Embed Size (px)

Citation preview

AQR Capital Management, LLC | Two Greenwich Plaza, Third Floor | Greenwich, CT 06830 | T: 203.742.3600 | F: 203.742.3100 | www.aqr.com

AQR C A P I T A L

M A N A G E M E N T

AQR Capital Management, LLC | Two Greenwich Plaza, Third Floor | Greenwich, CT 06830 | T: 203.742.3600 | F: 203.742.3100 | www.aqr.com

AQR C A P I T A L

M A N A G E M E N T

The information set forth herein has been obtained or derived from sources believed by AQR Capital Management, LLC (“AQR”) to be reliable. However, AQR does not make any representation or warranty,

express or implied, as to the information’s accuracy or completeness, nor does AQR recommend that the attached information serve as the basis of any investment decision. This document has been provided to

you solely for information purposes and does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase any securities or other financial instruments, and may not be

construed as such. This document is intended exclusively for the use of the person to whom it has been delivered by AQR Capital Management, LLC, and it is not to be reproduced or redistributed to any other

person. This document is subject to further review and revision. AQR hereby disclaims any duty to provide any updates or changes to the analyses contained in this presentation.

Thinking Outside Asset Classes: Style Premia

Antti Ilmanen

AQR Capital Management

Fiduciary Investors Symposium

22 October 2012

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T2

Most Portfolio Allocations Are Highly Directional... C

orr

ela

tio

n t

o M

SC

I W

orld

Rolling 36-Month Correlation to Global Equities

*For illustration purposes only and based on AQR backtest. Please see important risk disclosures in the Appendix.

The Global 60/40 portfolio consists of the MSCI World Index and the Barclays Global Aggregate Index (Hedged to USD). The Endowment Proxy consists of S&P 500 (8%), MSCI ACWI ex-US (7%), MSCI

EMG (5%), BarCap Global Agg hedged to USD (11%) , BarCap Global HY hedged to USD (4%), HFR (26%) as absolute return proxy, Russell 2500 Value as PE proxy (17%) and FTSE EPRA/NAREIT and

S&P GSCI (11% each) as two real asset proxies. The Hedge Fund Index is the HFR fund-weighted index. Chart above shows 36-month rolling correlations.

GET ME

OUTTA

HERE!

Concentrated risk makes many portfolios inefficient: One return source – equity

market direction – often explains >90% of portfolio fluctuations

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Global 60/40

Endowment Proxy

Hedge Fund Index

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

...And Typical Diversification Has Not Worked Well

Alternative assets have not helped much to diversify away the directionality of 60/40

3

Sources: The 60/40 portfolio consists of 60% MSCI World (developed equity markets) index, 40% Barclays Global Aggregate fixed-income index, currency-hedged to USD.

The Alternatives-4 is a composite of hedge funds (DJ CS index), commodity futures (SP GSCI index), direct real estate (NCREIF transaction-based index), and private equity

(Cambridge Associates private equity index). Diversification does not eliminate the risk of experiencing investment losses.

Quarterly Returns of 60/40 and Alternative Assets, 1997-2012

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T4

Looking Beyond Asset Classes: Complementary Perspectives

The Cube: Asset Class, Strategy Style and

Risk Factor Perspectives to Investing

Many Institutional Portfolios

Imply a Lopsided Cube

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

Alpha

Alternative Beta Premia

(Hedge fund risk premia

and style premia)

Market Risk Premia

(long-only asset class exposures)

5

AQR Pyramid of Return Sources: Harvest All !

• Highest Cost (“2 and 20”)

• Lowest Capacity

• Moderate Cost

• Medium Capacity

• Lowest Cost (Index Funds)

• Highest Capacity

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

Focus on Alternative Beta Premia

Alternative beta premia (or alternative risk premia, exotic betas, smart betas,...) are

systematic returns harvested through dynamic long-short strategies in liquid asset classes

• Potential to enhance returns and diversify portfolios

• Enables very low correlations with equity market direction and across strategy premia

Can be classified in different ways:

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

* Strategies are subject to change at any time without notice. Please see important disclosures in Appendix.

Hedge Fund Risk Premia Universe

Equity Oriented Strategies

Seek to take advantage of market inefficiencies

that cause specific stocks to be under- or over-

priced.

Arbitrage Strategies

Seek to capture relative mispricing between

two related assets.

Macro Strategies

Profit from dislocations in global equity, bond,

currency and commodity markets, including

those driven by investors’ behavioral biases.

EQUITY STRATEGIESMACRO STRATEGIES

ARBITRAGE STRATEGIES

- Dedicated Short Bias

- Equity Market Neutral

- Long/Short Equity

- Emerging Markets (Equity)

- Global Macro

- Managed Futures

- Emerging Markets (Macro)

- Convertible Arbitrage

- Event Driven

- Fixed Income Relative Value

EQUITY STRATEGIESMACRO STRATEGIES

ARBITRAGE STRATEGIES

- Dedicated Short Bias

- Equity Market Neutral

- Long/Short Equity

- Emerging Markets (Equity)

- Global Macro

- Managed Futures

- Emerging Markets (Macro)

- Convertible Arbitrage

- Event Driven

- Fixed Income Relative Value

Event

Driven

Fixed Income

Relative Value

Equity

Market

Neutral

Dedicated

Short Bias

Global

Macro

Emerging

Markets

Convertible

Arbitrage

Long/Short

Equity

Managed

Futures

7

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T8

Is Alpha Just Beta Waiting To Be Discovered?

ALPHA

ALPHA

HEDGE FUND

RISK PREMIA

OTHER MARKET

RISK PREMIA

EQUITY

RISK PREMIUM

ALPHA

EQUITY

RISK PREMIUM

Time

ALPHA

OTHER MARKET

RISK PREMIA

EQUITY

RISK PREMIUM

Prior to Cap-Weighted

Equity Indices

– Returns viewed as alpha

Equity Risk

Premium introduced

Examples:

– S&P 500 Index

– MSCI World

Other Market Risk

Premia introduced

Examples:

– BarCap Aggregate

– Commodity Indices

– Real Estate

Hedge Fund Risk

Premia introduced

Examples:

– Merger Arbitrage

– Convertible Arbitrage

- Trend Following

Hedge Fund Risk Premia capture the fundamental insights of a class of hedge fund strategies – along with a

meaningful portion of the expected returns those strategies earn – using a dynamic but clearly-defined trading process

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

HF indices suggest that the industry has earned significantly positive alpha, despite the large

market directional exposure. For example, the DJCS HF index outperformed cash by 0.44%

per month (5.3% p.a.) since 1994 and earned equity market alpha of 0.32% (3.9% p.a.).

Hedge Funds Contain Much Beta Exposure

Source: AQR, Dow Jones Credit Suisse. Data from January 1994 through June 2012.

Equity

exc. return

80%

60%

50%

40%

30%

20%

10%

0%

R˄

2

Explanatory Power (R˄2) of Factor Models on DJCS HF Index

1994-2012H1

Equity

exc. return

+ 3 other

market premia

+ 3 other

market premia

+ 9 hedge fund

risk premia

+ 9 hedge fund

risk premia

5.0%

4.0%

3.0%

2.0%

1.0%

0.0%

-1.0%

-2.0%

Alp

ha

(p

.a.)

Annualized Alpha in Factor Models on DJCS HF Index

1994-2012H1

+ 2 lags of EQ + 2 lags of EQ

The main risk by far is equity market beta, but looking beyond the one-factor alpha, one

can explain HF index returns further and reduce the measured alpha.

The broadest regression shows significant exposures to market factors, lagged equity

returns and several HF risk premia. Negative alpha may reflect fees (as factors do not

include fees).

9

Broadest regress ion Coefficient t Stat

ALPHA -0.13% 1.32-

EQUITY 0.30 4.74

EQ lag1 0.14 3.91

EQ lag2 0.08 2.13

CREDIT 0.08 1.71

INFLATION 0.10 3.00

NOM GOVT 0.11 2.89

Convertible Arb 0.10 3.32

Eq Mkt Neutral 0.04- 1.02-

L/S Equity 0.23 5.60

Ded Short Bias 0.03 1.15

Event Driven 0.00 0.00

Managed Futures 0.09 2.52

Emg Markets 0.06 1.39

FI Rel Val 0.08 1.99

Global Macro 0.03 0.61

70%

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T10

Style Premia – Sorting the Wheat From the Chaff

Introducing “The Big-4“ styles with the most consistent long-run rewards:

• Value – long cheap assets / short expensive ones

• Carry – long high-yielding assets / short low-yielders

• Momentum/Trend – long recent winners / short laggards

• Defensive – long low-risk assets / short high-risk ones

Diversification does not eliminate the risk of investment losses.

In long-only context, styles are deviations from market-weighted benchmarks based on

certain characteristics or risk exposures.

Long-short style factors are one useful perspective on alternative beta premia. To be

most effective, style/factor diversification requires leverage and shorting.

But which styles?

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T11

Styles With the Most Pervasive Success

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

fffff

Sources: Asness etal. (2011), Frazzini-Pedersen (2011), Ilmanen (2011), Moskowitz etal. (2011). Sample periods from 1972/75 to 2009/11.

For Each of These Styles, Assets with ‘High’ Characteristics Have

Outperformed Peers With ‘Low’ Charactersitics in Diverse Contexts

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

ffffffff

fffff

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Value Momentum Defensive Carry

Sh

arp

e R

ati

o (

19

72

/75-2

00

9/1

1)

Top Assets by Style Bottom Assets by Style

Across Stocks

Value Momentum Defensive Carry Trend

Across Asset Classes

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T12

Value Style: Buy Cheap Assets

Historically, value stocks (with low multiples) have outperformed the market and

growth stocks (with high multiples) over decades in all markets studied

Value also works in country/sector selection and in other asset classes

Both behavioral and risk-based explanations; both may contribute

100

1,000

10,000

Log scale

(Jan '7

5=

1000)

US Non-US

Value-vs-Growth Cumulative Outperformance

1926-2009 (US) / 1975-2009 (non-US)

Source: Kenneth French’s website. For U.S. stocks (blue line since 1926, “US”), value (growth) stocks are defined by high (low)

book-to-market ratios. For the international stocks (green line since 1975, “nonUS” or 20 other countries), value and growth stocks

are defined by a composite of four valuation ratios (book-to-market, earnings-to-price, dividend-to-price, cash flow-to-price).

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

Carry Style: Buy High-Yielders

In the long run, carry-seeking works in virtually every asset class or context studied

Below FX&FI; also works for stocks (dividend yields), commodities (backwardation), etc.

Certain carry strategies are highly risky; rare large losses concentrate in “bad times”

13

Cumulative Excess Returns of Carry-Seeking

Strategies in Four Asset Contexts, 1993-2009

Sources: Ilmanen (2011), Bloomberg, Barclays Capital, Citigroup, J.P.Morgan

0

100

200

300

400

500

600

700

FX G10 FX Emg FI G10 Credits

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

Trend/Momentum Style: Buy Recent Winners

Trend following has delivered positive long-run returns in most assets simulated

• Chasing past-year returns has added value, while chasing multi-year returns hurts

• Trend strategies are directional while ‘cousin‘ momentum strategies are cross-sectional

14

Source: Ilmanen (2011), Bloomberg.

0

100

200

300

400

500

600

Cmdty Futures Equity Indices Bond/Rate Futures Foreign Exchange

Cumulative Excess Returns of 12-Month Trend-Following

Strategies in Four Asset Contexts, 1993-2009

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

Detour: Trend-Following As Empirical Safe Haven ?

15

Net Returns of a Trend-Following Composite

Source: Hurst-Ooi-Pedersen (2012). Composite strategy is based on a simple average of 1/3/12-month trends and diversification

across a large number of liquid investments weighted by volatility. (Returns on cash proxies are used before futures were available.)

The main puzzle is not the strong paper returns of trend-following strategies but reconciling them

with the surprisingly consistent risk-reducing characteristics.

Ilmanen (2011) showed that a trend-following composite was profitable in 13 of the 15 worst

months for global equities over 25 years.

A new study by Hurst-Ooi-Pedersen (2012) shows below that a trend-following composite made

money in 9 of the 10 worst drawdowns for the U.S. 60/40 portfolio over 110 years.

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Total Returns of a U.S. 60/40 Portfolio and a Trend-Following Composite in the Ten Worst Drawdowns for 60/40, Simulated Data 1903-2012

60/40 Portfolio Returns

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

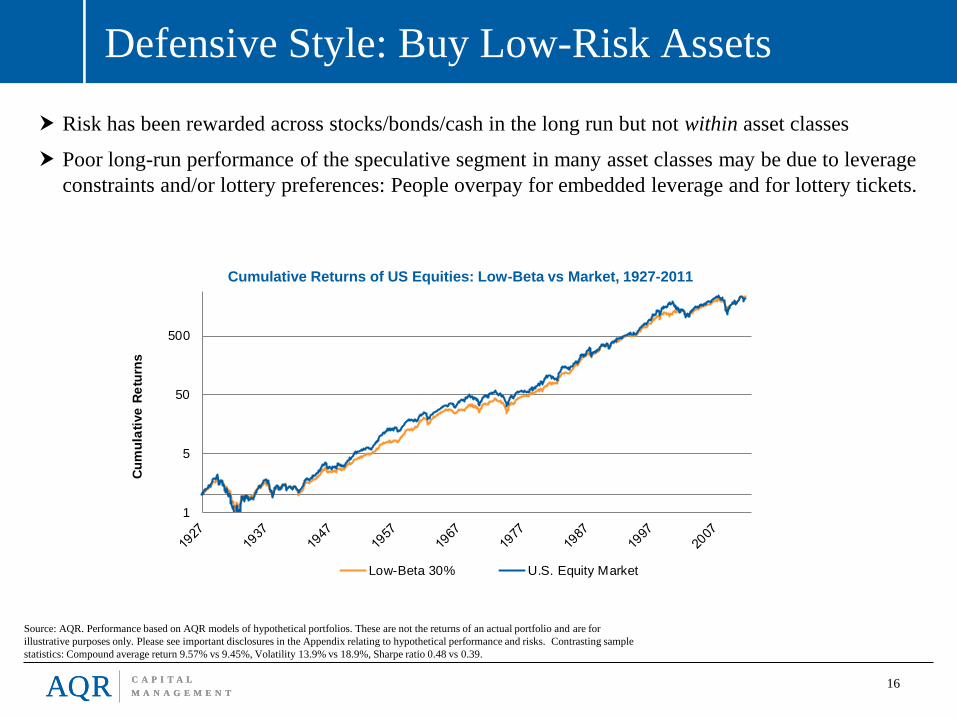

Defensive Style: Buy Low-Risk Assets

16

Risk has been rewarded across stocks/bonds/cash in the long run but not within asset classes

Poor long-run performance of the speculative segment in many asset classes may be due to leverage

constraints and/or lottery preferences: People overpay for embedded leverage and for lottery tickets.

Cumulative Returns of US Equities: Low-Beta vs Market, 1927-2011

Source: AQR. Performance based on AQR models of hypothetical portfolios. These are not the returns of an actual portfolio and are for

illustrative purposes only. Please see important disclosures in the Appendix relating to hypothetical performance and risks. Contrasting sample

statistics: Compound average return 9.57% vs 9.45%, Volatility 13.9% vs 18.9%, Sharpe ratio 0.48 vs 0.39.

1

5

50

500

Cu

mu

lati

ve

Re

turn

s

Low-Beta 30% U.S. Equity Market

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

‘Big-4’ Long-Short Style Premia: Ubiquitous

17

Source: AQR Capital Management. Simulated trading strategies gross of trading costs

and fees. For illustrative purposes only. The returns above do not represent the return of

an actual fund or AQR product.

Bet Against Beta Style: Sharpe Ratio Across Contexts, 1960s/90s-2009

Source: Frazzini-Pedersen (2010) BAB Factor SRs – All Asset Classes 1964-2009. Annualized Sharpe

ratios of BAB factors, where BAB is a portfolio short (de-leveraged) high beta assets and long (levered)

low beta assets.

Sh

arp

e R

ati

os

Sh

arp

e R

ati

os

Sh

arp

e R

ati

os

Sh

arp

e R

ati

os

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

Multi-Strategy Approach Is More Robust

18

We prefer a multi-strategy approach over single-strategy approaches. The former provides better

diversification (higher Sharpe ratio), reduces trading costs via netting, and induces less return chasing

(which often hurts investors)

Craftmanship in implementation (cost-effective harvesting) is essential when rely heavily on breadth

Temptation To Chase Returns: Rolling 3-Year Excess Return of a Simple Stock

Selection Portfolio in the U.S. (Simulated Value and Momentum), 1956-2011

Source: AQR.

-10%

-5%

0%

5%

10%

15%

20%

1956 1959 1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

Hyp

oth

eti

ca

l A

nn

ua

l R

etu

rn

(Ro

llin

g 3

-ye

ar)

Add More!

Add More! Add More!

Add More!

Add More!

I'm Out!

I'm Out! I'm Out!

I'm Out! I'm Out!

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T19

Style Diversification: Exceptionally Effective

Style diversification can be more effective than asset class diversification – as long as shorting is

allowed to avoid concentrated market-directional risk (and leverage to monetize volatility reduction)

In long-short, can fully benefit from low/negative correlations between styles and vs equity markets,

resulting in significant volatility reduction and Sharpe ratio boost

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Mkt, Value, Momentum (Long-only) Mkt, Value, Momentum (Long-Short)

Sharp

e R

atio

Average SR among 3 constituents Portfolio SR (Equal-vol-wtd composite)

Source: Monthly data 1973-2010 from Asness-Moskowitz-Pedersen (2011). Diversification does not eliminate the risk of experiencing investment losses.

Diversification Benefits From Combining Global Market, Value, and

Momentum Portfolios – More Effective Long-Short Than Long-Only

1973-2010

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T20

Why Are Alternative Betas Underutilized?

Style investing may help in both return enhancement and portfolio diversification, yet it

is only modestly utilized in most institutional portfolios. Why?

• Uncertainty: lack of conviction about sustainability

• Unconventionality – recall Keynes

• Aversion to the three dirty words in finance: Leverage, Shorting, Derivatives

• Capacity concerns – especially for ‘Giants‘

On the flipside, the same reasons explain why most investors continue to accept the

risk concentration implied in their over-reliance on the equity premium: best

conviction from theory and history; embedded leverage; high capacity; and

conventionality.

CAPM 2:1

Debt : Equity

Capacity

Everyone‘s

Doing It...

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

Buffett: A Successful Investor in Several Risk Premia

Extraordinary track record

What risk premia does Buffett exploit?

• Market risk premium

• Value

• Betting against beta:

• Buying low risk / high quality

• Using leverage

• Shorting options

Decomposing Buffett:

• Can the Buffett strategy be done in a systematic way?

Lessons from Buffett

• Systematic harvesting of these premia can even explain this great investor (with hindsight)

• Careful use of leverage

• Importance of the ability to stick with it

21

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T

Summary on Style Investing

Long-short style investing can enhance portfolio returns and diversification.

Long-only style tilts mainly boost returns, with less impact on diversification.

Four styles with the most consistent long-run performance across contexts:

Value

Momentum

Carry

Defensive

Diversifying across styles and volatility targeting improve style portfolios.

Further, a multi-strategy approach promotes patience over return chasing.

Implementation efficiency is essential when harvesting style premia

Underutilized. Why? Uncertainty, unconventionality, ‘LSD‘ aversion, capacity

22

AQR C A P I T A L

M A N A G E M E N TAQR C A P I T A L

M A N A G E M E N T23

Disclosures

The information set forth herein has been obtained or derived from sources believed by AQR Capital Management, LLC (“AQR”) to be reliable. However,

AQR does not make any representation or warranty, express or implied, as to the information’s accuracy or completeness, nor does AQR recommend that the

attached information serve as the basis of any investment decision. This document has been provided to you in response to an unsolicited specific request and

does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase any securities or other financial instruments, and may not

be construed as such. This document is intended exclusively for the use of the person to whom it has been delivered by AQR Capital Management, LLC, and

it is not to be reproduced or redistributed to any other person. This document is subject to further review and revision. For one-on-one presentation use

only.

Hypothetical performance results (e.g., quantitative backtests) have many inherent limitations, some of which, but not all, are described herein. No

representation is being made that any fund or account will or is likely to achieve profits or losses similar to those shown herein. In fact, there are frequently

sharp differences between hypothetical performance results and the actual results subsequently realized by any particular trading program. One of the

limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight. In addition, hypothetical trading does not

involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading. For example, the ability to

withstand losses or adhere to a particular trading program in spite of trading losses are material points which can adversely affect actual trading results. The

hypothetical performance results contained herein represent the application of the quantitative models as currently in effect on the date first written above and

there can be no assurance that the models will remain the same in the future or that an application of the current models in the future will produce similar

results because the relevant market and economic conditions that prevailed during the hypothetical performance period will not necessarily recur. There are

numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the

preparation of hypothetical performance results, all of which can adversely affect actual trading results. Discounting factors may be applied to reduce

suspected anomalies. This backtest’s return, for this period, may vary depending on the date it is run.

There is a risk of substantial loss associated with trading commodities, futures, options, derivatives and other financial instruments. Before trading, investors

should carefully consider their financial position and risk tolerance to determine if the proposed trading style is appropriate. Investors should realize that when

trading futures, commodities, options, derivatives and other financial instruments one could lose the full balance of their account. It is also possible to lose

more than the initial deposit when trading derivatives or using leverage. All funds committed to such a trading strategy should be purely risk capital.