: Growth to slow, led by weaker investment and exports, although the latter likely to be stronger than expected, while private consumption remains relatively stable. Rising food and oil prices pose downside risks to growth.

TAIWAN: Export growth remains relatively stable, posing upside risks to Taiwan’s growth in Q4 and 2011, while rising (CPI and real estate price) inflation points to sustained rate hikes.

THAILAND: Better-than-expected domestic and international (US) data pose upside risks to our Q4 2010 and 2011 GDP growth forecast for Thailand.

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 17

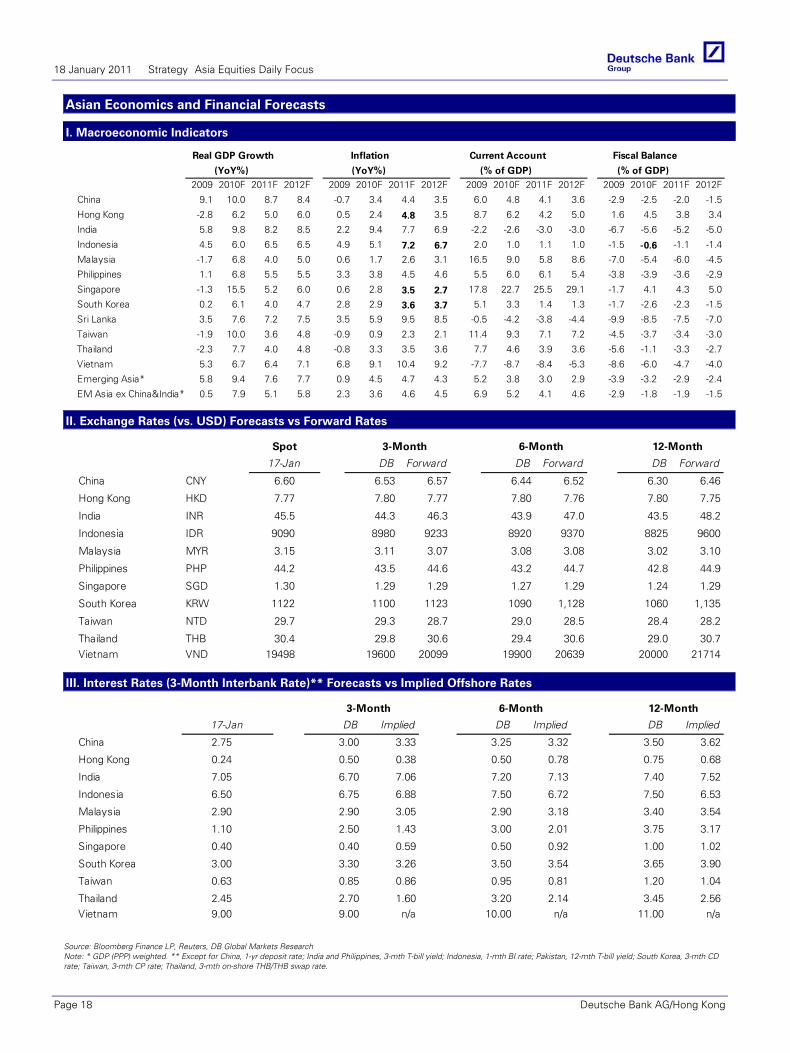

Asian Economics and Financial Forecasts

I. Macroeconomic Indicators

(YoY%) (YoY%) (% of GDP) (% of GDP)2009 2010F 2011F 2012F 2009 2010F 2011F 2012F 2009 2010F 2011F 2012F 2009 2010F 2011F 2012F

China 9.1 10.0 8.7 8.4 -0.7 3.4 4.4 3.5 6.0 4.8 4.1 3.6 -2.9 -2.5 -2.0 -1.5

Hong Kong -2.8 6.2 5.0 6.0 0.5 2.4 4.8 3.5 8.7 6.2 4.2 5.0 1.6 4.5 3.8 3.4

India 5.8 9.8 8.2 8.5 2.2 9.4 7.7 6.9 -2.2 -2.6 -3.0 -3.0 -6.7 -5.6 -5.2 -5.0

Indonesia 4.5 6.0 6.5 6.5 4.9 5.1 7.2 6.7 2.0 1.0 1.1 1.0 -1.5 -0.6 -1.1 -1.4

Malaysia -1.7 6.8 4.0 5.0 0.6 1.7 2.6 3.1 16.5 9.0 5.8 8.6 -7.0 -5.4 -6.0 -4.5

Philippines 1.1 6.8 5.5 5.5 3.3 3.8 4.5 4.6 5.5 6.0 6.1 5.4 -3.8 -3.9 -3.6 -2.9

Singapore -1.3 15.5 5.2 6.0 0.6 2.8 3.5 2.7 17.8 22.7 25.5 29.1 -1.7 4.1 4.3 5.0

South Korea 0.2 6.1 4.0 4.7 2.8 2.9 3.6 3.7 5.1 3.3 1.4 1.3 -1.7 -2.6 -2.3 -1.5

Sri Lanka 3.5 7.6 7.2 7.5 3.5 5.9 9.5 8.5 -0.5 -4.2 -3.8 -4.4 -9.9 -8.5 -7.5 -7.0

Taiwan -1.9 10.0 3.6 4.8 -0.9 0.9 2.3 2.1 11.4 9.3 7.1 7.2 -4.5 -3.7 -3.4 -3.0

Thailand -2.3 7.7 4.0 4.8 -0.8 3.3 3.5 3.6 7.7 4.6 3.9 3.6 -5.6 -1.1 -3.3 -2.7

Vietnam 5.3 6.7 6.4 7.1 6.8 9.1 10.4 9.2 -7.7 -8.7 -8.4 -5.3 -8.6 -6.0 -4.7 -4.0

Emerging Asia* 5.8 9.4 7.6 7.7 0.9 4.5 4.7 4.3 5.2 3.8 3.0 2.9 -3.9 -3.2 -2.9 -2.4

EM Asia ex China&India* 0.5 7.9 5.1 5.8 2.3 3.6 4.6 4.5 6.9 5.2 4.1 4.6 -2.9 -1.8 -1.9 -1.5

Real GDP Growth Inflation Current Account Fiscal Balance

II. Exchange Rates (vs. USD) Forecasts vs Forward Rates

DB Forward DB Forward DB Forward

China CNY 6.60 6.53 6.57 6.44 6.52 6.30 6.46

Hong Kong HKD 7.77 7.80 7.77 7.80 7.76 7.80 7.75

India INR 45.5 44.3 46.3 43.9 47.0 43.5 48.2

Indonesia IDR 9090 8980 9233 8920 9370 8825 9600

Malaysia MYR 3.15 3.11 3.07 3.08 3.08 3.02 3.10

Philippines PHP 44.2 43.5 44.6 43.2 44.7 42.8 44.9

Singapore SGD 1.30 1.29 1.29 1.27 1.29 1.24 1.29

South Korea KRW 1122 1100 1123 1090 1,128 1060 1,135

Taiwan NTD 29.7 29.3 28.7 29.0 28.5 28.4 28.2

Thailand THB 30.4 29.8 30.6 30.6 29.4 30.6 30.6 29.0 30.7 #Vietnam VND 19498 19600 20099 19900 20639 20000 21714

12-Month 6-Month 3-Month

17-Jan

Spot

III. Interest Rates (3-Month Interbank Rate)** Forecasts vs Implied Offshore Rates

DB Implied DB Implied DB Implied

China 2.75 3.00 3.33 3.25 3.32 3.50 3.62

Hong Kong 0.24 0.50 0.38 0.50 0.78 0.75 0.68

India 7.05 6.70 7.06 7.20 7.13 7.40 7.52

Indonesia 6.50 6.75 6.88 7.50 6.72 7.50 6.53

Malaysia 2.90 2.90 3.05 2.90 3.18 3.40 3.54

Philippines 1.10 2.50 1.43 3.00 2.01 3.75 3.17

Singapore 0.40 0.40 0.59 0.50 0.92 1.00 1.02

South Korea 3.00 3.30 3.26 3.50 3.54 3.65 3.90

Taiwan 0.63 0.85 0.86 0.95 0.81 1.20 1.04

Thailand 2.45 2.70 1.60 3.20 2.14 3.45 2.56Vietnam 9.00 9.00 n/a 10.00 n/a 11.00 n/a

17-Jan

3-Month 6-Month 12-Month

Source: Bloomberg Finance LP, Reuters, DB Global Markets Research Note: * GDP (PPP) weighted. ** Except for China, 1-yr deposit rate; India and Philippines, 3-mth T-bill yield; Indonesia, 1-mth BI rate; Pakistan, 12-mth T-bill yield; South Korea, 3-mth CD rate; Taiwan, 3-mth CP rate; Thailand, 3-mth on-shore THB/THB swap rate.

18 January 2011 Strategy Asia Equities Daily Focus

Page 18 Deutsche Bank AG/Hong Kong

Asia

17 January 2011

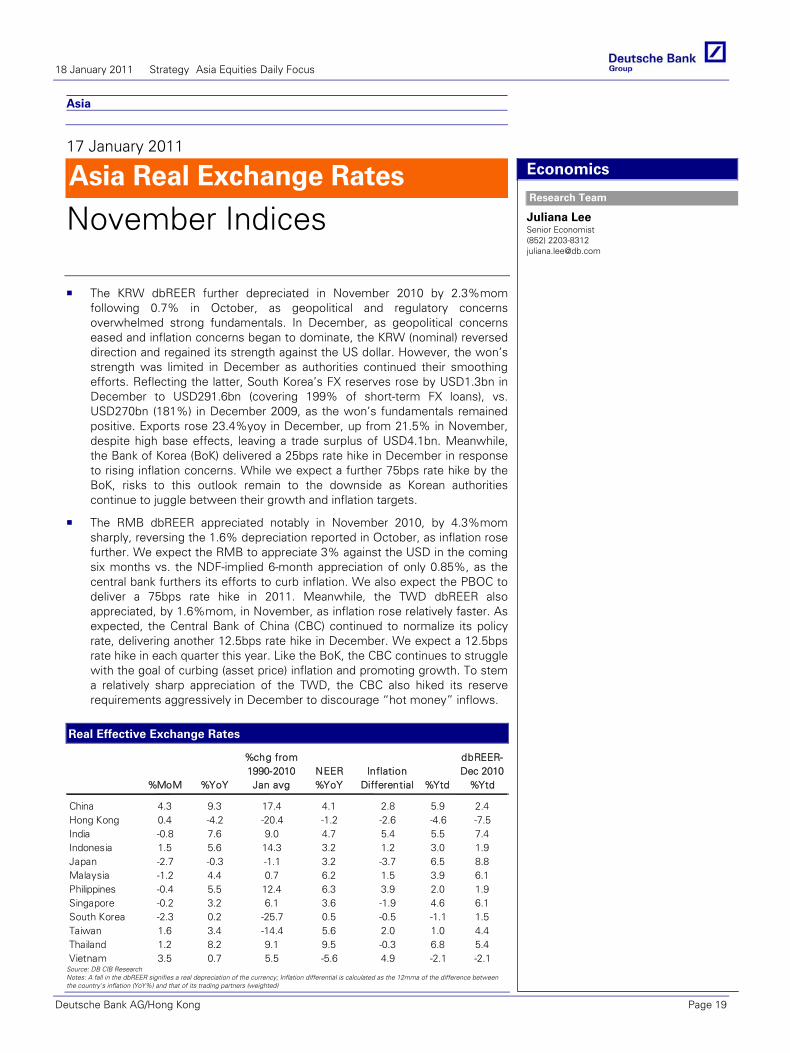

Asia Real Exchange Rates

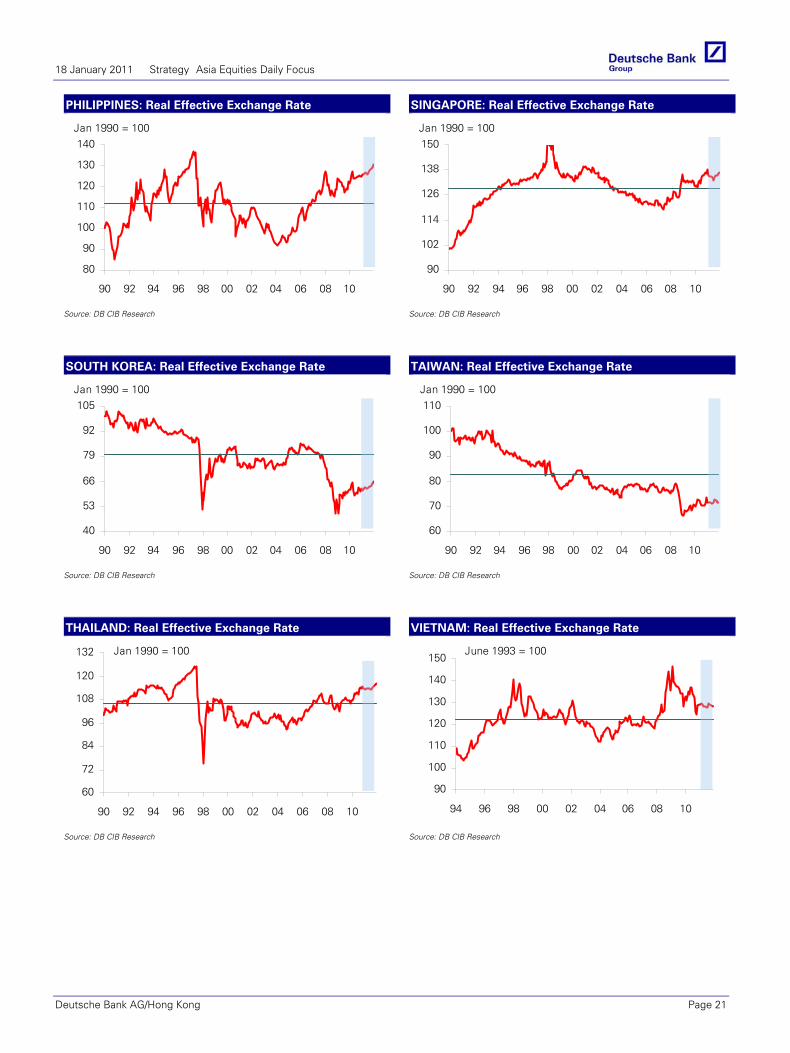

November Indices

Economics

Research Team

Juliana Lee Senior Economist (852) 2203-8312 [email protected]

Eco

no

mic

s

The KRW dbREER further depreciated in November 2010 by 2.3%mom following 0.7% in October, as geopolitical and regulatory concerns overwhelmed strong fundamentals. In December, as geopolitical concerns eased and inflation concerns began to dominate, the KRW (nominal) reversed direction and regained its strength against the US dollar. However, the won’s strength was limited in December as authorities continued their smoothing efforts. Reflecting the latter, South Korea’s FX reserves rose by USD1.3bn in December to USD291.6bn (covering 199% of short-term FX loans), vs. USD270bn (181%) in December 2009, as the won’s fundamentals remained positive. Exports rose 23.4%yoy in December, up from 21.5% in November, despite high base effects, leaving a trade surplus of USD4.1bn. Meanwhile, the Bank of Korea (BoK) delivered a 25bps rate hike in December in response to rising inflation concerns. While we expect a further 75bps rate hike by the BoK, risks to this outlook remain to the downside as Korean authorities continue to juggle between their growth and inflation targets.

The RMB dbREER appreciated notably in November 2010, by 4.3%mom sharply, reversing the 1.6% depreciation reported in October, as inflation rose further. We expect the RMB to appreciate 3% against the USD in the coming six months vs. the NDF-implied 6-month appreciation of only 0.85%, as the central bank furthers its efforts to curb inflation. We also expect the PBOC to deliver a 75bps rate hike in 2011. Meanwhile, the TWD dbREER also appreciated, by 1.6%mom, in November, as inflation rose relatively faster. As expected, the Central Bank of China (CBC) continued to normalize its policy rate, delivering another 12.5bps rate hike in December. We expect a 12.5bps rate hike in each quarter this year. Like the BoK, the CBC continues to struggle with the goal of curbing (asset price) inflation and promoting growth. To stem a relatively sharp appreciation of the TWD, the CBC also hiked its reserve requirements aggressively in December to discourage “hot money” inflows.

Real Effective Exchange Rates

%MoM %YoY

%chg from 1990-2010 Jan avg

NEER %YoY

Inflation Differential %Ytd

dbREER-Dec 2010

%Ytd

China 4.3 9.3 17.4 4.1 2.8 5.9 2.4Hong Kong 0.4 -4.2 -20.4 -1.2 -2.6 -4.6 -7.5India -0.8 7.6 9.0 4.7 5.4 5.5 7.4Indonesia 1.5 5.6 14.3 3.2 1.2 3.0 1.9Japan -2.7 -0.3 -1.1 3.2 -3.7 6.5 8.8Malaysia -1.2 4.4 0.7 6.2 1.5 3.9 6.1Philippines -0.4 5.5 12.4 6.3 3.9 2.0 1.9Singapore -0.2 3.2 6.1 3.6 -1.9 4.6 6.1South Korea -2.3 0.2 -25.7 0.5 -0.5 -1.1 1.5Taiwan 1.6 3.4 -14.4 5.6 2.0 1.0 4.4Thailand 1.2 8.2 9.1 9.5 -0.3 6.8 5.4Vietnam 3.5 0.7 5.5 -5.6 4.9 -2.1 -2.1

Source: DB CIB Research Notes: A fall in the dbREER signifies a real depreciation of the currency; Inflation differential is calculated as the 12mma of the difference between the country's inflation (YoY%) and that of its trading partners (weighted)

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 19

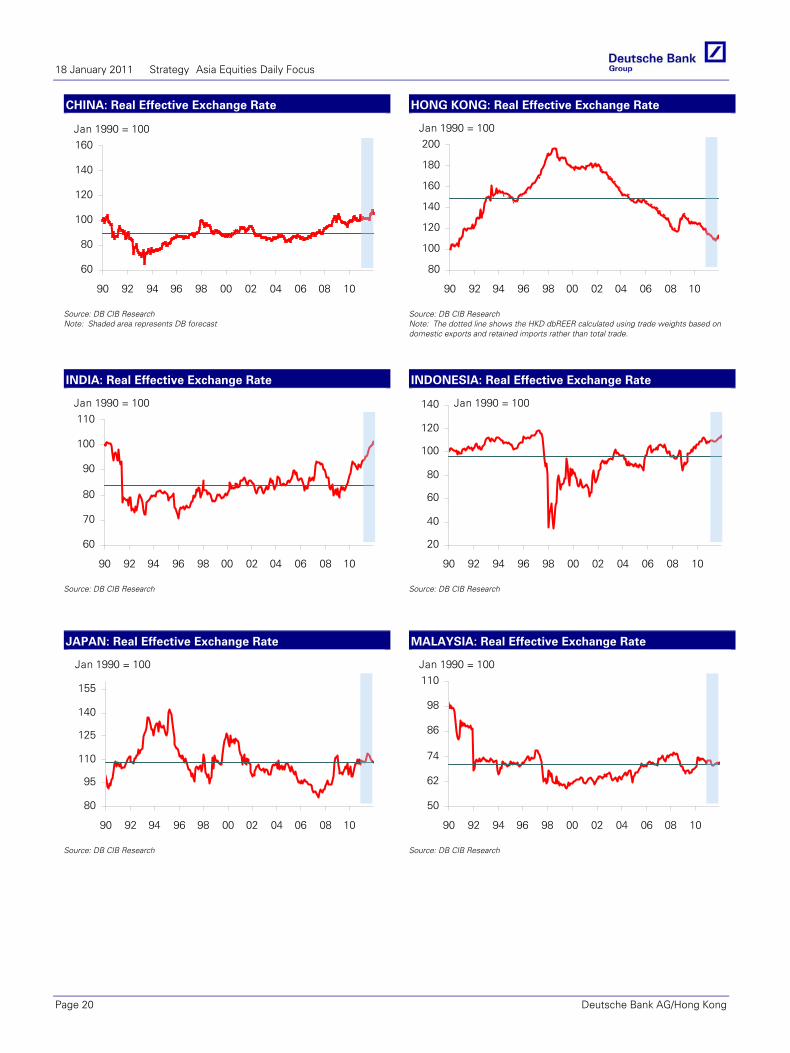

CHINA: Real Effective Exchange Rate HONG KONG: Real Effective Exchange Rate

60

80

100

120

140

160

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

80

100

120

140

160

180

200

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

Source: DB CIB Research Note: Shaded area represents DB forecast

Source: DB CIB Research Note: The dotted line shows the HKD dbREER calculated using trade weights based on domestic exports and retained imports rather than total trade.

INDIA: Real Effective Exchange Rate INDONESIA: Real Effective Exchange Rate

60

70

80

90

100

110

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

20

40

60

80

100

120

140

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

Source: DB CIB Research

Source: DB CIB Research

JAPAN: Real Effective Exchange Rate MALAYSIA: Real Effective Exchange Rate

80

95

110

125

140

155

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

50

62

74

86

98

110

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

Source: DB CIB Research

Source: DB CIB Research

18 January 2011 Strategy Asia Equities Daily Focus

Page 20 Deutsche Bank AG/Hong Kong

PHILIPPINES: Real Effective Exchange Rate SINGAPORE: Real Effective Exchange Rate

80

90

100

110

120

130

140

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

90

102

114

126

138

150

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

Source: DB CIB Research

Source: DB CIB Research

SOUTH KOREA: Real Effective Exchange Rate TAIWAN: Real Effective Exchange Rate

40

53

66

79

92

105

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

60

70

80

90

100

110

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

Source: DB CIB Research

Source: DB CIB Research

THAILAND: Real Effective Exchange Rate VIETNAM: Real Effective Exchange Rate

60

72

84

96

108

120

132

90 92 94 96 98 00 02 04 06 08 10

Jan 1990 = 100

90

100

110

120

130

140

150

94 96 98 00 02 04 06 08 10

June 1993 = 100

Source: DB CIB Research

Source: DB CIB Research

18 January 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 21

Global

17 January 2011

Global Commodities DailyHarsh weather and inflation

Deutsche Bank AG/London

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

Co

mm

od

itie

s

The Day Ahead

Time(EST) Country Event Previous Market View

00:00 Japan Consumer Confidence 40.6

16:00 US USDA crop progress report

19:01 UK Nationwide Consumer Confidence 45 44

19:01 UK RICS House Price Balance - 44% - 44%

21:00 China Actual FDI (YoY) 38.2% 11.2%

23:30 Japan Industrial Production (MoM) (Nov) 1%

Austria OPEC OMR 2011 release

Overview

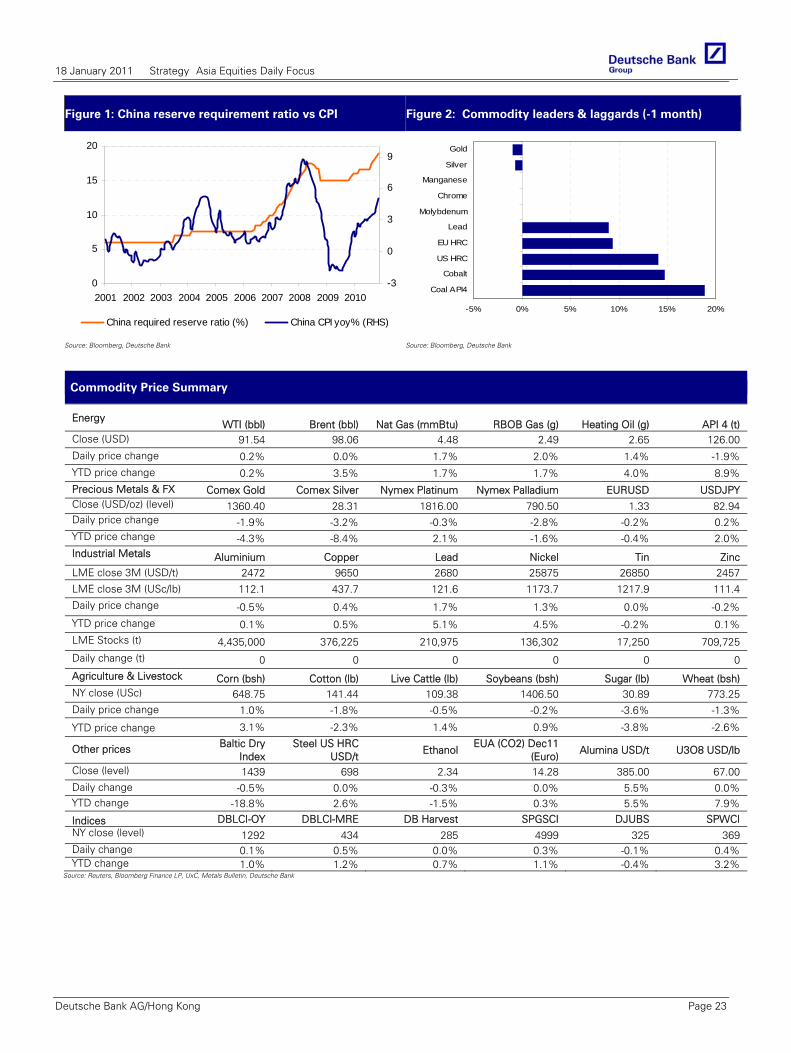

US macro data out last Friday appeared to have a neutral cast, but a strong start to the 4th quarter corporate earnings reports boosted the S&P500 index and lifted crude oil and industrial metals higher while sending precious metals lower. Friday’s expiry of the Brent contract added volatility. Copper bounced off intraday lows despite a 50bp increase in reserve requirement ratio by China’s PBOC to fight against inflation. This is the fourth hike in the RRR over the past two months. Our China economics team has revised up their CPI inflation forecast for 2011 to 4.4% from 4.1% previously, on higher than expected M2 growth target (16%) this year. They also see further upside risks to the new CPI forecast, a function of a bad weather conditions globally and stronger demand for commodities.

Harsh weather around the world continues to cause supply side disruptions fuelling inflation fears. A tropical cyclone has forced five nickel mines in New Caledonia to shut. The country accounts for 4% of global nickel output and has 25% of world’s reserves. Much of the nickel exported is for stainless steel production in Japan. Meanwhile, the flood situation which has severed damaged coal supplies in Australia may be improving. Gladstone Port has resumed coal loading over the weekend following re-opening of several rail lines. However, the port of Brisbane remains shut.

In UK gas, above-normal temperatures towards the end of last week offered storage operators a rare opportunity to inject gas, with Rough long-range storage gaining 36mcm and medium-range stocks building by 32mcm during the week. Supplies from LNG, imports from Norway, and UK production also fell in the second half of the week, helping to prevent a significant drop in prompt prices. Looking forward, a return to below-normal weather in the coming two weeks should lift total demand to c.380mcm. While this should provide support to prices, we believe the upside is limited as we do not expect much storage withdrawal to be necessary, given the excellent supply flexibility from other sources.

Looking at this week’s calendar, we believe Chinese data will dominate this week with CPI, IP, FAI and retail sales data released mid-week. China will also publish 2010 GDP growth. In energy, OPEC will release its Oil Market Report 2011 today.

Commodities & Global Markets

Commodities News In Brief • Inner Mongolia's coal output reached

782 mn tonnes last year, making it the nation's largest coal-producing region for a second year running, local authorities said.

• Indonesia exported 92,487 tonnes of tin last year down by 7% from 99,287 tons in 2009, Ministry of Trade said.

• Operations were normal at Peruvian copper mine Cerro Verde after workers reached a partial agreement with the company before a planned strike.

• Norway, the second-biggest exporter of natural gas, said gas output rose to 10.9 bn cubic meters from 10.0 bn and oil production dropped to 1.814 mn bpd from 1.998 mn, according to the Norwegian Petroleum Directorate

Global Markets News In Brief

• German CPI increased to 1.0% in Dec; 1.7% YoY

• EU Dec CPI (MoM) improves to 0.6%; (YoY) 2.2%

• EU Trade Balance posts a EUR0.4 B deficit in November from EUR4.7 B surplus in Oct

• US CPI in December rose 0.5 %, more than the 0.4% Bloomberg consensus.

• US Retail Sales ex-autos rose 0.5% in December vs. 1.0% in November.

• US IP increased 0.8% in December after having risen 0.3% in November.

• US Univ. of Michigan preliminary index of consumer sentiment for January fell to 72.7 from 74.5 in Dec.

Event Risks • IEA OMR 2011 release on Jan 18.

• US total net TIC flows on Jan 18.

• Germany ZEW survey on Jan 18.

• US NAHB Housing Market Index on Jan 18.

• China CPI, FAI, GDP, IP, retail sales on Jan 19.

• China Leading Index 25-29 Jan

Research Team Adam Sieminski Xiao Fu Research Analyst Research Analyst (1) 202 662 1624 (44) 20 754571558 [email protected] [email protected]

18 January 2011 Strategy Asia Equities Daily Focus

Page 22 Deutsche Bank AG/Hong Kong

Figure 1: China reserve requirement ratio vs CPI Figure 2: Commodity leaders & laggards (-1 month)

0

5

10

15

20

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010-3

0

3

6

9

China required reserve ratio (%) China CPI yoy% (RHS)-5% 0% 5% 10% 15% 20%

Coal API4

Cobalt

US HRC

EU HRC

Lead

Molybdenum

Chrome

Manganese

Silver

Gold

Source: Bloomberg, Deutsche Bank Source: Bloomberg, Deutsche Bank

Commodity Price Summary

Energy WTI (bbl) Brent (bbl) Nat Gas (mmBtu) RBOB Gas (g) Heating Oil (g) API 4 (t)

Close (USD) 91.54 98.06 4.48 2.49 2.65 126.00 Daily price change 0.2% 0.0% 1.7% 2.0% 1.4% -1.9% YTD price change 0.2% 3.5% 1.7% 1.7% 4.0% 8.9% Precious Metals & FX Comex Gold Comex Silver Nymex Platinum Nymex Palladium EURUSD USDJPY Close (USD/oz) (level) 1360.40 28.31 1816.00 790.50 1.33 82.94 Daily price change -1.9% -3.2% -0.3% -2.8% -0.2% 0.2% YTD price change -4.3% -8.4% 2.1% -1.6% -0.4% 2.0% Industrial Metals Aluminium Copper Lead Nickel Tin Zinc LME close 3M (USD/t) 2472 9650 2680 25875 26850 2457

LME close 3M (USc/lb) 112.1 437.7 121.6 1173.7 1217.9 111.4

Daily price change -0.5% 0.4% 1.7% 1.3% 0.0% -0.2%

YTD price change 0.1% 0.5% 5.1% 4.5% -0.2% 0.1% LME Stocks (t) 4,435,000 376,225 210,975 136,302 17,250 709,725

Daily change (t) 0 0 0 0 0 0

Agriculture & Livestock Corn (bsh) Cotton (lb) Live Cattle (lb) Soybeans (bsh) Sugar (lb) Wheat (bsh) NY close (USc) 648.75 141.44 109.38 1406.50 30.89 773.25 Daily price change 1.0% -1.8% -0.5% -0.2% -3.6% -1.3%

YTD price change 3.1% -2.3% 1.4% 0.9% -3.8% -2.6%

Other prices Baltic Dry Index

Steel US HRC USD/t

Ethanol EUA (CO2) Dec11

(Euro) Alumina USD/t U3O8 USD/lb

Close (level) 1439 698 2.34 14.28 385.00 67.00 Daily change -0.5% 0.0% -0.3% 0.0% 5.5% 0.0% YTD change -18.8% 2.6% -1.5% 0.3% 5.5% 7.9%

Indices DBLCI-OY DBLCI-MRE DB Harvest SPGSCI DJUBS SPWCI NY close (level) 1292 434 285 4999 325 369 Daily change 0.1% 0.5% 0.0% 0.3% -0.1% 0.4% YTD change 1.0% 1.2% 0.7% 1.1% -0.4% 3.2%

Source: Reuters, Bloomberg Finance LP, UxC, Metals Bulletin, Deutsche Bank