Embed Size (px)

Citation preview

Thinking Big by Thinking Microg g y g

Eamon Kelly & Jules Gribble© copyright E Kelly, J Gribblepy g y

C t t1. What is Microinsurance & the potential market?

Contents

2. Client Value in MI3 What is the business case for MI?3. What is the business case for MI?4. Policy, Regulatory and Supervisory aspects5. Learning’s from developing markets6. Role of Actuaries6. Role of Actuaries

B k d• Based on work completed by various research

Background

and technical agencies, PLUS• Our own experience of 4 years + in this sectorOur own experience of 4 years + in this sector

• No perfect answer, most MI operators are still learning…

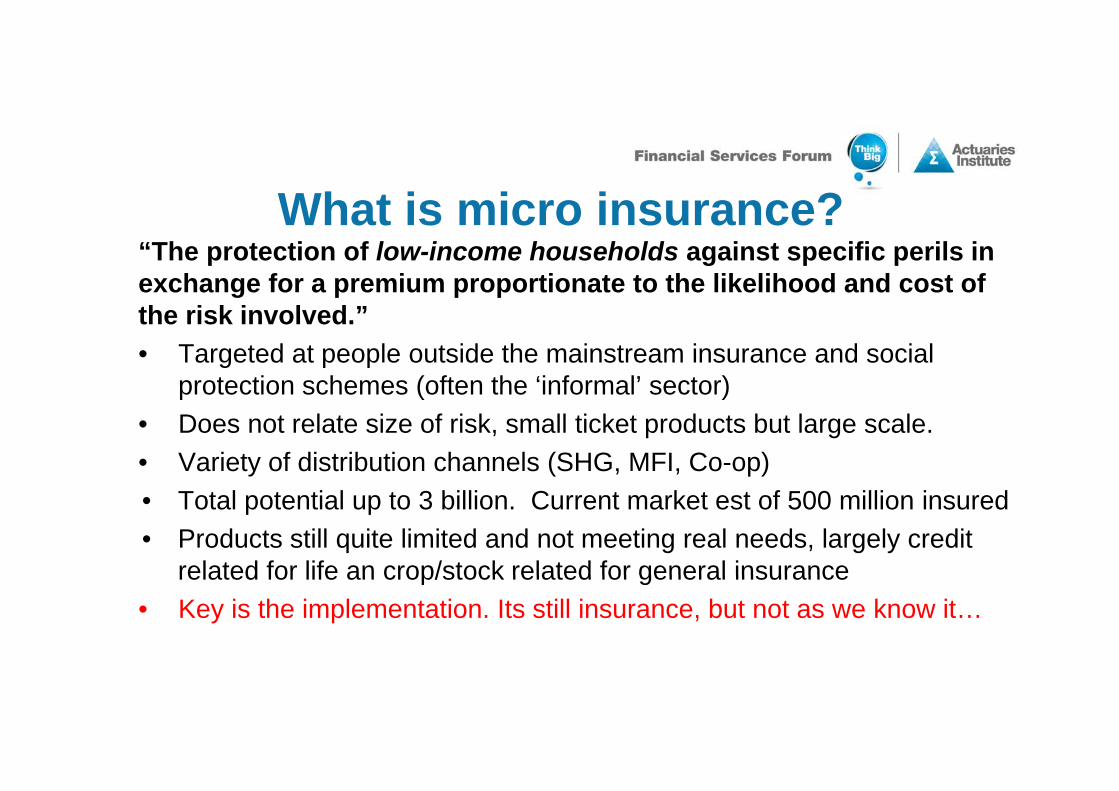

What is Microinsurance?

What is micro insurance?What is micro insurance? “The protection of low-income households against specific perils in exchange for a premium proportionate to the likelihood and cost of th i k i l d ”the risk involved.”• Targeted at people outside the mainstream insurance and social

protection schemes (often the ‘informal’ sector)p ( )• Does not relate size of risk, small ticket products but large scale.• Variety of distribution channels (SHG, MFI, Co-op)• Total potential up to 3 billion. Current market est of 500 million insured • Products still quite limited and not meeting real needs, largely credit

related for life an crop/stock related for general insurancerelated for life an crop/stock related for general insurance• Key is the implementation. Its still insurance, but not as we know it…

What is micro insurance?What is micro insurance? Key factors:• Low income people live in risky environments and generally more

vulnerable to various perils (illness, death, disability, loss of property (fire/theft), agricultural losses, disasters)

• Less able to financially cope when a crisis occurs The losses are notLess able to financially cope when a crisis occurs. The losses are not micro from the perspective of the user

• Poverty & vulnerability tend to reinforce each other• Exposure may lead to substantial financial loss, plus uncertainty about

when & how the loss might occur• Informal means to manage risks but insufficient protectionInformal means to manage risks but insufficient protection

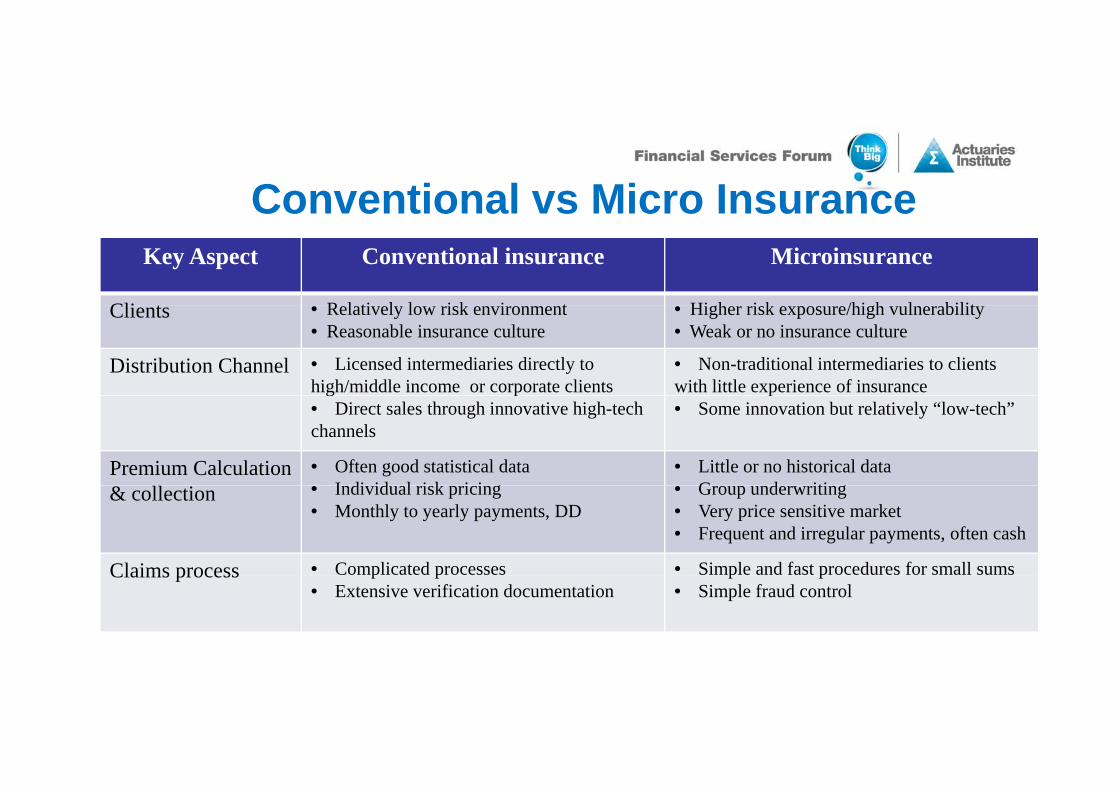

Conventional vs Micro InsuranceKey Aspect Conventional insurance Microinsurance

Cli t R l ti l l i k i t Hi h i k /hi h l bilitClients • Relatively low risk environment • Reasonable insurance culture

• Higher risk exposure/high vulnerability • Weak or no insurance culture

Distribution Channel • Licensed intermediaries directly to high/middle income or corporate clients

• Non-traditional intermediaries to clients with little experience of insurance g p

• Direct sales through innovative high-tech channels

p• Some innovation but relatively “low-tech”

Premium Calculation • Often good statistical data I di id l i k i i

• Little or no historical data G d iti& collection • Individual risk pricing

• Monthly to yearly payments, DD• Group underwriting• Very price sensitive market • Frequent and irregular payments, often cash

Claims process • Complicated processes • Simple and fast procedures for small sums Claims process p p• Extensive verification documentation

p p• Simple fraud control

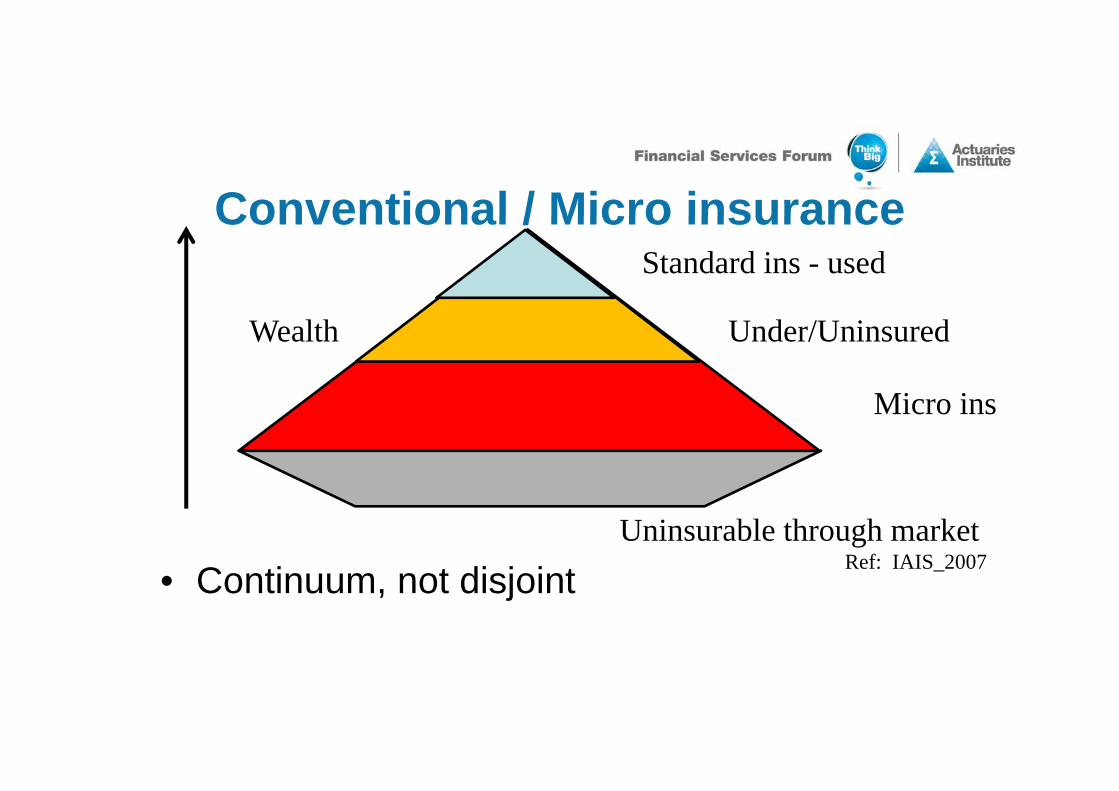

Conventional / Micro insuranceConventional / Micro insuranceStandard ins - used

Under/Uninsured

Mi i

Wealth

Micro ins

Continuum not disjoint Ref: IAIS_2007Uninsurable through market

• Continuum, not disjoint

A i Cli t V lAssessing Client Value

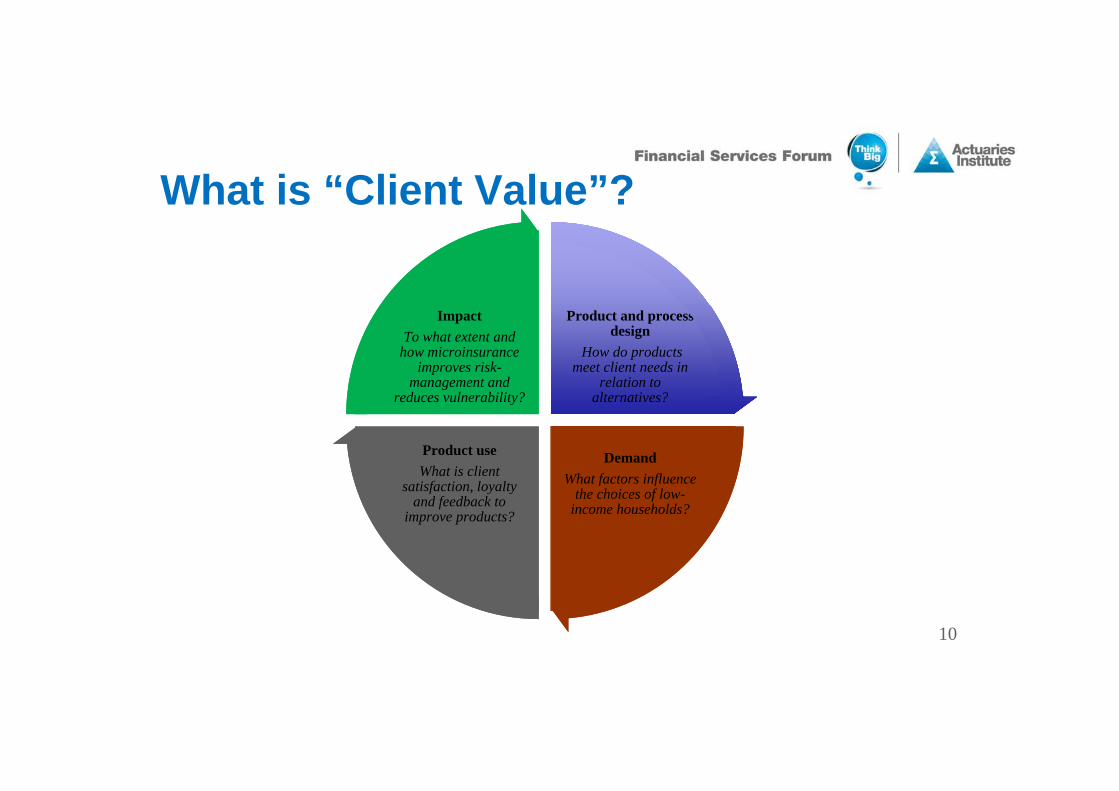

What is “Client Value”?

Product and process design

How do products meet client needs in

relation to alternatives?

Product and process design

How do products meet client needs in

relation to alternatives?

ImpactTo what extent and

how microinsurance improves risk-

management and reduces vulnerability?

ImpactTo what extent and

how microinsurance improves risk-

management and reduces vulnerability? alternatives?alternatives?

DemandWhat factors influence

Product useWhat is client

satisfaction loyalty

Product useWhat is client

satisfaction loyalty

reduces vulnerability?reduces vulnerability?

f fthe choices of low-

income households?satisfaction, loyalty

and feedback to improve products?

satisfaction, loyalty and feedback to

improve products?

10

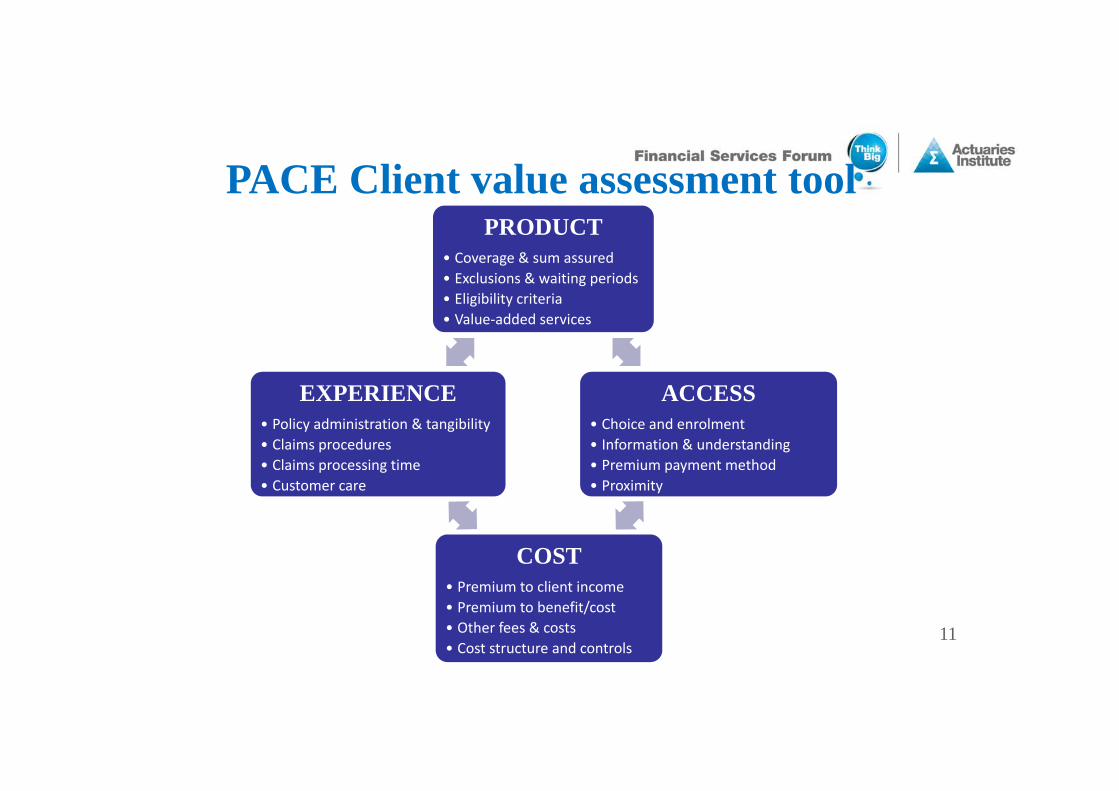

PACE Client value assessment toolPRODUCT

• Coverage & sum assured• Exclusions & waiting periods• Eligibility criteriag y• Value‐added services

ACCESSEXPERIENCE ACCESS• Choice and enrolment• Information & understanding• Premium payment method• Proximity

EXPERIENCE• Policy administration & tangibility• Claims procedures• Claims processing time• Customer care • Proximity

COST

• Customer care

• Premium to client income• Premium to benefit/cost• Other fees & costs• Cost structure and controls

11

• Core question: How and under what circumstances can MI be profitable for insurance organisations?be profitable for insurance organisations?

• MIF study examined experience of organisations who have y gintroduced a range of products over a number of years to identify indications – The profitability drivers are typical for insurance BUT the

fundamental difference between Conventional and Micro insurances remaininsurances remain

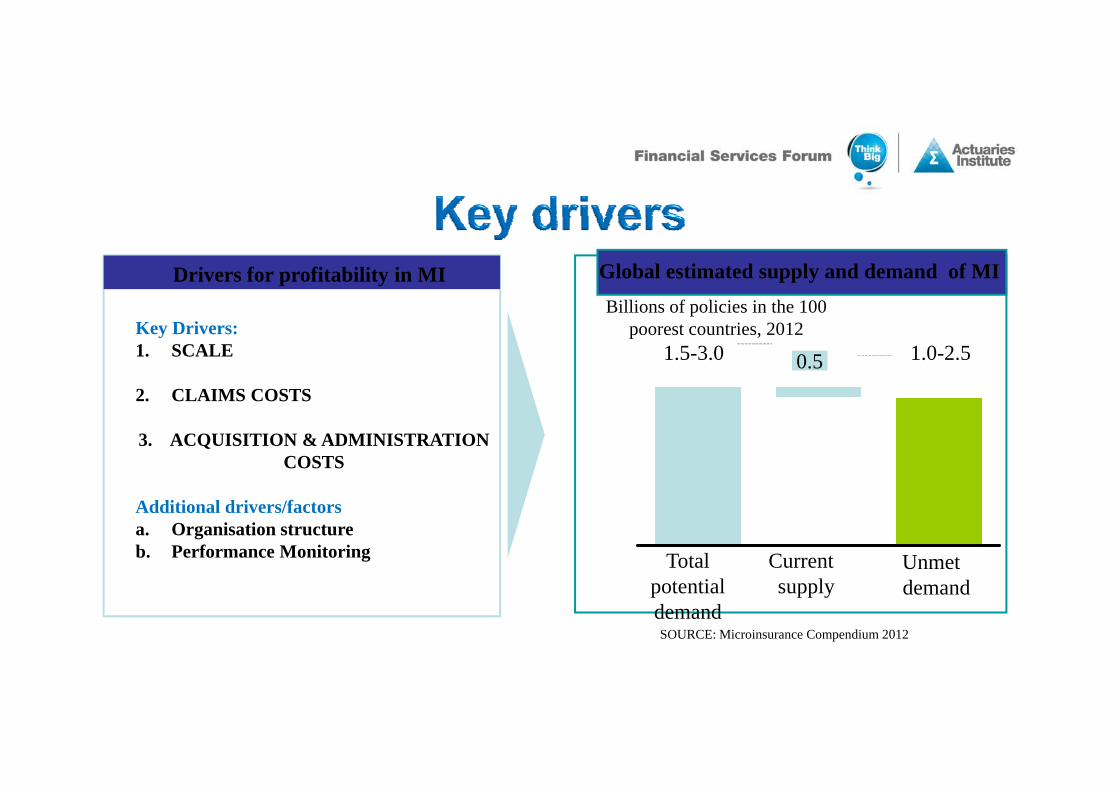

Drivers for profitability in MI Global estimated supply and demand of MIBillions of policies in the 100

Key Drivers:1. SCALE

2 CLAIMS COSTS

1.0-2.50.51.5-3.0

Billions of policies in the 100poorest countries, 2012

2. CLAIMS COSTS

3. ACQUISITION & ADMINISTRATION COSTS

Additional drivers/factorsa. Organisation structureb. Performance Monitoring Unmet Current Total

SOURCE: Microinsurance Compendium 2012

demandsupplypotential demand

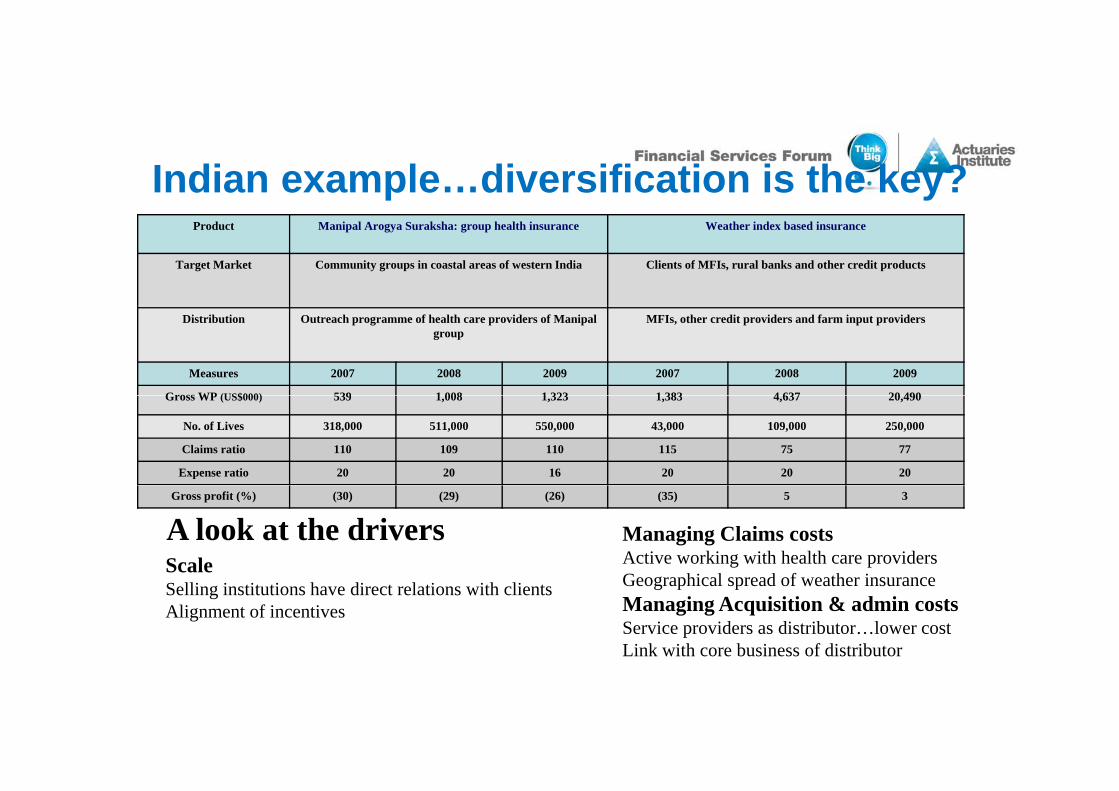

Indian example…diversification is the key?Product Manipal Arogya Suraksha: group health insurance Weather index based insurance

Target Market Community groups in coastal areas of western India Clients of MFIs, rural banks and other credit products

Distribution Outreach programme of health care providers of Manipalgroup

MFIs, other credit providers and farm input providers

Measures 2007 2008 2009 2007 2008 2009

Gross WP (US$000) 539 1 008 1 323 1 383 4 637 20 490Gross WP (US$000) 539 1,008 1,323 1,383 4,637 20,490

No. of Lives 318,000 511,000 550,000 43,000 109,000 250,000

Claims ratio 110 109 110 115 75 77

Expense ratio 20 20 16 20 20 20

Gross profit (%) (30) (29) (26) (35) 5 3

A look at the driversScale

Managing Claims costsActive working with health care providersG hi l d f th iSelling institutions have direct relations with clients

Alignment of incentives

Geographical spread of weather insuranceManaging Acquisition & admin costsService providers as distributor…lower costLink with core business of distributor

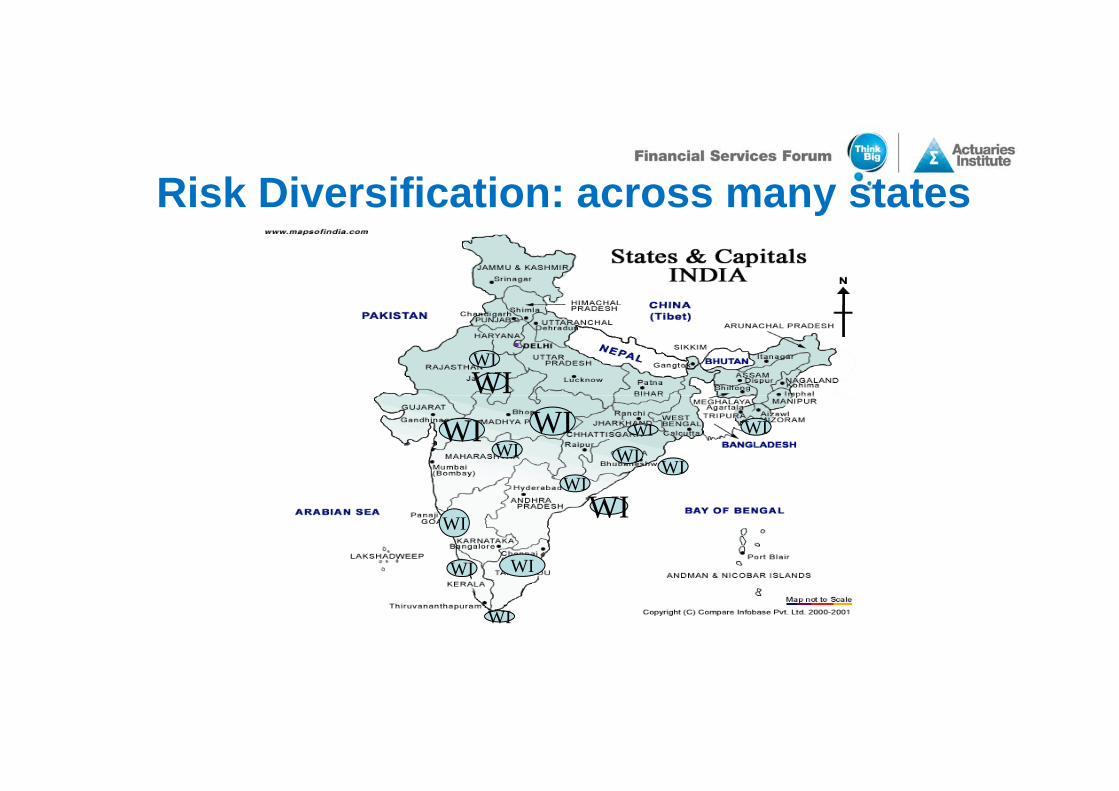

Risk Diversification: across many states y

WIWI

WI WI WI

WI

WI

WIWIWI

WIWI

WIWI

WI

WI

Policy regulation and supervisionPolicy, regulation and supervision• Regulation, and its interpretation through supervision,

provides framework for industry and MIprovides framework for industry and MI– Game rules and referee– MI often not specifically addressed

• For MI, consider if special characteristics need recognition– Avoid retaining unnecessary limitations/restrictions– Extension to address particular MI issues– Opportunity for regulatory leadership to enable industry

Separate reporting (data FRC etc)– Separate reporting (data, FRC etc)– Interaction with other regulators reflecting integrated nature of MI

Policy regulation and supervisionPolicy, regulation and supervision• Review Supervisor against IAIS Insurance Core Principles

– Latest version of October 2011– Latest version of October 2011– 26 ICPs, with supporting standards and guidance– IAIS considering augmenting ICP guidance re MI– Cover both Life and General insurance– Principle of ‘proportionality’

• Provides context to then develop MI Regulations– Address special MI characteristics

Develop capacity industry and supervisor– Develop capacity – industry and supervisor– Liaise with industry organisations

Policy regulation and supervisionPolicy, regulation and supervision• MI regulations typically retain current base insurance law

d i t d l / l ti / id t fit th tand introduce rules/regulations/guidance to fit the sector• Key areas of focus in the rules are typically

Definition of MI textual and quantatitive– Definition of MI, textual and quantatitive– Allowable products, key product features, disclosure requirements– Allowable Intermediaries – need flexible approachAllowable Intermediaries need flexible approach– Allowable risk takers, transition rules for current informal risk takers– Client protection; disclosure, process, client value– Prudential rules and additional regulatory reporting

Learnings from emerging marketsLearnings from emerging markets• Importance of alternative distribution mechanisms

( )– Mobile phones and (so) Telcos– Micro finance providers

• Avoid attempting to apply traditional approaches to a very• Avoid attempting to apply traditional approaches to a very non traditional market

• Challenges with voluntary products (selection scaleChallenges with voluntary products (selection, scale, distribution costs)

• Difficulty of building sufficient sustainable volume asDifficulty of building sufficient sustainable volume as individual policies are small

Learning’s from emerging marketsLearning s from emerging markets• Scale is important – eg amortising setup/fixed expenses• No culture of monitoring experience at all levels. So

Monitor & evaluation critical - claims AND expenses. C titi MI k t i d• Competitive MI markets are emerging and so are consequent practices (churn/discipline)Product evolution is important fix the problems• Product evolution is important – fix the problems

• Can be profitable but care with long term potential, public relations/perceptions & regulatory riskpublic relations/perceptions & regulatory risk

Role for ActuariesRole for Actuaries…What can actuaries do? …. Lots! • Holistic view and capacity to synthesis complex matters• Technical expertise

– Pricing and product development– Financial management, Risk management

• Be part of team of experts and specialists• Kudos with other parties

Role for Actuaries…Role for Actuaries…But…• First listen and learn about local context and issues, talk to local field

staff, NGO’s etc, to understand local culture, mores and needs• Seek lateral solutions reflecting core insurance principles without getting

tied up on esotericatied up on esoterica• Need a pragmatic mindset, good sense of humour and lots of patience!• Microinsurance needs SIMPLE products and solutions

• The actuarial challenge:– Apply complex skills to achieve simple, robust solutions for insuredspp y p p ,

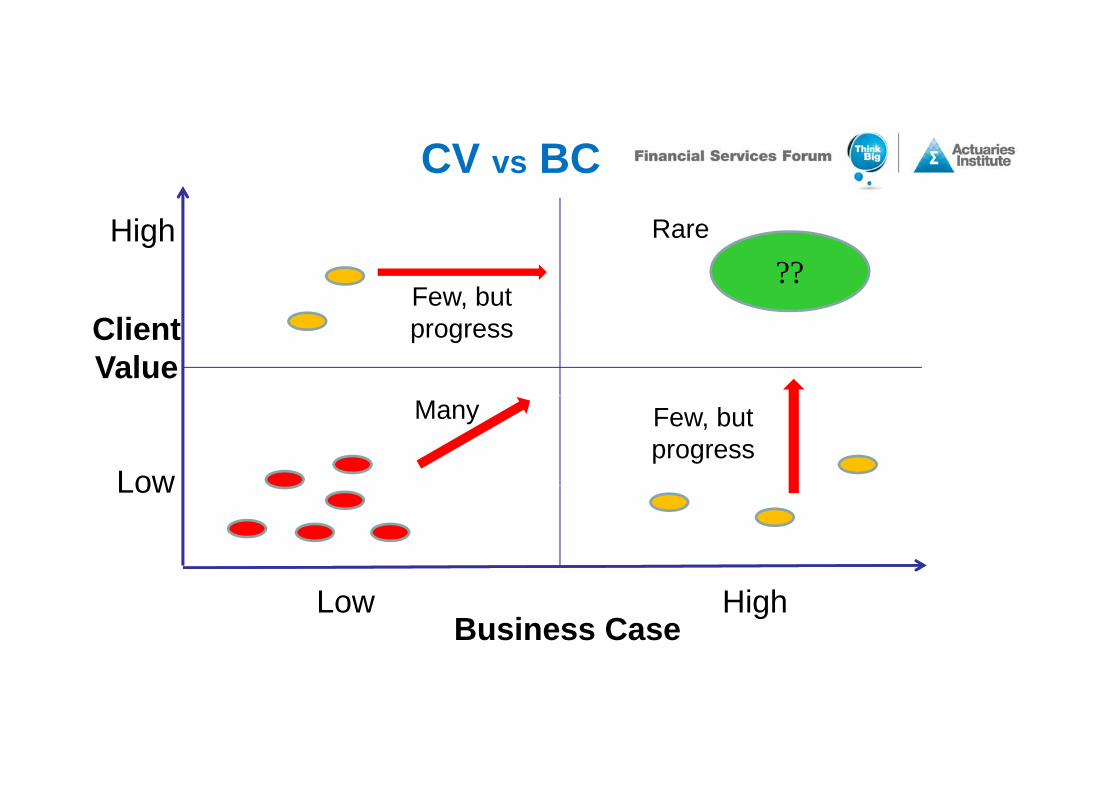

CV vs BCHigh

??Rare

Few, but Client Value

e , buprogress

Low

Many Few, but progress

Low

Business CaseLow High

Appendix

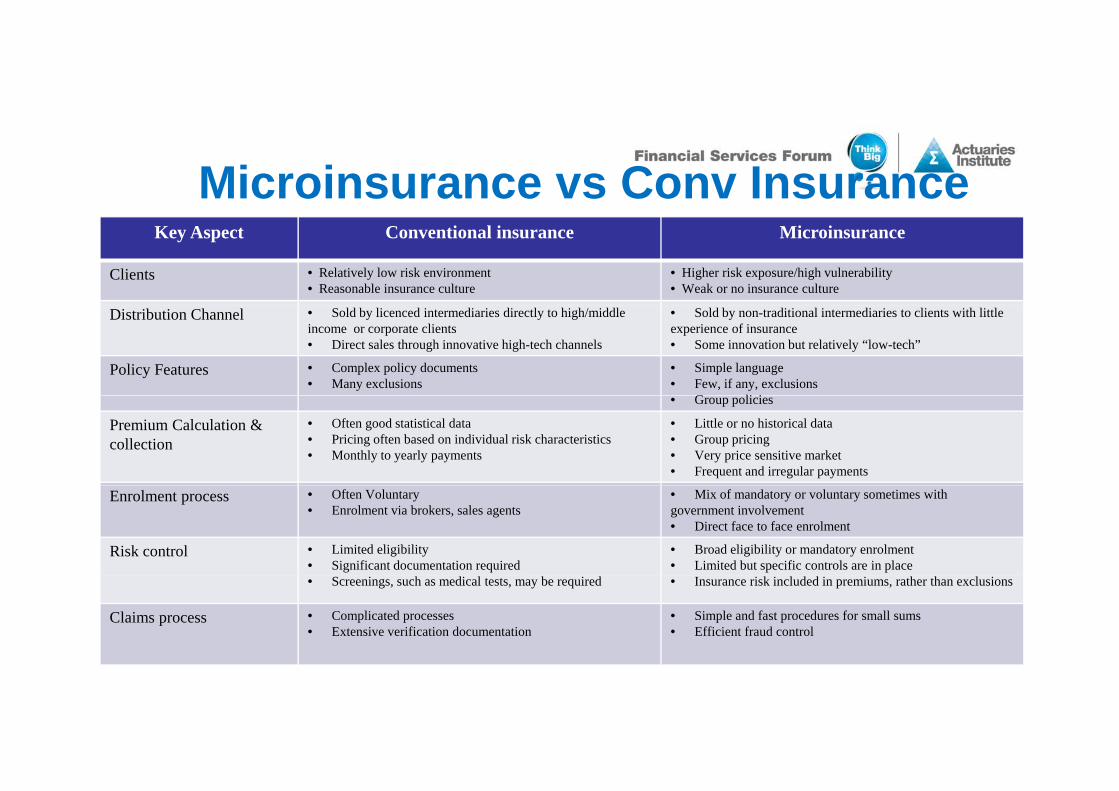

Microinsurance vs Conv InsuranceKey Aspect Conventional insurance Microinsurance

Clients • Relatively low risk environment • Reasonable insurance culture

• Higher risk exposure/high vulnerability • Weak or no insurance culture

Distribution Channel • Sold by licenced intermediaries directly to high/middle income or corporate clients• Direct sales through innovative high-tech channels

• Sold by non-traditional intermediaries to clients with little experience of insurance • Some innovation but relatively “low-tech”

Policy Features • Complex policy documents • Many exclusions

• Simple language • Few, if any, exclusions

G li i• Group policies

Premium Calculation & collection

• Often good statistical data • Pricing often based on individual risk characteristics • Monthly to yearly payments

• Little or no historical data • Group pricing • Very price sensitive market • Frequent and irregular payments

Enrolment process • Often Voluntary • Enrolment via brokers, sales agents

• Mix of mandatory or voluntary sometimes with government involvement • Direct face to face enrolment

Risk control • Limited eligibility • Significant documentation required

• Broad eligibility or mandatory enrolment • Limited but specific controls are in place

• Screenings, such as medical tests, may be required • Insurance risk included in premiums, rather than exclusions

Claims process • Complicated processes • Extensive verification documentation

• Simple and fast procedures for small sums • Efficient fraud control

Contact detailsContact detailsEamon Kelly

E il k ll j @ ilEmail: [email protected]: +44 776 092 6040

Jules GribbleEmail: [email protected]: +61 408 127 624