Embed Size (px)

Citation preview

SMERA MFI GRADING

This is to certify that

Network Of Entrepreneurship & Economic Development (NEED) has been assigned

a SMERA MFI Grading of

SMERA MF3

This grading indicates Above Average level of credit strength

This Grading is valid from August 31, 2016 to August 30, 2017

For SMERA Ratings Limited

Sankar Chakraborti Chief Executive Officer

Disclaimer: SMERA MFI Gradings are based on the data and information (Data) provided by the Entity and obtained by SMERA from sources it considers reliable. Although reasonable care has been taken to verify the Data, SMERA, makes no representation or warranty, expressed or

implied with respect to the accuracy, adequacy or completeness of any Data relied upon. SMERA is not responsible for any errors or omissions or for the results obtained from the use of the Grading or the Grading Report and especially states that it has no financial liability, whatsoever, for any direct, indirect or consequential loss of any kind arising from the use of its Gradings. A SMERA MFI Grading does not constitute an audit of the graded entity and should not be treated as a recommendation or opinion or a substitute for investor's independent assessment of

whether to buy, sell or hold any security. The SMERA MFI Grading Report should not be distributed/ published/ reproduced in any form without SMERA’s prior written approval.

1

SMERA MFI Grading Report

Date of Report : 31st August, 2016* Valid Till : 30th August, 2017

Legal Form : NGO - MFI

SMERA- MFI Grading : MF3 (Above Average)

MF1 Highest

MF2 High

MF3 Above Average

MF4 Average

MF5 Below Average

MF6 Inadequate

MF7 Low

MF8 Lowest

*This grading is a one-time exercise and does not envisage automatic surveillance. This grading is valid for a period of one year; subject to however, no significant changes / events occur during that period which could materially affect the business and financial parameters of the organization / project. SMERA recommends that the user of the Grading may seek a review of the Grading, if the rated entity experiences significant changes / events in the business. Recommended for review in next financial year.

NETWORK OF ENTREPRENEURSHIP & ECONOMIC DEVELOPMENT (NEED)

38-39, Neel Vihar, Sector – 14,

Near Powerhouse, Indira Nagar, Lucknow - 226 016

Uttar Pradesh India

2

SNAPSHOT

D&B D-U-N-S® Number 65-054-5986

MFI Name NETWORK OF ENTREPRENEURSHIP & ECONOMIC DEVELOPMENT (NEED)

Trade Style “NEED”

Registered Office Address

38-39, Neel Vihar, Sector – 14, Near Power House, Indira Nagar, Lucknow - 226 016 Uttar Pradesh India

Telex (91) (522) (2712671) (91) (522) (2712311)

Website www.needindia.org www.needindia.org.in

Email [email protected]

Line of Business

Microfinance services using Joint Liability Group (JLG) and Self Help Group (SHG) Model including value chain based producer groups

Chief Executive Mr.Anil K. Singh, An Ashoka Fellow Chief Executive Officer

SMERA MFI Grading MF3 (Above Average)

Legal Form NGO-MFI (The Societies Registration Act, 1860)

Date of Incorporation 22/Jun/1995

Year of Commencement of Microfinance Operations

2005

Total Employees 102

3

RATING RATIONALE

SMERA has assigned a rating of MF3 to NETWORK OF ENTREPRENEURSHIP & ECONOMIC

DEVELOPMENT (hereafter referred as NEED). The rating indicates that in SMERA’s current opinion, the

rated MFI’s ability with regards to credit strength is Above Average.

The rating assigned to NEED reflects following strengths:

Experienced and Qualified Management

NEED has experienced & qualified board members. NEED is managed by an international Advisory

Council Comprising Social Entrepreneurs, Trainers, Behavior Scientist, Volunteers,

Professors/Researchers, Consultants etc. Mr. Anil Singh, promoter is senior research fellow from Indian

Institute of Management (IIM) Ahmedabad who took specific action research project in remote tribal

villages of India. After working about 15 years in the formal sector, he started working for social and

economic entrepreneurship.

Standardized operational procedures

NEED has appointed department-wise personnel for operations, management information system (MIS),

Internal Audit (IA), Finance & Accounts, Risk cum Mobile Manager Team, Human Resource. The NGO-MFI

has documented operational policies covering details of loan products, field operations, credit approval and

monitoring process.

Diversity in Social and Economic Services

NEED with deeper penetration in the under-served states of Uttar Pradesh & Bihar is an organization of

280 social entrepreneurs focusing on following areas.

Market based skill training and entrepreneurship dev. (MBSED) as the lead agency of Ministry of

Textiles, DFID supported project in Bihar, World Bank sponsored JEEVIKA project. NEED has also

been recipient of National Award by a Sr. Policy Official of Ministry and Hon’ble Cabinet Ministry in

an august gathering.

Promoting Pro-Poor Livelihoods& micro-enterprises including entrepreneurship,

Micro-finance way to promoting Social & Economic Enterprises including Healthcare and Sanitation,

Safe Drinking Kits,

Nutrition,

Creating a cadre of community based Village Health Guides,

4

Community School Teachers

Micro-Planning with Village Councils with public and private service institutions.

Asset Quality NEED’s assets quality is at adequate levels with almost 99.5% on-time repayment rate during the period

under study.

However the rating is constrained by following weaknesses:

Moderate financial profile

Revenue has decreased during the period under study and stands at ` 24,729 (in thousands) for FY 2016 on

account of inability to scale up its portfolio. Further outstanding portfolio has been uneven during the period

under study and stands at Rs 118,722 (in thousands) as on 31/Mar/2016.

Operational expenses have declined to 8.7% in FY 2016 from 10.00% in FY 2014 on account of implementation

of better cost control measures.

Concentration risk

NEED is susceptible to portfolio/geographical concentration coupled with sociopolitical risk as 72.34 % of its

total outstanding portfolio as on 31/Mar/2016 is concentrated in State of Uttar Pradesh.

Adherence to compliance regulations

Considering current constitution and scale of operations, compliance observed is adequate; however, for

future expansion and broader financial inclusion, SMERA believes there is scope of improvement for the

same.

SMERA observed that the current constitution of NEED hinders the expansion of existing MFI business

growth in a smooth way and hence as informed by the management NEED have plans to demerge its

microfinance activities into a separate entity of Section-8 Company, Govt. of India and ultimately will aim for

getting NBFC-MFI accreditation from Reserve Bank of India in due course of time.

5

Moderate Systems

Considering the scale of operations, the current MIS system deployed in NEED is sufficient to access

complete micro finance solution. The demand collections are updated in the system on a daily basis and

same is reconciled at Head office. Further NEED conducts internal audit at regular interval and the

same is conducted by in house internal audit team.

Considering the projected growth, SMERA recommends NEED to strengthen its internal audit team and

refine its systems and processes to reduce the credit risk and operational risk

As informed by the management NEED is planning to develop in-house software including mobile

driven tracking for real tracking of day to day microfinance operations.

6

.

MFI BACKGROUND NETWORK OF ENTREPRENEURSHIP & ECONOMIC DEVELOPMENT (NEED) was established on

22nd June, 1995 as a Not for Profit entity under The Society Act, 1860 by Mr. Anil K. Singh after having

completed his post graduate study from Xavier Ranchi (Rural Management) and then after his long

association in advance research experience from IIM, Ahmedabad followed by his good length of

working experience in livelihoods cum micro entrepreneurship both in private and public institutions.

NEED with deeper penetration in the under-served states of Uttar Pradesh & Bihar is an organization of

280 social entrepreneurs in the entire organization i.e. MF and Non-MF activities focusing on following

areas

Market based skill training and entrepreneurship dev. (MBSED) as the lead agency of Ministry of

Textiles, DFID supported project in Bihar, World Bank sponsored JEEVIKA project. NEED has also been

recipient of National Award by a Sr. Policy Official of Ministry and Hon’ble Cabinet Ministry in an

august gathering. Kindly find a few photo attached herewith.

Promoting Pro-Poor Livelihoods& micro-enterprises including entrepreneurship,

Micro-finance way to promoting Social & Economic Enterprises including healthcare and sanitation,

Safe Drinking Kits,

Nutrition,

Creating a cadre of community based Village health Guides,

Community School Teachers

Micro-Planning with Village Councils with public and private service institutions.

The above diversity of services also supplements and supports the Micro-Credit Products of NEED and also

enhances the credentials and trustworthiness of relationship between NEED and Micro-Finance borrowers in

a very matured way The targeted communities mostly includes Minority groups, Youth, Artisans, Women,

Marginal farmers, Children and many others who are in a still very deprived and disadvantageous condition.

7

Product

INFORMATION ON LOAN PRODUCTS

Product Feature

Product 1 Product 2 Product 3 Product 4

Name of the Product

Start-up loan (Suruwati

Loan)

Livelihood Loan (Aajiveeka Loan)

Enterprising Loan (Udayami Loan)

Energy Efficiency Loan

Loan term (Tenure)

12 Months 12 -24 Months 24 Months 06 – 12 Months

Repayment Frequency

Monthly Monthly Monthly Monthly

Loan size (Amount in INR )

5000 - 15000 20,000 – 30,000 35,000 – 50,000 3000 - 5000

Interest rate 26% (Reducing Balance)

Loan processing fees

1%

Insurance

NEED has tied up with DHFL Pramerica Life Insurance Company Limited under which all the

borrowers and their spouses are covered with term insurance where the insured amount is equal to loan

amount outstanding.

8

Promoters’ Background

Mr. Anil Singh, CEO & Managing Director of NEED has done Post Graduate in Social Service (1978-80) with

specialization in Rural Management from Xavier Institute of Social Service (XISS). Mr. Anil Singh came in

contact with the pioneering Indian Institute of Management (IIM) Ahmedabad as Senior Research Fellow to

take-up a specific action research project in remote tribal villages of India. After working about 15 years in

the formal sector, he started working for social and economic entrepreurship. Mr. Singh has been selected as

a lifetime member of the Ashoka Global Fellowship Program and is a Fellow of the UK based initiative

Management in Development (MIND).

BOARD STRUCTURE

List of Executive Committee Members Years of Experience in Microfinance

Mr. Anil K. Singh. CEO & Member 11

Mrs. Pushpa Singh. Treasurer 11

Mrs. Usha Mishra Chairperson 06

Mrs. Nilanjana Das

Member

07

Mrs. Priyanka Dutta 07

Mrs. Lalti Devi 07

Shri Mahena Singh Gailakoti

08

SMERA COMMENTS

Board members have extensive experience in development sector. Going ahead considering the future

projected growth and plans to transform into NBFC-MFI, NEED will be requiring experienced and

qualified manpower with banking & Microfinance background. Further as informed by the

management NBFC-MFI board consisting of Sr. RBI Official, ex-Banker has already been formed and

submitted to RBI as an applicant for seeking fresh license.

9

Management Profile

Department Name of the person Educational

Qualification Designation

Years of experience in Microfinance

Operations Surendra Kumar Post Graduate Regional

Manager 11

Operations Pradeep Singh Post Graduate Operation,

Manager 06

MIS Shiv Kamal Tiwari B.Com MIS Head 08

Risk Management Surya Pratap MBA Risk Manager 06

Risk Management Jitendra Kumar M.com Risk Manager 09

Risk Management Deepak Kumar B.A Risk Manager 06

Finance &

Accounts Vijay Singh Rawat M.Com Finance Manager 11

Finance &

Accounts Usha B.A

Account

Manager 07

Administration &

Human Resource Mahendra Gailakoti Post Graduate HR Manager 15

Training

Vikram Singh, IPS Ex. DGP, UP

Vice Chancellor,

International University

PhD in

Management

Manager –

Training &

Development

11

Training Rajendra Prasad MBA

Manager –

Training &

Development

11

Audit G.P. Gupta M.Sc. Internal Auditor 21

Audit Firoj Ahmed M.Com Internal Auditor 07

IT & Systems Milind Kumar Graduate Hardware

engineer 06

IT & Systems Anubhav Singh B.Tech., CFA Software

Engineer 06

SMERA COMMENTS The current management has adequate understanding of microfinance and is sufficient to handle the current scale of operations.

10

HIGHLIGHTS OF NEED OPERATIONS

Particulars Mar 2012 Mar 2013 Mar 2014 Mar 2015 Mar 2016

No. of States 02 02 02 02 02

No. of branches 11 08 07 15 18

No. of districts covered 13 08 07 06 09

No. of villages covered 3,000 2,700 2,100 1,700 2,300

No. of Members 26,781 14,247 10,984 8,259 9,728

No. of SHGs 86 61 79 34 24

No. of JLGs 6,537 3,297 2,412 1,905 2,264

No. of active borrowers 25,835 13,576 10,115 7,885 9,464

Cumulative number of active borrowers

81,633 90,900 97,324 102,811 110,447

No. of Field officers (LSA) 88 64 56 44 62

Total No. of employees 139 96 87 73 102

Portfolio Outstanding (in INR thousands)

175,704 123,745 96,437 75,917 118,722

Disbursements (in INR thousands) during the period

159,590 135,958 86,716 89,880 135,225

Cumulative Disbursements (in INR thousands)

870,949 10,06,907 10,93,623 11,83,503 13,18,728

SMERA COMMENTS

Total outstanding portfolio decreased from FY 2012 to FY 2015 on account of inadequate supply of

funds from banks and financial institutions for fresh disbursement. Further in FY 2016, NEED

recorded an improvement in asset base supported by improvement in funding climate.

11

BRANCH WISE DETAILS AS ON 31/MAR/2016

Branch Name

No. of field

officers No. of

members

No. of active

borrowers

Cumulative Loan

disbursement (in ‘000)

Loan Outstanding

(in ‘000) Overdue (in ‘000)

PAR

(in ‘000)

Pahla 4 1,281 1,259 107,730 15,758 0 0

Mahmoodabad 6 1,967 1,802 144,504 21,374 0 0

Rampur Mathura

4 1,245 1,245 91,175 16,279 0 0

Biswa 2 461 461 21,233 5,783 0 0

Fatehpur 2 487 487 53,734 6,124 0 0

Kakori 0 0 0 33,203 0 0 0

Lucknow 0 0 0 76,060 0 0 0

Alambagh 0 0 0 42,430 0 0 0

Raibareli 0 0 0 13,363 0 0 0

Ballia 0 0 0 52,507 0 0 0

Motipur 0 0 0 284,895 0 0 0

Pukraira 5 95 95 53,100 126 0 0

Vaisali 5 248 248 70,795 2492 1 0

Paru 3 92 92 33,950 123 0 0

Mehasi 3 76 76 36,300 109 0 0

Barmadiya 3 98 98 54,545 128 0 0

Kesariya 3 651 651 32,430 10,491 7 7

Patna 5 938 938 47,930 10,505 23 22

Maner 5 513 513 12,355 5,870 0 0

Kudhni 0 0 0 16,845 0 0 0

Lalganj 0 0 0 9410 0 0 0

Lucknow 2 481 481 10,715 7,303 0 0

Malihabad 4 732 655 13,950 10,924 0 0

Koilwar 3 213 213 3,195 2,989 0 0

Nindura 2 116 116 1,715 1,684 0 0

Hashanganj 1 34 34 660 660 0 0

Total 62 9,728 9,464 1,318,729 118,722 31 29

SMERA COMMENTS

72.34 % of its total outstanding portfolio as on 31/Mar/2016 is concentrated in State of Uttar Pradesh..

12

SECTOR WISE LOAN OUTSTANDING

As on Mar-2013

Mar-2014 Mar-2015 Mar-2016

Sector Amount % Amount % Amount % Amount %

Income Generation

57,022 46 43,397 45 33,866 45 42,343 36

Animal Husbandry

27,991 23 25,074 26 18,873 25 17,424 15

Agriculture 19,849 16 18,323 19 14,500 19 42,412 36

Others 18,884 15 9,644 10 8,678 11 16,543 13

Total 123,746 100 96,438 100 75,917 100 118,722 100

SMERA COMMENTS More than 80% of the loans are given for Income generation activities.

13

AGEING SCHEDULE OF THE LOAN PORTFOLIO (` IN THOUSANDS)

As on Mar-14 Mar-15 Mar-16

Total loan outstanding that are

No. of Borrowers

Value of Portfolio

o/s

No. of Borrowers

Value of Portfolio

o/s

No. of Borrowers

Value of Portfolio

o/s

On time 10,867 95,986 8,254 75,893 9,727 118,720

Late (At least one payment)

1-30 days 13 40 0 1 2

31-60 days 20 87 1 1 0 0

61-90 days 33 58 0 0 0

91-180 days 51 265 4 22

Total Outstanding as on March after write off portfolio

10,984 96,436 8,259 75,916 9,728 118,722

181-360 days 33 347 10 68 5 7

> 361 days 4 45 4 22

Write off 33 347 14 113 9 29

Total portfolio with write off amount 11,017 96,783 8,273 76,029 9,737 118,751

SMERA COMMENTS

Assets quality stands at 99.50% on-time repayment rate during the period under study.

14

BALANCE SHEET (` IN THOUSANDS)

As on date 31/Mar/2014 31/Mar/2015 31/Mar/2016

SOURCES OF FUNDS

Equity Share Capital 51,420 63,848 51,045

Total Equity 51,420 63,848 51,045

Liabilities

Short-Term liabilities

Security deposits from borrowers -

Commercial Loans from banks/FI - 2,000 -

Interest payable on funding liabilities 526 35 0

Account payable & other short-term liabilities 1,306 5,768 2,951

Total Short-Term Liabilities 1,832 7,803 2,951

Long-Term liabilities

Commercial Loans from banks/FI 65,063 19,523 83,613

Total Long-Term Liabilities 65,063 19,523 83,613

Provision for loan loss 7,940 8,586 9,745

Total Provisions 7,940 8,586 9,745

TOTAL LIABILITIES 126,255 99,760 1,47,354

SMERA COMMENTS

Borrowings from commercial banks and financial institutions have increased in FY 2016 over FY 2015.

15

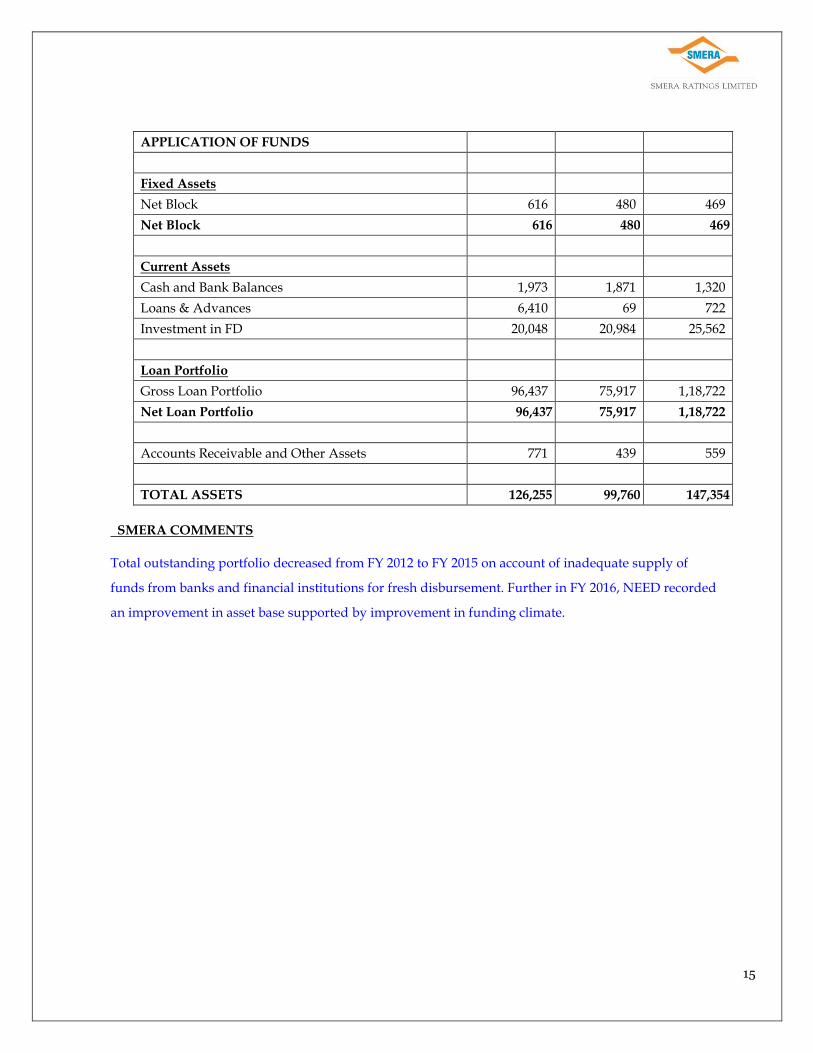

APPLICATION OF FUNDS

Fixed Assets

Net Block 616 480 469

Net Block 616 480 469

Current Assets

Cash and Bank Balances 1,973 1,871 1,320

Loans & Advances 6,410 69 722

Investment in FD 20,048 20,984 25,562

Loan Portfolio

Gross Loan Portfolio 96,437 75,917 1,18,722

Net Loan Portfolio 96,437 75,917 1,18,722

Accounts Receivable and Other Assets 771 439 559

TOTAL ASSETS 126,255 99,760 147,354

SMERA COMMENTS

Total outstanding portfolio decreased from FY 2012 to FY 2015 on account of inadequate supply of

funds from banks and financial institutions for fresh disbursement. Further in FY 2016, NEED recorded

an improvement in asset base supported by improvement in funding climate.

16

INCOME AND EXPENDITURE STATEMENT (` IN THOUSANDS)

Period FY 2014 FY 2015 FY 2016

Months 12 12 12

Financial revenue from operations 28,865 29,573 24,729

Less: Financial expenses from operations* 12,253 5,147 4,352

Gross profit 16,612 24,426 20,377

Less: Provision for Loan Loss / Write off 1,929 759 1,187

Net profit 14,683 23,667 19,190

Less: Operating Expenses

Personnel Expense 8,801 7,342 4,983

Depreciation and Amortization Expense 243 135 152

Other Administrative Expense 2,010 4,216 3,286

Net Operating Income

3,629

11,974

10,769

Non - Operating Revenue 1,808 454 603

Net Income Before Taxes 5,437 12,428 11,372

Less: Income Tax - - -

Net income after taxes 5,437 12,428 11,372

The above financials are taken from the audited financials.

SMERA COMMENTS

* Bad debts recovered have been taken under operating income

Income from operations has decreased on account of decrease in fresh disbursement during the

period under study.

17

RATIOS

Ratios Mar-2014 Mar-2015 Mar-2016

12 12 12

Capital Adequacy Ratio (CAR)

Capital Adequacy Ratio (%) 48% 73% 39%

Productivity / Efficiency Ratios*

No. of Active Borrowers Per Staff Member 116 108 93

No. of Active Borrowers per field executives 181 179 153

Gross Portfolio o/s per field executive (` in thousands)

1,722 1,725 1,915

Average Outstanding Balance Per borrower (In `)

9,534 9,628 12,545

Cost Per Active borrower (In `) 1,093 1,483 890

Asset / Liability Management

Yield on Portfolio (%) 21.3% 24.3% 20.3%

Profitability / Sustainability Ratios

Operational Self Sufficiency (%) 114.4% 168% 177%

SMERA COMMENTS

Operational Self Sufficiency has improved on account of exercising effective cost control measures Capital adequacy has declined in FY 2016 over FY 2015 as infusion of capital did not commensurate with increased asset base. AUDITOR Shailendra Vishnu& Co., (Chartered Accountants); 41- Chakkarpurwa, Paper Mill Colony Road, Nishatganj Lucknow – 226 006 Uttar Pradesh

18

PROJECTED BALANCE SHEET (` IN THOUSANDS)

As on date 31/Mar/2017 31/Mar/2018 31/Mar/2019

SOURCES OF FUNDS

Equity Share Capital 82,687 206,797 459,569

Total Equity (A) 82,687 206,797 459,569

Liabilities

Short-Term liabilities

Account payable & other short-term liabilities 7,509 10,264 20,267

Total Short-Term Liabilities (B) 7,509 10,264 20,267

Long-Term liabilities

Commercial Loans from banks/FI 245,710 574,878 1,060,789

Total Long-Term Liabilities (C) 245,710 574,878 1,060,789

Provision for loan loss 12,610 19,510 33,107

Total Provisions (D) 12,610 19,510 33,107

TOTAL LIABILITIES 348,516 811,440 1,573,732

APPLICATION OF FUNDS

Fixed Assets

Net Block (A) 1,247 2,080 2,958

Current Assets

Cash and Bank Balances (B) 2,304 2,959 3,761

Investment in FD (C) 35,942 83,088 159,700

Loan Portfolio

Gross Loan Portfolio (D) 306,522 719,122 1,400,622

Net Loan Portfolio 306,522 719,122 1,400,622

Accounts Receivable and Other Assets (E) 2,501 4,191 6,691

TOTAL ASSETS 348,516 811,440 1,573,732

19

PROJECTED INCOME AND EXPENDITURE STATEMENT (` IN THOUSANDS)

Period FY 2017 FY 2018 FY 2019

Months 12 12 12

Financial revenue from operations 87,100 205,200 415,700

Less: Financial expenses from operations 30,495 35,392 84,416

Gross financial margin 56,605 169,808 331,284

Less: Provision for Loan Loss / Write off 3,065 7,191 14,006

Net financial margin 53,540 162,617 317,278

Less: Operating Expenses

Personnel Expense 19,214 34,350 58,478

Depreciation and Amortization Expense 222 367 522

Other Administrative Expense 5,062 6,790 8,907

Net Operating Income 29,042 121,110 249,372

Non - Operating Revenue 2,600 3,000 3,400

Net Income 31,642 124,110 252,772

SMERA COMMENTS

The above projection has been shared by the client. SMERA believes the projected growth seems to be

highly optimistic considering the current scale of operations.

As informed by the management, NEED will be able to scale up its portfolio on account of funding

expected from banks and financial institutions in the coming financial year.

SMERA believes steady access to funds from banks/financial institutions will be a key in near future for

scaling up its portfolio.

20

EMPLOYEE(s) DETAILS FOR MICROFINANCE OPERATIONS

2013 2014 2015 2016

Total staff 96 87 73 102

No. of FOs 64 56 44 62

No. of managerial / Support staff 32 31 29 40

INFORMATION ON BANK(S)/ FINANCIAL INSTITUTION(S) AS ON 31/MAR/2016

SMERA COMMENTS

The average cost of funding stands at 14.66 % as majority of its borrowings are funded by financial

institutions but going ahead ability to attract funds at low cost will help to improve its profitability.

Name of the bank

/Financial Institution

Amount Sanctioned

Date of Sanctioning

Interest rate

(%)

Loan Tenor

(in months

)

Repayment

Frequency

Amount Disbursed

Amount Outstan

ding

Commercial Sources

Ananya Finance for Inclusive Growth - (through Ananya)

10 5-Jan-16 16.00

% 18 Monthly 10 8.33

Ananya Finance for Inclusive Growth - (through

PSIG)

10 15 , 29 Feb

& 28 March 2016

16.00%

18 Monthly 10 9.58

Gramin Bank of

Aryvavert (GBA)

121.52 24-Aug-09 14.50

% 36 Monthly 121.52 40.16

Union bank of India -

2nd

15 6-Jan-16 12.15

% 30 Monthly 15 15

Total 583.87 0 0 0 583.87 73.08

21

MONTHLY CASH AND BANK BALANCES (`IN THOUSANDS)

Cash Plus Bank Balances FY2013 FY2014 FY2015 FY2016

April 18,279 2,208 2,007 2,268

May 16,578 17,448 2,132 2,682

June 32,204 23,630 3,469 3,970

July 59,893 24,602 2,656 4,960

August 60,980 33,038 2,192 3,074

September 31,330 38,371 1,115 3,435

October 28,997 37,715 2,075 9,991

November 26,200 36,230 6,452 18,928

December 33,297 28,892 4,410 12,981

January 9,614 12,672 2,185 16,396

February 8,191 16,355 7,783 12,846

March 2,083 1,816 1,832 1,050

22

CURRENCY: All amounts in this report are in local currency unless otherwise stated.

----------------------------------------------------------------------------------------- -------------------------------------------

RIGHTS TO THE REPORT ARE WITH SMERA GRADINGS LIMITED (SMERA). THIS REPORT MAY NOT BE REPRODUCED IN WHOLE OR IN

PART IN ANY FORM OR MANNER WHATSOEVER. ------------------------------------------------------------------------------------------------------------------------------------ The SMERA – MFI Grading shall be read with the SMERA – MFI Grading Report on the subject issued by SMERA. All information contained in the SMERA – MFI Grading Report is obtained by SMERA from the subject and third party sources, and is believed to be accurate and reliable. Although reasonable care has been taken to ensure that the information in the Grading Report is true, such information is provided “as is” without any warranty of any kind and SMERA, in particular, makes no representation or warranty, express or implied, as to the accuracy, timeliness or completeness of any such information SMERA is not responsible for any errors in transmission and specifically states that SMERA shall have no financial liability whatsoever to the users of the Grading Report. The Grading does not constitute an audit and SMERA’s work is significantly different from that of an audit and accordingly, cannot be relied upon to provide the same level of assurance as an audit. Please note that the SMERA – MFI Grading Report is not a recommendation to purchase, sell or hold any securities and investors should take their own decision. In providing this Grading, SMERA does not underwrite the risks of any third party or that of the subject. SMERA is not liable to the Company or any third party in respect of any matter specified in the Grading Report. SMERA may revise, suspend or withdraw the Grading at any time in the future as a result of information changes in circumstances or unavailability of information. The SMERA – MFI Grading Report is not intended for distribution/ publication/ reproduction in any form without SMERA’s prior written approval.

-- End of Report --